Embed Size (px)

Citation preview

1

BY PEOPLE. WITH PEOPLE. FOR PEOPLE.

:: EBDC 2013 - SESSION III

COMPELLING MARKET OPPORTUNITIES FOR RARE AND ULTRA RARE DISEASES: WHAT ARE THE FINANCIAL, CLINICAL AND REGULATORY RIS KS INVOLVED?

DR. ALDO AMMENDOLA, DUESSELDORF, SEPTEMBER 24, 2013

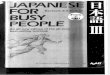

2

MOST RARE/ORPHAN DISEASES HAVE NO PARENTS…

US: when disease affects fewer than 7.5 in 10,000

individuals per year (<200,000)

6,000 – 8,000 rare diseases known (250 new diseases per year)

30 million people suffering from rare diseases in the EU

80% of genetic origin, 50% affecting pediatrics,chronic, severe, progressive, pain, disability, hig h rate of mortality,

few or no treatment options available

... but rare diseases are not so rare

20 million people suffering from rare diseases in the US

Sources: Orphanet, Eurordis, NORD

EU: when disease affects fewer than 5 per 10,000

individuals per year (<253,000)

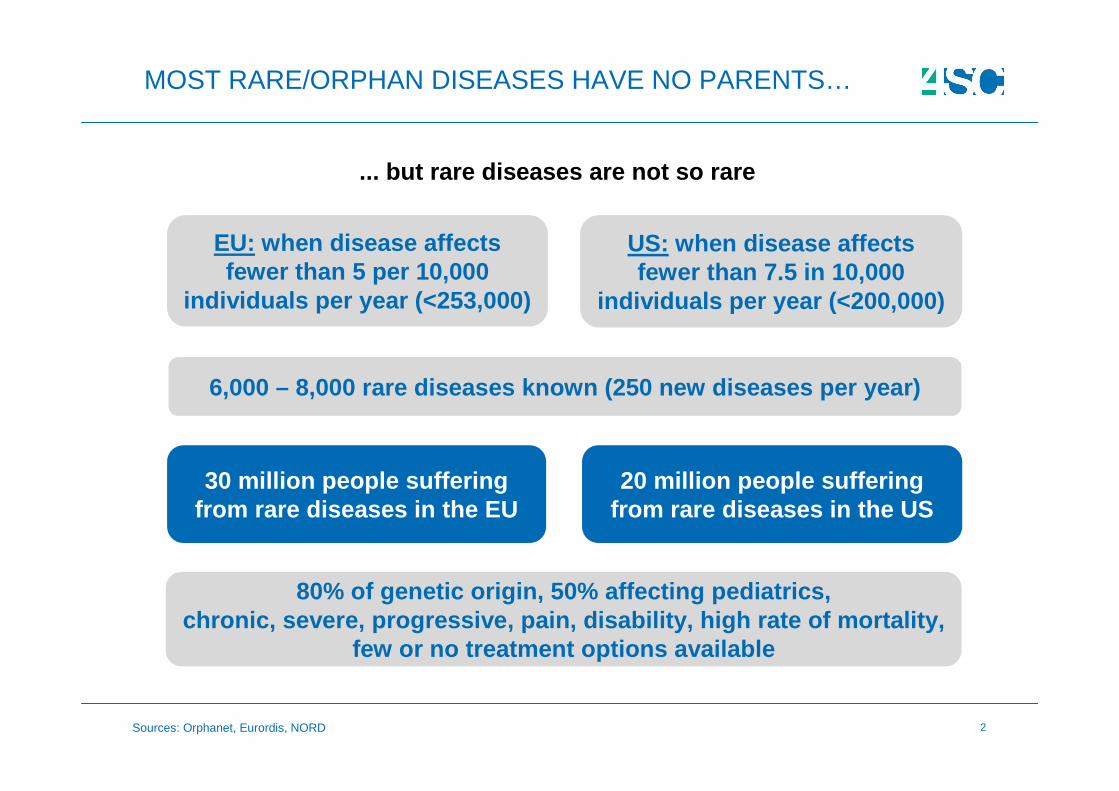

3

COMPELLING MARKET OPPORTUNITIES FOR RARE AND ULTRA RARE DISEASE DRUGS

Orphan Market: $83B in 2012growing to $127B by 2018

325 orphan drugs approvedin the period 1983-2004

Over 40 orphan drugs hit $1B global sales in 2012

460 drugs currently in clinical trials for rare diseases

About 4,000 products with orphan drug designation

Sources: Orphanet, EvaluatePharma

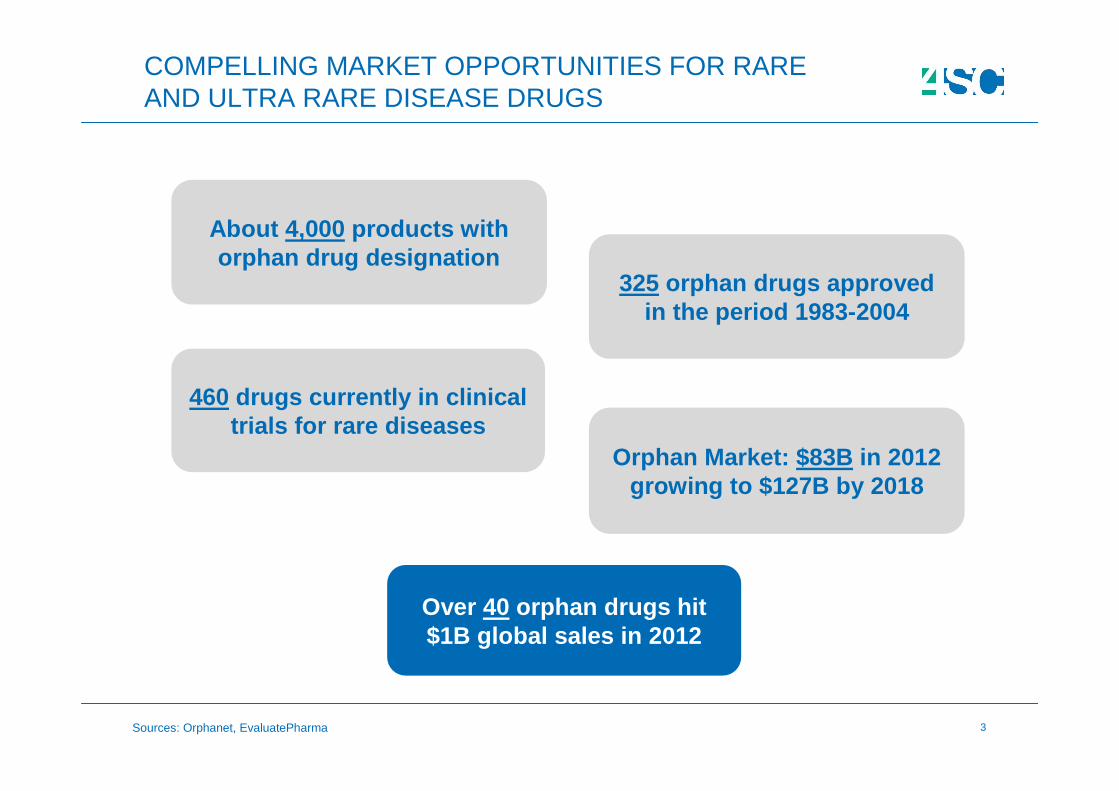

4

2012 SALES OF SELECTED DRUGS FOR RARE DISEASES

Rituxan/MabTheraNHL, CLL, RA

$7.2B

Gleevec/GlivecCML, ALL, GIST etc.

$4.7B

VelcadeMM

$2.3B

CopaxoneMS

$4.0B

RevlimidMM/MDS

$3.8B

Sources: Annual Reports, Thomson Reuters Cortellis, MedTrack, EvaluatePharma

Despite the smaller patient pool for rare diseases, orphan drugs

show great potential for commercialization

5

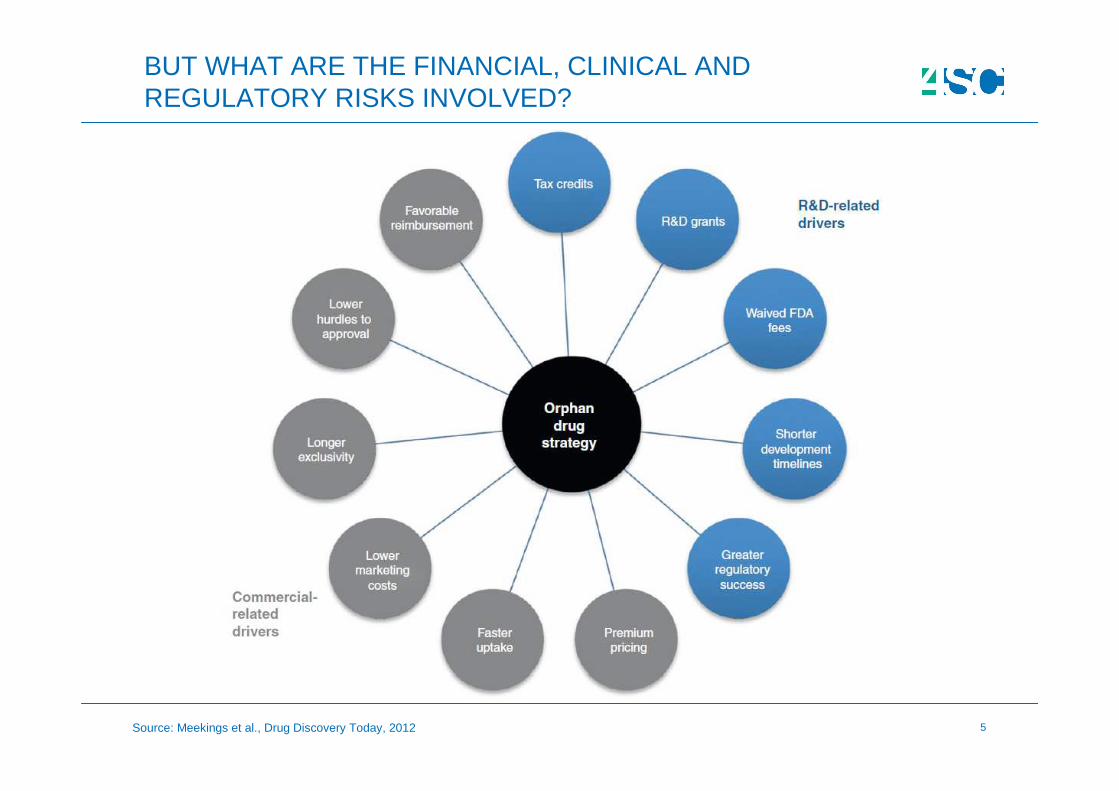

BUT WHAT ARE THE FINANCIAL, CLINICAL AND REGULATORY RISKS INVOLVED?

Source: Meekings et al., Drug Discovery Today, 2012

6

:: BY PEOPLE. WITH PEOPLE. FOR PEOPLE

RARE DISEASES

FINANCIAL RISKS

7

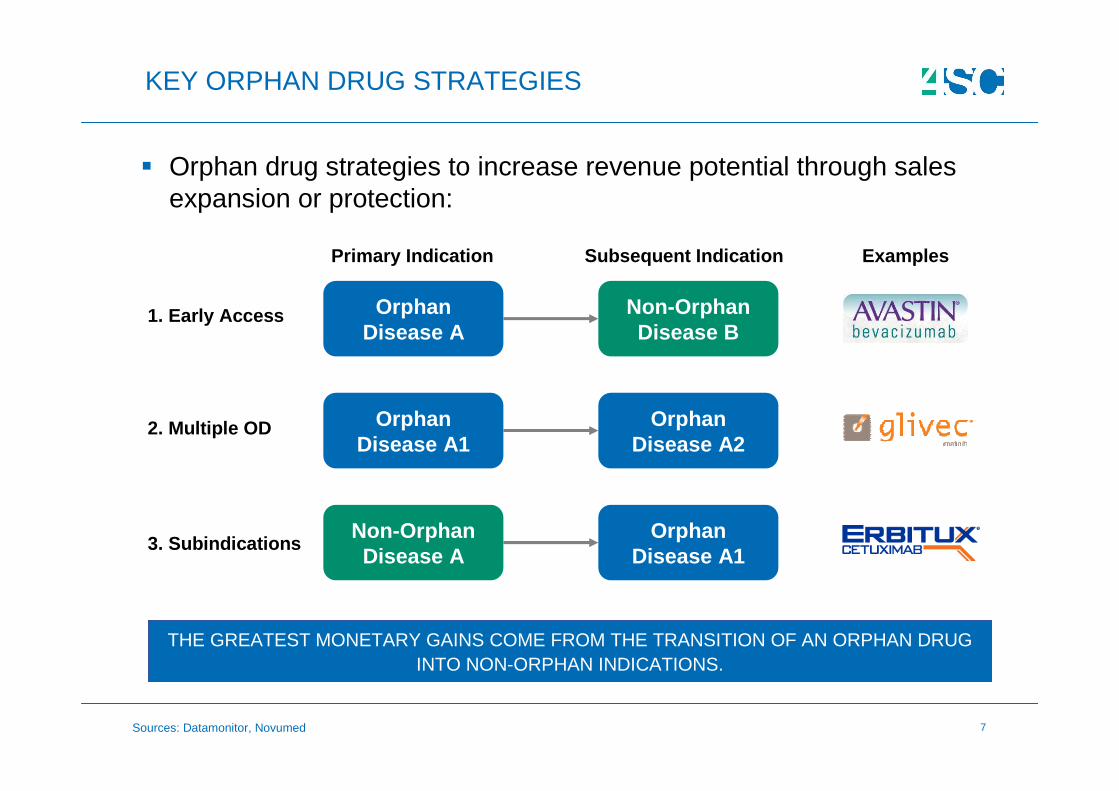

� Orphan drug strategies to increase revenue potential through sales expansion or protection:

KEY ORPHAN DRUG STRATEGIES

THE GREATEST MONETARY GAINS COME FROM THE TRANSITION OF AN ORPHAN DRUG INTO NON-ORPHAN INDICATIONS.

Examples

Orphan Disease A1

Orphan Disease A2

Orphan Disease A

Non-Orphan Disease B

Primary Indication Subsequent Indication

Orphan Disease A1

Non-Orphan Disease A

1. Early Access

2. Multiple OD

3. Subindications

Sources: Datamonitor, Novumed

8

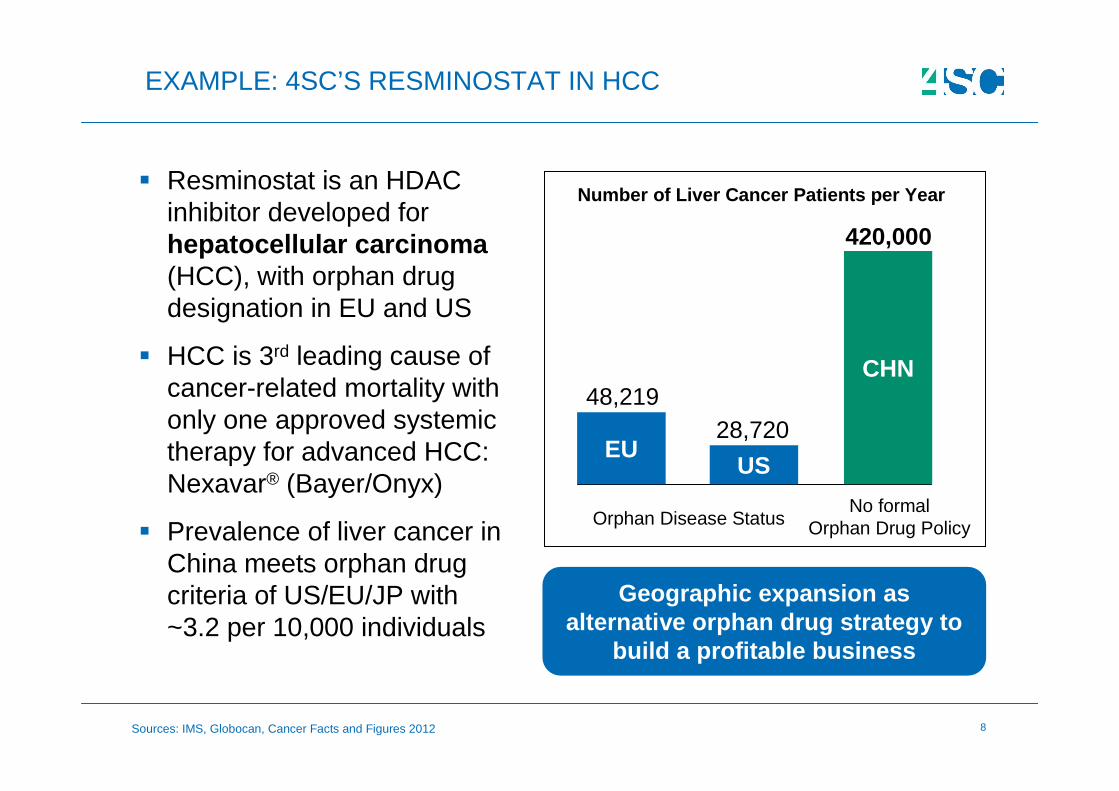

� Resminostat is an HDAC inhibitor developed for hepatocellular carcinoma (HCC), with orphan drug designation in EU and US

� HCC is 3rd leading cause of cancer-related mortality with only one approved systemic therapy for advanced HCC: Nexavar® (Bayer/Onyx)

� Prevalence of liver cancer in China meets orphan drug criteria of US/EU/JP with ~3.2 per 10,000 individuals

EXAMPLE: 4SC’S RESMINOSTAT IN HCC

Number of Liver Cancer Patients per Year

48,21928,720

420,000

Orphan Disease StatusNo formal

Orphan Drug Policy

Sources: IMS, Globocan, Cancer Facts and Figures 2012

EUUS

CHN

Geographic expansion as alternative orphan drug strategy to

build a profitable business

9

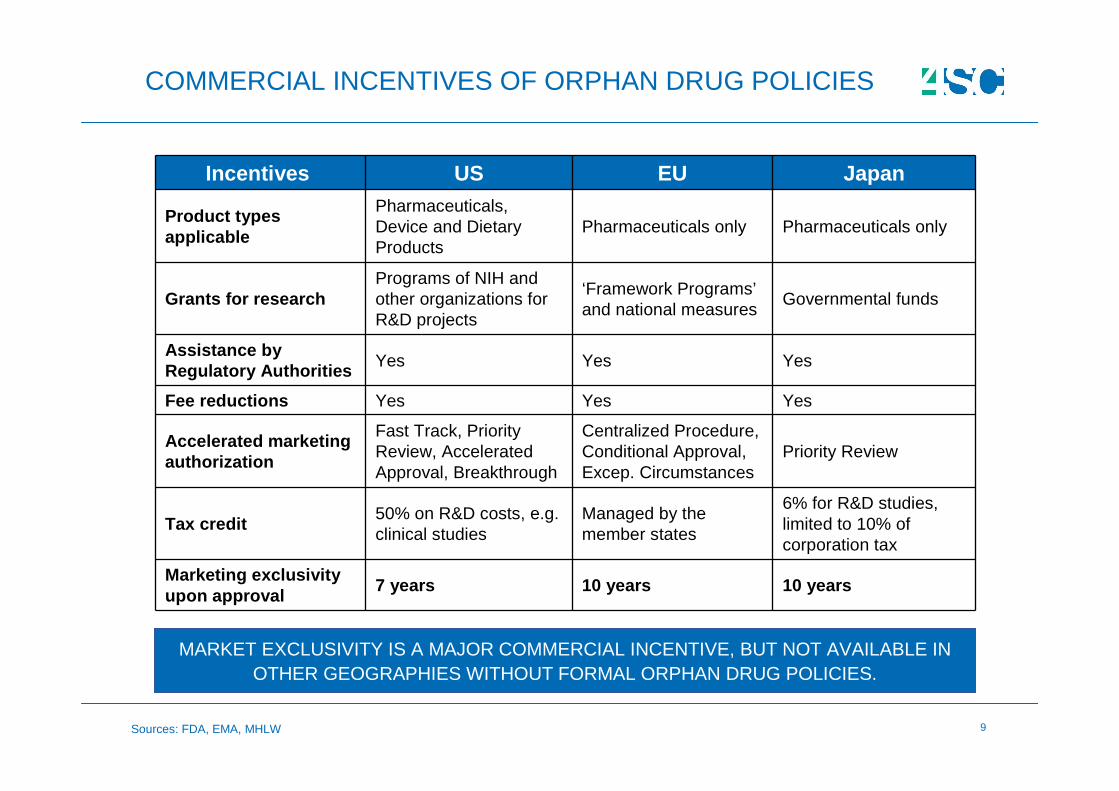

COMMERCIAL INCENTIVES OF ORPHAN DRUG POLICIES

Incentives US EU Japan

Product types applicable

Pharmaceuticals, Device and Dietary Products

Pharmaceuticals only Pharmaceuticals only

Grants for researchPrograms of NIH and other organizations for R&D projects

‘Framework Programs’and national measures

Governmental funds

Assistance by Regulatory Authorities Yes Yes Yes

Fee reductions Yes Yes Yes

Accelerated marketing authorization

Fast Track, Priority Review, Accelerated Approval, Breakthrough

Centralized Procedure, Conditional Approval, Excep. Circumstances

Priority Review

Tax credit50% on R&D costs, e.g. clinical studies

Managed by the member states

6% for R&D studies, limited to 10% of corporation tax

Marketing exclusivity upon approval

7 years 10 years 10 years

MARKET EXCLUSIVITY IS A MAJOR COMMERCIAL INCENTIVE, BUT NOT AVAILABLE IN OTHER GEOGRAPHIES WITHOUT FORMAL ORPHAN DRUG POLICIES.

Sources: FDA, EMA, MHLW

10

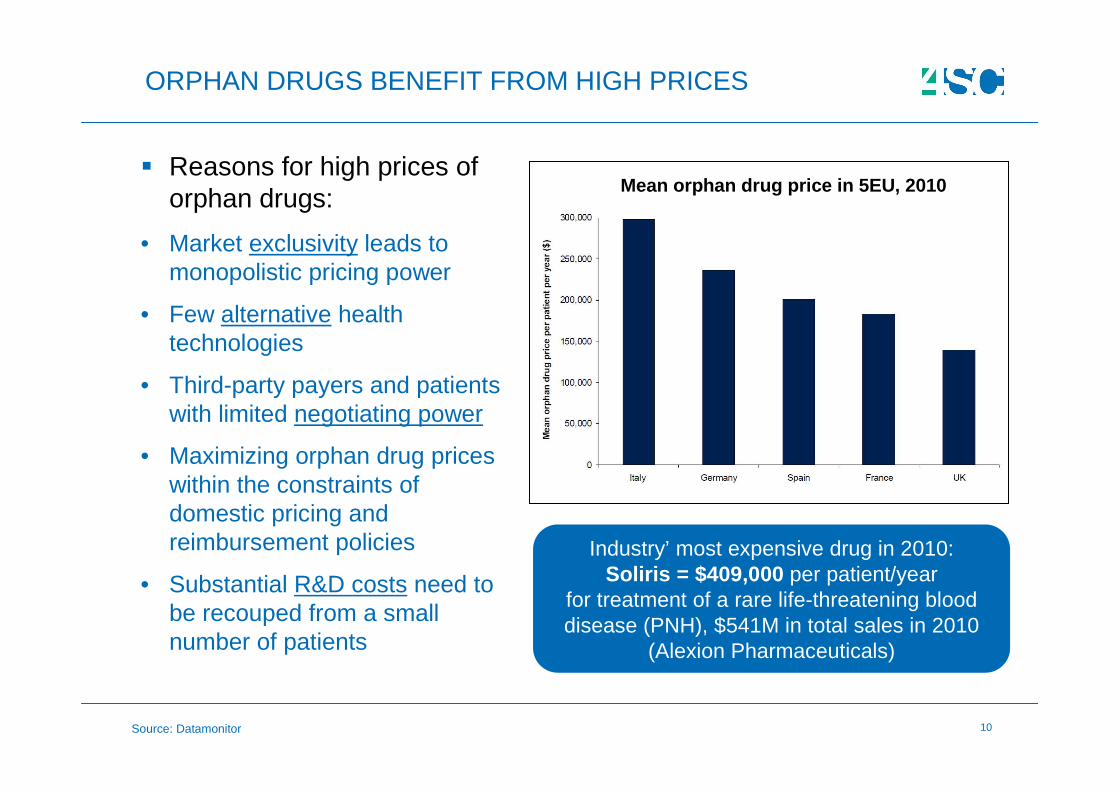

ORPHAN DRUGS BENEFIT FROM HIGH PRICES

� Reasons for high prices of orphan drugs:

• Market exclusivity leads to monopolistic pricing power

• Few alternative health technologies

• Third-party payers and patients with limited negotiating power

• Maximizing orphan drug prices within the constraints of domestic pricing and reimbursement policies

• Substantial R&D costs need to be recouped from a small number of patients

Industry’ most expensive drug in 2010:Soliris = $409,000 per patient/year

for treatment of a rare life-threatening blood disease (PNH), $541M in total sales in 2010

(Alexion Pharmaceuticals)

Mean orphan drug price in 5EU, 2010

Source: Datamonitor

11

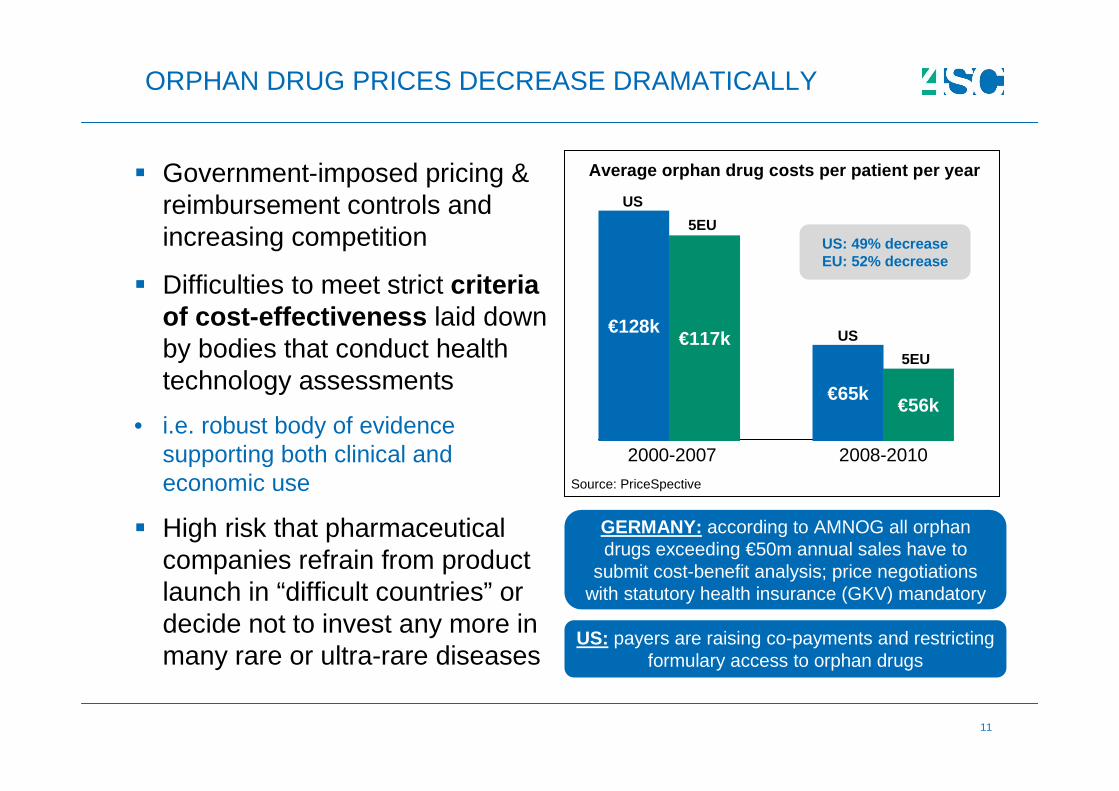

ORPHAN DRUG PRICES DECREASE DRAMATICALLY

� Government-imposed pricing & reimbursement controls and increasing competition

� Difficulties to meet strict criteria of cost-effectiveness laid down by bodies that conduct health technology assessments

• i.e. robust body of evidence supporting both clinical and economic use

� High risk that pharmaceutical companies refrain from product launch in “difficult countries” or decide not to invest any more in many rare or ultra-rare diseases

GERMANY: according to AMNOG all orphan drugs exceeding €50m annual sales have to

submit cost-benefit analysis; price negotiations with statutory health insurance (GKV) mandatory

US: payers are raising co-payments and restricting formulary access to orphan drugs

Average orphan drug costs per patient per year

2000-2007

€128k€117k

€65k€56k

2008-2010

Source: PriceSpective

US

5EU

US

5EUUS: 49% decreaseEU: 52% decrease

12

:: BY PEOPLE. WITH PEOPLE. FOR PEOPLE

RARE DISEASES

CLINICAL RISKS

13

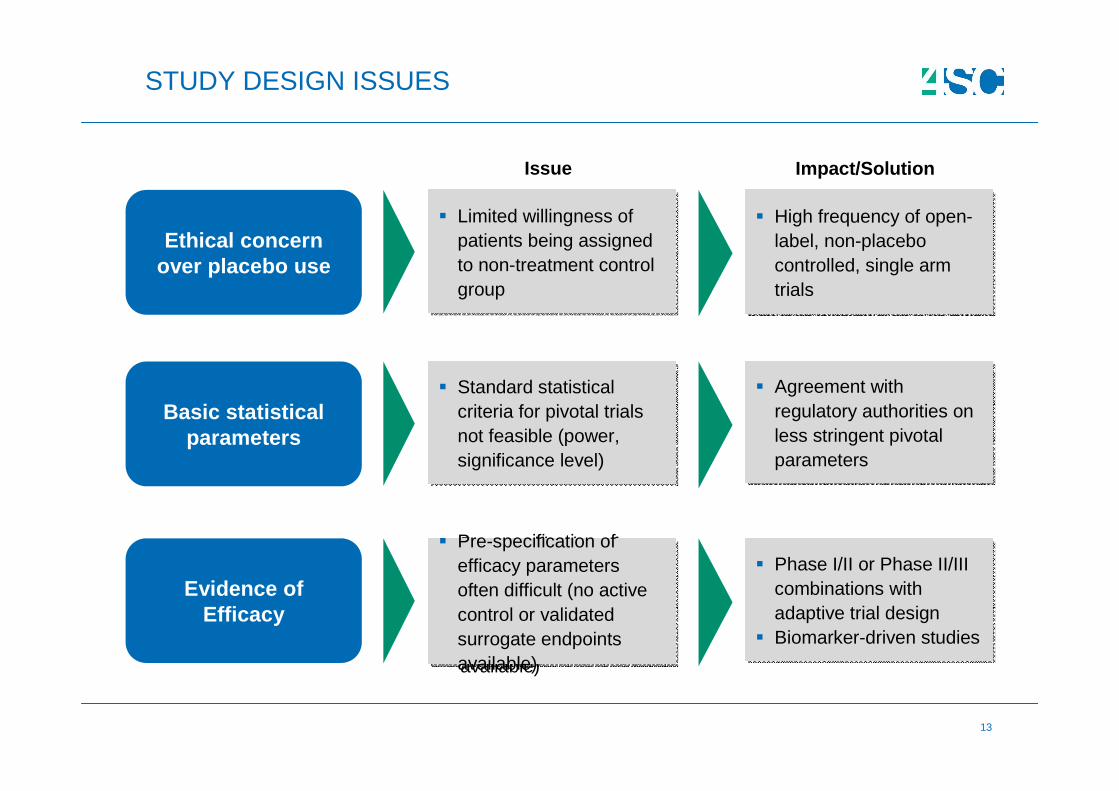

STUDY DESIGN ISSUES

Ethical concern over placebo use

� Limited willingness of patients being assigned to non-treatment control group

� Limited willingness of patients being assigned to non-treatment control group

� High frequency of open-label, non-placebo controlled, single arm trials

� High frequency of open-label, non-placebo controlled, single arm trials

Basic statistical parameters

� Standard statistical criteria for pivotal trials not feasible (power, significance level)

� Standard statistical criteria for pivotal trials not feasible (power, significance level)

� Agreement with regulatory authorities on less stringent pivotal parameters

� Agreement with regulatory authorities on less stringent pivotal parameters

Issue Impact/Solution

Evidence of Efficacy

� Pre-specification of efficacy parameters often difficult (no active control or validated surrogate endpoints available)

� Pre-specification of efficacy parameters often difficult (no active control or validated surrogate endpoints available)

� Phase I/II or Phase II/III combinations with adaptive trial design

� Biomarker-driven studies

� Phase I/II or Phase II/III combinations with adaptive trial design

� Biomarker-driven studies

14

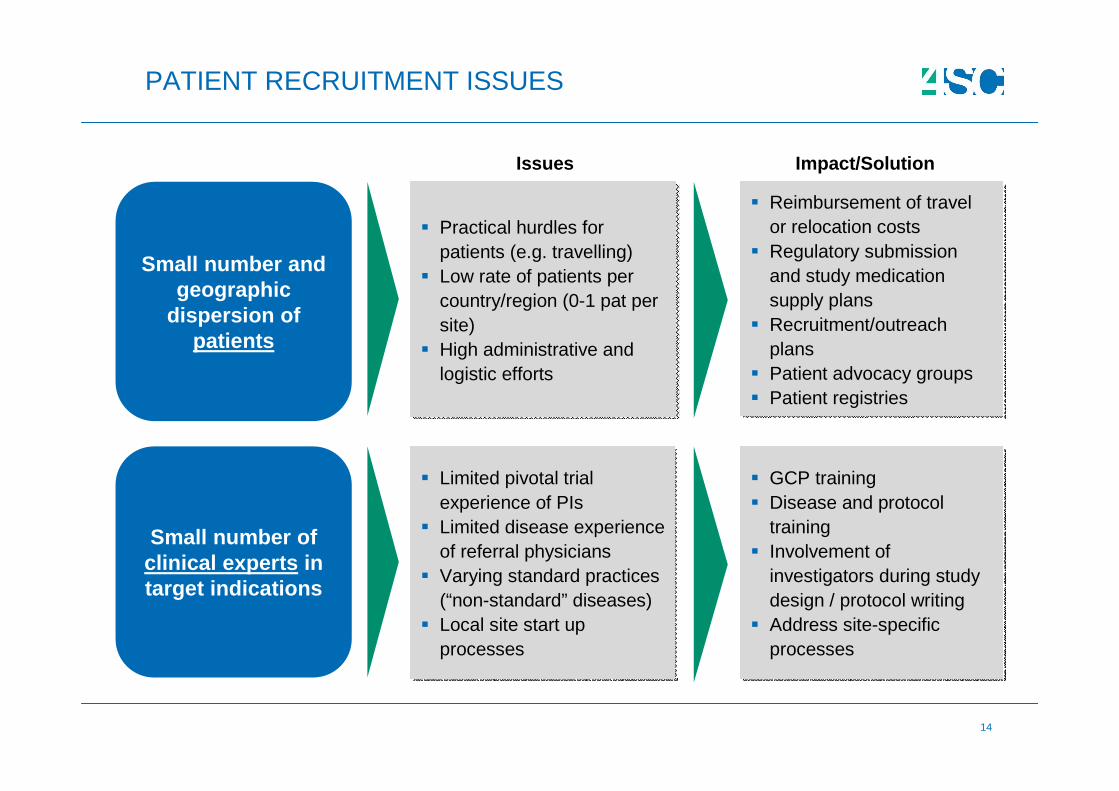

PATIENT RECRUITMENT ISSUES

Small number and geographic

dispersion of patients

Small number of clinical experts in target indications

� Practical hurdles for patients (e.g. travelling)

� Low rate of patients per country/region (0-1 pat per site)

� High administrative and logistic efforts

� Practical hurdles for patients (e.g. travelling)

� Low rate of patients per country/region (0-1 pat per site)

� High administrative and logistic efforts

� Reimbursement of travel or relocation costs

� Regulatory submission and study medication supply plans

� Recruitment/outreach plans

� Patient advocacy groups� Patient registries

� Reimbursement of travel or relocation costs

� Regulatory submission and study medication supply plans

� Recruitment/outreach plans

� Patient advocacy groups� Patient registries

� Limited pivotal trial experience of PIs

� Limited disease experience of referral physicians

� Varying standard practices (“non-standard” diseases)

� Local site start up processes

� Limited pivotal trial experience of PIs

� Limited disease experience of referral physicians

� Varying standard practices (“non-standard” diseases)

� Local site start up processes

� GCP training� Disease and protocol

training� Involvement of

investigators during study design / protocol writing

� Address site-specific processes

� GCP training� Disease and protocol

training� Involvement of

investigators during study design / protocol writing

� Address site-specific processes

Issues Impact/Solution

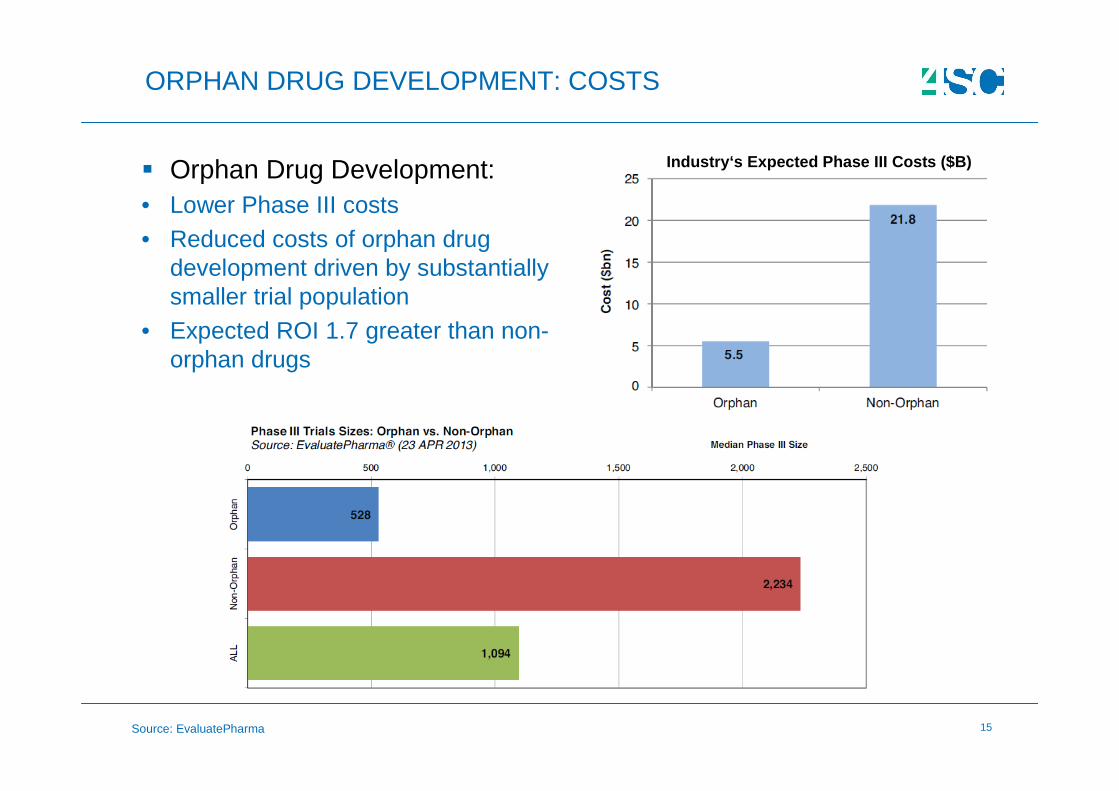

15Source: EvaluatePharma

ORPHAN DRUG DEVELOPMENT: COSTS

� Orphan Drug Development:• Lower Phase III costs• Reduced costs of orphan drug

development driven by substantially smaller trial population

• Expected ROI 1.7 greater than non-orphan drugs

Industry‘s Expected Phase III Costs ($B)

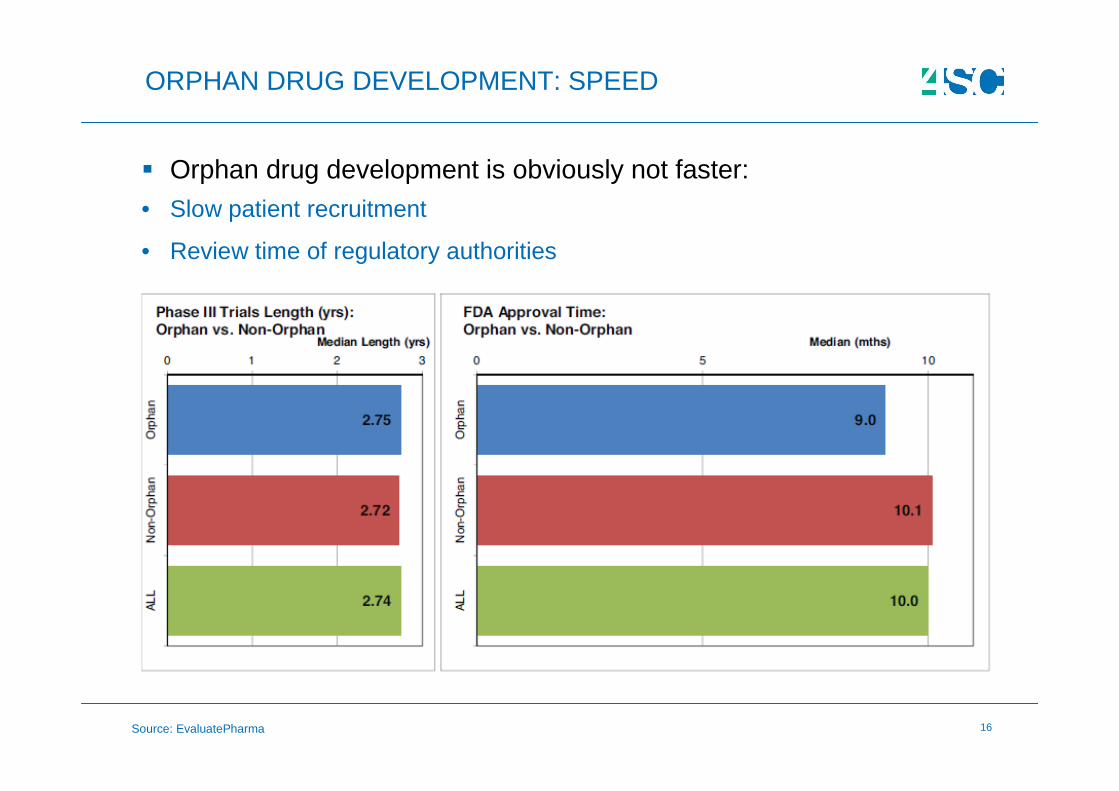

16Source: EvaluatePharma

ORPHAN DRUG DEVELOPMENT: SPEED

� Orphan drug development is obviously not faster:• Slow patient recruitment

• Review time of regulatory authorities

17

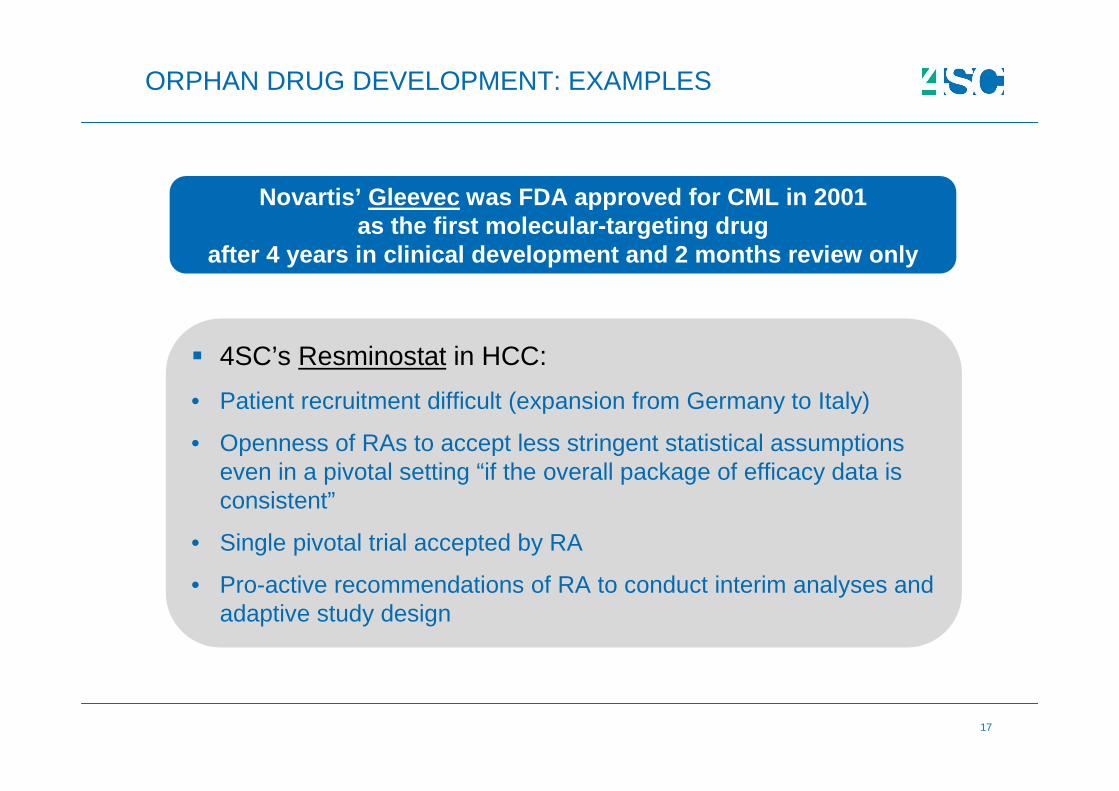

ORPHAN DRUG DEVELOPMENT: EXAMPLES

Novartis’ Gleevec was FDA approved for CML in 2001as the first molecular-targeting drug

after 4 years in clinical development and 2 months review only

� 4SC’s Resminostat in HCC:

• Patient recruitment difficult (expansion from Germany to Italy)

• Openness of RAs to accept less stringent statistical assumptionseven in a pivotal setting “if the overall package of efficacy data is consistent”

• Single pivotal trial accepted by RA

• Pro-active recommendations of RA to conduct interim analyses and adaptive study design

18

:: BY PEOPLE. WITH PEOPLE. FOR PEOPLE

RARE DISEASES

REGULATORY RISKS

19

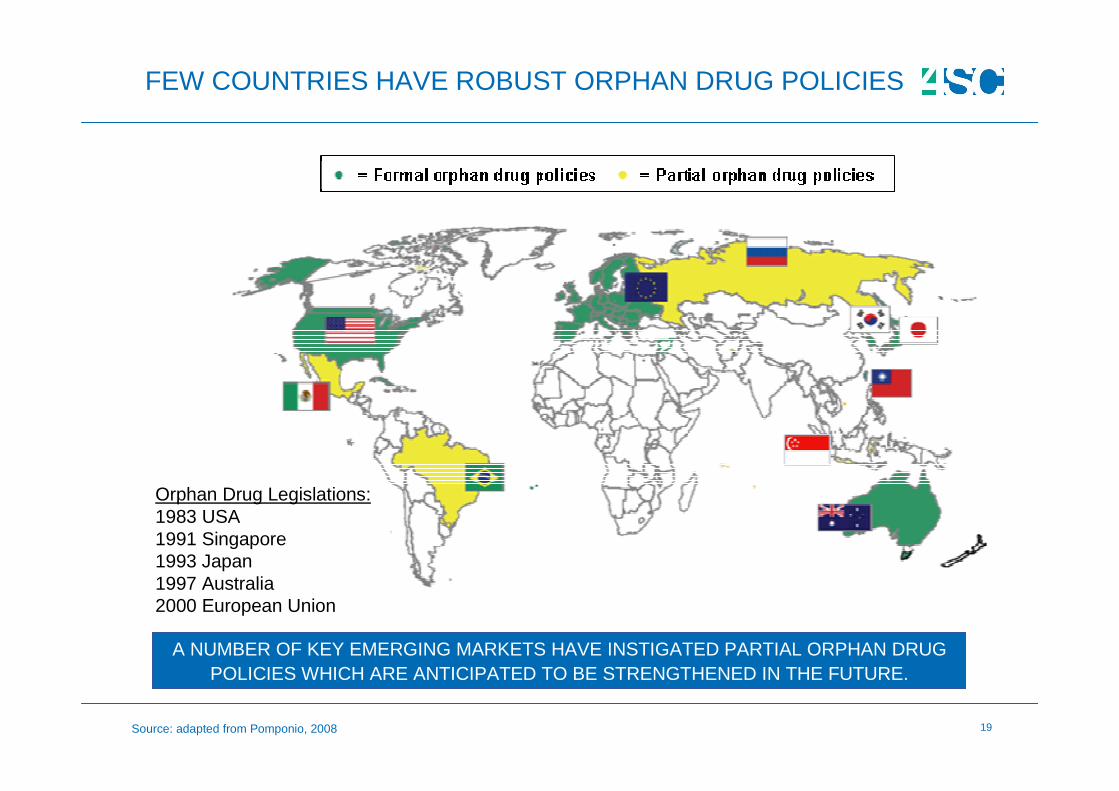

FEW COUNTRIES HAVE ROBUST ORPHAN DRUG POLICIES

A NUMBER OF KEY EMERGING MARKETS HAVE INSTIGATED PARTIAL ORPHAN DRUG POLICIES WHICH ARE ANTICIPATED TO BE STRENGTHENED IN THE FUTURE.

Orphan Drug Legislations:1983 USA1991 Singapore1993 Japan1997 Australia2000 European Union

Source: adapted from Pomponio, 2008

20

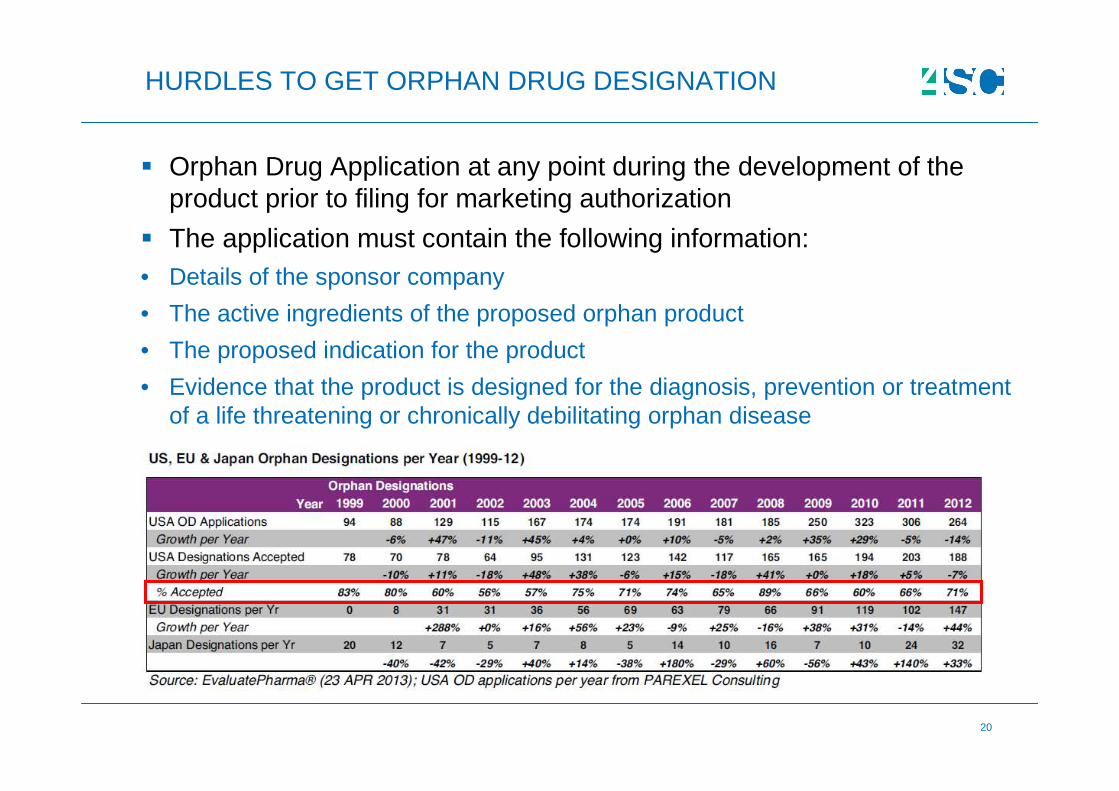

� Orphan Drug Application at any point during the development of the product prior to filing for marketing authorization

� The application must contain the following information:• Details of the sponsor company

• The active ingredients of the proposed orphan product

• The proposed indication for the product

• Evidence that the product is designed for the diagnosis, prevention or treatment of a life threatening or chronically debilitating orphan disease

HURDLES TO GET ORPHAN DRUG DESIGNATION

21

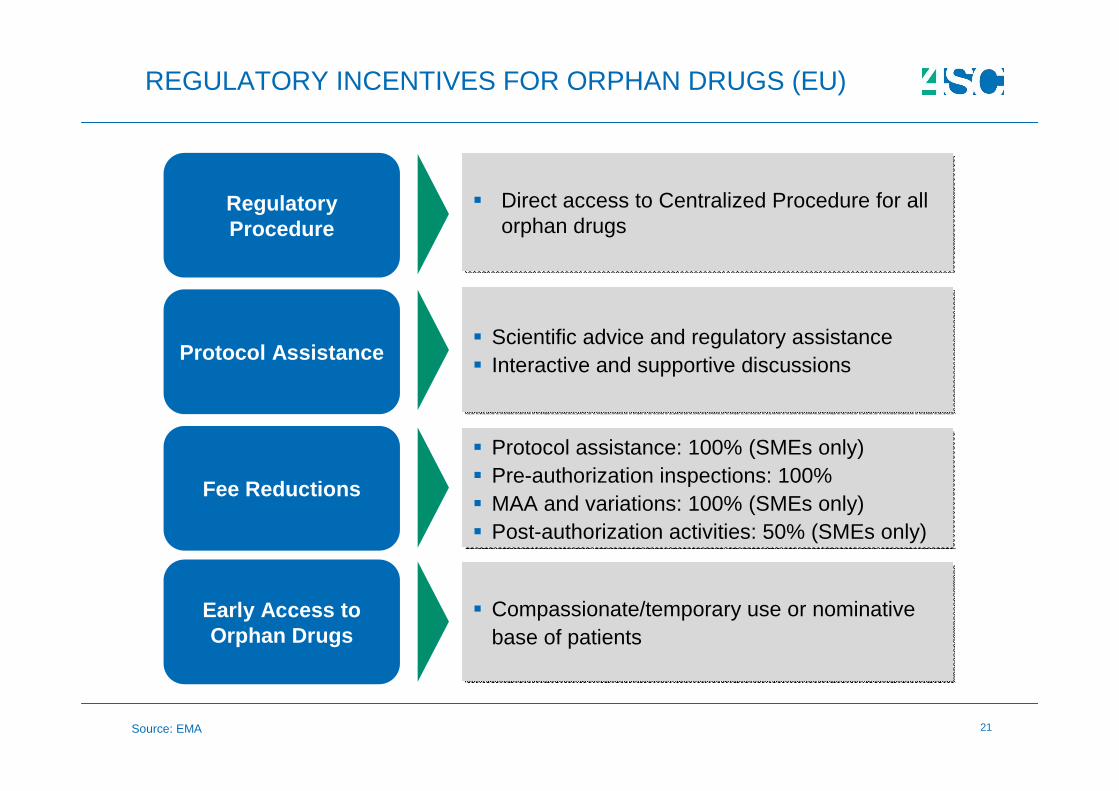

REGULATORY INCENTIVES FOR ORPHAN DRUGS (EU)

Regulatory Procedure

� Direct access to Centralized Procedure for all orphan drugs

� Direct access to Centralized Procedure for all orphan drugs

Protocol Assistance� Scientific advice and regulatory assistance� Interactive and supportive discussions

� Scientific advice and regulatory assistance� Interactive and supportive discussions

Fee Reductions

� Protocol assistance: 100% (SMEs only)� Pre-authorization inspections: 100%� MAA and variations: 100% (SMEs only)� Post-authorization activities: 50% (SMEs only)

� Protocol assistance: 100% (SMEs only)� Pre-authorization inspections: 100%� MAA and variations: 100% (SMEs only)� Post-authorization activities: 50% (SMEs only)

Early Access to Orphan Drugs

� Compassionate/temporary use or nominative base of patients

� Compassionate/temporary use or nominative base of patients

Source: EMA

22

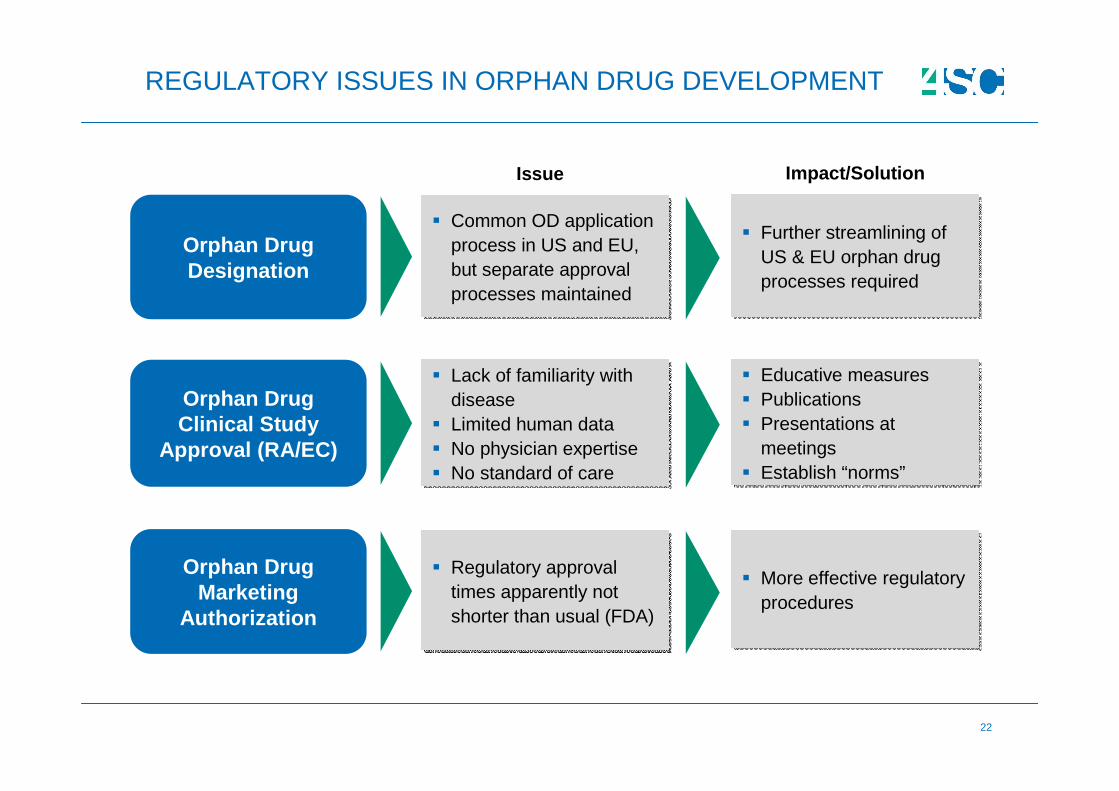

REGULATORY ISSUES IN ORPHAN DRUG DEVELOPMENT

Orphan Drug Designation

� Common OD application process in US and EU, but separate approval processes maintained

� Common OD application process in US and EU, but separate approval processes maintained

� Further streamlining of US & EU orphan drug processes required

� Further streamlining of US & EU orphan drug processes required

Orphan Drug Clinical Study

Approval (RA/EC)

� Lack of familiarity with disease

� Limited human data� No physician expertise� No standard of care

� Lack of familiarity with disease

� Limited human data� No physician expertise� No standard of care

� Educative measures� Publications� Presentations at

meetings� Establish “norms”

� Educative measures� Publications� Presentations at

meetings� Establish “norms”

Issue Impact/Solution

Orphan Drug Marketing

Authorization

� Regulatory approval times apparently not shorter than usual (FDA)

� Regulatory approval times apparently not shorter than usual (FDA)

� More effective regulatory procedures

� More effective regulatory procedures

23

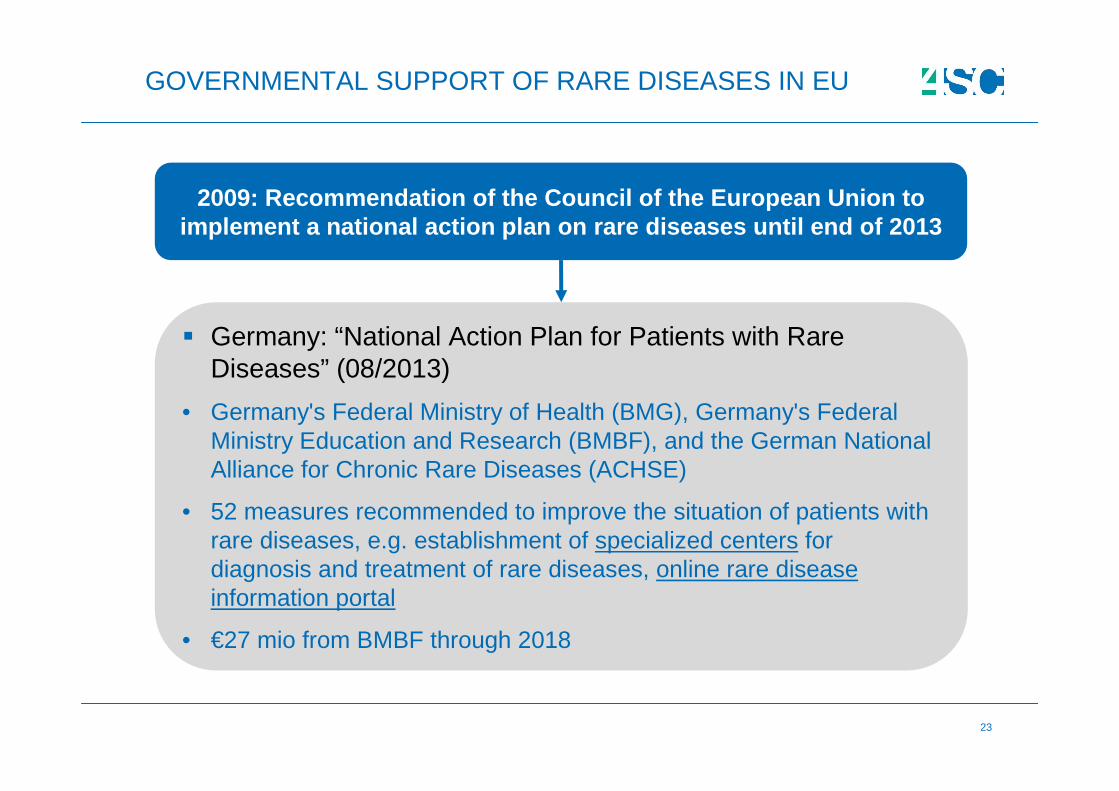

GOVERNMENTAL SUPPORT OF RARE DISEASES IN EU

2009: Recommendation of the Council of the European Union to implement a national action plan on rare diseases u ntil end of 2013

� Germany: “National Action Plan for Patients with Rare Diseases” (08/2013)

• Germany's Federal Ministry of Health (BMG), Germany's Federal Ministry Education and Research (BMBF), and the German National Alliance for Chronic Rare Diseases (ACHSE)

• 52 measures recommended to improve the situation of patients with rare diseases, e.g. establishment of specialized centers for diagnosis and treatment of rare diseases, online rare disease information portal

• €27 mio from BMBF through 2018

24

:: BY PEOPLE. WITH PEOPLE. FOR PEOPLE

RARE DISEASES

SUMMARY

25

� Financial:

• Difficulties to develop orphan medicines for global market

• Decreasing orphan drug prices

• Challenge of demonstrating “value” for reimbursement

� Clinical:

• Patient recruitment

• Duration of Phase III studies

� Regulatory:

• Duration of review times by regulatory authorities

• Lack of global orphan drug policy with harmonized regulations/incentives

WHAT ARE THE KEY FINANCIAL, CLINICAL AND REGULATORY RISKS INVOLVED IN RARE DISEASES?

ORPHAN DRUG DEVELOPMENT IS A SUCCESSFUL BUSINESS MODEL, BUT IS FACING SIGNIFICANT FINANCIAL, CLINICAL AND REGULATORY RISKS.

26

THANK YOU VERY MUCH !

::

:: BY PEOPLE. WITH PEOPLE. FOR PEOPLE

CONTACT

26

www.4sc.com

4SC AGAldo Ammendola PhD, MBA, RACDirector Strategic Planning& Regulatory Affairs

Am Klopferspitz 19a82152 Planegg-MartinsriedE-Mail: [email protected]: +49 89 700 763-0www.4sc.com