Embed Size (px)

Citation preview

Safe HarborThis presentation contains forward-looking statements concerning prospects and trends for the cable industry, demand for the products produced by ARRIS and general prospects for ARRIS in 2009 and beyond, expectations with respect to the combination of ARRIS, including expected benefits and synergies and the assumptions relating to the foregoing. The statements in this presentation that use such words as “believe," "expect," "intend," "anticipate," "contemplate," "estimate," or "plan," or similar expressions also are forward-looking statements. Actual results may differ materially from those contained in, or suggested by, any forward-looking statement. Specific factors that could cause such material differences include: the effectiveness and timing of the integration of the operations of ARRIS and C-COR and capital spending levels by our customers based in part on demand for broadband services. Other factors include the strength of the capital markets and the general economy, customer adoption of our technologies, development and marketing of technology by our competitors and risks associated with potential acquisitions. This list of factors is representative of the factors which could affect our forward-looking statements and is not intended as an all encompassing list of such factors. Additional information regarding these and other factors can be found in ARRIS’ reports filed with the Securities and Exchange Commission, including its Form 10-K for the year ended December 31, 2008. We disclaim any obligation to update these statements, whether as a result of new information, future events or otherwise.

March 2009 1Analyst / Investor Conference

2009 Analyst & Investor ConferenceBob StanzioneChairman & CEO

Optical Metro

Transport

ARRIS WorkAssure™ Work Force Management• Customer Satisfaction• Dispatch Control• Expense Reduction• Workforce Potential

Regal®Taps

MONARCH®Splitters and

Supplies

ARRIS CHP Max5000™Headend Optics

ARRIS ServAssure™ HFC Network Surveillance and Maintenance• Network Visibility• Network Management• New Service Deployment• Improved Service

ARRIS D5™ Universal Edge

QAM

ARRIS C4® CMTS

ARRIS Flex Max®Amplifiers

ARRIS Opti Max® Nodes

Touchstone® E-MTA

PacketCable™ and SIP

ARRIS CORWave™

Optical Transmitters

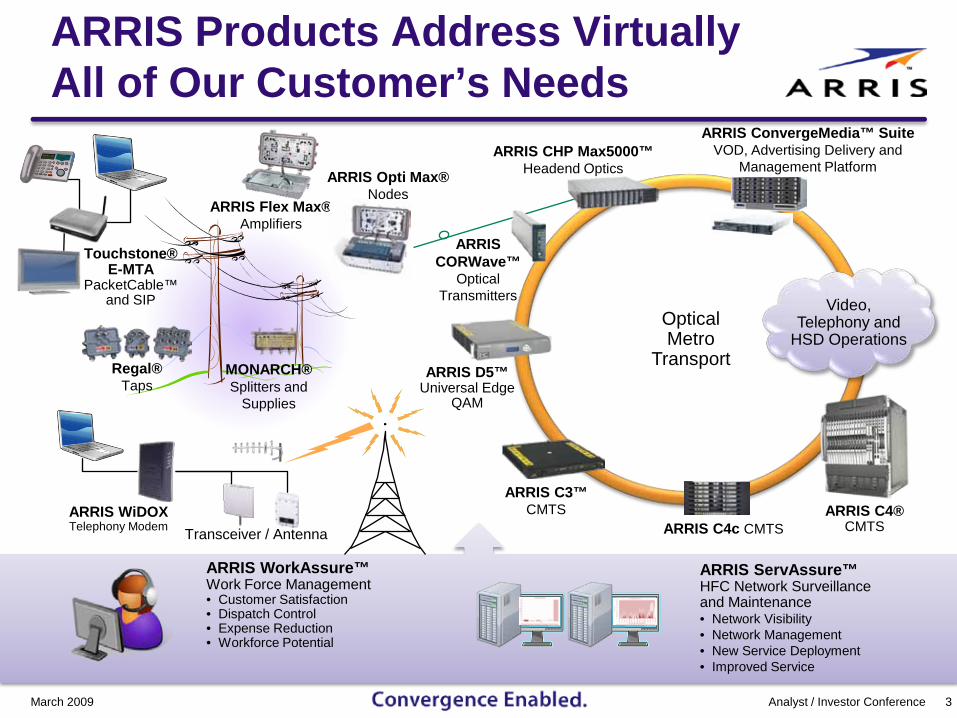

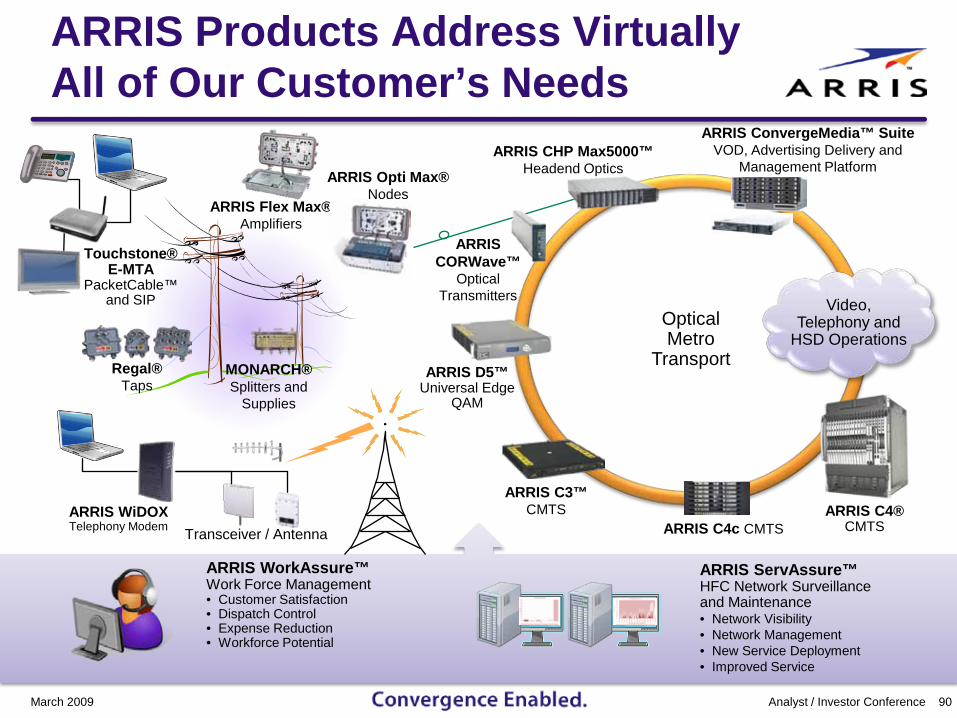

ARRIS Products Address Virtually All of Our Customer’s Needs

March 2009 3Analyst / Investor Conference

ARRIS C3™ CMTS

Transceiver / AntennaARRIS WiDOX Telephony Modem

Video, Telephony and

HSD Operations

ARRIS C4c CMTS

ARRIS ConvergeMedia™ SuiteVOD, Advertising Delivery and

Management Platform

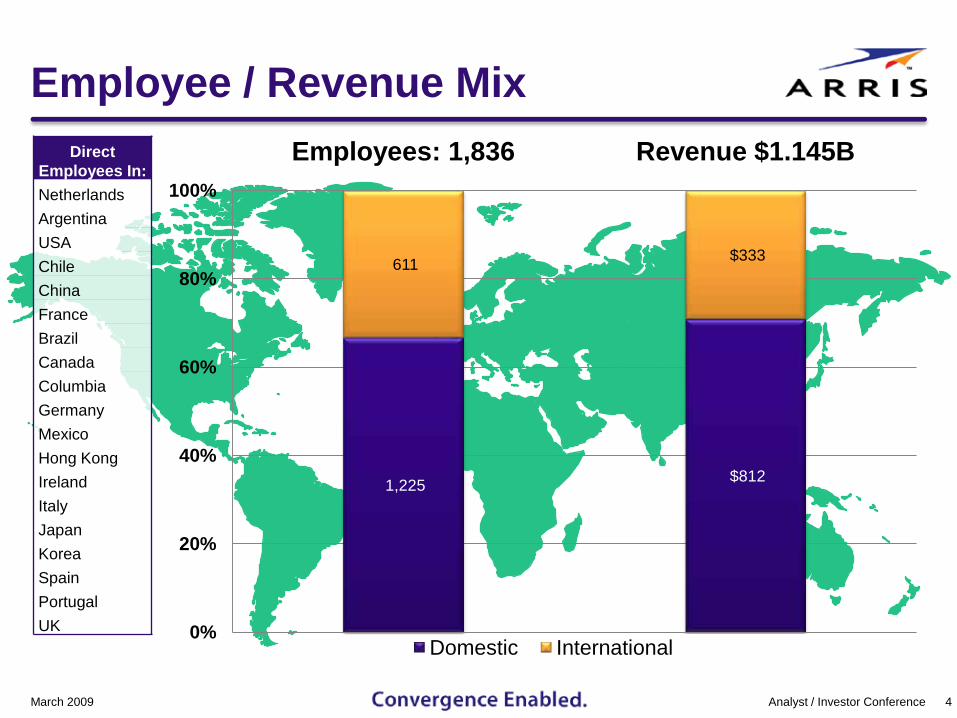

Employee / Revenue Mix

March 2009 4Analyst / Investor Conference

1,225 $812

611 $333

0%

20%

40%

60%

80%

100%

Employees: 1,836 Revenue $1.145B

Domestic International

Direct Employees In:NetherlandsArgentinaUSAChileChinaFranceBrazilCanadaColumbiaGermanyMexicoHong KongIrelandItalyJapanKoreaSpainPortugalUK

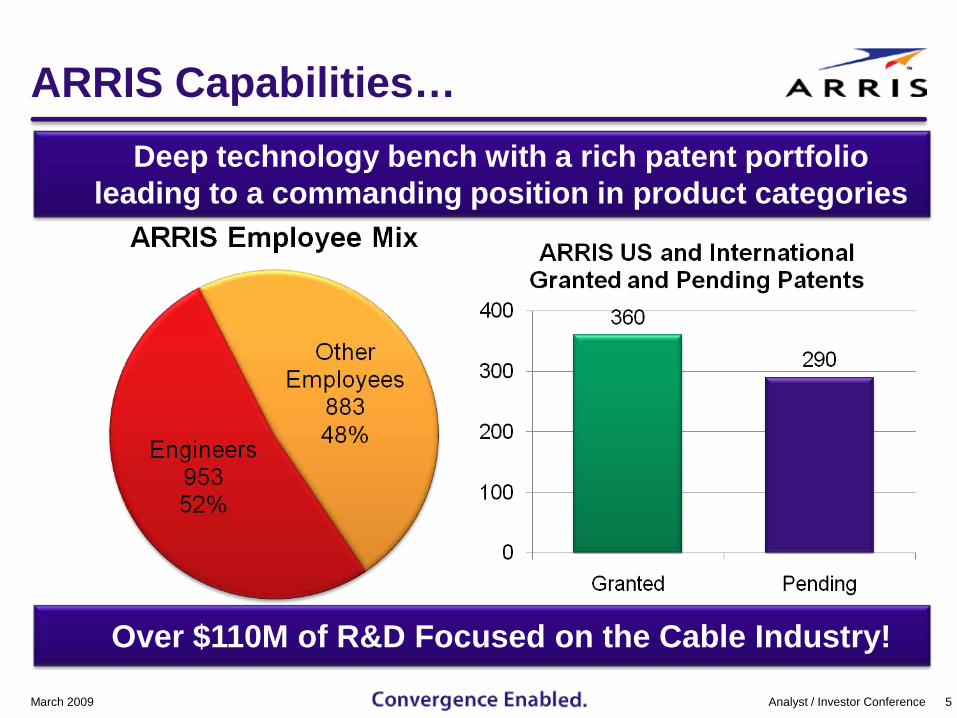

Deep technology bench with a rich patent portfolio leading to a commanding position in product categories

ARRIS Capabilities…

March 2009 5Analyst / Investor Conference

Over $110M of R&D Focused on the Cable Industry!

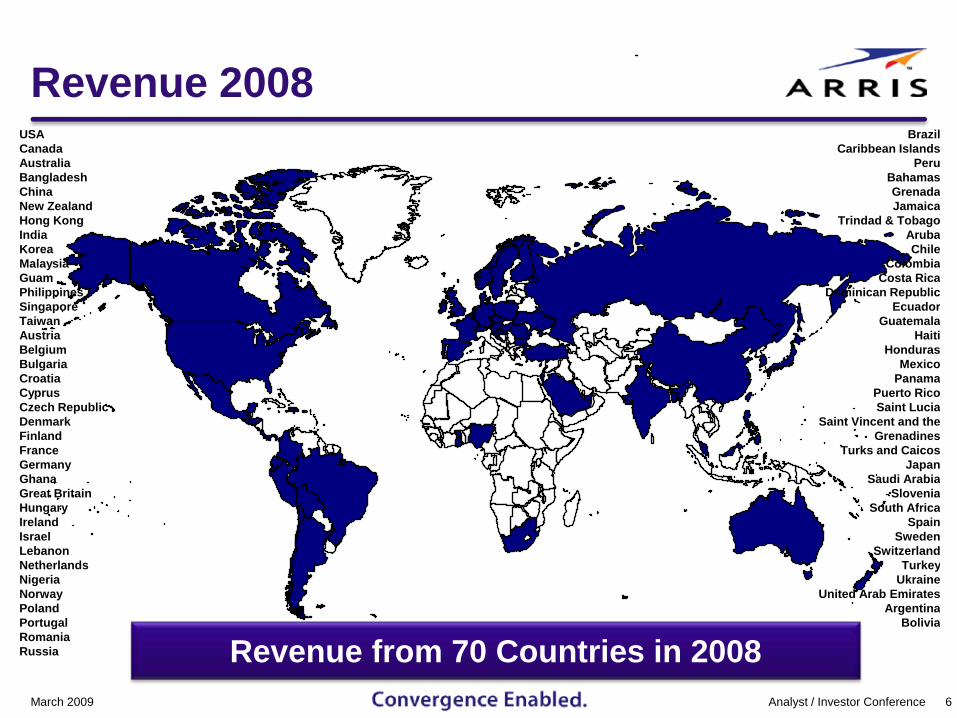

Revenue 2008

Revenue from 70 Countries in 2008

USA Canada Australia Bangladesh China New Zealand Hong Kong India Korea Malaysia GuamPhilippines Singapore Taiwan Austria Belgium Bulgaria Croatia Cyprus Czech Republic Denmark Finland France Germany Ghana Great Britain Hungary Ireland Israel Lebanon Netherlands Nigeria Norway Poland Portugal Romania Russia

Brazil Caribbean Islands

Peru Bahamas Grenada Jamaica

Trindad & Tobago Aruba Chile

Colombia Costa Rica

Dominican Republic Ecuador

Guatemala Haiti

Honduras Mexico

Panama Puerto Rico Saint Lucia

Saint Vincent and the Grenadines

Turks and Caicos Japan

Saudi Arabia Slovenia

South Africa Spain

Sweden Switzerland

Turkey Ukraine

United Arab Emirates Argentina

Bolivia

March 2009 6Analyst / Investor Conference

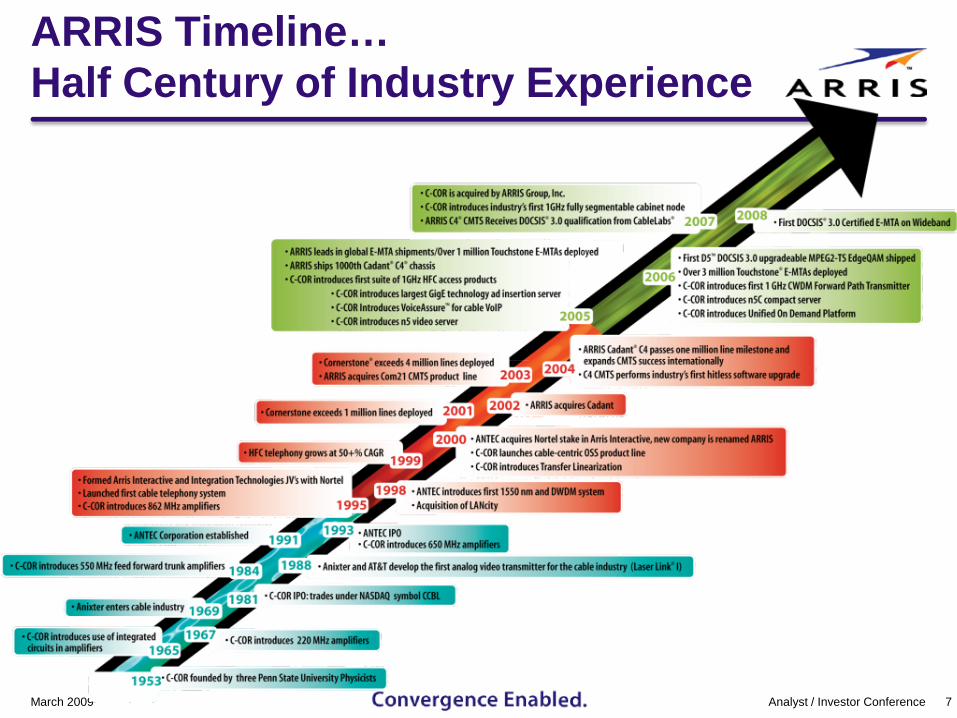

ARRIS Timeline… Half Century of Industry Experience

March 2009 7Analyst / Investor Conference

ARRIS Growth Strategy (2003)1. Maintain and Improve a strong Capital structure2. Leverage our current voice and data business: fill out

installed base of CBR Voice and establish a large installed base of high speed data

3. Transition to VoIP with an “Everything IP, Everywhere” philosophy and build on current market successes

4. Strengthen and grow our ARRIS TeleWire Supply® infrastructure distribution channel

5. Expand our existing product/services portfolio through internal developments, partnerships and acquisitions.

March 2009 8Analyst / Investor Conference

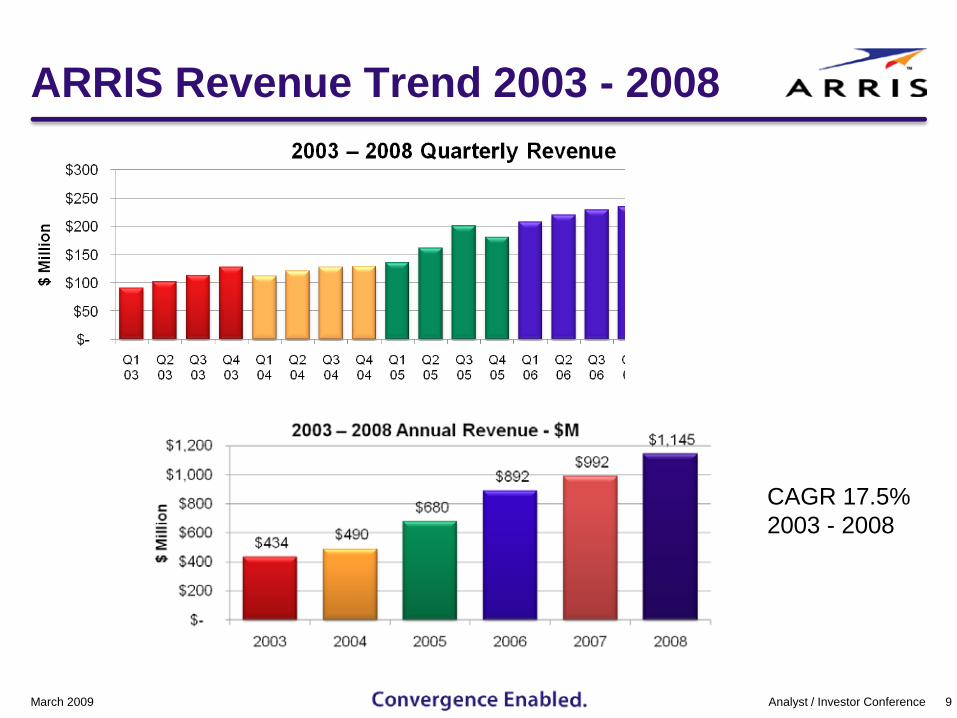

ARRIS Revenue Trend 2003 - 2008

March 2009 9Analyst / Investor Conference

CAGR 17.5% 2003 - 2008

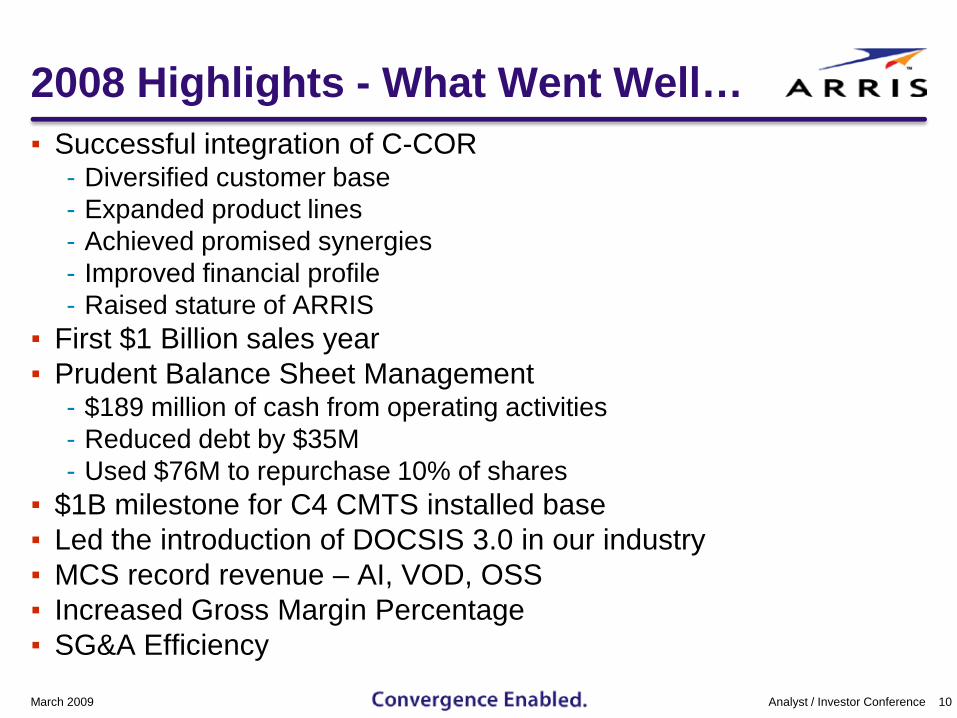

2008 Highlights - What Went Well…▪ Successful integration of C-COR

- Diversified customer base - Expanded product lines- Achieved promised synergies- Improved financial profile- Raised stature of ARRIS

▪ First $1 Billion sales year▪ Prudent Balance Sheet Management

- $189 million of cash from operating activities- Reduced debt by $35M- Used $76M to repurchase 10% of shares

▪ $1B milestone for C4 CMTS installed base▪ Led the introduction of DOCSIS 3.0 in our industry▪ MCS record revenue – AI, VOD, OSS▪ Increased Gross Margin Percentage▪ SG&A Efficiency

10Analyst / Investor ConferenceMarch 2009

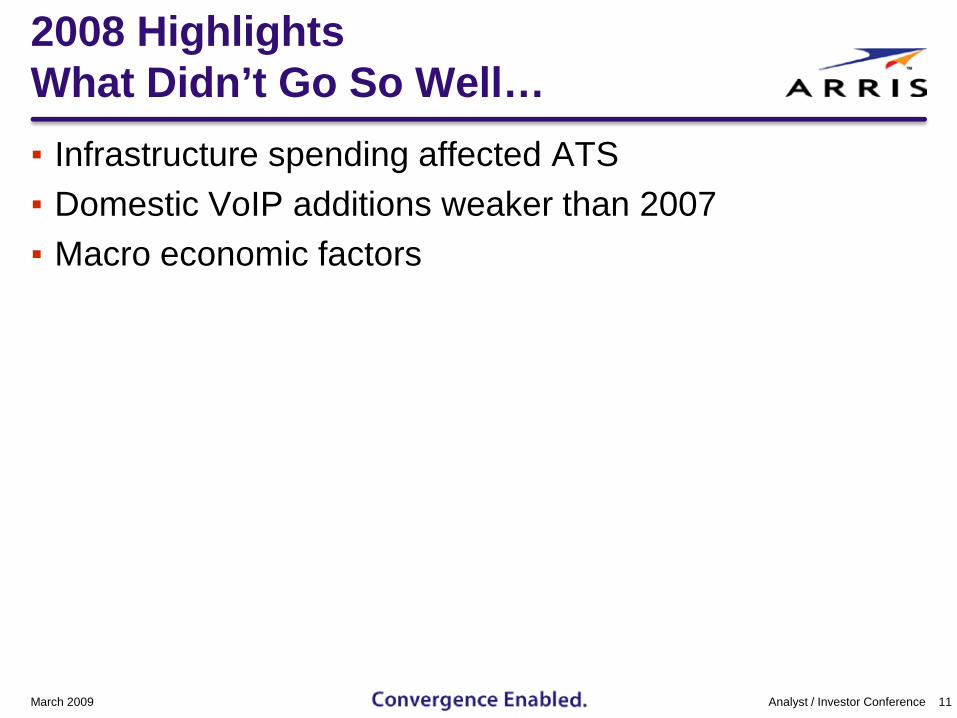

2008 HighlightsWhat Didn’t Go So Well…▪ Infrastructure spending affected ATS▪ Domestic VoIP additions weaker than 2007▪ Macro economic factors

March 2009 11Analyst / Investor Conference

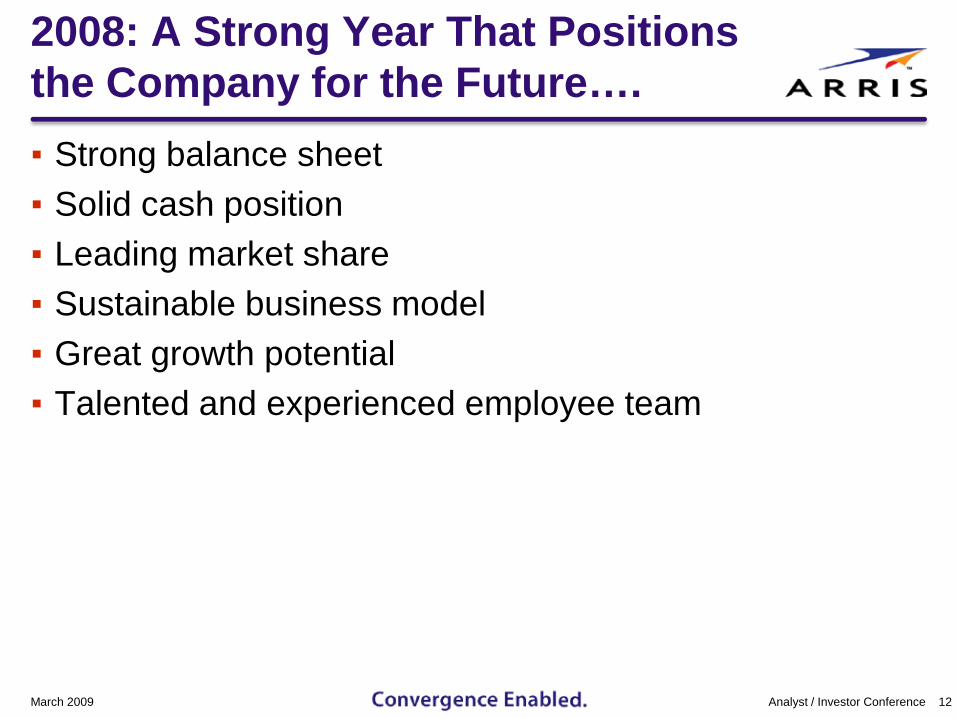

2008: A Strong Year That Positions the Company for the Future….▪ Strong balance sheet▪ Solid cash position▪ Leading market share▪ Sustainable business model▪ Great growth potential▪ Talented and experienced employee team

March 2009 12Analyst / Investor Conference

ARRIS Growth Strategy (2009)▪ Maintain a strong capital structure, mindful of our 2013 debt

maturity, share repurchase opportunities and other capital needs including M&A

▪ Grow our current businesses into a more complete portfolio including a strong video product suite. Continue to invest in the evolution toward enabling true network convergence onto an all IP platform (Convergence Enabled.)

▪ Continue to expand our product/service portfolio through internal developments, partnerships and acquisitions

▪ Expand our international business and begin to consider opportunities in markets other than cable

▪ Continue to invest in and evolve the ARRIS talent pool to implement to above…

March 2009 13Analyst / Investor Conference

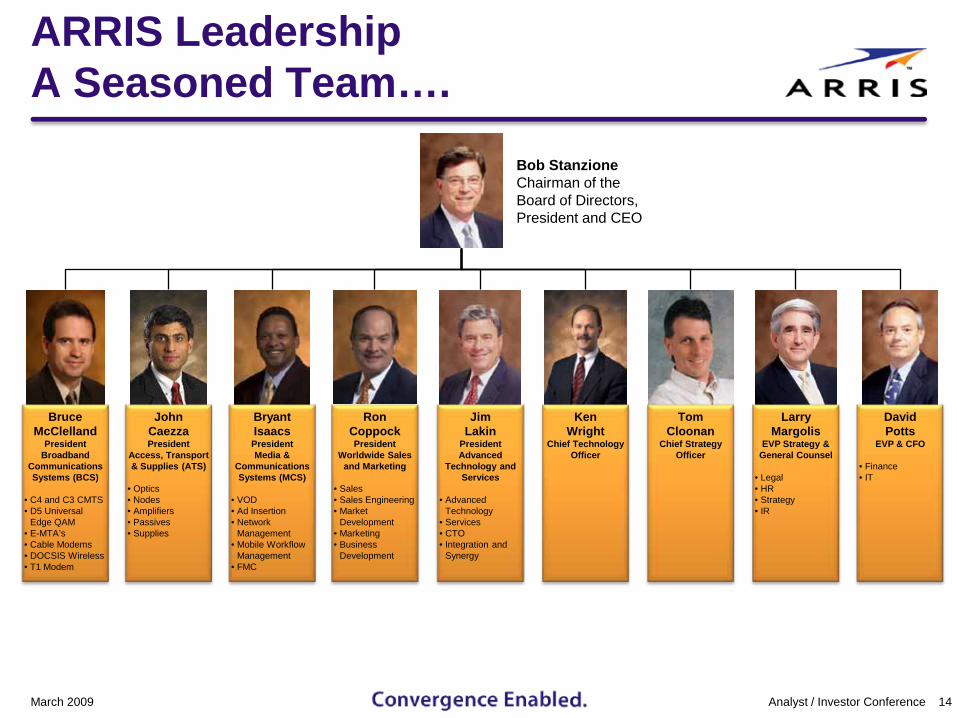

ARRIS Leadership A Seasoned Team….

March 2009 14Analyst / Investor Conference

Bob StanzioneChairman of the Board of Directors, President and CEO

Bruce McClelland

PresidentBroadband

Communications Systems (BCS)

• C4 and C3 CMTS• D5 Universal

Edge QAM• E-MTA’s• Cable Modems• DOCSIS Wireless• T1 Modem

John CaezzaPresident

Access, Transport & Supplies (ATS)

• Optics• Nodes• Amplifiers• Passives• Supplies

Ron CoppockPresident

Worldwide Sales and Marketing

• Sales• Sales Engineering• Market

Development• Marketing• Business

Development

JimLakin

PresidentAdvanced

Technology and Services

• Advanced Technology

• Services• CTO• Integration and

Synergy

Ken Wright

Chief Technology Officer

Tom Cloonan

Chief Strategy Officer

Larry Margolis

EVP Strategy & General Counsel

• Legal• HR• Strategy• IR

DavidPotts

EVP & CFO

• Finance• IT

Bryant IsaacsPresidentMedia &

Communications Systems (MCS)

• VOD• Ad Insertion• Network

Management• Mobile Workflow

Management• FMC

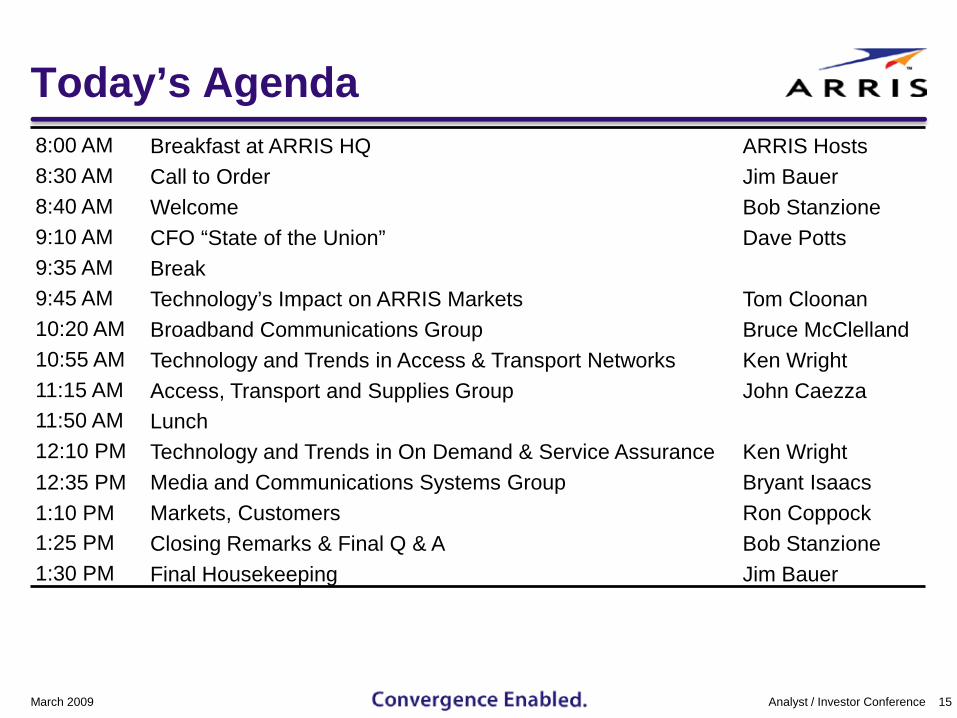

Today’s Agenda8:00 AM Breakfast at ARRIS HQ ARRIS Hosts8:30 AM Call to Order Jim Bauer8:40 AM Welcome Bob Stanzione9:10 AM CFO “State of the Union” Dave Potts9:35 AM Break9:45 AM Technology’s Impact on ARRIS Markets Tom Cloonan10:20 AM Broadband Communications Group Bruce McClelland10:55 AM Technology and Trends in Access & Transport Networks Ken Wright11:15 AM Access, Transport and Supplies Group John Caezza11:50 AM Lunch12:10 PM Technology and Trends in On Demand & Service Assurance Ken Wright12:35 PM Media and Communications Systems Group Bryant Isaacs1:10 PM Markets, Customers Ron Coppock1:25 PM Closing Remarks & Final Q & A Bob Stanzione1:30 PM Final Housekeeping Jim Bauer

March 2009 15Analyst / Investor Conference

Questions

Financial OverviewDavid PottsChief Financial Officer

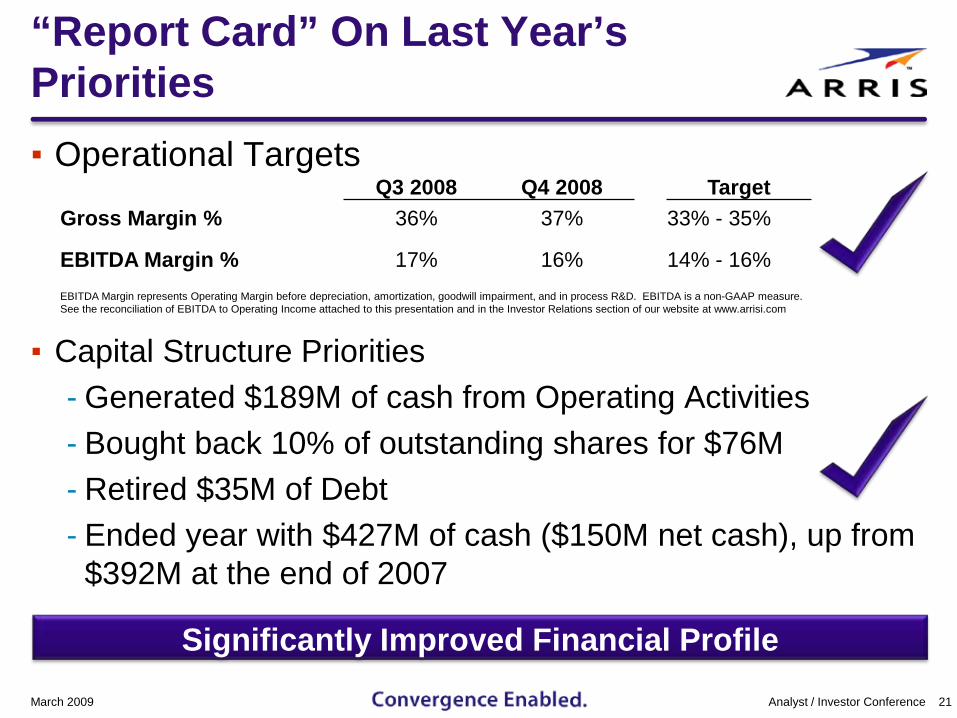

“Report Card” On Last Year’s Priorities

March 2009 18Analyst / Investor Conference

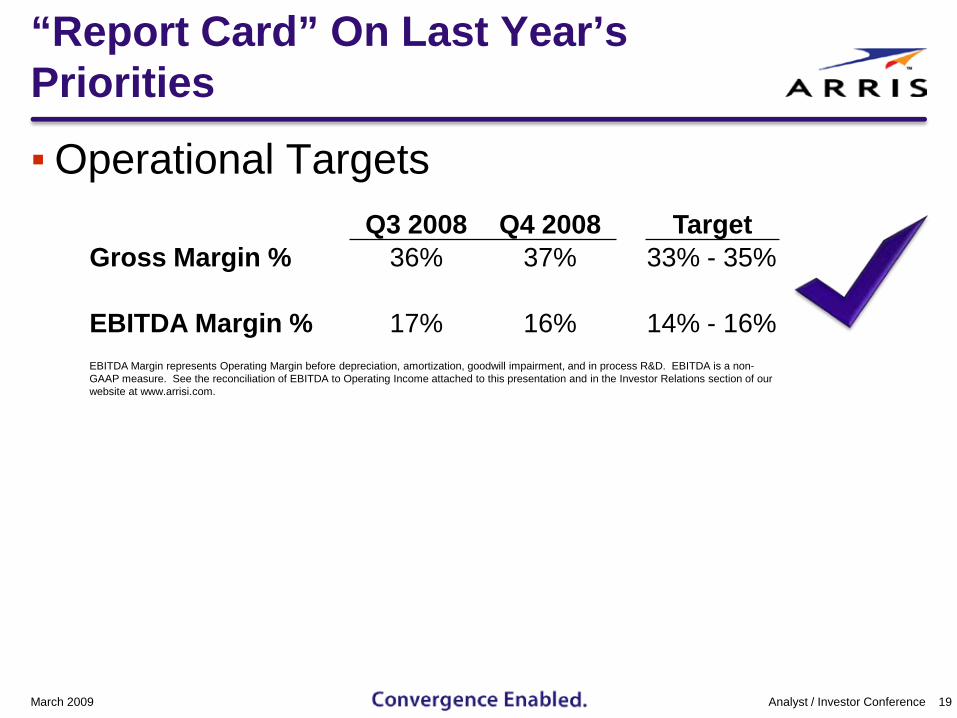

“Report Card” On Last Year’s Priorities

▪Operational Targets

March 2009 19Analyst / Investor Conference

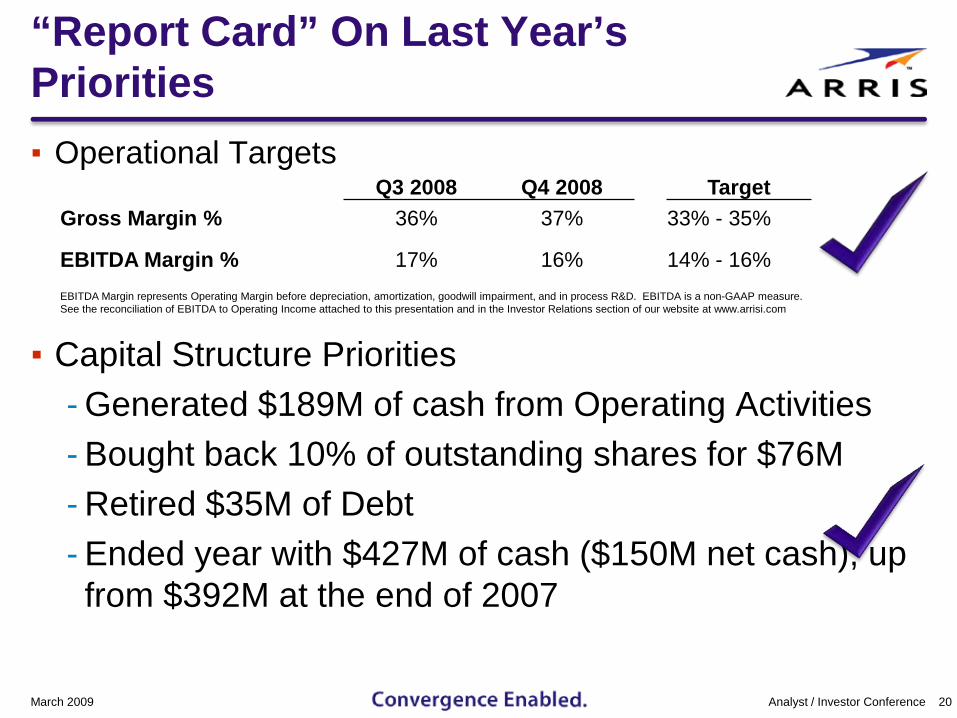

Q3 2008 Q4 2008 TargetGross Margin % 36% 37% 33% - 35%

EBITDA Margin % 17% 16% 14% - 16%EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com.

“Report Card” On Last Year’s Priorities▪ Operational Targets

▪ Capital Structure Priorities - Generated $189M of cash from Operating Activities- Bought back 10% of outstanding shares for $76M- Retired $35M of Debt- Ended year with $427M of cash ($150M net cash), up from $392M at the end of 2007

March 2009 20Analyst / Investor Conference

Q3 2008 Q4 2008 TargetGross Margin % 36% 37% 33% - 35%

EBITDA Margin % 17% 16% 14% - 16%EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com

“Report Card” On Last Year’s Priorities▪ Operational Targets

▪ Capital Structure Priorities - Generated $189M of cash from Operating Activities- Bought back 10% of outstanding shares for $76M- Retired $35M of Debt- Ended year with $427M of cash ($150M net cash), up from

$392M at the end of 2007

March 2009 21Analyst / Investor Conference

Significantly Improved Financial Profile

Q3 2008 Q4 2008 TargetGross Margin % 36% 37% 33% - 35%

EBITDA Margin % 17% 16% 14% - 16%EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com

We Have Made Excellent Progress

2007• Sales $992M• Gross Margin 28%• EBITDA Margin 11%

Analyst / Investor Conference 22March 2009

EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com

We Have Made Excellent Progress

March 2009 23Analyst / Investor Conference

2007• Sales $992M• Gross Margin 28%• EBITDA Margin 11%

2008• Sales $1,145M• Gross Margin 34%• EBITDA Margin 14%

EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com

We Have Made Excellent Progress

March 2009 24Analyst / Investor Conference

How we did it:• C-COR acquisition• CMTS success DOCSIS® 2.0 and 3.0• MCS success• Commitment to R&D• Disciplined spending and product cost

management• Created leverage in the business

2007• Sales $992M• Gross Margin 28%• EBITDA Margin 11%

2008• Sales $1,145M• Gross Margin 34%• EBITDA Margin 14%

EBITDA Margin represents Operating Margin before depreciation, amortization, goodwill impairment, and in process R&D. EBITDA is a non-GAAP measure. See the reconciliation of EBITDA to Operating Income attached to this presentation and in the Investor Relations section of our website at www.arrisi.com

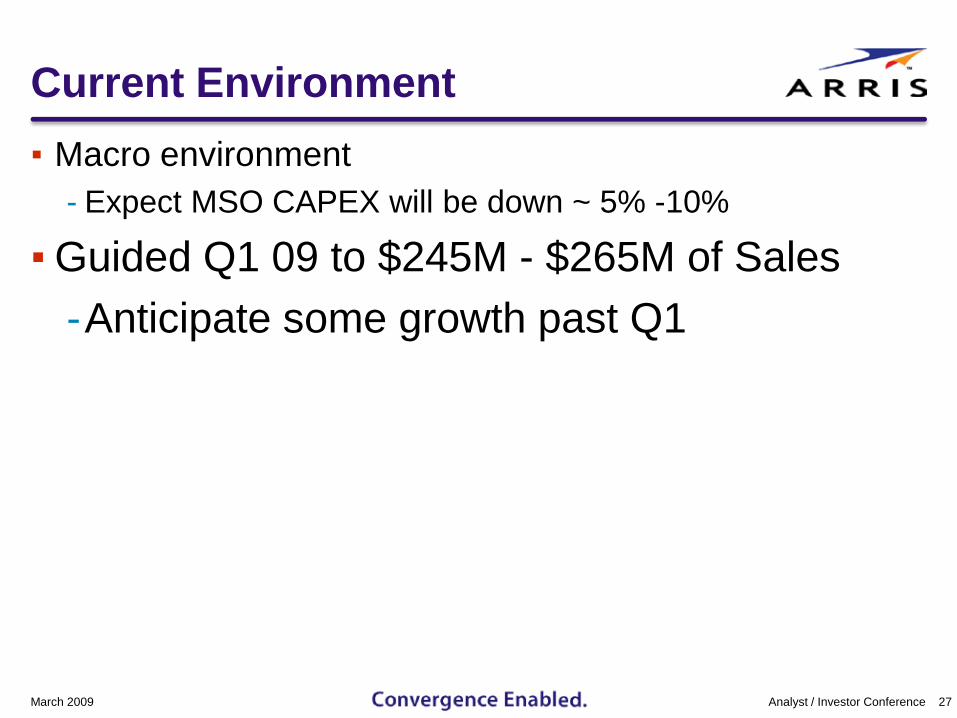

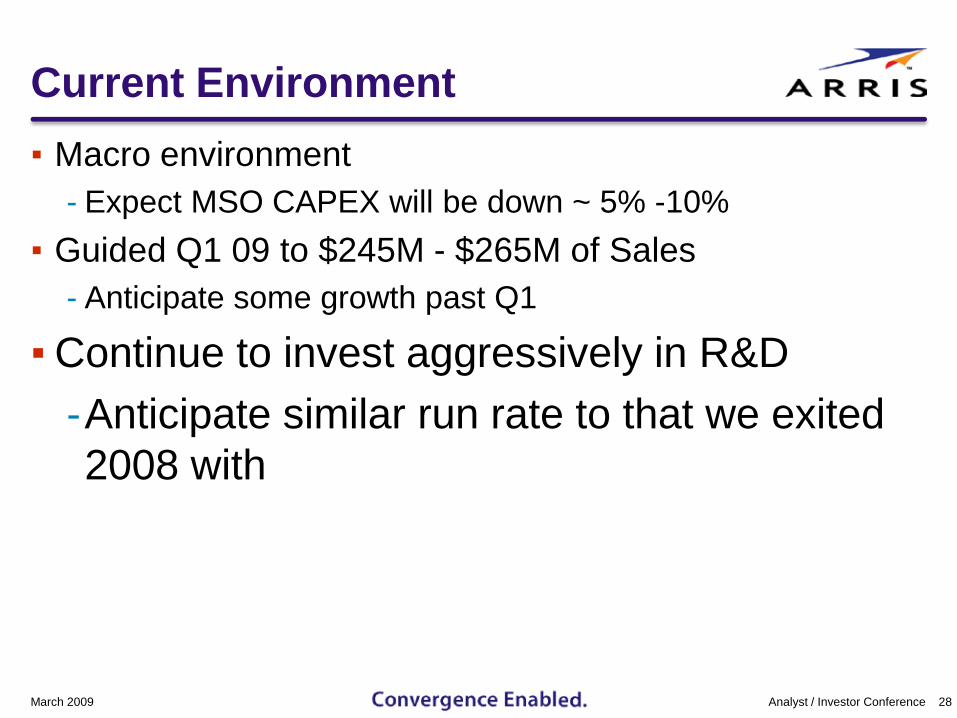

Current Environment

March 2009 25Analyst / Investor Conference

Current Environment

▪Macro environment -Expect MSO CAPEX will be down ~ 5% -10%

March 2009 26Analyst / Investor Conference

Current Environment▪ Macro environment

- Expect MSO CAPEX will be down ~ 5% -10%

▪Guided Q1 09 to $245M - $265M of Sales-Anticipate some growth past Q1

March 2009 27Analyst / Investor Conference

Current Environment▪ Macro environment

- Expect MSO CAPEX will be down ~ 5% -10%▪ Guided Q1 09 to $245M - $265M of Sales

- Anticipate some growth past Q1

▪Continue to invest aggressively in R&D-Anticipate similar run rate to that we exited 2008 with

March 2009 28Analyst / Investor Conference

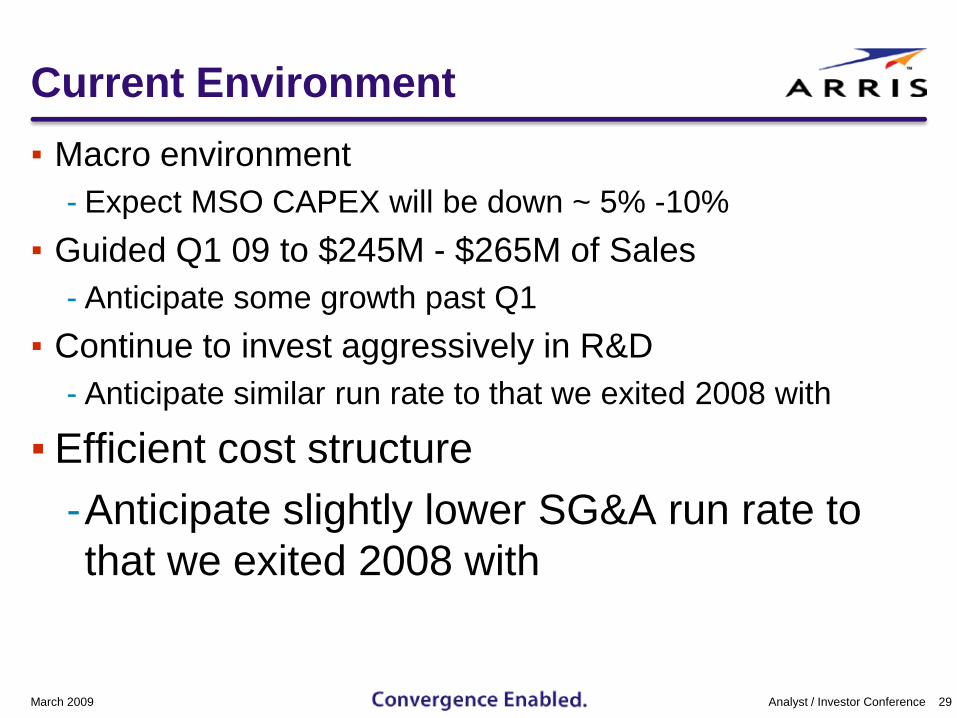

Current Environment▪ Macro environment

- Expect MSO CAPEX will be down ~ 5% -10%▪ Guided Q1 09 to $245M - $265M of Sales

- Anticipate some growth past Q1▪ Continue to invest aggressively in R&D

- Anticipate similar run rate to that we exited 2008 with

▪ Efficient cost structure-Anticipate slightly lower SG&A run rate to that we exited 2008 with

March 2009 29Analyst / Investor Conference

Current Environment▪ Macro environment

- Expect MSO CAPEX will be down ~ 5% -10%▪ Guided Q1 09 to $245M - $265M of Sales

- Anticipate some growth past Q1▪ Continue to invest aggressively in R&D

- Anticipate similar run rate to that we exited 2008 with▪ Efficient cost structure

- Anticipate slightly lower SG&A run rate to that we exited 2008 with

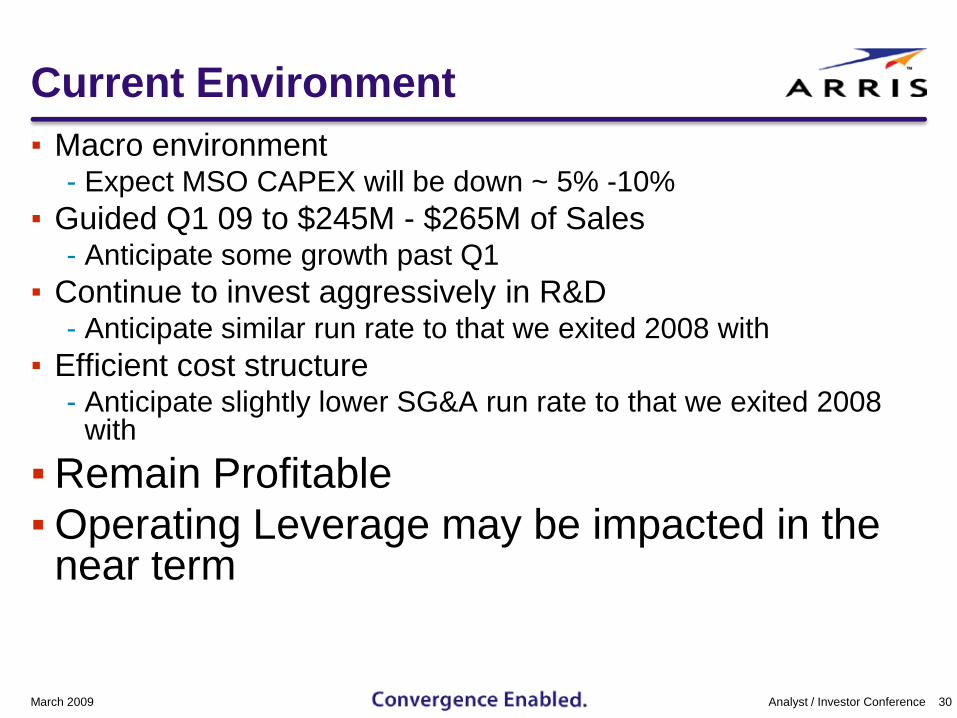

▪Remain Profitable▪Operating Leverage may be impacted in the

near term

March 2009 30Analyst / Investor Conference

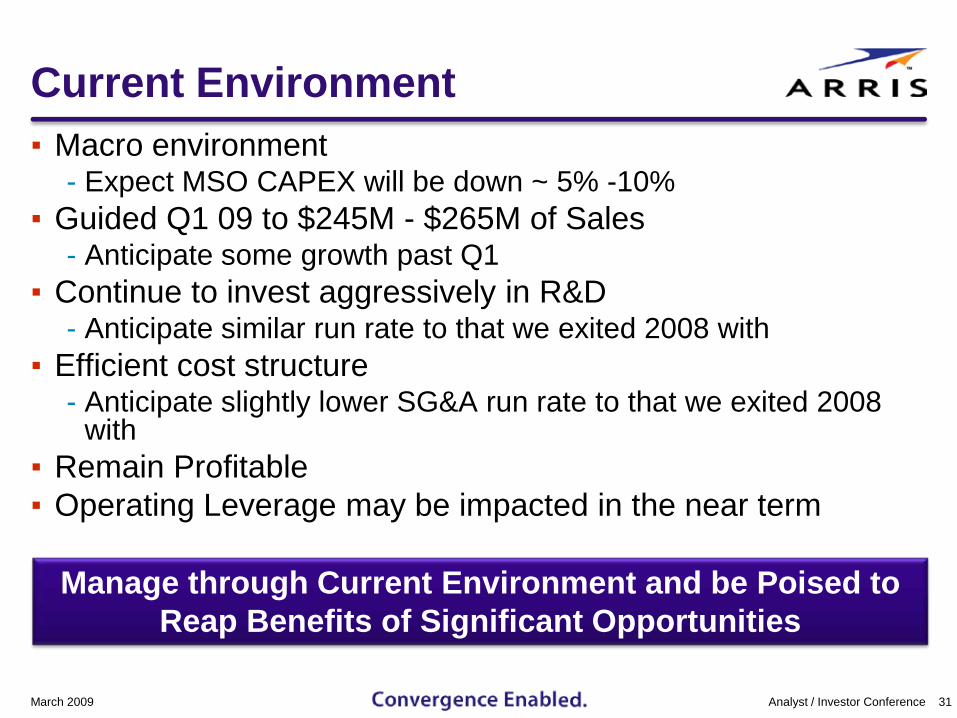

Current Environment▪ Macro environment

- Expect MSO CAPEX will be down ~ 5% -10%▪ Guided Q1 09 to $245M - $265M of Sales

- Anticipate some growth past Q1▪ Continue to invest aggressively in R&D

- Anticipate similar run rate to that we exited 2008 with▪ Efficient cost structure

- Anticipate slightly lower SG&A run rate to that we exited 2008 with

▪ Remain Profitable▪ Operating Leverage may be impacted in the near term

March 2009 31Analyst / Investor Conference

Manage through Current Environment and be Poised to Reap Benefits of Significant Opportunities

Capital Structure Priorities

March 2009 32Analyst / Investor Conference

Capital Structure Priorities

▪Continued cash generation

March 2009 33Analyst / Investor Conference

Capital Structure Priorities▪ Continued cash generation

▪ Ensure sufficient liquidity to run the business

March 2009 34Analyst / Investor Conference

Capital Structure Priorities▪ Continued cash generation▪ Ensure sufficient liquidity to run the business

▪ Ensure sufficient cash resources and access to capital for future acquisitions

March 2009 35Analyst / Investor Conference

Capital Structure Priorities▪ Continued cash generation▪ Ensure sufficient liquidity to run the business▪ Ensure sufficient cash resources and access to capital

for future acquisitions

▪Opportunistically repurchase shares – have increased authorization to $100M

March 2009 36Analyst / Investor Conference

Capital Structure Priorities▪ Continued cash generation▪ Ensure sufficient liquidity to run the business▪ Ensure sufficient cash resources and access to capital

for future acquisitions▪ Opportunistically repurchase shares – Have increased

authorization to $100M

▪Retire Convertible Debt on or before maturity in 2013

March 2009 37Analyst / Investor Conference

Capital Structure Priorities▪ Continued cash generation▪ Ensure sufficient liquidity to run the business▪ Ensure sufficient cash resources and access to capital

for future acquisitions▪ Opportunistically repurchase shares – have increased

authorization to $100M▪ Retire Convertible Debt on or before maturity in 2013

March 2009 38Analyst / Investor Conference

Cash Is King in this EnvironmentMust Prudently Balance Liquidity

and Potential Uses

Looking Forward……

March 2009 39Analyst / Investor Conference

Well Positioned For The Future

Looking Forward…

March 2009 40Analyst / Investor Conference

Future• Capture share of IP Video CAPEX…

Convergence Enabled. • Continued IP voice & data success• Growth in MCS products• Resurgence of ATS as the economy recovers• We have a strong balance sheet • Profitable growth… operating leverage

Today

Well Positioned For The Future

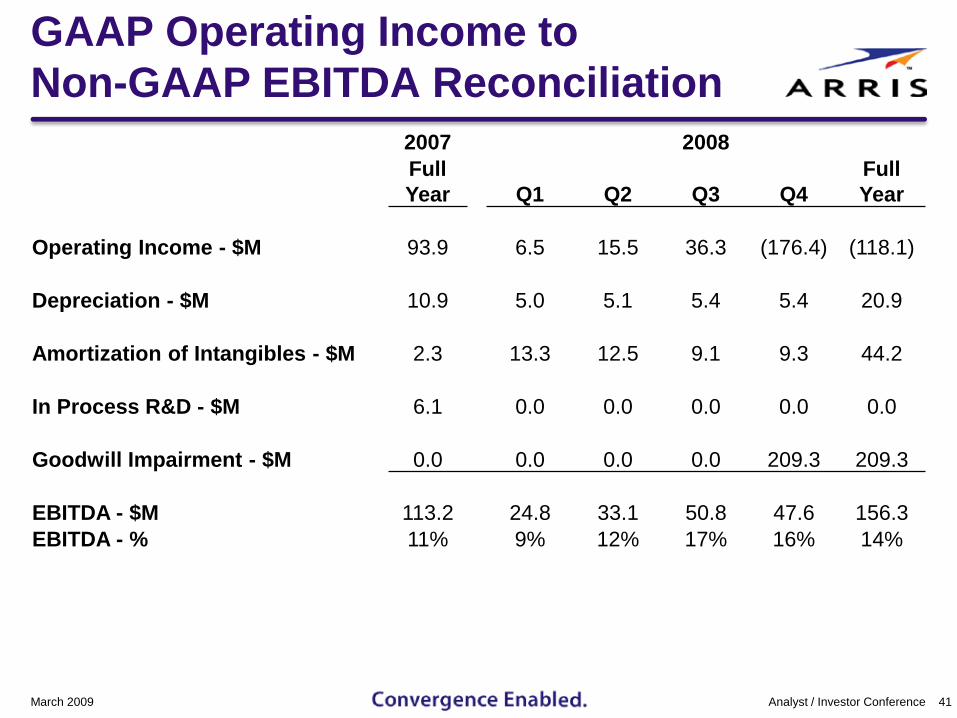

GAAP Operating Income to Non-GAAP EBITDA Reconciliation

2007 2008Full Year Q1 Q2 Q3 Q4

Full Year

Operating Income - $M 93.9 6.5 15.5 36.3 (176.4) (118.1)

Depreciation - $M 10.9 5.0 5.1 5.4 5.4 20.9

Amortization of Intangibles - $M 2.3 13.3 12.5 9.1 9.3 44.2

In Process R&D - $M 6.1 0.0 0.0 0.0 0.0 0.0

Goodwill Impairment - $M 0.0 0.0 0.0 0.0 209.3 209.3

EBITDA - $M 113.2 24.8 33.1 50.8 47.6 156.3 EBITDA - % 11% 9% 12% 17% 16% 14%

March 2009 41Analyst / Investor Conference

Questions

Break

March 2009 43Analyst / Investor Conference

Future Broadband Trends and the CMTS Architectural Evolution Beyond DOCSIS 3.0Tom CloonanChief Strategy Officer

ARRIS Confidential

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS® Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 45Analyst / Investor Conference

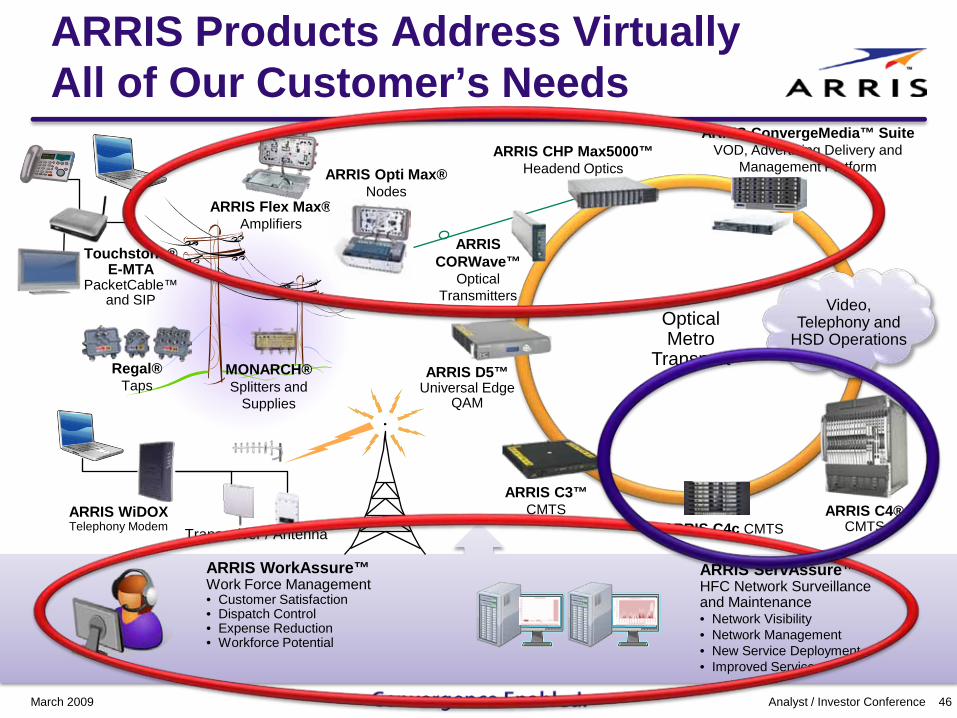

Optical Metro

Transport

ARRIS WorkAssure™ Work Force Management• Customer Satisfaction• Dispatch Control• Expense Reduction• Workforce Potential

Regal®Taps

MONARCH®Splitters and

Supplies

ARRIS CHP Max5000™Headend Optics

ARRIS ServAssure™ HFC Network Surveillance and Maintenance• Network Visibility• Network Management• New Service Deployment• Improved Service

ARRIS D5™ Universal Edge

QAM

ARRIS C4® CMTS

ARRIS Flex Max®Amplifiers

ARRIS Opti Max® Nodes

Touchstone® E-MTA

PacketCable™ and SIP

ARRIS CORWave™

Optical Transmitters

ARRIS Products Address Virtually All of Our Customer’s Needs

March 2009 46Analyst / Investor Conference

ARRIS C3™ CMTS

Transceiver / AntennaARRIS WiDOX Telephony Modem

Video, Telephony and

HSD Operations

ARRIS C4c CMTS

ARRIS ConvergeMedia™ SuiteVOD, Advertising Delivery and

Management Platform

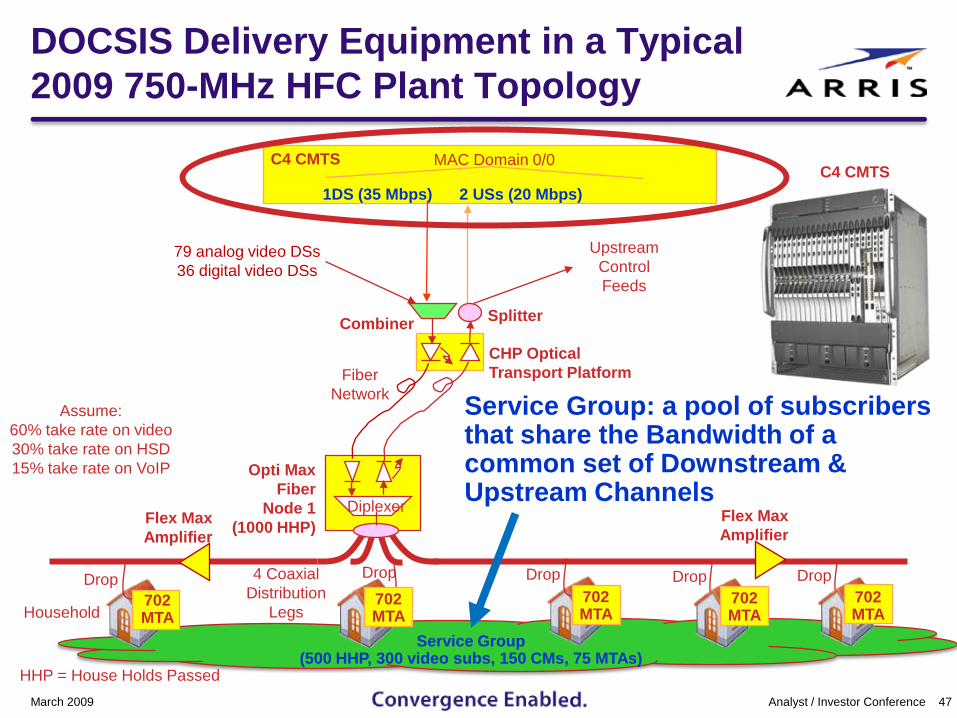

CHP Optical Transport Platform

1DS (35 Mbps) 2 USs (20 Mbps)

MAC Domain 0/0

Combiner

C4 CMTS

Splitter

UpstreamControlFeeds

HHP = House Holds Passed

Opti MaxFiber

Node 1(1000 HHP)

Drop

Household

Diplexer

4 CoaxialDistribution

Legs

Service Group(500 HHP, 300 video subs, 150 CMs, 75 MTAs)

Assume:60% take rate on video30% take rate on HSD15% take rate on VoIP

DropDrop

79 analog video DSs36 digital video DSs

DropDrop

Flex MaxAmplifier

Flex MaxAmplifier

FiberNetwork

702MTA

702MTA

702MTA

702MTA

702MTA

DOCSIS Delivery Equipment in a Typical 2009 750-MHz HFC Plant Topology

March 2009 47Analyst / Investor Conference

Service Group: a pool of subscribersthat share the Bandwidth of a common set of Downstream & Upstream Channels

C4 CMTS

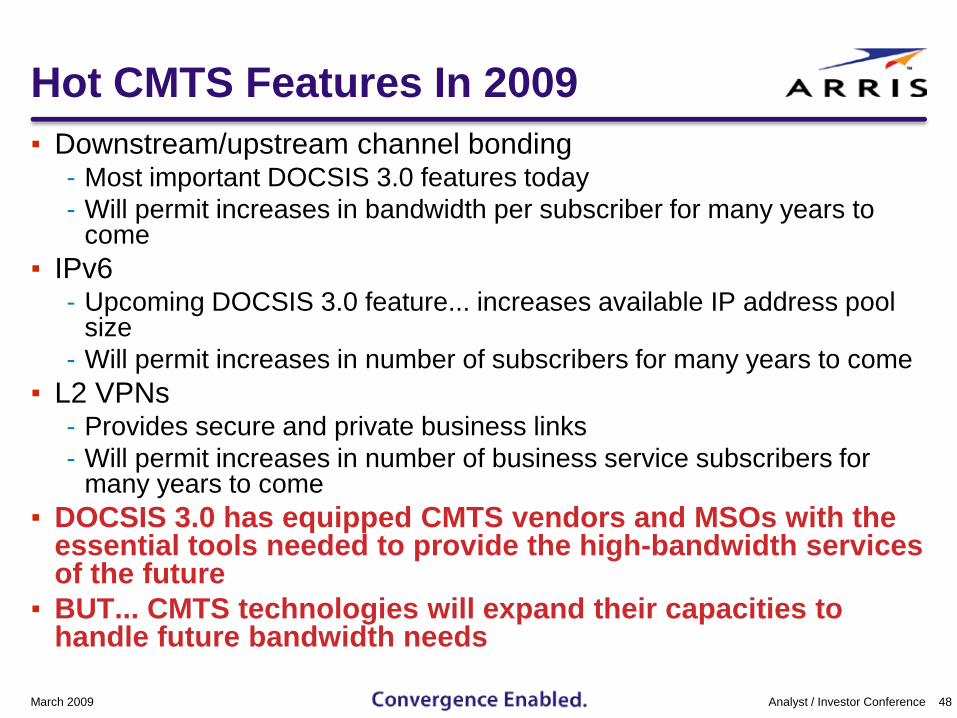

Hot CMTS Features In 2009▪ Downstream/upstream channel bonding

- Most important DOCSIS 3.0 features today- Will permit increases in bandwidth per subscriber for many years to

come▪ IPv6

- Upcoming DOCSIS 3.0 feature... increases available IP address pool size

- Will permit increases in number of subscribers for many years to come▪ L2 VPNs

- Provides secure and private business links- Will permit increases in number of business service subscribers for

many years to come▪ DOCSIS 3.0 has equipped CMTS vendors and MSOs with the

essential tools needed to provide the high-bandwidth services of the future

▪ BUT... CMTS technologies will expand their capacities to handle future bandwidth needs

March 2009 48Analyst / Investor Conference

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 49Analyst / Investor Conference

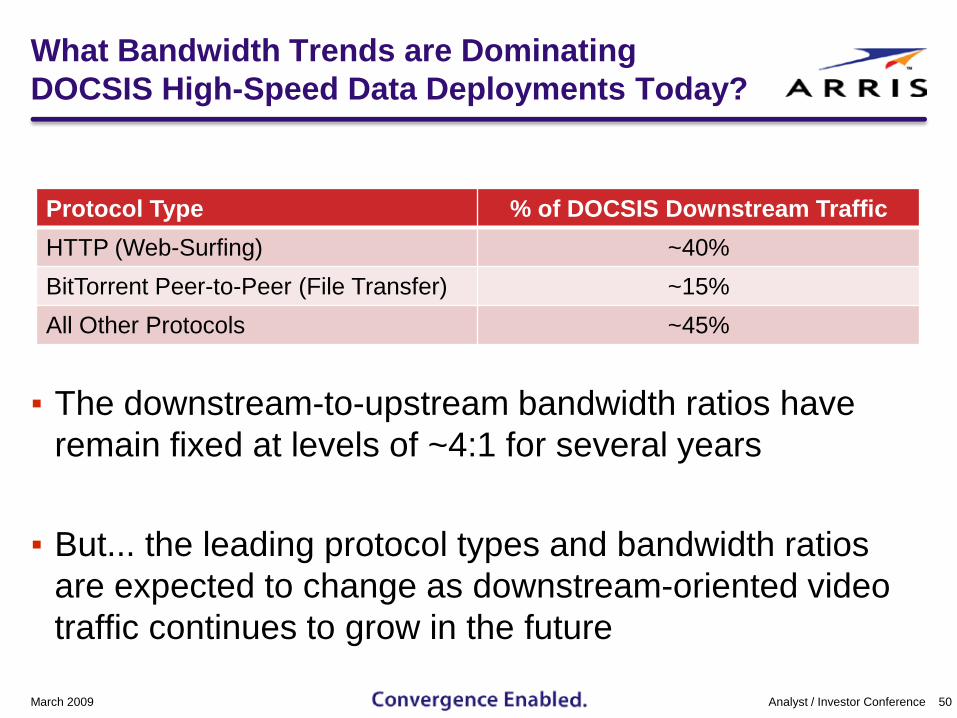

What Bandwidth Trends are Dominating DOCSIS High-Speed Data Deployments Today?

▪ The downstream-to-upstream bandwidth ratios have remain fixed at levels of ~4:1 for several years

▪ But... the leading protocol types and bandwidth ratios are expected to change as downstream-oriented video traffic continues to grow in the future

March 2009 50Analyst / Investor Conference

Protocol Type % of DOCSIS Downstream TrafficHTTP (Web-Surfing) ~40%BitTorrent Peer-to-Peer (File Transfer) ~15%All Other Protocols ~45%

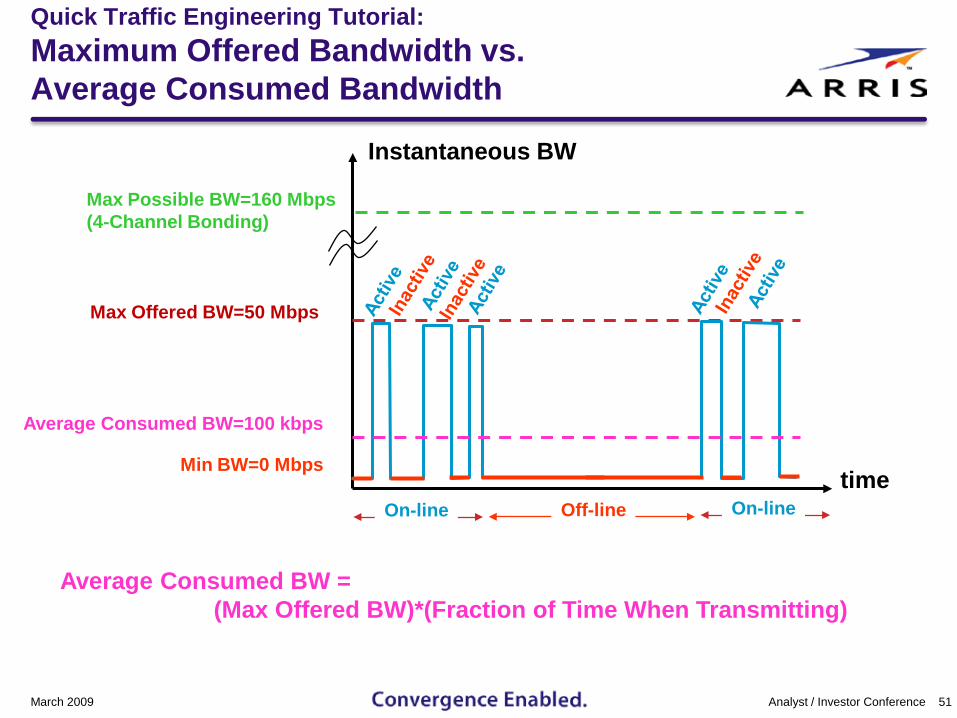

Quick Traffic Engineering Tutorial:Maximum Offered Bandwidth vs. Average Consumed Bandwidth

March 2009 51Analyst / Investor Conference

time

Instantaneous BW

Min BW=0 Mbps

Max Offered BW=50 Mbps

Max Possible BW=160 Mbps(4-Channel Bonding)

On-line On-lineOff-line

Average Consumed BW=100 kbps

Average Consumed BW = (Max Offered BW)*(Fraction of Time When Transmitting)

How Much HSD Capacity Growth Is Expected in the Future?

March 2009 52Analyst / Investor Conference

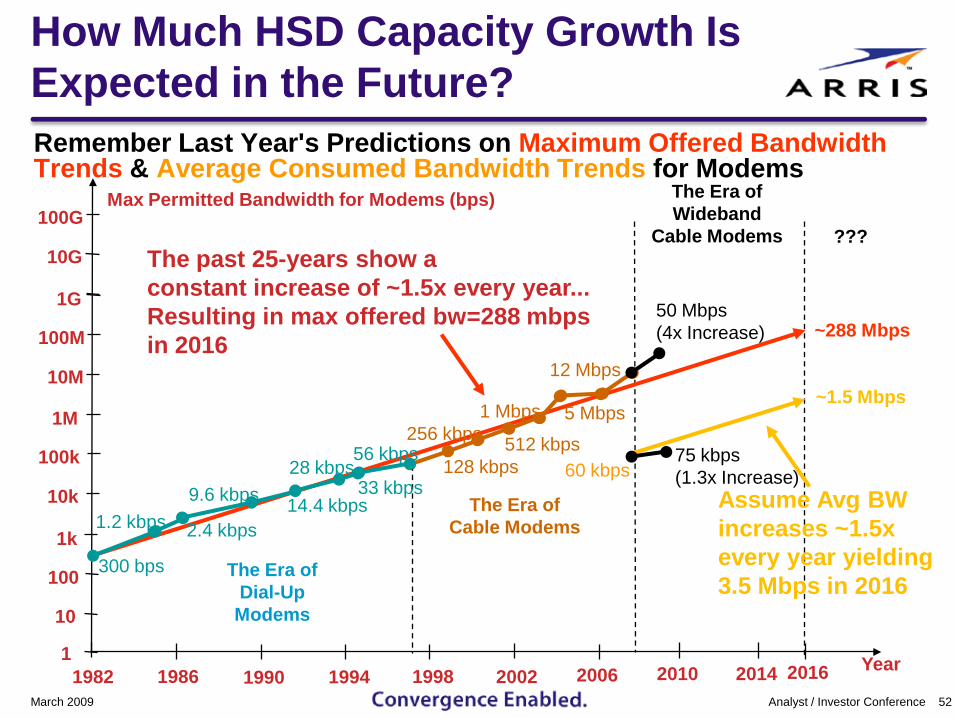

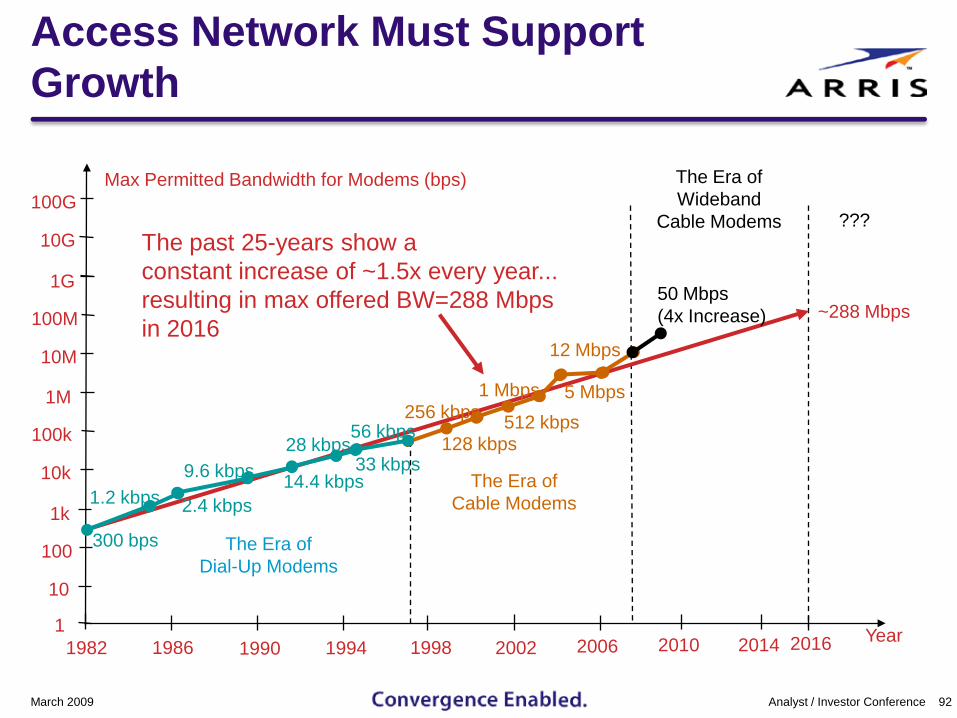

Remember Last Year's Predictions on Maximum Offered Bandwidth Trends & Average Consumed Bandwidth Trends for Modems

Max Permitted Bandwidth for Modems (bps)

1982 1986 1990 1994 19981

10

100

1k

2002 2006

10k

100k

1M

10M

100M

1G

2010 Year2014

10G

100G

2016

The Era ofWideband

Cable Modems ???

12 Mbps

The past 25-years show aconstant increase of ~1.5x every year...Resulting in max offered bw=288 mbpsin 2016

~288 Mbps

128 kbps

256 kbps 512 kbps

1 Mbps 5 Mbps

The Era ofCable Modems2.4 kbps

300 bps

56 kbps

1.2 kbps9.6 kbps 14.4 kbps

28 kbps33 kbps

The Era ofDial-Up

Modems

60 kbps

~1.5 Mbps

Assume Avg BWincreases ~1.5xevery year yielding3.5 Mbps in 2016

50 Mbps(4x Increase)

75 kbps(1.3x Increase)

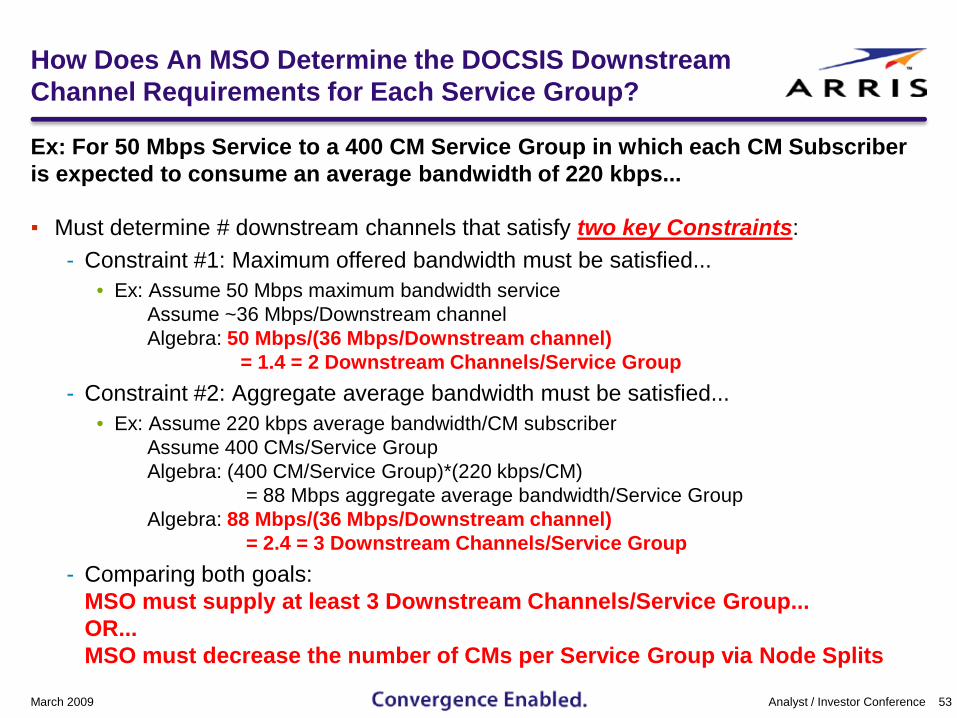

How Does An MSO Determine the DOCSIS Downstream Channel Requirements for Each Service Group?

Ex: For 50 Mbps Service to a 400 CM Service Group in which each CM Subscriber is expected to consume an average bandwidth of 220 kbps...

▪ Must determine # downstream channels that satisfy two key Constraints:- Constraint #1: Maximum offered bandwidth must be satisfied...

• Ex: Assume 50 Mbps maximum bandwidth serviceAssume ~36 Mbps/Downstream channelAlgebra: 50 Mbps/(36 Mbps/Downstream channel)

= 1.4 = 2 Downstream Channels/Service Group- Constraint #2: Aggregate average bandwidth must be satisfied...

• Ex: Assume 220 kbps average bandwidth/CM subscriberAssume 400 CMs/Service GroupAlgebra: (400 CM/Service Group)*(220 kbps/CM)

= 88 Mbps aggregate average bandwidth/Service GroupAlgebra: 88 Mbps/(36 Mbps/Downstream channel)

= 2.4 = 3 Downstream Channels/Service Group- Comparing both goals:

MSO must supply at least 3 Downstream Channels/Service Group... OR... MSO must decrease the number of CMs per Service Group via Node Splits

March 2009 53Analyst / Investor Conference

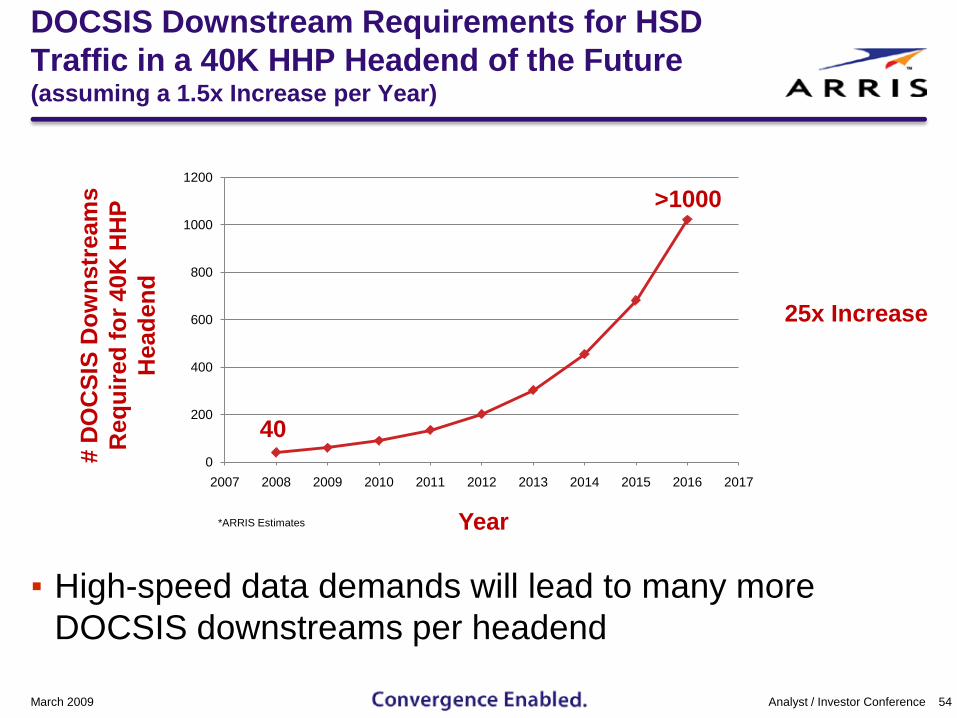

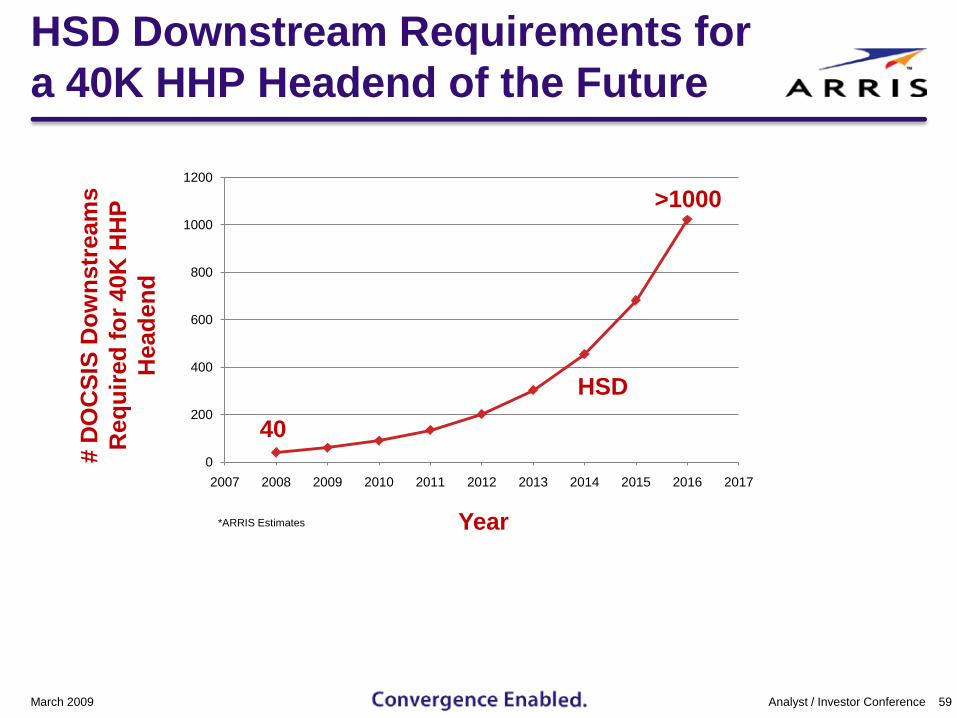

DOCSIS Downstream Requirements for HSD Traffic in a 40K HHP Headend of the Future(assuming a 1.5x Increase per Year)

▪ High-speed data demands will lead to many more DOCSIS downstreams per headend

54

0

200

400

600

800

1000

1200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

# D

OC

SIS

Dow

nstr

eam

sR

equi

red

for 4

0K H

HP

Hea

dend

Year

40

>1000

25x Increase

*ARRIS Estimates

Analyst / Investor ConferenceMarch 2009

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video and IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 55Analyst / Investor Conference

IP-Based Video and Its Effects On Future DOCSIS CMTSs▪ IP-based Video content viewing (ex: YouTube) increased by

34% last year1 !!!

▪ YouTube + Flash Video have grown to be ~10% of all Internet traffic as of December 20082

▪ Each future Standard-Definition MPEG-4 IP-based Video Feed will require ~1.2 Mbps of continuous DOCSIS bandwidth during the duration of the video !!!

▪ IP-based Over-the-Top Video Transport is growing and willplay a major role in the future of DOCSIS capacity needs...

March 2009 56Analyst / Investor Conference

1. comScore Press Release dated January 5, 20092. Measurements provided by an MSO

IPTV... The New Kid On The Block▪ IP-based Video could become a significant revenue source▪ Many MSOs would like to become THE primary sources for

IP-based Video... but want to deliver a new flavor▪ IPTV = Delivery of High-Quality Digital Video Services over a

Managed Broadband Network via Internet Protocol to:▪ Personal Computers in the Home▪Hand-Held Devices (cell phones &

PDAs) in the Home▪ TVs with IP STBs in the home

▪ MSOs are now seriously looking into IPTV delivery using DOCSIS

▪ This is a game-changer for future CMTS channel requirements

March 2009 57Analyst / Investor Conference

MSO ContentInternet Content

Any Device, Anywhere

Place and Time Shifting

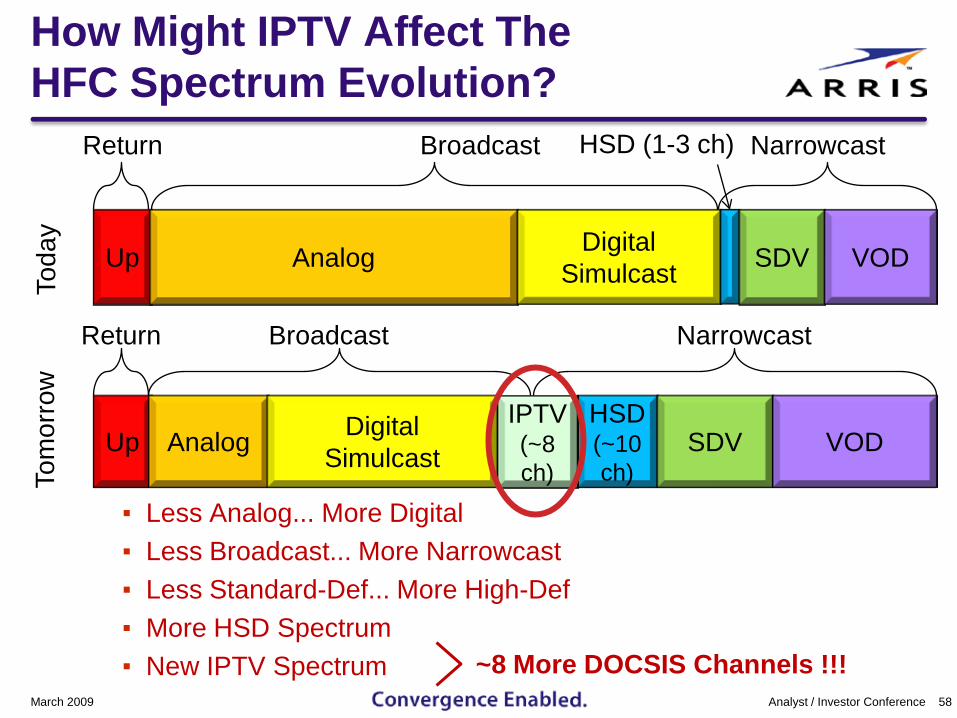

How Might IPTV Affect TheHFC Spectrum Evolution?

March 2009 58Analyst / Investor Conference

▪ Less Analog... More Digital▪ Less Broadcast... More Narrowcast ▪ Less Standard-Def... More High-Def▪ More HSD Spectrum▪ New IPTV Spectrum

Broadcast NarrowcastReturn

Up Analog DigitalSimulcast SDV VOD

Broadcast NarrowcastReturn

Toda

yTo

mor

row

Up Analog DigitalSimulcast

HSD(~10 ch)

SDV VODIPTV(~8 ch)

HSD (1-3 ch)

~8 More DOCSIS Channels !!!

HSD Downstream Requirements for a 40K HHP Headend of the Future

59

0

200

400

600

800

1000

1200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

# D

OC

SIS

Dow

nstr

eam

sR

equi

red

for 4

0K H

HP

Hea

dend

Year

40

>1000

HSD

*ARRIS Estimates

Analyst / Investor ConferenceMarch 2009

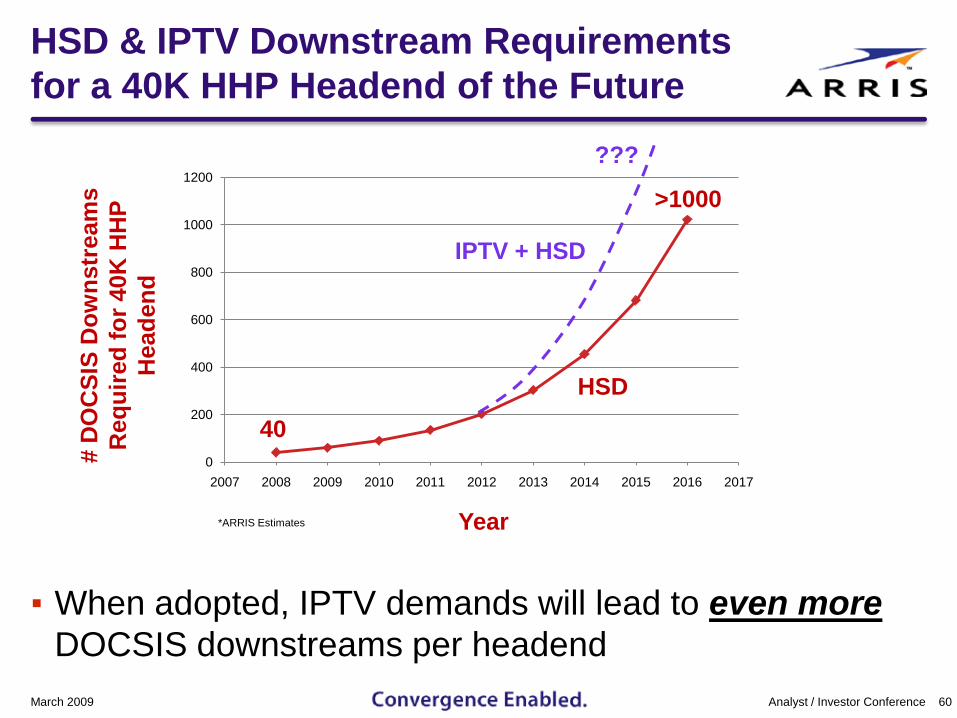

HSD & IPTV Downstream Requirements for a 40K HHP Headend of the Future

▪ When adopted, IPTV demands will lead to even more DOCSIS downstreams per headend

60

0

200

400

600

800

1000

1200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

# D

OC

SIS

Dow

nstr

eam

sR

equi

red

for 4

0K H

HP

Hea

dend

Year

40

>1000

HSD

IPTV + HSD

???

*ARRIS Estimates

Analyst / Investor ConferenceMarch 2009

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 61Analyst / Investor Conference

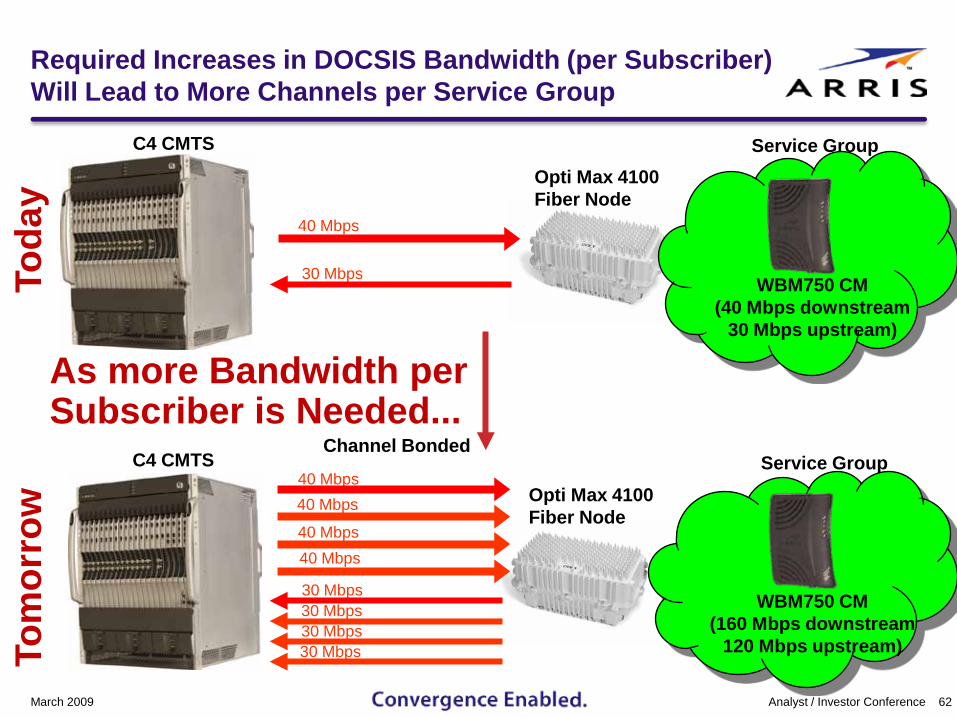

Required Increases in DOCSIS Bandwidth (per Subscriber) Will Lead to More Channels per Service Group

62

C4 CMTS

40 Mbps

30 Mbps

As more Bandwidth per Subscriber is Needed...

WBM750 CM(40 Mbps downstream

30 Mbps upstream)

Service GroupOpti Max 4100Fiber Node

Toda

y

WBM750 CM(160 Mbps downstream

120 Mbps upstream)

C4 CMTS40 Mbps40 Mbps

40 Mbps40 Mbps

30 Mbps30 Mbps30 Mbps30 Mbps

Service GroupOpti Max 4100Fiber Node

Channel Bonded

Tom

orro

w

Analyst / Investor ConferenceMarch 2009

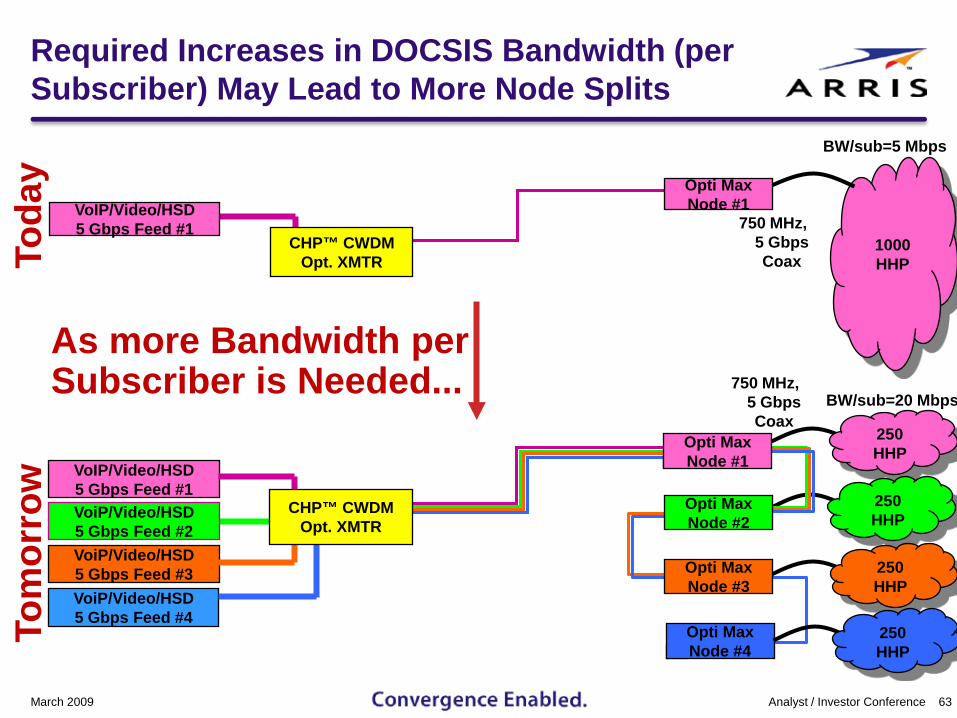

Required Increases in DOCSIS Bandwidth (per Subscriber) May Lead to More Node Splits

March 2009 63Analyst / Investor Conference

As more Bandwidth per Subscriber is Needed...

1000HHP

CHP™ CWDMOpt. XMTR

750 MHz,5 GbpsCoax

VoIP/Video/HSD5 Gbps Feed #1

Opti MaxNode #1

BW/sub=5 Mbps

Toda

y

VoIP/Video/HSD5 Gbps Feed #1

VoiP/Video/HSD5 Gbps Feed #3VoiP/Video/HSD5 Gbps Feed #4

VoiP/Video/HSD5 Gbps Feed #2

CHP™ CWDMOpt. XMTR

Opti MaxNode #2

Opti MaxNode #3

Opti MaxNode #4

Opti MaxNode #1

250HHP

250HHP

250HHP

250HHP

750 MHz,5 GbpsCoax

BW/sub=20 Mbps

Tom

orro

w

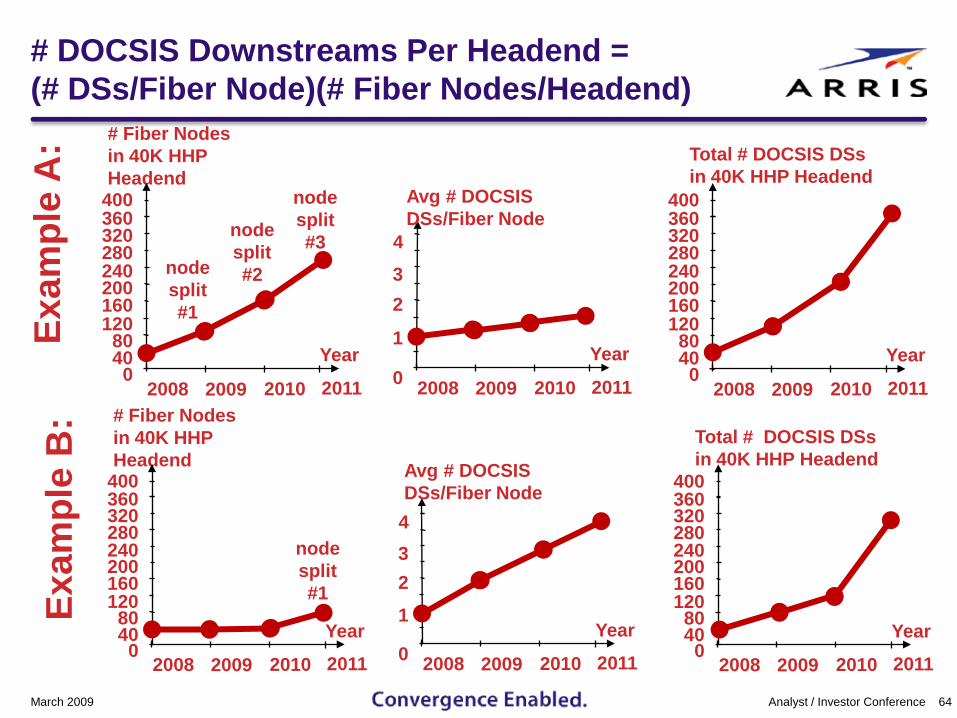

# DOCSIS Downstreams Per Headend = (# DSs/Fiber Node)(# Fiber Nodes/Headend)

March 2009 64Analyst / Investor Conference

# Fiber Nodesin 40K HHPHeadend

2008 2009 20100

4080

120

2011

160200240280320360

Year

400

Exam

ple

A:

nodesplit#1

nodesplit#2

nodesplit#3

2008 2009 20100 2011

1

23

Year

4

Avg # DOCSISDSs/Fiber Node

Total # DOCSIS DSsin 40K HHP Headend

2008 2009 20100

4080

120

2011

160200240280320360

Year

400

# Fiber Nodesin 40K HHPHeadend

2008 2009 20100

4080

120

2011

160200240280320360

Year

400

nodesplit#1

2008 2009 20100 2011

1

23

Year

4

Avg # DOCSISDSs/Fiber Node

Total # DOCSIS DSsin 40K HHP Headend

2008 2009 20100

4080

120

2011

160200240280320360

Year

400

Exam

ple

B:

The Ever-Growing Demand for Bandwidth…and its Impact on DOCSIS CMTS Requirements

March 2009 65Analyst / Investor Conference

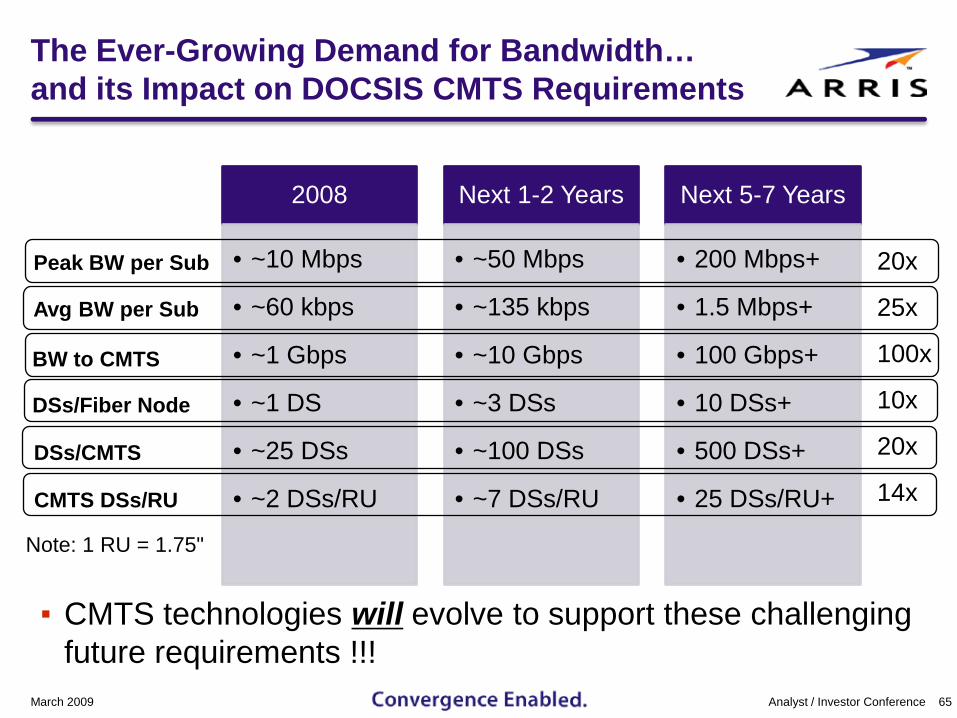

2008

• ~10 Mbps

• ~60 kbps

• ~1 Gbps

• ~1 DS

• ~25 DSs

• ~2 DSs/RU

Next 1-2 Years

• ~50 Mbps

• ~135 kbps

• ~10 Gbps

• ~3 DSs

• ~100 DSs

• ~7 DSs/RU

Next 5-7 Years

• 200 Mbps+

• 1.5 Mbps+

• 100 Gbps+

• 10 DSs+

• 500 DSs+

• 25 DSs/RU+

Peak BW per Sub

Avg BW per Sub

BW to CMTS

DSs/Fiber Node

DSs/CMTS

CMTS DSs/RU

▪ CMTS technologies will evolve to support these challenging future requirements !!!

Note: 1 RU = 1.75"

20x

25x

100x

10x

20x

14x

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 66Analyst / Investor Conference

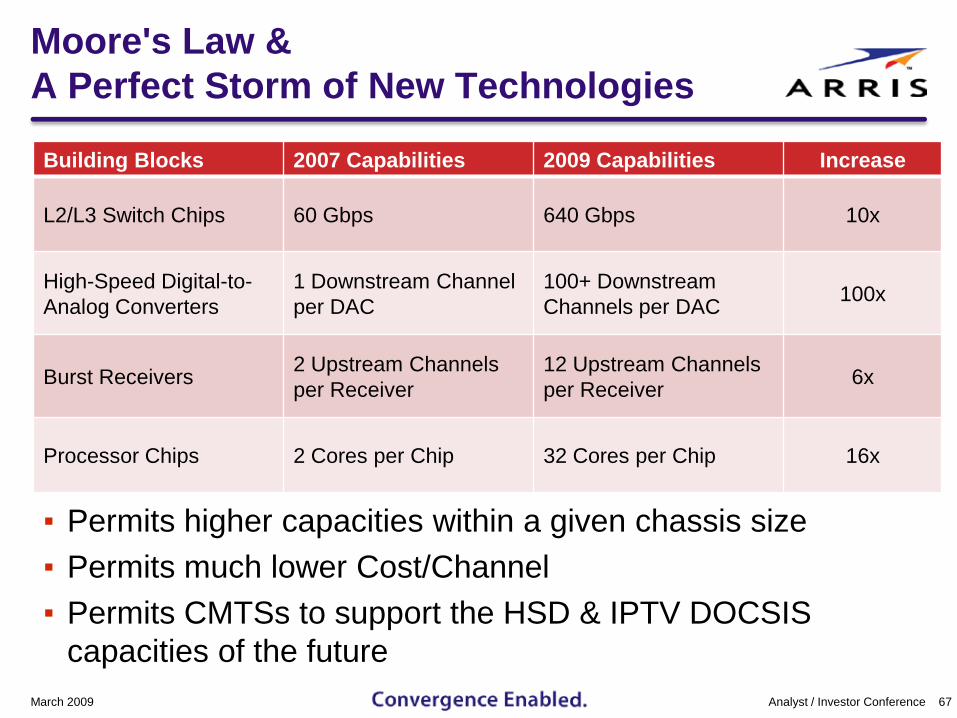

Moore's Law & A Perfect Storm of New Technologies

March 2009 67Analyst / Investor Conference

▪ Permits higher capacities within a given chassis size▪ Permits much lower Cost/Channel▪ Permits CMTSs to support the HSD & IPTV DOCSIS

capacities of the future

Building Blocks 2007 Capabilities 2009 Capabilities Increase

L2/L3 Switch Chips 60 Gbps 640 Gbps 10x

High-Speed Digital-to-Analog Converters

1 Downstream Channel per DAC

100+ Downstream Channels per DAC 100x

Burst Receivers 2 Upstream Channels per Receiver

12 Upstream Channels per Receiver 6x

Processor Chips 2 Cores per Chip 32 Cores per Chip 16x

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 68Analyst / Investor Conference

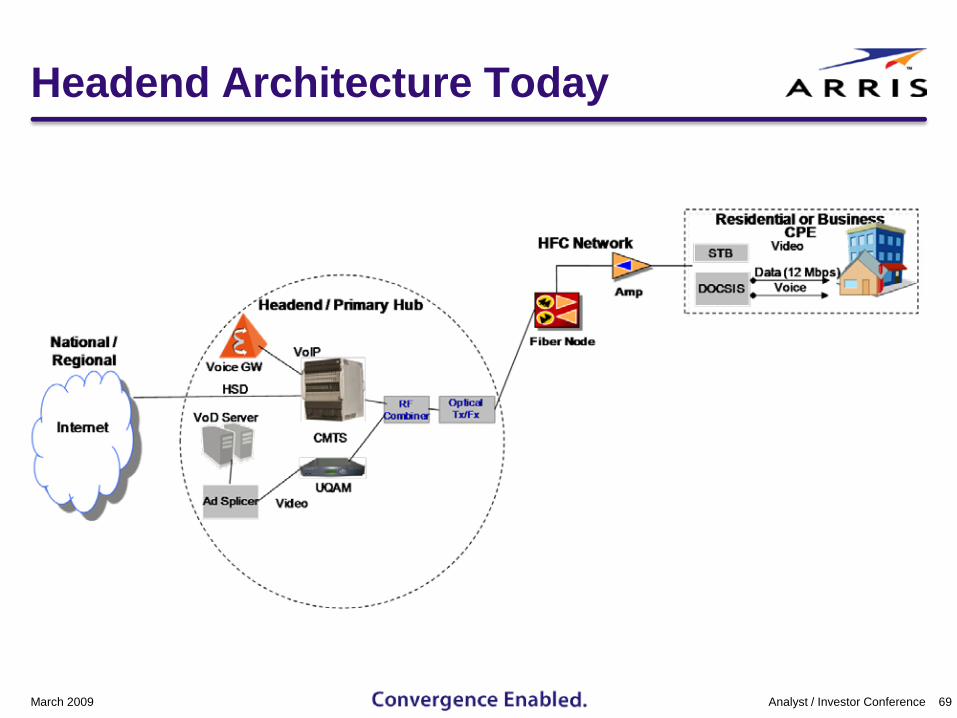

Headend Architecture Today

March 2009 69Analyst / Investor Conference

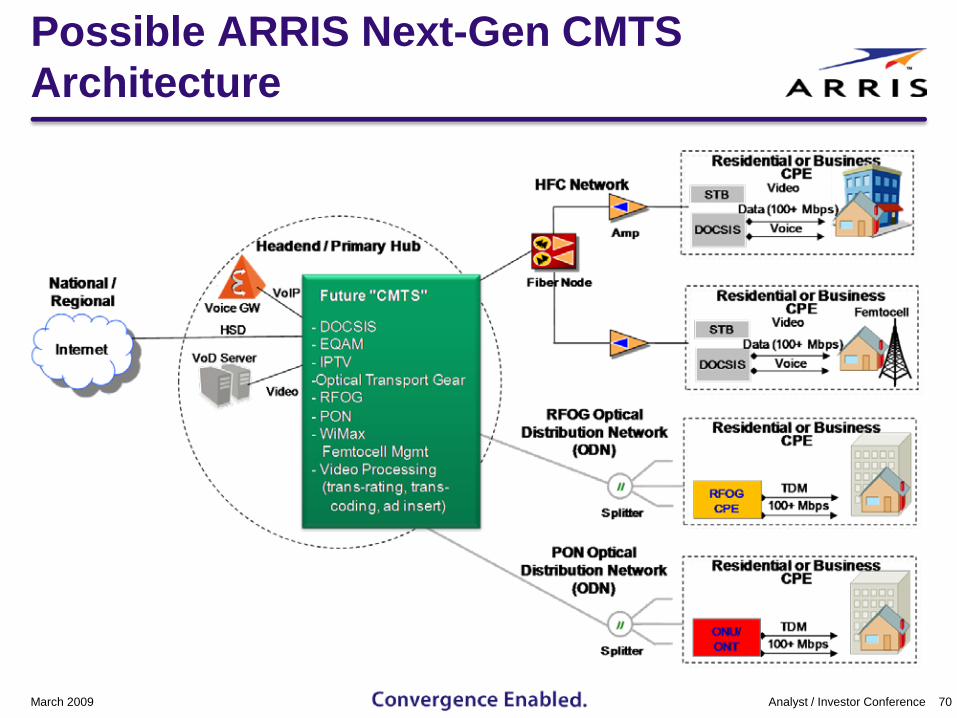

Possible ARRIS Next-Gen CMTS Architecture

March 2009 70Analyst / Investor Conference

Agenda▪ Introduction & CMTS Feature Trends▪ Future DOCSIS Bandwidth Growth

- High-Speed Data- IP-Based Video & IPTV

▪ MSO Response to DOCSIS Bandwidth Growth▪ Technologies for the Future▪ A Vision of the ARRIS CMTS Product Evolution▪ Conclusions

March 2009 71Analyst / Investor Conference

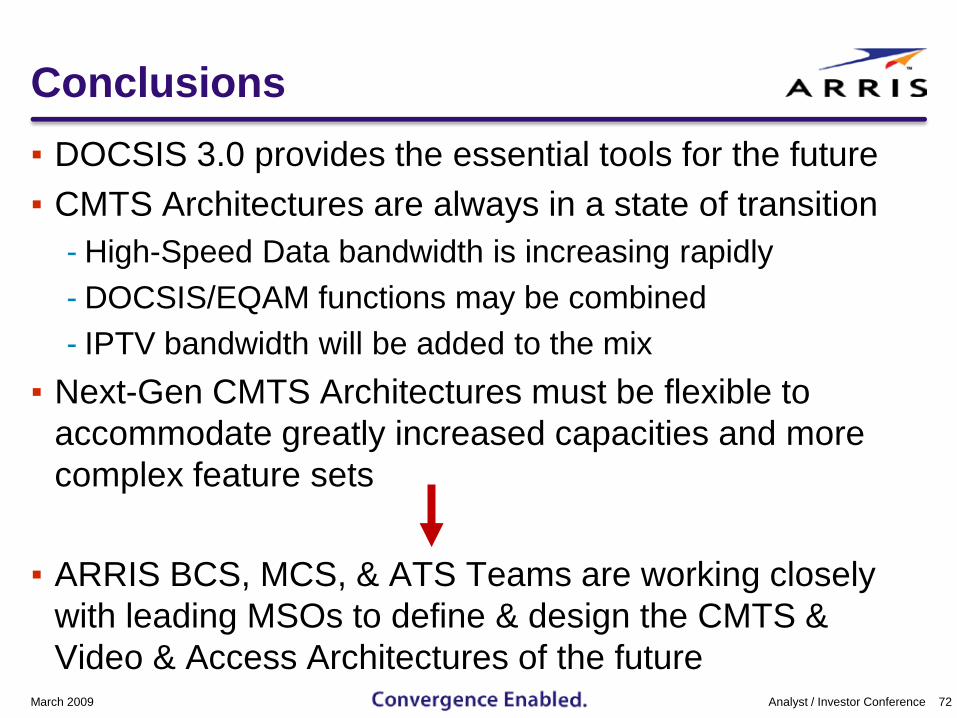

Conclusions▪ DOCSIS 3.0 provides the essential tools for the future▪ CMTS Architectures are always in a state of transition

- High-Speed Data bandwidth is increasing rapidly- DOCSIS/EQAM functions may be combined- IPTV bandwidth will be added to the mix

▪ Next-Gen CMTS Architectures must be flexible to accommodate greatly increased capacities and more complex feature sets

▪ ARRIS BCS, MCS, & ATS Teams are working closely with leading MSOs to define & design the CMTS & Video & Access Architectures of the future

March 2009 72Analyst / Investor Conference

ARRIS is Excited to be Developing the Technologies that MSOs Will Need in the Upcoming Decade...Questions

Broadband Communication Systems (BCS)Bruce McClellandPresidentARRIS Broadband Communication Systems (BCS)

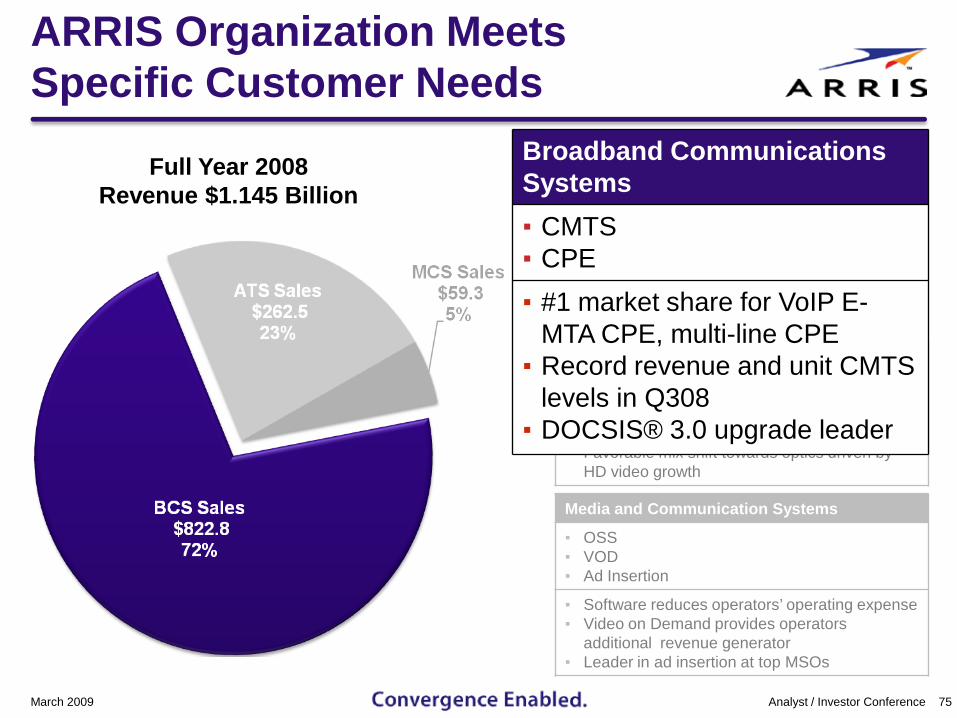

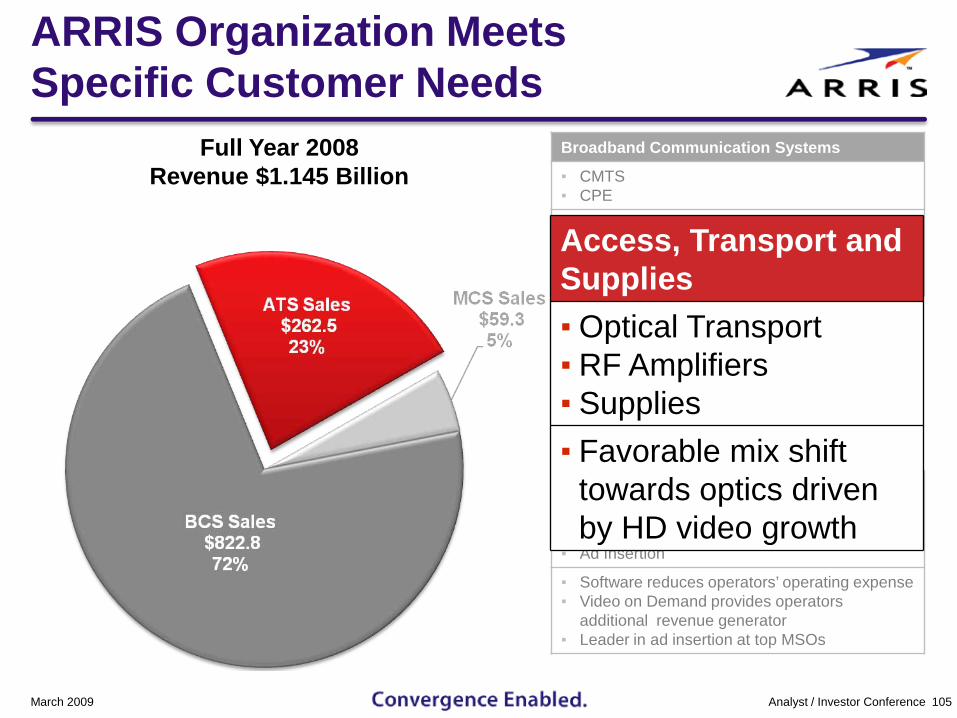

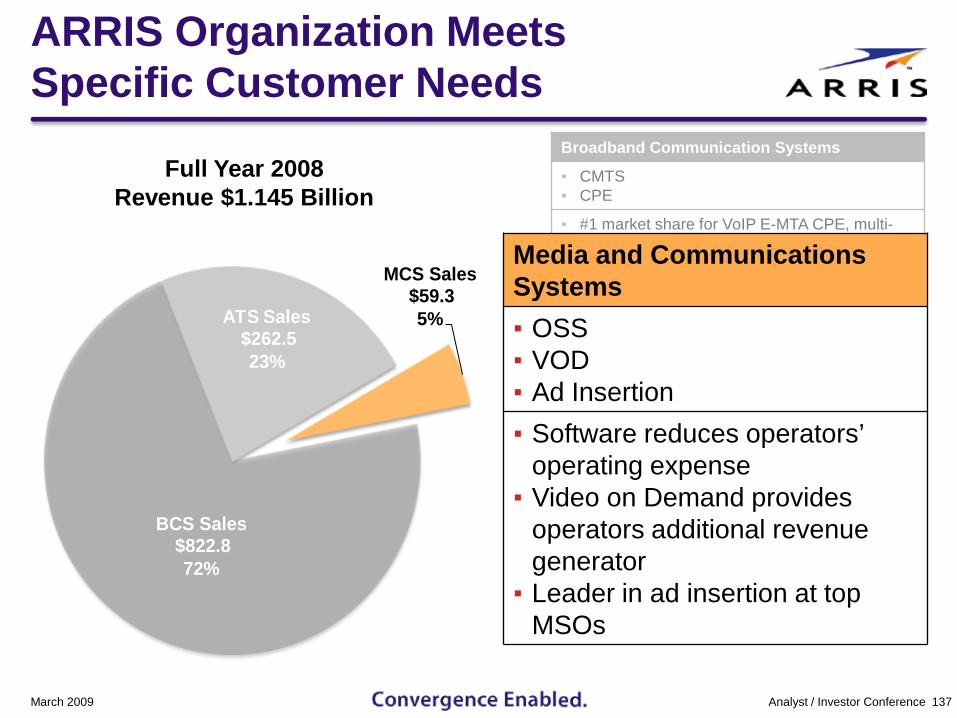

ARRIS Organization MeetsSpecific Customer Needs

March 2009 75Analyst / Investor Conference

Access, Transport and Supplies

▪ Optical▪ RF▪ Supplies

▪ Favorable mix shift towards optics driven by HD video growth

Media and Communication Systems

▪ OSS▪ VOD▪ Ad Insertion

▪ Software reduces operators’ operating expense▪ Video on Demand provides operators

additional revenue generator▪ Leader in ad insertion at top MSOs

Full Year 2008Revenue $1.145 Billion

Broadband Communications Systems▪ CMTS▪ CPE▪ #1 market share for VoIP E-

MTA CPE, multi-line CPE▪ Record revenue and unit CMTS

levels in Q308▪ DOCSIS® 3.0 upgrade leader

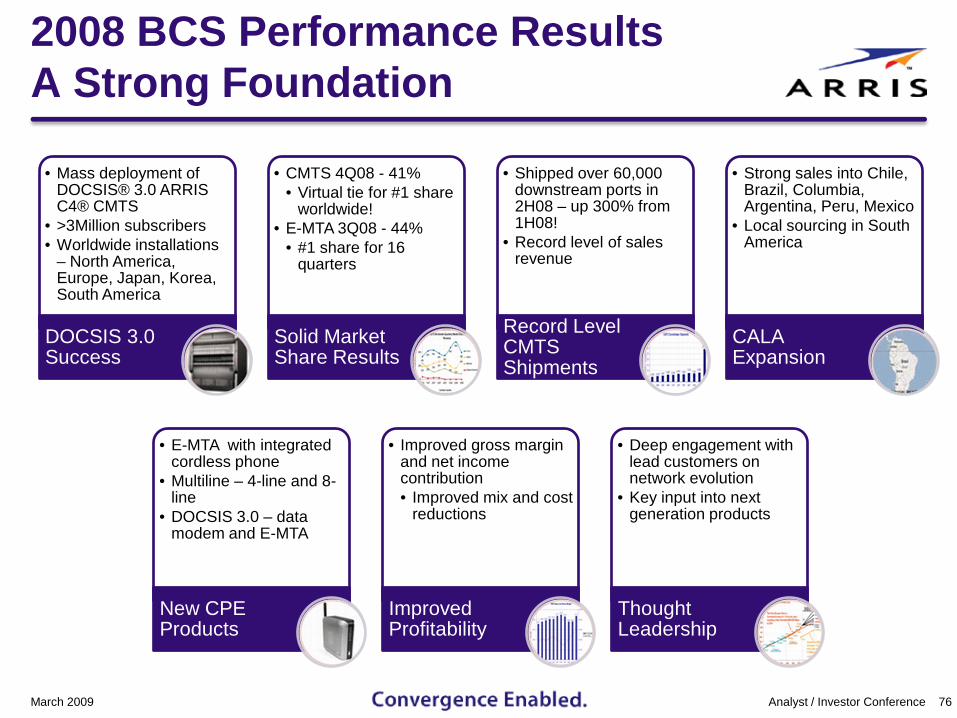

2008 BCS Performance ResultsA Strong Foundation

• Mass deployment of DOCSIS® 3.0 ARRIS C4® CMTS

• >3Million subscribers• Worldwide installations

– North America, Europe, Japan, Korea, South America

DOCSIS 3.0 Success

• CMTS 4Q08 - 41%• Virtual tie for #1 share

worldwide!• E-MTA 3Q08 - 44%

• #1 share for 16 quarters

Solid Market Share Results

• Shipped over 60,000 downstream ports in 2H08 – up 300% from 1H08!

• Record level of sales revenue

Record Level CMTS Shipments

• Strong sales into Chile, Brazil, Columbia, Argentina, Peru, Mexico

• Local sourcing in South America

CALA Expansion

• E-MTA with integrated cordless phone

• Multiline – 4-line and 8-line

• DOCSIS 3.0 – data modem and E-MTA

New CPE Products

• Improved gross margin and net income contribution• Improved mix and cost

reductions

Improved Profitability

• Deep engagement with lead customers on network evolution

• Key input into next generation products

Thought Leadership

76Analyst / Investor ConferenceMarch 2009

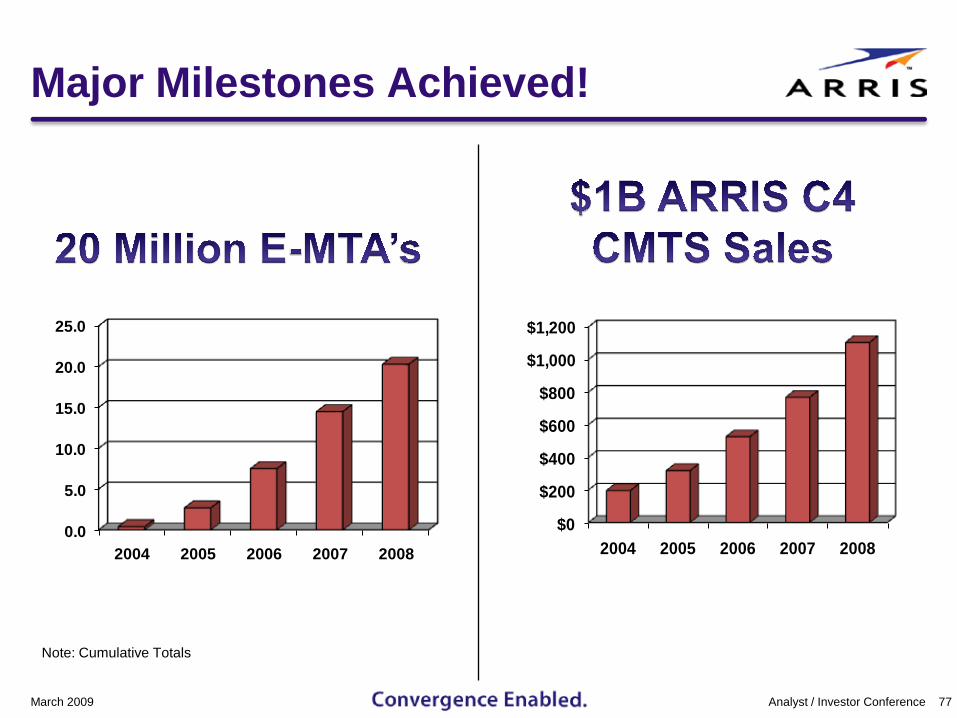

Major Milestones Achieved!

77Analyst / Investor Conference

Note: Cumulative Totals

March 2009

0.0

5.0

10.0

15.0

20.0

25.0

2004 2005 2006 2007 2008

$0

$200

$400

$600

$800

$1,000

$1,200

2004 2005 2006 2007 2008

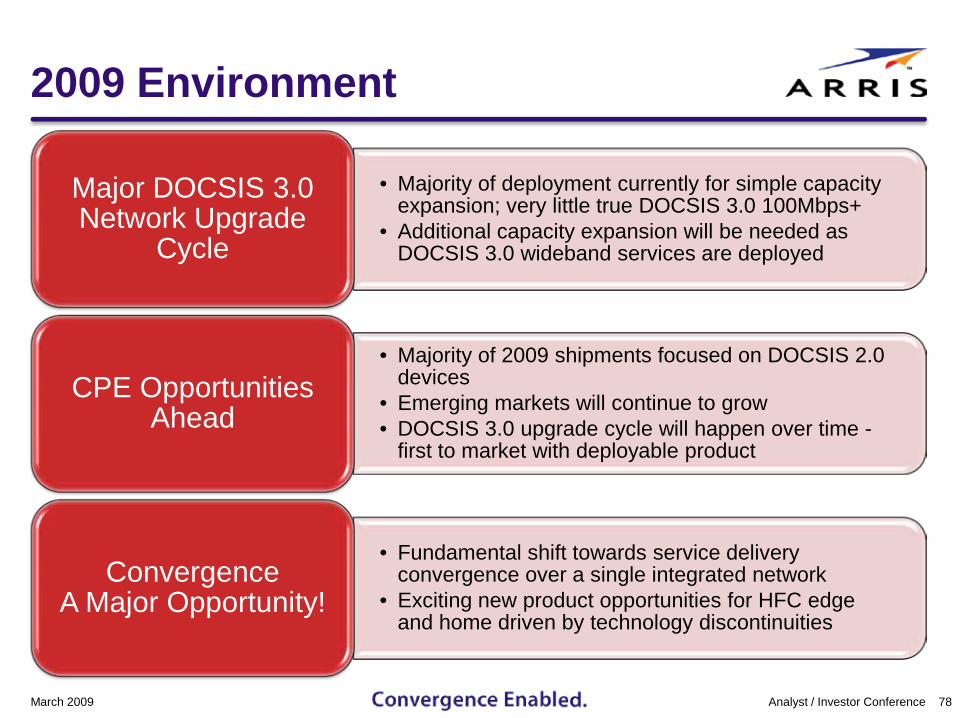

2009 Environment

• Majority of deployment currently for simple capacity expansion; very little true DOCSIS 3.0 100Mbps+

• Additional capacity expansion will be needed as DOCSIS 3.0 wideband services are deployed

Major DOCSIS 3.0 Network Upgrade

Cycle

• Majority of 2009 shipments focused on DOCSIS 2.0 devices

• Emerging markets will continue to grow• DOCSIS 3.0 upgrade cycle will happen over time -

first to market with deployable product

CPE Opportunities Ahead

• Fundamental shift towards service delivery convergence over a single integrated network

• Exciting new product opportunities for HFC edge and home driven by technology discontinuities

ConvergenceA Major Opportunity!

78Analyst / Investor ConferenceMarch 2009

BCS Growth OpportunitiesThree Year Horizon

79Analyst / Investor Conference

2009 – 2011 BCS Growth

OpportunitiesVOIP

Broadband Access

Digital Video IP Video

Home Networking

Small Business

Professional Services

March 2009

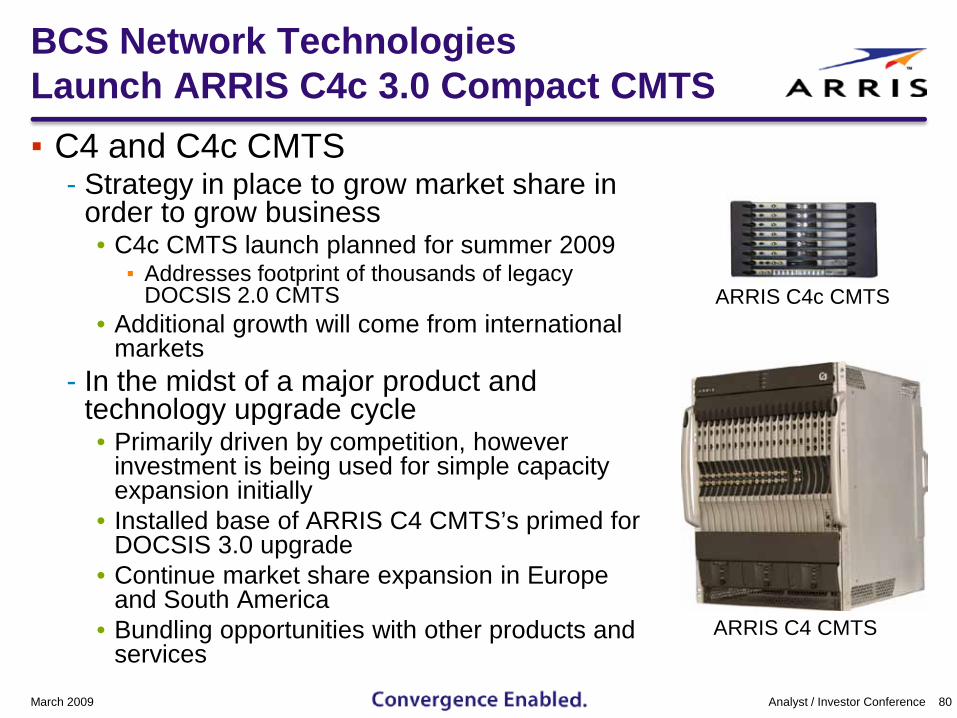

BCS Network TechnologiesLaunch ARRIS C4c 3.0 Compact CMTS▪ C4 and C4c CMTS

- Strategy in place to grow market share in order to grow business • C4c CMTS launch planned for summer 2009

▪ Addresses footprint of thousands of legacy DOCSIS 2.0 CMTS

• Additional growth will come from international markets

- In the midst of a major product and technology upgrade cycle• Primarily driven by competition, however

investment is being used for simple capacity expansion initially

• Installed base of ARRIS C4 CMTS’s primed for DOCSIS 3.0 upgrade

• Continue market share expansion in Europe and South America

• Bundling opportunities with other products and services

80Analyst / Investor Conference

ARRIS C4c CMTS

ARRIS C4 CMTS

March 2009

DTM602

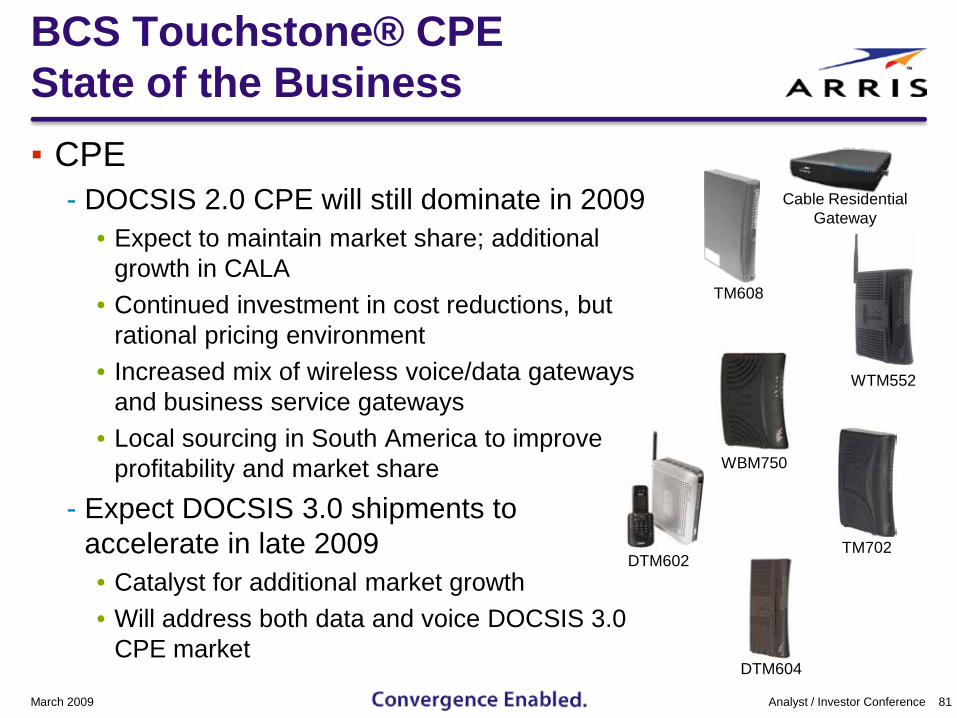

BCS Touchstone® CPEState of the Business▪ CPE

- DOCSIS 2.0 CPE will still dominate in 2009 • Expect to maintain market share; additional

growth in CALA• Continued investment in cost reductions, but

rational pricing environment• Increased mix of wireless voice/data gateways

and business service gateways • Local sourcing in South America to improve

profitability and market share- Expect DOCSIS 3.0 shipments to

accelerate in late 2009 • Catalyst for additional market growth• Will address both data and voice DOCSIS 3.0

CPE market

81Analyst / Investor ConferenceMarch 2009

WBM750

TM702

WTM552

TM608

DTM604

Cable Residential Gateway

All images are the property of their respective copyright owners.© Copyright 2008. Broadband Directions LLC. All rights reserved.

Video Will Drive Growth

82Analyst / Investor ConferenceMarch 2009

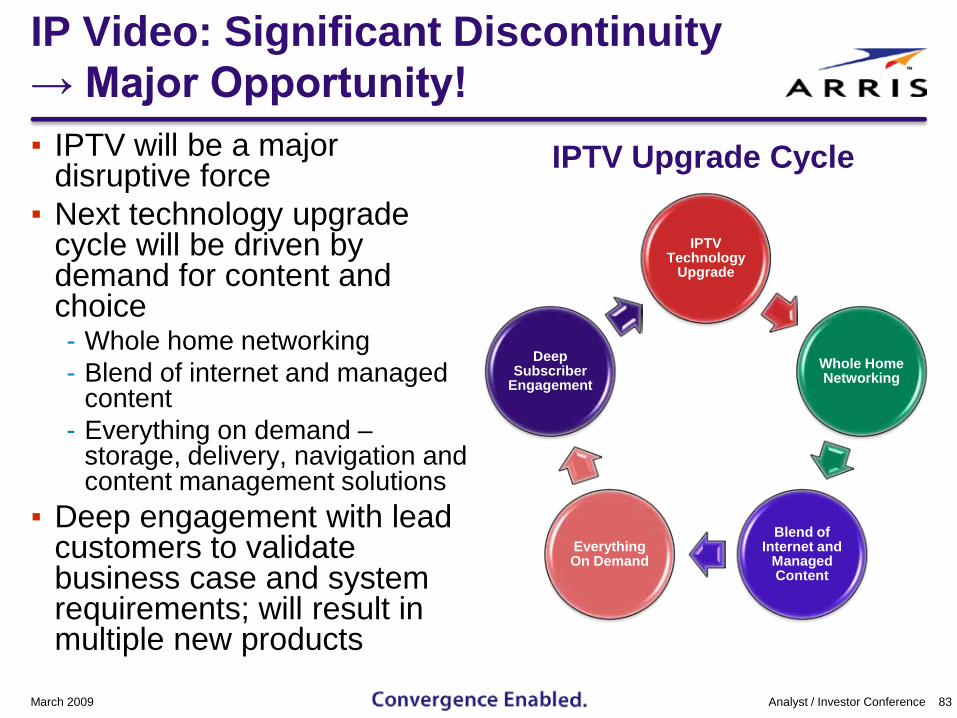

IP Video: Significant Discontinuity → Major Opportunity!▪ IPTV will be a major

disruptive force ▪ Next technology upgrade

cycle will be driven by demand for content and choice- Whole home networking- Blend of internet and managed

content- Everything on demand –

storage, delivery, navigation and content management solutions

▪ Deep engagement with lead customers to validate business case and system requirements; will result in multiple new products

IPTV Technology

Upgrade

Whole Home Networking

Blend of Internet and

Managed Content

Everything On Demand

Deep Subscriber

Engagement

83Analyst / Investor Conference

IPTV Upgrade Cycle

March 2009

Broadcast

Narrowcast

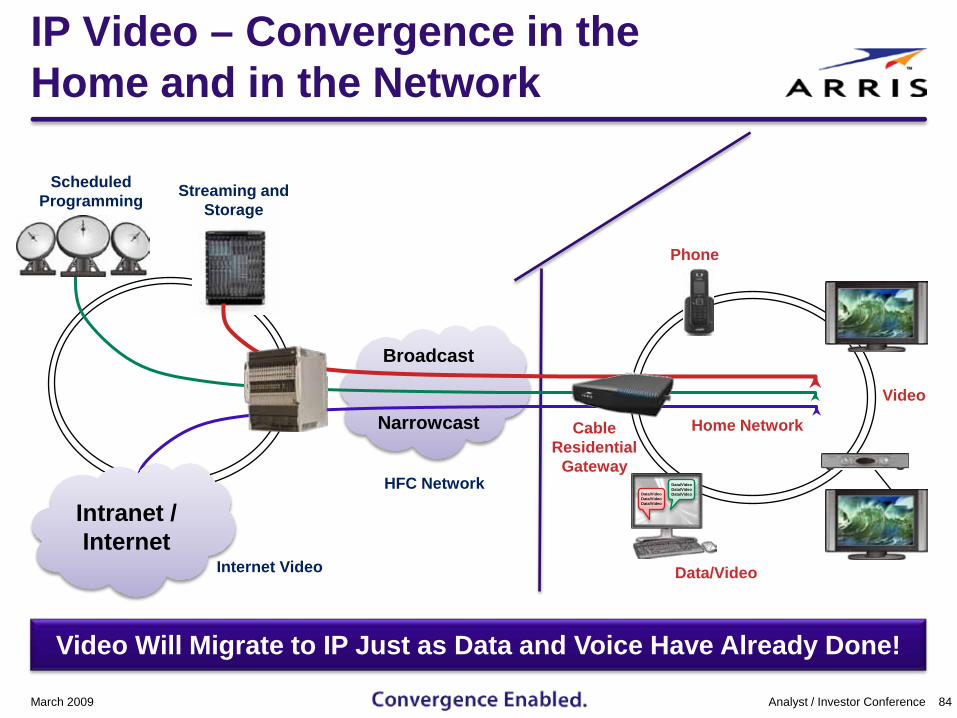

IP Video – Convergence in the Home and in the Network

84Analyst / Investor Conference

Scheduled Programming

Phone

Video

Data/VideoInternet Video

Cable Residential

Gateway

Home Network

HFC Network

Intranet / Internet

Video Will Migrate to IP Just as Data and Voice Have Already Done!

Data/VideoData/VideoData/VideoData/Video

Data/VideoData/Video

March 2009

Streaming and Storage

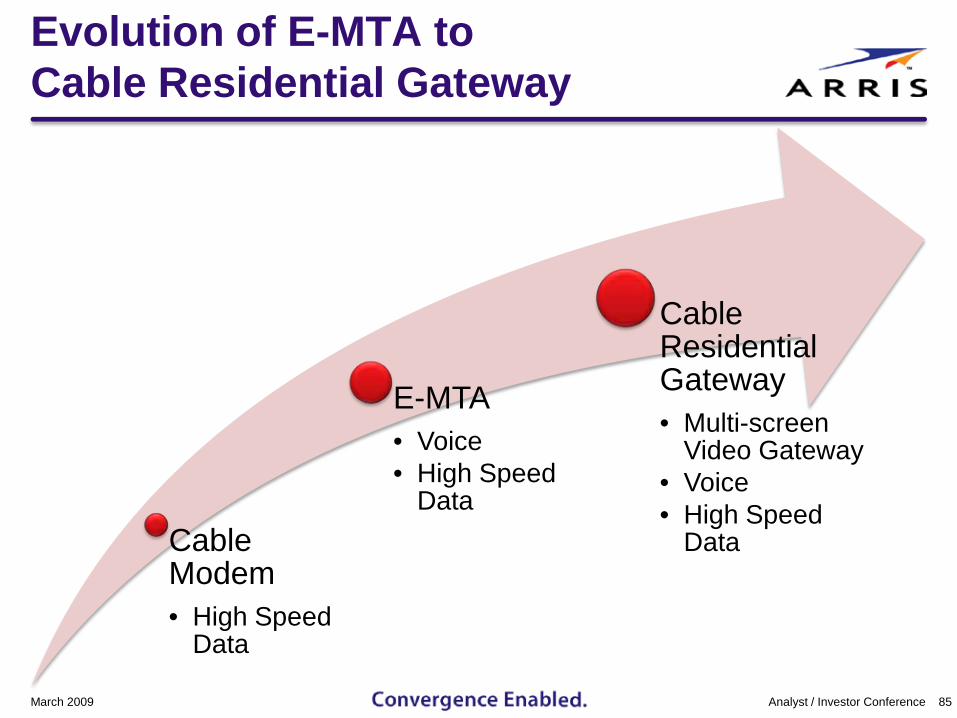

Evolution of E-MTA to Cable Residential Gateway

Cable Modem• High Speed

Data

E-MTA• Voice• High Speed

Data

CableResidential Gateway• Multi-screen

Video Gateway• Voice• High Speed

Data

85Analyst / Investor ConferenceMarch 2009

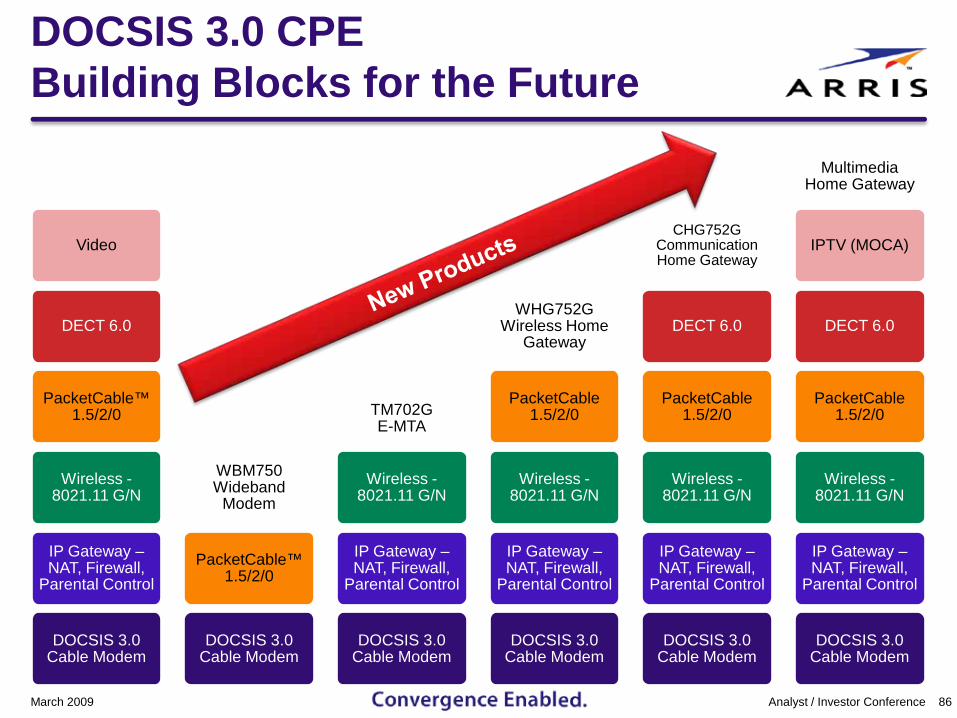

DOCSIS 3.0 CPEBuilding Blocks for the Future

Video

DECT 6.0

PacketCable™ 1.5/2/0

Wireless -8021.11 G/N

IP Gateway –NAT, Firewall,

Parental Control

DOCSIS 3.0 Cable Modem

WBM750 Wideband

Modem

PacketCable™ 1.5/2/0

DOCSIS 3.0 Cable Modem

TM702G E-MTA

Wireless -8021.11 G/N

IP Gateway –NAT, Firewall,

Parental Control

DOCSIS 3.0 Cable Modem

WHG752G Wireless Home

Gateway

PacketCable1.5/2/0

Wireless -8021.11 G/N

IP Gateway –NAT, Firewall,

Parental Control

DOCSIS 3.0 Cable Modem

CHG752G Communication Home Gateway

DECT 6.0

PacketCable1.5/2/0

Wireless -8021.11 G/N

IP Gateway –NAT, Firewall,

Parental Control

DOCSIS 3.0 Cable Modem

Multimedia Home Gateway

IPTV (MOCA)

DECT 6.0

PacketCable1.5/2/0

Wireless -8021.11 G/N

IP Gateway –NAT, Firewall,

Parental Control

DOCSIS 3.0 Cable Modem

Analyst / Investor Conference 86March 2009

BCS 2009-2011 Outlook Summary▪ Proven team capable of delivering results, even in a

difficult operating environment- Established market leader in competitive CMTS and VoIP

CPE markets- Focused on controlling OPEX and maintaining profitability

▪ Will build on past success- Must maintain closeness with each customer- Customer support is key- Strong outlook – must continue to execute

▪ IPTV/Video will drive major discontinuity and opportunity for significant growth

87Analyst / Investor ConferenceMarch 2009

Questions

Technology and Trends in Access & Transport Networks

Ken WrightCTO

Optical Metro

Transport

ARRIS WorkAssure™ Work Force Management• Customer Satisfaction• Dispatch Control• Expense Reduction• Workforce Potential

Regal®Taps

MONARCH®Splitters and

Supplies

ARRIS CHP Max5000™Headend Optics

ARRIS ServAssure™ HFC Network Surveillance and Maintenance• Network Visibility• Network Management• New Service Deployment• Improved Service

ARRIS D5™ Universal Edge

QAM

ARRIS C4® CMTS

ARRIS Flex Max®Amplifiers

ARRIS Opti Max® Nodes

Touchstone® E-MTA

PacketCable™ and SIP

ARRIS CORWave™

Optical Transmitters

ARRIS Products Address Virtually All of Our Customer’s Needs

March 2009 90Analyst / Investor Conference

ARRIS C3™ CMTS

Transceiver / AntennaARRIS WiDOX Telephony Modem

Video, Telephony and

HSD Operations

ARRIS C4c CMTS

ARRIS ConvergeMedia™ SuiteVOD, Advertising Delivery and

Management Platform

Regal®Taps

MONARCH®Splitters and

Supplies

ARRIS CHP Max5000™Headend Optics

ARRIS Flex Max®Amplifiers

ARRIS Opti Max® Nodes

ARRIS CORWave™

Optical Transmitters

ARRIS Products Address Virtually All of Our Customer’s Needs

March 2009 91Analyst / Investor Conference

Access Network Must Support Growth

March 2009 92Analyst / Investor Conference

Max Permitted Bandwidth for Modems (bps)

1982 1986 1990 1994 19981

10

100

1k

2002 2006

10k

100k

1M

10M

100M

1G

2010 Year2014

10G

100G

2016

The Era ofWideband

Cable Modems ???

12 Mbps

The past 25-years show aconstant increase of ~1.5x every year...resulting in max offered BW=288 Mbpsin 2016

~288 Mbps

128 kbps

256 kbps 512 kbps

1 Mbps 5 Mbps

The Era ofCable Modems2.4 kbps

300 bps

56 kbps

1.2 kbps9.6 kbps 14.4 kbps

28 kbps33 kbps

The Era ofDial-Up Modems

50 Mbps(4x Increase)

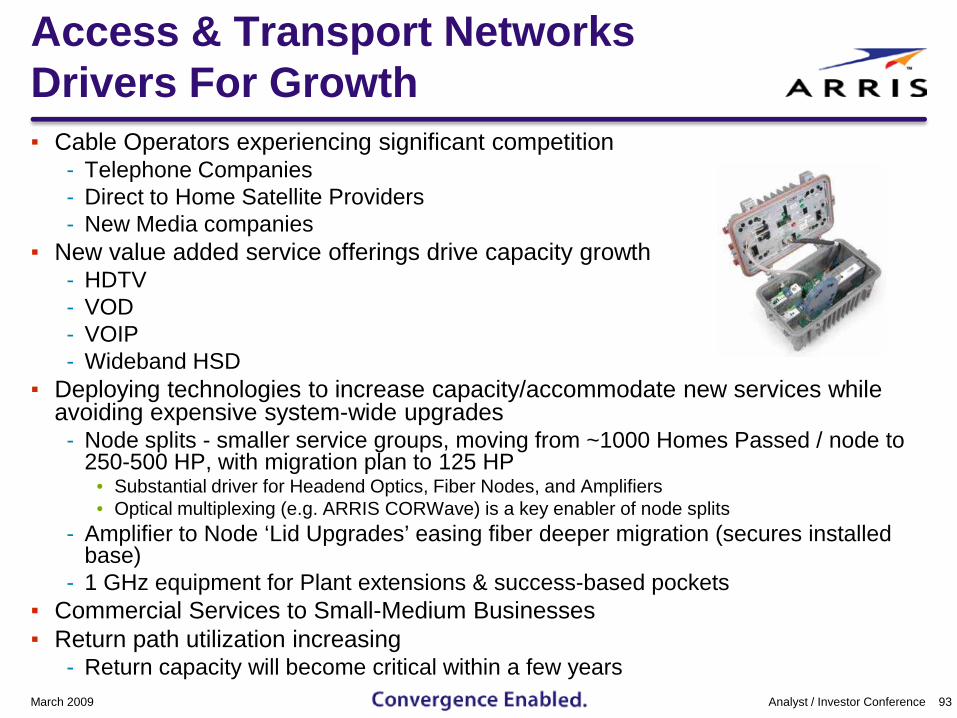

Access & Transport NetworksDrivers For Growth▪ Cable Operators experiencing significant competition

- Telephone Companies- Direct to Home Satellite Providers- New Media companies

▪ New value added service offerings drive capacity growth- HDTV - VOD- VOIP- Wideband HSD

▪ Deploying technologies to increase capacity/accommodate new services while avoiding expensive system-wide upgrades- Node splits - smaller service groups, moving from ~1000 Homes Passed / node to

250-500 HP, with migration plan to 125 HP• Substantial driver for Headend Optics, Fiber Nodes, and Amplifiers• Optical multiplexing (e.g. ARRIS CORWave) is a key enabler of node splits

- Amplifier to Node ‘Lid Upgrades’ easing fiber deeper migration (secures installed base)

- 1 GHz equipment for Plant extensions & success-based pockets▪ Commercial Services to Small-Medium Businesses▪ Return path utilization increasing

- Return capacity will become critical within a few yearsMarch 2009 93Analyst / Investor Conference

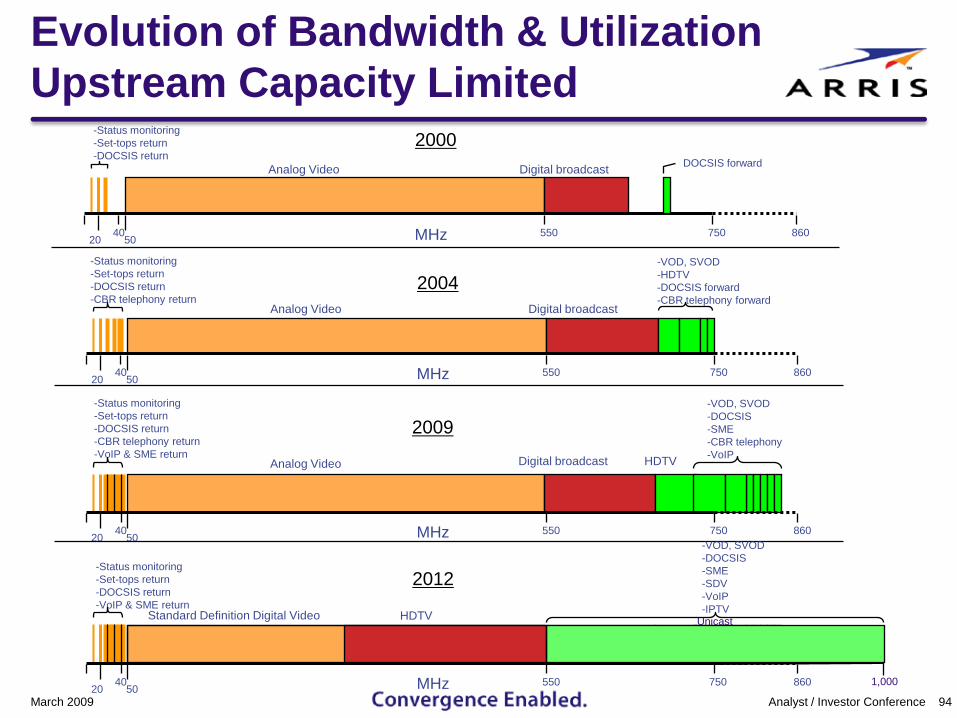

Evolution of Bandwidth & UtilizationUpstream Capacity Limited

March 2009 94Analyst / Investor Conference

-Status monitoring-Set-tops return-DOCSIS return

Analog Video Digital broadcast

2040

50550 750 860MHz

DOCSIS forward

2000

-Status monitoring-Set-tops return-DOCSIS return-CBR telephony return

Analog Video Digital broadcast

-VOD, SVOD-HDTV-DOCSIS forward-CBR telephony forward

2040

50550 750 860MHz

2004

2009-VOD, SVOD-DOCSIS-SME-CBR telephony-VoIP

-Status monitoring-Set-tops return-DOCSIS return-CBR telephony return-VoIP & SME return

Analog Video Digital broadcast HDTV

2040

50550 750 860MHz

2012

-VOD, SVOD-DOCSIS-SME-SDV-VoIP-IPTV

-Status monitoring-Set-tops return-DOCSIS return-VoIP & SME return

Standard Definition Digital Video HDTV

2040

50550 750 860

Unicast

MHz 1,000

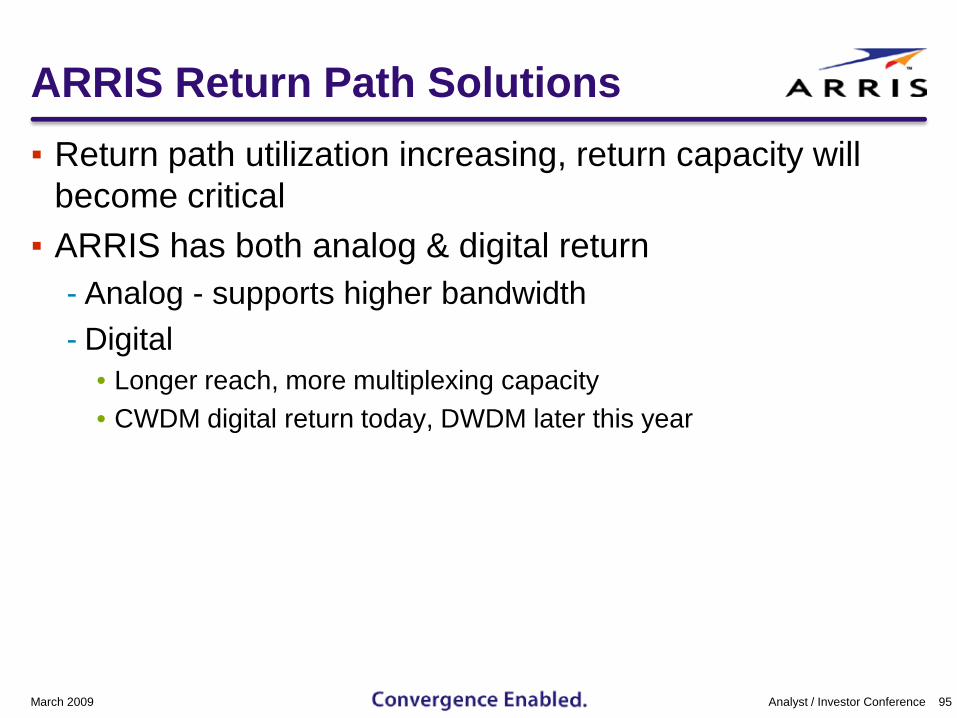

ARRIS Return Path Solutions▪ Return path utilization increasing, return capacity will

become critical▪ ARRIS has both analog & digital return

- Analog - supports higher bandwidth- Digital

• Longer reach, more multiplexing capacity • CWDM digital return today, DWDM later this year

March 2009 95Analyst / Investor Conference

Limitations of Overlay Architectures

March 2009 96Analyst / Investor Conference

Hub500

Homes

Headend

Home Run

Hub1200

Homes

Headend CAPA

CITY

MG

MTBroadcast l

Narrowcast lsReturn ls

OTNSecondary Ring

Overlay

▪ Broadcast & Narrowcast signals carried separately, combined at OTN or Node▪ Node segmentation limited by fiber count in secondary ring▪ Growth of narrowcast services (VOD, DOCSIS 3.0, SDV) requires increased fiber

capacity

CORWave II Solves Issues in Overlay Architecture▪ Substantial portion of existing fiber links are in Overlay

Architecture

▪ ARRIS CORWave II Benefits- For the 1st time, enables multiple full bandwidth, analog

forward signals on a single fiber- Solves the limitation on Narrowcast in QAM Overlay

architecture- Provides extended reach of QAM Overlay, with lower cost

and complexity- Enables up to 16 full bandwidth analog forward signals on

a single fiber, with distances up to 65Km

March 2009 97Analyst / Investor Conference

EvolutionFiber to the Home▪ MSOs want migration path to Fiber To The Home, without

stranding existing investment▪ RFoG (RF over Glass)

- Uses existing HFC infrastructure (CMTS, QAMs, optics, etc.) for easy as-needed migration

- Moves optical-RF conversion to premises- DOCSIS-friendly Passive Optical Network

▪ PON- Longer term evolutionary step- Can share fiber infrastructure with HFC/RFoG- Can overlay as needed

▪ Product migration to RFoG & PON offerings- Much of architecture uses current products- Complimentary products in development

March 2009 98Analyst / Investor Conference

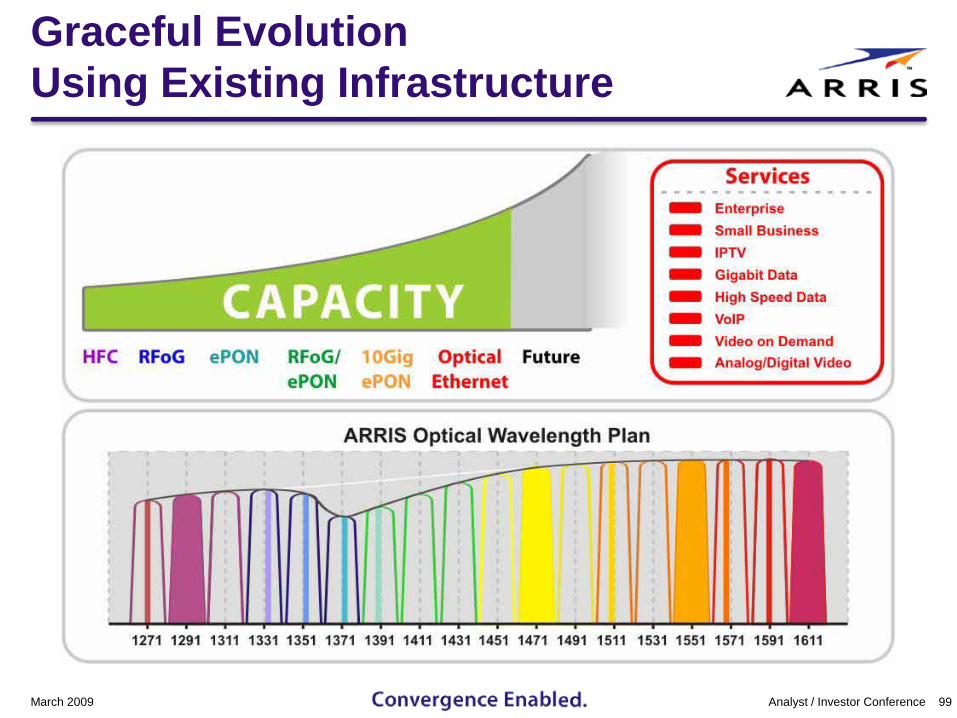

Graceful EvolutionUsing Existing Infrastructure

March 2009 99Analyst / Investor Conference

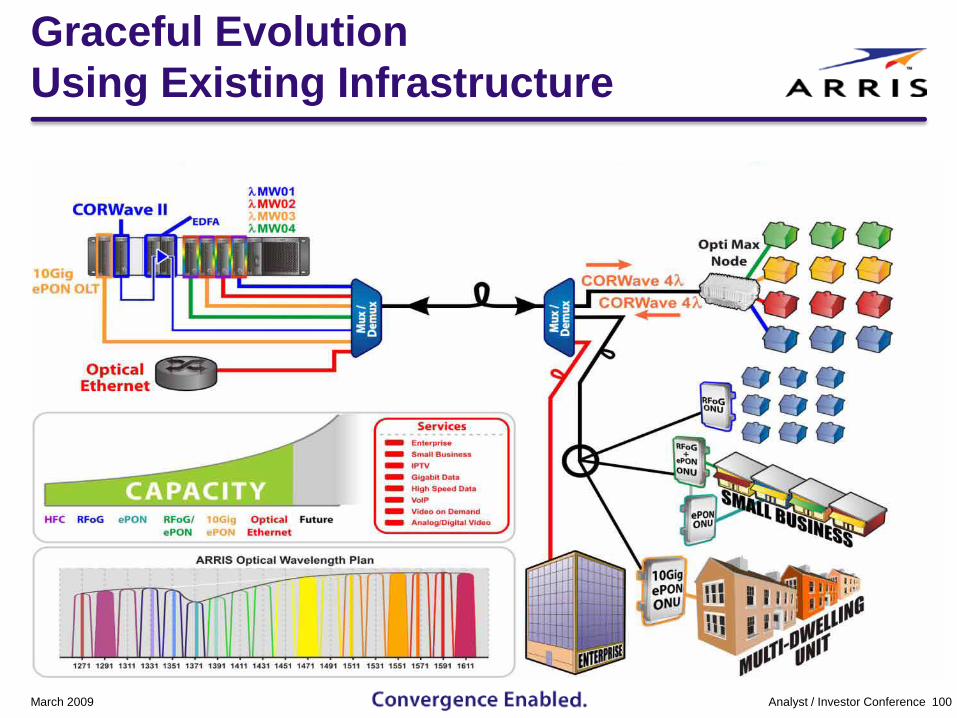

Graceful EvolutionUsing Existing Infrastructure

March 2009 100Analyst / Investor Conference

Key Take-awaysAccess & Transport▪ Engaged in innovative solutions enabling more capacity

from existing infrastructure▪ Cost-effective evolution to all fiber networks of the future▪ Key building blocks in place to enable MSO network

migration

March 2009 101Analyst / Investor Conference

Questions?

March 2009 103Analyst / Investor Conference

Access, Transport & SuppliesJohn CaezzaPresident

ARRIS Organization MeetsSpecific Customer Needs

March 2009 105Analyst / Investor Conference

Broadband Communication Systems

▪ CMTS▪ CPE

▪ #1 market share for VoIP E-MTA CPE, multi-line CPE

▪ Record revenue and unit CMTS levels in Q308▪ DOCSIS® 3.0 upgrade leader

▪ Media and Communication Systems

▪ OSS▪ VOD▪ Ad Insertion

▪ Software reduces operators’ operating expense▪ Video on Demand provides operators

additional revenue generator▪ Leader in ad insertion at top MSOs

Full Year 2008Revenue $1.145 Billion

Access, Transport and Supplies▪ Optical Transport▪ RF Amplifiers▪ Supplies▪ Favorable mix shift

towards optics driven by HD video growth

Access, Transport & Supplies Mission▪ Premiere provider of robust, innovative, high value and

cost effective infrastructure solutions to the Multi System Operators that meet their technology and service needs today and in the future- Optical Transport

• HFC• Passive Networks

- RF Amplifiers- Customer Premise Infrastructure

March 2009 106Analyst / Investor Conference

Current ATS Business Environment▪ 2008 ATS revenues down from 2007▪ Macro Economic conditions impacted the business

- Major rebuild/upgrade/plant extension projects• Slowing in North America• Growing internationally

- Decline in housing starts- Constrained customer CAPEX

March 2009 107Analyst / Investor Conference

Despite Macro Economic ConditionsWe Remain Optimistic

Reasons for Optimism▪ Billions of installed base will need

upgrades and enhancements to support growing capacity demands- Bandwidth upgrades- Amplifiers upgrade to nodes- Transmitter replacements

▪ Investment in technology and supply chain will help command superior market position- Advanced optical transport- CORWave™ multi-wavelength optics- Commercial services expanding- Fulfillment solutions expanding

March 2009 108Analyst / Investor Conference

Keys to serving our customers • Focused

technology innovations

• Superior fulfillment solutions

• Agile supply chain

2008 Business Performance▪ Market Share has remained stable▪ Q4’08 Gross Margins increased quarter over quarter

- Gains were primarily driven by the strength of the Optics Platforms and the realization of Supply Chain savings

▪ Reduced gross inventories significantly▪ Recently announced CORWave product is into

deployments with top domestic and international MSO’s▪ Three of the top five US MSO’s selected ARRIS

Supplies as primary supplier for key infrastructure builds▪ Fulfillment program with top MSO’s continues to expand

with good results

March 2009 109Analyst / Investor Conference

A Few of the ATS Initiatives▪ Expansion of Optical platforms from traditional

residential HFC applications to support new markets- Commercial services- RF over Glass- GePON and 10GePON

▪ Extended reach transmitters- Complement RFoG and PON needs

▪ Interfaces for RFoG and GePON- Headend (OLT)- Subscriber (ONU)

March 2009 110Analyst / Investor Conference

CHP Max5000 Platform

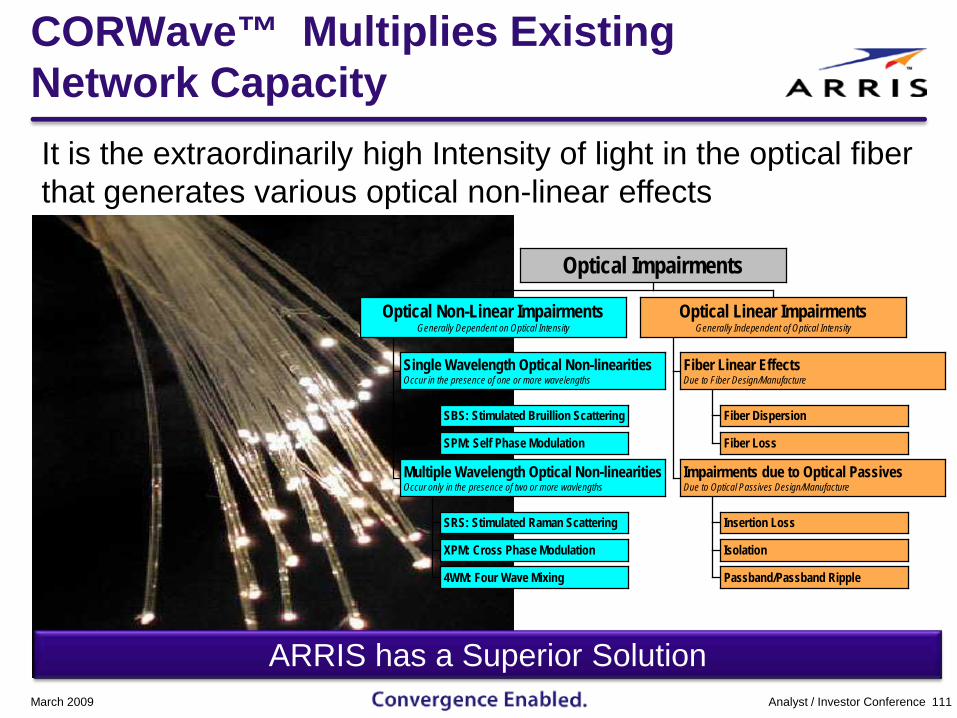

CORWave™ Multiplies Existing Network Capacity

March 2009 111Analyst / Investor Conference

It is the extraordinarily high Intensity of light in the optical fiber that generates various optical non-linear effects

SBS: Stimulated Bruillion Scattering

SPM: Self Phase Modulation

Single Wavelength Optical Non-linearitiesOccur in the presence of one or more wavelengths

SRS: Stimulated Raman Scattering

XPM: Cross Phase Modulation

4WM: Four Wave Mixing

Multiple Wavelength Optical Non-linearitiesOccur only in the presence of two or more wavlengths

Optical Non-Linear ImpairmentsGenerally Dependent on Optical Intensity

Fiber Dispersion

Fiber Loss

Fiber Linear EffectsDue to Fiber Design/Manufacture

Insertion Loss

Isolation

Passband/Passband Ripple

Impairments due to Optical PassivesDue to Optical Passives Design/Manufacture

Optical Linear ImpairmentsGenerally Independent of Optical Intensity

Optical Impairments

ARRIS has a Superior Solution

The CORWave™ Optical Platform…▪ Enables today’s advanced optical transport▪ Optimizes capacity of existing infrastructures▪ Gracefully supports revenue driven expansion▪ Readily supports Commercial service delivery▪ Provides future flexibility and service capabilities

March 2009 112Analyst / Investor Conference

Based on proven Head End optics (CHP) and Optical Node (OptiMax) technologies.

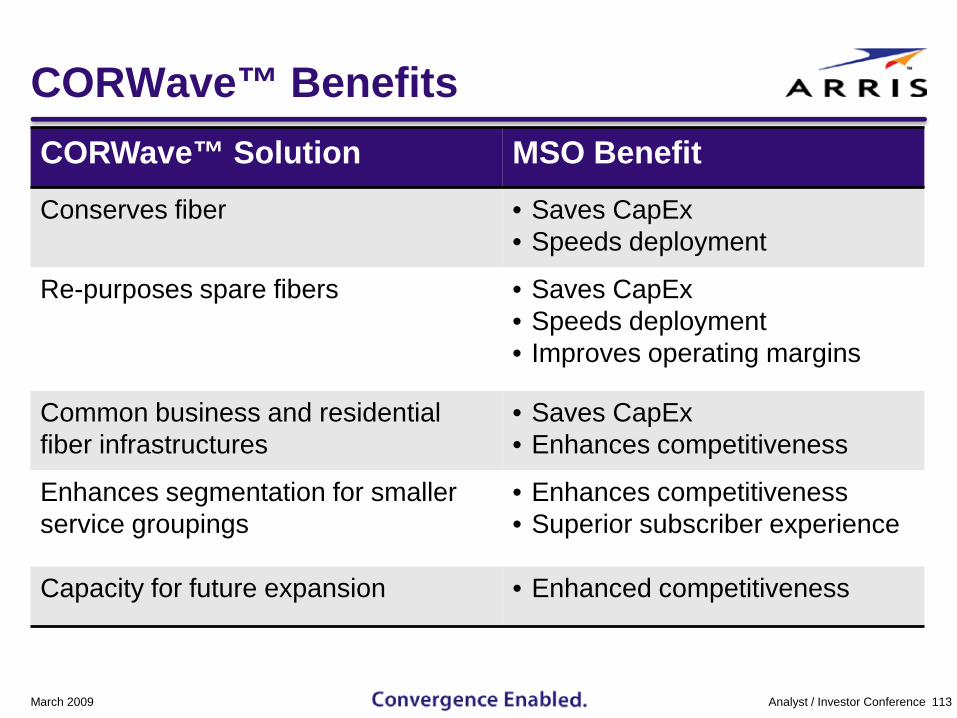

CORWave™ BenefitsCORWave™ Solution MSO BenefitConserves fiber • Saves CapEx

• Speeds deployment

Re-purposes spare fibers • Saves CapEx• Speeds deployment• Improves operating margins

Common business and residential fiber infrastructures

• Saves CapEx• Enhances competitiveness

Enhances segmentation for smaller service groupings

• Enhances competitiveness• Superior subscriber experience

Capacity for future expansion • Enhanced competitiveness

March 2009 113Analyst / Investor Conference

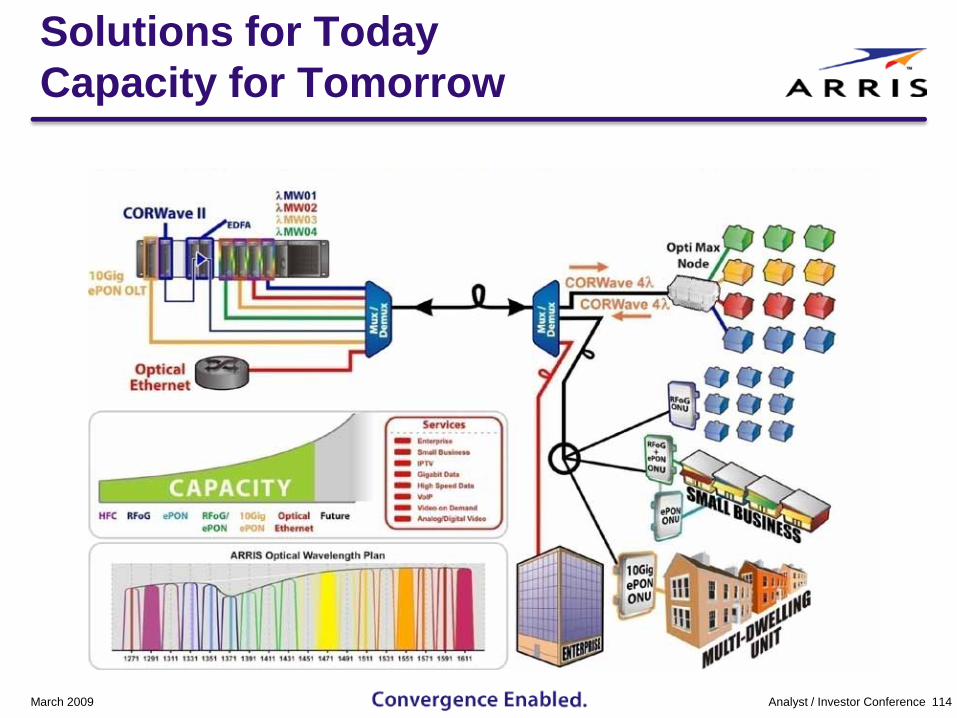

March 2009 114Analyst / Investor Conference

Solutions for TodayCapacity for Tomorrow

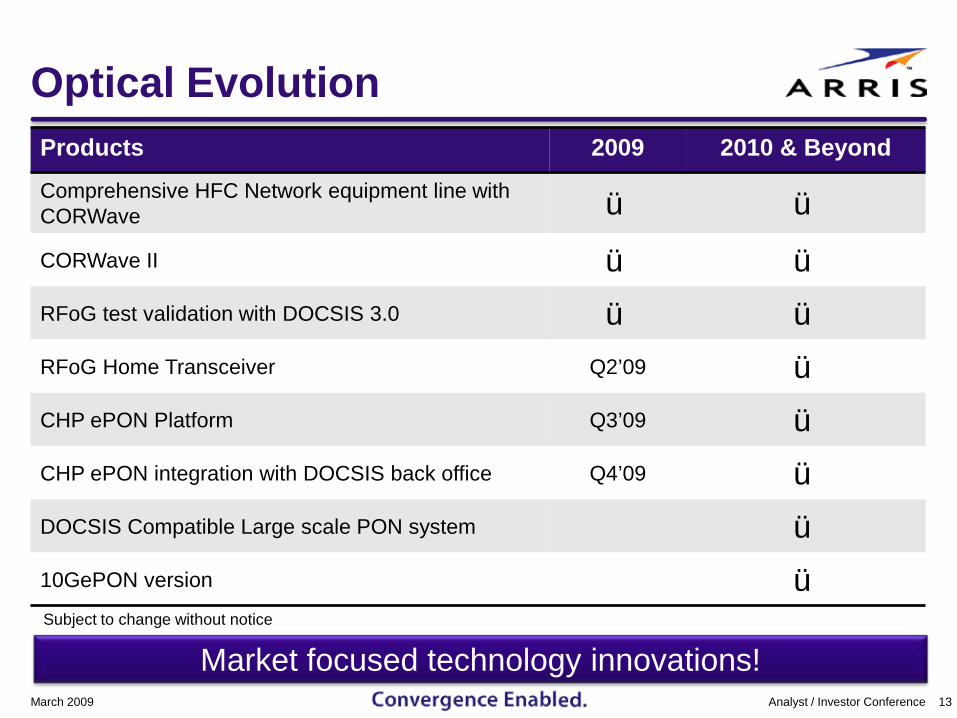

Optical EvolutionProducts 2009 2010 & Beyond

Comprehensive HFC Network equipment line with CORWave ü ü

CORWave II ü ü

RFoG test validation with DOCSIS 3.0 ü ü

RFoG Home Transceiver Q2’09 ü

CHP ePON Platform Q3’09 ü

CHP ePON integration with DOCSIS back office Q4’09 ü

DOCSIS Compatible Large scale PON system ü

10GePON version ü

March 2009 13Analyst / Investor Conference

Market focused technology innovations!Subject to change without notice

ATS Well Positioned for Success▪ Solutions positioned to enable MSOs use of existing

infrastructures and position for future growth; will mine billions of installed base of ATS products

▪ Internal business unit controls well implemented and managed; intense focus on technology, supply chain and sales execution

▪ Strong customer interest in optics platforms and fulfillment solutions; initial CORWave trials resulting in renewed optics traction

March 2009 116Analyst / Investor Conference

Positioned to Capture the Next Wave of Spending

Questions?

March 2009 117Analyst / Investor Conference

Technology and Trends in On Demand & Service Assurance

Ken WrightCTO

Topics of Discussion

▪ On Demand

▪ OSS/Service Assurance

March 2009 119Analyst / Investor Conference

On DemandDrivers For Growth▪ Consumers increasingly dissatisfied with linear

scheduled content, turning to- PVR – Local and Network- Video over the Internet- Startover- Mobile Video

▪ Interactive Advertising on the rise- Advertisers have been shifting $ to online ads- Profile driven targeted ads- Ads On Demand & Ad supported VOD- Feedback to advertisers

March 2009 120Analyst / Investor Conference

All images are the property of their respective copyright owners.© Copyright 2008. Broadband Directions LLC. All rights reserved.

On DemandDrivers For Growth

121Analyst / Investor ConferenceMarch 2009

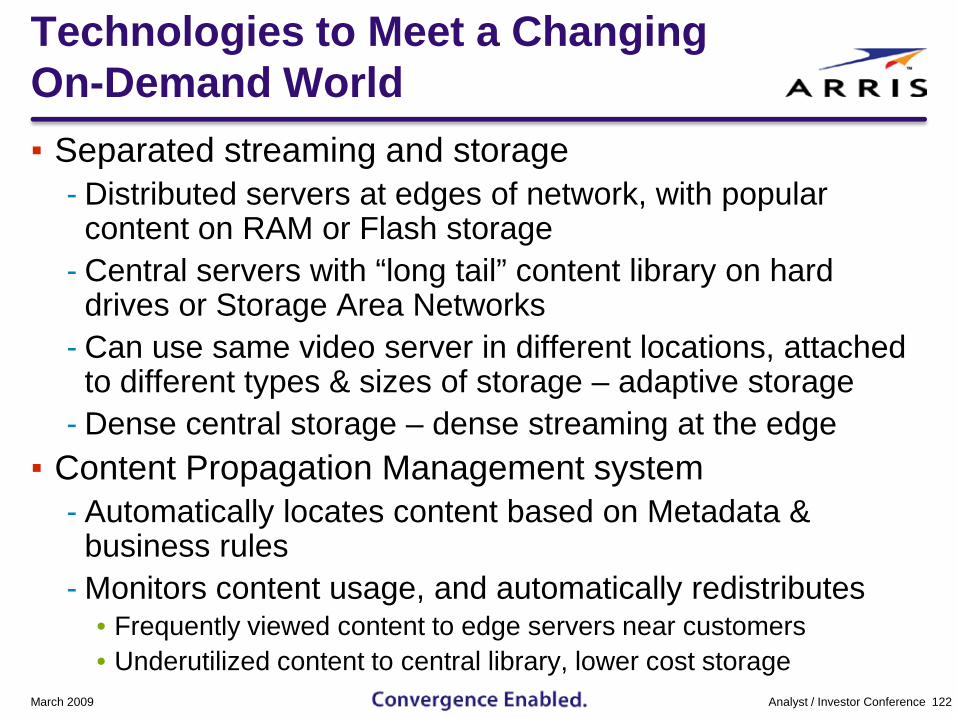

Technologies to Meet a Changing On-Demand World▪ Separated streaming and storage

- Distributed servers at edges of network, with popular content on RAM or Flash storage

- Central servers with “long tail” content library on hard drives or Storage Area Networks

- Can use same video server in different locations, attached to different types & sizes of storage – adaptive storage

- Dense central storage – dense streaming at the edge▪ Content Propagation Management system

- Automatically locates content based on Metadata & business rules

- Monitors content usage, and automatically redistributes• Frequently viewed content to edge servers near customers• Underutilized content to central library, lower cost storage

March 2009 122Analyst / Investor Conference

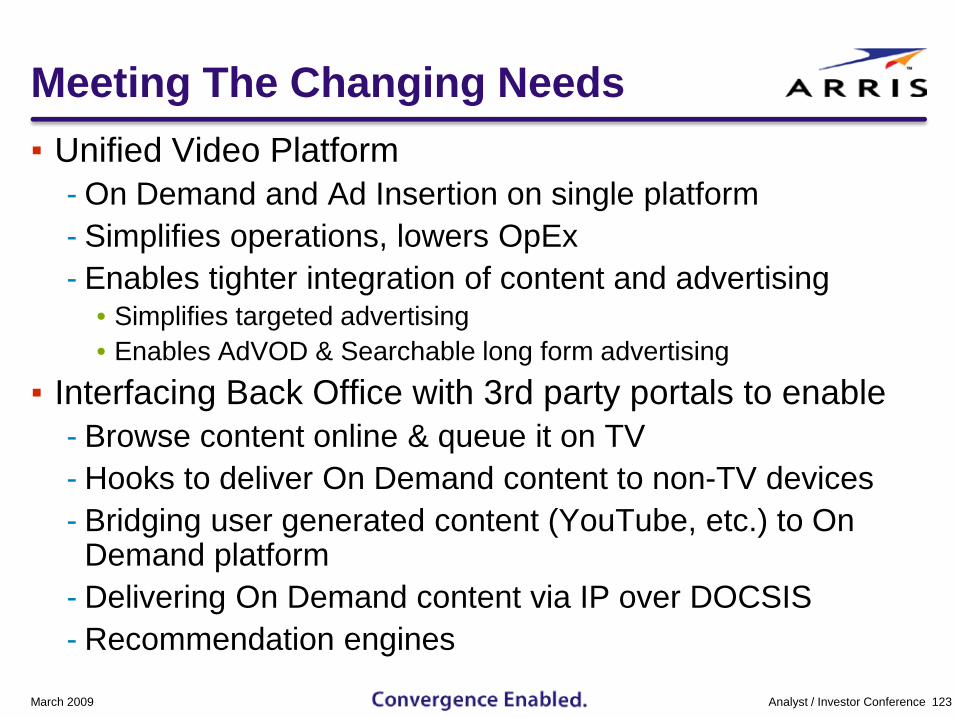

Meeting The Changing Needs▪ Unified Video Platform

- On Demand and Ad Insertion on single platform- Simplifies operations, lowers OpEx- Enables tighter integration of content and advertising

• Simplifies targeted advertising• Enables AdVOD & Searchable long form advertising

▪ Interfacing Back Office with 3rd party portals to enable- Browse content online & queue it on TV- Hooks to deliver On Demand content to non-TV devices- Bridging user generated content (YouTube, etc.) to On

Demand platform- Delivering On Demand content via IP over DOCSIS- Recommendation engines

March 2009 123Analyst / Investor Conference

Topics of Discussion▪ On Demand

▪ OSS/Service Assurance

March 2009 124Analyst / Investor Conference

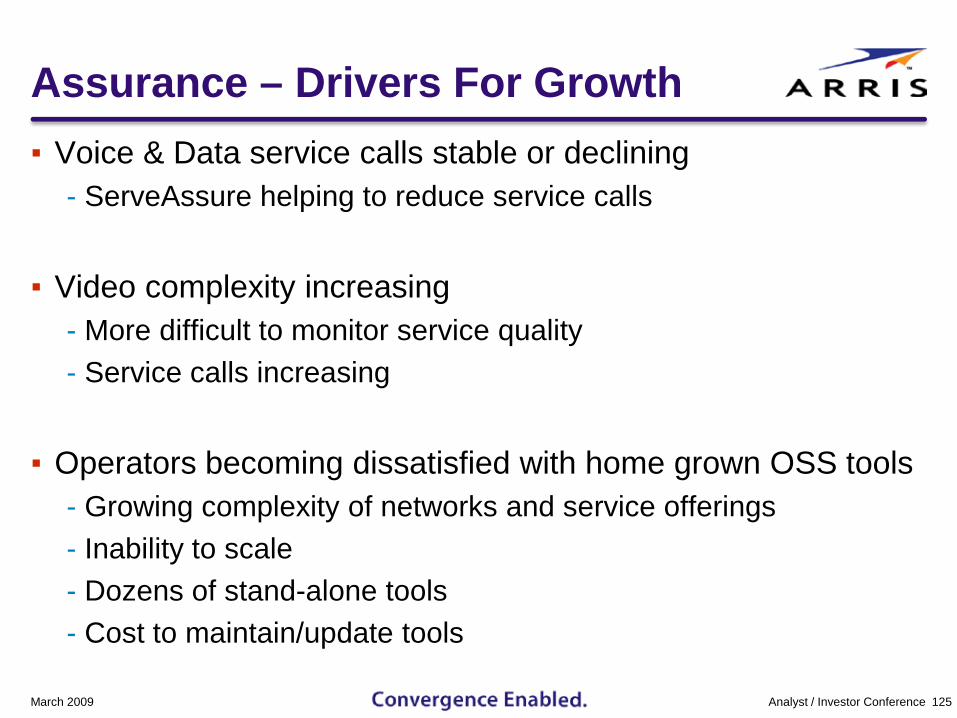

Assurance – Drivers For Growth▪ Voice & Data service calls stable or declining

- ServeAssure helping to reduce service calls

▪ Video complexity increasing- More difficult to monitor service quality- Service calls increasing

▪ Operators becoming dissatisfied with home grown OSS tools- Growing complexity of networks and service offerings- Inability to scale- Dozens of stand-alone tools- Cost to maintain/update tools

March 2009 125Analyst / Investor Conference

Assurance – Drivers For Growth▪ Increasing momentum to add intelligence/automation

- Continual drive to reduce OPEX through more efficient operations

- Competition – Cable, Telcos and Satellite all are about bandwidth and delivering content. Differentiator is Quality of Experience

- Several MSOs:• “2009 is the year of Operational Excellence”• Service quality = customer satisfaction = reduced churn

March 2009 126Analyst / Investor Conference

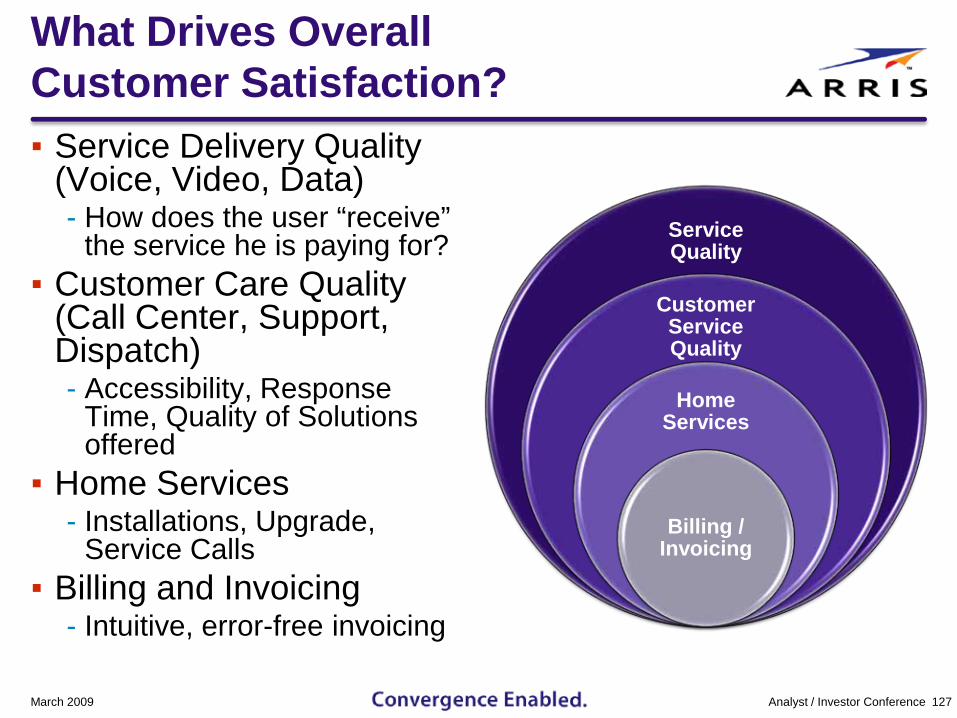

What Drives OverallCustomer Satisfaction?▪ Service Delivery Quality

(Voice, Video, Data)- How does the user “receive”

the service he is paying for?▪ Customer Care Quality

(Call Center, Support, Dispatch)- Accessibility, Response

Time, Quality of Solutions offered

▪ Home Services- Installations, Upgrade,

Service Calls▪ Billing and Invoicing

- Intuitive, error-free invoicing

Service Quality

Customer Service Quality

Home Services

Billing / Invoicing

March 2009 127Analyst / Investor Conference

What are MSO’s Looking for inAssurance Tools?▪ Automation to increase technician productivity▪ Proactive monitoring of service quality, allowing

detection and correction of plant issues before customers see degradation

▪ Substantially reduced Mean Time To Repair of network issues

▪ Awareness of slowed data traffic due to congestion, and ability to manage traffic to restore speeds

▪ Monitoring of network powering, to avoid key cause of service outages

March 2009 128Analyst / Investor Conference

ARRIS Assurance Delivers All These and More…

Service AssuranceExample of an integrated solution▪ ARRIS has offered industry leading data & voice

diagnostics for years

▪ Recent changes in CableLabs specs (Tru2Way) give set-top hooks for more video diagnostics, but 1-2 years out

▪ In advance of Tru2way, ARRIS current assurance tools• Have done basic video diagnostics for years• Extended video diagnostics in lab trials now, field deployable mid-

year

March 2009 129Analyst / Investor Conference

ServAssure Collects, Analyzes and Shares Network Health Information Throughout the Company

March 2009 130Analyst / Investor ConferenceCustomer CSR/TSR NOC

Set Top Monitoring

Dispatch

Services Dependencies & Root Cause

Technician

Business Rule, Events, CASA

Billing /EMS Data

HFC Plant Equipment

Line Extender

Amplifier

Service-specific Infrastructure

Soft Switch

Switch

CMTS

Router

Network Connectivity CPE Devices

Set Top Boxes

DOCSIS Cable Modems MTA’s

Example: ServAssure HSD Diagnostics

March 2009 131Analyst / Investor Conference

31% of CMs are in a “degraded” condition (HSD @ 50% and VoIP

starts to have problems)5% of the CMs are not functioning at all

Example: ServAssure Voice Diagnostics

March 2009 132Analyst / Investor Conference

Analyze network problems based on the distribution of VOIP service quality for a certain period

Detect trends in positive or negative VOIP service quality by analyzing historical MOS graphs

Key Take-aways▪ On-Demand

- Significant trends indicate growing customer need for everything on demand

- Field experience in Interactive Advertising and continuing development

- Unified Platform enables integration of On Demand & Advertising

- Superior technology portfolio to address customer usage shift

▪ OSS/Service Assurance- Increased customer focus on OPEX and service quality- Solutions address workforce productivity and improving

service quality in face of increased network complexity

March 2009 133Analyst / Investor Conference

Questions?

March 2009 135Analyst / Investor Conference

Media & Communications Systems (MCS) Bryant IsaacsPresidentMedia & Communications Systems

BCS Sales$822.8 72%

ATS Sales$262.5 23%

MCS Sales$59.3 5%

ARRIS Organization MeetsSpecific Customer Needs

March 2009 137Analyst / Investor Conference

Access, Transport and Supplies

▪ Optical▪ RF▪ Supplies

▪ Favorable mix shift towards optics driven by HD video growth

Broadband Communication Systems

▪ CMTS▪ CPE

▪ #1 market share for VoIP E-MTA CPE, multi-line CPE

▪ Record revenue and unit CMTS levels in Q308▪ DOCSIS® 3.0 upgrade leader

Media and Communications Systems▪ OSS▪ VOD▪ Ad Insertion▪ Software reduces operators’

operating expense▪ Video on Demand provides

operators additional revenue generator

▪ Leader in ad insertion at top MSOs

Full Year 2008Revenue $1.145 Billion

Media & Communications SystemsOverview▪ Mission

- Deliver solutions to satisfy present and emerging needs of our service provider customer base in the areas of: • Service Assurance and Mobile Workforce Management• Video Content Delivery, Management and Advertising• Fixed Mobile Convergence

March 2009 138Analyst / Investor Conference

Continued Focus in Areas of Strong Industry Growth

Market Drivers: MCS Addresses Key Operator Needs

▪ Intense Competition for Subscribers

▪ Lower CAPEX and OPEX Enabling Solutions

▪ Everything On Demand▪ HDTV▪ Advanced Advertising▪ Mobility: Three Screen

Play

Assurance

On Demand

FMC

March 2009 139Analyst / Investor Conference

Assurance Solutions

Analyst / Investor Conference 140March 2009

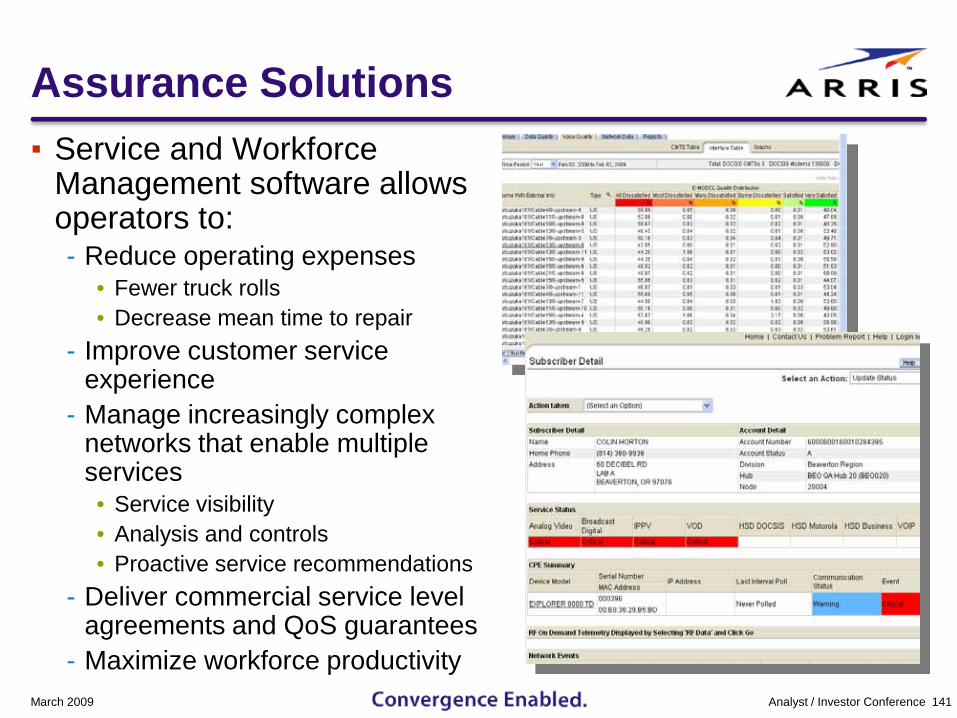

Assurance Solutions▪ Service and Workforce

Management software allows operators to:- Reduce operating expenses

• Fewer truck rolls• Decrease mean time to repair

- Improve customer service experience

- Manage increasingly complex networks that enable multiple services• Service visibility• Analysis and controls• Proactive service recommendations

- Deliver commercial service level agreements and QoS guarantees

- Maximize workforce productivityMarch 2009 141Analyst / Investor Conference

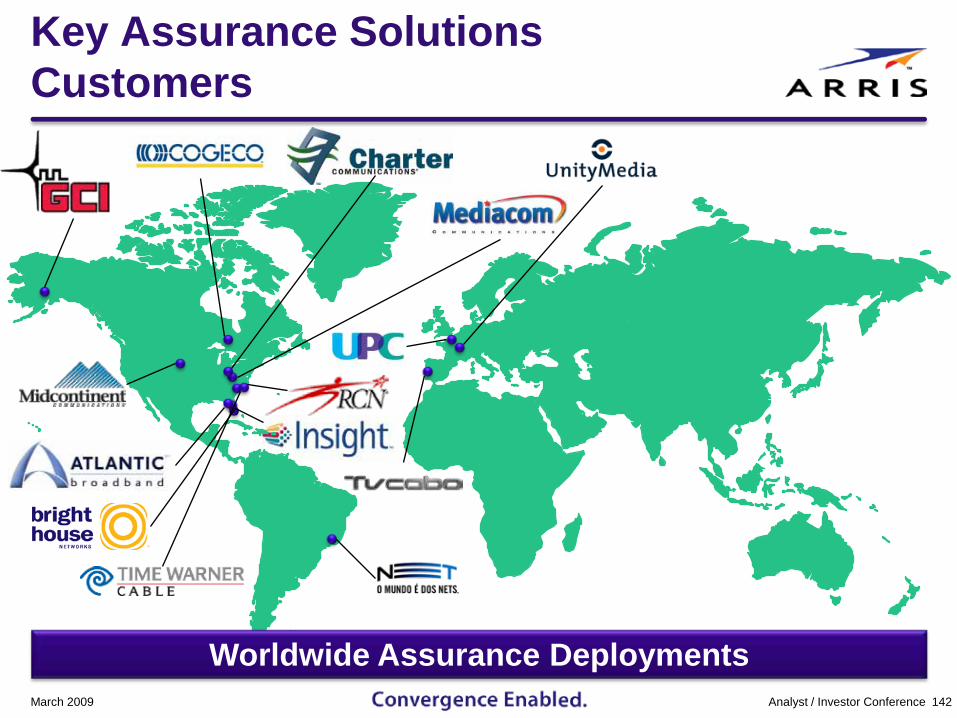

Key Assurance Solutions Customers

Worldwide Assurance DeploymentsMarch 2009 142Analyst / Investor Conference

Assurance Market View Strong Market Position and High Growth Potential

▪ Estimate ServAssure™ solution can be applied to ~246M Revenue Generating Units (RGUs) worldwide- ServAssure software currently manages 59M RGUs

▪ WorkAssure™ solution can be applied to any mobile workforce- Estimate ~165K CATV technicians worldwide

• ~104K are managed by a workforce solution - commercial or in-house

• WorkAssure software currently manages 30K technicians

March 2009 143Analyst / Investor Conference

2008 MCS Assurance Highlights▪ Best Revenue Year Ever

- NET Serviços rollout of WorkAssure solution• Over 1,600 field technicians in first phase

- Launched WorkAssure HouseCheck™ solution • Integration with ServAssure software for the field technician

- Added Comcast as a customer• Acquisition and integration of OpsLogic™ products

- Launched and deployed ServAssure DOCSIS 3.0 functionality

- Integrated E-MTA voice quality metrics with ServAssure solution

March 2009 144Analyst / Investor Conference

ARRIS WorkAssure Workforce ManagementA Revolution for NET’s Field Support

March 2009 145Analyst / Investor Conference

“Field”: A new tool just arrived to create a revolution in NET’s technical area

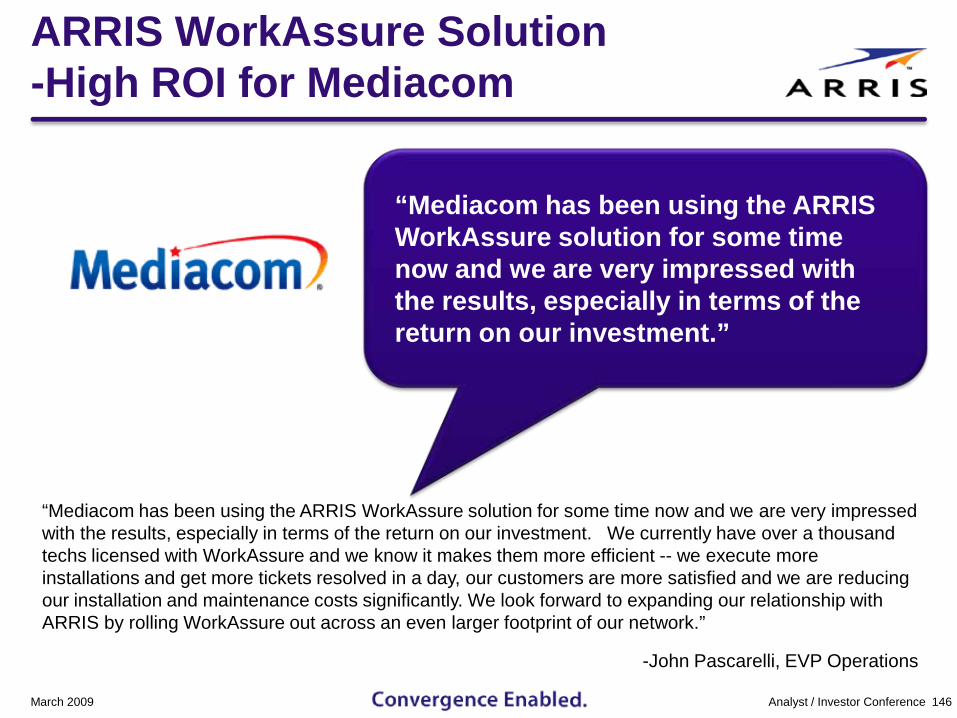

ARRIS WorkAssure Solution-High ROI for Mediacom

March 2009 146Analyst / Investor Conference

“Mediacom has been using the ARRIS WorkAssure solution for some time now and we are very impressed with the results, especially in terms of the return on our investment.”

“Mediacom has been using the ARRIS WorkAssure solution for some time now and we are very impressed with the results, especially in terms of the return on our investment. We currently have over a thousand techs licensed with WorkAssure and we know it makes them more efficient -- we execute more installations and get more tickets resolved in a day, our customers are more satisfied and we are reducing our installation and maintenance costs significantly. We look forward to expanding our relationship with ARRIS by rolling WorkAssure out across an even larger footprint of our network.”

-John Pascarelli, EVP Operations

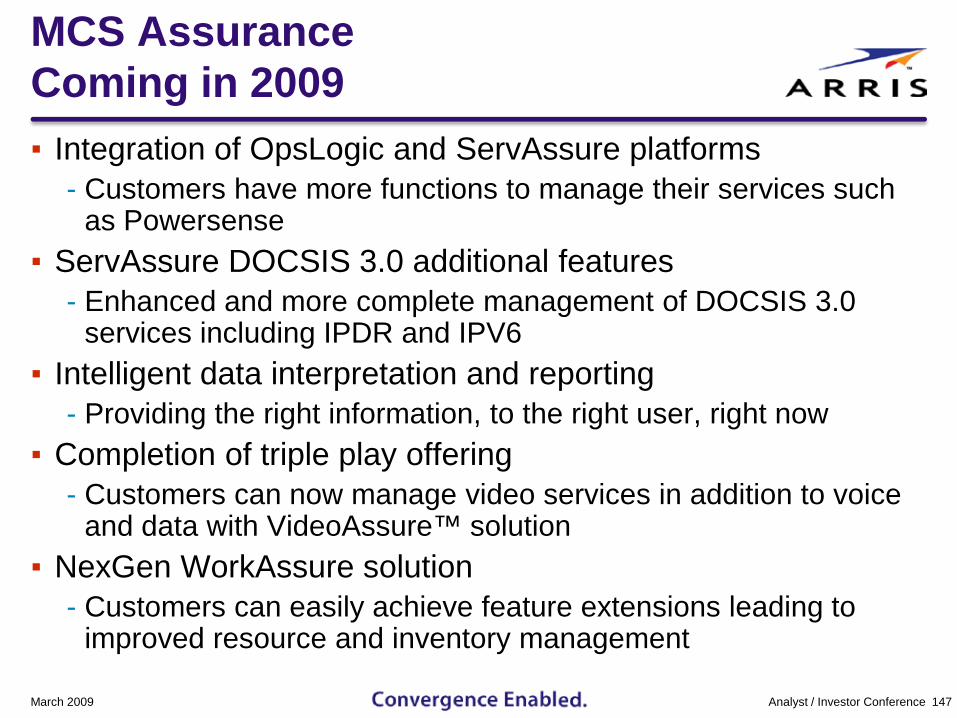

MCS AssuranceComing in 2009▪ Integration of OpsLogic and ServAssure platforms

- Customers have more functions to manage their services such as Powersense

▪ ServAssure DOCSIS 3.0 additional features- Enhanced and more complete management of DOCSIS 3.0

services including IPDR and IPV6▪ Intelligent data interpretation and reporting

- Providing the right information, to the right user, right now▪ Completion of triple play offering

- Customers can now manage video services in addition to voice and data with VideoAssure™ solution

▪ NexGen WorkAssure solution- Customers can easily achieve feature extensions leading to

improved resource and inventory management

March 2009 147Analyst / Investor Conference

On Demand

Analyst / Investor Conference 148March 2009

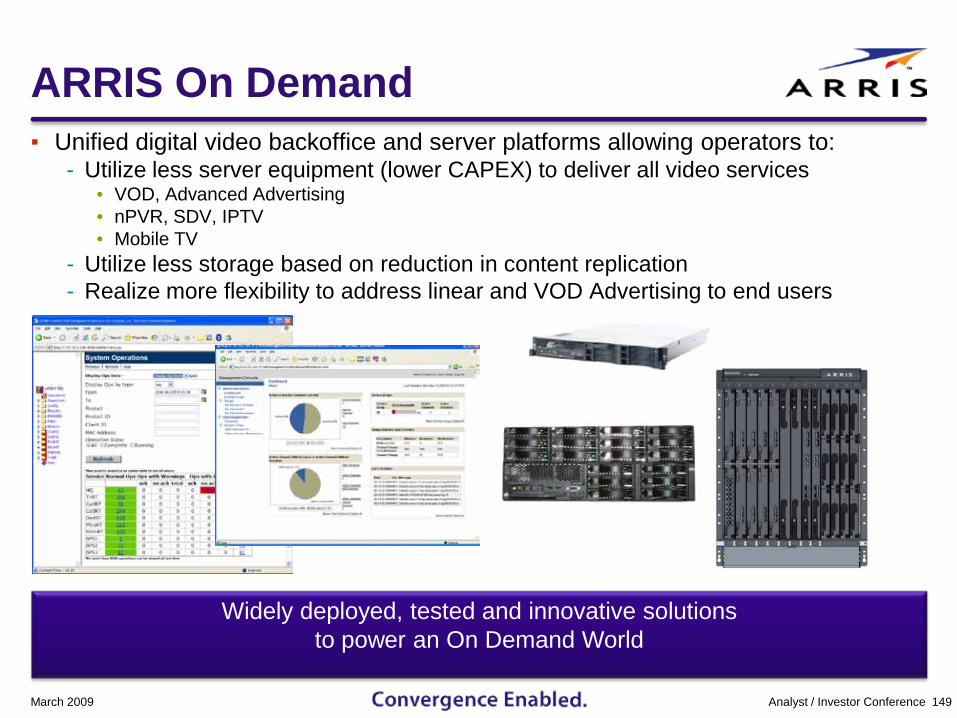

ARRIS On Demand▪ Unified digital video backoffice and server platforms allowing operators to:

- Utilize less server equipment (lower CAPEX) to deliver all video services• VOD, Advanced Advertising• nPVR, SDV, IPTV• Mobile TV

- Utilize less storage based on reduction in content replication- Realize more flexibility to address linear and VOD Advertising to end users

149

Widely deployed, tested and innovative solutions to power an On Demand World

Home | Contact Us | User’s Guide | Log OutManagement Console

Analyst / Investor ConferenceMarch 2009

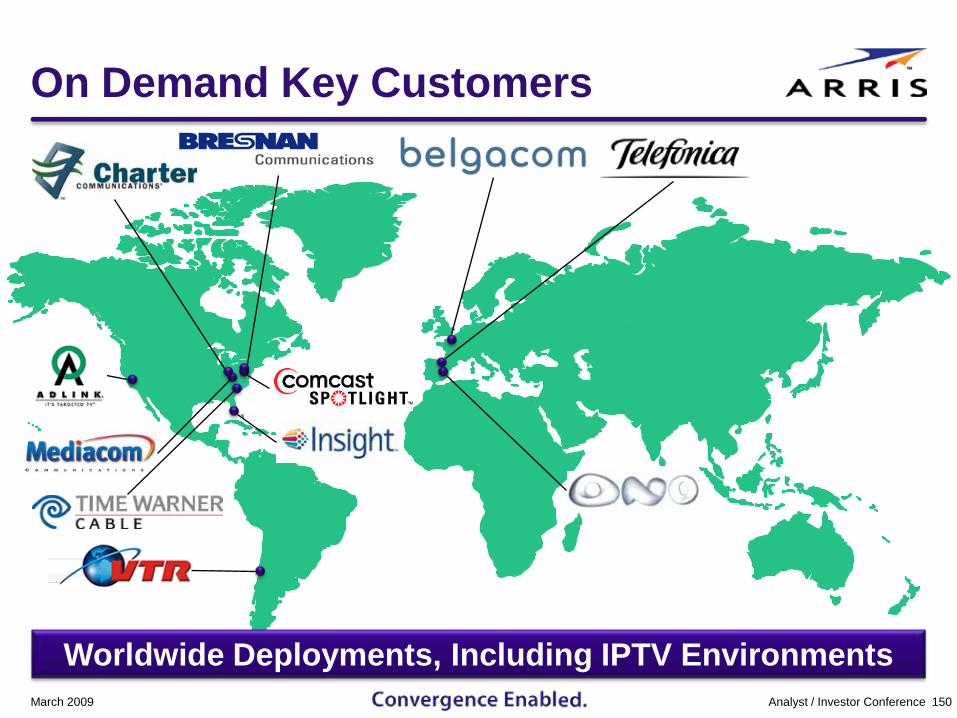

On Demand Key Customers

Worldwide Deployments, Including IPTV EnvironmentsMarch 2009 150Analyst / Investor Conference

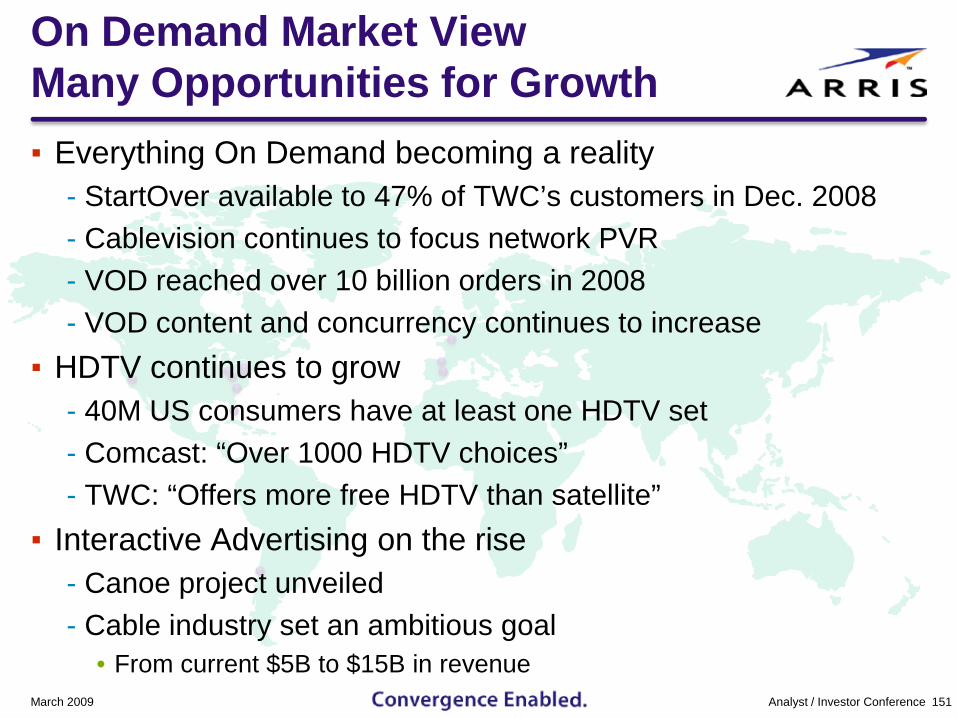

On Demand Market View Many Opportunities for Growth▪ Everything On Demand becoming a reality

- StartOver available to 47% of TWC’s customers in Dec. 2008- Cablevision continues to focus network PVR- VOD reached over 10 billion orders in 2008- VOD content and concurrency continues to increase

▪ HDTV continues to grow- 40M US consumers have at least one HDTV set- Comcast: “Over 1000 HDTV choices”- TWC: “Offers more free HDTV than satellite”

▪ Interactive Advertising on the rise- Canoe project unveiled- Cable industry set an ambitious goal

• From current $5B to $15B in revenueMarch 2009 151Analyst / Investor Conference

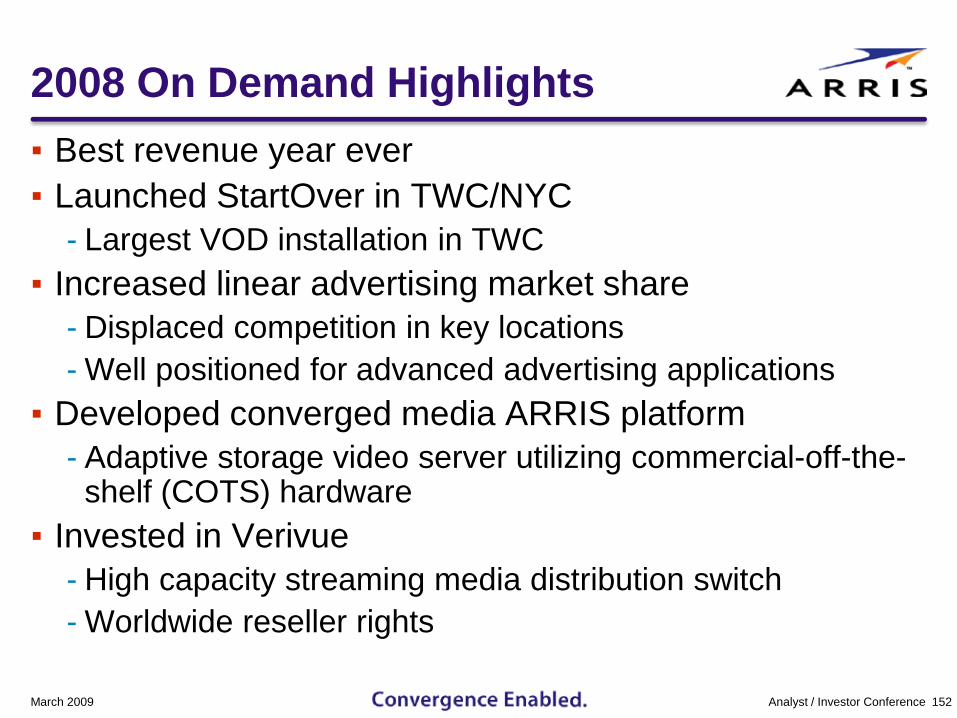

2008 On Demand Highlights▪ Best revenue year ever▪ Launched StartOver in TWC/NYC

- Largest VOD installation in TWC▪ Increased linear advertising market share

- Displaced competition in key locations- Well positioned for advanced advertising applications

▪ Developed converged media ARRIS platform- Adaptive storage video server utilizing commercial-off-the-

shelf (COTS) hardware▪ Invested in Verivue

- High capacity streaming media distribution switch- Worldwide reseller rights

March 2009 152Analyst / Investor Conference

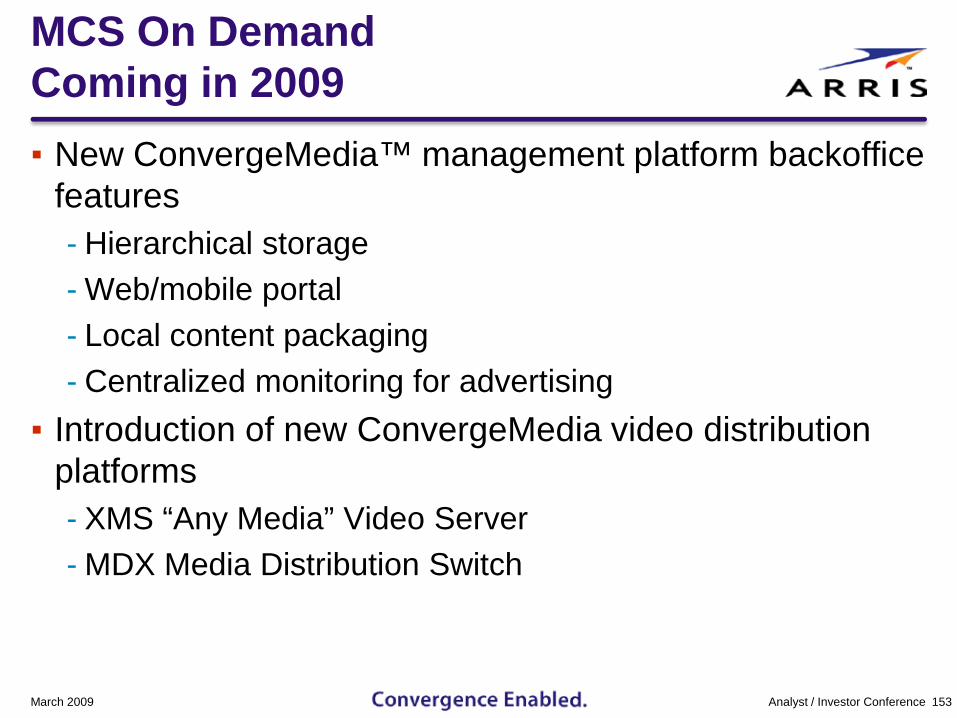

MCS On DemandComing in 2009▪ New ConvergeMedia™ management platform backoffice

features- Hierarchical storage- Web/mobile portal- Local content packaging- Centralized monitoring for advertising

▪ Introduction of new ConvergeMedia video distribution platforms- XMS “Any Media” Video Server- MDX Media Distribution Switch

March 2009 153Analyst / Investor Conference

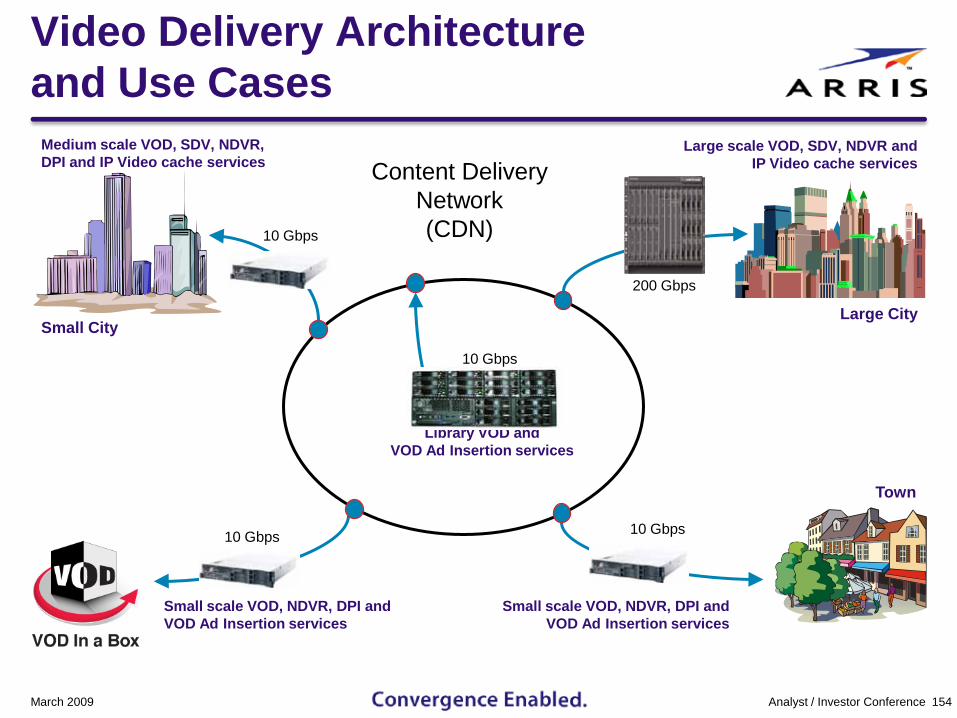

Video Delivery Architecture and Use Cases

March 2009 154Analyst / Investor Conference

Town

Large CitySmall City

10 Gbps

200 Gbps

10 Gbps

10 Gbps

10 Gbps

Large scale VOD, SDV, NDVR andIP Video cache services

Small scale VOD, NDVR, DPI and VOD Ad Insertion services

Small scale VOD, NDVR, DPI and VOD Ad Insertion services

Medium scale VOD, SDV, NDVR, DPI and IP Video cache services

Library VOD andVOD Ad Insertion services

Content Delivery Network(CDN)

ConvergeMedia Distribution▪ Two media switching families designed to consolidate

and distribute multiple media types over any network to any device

▪ Origin servers- ARRIS XMS: any “X” media stored

and streamed- High storage to streams ratio- Central and regional for large video libraries

▪ Network appliances with storage- ARRIS MDX: media distribution switch “X”- High streams to storage ratio- Edge switch/cache for large streaming

capacity

March 2009 155Analyst / Investor Conference

XMS

ARRIS ConvergeMedia XMS▪ High storage to streams ratio

- Ideal for centralized, or lightly-networked distributed architectures

▪ 100% COTS based platform- Optimized cost/performance across 200 to

20,000 streams▪ Adaptive storage design

- SAS, SATA, SSD or RAM- Additional cost/performance optimization- 2 to 96 TB storage

▪ Cost-effective for network PVR (nPVR) applications

▪ Unified Platform: built-in linear and On Demand advertising support

March 2009 156Analyst / Investor Conference

MDX9200

by Verivue

ARRIS ConvergeMedia MDX▪ High streams to storage ratio

- Ideal for content delivery network architectures▪ VueStore™ solid state storage

- Purpose built flash optimization- High density FLASH storage- Green approach / lowest power

▪ Seamless multi-screen convergence- Web engine delivers Internet video

streams - Broadband video streaming at

line rates▪ Penalty-free high speed content ingest▪ MDX9200: up to 50,000 SD streams

200Gb/sec, up to 24TB local storageMarch 2009 157Analyst / Investor Conference

SummaryMedia & Communications Systems

March 2009 158Analyst / Investor Conference

ARRIS MCSPositioned for Growth▪ Assurance delivers key OSS products

- Results in higher customer satisfaction and retention - Optimizes field workforce- Leading to lower OPEX and CAPEX

▪ On Demand delivers a unified video management and delivery platform including dual families of video servers

▪ Meets the ever increasing needs for HDTV and demand driven video services for a variety of architectures- Allows integration of managed and internet streamed video

services- Delivers on the promise of Advanced Advertising

▪ Coming off best revenue year with strong bookings ▪ ARRIS increasing investment in these key areasMarch 2009 159Analyst / Investor Conference

QuestionsBryant IsaacsPresidentMedia and Communications Systems

Sales and Market ReviewRon CoppockPresident, Sales and Marketing

2009 and Beyond Sales Objectives▪ Continue to capture an increasing share of customer

CAPEX and OPEX

▪ Ensure premier industry sales force is deployed in the right place at the right time

March 2009 162Analyst / Investor Conference

Worldwide Sales Commitment▪ 200 sales professionals deployed in 19 countries

- Direct sales - Sales engineering - Inside sales - customer service - Business development - Global VAR network

▪ Enhanced industry stature▪ Seasoned and experienced sales team▪ Customers are engaging us earlier in buying process▪ Strong record of superior technology and service

March 2009 163Analyst / Investor Conference

Doing Business with Approximately 1,000 Customers in 70 Countries

March 2009 164Analyst / Investor Conference

ARRIS Sales Offices

March 2009 165Analyst / Investor Conference

Mexico City

Philadelphia

Atlanta

BostonChicagoDenver

State College

Beaverton Wallingford

Amsterdam

Barcelona

BerlinCorkFrankfurtLondon

Madrid

Milan

Singapore

Beijing

Hong Kong

Seoul

ShanghaiShenzhen

Tokyo

Bogota

Buenos AiresSantiagoSao Paulo

ARRIS Sales Offices

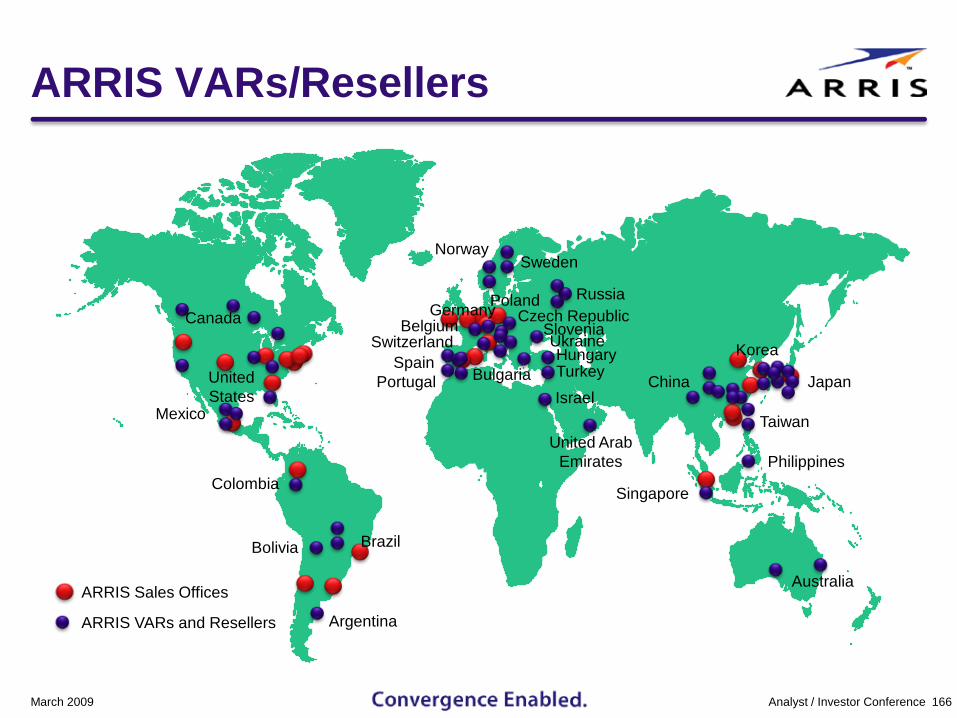

ARRIS VARs/Resellers

March 2009 166Analyst / Investor Conference

ARRIS Sales Offices

Poland

Sweden

Canada

Colombia

BrazilBolivia

Mexico

United States

Argentina

Australia

China

Philippines

Korea

Japan

Taiwan

Ukraine

Bulgaria

Belgium

Norway

Russia

United Arab Emirates

PortugalIsrael

Hungary

Germany Czech Republic

Turkey

SwitzerlandSpain

Slovenia

Singapore

ARRIS VARs and Resellers

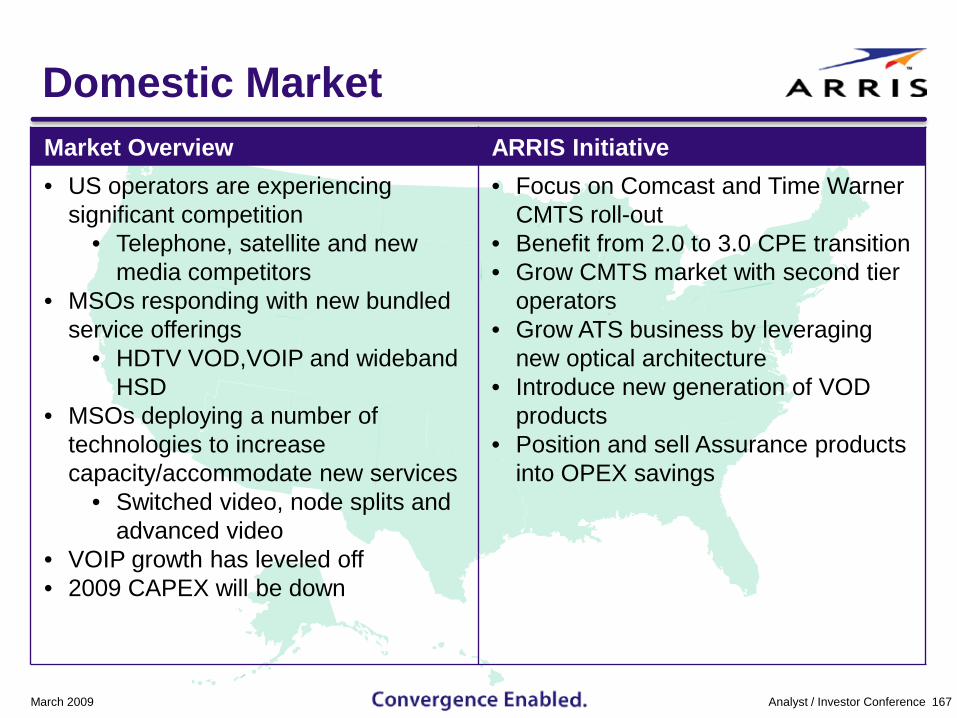

Domestic Market Market Overview ARRIS Initiative• US operators are experiencing

significant competition • Telephone, satellite and new

media competitors• MSOs responding with new bundled

service offerings• HDTV VOD,VOIP and wideband

HSD• MSOs deploying a number of

technologies to increase capacity/accommodate new services

• Switched video, node splits and advanced video

• VOIP growth has leveled off• 2009 CAPEX will be down

• Focus on Comcast and Time Warner CMTS roll-out

• Benefit from 2.0 to 3.0 CPE transition • Grow CMTS market with second tier

operators• Grow ATS business by leveraging

new optical architecture• Introduce new generation of VOD

products • Position and sell Assurance products

into OPEX savings

March 2009 167Analyst / Investor Conference

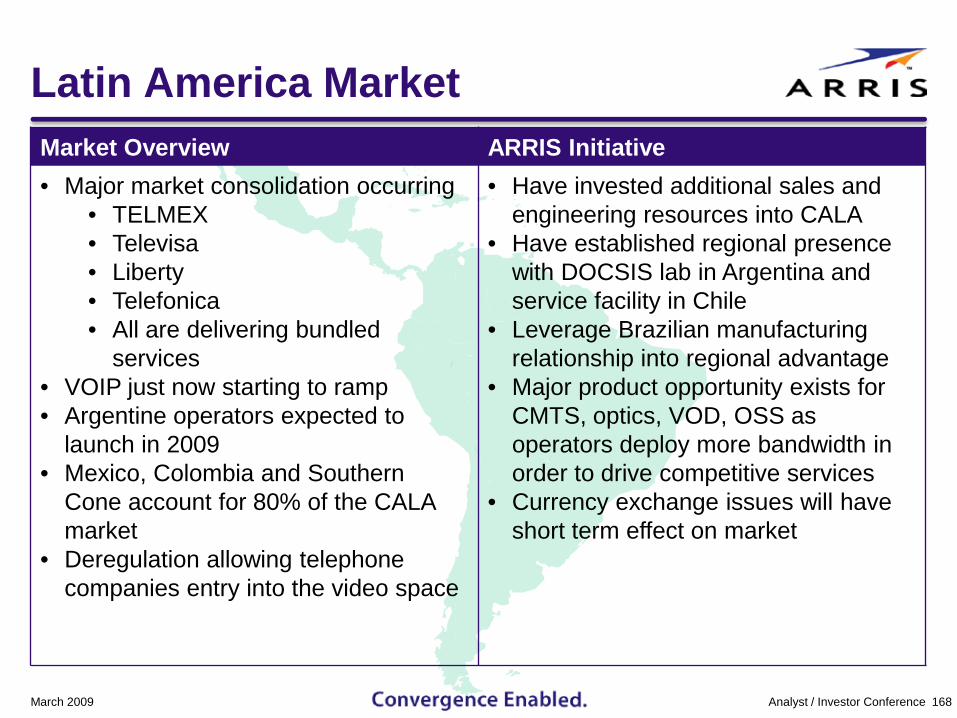

Latin America MarketMarket Overview ARRIS Initiative• Major market consolidation occurring

• TELMEX• Televisa• Liberty• Telefonica• All are delivering bundled

services• VOIP just now starting to ramp• Argentine operators expected to

launch in 2009• Mexico, Colombia and Southern

Cone account for 80% of the CALA market

• Deregulation allowing telephone companies entry into the video space

• Have invested additional sales and engineering resources into CALA

• Have established regional presence with DOCSIS lab in Argentina and service facility in Chile

• Leverage Brazilian manufacturing relationship into regional advantage

• Major product opportunity exists for CMTS, optics, VOD, OSS as operators deploy more bandwidth in order to drive competitive services

• Currency exchange issues will have short term effect on market

March 2009 168Analyst / Investor Conference

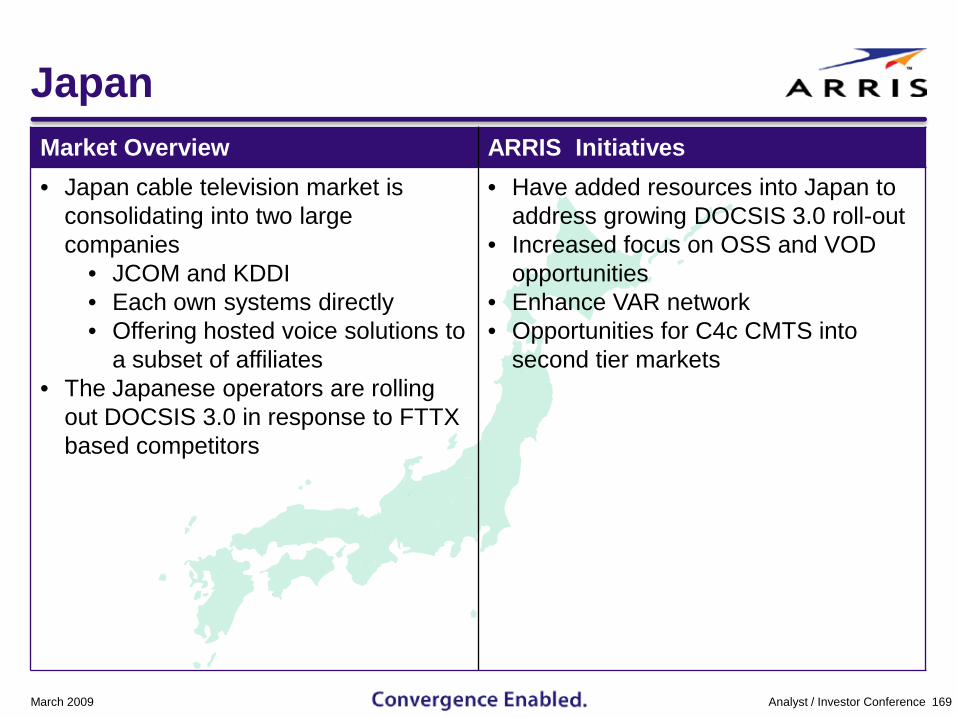

Japan

March 2009 169Analyst / Investor Conference

Market Overview ARRIS Initiatives• Japan cable television market is

consolidating into two large companies

• JCOM and KDDI• Each own systems directly • Offering hosted voice solutions to

a subset of affiliates• The Japanese operators are rolling

out DOCSIS 3.0 in response to FTTX based competitors

• Have added resources into Japan to address growing DOCSIS 3.0 roll-out

• Increased focus on OSS and VOD opportunities

• Enhance VAR network• Opportunities for C4c CMTS into

second tier markets

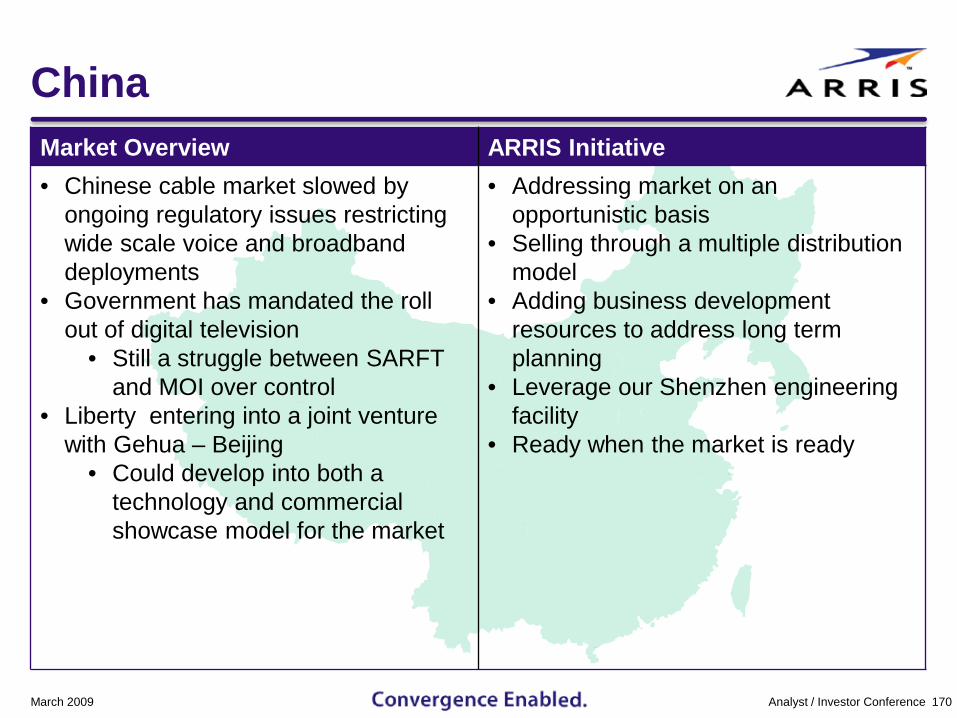

China

March 2009 170Analyst / Investor Conference

Market Overview ARRIS Initiative• Chinese cable market slowed by

ongoing regulatory issues restricting wide scale voice and broadband deployments

• Government has mandated the roll out of digital television

• Still a struggle between SARFT and MOI over control

• Liberty entering into a joint venture with Gehua – Beijing

• Could develop into both a technology and commercial showcase model for the market

• Addressing market on an opportunistic basis

• Selling through a multiple distribution model

• Adding business development resources to address long term planning

• Leverage our Shenzhen engineering facility

• Ready when the market is ready

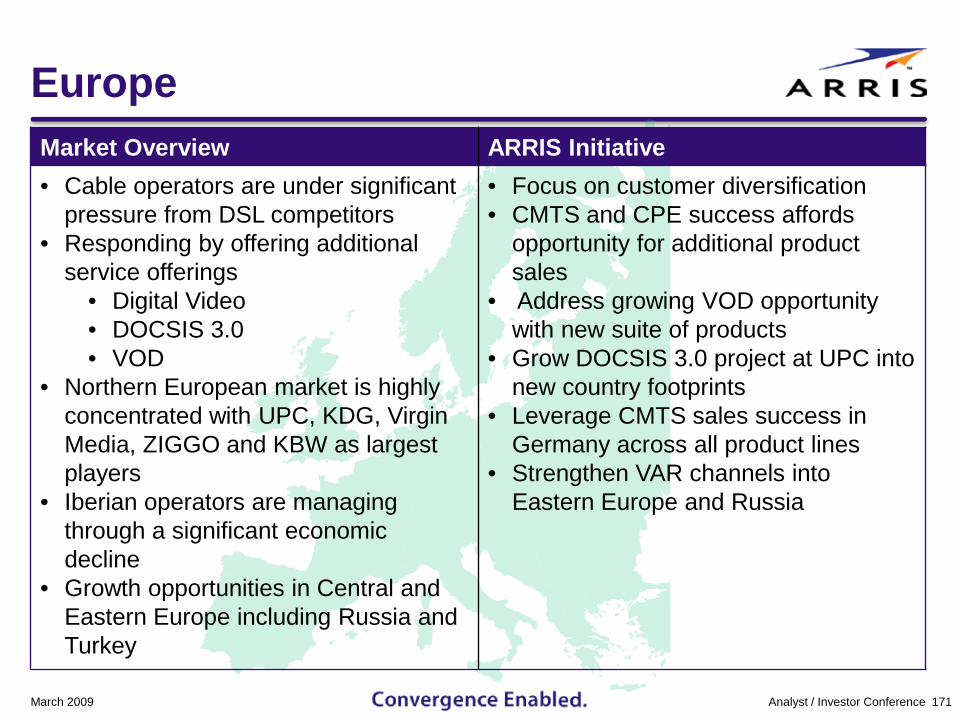

EuropeMarket Overview ARRIS Initiative• Cable operators are under significant

pressure from DSL competitors• Responding by offering additional

service offerings• Digital Video• DOCSIS 3.0• VOD

• Northern European market is highly concentrated with UPC, KDG, Virgin Media, ZIGGO and KBW as largest players

• Iberian operators are managing through a significant economic decline

• Growth opportunities in Central and Eastern Europe including Russia and Turkey

• Focus on customer diversification • CMTS and CPE success affords

opportunity for additional product sales

• Address growing VOD opportunitywith new suite of products

• Grow DOCSIS 3.0 project at UPC into new country footprints

• Leverage CMTS sales success in Germany across all product lines