Embed Size (px)

Citation preview

© 2015 Snell & Wilmer1 © 2015 Snell & Wilmer

Common Errors in Qualified Retirement Plans

April 2, 2015

Presenter:Greg Gautam

Arizona Total Rewards Association

© 2015 Snell & Wilmer2

Types of Plan Errors• Operational Errors• Plan Document Errors• Fiduciary Errors

© 2015 Snell & Wilmer3

Operational Errors• Failure to administer the plan in accordance with its

terms• Can usually be corrected using the IRS’ Employee

Plans Compliance Resolution System

© 2015 Snell & Wilmer4

Common Operational Failures• Eligibility failures• Vesting failures• Contribution failures• Distribution failures• Plan Loan failures

© 2015 Snell & Wilmer5

Eligibility Failures• The Code allows a plan sponsor to impose certain

restrictions before an employee can participate in a plan (e.g., waiting period up to one year, age limit, service threshold of 1,000 hours)

• Mistakes often arise due to a failure to understand plan terms

• The best way to avoid eligibility failures is to read your plan document!

© 2015 Snell & Wilmer6

Eligibility Failures (cont’d)• Plan sponsor’s failure to include employees in the plan when they first

meet the plan’s eligibility requirements– Plan has 1,000 hour service requirement. Employee who normally

works part-time filled in for a colleague during 2014 and worked 1,050 hours. Plan administrator failed to notify employee that he or she was eligible to participate in the plan as of January 1, 2015

– Plan provides that employees are automatically enrolled after 60 days of employment unless they opt out. Plan sponsor must automatically enroll employees within the 60-day period unless they opt out

– Plan sponsor fails to provide initial safe harbor notice to newly eligible employees. Due to the failure, certain employees were not aware of their eligibility to participate, so they did not complete deferral election forms and missed out on a company matching contribution

© 2015 Snell & Wilmer7

Eligibility Failures (cont’d)• Plan sponsor’s inclusion of employees in the plan before

they first satisfy the plan’s eligibility requirements– Inclusion of ineligible class of employees (e.g.,

employees who work for a non-adopting affiliate)• If a company acquires an entity that is an affiliate,

the company’s plan must be amended to allow participation of the affiliate’s employees before they can make deferrals

– Inclusion prior to satisfaction of the plan’s age and service requirements

© 2015 Snell & Wilmer8

Vesting Failures• The Code allows a plan sponsor to vest participants

in their matching and profit-sharing contributions pursuant to specified vesting schedules

• Mistakes often arise due to a failure to accurately track dates of hire and completed service

• Vesting failures often result in the under or over payment of benefits

© 2015 Snell & Wilmer9

Vesting Failures (cont’d)• Forfeiture of vested benefits (Underpayment)– Plan credits the participant with less vesting service

than the participant earned. The participant terminates employment and receives a smaller benefit when the account is distributed

• Distribution of nonvested benefits (Overpayment)– Plan credits the participant with more vesting service

than the participant earned. The participant terminates employment and receives a larger benefit when the account is distributed

© 2015 Snell & Wilmer10

Contribution Failures• Disconnect between plan’s definition of “compensation” and

the payroll system definition of “compensation”– A plan might define compensation as W-2 compensation,

excluding certain fringe benefits. When items of compensation are coded into the payroll system, some of the fringe benefits are mistakenly coded as compensation for purposes of making 401(k) deferrals. Now participants can make deferrals on items of compensation that the plan terms do not allow

• Contributions in excess of prescribed IRS limits (e.g., the Section 402(g) limit, the Section 415 limit, the Section 401(a)(17) limit)

• Contributions in excess of the plan’s prescribed limits

© 2015 Snell & Wilmer11

Distribution Failures• Improper hardship distributions

– Plan does not permit hardships or the event does not qualify as a hardship under the plan

– No supporting documentation– Distribution in excess of hardship amount– Failure to suspend elective deferrals for 6 months after hardship

distribution– Failure to restart elective deferrals after hardship distribution (if that is

what the plan provides)– Failure to exhaust other available distributions and loans before taking

hardship• Failure to distribute required minimum distributions• Failure to offer distribution option permitted under the plan or permitting

distribution option not available under the plan

© 2015 Snell & Wilmer12

Plan Loan Failures• Improper amortization– Unless the loan is for the purchase of a principal

residence, loans need to be repaid 5 years from the origination date (not 5 years from the payroll period following the loan origination date)

• Failure to default loan on time• Use of incorrect interest rate– If interest is charged at prime + 2%, make sure you know

whether the plan sponsor or third party administrator will update prime

© 2015 Snell & Wilmer13

Plan Document Errors• Failure to timely amend for changes in the law

– Good faith EGTRRA amendment– Automatic rollover amendment (Section 401(a)(31)(B))– Final 401(a)(9) regulations– Final 401(k) & (m) regulations– Final 415 regulations– Pension Protection Act of 2006– HEART Act

• Failure to timely amend for discretionary changes• Failure of a participating affiliate to adopt plan• Failure to timely adopt written plan document

© 2015 Snell & Wilmer14

Fiduciary Errors• Plan fiduciaries must act prudently and for the

exclusive benefit of plan participants• Plan expense failures– Use of plan assets to pay excessive fees to service

providers– Use of plan assets to pay improper expenses• Plans cannot pay for settlor functions (e.g., plan

design studies or the drafting of discretionary amendments)

© 2015 Snell & Wilmer15

Fiduciary Errors (cont’d)• Failure to timely forward contributions to the trust– Must deposit as soon as possible– Seven business day safe harbor for small plans, even if

deposit could have been made earlier– Late contributions are a fiduciary violation under ERISA– Be consistent• If it generally takes a large plan 10 days to forward

contributions to the trust, if one time contributions were forwarded in 4 days, the DOL may take the position that contributions always should be forwarded in 4 days

© 2015 Snell & Wilmer16

Correction of Plan Failures

© 2015 Snell & Wilmer17

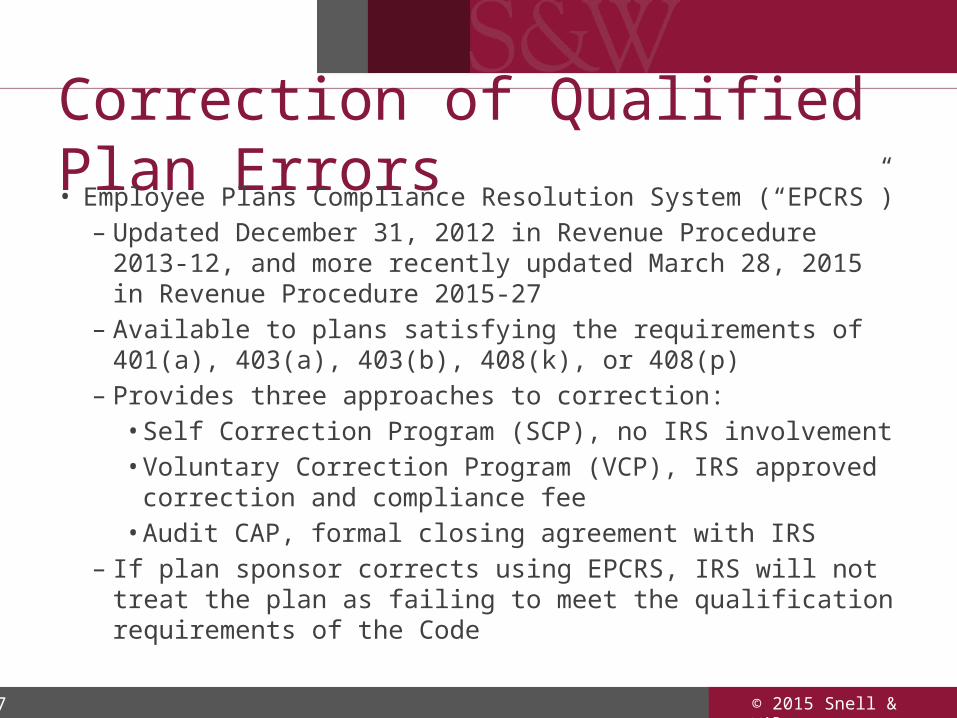

Correction of Qualified Plan Errors• Employee Plans Compliance Resolution System (“EPCRS”)

– Updated December 31, 2012 in Revenue Procedure 2013-12, and more recently updated March 28, 2015 in Revenue Procedure 2015-27

– Available to plans satisfying the requirements of 401(a), 403(a), 403(b), 408(k), or 408(p)

– Provides three approaches to correction:• Self Correction Program (SCP), no IRS involvement• Voluntary Correction Program (VCP), IRS approved correction

and compliance fee• Audit CAP, formal closing agreement with IRS

– If plan sponsor corrects using EPCRS, IRS will not treat the plan as failing to meet the qualification requirements of the Code

© 2015 Snell & Wilmer18

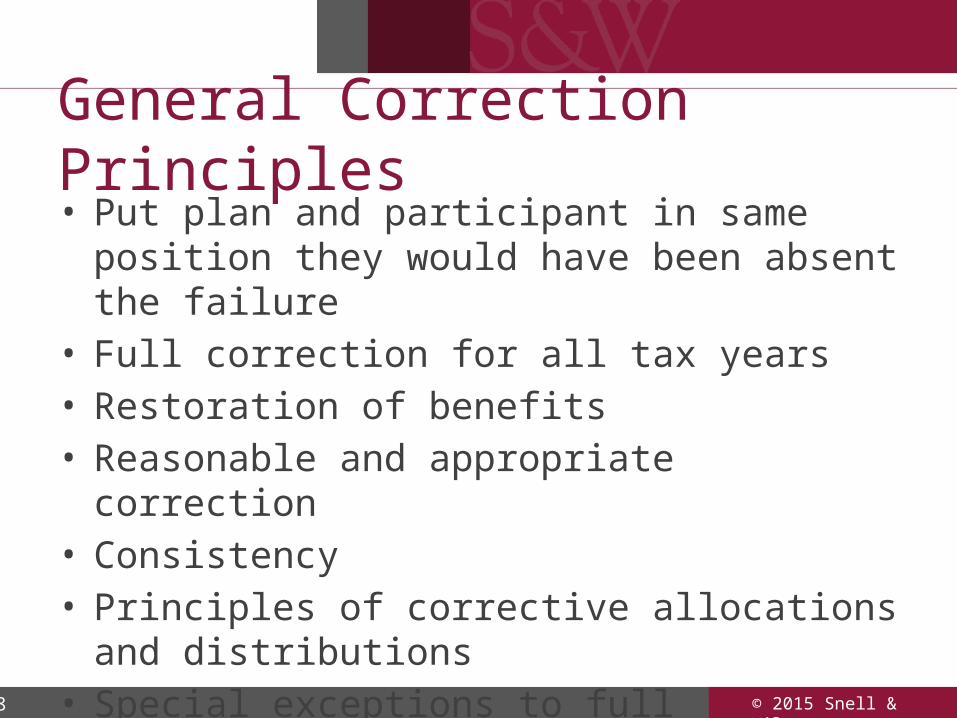

General Correction Principles• Put plan and participant in same position they would

have been absent the failure• Full correction for all tax years• Restoration of benefits• Reasonable and appropriate correction• Consistency• Principles of corrective allocations and distributions• Special exceptions to full correction

© 2015 Snell & Wilmer19

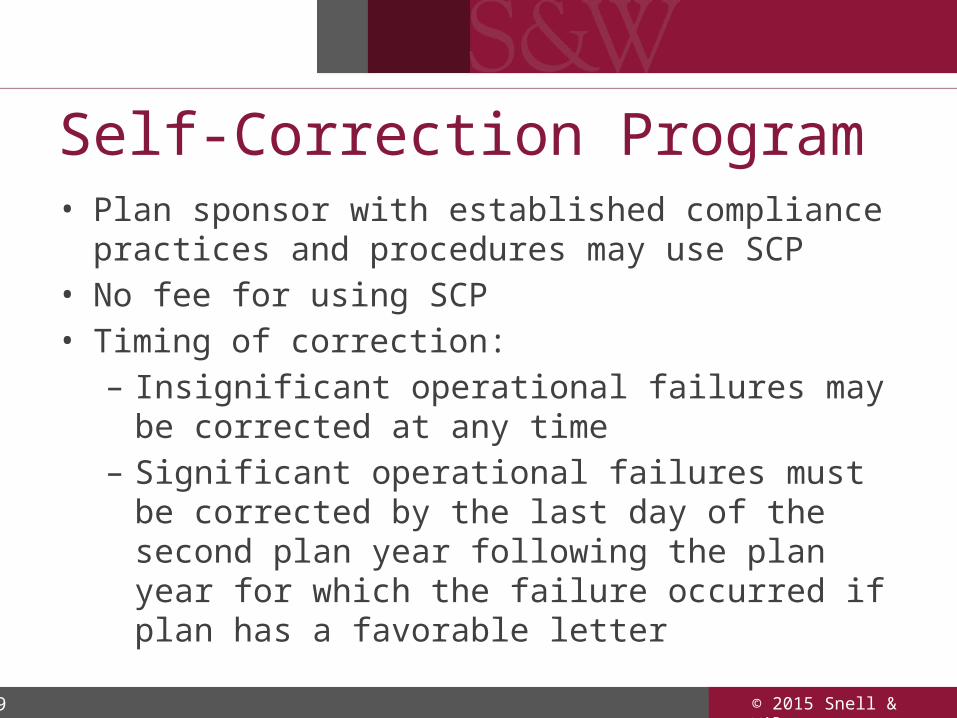

Self-Correction Program• Plan sponsor with established compliance practices and

procedures may use SCP• No fee for using SCP• Timing of correction:– Insignificant operational failures may be corrected at any

time– Significant operational failures must be corrected by the

last day of the second plan year following the plan year for which the failure occurred if plan has a favorable letter

© 2015 Snell & Wilmer20

Self-Correction Program (cont’d)• Is the failure significant or insignificant?• Factors to determine significance:

– Other failures during the period– Percentage of plan assets and contributions involved– Number of years of the failure– Number of participants affected– Number affected relative to the number that could have been

affected– Timeliness of correction– Reason for the failure (e.g., minor arithmetic errors)

• If a plan has multiple failures, the failures are eligible for SCP only if all of the operational failures are insignificant in the aggregate

© 2015 Snell & Wilmer21

Voluntary Correction Program• VCP allows a plan to pay a compliance fee and seek IRS

approval of the correction• Generally protected from IRS examination while VCP is

pending– No protection if VCP is submitted anonymously– Not available if plan is under examination

• Compliance fee is based on number of plan participants – Fee ranges from $750 (20 or fewer participants) to

$25,000 (over 10,000 participants)– Reduced compliance fees for certain submissions:

© 2015 Snell & Wilmer22

Audit Closing Agreement Program (“CAP”)• Used to correct failures discovered during a plan audit or

review of determination letter application• Plan sponsors enter into a closing agreement with the IRS

instead of facing plan disqualification• Plan sponsor may correct the failure and pay a sanction

based on a negotiated percentage of the maximum payment amount– Maximum payment amount is approximately equal to the

sum of the taxes and penalties that would be paid if the plan were disqualified for all open taxable years

– Audit CAP sanction will be more than VCP compliance fee

© 2015 Snell & Wilmer23

Helpful Hints for Corrections• Regularly review procedures and plan documents to

determine if have qualification failures• If you have a failure, correct it as soon as possible– Use SCP, if available– Document the analysis of the correction and the

correction methodology• If filing VCP submission, correct all failures for one

VCP fee• Read and understand your plan document

© 2015 Snell & Wilmer24

Questions?