Embed Size (px)

Citation preview

© 2008 Pearson Addison Wesley. All rights reserved

Chapter Six

Firms and Production

Firms and Production

• In this chapter, we examine six topics

- The Ownership and Management of Firms

- Production

- Short-Run Production

- Long-Run Production

- Returns to Scale

- Productivity and Technical Change

© 2008 Pearson Addison Wesley. All rights reserved. 6-2

The Ownership and Management of Firms

• Firm

–an organization that converts inputs such as labor, materials, energy, and capital into outputs, the goods and services that it sells.

© 2008 Pearson Addison Wesley. All rights reserved. 6-3

The Ownership and Management of Firms

• In most countries, for-profit firms have one of three legal forms:– Sole proprietorships are firms owned and run by a single individual.

– Partnerships are businesses jointly owned and controlled by two or more people. The owners operate under a partnership agreement.

– Corporations are owned by shareholders in proportion to the numbers of shares of stock they hold. The shareholders elect a board of directors who run the firm.

© 2008 Pearson Addison Wesley. All rights reserved. 6-4

The Ownership of Firms

• Corporations differ from the other two forms of ownership in terms of personal liability for the debts of the firm.

• Corporations have limited liability: The personal assets of the corporate owners cannot be taken to pay a corporation’s debts if it goes into bankruptcy.

© 2008 Pearson Addison Wesley. All rights reserved. 6-5

The Ownership of Firms

• Limited Liability–condition whereby the personal assets of the owners of the corporation cannot be taken to pay a corporation’s debts if it goes into bankruptcy

• Sole proprietors and partnerships have unlimited liability - that is, even their personal assets can be taken to pay the firm’s debts.

© 2008 Pearson Addison Wesley. All rights reserved. 6-6

The Management of Firms

• In a small firm, the owner usually manages the firm’s operations.

• In larger firms, typically corporations and larger partnerships, a manager or team of managers usually runs the company.

© 2008 Pearson Addison Wesley. All rights reserved. 6-7

What Owners Want

• Economists usually assume that a firm’s owners try to maximize profit.

• profit ( )–the difference between revenues, R, and costs, C: = R - C

• To maximize profits, a firm must produce as efficiently as possible as we will consider in this chapter.

© 2008 Pearson Addison Wesley. All rights reserved. 6-8

What Owners Want

• Efficient Production or Technological Efficiency–situation in which the current level of output cannot be produced with fewer inputs, given existing knowledge about technology and the organization of production

• If the firm does not produce efficiently, it cannot be profit maximizing - so efficient production is a necessary condition for profit maximization.

© 2008 Pearson Addison Wesley. All rights reserved. 6-9

Production

• A firm uses a technology or production process to transform inputs or factors of production into outputs.

–Capital (K)–Labor (L)–Materials (M)

© 2008 Pearson Addison Wesley. All rights reserved. 6-10

Production Functions

• The various ways inputs can be transformed into output are summarized in the production function: the relationship between the quantities of inputs used and the maximum quantity of output that can be produced, given current knowledge about technology and organization. The production function for a firm that uses only labor (L) and capital (K) is

q = f (L, K), (6.2)

where q units of output are produced. © 2008 Pearson Addison Wesley. All rights reserved. 6-11

Production Functions

• The production function shows only the maximum amount of output that can be produced from given levels of labor and capital, because the production function includes only efficient production processes.

© 2008 Pearson Addison Wesley. All rights reserved. 6-12

Time and the Variability of Inputs

• Short Run–a period of time so brief that at least one factor of production cannot be varied practically

• Fixed Input–a factor of production that cannot be varied practically in the short run

© 2008 Pearson Addison Wesley. All rights reserved. 6-13

Time and the Variability of Inputs

• Variable Input –a factor of production whose quantity can be changed readily by the firm during the relevant time period

• Long Run–a lengthy enough period of time that all inputs can be varied

© 2008 Pearson Addison Wesley. All rights reserved. 6-14

Short-Run Production: One Variable and One Fixed Input

• In the short run, we assume that capital is fixed input and labor is a variable input.

• In the short run, the firm’s production function is

(6.3)

where q is output, L is workers, and is the fixed number of units of capital.

© 2008 Pearson Addison Wesley. All rights reserved. 6-15

K

Total Product of Labor

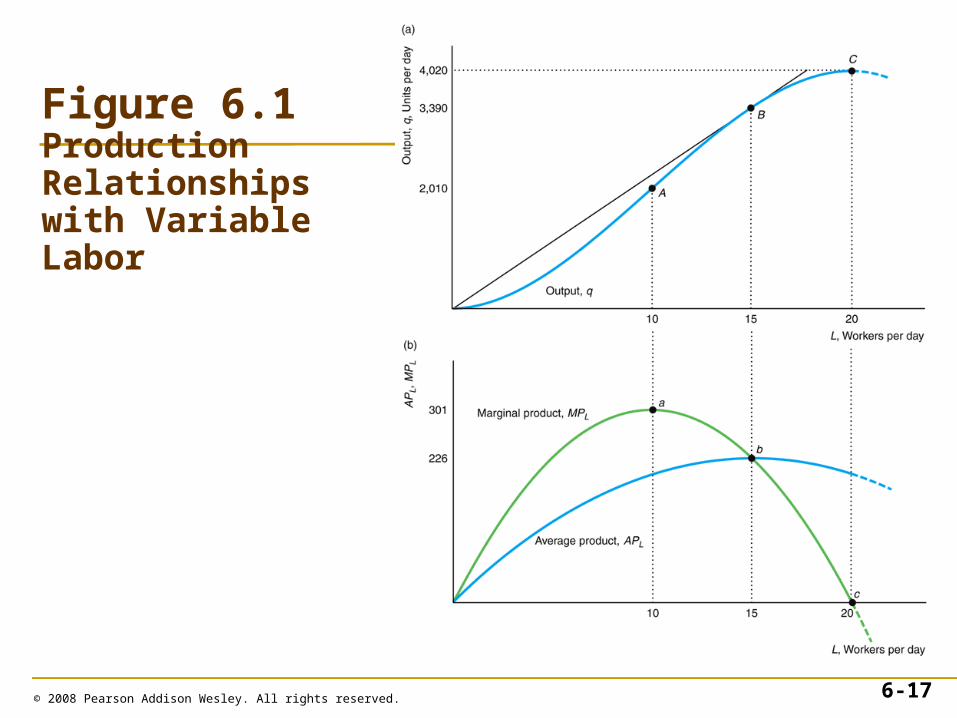

• The exact relationship between output or total product and labor can be illustrated by using a particular function, Equation 6.3, or a figure, Figure 6.1.

© 2008 Pearson Addison Wesley. All rights reserved. 6-16

© 2008 Pearson Addison Wesley. All rights reserved. 6-17

Figure 6.1Production Relationships with Variable Labor

Marginal Product of Labor

• marginal product of labor (MPL)

–the change in total output, , resulting from using an extra unit of labor, , holding other factors constant.

–The marginal product of labor is the partial derivative of the production function with respect to labor,

© 2008 Pearson Addison Wesley. All rights reserved. 6-18

q ( , )

f L K

MPLL L

q

L

Average Product of Labor

• average product of labor (APL)

–the ratio of output, q, to the number of workers, L, used to produce that output:

APL = q/L

© 2008 Pearson Addison Wesley. All rights reserved. 6-19

Relationship of the Product Curves

• The average product of labor curve slopes upward where the marginal product of labor curve is above it and slopes downward where the marginal product curve is below it.

© 2008 Pearson Addison Wesley. All rights reserved. 6-20

Law of Diminishing Marginal Returns

• The law of diminishing marginal returns (or diminishing marginal product) holds that, if a firm keeps increasing an input, holding all other inputs and technology constant, the corresponding increases in output will become smaller eventually.

© 2008 Pearson Addison Wesley. All rights reserved. 6-21

Law of Diminishing Marginal Returns

• Where there are “diminishing marginal returns,” the MPL curve is falling.

• Within “diminishing returns,” extra labor causes output to fall.

• Thus saying that there are diminishing returns is much stronger than saying that there are diminishing marginal returns.

© 2008 Pearson Addison Wesley. All rights reserved. 6-22

Long-Run Production: Two Variable Inputs

• In the long run, however, both inputs are variable. With both factors variable, a firm can usually produce a given level of output by using a great deal of labor and very little capital, a great deal of capital and very little labor, or moderate amounts of both.

© 2008 Pearson Addison Wesley. All rights reserved. 6-23

© 2008 Pearson Addison Wesley. All rights reserved. 6-24

Equation 6.4

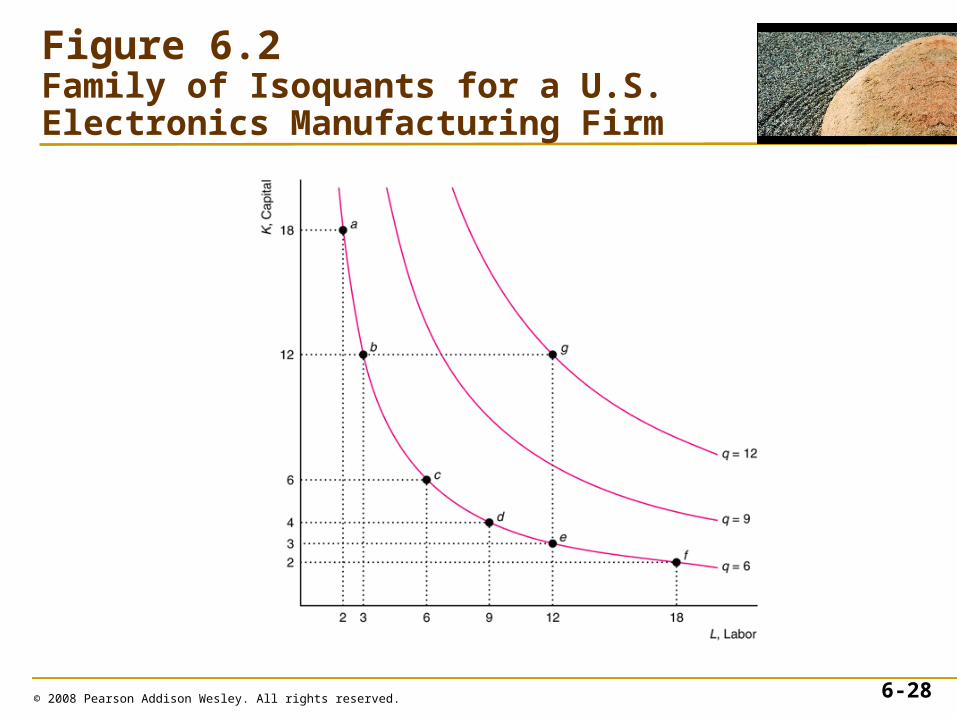

Isoquants

• isoquant

–a curve that shows the efficient combinations of labor and capital that can produce a single (iso) level of output (quantity)

• We can use these isoquants to illustrate what happens in the short run when capital is fixed and only labor varies.

© 2008 Pearson Addison Wesley. All rights reserved. 6-25

© 2008 Pearson Addison Wesley. All rights reserved. 6-26

Equation 6.5

Properties of Isoquants

• First, the farther an isoquant is from the origin, the greater the level of output.

• Second, isoquants do not cross.

• Third, isoquants slope downward.

© 2008 Pearson Addison Wesley. All rights reserved. 6-27

© 2008 Pearson Addison Wesley. All rights reserved. 6-28

Figure 6.2Family of Isoquants for a U.S. Electronics Manufacturing Firm

Shape of Isoquants

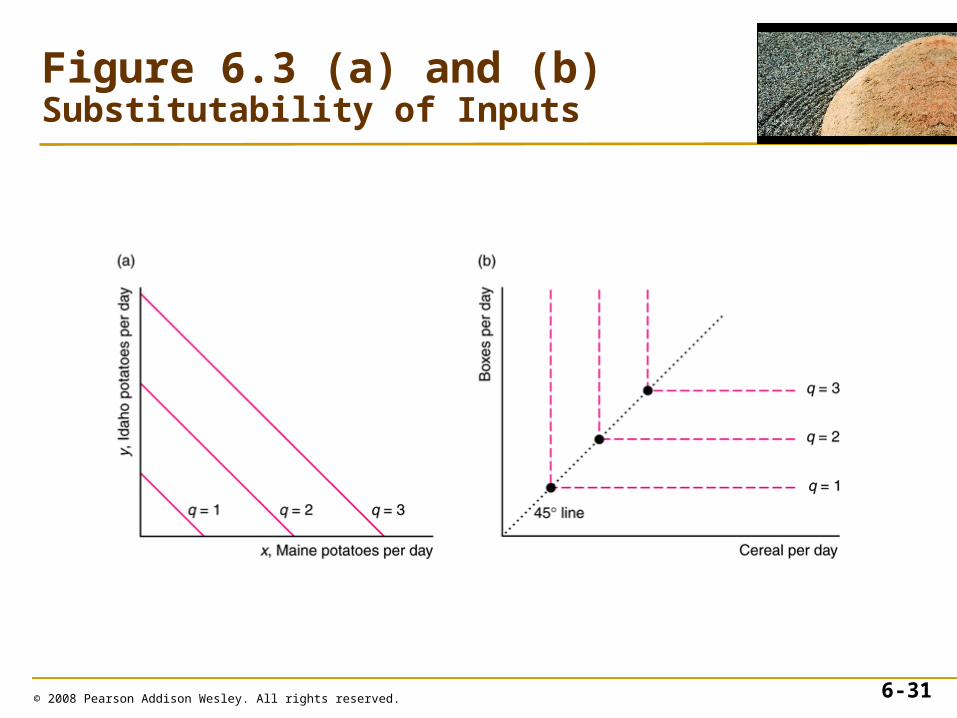

• The curvature of an isoquant shows how readily a firm can substitute one input for another.

• If the inputs are perfect substitutes, each isoquant is a straight line.

• The production function is

q = x + y

© 2008 Pearson Addison Wesley. All rights reserved. 6-29

Shape of Isoquants

• Sometimes it is impossible to substitute one input for the other: Inputs must be used in fixed proportion.

• Such a production function is called a fixed-proportions production function.

• The fixed-proportions production function is given by:

q = min(g, b).

© 2008 Pearson Addison Wesley. All rights reserved. 6-30

© 2008 Pearson Addison Wesley. All rights reserved. 6-31

Figure 6.3 (a) and (b)Substitutability of Inputs

© 2008 Pearson Addison Wesley. All rights reserved. 6-32

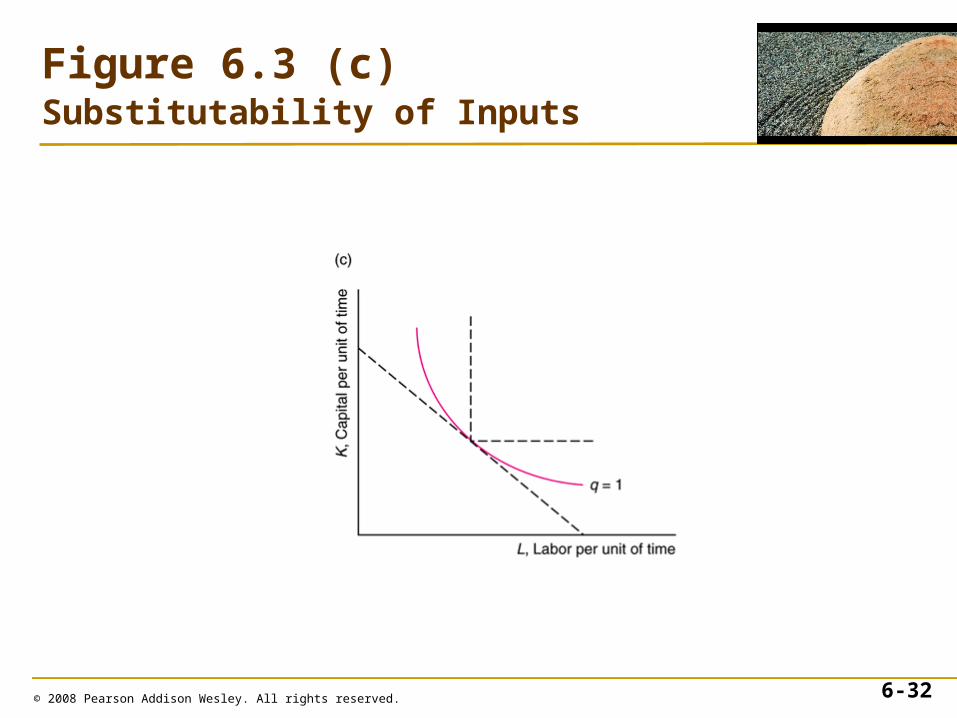

Figure 6.3 (c)Substitutability of Inputs

Substituting Inputs

• The slope of an isoquant shows the ability of a firm to replace one input with another while holding output constant.

• The slope of an isoquant is called the marginal rate of technological substitution (MRTS).

© 2008 Pearson Addison Wesley. All rights reserved. 6-33

© 2008 Pearson Addison Wesley. All rights reserved. 6-34

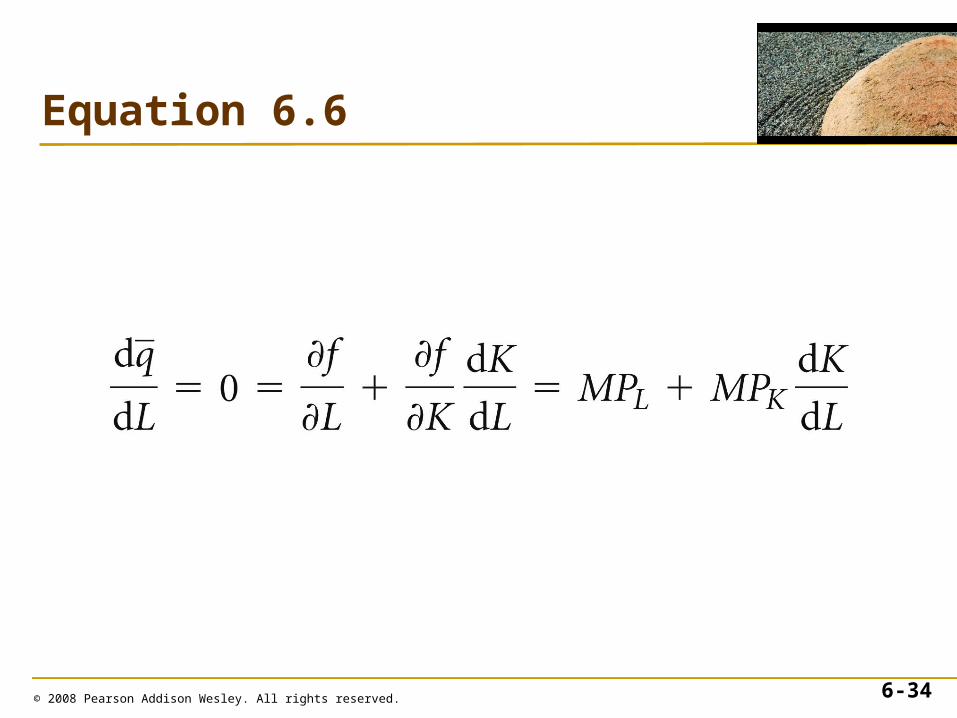

Equation 6.6

© 2008 Pearson Addison Wesley. All rights reserved. 6-35

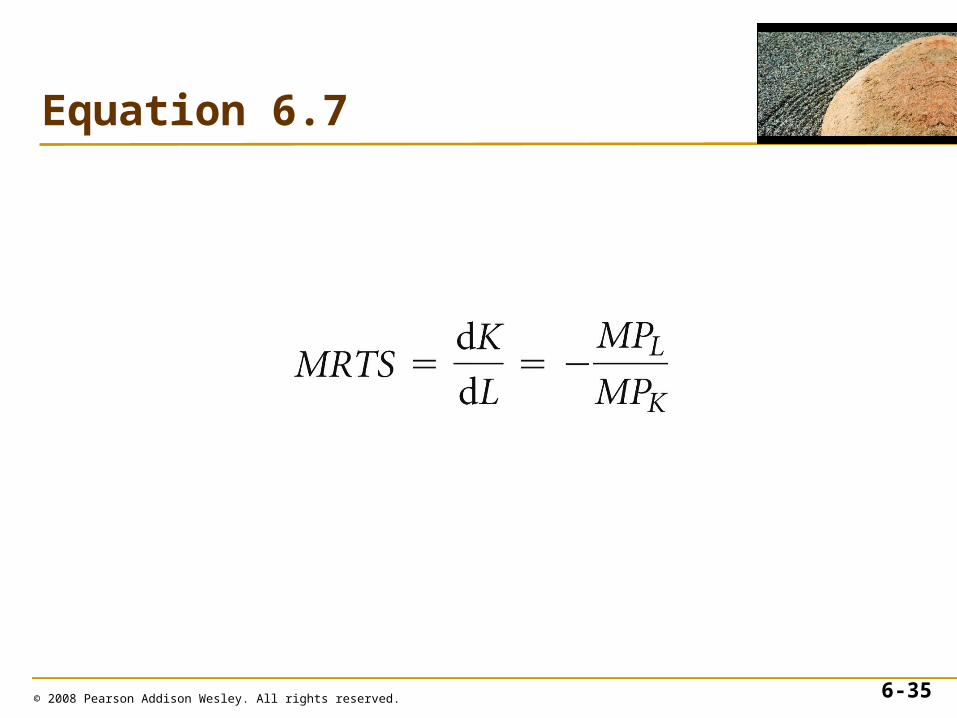

Equation 6.7

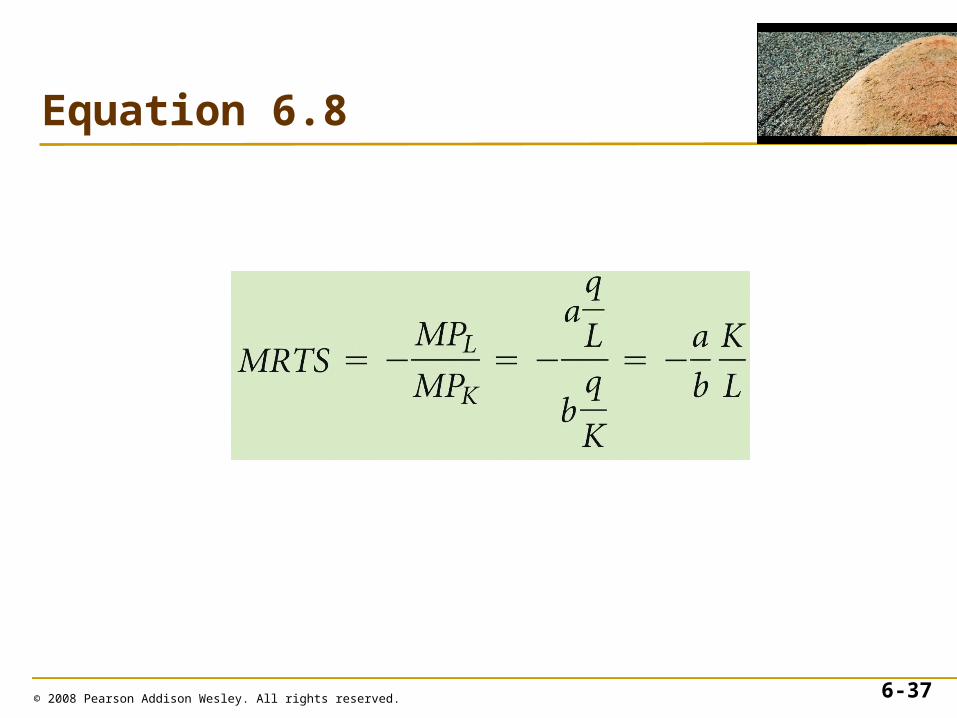

Solved Problem 6.3

• What is the marginal rate of technical substitution for a general Cobb-Douglas production function,

q = ALaKb ?

© 2008 Pearson Addison Wesley. All rights reserved. 6-36

© 2008 Pearson Addison Wesley. All rights reserved. 6-37

Equation 6.8

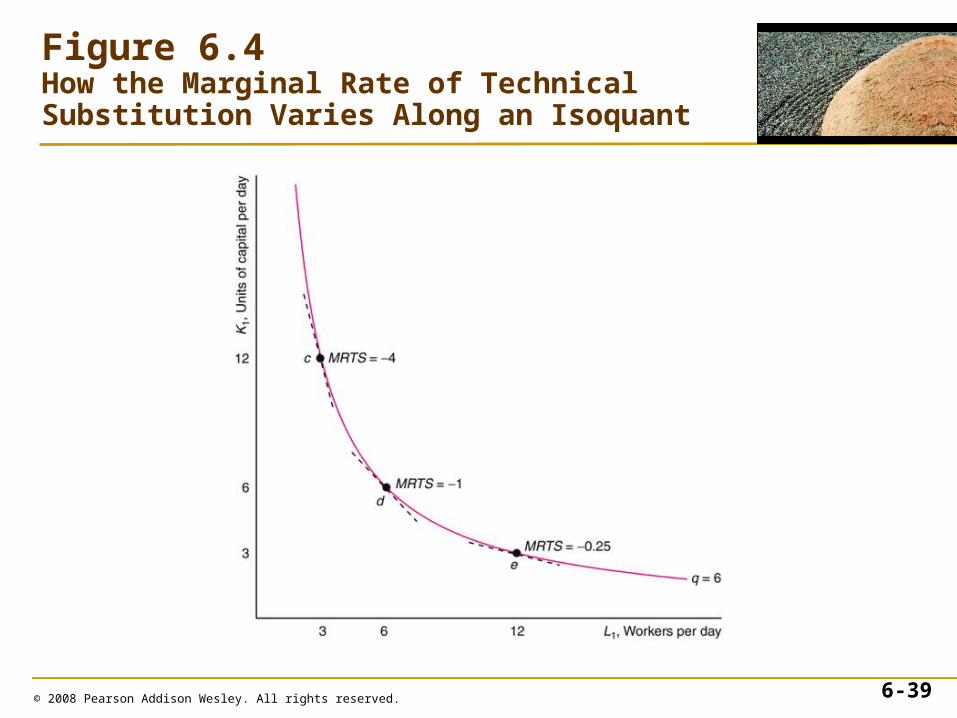

Diminishing Marginal Rates of Technical Substitution

• The marginal rate of technical substitution varies along a curved isoquant.

• This decline in the MRTS (in absolute value) along an isoquant as the firm increases labor illustrates diminishing marginal rates of technical substitution.

© 2008 Pearson Addison Wesley. All rights reserved. 6-38

© 2008 Pearson Addison Wesley. All rights reserved. 6-39

Figure 6.4How the Marginal Rate of Technical Substitution Varies Along an Isoquant

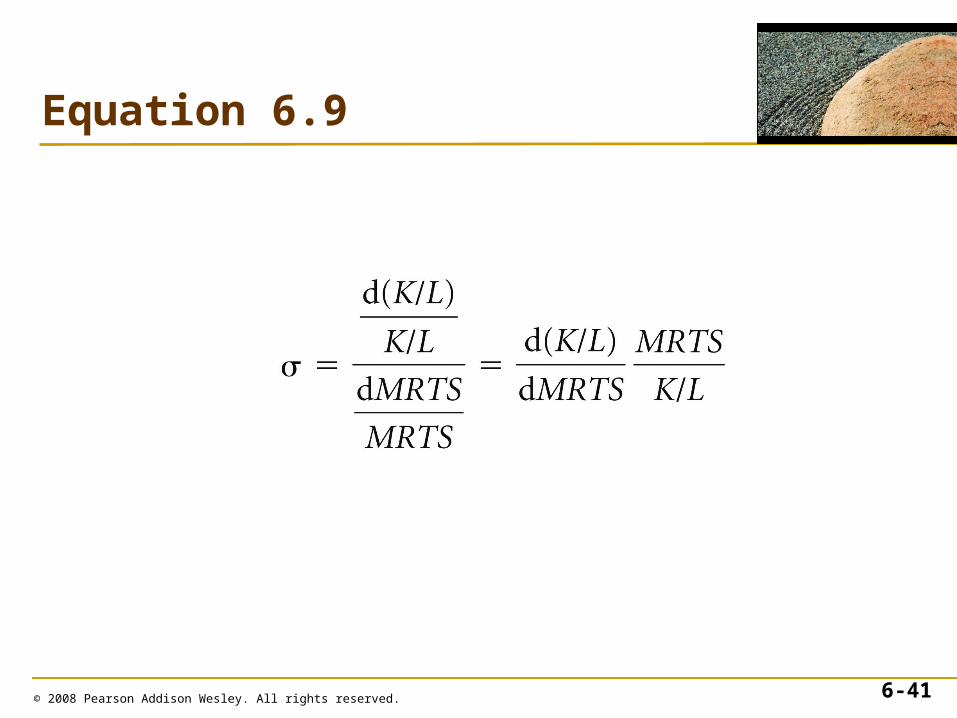

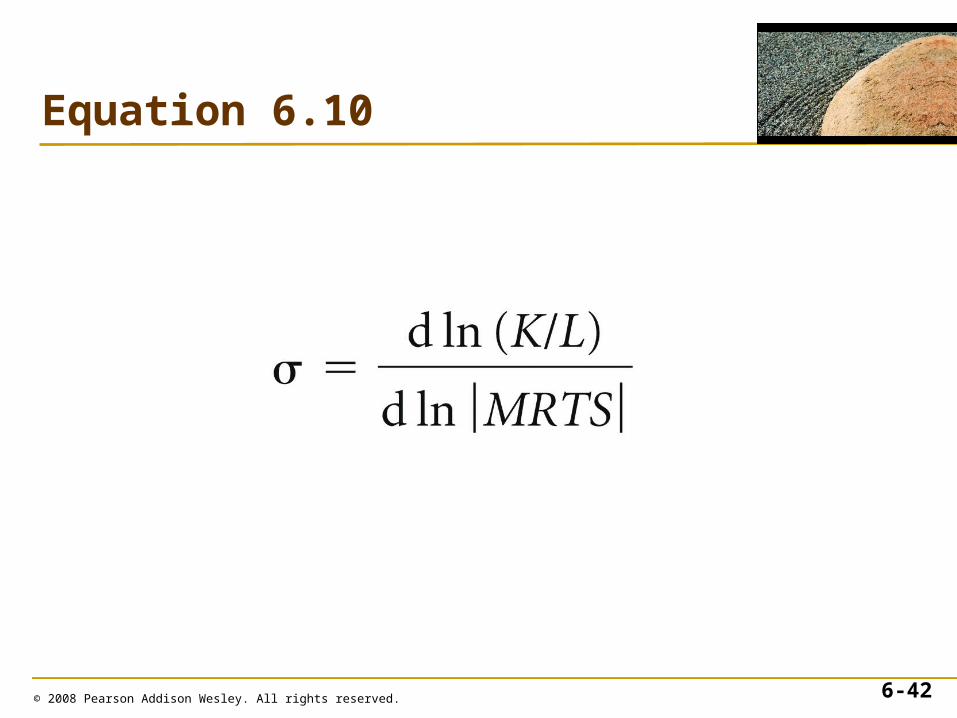

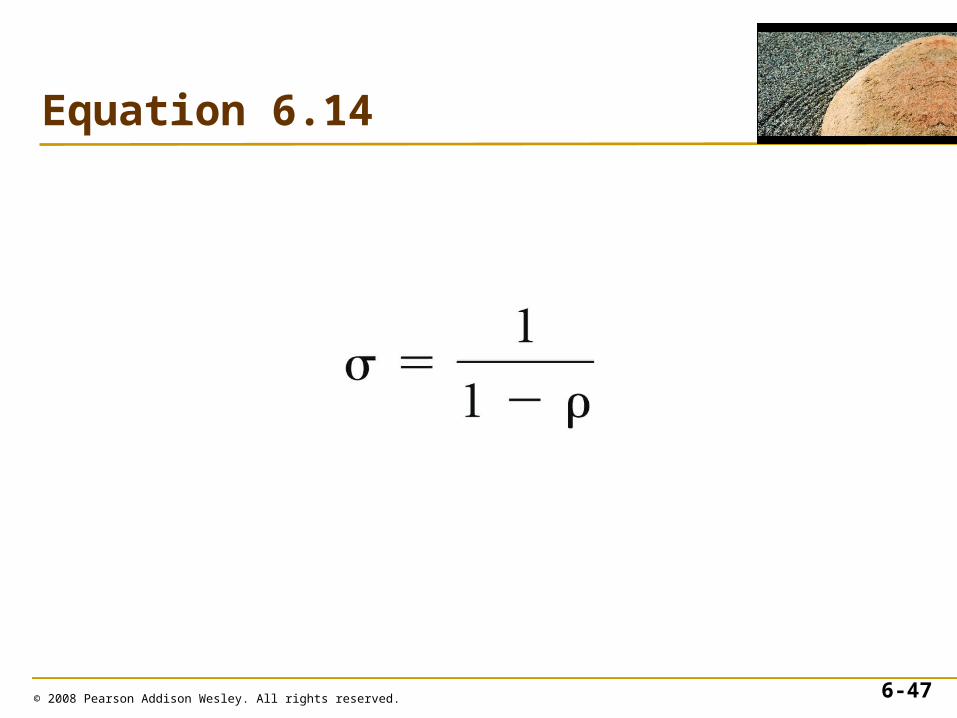

The Elasticity of Substitution

• The elasticity of substitution, , is the percentage change in the capital-labor ratio divided by the percentage change in the MRTS.

• This measure reflects the ease with which a firm can substitute capital for labor.

© 2008 Pearson Addison Wesley. All rights reserved. 6-40

© 2008 Pearson Addison Wesley. All rights reserved. 6-41

Equation 6.9

© 2008 Pearson Addison Wesley. All rights reserved. 6-42

Equation 6.10

The Elasticity of Substitution

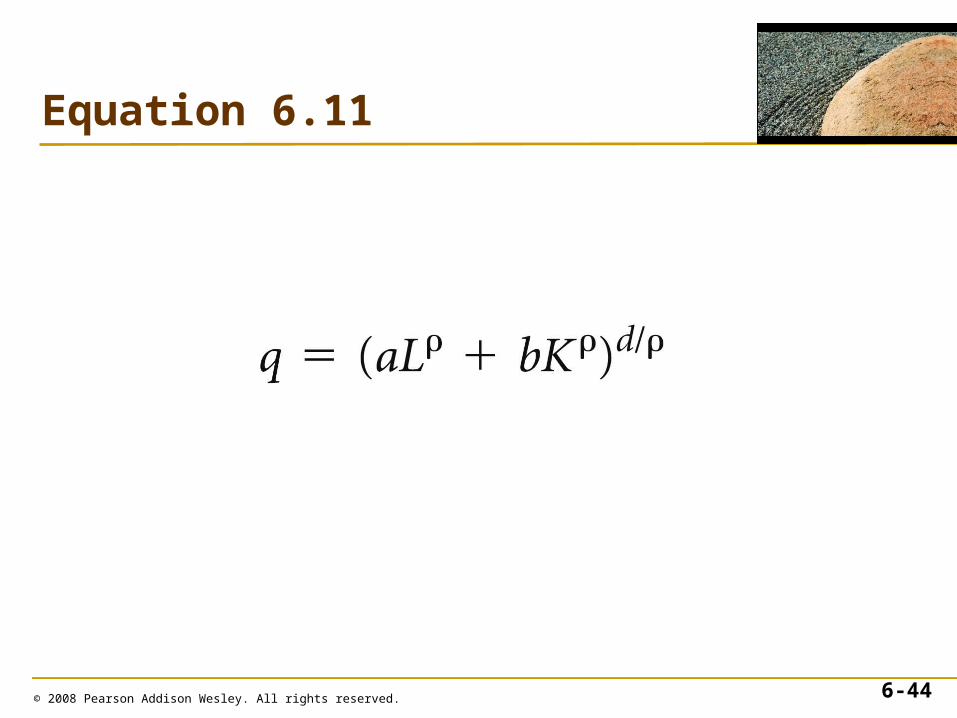

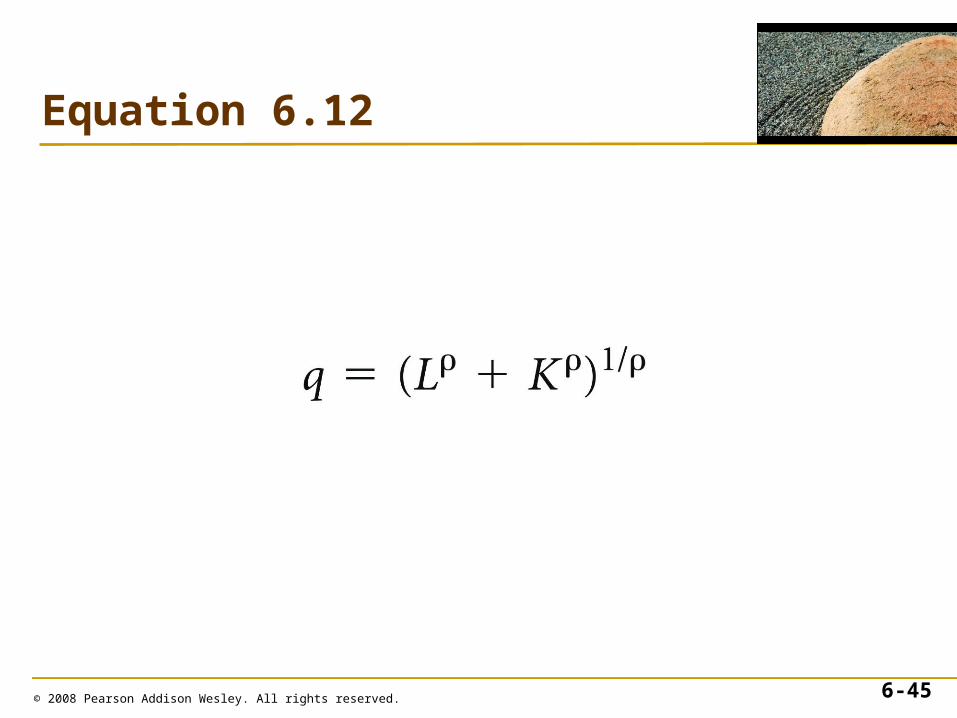

• Constant Elasticity of Substitution Production

- In general, the elasticity of substitution varies along an isoquant. An exception is the constant elasticity of substitution (CES) production function.

© 2008 Pearson Addison Wesley. All rights reserved. 6-43

© 2008 Pearson Addison Wesley. All rights reserved. 6-44

Equation 6.11

© 2008 Pearson Addison Wesley. All rights reserved. 6-45

Equation 6.12

© 2008 Pearson Addison Wesley. All rights reserved. 6-46

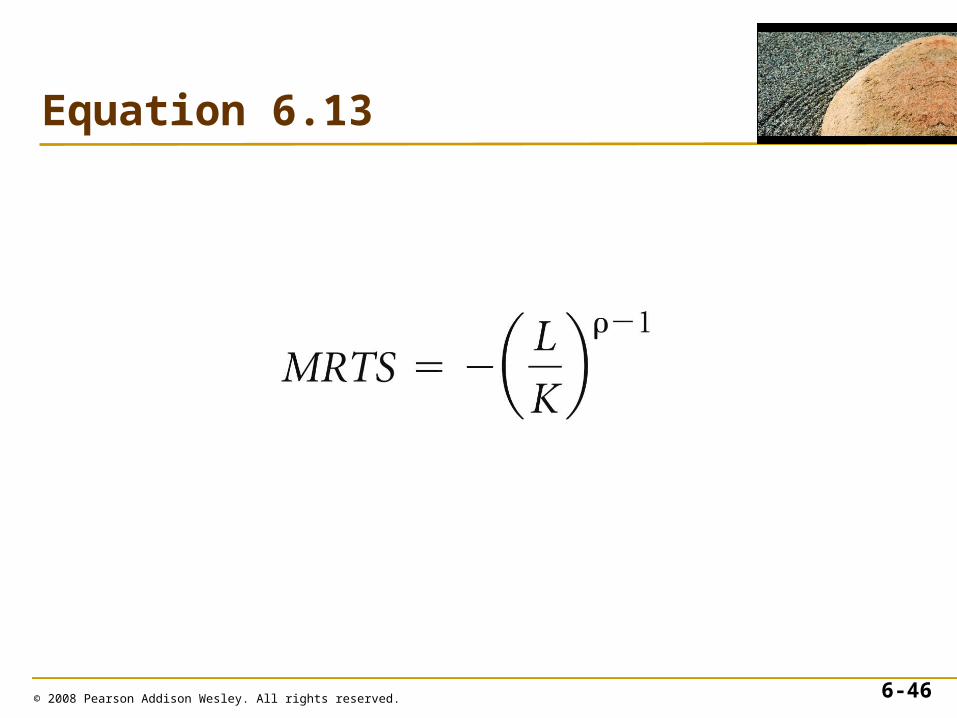

Equation 6.13

© 2008 Pearson Addison Wesley. All rights reserved. 6-47

Equation 6.14

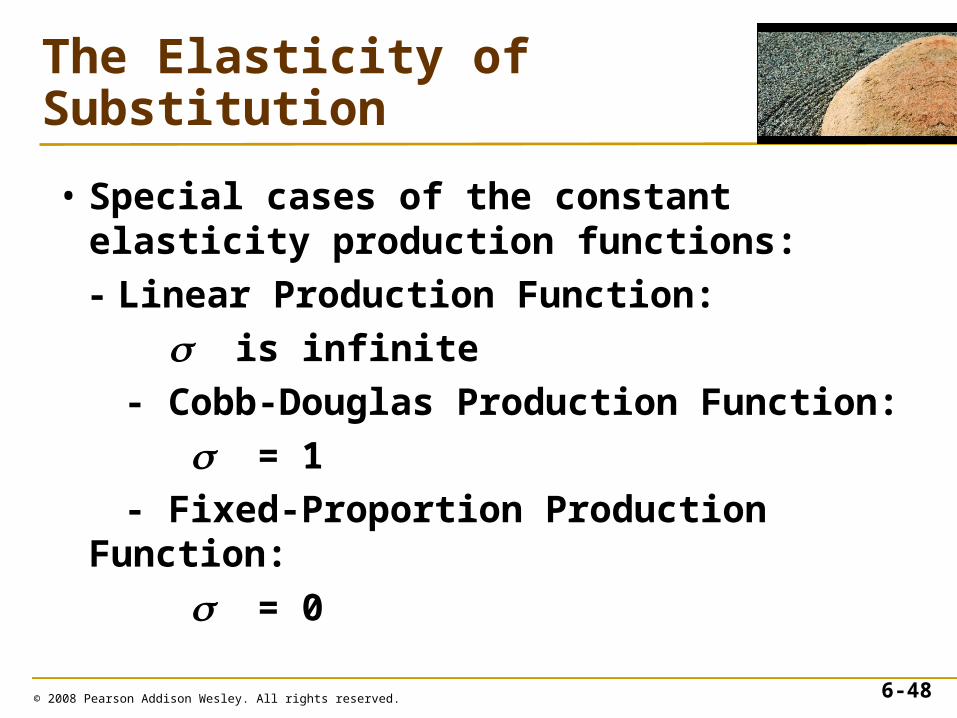

The Elasticity of Substitution

• Special cases of the constant elasticity production functions:

- Linear Production Function:

is infinite

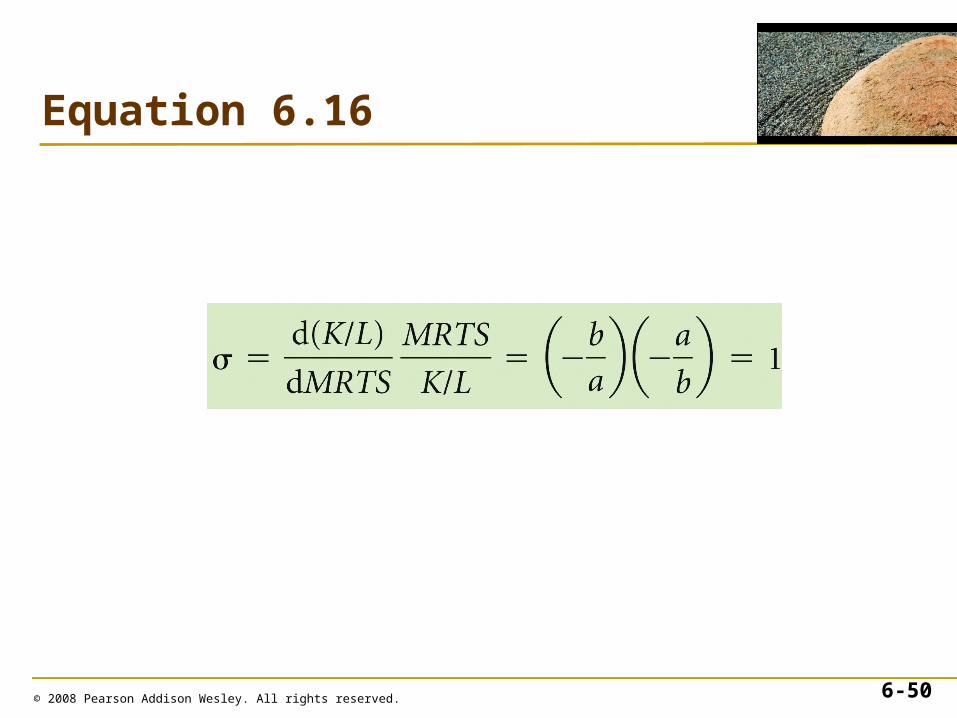

- Cobb-Douglas Production Function:

= 1

- Fixed-Proportion Production Function:

= 0

© 2008 Pearson Addison Wesley. All rights reserved. 6-48

© 2008 Pearson Addison Wesley. All rights reserved. 6-49

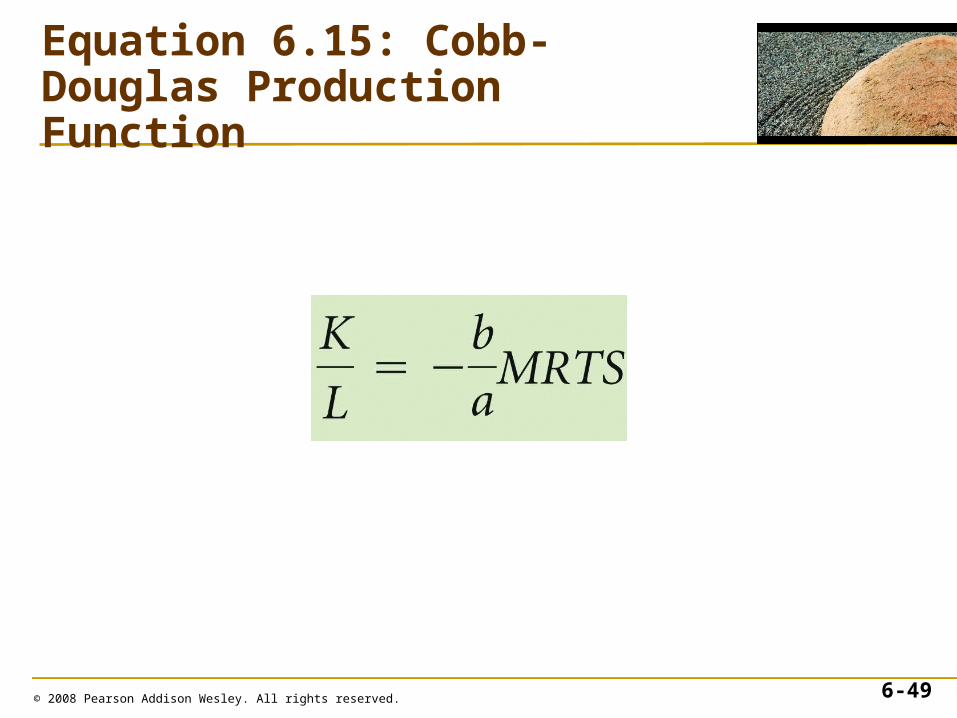

Equation 6.15: Cobb-Douglas Production Function

© 2008 Pearson Addison Wesley. All rights reserved. 6-50

Equation 6.16

Returns to Scale

• How much output changes if a firm increases all its inputs proportionately? The answer helps a firm determine its scale or size in the long run.

© 2008 Pearson Addison Wesley. All rights reserved. 6-51

Constant, Increasing, and Decreasing Returns to Scale

• constant returns to scale (CRS)

–property of a production function whereby when all inputs are increased by a certain percentage, output increases by that same percentage

© 2008 Pearson Addison Wesley. All rights reserved. 6-52

Constant, Increasing, and Decreasing Returns to Scale

• increasing returns to scale (IRS)–property of a production function whereby when output rises more than in proportion to an equal increase in all inputs

• A technology exhibits increasing returns to scale if doubling inputs more than doubles the output:

f(2L, 2K) > 2f(L, K)

© 2008 Pearson Addison Wesley. All rights reserved. 6-53

Constant, Increasing, and Decreasing Returns to Scale

• decreasing returns to scale (DRS)–property of a production function whereby output increase less than in proportion to an equal percentage increase in all inputs

• A technology exhibits decreasing returns to scale if doubling inputs causes output to rise less than in proportion: f(2L, 2K) < 2f(L, K)

© 2008 Pearson Addison Wesley. All rights reserved. 6-54

© 2008 Pearson Addison Wesley. All rights reserved. 6-55

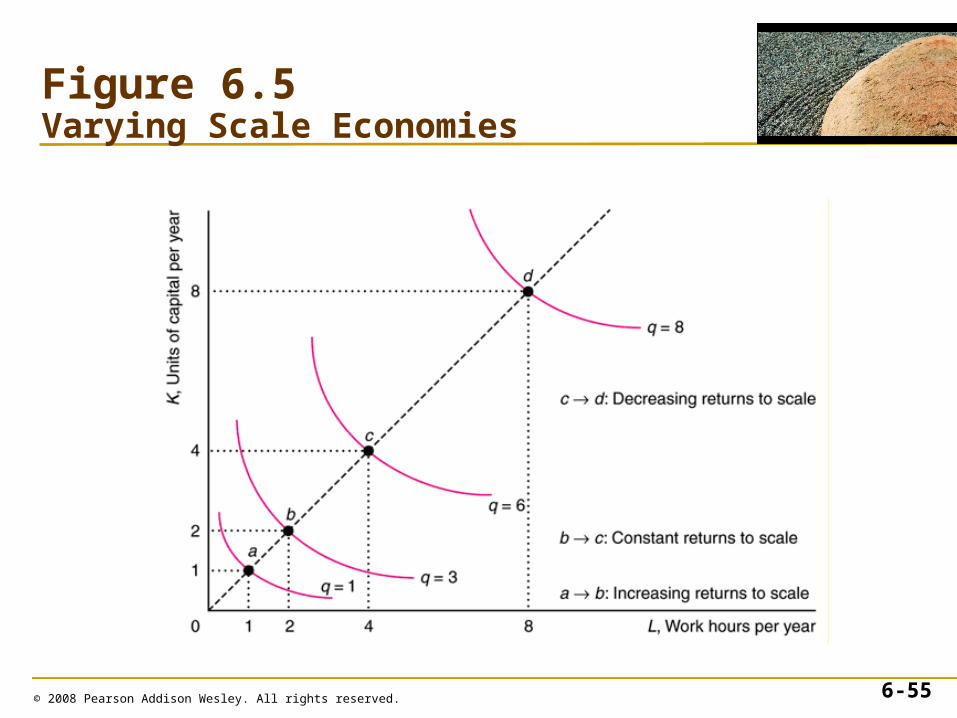

Figure 6.5Varying Scale Economies

Varying Returns to Scale

• Many production functions have increasing returns to scale for small amounts of output, constant returns for moderate amounts of output, and decreasing returns for large amounts of output.

• The spacing of the isoquants reflects the returns to scale.

© 2008 Pearson Addison Wesley. All rights reserved. 6-56

Productivity and Technical Change

• Relative Productivity–We can measure the relative productivity of a firm by expressing the firm’s actual output, q, as a percentage of the output that the most productive firm in the industry could have produced, q*, from the same amount of inputs: 100q/q*.

© 2008 Pearson Addison Wesley. All rights reserved. 6-57

Innovations

• Technical Progress–an advance in knowledge that allows more output to be produced with the same level of inputs

• Neutral Technical Progress

- The firm can produce more output using the same ratio of inputs.

q = A(t)f(L, K)© 2008 Pearson Addison Wesley. All rights reserved. 6-58

© 2008 Pearson Addison Wesley. All rights reserved. 6-59

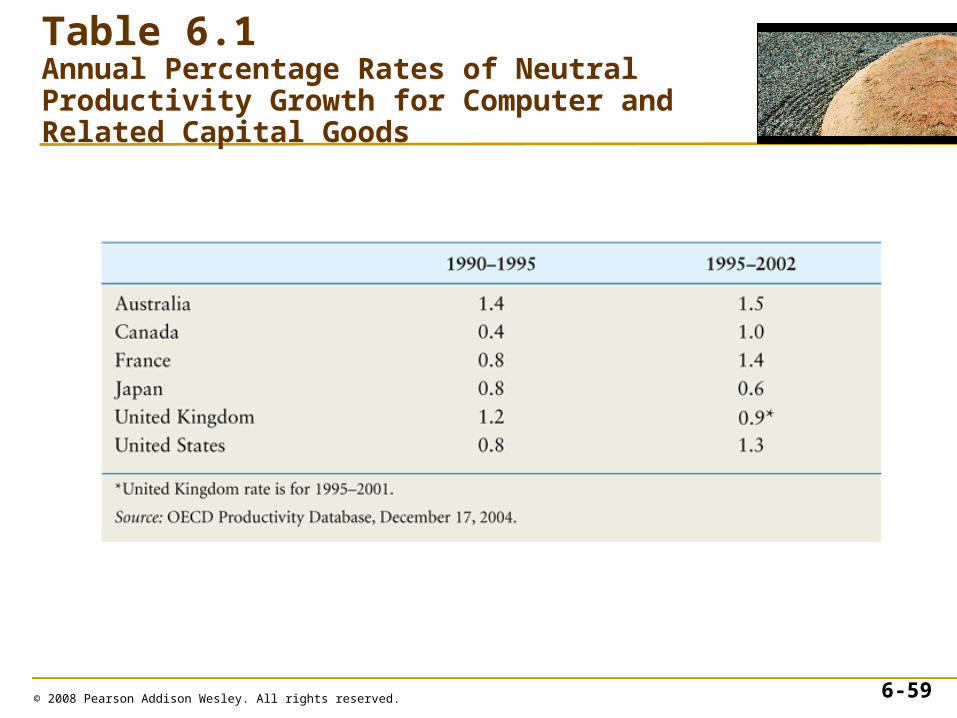

Table 6.1Annual Percentage Rates of Neutral Productivity Growth for Computer and Related Capital Goods

Innovations

• Nonneutral technical changes are innovations that alter the proportion in which inputs are used.

• Labor saving innovation: The ratio of labor to the other inputs used to produce a given level of output falls after the innovation.

© 2008 Pearson Addison Wesley. All rights reserved. 6-60

Organizational Change

• Organizational changes may also alter the production function and increase the amount of output produced by a given amount of inputs.

© 2008 Pearson Addison Wesley. All rights reserved. 6-61