Embed Size (px)

Citation preview

1

CHAPTER 9

Mortgage Markets

2

CHAPTER 9 OVERVIEW

This chapter will:

A. Describe the characteristics of residential mortgages

B. Describe the common types of residential mortgages

B. Explain how mortgage-backed securities are used

C. Explain how to make an amortization schedule

3

Characteristics of Residential Mortgages

1. Mortgage is a securities (debt) used to finance real estate purchases. This contract should specify

a. if the mortgage is federally insured

b. the amount of the loan

c. fixed or adjustable interest rate

d. The maturity

e. Other provisions

4

Common Types of Residential Mortgages

1. Residential Mortgage Types:

a. Fixed-rate

b. Adjustable-rate (ARM)

c. Others

5

Common Types of Residential Mortgages

Fixed-Rate Mortgages

1. Locks in the borrower’s interest rate over the life of the mortgage.

2. Makes the lender exposed to interest rate risk because it commonly uses funds obtained from short-term deposits to make long-term mortgage loans.

What if the market interest rate goes up or down afterwards?

6

Common Types of Residential Mortgages

Adjustable-Rate Mortgages

1. Allows the mortgage interest rate to adjust to market conditions.

2. Adjustable-rate is typically lower than the fixed-rate as the lender has a lower interest rate risk.

What if the market interest rate goes up or down afterwards?

7

Amortization Schedule

It breaks down the monthly payments into principal and interest.

Note:

a. Interest payment decreases over time

b. Principal repayment increases over time

8

Example of loan amortization 1

You have borrowed $8,000 from a bank and have promised to repay the loan in five equal yearly payments. The first payment is at the end of the first year. The interest rate is 10 percent. Draw up the amortization schedule for this loan.

Amortization schedule is just a table that shows how each payment is split into principal repayment and interest payment.

9

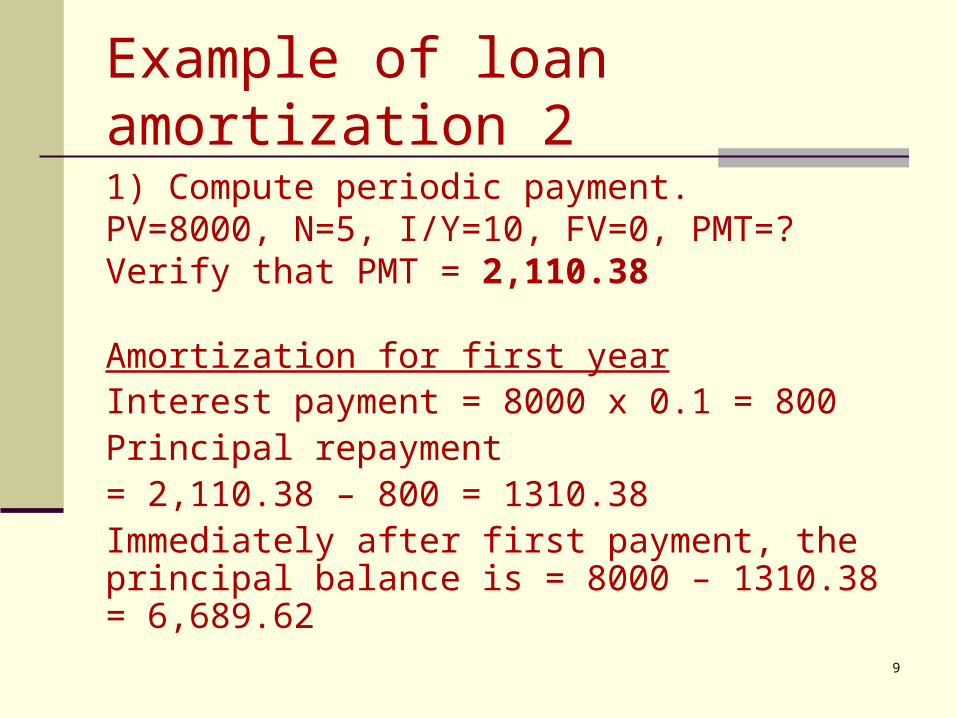

Example of loan amortization 2

1) Compute periodic payment.PV=8000, N=5, I/Y=10, FV=0, PMT=?Verify that PMT = 2,110.38

Amortization for first yearInterest payment = 8000 x 0.1 = 800Principal repayment = 2,110.38 – 800 = 1310.38Immediately after first payment, the principal balance is = 8000 – 1310.38 = 6,689.62

10

Example of loan amortization 3

Amortization for second yearInterest payment = 6689.62 x 0.1 = 668.96(using the new balance!)Principal repayment = 2,110.38 – 668.96 = 1441.42Immediately after second payment, the principal balance is = 6,689.62 – 1441.42 = 5,248.20

Verify the entire schedule (on following slide)

11

Verify the amortization schedule

YearBeg.

Balance Payment Interest PrincipalEnd.

Balance

0 8,000.00

1 8,000.00 2,110.38 800.00 1,310.38 6,689.62

2 6689.62 2,110.38 668.96 1,441.42 5,248.20

3 5248.20 2,110.38 524.82 1,585.56 3,662.64

4 3662.64 2,110.38 366.26 1,744.12 1,918.53

5 1918.53 2,110.38 191.85 1,918.53 0.00

12

Using financial calculator to generate amortization schedule 1

Very often, amortization problems involve long periods of time, e.g., 30 year mortgage with monthly payments => 360 periods.

To generate amortization schedule in such problems, it’s more efficient to use the financial calculator.

Let’s reuse the last problem (Problem 7.25). First, find the monthly payment. Key in:

PV=8000, N=5, I/Y=10, FV=0, PMT=?We already worked out that PMT = 2,110.38.

13

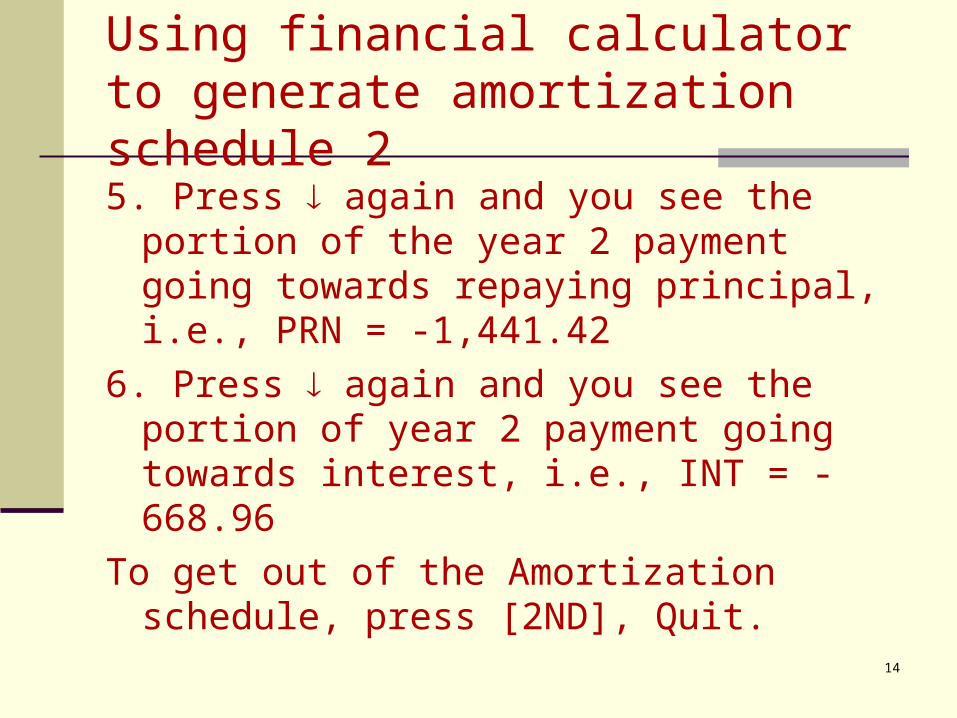

Using financial calculator to generate amortization schedule 2

Suppose we want to work out the remaining balance immediately after the 2nd payment.

1. Press [2ND], [Amort] to activate the Amortization worksheet in BA II Plus.

2. Press P1=2, press 3. Press P2=2, press 4. You will see BAL=5,248.20

14

5. Press again and you see the portion of the year 2 payment going towards repaying principal, i.e., PRN = -1,441.42

6. Press again and you see the portion of year 2 payment going towards interest, i.e., INT = -668.96

To get out of the Amortization schedule, press [2ND], Quit.

Using financial calculator to generate amortization schedule 2

15

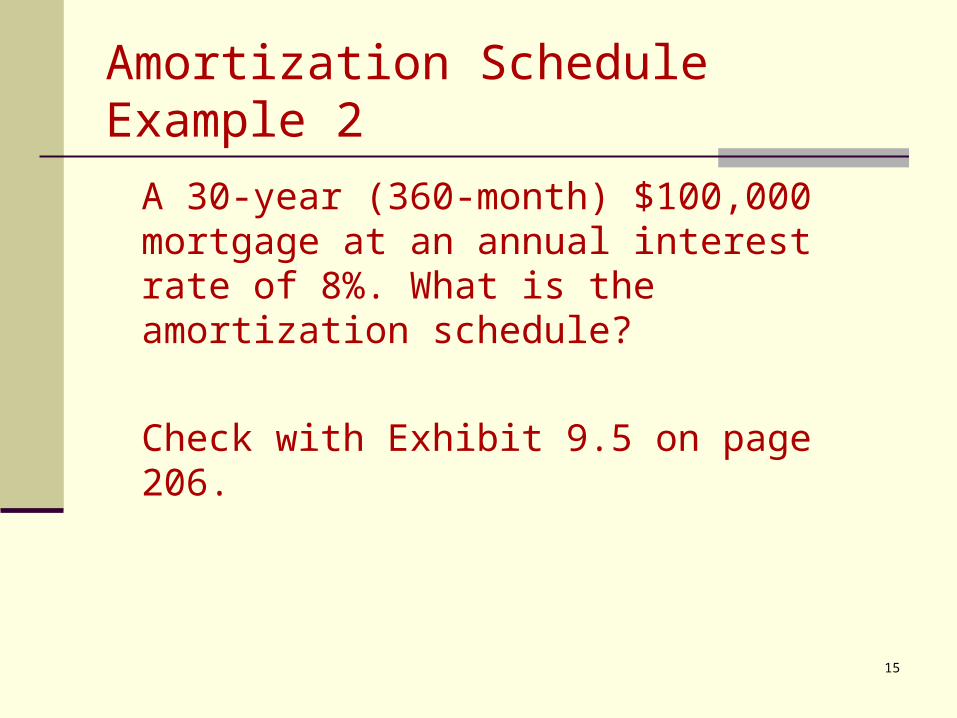

A 30-year (360-month) $100,000 mortgage at an annual interest rate of 8%. What is the amortization schedule?

Check with Exhibit 9.5 on page 206.

Amortization Schedule Example 2

Exhibit 9.5 Amortization Schedule for Selected Years

16

17

On Dec 31, 2005, I borrowed a 30-year $100,000 home mortgage loan at an annual interest rate of 12%. How much interest

did I paid in 2009?

Amortization Schedule Example 3

18

Institutional Use of Mortgage Markets

Two Broad classification: institutions that

a. Originate and service a mortgage

Commercial banks and savings banks

b. Finance a mortgage (secondary market)

Fannie Mae, Ginnie Mae, and Freddie Mac

19

Mortgage Securitization

Securitization

1.) the pooling and repackaging of loans into securities

2.) removes loans from the balance sheet of the bank that originally created them

3.) Future cash flows to the investors of these securities are the mortgage payment.

20

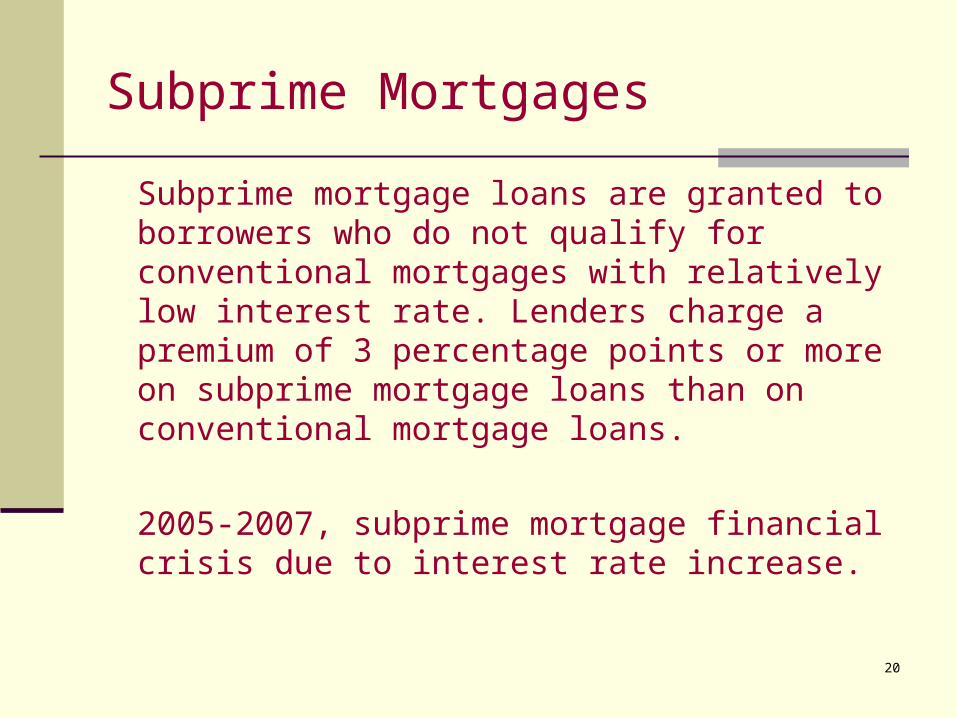

Subprime Mortgages

Subprime mortgage loans are granted to borrowers who do not qualify for conventional mortgages with relatively low interest rate. Lenders charge a premium of 3 percentage points or more on subprime mortgage loans than on conventional mortgage loans.

2005-2007, subprime mortgage financial crisis due to interest rate increase.

21

Valuation of Mortgages

Factors That Affect the Risk-Free Interest Rate

1.) Inflationary Expectations

2.) Economic Growth

3.) Money Supply Growth

4.) Budget Deficit

22

Risk from Investing in Mortgages

a. Interest Rate RiskLimiting Exposure to Interest Rate Risk

b. Prepayment RiskLimiting Exposure to Prepayment Risk

c. Credit RiskLimiting Exposure to Credit Risk

23

Mortgage-Backed Securities

Mortgage Pass-Through Securities

The interest and principal payments on the mortgages are sent to the financial institution, which then transfers the payments to the owners of the mortgage-backed securities after deducting fees for servicing. Thus, the mortgage issuer earn fees from servicing while avoiding exposure to interest rate risk and credit risk.

Summary

Risk with mortgage Amortization schedule Mortgage pass-through securities Assignment 6:

questions and applications, 4, 16

Problem: 1

24