Embed Size (px)

Citation preview

© Chia Fah Choy 2005

Topic 2 – Investment Appraisal: Background and Techniques

© Chia Fah Choy 2005

Learning Objectives

After studying this topic you will:• understand the basis of long-term decision making;• be able to use traditional appraisal techniques of

Accounting Rate of Return and Payback;• know the reasons why Discounted Cash Flow (DCF)

techniques are used;• be able to calculate and interpret Net Present Value

(NPV);• understand Internal rate of Return (IRR);• know what is meant by the Excess Present Value Index;• understand the effects of inflation on investment

appraisal

© Chia Fah Choy 2005

Long Run Decision Making

Assuming that finance is available the decision to invest will be based on three major factors:

• The investor’s beliefs in the future• The alternative available in which to invest• The investor’s attitude to risk

© Chia Fah Choy 2005

Traditional Investment Appraisal Techniques

• Accounting rate of return

• Payback

© Chia Fah Choy 2005

Accounting Rate of Return

• This is the ratio of average annual profits, after depreciation, to the capital invested.

• Alternative term: Return on Capital Employed (ROCE).

© Chia Fah Choy 2005

A firm is considering three projects each with an initial investment of $1,000 and a life of 5 years. The profits generated by the projects are estimated to be as follows:

Year Project I Project II Project III

1 200 350 150

2 200 200 150

3 200 150 150

4 200 150 200

5 200 150 350

Total 1,000 1,000 1,000

After tax and depreciation profits

Calculate the accounting rate of return (ARR) ona. Initial capitalb. Average capital

Example 1

© Chia Fah Choy 2005

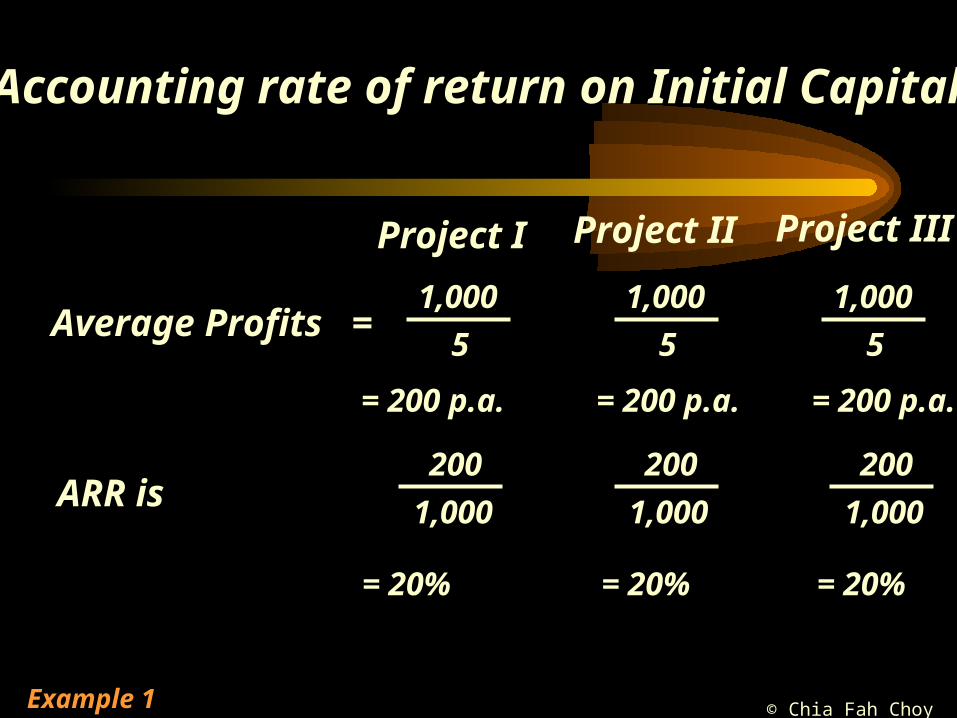

Accounting rate of return on Initial Capital

Project I Project II Project III

Average Profits =1,000

5

1,000

5

1,000

5

= 200 p.a. = 200 p.a. = 200 p.a.

200

1,000

= 20%

ARR is200

1,000

= 20%

200

1,000

= 20%

Example 1

© Chia Fah Choy 2005

Accounting rate of return on Average Capital

Project I Project II Project III

Average capital =1,000

2

1,000

2

1,000

2

= 500 = 500 = 500

200

500

= 40%

ARR is

= 40% = 40%

200

500

200

500

Example 1

© Chia Fah Choy 2005

Payback

• A period, usually expressed in years which it takes for the project’s net cash inflows to recoup the original investment.

• The usual decision rules is to accept the project with the shortest payback period.

© Chia Fah Choy 2005

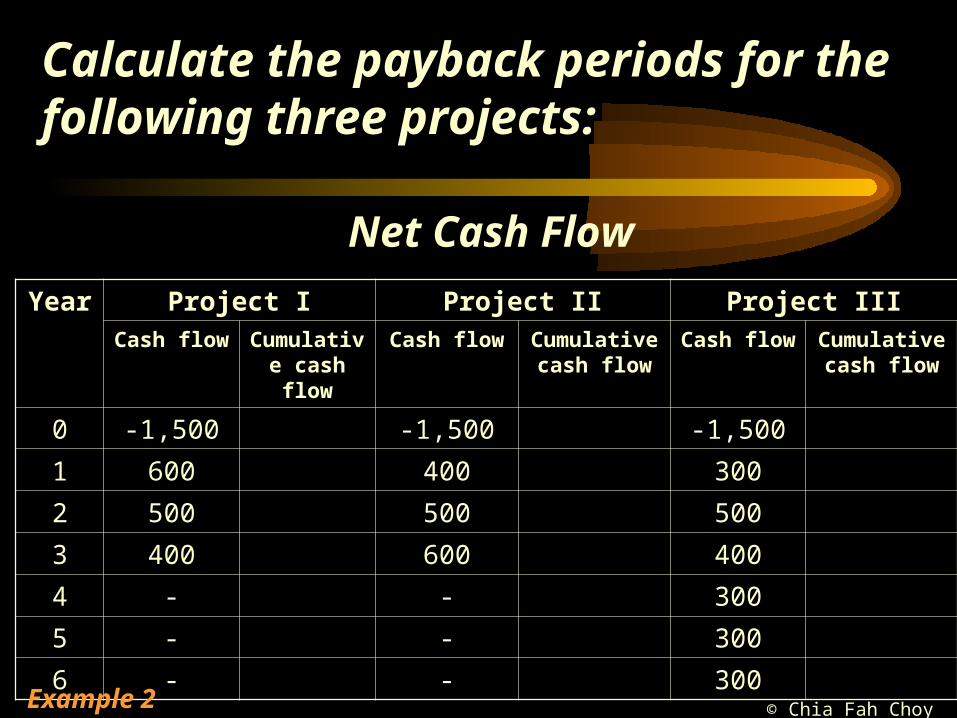

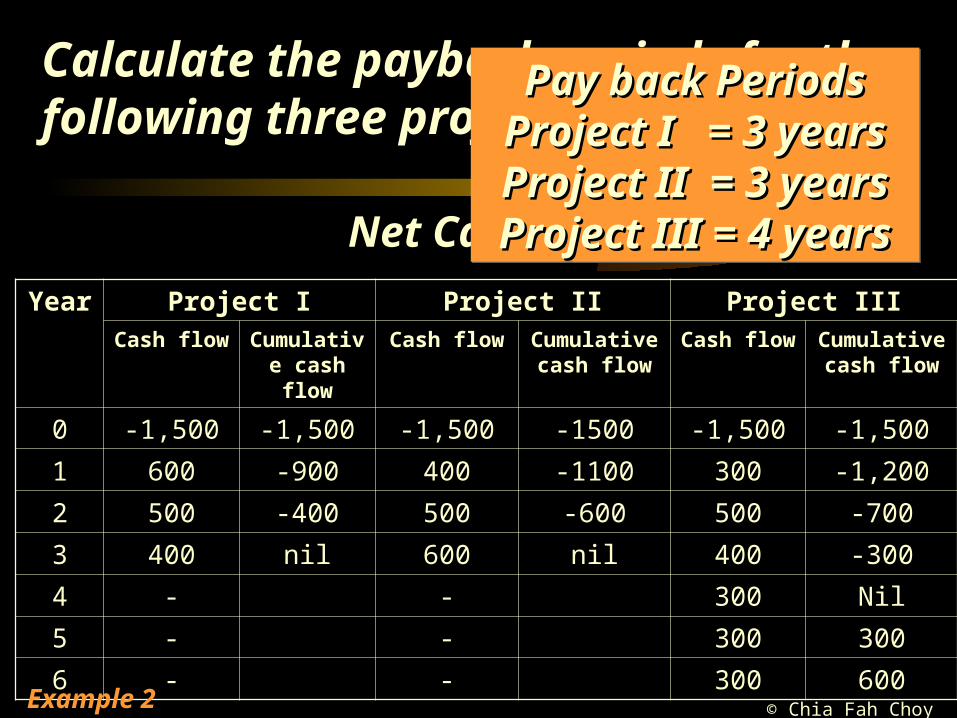

Calculate the payback periods for the following three projects:

Year Project I Project II Project IIICash flow Cumulative

cash flowCash flow Cumulative

cash flowCash flow Cumulative

cash flow

0 -1,500 -1,500 -1,500

1 600 400 300

2 500 500 500

3 400 600 400

4 - - 300

5 - - 300

6 - - 300

Net Cash Flow

Example 2

© Chia Fah Choy 2005

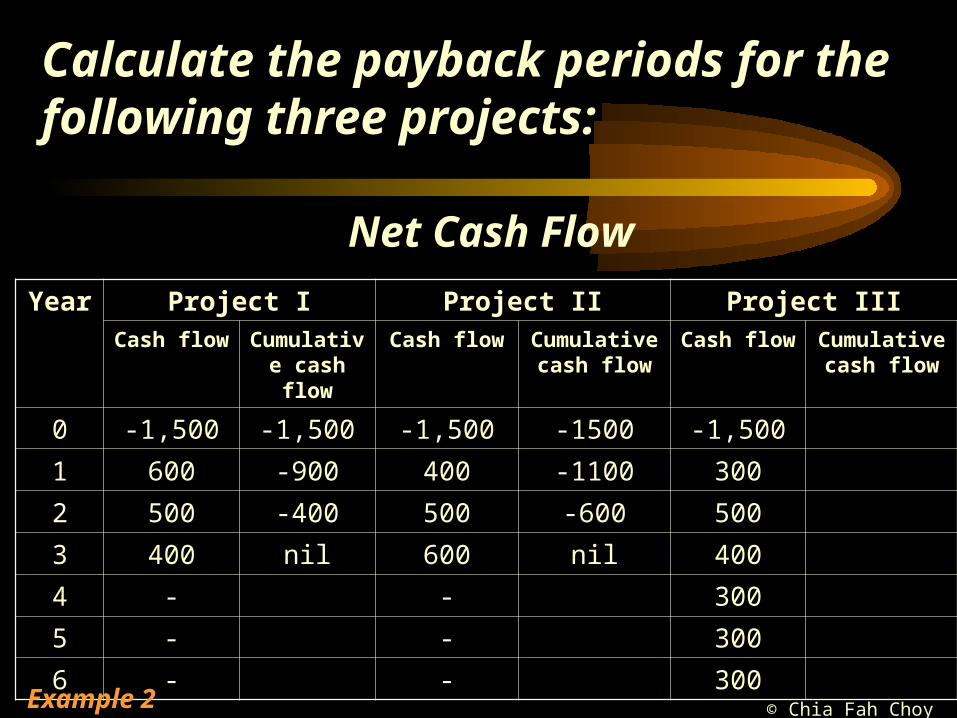

Calculate the payback periods for the following three projects:

Year Project I Project II Project IIICash flow Cumulative

cash flowCash flow Cumulative

cash flowCash flow Cumulative

cash flow

0 -1,500 -1,500 -1,500 -1,500

1 600 -900 400 300

2 500 -400 500 500

3 400 nil 600 400

4 - - 300

5 - - 300

6 - - 300

Net Cash Flow

Example 2

© Chia Fah Choy 2005

Calculate the payback periods for the following three projects:

Year Project I Project II Project IIICash flow Cumulative

cash flowCash flow Cumulative

cash flowCash flow Cumulative

cash flow

0 -1,500 -1,500 -1,500 -1500 -1,500

1 600 -900 400 -1100 300

2 500 -400 500 -600 500

3 400 nil 600 nil 400

4 - - 300

5 - - 300

6 - - 300

Net Cash Flow

Example 2

© Chia Fah Choy 2005

Calculate the payback periods for the following three projects:

Year Project I Project II Project IIICash flow Cumulative

cash flowCash flow Cumulative

cash flowCash flow Cumulative

cash flow

0 -1,500 -1,500 -1,500 -1500 -1,500 -1,500

1 600 -900 400 -1100 300 -1,200

2 500 -400 500 -600 500 -700

3 400 nil 600 nil 400 -300

4 - - 300 Nil

5 - - 300 300

6 - - 300 600

Net Cash Flow

Pay back PeriodsPay back PeriodsProject I = 3 yearsProject I = 3 yearsProject II = 3 yearsProject II = 3 yearsProject III = 4 yearsProject III = 4 years

Pay back PeriodsPay back PeriodsProject I = 3 yearsProject I = 3 yearsProject II = 3 yearsProject II = 3 yearsProject III = 4 yearsProject III = 4 years

Example 2

© Chia Fah Choy 2005

Discounted Cash Flow (DCF)

• Net Present Value (NPV)

• Internal Rate of Return (IRR)

© Chia Fah Choy 2005

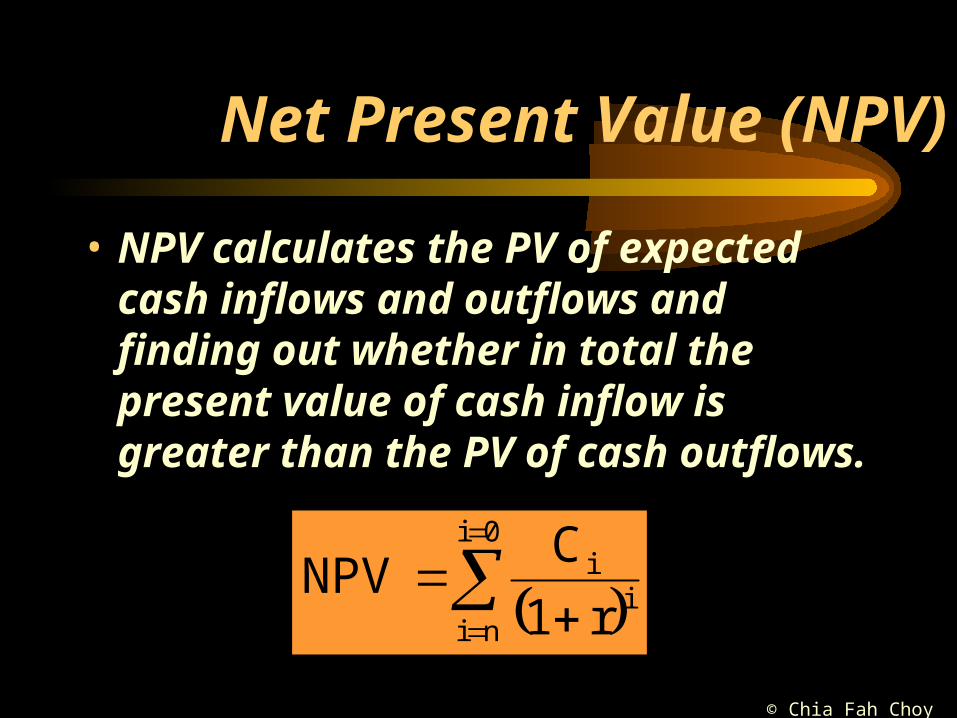

Net Present Value (NPV)

• NPV calculates the PV of expected cash inflows and outflows and finding out whether in total the present value of cash inflow is greater than the PV of cash outflows.

ii

0i

ni r1

CNPV

© Chia Fah Choy 2005

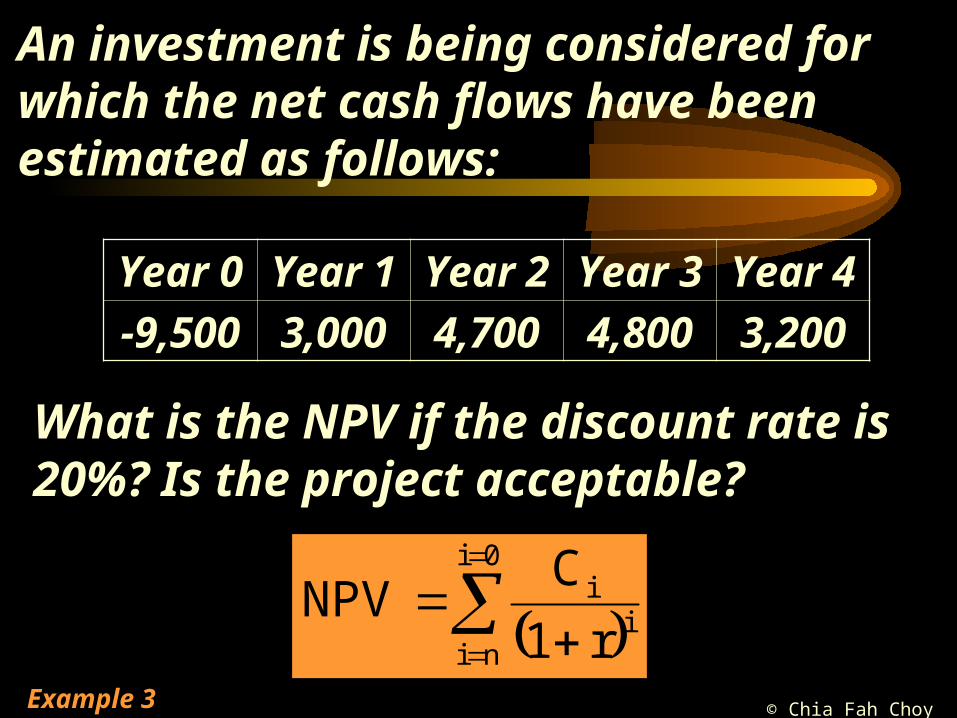

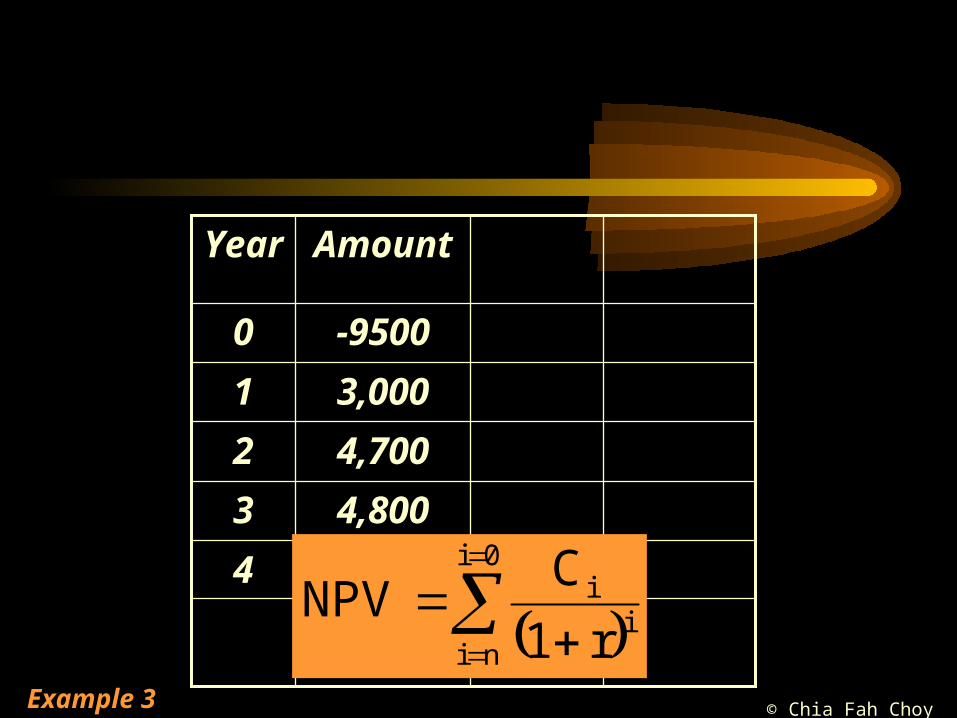

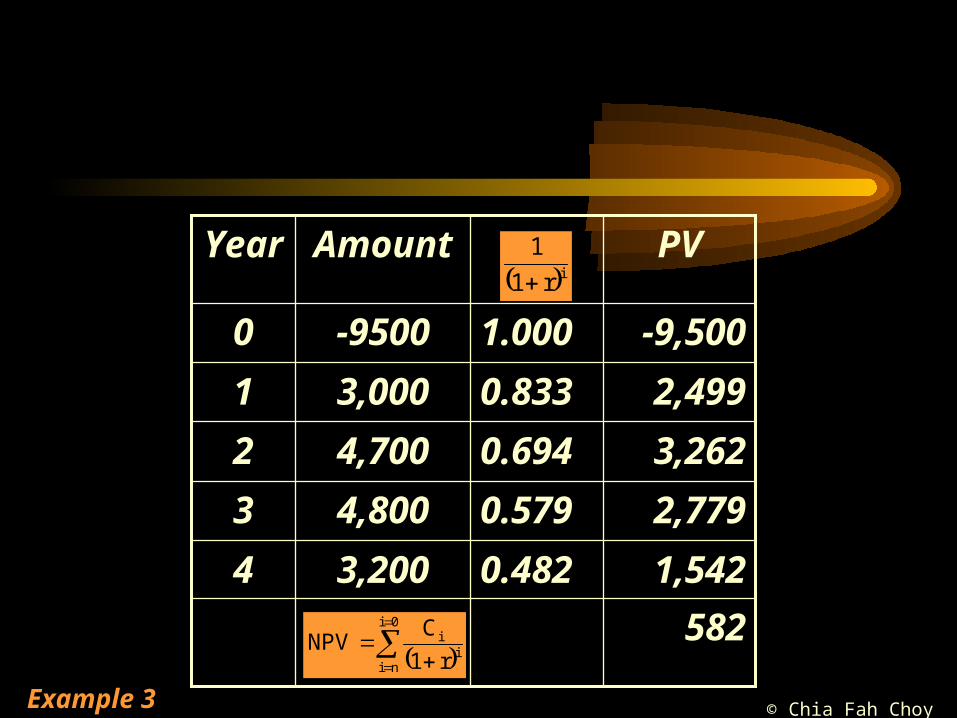

An investment is being considered for which the net cash flows have been estimated as follows:

What is the NPV if the discount rate is 20%? Is the project acceptable?

Year 0 Year 1 Year 2 Year 3 Year 4

-9,500 3,000 4,700 4,800 3,200

Example 3

© Chia Fah Choy 2005

An investment is being considered for which the net cash flows have been estimated as follows:

What is the NPV if the discount rate is 20%? Is the project acceptable?

Year 0 Year 1 Year 2 Year 3 Year 4

-9,500 3,000 4,700 4,800 3,200

ii

0i

ni r1

CNPV

Example 3

© Chia Fah Choy 2005

3,2004

AmountYear

-95000

4,8003

4,7002

3,0001

ii

0i

ni r1

CNPV

Example 3

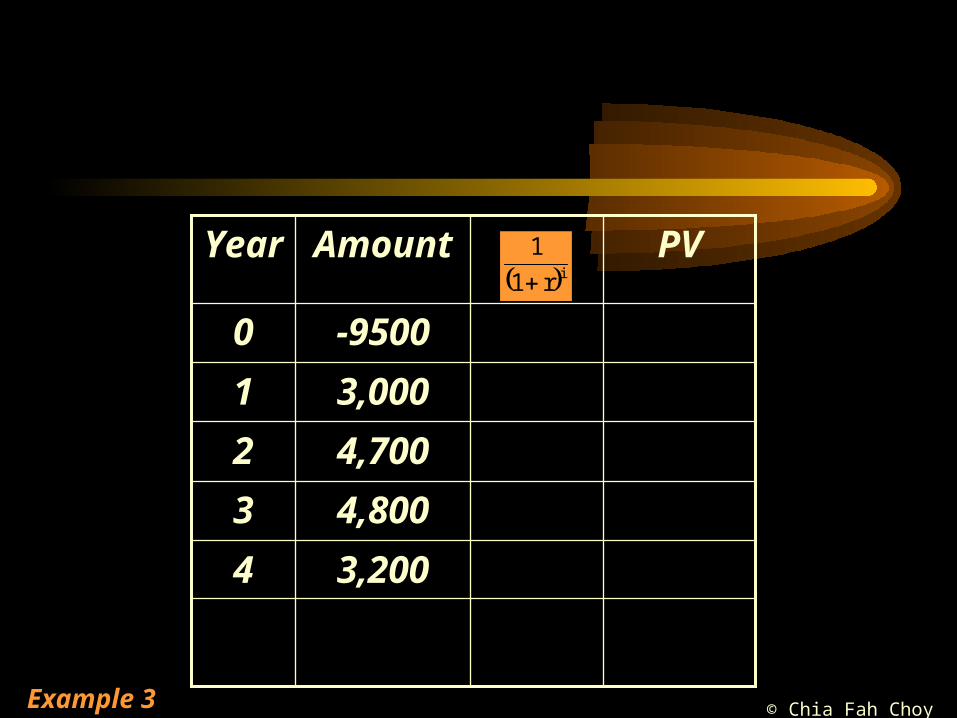

© Chia Fah Choy 2005

3,2004

PVAmountYear

-95000

4,8003

4,7002

3,0001

ir1

1

Example 3

© Chia Fah Choy 2005

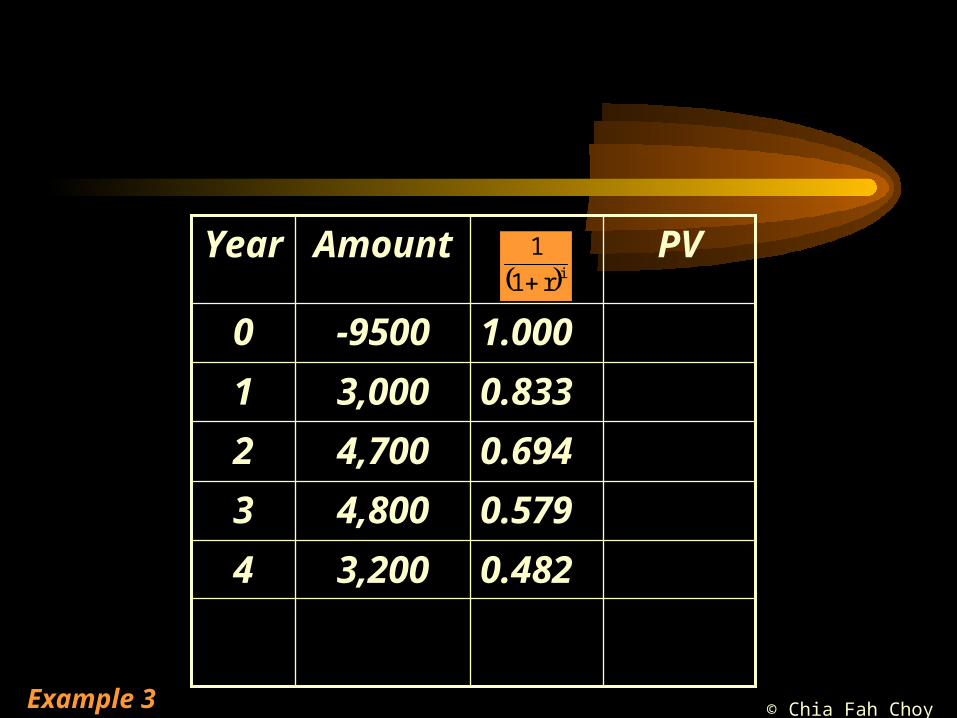

0.4823,2004

0.579

0.694

0.833

1.000

PVAmountYear

-95000

4,8003

4,7002

3,0001

ir1

1

Example 3

© Chia Fah Choy 2005

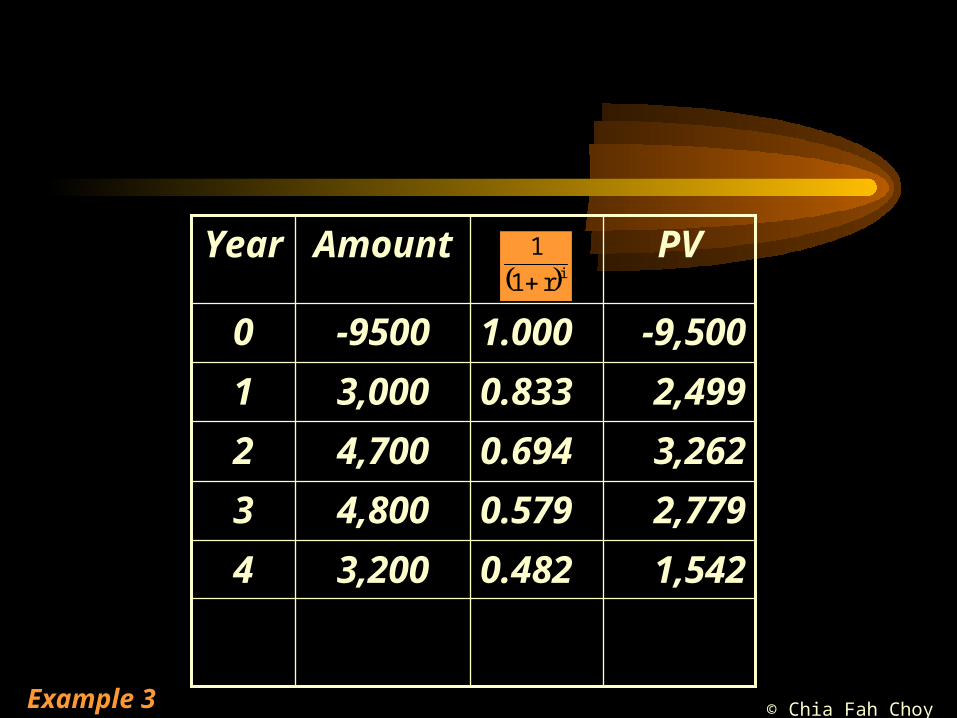

1,5420.4823,2004

0.579

0.694

0.833

1.000

PVAmountYear

-9,500-95000

2,7794,8003

3,2624,7002

2,4993,0001

ir1

1

Example 3

© Chia Fah Choy 2005

1,5420.4823,2004

0.579

0.694

0.833

1.000

PVAmountYear

-9,500-95000

582

2,7794,8003

3,2624,7002

2,4993,0001

ir1

1

ii

0i

ni r1

CNPV

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500

End Year 2

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900

End Year 2

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000

End Year 2

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2 8,400

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2 8,400 1,680 4,700 5,380

End Year 3

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2 8,400 1,680 4,700 5,380

End Year 3 5,380 1,076 4,800 1,656

End Year 4

Example 3

© Chia Fah Choy 2005

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2 8,400 1,680 4,700 5,380

End Year 3 5,380 1,076 4,800 1,656

End Year 4 1,656 331 3,200 1,213

Example 3

© Chia Fah Choy 2005

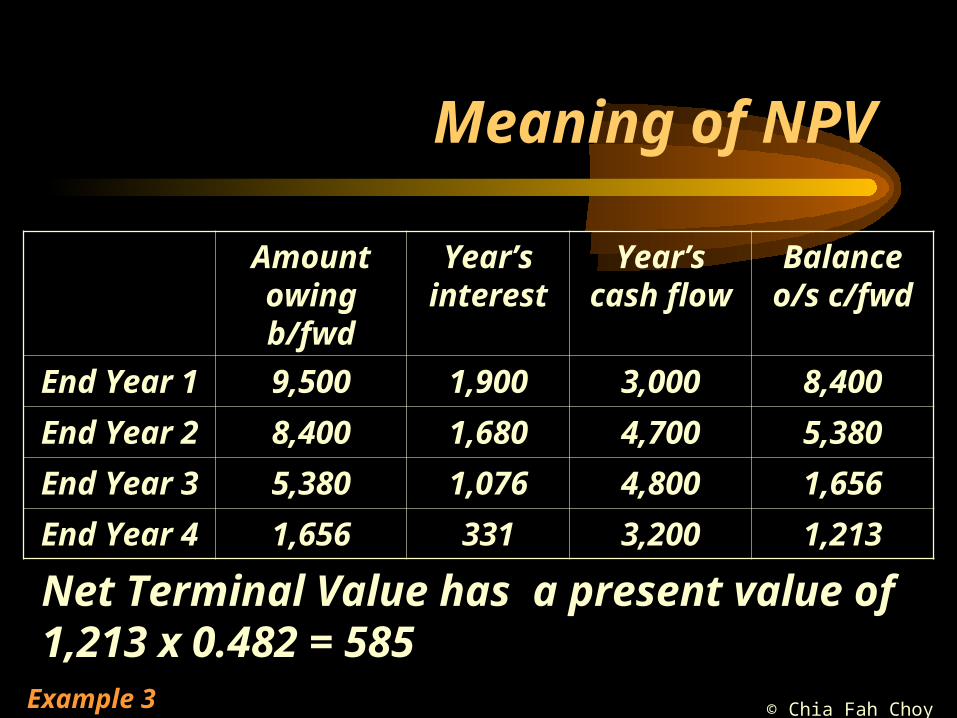

Meaning of NPV

Amount owing b/fwd

Year’s interest

Year’s cash flow

Balance o/s c/fwd

End Year 1 9,500 1,900 3,000 8,400

End Year 2 8,400 1,680 4,700 5,380

End Year 3 5,380 1,076 4,800 1,656

End Year 4 1,656 331 3,200 1,213

Net Terminal Value has a present value of 1,213 x 0.482 = 585

Example 3

© Chia Fah Choy 2005

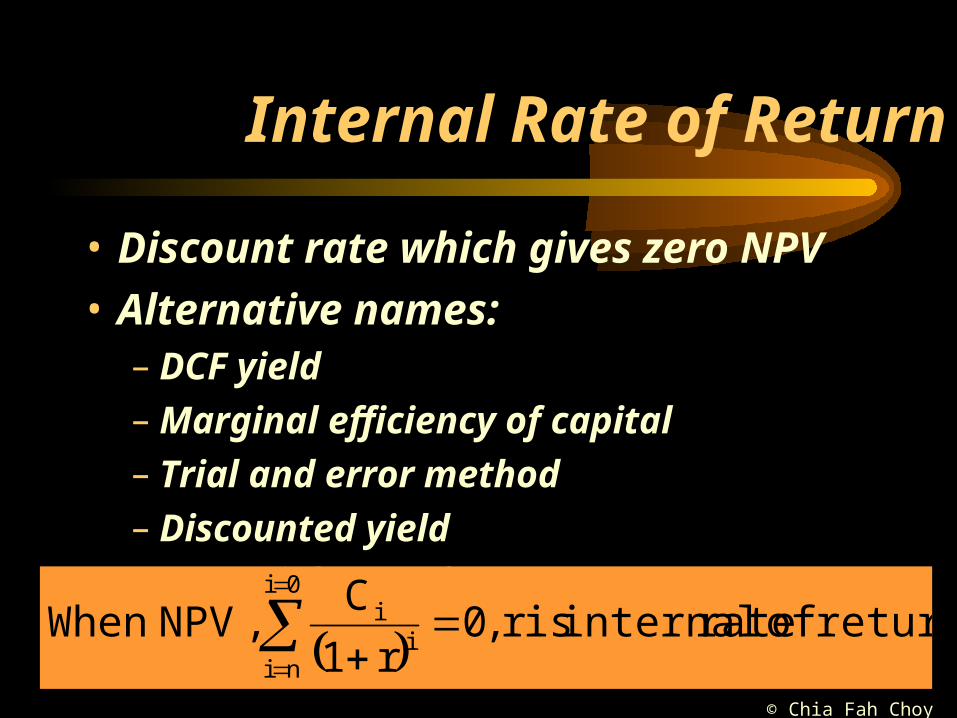

Internal Rate of Return

• Discount rate which gives zero NPV

• Alternative names:– DCF yield– Marginal efficiency of capital– Trial and error method– Discounted yield– Actuarial rate of return

return. of rate internal isr ,0

r1

C,NPVWhen i

i0i

ni

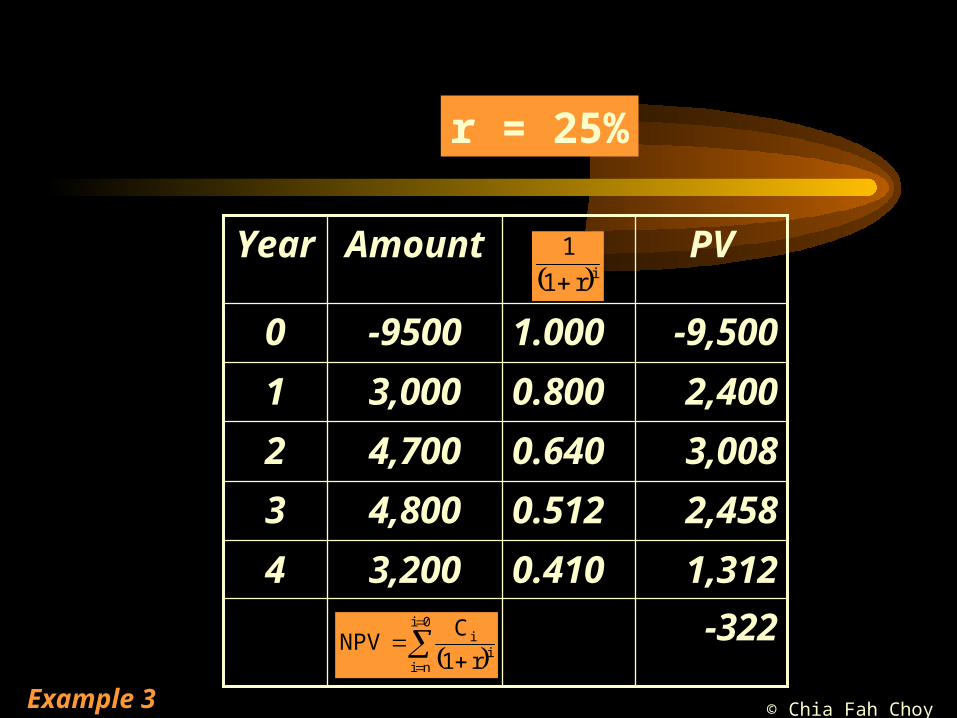

© Chia Fah Choy 2005

1,3120.4103,2004

0.512

0.640

0.800

1.000

PVAmountYear

-9,500-95000

-322

2,4584,8003

3,0084,7002

2,4003,0001

ir1

1

ii

0i

ni r1

CNPV

r = 25%

Example 3

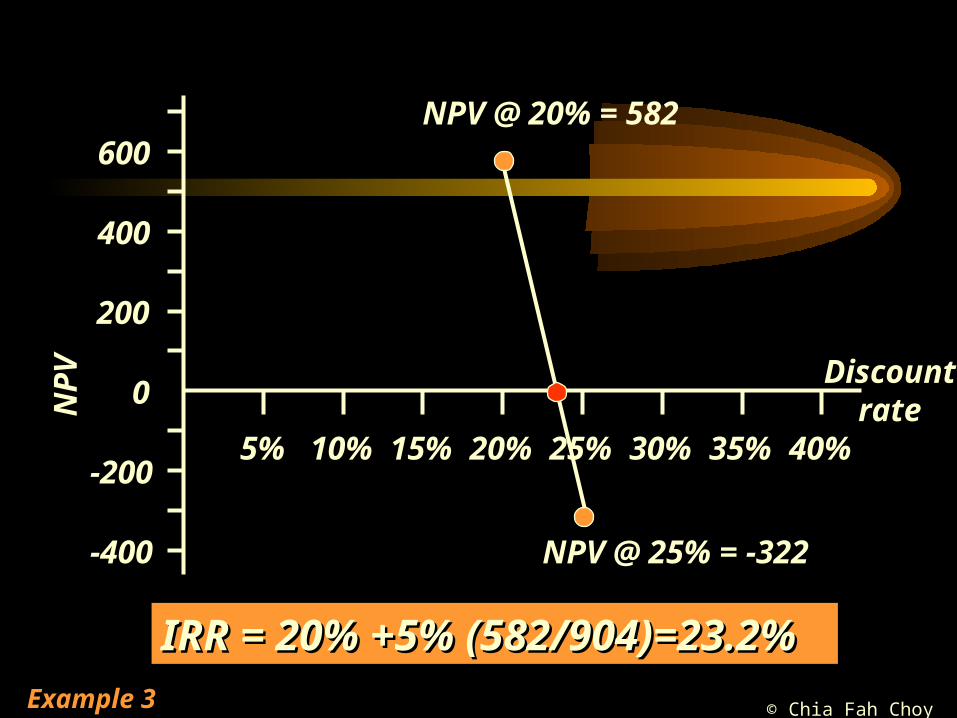

© Chia Fah Choy 2005

-200

-400

200

400

600

0NP

V

5% 10% 15% 20% 25% 30% 35% 40%

Discount rate

NPV @ 20% = 582

NPV @ 25% = -322

IRR = 20% +5% (582/904)=23.2%IRR = 20% +5% (582/904)=23.2%Example 3

© Chia Fah Choy 2005

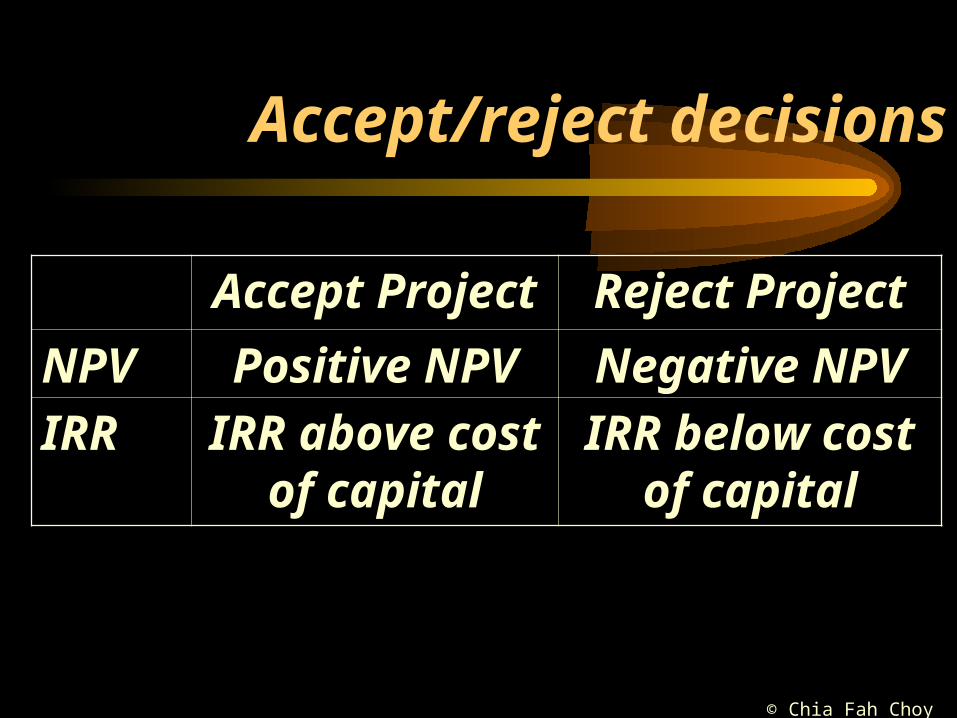

Decision rule using IRR

• Where the calculated IRR is greater than the company’s cost of capital then the project is acceptable.

© Chia Fah Choy 2005

NPV and IRR compared

• Accept/reject decisions

• Absolute and relative measures

• Mutually exclusive projects

© Chia Fah Choy 2005

Accept/reject decisions

Accept Project Reject Project

NPV Positive NPV Negative NPV

IRR IRR above cost of capital

IRR below cost of capital

© Chia Fah Choy 2005

Absolute and relative measures

• NPV is an absolute measure of the return on a project

• IRR is a relative measure relating the size and timing of the cash flows to the initial investment

© Chia Fah Choy 2005

Assume a project has the following cash flows:

Project acceptable by both methods – assuming 10% is the cost of capital.

Year 0 Year 5

Project x -20,000 40,241

NPV@10% 4,990

IRR 15%

Now assume that the project is scaled up by a factor of 10.

Year 0 Year 5

Project 10x -200,000 402,410

NPV@10% 49,900

IRR 15%

The NPV method clearly discriminates between Project X and Project 10X whereas the IRR remains unchanged at 15%.

Example 4

© Chia Fah Choy 2005

Mutually exclusive projects

• Only one of several alternative projects can be chosen

© Chia Fah Choy 2005

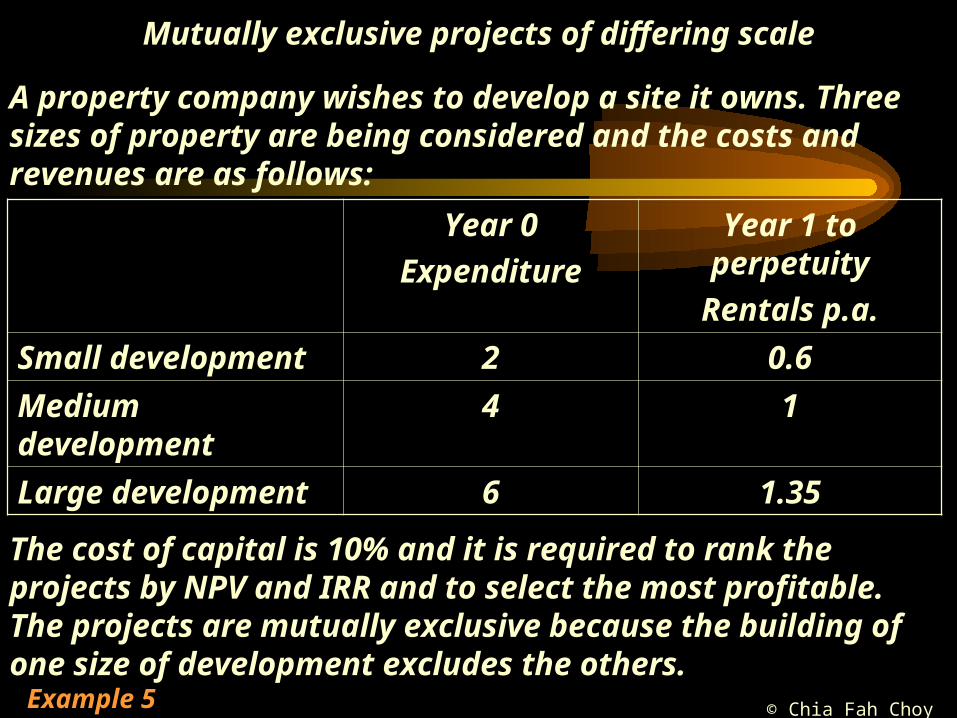

Mutually exclusive projects of differing scale

A property company wishes to develop a site it owns. Three sizes of property are being considered and the costs and revenues are as follows:

Year 0

Expenditure

Year 1 to perpetuity

Rentals p.a.

Small development 2 0.6

Medium development

4 1

Large development 6 1.35

The cost of capital is 10% and it is required to rank the projects by NPV and IRR and to select the most profitable.The projects are mutually exclusive because the building of one size of development excludes the others.

Example 5

© Chia Fah Choy 2005

Expenditure P.V. of rentals

NPV IRR %

Small 2 6 4 30

Medium 4 10 6 25

Large 6 13.5 7.5 22.5

Incremental expenditure

Incremental rental

Incremental IRR

Stage 1 (small) 2 0.6 30Stage 2 (medium - small) 2 0.4 20Stage 3 (large - medium) 2 0.35 17.5

Example 5

Ranking of NPV and IRR

Incremental IRR

© Chia Fah Choy 2005

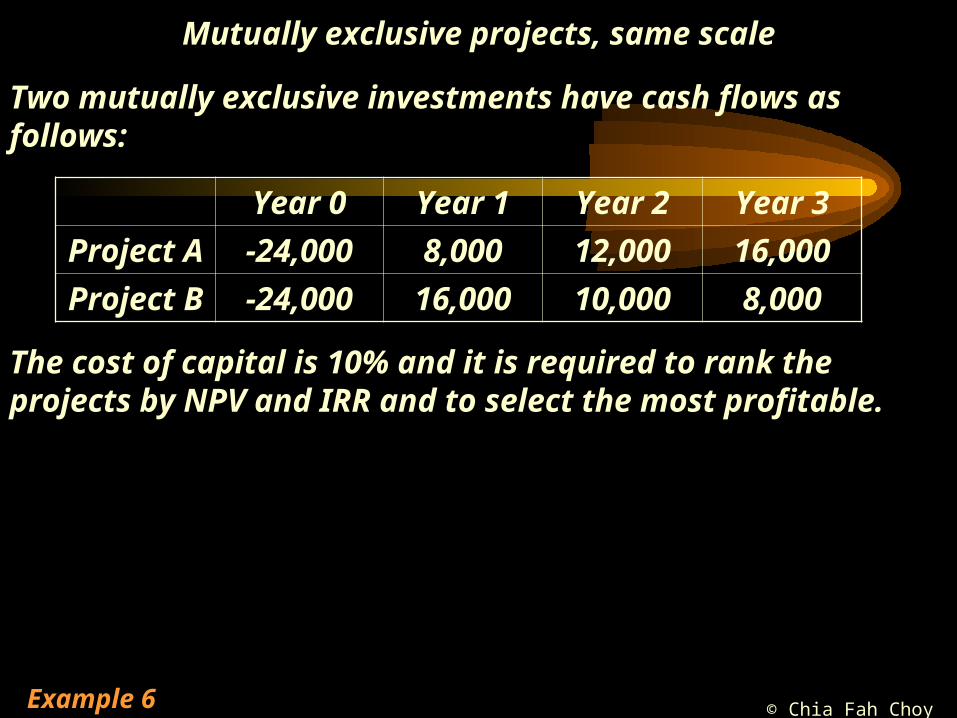

Mutually exclusive projects, same scale

Two mutually exclusive investments have cash flows as follows:

Year 0 Year 1 Year 2 Year 3

Project A -24,000 8,000 12,000 16,000

Project B -24,000 16,000 10,000 8,000

The cost of capital is 10% and it is required to rank the projects by NPV and IRR and to select the most profitable.

Example 6

© Chia Fah Choy 2005

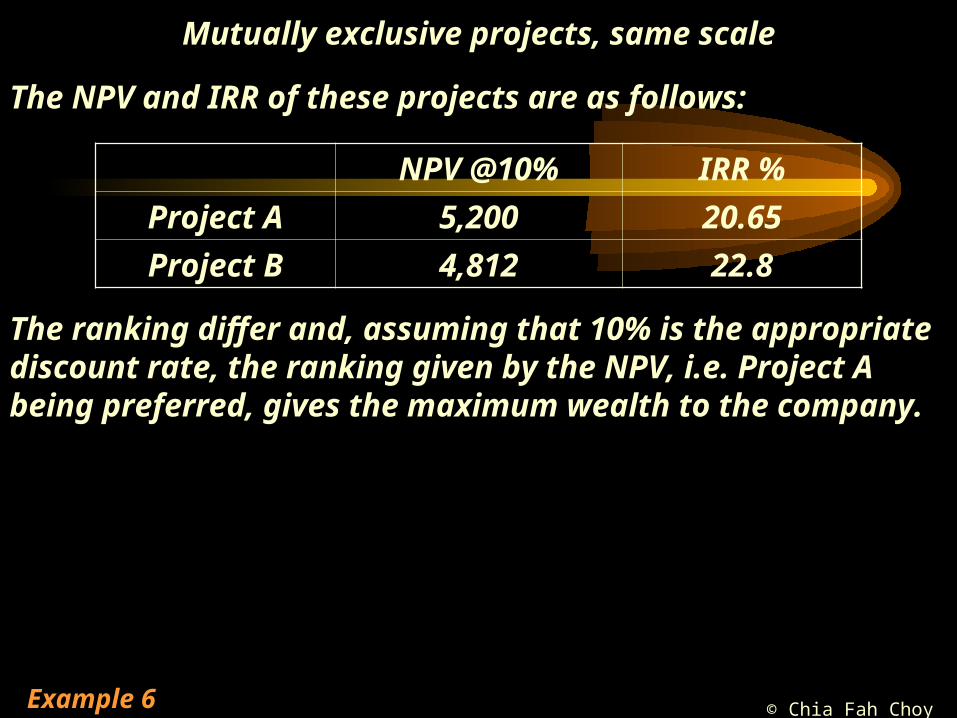

Mutually exclusive projects, same scale

The NPV and IRR of these projects are as follows:

NPV @10% IRR %

Project A 5,200 20.65

Project B 4,812 22.8

The ranking differ and, assuming that 10% is the appropriate discount rate, the ranking given by the NPV, i.e. Project A being preferred, gives the maximum wealth to the company.

Example 6

© Chia Fah Choy 2005

Non-conventional cash flows

© Chia Fah Choy 2005

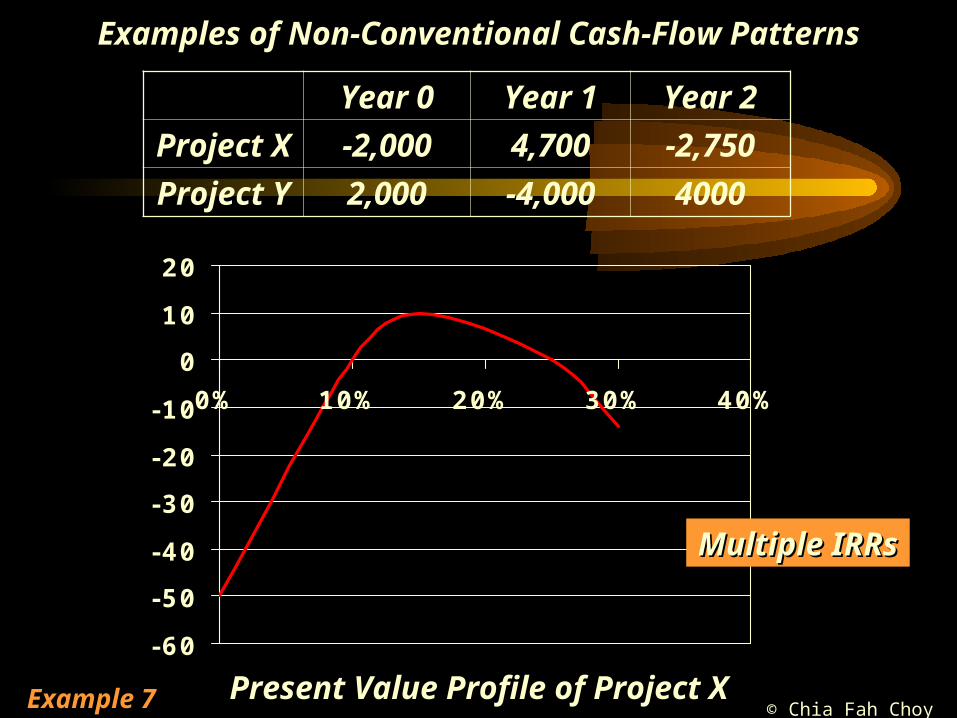

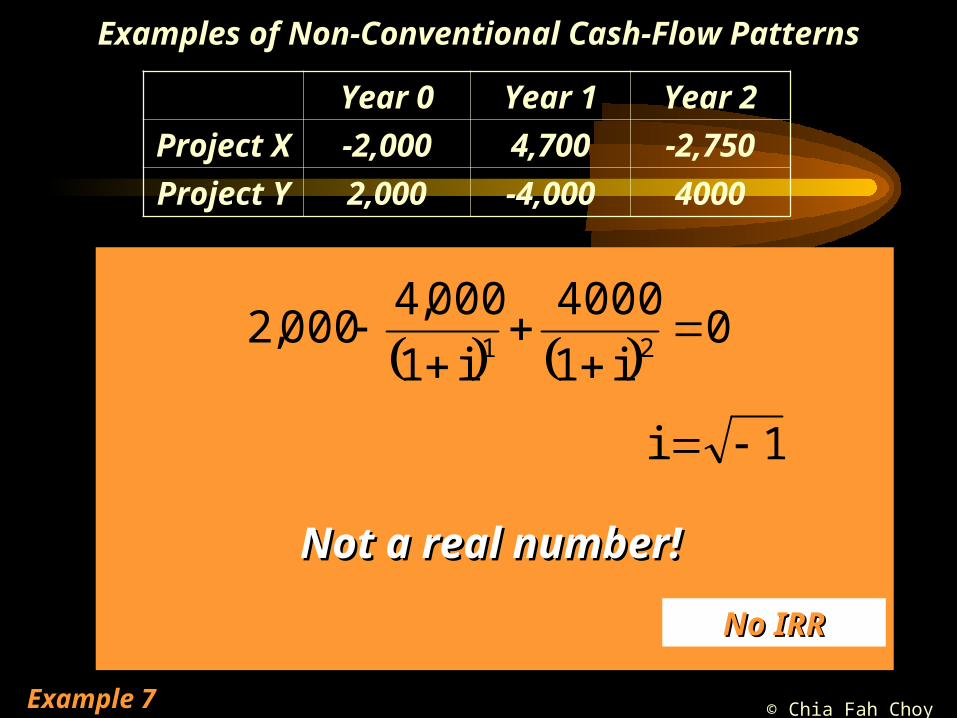

Examples of Non-Conventional Cash-Flow Patterns

Year 0 Year 1 Year 2

Project X -2,000 4,700 -2,750

Project Y 2,000 -4,000 4000

• Project X has 2 outflows and is thus non-conventional

• Project Y has an outflow in a year’s time instead of initially and is thus non-conventional

• When a project has non-conventional cash flows it may have– One IRR

– Multiple IRRs

– No IRR

Example 7

© Chia Fah Choy 2005

Examples of Non-Conventional Cash-Flow Patterns

Year 0 Year 1 Year 2

Project X -2,000 4,700 -2,750

Project Y 2,000 -4,000 4000

-60

-50

-40

-30

-20

-10

0

10

20

0% 10% 20% 30% 40%

Present Value Profile of Project X

Multiple IRRsMultiple IRRs

Example 7

© Chia Fah Choy 2005

Examples of Non-Conventional Cash-Flow Patterns

Year 0 Year 1 Year 2

Project X -2,000 4,700 -2,750

Project Y 2,000 -4,000 4000

0

i1

4000

i1

000,4000,2 21

1i

Not a real number!Not a real number!

No IRRNo IRR

Example 7

© Chia Fah Choy 2005

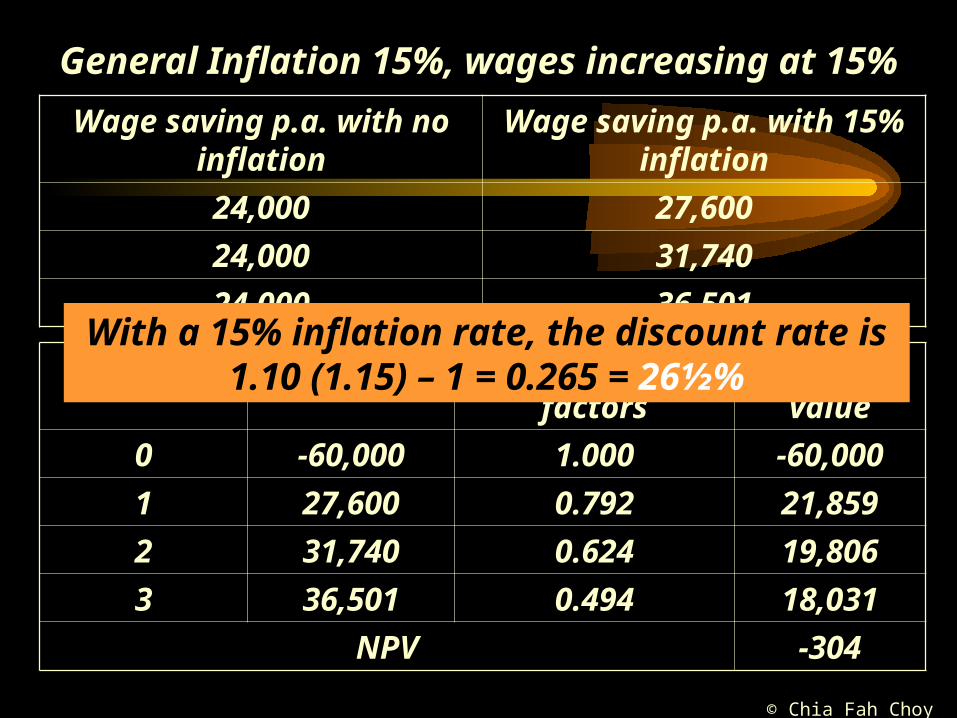

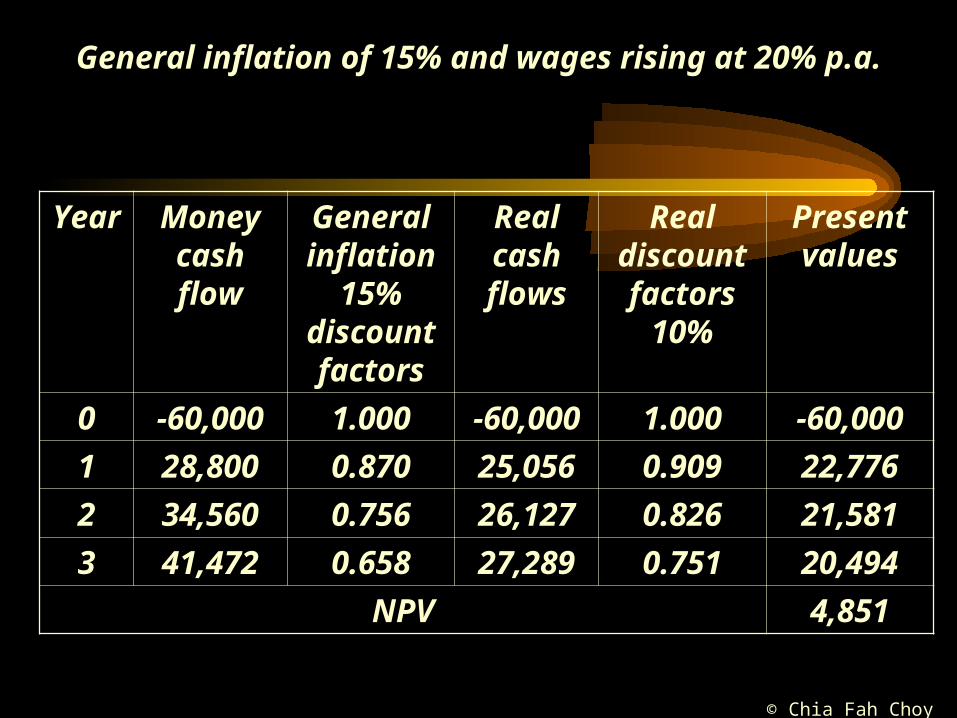

A labour saving machine costs $60,000 and will save $24,000 p.a. at current wage rates. The machine is expected to have a 3 year life and nil scrap value. The firm’s cost of capital is 10%.

Calculate the project’s NPVa. With no inflationb.With general inflation of 15% which wage

rates are expected to follow (i.e. synchronised inflation).

c. With general inflation of 15% and wages rising at 20% p.a. (i.e. differential inflation).

Example 8

© Chia Fah Choy 2005

%103A000,24000,60

NPV – No inflation

487.2000,24000,60 312

Project unacceptable as it has a negative NPV at company’s cost of

capital.

1.0

1.01

11 3

© Chia Fah Choy 2005

General Inflation 15%, wages increasing at 15%

487.2000,24000,60 312

Wage saving p.a. with no inflation

Wage saving p.a. with 15% inflation

24,000 27,600

24,000 31,740

24,000 36,501

Year Cash flow 26 ½% Discount factors

Present value

0 -60,000 1.000 -60,000

1 27,600 0.792 21,859

2 31,740 0.624 19,806

3 36,501 0.494 18,031

NPV -304

With a 15% inflation rate, the discount rate is 1.10 (1.15) – 1 = 0.265 = 26½%

© Chia Fah Choy 2005

General inflation of 15% and wages rising at 20% p.a.

487.2000,24000,60 312

Year Money cash flow

General inflation

15% discount factors

Real cash flows

Real discount factors

10%

Present values

0 -60,000 1.000 -60,000 1.000 -60,000

1 28,800 0.870 25,056 0.909 22,776

2 34,560 0.756 26,127 0.826 21,581

3 41,472 0.658 27,289 0.751 20,494

NPV 4,851

© Chia Fah Choy 2005

Summary• Investment decisions are long run decisions

where consumption and investment opportunities are balanced over time.

• The decision to invest is based on many factors including: the investor’s beliefs in the future, the alternatives available and his attitude to risk.

• The ‘traditional’ investment appraisal techniques are the accounting rate of return and payback.

• Discount Cash Flow (DCF) techniques use cash flows rather than profits and take account of the time value of money.

© Chia Fah Choy 2005

Summary• The formula for Net Present Value is

and given the assumption of the basic model, a project is acceptable if it has a positive NPV at the firm’s cost of capital.

• NPV can be interpreted as the potential increase in consumption made possible by the project valued in present day terms.

ii

0i

ni r1

CNPV

© Chia Fah Choy 2005

Summary• Internal Rate of Return (IRR) is the discount rate

which gives zero NPV and can be found graphically or by linear interpolation.

• With conventional projects IRR and NPV give the same accept or reject decision. NPV is an absolute measure whereas IRR is a relative one.

• NPV is a more appropriate measure for choosing between mutually exclusive projects and in general is technically superior to IRR.

© Chia Fah Choy 2005

Summary• The discount rate used in DCF calculations is

known as the cost of capital.• Specific inflation is of more direct concern in

investment appraisal and differential inflation is commonly encountered.

• The general treatment of inflation in investment appraisal means distinguishing between money and real cash flows

• The amount and timing of tax payment and other tax effects must be considered

© Chia Fah Choy 2005

Points to note!!• Successful investment appraisal is entirely

dependent on the accuracy of cost and revenue estimates. No appraisal technique can overcome significant inaccuracies in the estimates.

© Chia Fah Choy 2005

Learning Objectives

After studying this topic you will:• understand the basis of long-term decision making;• be able to use traditional appraisal techniques of

Accounting Rate of Return and Payback;• know the reasons why Discounted Cash Flow (DCF)

techniques are used;• be able to calculate and interpret Net Present Value

(NPV);• understand Internal rate of Return (IRR);• know what is meant by the Excess Present Value Index;• understand the effects of inflation on investment

appraisal