Embed Size (px)

Citation preview

1Brenda Mallouk

Overhead Variance Analysis

Management Accounting One

2Brenda Mallouk

• Compare to original plans

• Pinpoint discrepancies

• Take corrective action

Advantage of Identification of Variances

3Brenda Mallouk

Analyzing Overhead Variances

Split mixed costs into their fixed

Establish a fixed overhead rate anda variable overhead rate

and variable components

4Brenda Mallouk

Overhead Variances Can Result From

Actual Overhead > or < Budget

Actual Production > or < 100% of Normal Capacity

5Brenda Mallouk

Two Way Variance Analysis

Overhead Budget (Controllable) Variance

Overhead Volume Variance

(combines the spending and efficiency overhead variances)

6Brenda Mallouk

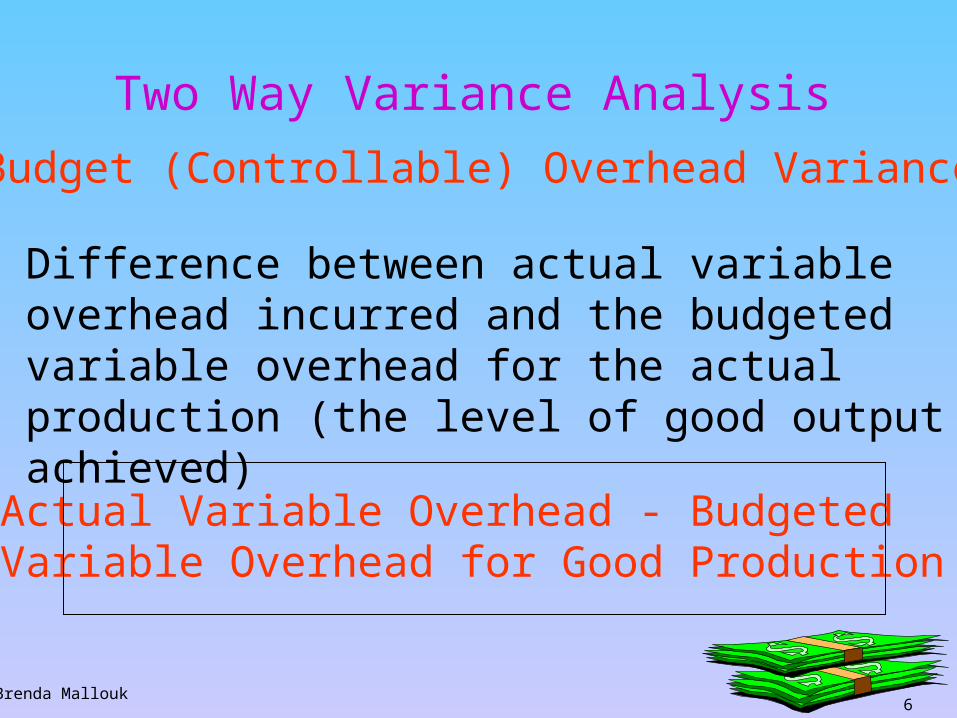

Budget (Controllable) Overhead Variance

Two Way Variance Analysis

Difference between actual variable overhead incurred and the budgeted variable overhead for the actual production (the level of good output achieved)

Actual Variable Overhead - Budgeted Variable Overhead for Good Production

7Brenda Mallouk

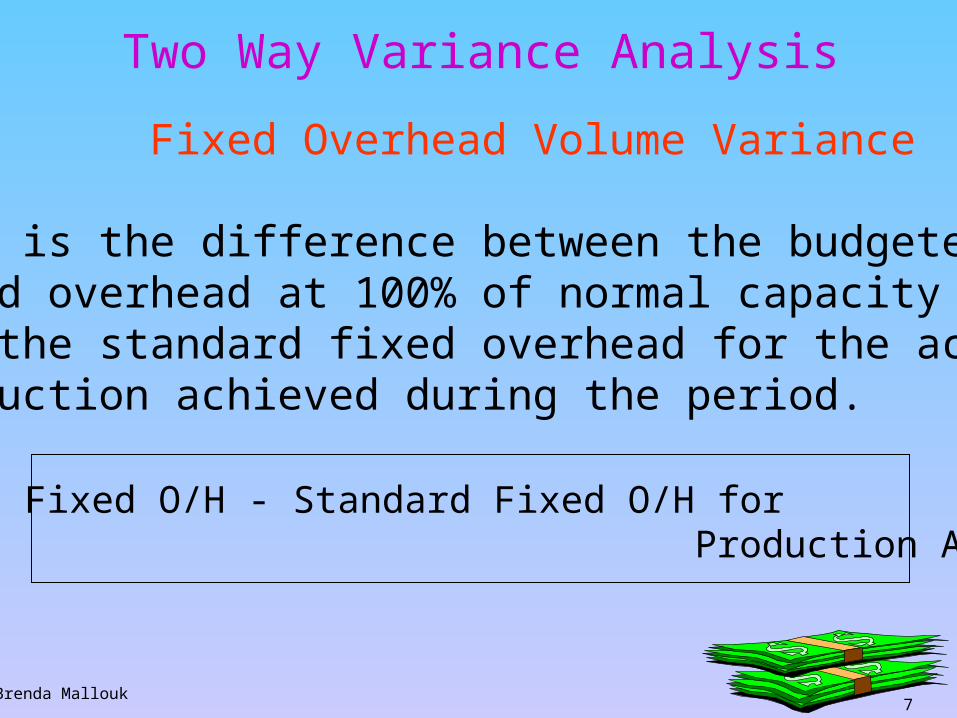

Fixed Overhead Volume Variance This is the difference between the budgetedfixed overhead at 100% of normal capacityand the standard fixed overhead for the actualproduction achieved during the period.

Budgeted Fixed O/H - Standard Fixed O/H for Production Attained

Two Way Variance Analysis

8Brenda Mallouk

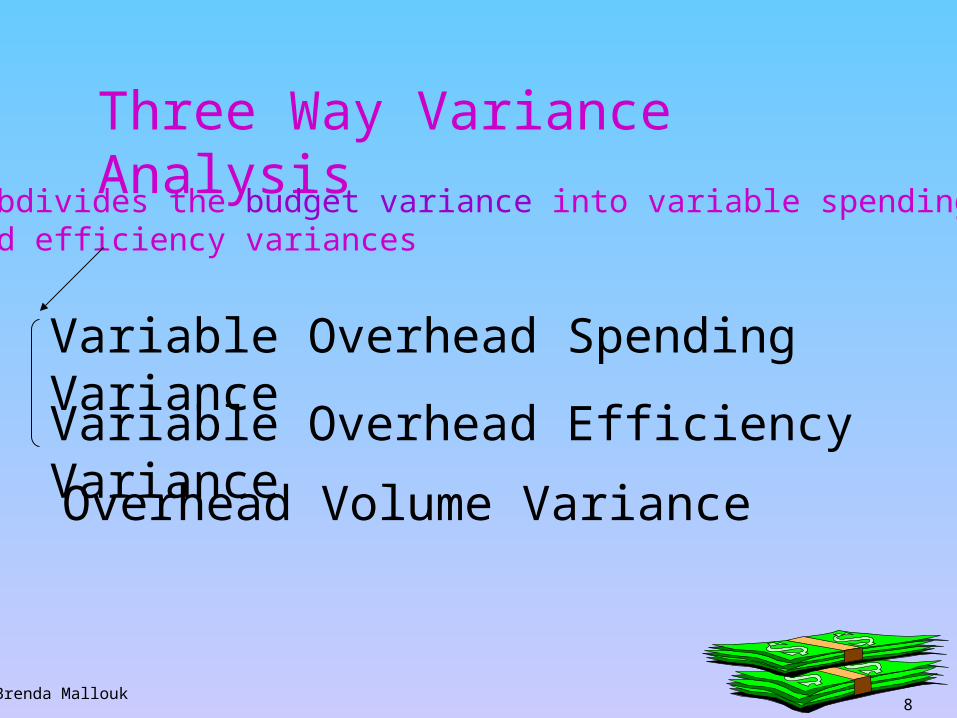

Three Way Variance Analysis

Variable Overhead Spending Variance

Overhead Volume Variance

Variable Overhead Efficiency Variance

subdivides the budget variance into variable spending and efficiency variances

9Brenda Mallouk

Indicates the difference between actual variableoverhead costs and variable overhead costsallowed for the actual hours

Three Way Analysis

Variable Overhead Spending Variance --

Formula:

Total Actual Variable Overhead Costs - (Actual Hours x Standard Variable Overhead Rate)

10Brenda Mallouk

Three Way Analysis

Indicates the difference between the standardvariable overhead cost for actual hours and thestandard variable overhead cost for the allowed hours for the production attained.

Variable Overhead Efficiency Variance --

Formula:

(Actual Hours x Standard Variable Overhead Rate) - (SHA x SVR)

11Brenda Mallouk

Three Way Analysis

Overhead Volume Variance

Same as two way variance analysis

12Brenda Mallouk

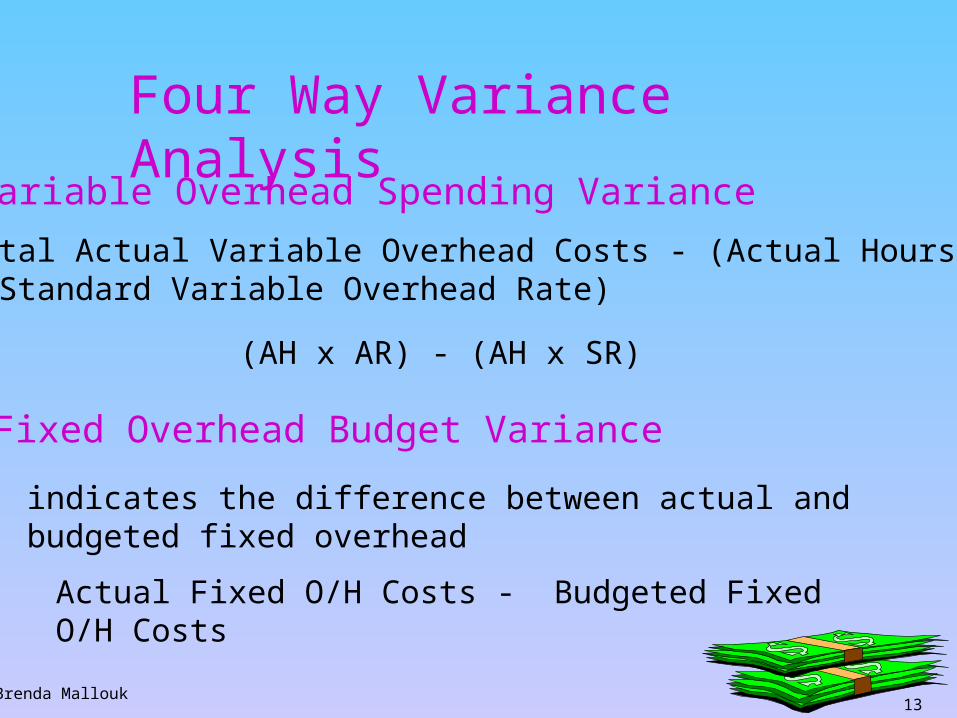

Four Way Variance Analysis

Variable Overhead Spending Variance

Fixed Overhead Volume Variance

Variable Overhead Efficiency Variance

Fixed Overhead Budget Variance *

* (Indicates the difference between actual and budgeted fixed factory overhead)

13Brenda Mallouk

Four Way Variance Analysis

Variable Overhead Spending Variance

(AH x AR) - (AH x SR)

Fixed Overhead Budget Variance

indicates the difference between actual and budgeted fixed overhead

Actual Fixed O/H Costs - Budgeted Fixed O/H Costs

Total Actual Variable Overhead Costs - (Actual Hoursx Standard Variable Overhead Rate)

14Brenda Mallouk

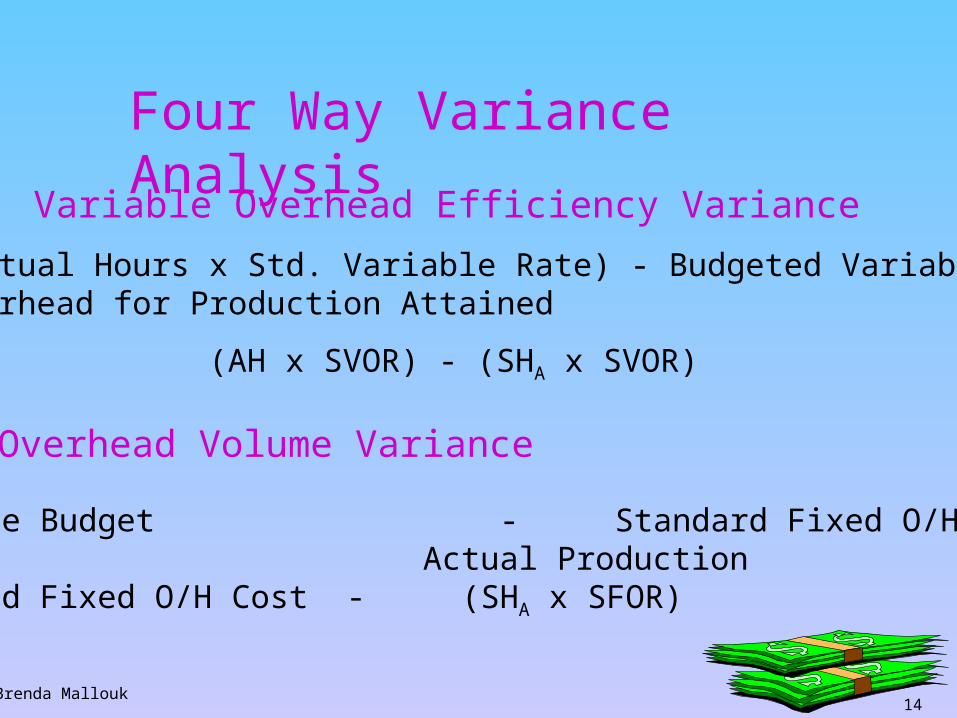

Four Way Variance Analysis

Variable Overhead Efficiency Variance

(AH x SVOR) - (SHA x SVOR)

(Actual Hours x Std. Variable Rate) - Budgeted VariableOverhead for Production Attained

Overhead Volume Variance

Flexible Budget - Standard Fixed O/H for Actual Production

Budgeted Fixed O/H Cost - (SHA x SFOR)

15Brenda Mallouk

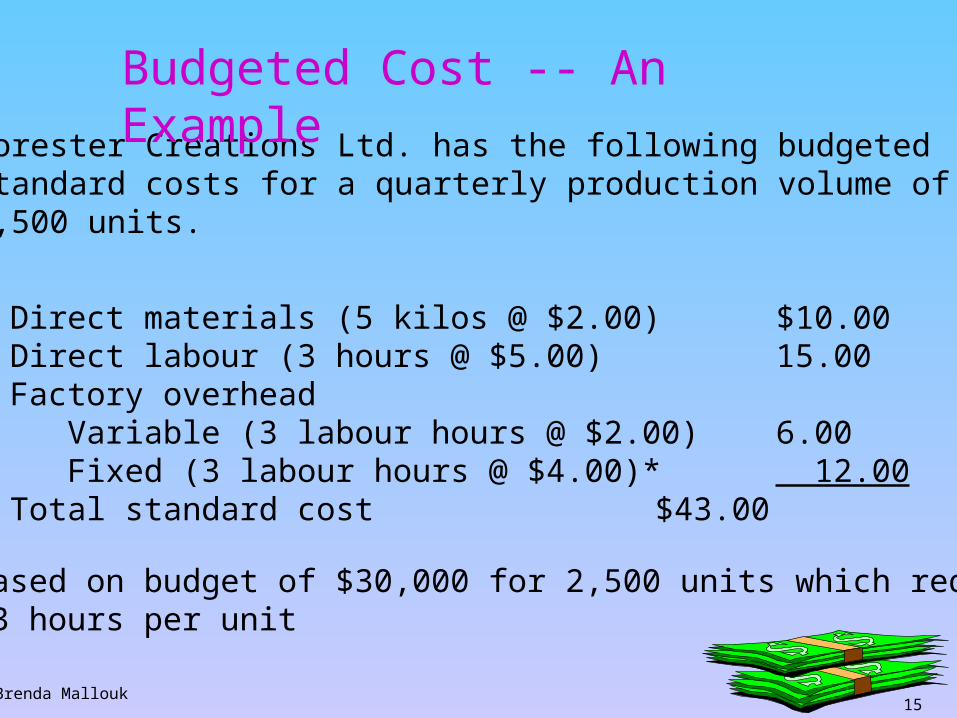

Forester Creations Ltd. has the following budgetedstandard costs for a quarterly production volume of 2,500 units.

Budgeted Cost -- An Example

Direct materials (5 kilos @ $2.00) $10.00Direct labour (3 hours @ $5.00) 15.00Factory overhead Variable (3 labour hours @ $2.00) 6.00 Fixed (3 labour hours @ $4.00)* 12.00Total standard cost $43.00

* based on budget of $30,000 for 2,500 units which require 3 hours per unit

16Brenda Mallouk

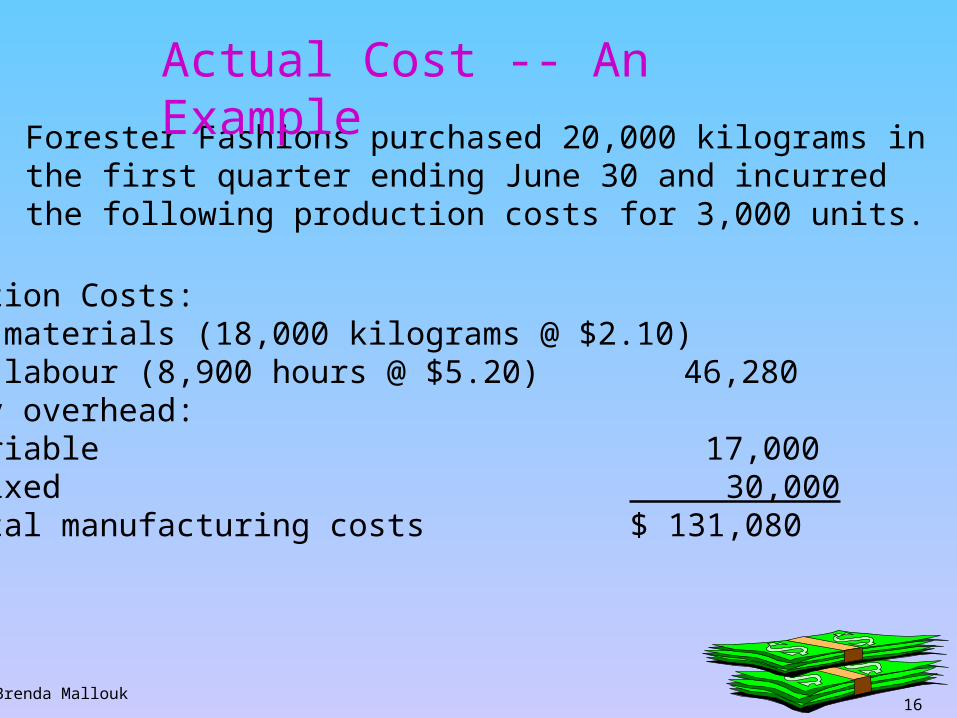

Forester Fashions purchased 20,000 kilograms in the first quarter ending June 30 and incurred the following production costs for 3,000 units.

Production Costs:Direct materials (18,000 kilograms @ $2.10) 37,800Direct labour (8,900 hours @ $5.20) 46,280 Factory overhead: Variable 17,000 Fixed 30,000 Total manufacturing costs $ 131,080

Actual Cost -- An Example

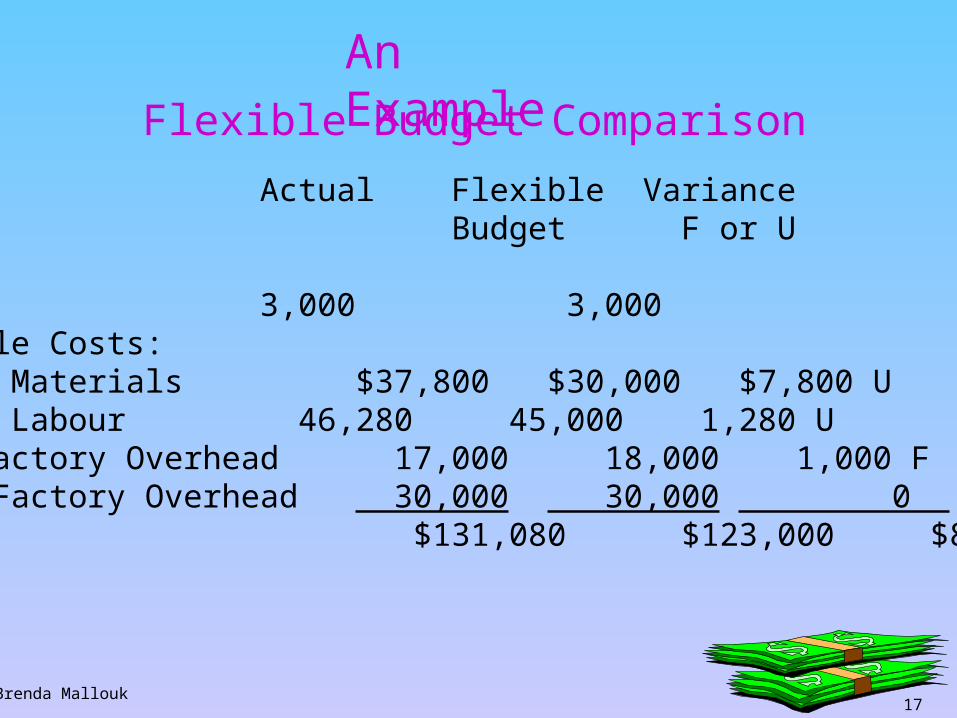

17Brenda Mallouk

Flexible Budget Comparison

Actual Flexible VarianceBudget F or U

Volume 3,000 3,000Variable Costs:Direct Materials $37,800 $30,000 $7,800 UDirect Labour 46,280 45,000 1,280 UVar. Factory Overhead 17,000 18,000 1,000 FFixed Factory Overhead 30,000 30,000 0 Total $131,080 $123,000 $8,080 U

An Example

18Brenda Mallouk

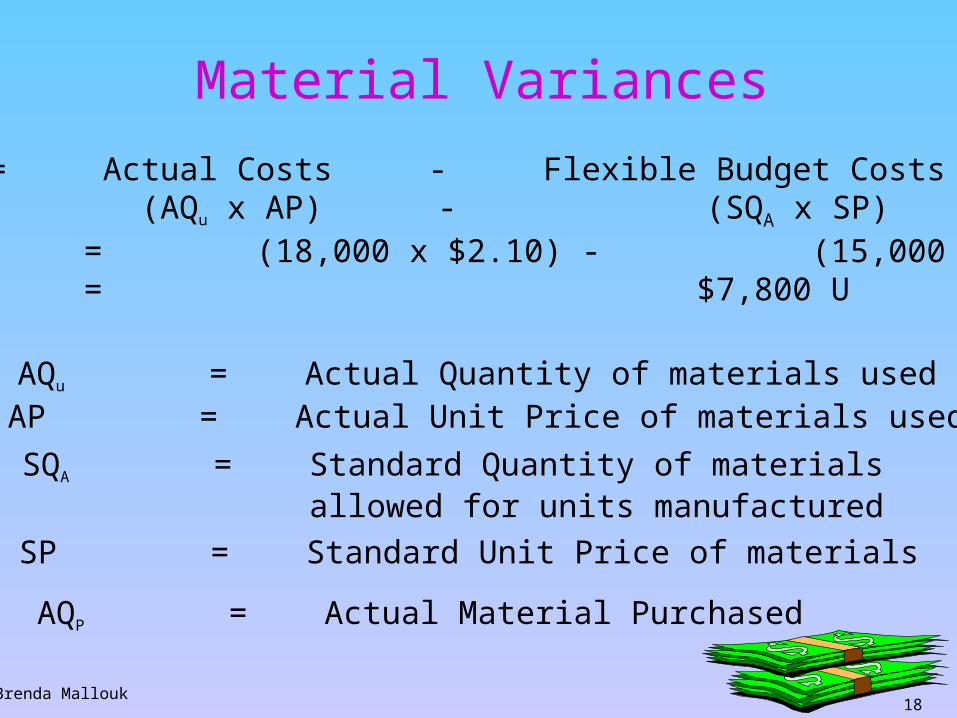

Material Variances

TMV = Actual Costs - Flexible Budget Costs (AQu x AP) - (SQA x SP)

= (18,000 x $2.10) - (15,000 x $2) = $7,800 U

AQu = Actual Quantity of materials used

SP = Standard Unit Price of materials

SQA = Standard Quantity of materialsallowed for units manufactured

AP = Actual Unit Price of materials used

AQP = Actual Material Purchased

19Brenda Mallouk

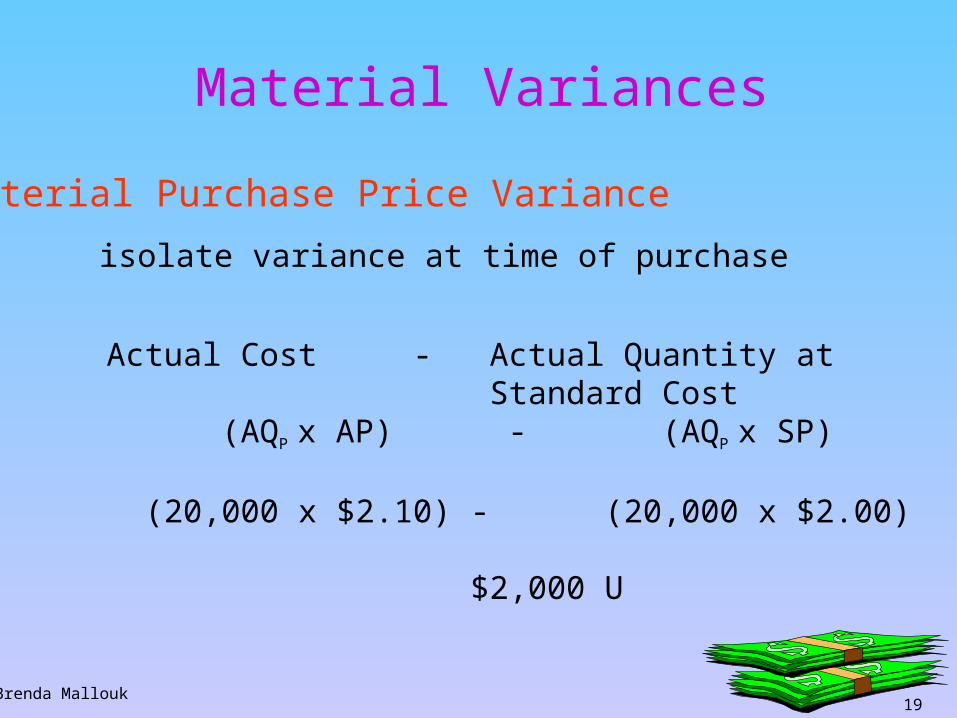

Material Variances

Actual Cost - Actual Quantity at Standard Cost

(AQP x AP) - (AQP x SP)

(20,000 x $2.10) - (20,000 x $2.00)

$2,000 U

Material Purchase Price Variance

isolate variance at time of purchase

20Brenda Mallouk

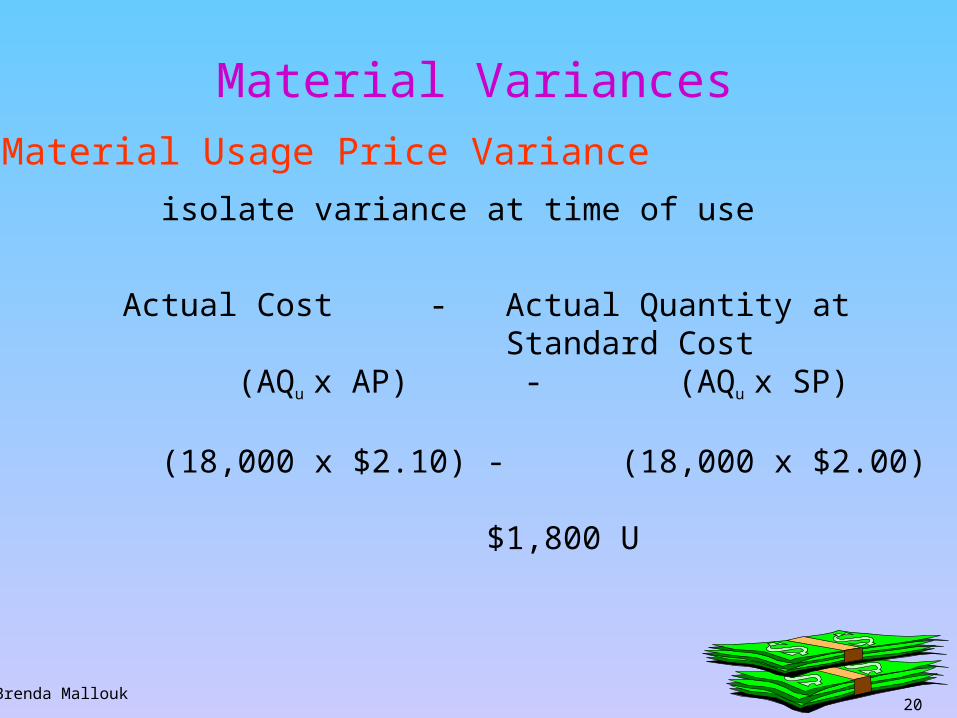

Material Variances

Actual Cost - Actual Quantity at Standard Cost

(AQu x AP) - (AQu x SP)

(18,000 x $2.10) - (18,000 x $2.00)

$1,800 U

Material Usage Price Variance

isolate variance at time of use

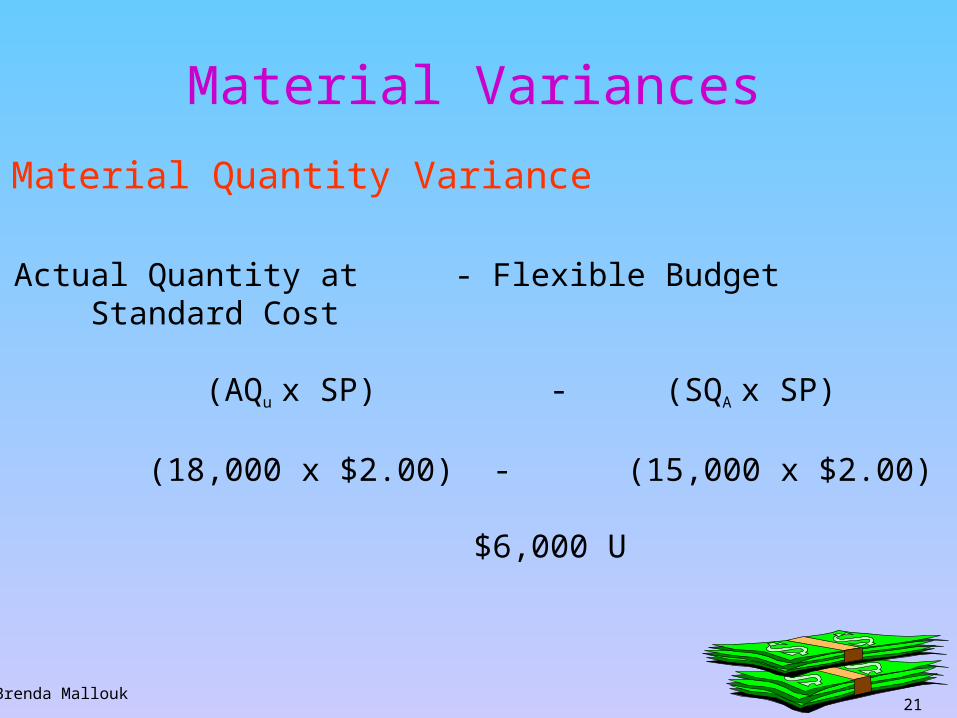

21Brenda Mallouk

Material Variances

Actual Quantity at - Flexible Budget Standard Cost

(AQu x SP) - (SQA x SP)

(18,000 x $2.00) - (15,000 x $2.00)

$6,000 U

Material Quantity Variance

22Brenda Mallouk

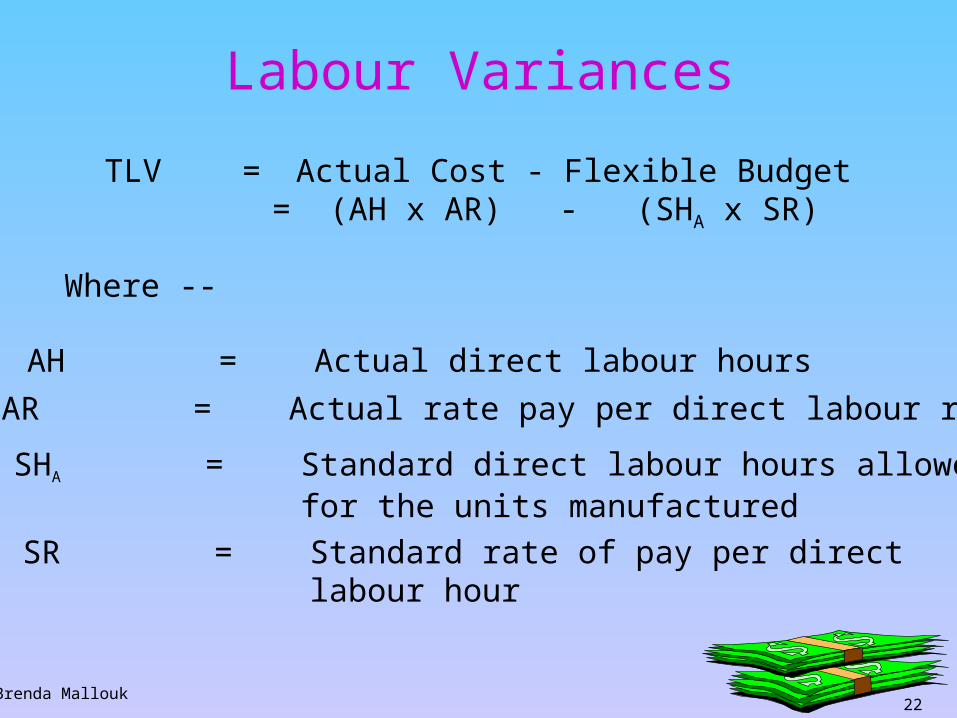

AH = Actual direct labour hours

SR = Standard rate of pay per directlabour hour

SHA = Standard direct labour hours allowedfor the units manufactured

AR = Actual rate pay per direct labour rate

Labour Variances

TLV = Actual Cost - Flexible Budget = (AH x AR) - (SHA x SR)

Where --

23Brenda Mallouk

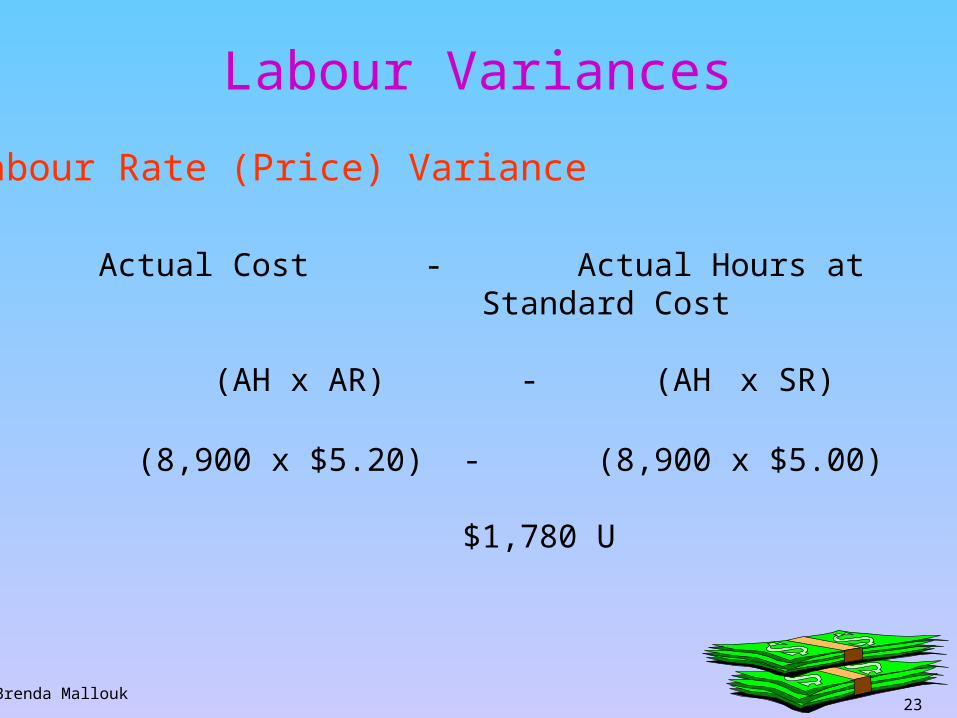

Labour Variances

Actual Cost - Actual Hours at Standard Cost

(AH x AR) - (AH x SR)

(8,900 x $5.20) - (8,900 x $5.00)

$1,780 U

Labour Rate (Price) Variance

24Brenda Mallouk

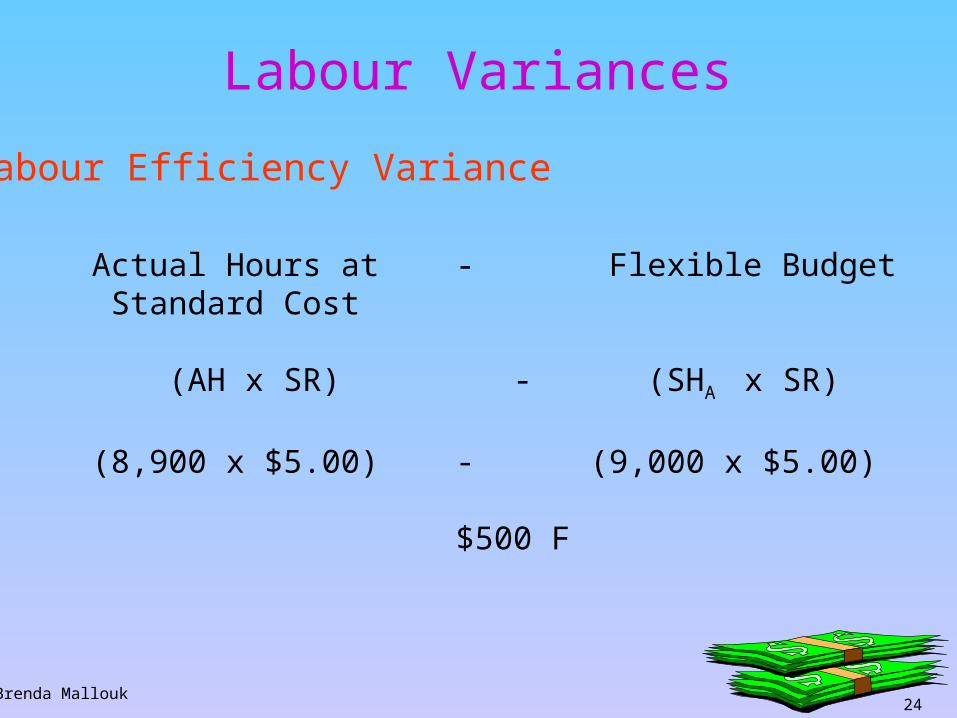

Labour Variances

Actual Hours at - Flexible Budget Standard Cost

(AH x SR) - (SHA x SR)

(8,900 x $5.00) - (9,000 x $5.00)

$500 F

Labour Efficiency Variance

25Brenda Mallouk

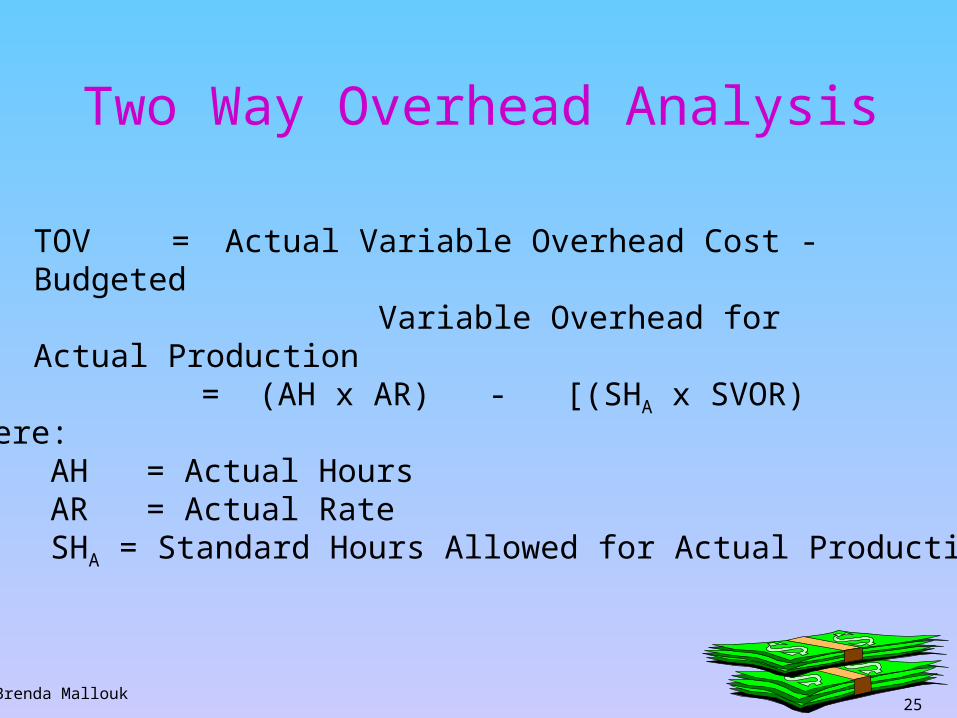

Two Way Overhead Analysis

TOV = Actual Variable Overhead Cost - Budgeted Variable Overhead for Actual Production = (AH x AR) - [(SHA x SVOR)

Where:AH = Actual HoursAR = Actual RateSHA = Standard Hours Allowed for Actual Production

26Brenda Mallouk

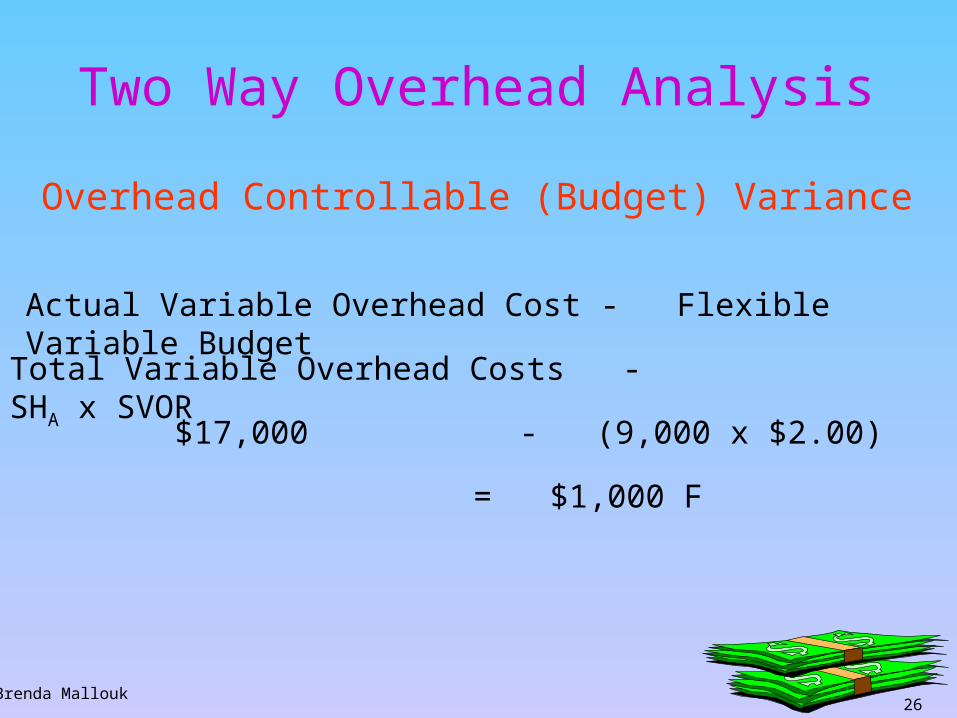

Two Way Overhead Analysis

Overhead Controllable (Budget) Variance

$17,000 - (9,000 x $2.00)

Actual Variable Overhead Cost - Flexible Variable Budget

Total Variable Overhead Costs - SHA x SVOR

= $1,000 F

27Brenda Mallouk

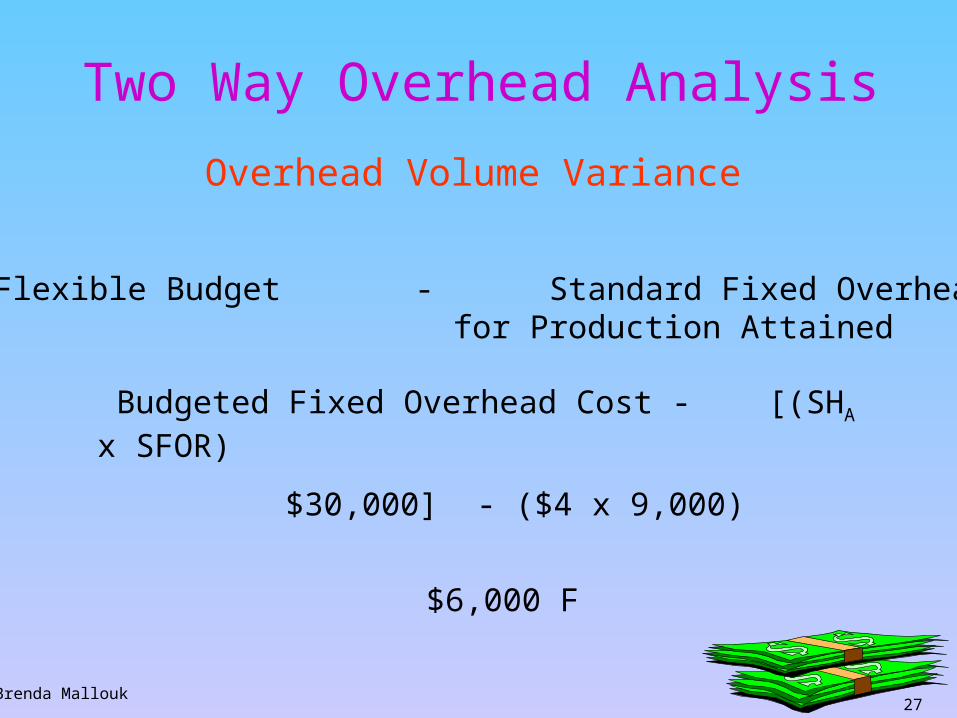

Two Way Overhead Analysis

Overhead Volume Variance

$30,000] - ($4 x 9,000)

Flexible Budget - Standard Fixed Overhead for Production Attained

Budgeted Fixed Overhead Cost - [(SHA x SFOR)

$6,000 F

28Brenda Mallouk

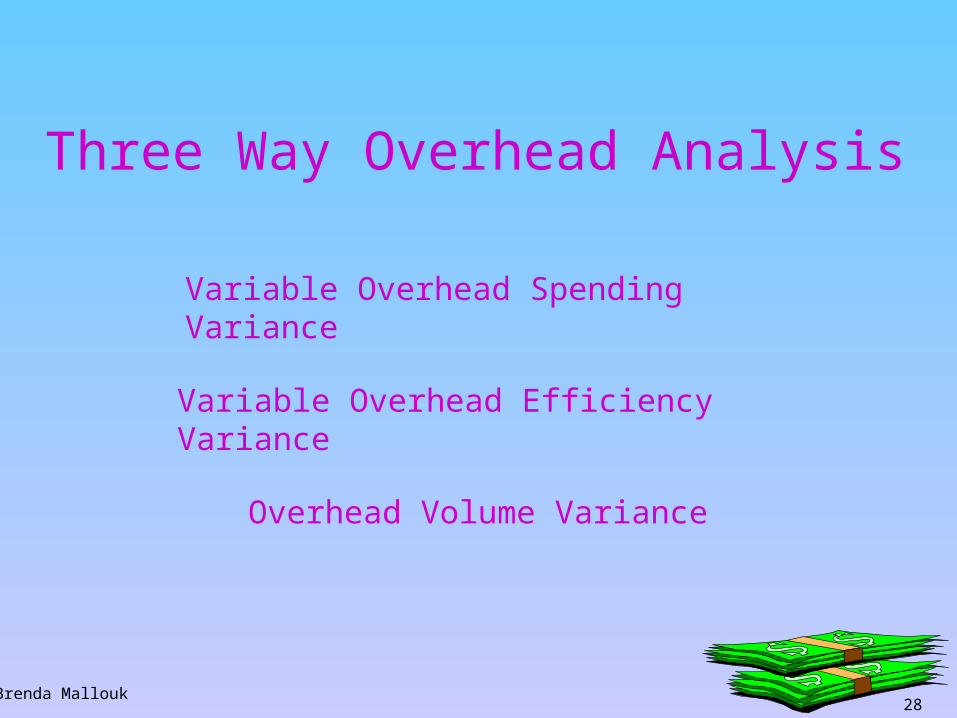

Three Way Overhead Analysis

Variable Overhead Spending Variance

Variable Overhead Efficiency Variance

Overhead Volume Variance

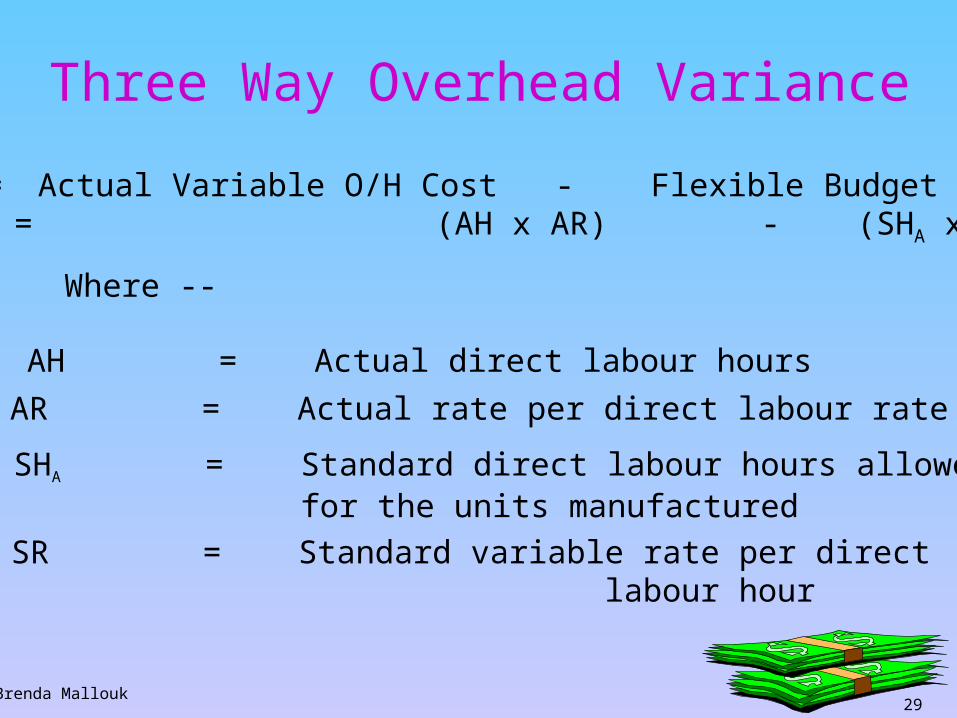

29Brenda Mallouk

AH = Actual direct labour hours

SR = Standard variable rate per direct labour hour

SHA = Standard direct labour hours allowedfor the units manufactured

AR = Actual rate per direct labour rate

Three Way Overhead Variance

TVOV = Actual Variable O/H Cost - Flexible Budget = (AH x AR) - (SHA x SVOR)

Where --

30Brenda Mallouk

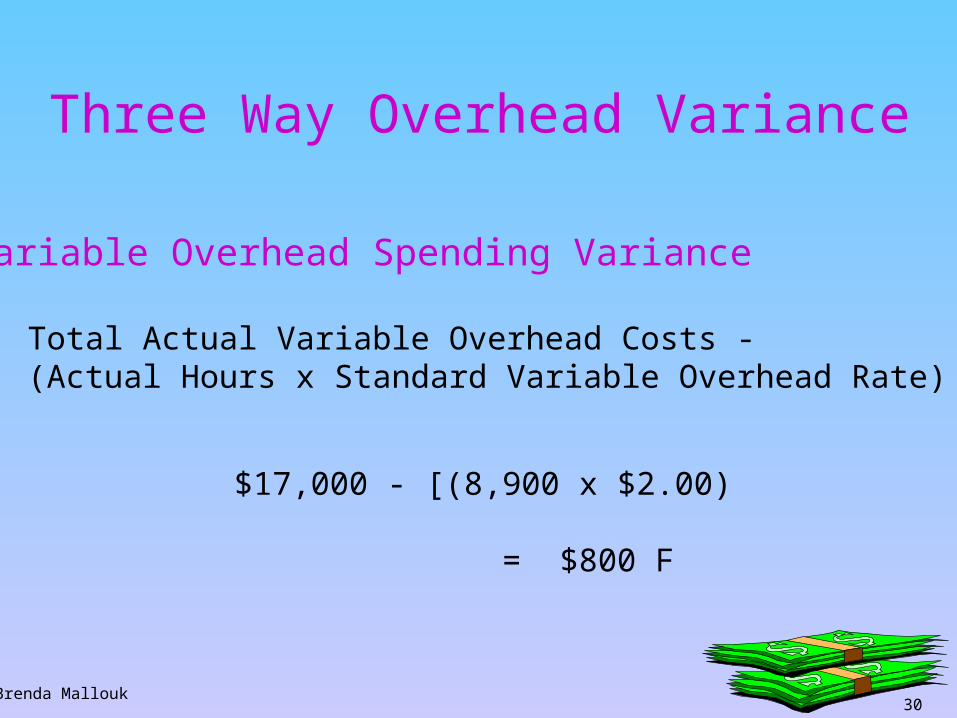

Variable Overhead Spending Variance

Total Actual Variable Overhead Costs - (Actual Hours x Standard Variable Overhead Rate)

$17,000 - [(8,900 x $2.00)

= $800 F

Three Way Overhead Variance

31Brenda Mallouk

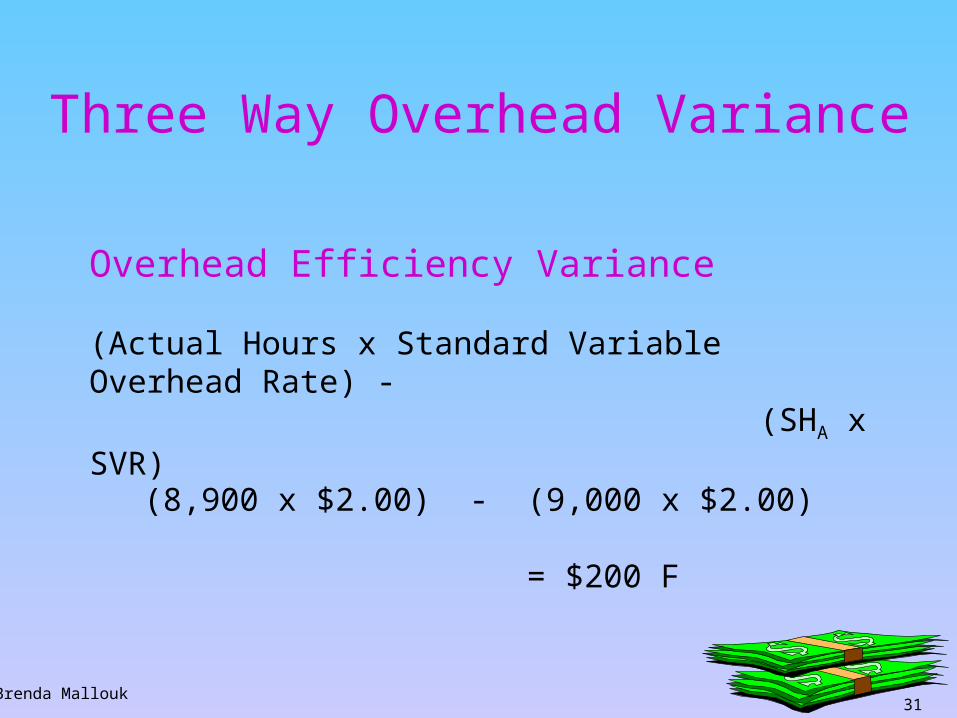

Overhead Efficiency Variance

(Actual Hours x Standard Variable Overhead Rate) - (SHA x SVR)

(8,900 x $2.00) - (9,000 x $2.00) = $200 F

Three Way Overhead Variance

32Brenda Mallouk

Three Way Overhead Variance

Overhead Volume Variance

Same as the Two Variance Method

33Brenda Mallouk

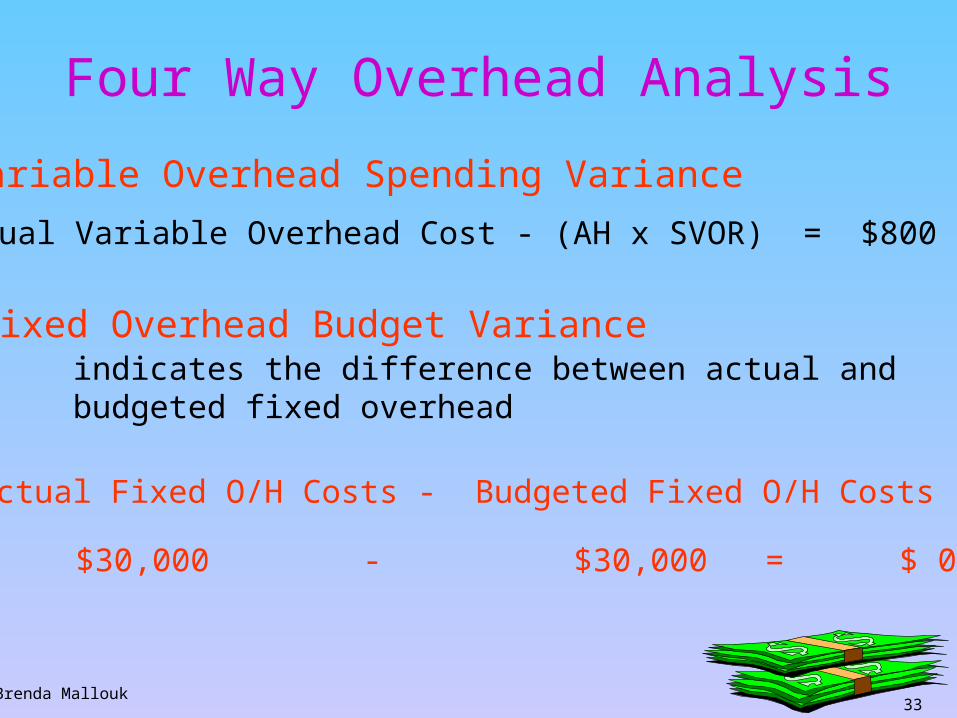

Four Way Overhead Analysis

Variable Overhead Spending Variance

Actual Variable Overhead Cost - (AH x SVOR) = $800 F

Fixed Overhead Budget Varianceindicates the difference between actual and budgeted fixed overhead

Actual Fixed O/H Costs - Budgeted Fixed O/H Costs

$30,000 - $30,000 = $ 0

34Brenda Mallouk

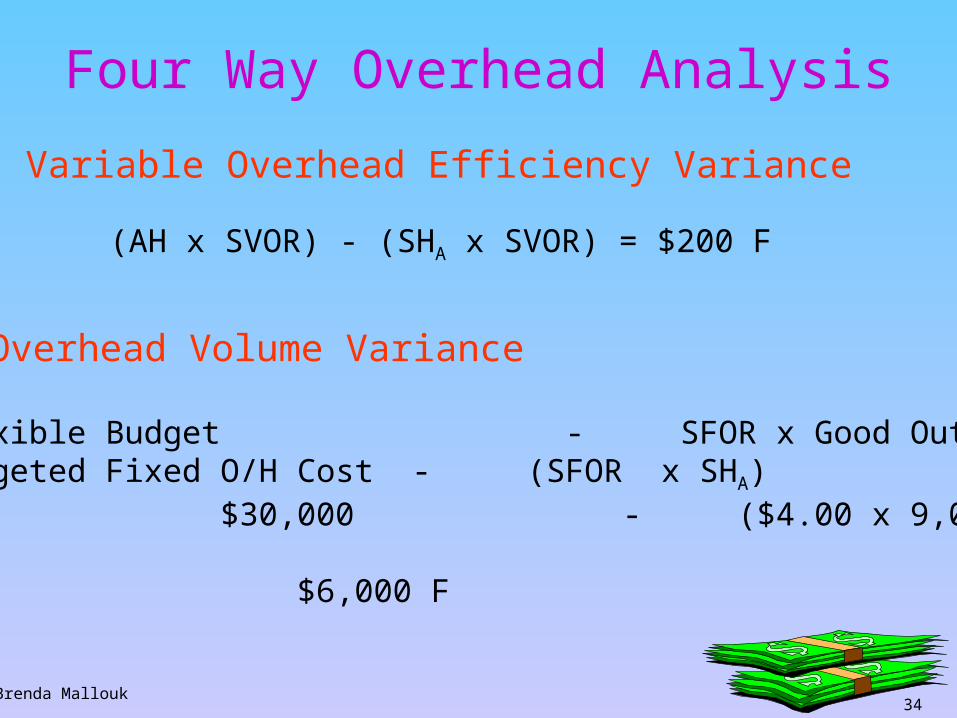

Four Way Overhead Analysis

Variable Overhead Efficiency Variance

(AH x SVOR) - (SHA x SVOR) = $200 F

Overhead Volume Variance

Flexible Budget - SFOR x Good OutputBudgeted Fixed O/H Cost - (SFOR x SHA) $30,000 - ($4.00 x 9,000)

$6,000 F

35Brenda Mallouk

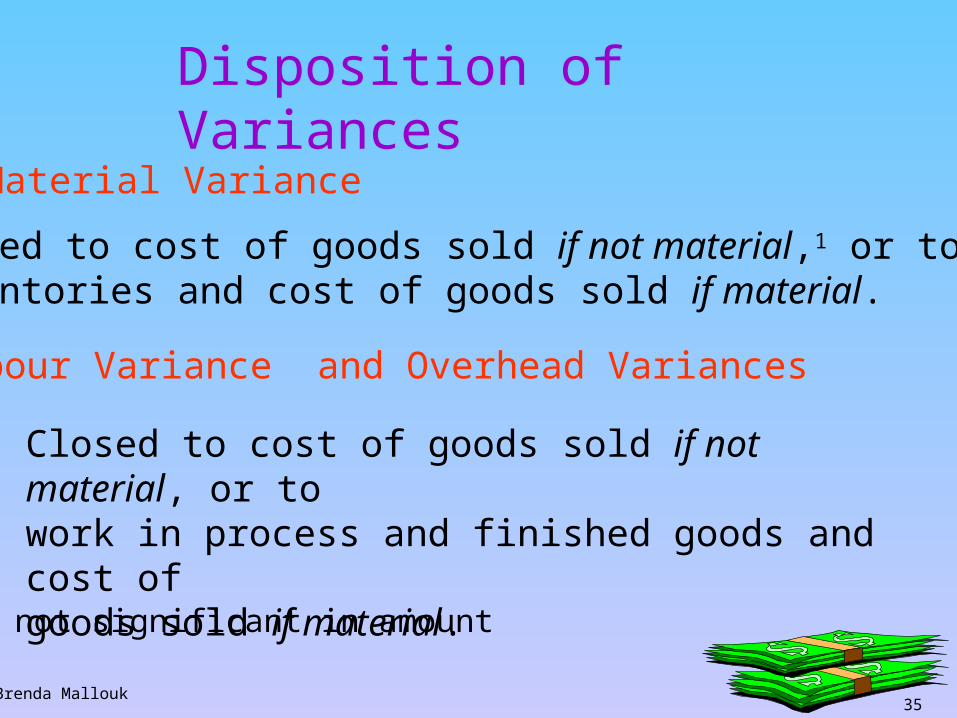

Disposition of Variances

Material Variance

Closed to cost of goods sold if not material,1 or to all inventories and cost of goods sold if material.

Labour Variance and Overhead Variances

Closed to cost of goods sold if not material, or towork in process and finished goods and cost of goods sold if material.

1 not significant in amount

![BRENDA Tutorial · BRENDA eli Jr Term or Synonym: AND trjct to BRENDA links: te of Download s cf went s 8 of el —t R] IS to from went n' I n to BRENDA evaluate BRENDA.' Tissue C)](https://img.pdfslide.us/doc/110x75/5fc744537d89516d5976c1f7/brenda-tutorial-brenda-eli-jr-term-or-synonym-and-trjct-to-brenda-links-te-of.jpg)