Embed Size (px)

Citation preview

Annual Report2004

Annual Report2004

C E N T R A L P R O V I D E N T F U N D B O A R D

Contents

09 Mission, Vision and Values

10 Board of Directors

12 Senior Management

14 Organisational Structure

17 Review of Operations

39 Financial Statements

67 Annexes

06

07

SINGAPORE QUALITY AWARD (SQA) WINNER

“By living out our core values, staff are able to excel

in our fi ve areas of excellence

– Benefi ts, Customers, Processes, People and Finance –

which helps us achieve our mission and advances us on

the journey towards business excellence.”

Willie Tan, Chief Executive Offi cer, CPF Board

“CPF’s customer-driven quality mindset has resulted in the

development of a multi-channel information delivery system.”

“CPF staff is actively engaged in skills upgrading and innovation.

There is a keen desire by all staff to provide excellent customer

service and a strong sense of identity to the organisation.”

“Leading from the front, the Board’s senior management

has set in place an integrated approach to drive, permeate

and operationalise its Mission, Vision, Values and 5 Areas of

Excellence through a well-articulated CPF Lifestyle value

concept across all levels of staff.”

SQA Award, SPRING Singapore

08

09

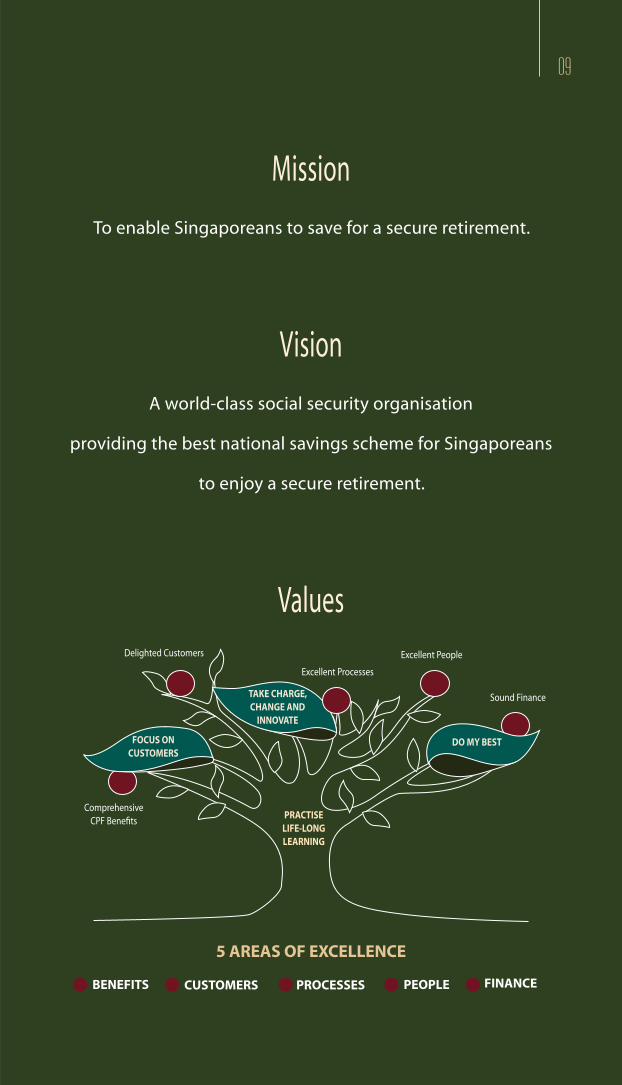

Mission

To enable Singaporeans to save for a secure retirement.

Vision

A world-class social security organisation

providing the best national savings scheme for Singaporeans

to enjoy a secure retirement.

Values

09

Excellent Processes

Excellent People

Sound Finance

Delighted Customers

Comprehensive CPF Benefi ts

TAKE CHARGE, CHANGE AND

INNOVATE

FOCUS ON CUSTOMERS

DO MY BEST

PRACTISE LIFE-LONG LEARNING

5 AREAS OF EXCELLENCE

BENEFITS CUSTOMERS PROCESSES PEOPLE FINANCE

10 Central Provident Fund Board | Annual Report 200410 Central Provident Fund Board | Annual Report 2004

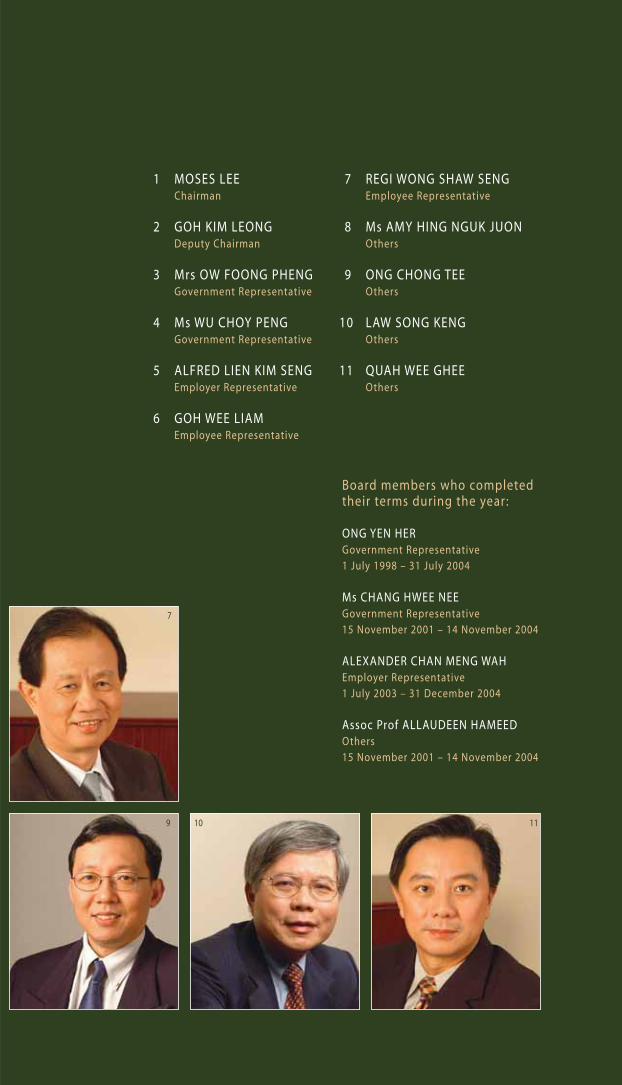

Board Members

8

65

432

1

11Running Head

1 MOSES LEE Chairman

2 GOH KIM LEONG Deputy Chairman

3 Mrs OW FOONG PHENG Government Representative

4 Ms WU CHOY PENG Government Representative

5 ALFRED LIEN KIM SENG Employer Representative

6 GOH WEE LIAM Employee Representative

1110

7

9

7 REGI WONG SHAW SENG Employee Representative

8 Ms AMY HING NGUK JUON Others

9 ONG CHONG TEE Others

10 LAW SONG KENG Others

11 QUAH WEE GHEE Others

Board members who completed their terms during the year :

ONG YEN HER Government Representative1 July 1998 – 31 July 2004

Ms CHANG HWEE NEEGovernment Representative15 November 2001 – 14 November 2004

ALEXANDER CHAN MENG WAHEmployer Representative1 July 2003 – 31 December 2004

Assoc Prof ALLAUDEEN HAMEEDOthers15 November 2001 – 14 November 2004

12 Central Provident Fund Board | Annual Report 200412 Central Provident Fund Board | Annual Report 2004

Senior Management

1 (from left) TAN YOKE MENG WILLIE Chief Executive Officer

WU WAI MUN Deputy Chief Executive Officer

(Policy and Corporate Support Group)

LEONG LICK TIEN Deputy Chief Executive Officer (Services Group)

1

13

2 (from left) CHANG LONG KIAT Director (Corporate Affairs)

GOH TECK SOON Director (Infocomm Technology Services)

LIM BOON CHYE Director (Policy and Planning)

3 (from left) TEOH SEE LEONG Director (Housing and Healthcare)

SOH CHIN HENG Director (Retirement and Investment)

4 (from left) NG HOCK KEONG Director (Customer Relations)

LO TAK WAH Director (Collections and Recovery)

4

32

Senior Management

14 Central Provident Fund Board | Annual Report 2004

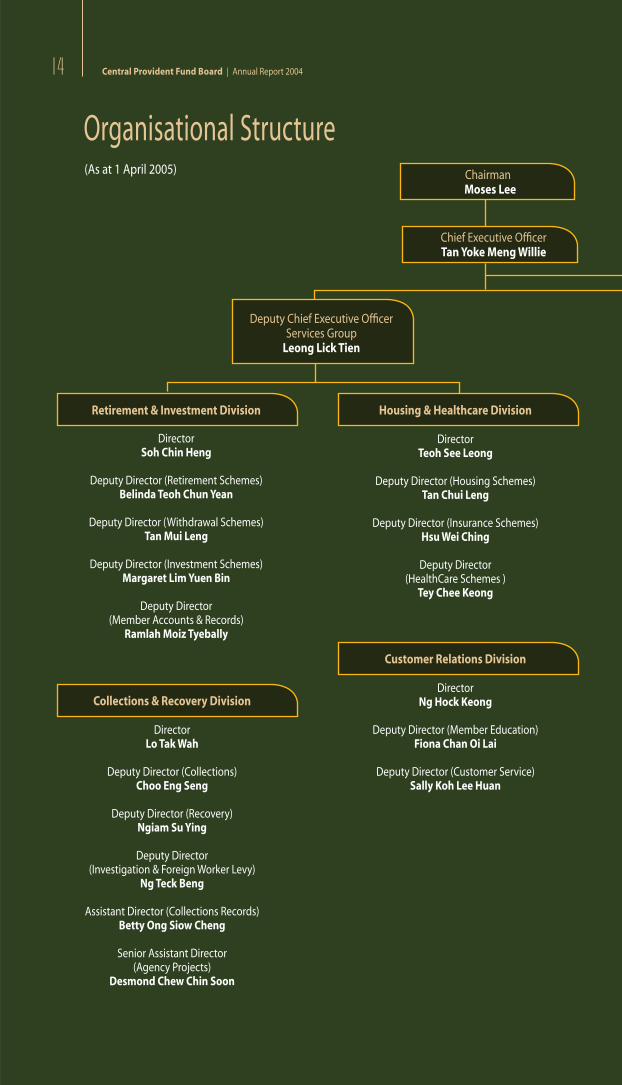

Organisational Structure(As at 1 April 2005)

14 Central Provident Fund Board | Annual Report 2004

Chairman Moses Lee

Chief Executive Offi cerTan Yoke Meng Willie

Deputy Chief Executive Offi cerServices Group

Leong Lick Tien

Retirement & Investment Division

DirectorSoh Chin Heng

Deputy Director (Retirement Schemes)Belinda Teoh Chun Yean

Deputy Director (Withdrawal Schemes)Tan Mui Leng

Deputy Director (Investment Schemes)Margaret Lim Yuen Bin

Deputy Director (Member Accounts & Records)

Ramlah Moiz Tyebally

Housing & Healthcare Division

DirectorTeoh See Leong

Deputy Director (Housing Schemes)Tan Chui Leng

Deputy Director (Insurance Schemes)Hsu Wei Ching

Deputy Director (HealthCare Schemes )

Tey Chee Keong

Collections & Recovery Division

DirectorLo Tak Wah

Deputy Director (Collections)Choo Eng Seng

Deputy Director (Recovery)Ngiam Su Ying

Deputy Director (Investigation & Foreign Worker Levy)

Ng Teck Beng

Assistant Director (Collections Records)Betty Ong Siow Cheng

Senior Assistant Director (Agency Projects)

Desmond Chew Chin Soon

Customer Relations Division

DirectorNg Hock Keong

Deputy Director (Member Education)Fiona Chan Oi Lai

Deputy Director (Customer Service)Sally Koh Lee Huan

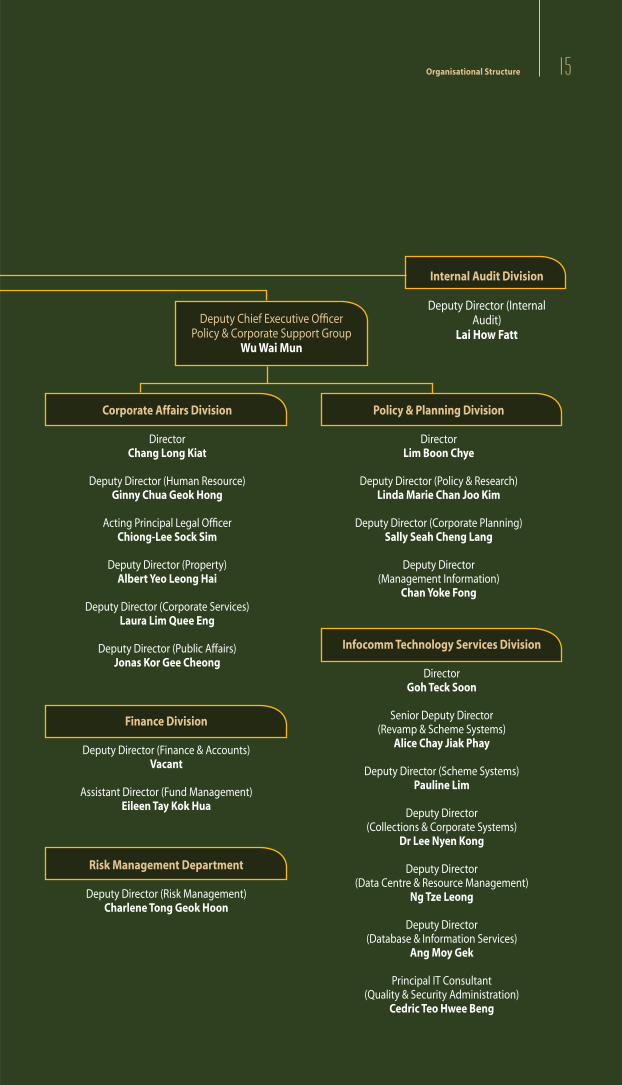

15Organisational Structure 15

Internal Audit Division

Deputy Director (Internal Audit)

Lai How FattDeputy Chief Executive Offi cer

Policy & Corporate Support GroupWu Wai Mun

Corporate Affairs Division

DirectorChang Long Kiat

Deputy Director (Human Resource)Ginny Chua Geok Hong

Acting Principal Legal Offi cerChiong-Lee Sock Sim

Deputy Director (Property)Albert Yeo Leong Hai

Deputy Director (Corporate Services)Laura Lim Quee Eng

Deputy Director (Public Affairs)Jonas Kor Gee Cheong

Infocomm Technology Services Division

DirectorGoh Teck Soon

Senior Deputy Director (Revamp & Scheme Systems)

Alice Chay Jiak Phay

Deputy Director (Scheme Systems)Pauline Lim

Deputy Director (Collections & Corporate Systems)

Dr Lee Nyen Kong

Deputy Director (Data Centre & Resource Management)

Ng Tze Leong

Deputy Director (Database & Information Services)

Ang Moy Gek

Principal IT Consultant (Quality & Security Administration)

Cedric Teo Hwee Beng

Policy & Planning Division

DirectorLim Boon Chye

Deputy Director (Policy & Research)Linda Marie Chan Joo Kim

Deputy Director (Corporate Planning)Sally Seah Cheng Lang

Deputy Director (Management Information)

Chan Yoke Fong

Finance Division

Deputy Director (Finance & Accounts)Vacant

Assistant Director (Fund Management)Eileen Tay Kok Hua

Risk Management Department

Deputy Director (Risk Management)Charlene Tong Geok Hoon

This page is intentionally left blank

17Review of Operations

Review of Operations

18 Central Provident Fund Board | Annual Report 2004

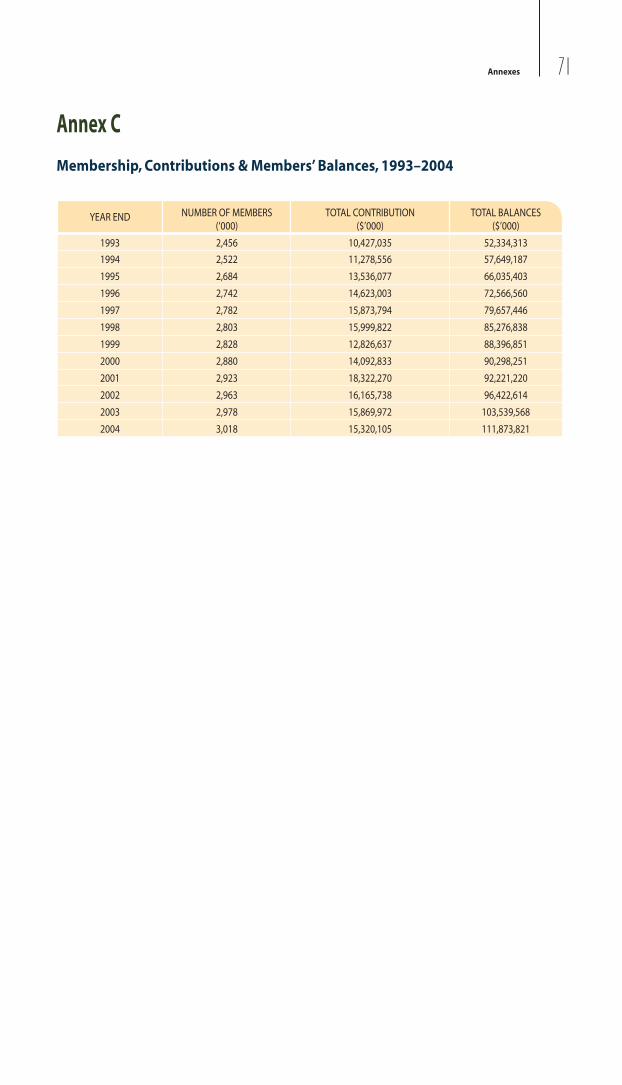

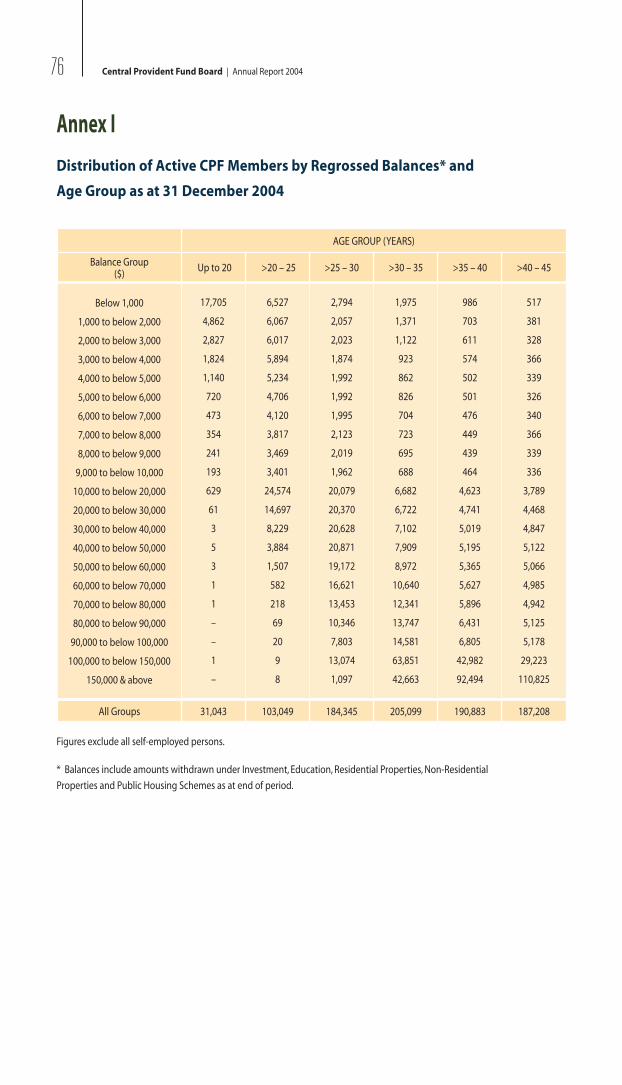

Membership

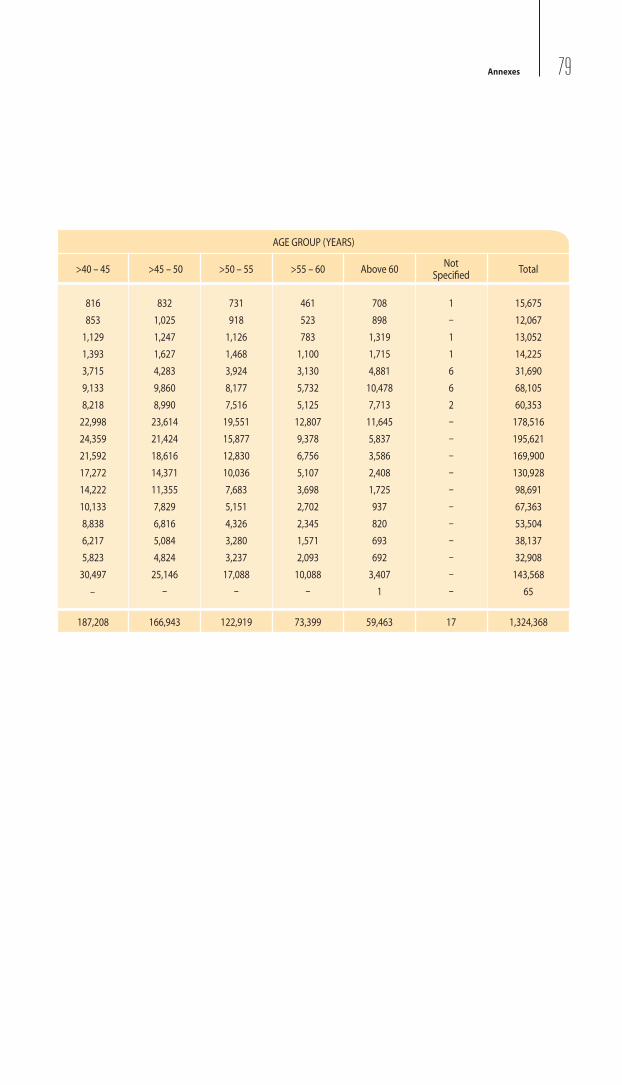

In 2004, CPF membership rose by 1.3% to 3,018,014 as at 31 December

2004. Of this number, 1,324,368 were active members.

Members’ Balance

Total members’ balance grew by 8%, from $103,539.6 million in 2003 to

$111,873.8 million in 2004.

Membership as at 31 December

2004 3,018,014

2003 2,978,493

2002 2,963,160

2001 2,922,673

2000 2,879,956

Members’ Balance as at 31 December

2004 $111,873.8 m

2003 $103,539.6 m

2002 $96,422.6 m

2001 $92,221.2 m

2000 $90,298.3 m

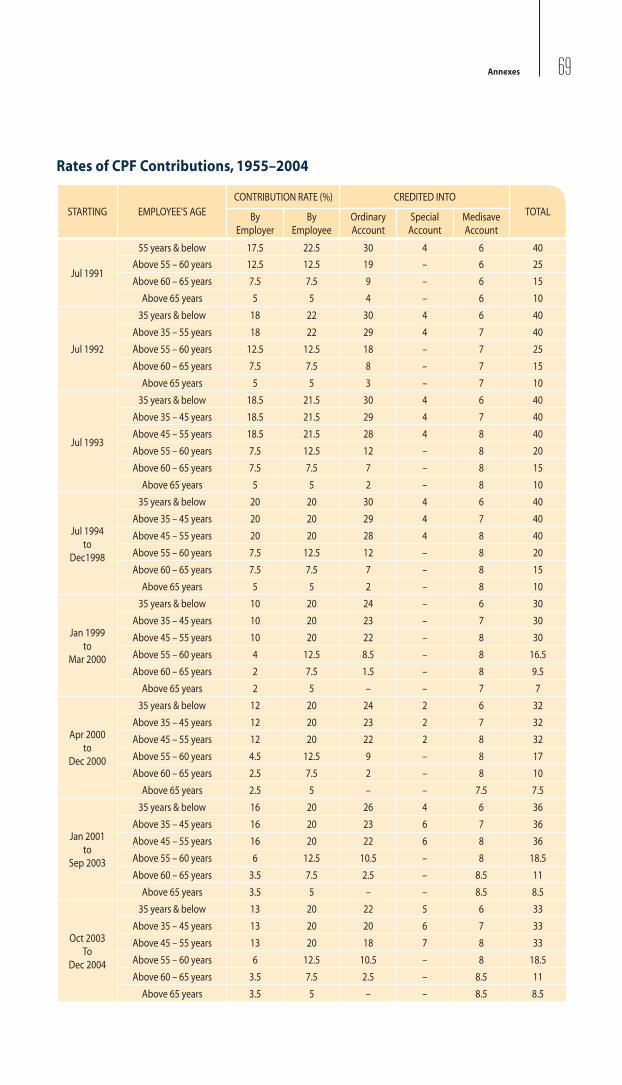

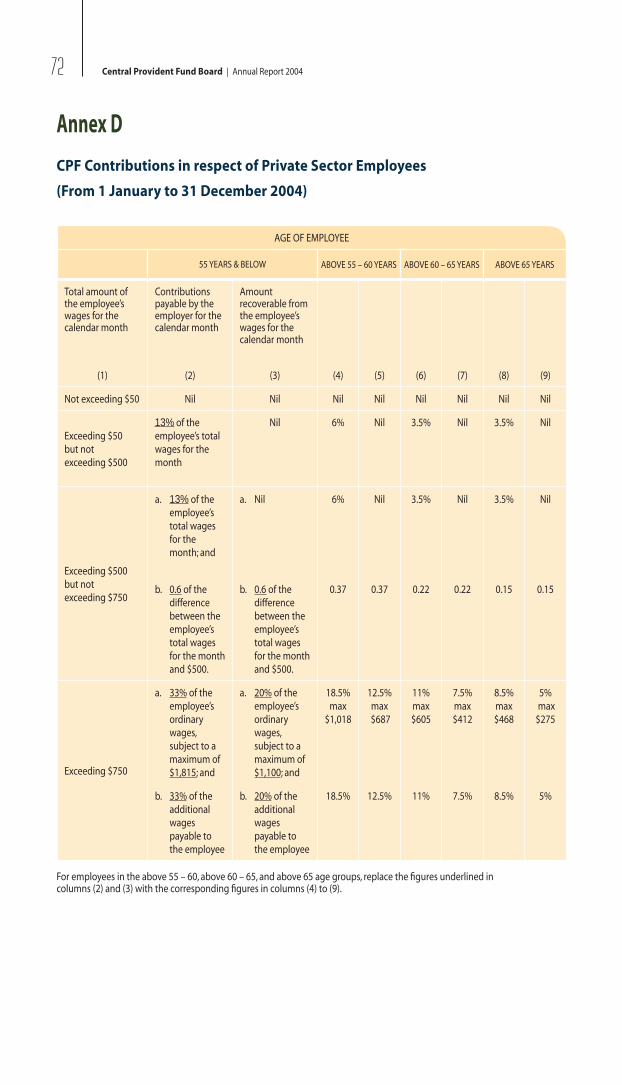

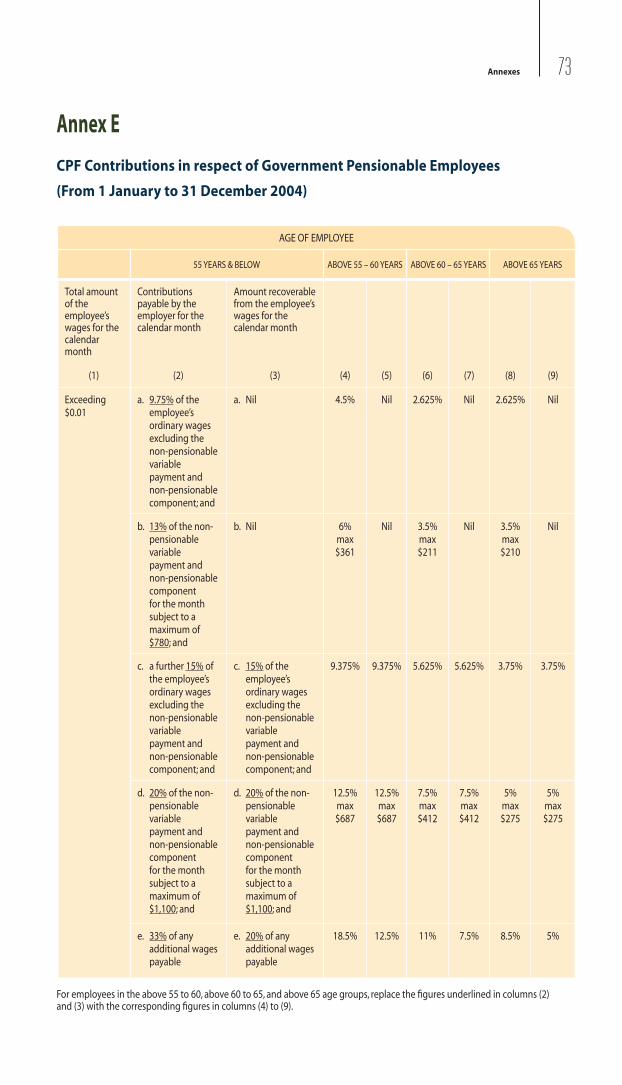

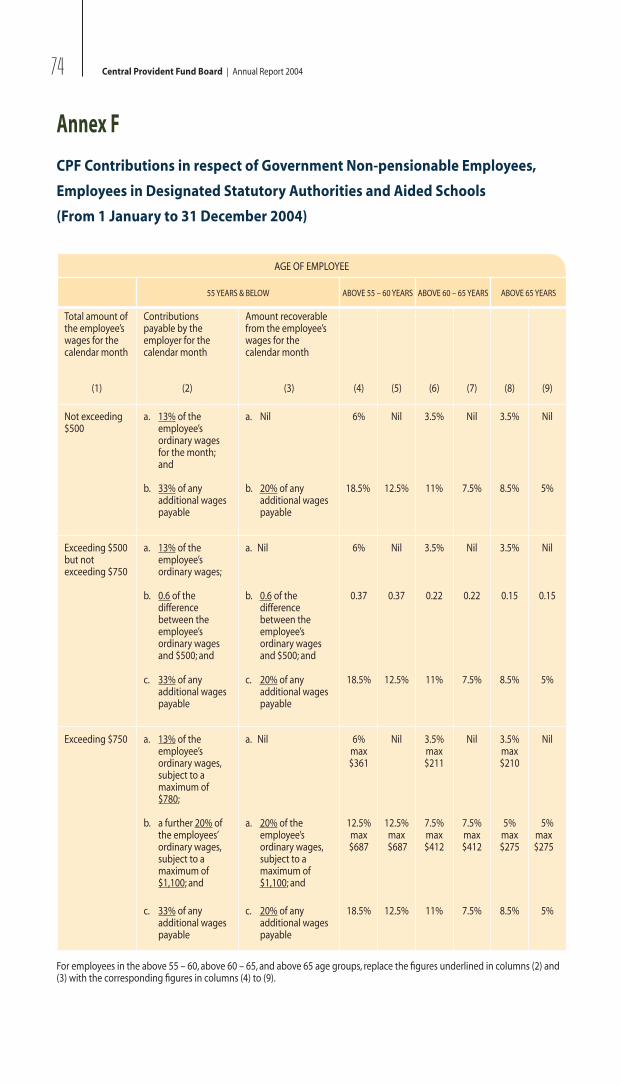

CPF Contribution Rates

The CPF wage bands were revised from 1 October 2002, with the intent

to help the lower-income members increase their take-home pay. Now,

employees who earn more than $500 per month need to contribute

to their CPF accounts. For employers, CPF contributions are payable for

employees whose wages exceed $50 a month.

The maximum monthly contribution payable for all age groups in 2004

is based on a salary ceiling of $5,500 a month.

Members’ Accounts

A CPF member maintains three accounts with the Board – Ordinary,

Medisave and Special Accounts. At age 55, he also has a Retirement

Account under the Minimum Sum Scheme.

19Review of Operations

The allocation of CPF contributions to members’ accounts is as follows.

ALLOCATION OF CPF CONTRIBUTIONS

FROM 1 JANUARY TO 31 DECEMBER 2004

Age groupOrdinary

Account (%)Special

Account (%)Medisave

Account (%)Total (%)

35 years & below 22 5 6 33

Above 35–45 years 20 6 7 33

Above 45–55 years 18 7 8 33

Above 55–60 years 10.5 – 8 18.5

Above 60–65 years 2.5 – 8.5 11

Above 65 years – – 8.5 8.5

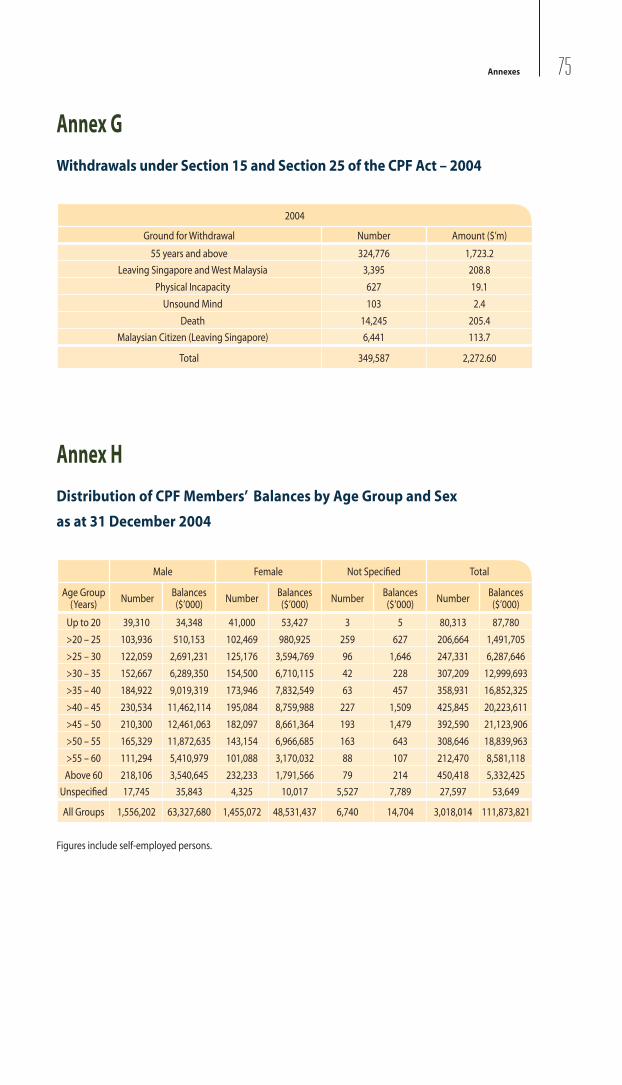

Contributions amounting to $15,320.1 million were collected and credited

into members’ accounts during the year. Withdrawals from members’

balances totalled $10,310.3 million in 2004, compared to $11,816.5 million

in the previous year.

Contributions Received

2004 $15,320.1 m

2003 $15,870.0 m

2002 $16,165.7 m

2001 $18,322.3 m

2000 $14,092.8 m

Annual Withdrawals*

2004 $10,310.3 m

2003 $11,816.5 m

2002 $14,821.4 m

2001 $18,860.4 m

2000 $14,555.9 m

* Include withdrawals under Section 15 & CPF schemes

21Review of Operations

In 2004, 48,858 members were brought into the Minimum Sum

Scheme. Of these, 2,989 bought annuities, 19,231 pledged their properties

and 13,988 left their Minimum Sum either with banks or the Board. The

remaining 12,650 were members who had no Minimum Sum to set aside

as they had small balances, and those who were exempted from the

scheme because they were terminally ill, had passed away, had their own

annuities, had left the country permanently or were pensioners in receipt

of a monthly pension.

Topping-Up of the Minimum Sum

The topping-up of the Minimum Sum gives individuals the opportunity

to top up their own, their spouses’ and their parents’ Retirement Accounts.

Accounts can be topped up with cash or transfers of CPF savings. Individuals

can also top up their grandparents’ accounts using cash.

In 2004, 2,880 individuals made cash and CPF top-ups amounting to

$21.21 million.

Withdrawals upon Death, Permanent Disability

and Other Grounds

Upon a member’s death, his savings will be paid to his nominated

benefi ciaries. If no nomination was made, the savings will be handed to

the Public Trustee for distribution according to the law. Members who

become permanently disabled can apply to withdraw their CPF savings at

any time. During the year, $226.9 million was withdrawn on these grounds.

Members who left Singapore and West Malaysia permanently withdrew

$322.5 million.

Transfer of Ordinary Account Savings to Special Account

CPF members below age 55 who want to put aside more cash for old age

can transfer their CPF savings from the Ordinary Account to the Special

Account up to a limit of $84,500, which is the prevailing Minimum Sum.

The transfer is irreversible. With the transfer, CPF members will enjoy a

higher interest rate paid on their CPF savings in the Special Account,

which is currently 4%. In 2004, 15,503 CPF members transferred/topped-up

$158.1 million into to their Special Accounts.

22 Central Provident Fund Board | Annual Report 2004

Retirement Planning

To encourage members to plan early for their retirement, the Board

launched “my cpf” at www.cpf.gov.sg. ”my cpf” is a comprehensive guide

for members to help them plan for their CPF savings at different life stages

such as Starting Work, Buying a House and Reaching 55.

The Board organised its fi rst ”my cpf & me” road show and retirement

planning seminar at the HDB Hub. It drew more than 50,000 members.

The public gave positive feedback and affi rmed that such events are

useful channels to obtain information in helping them plan for their

old age.

The event also marked the launch of the CPF Retirement Planner and

Housing Site. The Retirement Planner is an online tool that helps members

assess their fi nancial situation, determines their current savings adequacy

and provides suggestions on how to reach their goals. The Housing Site

provides housing-related information and useful calculators to guide

members in making prudent fi nancial decisions when buying their dream

home.

HEALTHCARE

Medisave, MediShield and MediShield Plus help CPF members and their

dependants pay for hospitalisation expenses. Prudent use of savings

in the Medisave Account, coupled with a catastrophic illness insurance

scheme such as MediShield, will go a long way towards meeting members’

healthcare needs.

Medisave

From 1 July 2004, members are required to maintain up to $30,500 in

their Medisave Account. Those who withdraw their savings at age 55 need

to set aside $25,500 or the actual Medisave balance, whichever is lower,

in their Medisave Account to meet healthcare needs during retirement.

Members who are government pensioners under the Fixed Amount

on Ward Charges scheme (FAW) are not required to maintain any savings

in the Medisave Account whereas government pensioners under the Co-

Payment on Ward Charges scheme (CPW) are required to maintain up to

$15,250 in their Medisave Account. They have to set aside $12,750 in their

Medisave Account when they withdraw their savings at age 55.

23Review of Operations

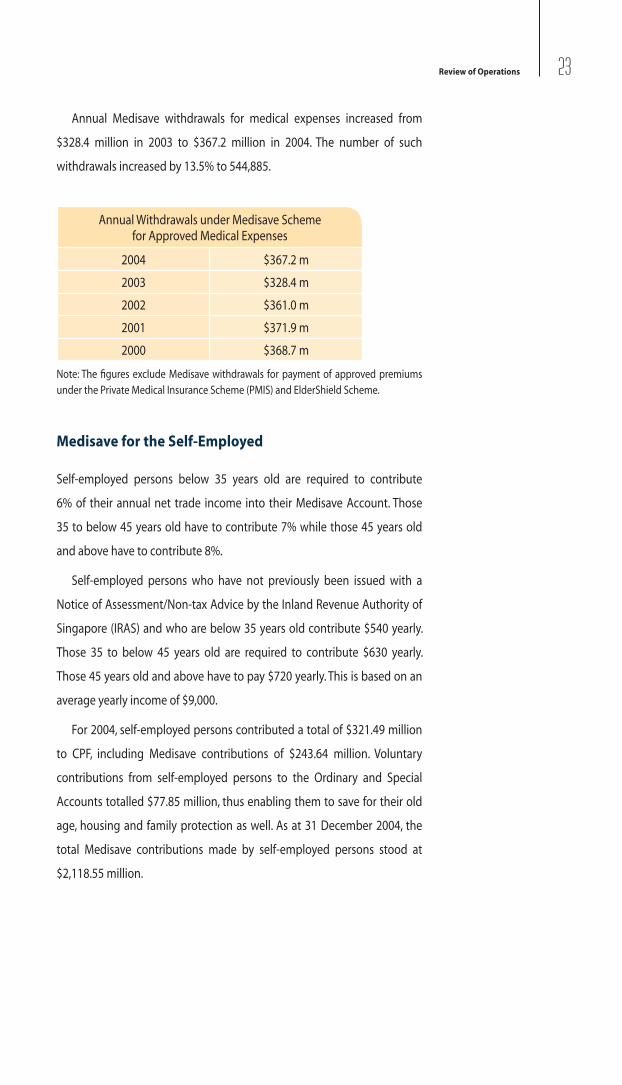

Annual Medisave withdrawals for medical expenses increased from

$328.4 million in 2003 to $367.2 million in 2004. The number of such

withdrawals increased by 13.5% to 544,885.

Annual Withdrawals under Medisave Scheme for Approved Medical Expenses

2004 $367.2 m

2003 $328.4 m

2002 $361.0 m

2001 $371.9 m

2000 $368.7 m

Note: The fi gures exclude Medisave withdrawals for payment of approved premiums under the Private Medical Insurance Scheme (PMIS) and ElderShield Scheme.

Medisave for the Self-Employed

Self-employed persons below 35 years old are required to contribute

6% of their annual net trade income into their Medisave Account. Those

35 to below 45 years old have to contribute 7% while those 45 years old

and above have to contribute 8%.

Self-employed persons who have not previously been issued with a

Notice of Assessment/Non-tax Advice by the Inland Revenue Authority of

Singapore (IRAS) and who are below 35 years old contribute $540 yearly.

Those 35 to below 45 years old are required to contribute $630 yearly.

Those 45 years old and above have to pay $720 yearly. This is based on an

average yearly income of $9,000.

For 2004, self-employed persons contributed a total of $321.49 million

to CPF, including Medisave contributions of $243.64 million. Voluntary

contributions from self-employed persons to the Ordinary and Special

Accounts totalled $77.85 million, thus enabling them to save for their old

age, housing and family protection as well. As at 31 December 2004, the

total Medisave contributions made by self-employed persons stood at

$2,118.55 million.

24 Central Provident Fund Board | Annual Report 2004

Percentage of Employees* who have the Required Medisave Balance at Age 55

2004 57.5%

2003 54.6%

2002 54.7%

2001 55.2%

2000 56.0%

*Excludes pensioners and self-employed persons

Average Balance in the Medisave Accounts of Employees* at Age 55

2004 $22,292

2003 $20,512

2002 $18,983

2001 $17,842

2000 $16,059

*Excludes pensioners and self-employed persons

MediShield and MediShield Plus

MediShield, the low-cost national catastrophic illness insurance scheme,

provides members and their dependants with fi nancial protection

against high medical expenses arising from prolonged or serious illnesses.

MediShield Plus is also available for members who want a higher coverage

than MediShield and is designed to meet a signifi cant portion of the

higher hospital charges of Class A or B1 wards. It works in the same way as

MediShield and has two plans – Plan A and Plan B. Premiums for MediShield

and MediShield Plus can be paid from the Medisave Account, subject to a

maximum of $660 per insured person per policy year.

Those who have been insured continuously under any of the MediShield

plans since age 60 or earlier will enjoy a discount on their premiums from

ages 71 to 75. Depending on how long a person remains insured and the

type of plan he is under, he will enjoy yearly premium discounts ranging

from $20.40 to $480.

25Review of Operations

For MediShield, the annual premiums are between $12 and $390,

depending on the insured’s age. The annual claim limit is $30,000 with a

lifetime claim limit of $120,000.

As at 31 December 2004, 1,294,894 CPF members and dependants

were covered under MediShield. During the year, $70.1 million was

approved to meet 101, 894 claims.

For MediShield Plus Plan A, the annual premiums are between $60

and $1,950. The annual claim limit is $100,000 with a lifetime claim limit

of $300,000. For Plan B, the annual premiums are between $36 and $1,170

with an annual claim limit of $75,000 and lifetime claim limit of $225,000.

As at 31 December 2004, 337,293 CPF members and their dependants

were covered under MediShield Plus. In 2004, $16.7 million was paid out to

meet 13,258 claims.

HOME OWNERSHIP

CPF members are able to own their own home with the help of the Public

Housing Scheme and the Residential Properties Scheme.

Public Housing Scheme

The Public Housing Scheme allows members to use their CPF savings

to buy HDB fl ats and to pay their housing instalments. During the year,

$5,254.3 million was withdrawn by 655,239 members to pay for their HDB

fl ats and to service their HDB housing loans. Since January 2003, members

were allowed to obtain loans from banks to purchase HDB fl ats. In the year

2004, 69,096 members used $1,537.8 million of their CPF to service the

bank loans or to buy HDB fl ats fi nanced with bank loans.

From 1 January 2004, the CPF Withdrawal Limit for members using CPF

to service their bank loan was 144% of the Valuation Limit subject to

suffi cient Available Housing Withdrawal Limit. The CPF Withdrawal Limit

will be reduced to 138% for those who buy their fl at or refi nance from

HDB loan to bank loan with effect from 1 January 2005. This limit will be

further reduced by six percentage points every year until it reaches 120%

in year 2008.

26 Central Provident Fund Board | Annual Report 2004

Residential Properties Scheme

Under the Residential Properties Scheme, members can use their CPF

savings to buy private residential properties and executive condominiums,

and to pay their housing loan instalments. The CPF Withdrawal Limit for

new purchases or loan refi nanced on or after 1 January 2004 was 144%

of the Valuation Limit subject to suffi cient Available Housing Withdrawal

Limit. This limit will be further reduced by six percentage points every year

until it reaches 120% in year 2008.

The number of applications increased by 1.6% to 9,815 in 2004. In 2004,

a gross amount of $3,246.0 million was withdrawn under the scheme, an

increase of 5.8% over 2003’s fi gure.

Use of Special Account Savings

for Housing Instalments

Arising from the cut in the CPF contribution to the Ordinary Account

(OA) from October 2003, members whose housing loan was affected

were allowed to make up for the shortfall by using their Special Account

(SA) to service their housing loan. A higher SA withdrawal limit was set

for members who were allowed to use their SA to top up their monthly

housing payments. This higher SA withdrawal limit was the combination

of the limit allowed in 1999 plus the new limit resulting from the

additional CPF cut to the OA. As at 31 December 2004, 178,350 members

had used $279.5 million from SA savings to pay for their housing loan

instalments.

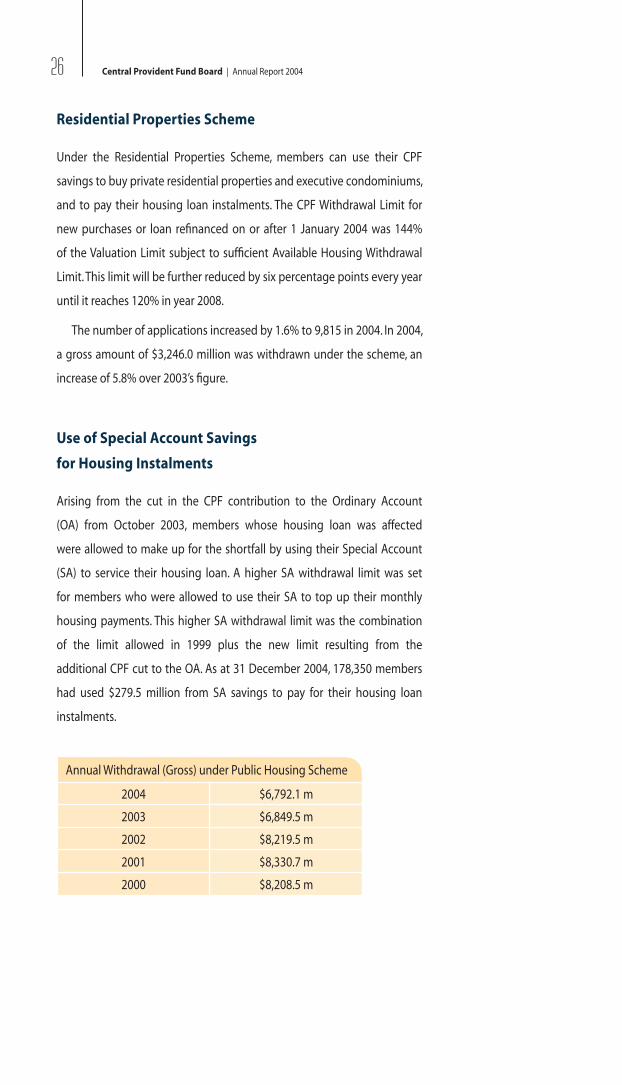

Annual Withdrawal (Gross) under Public Housing Scheme

2004 $6,792.1 m

2003 $6,849.5 m

2002 $8,219.5 m

2001 $8,330.7 m

2000 $8,208.5 m

27Review of Operations

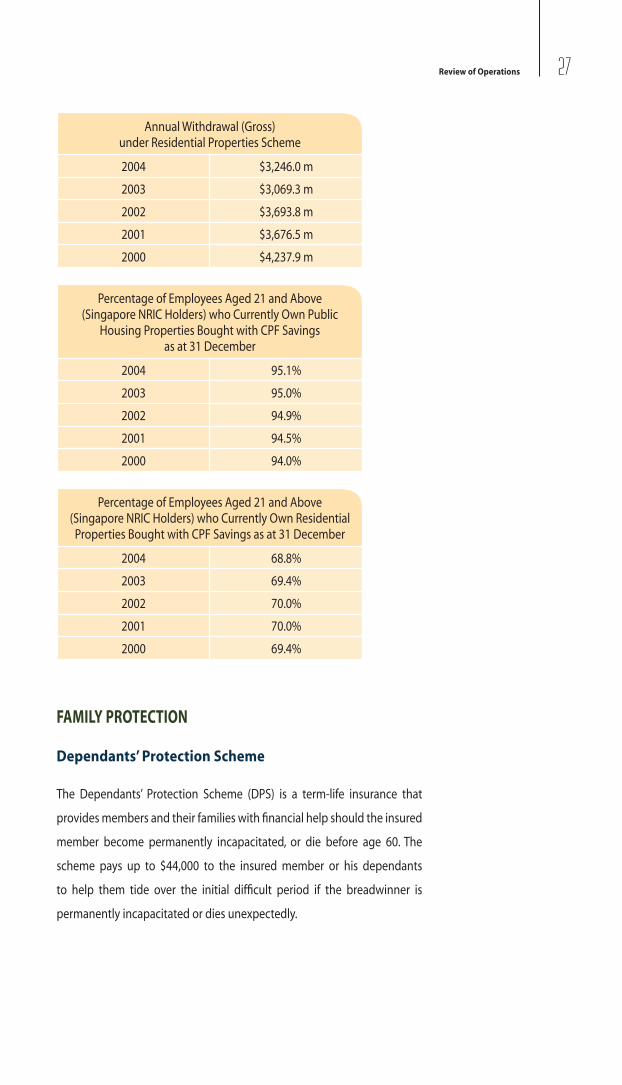

Annual Withdrawal (Gross) under Residential Properties Scheme

2004 $3,246.0 m

2003 $3,069.3 m

2002 $3,693.8 m

2001 $3,676.5 m

2000 $4,237.9 m

Percentage of Employees Aged 21 and Above (Singapore NRIC Holders) who Currently Own Public

Housing Properties Bought with CPF Savings as at 31 December

2004 95.1%

2003 95.0%

2002 94.9%

2001 94.5%

2000 94.0%

Percentage of Employees Aged 21 and Above (Singapore NRIC Holders) who Currently Own Residential Properties Bought with CPF Savings as at 31 December

2004 68.8%

2003 69.4%

2002 70.0%

2001 70.0%

2000 69.4%

FAMILY PROTECTION

Dependants’ Protection Scheme

The Dependants’ Protection Scheme (DPS) is a term-life insurance that

provides members and their families with fi nancial help should the insured

member become permanently incapacitated, or die before age 60. The

scheme pays up to $44,000 to the insured member or his dependants

to help them tide over the initial diffi cult period if the breadwinner is

permanently incapacitated or dies unexpectedly.

28 Central Provident Fund Board | Annual Report 2004

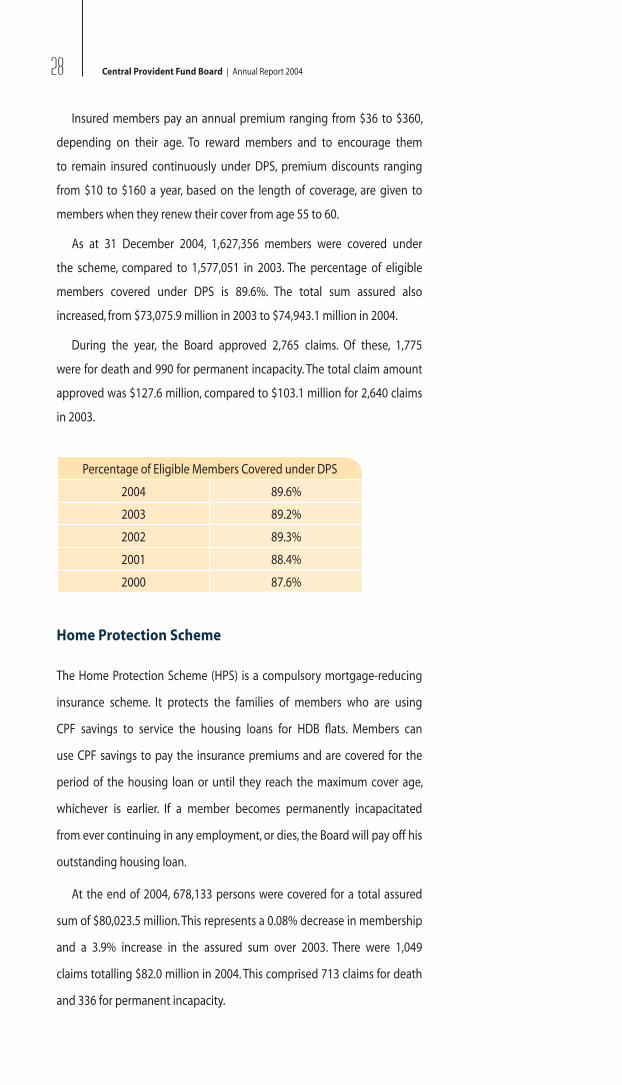

Insured members pay an annual premium ranging from $36 to $360,

depending on their age. To reward members and to encourage them

to remain insured continuously under DPS, premium discounts ranging

from $10 to $160 a year, based on the length of coverage, are given to

members when they renew their cover from age 55 to 60.

As at 31 December 2004, 1,627,356 members were covered under

the scheme, compared to 1,577,051 in 2003. The percentage of eligible

members covered under DPS is 89.6%. The total sum assured also

increased, from $73,075.9 million in 2003 to $74,943.1 million in 2004.

During the year, the Board approved 2,765 claims. Of these, 1,775

were for death and 990 for permanent incapacity. The total claim amount

approved was $127.6 million, compared to $103.1 million for 2,640 claims

in 2003.

Percentage of Eligible Members Covered under DPS

2004 89.6%

2003 89.2%

2002 89.3%

2001 88.4%

2000 87.6%

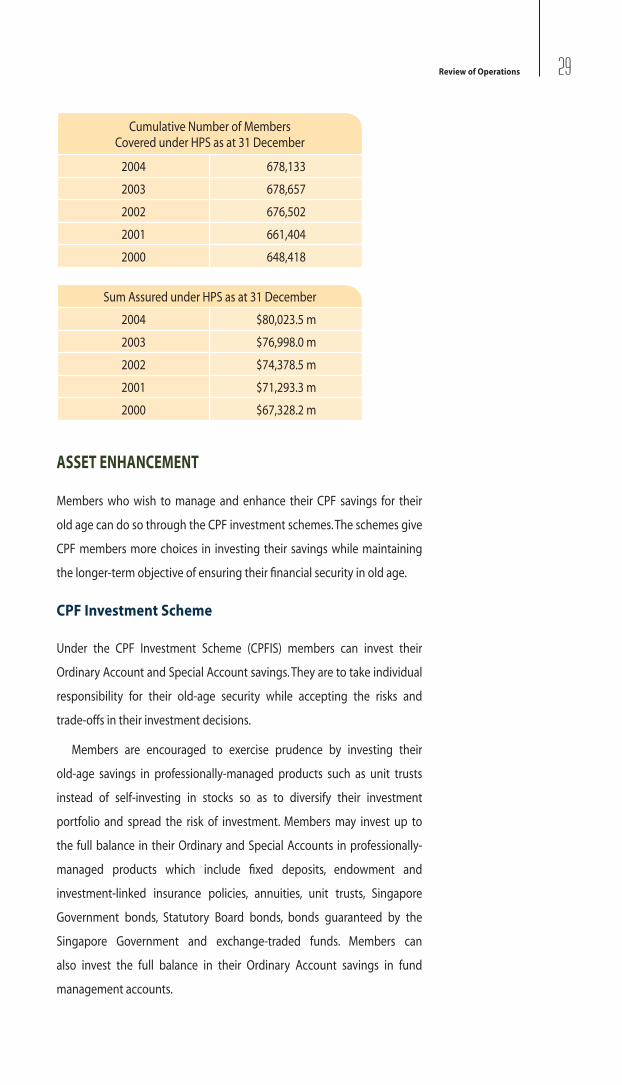

Home Protection Scheme

The Home Protection Scheme (HPS) is a compulsory mortgage-reducing

insurance scheme. It protects the families of members who are using

CPF savings to service the housing loans for HDB fl ats. Members can

use CPF savings to pay the insurance premiums and are covered for the

period of the housing loan or until they reach the maximum cover age,

whichever is earlier. If a member becomes permanently incapacitated

from ever continuing in any employment, or dies, the Board will pay off his

outstanding housing loan.

At the end of 2004, 678,133 persons were covered for a total assured

sum of $80,023.5 million. This represents a 0.08% decrease in membership

and a 3.9% increase in the assured sum over 2003. There were 1,049

claims totalling $82.0 million in 2004. This comprised 713 claims for death

and 336 for permanent incapacity.

29Review of Operations

Cumulative Number of Members Covered under HPS as at 31 December

2004 678,133

2003 678,657

2002 676,502

2001 661,404

2000 648,418

Sum Assured under HPS as at 31 December

2004 $80,023.5 m

2003 $76,998.0 m

2002 $74,378.5 m

2001 $71,293.3 m

2000 $67,328.2 m

ASSET ENHANCEMENT

Members who wish to manage and enhance their CPF savings for their

old age can do so through the CPF investment schemes. The schemes give

CPF members more choices in investing their savings while maintaining

the longer-term objective of ensuring their fi nancial security in old age.

CPF Investment Scheme

Under the CPF Investment Scheme (CPFIS) members can invest their

Ordinary Account and Special Account savings. They are to take individual

responsibility for their old-age security while accepting the risks and

trade-offs in their investment decisions.

Members are encouraged to exercise prudence by investing their

old-age savings in professionally-managed products such as unit trusts

instead of self-investing in stocks so as to diversify their investment

portfolio and spread the risk of investment. Members may invest up to

the full balance in their Ordinary and Special Accounts in professionally-

managed products which include fi xed deposits, endowment and

investment-linked insurance policies, annuities, unit trusts, Singapore

Government bonds, Statutory Board bonds, bonds guaranteed by the

Singapore Government and exchange-traded funds. Members can

also invest the full balance in their Ordinary Account savings in fund

management accounts.

30 Central Provident Fund Board | Annual Report 2004

Under CPFIS-Ordinary Account (CPFIS-OA), members can invest up to

35% of investible savings in shares, corporate bonds and property funds,

while 10% can be invested in gold. Investible savings is defi ned as the

Ordinary Account balance plus net amounts withdrawn for education and

investments.

As at 31 December 2004, 741,679 members had invested a gross

amount of $24,126.3 million of their CPF savings under the CPFIS-OA and

432,965 members had invested $4,628.6 million of their CPF savings under

the CPFIS-SA.

NON-RESIDENTIAL PROPERTIES SCHEME

The Non-Residential Properties Scheme enables members to enhance

their CPF savings by investing them in non-residential properties. In 2004,

a gross amount of $54.2 million was withdrawn under the scheme, an

increase of 7.3% from 2003.

Education Scheme

The Education Scheme is basically a loan scheme to help CPF members

fi nance their children’s or their own tertiary education. The scheme covers

all full-time undergraduate courses at the National University of Singapore,

Nanyang Technological University and Singapore Management University,

and all full-time diploma courses at LaSalle-SIA College of the Arts, Nanyang

Academy of Fine Arts, Nanyang Polytechnic, Ngee Ann Polytechnic, Republic

Polytechnic, Singapore Polytechnic and Temasek Polytechnic.

During the year, 13,071 applications were processed under the scheme,

an increase of 0.5% from 2003. The gross amount withdrawn (tuition and

administrative fees) increased from $91.2 million in 2003 to $95.3 million in

2004. The total amount repaid was $47.5 million.

MEMBERSHIP PRIVILEGES

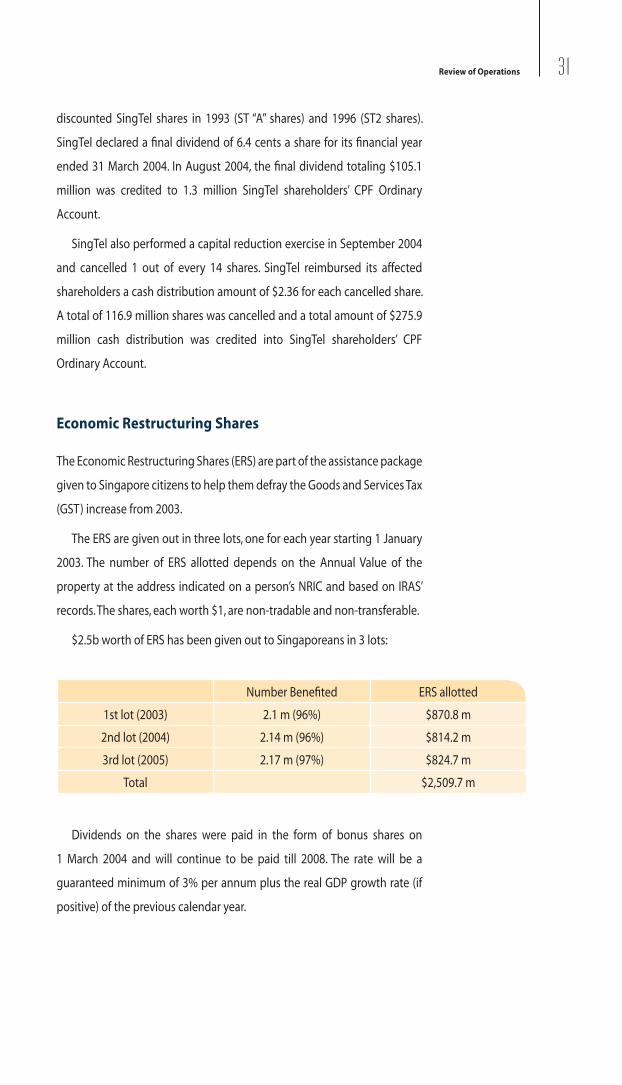

Discounted SingTel Shares

To make Singapore a share-owning society and give Singaporeans a

greater stake in the country, Singaporean CPF members were able to buy

31Review of Operations

discounted SingTel shares in 1993 (ST “A” shares) and 1996 (ST2 shares).

SingTel declared a fi nal dividend of 6.4 cents a share for its fi nancial year

ended 31 March 2004. In August 2004, the fi nal dividend totaling $105.1

million was credited to 1.3 million SingTel shareholders’ CPF Ordinary

Account.

SingTel also performed a capital reduction exercise in September 2004

and cancelled 1 out of every 14 shares. SingTel reimbursed its affected

shareholders a cash distribution amount of $2.36 for each cancelled share.

A total of 116.9 million shares was cancelled and a total amount of $275.9

million cash distribution was credited into SingTel shareholders’ CPF

Ordinary Account.

Economic Restructuring Shares

The Economic Restructuring Shares (ERS) are part of the assistance package

given to Singapore citizens to help them defray the Goods and Services Tax

(GST) increase from 2003.

The ERS are given out in three lots, one for each year starting 1 January

2003. The number of ERS allotted depends on the Annual Value of the

property at the address indicated on a person’s NRIC and based on IRAS’

records. The shares, each worth $1, are non-tradable and non-transferable.

$2.5b worth of ERS has been given out to Singaporeans in 3 lots:

Number Benefi ted ERS allotted

1st lot (2003) 2.1 m (96%) $870.8 m

2nd lot (2004) 2.14 m (96%) $814.2 m

3rd lot (2005) 2.17 m (97%) $824.7 m

Total $2,509.7 m

Dividends on the shares were paid in the form of bonus shares on

1 March 2004 and will continue to be paid till 2008. The rate will be a

guaranteed minimum of 3% per annum plus the real GDP growth rate (if

positive) of the previous calendar year.

32 Central Provident Fund Board | Annual Report 2004

CPF SERVICES

CPF PAL-Internet

2004 saw more new e-services being offered to members under the CPF

PAL-Internet. “My Statement” shows members their CPF balance in a single,

easy-to-read consolidated page that makes checking the statement a

breeze. “My Requests” is a step-by-step guide to help members fi nd and

complete the right online application form. “My Activities” tracks the status

of members’ online applications. Lastly, “My Messages” shows a member’s

participation in the various CPF schemes.

To assist members in the use of “my cpf” Online Services, an Online

Demo service was implemented in October 2004 on the CPF website. This

video clip gives members a guided view of what they can expect in the

online service.

Other online tools implemented last year are the intelligent search

facility, “Ask Us”, and the Retirement Planner.

In 2004, PAL-Internet received over 9 million hits. The number of

transactions made was 13 million, an increase of more than 140% above

the 5.4 million transactions in 2003.

Electronic Services for Employers

Employers can submit the CPF contribution details electronically at their

convenience through the CPF PAL-Internet (Employer Returns) by stating

the contribution details in the online form or using a fi le transfer. For fi le

transfer, employers can simply extract contribution details from their

payroll software and submit these to the Board for processing through a

secured web page. Upon successful processing of the details submitted

by employers, the system will send employers a soft copy of the Record

of Payment (ROP). Employers can retrieve and fi le or print the electronic

ROP at their convenience. To use CPF PAL-Internet (Employer Returns), all

employers need is a SingPass and a GIRO facility. The service is available 24

hours a day, 7 days a week.

Alternatively, employers can also use the CPF/IRAS Line. The CPF/IRAS

Line enables businesses to submit their monthly CPF contribution details

33Review of Operations

and Goods and Services Tax returns electronically to the CPF Board and the

Inland Revenue Authority of Singapore respectively.

mPAL

The Mobile Personal Auto-Link (mPAL) allows employers with 10 or less

employees to submit CPF contributions via a GPRS (General Packet Radio

Service) mobile phone.

The mPAL is built on a wireless platform. Submissions are made over

a public network and data is encrypted end-to-end. All information

transmitted is secured and confi dential. Payment will be deducted via

GIRO when the submission is received.

Like PAL-Internet, mPAL is a generic platform that can eventually be

extended to other transactions for members, employers and self-employed

persons.

CPF E-Lobby, e-Counters and SingPass

CPF E-Lobbies, located in all CPF offi ces, feature automated self-service

e-counters that allow members to view and print their latest CPF statement

during offi ce hours. Members can also access other CPF services online at

the e-counters. All they need is their SingPass, an alphanumeric password

comprising a minimum of 8 and a maximum of 24 characters.

Should members require a new SingPass or forget their SingPass,

they can make use of the SingPass Online Request service available

on www.cpf.gov.sg or the SingPass Request Hotline (1800-327 1133), a

new service implemented in December 2004, to request for one. A new

SingPass will be posted to them within 5 working days.

Call Centre

The Board’s Call Centre received about 1.75 million calls from both

members and employers regarding CPF schemes and services in

2004. Over 350,000 calls concerned national projects such as the New

Singapore Shares and the Economic Restructuring Shares.

34 Central Provident Fund Board | Annual Report 2004

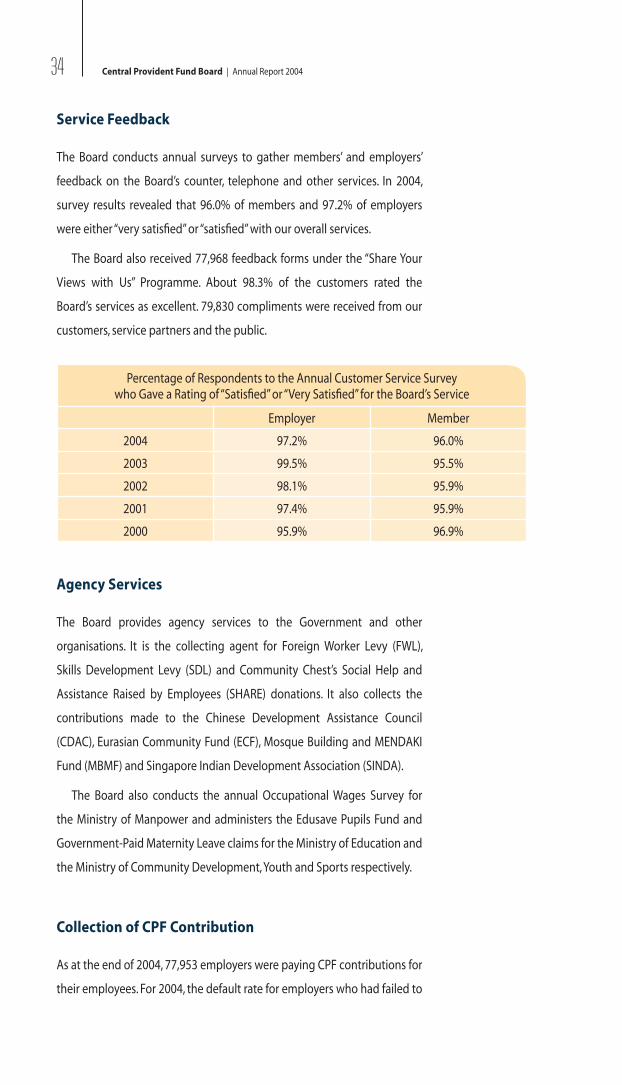

Service Feedback

The Board conducts annual surveys to gather members’ and employers’

feedback on the Board’s counter, telephone and other services. In 2004,

survey results revealed that 96.0% of members and 97.2% of employers

were either “very satisfi ed” or “satisfi ed” with our overall services.

The Board also received 77,968 feedback forms under the “Share Your

Views with Us” Programme. About 98.3% of the customers rated the

Board’s services as excellent. 79,830 compliments were received from our

customers, service partners and the public.

Percentage of Respondents to the Annual Customer Service Survey who Gave a Rating of “Satisfi ed” or “Very Satisfi ed” for the Board’s Service

Employer Member

2004 97.2% 96.0%

2003 99.5% 95.5%

2002 98.1% 95.9%

2001 97.4% 95.9%

2000 95.9% 96.9%

Agency Services

The Board provides agency services to the Government and other

organisations. It is the collecting agent for Foreign Worker Levy (FWL),

Skills Development Levy (SDL) and Community Chest’s Social Help and

Assistance Raised by Employees (SHARE) donations. It also collects the

contributions made to the Chinese Development Assistance Council

(CDAC), Eurasian Community Fund (ECF), Mosque Building and MENDAKI

Fund (MBMF) and Singapore Indian Development Association (SINDA).

The Board also conducts the annual Occupational Wages Survey for

the Ministry of Manpower and administers the Edusave Pupils Fund and

Government-Paid Maternity Leave claims for the Ministry of Education and

the Ministry of Community Development, Youth and Sports respectively.

Collection of CPF Contribution

As at the end of 2004, 77,953 employers were paying CPF contributions for

their employees. For 2004, the default rate for employers who had failed to

35Review of Operations

pay the monthly contributions on time continued to improve. It was 0.53%

compared to 0.61% in 2003.

CORPORATE CITIZENSHIP

In 2004, the Board continued to organise various charity events such as

Valentine’s Day Charity Rose Sale and Charity Jumble Sale to raise funds to

help the less fortunate. CPF staff continued to care for the residents of the

Society for the Aged Sick, the Board’s adopted home under its Community

Service Programme. Besides raising funds, the Board also organised regular

visits to the home to bring cheer to the residents.

On CPF’s Family Day, a group of underprivileged children from

Gracehaven Children’s Home were treated to a day of fun and laughter

with the Board’s staff and families. The Board also assisted charitable

organisations in recruiting volunteers in the sales of donation draw tickets.

Contributing to the community has become a way of life at the Board

as seen in active staff participation in the SHARE programme, winning

the Board, for the 12th time, the SHARE Programme Platinum Award. This

award was given out by Community Chest to acknowledge the Board’s

unstinting efforts.

Besides caring for the less fortunate, the Board continued to support

the national drive towards a “clean and green environment”. During the

year, 36,470 kg of paper was collected for recycling. CPF staff also

participated actively in the beach-cleaning activities organised by the

Board.

The Board recognises that a strong and healthy workforce is integral

to its success. For its strong support in promoting healthy lifestyle and

health programmes at the workplace, the Board received the Singapore

H.E.A.L.T.H. (Helping Employees Achieve Life-Time Health) Platinum Award

from the Health Promotion Board. This award is given to organisations that

have achieved the Gold Award for three or more consecutive years and

that have also demonstrated tangible results in their workplace health

promotion programmes.

36 Central Provident Fund Board | Annual Report 2004

ADMINISTRATION & FINANCE

SQA Winner 2004

The Board was awarded the Singapore Quality Award (SQA) on 21

September 2004. The SQA is the most prestigious award conferred on

organisations that have achieved the highest standards of business

excellence.

Effective leadership, innovative processes, excellent customer service

and a committed and engaged workforce are some of the factors that had

contributed to the Board’s success in winning the SQA in 2004.

Promotion of Innovation Programmes

The Board’s WITs (Work Improvement Teams) programme, which started in

1981, has remained active for the past 23 years. In 2004, there was 100%

participation in the Board’s WITs programme. The Board’s 136 WITS teams

completed an average of 5.01 projects per team.

Under the “My Ideas” scheme introduced in 1983, there was 100% staff

participation in 2004. Each staff member submitted an average of 9.4

ideas. The percentage of quality ideas (ideas accepted for implementation)

was 48%.

The CPF “WOW” Ideas Award was introduced in 2001 to encourage more

impactful and creative ideas from staff. In 2004, a total of 74 “WOW” ideas

were generated from staff – a 7.25% increase from 2003. Of these, four ideas

were shortlisted for presentation at the “WOW” Ideas Conference held in

October 2004.

In 2004, the CPFB Innovation Fund funded two projects for trial. Two

projects from 2003 were approved for implementation. These projects

benefi ted both employers and members.

Public Offi cers Working on Eliminating Red-tape (POWER), an initiative

by the civil service, was introduced in the Board in August 2001. A total of

125 rules were reviewed in 2004, of which 51 were improved or removed.

37Review of Operations

Staff Development

We encourage our staff to continuously upgrade their skills through the

numerous learning opportunities available in the Board. As an indicator of

our achievement in promoting life-long learning, the Board accomplished

an average of 118.41 training hours per staff in 2004.

Recognition for Staff Excellence

In 2004, 14 staff were presented with the Staff Excellence Award, in

recognition for their excellent overall performance and service to

customers. These prestigious awards were fi rst introduced in 1989 to

recognise outstanding frontline and non-frontline staff.

International Relations

The Board received more than 260 visitors from foreign national provident

funds, government bodies and private organisations in 2004.

CPFB is one of the founding members of the ASEAN Social Security

Association (ASSA).

ASSA aims to promote the development of social security in its member

countries in line with the aspirations, laws and regulations of these

countries. Formed as a forum, member institutions are free to exchange

and share views and experiences on social security issues.

ASSA now comprises 11 social security organisations from Brunei,

Indonesia, Lao PDR, Malaysia, the Philippines, Singapore, Thailand and

Vietnam.

38 Central Provident Fund Board | Annual Report 2004

National Education

The Board has always played an active role in nation-building. As per

previous years, the Board’s “CPF and You” programme reached out to

more than 1,238 junior college students in 2004. During these sessions,

students were able to learn more about CPF schemes and the role that CPF

plays in nation-building. The programme is part of the Learning Journey

Programme coordinated by the Ministry of Education for students to

understand the factors behind Singapore’s nation-building and to instil a

sense of pride in the future leaders of Singapore. The Board is one of the

key national institutions invited to participate in the Learning Journey

Programme.

Finance

As at 31 December 2004, CPF members’ funds amounted to $111,873.8

million. Of this, $108,462.4 million was invested in Singapore Government

Bonds and $3,411.4 million placed as Advance Deposits with the Monetary

Authority of Singapore pending the issue of such bonds.

The insurance funds stood at $3,166.7 million as at 31 December 2004.

They were mainly invested in bonds, equities and deposits by institutional

fund managers.

39Financial Statements

Financial Statements

40 Central Provident Fund Board | Annual Report 200440 Central Provident Fund Board | Annual Report 2004

Report on the Audit of the Financial Statements of the Central Provident Fund Board for the Year Ended 31 December 2004

The fi nancial statements of the Central Provident Fund Board, set out on pages 41 to 65, have been

audited under my direction and in accordance with the provisions of the Central Provident Fund Act (Cap.

36, 2001 Revised Edition). These fi nancial statements are the responsibility of the Board’s management.

My responsibility is to express an opinion on these fi nancial statements based on the audit.

The audit was conducted in accordance with the Central Provident Fund Act (Cap. 36, 2001 Revised

Edition) and Singapore Standards on Auditing. Those Standards require that the audit be planned and

performed in order to obtain reasonable assurance about whether the fi nancial statements are free of

material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts

and disclosures in the fi nancial statements. An audit also includes assessing the accounting principles

used and signifi cant estimates made by the Board’s management, as well as evaluating the overall

fi nancial statements presentation. I believe that the audit provides a reasonable basis for my opinion.

In my opinion,

(a) the fi nancial statements are properly drawn up in accordance with the provisions of the Central

Provident Fund Act (Cap. 36, 2001 Revised Edition) and Singapore Financial Reporting Standards so

as to give a true and fair view of the state of affairs of the Board as at 31 December 2004, and the

results, changes in equity and cash fl ows of the Board for the year ended on that date;

(b) proper accounting and other records have been kept, including records of all assets of the Board

whether purchased, donated or otherwise; and

(c) receipts, expenditure and investment of moneys and the acquisition and disposal of assets by

the Board during the fi nancial year have been in accordance with the provisions of the Central

Provident Fund Act (Cap. 36, 2001 Revised Edition).

CHUANG KWONG YONGAuditor-GeneralSingapore28 March 2005

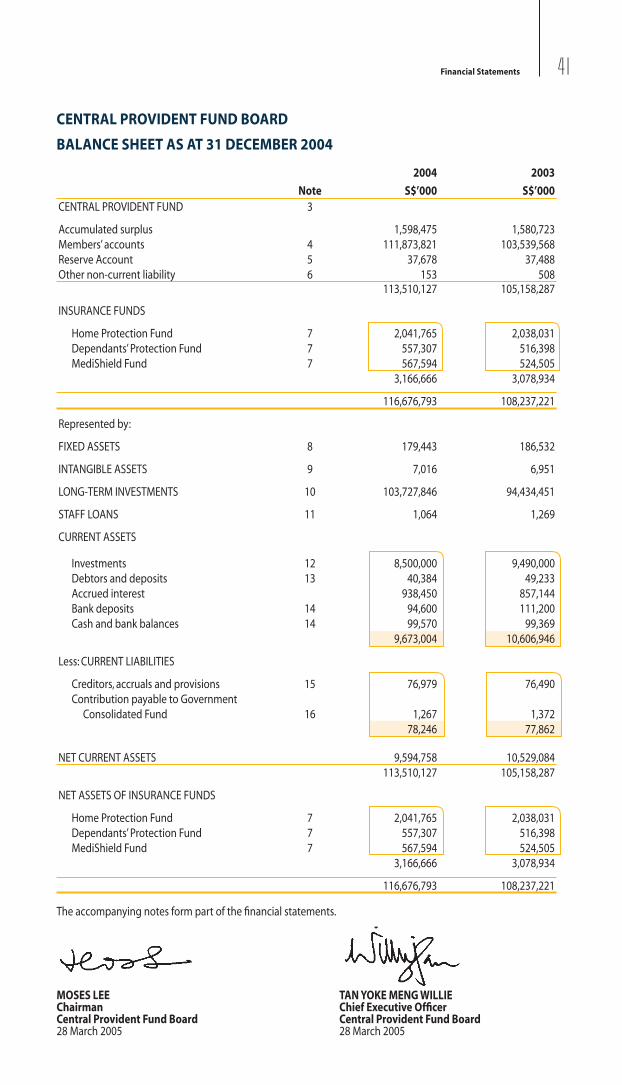

41Financial Statements

CENTRAL PROVIDENT FUND BOARD

BALANCE SHEET AS AT 31 DECEMBER 2004

2004 2003

Note S$’000 S$’000CENTRAL PROVIDENT FUND 3

Accumulated surplus 1,598,475 1,580,723 Members’ accounts 4 111,873,821 103,539,568 Reserve Account 5 37,678 37,488 Other non-current liability 6 153 508

113,510,127 105,158,287

INSURANCE FUNDS

Home Protection Fund 7 2,041,765 2,038,031 Dependants’ Protection Fund 7 557,307 516,398 MediShield Fund 7 567,594 524,505

3,166,666 3,078,934

116,676,793 108,237,221

Represented by:

FIXED ASSETS 8 179,443 186,532

INTANGIBLE ASSETS 9 7,016 6,951

LONG-TERM INVESTMENTS 10 103,727,846 94,434,451

STAFF LOANS 11 1,064 1,269

CURRENT ASSETS

Investments 12 8,500,000 9,490,000 Debtors and deposits 13 40,384 49,233 Accrued interest 938,450 857,144 Bank deposits 14 94,600 111,200 Cash and bank balances 14 99,570 99,369

9,673,004 10,606,946

Less: CURRENT LIABILITIES

Creditors, accruals and provisions 15 76,979 76,490 Contribution payable to Government Consolidated Fund 16 1,267 1,372

78,246 77,862

NET CURRENT ASSETS 9,594,758 10,529,084 113,510,127 105,158,287

NET ASSETS OF INSURANCE FUNDS

Home Protection Fund 7 2,041,765 2,038,031 Dependants’ Protection Fund 7 557,307 516,398 MediShield Fund 7 567,594 524,505

3,166,666 3,078,934

116,676,793 108,237,221

The accompanying notes form part of the fi nancial statements.

MOSES LEEChairmanCentral Provident Fund Board28 March 2005

TAN YOKE MENG WILLIEChief Executive Offi cerCentral Provident Fund Board28 March 2005

42 Central Provident Fund Board | Annual Report 2004

CENTRAL PROVIDENT FUND BOARD

INCOME AND EXPENDITURE STATEMENT FOR CENTRAL PROVIDENT FUND FOR THE YEAR ENDED 31 DECEMBER 2004

2004 2003Note S$’000 S$’000

INCOME

Investment income 3,461,829 3,190,913 Agency, consultancy and data processing fees 17 29,817 33,221 Penalty interest on late contributions 12,679 15,139 Rent, service charges and car park receipts 18 11,913 11,701 Miscellaneous revenue 1,149 1,186 Interest from bank deposits 874 1,256

3,518,261 3,253,416

Less:EXPENDITURE

Salaries and staff benefi ts 19 75,041 67,208 Depreciation and amortisation 8,9 11,647 11,246 Computer software and supplies 8,849 8,035 Maintenance of buildings and equipment 7,047 7,883 Printing and postage 6,157 8,299 Agency fees and other professional charges 5,875 5,336 General and administrative expenditure 20 3,305 3,909 Public utilities 2,624 2,609 Property tax 2,147 1,250 Publicity and campaigns 1,248 1,725 Finance cost 37 31 Bad debts expense – 49

123,977 117,580

Interest credited to members’ accounts 3,375,266 3,115,273

SURPLUS FOR THE YEARbefore contribution to Government Consolidated Fund 19,018 20,563

Less: Contribution to Government Consolidated Fund 16 1,266 1,371 NET SURPLUS FOR THE YEAR 17,752 19,192

Accumulated surplus as at 1 January 1,580,723 1,561,531

Accumulated surplus as at 31 December 1,598,475 1,580,723

The accompanying notes form part of the fi nancial statements.

43Financial Statements

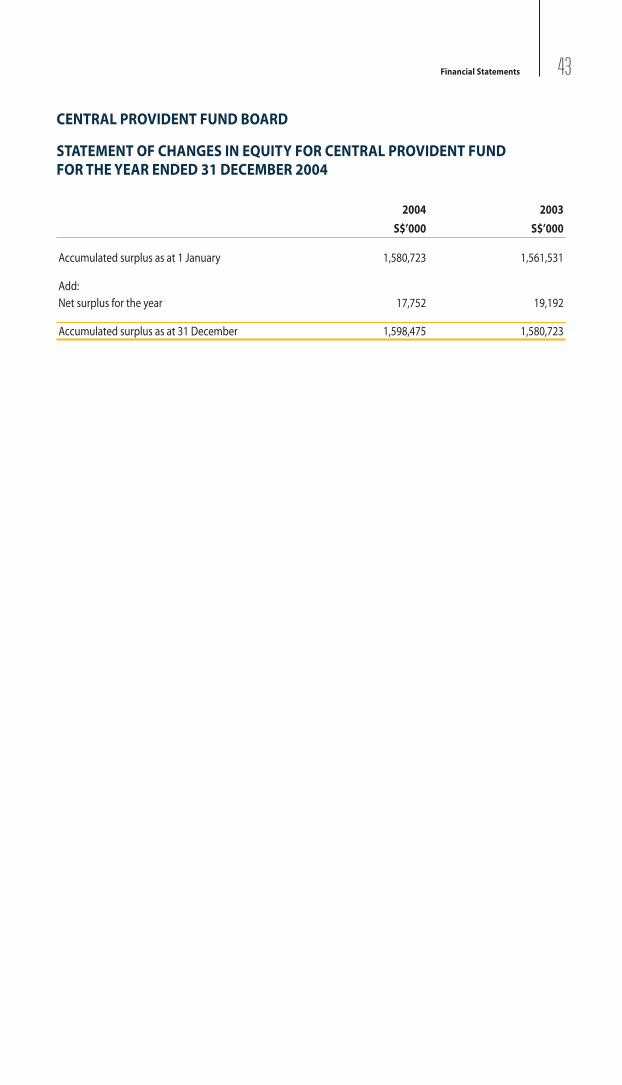

CENTRAL PROVIDENT FUND BOARD

STATEMENT OF CHANGES IN EQUITY FOR CENTRAL PROVIDENT FUNDFOR THE YEAR ENDED 31 DECEMBER 2004

2004 2003

S$’000 S$’000

Accumulated surplus as at 1 January 1,580,723 1,561,531

Add:Net surplus for the year 17,752 19,192

Accumulated surplus as at 31 December 1,598,475 1,580,723

44 Central Provident Fund Board | Annual Report 2004

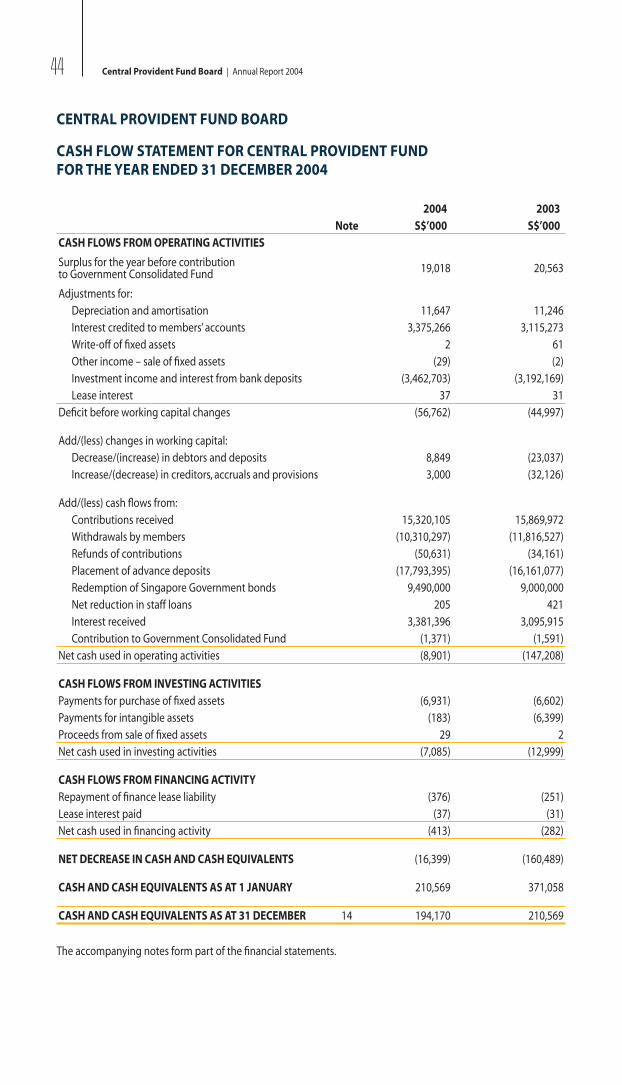

CENTRAL PROVIDENT FUND BOARD

CASH FLOW STATEMENT FOR CENTRAL PROVIDENT FUND FOR THE YEAR ENDED 31 DECEMBER 2004

2004 2003Note S$’000 S$’000

CASH FLOWS FROM OPERATING ACTIVITIES

Surplus for the year before contribution to Government Consolidated Fund 19,018 20,563

Adjustments for:Depreciation and amortisation 11,647 11,246 Interest credited to members’ accounts 3,375,266 3,115,273 Write-off of fi xed assets 2 61 Other income – sale of fi xed assets (29) (2)Investment income and interest from bank deposits (3,462,703) (3,192,169)Lease interest 37 31

Defi cit before working capital changes (56,762) (44,997)

Add/(less) changes in working capital:Decrease/(increase) in debtors and deposits 8,849 (23,037)Increase/(decrease) in creditors, accruals and provisions 3,000 (32,126)

Add/(less) cash fl ows from:Contributions received 15,320,105 15,869,972 Withdrawals by members (10,310,297) (11,816,527)Refunds of contributions (50,631) (34,161)Placement of advance deposits (17,793,395) (16,161,077)Redemption of Singapore Government bonds 9,490,000 9,000,000 Net reduction in staff loans 205 421 Interest received 3,381,396 3,095,915 Contribution to Government Consolidated Fund (1,371) (1,591)

Net cash used in operating activities (8,901) (147,208)

CASH FLOWS FROM INVESTING ACTIVITIESPayments for purchase of fi xed assets (6,931) (6,602)Payments for intangible assets (183) (6,399)Proceeds from sale of fi xed assets 29 2 Net cash used in investing activities (7,085) (12,999)

CASH FLOWS FROM FINANCING ACTIVITYRepayment of fi nance lease liability (376) (251)Lease interest paid (37) (31)Net cash used in fi nancing activity (413) (282)

NET DECREASE IN CASH AND CASH EQUIVALENTS (16,399) (160,489)

CASH AND CASH EQUIVALENTS AS AT 1 JANUARY 210,569 371,058

CASH AND CASH EQUIVALENTS AS AT 31 DECEMBER 14 194,170 210,569

The accompanying notes form part of the fi nancial statements.

45Financial Statements

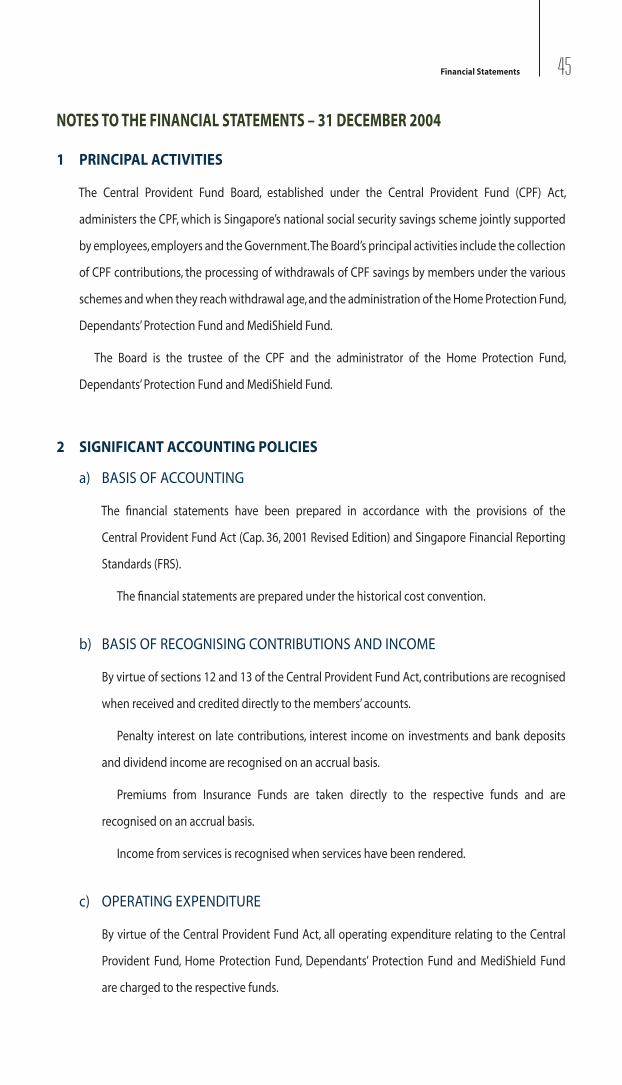

NOTES TO THE FINANCIAL STATEMENTS – 31 DECEMBER 2004

1 PRINCIPAL ACTIVITIES

The Central Provident Fund Board, established under the Central Provident Fund (CPF) Act,

administers the CPF, which is Singapore’s national social security savings scheme jointly supported

by employees, employers and the Government. The Board’s principal activities include the collection

of CPF contributions, the processing of withdrawals of CPF savings by members under the various

schemes and when they reach withdrawal age, and the administration of the Home Protection Fund,

Dependants’ Protection Fund and MediShield Fund.

The Board is the trustee of the CPF and the administrator of the Home Protection Fund,

Dependants’ Protection Fund and MediShield Fund.

2 SIGNIFICANT ACCOUNTING POLICIES

a) BASIS OF ACCOUNTING

The fi nancial statements have been prepared in accordance with the provisions of the

Central Provident Fund Act (Cap. 36, 2001 Revised Edition) and Singapore Financial Reporting

Standards (FRS).

The fi nancial statements are prepared under the historical cost convention.

b) BASIS OF RECOGNISING CONTRIBUTIONS AND INCOME

By virtue of sections 12 and 13 of the Central Provident Fund Act, contributions are recognised

when received and credited directly to the members’ accounts.

Penalty interest on late contributions, interest income on investments and bank deposits

and dividend income are recognised on an accrual basis.

Premiums from Insurance Funds are taken directly to the respective funds and are

recognised on an accrual basis.

Income from services is recognised when services have been rendered.

c) OPERATING EXPENDITURE

By virtue of the Central Provident Fund Act, all operating expenditure relating to the Central

Provident Fund, Home Protection Fund, Dependants’ Protection Fund and MediShield Fund

are charged to the respective funds.

46 Central Provident Fund Board | Annual Report 2004

d) INSURANCE FUNDS

Insurance Funds are established by the Board under the Central Provident Fund Act to account

for receipts and payments under the Home Protection Scheme, Dependants’ Protection Scheme

and MediShield Scheme. These funds are controlled and administered by the Board.

Receipts and payments of these funds are taken directly to the funds and the excess of the

funds’ assets over their liabilities is refl ected separately in the balance sheet. These funds are

accounted for on an accrual basis.

e) FIXED ASSETS AND DEPRECIATION

Fixed assets are stated at cost less accumulated depreciation and accumulated impairment

losses. Depreciation is calculated using a straight-line method to write off the cost of the fi xed

assets over their estimated useful lives. The estimated useful lives are as follows:

Leasehold land – period of the lease

Buildings – 50 years or period of the lease, whichever is shorter

Building renovation and improvement – remaining life of the building

Machinery and equipment – 4 to 20 years

Furniture and fi ttings – 8 years

Data-processing equipment – 3 to 5 years

Other assets – 30 years

A full year’s depreciation is charged in the year of acquisition of the assets and no

depreciation is charged in the year of disposal. No depreciation is provided for freehold land,

land with statutory grant and construction-in-progress.

The carrying amounts of fi xed assets are reviewed at each balance sheet date to assess

whether they are recorded in excess of their recoverable amounts, and if carrying amounts

exceed recoverable amounts, assets are written down to recoverable amounts.

Fully depreciated assets are retained in the books until they are disposed of.

Assets costing below S$2,000 per item are charged against income in the year of purchase.

47Financial Statements

f ) INTANGIBLE ASSETS AND AMORTISATION

Computer software including software development cost is stated at cost less accumulated

amortisation and accumulated impairment losses, if any. Amortisation is calculated using a

straight-line basis to write off the cost of the computer software over their estimated useful

lives ranging from 3 to 20 years.

A full year’s amortisation is charged in the year the asset is available for use and no

amortisation is charged in the year of disposal. No amortisation is provided for intangible

assets under development.

The carrying amounts of computer software are reviewed at each balance sheet date

to assess whether they are recorded in excess of their recoverable amounts, and if carrying

amounts exceed recoverable amounts, assets are written down to recoverable amounts.

Fully amortised assets are retained in the books until they are disposed of.

Computer software costing below S$2,000 per item is charged against income in the year

of purchase.

g) FINANCE LEASE

Assets fi nanced by lease agreements, which effectively transfer to the Board substantially all

the risks and benefi ts incidental to ownership of the leased items, are capitalised at the present

value of the minimum lease payments at the inception of the lease term. The corresponding

lease commitments are included under liabilities. The excess of the lease payments over the

recorded lease obligations are treated as fi nance charges which are amortised over each lease

term to give a constant rate of charge on the remaining balance of the obligation. Finance

charges are charged directly to the income and expenditure statement.

Capitalised lease assets are depreciated over the shorter of the estimated useful life of the

assets or the lease term.

h) INVESTMENTS

Investments in securities and derivatives are stated at the lower of cost or market value, and

determined on a portfolio basis. Provision is made for any diminution in the value of these

investments.

48 Central Provident Fund Board | Annual Report 2004

Amortisation of premiums or discounts on bonds and negotiable certifi cates of deposit is

provided on an individual counter basis. Premiums paid or discounts received upon acquisition

are amortised over the period from the date of purchase to the date of maturity of the related

securities, and the amortised premium or discount is taken to the income and expenditure

statement each year.

Investments under Insurance Funds are managed by external fund managers.

i) FOREIGN CURRENCIES

Transactions in foreign currencies are measured and recorded in Singapore dollars, using the

exchange rates in effect at the date of the transactions. Foreign currency monetary assets and

liabilities are translated to Singapore dollars at the rates of exchange prevailing at the balance

sheet date. Exchange differences are taken to the respective funds.

j) EMPLOYEE BENEFITS

Defi ned Contribution Plans

Contributions are made to the Central Provident Fund (CPF), as required by law. The CPF

contributions are recognised as compensation expense in the same period as the employment

that gives rise to the contributions.

Employee Leave Entitlement

Employee entitlements to annual leave are recognised when they are accrued to employees.

A provision is made for the estimated liability for leave as a result of services rendered by

employees up to the balance sheet date.

3 CENTRAL PROVIDENT FUND

The Central Provident Fund is established by the Central Provident Fund Act. All contributions

authorised under this Act are paid into the Fund and all payments authorised under this Act are

paid out of the Fund.

49Financial Statements

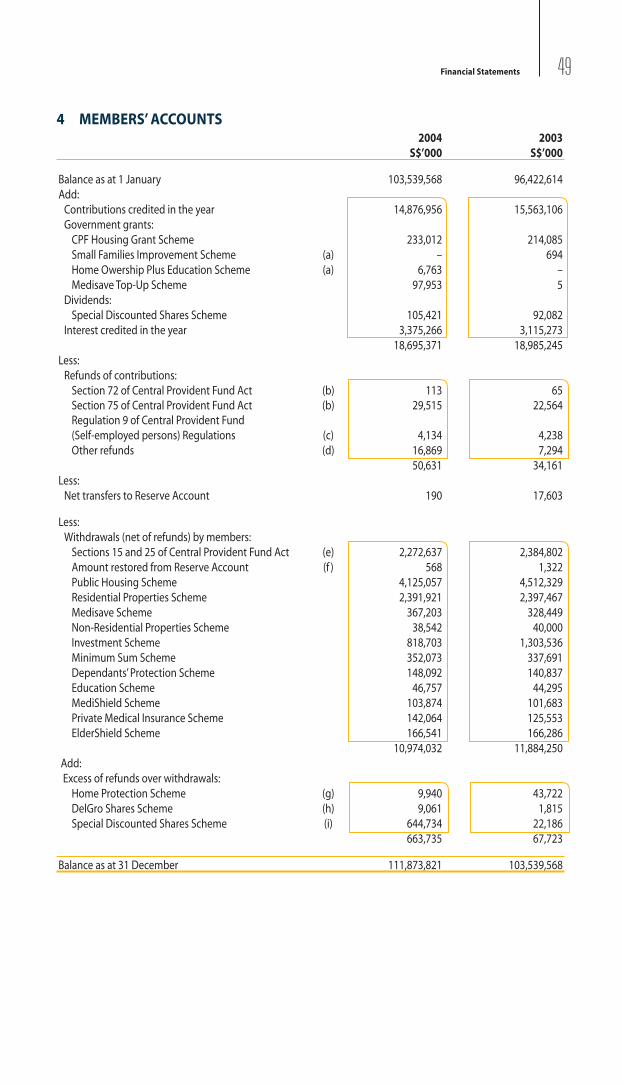

4 MEMBERS’ ACCOUNTS2004 2003

S$’000 S$’000

Balance as at 1 January 103,539,568 96,422,614 Add:

Contributions credited in the year 14,876,956 15,563,106 Government grants:

CPF Housing Grant Scheme 233,012 214,085 Small Families Improvement Scheme (a) – 694 Home Owership Plus Education Scheme (a) 6,763 – Medisave Top-Up Scheme 97,953 5

Dividends:Special Discounted Shares Scheme 105,421 92,082

Interest credited in the year 3,375,266 3,115,273 18,695,371 18,985,245

Less:Refunds of contributions:

Section 72 of Central Provident Fund Act (b) 113 65 Section 75 of Central Provident Fund Act (b) 29,515 22,564 Regulation 9 of Central Provident Fund(Self-employed persons) Regulations (c) 4,134 4,238 Other refunds (d) 16,869 7,294

50,631 34,161 Less:

Net transfers to Reserve Account 190 17,603

Less:Withdrawals (net of refunds) by members:

Sections 15 and 25 of Central Provident Fund Act (e) 2,272,637 2,384,802 Amount restored from Reserve Account (f ) 568 1,322 Public Housing Scheme 4,125,057 4,512,329 Residential Properties Scheme 2,391,921 2,397,467 Medisave Scheme 367,203 328,449 Non-Residential Properties Scheme 38,542 40,000 Investment Scheme 818,703 1,303,536 Minimum Sum Scheme 352,073 337,691 Dependants’ Protection Scheme 148,092 140,837 Education Scheme 46,757 44,295 MediShield Scheme 103,874 101,683 Private Medical Insurance Scheme 142,064 125,553 ElderShield Scheme 166,541 166,286

10,974,032 11,884,250 Add: Excess of refunds over withdrawals:

Home Protection Scheme (g) 9,940 43,722 DelGro Shares Scheme (h) 9,061 1,815 Special Discounted Shares Scheme (i) 644,734 22,186

663,735 67,723

Balance as at 31 December 111,873,821 103,539,568

50 Central Provident Fund Board | Annual Report 2004

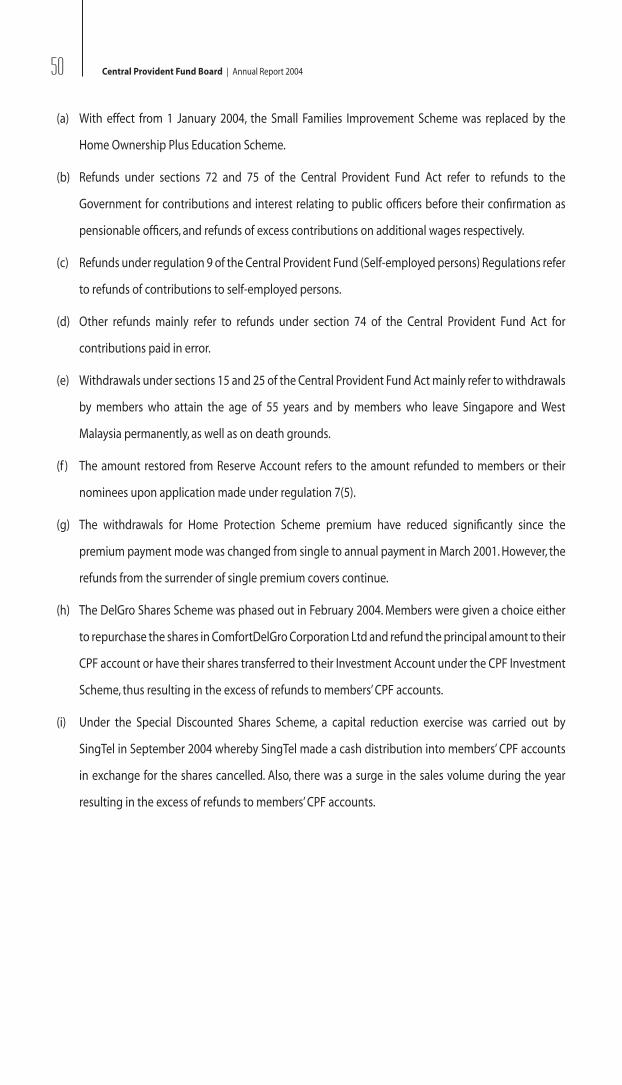

(a) With effect from 1 January 2004, the Small Families Improvement Scheme was replaced by the

Home Ownership Plus Education Scheme.

(b) Refunds under sections 72 and 75 of the Central Provident Fund Act refer to refunds to the

Government for contributions and interest relating to public offi cers before their confi rmation as

pensionable offi cers, and refunds of excess contributions on additional wages respectively.

(c) Refunds under regulation 9 of the Central Provident Fund (Self-employed persons) Regulations refer

to refunds of contributions to self-employed persons.

(d) Other refunds mainly refer to refunds under section 74 of the Central Provident Fund Act for

contributions paid in error.

(e) Withdrawals under sections 15 and 25 of the Central Provident Fund Act mainly refer to withdrawals

by members who attain the age of 55 years and by members who leave Singapore and West

Malaysia permanently, as well as on death grounds.

(f ) The amount restored from Reserve Account refers to the amount refunded to members or their

nominees upon application made under regulation 7(5).

(g) The withdrawals for Home Protection Scheme premium have reduced signifi cantly since the

premium payment mode was changed from single to annual payment in March 2001. However, the

refunds from the surrender of single premium covers continue.

(h) The DelGro Shares Scheme was phased out in February 2004. Members were given a choice either

to repurchase the shares in ComfortDelGro Corporation Ltd and refund the principal amount to their

CPF account or have their shares transferred to their Investment Account under the CPF Investment

Scheme, thus resulting in the excess of refunds to members’ CPF accounts.

(i) Under the Special Discounted Shares Scheme, a capital reduction exercise was carried out by

SingTel in September 2004 whereby SingTel made a cash distribution into members’ CPF accounts

in exchange for the shares cancelled. Also, there was a surge in the sales volume during the year

resulting in the excess of refunds to members’ CPF accounts.

51Financial Statements

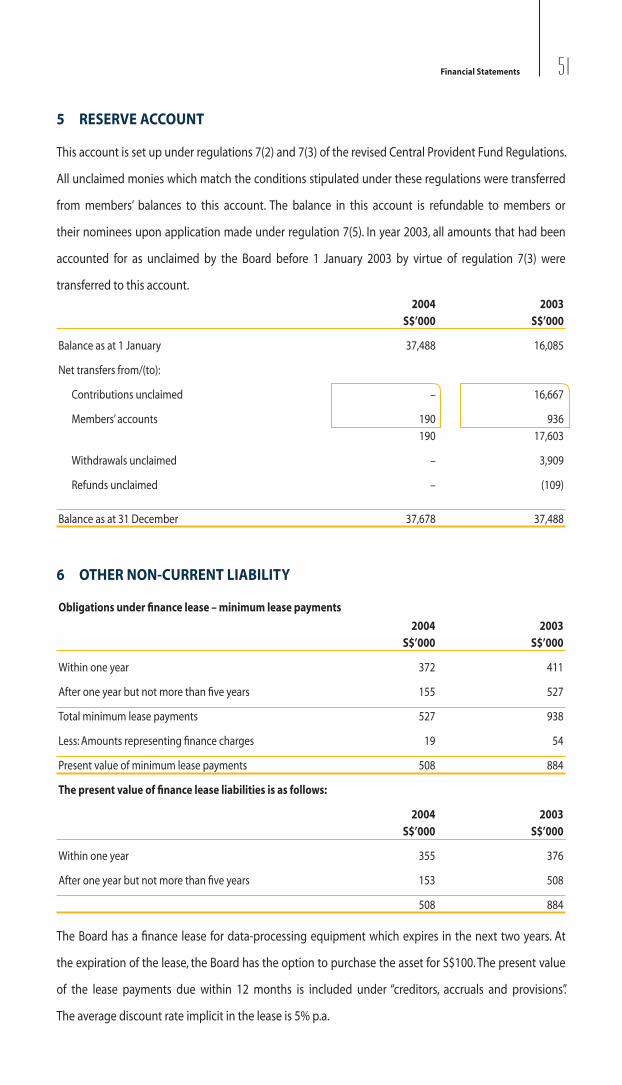

5 RESERVE ACCOUNT

This account is set up under regulations 7(2) and 7(3) of the revised Central Provident Fund Regulations.

All unclaimed monies which match the conditions stipulated under these regulations were transferred

from members’ balances to this account. The balance in this account is refundable to members or

their nominees upon application made under regulation 7(5). In year 2003, all amounts that had been

accounted for as unclaimed by the Board before 1 January 2003 by virtue of regulation 7(3) were

transferred to this account.2004 2003

S$’000 S$’000

Balance as at 1 January 37,488 16,085

Net transfers from/(to):

Contributions unclaimed – 16,667

Members’ accounts 190 936 190 17,603

Withdrawals unclaimed – 3,909

Refunds unclaimed – (109)

Balance as at 31 December 37,678 37,488

6 OTHER NON-CURRENT LIABILITY

Obligations under fi nance lease – minimum lease payments

2004 2003S$’000 S$’000

Within one year 372 411

After one year but not more than fi ve years 155 527

Total minimum lease payments 527 938

Less: Amounts representing fi nance charges 19 54

Present value of minimum lease payments 508 884

The present value of fi nance lease liabilities is as follows:

2004 2003S$’000 S$’000

Within one year 355 376

After one year but not more than fi ve years 153 508

508 884

The Board has a fi nance lease for data-processing equipment which expires in the next two years. At

the expiration of the lease, the Board has the option to purchase the asset for S$100. The present value

of the lease payments due within 12 months is included under “creditors, accruals and provisions”.

The average discount rate implicit in the lease is 5% p.a.

52 Central Provident Fund Board | Annual Report 2004

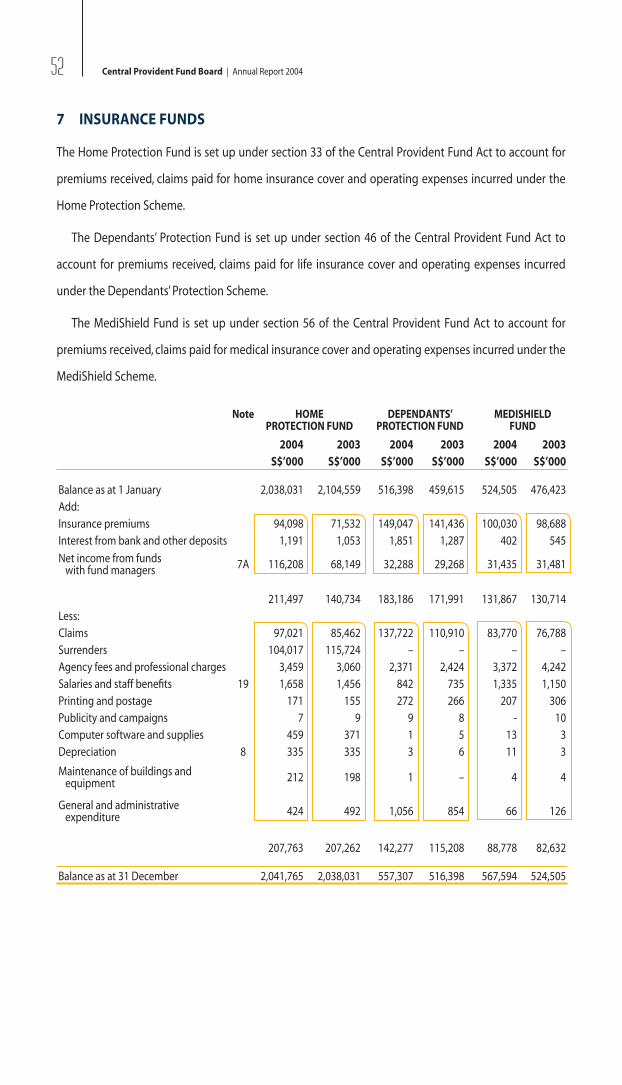

7 INSURANCE FUNDS

The Home Protection Fund is set up under section 33 of the Central Provident Fund Act to account for

premiums received, claims paid for home insurance cover and operating expenses incurred under the

Home Protection Scheme.

The Dependants’ Protection Fund is set up under section 46 of the Central Provident Fund Act to

account for premiums received, claims paid for life insurance cover and operating expenses incurred

under the Dependants’ Protection Scheme.

The MediShield Fund is set up under section 56 of the Central Provident Fund Act to account for

premiums received, claims paid for medical insurance cover and operating expenses incurred under the

MediShield Scheme.

Note HOME PROTECTION FUND

DEPENDANTS’ PROTECTION FUND

MEDISHIELD FUND

2004 2003 2004 2003 2004 2003S$’000 S$’000 S$’000 S$’000 S$’000 S$’000

Balance as at 1 January 2,038,031 2,104,559 516,398 459,615 524,505 476,423 Add:Insurance premiums 94,098 71,532 149,047 141,436 100,030 98,688 Interest from bank and other deposits 1,191 1,053 1,851 1,287 402 545

Net income from funds with fund managers 7A 116,208 68,149 32,288 29,268 31,435 31,481

211,497 140,734 183,186 171,991 131,867 130,714 Less:Claims 97,021 85,462 137,722 110,910 83,770 76,788 Surrenders 104,017 115,724 – – – –Agency fees and professional charges 3,459 3,060 2,371 2,424 3,372 4,242 Salaries and staff benefi ts 19 1,658 1,456 842 735 1,335 1,150 Printing and postage 171 155 272 266 207 306 Publicity and campaigns 7 9 9 8 - 10 Computer software and supplies 459 371 1 5 13 3 Depreciation 8 335 335 3 6 11 3

Maintenance of buildings and equipment 212 198 1 – 4 4

General and administrative expenditure 424 492 1,056 854 66 126

207,763 207,262 142,277 115,208 88,778 82,632

Balance as at 31 December 2,041,765 2,038,031 557,307 516,398 567,594 524,505

53Financial Statements

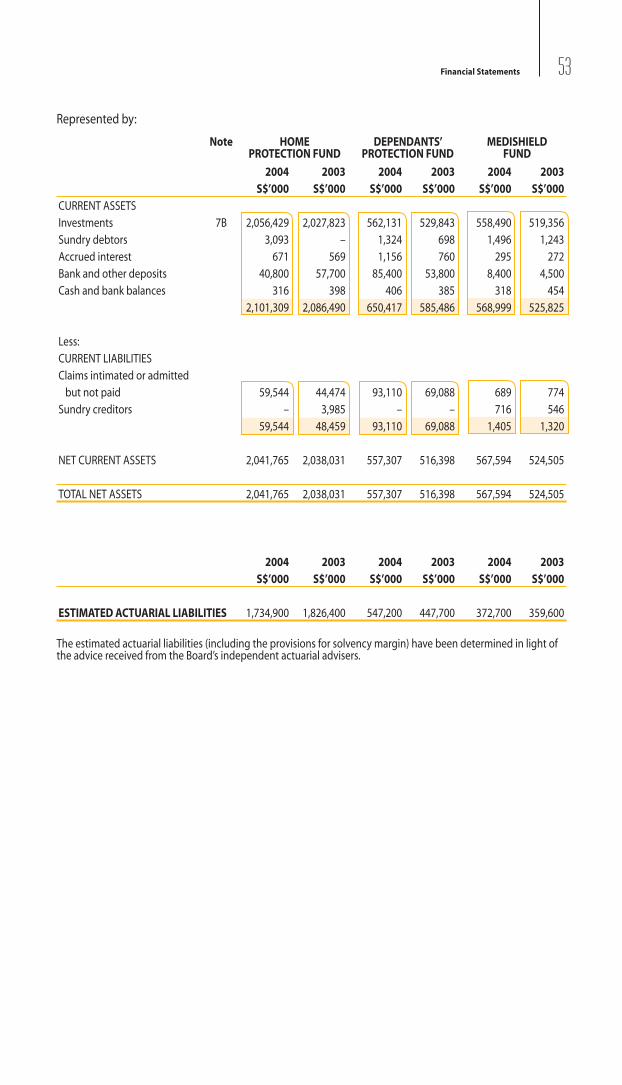

Represented by:

Note HOME PROTECTION FUND

DEPENDANTS’ PROTECTION FUND

MEDISHIELD FUND

2004 2003 2004 2003 2004 2003 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000

CURRENT ASSETSInvestments 7B 2,056,429 2,027,823 562,131 529,843 558,490 519,356 Sundry debtors 3,093 – 1,324 698 1,496 1,243 Accrued interest 671 569 1,156 760 295 272 Bank and other deposits 40,800 57,700 85,400 53,800 8,400 4,500 Cash and bank balances 316 398 406 385 318 454

2,101,309 2,086,490 650,417 585,486 568,999 525,825

Less:CURRENT LIABILITIESClaims intimated or admitted but not paid 59,544 44,474 93,110 69,088 689 774 Sundry creditors – 3,985 – – 716 546

59,544 48,459 93,110 69,088 1,405 1,320

NET CURRENT ASSETS 2,041,765 2,038,031 557,307 516,398 567,594 524,505

TOTAL NET ASSETS 2,041,765 2,038,031 557,307 516,398 567,594 524,505

2004 2003 2004 2003 2004 2003 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000

ESTIMATED ACTUARIAL LIABILITIES 1,734,900 1,826,400 547,200 447,700 372,700 359,600

The estimated actuarial liabilities (including the provisions for solvency margin) have been determined in light of the advice received from the Board’s independent actuarial advisers.

54 Central Provident Fund Board | Annual Report 2004

7A NET INCOME FROM FUNDS WITH FUND MANAGERS HOME

PROTECTION FUNDDEPENDANTS’

PROTECTION FUNDMEDISHIELD

FUND

2004 2003 2004 2003 2004 2003

S$’000 S$’000 S$’000 S$’000 S$’000 S$’000

INCOMEInvestment income 58,861 62,882 16,007 12,695 15,401 13,443 Interest from bank and other deposits 524 492 86 160 92 120 Foreign exchange gain 23,230 – 3,744 – 6,076 –Profi t on sale of investments 41,528 9,573 14,721 – 12,044 –Diminution in value of investments written back – 10,344 – 24,906 – 28,063 Miscellaneous revenue 1 3 – 3 – 1

124,144 83,294 34,558 37,764 33,613 41,627

Less:EXPENDITUREForeign exchange loss – 9,508 – 1,627 – 1,366 Loss on sale of investments – – – 5,175 – 7,220 Fund management fees 7,936 5,637 2,270 1,694 2,178 1,560

7,936 15,145 2,270 8,496 2,178 10,146

NET INCOME FROM FUNDS WITH FUND MANAGERS 116,208 68,149 32,288 29,268 31,435 31,481

7B INVESTMENTSHOME

PROTECTION FUNDDEPENDANTS’

PROTECTION FUNDMEDISHIELD

FUND

2004 2003 2004 2003 2004 2003 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000

COST

Funds managed by fund managers 2,056,429 2,027,823 562,131 529,843 558,490 519,356

Represented by:

Fixed income securities 1,674,840 1,551,283 282,598 269,824 300,168 265,619 Equities 494,092 523,886 291,859 273,737 271,572 269,279 Derivatives (1,206) 12,721 – – – –

2,167,726 2,087,890 574,457 543,561 571,740 534,898

Add/(less):Interest and other receivables 52,825 71,654 11,475 7,411 11,332 7,129 Accruals and payables (186,593) (151,249) (33,059) (25,148) (32,815) (26,356)Bank deposits 19,474 17,151 8,727 3,812 7,781 3,448 Cash balances 2,997 2,377 531 207 452 237

(111,297) (60,067) (12,326) (13,718) (13,250) (15,542)2,056,429 2,027,823 562,131 529,843 558,490 519,356

MARKET VALUE

Funds managed by fund managersFixed income securities 1,731,641 1,590,305 295,070 275,328 312,260 273,030 Equities 581,850 593,811 349,368 317,672 321,026 304,193 Derivatives 1,241 10,299 – – – –

2,314,732 2,194,415 644,438 593,000 633,286 577,223

55Financial Statements

7C DEPENDANTS’ PROTECTION FUND

The Dependants’ Protection Scheme will be privatised in the 3rd quarter of 2005. After the privatisation,

part of the Dependants’ Protection Fund will be transferred to the appointed private insurers who will be

responsible for the insurance operations as well as the fi nancial solvency of the scheme.

7D MEDISHIELD FUND

The MediShield Plus portfolio will be tendered out to a private insurer in the 4th quarter of 2005. Part

of the MediShield Fund will be transferred to the appointed private insurer taking over the MediShield

Plus portfolio. The insurer taking over the MediShield Plus portfolio will be responsible for the insurance

operations as well as the fi nancial solvency of the MediShield Plus portfolio.

56 Central Provident Fund Board | Annual Report 2004

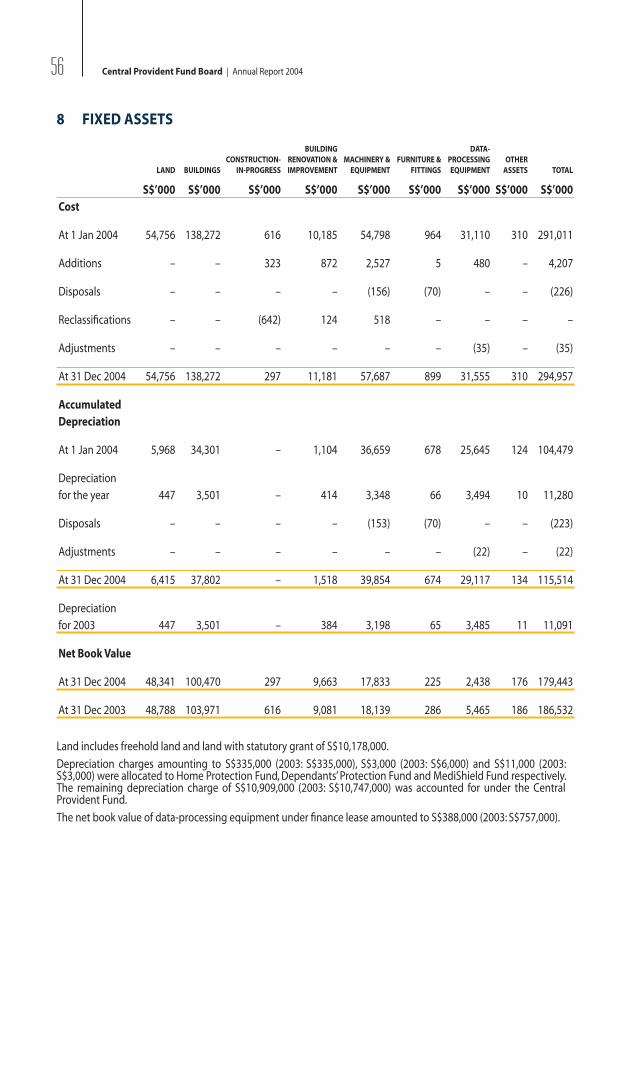

8 FIXED ASSETS

LAND BUILDINGSCONSTRUCTION-

IN-PROGRESS

BUILDINGRENOVATION &

IMPROVEMENTMACHINERY &

EQUIPMENTFURNITURE &

FITTINGS

DATA-PROCESSINGEQUIPMENT

OTHER ASSETS TOTAL

S$’000 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000 S$’000Cost

At 1 Jan 2004 54,756 138,272 616 10,185 54,798 964 31,110 310 291,011

Additions – – 323 872 2,527 5 480 – 4,207

Disposals – – – – (156) (70) – – (226)

Reclassifi cations – – (642) 124 518 – – – –

Adjustments – – – – – – (35) – (35)

At 31 Dec 2004 54,756 138,272 297 11,181 57,687 899 31,555 310 294,957

Accumulated Depreciation

At 1 Jan 2004 5,968 34,301 – 1,104 36,659 678 25,645 124 104,479

Depreciation for the year 447 3,501 – 414 3,348 66 3,494 10 11,280

Disposals – – – – (153) (70) – – (223)

Adjustments – – – – – – (22) – (22)

At 31 Dec 2004 6,415 37,802 – 1,518 39,854 674 29,117 134 115,514

Depreciationfor 2003 447 3,501 – 384 3,198 65 3,485 11 11,091

Net Book Value

At 31 Dec 2004 48,341 100,470 297 9,663 17,833 225 2,438 176 179,443

At 31 Dec 2003 48,788 103,971 616 9,081 18,139 286 5,465 186 186,532

Land includes freehold land and land with statutory grant of S$10,178,000.

Depreciation charges amounting to S$335,000 (2003: S$335,000), S$3,000 (2003: S$6,000) and S$11,000 (2003: S$3,000) were allocated to Home Protection Fund, Dependants’ Protection Fund and MediShield Fund respectively. The remaining depreciation charge of S$10,909,000 (2003: S$10,747,000) was accounted for under the Central Provident Fund.

The net book value of data-processing equipment under fi nance lease amounted to S$388,000 (2003: S$757,000).

57Financial Statements

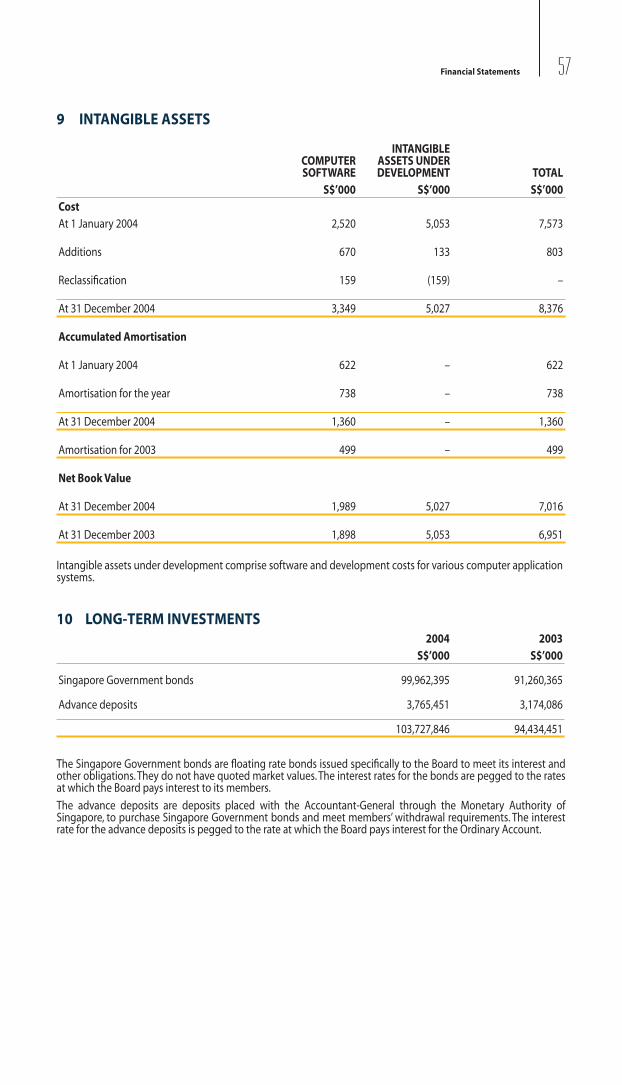

9 INTANGIBLE ASSETS

COMPUTERSOFTWARE

INTANGIBLEASSETS UNDERDEVELOPMENT TOTAL

S$’000 S$’000 S$’000CostAt 1 January 2004 2,520 5,053 7,573

Additions 670 133 803

Reclassifi cation 159 (159) –

At 31 December 2004 3,349 5,027 8,376

Accumulated Amortisation

At 1 January 2004 622 – 622

Amortisation for the year 738 – 738

At 31 December 2004 1,360 – 1,360

Amortisation for 2003 499 – 499

Net Book Value

At 31 December 2004 1,989 5,027 7,016

At 31 December 2003 1,898 5,053 6,951

Intangible assets under development comprise software and development costs for various computer application systems.

10 LONG-TERM INVESTMENTS2004 2003

S$’000 S$’000

Singapore Government bonds 99,962,395 91,260,365

Advance deposits 3,765,451 3,174,086

103,727,846 94,434,451

The Singapore Government bonds are fl oating rate bonds issued specifi cally to the Board to meet its interest and other obligations. They do not have quoted market values. The interest rates for the bonds are pegged to the rates at which the Board pays interest to its members.

The advance deposits are deposits placed with the Accountant-General through the Monetary Authority of Singapore, to purchase Singapore Government bonds and meet members’ withdrawal requirements. The interest rate for the advance deposits is pegged to the rate at which the Board pays interest for the Ordinary Account.

58 Central Provident Fund Board | Annual Report 2004

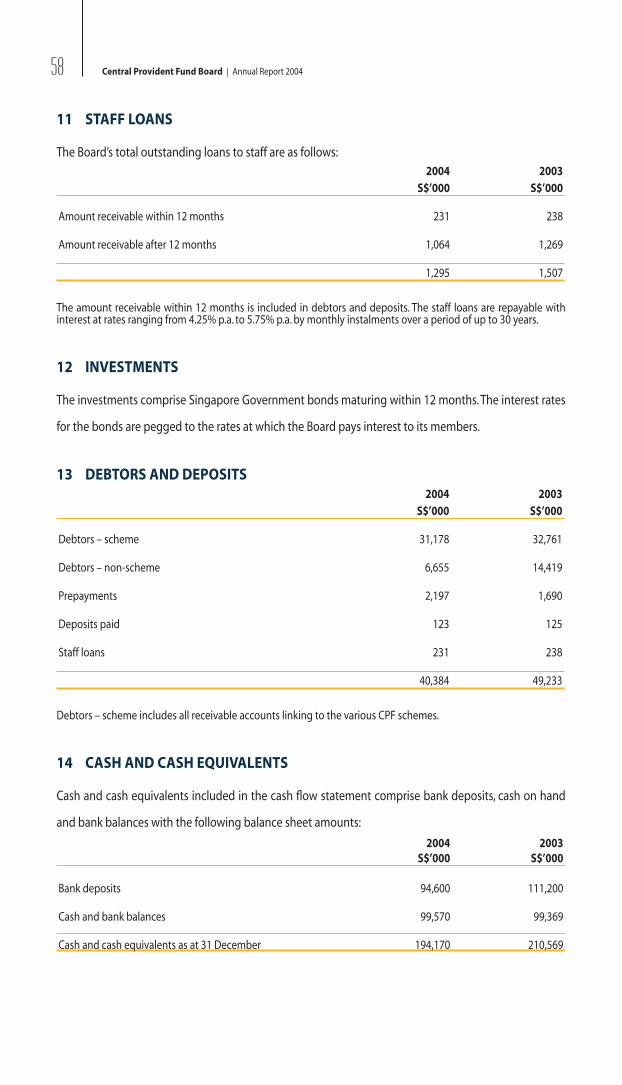

11 STAFF LOANS

The Board’s total outstanding loans to staff are as follows:2004 2003

S$’000 S$’000

Amount receivable within 12 months 231 238

Amount receivable after 12 months 1,064 1,269

1,295 1,507

The amount receivable within 12 months is included in debtors and deposits. The staff loans are repayable with interest at rates ranging from 4.25% p.a. to 5.75% p.a. by monthly instalments over a period of up to 30 years.

12 INVESTMENTS

The investments comprise Singapore Government bonds maturing within 12 months. The interest rates

for the bonds are pegged to the rates at which the Board pays interest to its members.

13 DEBTORS AND DEPOSITS2004 2003

S$’000 S$’000

Debtors – scheme 31,178 32,761

Debtors – non-scheme 6,655 14,419

Prepayments 2,197 1,690

Deposits paid 123 125

Staff loans 231 238

40,384 49,233

Debtors – scheme includes all receivable accounts linking to the various CPF schemes.

14 CASH AND CASH EQUIVALENTS

Cash and cash equivalents included in the cash fl ow statement comprise bank deposits, cash on hand

and bank balances with the following balance sheet amounts:

2004 2003S$’000 S$’000

Bank deposits 94,600 111,200

Cash and bank balances 99,570 99,369

Cash and cash equivalents as at 31 December 194,170 210,569

59Financial Statements

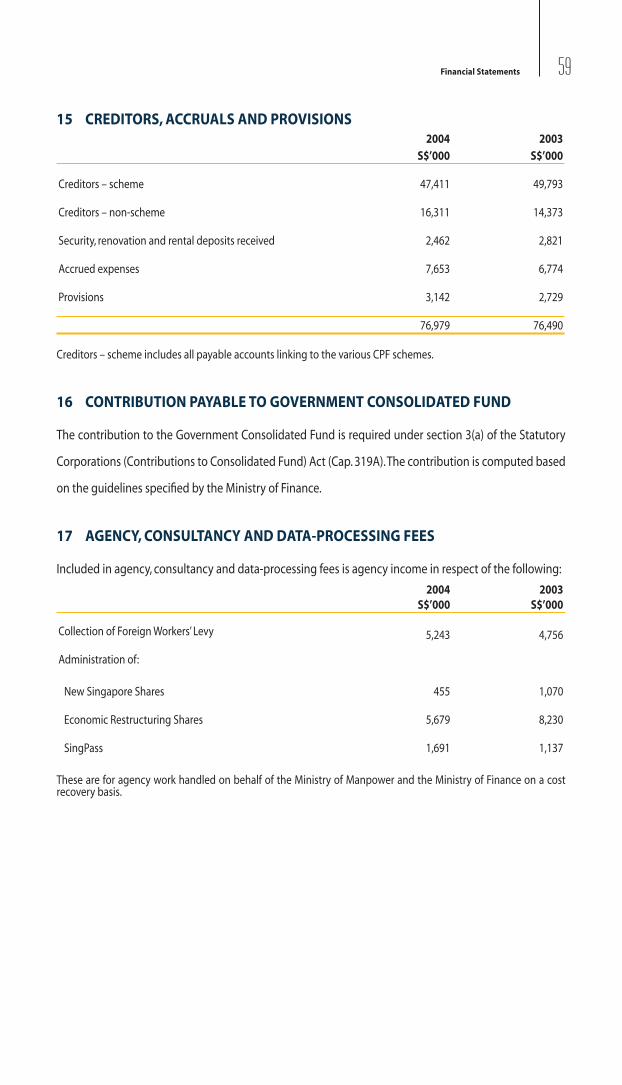

15 CREDITORS, ACCRUALS AND PROVISIONS2004 2003

S$’000 S$’000

Creditors – scheme 47,411 49,793

Creditors – non-scheme 16,311 14,373

Security, renovation and rental deposits received 2,462 2,821

Accrued expenses 7,653 6,774

Provisions 3,142 2,729

76,979 76,490

Creditors – scheme includes all payable accounts linking to the various CPF schemes.

16 CONTRIBUTION PAYABLE TO GOVERNMENT CONSOLIDATED FUND

The contribution to the Government Consolidated Fund is required under section 3(a) of the Statutory

Corporations (Contributions to Consolidated Fund) Act (Cap. 319A). The contribution is computed based

on the guidelines specifi ed by the Ministry of Finance.

17 AGENCY, CONSULTANCY AND DATA-PROCESSING FEES

Included in agency, consultancy and data-processing fees is agency income in respect of the following:

2004 2003S$’000 S$’000

Collection of Foreign Workers’ Levy 5,243 4,756

Administration of:

New Singapore Shares 455 1,070

Economic Restructuring Shares 5,679 8,230

SingPass 1,691 1,137

These are for agency work handled on behalf of the Ministry of Manpower and the Ministry of Finance on a cost recovery basis.

60 Central Provident Fund Board | Annual Report 2004

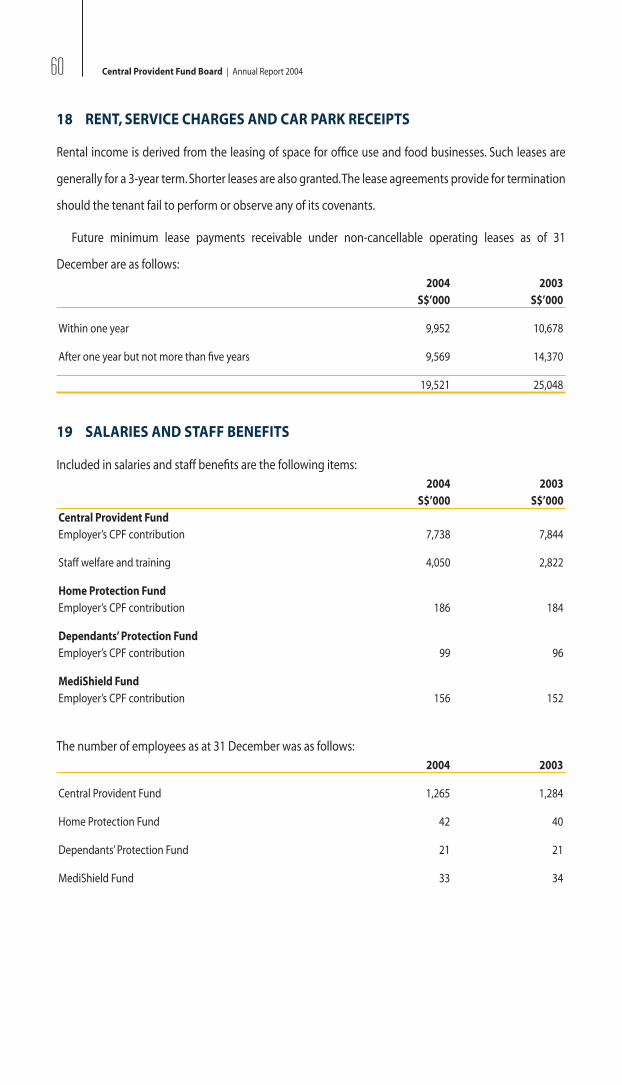

18 RENT, SERVICE CHARGES AND CAR PARK RECEIPTS

Rental income is derived from the leasing of space for offi ce use and food businesses. Such leases are

generally for a 3-year term. Shorter leases are also granted. The lease agreements provide for termination

should the tenant fail to perform or observe any of its covenants.

Future minimum lease payments receivable under non-cancellable operating leases as of 31

December are as follows:2004 2003

S$’000 S$’000

Within one year 9,952 10,678

After one year but not more than fi ve years 9,569 14,370

19,521 25,048

19 SALARIES AND STAFF BENEFITS

Included in salaries and staff benefi ts are the following items:2004 2003

S$’000 S$’000Central Provident FundEmployer’s CPF contribution 7,738 7,844

Staff welfare and training 4,050 2,822

Home Protection FundEmployer’s CPF contribution 186 184

Dependants’ Protection FundEmployer’s CPF contribution 99 96

MediShield FundEmployer’s CPF contribution 156 152

The number of employees as at 31 December was as follows:2004 2003

Central Provident Fund 1,265 1,284

Home Protection Fund 42 40

Dependants’ Protection Fund 21 21

MediShield Fund 33 34

61Financial Statements

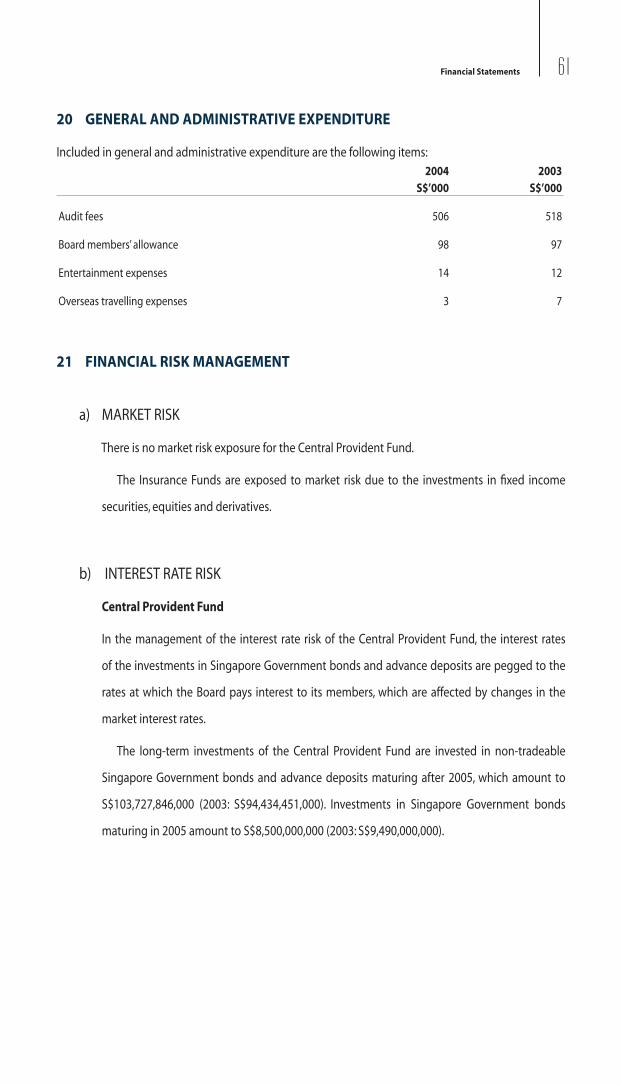

20 GENERAL AND ADMINISTRATIVE EXPENDITURE

Included in general and administrative expenditure are the following items:2004 2003

S$’000 S$’000

Audit fees 506 518

Board members’ allowance 98 97

Entertainment expenses 14 12

Overseas travelling expenses 3 7

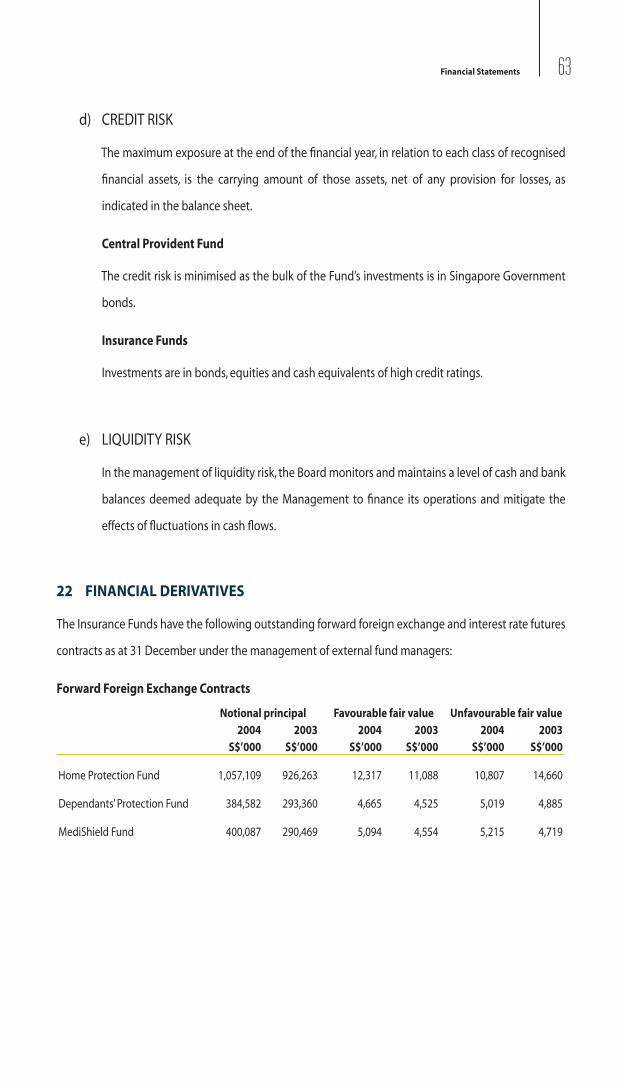

21 FINANCIAL RISK MANAGEMENT

a) MARKET RISK

There is no market risk exposure for the Central Provident Fund.

The Insurance Funds are exposed to market risk due to the investments in fi xed income

securities, equities and derivatives.

b) INTEREST RATE RISK

Central Provident Fund

In the management of the interest rate risk of the Central Provident Fund, the interest rates

of the investments in Singapore Government bonds and advance deposits are pegged to the

rates at which the Board pays interest to its members, which are affected by changes in the

market interest rates.

The long-term investments of the Central Provident Fund are invested in non-tradeable

Singapore Government bonds and advance deposits maturing after 2005, which amount to

S$103,727,846,000 (2003: S$94,434,451,000). Investments in Singapore Government bonds

maturing in 2005 amount to S$8,500,000,000 (2003: S$9,490,000,000).

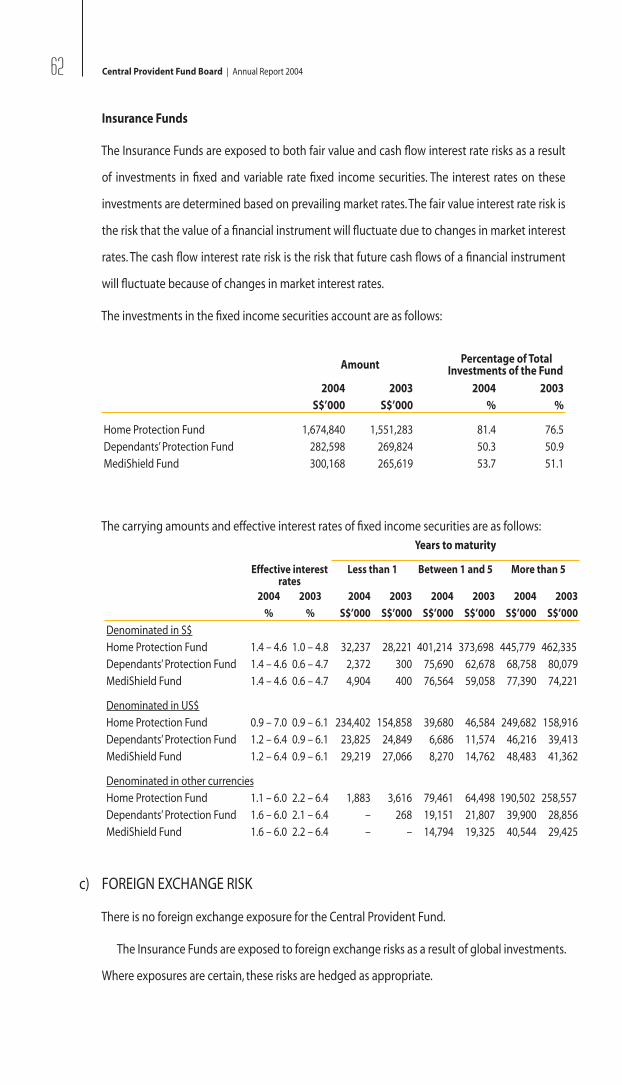

62 Central Provident Fund Board | Annual Report 2004

Insurance Funds