Embed Size (px)

Citation preview

© 2016 LMC International. All rights reserved. www.lmc.co.uk

The reform of the EU sugar and HFS markets and its implications for the global starch sector

Mrs Sara Girardello – Head of Starch and High Intensity Sweetener Research5th Starch World Asia, 25‐27th January 2016

© 2016 LMC International. All rights reserved. January 2016

LMC International

LMC International is the leading independent economic and business consultancy for the agribusiness sector around the world.

From crops and agricultural commodities to agro-industrial products and downstream end-uses, we provide global business intelligence and market analysis on issues of production and demand, prices, including forecasts, trade and policy. Founded in 1980, the company has offices in:

We are entirely independent: we do not trade, broker, offer finance or produce any commodity, meaning that our analysis and advice is entirely objective.

• Oxford • New York • Singapore • Kuala Lumpur • Sao Paolo (partner)

2

© 2016 LMC International. All rights reserved. January 2016

Structure of the presentation

The world sugar market – Recent developments and outlook

The 2017 reform of the EU sugar and HFS sectors –Implications for the EU starch sector

The EU potato starch sector – Asia is the largest export market

The role of cassava starch in the EU –Opportunities for South East Asian starch

3

The world sugar marketRecent developments and outlook

© 2016 LMC International. All rights reserved. January 2016

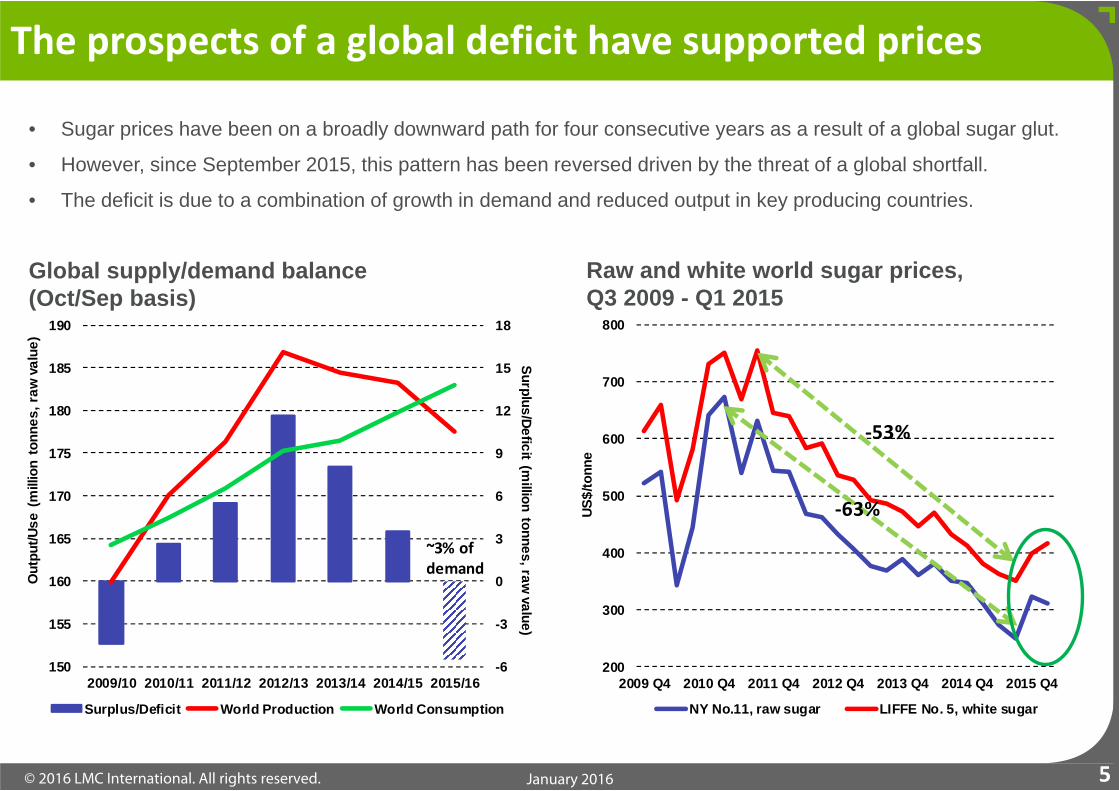

• Sugar prices have been on a broadly downward path for four consecutive years as a result of a global sugar glut.

• However, since September 2015, this pattern has been reversed driven by the threat of a global shortfall.

• The deficit is due to a combination of growth in demand and reduced output in key producing countries.

Global supply/demand balance (Oct/Sep basis)

Raw and white world sugar prices, Q3 2009 - Q1 2015

The prospects of a global deficit have supported prices

5

-6

-3

0

3

6

9

12

15

18

150

155

160

165

170

175

180

185

190

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16

Surplus/Deficit (million tonnes, raw

value)

Out

put/U

se (

mill

ion

tonn

es, r

aw va

lue)

Surplus/Deficit World Production World Consumption

~3% of demand

200

300

400

500

600

700

800

2009 Q4 2010 Q4 2011 Q4 2012 Q4 2013 Q4 2014 Q4 2015 Q4

US$/

tonn

e

NY No.11, raw sugar LIFFE No. 5, white sugar

‐63%

‐53%

The 2017 reform of the EU sweetener marketImplications for the EU starch sector

© 2016 LMC International. All rights reserved. January 2016

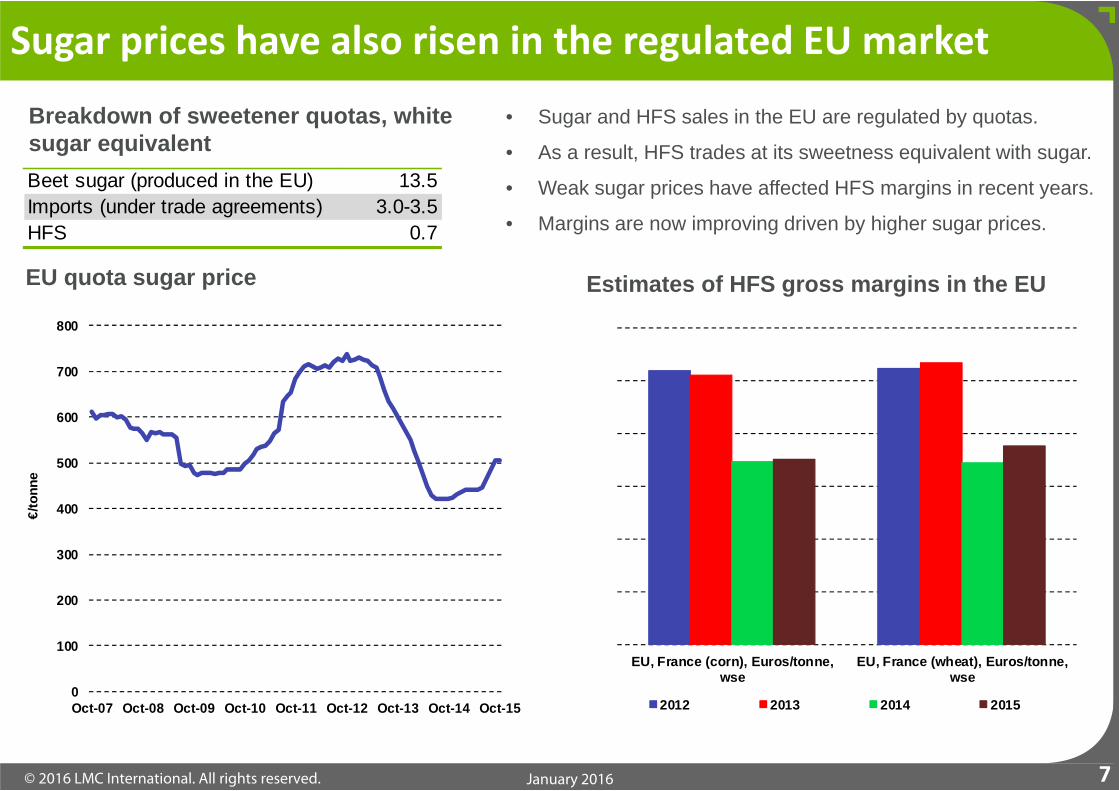

• Sugar and HFS sales in the EU are regulated by quotas.

• As a result, HFS trades at its sweetness equivalent with sugar.

• Weak sugar prices have affected HFS margins in recent years.

• Margins are now improving driven by higher sugar prices.

Breakdown of sweetener quotas, white sugar equivalent

EU quota sugar price

Sugar prices have also risen in the regulated EU market

7

Beet sugar (produced in the EU) 13.5Imports (under trade agreements) 3.0-3.5HFS 0.7

Estimates of HFS gross margins in the EU

0

100

200

300

400

500

600

700

800

Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Oct-12 Oct-13 Oct-14 Oct-15

€/to

nne

0

100

200

300

400

500

600

EU, France (corn), Euros/tonne,wse

EU, France (wheat), Euros/tonne,wse

2012 2013 2014 2015

© 2016 LMC International. All rights reserved. January 2016

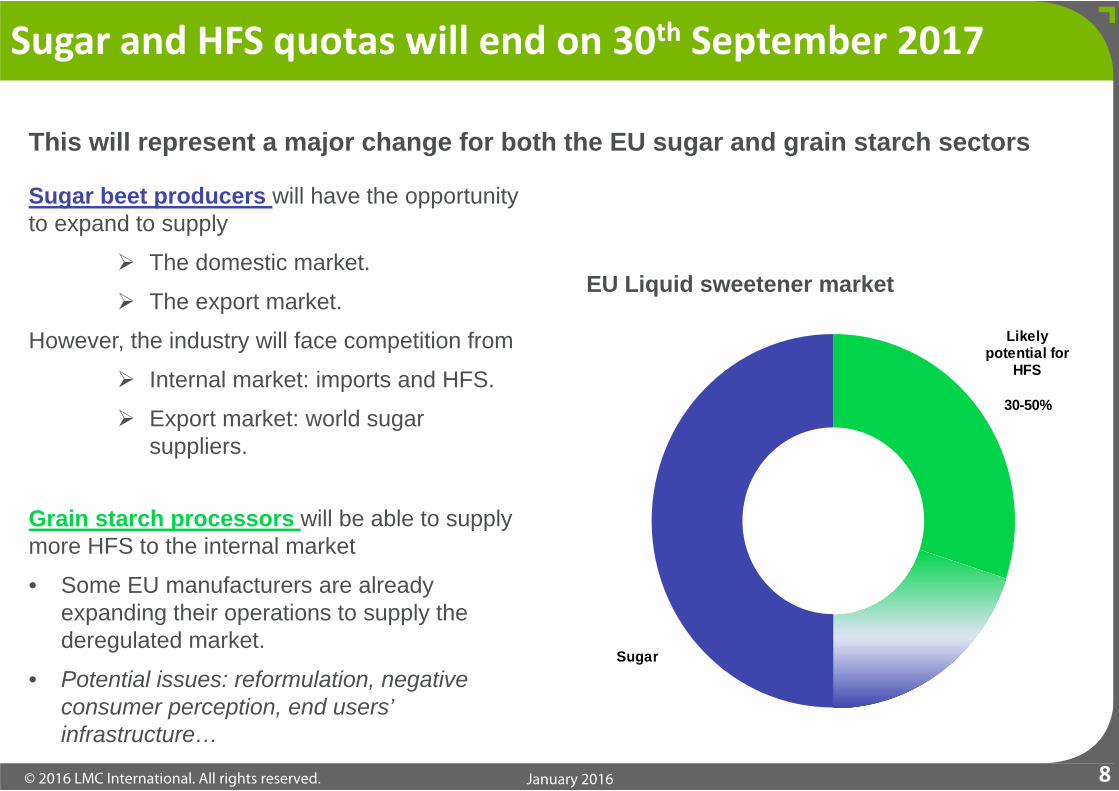

Sugar beet producers will have the opportunity to expand to supply

The domestic market.

The export market.

However, the industry will face competition from

Internal market: imports and HFS.

Export market: world sugar suppliers.

Grain starch processors will be able to supply more HFS to the internal market

• Some EU manufacturers are already expanding their operations to supply the deregulated market.

• Potential issues: reformulation, negative consumer perception, end users’ infrastructure…

Sugar and HFS quotas will end on 30th September 2017

8

EU Liquid sweetener market

This will represent a major change for both the EU sugar and grain starch sectors

Likely potential for

HFS

30-50%

Sugar

© 2016 LMC International. All rights reserved. January 2016

Currently, there is great uncertainty around the plans of the main grain processors.

• The additional HFS volumes are likely to tighten capacity utilisation. This will improve margins in the sector.

These developments, however, are unlikely to affect significantly the potato and cassava sectors.

• In the EU, potato and cassava starches are ‘premium’ starches.

• The EU potato starch sector is the largest globally. There is no cassava starch in the EU.

What does this mean for the EU starch sector?

9

The EU potato starch sectorAsia is the largest export market

© 2016 LMC International. All rights reserved. January 2016

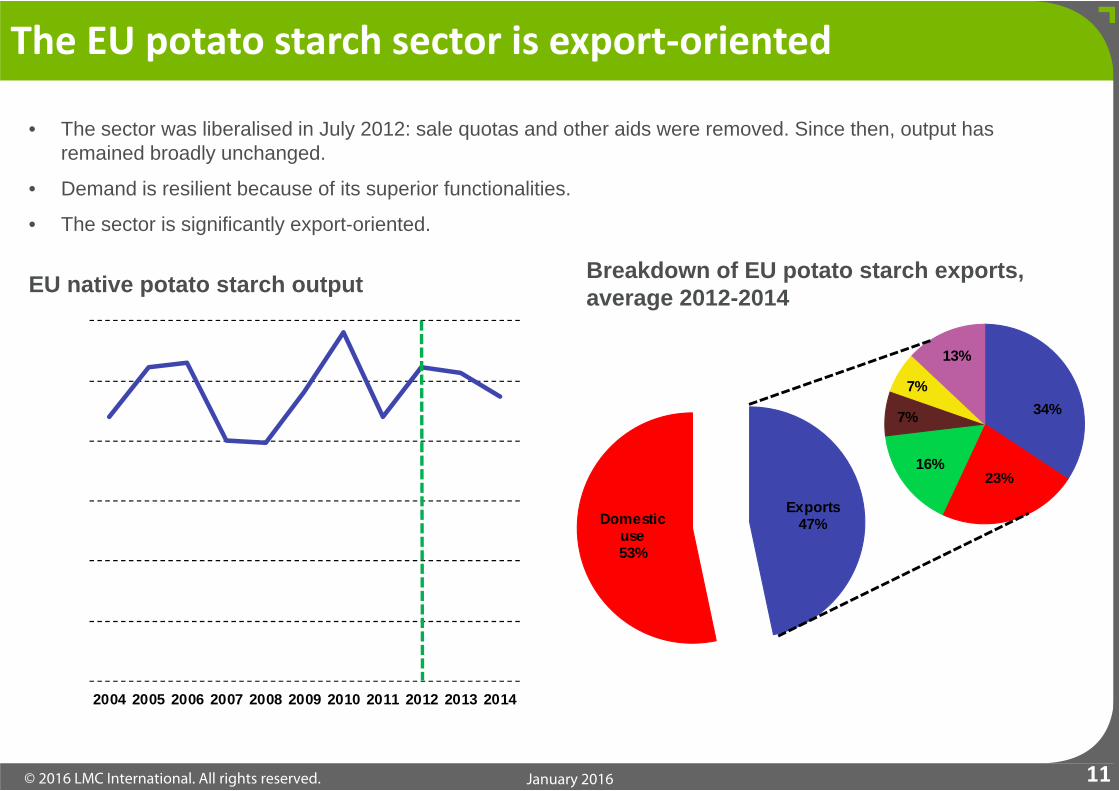

Exports47%Domestic

use53%

34%

23%16%

7%

7%

13%

• The sector was liberalised in July 2012: sale quotas and other aids were removed. Since then, output has remained broadly unchanged.

• Demand is resilient because of its superior functionalities.

• The sector is significantly export-oriented.

EU native potato starch output Breakdown of EU potato starch exports, average 2012-2014

The EU potato starch sector is export‐oriented

11

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

tonn

es

© 2016 LMC International. All rights reserved. January 2016

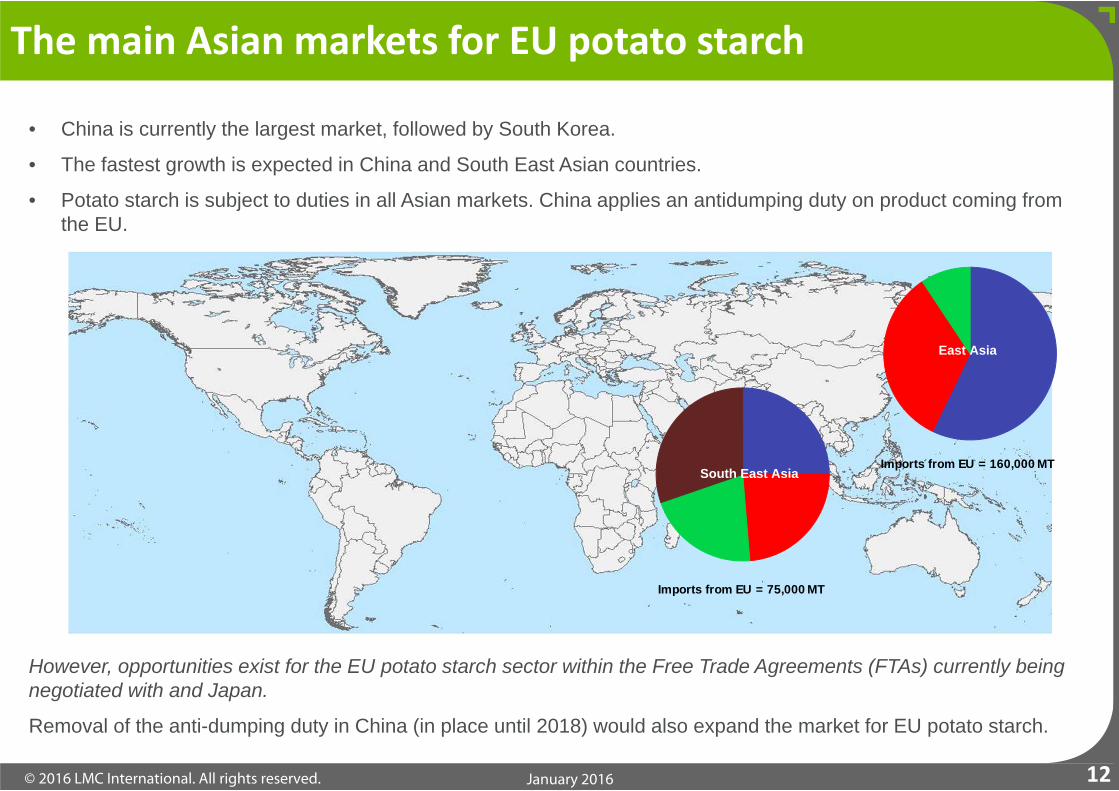

• China is currently the largest market, followed by South Korea.

• The fastest growth is expected in China and South East Asian countries.

• Potato starch is subject to duties in all Asian markets. China applies an antidumping duty on product coming from the EU.

The main Asian markets for EU potato starch

However, opportunities exist for the EU potato starch sector within the Free Trade Agreements (FTAs) currently being negotiated with and Japan.

Removal of the anti-dumping duty in China (in place until 2018) would also expand the market for EU potato starch.

12

Imports from EU = 75,000 MT

South East AsiaImports from EU = 160,000 MT

East Asia

The role of cassava starch in the EUOpportunities for South East Asian starch

© 2016 LMC International. All rights reserved. January 2016

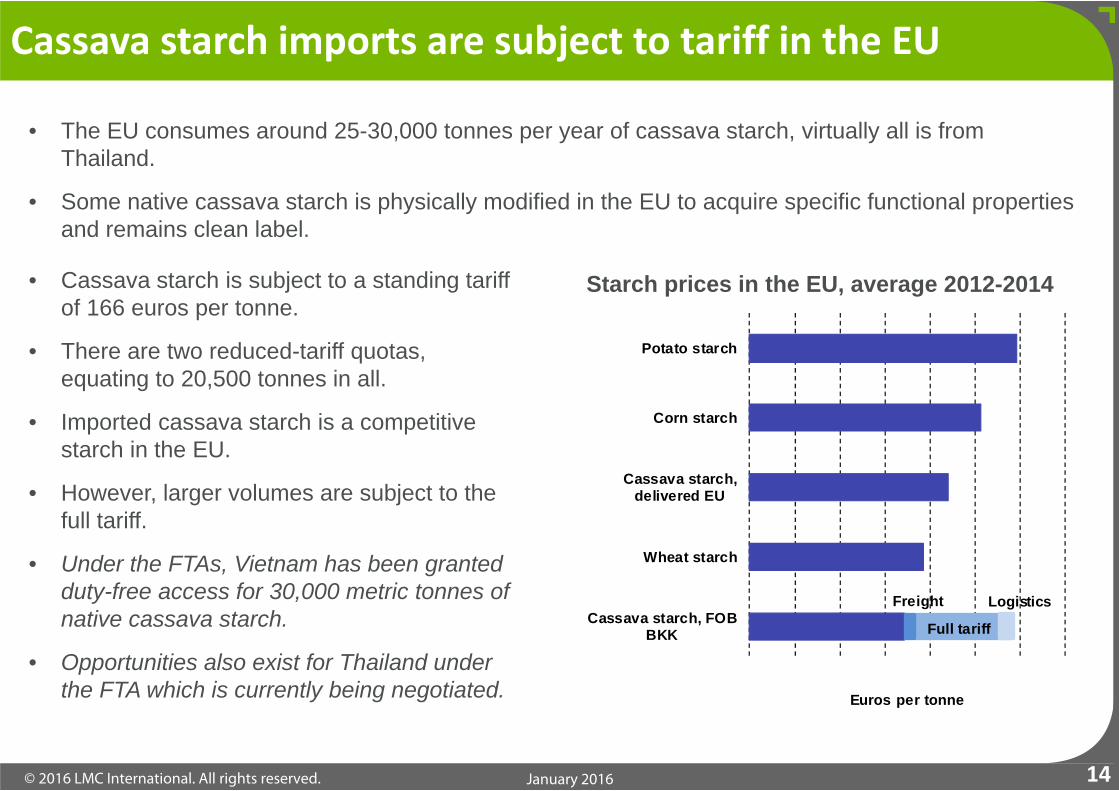

• Cassava starch is subject to a standing tariff of 166 euros per tonne.

• There are two reduced-tariff quotas, equating to 20,500 tonnes in all.

• Imported cassava starch is a competitive starch in the EU.

• However, larger volumes are subject to the full tariff.

• Under the FTAs, Vietnam has been granted duty-free access for 30,000 metric tonnes of native cassava starch.

• Opportunities also exist for Thailand under the FTA which is currently being negotiated.

Cassava starch imports are subject to tariff in the EU

• The EU consumes around 25-30,000 tonnes per year of cassava starch, virtually all is from Thailand.

• Some native cassava starch is physically modified in the EU to acquire specific functional properties and remains clean label.

14

Starch prices in the EU, average 2012-2014

0 100 200 300 400 500 600 700

Cassava starch, FOBBKK

Wheat starch

Cassava starch,delivered EU

Corn starch

Potato starch

Euros per tonne

Full tariff

Freight Logistics

Summary and conclusions

© 2016 LMC International. All rights reserved. January 2016

• World sugar prices rose in recent months driven by the threat of a global deficit.

• This developments spilled to the EU sugar and HFS markets.• These markets will be fully liberalised in October 2017.• This provides expansion opportunities to both the EU beet sugar

producers and grain processors.• While it remains to be seen how the grain processing sector will

react, there are reasons to believe that the liberalisation will support grain starch margins.

Summary and conclusions ‐World and EU

16

© 2016 LMC International. All rights reserved. January 2016

• The EU potato starch sector is currently doing well, after support was removed in 2012.

• The industry is greatly export-oriented. China and South East Asia are the largest markets.

• The FTAs being negotiated with Japan and the removal of the anti-dumping duty in China could offer opportunities to EU producers.

• The EU cassava starch market is very small. Imports outside quota are subject to the full tariff.

• Waiving of the import tariff under the FTAs would make Thai and Vietnamese cassava starch very competitive in the EU market.

• However, any duty-free imports will be subject to quotas.

Summary and conclusions – Potato and cassava starch

17

© 2016 LMC International. All rights reserved. January 2016

Singapore16 Collyer Quay #21-00

Singapore 049318Singapore

Tel: +65 6818 9231

This presentation and its contents are to be held confidential by the client, and are not to be disclosed, in whole or in part, in any manner, to a third party without the prior written consent of LMC International.

While LMC has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this presentation, any decisions based on them (including those involving investment and planning) are at the client’s own risk.

LMC International can accept no liability regarding information analysis and forecasts contained in this presentation.

© LMC International, 2016All rights reserved

New York1841 Broadway

New York, NY 10023USA

T +1 (212) 586-2427F +1 (212) 397-4756

Oxford 4th Floor, Clarendon House

52 Cornmarket StreetOxford OX1 3HJ

UK

T +44 1865 791737F +44 1865 791739

Kuala LumpurB-03-19, Empire Soho

Empire SubangJalan SS16/1, SS1647500 Subang Jaya

Selangor Darul EhsanMalaysia

T +603 5611 9337

www.lmc.co.uk