Embed Size (px)

Citation preview

© 2005 Towers Perrin 1

Medical Malpractice Overview

Financial Update

Claim Trends and Observations

Market Realities

PLUS Medical PL Symposium

March 16, 2005

March 16, 2005

James D. Hurley ACAS, MAAA

© 2005 Towers Perrin

Medical Malpractice – Financial Update

This document is incomplete without the accompanying discussion; it is confidential and intended solely for the information and benefit of the immediate recipient hereof.

3© 2005 Towers Perrin

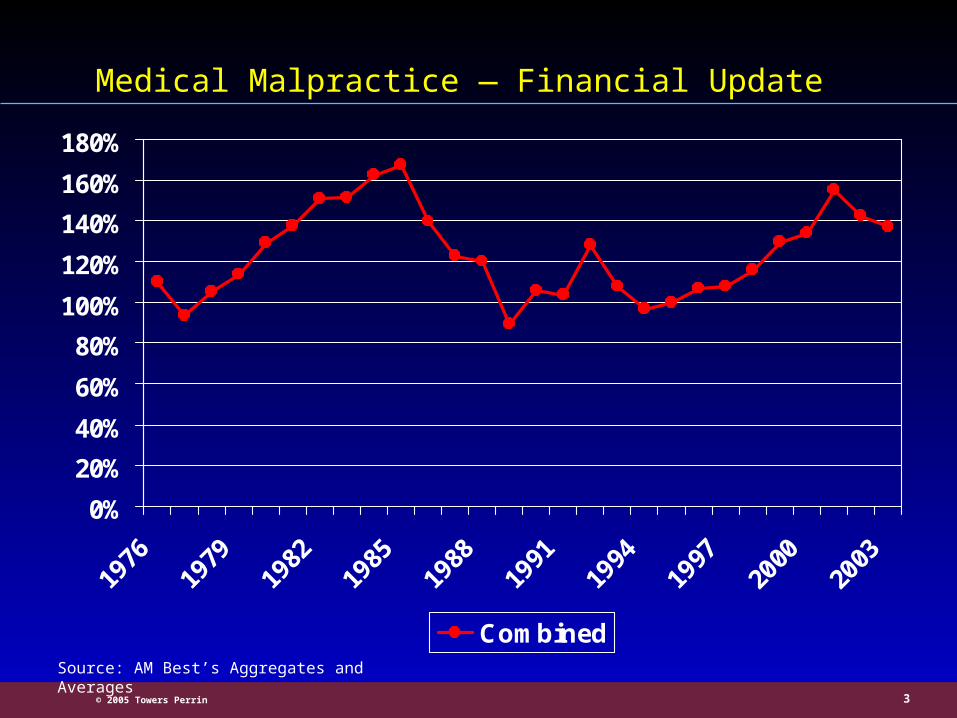

Medical Malpractice — Financial Update

Source: AM Best’s Aggregates and Averages

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Combined

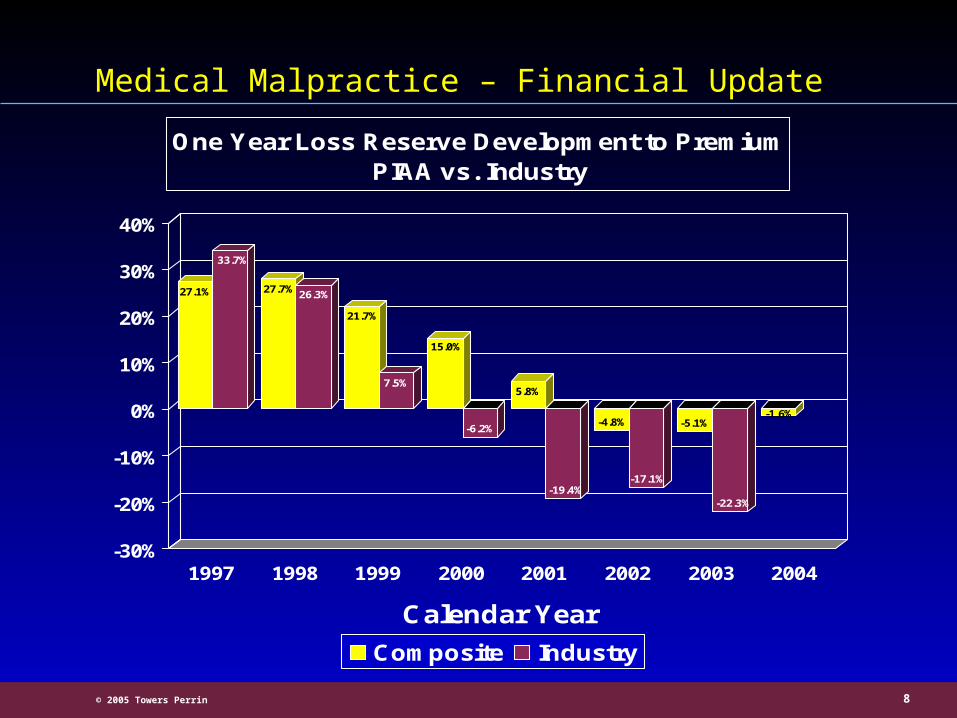

4© 2005 Towers Perrin

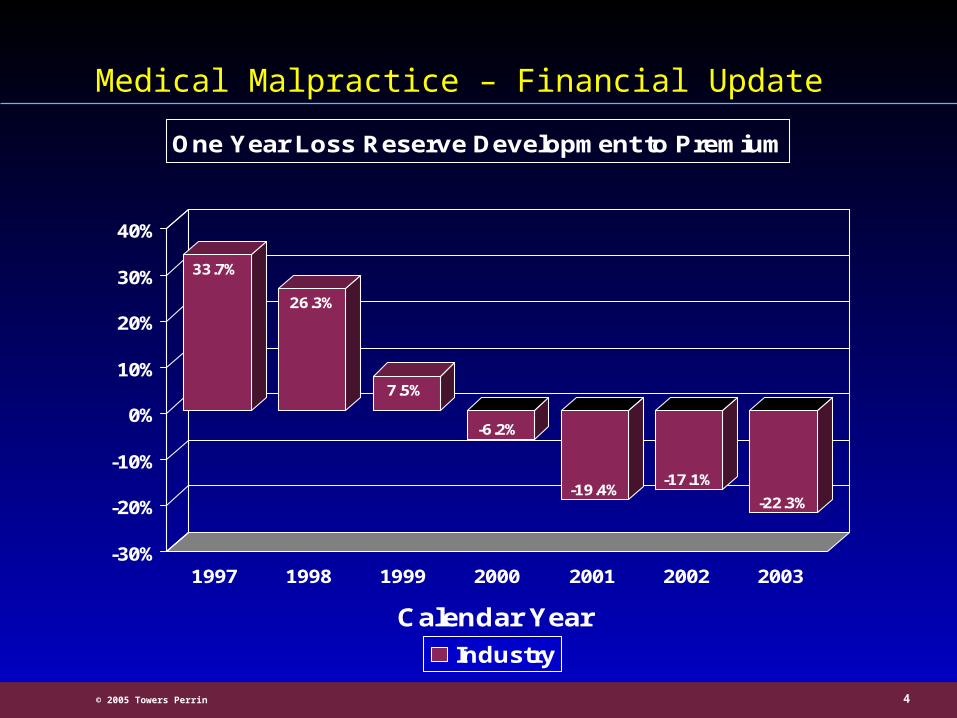

Medical Malpractice – Financial Update

33.7%

26.3%

7.5%

-6.2%

-19.4%-17.1%

-22.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1997 1998 1999 2000 2001 2002 2003

Calendar Year

One Year Loss Reserve Development to Premium

Industry

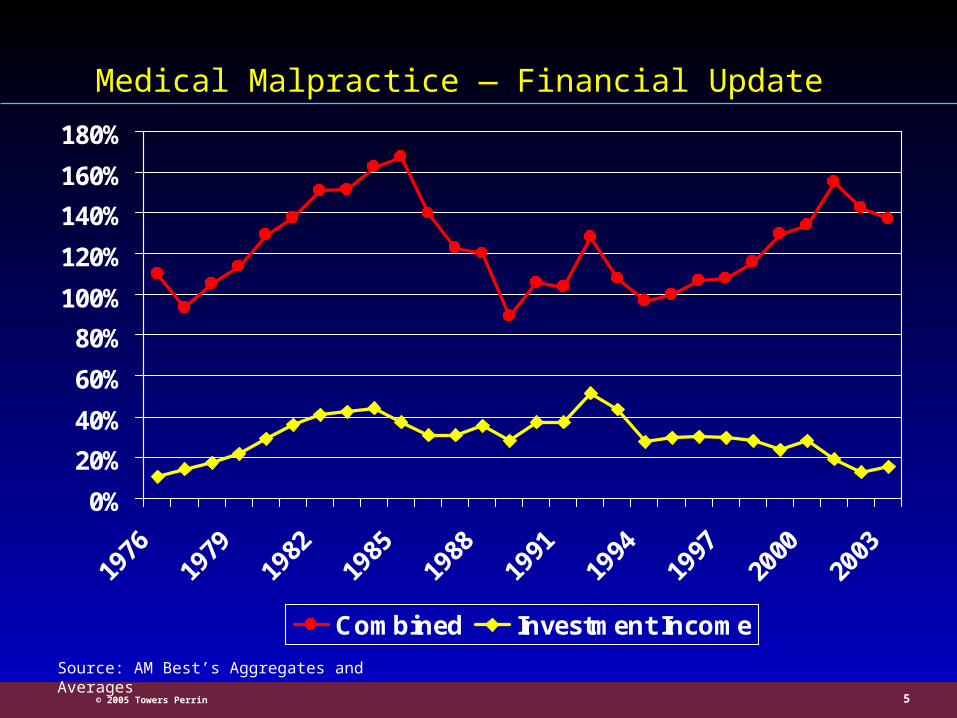

5© 2005 Towers Perrin

Medical Malpractice — Financial Update

Source: AM Best’s Aggregates and Averages

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Combined Investment Income

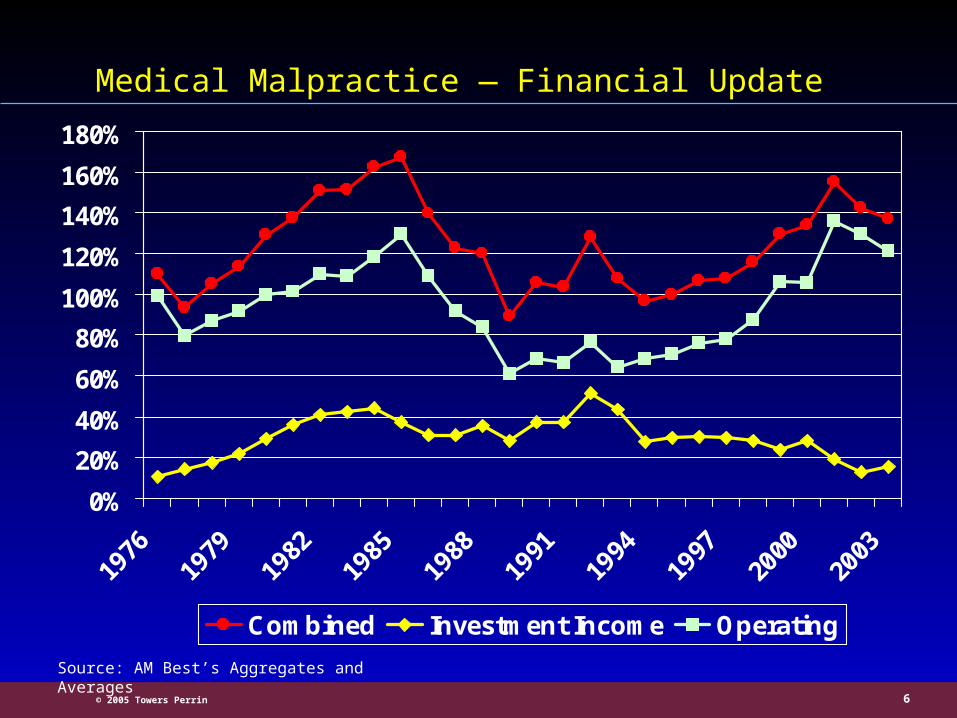

6© 2005 Towers Perrin

Medical Malpractice — Financial Update

Source: AM Best’s Aggregates and Averages

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Combined Investment Income Operating

7© 2005 Towers Perrin

Medical Malpractice — Financial Update

Messages

Financial results – a work in progress

Underwriting Combined ratio still too high

— Best says 130% for 2004 and 2005— Composite of 30 companies ≈ 110% for 2004

Rate increases still to be ‘felt’ Question is reserves

8© 2005 Towers Perrin

Medical Malpractice – Financial Update

27.1%

33.7%

27.7% 26.3%

21.7%

7.5%

15.0%

-6.2%

5.8%

-19.4%

-4.8%

-17.1%

-5.1%

-22.3%

-1.6%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1997 1998 1999 2000 2001 2002 2003 2004

Calendar Year

One Year Loss Reserve Development to PremiumPIAA vs. Industry

Composite Industry

9© 2005 Towers Perrin

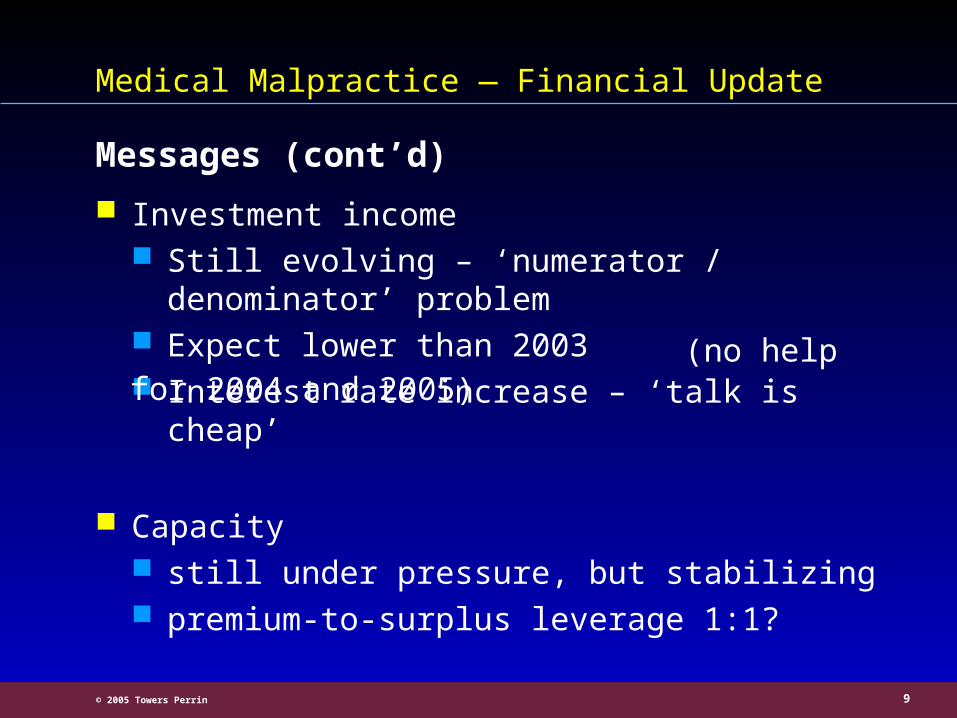

Medical Malpractice — Financial Update

Messages (cont’d)

Investment income Still evolving – ‘numerator / denominator’ problem Expect lower than 2003 Interest rate increase – ‘talk is cheap’

Capacity still under pressure, but stabilizing premium-to-surplus leverage 1:1?

(no helpfor 2004 and 2005)

Medical MalpracticeTrends and Observations

Raymond BirkinshaGE Insurance SolutionsMarch 16, 2005

11 GE Insurance SolutionsRaymond BirkinshaMarch 2005

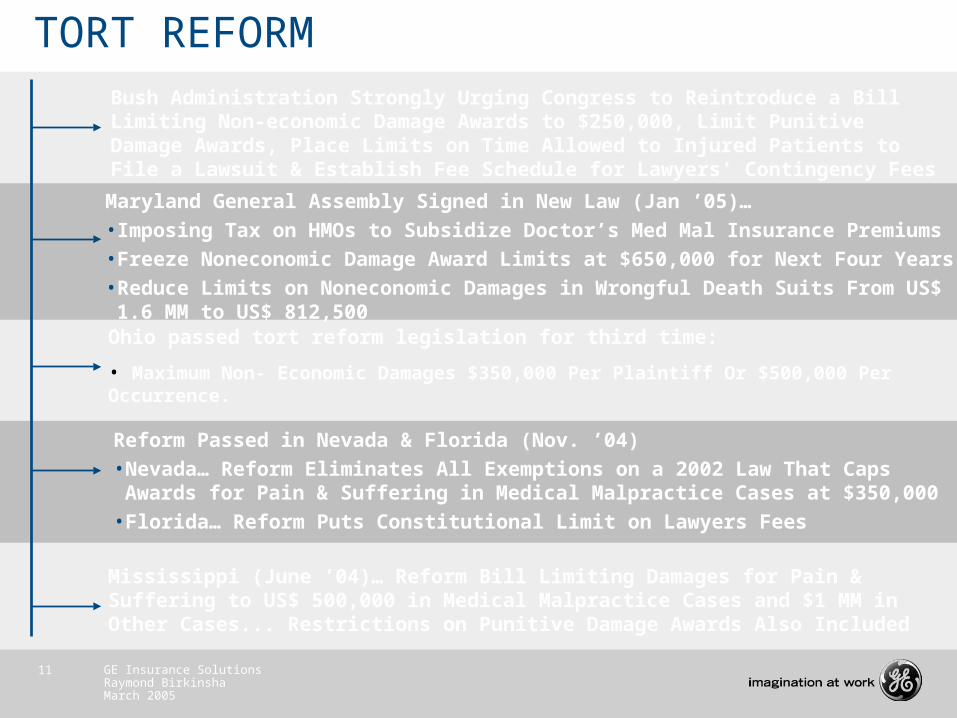

TORT REFORMBush Administration Strongly Urging Congress to Reintroduce a Bill Limiting Non-economic Damage Awards to $250,000, Limit Punitive Damage Awards, Place Limits on Time Allowed to Injured Patients to File a Lawsuit & Establish Fee Schedule for Lawyers’ Contingency Fees

Reform Passed in Nevada & Florida (Nov. ’04) • Nevada… Reform Eliminates All Exemptions on a 2002 Law That Caps Awards for Pain

& Suffering in Medical Malpractice Cases at $350,000• Florida… Reform Puts Constitutional Limit on Lawyers Fees

Maryland General Assembly Signed in New Law (Jan ’05)…• Imposing Tax on HMOs to Subsidize Doctor’s Med Mal Insurance Premiums• Freeze Noneconomic Damage Award Limits at $650,000 for Next Four Years• Reduce Limits on Noneconomic Damages in Wrongful Death Suits From US$ 1.6 MM to

US$ 812,500Ohio passed tort reform legislation for third time:

• Maximum Non- Economic Damages $350,000 Per Plaintiff Or $500,000 Per Occurrence.

Mississippi (June ’04)… Reform Bill Limiting Damages for Pain & Suffering to US$ 500,000 in Medical Malpractice Cases and $1 MM in Other Cases... Restrictions on Punitive Damage Awards Also Included

12 GE Insurance SolutionsRaymond BirkinshaMarch 2005

APPEAL BONDS

The Issue: Insolvent Carriers leading to Bond Issues

The Solution: Caps on Bonds

• GEORGIA $25,000,000 • VIRGINIA $25,000,000 • NEBRASKA 50% or $50,000,000• IOWA $100,000,000 • MINNESOTA $100,000,000• SOUTH CAROLINA NO BOND!

13 GE Insurance SolutionsRaymond BirkinshaMarch 2005

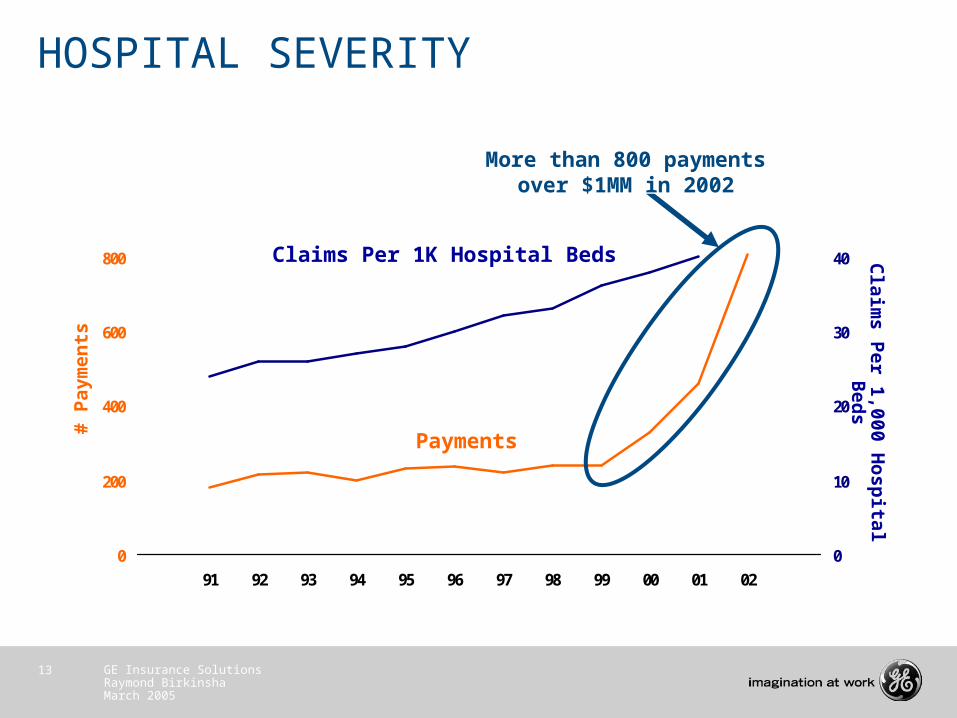

0

200

400

600

800

91 92 93 94 95 96 97 98 99 00 01 02

0

10

20

30

40

# P

aym

ents

Source: National Practitioners Data Bank Public Use Files; AON HealthLine Special Edition 2003

Claim

s P

er 1 ,0 00 Ho

sp

i ta l Be d

s

Claims Per 1K Hospital Beds

Payments

More than 800 paymentsover $1MM in 2002

HOSPITAL SEVERITY

14 GE Insurance SolutionsRaymond BirkinshaMarch 2005

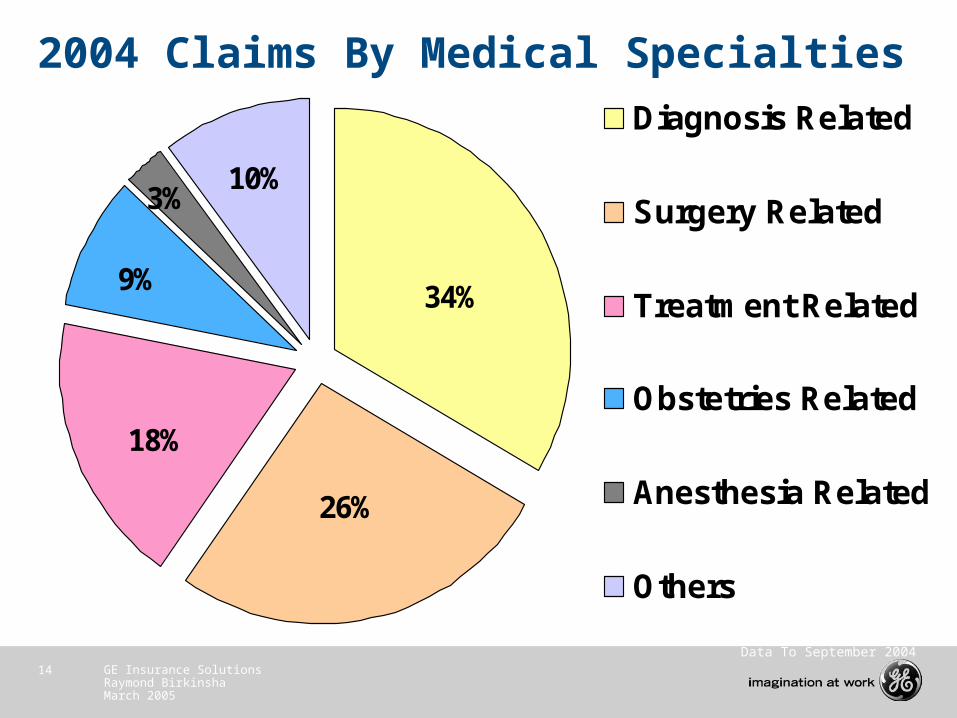

2004 Claims By Medical Specialties

3%10%

26%

34%

18%

9%

Diagnosis Related

Surgery Related

Treatment Related

Obstetries Related

Anesthesia Related

OthersSource: National Practitioner Data Bank Public Use File - Data To

September 2004

15 GE Insurance SolutionsRaymond BirkinshaMarch 2005

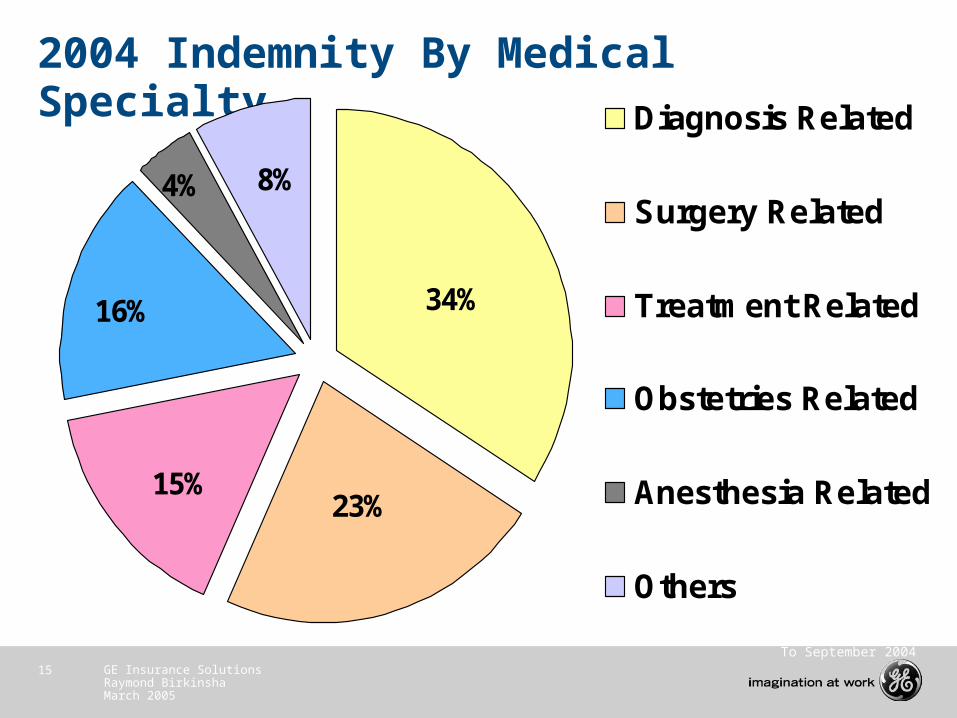

2004 Indemnity By Medical Specialty

4% 8%

23%

34%

15%

16%

Diagnosis Related

Surgery Related

Treatment Related

Obstetries Related

Anesthesia Related

OthersSource: National Practitioner Data Bank Public Use File - Data To September

2004

16 GE Insurance SolutionsRaymond BirkinshaMarch 2005

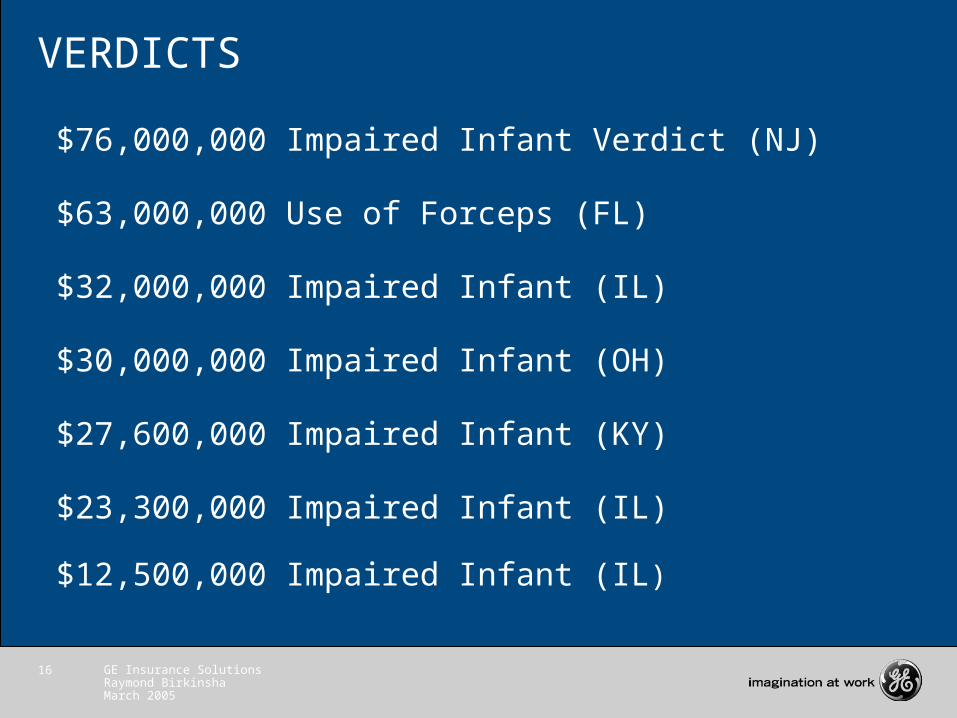

VERDICTS

$76,000,000 Impaired Infant Verdict (NJ)

$63,000,000 Use of Forceps (FL)

$32,000,000 Impaired Infant (IL)

$30,000,000 Impaired Infant (OH)

$27,600,000 Impaired Infant (KY)

$23,300,000 Impaired Infant (IL)

$12,500,000 Impaired Infant (IL)

17 GE Insurance SolutionsRaymond BirkinshaMarch 2005

SETTLEMENTS

$15,000,000 Hypoxic Birth Injury

$17,250,000 Failure to Monitor Anticoagulation

$18,000,000 Pre-eclampsia Allegations

$20,000,000 Brain Injury Post Surgery

$20,000,000 Failure to Perform C-Section

$35,000,000 Birth Trauma – Brain Injury

18 GE Insurance SolutionsRaymond BirkinshaMarch 2005

PLAINTIFF’S SUCCESS

Developed Plaintiff’s Models

Focus on Emotion

No Incentive To Settle

Less Cooperation

Value of Money

19 GE Insurance SolutionsRaymond BirkinshaMarch 2005

• Jury Selection

• Mock Trials

• Trial Consultants

• Sophisticated Evidence and Exhibits

RESOURCES

20 GE Insurance SolutionsRaymond BirkinshaMarch 2005

THE NURSING HOME MODEL

Surveys

Ex-Employees

Medical Chart

Loss of Dignity

21 GE Insurance SolutionsRaymond BirkinshaMarch 2005

TRENDS

FEWER PLAYERS

MORE INSOLVENCY ISSUES

LARGER RETENTIONS

RESTRICTIVE COVERAGE

TORT REFORM

22 GE Insurance SolutionsRaymond BirkinshaMarch 2005

RECOMENDATIONS

Support Tort Reform

Professional Claim Analysts

Identify the Big Cases

Evaluate Cases Early

23 GE Insurance SolutionsRaymond BirkinshaMarch 2005

RECOMENDATIONS

See Resolution as a Process

Engage Appropriate Resources Counsel Experts Trial Resources Witness Coaches

March 16, 2005 James D. Hurley ACAS, MAAA 24Leadership. Innovation.Results.

INSURING THE FINANCIAL HEALTH OF HEALTHCARE PROVIDERS

Gallagher Healthcare

Medical MalpracticeMarket Realities

Philip E. Reischman

Gallagher Healthcare Insurance Services, Inc.

March 16, 2005

Leadership.Innovation.Results.

25

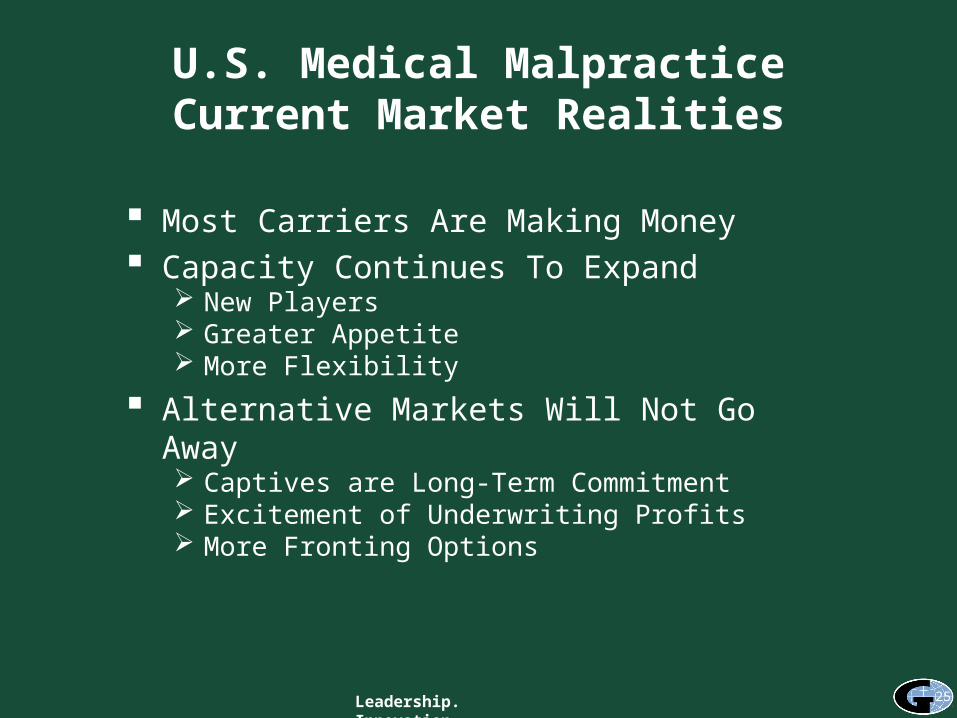

U.S. Medical MalpracticeCurrent Market Realities

Most Carriers Are Making Money Capacity Continues To Expand

New Players Greater Appetite More Flexibility

Alternative Markets Will Not Go Away Captives are Long-Term Commitment Excitement of Underwriting Profits More Fronting Options

Leadership.Innovation.Results.

26

U.S. Medical MalpracticeCurrent Market Realities

Some Start-Ups Will Fail Low Volume Expense Ratios

Carrier Ratings Are Still A Concern Downgrades Flight To Quality

Tort Reform And Risk Management Are Driving Rate Decreases

Contingent Commissions Not Material

Leadership.Innovation.Results.

27

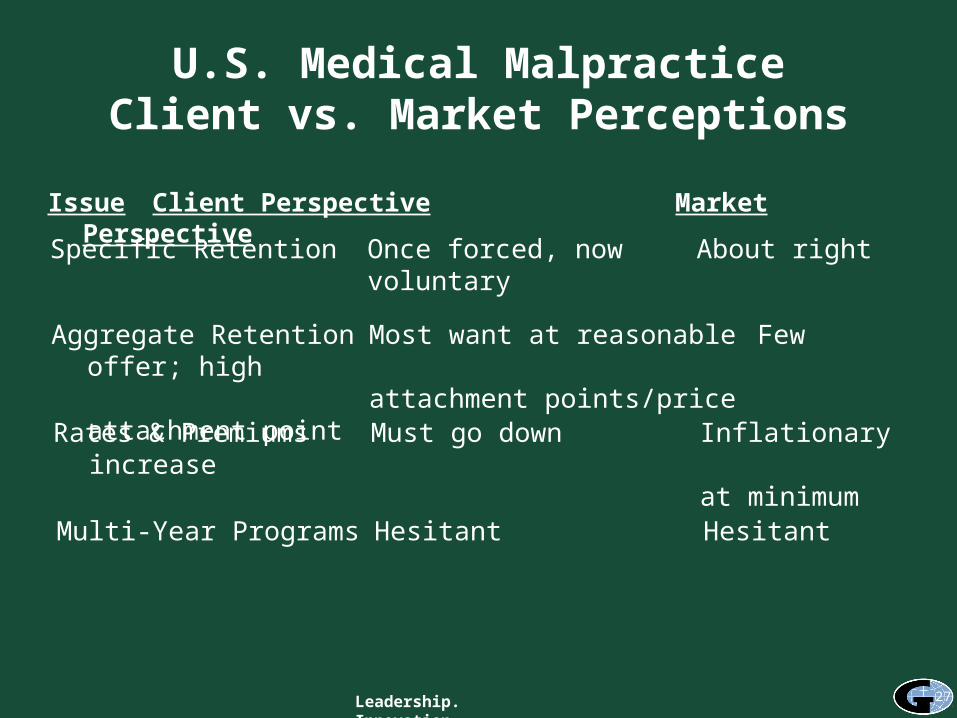

U.S. Medical MalpracticeClient vs. Market Perceptions

Issue Client Perspective Market PerspectiveSpecific Retention Once forced, now About right

voluntary

Aggregate Retention Most want at reasonable Few offer; highattachment points/price attachment point

Rates & Premiums Must go down Inflationary increase

at minimumMulti-Year Programs Hesitant Hesitant

Leadership.Innovation.Results.

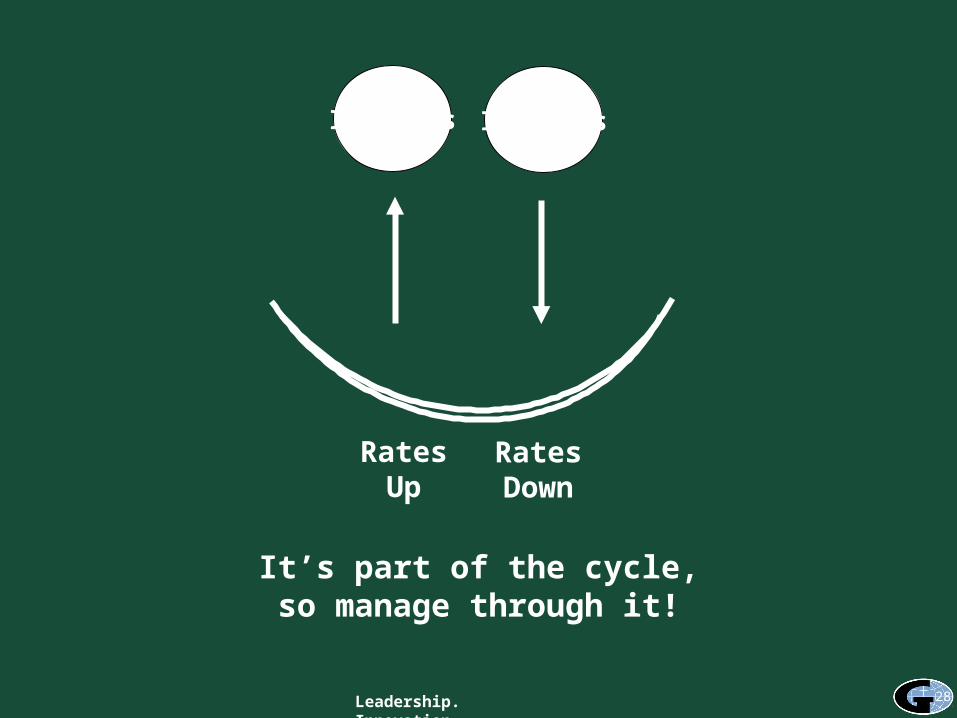

28

Insureds

RatesDown

RatesUp

Insurers

It’s part of the cycle,so manage through it!

Questions?