Embed Size (px)

Citation preview

©

Offshore WindA big opportunity?

GA-EMA Conferences

22 October 2014

©

CONTENTS

2

1. Global context of Renewables

2. Offshore Wind• Markets• Concepts and key figures• Risks

3. Conclusions

©

CONTENTS

3

1. Global context of Renewables

2. Offshore Wind• Markets• Concepts and key figures• Risks

3. Conclusions

© 4

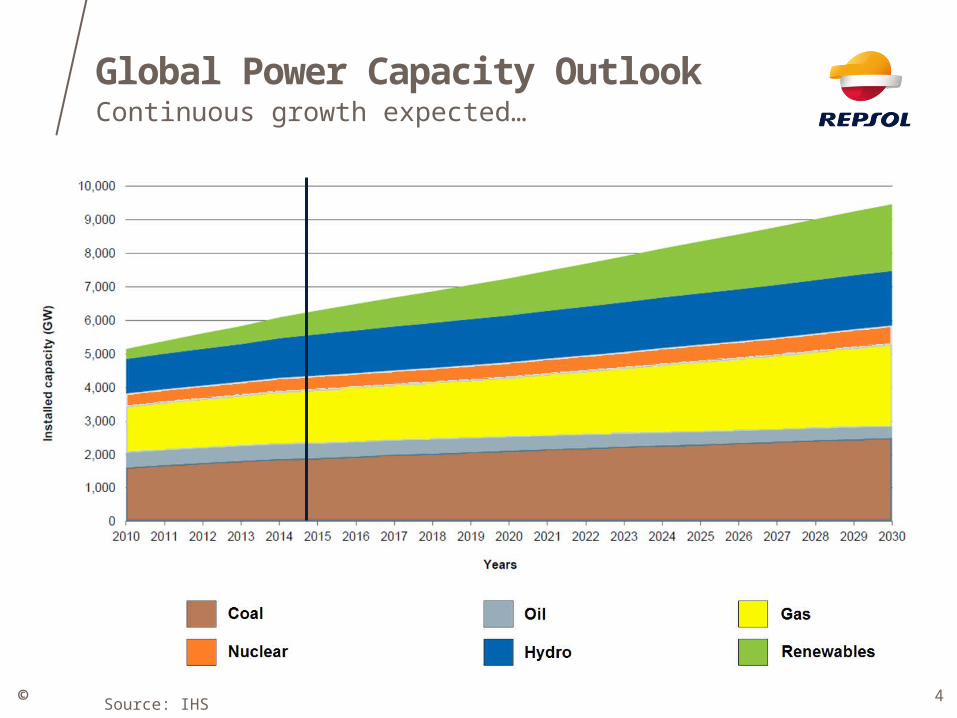

Global Power Capacity OutlookContinuous growth expected…

Source: IHS

© 5

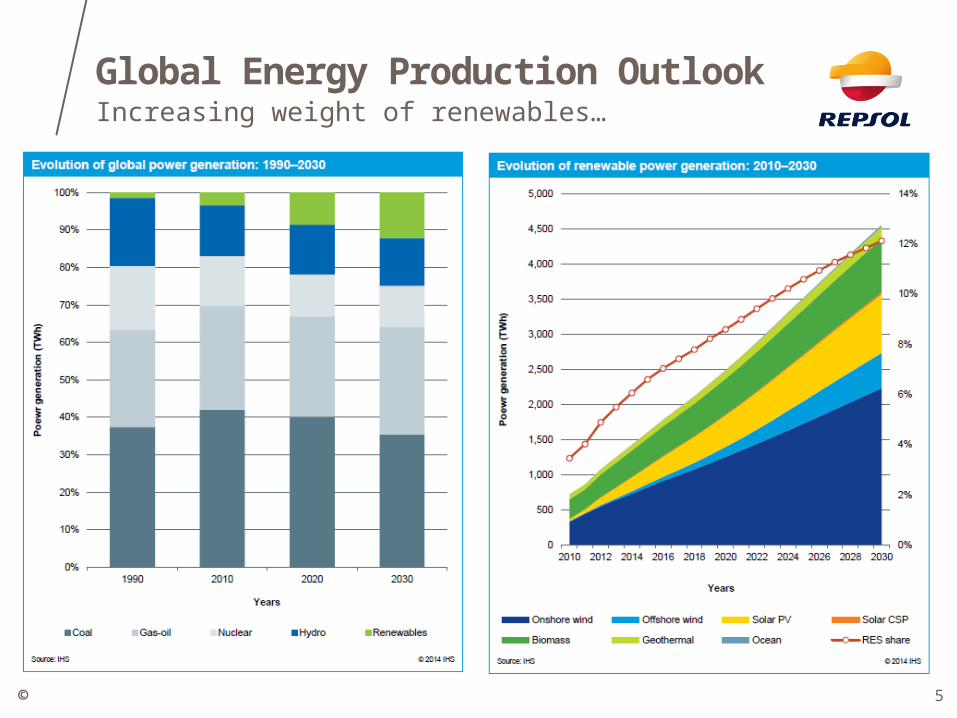

Global Energy Production OutlookIncreasing weight of renewables…

©

CONTENTS

6

1. Global context of renewables

2. Offshore Wind• Markets• Concepts and key figures• Risks

3. Conclusions

© 7

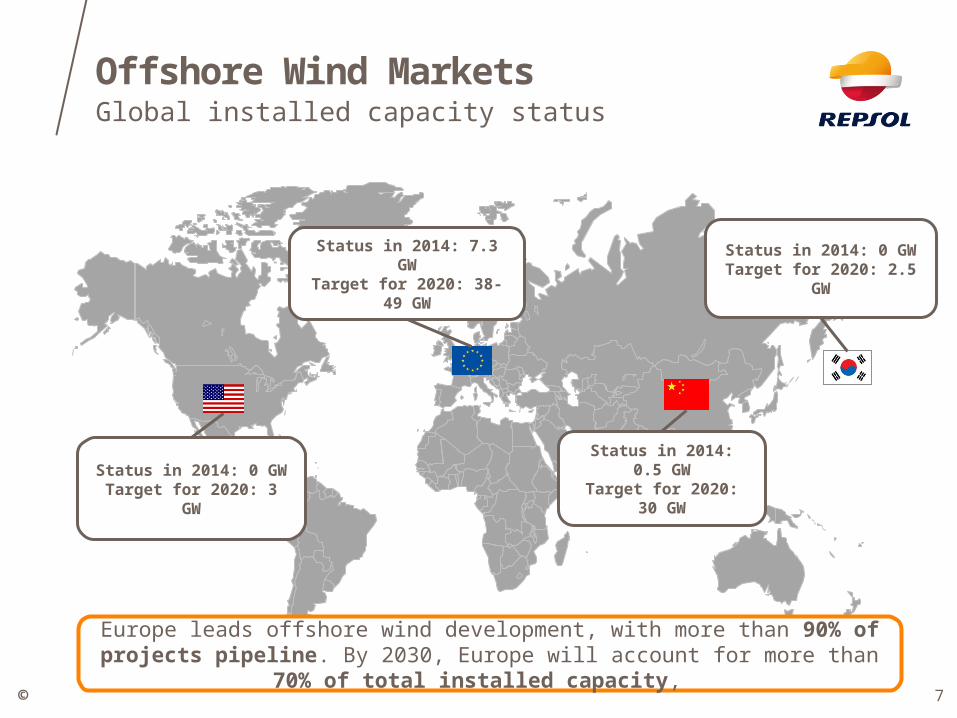

Offshore Wind MarketsGlobal installed capacity status

Status in 2014: 0 GWTarget for 2020: 3 GW

Status in 2014: 7.3 GWTarget for 2020: 38-49 GW

Status in 2014: 0.5 GWTarget for 2020: 30 GW

Status in 2014: 0 GWTarget for 2020: 2.5 GW

Europe leads offshore wind development, with more than 90% of projects pipeline. By 2030, Europe will account for more than 70% of total installed capacity,

© 8

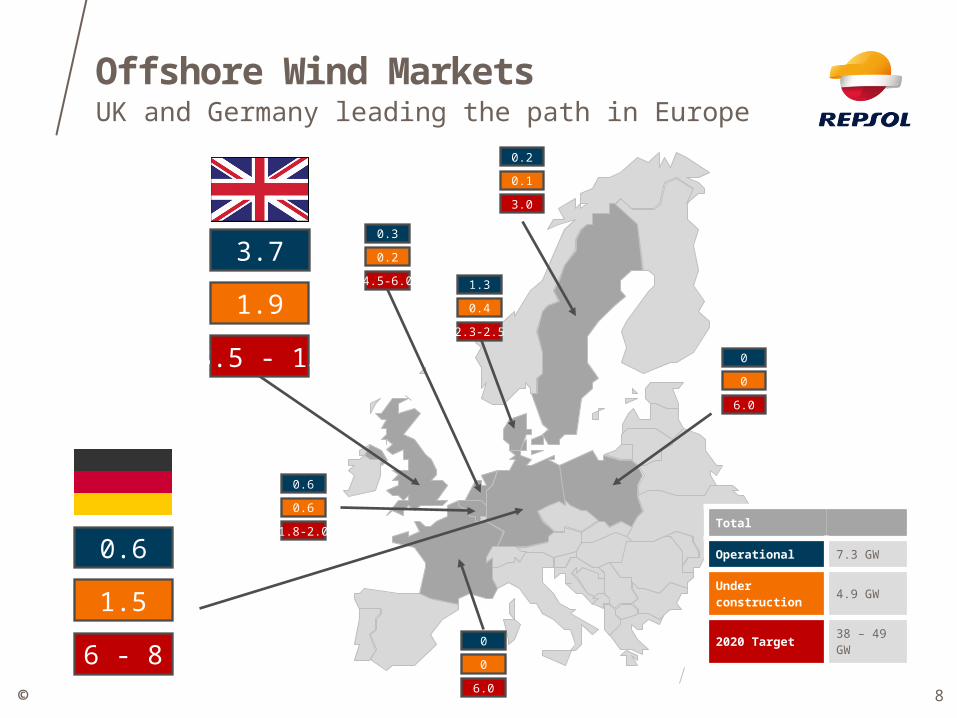

Offshore Wind MarketsUK and Germany leading the path in Europe

Total

Operational 7.3 GW

Under construction

4.9 GW

2020 Target38 – 49 GW

0.6

0.6

1.8-2.0

3.7

1.9

8.5 - 13

0.3

0.2

4.5-6.0

0.2

0.1

3.0

0.6

1.5

6 - 8

1.3

0.4

2.3-2.5

0

0

6.0

0

0

6.0

© 9

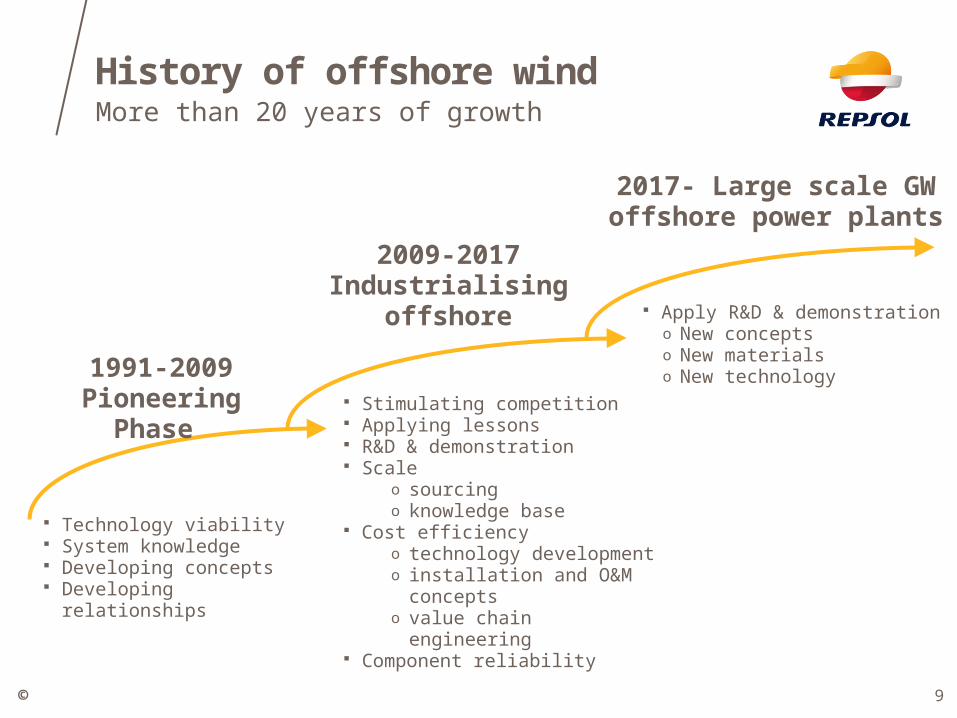

History of offshore windMore than 20 years of growth

Technology viability System knowledge Developing concepts Developing relationships

1991-2009Pioneering Phase

2009-2017Industrialising

offshore

2017- Large scale GW offshore power plants

Stimulating competition Applying lessons R&D & demonstration Scale

o sourcingo knowledge base

Cost efficiencyo technology developmento installation and O&M conceptso value chain engineering

Component reliability

Apply R&D & demonstration o New conceptso New materialso New technology

© 10

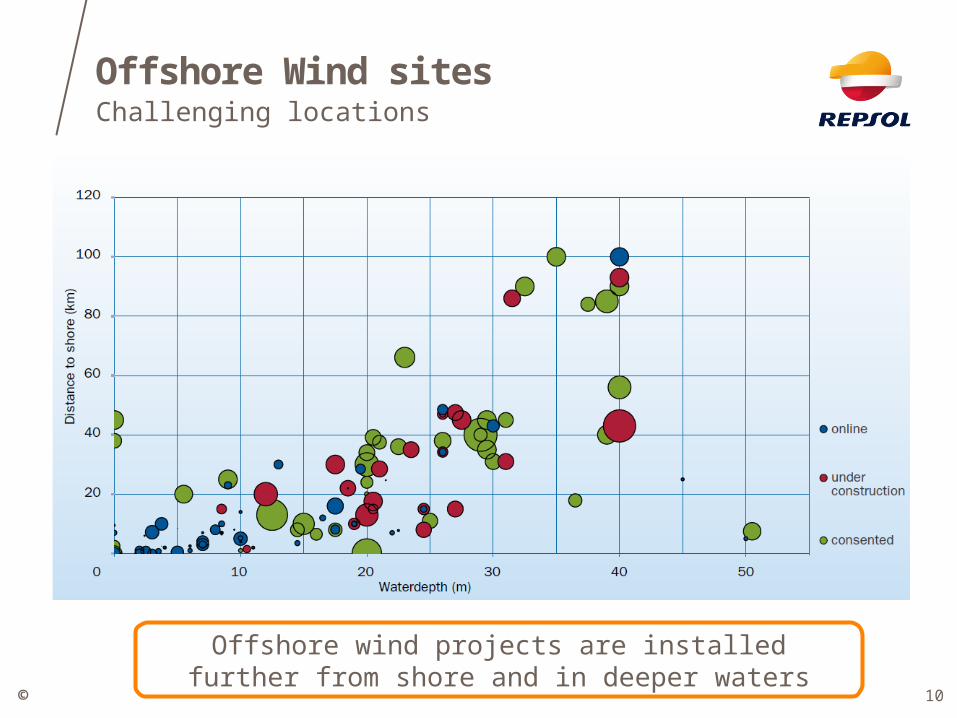

Offshore Wind sitesChallenging locations

Offshore wind projects are installed further from shore and in deeper waters

© 11

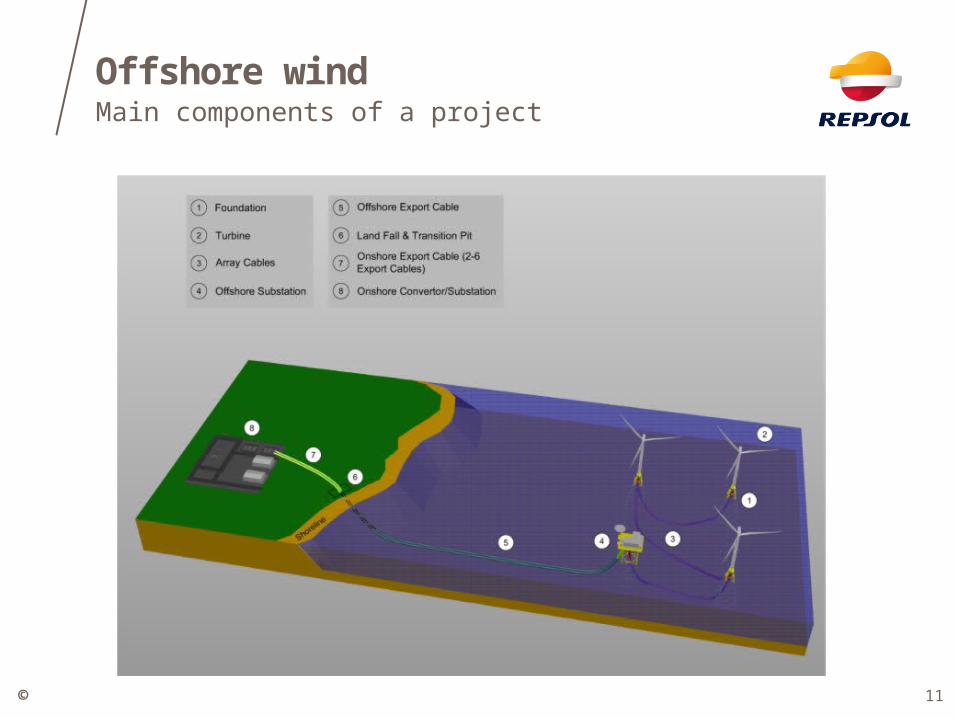

Offshore windMain components of a project

© 12

Offshore windSize and Logistics

© 13

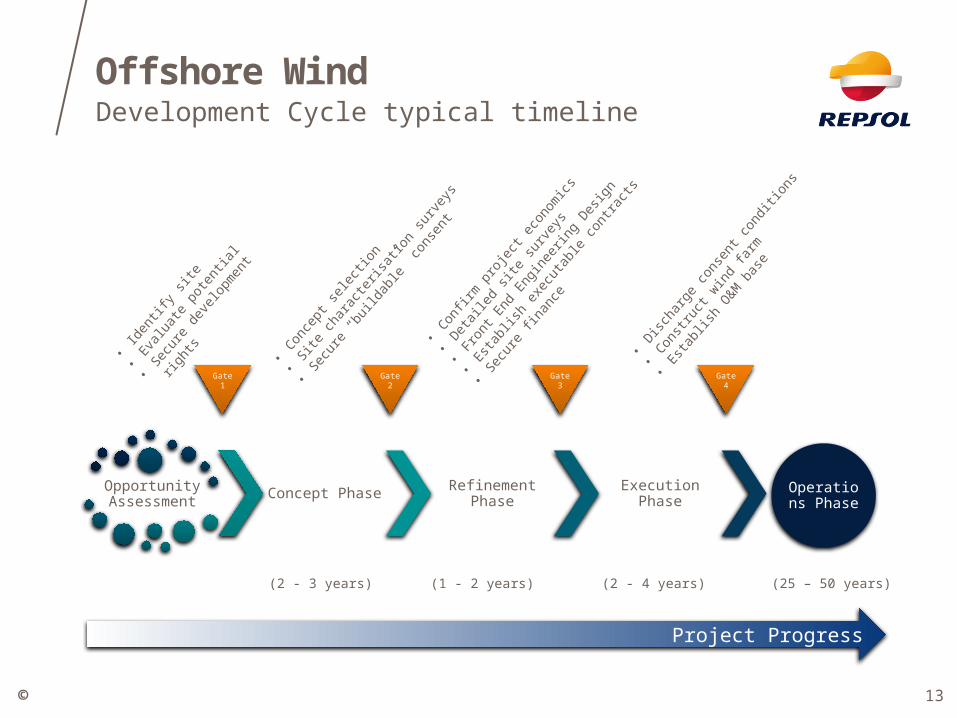

Offshore WindDevelopment Cycle typical timeline

Opportunity Assessment

Concept Phase Refinement Phase Execution Phase Operations

Phase

Gate 1 Gate 2 Gate 3 Gate 4

•Id

entif

y sit

e

•Eva

luat

e po

tent

ial

•Sec

ure

deve

lopm

ent r

ight

s

•Con

cept

sel

ectio

n

•Site

cha

ract

erisa

tion

surv

eys

•Sec

ure

“bui

ldab

le” c

onse

nt•

Confir

m p

roje

ct e

cono

mics

•Det

aile

d sit

e su

rvey

s

•Fr

ont E

nd E

ngin

eerin

g Des

ign

•Est

ablis

h ex

ecut

able

con

tract

s

•Sec

ure

finan

ce

•Disc

harg

e co

nsen

t con

ditio

ns

•Con

stru

ct w

ind

farm

•Est

ablis

h O

&M b

ase

Project Progress

(2 - 3 years) (1 - 2 years) (2 - 4 years) (25 – 50 years)

© 14

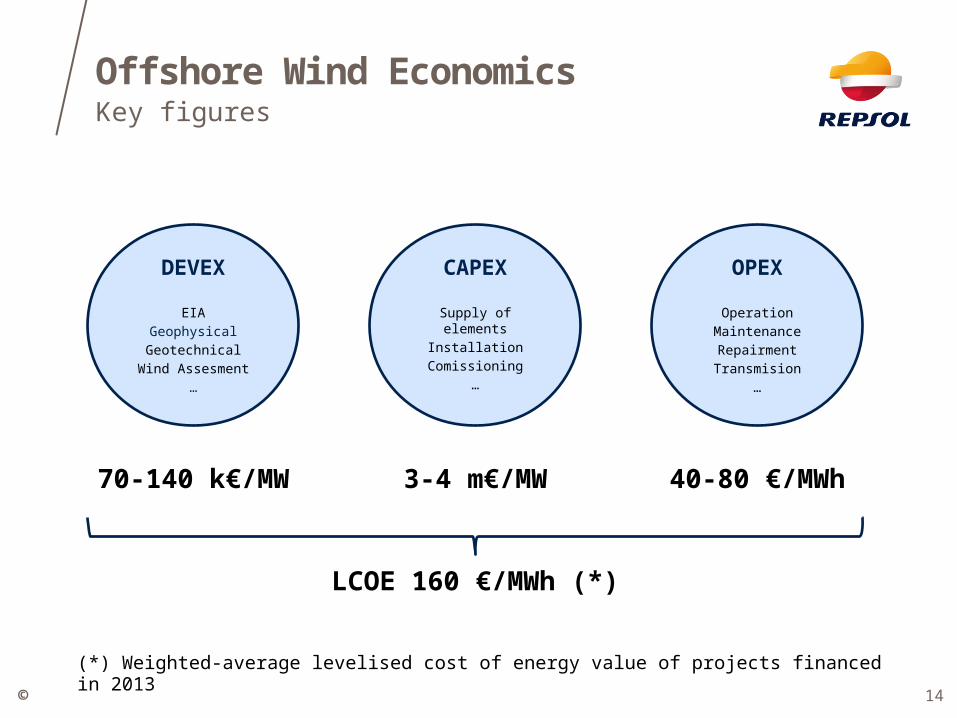

Offshore Wind EconomicsKey figures

DEVEX

EIA

Geophysical

Geotechnical

Wind Assesment

…

CAPEX

Supply of elements

Installation

Comissioning

…

OPEX

Operation

Maintenance

Repairment

Transmision

…

70-140 k€/MW 3-4 m€/MW 40-80 €/MWh

LCOE 160 €/MWh (*)

(*) Weighted-average levelised cost of energy value of projects financed in 2013

©

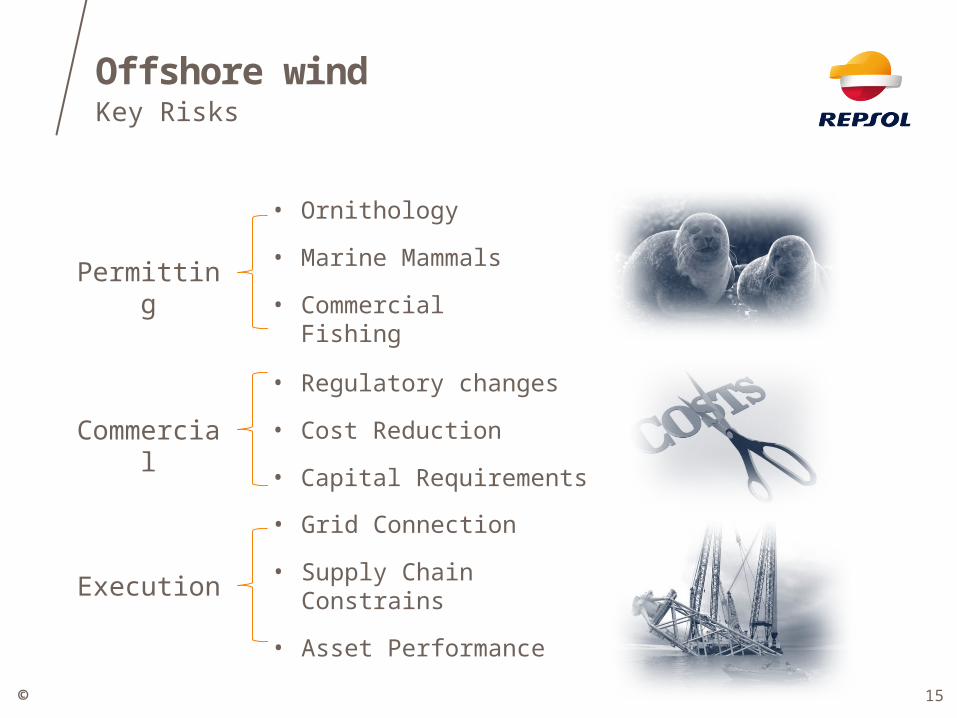

Offshore windKey Risks

• Ornithology

• Marine Mammals

• Commercial Fishing

Permitting

• Regulatory changes

• Cost Reduction

• Capital Requirements

Commercial

• Grid Connection

• Supply Chain Constrains

• Asset Performance

Execution

15

© 16

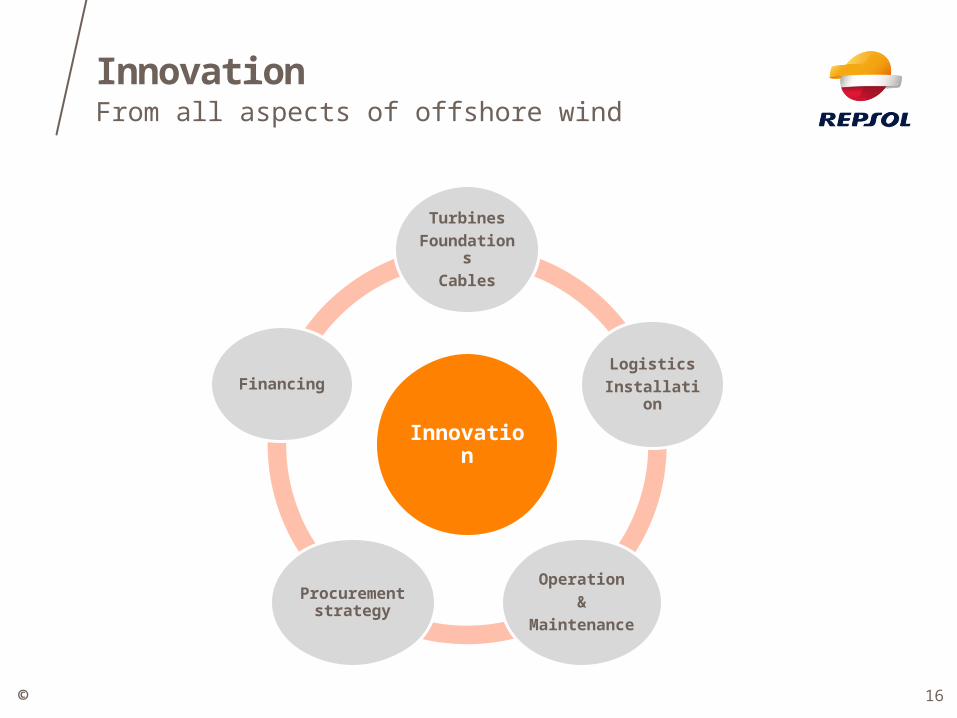

InnovationFrom all aspects of offshore wind

Innovation

Turbines

Foundations

Cables

Logistics

Installation

Operation

&

Maintenance

Procurement strategy

Financing

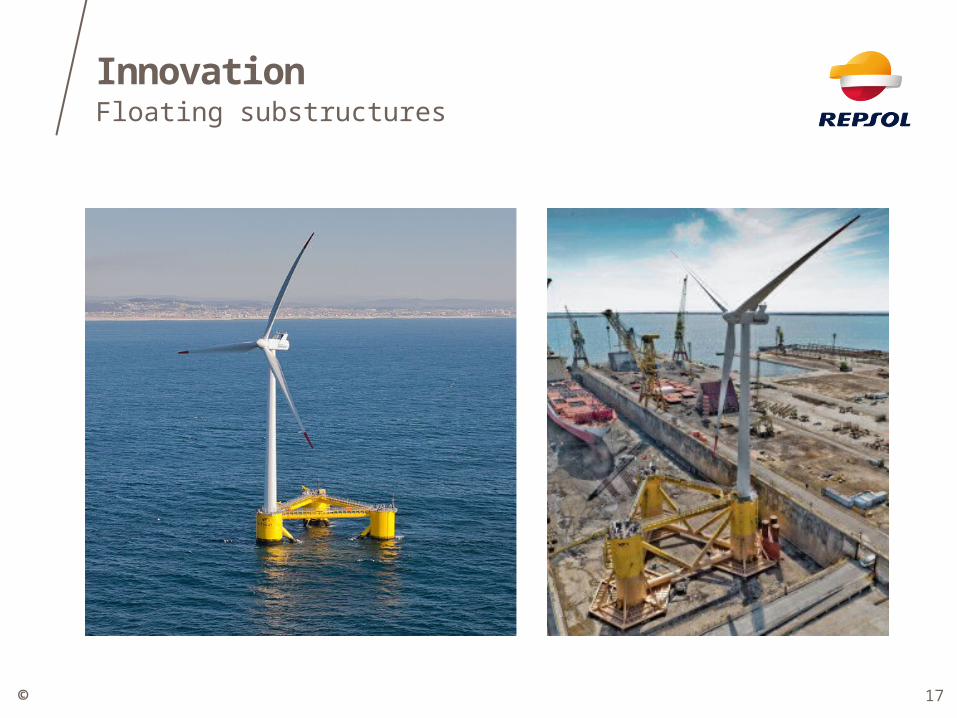

© 17

InnovationFloating substructures

© 18

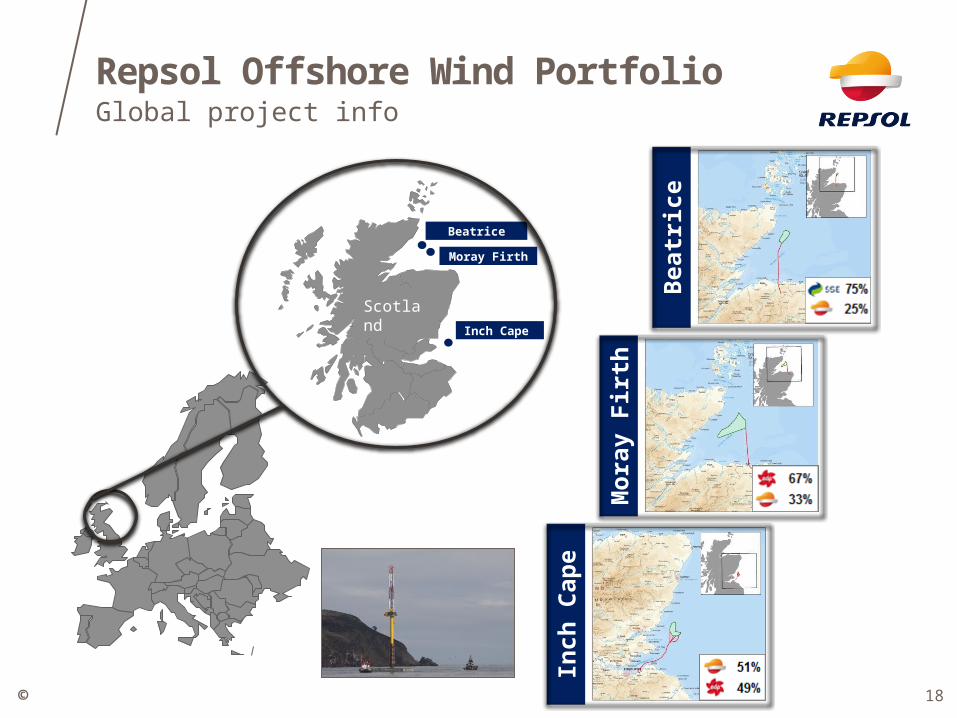

Repsol Offshore Wind PortfolioGlobal project info

Inch

Cap

e

Mo

ray

Fir

th

Bea

tric

e

Moray Firth

Beatrice

Scotland

Inch Cape

© 19

Repsol Offshore Wind PortfolioMet Mast

©

CONTENTS

20

1. Global context of renewables

2. Offshore Wind• Markets• Concepts and key figures• Risks

3. Conclusions

© 21

ConclusionsOffshore Wind

● Installed capacity is expected to grow during this decade, mainly in Europe, although not as much as estimated 3-4 years ago

● Interest in the offshore sector continues to grow, with investor commitments, policy support and technological innovations driving the industry forward

● Growing cost concerns, due to deeper waters and further from shore, need to be addressed for offshore to become cost-competitive

● More competition has to be achieved at the supply chain level in order to allow cost reduction and standardization

● Offshore wind presents significant risks at all stages of the project (Development, Construction and Operation) but can be mitigated through proper project management