Embed Size (px)

Citation preview

2/3/2015

1

References:Atrill, P., E. Mclaney, D. Harvey, and M. Jenner, Accounting: An Introduction, 4edn. 2009, Prentice Hall.

Atrill, P., and E. Mclaney, Accounting and Finance: For Non-Specialists, 8edn. 2013, Prentice Hall.

Atrill, P., and E. Mclaney, Management Accounting: For Decision Makers, 4edn. 2005, Prentice Hall.

Atrill, P., Financial Management: For Decision Makers, 5edn. 2009, Prentice Hall

Accounting/Finance function within a business is a central part of its management information systems (MIS).

The main purpose of accounting/finance information is to help managers make decisions with respect to: Allocation of resources; Performance evaluation and control; Continue with certain business operations; Invest in particular projects or new ventures; Sell particular products

• Finance is concerned with the ways in which funds for a business are raised and invested.

• Financial information is to understand main forms of finance available; risks associated with each form of finance; the returns from available investments; and risks associated with that investment.

• Accounting is concerned with the collection, analysis and communication of financial information.

• Accounting information is a tool for decision-making, planning and control of business.

3. Businesses prepare reports to showthe results of their operations.

2. Business transactions occur.

1. People make decisions.

2/3/2015

2

• Planning is essential for business success

• Prudent decision-making is closely linked to

effective planning

• Planning covers both long-term and short-term

scenarios

• Over time, plans are normally adapted to changing

circumstances

Planning is usually broken down into three stages:

1. Setting the objectives or mission of the business(Detailing what the business is basically trying to achieve)

2. Setting long-term plans(Describing how the business will set out to achieve its long-term objectives)

3. Setting detailed short-term plans or budgets(Typically financial plans for one year ahead)

2/3/2015

3

• Control is the process of making planned events actually occur

• Accounting is useful in control to compare planned outcomes with actual outcomes in commonly specified terms

• Managers can take steps to get the business back on track if variances are highlighted between planned and actual outcomes

Step 1

Step 2

Step 3

Step 4

Step 5

Step 6

Step 7

Identify business objectives

Consider options

Prepare a long-term plan based on themost appropriate option(s)

Perform and collect information on actual performance

Prepare short-term plans (budgets)

Respond to divergences between plans and actuals,and exercise control

Revise plans and budgets if necessary

The popular suggested business objectives include:

• Maximisation of sales revenue (this does not consider the need to cover business costs)

• Maximisation of profit (this takes in to account sales revenues as well as expenses, but is limited as it does not include other factors such as risk.

• Maximisation of return on capital employed (accounts for level of profit as well as the level of investment)

•Survival (This is the aim of most businesses, however it is rarely a primary objective)

•Long-term stability (Like survival, most businesses aim for it, but it is rarely a primary objective)

2/3/2015

4

• Growth (Encompasses survival and long-term stability and aims to strike a balance between short and long-term benefits, however it is probably not a specific enough target)

• Satisficing (Attempting to grant a satisfactory return to all stakeholders - not just the owners. Difficult to define as a practical benchmark for business decisions.)

• Achieving sustainable development (Achieving economic growth while minimising or eliminating environmental impact and meeting society’s expectations of good corporate citizenship.)

• Enhancement / maximisation of business wealth

• Means the business takes decisions intended to make it worth more.

• Encompasses all the valuable features of the previous suggested objectives.

• Likely to be the main financial objective for many businesses )

• Management accounting is concerned with providing managers with information required for day-to-day running of the business

• Financial accounting is concerned with providing the other users with useful information

2/3/2015

5

Financial Accounting Management AccountingFocus Mainly external Internal only

Nature of reports General purpose Specific purpose

Level of detail Broad overview Quite detailed

Restrictions Accounting standards and other regulations

No restrictions

Reporting interval Mainly annual, sometimes semi-annual or quarterly

Whenever required – weekly, monthly

Time horizon Mainly historical Both past and future

Range of information Quantifiable in money terms; focus on objective and verifiable data

Can contain non-financial information; less focus on objectivity and verifiability

There are three main financial reports:

• The Cash Flow Statement (shows the sources and uses of cash for a period i.e. cash movements – cash in & cash out)

• The Income Statement - statement of financial performance(traditionally known as Profit and Loss; measures and reports how much profit has been generated in a period )

• The Balance Sheet - statement of financial position (shows overall net financial position at the end of a particular period)

• Paul starts a wrapping paper sales business with $100

• On the first day, he uses the $100 to purchase wrapping

paper (“inventory”)

• On the same day he sells 75% of that inventory for $110 in

total

What cash movements took place in the first day of trading?

• Closing cash balance for the day is $110 (opening balance

$100 - $100 stock purchase + $110 sales = $110)

How much did wealth increase (financial performance) as a result of the first day’s trading?

• The increase or decrease in wealth is measured as the difference between sales made and the cost of goods sold

• sales were $110 less cost of goods sold $75 = profit of $35

Note that only the cost of the paper sold is measured against the sales to find profit, not the total cost of the wrapping paper purchased.

2/3/2015

6

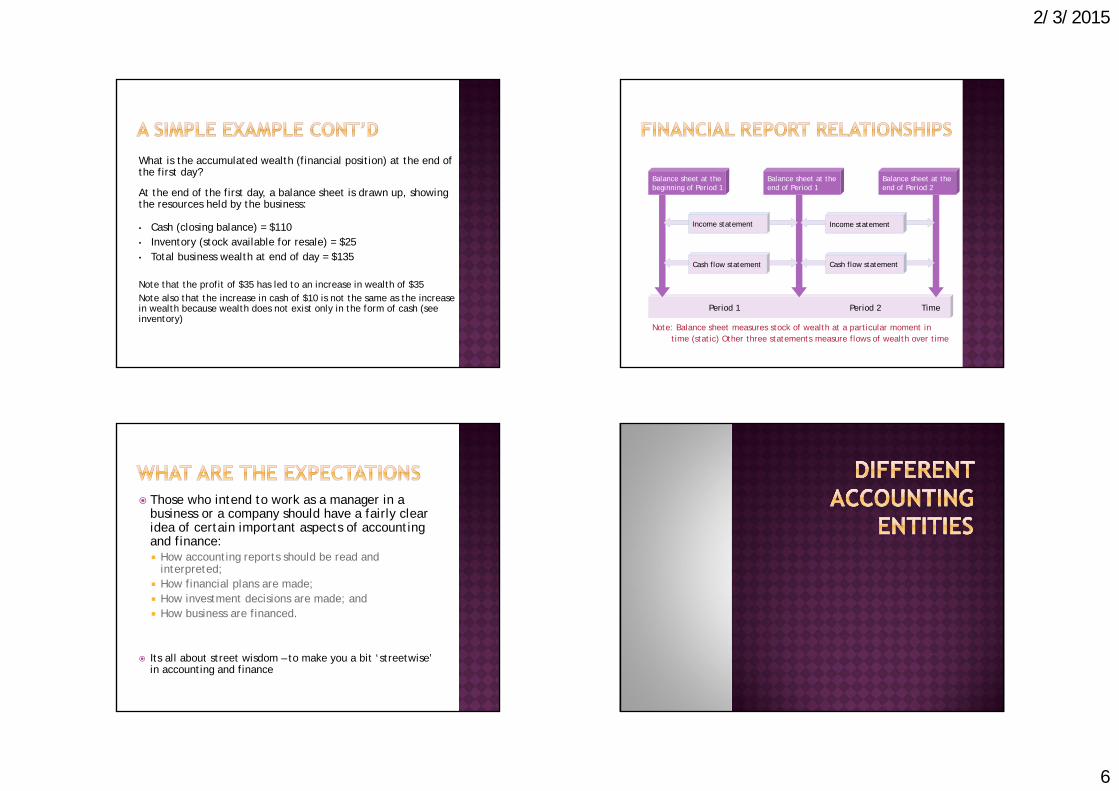

What is the accumulated wealth (financial position) at the end of the first day?

At the end of the first day, a balance sheet is drawn up, showing the resources held by the business:

• Cash (closing balance) = $110• Inventory (stock available for resale) = $25• Total business wealth at end of day = $135

Note that the profit of $35 has led to an increase in wealth of $35Note also that the increase in cash of $10 is not the same as the increase in wealth because wealth does not exist only in the form of cash (see inventory)

Balance sheet at the beginning of Period 1

Balance sheet at the end of Period 2

Balance sheet at the end of Period 1

Period 1 Period 2 Time

Income statement Income statement

Cash flow statement Cash flow statement

Note: Balance sheet measures stock of wealth at a particular moment in time (static) Other three statements measure flows of wealth over time

Those who intend to work as a manager in a business or a company should have a fairly clear idea of certain important aspects of accounting and finance: How accounting reports should be read and

interpreted; How financial plans are made; How investment decisions are made; and How business are financed.

Its all about street wisdom – to make you a bit ‘streetwise’ in accounting and finance

2/3/2015

7

• Sole Proprietorship (single owner called the proprietor)

• Partnership (two or more owners established by a formal partnership agreement or informal arrangement)

• Company (owned by many people who have invested in the business)• Public Limited Company / Berhad• Private Limited Company / Sendirian Berhad

• No separate legal entity (no distinction between the owner and the business, but distinct as an accounting entity)

• Limited life (restricted to the period the owner continues to operate the business)

• Unlimited liability (the owner is fully responsible for the debts and obligations of the business)

• Minimum reporting regulations (minimal compared with other entity structures)

• Limited access to funds (restricted to the personal resources of a single owner)

• Low establishment costs (comparatively much lower compared to other entity structures)

Some advantages of sole proprietorships include:

• Simple and inexpensive to establish and operate

• Minimal financial reporting regulations

• Ownership and management are normally combined

• Financial rewards flow directly to the owner

• Timely decision-making is possible

Some disadvantages of sole proprietorships include:

• Unlimited liability of the owner

• Restricted access to ownership funds

• Limited access to non-ownership funding

• inflexibility in management - sole owner is the sole

manager

2/3/2015

8

A partnership may be described as: The relationship that exists between two or more persons carrying on a business with a view to profit.

• The relationship may be established by a formal partnership agreement or an informal arrangement between the parties, or it may be inferred by the actions of two or more individuals.

• The partnership maintains individual records of each partner’s transactions according to:• Resource contributions (capital)• Resource withdrawals (drawings)• Share of undistributed profits (either current or retained

earnings)

• No separate legal entity (no distinction between the partners and the business, but distinct as an accounting entity)

• Limited life (as long as the partnership exists)

• Unlimited liability (jointly and separately for debts of business) • Mutual agency (each partner is responsible for the actions of

the other partners)• Co-ownership of assets (the partnership assets are owned by

the partners in aggregate, not individually)

• Co-ownership of profits (equally or in agreed proportions)• Limited membership (a restriction on the number of partners

allowed. Normally twenty is the limit. Some exemptions exist e.g. accounting practices)

• Increased regulation (most states have Partnership Acts for direction of activities and rights and responsibilities of partners)

Advantages of partnership as against sole proprietorships:

• Greater access to capital (two or more owners)

• Different skills are brought together (partners)

• Greater management flexibility (more than one

owner)

• Taxation advantages (income sharing)

Disadvantages of partnership as against sole proprietorships:

• higher level of regulation (partnership acts)

• profit sharing with other owners (co-ownership)

• asset sharing with other owners (co-ownership)

• reduced decision-making authority (shared management)

• responsibility for the business actions of other partners

(mutual agency)

2/3/2015

9

Disadvantages of partnership as against a company entity:

• limited life affects long-term planning

• unlimited liability creates greater risk for ownership

investment

• absence of specialist management team

• mutual agency imposes extra responsibility for the

business actions of other partners

• limited access to both ownership funds and debt funds

• Important to have a detailed and formal agreement so that most potential problems can be avoided

• Issues not covered by the partnership agreement will be governed by Partnership Act

On distribution of partnership profit, most Partnership Acts indicate:• Partners not entitled to a salary or wage• Partners not entitled to interest on capital contributed• Equal shares of profits and lossesThese rules apply only in the absence of an agreement, partners may

agree to share profits in any way they choose

There are a number of company types, the most common being the company limited by shares, or ‘limited company’

A limited company may be defined as: An artificial legal person which has an identity separate from that of those who own and manage it.

Ownership interest is broken down into ‘shares’ hence the term ‘shareholders’ to describe the owners, who have invested in the business.

• Separate legal entity (a limited company has the legal capacity of a person and is separate from those who own the entity i.e. can sue and be sued, buy, borrow, lend and employ in its own right as a legal person)

• Unlimited (perpetual) life (the life of the company is indefinite and not related to the life of the owners)

• Limited liability (the entity is responsible for its own debts and obligations because it is a legal person. Shareholder’s obligations cease upon full payment of the agreed price of their shares.)

• Company ownership of assets (assets owned by the company in its own right as a legal person)

• Company profits belong to the shareholders (profits are either distributed or retained for the benefit of shareholders)

2/3/2015

10

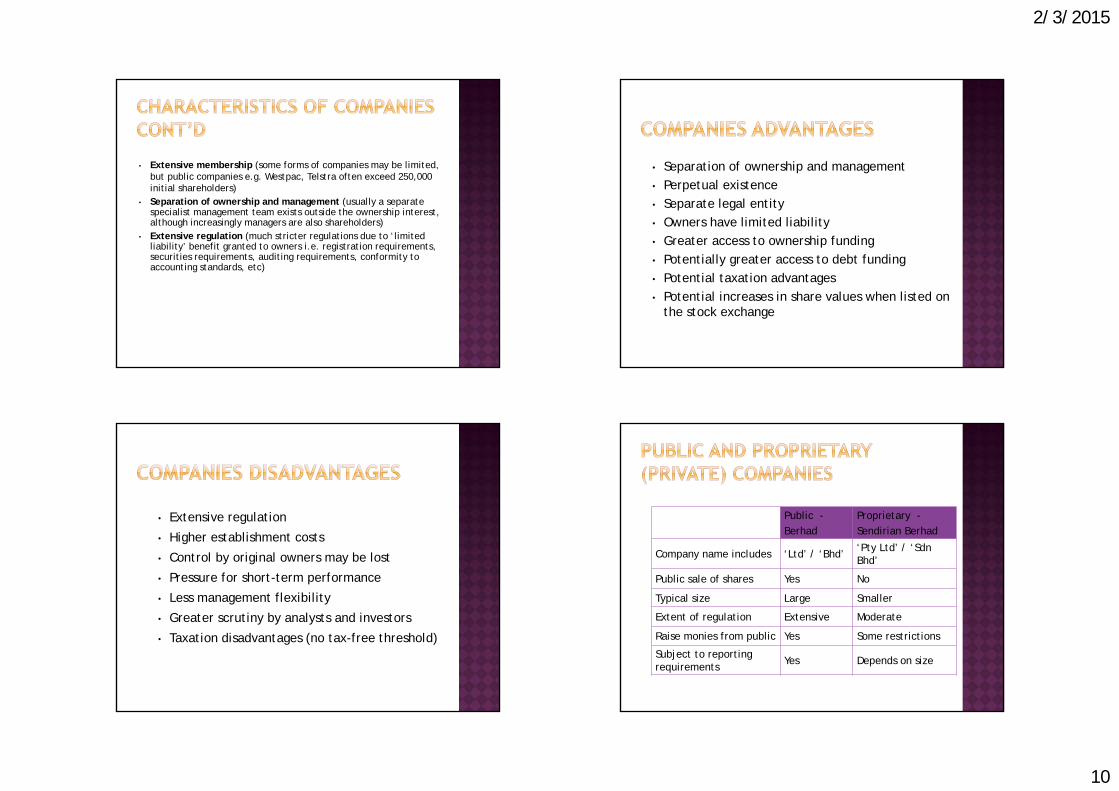

• Extensive membership (some forms of companies may be limited, but public companies e.g. Westpac, Telstra often exceed 250,000 initial shareholders)

• Separation of ownership and management (usually a separate specialist management team exists outside the ownership interest, although increasingly managers are also shareholders)

• Extensive regulation (much stricter regulations due to ‘limited liability’ benefit granted to owners i.e. registration requirements, securities requirements, auditing requirements, conformity to accounting standards, etc)

• Separation of ownership and management• Perpetual existence• Separate legal entity• Owners have limited liability• Greater access to ownership funding • Potentially greater access to debt funding• Potential taxation advantages• Potential increases in share values when listed on

the stock exchange

• Extensive regulation

• Higher establishment costs

• Control by original owners may be lost

• Pressure for short-term performance

• Less management flexibility

• Greater scrutiny by analysts and investors

• Taxation disadvantages (no tax-free threshold)

Public -Berhad

Proprietary -Sendirian Berhad

Company name includes ‘Ltd’ / ‘Bhd’ ‘Pty Ltd’ / ‘Sdn Bhd’

Public sale of shares Yes No

Typical size Large Smaller

Extent of regulation Extensive Moderate

Raise monies from public Yes Some restrictions

Subject to reporting requirements Yes Depends on size

2/3/2015

11

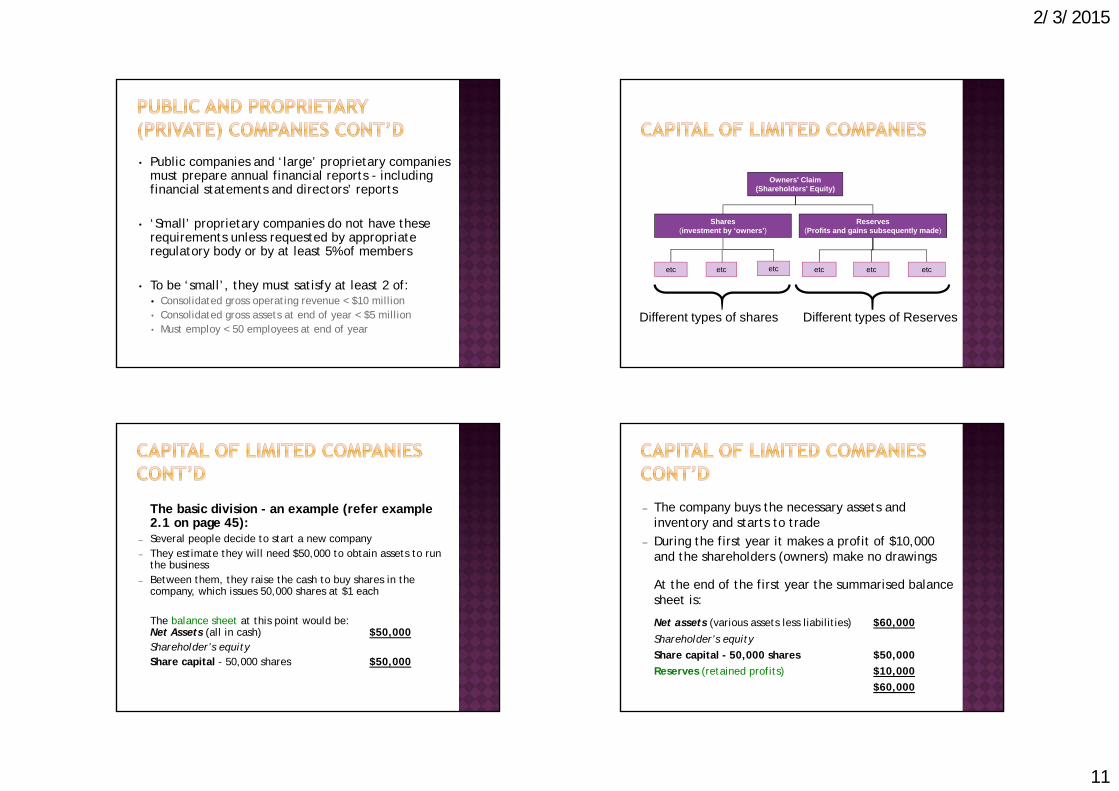

• Public companies and ‘large’ proprietary companies must prepare annual financial reports - including financial statements and directors’ reports

• ‘Small’ proprietary companies do not have these requirements unless requested by appropriate regulatory body or by at least 5% of members

• To be ‘small’, they must satisfy at least 2 of:• Consolidated gross operating revenue < $10 million• Consolidated gross assets at end of year < $5 million• Must employ < 50 employees at end of year

Different types of shares Different types of Reserves

Owners' Claim(Shareholders' Equity)

Shares(investment by ‘owners’)

Reserves(Profits and gains subsequently made)

etc etc etc etc etc etc

The basic division - an example (refer example 2.1 on page 45):

Several people decide to start a new company They estimate they will need $50,000 to obtain assets to run

the business Between them, they raise the cash to buy shares in the

company, which issues 50,000 shares at $1 each

The balance sheet at this point would be:Net Assets (all in cash) $50,000Shareholder’s equityShare capital - 50,000 shares $50,000

The company buys the necessary assets and inventory and starts to trade

During the first year it makes a profit of $10,000 and the shareholders (owners) make no drawings

At the end of the first year the summarised balance sheet is:

Net assets (various assets less liabilities) $60,000Shareholder’s equityShare capital - 50,000 shares $50,000Reserves (retained profits) $10,000

$60,000

2/3/2015

12

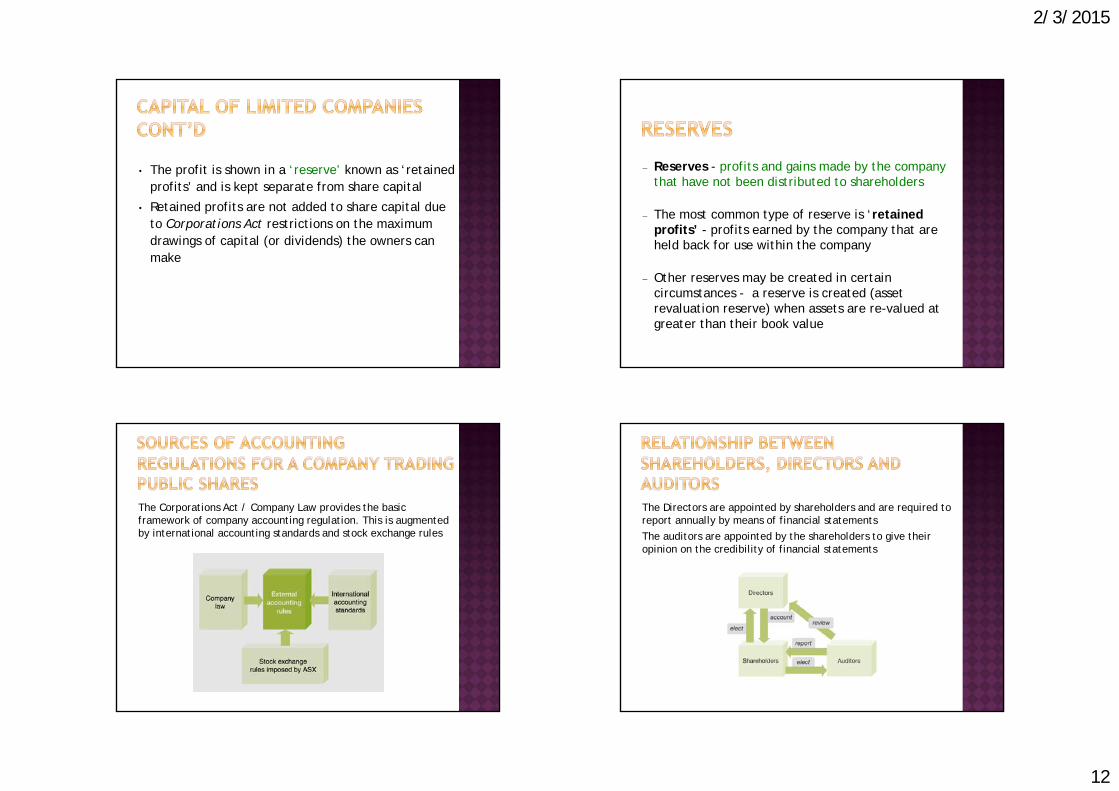

• The profit is shown in a ‘reserve’ known as ‘retained profits’ and is kept separate from share capital

• Retained profits are not added to share capital due to Corporations Act restrictions on the maximum drawings of capital (or dividends) the owners can make

Reserves - profits and gains made by the company that have not been distributed to shareholders

The most common type of reserve is ‘retained profits’ - profits earned by the company that are held back for use within the company

Other reserves may be created in certain circumstances - a reserve is created (asset revaluation reserve) when assets are re-valued at greater than their book value

The Corporations Act / Company Law provides the basic framework of company accounting regulation. This is augmented by international accounting standards and stock exchange rules

The Directors are appointed by shareholders and are required to report annually by means of financial statementsThe auditors are appointed by the shareholders to give their opinion on the credibility of financial statements