Embed Size (px)

Citation preview

Making Investment Decisions with the Net Present Value Rule

Principles of Corporate FinanceBrealey and Myers Sixth Edition

Slides by

Matthew Will Chapter 6

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 2

Topics Covered

What To Discount IM&C Project Project Interaction

Timing Equivalent Annual Cost Replacement Cost of Excess Capacity Fluctuating Load Factors

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 3

What To Discount

Only Cash Flow is Relevant

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 4

What To Discount

Only Cash Flow is Relevant

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 5

What To Discount

Do not confuse average with incremental payoff.

Include all incidental effects.Do not forget working capital requirements.Forget sunk costs.Include opportunity costs.Beware of allocated overhead costs.

Points to “Watch Out For”

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 6

Be consistent in how you handle inflation!! Use nominal interest rates to discount

nominal cash flows. Use real interest rates to discount real cash

flows. You will get the same results, whether you

use nominal or real figures.

Inflation

INFLATION RULEINFLATION RULE

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 7

Inflation

Example

You own a lease that will cost you $8,000 next year, increasing at 3% a year (the forecasted inflation rate) for 3 additional years (4 years total). If discount rates are 10% what is the present value cost of the lease?

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 8

Inflation

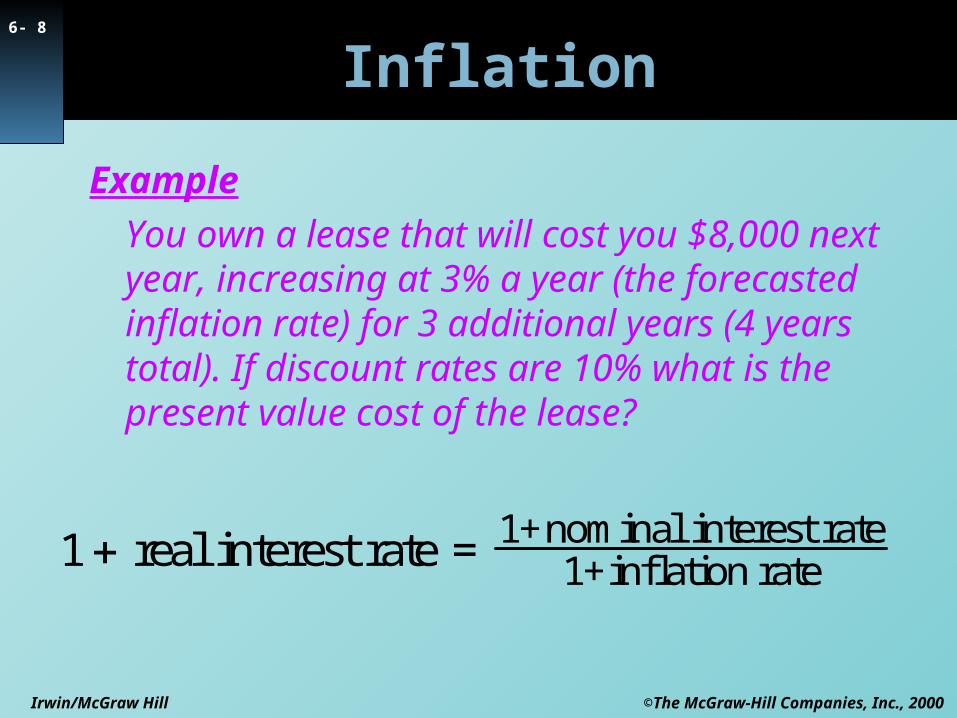

Example

You own a lease that will cost you $8,000 next year, increasing at 3% a year (the forecasted inflation rate) for 3 additional years (4 years total). If discount rates are 10% what is the present value cost of the lease?

1 real interest rate = 1+nominal interest rate1+inflation rate

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 9

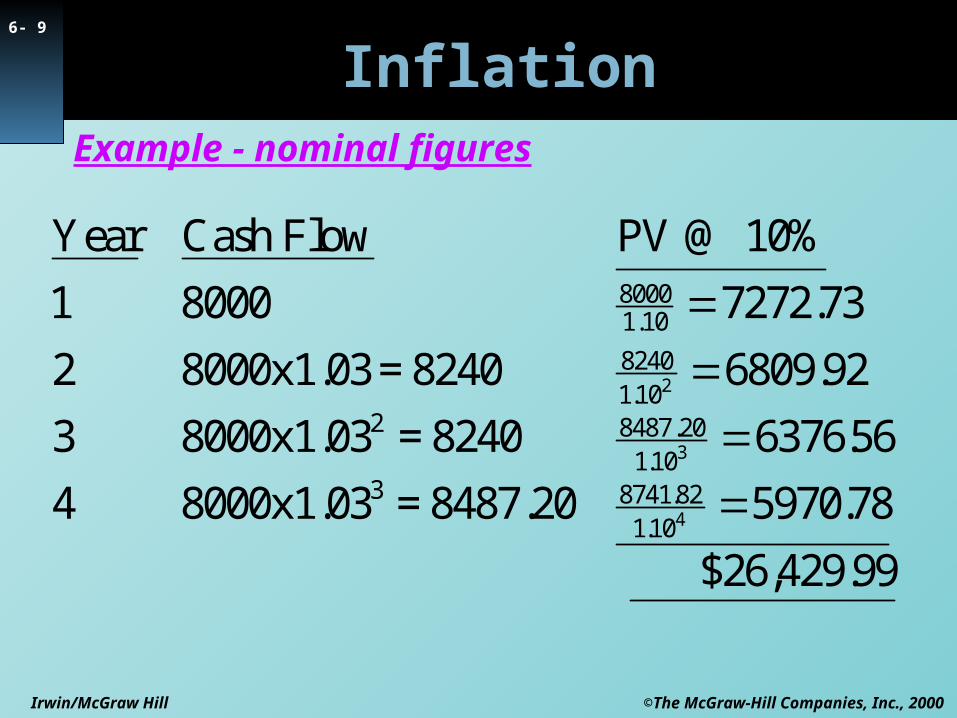

InflationExample - nominal figures

Year Cash Flow PV @ 10%

1 8000

2 8000x1.03 = 8240

8000x1.03 = 8240

8000x1.03 = 8487.20

80001.10

2

3

7272 73

6809 92

3 6376 56

4 5970 78

429 99

82401 108487 20

1 108741 82

1 10

2

3

4

.

.

.

.

$26, .

..

..

.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 10

InflationExample - real figures

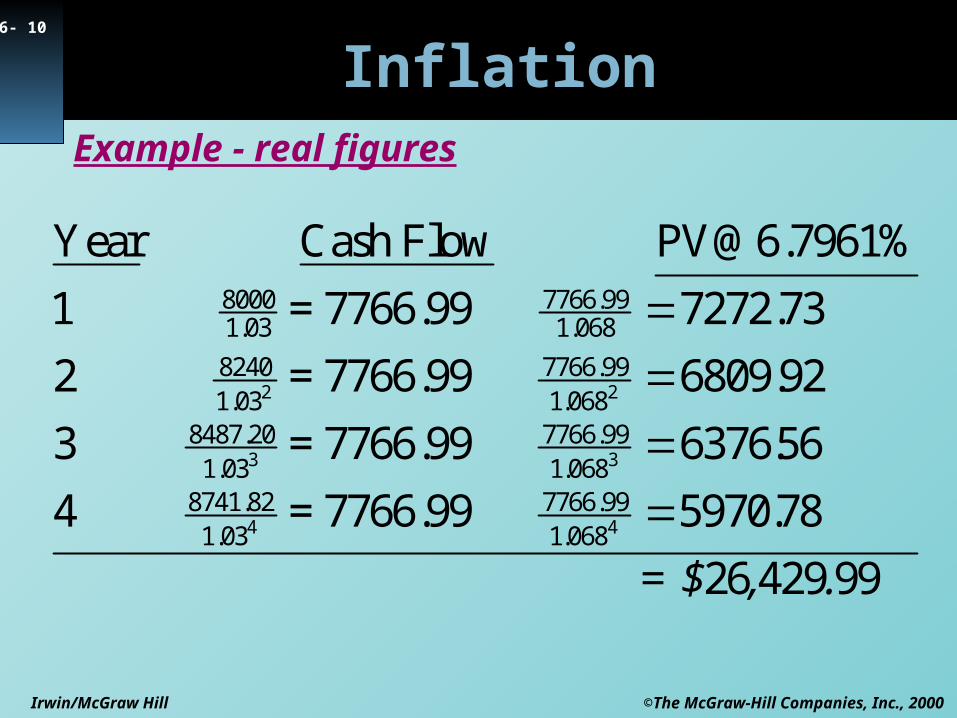

Year Cash Flow [email protected]%

1 = 7766.99

2 = 7766.99

= 7766.99

= 7766.99

80001.03

7766.991.068

82401.03

8487.201.03

8741.821.03

2

3

4

7272 73

6809 92

3 6376 56

4 5970 78

26 429 99

7766 991 068

7766 991 068

7766 991 068

2

3

4

.

.

.

.

..

..

..

= $ , .

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 11

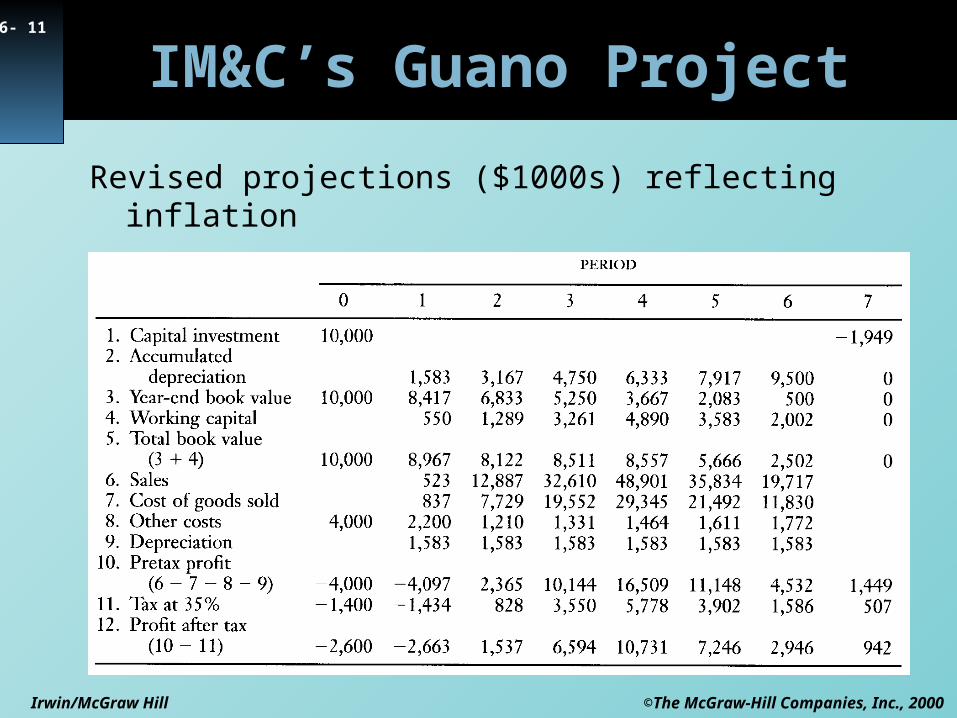

IM&C’s Guano Project

Revised projections ($1000s) reflecting inflation

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 12

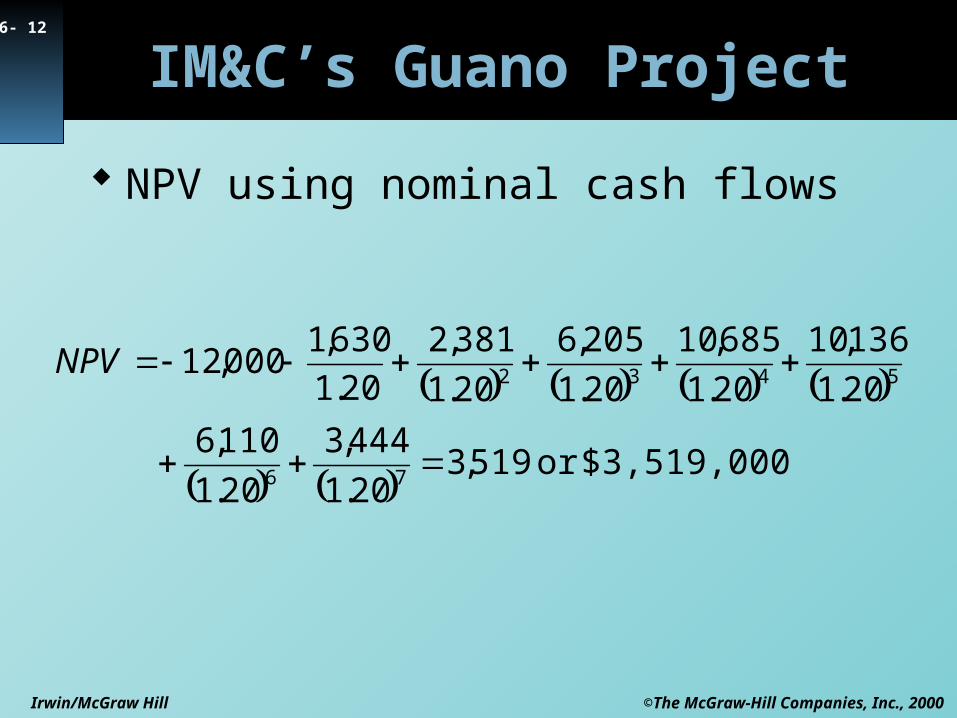

IM&C’s Guano Project

NPV using nominal cash flows

$3,519,000or 519,320.1

444,3

20.1

110,6

20.1

136,10

20.1

685,10

20.1

205,6

20.1

381,2

20.1

630,1000,12

76

5432

NPV

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 13

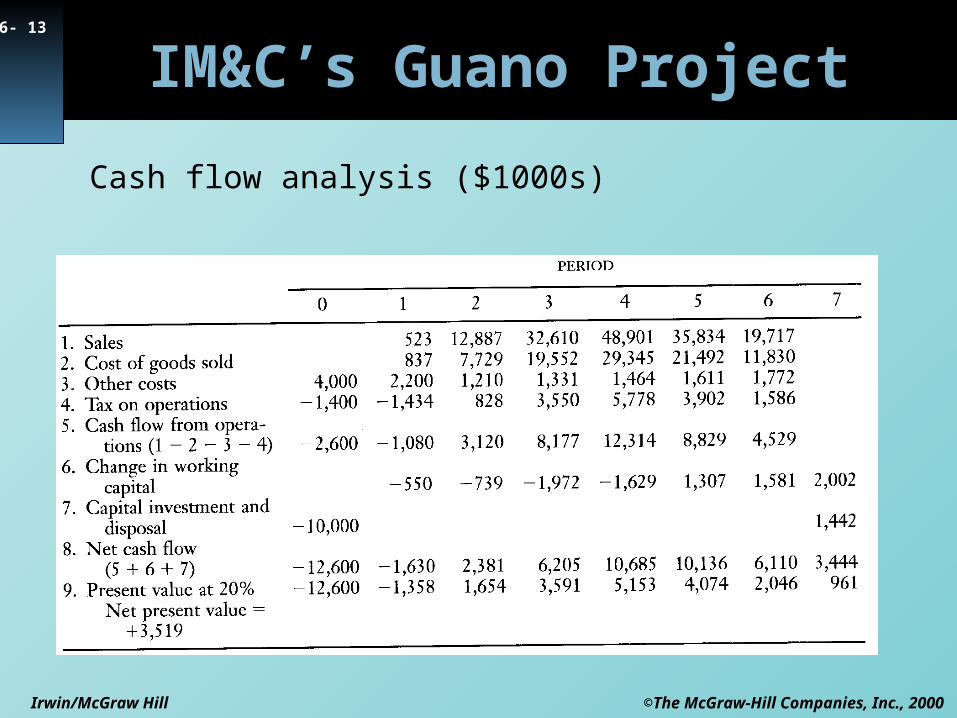

IM&C’s Guano Project

Cash flow analysis ($1000s)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 14

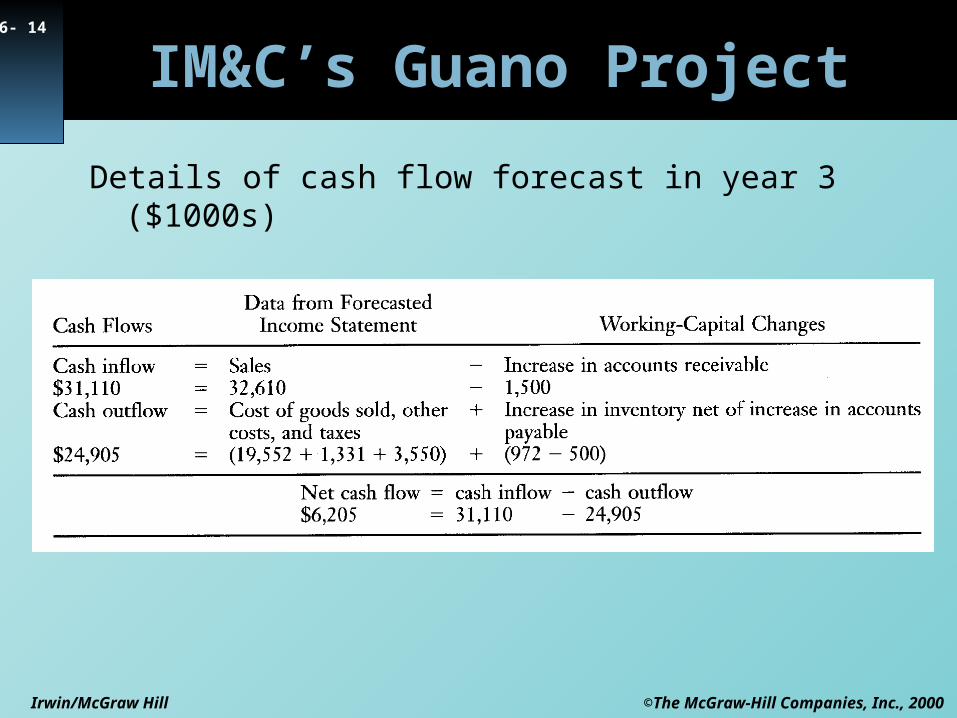

IM&C’s Guano Project

Details of cash flow forecast in year 3 ($1000s)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 15

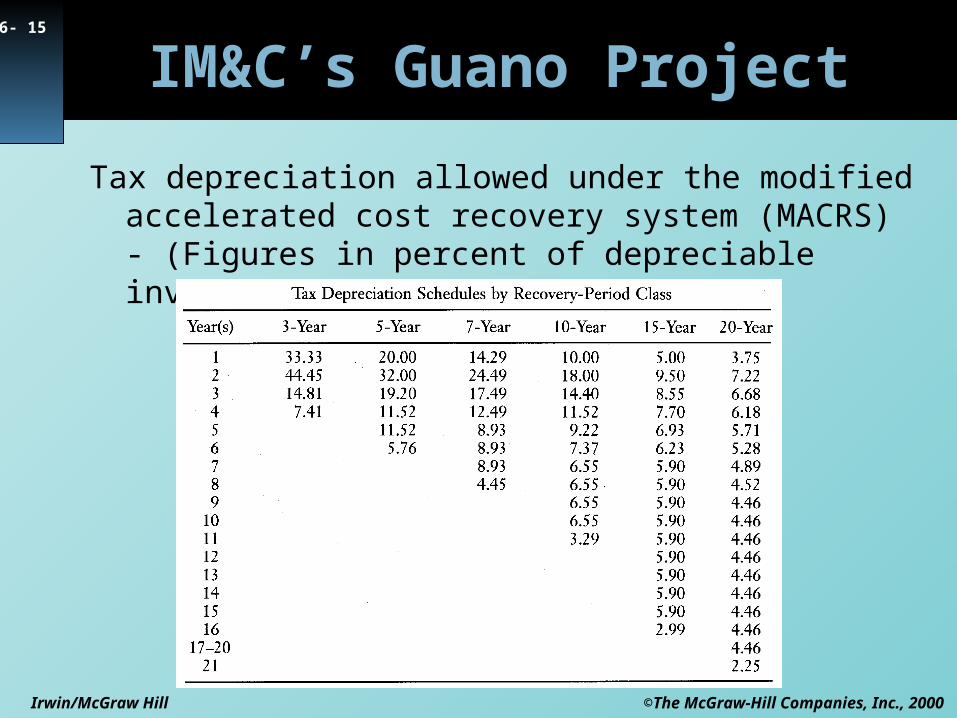

IM&C’s Guano Project

Tax depreciation allowed under the modified accelerated cost recovery system (MACRS) - (Figures in percent of depreciable investment).

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 16

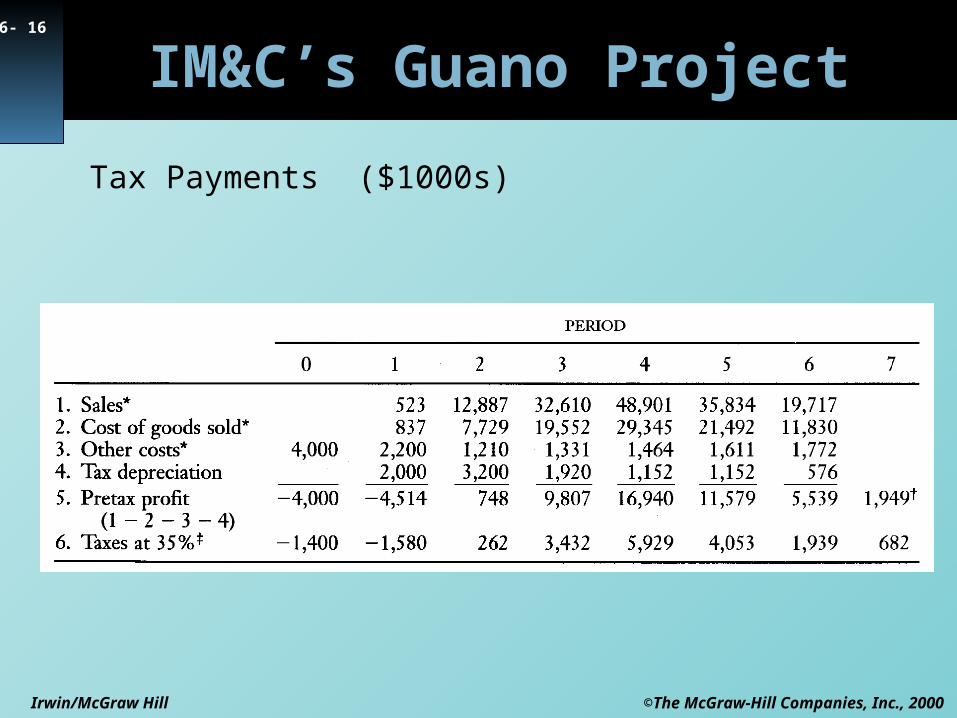

IM&C’s Guano Project

Tax Payments ($1000s)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 17

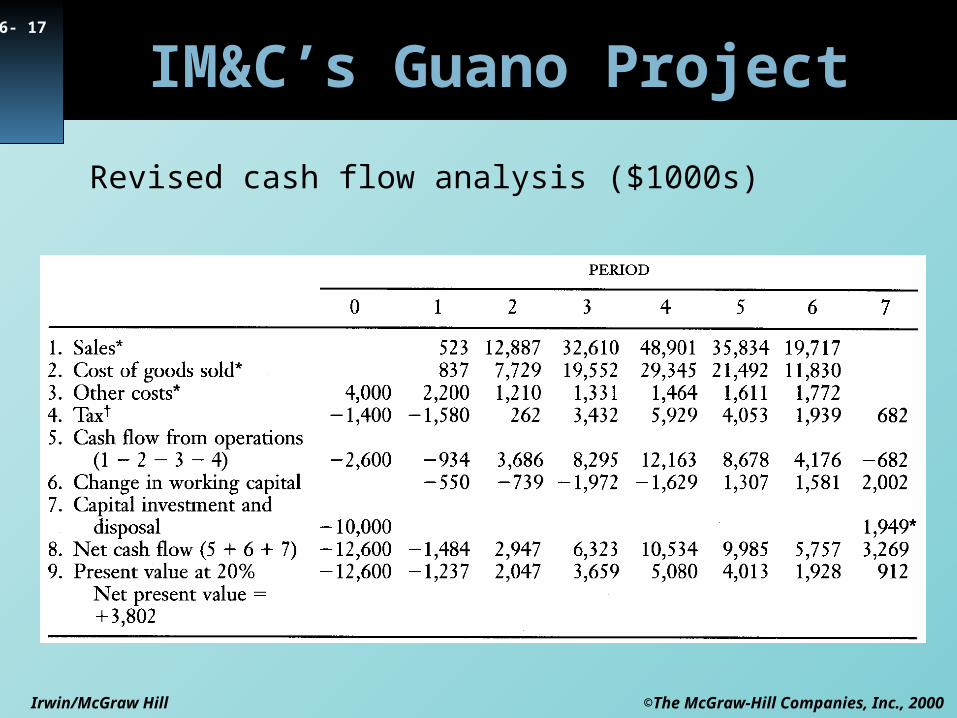

IM&C’s Guano Project

Revised cash flow analysis ($1000s)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 18

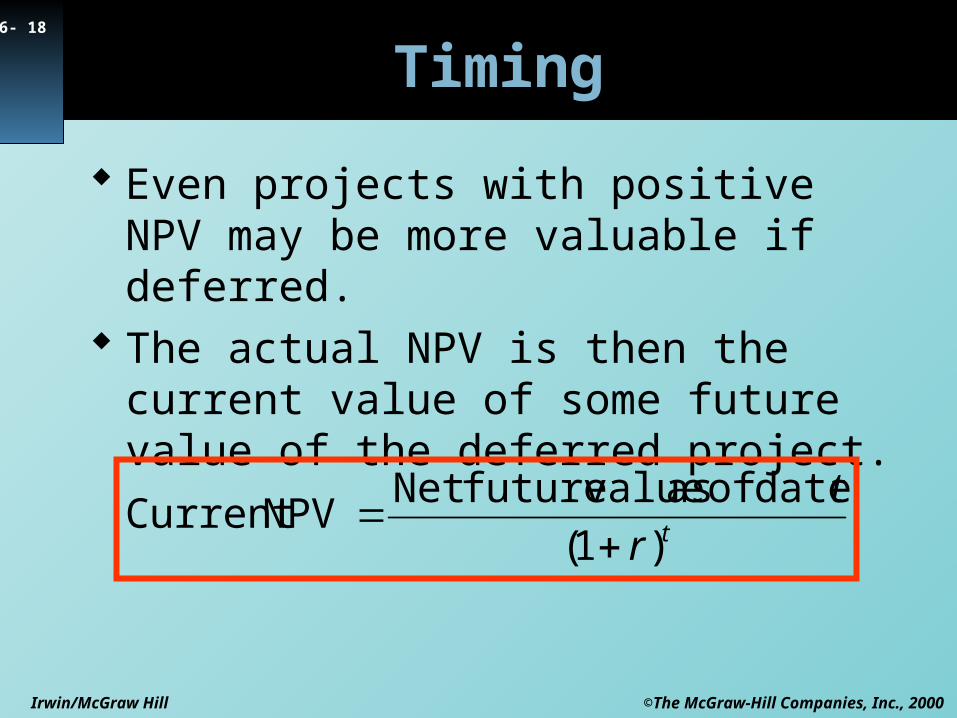

Timing

Even projects with positive NPV may be more valuable if deferred.

The actual NPV is then the current value of some future value of the deferred project.

tr

t

)1(

date of as valuefutureNet NPVCurrent

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 19

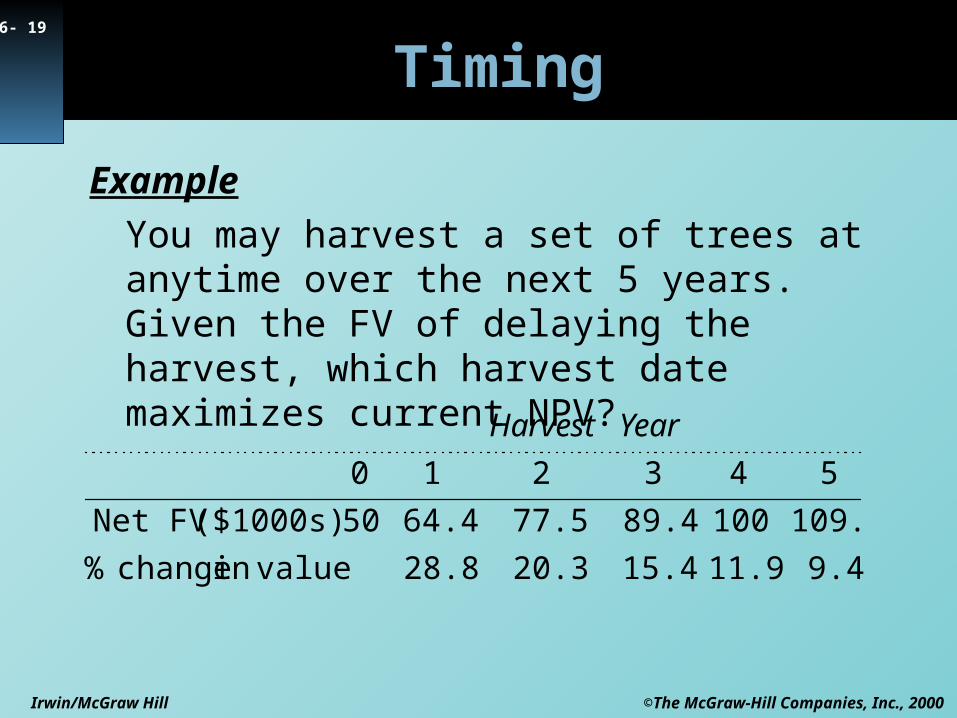

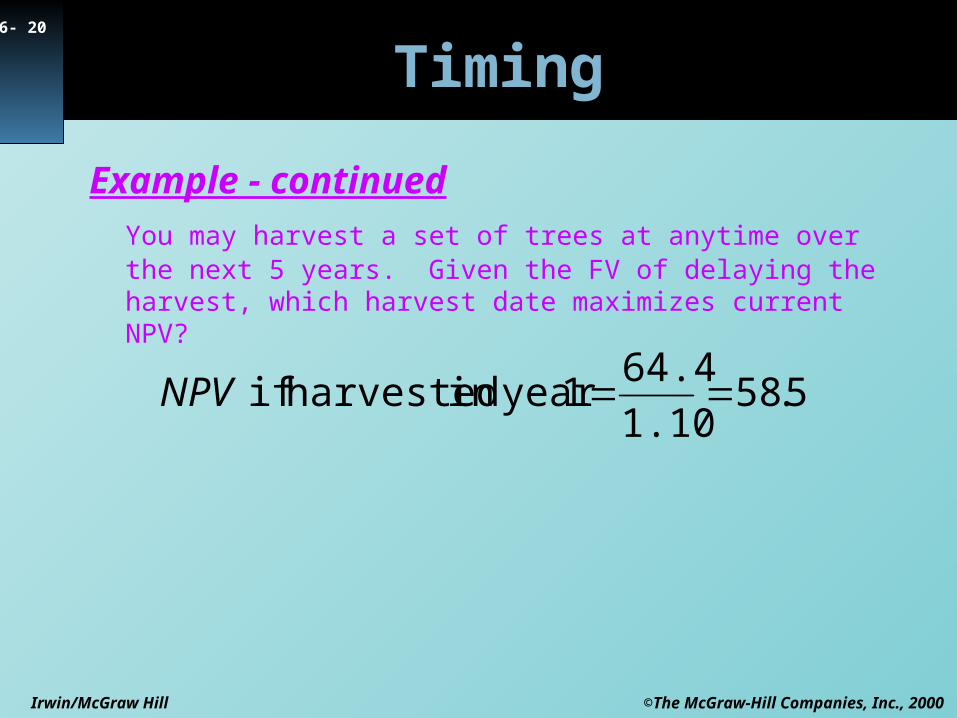

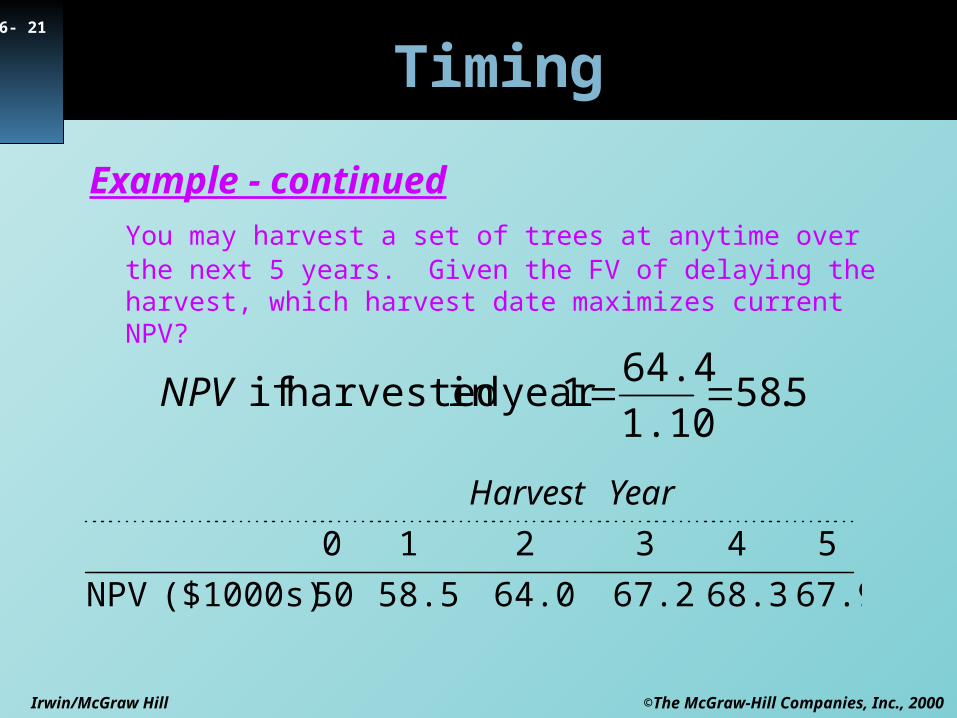

Timing

Example

You may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

9.411.915.420.328.8 valuein change %

109.410089.477.564.450($1000s) Net FV

543210

YearHarvest

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 20

Timing

Example - continuedYou may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

5.581.10

64.41 year in harvested if NPV

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 21

Timing

Example - continuedYou may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

5.581.10

64.41 year in harvested if NPV

67.968.367.264.058.550($1000s) NPV

543210

YearHarvest

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 22

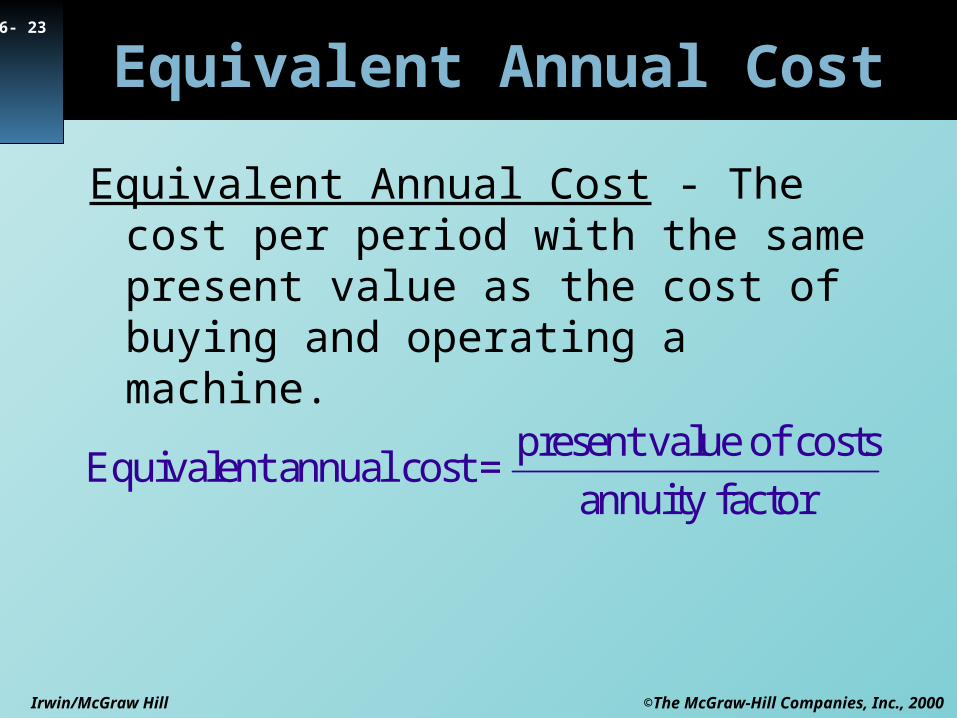

Equivalent Annual Cost

Equivalent Annual Cost - The cost per period with the same present value as the cost of buying and operating a machine.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 23

Equivalent Annual Cost

Equivalent Annual Cost - The cost per period with the same present value as the cost of buying and operating a machine.

Equivalent annual cost =present value of costs

annuity factor

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 24

Equivalent Annual Cost

Example

Given the following costs of operating two machines and a 6% cost of capital, select the lower cost machine using equivalent annual cost method.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 25

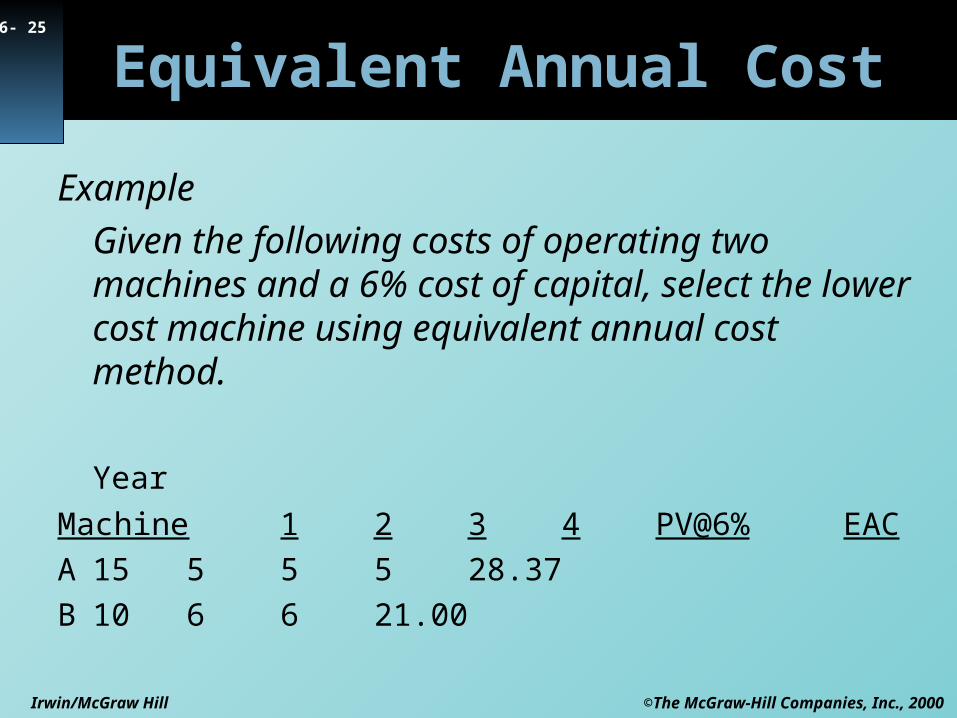

Equivalent Annual Cost

Example

Given the following costs of operating two machines and a 6% cost of capital, select the lower cost machine using equivalent annual cost method.

Year

Machine 1 2 3 4 PV@6% EAC

A 15 5 5 5 28.37

B 10 6 6 21.00

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 26

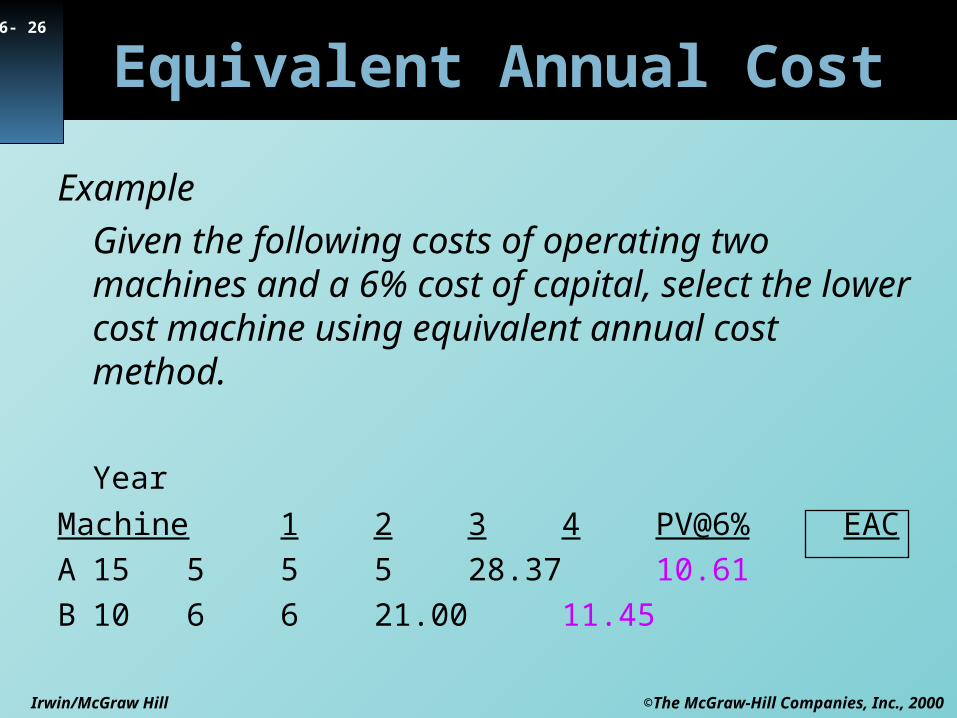

Example

Given the following costs of operating two machines and a 6% cost of capital, select the lower cost machine using equivalent annual cost method.

Year

Machine 1 2 3 4 PV@6% EAC

A 15 5 5 5 28.37 10.61

B 10 6 6 21.00 11.45

Equivalent Annual Cost

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

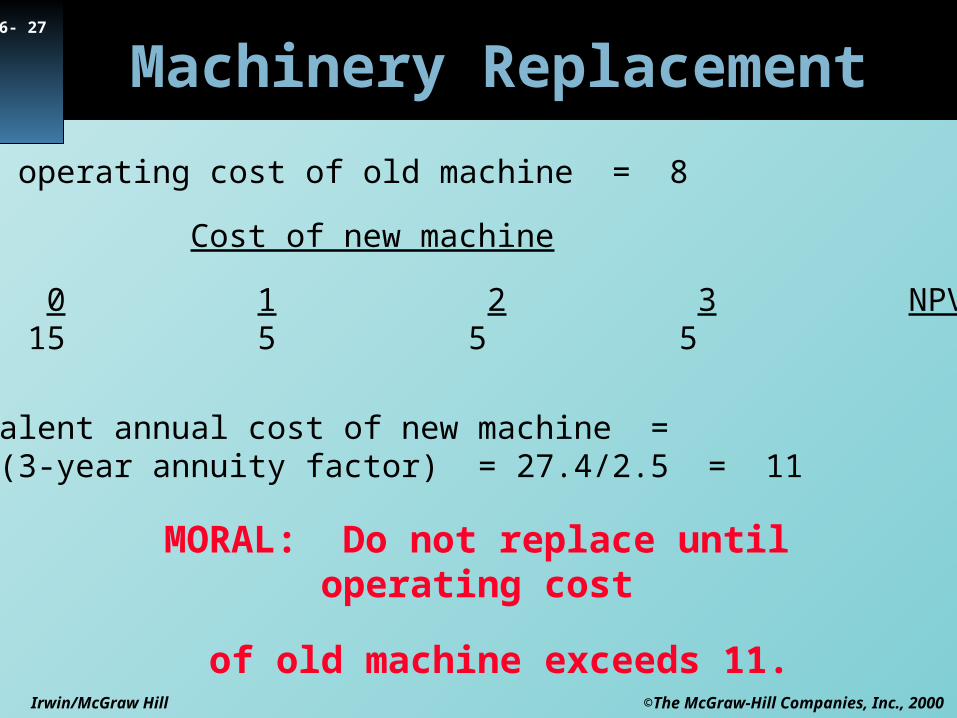

6- 27

Machinery Replacement

Annual operating cost of old machine = 8

Cost of new machine

Year: 0 1 2 3 NPV @ 10% 15 5 5 5 27.4

Equivalent annual cost of new machine = 27.4/(3-year annuity factor) = 27.4/2.5 = 11

MORAL: Do not replace until operating cost

of old machine exceeds 11.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 28

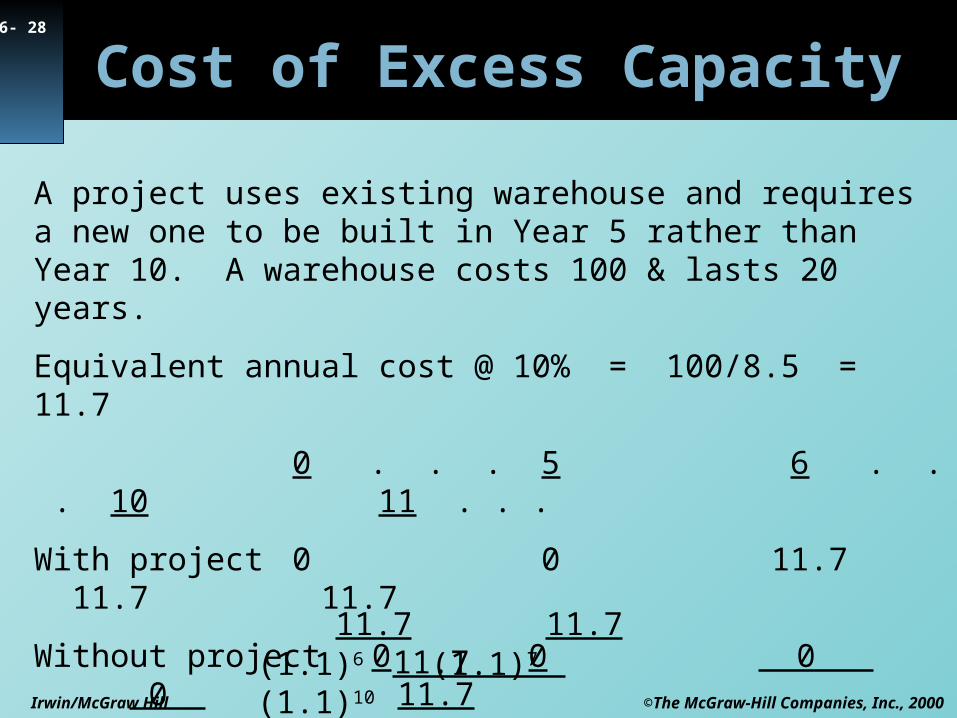

Cost of Excess Capacity

A project uses existing warehouse and requires a new one to be built in Year 5 rather than Year 10. A warehouse costs 100 & lasts 20 years.

Equivalent annual cost @ 10% = 100/8.5 = 11.7

0 . . . 5 6 . . . 10 11 . . .

With project 0 0 11.7 11.7 11.7

Without project 0 0 0 0 11.7

Difference 0 0 11.7 11.7 0

PV extra cost = + + . . . + = 27.6 11.7 11.7 11.7 (1.1)6 (1.1)7 (1.1)10

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 29

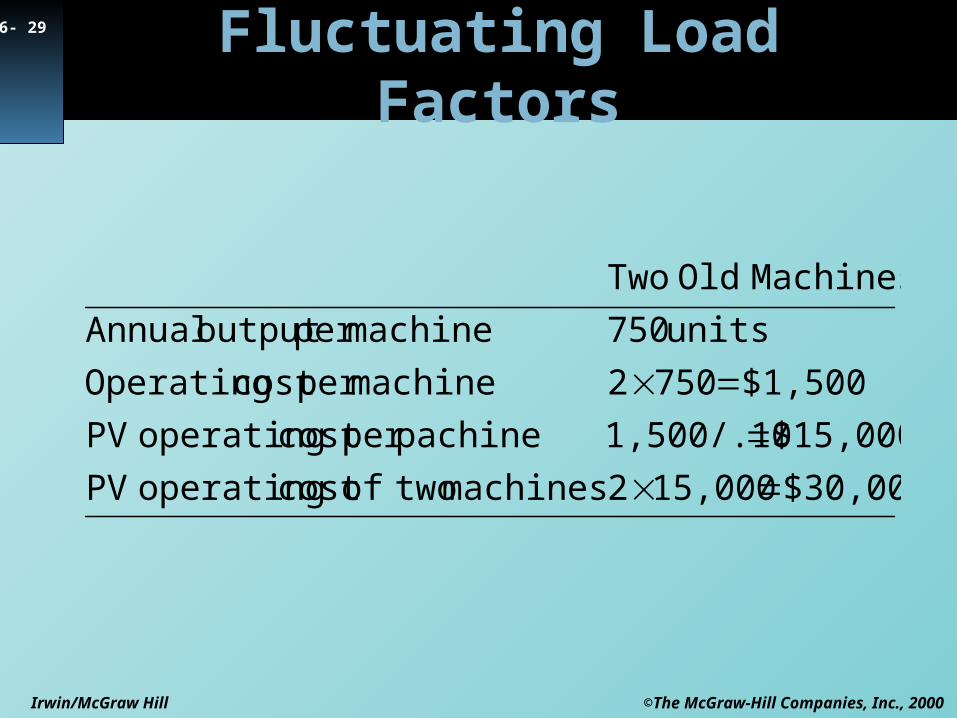

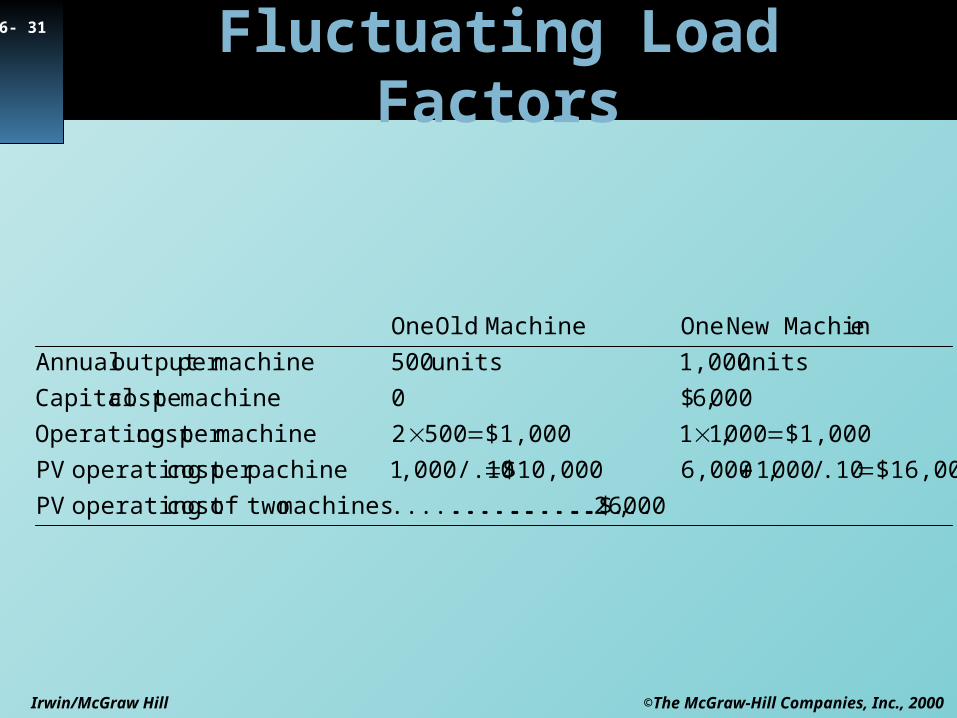

Fluctuating Load Factors

$30,00015,0002machines twoofcost operating PV

$15,0001,500/.10pachineper cost operating PV

$1,5007502machineper cost Operating

units 750machineper output Annual

MachinesOld Two

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 30

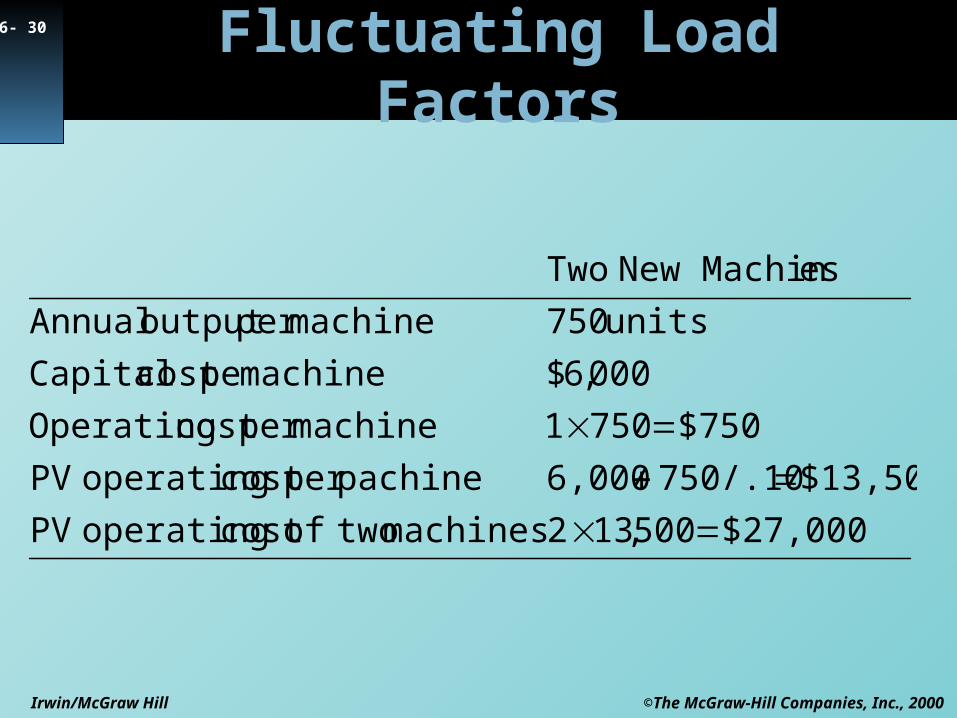

Fluctuating Load Factors

$27,000500,132machines twoofcost operating PV

$13,500750/.106,000pachineper cost operating PV

$7507501machineper cost Operating

000,6$machine pecost Capital

units 750machineper output Annual

esNew Machin Two

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

6- 31

Fluctuating Load Factors

000,26..$..............................machines twoofcost operating PV

$16,000.10/000,16,000$10,000,000/.101pachineper cost operating PV

$1,000000,11$1,0005002machineper cost Operating

000,6$0machine pecost Capital

units 1,000units 500machineper output Annual

eNew Machin One MachineOld One