Embed Size (px)

Citation preview

Financial management & reporting system

Three aspects: Accounting, Reporting & Management

Money in - Money out

Accounts Receivable, Payroll and Accounts Payable

Assets, Liabilities, & Equity

Income, Expense, Profits

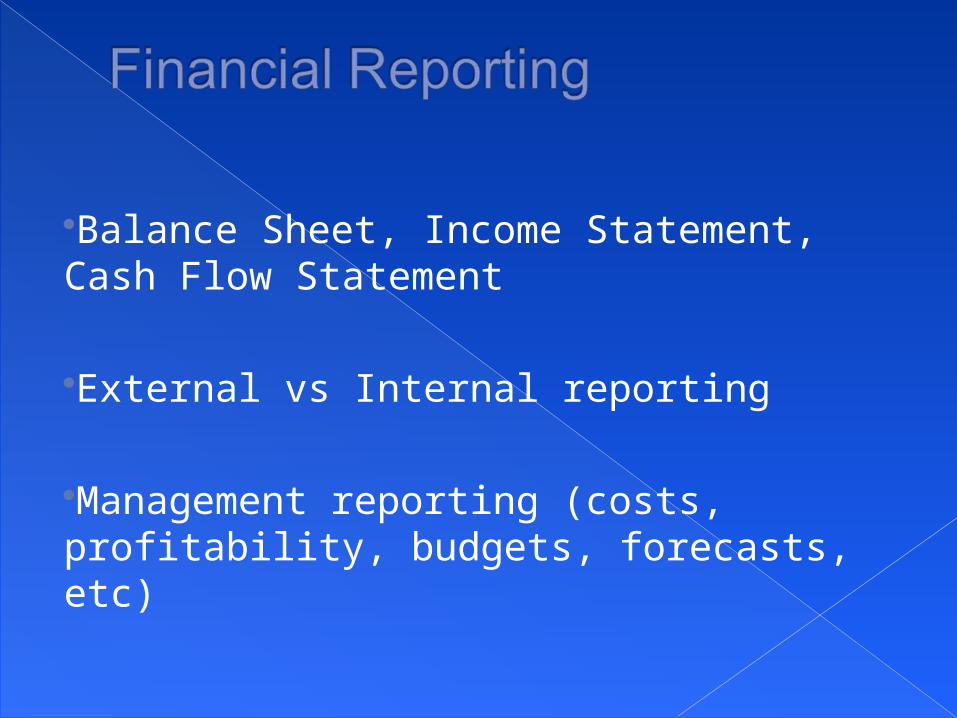

Balance Sheet, Income Statement, Cash Flow Statement

External vs Internal reporting

Management reporting (costs, profitability, budgets, forecasts, etc)

Allocation of capital

Who gets paid & when?

Cost management

1. Lay a good foundation

2. Keep it simple

3. Avoid the landmines

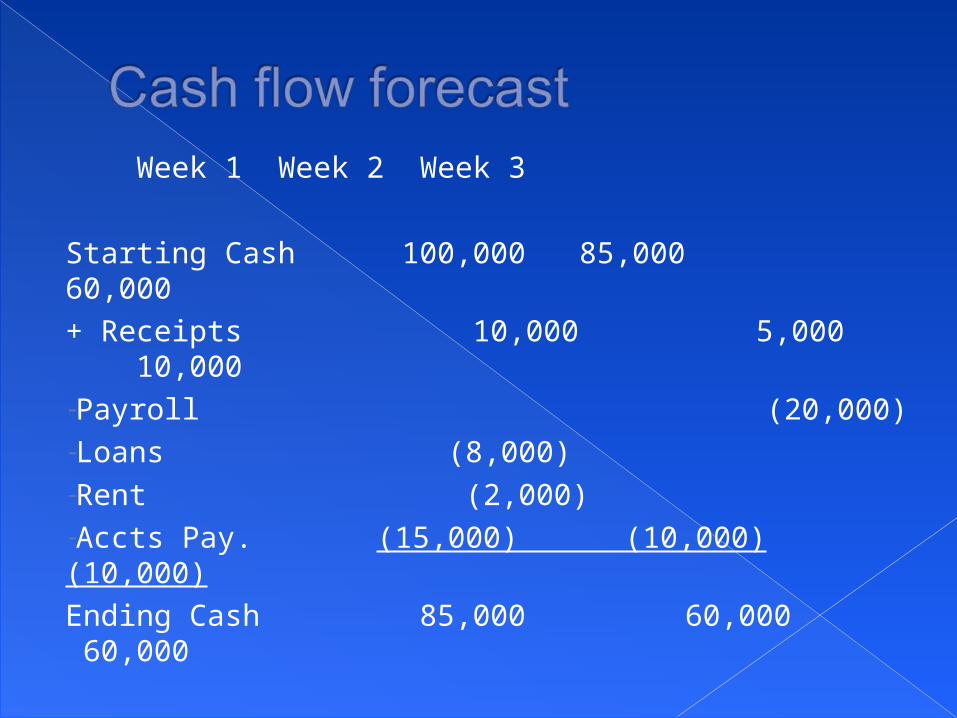

Cash flow forecast

Accounting software system

Internal controls

Procedures

Week 1 Week 2 Week 3

Starting Cash 100,000 85,000 60,000

+ Receipts 10,000 5,000 10,000 -Payroll (20,000)-Loans (8,000)-Rent (2,000)-Accts Pay. (15,000) (10,000) (10,000)

Ending Cash 85,000 60,000 60,000

Industry-Specific vs. Generic

Cloud vs. LAN

Plan for near term growth

Consider cost of maintenance

Accounting staff familiarity

Protection of assets

Reduce risk of errors in reporting

Separation of duties

Bank reconciliations

Check signing authorizations

System security controls

Keep it simple

Who does what and when

Routine deadlines – weekly, monthly, quarterly and annually

Monthly closeout schedule

Address significant accounting policies

Payroll taxes› “Responsible Person”› Trust Fund Recovery Penalty› OUTSOURCE!!

Sales taxes› Taxable vs Non-taxable sales› State specific› “Nexus”

Nexus for California:

“for sales and use tax purposes include (but are not limited to) the following:

Maintaining, occupying or using any type of office, sales room, warehouse or other place of business in California. This includes use that is temporary, indirect or through an agent or other representative.Having any kind of representative operating in the state for the purpose of taking orders, making sales or deliveries, installing, or assembling tangible personal property.Making repairs or providing maintenance or service to property sold, whether by employees, agents or other representatives.Deriving rentals from a lease of tangible personal property located in California.”

Employee vs Contractor› Employer is responsible for employees’ payroll taxes› Contractor is responsible for self-employment taxes› 20 Factor test – IRS Revenue Ruling 87-41

“In September 2011, former Secretary of Labor Hilda L. Solis announced a major step forward with the signing of a Memorandum of Understanding (MOU) between the Department and the Internal Revenue Service (IRS). Under this agreement, the agencies will work together and share information to reduce the incidence of misclassification of employees, to help reduce the tax gap, and to improve compliance with federal labor laws.”

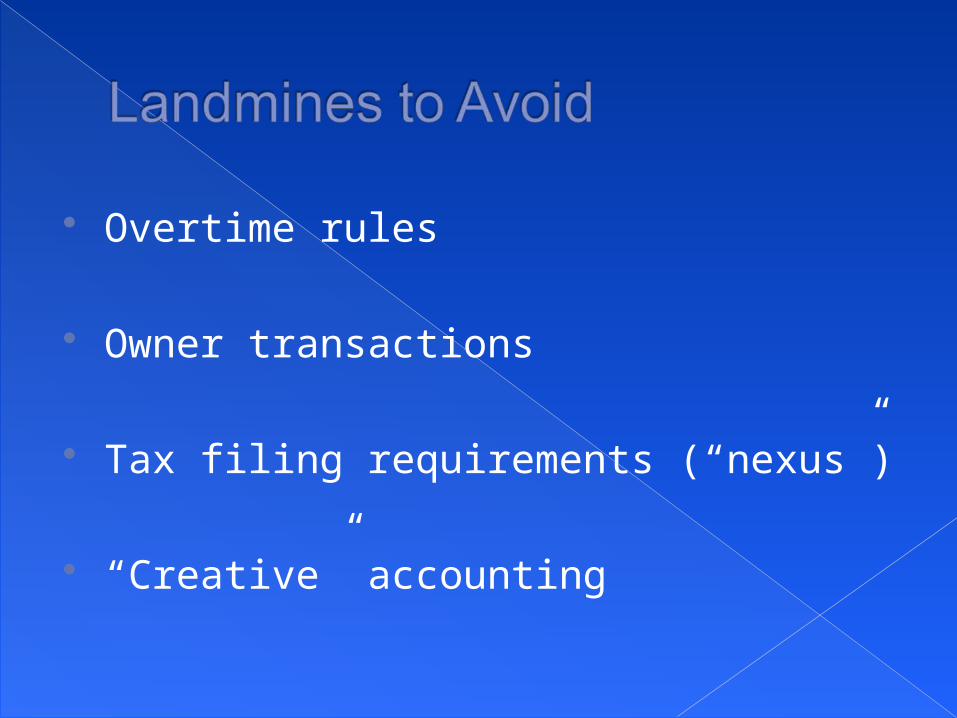

Overtime rules

Owner transactions

Tax filing requirements (“nexus”)

“Creative” accounting

Todd Giustiniano, CPA

E.K. Lozano & Company

CPA’s & Consultants

220 Dalwill Drive

Mandeville, La 70471

985-727-9695