Embed Size (px)

Citation preview

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

The Status of National Health Care Reform

2nd Annual Greenbrier ConferenceApril 15, 2012

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Presenter:

Thomas W. Hess, Esq.Dinsmore & Shohl LLPColumbus, Ohio (614) [email protected]

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

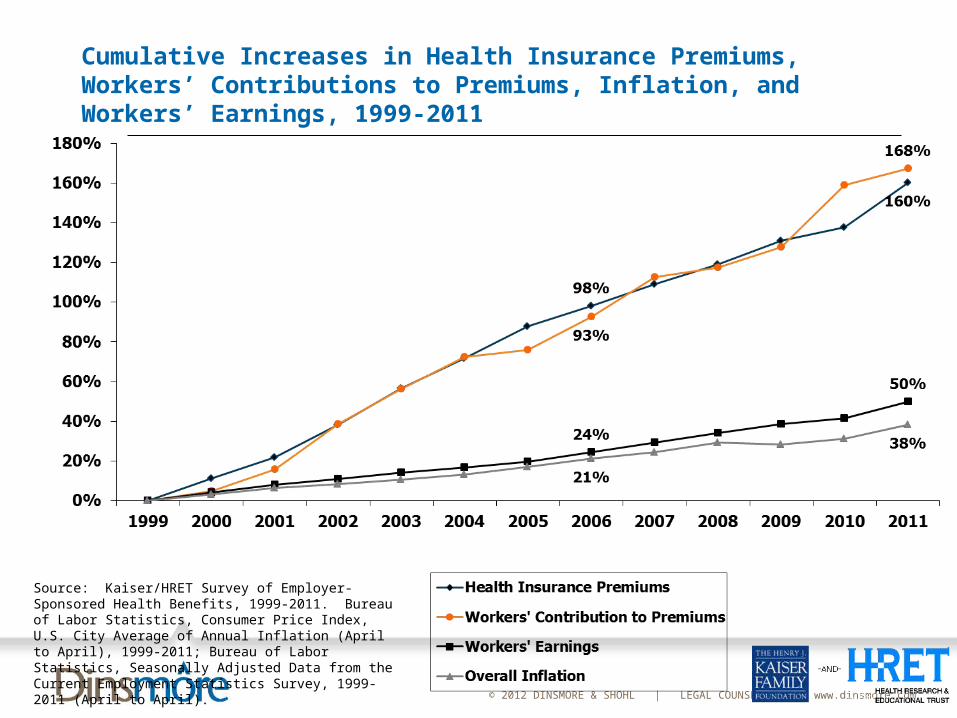

Cumulative Increases in Health Insurance Premiums, Workers’ Contributions to Premiums, Inflation, and Workers’ Earnings, 1999-2011

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2011. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 1999-2011; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1999-2011 (April to April).

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

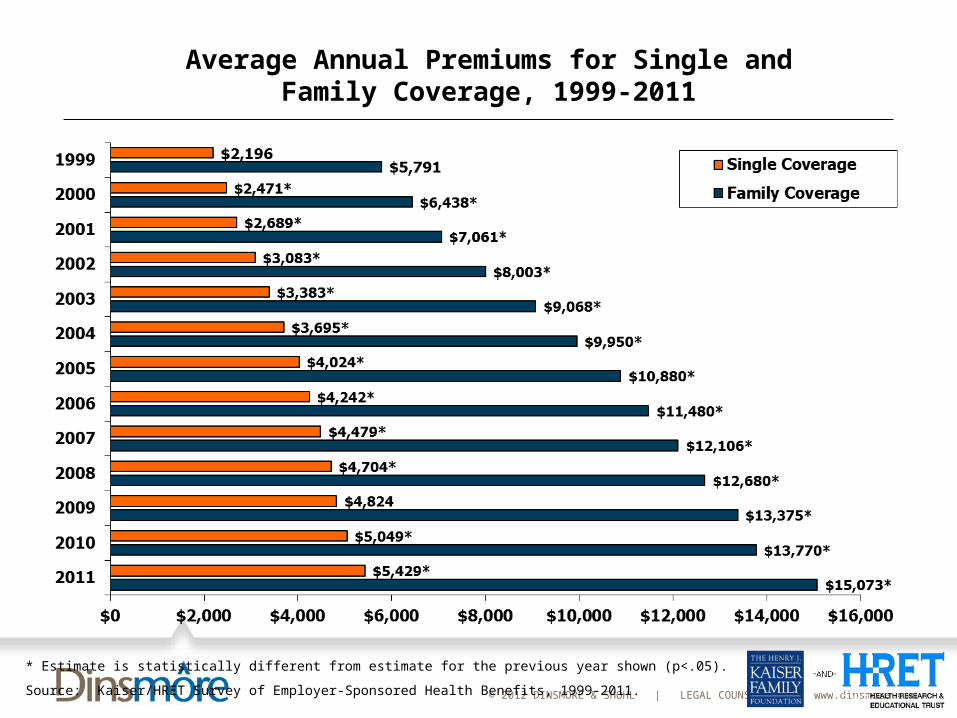

Average Annual Premiums for Single and Family Coverage, 1999-2011

* Estimate is statistically different from estimate for the previous year shown (p<.05).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2011.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

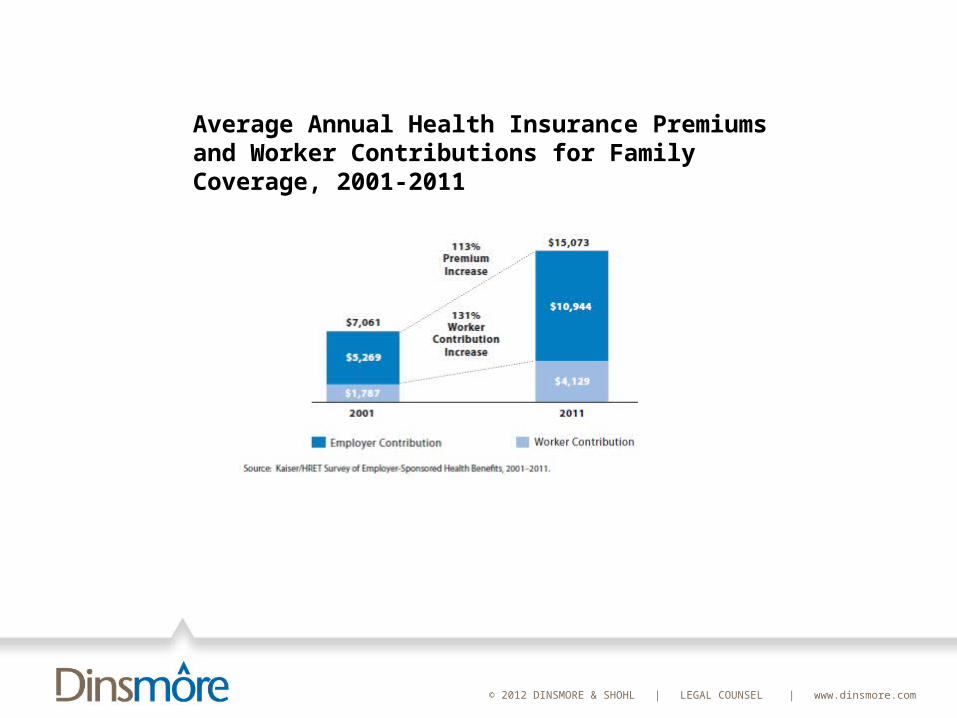

Average Annual Health Insurance Premiums and Worker Contributions for Family Coverage, 2001-2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

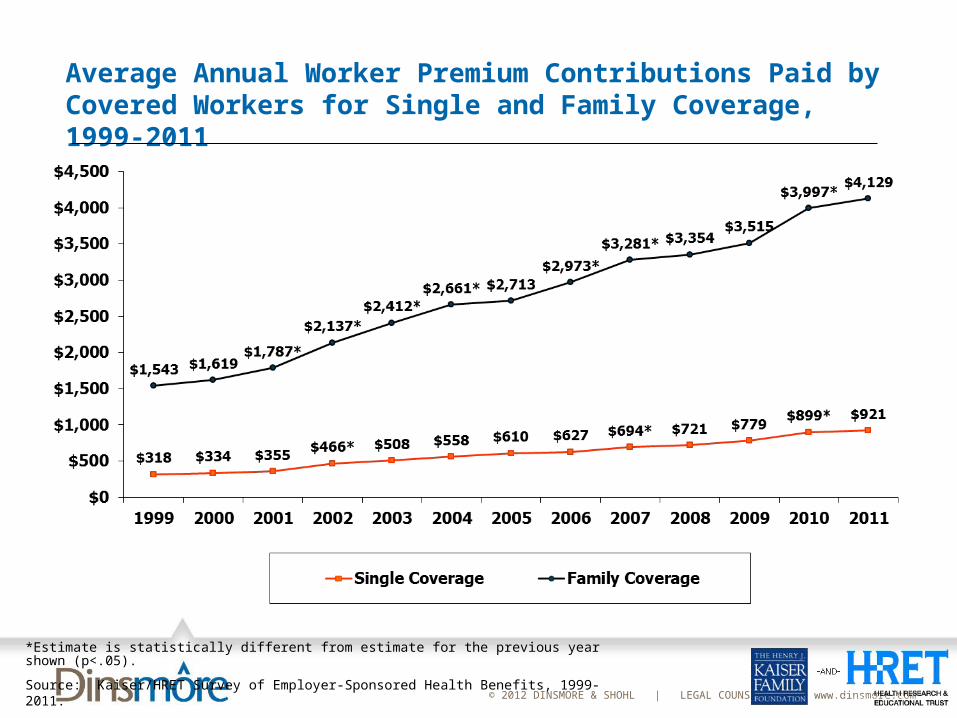

Average Annual Worker Premium Contributions Paid by Covered Workers for Single and Family Coverage, 1999-2011

*Estimate is statistically different from estimate for the previous year shown (p<.05).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2011.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Single Coverage Family Coverage

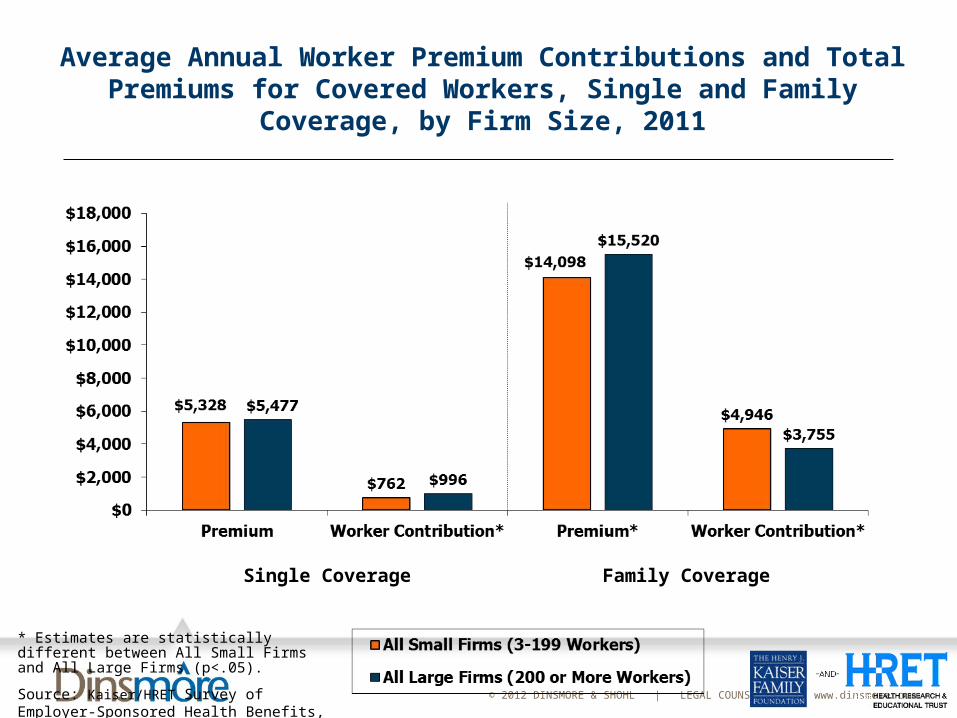

Average Annual Worker Premium Contributions and Total Premiums for Covered Workers, Single and Family

Coverage, by Firm Size, 2011

* Estimates are statistically different between All Small Firms and All Large Firms (p<.05).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2011.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

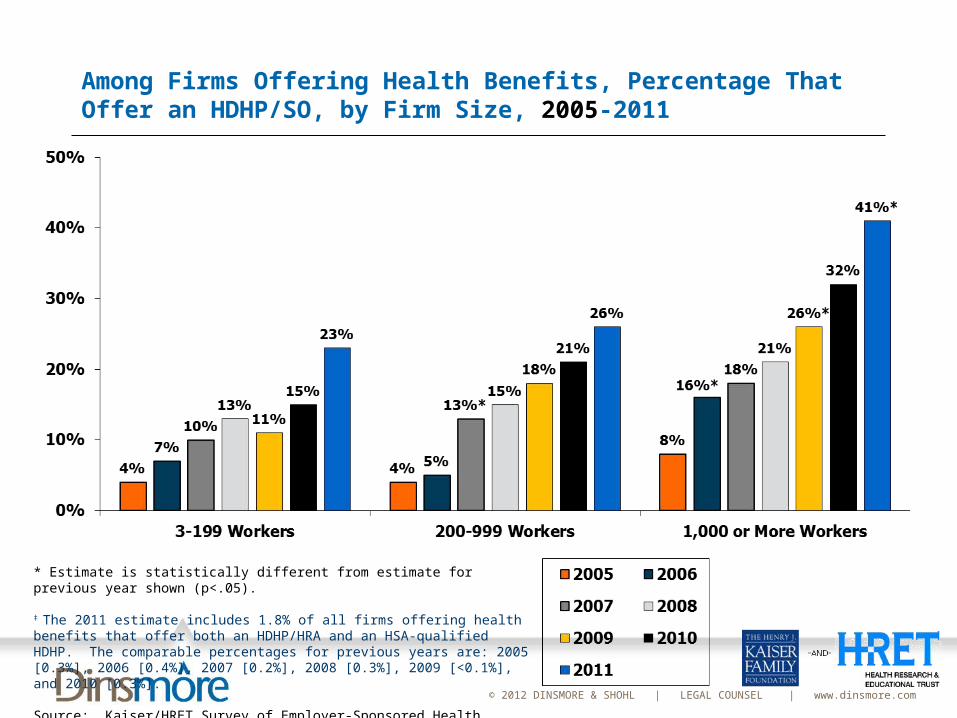

Among Firms Offering Health Benefits, Percentage That Offer an HDHP/SO, by Firm Size, 2005-2011

* Estimate is statistically different from estimate for previous year shown (p<.05).

‡ The 2011 estimate includes 1.8% of all firms offering health benefits that offer both an HDHP/HRA and an HSA-qualified HDHP. The comparable percentages for previous years are: 2005 [0.3%], 2006 [0.4%], 2007 [0.2%], 2008 [0.3%], 2009 [<0.1%], and 2010 [0.3%].

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2005-2011.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future?

MedicareMedicare expenditures are increasing 40% faster than

employer-sponsored health care costsPart A

The projected date of the Part A “Hospital Insurance” Trust Fund exhaustion is 2017

To make Part A expenses equal Part A revenues over the next 75 years: an immediate 134 percent increase in the payroll tax (from a rate of 2.9 percent to 6.78 percent), or an immediate 53 percent reduction in program outlays, or some combination of the two.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

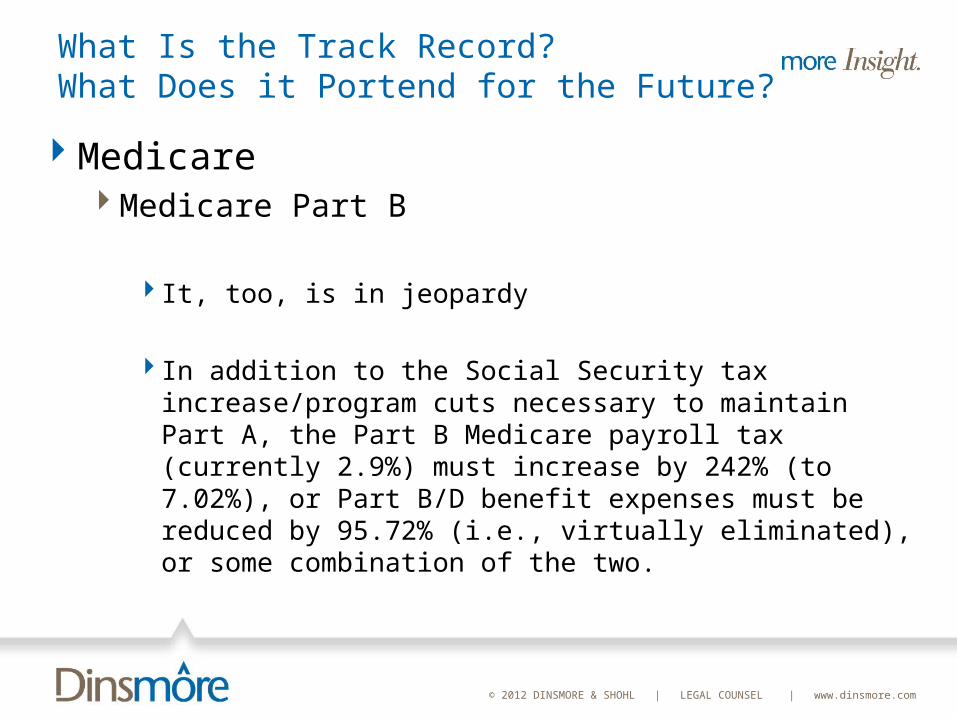

What Is the Track Record? What Does it Portend for the Future?

MedicareMedicare Part B

It, too, is in jeopardy

In addition to the Social Security tax increase/program cuts necessary to maintain Part A, the Part B Medicare payroll tax (currently 2.9%) must increase by 242% (to 7.02%), or Part B/D benefit expenses must be reduced by 95.72% (i.e., virtually eliminated), or some combination of the two.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

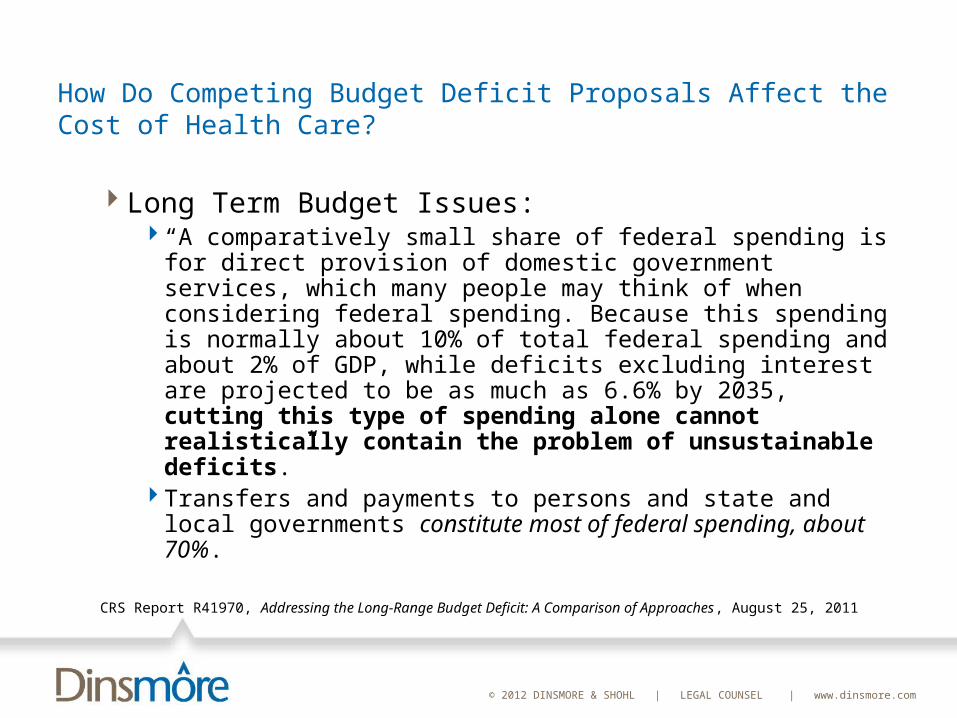

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

Long Term Budget Issues: “A comparatively small share of federal spending is for direct

provision of domestic government services, which many people may think of when considering federal spending. Because this spending is normally about 10% of total federal spending and about 2% of GDP, while deficits excluding interest are projected to be as much as 6.6% by 2035, cutting this type of spending alone cannot realistically contain the problem of unsustainable deficits.”

Transfers and payments to persons and state and local governments constitute most of federal spending, about 70%.

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

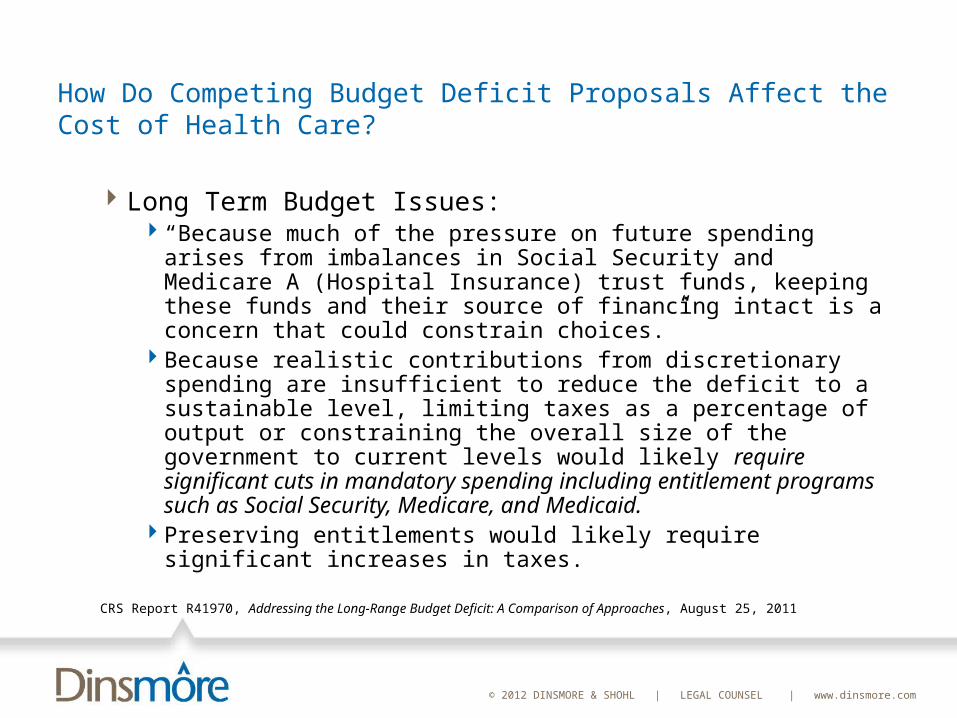

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

Long Term Budget Issues: “Because much of the pressure on future spending arises from

imbalances in Social Security and Medicare A (Hospital Insurance) trust funds, keeping these funds and their source of financing intact is a concern that could constrain choices.”

Because realistic contributions from discretionary spending are insufficient to reduce the deficit to a sustainable level, limiting taxes as a percentage of output or constraining the overall size of the government to current levels would likely require significant cuts in mandatory spending including entitlement programs such as Social Security, Medicare, and Medicaid.

Preserving entitlements would likely require significant increases in taxes.

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

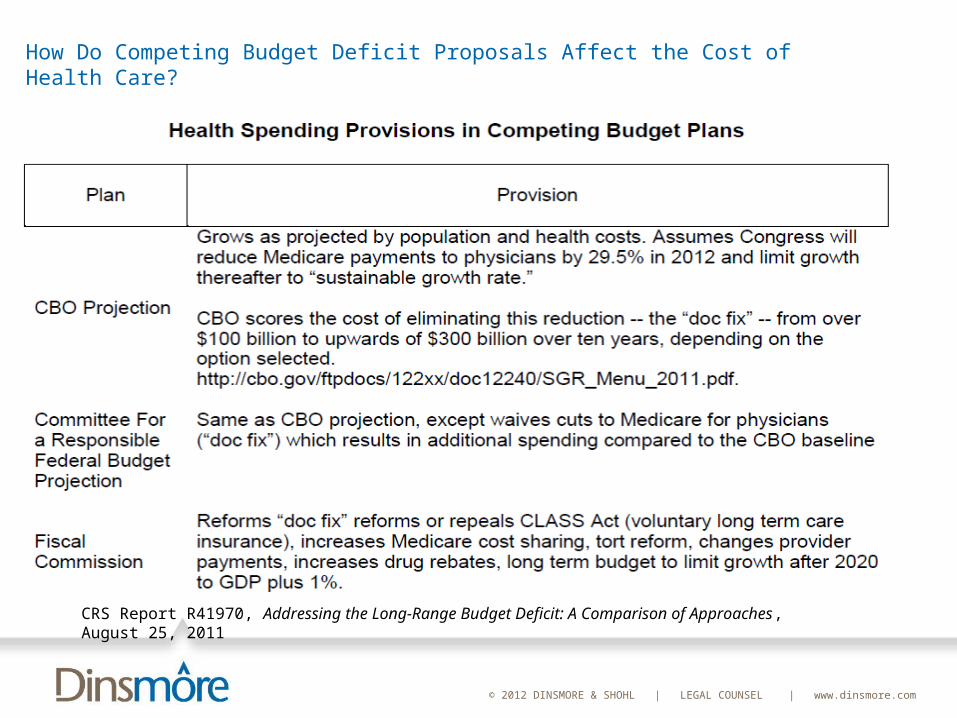

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

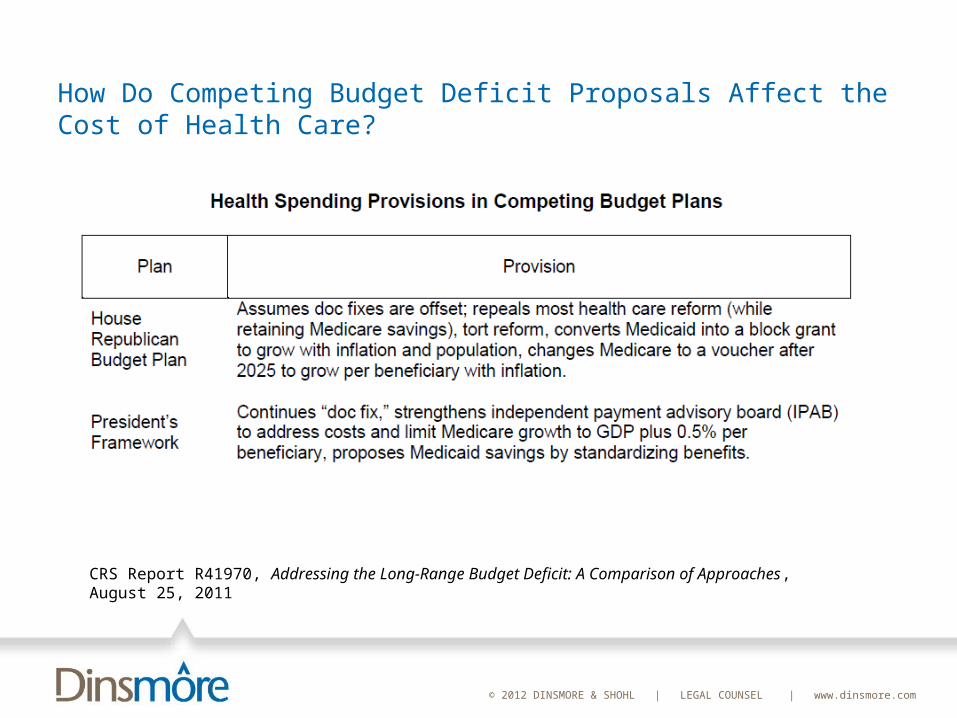

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

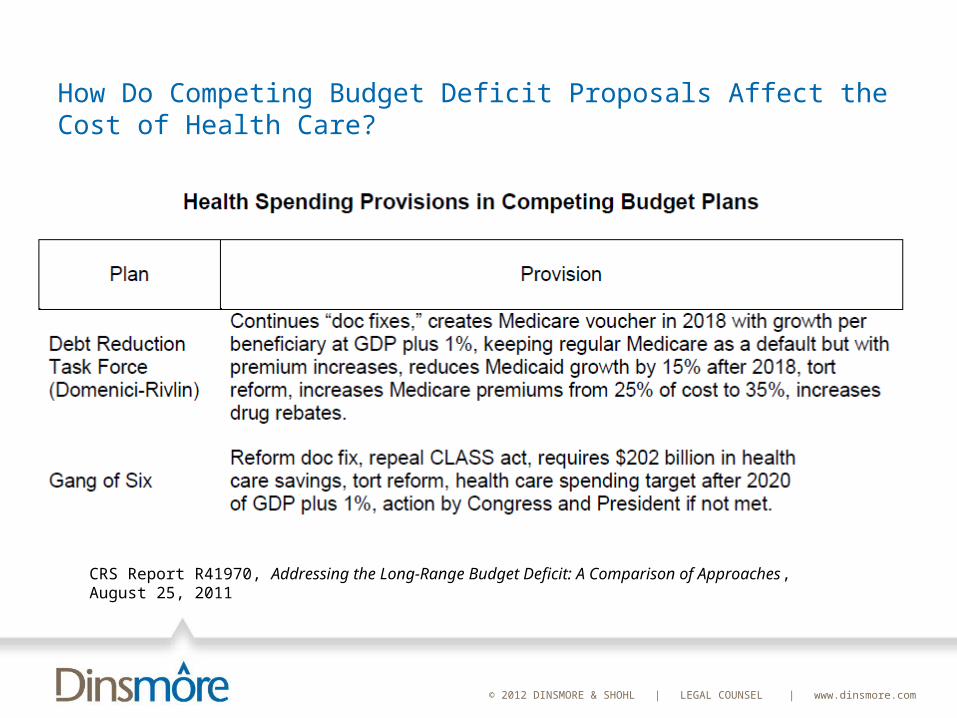

How Do Competing Budget Deficit Proposals Affect the Cost of Health Care?

CRS Report R41970, Addressing the Long-Range Budget Deficit: A Comparison of Approaches, August 25, 2011

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

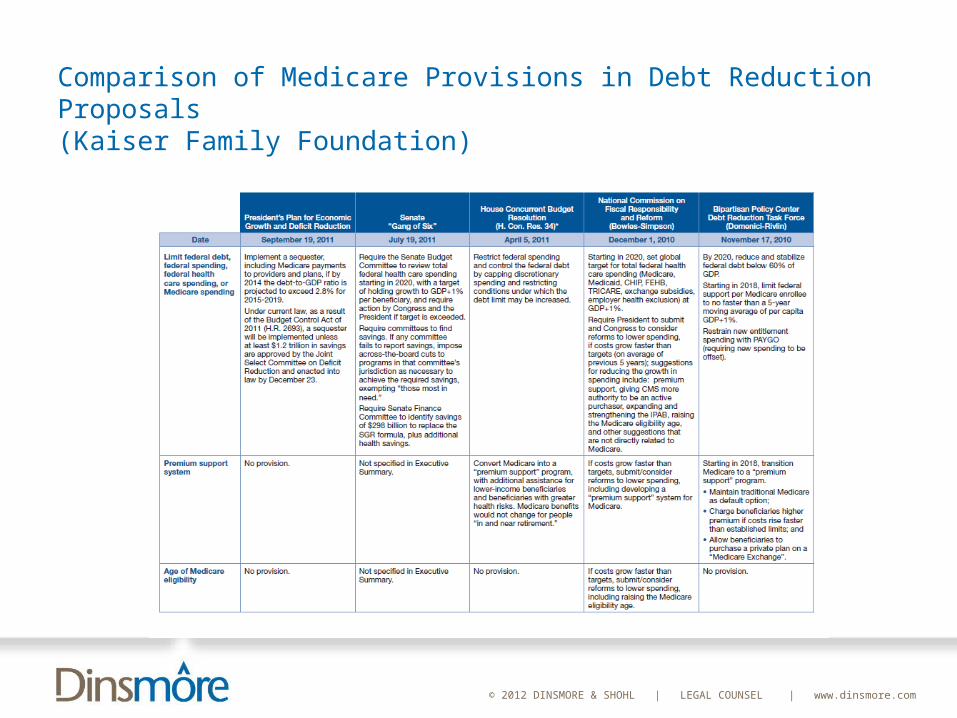

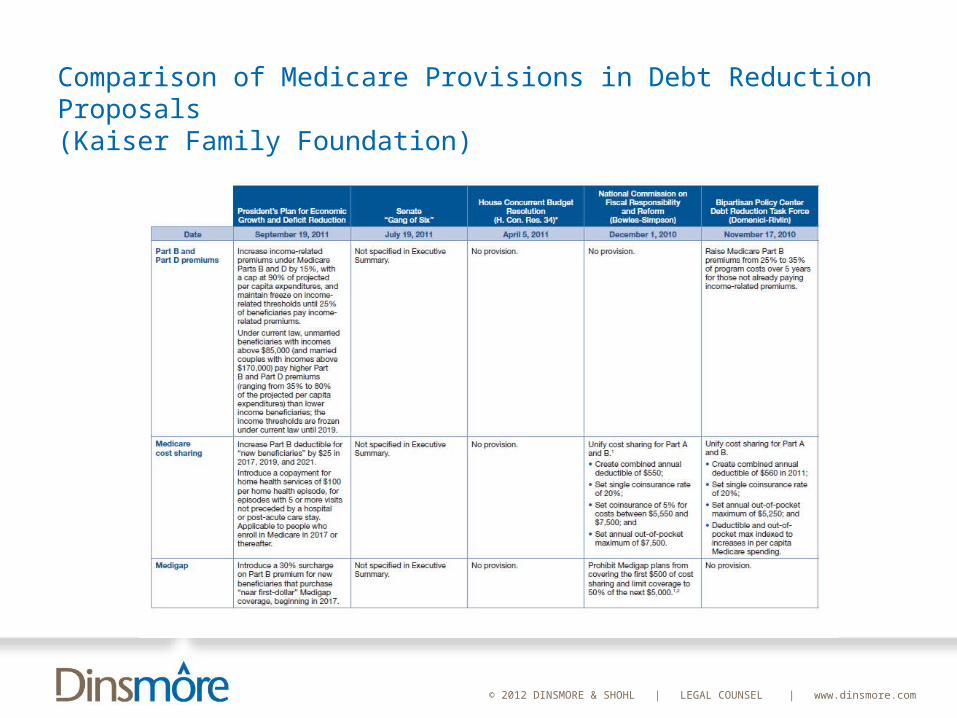

Comparison of Medicare Provisions in Debt Reduction Proposals(Kaiser Family Foundation)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

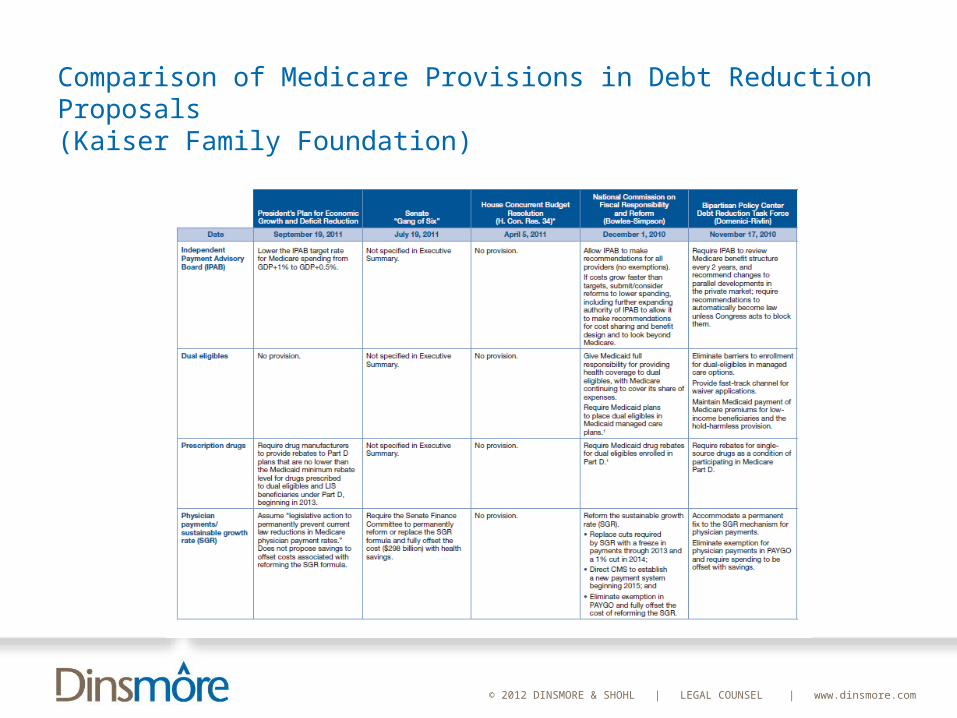

Comparison of Medicare Provisions in Debt Reduction Proposals(Kaiser Family Foundation)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Comparison of Medicare Provisions in Debt Reduction Proposals(Kaiser Family Foundation)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a

Lower Cost?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

Medicare Benefit Design Current FFS benefit design: no upper limit on the amount of

Medicare cost-sharing expenses a beneficiary could incur. Result: more than 90 percent of Medicare beneficiaries

purchase supplemental coverage. The most widely used types of supplemental coverage fill in

all or nearly all of Medicare’s cost sharing. MedPAC: “We have found that when beneficiaries are

insured against Medicare’s cost-sharing requirements, on average they use more care and Medicare spends more on them.”

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

Medicare Benefit DesignMedPAC: “In the near term, potential improvements to

benefit design could, for example, involve adding a cap on beneficiaries’ out-of-pocket (OOP) costs and, at the same time, requiring supplemental policies to have fixed-dollar copayments for services such as office visits and emergency room use instead of simply filling in all cost sharing. Such restrictions on supplemental coverage could lead to reductions in the use of Medicare services sufficient to help finance the addition of an OOP cap… These strategies could also be coupled with cost-sharing protections for low-income beneficiaries so that they would not forgo needed care.”

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

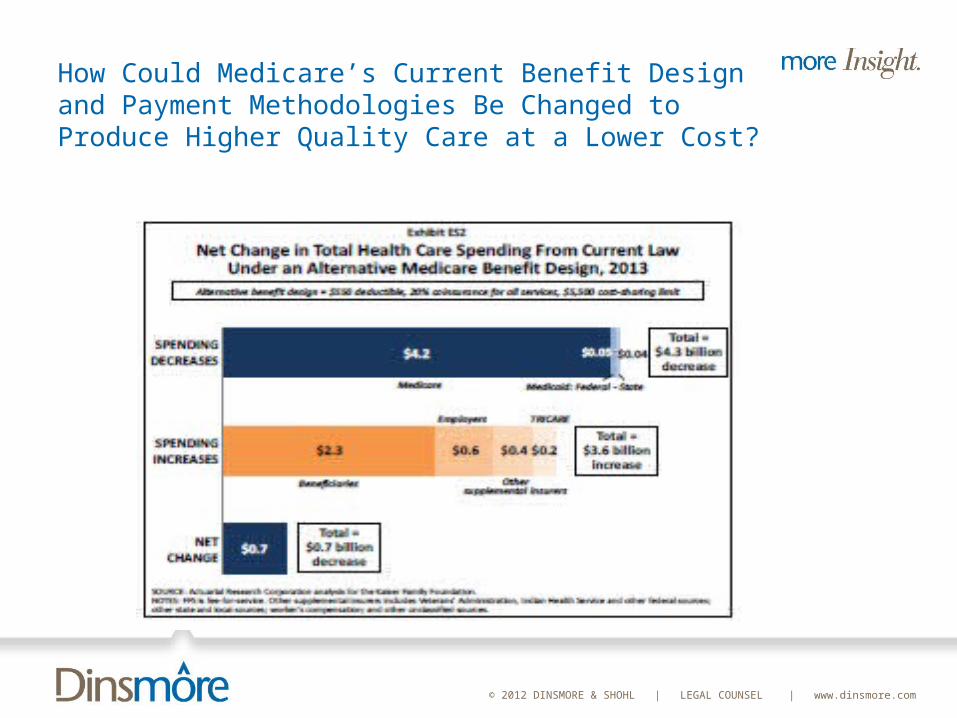

Kaiser Family Foundation Study: Effect of Restructuring Medicare With These Features --a single deductible for Parts A and B of $55020 percent coinsurance on most Medicare-covered

servicesa $5,500 annual limit on cost sharing

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

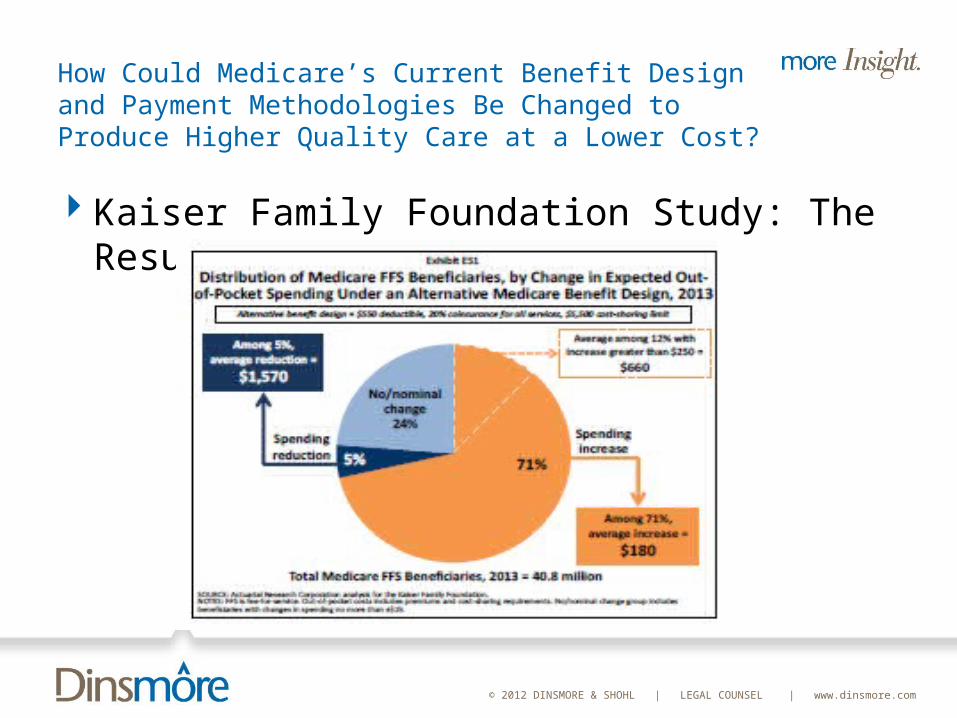

Kaiser Family Foundation Study: The Results

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

Kaiser Family Foundation Study: The Results

Supplemental Coverage: Coverage would expand – but higher premiums will offset some (or all) of the savings for many enrollees

Enrollees with lower utilization – a few physician visits and no inpatient care – will face higher costs. The unified $550 deductible exceeds the Part B deductible under current law.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Could Medicare’s Current Benefit Design and Payment Methodologies Be Changed to Produce Higher Quality Care at a Lower Cost?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future? MedPAC’s Report

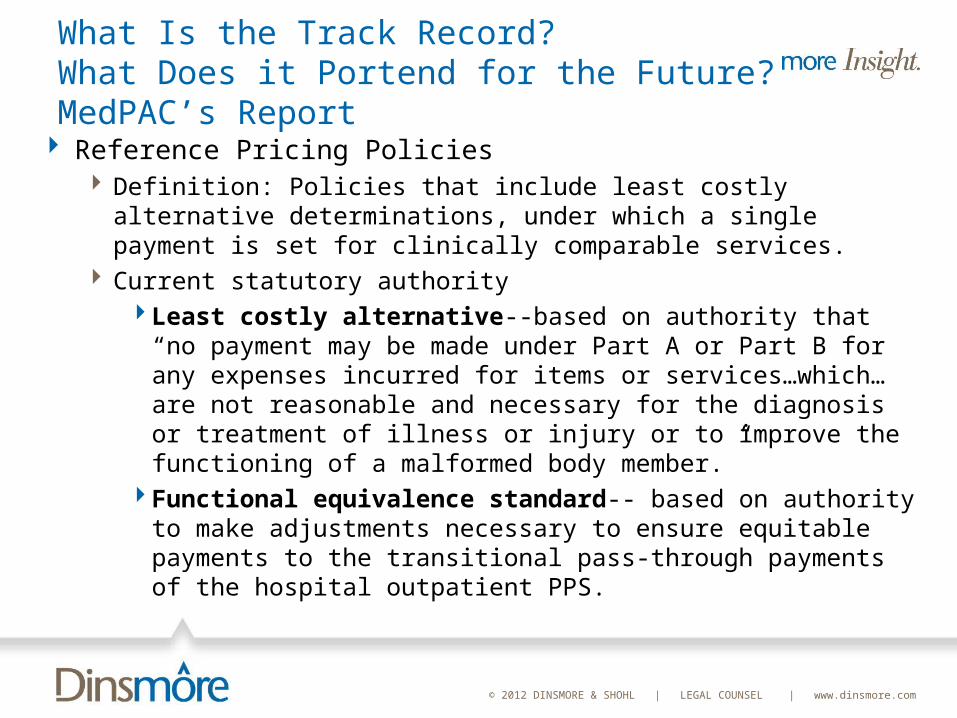

Reference Pricing Policies Definition: Policies that include least costly alternative

determinations, under which a single payment is set for clinically comparable services.

Current statutory authorityLeast costly alternative--based on authority that “no payment

may be made under Part A or Part B for any expenses incurred for items or services…which…are not reasonable and necessary for the diagnosis or treatment of illness or injury or to improve the functioning of a malformed body member.”

Functional equivalence standard-- based on authority to make adjustments necessary to ensure equitable payments to the transitional pass-through payments of the hospital outpatient PPS.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future? MedPAC’s Report

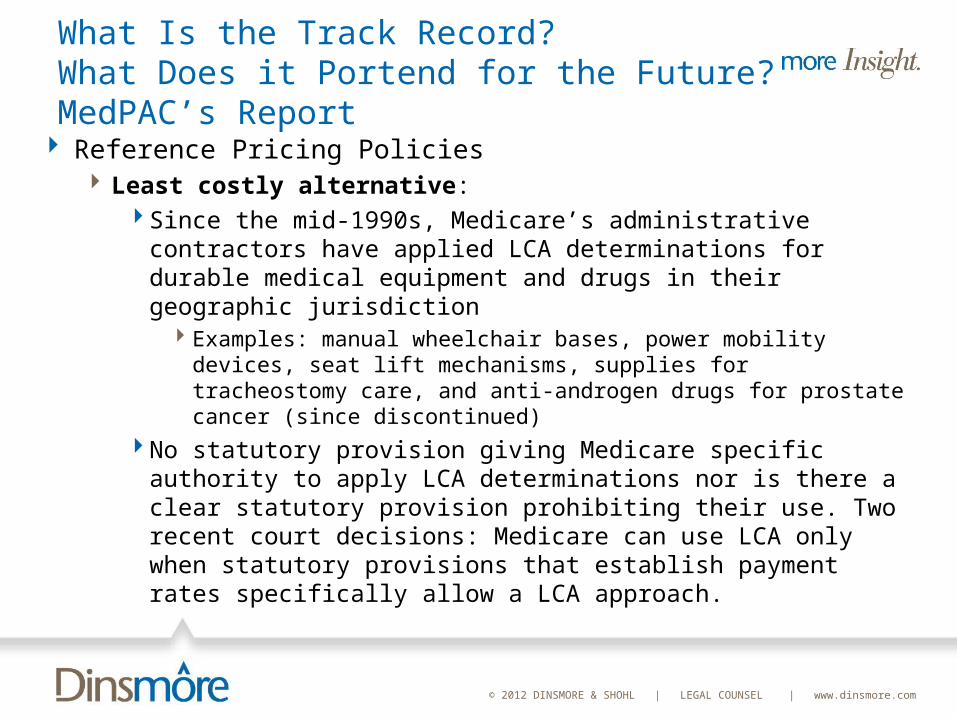

Reference Pricing Policies Least costly alternative:

Since the mid-1990s, Medicare’s administrative contractors have applied LCA determinations for durable medical equipment and drugs in their geographic jurisdiction

Examples: manual wheelchair bases, power mobility devices, seat lift mechanisms, supplies for tracheostomy care, and anti-androgen drugs for prostate cancer (since discontinued)

No statutory provision giving Medicare specific authority to apply LCA determinations nor is there a clear statutory provision prohibiting their use. Two recent court decisions: Medicare can use LCA only when statutory provisions that establish payment rates specifically allow a LCA approach.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future? MedPAC’s Report

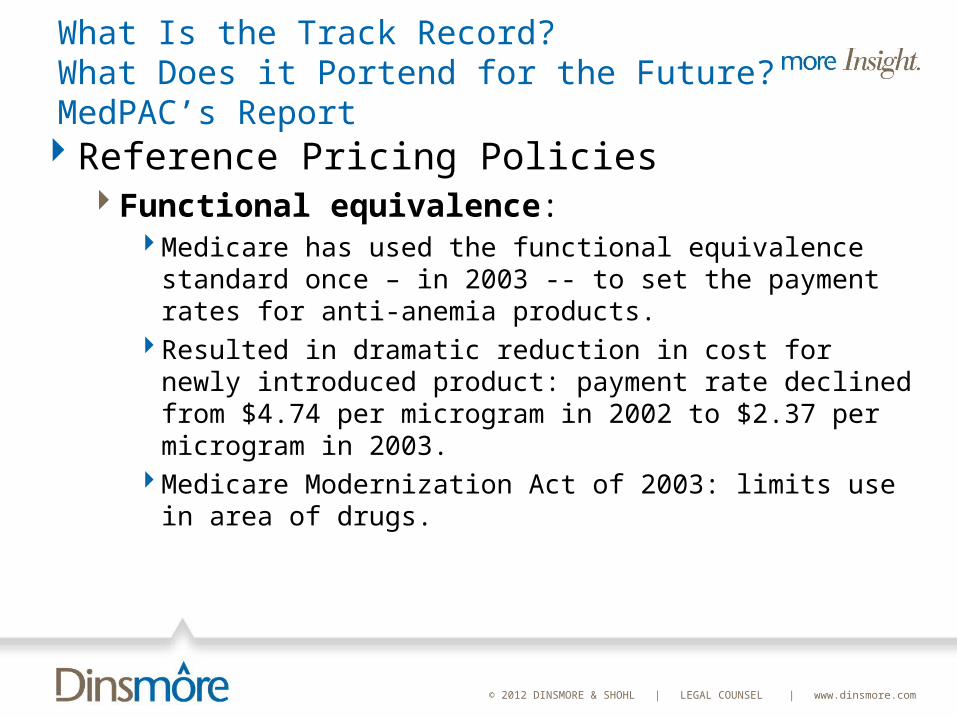

Reference Pricing PoliciesFunctional equivalence:

Medicare has used the functional equivalence standard once – in 2003 -- to set the payment rates for anti-anemia products.

Resulted in dramatic reduction in cost for newly introduced product: payment rate declined from $4.74 per microgram in 2002 to $2.37 per microgram in 2003.

Medicare Modernization Act of 2003: limits use in area of drugs.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

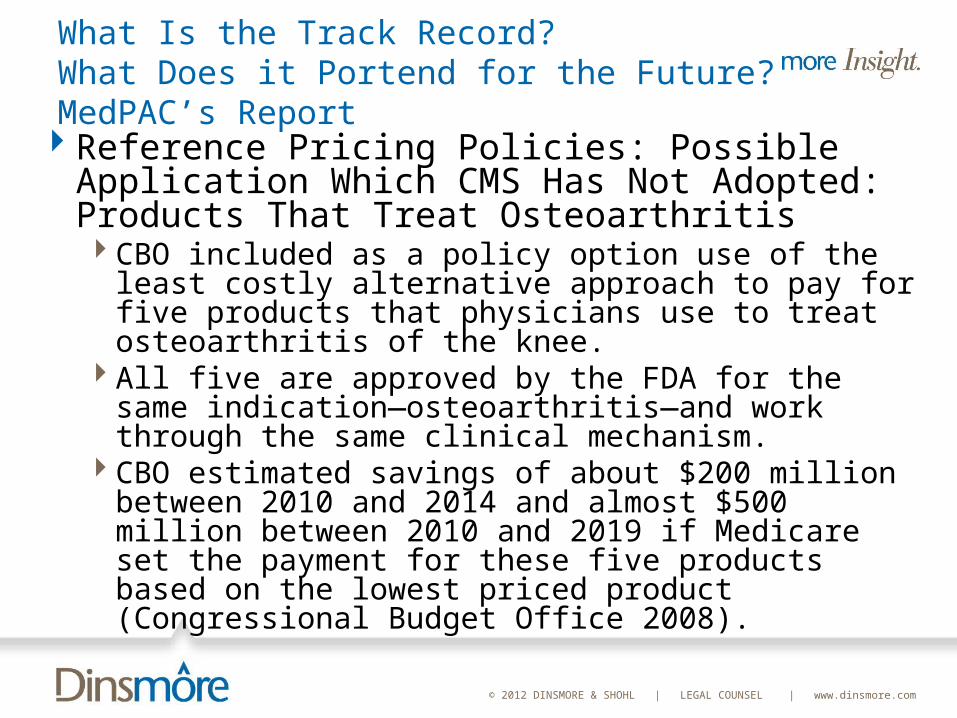

What Is the Track Record? What Does it Portend for the Future? MedPAC’s Report

Reference Pricing Policies: Possible Application Which CMS Has Not Adopted: Products That Treat Osteoarthritis CBO included as a policy option use of the least costly

alternative approach to pay for five products that physicians use to treat osteoarthritis of the knee.

All five are approved by the FDA for the same indication—osteoarthritis—and work through the same clinical mechanism.

CBO estimated savings of about $200 million between 2010 and 2014 and almost $500 million between 2010 and 2019 if Medicare set the payment for these five products based on the lowest priced product (Congressional Budget Office 2008).

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Competitive is the Marketplace for Employer-Sponsored Group Health Insurance? Will Providers Seek to Recoup Reduced Medicare

Payments from the Private Sector?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

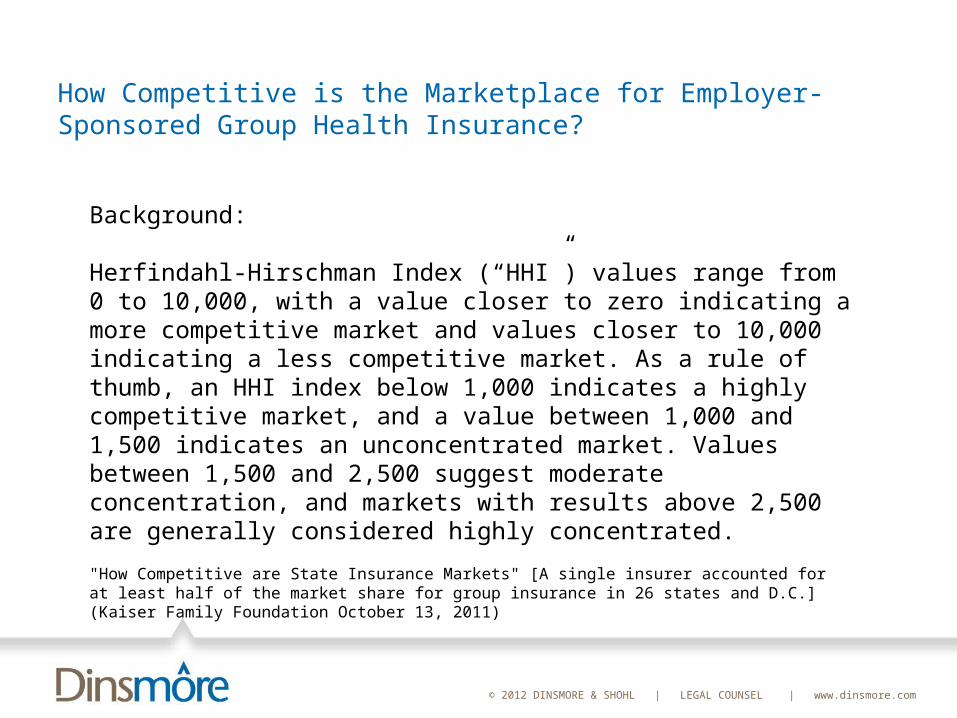

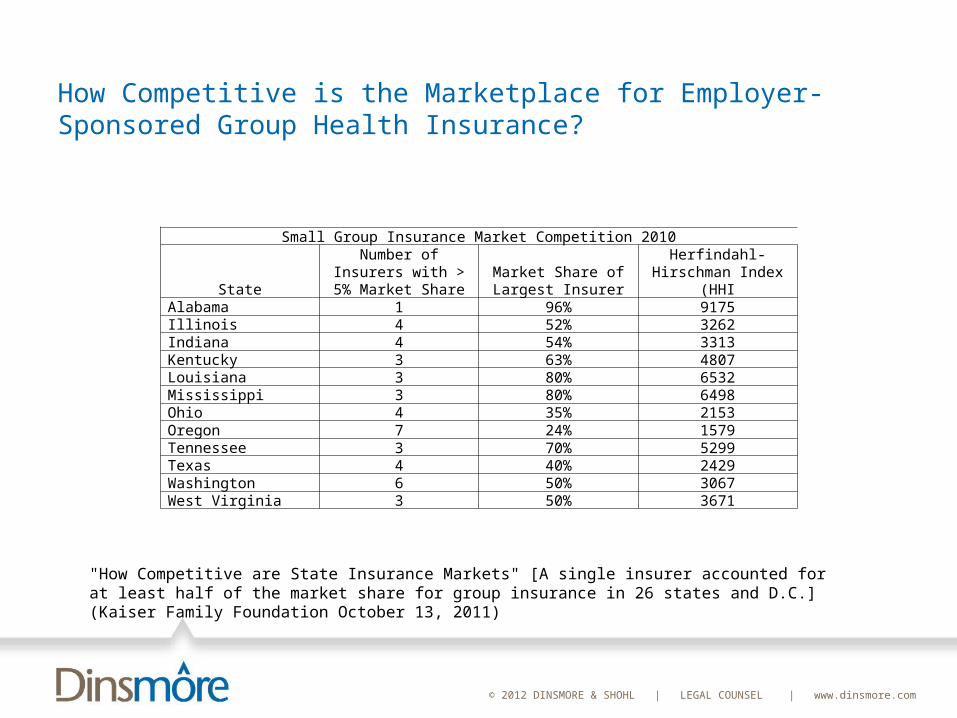

How Competitive is the Marketplace for Employer-Sponsored Group Health Insurance?

"How Competitive are State Insurance Markets" [A single insurer accounted for at least half of the market share for group insurance in 26 states and D.C.] (Kaiser Family Foundation October 13, 2011)

Background:

Herfindahl-Hirschman Index (“HHI”) values range from 0 to 10,000, with a value closer to zero indicating a more competitive market and values closer to 10,000 indicating a less competitive market. As a rule of thumb, an HHI index below 1,000 indicates a highly competitive market, and a value between 1,000 and 1,500 indicates an unconcentrated market. Values between 1,500 and 2,500 suggest moderate concentration, and markets with results above 2,500 are generally considered highly concentrated.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

How Competitive is the Marketplace for Employer-Sponsored Group Health Insurance?

"How Competitive are State Insurance Markets" [A single insurer accounted for at least half of the market share for group insurance in 26 states and D.C.] (Kaiser Family Foundation October 13, 2011)

Small Group Insurance Market Competition 2010

State

Number of Insurers with > 5% Market

ShareMarket Share of Largest

InsurerHerfindahl-Hirschman

Index (HHIAlabama 1 96% 9175Illinois 4 52% 3262Indiana 4 54% 3313Kentucky 3 63% 4807Louisiana 3 80% 6532Mississippi 3 80% 6498Ohio 4 35% 2153Oregon 7 24% 1579Tennessee 3 70% 5299Texas 4 40% 2429Washington 6 50% 3067West Virginia 3 50% 3671

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

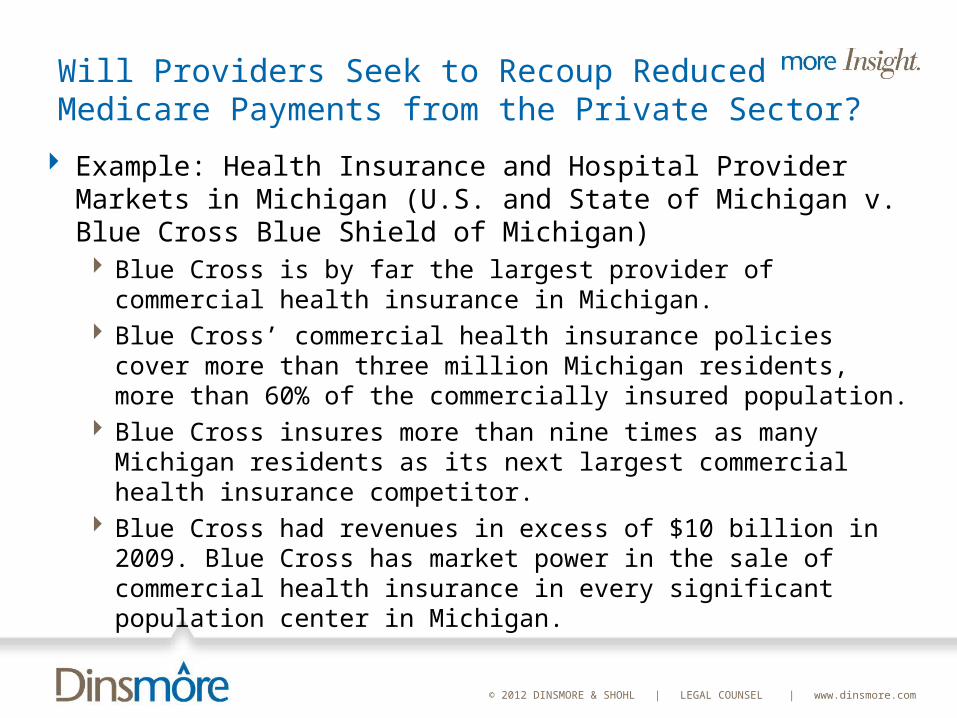

Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan) Blue Cross is by far the largest provider of commercial health

insurance in Michigan. Blue Cross’ commercial health insurance policies cover more than

three million Michigan residents, more than 60% of the commercially insured population.

Blue Cross insures more than nine times as many Michigan residents as its next largest commercial health insurance competitor.

Blue Cross had revenues in excess of $10 billion in 2009. Blue Cross has market power in the sale of commercial health insurance in every significant population center in Michigan.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

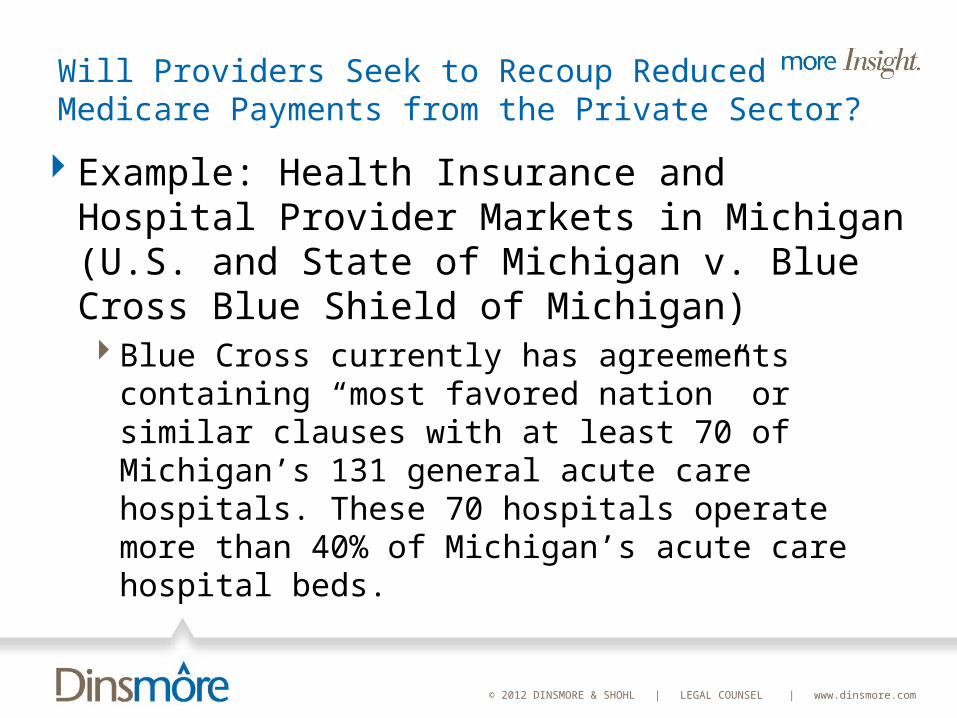

Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan)Blue Cross currently has agreements containing “most

favored nation” or similar clauses with at least 70 of Michigan’s 131 general acute care hospitals. These 70 hospitals operate more than 40% of Michigan’s acute care hospital beds.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

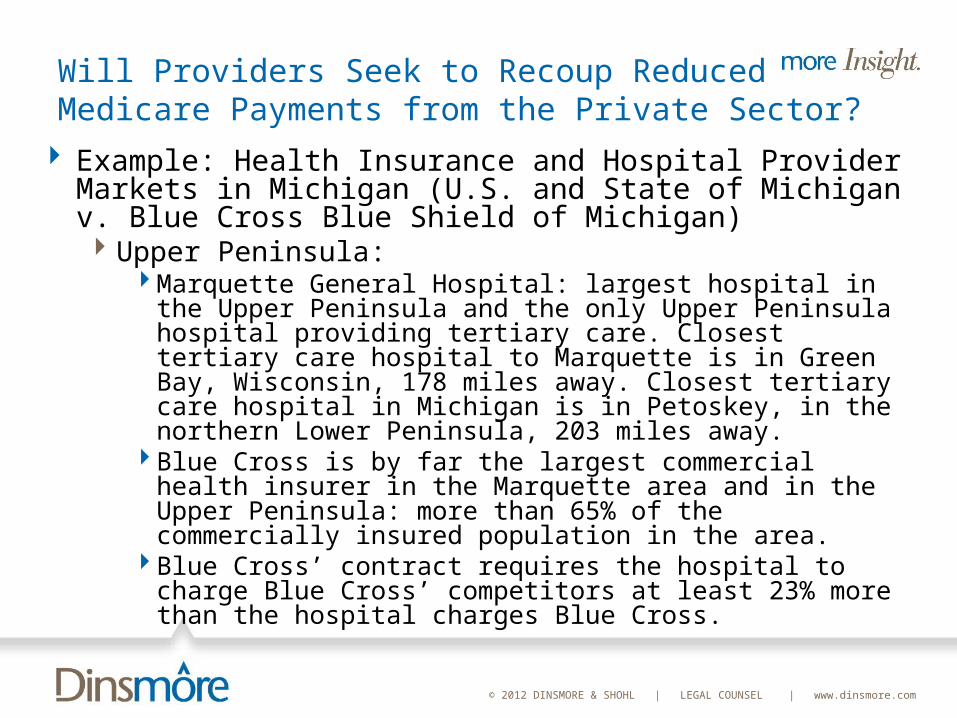

Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan) Upper Peninsula:

Marquette General Hospital: largest hospital in the Upper Peninsula and the only Upper Peninsula hospital providing tertiary care. Closest tertiary care hospital to Marquette is in Green Bay, Wisconsin, 178 miles away. Closest tertiary care hospital in Michigan is in Petoskey, in the northern Lower Peninsula, 203 miles away.

Blue Cross is by far the largest commercial health insurer in the Marquette area and in the Upper Peninsula: more than 65% of the commercially insured population in the area.

Blue Cross’ contract requires the hospital to charge Blue Cross’ competitors at least 23% more than the hospital charges Blue Cross.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

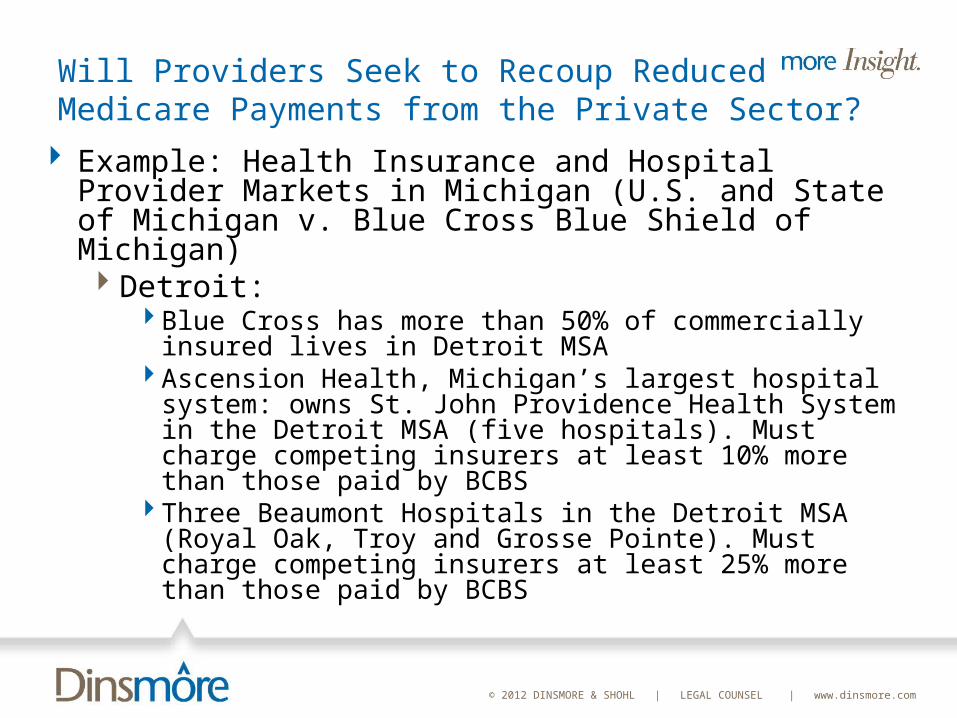

Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan) Detroit:

Blue Cross has more than 50% of commercially insured lives in Detroit MSA

Ascension Health, Michigan’s largest hospital system: owns St. John Providence Health System in the Detroit MSA (five hospitals). Must charge competing insurers at least 10% more than those paid by BCBS

Three Beaumont Hospitals in the Detroit MSA (Royal Oak, Troy and Grosse Pointe). Must charge competing insurers at least 25% more than those paid by BCBS

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan)Result:

Major hospitals receive super-competitive reimbursements Insurer locks out competing insurersEmployers pay higher rates – and have no viable alternative but

to pay the higher rates.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

What Is the Track Record? What Does it Portend for the Future? Will Providers Seek to Recoup Reduced Medicare Payments from the Private Sector?

Example: Health Insurance and Hospital Provider Markets in Michigan (U.S. and State of Michigan v. Blue Cross Blue Shield of Michigan)Result:

Major hospitals receive super-competitive reimbursements Insurer locks out competing insurersEmployers pay higher rates – and have no viable alternative but

to pay the higher rates.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Accountable Care Organizations

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS

March 31, 2011:CMS issues Proposed Rule on ACOs (published in the

Federal Register on April 7, 2011).FTC and DOJ issue “Proposed Statement of Antitrust

Enforcement Policy Regarding Accountable Care Organizations”

IRS issues Notice 2011-20--solicitation of comments regarding need for additional guidance for tax-exempt organizations participating in an accountable care organization and a proposed safe harbor.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

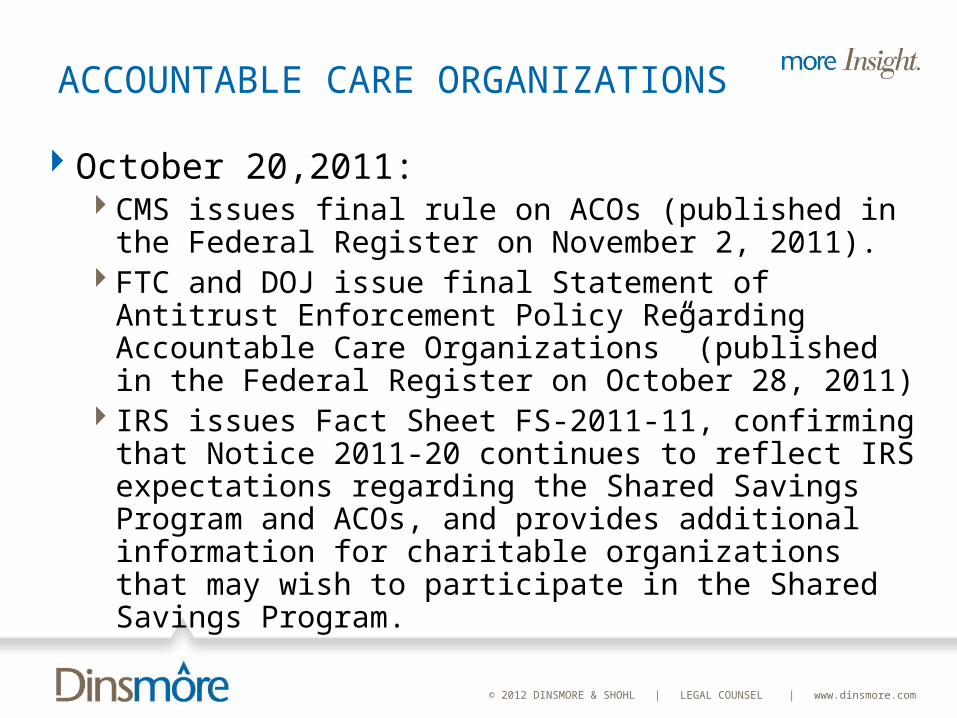

ACCOUNTABLE CARE ORGANIZATIONS

October 20,2011:CMS issues final rule on ACOs (published in the Federal

Register on November 2, 2011).FTC and DOJ issue final Statement of Antitrust

Enforcement Policy Regarding Accountable Care Organizations” (published in the Federal Register on October 28, 2011)

IRS issues Fact Sheet FS-2011-11, confirming that Notice 2011-20 continues to reflect IRS expectations regarding the Shared Savings Program and ACOs, and provides additional information for charitable organizations that may wish to participate in the Shared Savings Program.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS

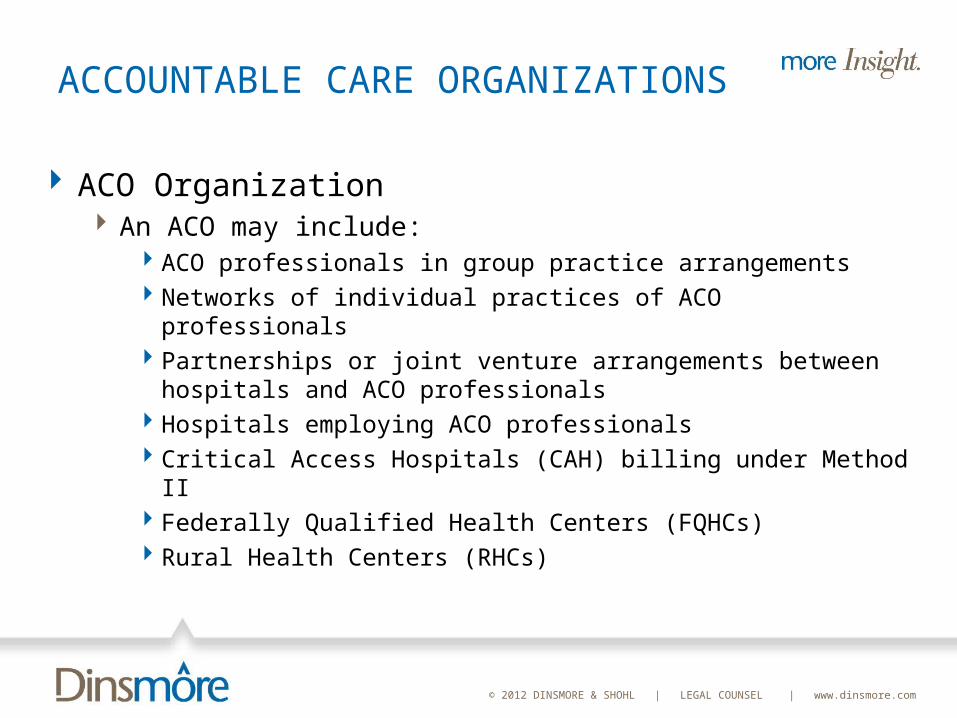

ACO Organization An ACO may include:

ACO professionals in group practice arrangements Networks of individual practices of ACO professionals Partnerships or joint venture arrangements between hospitals and ACO

professionals Hospitals employing ACO professionals Critical Access Hospitals (CAH) billing under Method II Federally Qualified Health Centers (FQHCs) Rural Health Centers (RHCs)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS

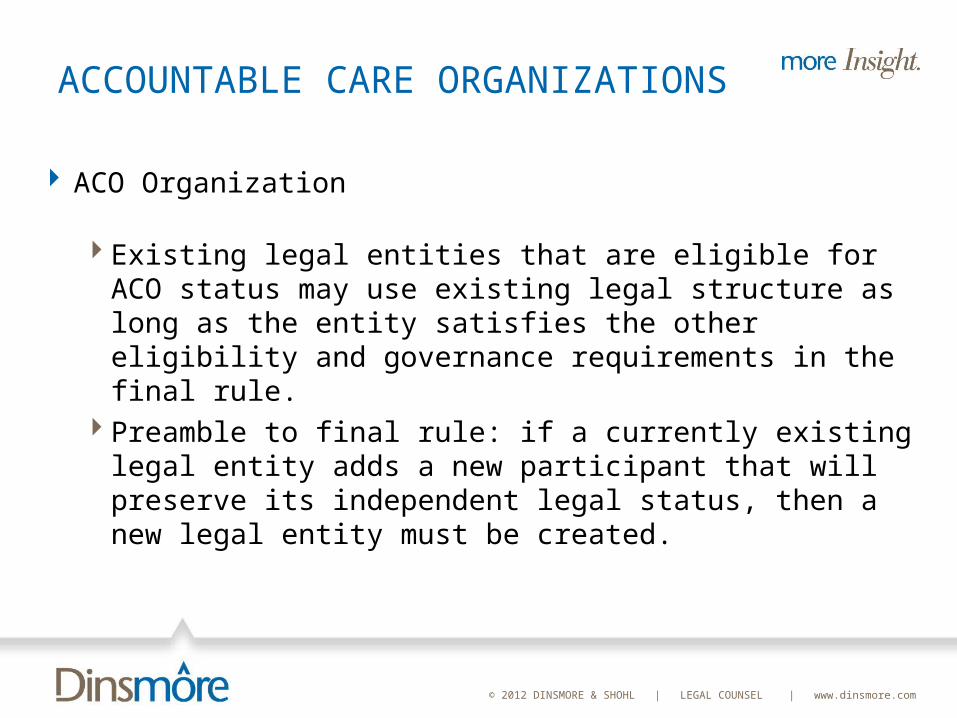

ACO Organization

Existing legal entities that are eligible for ACO status may use existing legal structure as long as the entity satisfies the other eligibility and governance requirements in the final rule.

Preamble to final rule: if a currently existing legal entity adds a new participant that will preserve its independent legal status, then a new legal entity must be created.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS

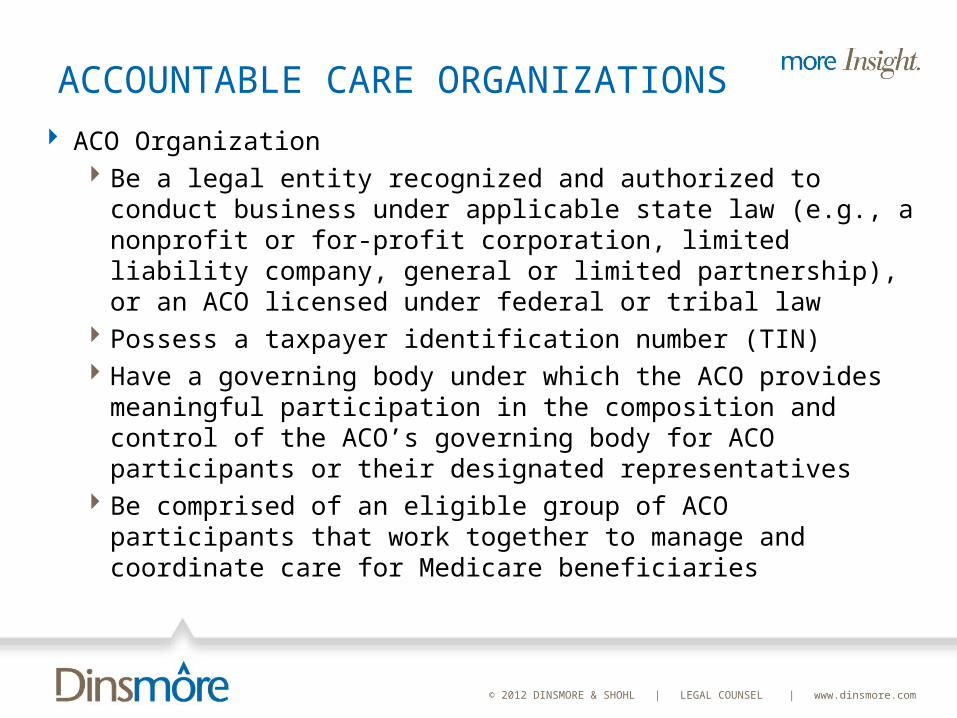

ACO Organization Be a legal entity recognized and authorized to conduct

business under applicable state law (e.g., a nonprofit or for-profit corporation, limited liability company, general or limited partnership), or an ACO licensed under federal or tribal law

Possess a taxpayer identification number (TIN) Have a governing body under which the ACO provides

meaningful participation in the composition and control of the ACO’s governing body for ACO participants or their designated representatives

Be comprised of an eligible group of ACO participants that work together to manage and coordinate care for Medicare beneficiaries

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

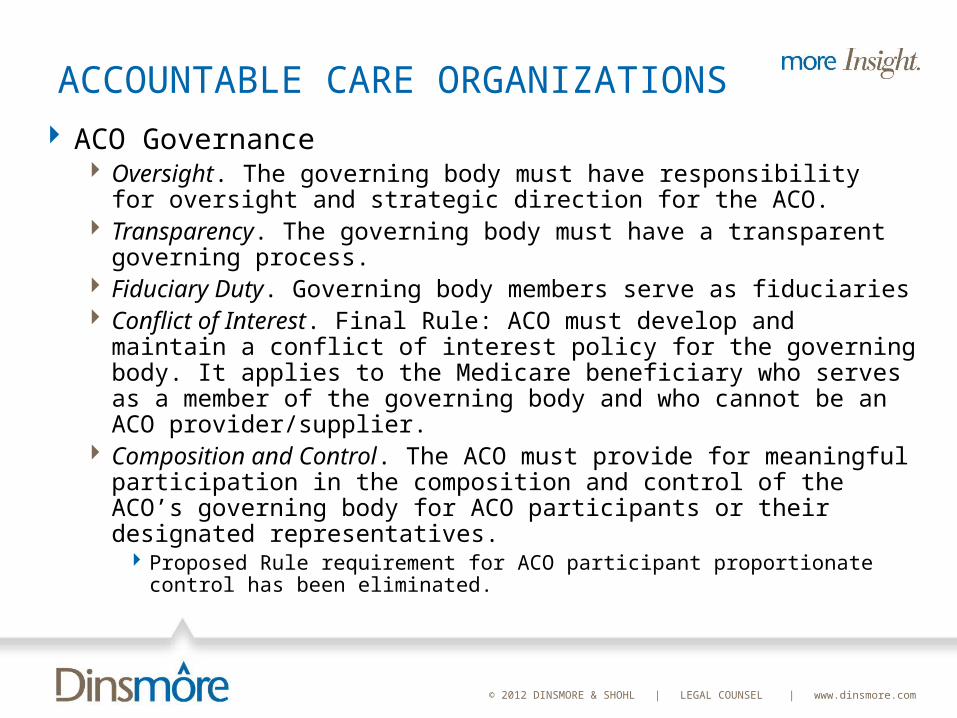

ACCOUNTABLE CARE ORGANIZATIONS

ACO Governance Oversight. The governing body must have responsibility for

oversight and strategic direction for the ACO. Transparency. The governing body must have a transparent

governing process. Fiduciary Duty. Governing body members serve as fiduciaries Conflict of Interest. Final Rule: ACO must develop and maintain a

conflict of interest policy for the governing body. It applies to the Medicare beneficiary who serves as a member of the governing body and who cannot be an ACO provider/supplier.

Composition and Control. The ACO must provide for meaningful participation in the composition and control of the ACO’s governing body for ACO participants or their designated representatives.

Proposed Rule requirement for ACO participant proportionate control has been eliminated.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: SHARED SAVINGS REQUIREMENTS

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

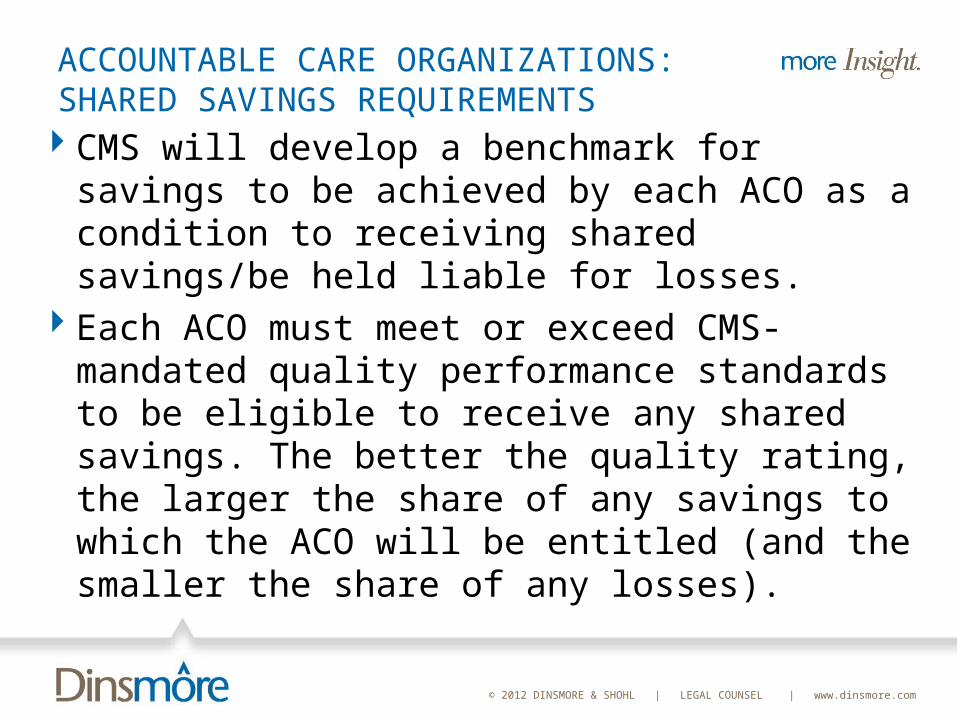

ACCOUNTABLE CARE ORGANIZATIONS:SHARED SAVINGS REQUIREMENTS

CMS will develop a benchmark for savings to be achieved by each ACO as a condition to receiving shared savings/be held liable for losses.

Each ACO must meet or exceed CMS-mandated quality performance standards to be eligible to receive any shared savings. The better the quality rating, the larger the share of any savings to which the ACO will be entitled (and the smaller the share of any losses).

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

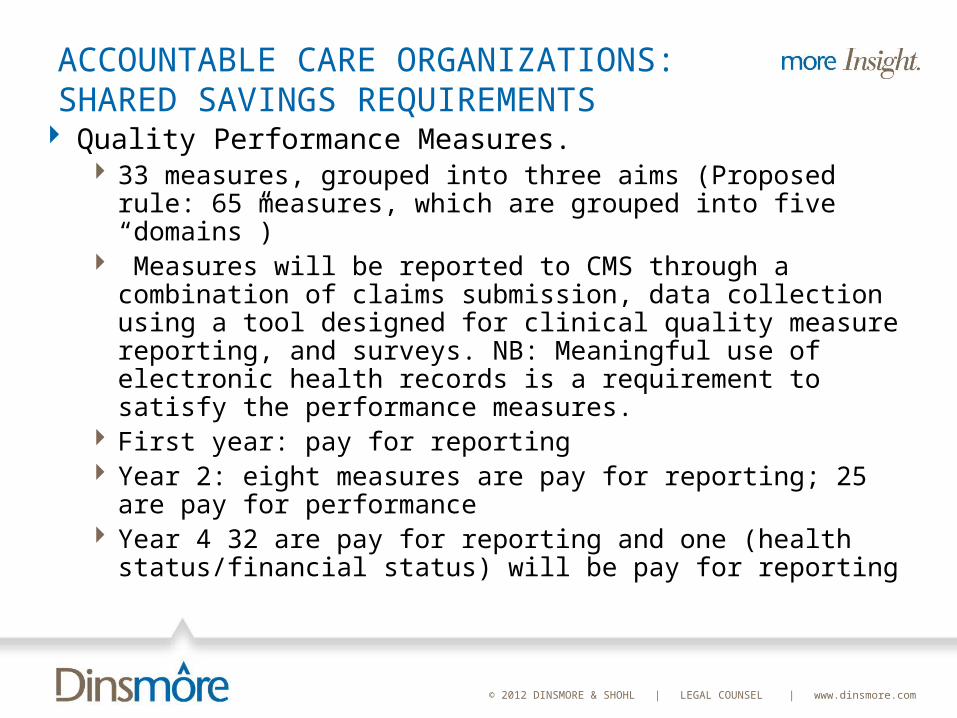

ACCOUNTABLE CARE ORGANIZATIONS:SHARED SAVINGS REQUIREMENTS

Quality Performance Measures. 33 measures, grouped into three aims (Proposed rule: 65

measures, which are grouped into five “domains”) Measures will be reported to CMS through a combination of claims

submission, data collection using a tool designed for clinical quality measure reporting, and surveys. NB: Meaningful use of electronic health records is a requirement to satisfy the performance measures.

First year: pay for reporting Year 2: eight measures are pay for reporting; 25 are pay for

performance Year 4 32 are pay for reporting and one (health status/financial

status) will be pay for reporting

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

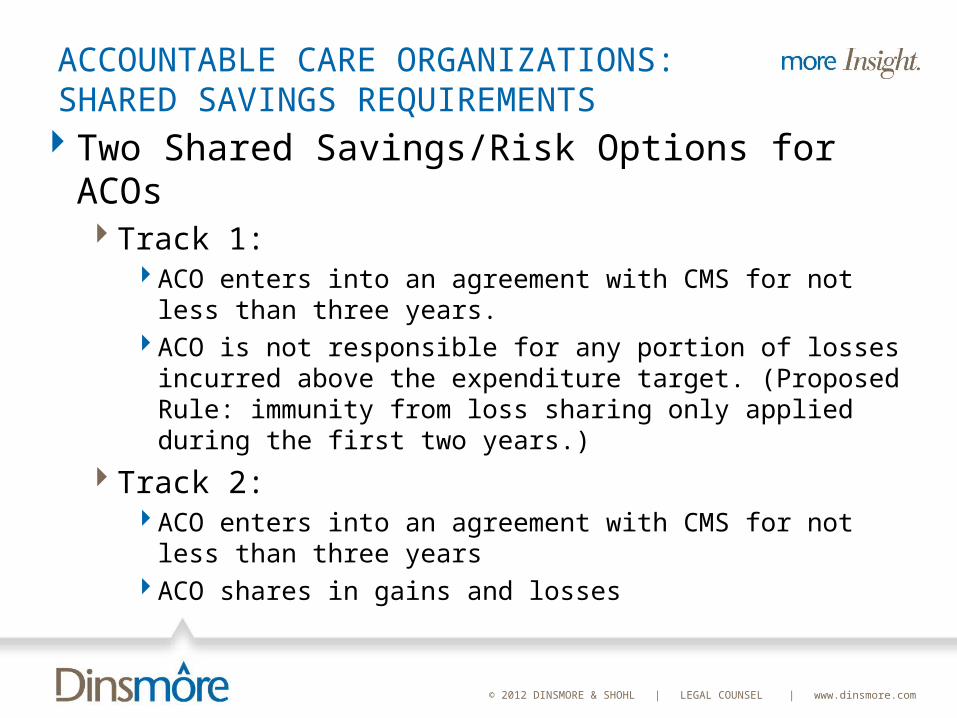

ACCOUNTABLE CARE ORGANIZATIONS:SHARED SAVINGS REQUIREMENTS

Two Shared Savings/Risk Options for ACOsTrack 1:

ACO enters into an agreement with CMS for not less than three years.

ACO is not responsible for any portion of losses incurred above the expenditure target. (Proposed Rule: immunity from loss sharing only applied during the first two years.)

Track 2:ACO enters into an agreement with CMS for not less than three

yearsACO shares in gains and losses

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

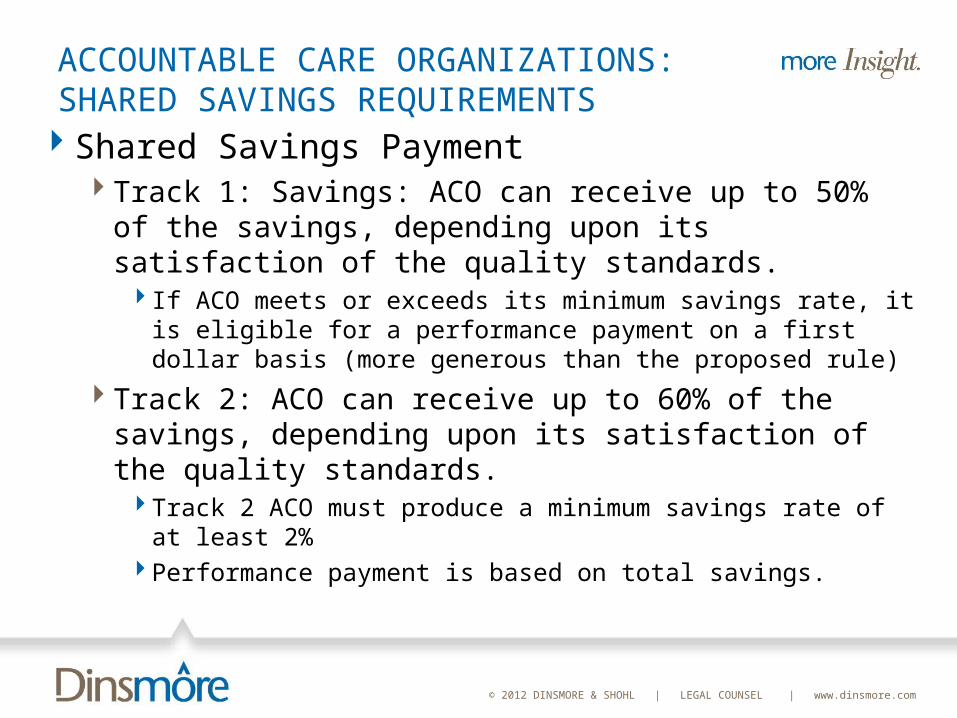

ACCOUNTABLE CARE ORGANIZATIONS:SHARED SAVINGS REQUIREMENTS

Shared Savings PaymentTrack 1: Savings: ACO can receive up to 50% of the

savings, depending upon its satisfaction of the quality standards. If ACO meets or exceeds its minimum savings rate, it is eligible

for a performance payment on a first dollar basis (more generous than the proposed rule)

Track 2: ACO can receive up to 60% of the savings, depending upon its satisfaction of the quality standards.Track 2 ACO must produce a minimum savings rate of at least

2%Performance payment is based on total savings.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

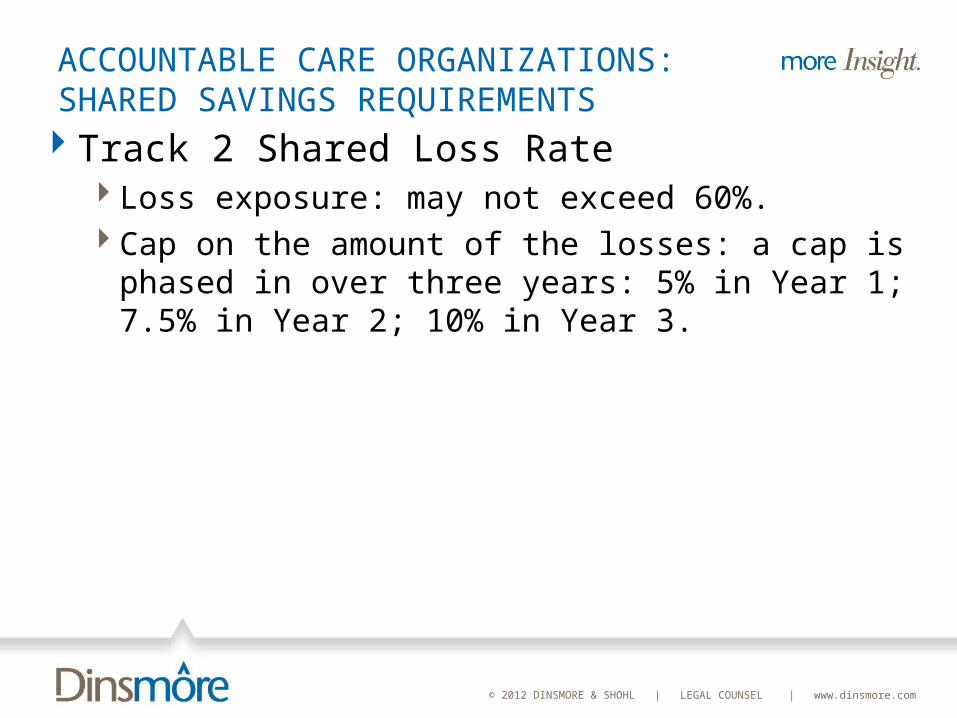

ACCOUNTABLE CARE ORGANIZATIONS:SHARED SAVINGS REQUIREMENTS

Track 2 Shared Loss RateLoss exposure: may not exceed 60%.Cap on the amount of the losses: a cap is phased in

over three years: 5% in Year 1; 7.5% in Year 2; 10% in Year 3.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

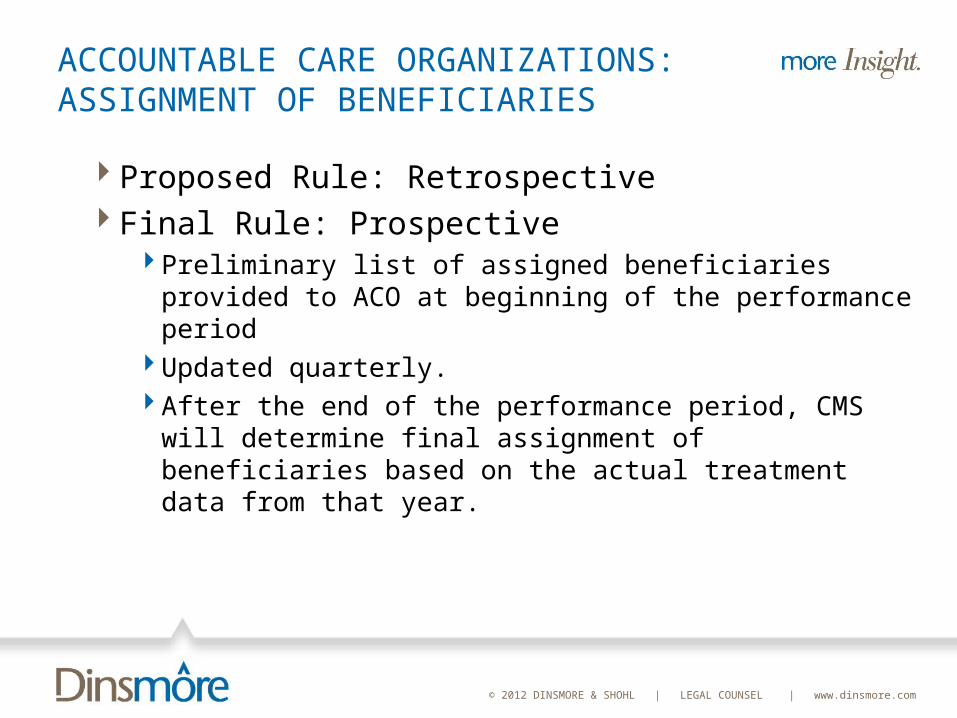

ACCOUNTABLE CARE ORGANIZATIONS:ASSIGNMENT OF BENEFICIARIES

Proposed Rule: RetrospectiveFinal Rule: Prospective

Preliminary list of assigned beneficiaries provided to ACO at beginning of the performance period

Updated quarterly.After the end of the performance period, CMS will determine

final assignment of beneficiaries based on the actual treatment data from that year.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: IRS RULES FOR TAX-EXEMPT

PROVIDERS

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

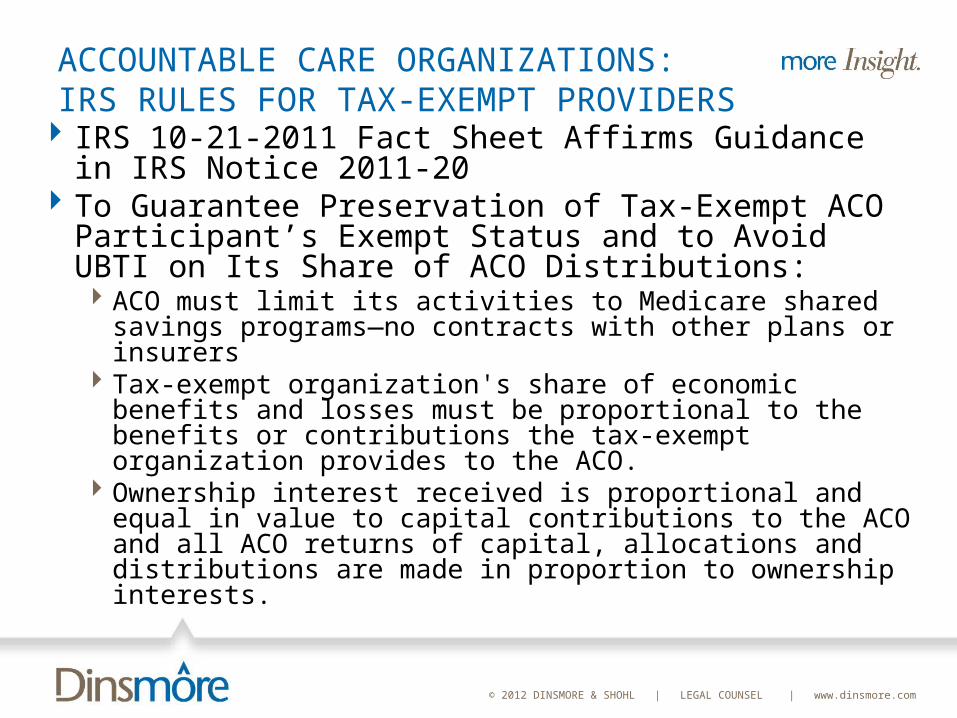

ACCOUNTABLE CARE ORGANIZATIONS: IRS RULES FOR TAX-EXEMPT PROVIDERS

IRS 10-21-2011 Fact Sheet Affirms Guidance in IRS Notice 2011-20

To Guarantee Preservation of Tax-Exempt ACO Participant’s Exempt Status and to Avoid UBTI on Its Share of ACO Distributions: ACO must limit its activities to Medicare shared savings

programs—no contracts with other plans or insurers Tax-exempt organization's share of economic benefits and

losses must be proportional to the benefits or contributions the tax-exempt organization provides to the ACO.

Ownership interest received is proportional and equal in value to capital contributions to the ACO and all ACO returns of capital, allocations and distributions are made in proportion to ownership interests.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

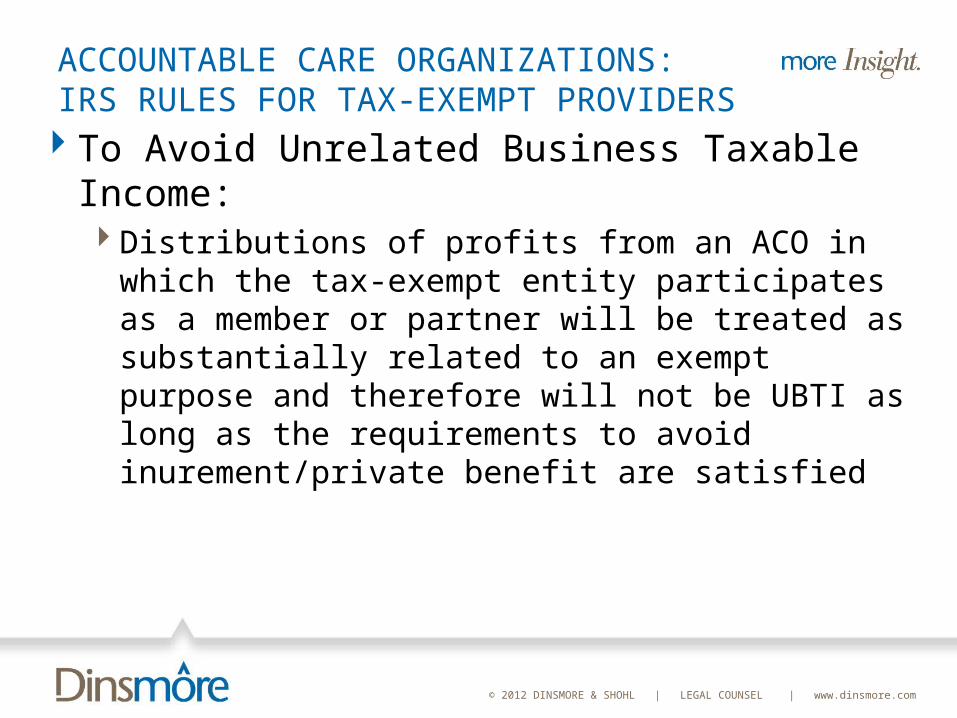

ACCOUNTABLE CARE ORGANIZATIONS: IRS RULES FOR TAX-EXEMPT PROVIDERS

To Avoid Unrelated Business Taxable Income:Distributions of profits from an ACO in which the tax-

exempt entity participates as a member or partner will be treated as substantially related to an exempt purpose and therefore will not be UBTI as long as the requirements to avoid inurement/private benefit are satisfied

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ GUIDELINES

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

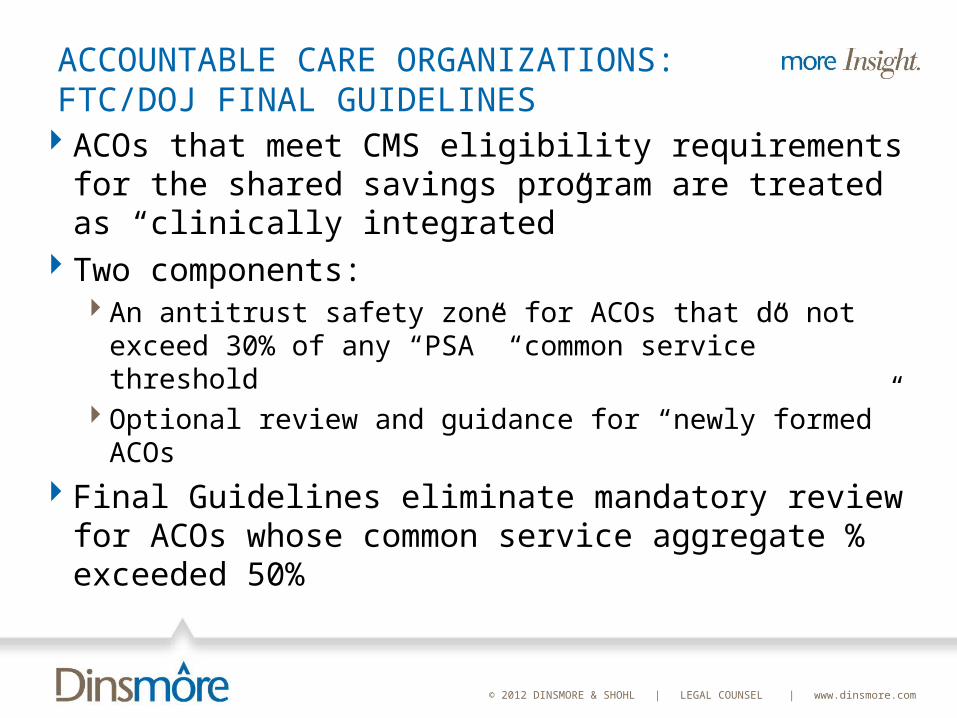

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ FINAL GUIDELINES

ACOs that meet CMS eligibility requirements for the shared savings program are treated as “clinically integrated”

Two components:An antitrust safety zone for ACOs that do not exceed

30% of any “PSA” “common service” thresholdOptional review and guidance for “newly formed” ACOs

Final Guidelines eliminate mandatory review for ACOs whose common service aggregate % exceeded 50%

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

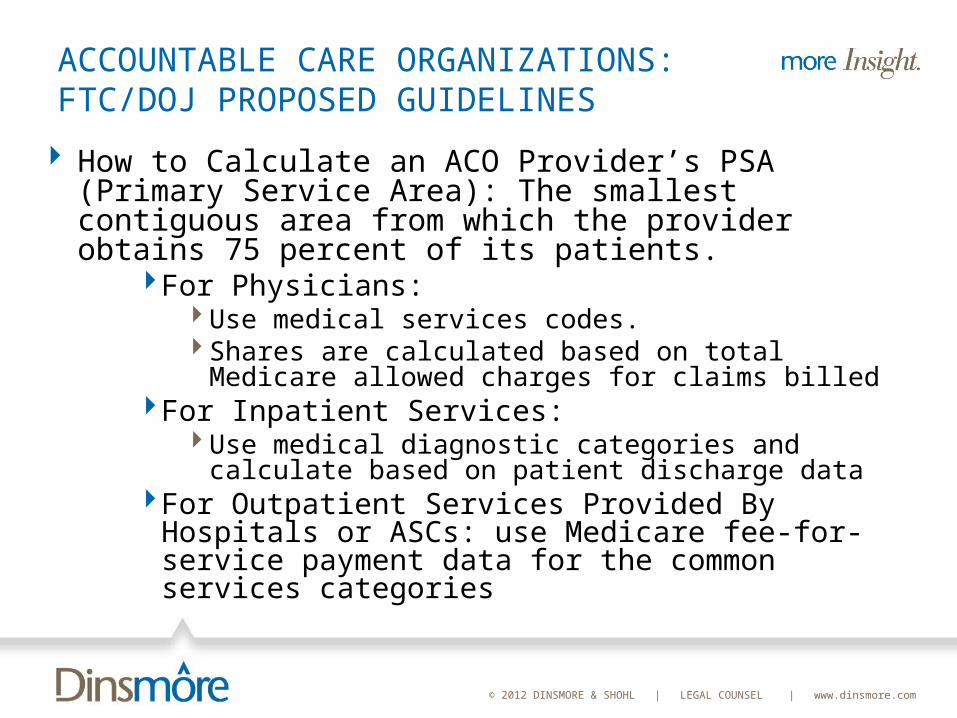

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ PROPOSED GUIDELINES

How to Calculate an ACO Provider’s PSA (Primary Service Area): The smallest contiguous area from which the provider obtains 75 percent of its patients.

For Physicians:Use medical services codes.Shares are calculated based on total Medicare allowed

charges for claims billedFor Inpatient Services:

Use medical diagnostic categories and calculate based on patient discharge data

For Outpatient Services Provided By Hospitals or ASCs: use Medicare fee-for-service payment data for the common services categories

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

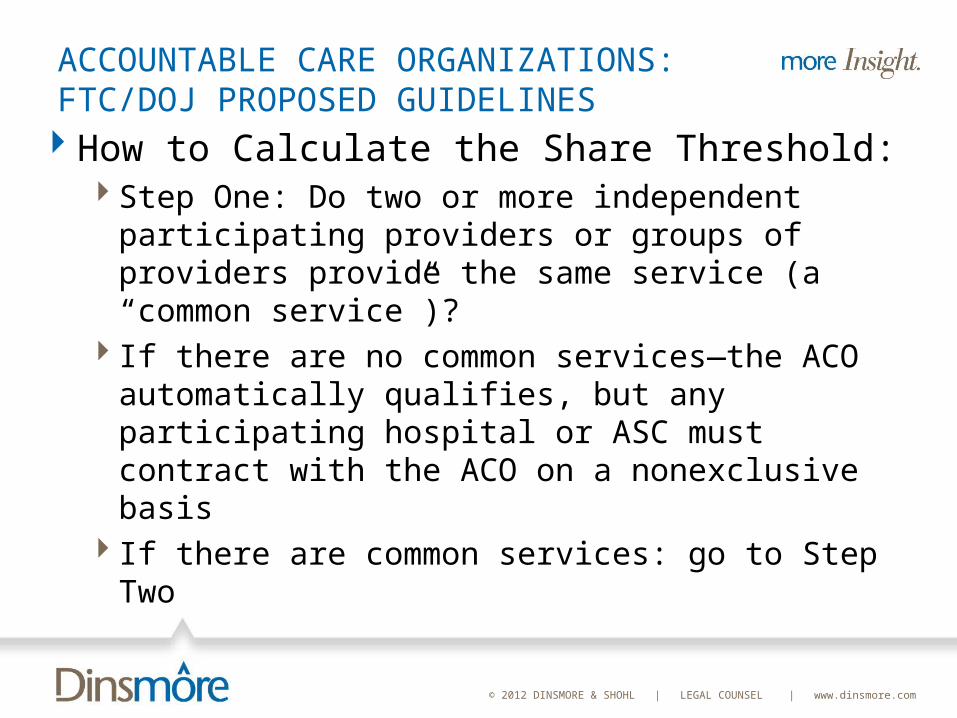

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ PROPOSED GUIDELINES

How to Calculate the Share Threshold:Step One: Do two or more independent participating

providers or groups of providers provide the same service (a “common service”)?

If there are no common services—the ACO automatically qualifies, but any participating hospital or ASC must contract with the ACO on a nonexclusive basis

If there are common services: go to Step Two

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

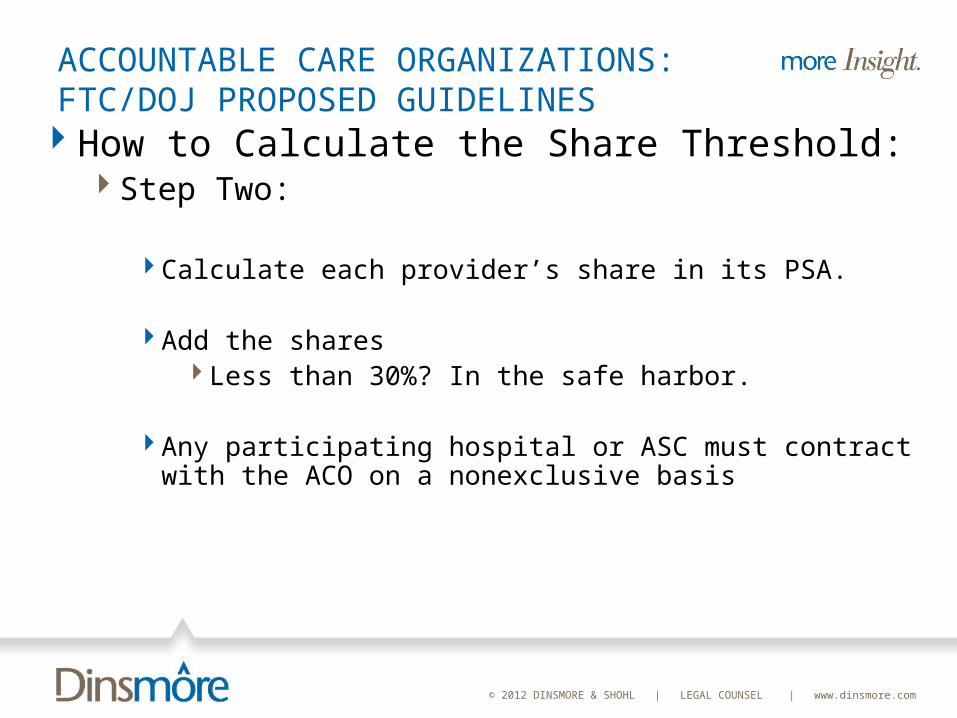

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ PROPOSED GUIDELINES

How to Calculate the Share Threshold:Step Two:

Calculate each provider’s share in its PSA.

Add the sharesLess than 30%? In the safe harbor.

Any participating hospital or ASC must contract with the ACO on a nonexclusive basis

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

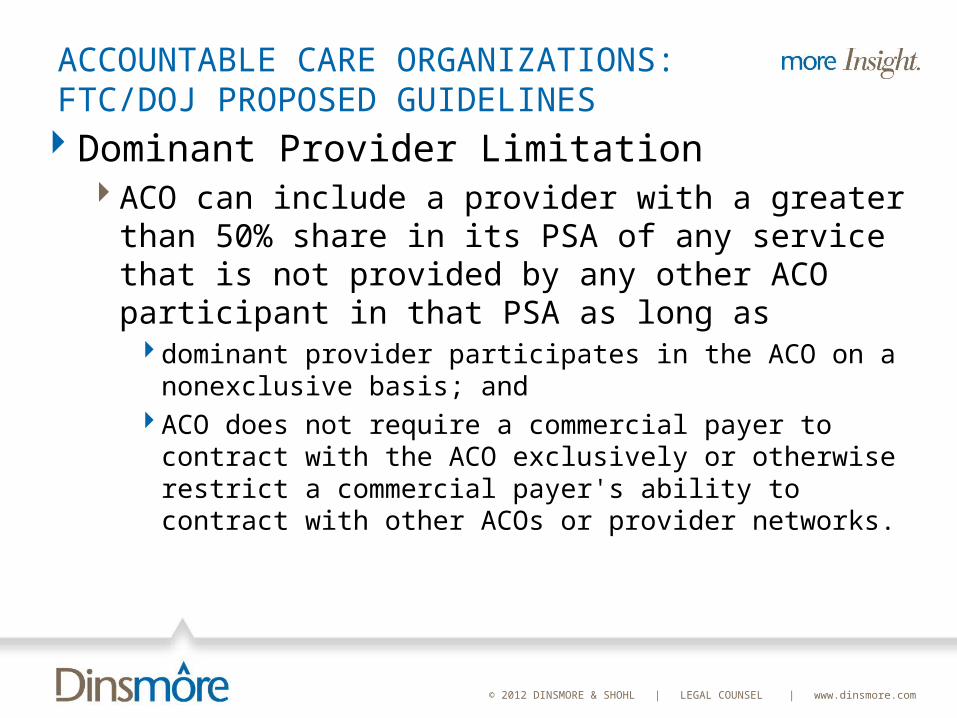

ACCOUNTABLE CARE ORGANIZATIONS: FTC/DOJ PROPOSED GUIDELINES

Dominant Provider LimitationACO can include a provider with a greater than 50%

share in its PSA of any service that is not provided by any other ACO participant in that PSA as long asdominant provider participates in the ACO on a nonexclusive

basis; andACO does not require a commercial payer to contract with the

ACO exclusively or otherwise restrict a commercial payer's ability to contract with other ACOs or provider networks.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: HOW MUCH WILL IT COST TO DEVELOP

AN ACO?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

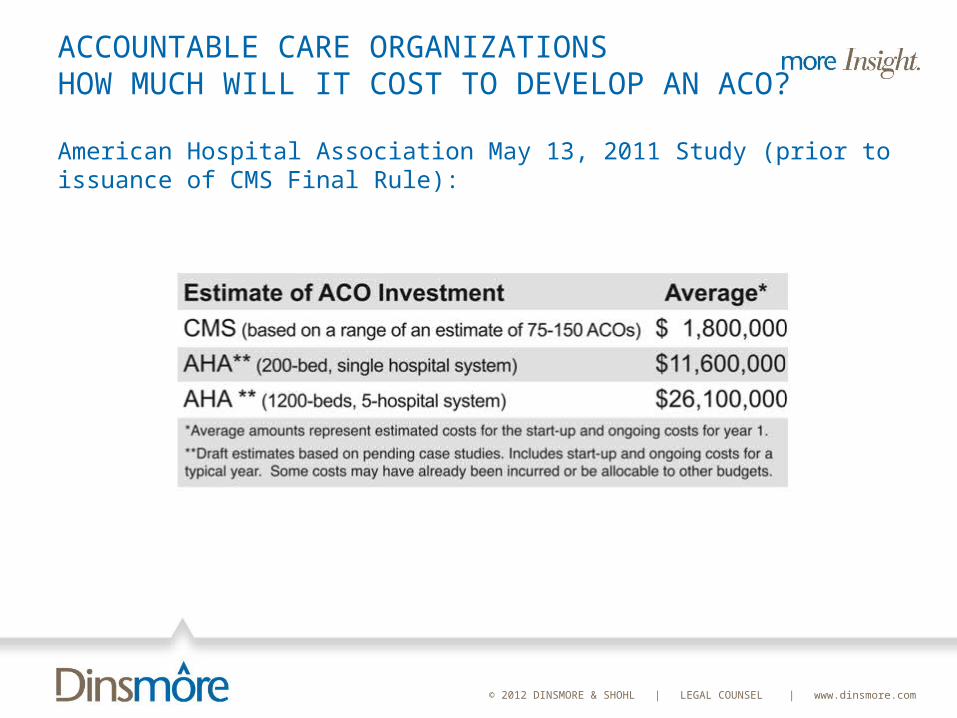

ACCOUNTABLE CARE ORGANIZATIONS HOW MUCH WILL IT COST TO DEVELOP AN ACO?

American Hospital Association May 13, 2011 Study (prior to issuance of CMS Final Rule):

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS HOW MUCH WILL IT COST TO DEVELOP AN ACO?

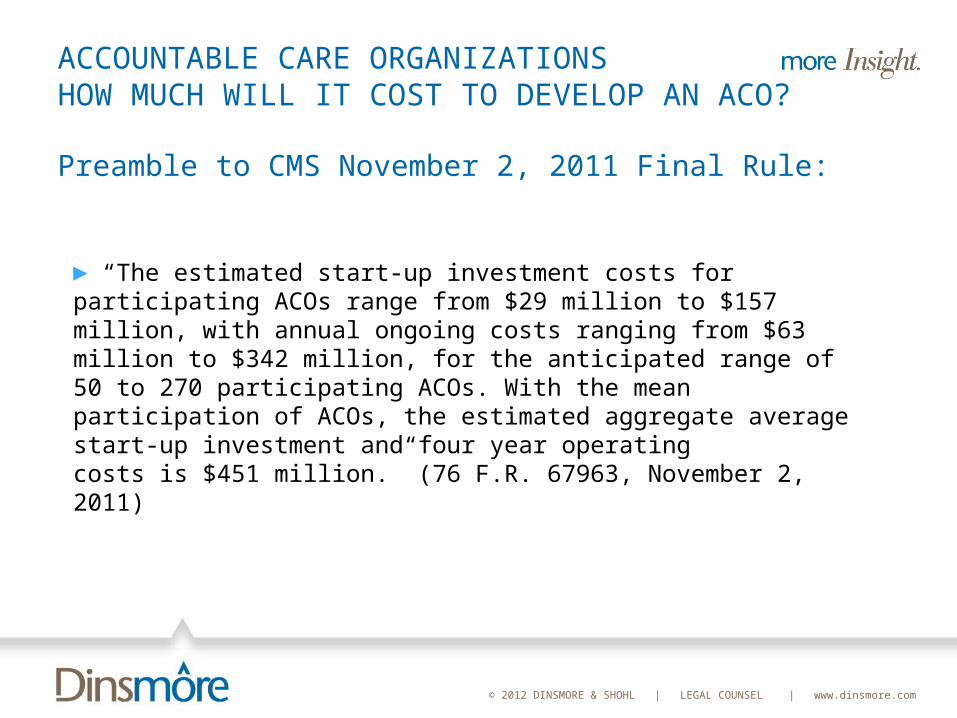

Preamble to CMS November 2, 2011 Final Rule:

► “The estimated start-up investment costs for participating ACOs range from $29 million to $157 million, with annual ongoing costs ranging from $63 million to $342 million, for the anticipated range of 50 to 270 participating ACOs. With the mean participation of ACOs, the estimated aggregate average start-up investment and four year operatingcosts is $451 million.” (76 F.R. 67963, November 2, 2011)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: ARE THEY BEING FORMED? WILL THEY IMPROVE QUALITY AND SAVE MONEY?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: ARE THEY BEING FORMED?

“At least eight private health insurance plans have entered into ACO contracts with providers using a shared risk payment model, making providers eligible for both bonuses and financial penalties.

“Many more (27, by one count) have entered into shared savings contracts, which make providers eligible for bonuses, but do not put them at financial risk if they exceed spending targets.

“The private ACO contracts that have been identified so far use shared savings, shared risk, or partial capitation; none have moved all the way to full capitation yet.

“Accountable Care Organizations in Medicare and the Private Sector: A Status Update,” Urban Institute, November 2011 (http://www.urban.org/UploadedPDF/412438-Accountable-Care-Organizations-in-Medicare-and-the-Private-Sector.pdf)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: ARE THEY BEING FORMED?

“The private ACO contracts using shared risk include several Blue Cross Blue Shield plans in different states (e.g., Illinois, Massachusetts, New Jersey, North Carolina), Aetna, and Anthem/WellPoint.

“Several private ACO contracts are offering providers 50 percent of the savings they generate (the same level of savings offered in the bonus only option of the MSSP), and intend to transition their private ACO contracts to some form of capitation in coming years…”

“Accountable Care Organizations in Medicare and the Private Sector: A Status Update,” Urban Institute, November 2011 (http://www.urban.org/UploadedPDF/412438-Accountable-Care-Organizations-in-Medicare-and-the-Private-Sector.pdf)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: WILL THEY SAVE MONEY?

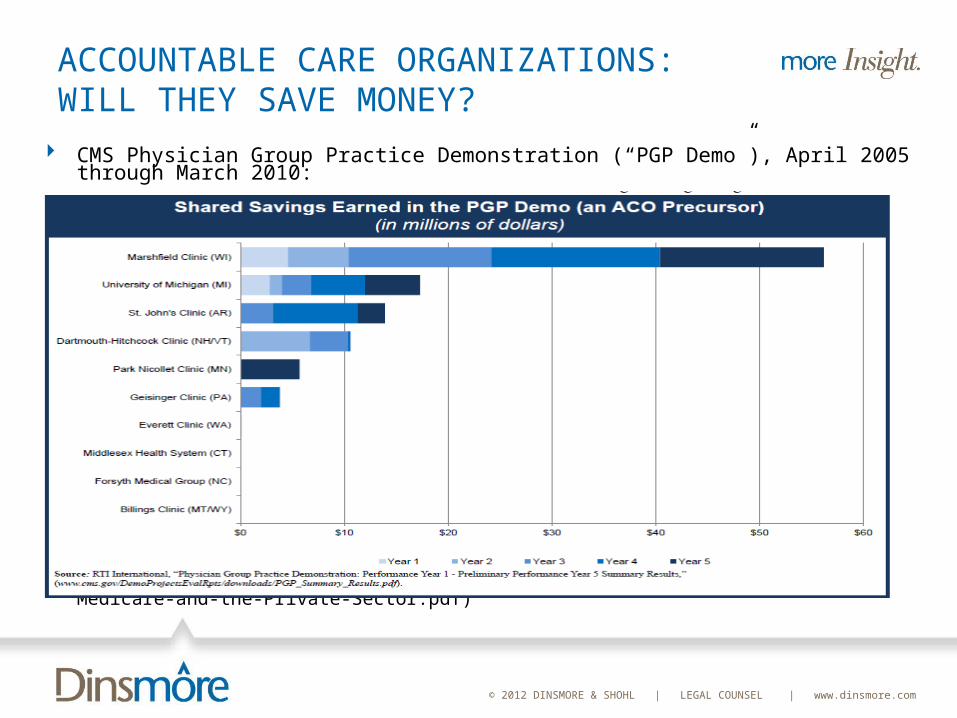

CMS Physician Group Practice Demonstration (“PGP Demo”), April 2005 through March 2010:

“Accountable Care Organizations in Medicare and the Private Sector: A Status Update,” Urban Institute, November 2011 (http://www.urban.org/UploadedPDF/412438-Accountable-Care-Organizations-in-Medicare-and-the-Private-Sector.pdf)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: WILL THEY SAVE MONEY?

The PGP Demo “suggests ACOs will be able to improve the quality of care they deliver (at least as measured by process-oriented clinical quality measures), but will have a harder time generating savings.”

Savings was small: Annual shared savings per participating group averaged $5.4 million

(for those groups that earned any shared savings), with a range of a few hundred thousand dollars to $16 million

Only two participants lowered spending sufficiently to earn bonuses in all five years of the demo

Three of the ten participants earned no bonus in any year

“Accountable Care Organizations in Medicare and the Private Sector: A Status Update,” Urban Institute, November 2011 (http://www.urban.org/UploadedPDF/412438-Accountable-Care-Organizations-in-Medicare-and-the-Private-Sector.pdf)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

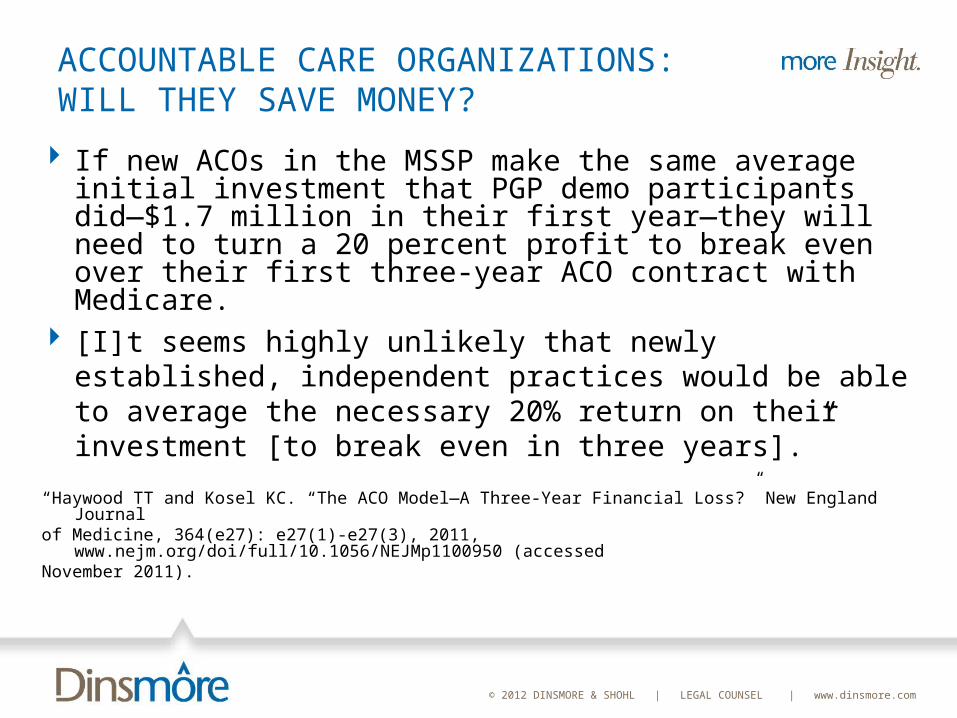

ACCOUNTABLE CARE ORGANIZATIONS: WILL THEY SAVE MONEY?

If new ACOs in the MSSP make the same average initial investment that PGP demo participants did—$1.7 million in their first year—they will need to turn a 20 percent profit to break even over their first three-year ACO contract with Medicare.

[I]t seems highly unlikely that newly established, independent practices would be able to average the necessary 20% return on their investment [to break even in three years].”

“Haywood TT and Kosel KC. “The ACO Model—A Three-Year Financial Loss?” New England Journalof Medicine, 364(e27): e27(1)-e27(3), 2011, www.nejm.org/doi/full/10.1056/NEJMp1100950 (accessedNovember 2011).

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

ACCOUNTABLE CARE ORGANIZATIONS: WILL THEY SAVE MONEY?

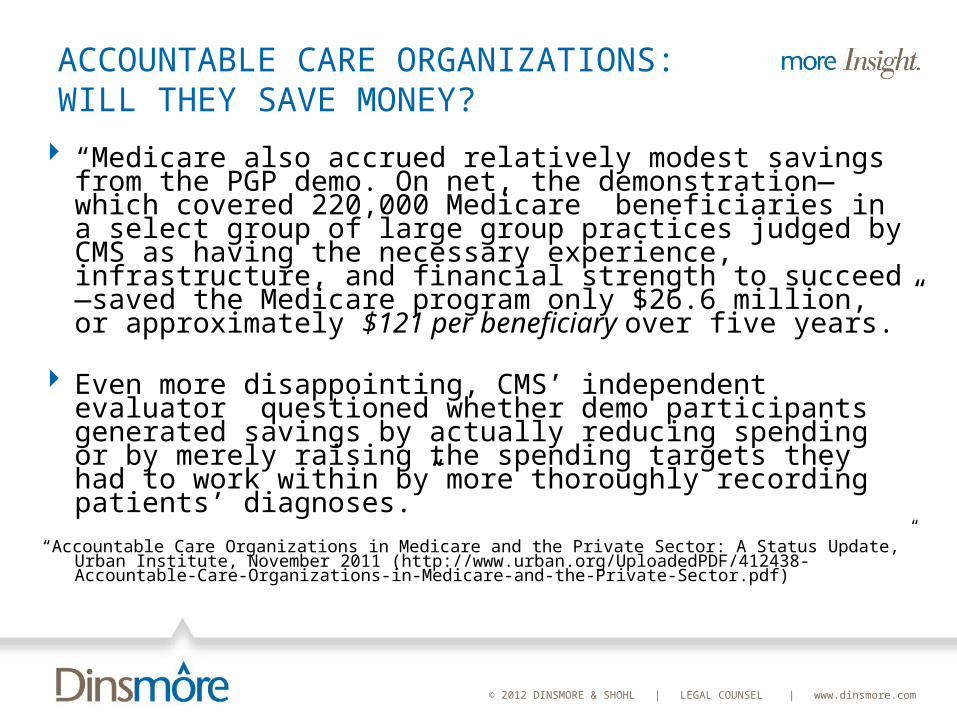

“Medicare also accrued relatively modest savings from the PGP demo. On net, the demonstration—which covered 220,000 Medicare beneficiaries in a select group of large group practices judged by CMS as having the necessary experience, infrastructure, and financial strength to succeed —saved the Medicare program only $26.6 million, or approximately $121 per beneficiary over five years.”

Even more disappointing, CMS’ independent evaluator questioned whether demo participants generated savings by actually reducing spending or by merely raising the spending targets they had to work within by more thoroughly recording patients’ diagnoses.”

“Accountable Care Organizations in Medicare and the Private Sector: A Status Update,” Urban Institute, November 2011 (http://www.urban.org/UploadedPDF/412438-Accountable-Care-Organizations-in-Medicare-and-the-Private-Sector.pdf)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

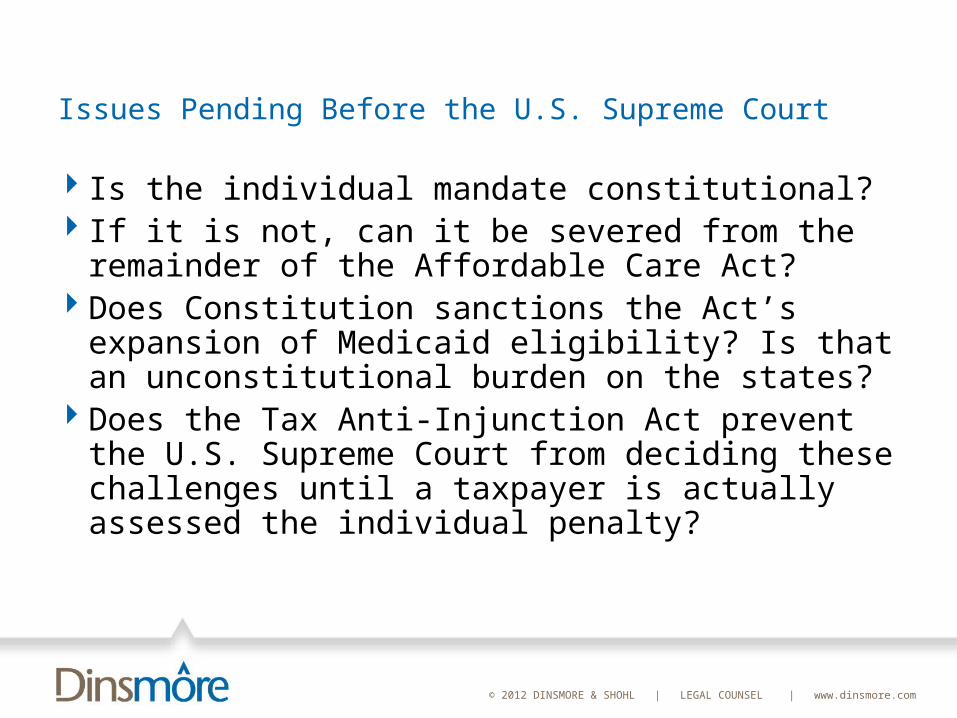

Is the individual mandate constitutional? If it is not, can it be severed from the remainder

of the Affordable Care Act? Does Constitution sanctions the Act’s expansion

of Medicaid eligibility? Is that an unconstitutional burden on the states?

Does the Tax Anti-Injunction Act prevent the U.S. Supreme Court from deciding these challenges until a taxpayer is actually assessed the individual penalty?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: The Individual Mandate

Commerce Clause (Article I, §8): “Congress shall have Power. . . to regulate Commerce with foreign Nations, and among the several States, and with Indian Tribes.”

Past cases: Congress can regulate any economic activity that Congress rationally concludes is in the stream of or substantially affects interstate commerce.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: The Individual Mandate

Plaintiffs: inactivity – decision not to purchase insurance – is not commerce.ACA attempts to force individuals to enter stream of

commerce If Congress can force people to buy insurance, why

not broccoli? Government:

Everyone uses health care at some time and, if not insured, shift costs to others. That constitutes interstate commerce and Congress can regulate it.

Ability to vote out the bums limits Congress’s power

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: The Individual Mandate

Plaintiffs: inactivity – decision not to purchase insurance – is not commerce.ACA attempts to force individuals to enter stream of

commerce If Congress can force people to buy insurance, why

not broccoli? Government:

Everyone uses health care at some time and, if not insured, shift costs to others. That constitutes interstate commerce and Congress can regulate it.

Ability to vote out the bums limits Congress’s power

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: The Individual Mandate

Necessary & Proper Clause: “Congress shall have Power …to make all Laws which shall be necessary and proper for carrying into Execution the foregoing PowersGovernment: the Necessary & Proper Clause also

sanctions Congress’s power to enact the individual mandate

Plaintiffs: No it doesn’t – it only authorizes acts that are necessary and proper to regulate interstate commerce.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: The Individual Mandate

Taxing PowerGovernment: solely for this purpose, the individual

mandate is a tax and therefore is sanctioned by the constitutional power to tax

Plaintiffs: No it isn’t: the individual mandate operates as a penalty, not as a tax.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Severability

11th Circuit: unconstitutional but severableGovernment: if the individual mandate is

unconstitutional, only two provisions of the Act are adversely affected: guaranteed issue and community rating

Plaintiffs: The entire Act depends upon the individual mandate, not just two provisions. If the individual mandate is unconstitutional, then the entire Act should be held unconstitutional.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Medicaid

BackgroundThe ACA expands Medicaid’s mandatory coverage:

A participating state must cover nearly all non-disabled adults under age 65 with household between 100% and133% of the FPL, beginning in January, 2014

Currently, some states do not cover adults without dependent children or cover parents only at income levels far below 100% of FPL

ACA: Federal government pays 100% of the states’ increased cost through 2016, decreasing to 90% by 2020

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Medicaid

BackgroundConstitution’s grant of spending power: Article 1, §8:

“Congress shall have Power . . . [to] provide for the common Defense and general Welfare of the United States.”

Prior cases: Supreme Court has permitted Congress’s attaching conditions to states’ receipt of federal funds – and done so generously

Four factor test (South Dakota v. Dole): condition must be – related to the general welfarestated unambiguouslyclearly related to the program’s purpose, andnot otherwise unconstitutional.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Medicaid

BackgroundSupreme Court never has invalidated a condition on

federal funding as unconstitutionally coercing the states and has never prescribed standards for how to determine unconstitutional level of coercion.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Medicaid

States’ ArgumentSupreme Court should demand more than the four

factors in Dole to limit the federal government’s power to use its Spending Clause authority to force states to spend their own funds

The Affordable Care Act effectively converts Medicaid from a voluntary program to a mandatory programStates depend on federal government support to fund a

program that states can no longer abandon for the electorate now regards Medicaid as a right, not a privilege

Look at the funds states lose if they reject Congress’s terms, not how much they must spend if they accept

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Medicaid

Federal Government’s ArgumentMedicaid expansion and its conditions for federal

support for overall Medicaid fit within the four factors in Dole

No court has ever held federal funding conditions rise to the level of being unconstitutionally coercive – and this is not the case for reaching that conclusion

Conditions ≡ core Congressional purpose – States should not be allowed to pick and choose among various conditions

The Act’s expansion + generous funding is not new or unique to the history of Medicaid

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Anti-Injunction Act

Anti-Injunction Act: “no suit for the purpose of restraining the assessment or collection of any tax shall be maintained in any court by any person.”

Anti-Injunction Act applies to taxes – but not to other sanctions, such as non-tax penalties

Issue: is the sanction for an individual’s failure to acquire minimum essential coverage a “tax” or a “penalty”?

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court: Anti-Injunction Act

States’ argument: AIA is not a jurisdictional bar: it’s a claims-processing rule

that applies only if a party raises it. Since none of the parties raises it, the AIA does not apply.

Even if it is a jurisdictional statute that doesn’t require a party’s raising its existence to apply –The sanction is a penalty, not a taxThe states are challenging the obligation to purchase minimum

essential coverage, not the sanction for failure to do soEven if the sanction is a tax, the states should not be barred

from challenging constitutionality, for they won’t pay and would therefore never be able to challenge the constitutionality of the mandate

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

How are the Justices likely to vote?Justices Kagan, Sotomayor, Breyer, and Ginsburg (all

appointed by Democratic Presidents): uphold constitutionality of the Act

That’s four votes. The proponents need to persuade only one more Justice

Justice Clarence Thomas: based on prior opinions, commenters believe Justice Thomas will almost certainly vote that the individual mandate is unconstitutional (and may also advocate that it cannot be severed from the balance of the Act)

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

Justice Scalia: likely to find the disputed provisions unconstitutionalSee Coleman v. Court of Appeals of Maryland

(decided yesterday, March 20, 2012): May Congress subject states to liability to employees for violation of FMLA self-care leave provision?Justices Roberts and Kennedy, joined in the result by

Justices Thomas and Scalia): No – that’s unconstitutionalDissenters: Justices Breyer, Ginsburg, Kagan, and

Sotomayor: Yes, it is constitutional

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

Here is what Justice Scalia had to say in his concurring opinion:

The plurality’s opinion [holding unconstitutional Congress’s attempt to abrogate State immunity from claims of FMLA self-care leave] seems to me a faithful application of our ‘congruence and proportionality’ jurisprudence [which sanctioned Congress’s overriding State immunity for FMLA family leave]. So does the opinion of the dissent [which would sustain the constitutionality of Congress’s attempt to abrogate State immunity from claims of FMLA self-care leave]. That is because the varying outcomes we have arrived at under the ‘congruence and proportionality’ test make no sense.

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

Which in turn is because that flabby test is “a standing invitation to judicial arbitrariness and policy-driven decisionmaking,” Tennessee v. Lane, 541 U. S. 509, 557–558 (2004) (SCALIA, J., dissenting). Moreover, in the process of applying (or seeming to apply) the test, we must scour the legislative record in search of evidence that supports the congressional action…This grading of Congress’s homework is a task we are ill suited to perform and ill advised to undertake.”

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

That leaves Justices Roberts and KennedyJustice Roberts:

Chief JusticeConcerned about politicization of the Court?

Justice KennedyThe wildcardNote Justice Kennedy’s opinion in Coleman: willing to

investigate legislative history.Might vote to sustain constitutionality

The four Democratically-appointed Justices only need one additional vote

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Issues Pending Before the U.S. Supreme Court

If the U.S. Supreme Court concludes that the individual mandate is unconstitutional but can be severed from the remainder of the Affordable Care Act, which provisions of the Act are adversely affected? The Act’s Mandated use of modified community ratingProhibition on pre-existing condition exclusionsRequirement that individuals may, every year, opt in

or out of Exchange coverage and change levels of Exchange coverage

© 2012 DINSMORE & SHOHL | LEGAL COUNSEL | www.dinsmore.com

Questions?

Thomas W. HessDinsmore & Shohl LLPColumbus, Ohio(614) [email protected]