Embed Size (px)

Citation preview

This report is solely for the use of Zinnov Client and Zinnov Personnel. No Part of it may be quoted, circulated or reproduced for distribution outside

the client organization without prior written approval from Zinnov.

Zinnov Zones -2016Product Engineering Services

December, 2016

Global Engineering R&D Landscape

Key Trends in Global Engineering & RD Services

Zinnov Zones – 2016 Rating

$621 Billion G500 R&D spend in 2016

Global Engineering R&D Landscape

Key Trends in Global Engineering & RD Services

Zinnov Zones – 2016 Rating

Companies from the Consumer / eWeb 2.0 & E-Commerce vertical have significantly increased their R&D spending

Automotive

$ 107 BN

Top R&D Spenders

Consumer

Electronics

$ 45 BN

USD 621 Billion

Volkswagen -6% 3%

Toyota Motor -6% 10%

General

Motors1% 1%

Robert

Bosch

18%

29%

Ford Motor -3% -3%

Samsung

Electronics-3% 0%

Apple 34% 34%

LG 3% 7%

Sony -15% 0%

Panasonic -19% -4%

Y% -Constant Currency Growth rates from 2015X% -Growth Rates in USD from 2015

X%

Y%

% Increase in R&D spend over 2015

% decrease in R&D spend over 2015

No change in R&D spend from 2015Z%

4%

4

Aerospace &

Defense

$ 27 BN

Airbus Group -7% 2%

Boeing 9% 9%

Safran -3% 6%

BAE Systems -8% -6%

Finmeccanica -13% -5%

Computer

Peripherals &

Storage

$ 20 BN

Hewlett-

Packard2% 2%

EMC 6% 6%

Canon 5% 6%

HP Enterprise 5% 5%

Western Digital -1% -1%

Software / Internet

$ 88 BN

Medical

$ 21 BN

Medtronic 11% 11%

Boston

Scientific7% 7%

Thermo

Fisher

Scientific

0% 0%

St Jude

Medical-2% -2%

Becton

Dickinson15% 15%

Semiconductor

$ 49 BN

Intel 5% 5%

Qualcomm 0% 0%

Taiwan

Semiconductor15%15%

Foxconn

Technology7% 7%

Mediatek 14%14%

Telecom &

Networking

$ 43 BN

Huawei

Technologies44% 46%

Cisco Systems -1% -1%

Ericsson -11% 4%

Nokia 9% 19%

ZTE 34% 35%

Energy &

Utilities

$ 21 BN

Amazon 35% 35%

Alphabet 25% 25%

Facebook 81% 81%

Microsoft 6% 6%

Oracle 12% 12%

Source: Global Engineering Insights Platform (GEIP) |

Petrochina -11% -9%

Schlumberg

er-10% -10%

Dutch Shell -11% -11%

Total -21% -21%

Exxon Mobil 4% 4%

18%4% 11% 5%4%7% 4.5% 4%

Growth rates reported in constant

currency

Global Engineering R&D Landscape – And equally diverse ecosystem

$ 621 B

5Source: Global Engineering Insights Platform (GEIP) |

27%

10%

84%

85%

6%60%

100%

90%

67%

87%3%

3%

93%

30%

2%

6%

3%13%

12%

1%

100%

10%

8%

Automotive Aerospace ComputerPeripherals

ConsumerElectronics

Energy & Utilities Software/Internet Medical Devices Semiconductors Telecom

Embedded Mechanical Software

$ 107 BN

$ 45 BN

$ 27 BN

$ 20 BN

$ 88 BN

$ 21 BN

$ 49 BN

$ 43 BN

$ 21 BN

Vertical Top Spender Highest Growth in R&D Spend

Automotive VolkswagenTesla Motors (54%), ZF Group(48%)

Chongqing Changan(26%)

Industrial 3MFanuc(30%), Metallurgical corp. of china(26%),

Arkema(23%)

Consumer

ElectronicsSamsung

Sega Sammy(44%), Apple(34%), BSH

Bosch(24%)

Medical

DevicesMedtronic

Zimmer(43%), Fresenius(15%),

Becton Dickinson(15%)

Semiconductor IntelCypress Semicon(75%), Cirrus Logic (57%),

Avago Technologies(51%)

TelecomHuawei

Technologies

Harris(254%), Huawei Technologies(44%),

Telecom Italia(39%)

ISV AmazonAlibaba (108%), Cerner(87%),

JD.com(82%)

Source: Zinnov Research and Analysis

3.4%

6.2%

4.8%

4.2%

5.9%

11.2%

5.3%

12.8%

Industrial

Medical Devices

Aerospace and

Defence

Automotive

Telecommunication

Semiconductor

Consumer

Electronics

ISV

R&D Spend as Percentage of Revenue ( USD Billion)

Top R&D spenders

are from

Automotive vertical

5

20Hi-Tech and ISV

segments share in

G500 spenders

34%

China’s R&D Growth

rate is more than 2x of

USA’s R&D growth rate

16% 8%

Star Spenders

Hi-Tech Verticals

Increased demand for embedded and software content is driving the R&D spend

7

602 614 621

4.13%4.31%

4.95%

Total Global 500 R&D Spend X% R&D Spend as a % of revenue

G500 R&D Spend(In USD billion) 146

Billion Dollar Spenders in

2016

35New Entrants

42High Growth* R&D

Spenders

4.95%Average R&D Spend

as % of Revenue

• The R&D spending by the Billion Dollar spenders

totalled up to USD 471 Billion

• Five new companies have entered the billion dollar

R&D spender club this year

• Majority of the new entrants were from Industrial

and Semiconductor verticals

• 5 companies within G500 got acquired, 12

companies reduced their R&D spend and 2

companies went Private and left the list

• Nearly 40% of the high growth R&D spenders

were from Consumer/Web 2.0 & E-Commerce,

Enterprise Software and Semiconductor verticals

• Companies from verticals like Consumer/Web 2.0

& E-Commerce, Semiconductor and Enterprise

Software & Enterprise 2.0 have R&D intensities

greater than 10% while Energy & Utility firms have

R&D intensities less than 1%

Note: *High Growth R&D Spenders are companies that increased their R&D spend by 30% or more over previous year

*The Revenues of the top companies from Energy and Utility have substantially gone down without much increase in their R&D spent, hence the surge in R&D Intensity

2014 2015 2016

R&D spend by G500 companies is growing consistently at ~1.5% over the last two years

0.2

1.2

2.2

3.2

4.2

5.2

6.2

7.2

8.2

9.2

10.2

11.2

12.2

13.2

1 101 201 301 401

Contribution of G500 R&D Spenders

2016 R&D Spend Ranking

66.5%

16.4%

8.4%5.2% 3.5%

R&

D S

pen

d in

Billio

n

621 Billion8

R&D spending continues to stay highly consolidated with top 100 R&D spenders accounting for two-third of the total R&D Spend

Source: Zinnov Research and Analysis

61%

40%

76%

38%

28%41%

49% 54% 59%

39%

60%

24%

62%72%

59%51% 46% 41%

Aerospace

& Defense*

Automotive Consumer Electronics Energy &

Utilities

Industrial

Automation

Medical

Devices

Semiconductors Software/

Internet

Telecom &

Networking

Contribution of top 5 companies to R&D spend in each vertical

*Excludes Government spending on Defence; Source: Zinnov Research and Analysis

19 61 24 28 46 23 43 61 28

Total number of G500 companies in each vertical

14

R&D spending in Consumer Electronics and Aerospace is highly consolidated with top 5 players accounting for >60% total vertical R&D Spending

Source: Zinnov Research and Analysis

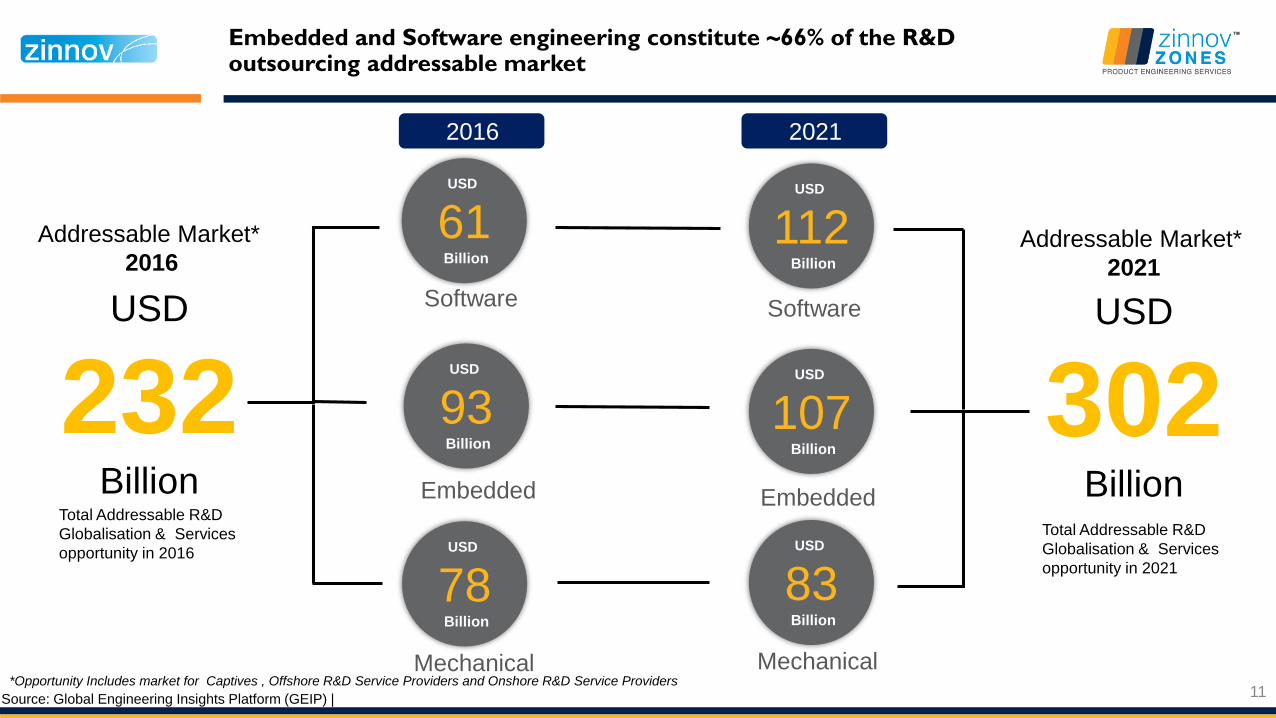

The addressable Engineering and R&D globalization and services opportunity stands at USD 215 billion

Current Addressed ER&D market through

offshore in-house R&D Centres

Addressed ER&D Globalisation & Services

market through Outsourcing partners

*Opportunity Includes market for Captives , Offshore R&D Service Providers and Onshore R&D

Service Providers

USD

232Billion

Addressable Market*

Total Addressable R&D

Globalisation & Services

opportunity

USD

85Billion

Total Addressed R&D Globalisation

and Services Market

USD

34Billion

USD

51Billion

Addressed Market

*Opportunity Includes market for Captives , Offshore R&D Service Providers and Onshore R&D Service Providers

USD

61Billion

SoftwareUSD

232Billion

Total Addressable R&D

Globalisation & Services

opportunity in 2016 USD

78Billion

USD

93Billion

Embedded

Mechanical

USD

112Billion

USD

107Billion

USD

83Billion

2021

USD

302Billion

Total Addressable R&D

Globalisation & Services

opportunity in 2021

Addressable Market*

2016Addressable Market*

2021

Software

Embedded

Mechanical

Embedded and Software engineering constitute ~66% of the R&D outsourcing addressable market

11Source: Global Engineering Insights Platform (GEIP) |

2016

India, Western Europe and North America capture ~75% of the global Engineering R&D Services market

8.9 BN

7.0 BN19.5 BN

3.0 BN

10.4 BN

India

Eastern

Europe

Western Europe

North

America

R&D Outsourcing HotspotsEngineering R&D

Outsourced Services

Addressed ER&D Globalisation & Services

market through Outsourcing partners

Billion

USD

9.3% Growth Rate over 2015

Latin

America

2.2 BN

Rest of

Asia

51

$7.9 Bn $8.9 Bn

$15.1 Bn$12.25 Bn $13.4 Bn

$22.4 Bn

FY 2015 FY 2016 FY 2020

Service

Providers

In-house

R&D CentersService

Providers

In-house

R&D Centers

Service

Providers

In-house

R&D Centers

Product Engineering Services Growth Rate ( In USD Billions)

FY 2015 FY 2016 FY 2020(E)

11% 13.7%

Growth rateGrowth rate

(Expected)USD

20.1 Billion

USD

22.3Billion

USD

37.5Billion

India’s ER&D globalization and services market is expected to reach $38 Billion by 2020

9.4%

12.7% 13.97%

13.3%

R&D Globalization as a phenomenon is here to stay with locations in emerging economies being the hotspot

13.4 Bn

India

10.2 Bn

China

2.3 Bn

South Africa

3.2 Bn

Brazil

1.5 Bn

Eastern

Europe

G500 globalisation intensity

Billion

USD

Overall R&D Globalisation in

Emerging Economies

8.6%

Growth Rate over 2015

34

Global Engineering R&D Landscape

Engineering Services

is getting re-definedKey Trends in Global Engineering & RD Services

Zinnov Zones– 2016 Rating

Key trends in Global

Engineering

R&D

Services

The drivers for outsourcing have changed tremendously over the last year and some newer trends have emerged

12

Service Providers strengthen Bay Area delivery presence to position as innovation

partner to bay area based R&D spenders4

3 Emergence of End-to-End Full stack Product Engineering Service providers

Rise of the GlobalShore model: Engineering Services Delivery becoming more global with

offshore players expanding to onshore delivery locations and Europe ESPs building offshore

presence

R&D Service providers explore engineering opportunities beyond Product Development Life Cycle (PDLC)

activities

Global Engineering R&D Landscape

Engineering Services

is getting re-definedKey Trends in Global Engineering & RD Services

Zinnov Zones – 2016 Rating

Specialization, R&D practice maturity (depth and maturity services), Innovation & IP, Eco-System Linkages

Niche

Expansive

EstablishedEmerging

Sca

le, #

of

Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

Partial Participation by Service Providers

Complete Participation by Service Provider

Overall Rating - 2016

TCS

WiproHCLAltran

L&T TSTech Mahindra

Cyient

HARMAN Connected ServicesInfosys

Aricent QuEST GlobalMindtree

Global Logic

CognizantTata Technologies

Tata Elxsi

Sasken eInfochips

EPAM

Persistent SystemsCybage

Luxoft

Ness Digital Engineering

Genpact

GlobalEdge

KPIT Technologies

Pactera

Sonata Software

Infogain

Happiest MindsInnominds

Hughes Systique

Aspire Systems

*Capgemini

R Systems

Xoriant

ITC Infotech

Talentica

Akka TechAssystem

Alten

Specialization, R&D practice maturity (depth and maturity services), Innovation & IP, Eco-System Linkages

Niche

Expansive

EstablishedEmerging

Sca

le, #

of

Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

Partial Participation by Service Providers

Complete Participation by Service Provider

Mechanical Engineering Services Ratings - 2016

Altran

TCSTech Mahindra

QuEST GlobalCyient

AltenAkka

Assystem

HCL

Tata Technologies

InfosysL&T TS

Wipro

Genpact

KPIT Technologies

Tata Elxsi

HARMAN Connected Services

*Capgemini

Specialization, R&D practice maturity (depth and maturity services), Innovation & IP, Eco-System Linkages

Niche

Expansive

EstablishedEmerging

Sca

le, #

of

Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

Partial Participation by Service Providers

Complete Participation by Service Provider

Embedded Systems Rating - 2016

WiproHCL

TCS

L&T TS

Tech Mahindra

HARMAN Connected ServicesAricent

Alten

Altran

Tata Elxsi

Infosys

Mindtree

eInfochips

KPIT Technologies

Sasken

Global Logic

QuEST Global

Cognizant

Global Edge

Pactera

Tata Technologies

Innominds

Happiest Minds

EPAM

Hughes Systique

*Capgemini

R Systems

ITC Infotech

Cyient

Luxoft

Aerospace Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service ProvidersSc

ale

, # o

f Su

b-V

erti

cals

ser

vice

d, C

lien

t Sp

rea

d

ITC Infotech

Partial Participation by Service ProviderAkka Tech

Atkins

SOFT LAUNCH

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

Alten

Assystem

P3

Bertrandt

Altran

Cyient

Tech Mahindra

QuEST Global

*Capgemini

HCL

TCS

L&T TS

Tata Technologies

Genpact

Wipro

eInfochipsTata Elxsi

Infosys

Automotive Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

Sasken

Happiest Minds

Global LogicGlobal Edge

ITC Infotech

Hughes Systique

Ness Digital Engineering

Innominds

Partial Participation by Service Provider

AkkaTechnologies

Assystem

Alten

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Neusoft

BertrandtESG Automation

IAV

TCS

Altran

HARMAN Connected

Services

L&T TS

*Capgemini

HCLTech

MahindraTata Elxsi

Wipro

Tata Technologies

Aricent

KPIT Technologies

Mindtree

Infosys

QuEST Global

Luxoft

Computer Peripherals and Storage Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

ITC Infotech InnomindsSca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Wipro

TCS

*Capgemini

HCL

HARMAN Connected Services

EPAM

Happiest Minds

Infosys

Construction and Heavy Machinery Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service ProvidersSc

ale

, # o

f Su

b-V

erti

cals

ser

vice

d, C

lien

t Sp

rea

d

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

L&T TS

TCS

Tata Technologies

Cyient

EPAM

Wipro

*Capgemini

Tech Mahindra

HCL

Innominds

Infosys

Consumer Electronics Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service ProvidersSc

ale

, # o

f Su

b-V

erti

cals

ser

vice

d, C

lien

t Sp

rea

d

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Partial Participation by Service Provider

Alten

Vault

Solize GroupWipro

HCL

TCS

Tata Elxsi

HARMAN Connected Services

Tech Mahindra

Mindtree

L&T TS

Sasken

AricentCyient

Happiest Minds

GlobalLogic

R Systems

Ness Digital Engineering

Hughes Systique

Innominds

Cognizant

Infosys

EPAM

Energy & Utilities Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

Wipro

TCS

Tech Mahindra

L&T TS

Altran

QuEST Global

Cyient

*Capgemini

Genpact

EPAM

ITC Infotech

Happiest Minds

Alten

Partial Participation by Service Provider

Infosys

HARMAN Connected

Services

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Atkins

P3

Innominds

Industrial Automation Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service ProvidersSc

ale

, # o

f Su

b-V

erti

cals

ser

vice

d, C

lien

t Sp

rea

d

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Partial Participation by Service Provider Alten

Beyondsoft

Sii Poland

L&T TSAltran

*Capgemini

TCSWipro

HCL

Tech Mahindra

Aricent

Cognizant

QuEST Global

Innominds

ITC InfotechSasken

Ness Digital Engineering

Happiest Minds

Hughes Systique

EPAM

eInfochips

Infosys

HARMAN Connected Services

Medical Devices Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

EPAM

Tata Elxsi Tech Mahindra

HARMAN Connected Services

Global Logic

CyienteInfochips

GenpactInnomindsITC Infotech

AltenPartial Participation by Service Provider

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Akka Tech

Infinite Computer Solutions

*Capgemini

HCL

TCSAltran

Wipro

L&T TS

QuEST Global

Infosys

High

Low

Zinnov Zones – Leading Service Providers

HARMAN Connected Services

HCLPersistent Systems

EPAM

Global Logic

Mindtree

Cybage Cognizant

Sonata

Sasken

Aspire

Xoriant

Infogain

Aricent

InnomindsITC Infotech

Tech Mahindra

Capgemini

PacteraAltran

Happiest Minds

Ness Digital Engineering TCS

Infosys

Wipro

Scalability

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

Enterprise Software Rating - 2016

• Capable of performing concept to Go-To-Market for the product

• Formal innovation culture, resulting in IP’s and strategic innovations

• Worlds Largest ISVs

• Capable of delivering complete product development as a true engineering partner

• Reusable components IP’s built, and benefits quantified

• Large ISVs and Niche ISVs

• On the way into big league

• Innovation frameworks resulting in tangible benefit to customers

• Niche ISVs

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic ISVs, Startups

R&D Practice Maturity

Innovation

Customer Type

Nurture Zone

SOFT LAUNCH

Breakout Zone Execution Zone Leadership Zone

Accenture

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

HARMAN Connected

Services

HCL

Persistent Systems

Wipro

EPAMGlobal Logic

Mindtree Ness Digital Engineering

Cybage

Pactera

Cognizant

Sonata

Sasken

Aspire

Talentica

eInfochips

Happiest Minds Infogain

Aricent

Innominds

ITC Infotech

Infosys

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

Consumer Software Rating - 2016

• Capable of performing concept to Go-To-Market for the product

• Formal innovation culture, resulting in IP’s and strategic innovations

• Large Internet and Consumer ISVs

• Capable of delivering complete product development as a true engineering partner

• Reusable components IP’s built, and benefits quantified

• Large Internet and Consumer ISVs

• On the way into big league

• Innovation frameworks resulting in tangible benefit to customers

• Niche ISVs

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic ISVs, Startups

R&D Practice Maturity

Innovation

Customer Type

SOFT LAUNCH

Semiconductor Rating – 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service ProvidersSc

ale

, # o

f Su

b-V

erti

cals

ser

vice

d, C

lien

t Sp

rea

d

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

R&D Practice Maturity

Innovation

Eco-system Connect

SOFT LAUNCH

Partial Participation by Service Provider

Valuelabs

VVDN

Wipro

TCS

HARMAN Connected Services

Altran

Aricent

HCL

eInfochips

Sasken

Mindtree

L&T TSTata Elxsi

GlobalLogic

GlobalEdge

Cyient

Innominds

ITC Infotech

Happiest Minds

Infosys

Telecommunication Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

Wipro

Aricent

Tech MahindraTCS

Altran

HCL

Mindtree

L&T TS

HARMAN Connected Services

Sasken

Tata Elxsi

Pactera

Cognizant

R Systems

Global Edge

EPAM

Innominds

Happiest Minds

Hughes Systique

Alten

Partial Participation by Service Provider Infosys

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Infinite Computer Solutions

Sii Poland

GlobalLogic

Cyient

Luxoft

Transport Rating - 2016

High

Low

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Scalability

Zinnov Zones – Leading Service Providers

Partial Participation by Service Provider

Assystem

Akka Tech

Alten

Sca

le, #

of

Sub

-Ver

tica

ls s

ervi

ced

, Clie

nt

Spre

ad

• On the way into big league, delivering R&D services effectively, tear down , purpose fit labs

• Generic Capability across Engg, Embedded and Software services and Niche capability in one area

• Innovation frameworks resulting in tangible benefit to customers

• Specific industry alliances, partnerships and membership in Global forums

• R&D and PES as a focus area

• Niche capability in one type of PES service (Engineering / Embedded / Software)

• Innovation, if at all, in process optimization

• Generic - MoUs with universities and alliances

• Capable of performing concept to Go-To-Market for the product –Significant investment in Lab infrastructure

• Niche capability across Engineering, Embedded and Software services

• Formal innovation culture, resulting in IP’s and strategic innovations

• Leadership role in alliances, leverage startups, Specific academic research, and co-creation with customers

• Capable of delivering complete product development as a true engineering partner, Customer Labs

• Niche capability spans across two service types and at least generic capability level in one service type

• Reusable IP’s built, and benefits quantified

• Alliances with Customers who are Industry Leaders

R&D Practice Maturity

Breadth

Innovation

Eco-system Connect

SOFT LAUNCH

Atkins

Wipro

TCS

Tata Elxsi

Tech Mahindra

L&T TS

Altran

QuEST Global

Innominds

Ness Digital Engineering

Cyient

Infosys

Bangalore

69 "Prathiba Complex",

4th 'A' Cross,

Koramangala 5th Block,

Bangalore-560 095.

Phone: +91-80-41127925/6

Singapore

Level 42, Suntec Tower Three

8 Temasek Boulevard

Singapore 038988

Phone:+65 6829 2123

Texas

21, Waterway Ave

Suite 300

The Woodlands

TX-77380 USA

Phone:+1-281-362-2773

Beijing

Meilifang Tower 4, Entrance 4,

10/F #1003,

11 Beiyuan Shuangying Road,

Chaoyang District, Beijing

China 100012

Thank You

Gurgaon Office:

First Floor,

Plot no. 131, Sector 44,

Gurgaon-122002,

Phone: +91 124 4420100

California Office

3080 Olcott Street

Suite A125,

Santa Clara, CA 95054

Phone: +408-716-8432

![Sonata recognized in the Leadership zone for Software Product Engineering by Zinnov [Company Update]](https://img.pdfslide.us/doc/110x75/577ca6e21a28abea748c1429/sonata-recognized-in-the-leadership-zone-for-software-product-engineering-by.jpg)