Embed Size (px)

Citation preview

1

2012 Economic Outlook

Phoenix Chamber of Commerce Economic Outlook BreakfastSeptember 30, 2011

Beckie HolmesDiretor, Marketing Science, Cox Communications Arizona

2

Overview

• The recession has left lasting damage• Credit markets still fundamentally weak• No political will for further fiscal support, unclear that

monetary policy can help• Bottom line: Slow and painful recovery continues into 2012;

risk of recession is high

3

The Post-Recession Economy: More Services, Government, Exports, Less Investment, Durable Goods

Percent Change Real GDP: 2007Q4 to 2011Q2

-0.5% 0.9% 1.4% 0.7%

-31.5%

-1.3%

-38.1%

8.7%-0.1%

13.4% 17.6%

-5.0%

-50%-40%-30%-20%-10%

0%10%20%30%

GDP DurableGoods

NondurableGoods

Services CommercialStructures

BusinessEquip &

Software

Residential Exports Imports NationalDefense

FederalNondefense

State andLocal

Perc

ent C

hang

e

Net Exports -25.4% Government +2.2%Consumption +0.8% Investment -16.3%

Changing Share of GDP: 2011Q2 vs 2007Q4

-0.77%

0.86%1.23%

-1.28%

-0.51%

-1.72%

1.52%

-0.68%

0.77%0.46%

-0.18%

-2.0%-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%

DurableGoods

NondurableGoods

Services CommercialStructures

BusinessEquip &

Software

Residential Exports Imports NationalDefense

FederalNondefense

State andLocal

Perc

ent o

f GD

P

Consumption +1.3% Investment -3.2% Net Exports +0.8% Government +1.0%

Source: Department of Commerce, Bureau of Economic Statistics

4

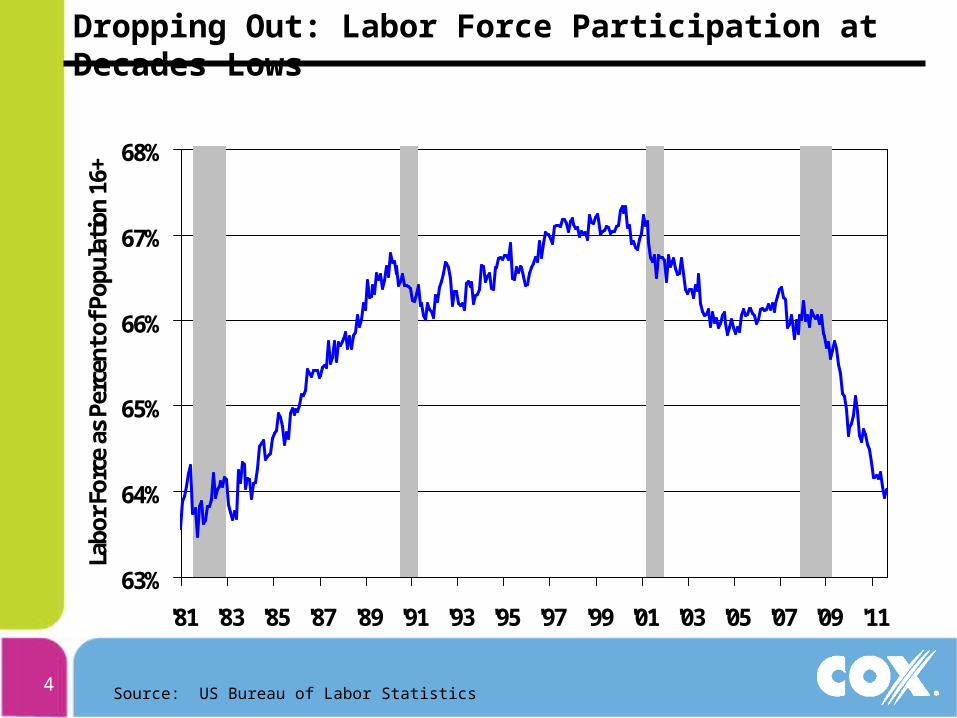

Dropping Out: Labor Force Participation at Decades Lows

63%

64%

65%

66%

67%

68%

'81 '83 '85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11

Labo

r For

ce a

s Pe

rcen

t of P

opul

ation

16+

Source: US Bureau of Labor Statistics

55

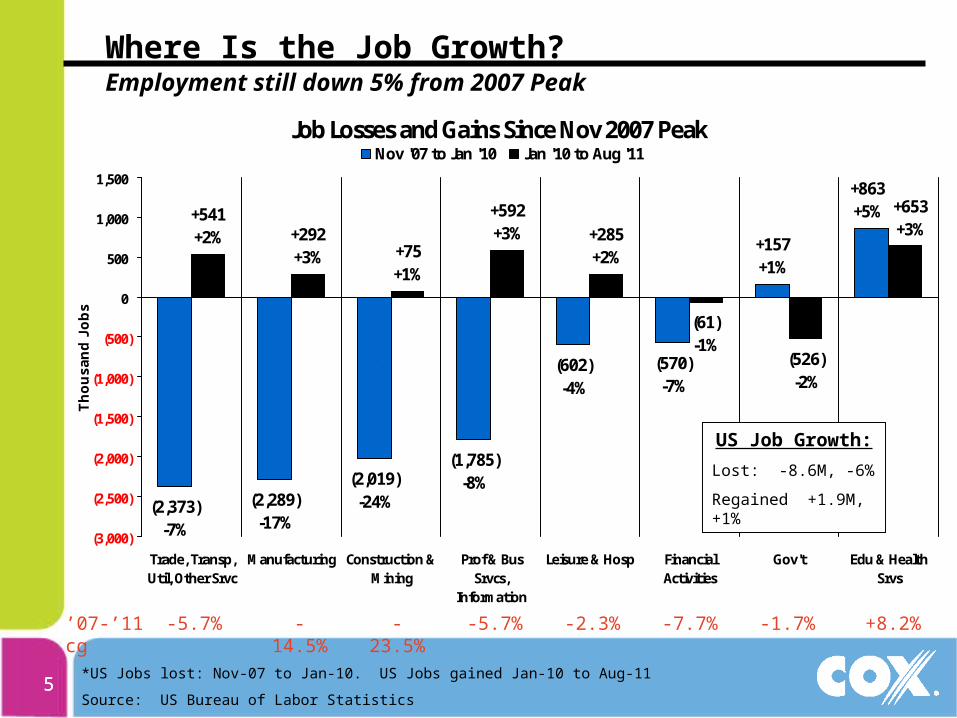

Where Is the Job Growth? Employment still down 5% from 2007 Peak

Job Losses and Gains Since Nov 2007 Peak

+863 +5%

(570)-7%

(602)-4%

(1,785)-8%(2,019)

-24%(2,289)-17%

(2,373)-7%

+157+1%

+653+3%

(526)-2%

(61)-1%

+285 +2%

+592 +3%

+75+1%

+292 +3%

+541 +2%

(3,000)

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

1,500

Trade, Transp,Util, Other Srvc

Manufacturing Construction &Mining

Prof & BusSrvcs,

Information

Leisure & Hosp FinancialActivities

Gov't Edu & HealthSrvs

Th

ou

sa

nd

Jo

bs

Nov '07 to Jan '10 Jan '10 to Aug '11

`

*US Jobs lost: Nov-07 to Jan-10. US Jobs gained Jan-10 to Aug-11

Source: US Bureau of Labor Statistics

US Job Growth:

Lost: -8.6M, -6%

Regained +1.9M, +1%

-5.7% -23.5%-14.5% -5.7% -1.7% +8.2%-7.7%-2.3%’07-’11 cg

6

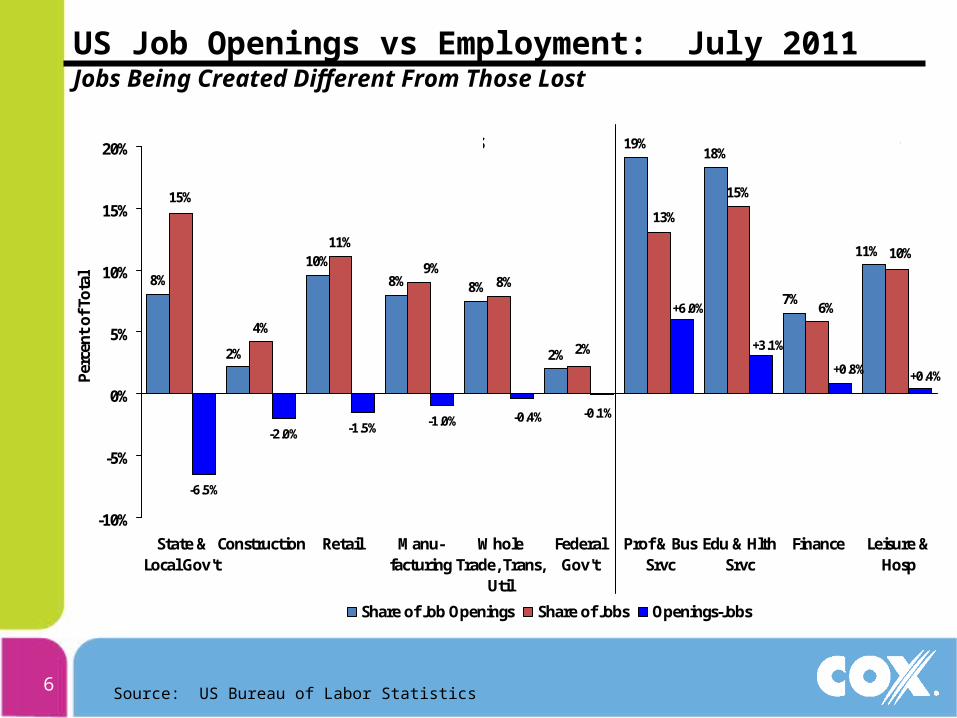

US Job Openings vs Employment: July 2011 Jobs Being Created Different From Those Lost

8%10%

8% 8%

2%

19%18%

4%

11%

15%

-6.5%

-2.0% -1.5% -1.0%

11%

2%

7%

10%

2%

8%

13%

6%

15%

9%

+6.0%

+0.4%

-0.4%

+0.8%

+3.1%

-0.1%

-10%

-5%

0%

5%

10%

15%

20%

State &Local Gov't

Construction Retail Manu-facturing

WholeTrade, Trans,

Util

FederalGov't

Prof & BusSrvc

Edu & HlthSrvc

Finance Leisure &Hosp

Perc

ent

of T

otal

Share of Job Openings Share of Jobs Openings-Jobs

Surplus Workers Worker Shortage

Source: US Bureau of Labor Statistics

7

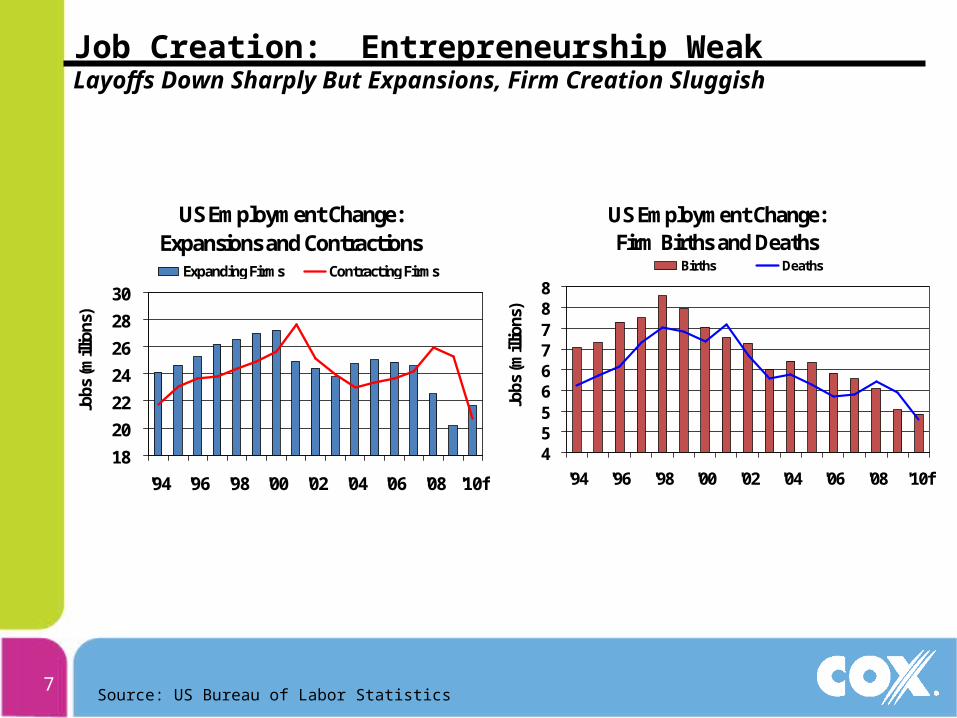

Job Creation: Entrepreneurship WeakLayoffs Down Sharply But Expansions, Firm Creation Sluggish

US Employment Change: Expansions and Contractions

18

20

22

2426

28

30

'94 '96 '98 '00 '02 '04 '06 '08 '10f

Jobs

(mill

ions

)

Expanding Firms Contracting Firms

Source: US Bureau of Labor Statistics

US Employment Change: Firm Births and Deaths

455667788

'94 '96 '98 '00 '02 '04 '06 '08 '10f

Jobs

(mill

ions

)

Births Deaths

8

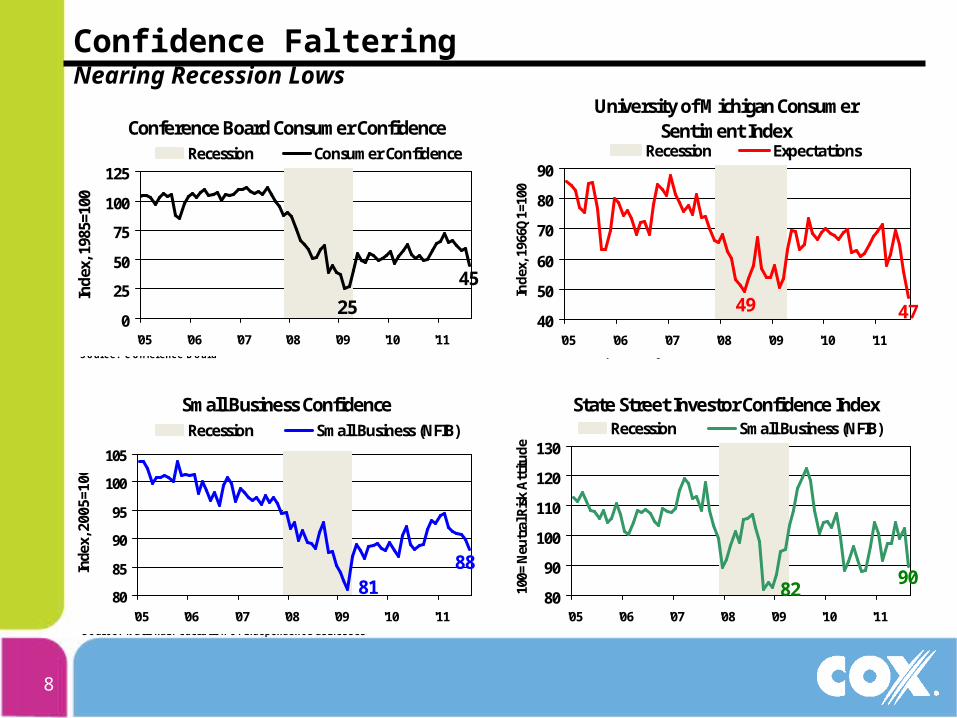

Confidence Faltering Nearing Recession Lows

Conference Board Consumer Confidence

45

250

25

50

75

100

125

'05 '06 '07 '08 '09 '10 '11

Inde

x, 1

985=

100

Recession Consumer Confidence

Source: Conference Board

Small Business Confidence

8881

80

85

90

95

100

105

'05 '06 '07 '08 '09 '10 '11

Inde

x, 2

005=

100

Recession Small Business (NFIB)

Source: National Federation of Independent Businesses

University of Michigan Consumer Sentiment Index

474940

50

60

70

80

90

'05 '06 '07 '08 '09 '10 '11

Inde

x, 1

966Q

1=10

0

Recession Expectations

Source: University of Michigan

State Street Investor Confidence Index

908280

90

100

110

120

130

'05 '06 '07 '08 '09 '10 '11

100=

Neu

tral

Ris

k A

ttitu

de

Recession Small Business (NFIB)

Source: State Street Global Markets

9

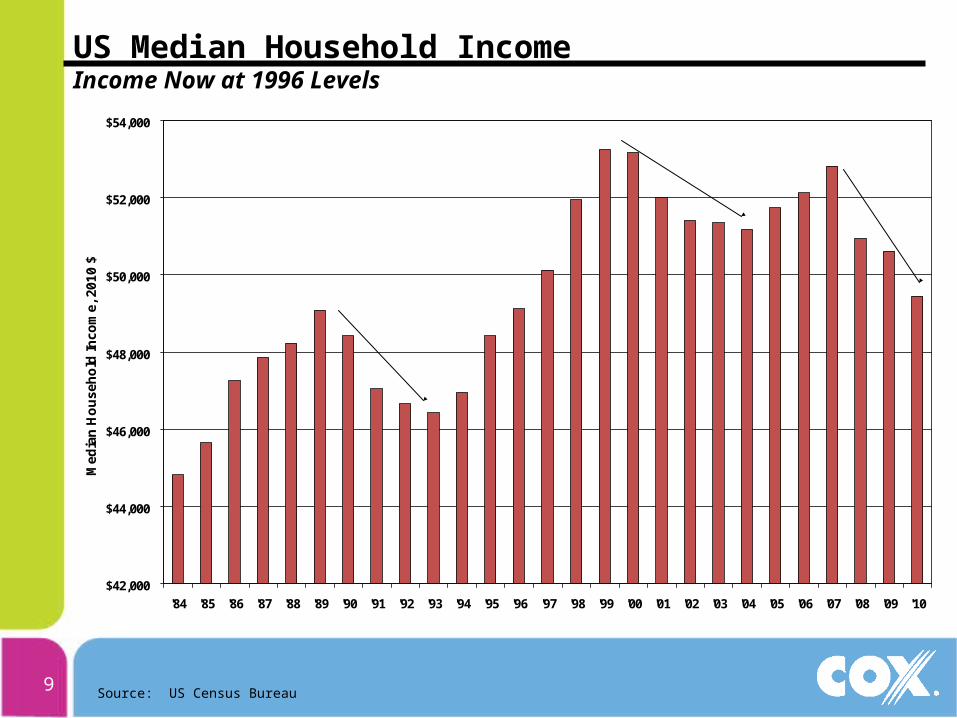

US Median Household IncomeIncome Now at 1996 Levels

$42,000

$44,000

$46,000

$48,000

$50,000

$52,000

$54,000

'84 '85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Me

dia

n H

ou

seh

old

Inco

me

, 201

0 $

'89-'93-5.4%

'99-'04-3.9%

'07-'10-6.4%

Source: US Census Bureau

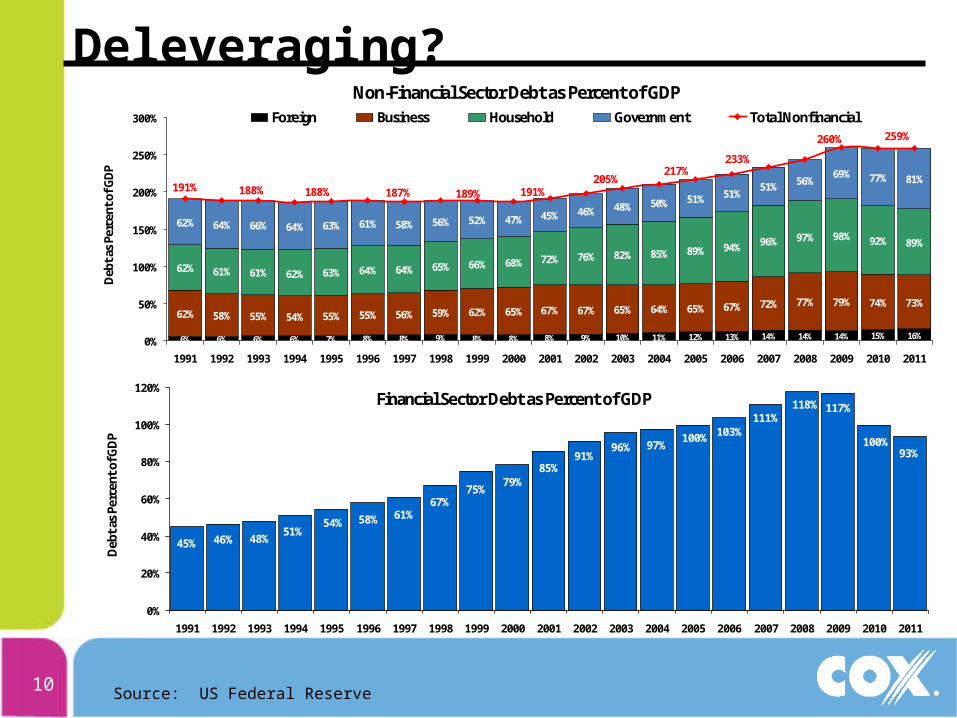

10

Deleveraging?Non-Financial Sector Debt as Percent of GDP

6% 6% 6% 6% 7% 8% 8% 9% 8% 8% 8% 9% 10% 11% 12% 13% 14% 14% 15% 16%

62% 58% 55% 54% 55% 55% 56% 59% 62% 65% 67% 67% 65% 64% 65% 67% 72% 77% 79% 74% 73%

62% 61% 61% 62% 63% 64% 64% 65% 66% 68% 72% 76% 82% 85% 89% 94% 96% 97% 98% 92% 89%

62% 64% 66% 64% 63% 61% 58% 56% 52% 47% 45% 46% 48% 50% 51% 51%51% 56%

69% 77% 81%

14%

191% 188% 188% 187% 189% 191%205%

217%233%

260% 259%

0%

50%

100%

150%

200%

250%

300%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Deb

t as

Perc

ent o

f GD

PForeign Business Household Government Total Nonfinancial

Financial Sector Debt as Percent of GDP

45% 46% 48%51%

54% 58% 61%67%

75%79%

85%91%

96% 97%100% 103%

111%118% 117%

100%93%

0%

20%

40%

60%

80%

100%

120%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Deb

t as

Perc

ent o

f GD

P

Source: US Federal Reserve

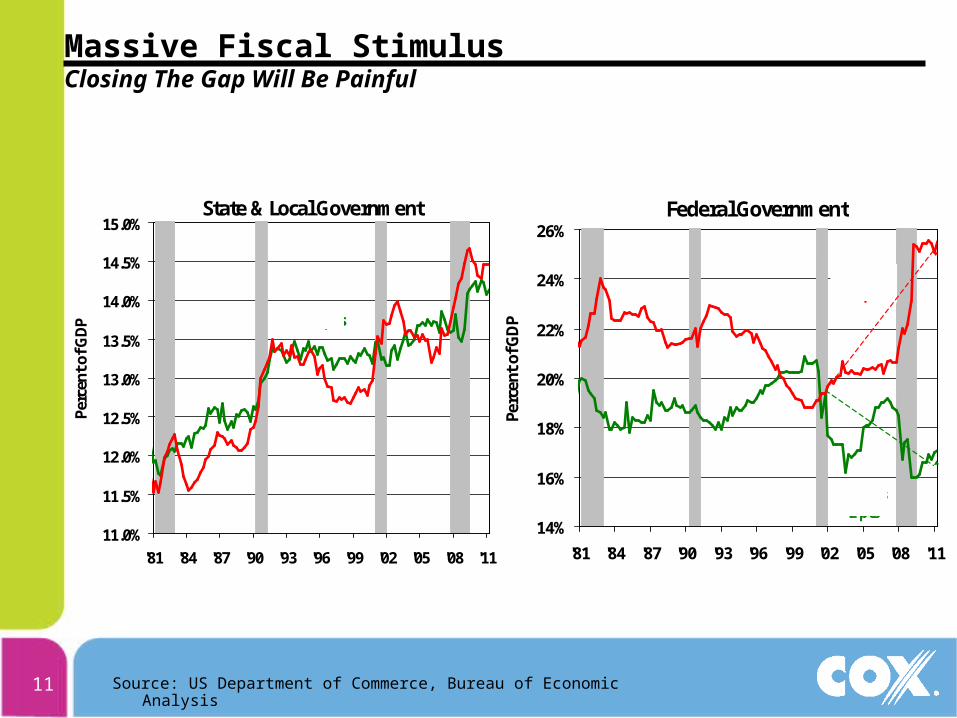

11

Massive Fiscal StimulusClosing The Gap Will Be Painful

State & Local Government

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

15.0%

'81 '84 '87 '90 '93 '96 '99 '02 '05 '08 '11

Perc

ent o

f GDP

Spending

Receipts

Federal Government

14%

16%

18%

20%

22%

24%

26%

'81 '84 '87 '90 '93 '96 '99 '02 '05 '08 '11

Perc

ent o

f GD

P

Spending+6 pts

Receipts-2 pts

Source: US Department of Commerce, Bureau of Economic Analysis

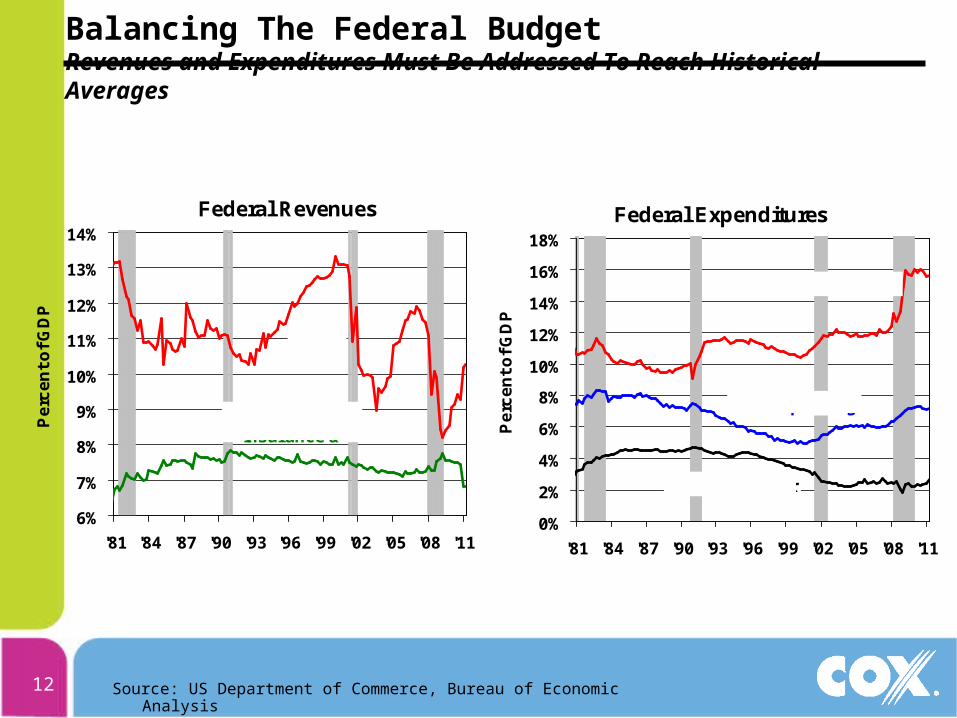

12

Balancing The Federal BudgetRevenues and Expenditures Must Be Addressed To Reach Historical Averages

Federal Revenues

6%

7%

8%

9%

10%

11%

12%

13%

14%

'81 '84 '87 '90 '93 '96 '99 '02 '05 '08 '11

Pe

rce

nt

of

GD

P

Social Insurance &

Taxes

Federal Expenditures

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

'81 '84 '87 '90 '93 '96 '99 '02 '05 '08 '11

Pe

rce

nt

of

GD

P

Transfers

Interest & Other

Gov't Spending

Source: US Department of Commerce, Bureau of Economic Analysis

13

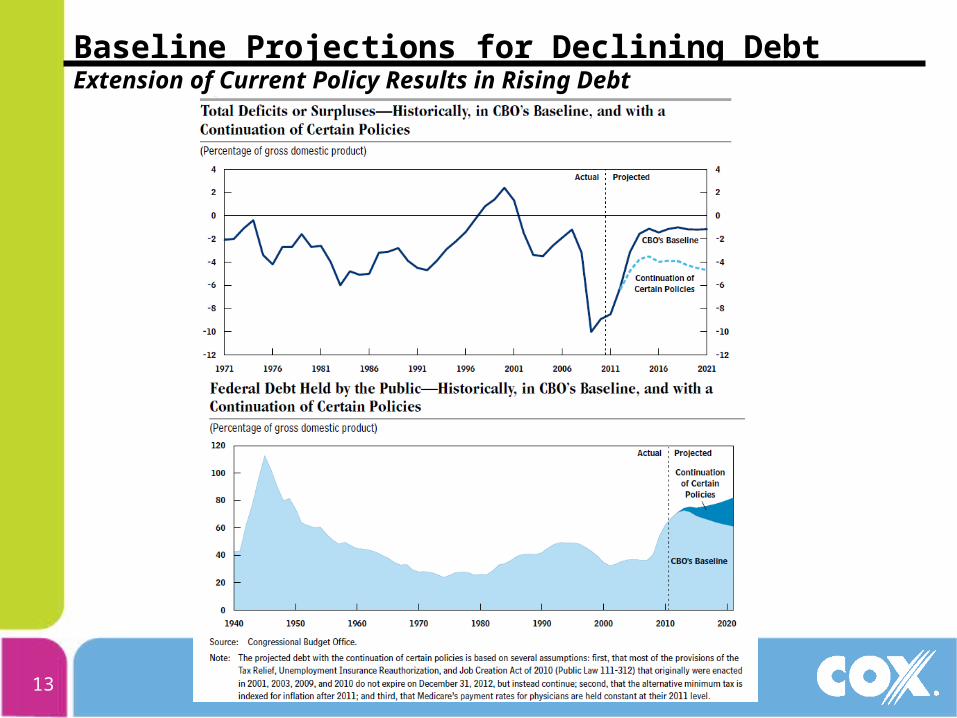

Baseline Projections for Declining DebtExtension of Current Policy Results in Rising Debt

14

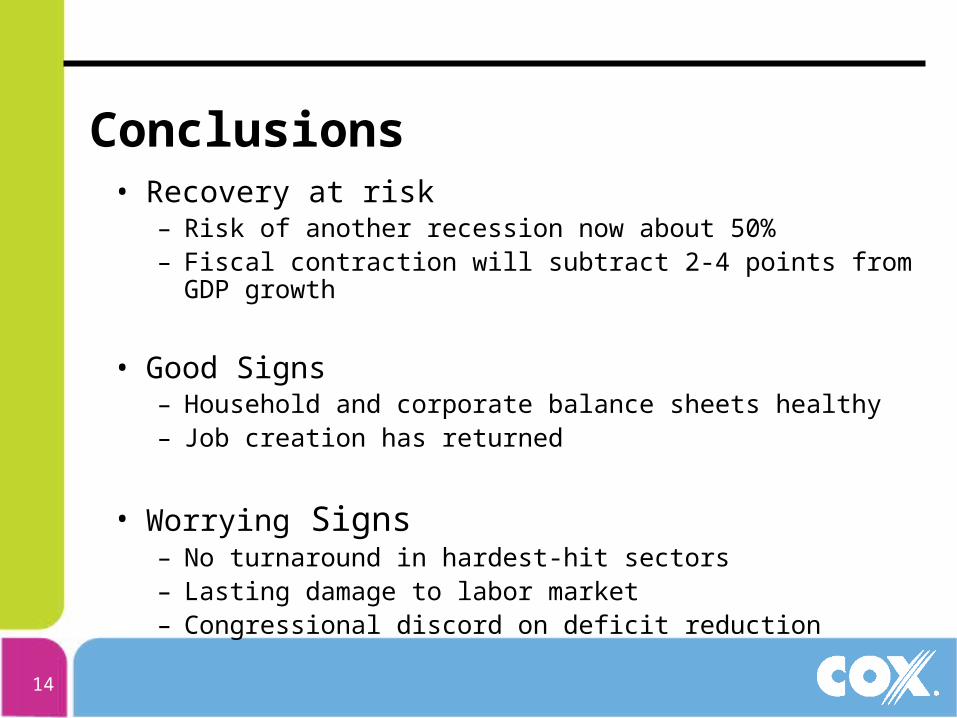

Conclusions• Recovery at risk

– Risk of another recession now about 50%– Fiscal contraction will subtract 2-4 points from GDP growth

• Good Signs– Household and corporate balance sheets healthy– Job creation has returned

• Worrying Signs– No turnaround in hardest-hit sectors– Lasting damage to labor market– Congressional discord on deficit reduction