Embed Size (px)

Citation preview

1

C

H A

P T

E R

3

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Markets in the Global Economy

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Markets in the Global Economy

A market system facilitates the exchange of money and products.

Markets exist because individuals are not self-sufficient but instead consume many products produced by others.

A market is an arrangement that allows buyers and sellers to exchange things.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Specialization and the Gains From Trade

We can use the principle of opportunity cost to explain the benefits from specialization and trade.

PRINCIPLE of Opportunity CostThe opportunity cost of something is what you sacrifice to get it.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Specialization and the Gains From Trade

Why do we specialize? Because output for society as a whole will

increase if the task of producing something is assigned to the country or person who can produce it more efficiently.

Each of us specializes in producing just a few products and uses the market to exchange goods and services.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

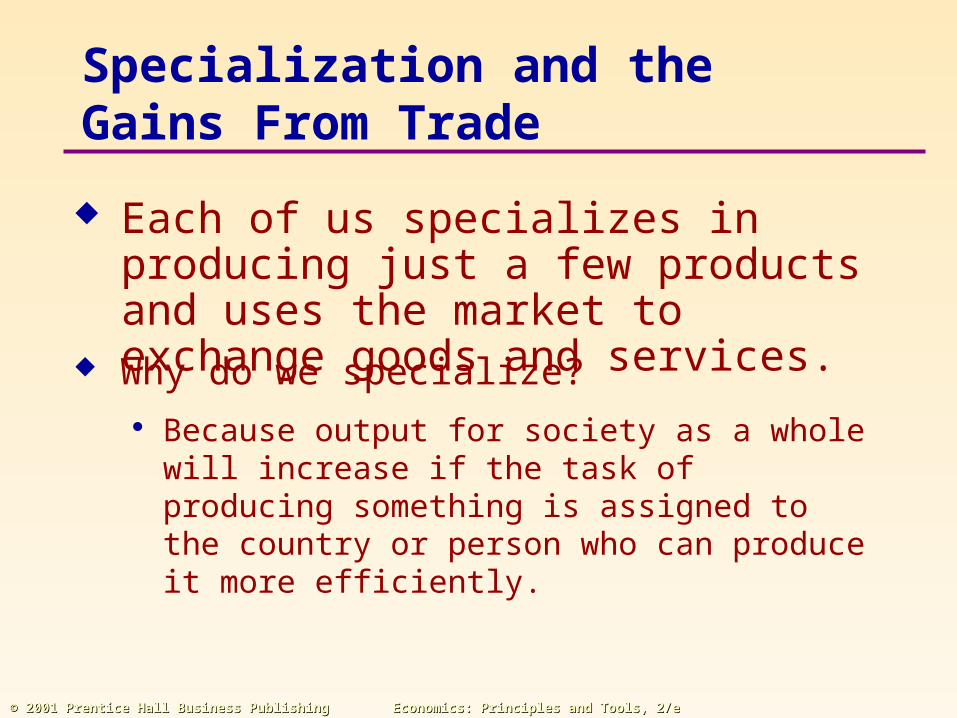

Absolute Versus Comparative Advantage

Consider this productivity table.

However, the decision as to who should specialize in the production of one good or the other is based not on absolute but on comparative advantage.

Brenda can produce more bread or shirts per hour than Sam. Therefore, she has an absolute advantage over Sam.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

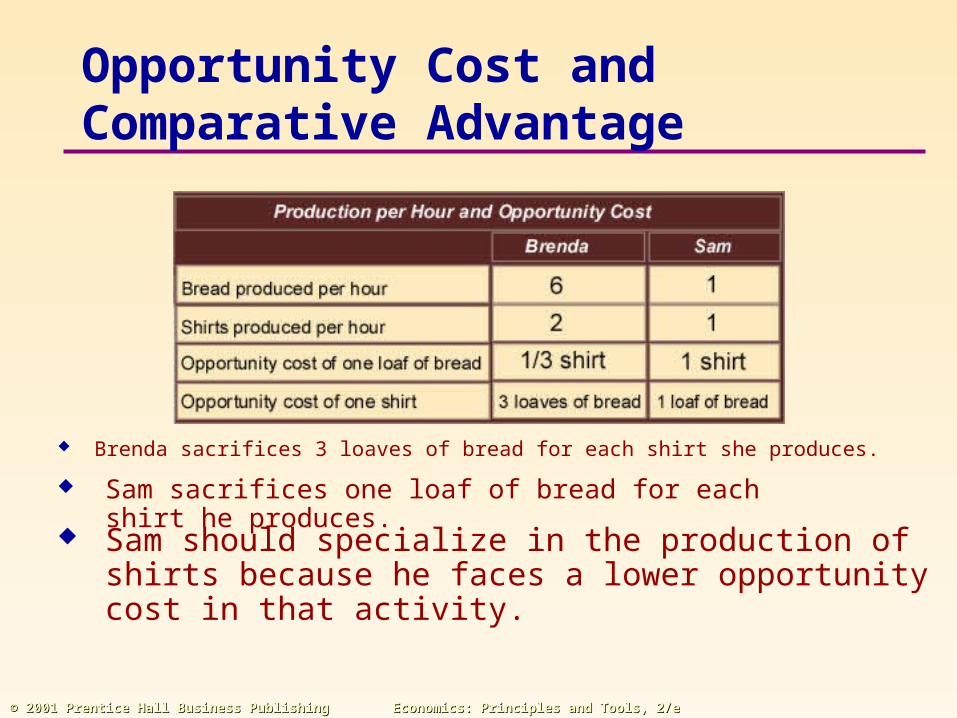

Opportunity Cost and Comparative Advantage

Brenda sacrifices 3 loaves of bread for each shirt she produces. Sam sacrifices one loaf of bread for each shirt he produces.

Sam should specialize in the production of shirts because he faces a lower opportunity cost in that activity.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Opportunity Cost and Comparative Advantage

Specialization is beneficial if there are differences in opportunity cost that generate a comparative advantage.

Comparative advantage is the ability of one person or nation to produce a good at an opportunity cost that is lower than the opportunity cost of another person or nation.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

The Circular Flow Diagram

The circular flow diagram is a schematic representation of output and input markets, and the role of participants in those markets, mainly households and business firms.

• Factor, or input markets allow owners of land, labor and capital to sell these resources to organizations that will transform them into goods.

• Product, or output markets allow organizations to sell their goods and services to consumers.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Households and Firms

A household is an individual or group of people who live in the same housing unit.

A firm is an organization that uses resources to produce a product for sale.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

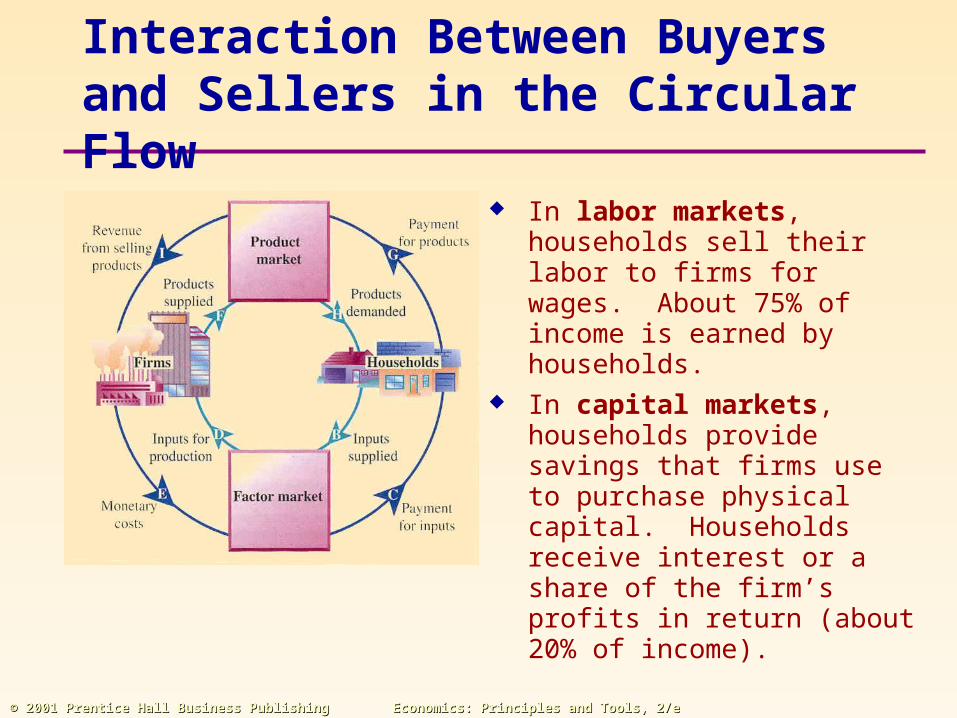

Interaction Between Buyers and Sellers in the Circular Flow

In labor markets, households sell their labor to firms for wages. About 75% of income is earned by households.

In capital markets, households provide savings that firms use to purchase physical capital. Households receive interest or a share of the firm’s profits in return (about 20% of income).

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

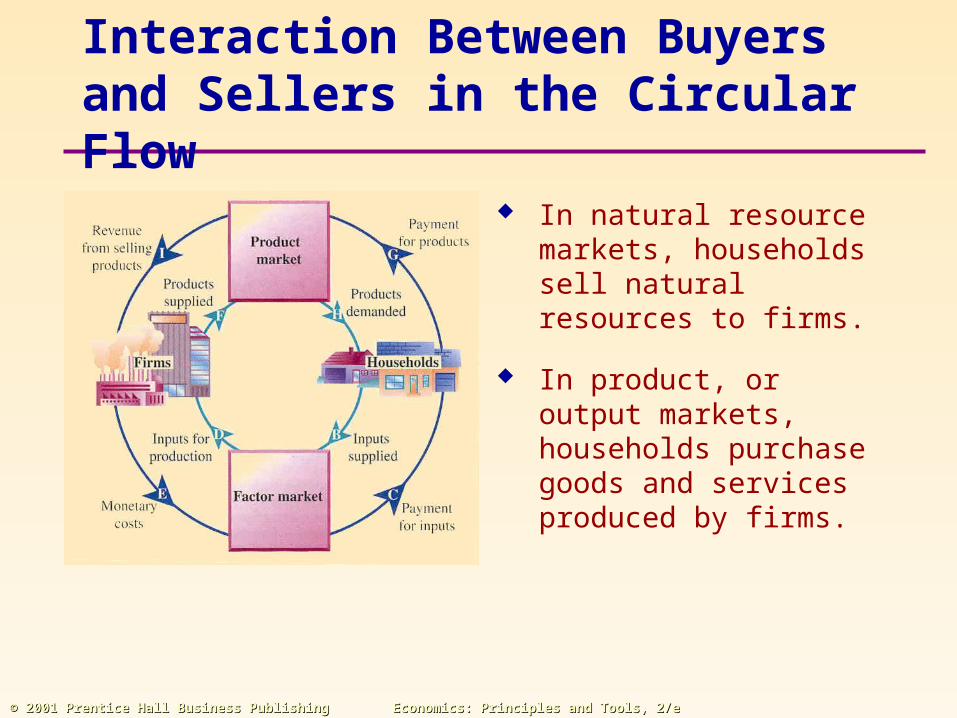

Interaction Between Buyers and Sellers in the Circular Flow

In natural resource markets, households sell natural resources to firms.

In product, or output markets, households purchase goods and services produced by firms.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

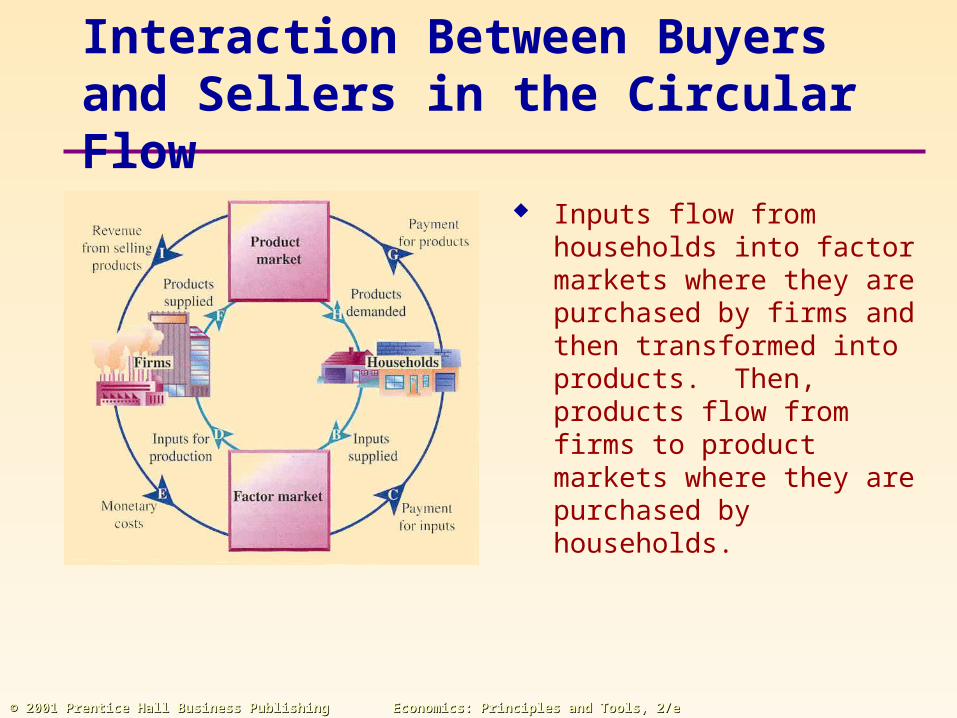

Interaction Between Buyers and Sellers in the Circular Flow

Inputs flow from households into factor markets where they are purchased by firms and then transformed into products. Then, products flow from firms to product markets where they are purchased by households.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

The Global Economy

Exports are goods produced in this country and sold elsewhere. Imports are goods produced elsewhere and sold in this country.

Trade among countries is based on the same principles of trade between individuals. Specialization based on comparative advantage results in gains for all participants.

Smaller nations rely more on trade because they have fewer opportunities for specialization within their borders.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Currency Markets and Exchange Rates

Foreign exchange markets allow people to exchange one currency for another. The exchange rate is the price of one currency in terms of another.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

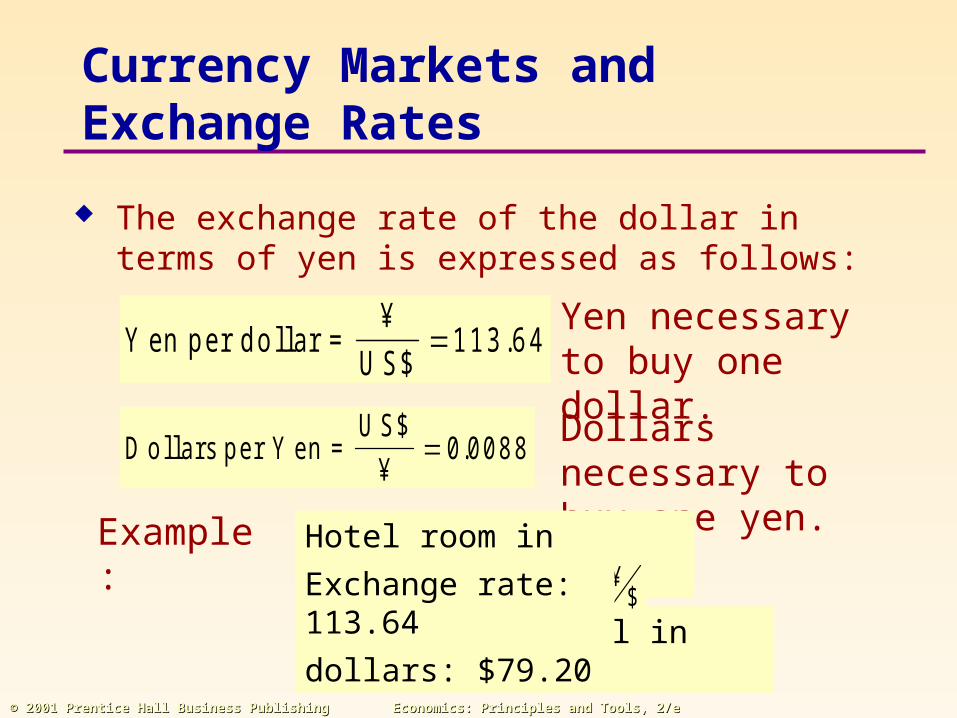

Currency Markets and Exchange Rates

The exchange rate of the dollar in terms of yen is expressed as follows:

Y en p er d o llar =¥

U S11 3 .6 4

$

D o llars p e r Y en =U S

¥0

$. 0 0 8 8

Yen necessary to buy one dollar.

Dollars necessary to buy one yen.

Hotel room in Japan: ¥ 9,000

Cost of the hotel in dollars: $79.20

Example:¥

$Exchange rate: 113.64

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

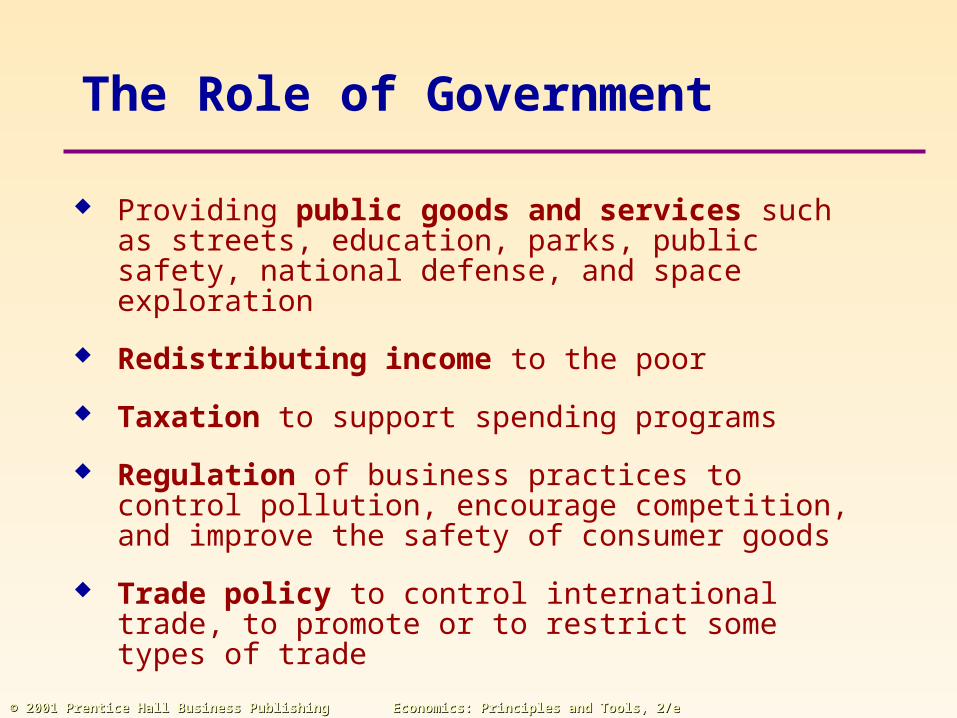

The Role of Government

Providing public goods and services such as streets, education, parks, public safety, national defense, and space exploration

Redistributing income to the poor

Taxation to support spending programs

Regulation of business practices to control pollution, encourage competition, and improve the safety of consumer goods

Trade policy to control international trade, to promote or to restrict some types of trade

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

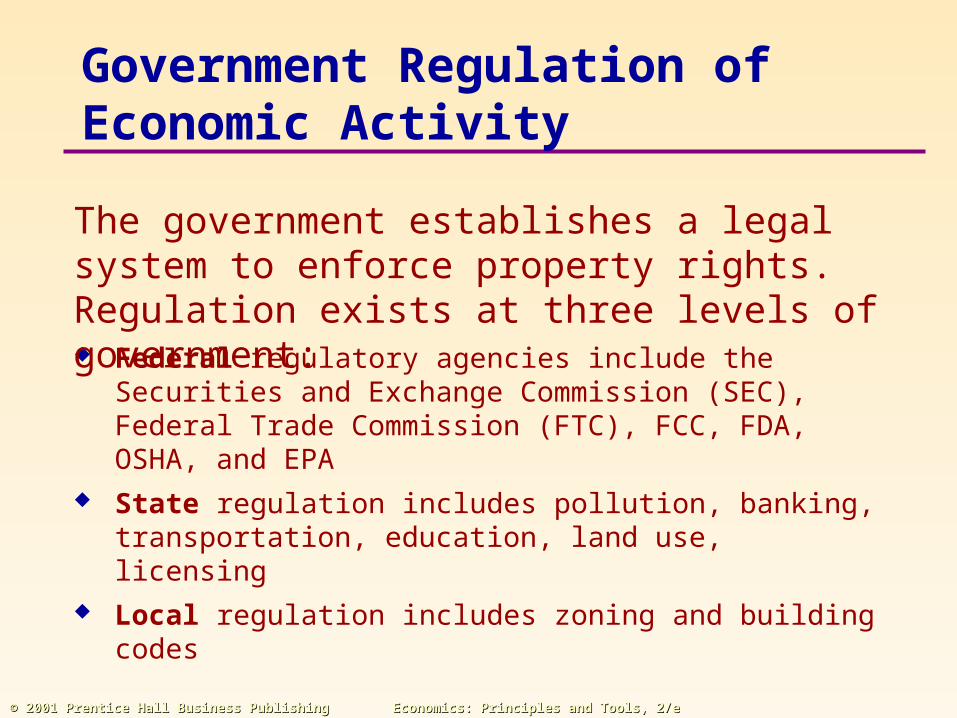

Government Regulation of Economic Activity

Federal regulatory agencies include the Securities and Exchange Commission (SEC), Federal Trade Commission (FTC), FCC, FDA, OSHA, and EPA

State regulation includes pollution, banking, transportation, education, land use, licensing

Local regulation includes zoning and building codes

The government establishes a legal system to enforce property rights. Regulation exists at three levels of government:

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

The United States has a mixed economy because it combines a free-market system with extensive government interaction.

An alternative to a market system is a centrally planned economy in which production and consumption choices are made by a central government rather than by markets.

Most of the formerly centrally planned economies have been making a transition to a market system. This is a difficult process that requires privatization of previously state-owned firms and resources.

Alternative Economic Systems —

Centrally Planned Economies

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Protectionist Policies

Tariffs or taxes on imports

Quotas or limits on the quantity of imports

Voluntary export restraints or agreements between governments to limit imports

Nontariff trade barriers or subtle practices that hinder trade

Trade barriers are rules that restrict the free flow of goods between nations. They include:

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Tariff and Trade Agreements

GATT, the General Agreement on Tariffs and Trade, was initiated in 1947 by the United States and 23 other countries to lower tariff barriers among participants. It has over 100 members today.

WTO, the World Trade Organization, is an organization that oversees GATT and other international trade agreements.

© 2001 Prentice Hall Business Publishing© 2001 Prentice Hall Business Publishing Economics: Principles and Tools, 2/eEconomics: Principles and Tools, 2/e O’Sullivan & SheffrinO’Sullivan & Sheffrin

Tariff and Trade Agreements

NAFTA, the North American Free Trade Agreement, which took effect in 1994, lowers barriers between the United States, Mexico, and Canada.

EU, the European Union, has reduced trade barriers within Europe; 15 nations are members.

APEC, the Asian Pacific Economic Cooperation, is an 18-member organization of Asian nations that attempts to reduce trade barriers.