Embed Size (px)

Citation preview

1

Define asset allocation. List the asset classes and subcategories

an investor can select from. Explain how asset allocation can

maximize return and reduce risk. Explain rebalancing. Evaluate the asset allocation of a

portfolio.

2

Most investors hold a well-diversified portfolio.

Humans were meant to stock pick. Investing will always be partly a guessing

game.

3

4

5

Major Asset Classes

AssetClasses

Categories Subcategories

CashGrowth or valueLarge, medium, or small cap

U.S.

Sector and industriesBy region or country (Asia, Europe)

Stock

InternationalEmerging marketsCorporateTreasuryMunicipalMortgage backedShort, medium, or long maturity

U.S.

Investment gradeDeveloped or emerging

Bond

GlobalBy region or country

Region Northeast, West, Midwest, South,Southwest

Real estate

Type of Use Healthcare, residential, shopping mallsMetals Gold, copper, aluminum, etc.CommoditiesAgricultural Products Pork bellies, coffee, etc.

6

0% 20% 40% 60% 80% 100% 120% 140% 160%

1980 Small Stocks

1981 Treasury Bills

1982 Government Bonds

1983 Small Stocks

1984 Corporate Bonds

1985 Europe

1986 EAFE

1987 Emerging Asia

1988 Emerging Asia

1989 Latin America

1990 Corporate Bonds

1991 Latin America

1992 Small Stocks

1993 Emerging Asia

1994 Latin America

1995 S&P 500

1996 S&P 500

1997 S&P 500

1998 S&P 500

1999 Latin America

2000 Mid Cap Stocks

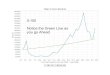

Best-Performing Asset Class(1980-2000)

Based on Index

7

Major Asset Classes(1991-2000)

-5%

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Average Annual Standard Deviation

Ave

rag

e A

nn

ua

l R

etu

rn

U.S. Stocks

Bonds

Global

S&P 500Russell 2000

NASDAQ

DJIAS&P 400

GovernmentBonds

CorporateBonds

T-Bills

Japan

EAFE

Europe

World

Source: Global Financial Data www.globalfindata.com

8

The key is having two

investments which aren’t correlated.

9

Adding 10% stock to a T-bill portfolio

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

2.0% 2.2% 2.4% 2.6% 2.8% 3.0% 3.2% 3.4% 3.6% 3.8% 4.0%

Risk (Standard Deviation)

Ret

urn

(A

vera

ge

An

nu

al %

)

90% T-Bill, 10% Stock

100% T-Bill

Increases return.

Reducesrisk!

Data based on 20 years of returns.

10

Adding stock to a T-bill portfolio

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

1.5% 3.5% 5.5% 7.5% 9.5% 11.5% 13.5% 15.5%

10% Stock

0% Stock

20% Stock

30% 40%

50%

60%

70%

80%

90%

100% Stock

Data based on 20 years of returns.

20% stock gives more return with about the same amount of risk

as 0% stock.

11

Year-End Close

Price Annual Gain

Ford J&J Ford J&J

1990 7.44 15.08 1991 7.86 24.49 6% 62% 1992 11.98 21.99 52% -10% 1993 18.03 20.02 51% -9% 1994 15.58 25.03 -14% 25% 1995 16.14 39.83 4% 59% 1996 18.03 47.05 12% 18% 1997 27.15 63.18 51% 34% 1998 32.82 81.49 21% 29% 1999 29.82 91.65 -9% 12% 2000 23.19 104.71 -22% 14%

Average annual return

15% 24%

Standard deviation 26% 23%

12

Year-End Close Price Annual Gain Asset Allocation 20% Ford , 80% J&J

Ford Year J&J Year Ford J&J

1990 7.44 15.08 1991 7.86 24.49 6% 62% (20% x 6%) + (80% x 62%) = 51% 1992 11.98 21.99 52% -10% (20% x 52%) + (80% x –10%) = 2% 1993 18.03 20.02 51% -9% (20% x 51%) + (80% x –9%) = 3% 1994 15.58 25.03 -14% 25% (20% x -14%) + (80% x 25%) = 17% 1995 16.14 39.83 4% 59% (20% x 4%) + (80% x 59%) = 48% 1996 18.03 47.05 12% 18% (20% x 12%) + (80% x 18%) = 17% 1997 27.15 63.18 51% 34% (20% x 51%) + (80% x 34%) = 37% 1998 32.82 81.49 21% 29% (20% x 21%) + (80% x 29%) = 27% 1999 29.82 91.65 -9% 12% (20% x -9%) + (80% x 12%) =8% 2000 23.19 104.71 -22% 14% (20% x -22%) + (80% x 14%) = 7%

Average annual return 15% 24% 22% Standard deviation 26% 23% 17%

13

14

The Efficient Portfolio

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Risk (5-Year Standard Deviation)

Re

turn

(5-

Ye

ar A

ve

rag

e A

nn

ual

Re

turn

)

Indexes

Industries

Source: Representative funds from Thomson Investor Network www.thomsoninvest.net

S&P 500

Long-TermBonds

Real Estate

Convertible

Pacific

Emerging Markets

Small Cap

High YieldCorporate

IntermediateBonds

Short-TermBond

GNMA

European

Gold

Electronics

Technology

Brokerage

Software

Insurance

NaturalGas

Health Care

Telecommunications

Biotechnology

Computers

Financial Services

Mix and match combinations of investments to

maximize return for risk.

Select where you want to be based on risk you want

to take.

Low Risk

High Risk

15

16

17

18

19

Calpers is the California pension system. Check out their 2007 to 2008 target asset allocation (available on their Web site www.calpers.ca.gov under Investments). What differences do you see? What does their target allocation suggest?

20

Cash, 1%International Equities, 23%

Domestic Equities, 40%

Global Fixed Income, 23%

Real Estate, 8%Direct

Partnership, 6%

California Pension System $230.3 Billion

Source: www.calpers.ca.gov Investment Portfolio Market Value as of Dec. 31, 2006

21

15%

45%

Private Equity, 5%

International equities, 11%

Cash, 13%

Investment real estate, 7%

Other, 2%

Hedge Funds, 1%

Commodities, 1%

Households with investable assets

of $1 million to $10

million

Source: Fortune, 3/5/2007

22

Domestic equity, 30%

Foreign developed equity, 15%

Emerging market equity, 5%

Real Estate, 20%

US Treasury bonds, 15%

US Treasury Inflation Protected,

15%

Source: Swensen, David, (2005) Unconventional Success, Free Press

23

Adjusting portfolio based on asset allocation goals

9/12/07 24

9/12/07 25

Determine what your asset allocation will be. For example: ◦ 60% stocks◦ 40% bonds

Adjust your portfolio when your allocation exceeds 5% difference from your target so that you keep your asset allocation goals, that is 60% stocks and 40% bonds

9/12/07 26

If you didn’t rebalance your portfolio, the allocation of stocks would grow to 73% and the allocation of bonds would shrink to 27%

9/12/07 27

Year Bond Stock1992 40% 60%1993 40% 60%1994 39% 61%1995 35% 65%1996 32% 68%1997 27% 73%1998 24% 76%1999 21% 79%2000 24% 76%2001 28% 72%2002 36% 64%2003 31% 69%2004 30% 70%2005 29% 71%2006 27% 73%

Rebalancing naturally sells high and buys low

You end up with more gains

It reduces the lows.

9/12/07 28

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

No action

Rebalanced

Final Value - No Action Portfolio $376,353Final Value Rebalance Portfolio - $381,608

9/12/07 29

Protect your wealth.

Safeguard all your financial information Keep good records and reconcile all your

accounts Check your credit report If you feel that you have been a victim of

fraud, file a complaint with the DFI at 1-877-RING-DFI or at their website www.dfi.wa.gov.

9/12/07 30

Take time to pick an investment advisor who is appropriate for you. Look at Certified Financial Planner website for tips on how: http://www.cfp.net/

Immunize yourself against investment fraud – check out all advisors and investments – google them and check with www.dfi.wa.gov

9/12/07 31

9/12/07 32

9/12/07 33

Roth IRA Traditional IRA

Who is eligible Anyone who had income from working and his or her nonworking spouse.There are income limits.

Anyone up with age 70 ½ with income from working and his or her nonworking spouse. There are no income limits.

Maximum you can contribute You cannot contribution more than you earn in compensation. Up to $8000 ($4000 each) combined contribution or $10,000 ($5000 each) for those 50 and over.The maximum will go up $1000 in 2008.

You cannot contribute more than you earn in compensation. Up to $8000 ($4000 each) combined contribution or $10,000 ($5000 each) for those 50 and over.The maximum will go up $1000 in 2008.

Tax status of contributions Contributions must be after-tax. Contributions may be pretax up to certain income limits.

Tax status of earnings Earnings are tax free. Earnings are tax deferred. You pay ordinary income tax when you take the money out therefore missing out on lower capital gains tax.

Withdrawals Contributions may be withdrawn without penalty.Earnings can be withdrawn without penalty for some expenses.

Withdrawals made before age 59 ½ will be subject to a penalty of 10% in addition to tax.

Mandatory age for withdrawals

None 70 1/2

Check www.irs.gov Publication 590 for more information.

529 Plans – after-tax contributions, tax exempt distributions if used for qualified educational expenses◦ College savings plan◦ Prepaid college tuition plan (Washington GET

www.get.wa.gov) Coverdell – after-tax contributions, tax

exempt distributions. Some restrictions.

9/12/07 34

1. Set goals and develop a life-long saving plan.

2. Learn about returns and risk.3. Evaluate your investments.4. Asset allocate.5. Protect your wealth.6. Use tax-advantaged saving.

9/12/07 35