Embed Size (px)

Citation preview

© 2010 Frederick J. Caspar

2010/2011 INCOME TAX PLANNING;

BASIC ESTATE PLANNING

ANDBEYOND Dinsmore & Shohl LLPFrederick J. Caspar, J.D.

10 Courthouse Plaza, S.W., Suite 1100Dayton, Ohio 45402

(513) [email protected]

November 11, 2010

2

BRIEF SUMMARY OF UPCOMING CHANGES

3

ROTH IRA CONVERSIONS Roth Conversion (previously 100,000 AGI limit)

• Pay taxes in 2010, or• Spread income equally in 2011 and 2012

○ Election not due until 2010 tax return filed.

4

SMALL BUSINESS JOBS AND CREDIT ACT (9/2010)• Section 179 Deduction for Equipment

○ Limit increased from $250,000 to $500,000 in 2010 and 2011.

○ Phase-out starts at $2 Million of qualified property vs. $800,000 previously.

50% Bonus Depreciation Extended to 2010 Self-employed taxpayers able to deduct health

insurance premiums from earned income in 2010.

5

HEALTH REFORM ACT (3/2010) In 2010 forward, sliding scale tax credit for

qualified small employers to offset employer health insurance cost.• See calculation at www.NFIB.com/creditcalculator

In 2013 forward:• Additional tax of 0.9% on earned income over $200,000/$250,000 for single/joint taxpayers.• Additional tax of 3.8% on unearned income to the extent modified AGI exceeds $200,000/$250,000.

In 2018 forward: 40% excise tax on health insurance premiums in excess of $10,800/$27,500 for individual/family coverage

6

INCOME TAX CHANGES2010 Joint Tax Rates

$0 to $16,750 10% of amount over $016,750 to 68,000 $1,675.00 + 15% of amount over $16,75068,000 to 137,300 $9,362.50 + 25% of amount over 68,000137,300 to 209,250 $26,687.50 + 28% of amount over $137,300209,250 to 373,650 $46,833.50 + 33% of amount over 209,250Over 373,650 $101,085.50 + 35% of amount over 373,650

7

Expected 2011 Tax RatesIf taxable income

Is over But not over The tax is:$0 $60,699 15% of the amount over $0$60,699 $146,660 $9,104.80 plus 28% of the amount over $60,699$146,660 $223,485 $33,173.86 plus 31% of the amount over $146,660$223,485 $399,144 $56,989.60 plus 36% of the amount over $223,485$399,144 unlimited $120,226.94 plus 39.6% of the amount over

$399,144

8

Simple Example Married couple has the $100k AGI, 4

exemptions & no deductions. What is their tax for each year?

2010 2011

Taxable Income $74,000 $75,200

Tax $10,863 $13,451

Effective Average Tax Rate

10.86% 13.45%

Marginal Bracket 25% 28%

9

Example with Unearned Income Married couple has the $400k AGI, $300k dividend,

$100k ordinary income, 4 exemptions & no deductions.

What is their tax for each year?

2010 2011

Taxable Income $374,000 $390,200

Tax $ 55,863 $118,043

Effective Average Tax Rate

13.97% 29.5%

Marginal Bracket 35% 40%

10

To Net $1After Federal Income Taxes

Capital Gains Max. Rate Gross Increase

2010 15.0% $ 1.18

2011-2012 20.0% $ 1.25 6%

2013 & later (HI tax)

23.8% $ 1.31 11%

Dividends Max. Rate Gross Increase

2010 15.0% $ 1.18

2011-2012 39.6% $ 1.66 40%

2013 & later (HI tax)

43.4% $ 1.77 50%

11

Some 2010 Year-End Planning

12

Will 2010 Rates be Extended If not

• Roth conversion in 2010.• Trigger capital gains/buy back stocks if desired.

○ If capital loss carry-forwards would offset, no benefit.• Avoid taking capital losses until 2011.• Sell property on installment basis.

○ Have until as late as 10/15/11 to decide whether to report in 2010 or 2011.

• Should expenditures be capitalized and not expended.○ Sections 59(e), 174, 263, 266

• Consider avoiding tax free exchanges/rollovers.• Pay bonuses after March 15, 2011.

○ Employees may want to accelerate bonuses.• Avoid bonus depreciation/use slower depreciation.• Accelerate 15% C corporation dividends into 2010.

13

BASIC ESTATE PLANNING AND

BEYOND

14

ESTATE TAX RATE CHANGES

Year Estate Tax Exemption Top Estate Tax

2009 $3,500,000 45%

2010 Estate tax repealed 0%

2011 and beyond $1,000,000 55%

15

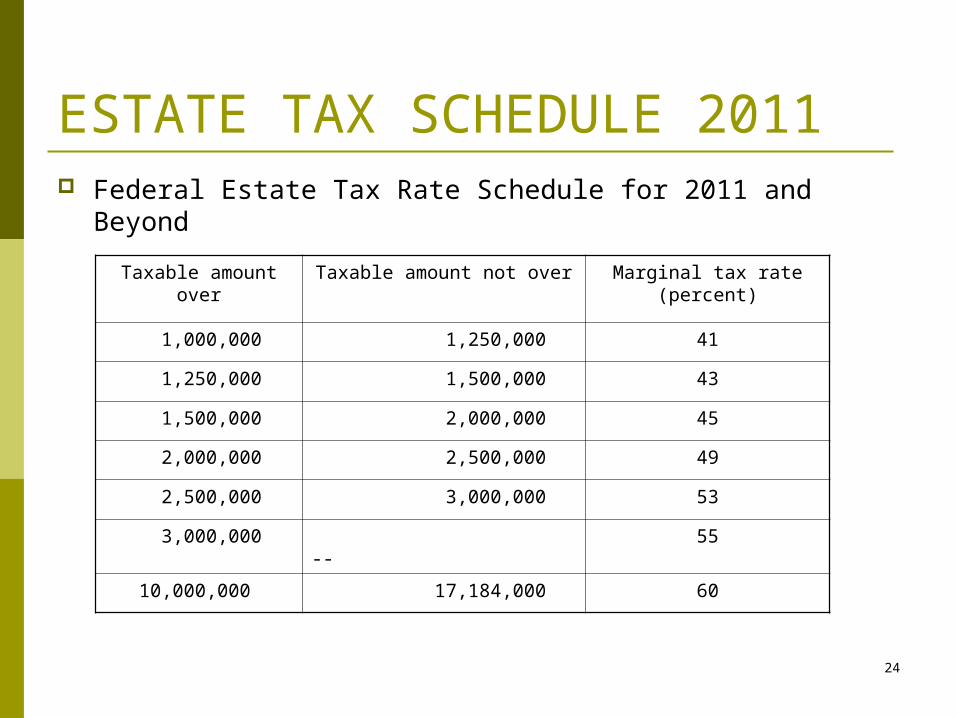

Federal Estate Tax Rate Schedule for 2011 and Beyond.

Taxable amount over

Taxable amount not over Marginal tax rate (percent)

1,000,000 1,250,000 41

1,250,000 1,500,000 43

1,500,000 2,000,000 45

2,000,000 2,500,000 49

2,500,000 3,000,000 53

3,000,000 -- 55

10,000,000 17,184,000 60

16

GIFT TAX CHANGES• 35% tax rate in 2010.• 41% to 60% tax rate in 2011 and beyond.

17

THE NEED FOR ESTATE PLANNING NON-FINANCIAL GOALS

• Give what you want.• To whom you want.• When and in the manner in which you want.

FINANCIAL GOALS• At the least possible tax cost, consistent with

other goals.• With needed liquidity to allow for

implementation of non-financial goals.

18

SOME RESULTS OF BAD PLANNING Allow the State to decide who is entitled to

your assets, and when. Significantly and unnecessarily reduce

family wealth. Jeopardize family business. Jeopardize the financial and mental health

of your beneficiaries.

19

SOME NON-FINANCIAL DECISIONS GUARDIAN

• For minor children• For you• Successor

EXECUTOR• Role• Fees

TRUSTEE• For children

○ Special needs trust• For parents, or other family members• Asset protection for beneficiaries• Business transition

20

SOME NON-FINANCIAL DECISIONS (cont.) AVOIDANCE OF PROBATE—ADVANTAGES OF FUNDING A LIVING

TRUST• Probate Administration with respect to assets in trust is avoided.

○ Court fees saved○ Court delays avoided○ Executor and attorney fees saved○ Especially important to avoid multiple probates if property is

owned in other states• Confidentiality.

○ Estate, its value, and identity of beneficiaries is not a matter of public record

WHAT A LIVING TRUST WILL NOT DO• Save estate taxes• Protect assets from creditors during life

OTHER WAYS TO AVOID PROBATE• Transfer/payable on death• Beneficiary designation

21

SOME NON-FINANCIAL DECISIONS (cont.) DURABLE POWERS OF ATTORNEY

• Name Attorney-in-Fact/Successor• Name Guardian of you/children

HEALTH CARE POWERS/LIVING WILLS• Allows you to make your own choice• Organ Donation• DNR Orders

22

SOME NON-FINANCIAL DECISIONS (cont.) LEAVE ROADMAP

• Consolidate assets• Consolidate papers• Leave financial statement• Leave advisor information

23

SOME FINANCIAL OBJECTIVES PRENUPTUAL

• Family Partnership/Trusts can also maintain separate property nature of assets

LONGTERM CARE/MEDICAID• Insurance• Asset planning

GIFTING PROGRAMS• Gift and estate taxes are here to stay• Annual exclusion• Section 529 plans• Custodian accounts• “Formal” trusts• Can reduce income taxes

MINIMIZE ESTATE TAXES

24

ESTATE TAX SCHEDULE 2011 Federal Estate Tax Rate Schedule for 2011 and Beyond

Taxable amount over

Taxable amount not over Marginal tax rate (percent)

1,000,000 1,250,000 41

1,250,000 1,500,000 43

1,500,000 2,000,000 45

2,000,000 2,500,000 49

2,500,000 3,000,000 53

3,000,000 -- 55

10,000,000 17,184,000 60

25

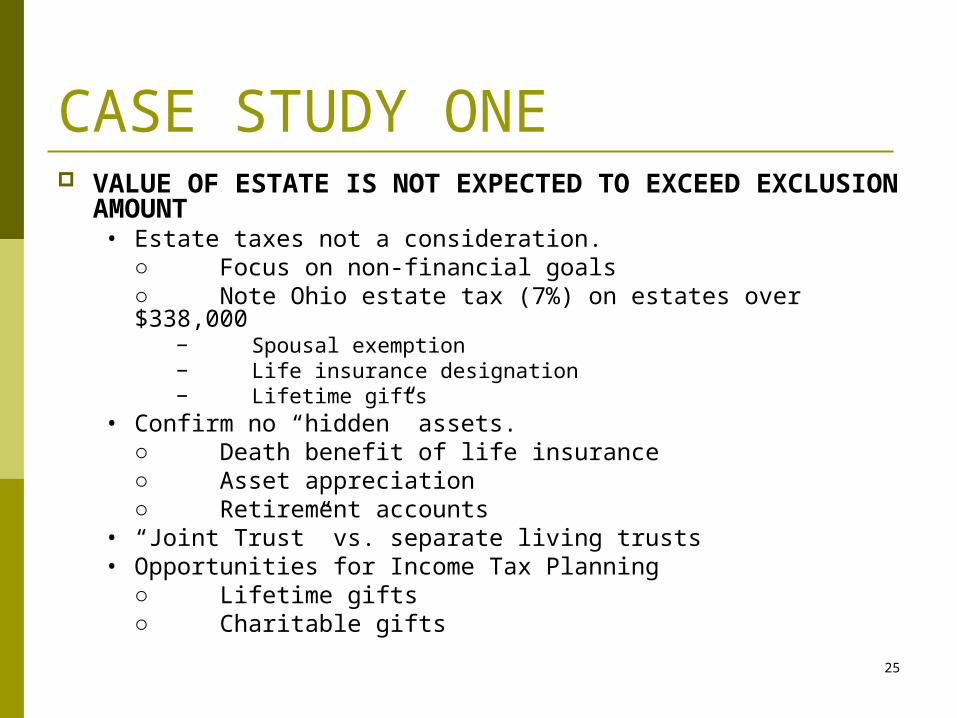

CASE STUDY ONE VALUE OF ESTATE IS NOT EXPECTED TO EXCEED

EXCLUSION AMOUNT• Estate taxes not a consideration.

○ Focus on non-financial goals○ Note Ohio estate tax (7%) on estates over $338,000

− Spousal exemption− Life insurance designation− Lifetime gifts

• Confirm no “hidden” assets.○ Death benefit of life insurance○ Asset appreciation○ Retirement accounts

• “Joint Trust” vs. separate living trusts• Opportunities for Income Tax Planning

○ Lifetime gifts○ Charitable gifts

26

CASE STUDY ONE (CONT.) GIFTS OF APPRECIATED STOCK OR REAL ESTATE

• By avoiding capital gains tax, a $1,000 contribution made this way can cost as little as $450.

Contribution $1,000Less capital gain tax avoided (20% x 1,000) (200)Less tax savings to donor from deduction (1,000 x 35%) (350)Net Cost to Donor $ 450

CHARITABLE BEQUESTS

• A charitable bequest is a gift by Will (or trust) to a charity. If the gift is so-called IRD (Income in Respect of a Decedent), such as an IRA or a 401(k) benefit, it reduces estate taxes and income taxes. An IRA or 401(k) benefit is subject to both estate and income taxes at death of up to 68 percent; naming a charity as a beneficiary avoids both of these taxes.

• Note Section 691(c) income tax deduction if there is estate tax on IRD.

27

CASE STUDY TWO VALUE OF ESTATE EXCEEDS EXCLUSION AMOUNT FOR

ONE SPOUSE, BUT NOT FOR BOTH SPOUSES(Assumes $1,000,000 Exclusion per spouse)

Residence $ 300,000Investments 700,000 (including retirement accounts)Family Business/Rental Real Estate 500,000Life Insurance on Mr. Brown 500,000

TOTAL VALUE OF ESTATE $2,000,000

28

CASE STUDY TWO (cont.)Mr. Brown’s Estate

$2,000,000

Mrs. Brown’s Estate

$435,000 $1,565,000

IRS John, Sue and Debbie

29

ESTATE TAX PLANNING WITH CREDIT SHELTER (“B”) TRUST

Mr. Brown’s Estate

$1,000,000 $1,000,000

On Mrs. Brown’s Death

$0 $2,000,000

IRS John, Sue and Debbie

To Mrs. Brown's "A” Trust• Distributable to Mrs. Brown without restriction

To Mrs. Brown’s “B” Trust• Net income to Mrs. Brown• Discretion in Trustee on principal to Mrs. Brown for health, maintenance and support• Up to 5% of principal each year at Mrs. Brown’s election for any reason• Mrs. Brown is Trustee

30

TITLING OF ASSETSSplit between spouses

○ Do not know who will pass first

Adjust beneficiary/joint and survivor designations

Asset protection from acts of one spouse

31

CASE STUDY THREE

VALUE OF ASSETS EXCEED BOTH SPOUSES EXCLUSION AMOUNT

32

CASE STUDY THREE (cont.) Add Insurance Trust

Mr. Brown’s Estate

$2,000,000 Premiums Funded

$1,000,000 $1,000,000 Insurance Trust

To Mrs. Brown’s “A” Trust

• Distributable to Mrs. Brown without restriction.

To Mrs. Brown’s “B” Trust and Insurance Trust

• Net Income to Mrs. Brown. • Discretion in Trustee on principal to Mrs. Brown for health, maintenance and support.• Up to 5% of principal each year at Mrs. Brown’s election for any reason.• Mrs. Brown is Trustee.

$500,000

On Mrs. Brown’s Death

$0 $2,500,000

IRS John, Sue & Debbie

33

CASE STUDY THREE (cont.) Add Annual GiftsYear Annual Gifts* Value in Year 10 @ 6%1 $78,000 $ 139,6802 $78,000 131,7803 $78,000 124,3204 $78,000 117,2805 $78,000 110,6406 $78,000 104,3807 $78,000 98,4708 $78,000 92,9009 $78,000 87,64010 $78,000 82,680

Total Value Transferred $ 1,089,770Estate Tax Rate x55%Transfer Tax Savings through Year 10 $ 599,375

* Assumes three donees.

34

ADD NON-VOTING COMMON STOCK/FAMILY LIMITED PARTNERSHIP, LLC

Mrs. Brown(or Living Trust)

Mrs. Brown(or Living Trust)

Outright or to Trusts for Children

Voting Stock/

General Partner

Non-Voting Stock/Limited Partner

Non-Voting Stock/Limited Partner

Voting Stock/General Partner

John Sue Debbie

BROWN FAMILY BUSINESS OR LIMITED PARTNERSHIP

Owns:• Family Business, or rental Real Estate/InvestmentsAllows For:• Control separate from economic ownership• Asset protection• Discounted gifting

35

LEVERAGED ANNUAL GIFTS

YearAnnual Gift of Non-Voting Stock or

Limited Partner InterestsPost Discount Annual Gifts*

Value in Year 10 @ 7%

1 $130,000 $78,000 $232,800

2 $130,000 $78,000 219,630

3 $130,000 $78,000 207,200

4 $130,000 $78,000 195,470

5 $130,000 $78,000 184,400

6 $130,000 $78,000 173,970

7 $130,000 $78,000 164,100

8 $130,000 $78,000 154,800

9 $130,000 $78,000 146,000

10 $130,000 $78,000 137,800

Total Value Transferred $1,816,170

Estate Tax Rate x55%

Transfer Tax Savings through Year 10 $ 998,894

Additional Tax Savings as Compared to Non-Leveraged Gifts $ 399,519

* Assumes three donees; 40% discount.

36

LEVERAGED ANNUAL GIFTS (cont.) ADDITIONAL BENEFITS OF FAMILY ENTITY

STRUCTURE• Asset protection• To hold and manage family assets• To provide centralized management• To encourage children to become knowledgeable in family

investment activities• To provide investment diversification to donees• To provide a degree of asset protection from divorce or

creditor judgments for non-managing/non-voting members• To provide opportunity to transfer wealth to future generations

while allowing the donor to retain managerial control• To provide an administratively easier way to transfer a

“basket” of assets• To avoid fractionalizing management and control of

undividable property

37

ADDITIONAL GIFTING TECHNIQUES Grantor Retained Annuity Trusts Defective Grantor Trust Installment Sale Planning for Businesses Qualified Personal Residence Trust Charitable Lead Trust Charitable Remainder Trust Additional Leveraging with Life Insurance