Embed Size (px)

Citation preview

1

Chapter 4

Copyright ©2006 Thomson South-Western, Mason, Ohio

William A. Raabe, Gerald E. Whittenburg, &

Debra L. Sanders

Administrative Regulations & Rulings

2

Overview of Regulations(1 of 2)

Regulations are the Treasury Department’s official interpretations of Code

Code authorizes the Treasury Secretary to prescribe Regs under §7805(a)

Issued in the form of Treasury Decisions

3

Treasury DepartmentAdministers the U.S. tax lawsSecretary of the Treasury

• Member of Presidential cabinet

IRS• Commissioner appointed by the President• A division of Treasury Department

Overview of Regulations(2 of 2)

4

Types of Regulations

There are three types:

Proposed

Final

Temporary

5

Proposed Regulations(Proposed Treasury Decisions)

Issued at least 30 days prior to publishing final Treasury Decision

Comments (public hearings) can affect final form

Do NOT have the effect of law Must be followed after becoming a final

regulation

6

Final Regulations

Final Treasury Decisions are integrated with previously approved Regulations (TDs)

Two Types:General Legislative

7

Issued under general authority of IRS to interpret the language of the Code

Do not carry same authority as the statutes by law (Code)

General Regulations

8

Legislative Regulations

Congress directs IRS to provide details for certain tax statutes

Carries same authority as the statutes (e.g. Consolidated Regs.)

9

Temporary Regulations

Issued in response to congressional or judicial change

Provide immediate guidanceSimultaneously issued as proposed regs.Have the same force as a final reg.

Must be followed until supersededExpire after three years (§7805)

10

Effective Date for Regulations(1 of 2)

Generally effective on the date filed with the Federal Register [§7805(b)]

Retroactive under certain conditions:1. Issued within 18 months of a statute’s

enactment

2. Prevents taxpayer abuse

3. Corrects defect in prior Regulation

Cont’d on next slide

11

Effective Date for Regulations(2 of 2)

4. Relates to Treasury policies

5. Congressional directive

6. Commissioner may allow taxpayers to elect to apply Regulation retroactively

12

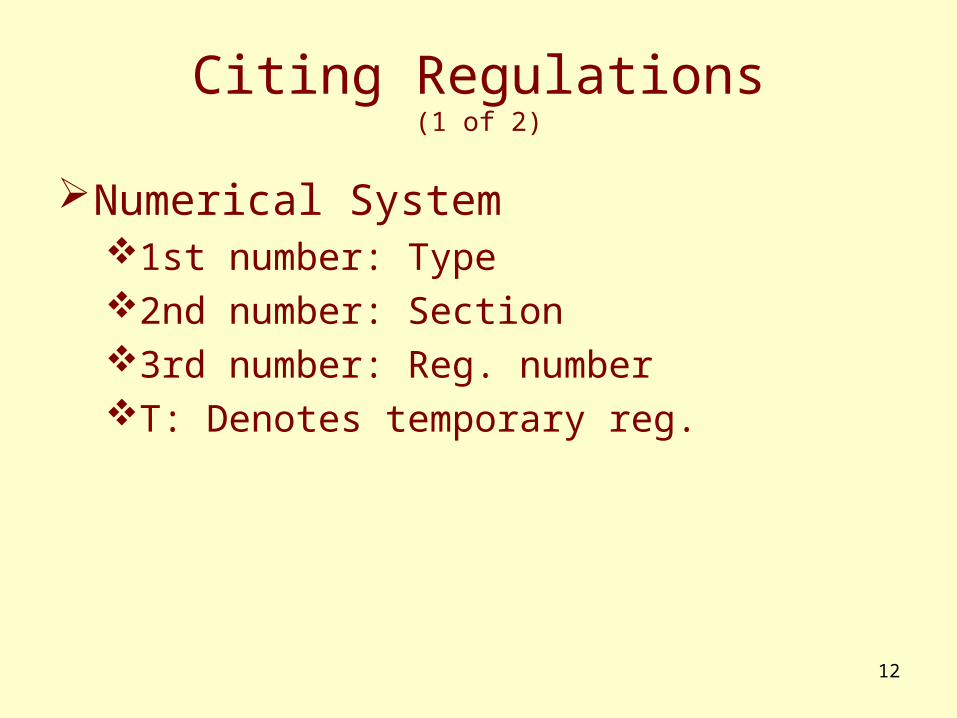

Citing Regulations(1 of 2)

Numerical System1st number: Type2nd number: Section3rd number: Reg. numberT: Denotes temporary reg.

13

Citing Regulations(2 of 2)

Commonly encountered types of Regulations1: Income tax20: Estate tax25: Gift tax31: Employment tax301: Procedural mattersOdd ones:

• 15A – Installment Sales Revision Act of 1980

14

Assessing Regulations

If assert regulations are improper, t/p bears burden of proofDifficult, particularly if legislative reg

Disregard of regs may result in a negligence penalty§6662: 20% of underpayment

15

Locating Regulations

Internal Revenue Bulletin (IRB)Weekly newsletter of the IRS

Cumulative Bulletin (C.B.)Permanently bound version of IRB

• Organized by Code section• Bound twice a year

Commercial publishers

16

Revenue Rulings: Overview

Official pronouncements of the IRS National Office

Application of Code and Regs to specific factual situations (usually submitted by a taxpayer)

Less authority than Regulations

17

Form of a Written Revenue Rulings

Similar to a tax memo in a client file:Issue: a statement of the issue in questionFacts: facts on which Revenue Ruling is

basedLaw and analysis: IRS’s application of

current law to the issueHolding: how IRS will treat the transaction

18

Example of a Temporary Rev. Rul. Citation

19

Example of a Permanent Rev. Rul. Citation

20

Revenue Procedures Concern IRS internal practices and procedures in

administering tax law

Used to release information to taxpayers

Same as Revenue Rulings in authority and citation

Published in IRB and Cumulative Bulletin

Example: Rev. Proc. 2001-21, 2001-1 C.B. 742

21

Letter Rulings

May come in the form of:Private Letter RulingsTechnical Advice MemorandaDetermination Letters

Available to the public through several commercial tax sources

22

Private Letter Rulings(1 of 2)

Issued by IRS National OfficeResponse to a taxpayer’s request on a

specific issue• Issued only to taxpayer who requested the ruling• Taxpayer describes proposed transaction and

business purpose

23

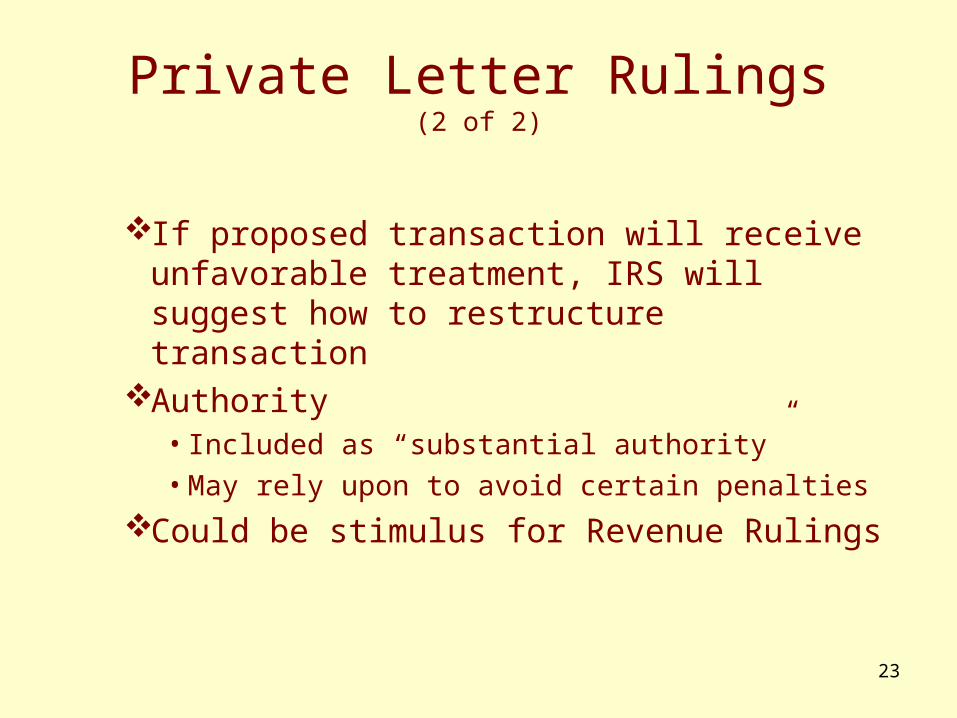

If proposed transaction will receive unfavorable treatment, IRS will suggest how to restructure transaction

Authority• Included as “substantial authority”• May rely upon to avoid certain penalties

Could be stimulus for Revenue Rulings

Private Letter Rulings(2 of 2)

24

Technical Advice Memoranda

Issued by IRS National OfficeConcern completed transactionsRequested by IRS agent during an auditAuthority

• May not be cited as authority• Rely on to avoid certain penalties

25

Determination Letters

Similar to Private Letter RulingsIssued by local IRS District Directors

Not controversialDeal with completed transactionsAuthority

• May not be cited as authority• Rely on to avoid certain penalties

26

Public Inspection of Written Determinations (1 of 2)

Public can receive copies of any unpublished IRS Letter RulingsPrivate Letter RulingsTechnical Advice MemorandaDetermination Letters

27

Public Inspection of Written Determinations (2 of 2)

Taxpayer’s name, other identifying information, and sensitive information are removed

Taxpayers who oppose disclosure of their written determination can bring matter before IRS and Tax Court prior to release

28

Citing Letter Rulings9 digits (7 digits prior to 2000)1st four digits: Year

• 2 digits prior to 2000

2nd two digits: WeekLast three digits: Ruling number

Written Determination Numbering System

29

Example of a Letter Ruling citation

30

Other IRS Pronouncements

Acquiescences and nonacquiescencesChief Council MemorandaAnnouncements and noticesMiscellaneous Publications

31

Acquiescences and Nonacquiescences

IRS decides to follow (acquiescence) or not follow in part or whole (non-acquiescence) a decision adverse to the IRS

Published in IRB and Cumulative BulletinBest to find in Citator or AOD file

32

Internal Revenue Bulletin

The IRS’s official publication for its pronouncements, which includes:Revenue Rulings and Revenue ProceduresAcquiescences and nonacquiescencesNew tax laws, issued by Congress as Public LawsCommittee Reports underlying tax statutesProcedural rulesNew tax treatiesTreasury Decisions (which become Regulations)Other notices

33

Chief Council Memoranda

General Council's Memorandum (GCM) generated upon request of the IRS to assist in preparing Revenue Rulings and Private Letter Rulings

Action on Decision (AOD) prepared when IRS loses a case in court (to acquiesce or nonacquiesce)

Others

34

Announcements and Notices

Concern items of general importance to taxpayers (e.g., notice to announce mailing of individual tax return forms)

35

Miscellaneous Publications

Numerous specialized documents available directly from the IRS

Documents prepared from the government’s point of view