Embed Size (px)

Citation preview

1

Chapter 2Chapter 2

Copyright ©2006 Thomson South-Western, Mason, Ohio

William A. Raabe, Gerald E. Whittenburg, &

Debra L. Sanders

Tax Research Tax Research MethodologyMethodology

2

3

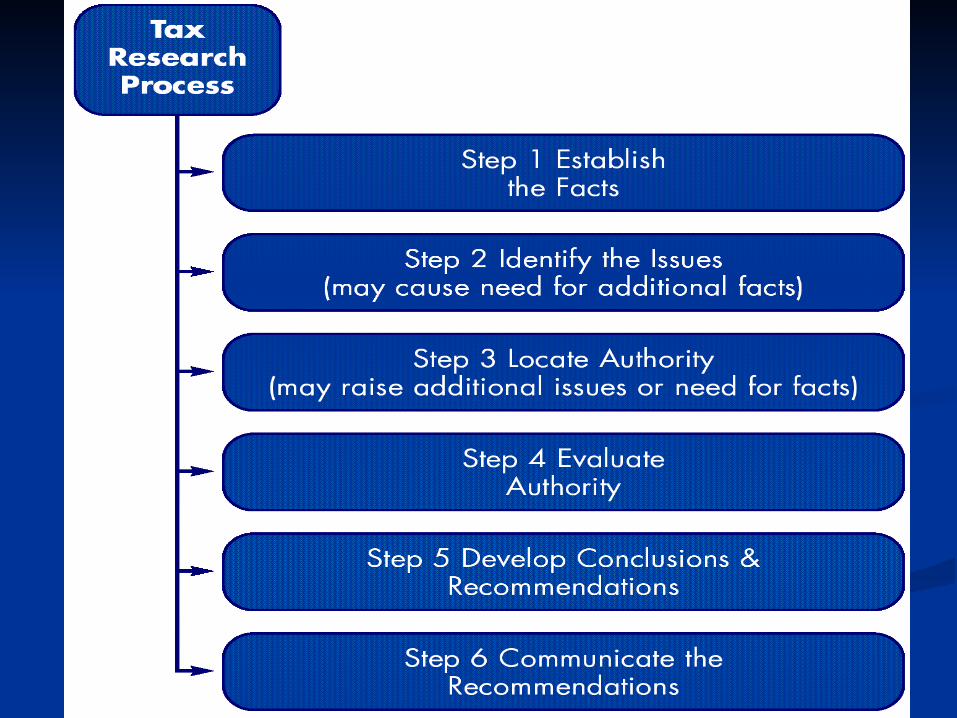

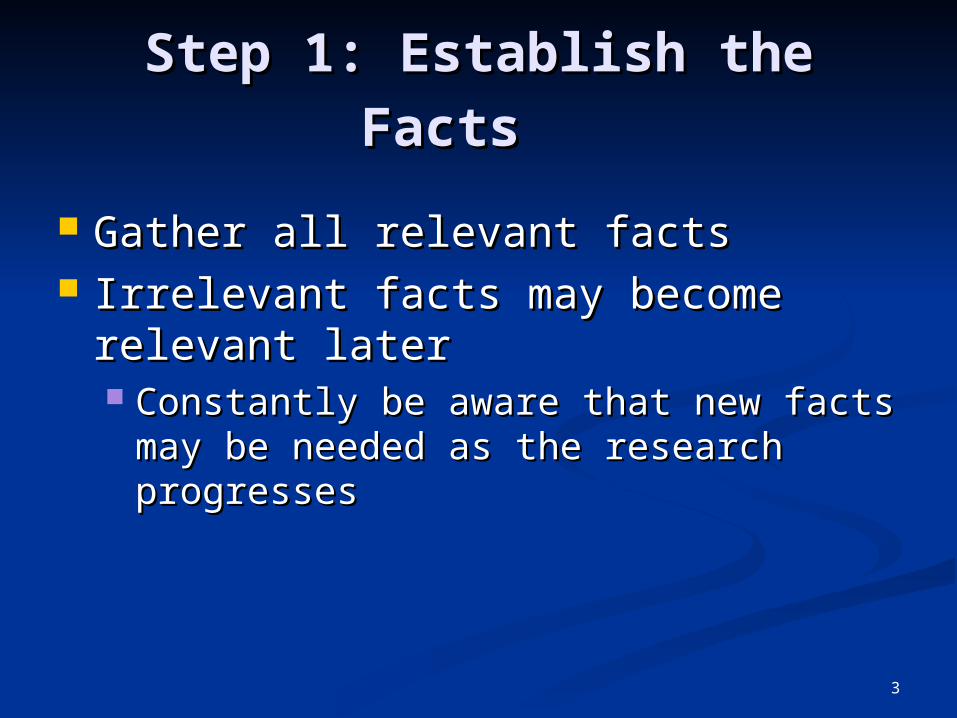

Step 1: Establish the FactsStep 1: Establish the Facts

Gather all relevant facts Gather all relevant facts Irrelevant facts may become Irrelevant facts may become

relevant laterrelevant later Constantly be aware that new facts may Constantly be aware that new facts may

be needed as the research progressesbe needed as the research progresses

4

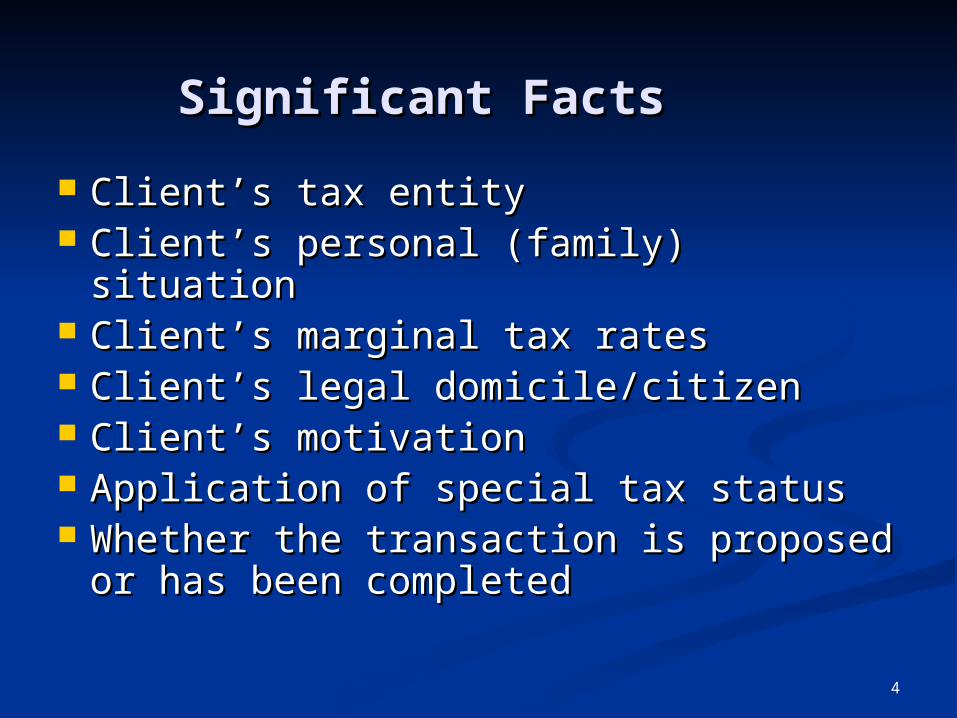

Significant FactsSignificant Facts Client’s tax entity Client’s tax entity Client’s personal (family) situationClient’s personal (family) situation Client’s marginal tax ratesClient’s marginal tax rates Client’s legal domicile/citizenClient’s legal domicile/citizen Client’s motivation Client’s motivation Application of special tax status Application of special tax status Whether the transaction is proposed Whether the transaction is proposed

or has been completedor has been completed

5

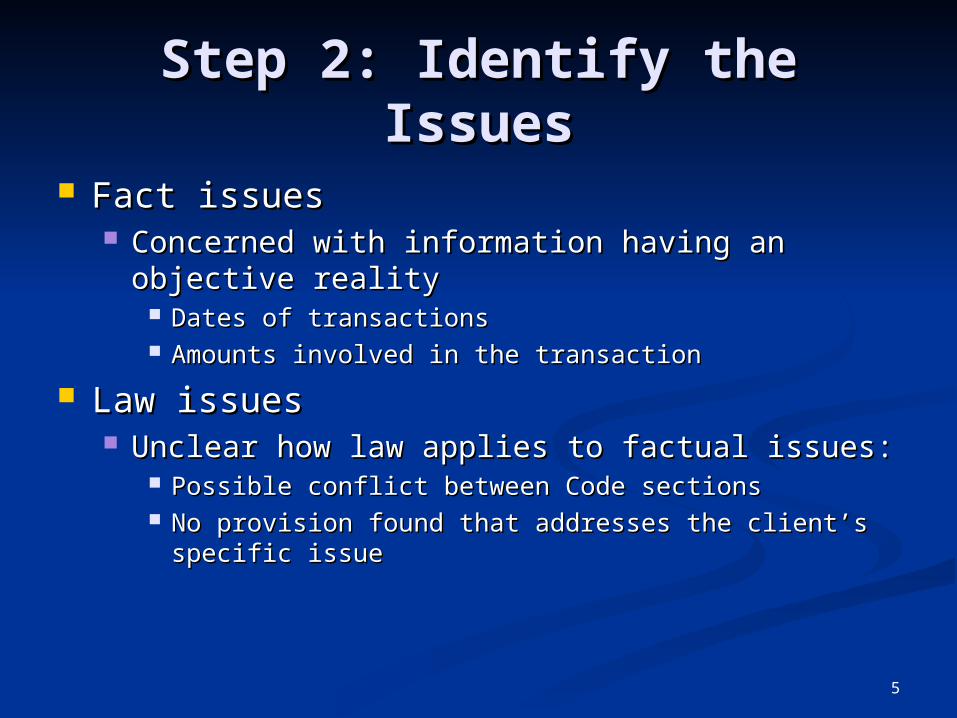

Step 2: Identify the IssuesStep 2: Identify the Issues

Fact issues Fact issues Concerned with information having an Concerned with information having an

objective realityobjective reality Dates of transactionsDates of transactions Amounts involved in the transactionAmounts involved in the transaction

Law issuesLaw issues Unclear how law applies to factual issues:Unclear how law applies to factual issues:

Possible conflict between Code sectionsPossible conflict between Code sections No provision found that addresses the client’s No provision found that addresses the client’s

specific issuespecific issue

6

Simple situations can generate many Simple situations can generate many research issues research issues

New issues may arise when solving New issues may arise when solving the original problem the original problem

Step 2: Identify the IssuesStep 2: Identify the Issues

7

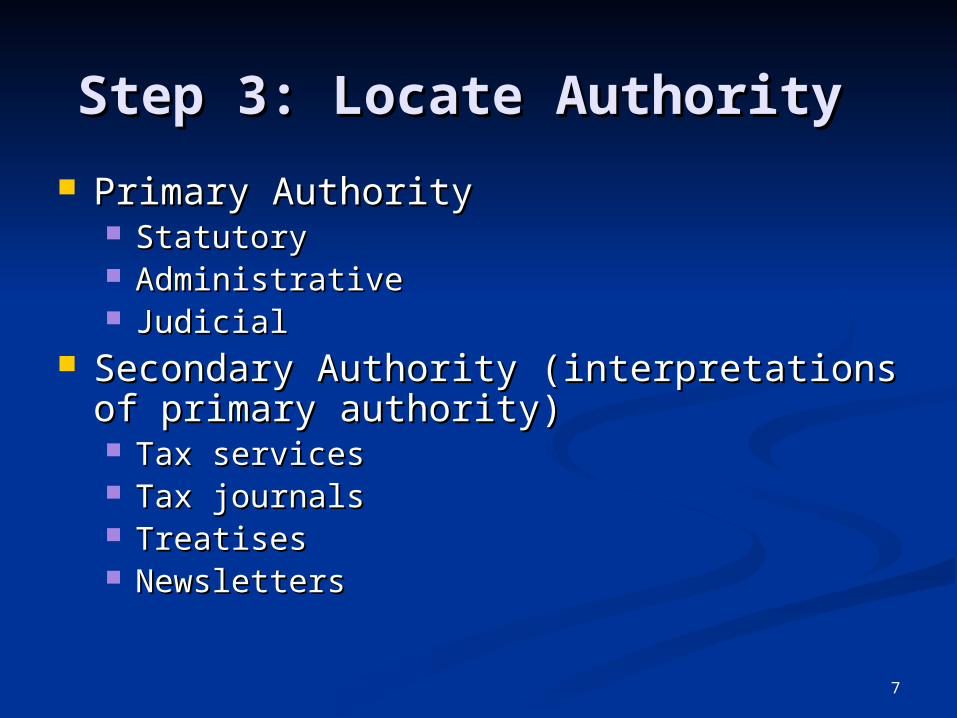

Step 3: Locate AuthorityStep 3: Locate Authority Primary AuthorityPrimary Authority

Statutory Statutory Administrative Administrative JudicialJudicial

Secondary Authority (interpretations of Secondary Authority (interpretations of primary authority)primary authority) Tax servicesTax services Tax journals Tax journals Treatises Treatises NewslettersNewsletters

8

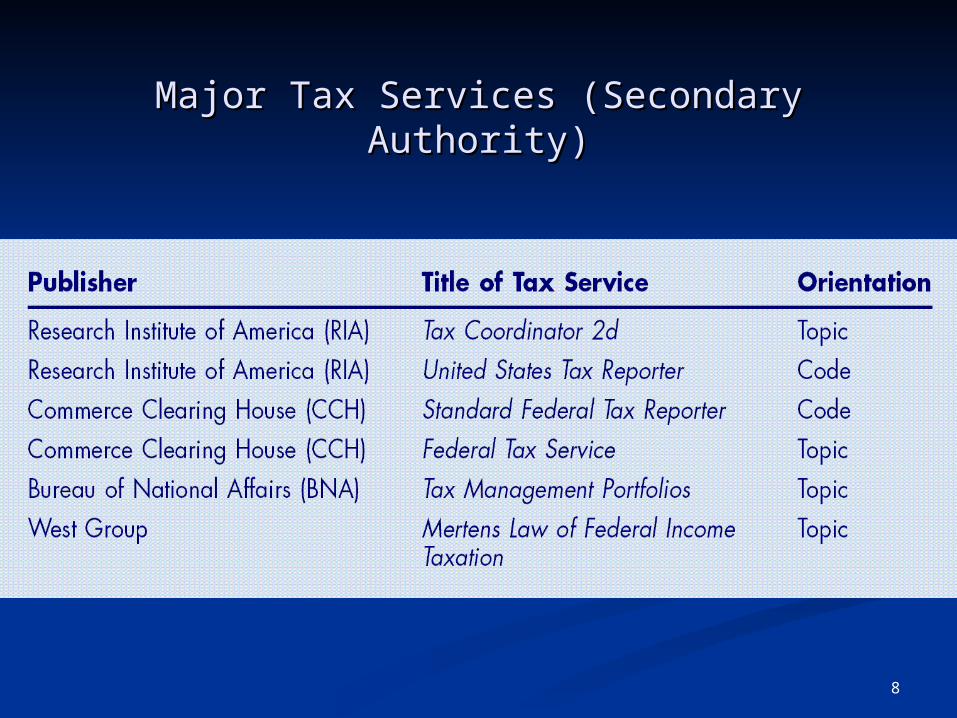

Major Tax Services (Secondary Authority)Major Tax Services (Secondary Authority)

9

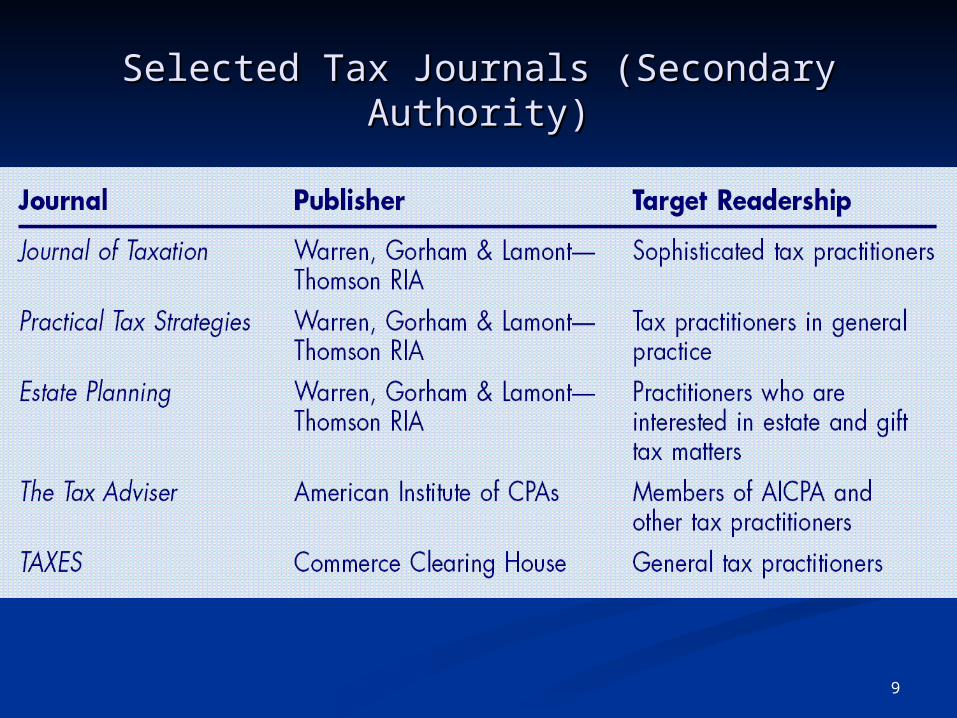

Selected Tax Journals (Secondary Authority)Selected Tax Journals (Secondary Authority)

10

Step 4: Evaluate AuthorityStep 4: Evaluate Authority Different authorities may suggest Different authorities may suggest

different treatments (e.g., courts vs. different treatments (e.g., courts vs. IRS)IRS)

Different authorities have different Different authorities have different precedential values precedential values

11

Step 5: Develop Step 5: Develop Conclusions & Conclusions &

RecommendationsRecommendations May have no single “best” May have no single “best”

alternative alternative Alternatives must be considered Alternatives must be considered

Recommendations should include Recommendations should include alternatives where appropriatealternatives where appropriate

12

Step 6: Communicate the Step 6: Communicate the RecommendationsRecommendations

Memo to client fileMemo to client file Include the facts, assumptions, issues, Include the facts, assumptions, issues,

authorities, and recommendationsauthorities, and recommendations Letter to clientLetter to client

Be certain to use clear language for Be certain to use clear language for client understandingclient understanding

13

Overview of Overview of Computerized Tax Computerized Tax

ResearchResearch Online systems and CD-ROM Systems Online systems and CD-ROM Systems Benefits of using a computerized tax Benefits of using a computerized tax

serviceservice Factors in choosing a computerized tax Factors in choosing a computerized tax

serviceservice Using a computer in tax researchUsing a computer in tax research IRS web site researchIRS web site research

14

Online SystemsOnline Systems

Online tax research systemsOnline tax research systems Accessible with a computer through the Accessible with a computer through the

internetinternet Documents may be printed or saved to Documents may be printed or saved to

computercomputer

15

Online Tax ResearchOnline Tax Research

RIA CheckpointRIA Checkpoint CCH Tax Research NetworkCCH Tax Research Network BNABNA LexisNexisLexisNexis WestlawWestlaw

16

CD-ROM SystemsCD-ROM Systems

CD-ROM tax research systemsCD-ROM tax research systems Similar to online tax research systems Similar to online tax research systems

except databases are stored on CD-except databases are stored on CD-ROMs instead of central computers ROMs instead of central computers that are accessible through the internetthat are accessible through the internet

17

Benefits of Using a Benefits of Using a ComputerizedComputerized

Tax ServiceTax Service Current law (updated daily)Current law (updated daily) Create searches using key termsCreate searches using key terms Hyperlinks allow ease of moving among Hyperlinks allow ease of moving among

documentsdocuments Computer can quickly process large Computer can quickly process large

volume of materialvolume of material Cost effectiveCost effective

18

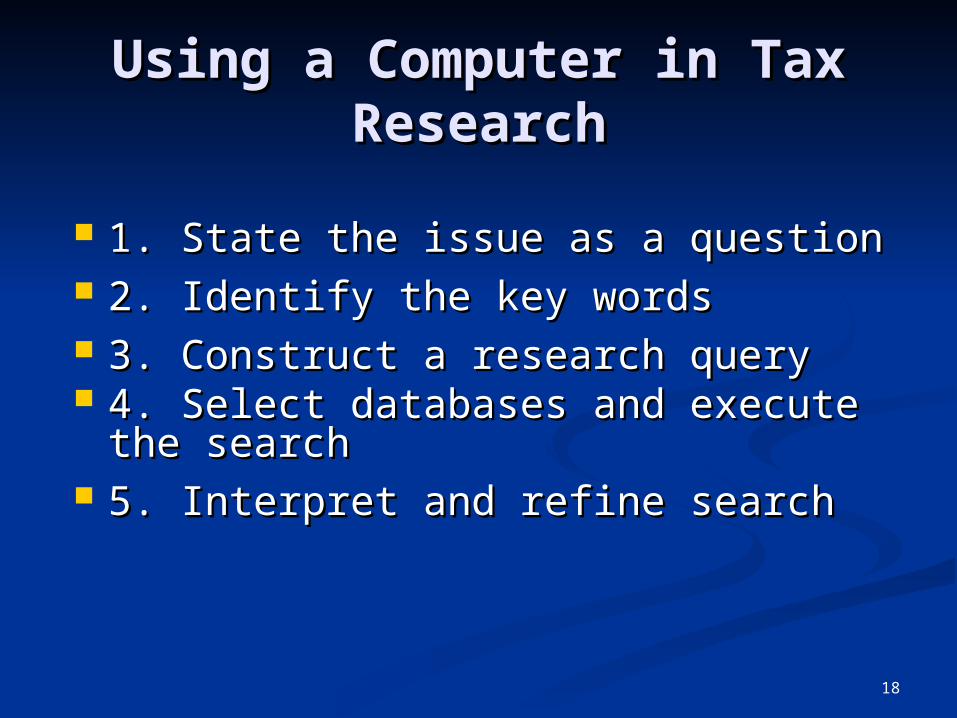

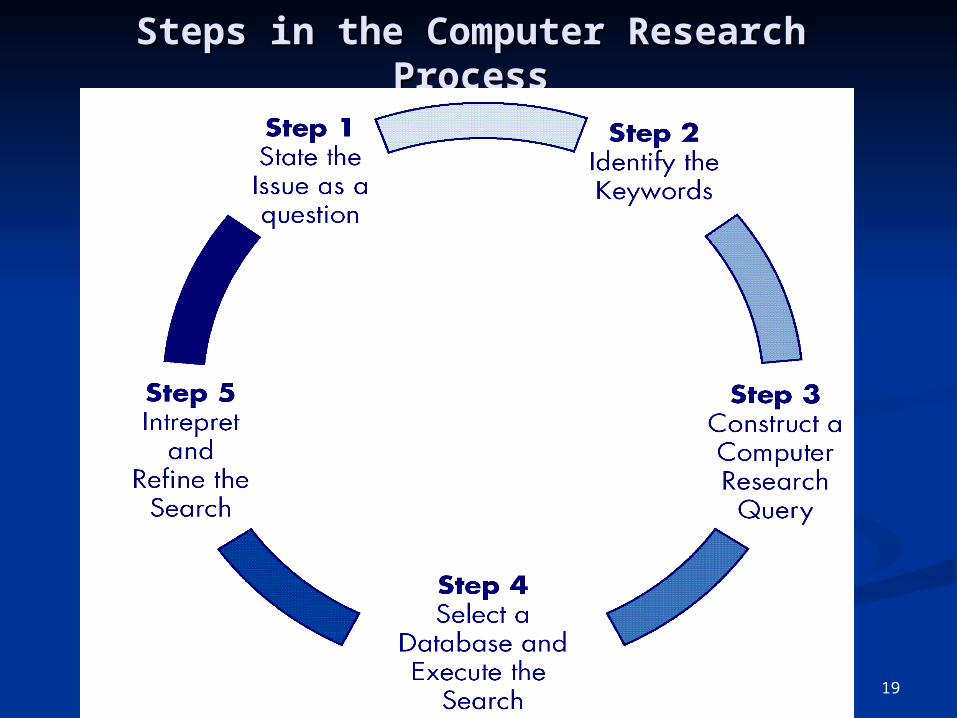

Using a Computer in Tax Using a Computer in Tax ResearchResearch

1. State the issue as a question1. State the issue as a question 2. Identify the key words2. Identify the key words 3. Construct a research query3. Construct a research query 4. Select databases and execute 4. Select databases and execute

the searchthe search 5. Interpret and refine search5. Interpret and refine search

19

Steps in the Computer Research Steps in the Computer Research ProcessProcess

20

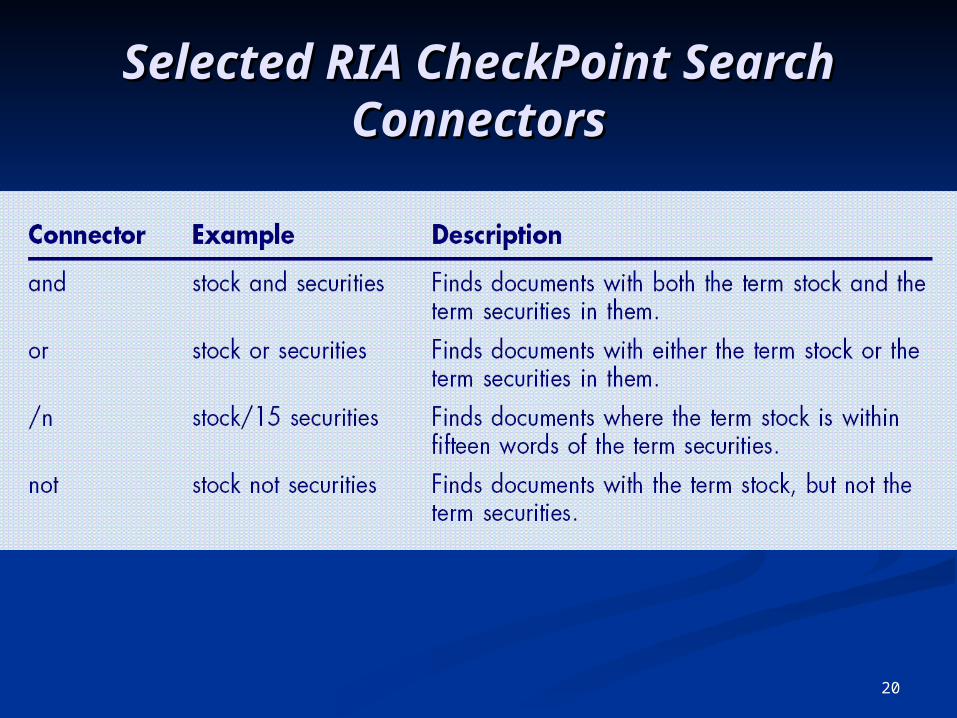

Selected RIA CheckPoint Selected RIA CheckPoint Search ConnectorsSearch Connectors

21

IRS Web Site ResearchIRS Web Site Research

IRS web IRS web site is not a full-service tax site is not a full-service tax research siteresearch site

Limited tax research can be conductedLimited tax research can be conducted Contains searchable and downloadable Contains searchable and downloadable

tax information including:tax information including: Tax forms,Tax forms, Instructions,Instructions, IRS publications, andIRS publications, and Other IRS informationOther IRS information

![[Paul R. Raabe] Psalm Structures a Study of Psalm(BookFi.org)](https://img.pdfslide.us/doc/110x75/55cf9730550346d033902bb9/paul-r-raabe-psalm-structures-a-study-of-psalmbookfiorg.jpg)