Embed Size (px)

Citation preview

Taxation of energy products used in metallurgical and mineralogical

processes European Commission workshop

Prague, November 2015 Frank Buijs – VNMI

Association of the Dutch metallurgical industry

Contents

This presentation was drafted by VNMI in collaboration with energy management experts employed by metallurgical and mineralogical industrial production companies active in the Netherlands. The presentation aims to clarify why an exemption for metallurgical and mineralogical use of energy products, such as electricity & natural gas is fair & reasonable. Touching on current experiences in the Netherlands with exemptions for energy use in (chemical, petrochemical,) metallurgical & mineralogical processes, this presentation tries to illustrate how this exemption should be enforced, in light of the use of motor fuels, energy products and electricity in the furnaces and in stationary motors. In the context of metal working processes, it tries to exemplify to what extent –and on what basis- exemptions should be restricted. As for the mineralogical industry, a distinction is made between core production activities in production processes and the necessity of delineation between core and auxiliary production activities.

Fair and Reasonable - Since 1992* the Commission has a long standing approach to

subject only energy products used as heating or motor fuel to a Community Framework

- Comprehensive assessment of the nature and logic of the Community energy tax system took place between 1998-2003 and Member States once again considered that energy tax should concentrate on motor fuels and heating fuels

- Council and Commission therefore considered it the nature and logic of the tax system to exclude from the scope of the Directive “other uses than as motor fuels or as heating fuels”

*(Council Directive 92/81/EEC duties mineral oil)

Essential starting points

• A global level playing field in taxation of energy use products is the desired end result

• To avoid market distortions, it is important that tax treatment of different industrial processes, manufacturing identical products, should be as similar as possible

• Basis for exemption as sharp and simple as possible; staying in line with original intentions of the directive will preempt that ever more sectors, products and processes are covered

• Conformity between exemptions for metallurgical and mineralogical energy taxes for use of electricity and gas in products and processes

• Energy for dual use purpose should be treated the same way as energy products for non-fuel use considering that, in a dual-use process

– the two uses can hardly be distinguished

– the quantities of the product cannot readily be apportioned to each use

Applying the definition to metallurgical processes

• Metallurgical processes: all processes with which metals are separated from their ores or scrap, the purification of metal, alloying of metals and/or creating usable objects out of metals, considering that

– The purpose of these processes is to produce metals and not to make products out of it (bending, welding, etc.)

– the crystalline structure and the characteristics of the metal are irreversibly changed,

– all parts of the process are covered (direct and indirect processes, including auxiliary and preparatory processes), AND

– all processes are located on one geographic location

• Examples of indirect metallurgical processes: e.g. preparation of ore, scrap and coal/cokes, sinter, pellets, hot wind, oxygen, cooling of the blast furnace, ventilation in dust removal plant, motors to transport (hot) metal in and between the processes. Without these processes the metallurgical process of metal production is not possible.

Applying the definition to mineralogical processes

• Energy for mineralogical processes has been explicitly considered “a use other than motor or heating fuels”

• Mineralogical processes that are energy intensive in the sense of the Directive – Purchases of energy products and electricity amount >> 3% of production value

• Fuels and electricity are used in a high temperature (chemical) transformation process where minerals are irreversibly transformed into new materials

• There is an integrated whole of core production steps that are considered as one installation. To produce the material/product, none of the steps can be left out. o Example: mixing, weighing, melting, fining, forming, annealing and (depending on

products) coating, winding, cutting etc.

• Installations directly linked to the core production steps should also remain out of the scope of the Directive. o Example: production cannot take place and the production installation cannot survive

without activities of cooling, ventilation, transport between production steps etc.

Questions from working document

1. Do you consider that motor fuels used in stationary motors and auxiliary activities are not included in the wording of Article 2(4)(b), second indent? The Directive states that “energy products used for chemical reduction, or in electrolytic and metallurgical processes shall be regarded as dual use”. This means that if a stationary motor or auxiliary activity is part of these processes than it is regarded as dual use. For example: producing oxygen for producing steel should be covered by the definition, but powering motors in cleaning should not be covered.

2. What is your opinion of ‘physical metallurgical processes’ such as forging? If the crystalline structure of the metal is irreversibly changed, such as forging, this should be covered by the definition. Using metal to produce something else should not be covered by the definition, including those processes that have short heating.

3. Do you agree that electricity used in stationary motors and auxiliary activities is not included in the wording of Article 2(4)(b), third indent? Same as first bullet; as long as it is clear that motors used (either directly or indirectly) for enabling metallurgical / mineralogical processes are covered by the definition. It would help to explicitly include these in the definition and/or preamble.

4. Do you believe that there are cases where the metallurgical processes or facilities do not allow distinguishing between the use of energy products and electricity in the furnaces and in stationary motors? Could you provide examples? Yes, such as (for example) producing oxygen in order to produce steel on location, producing coking coal on the same location as making iron. A direct link should be possible between e.g. the piping network, the conveyors et cetera in order to qualify for the exemption.

Questions from the working document (continued)

5. Do you consider that metal working processes (e.g. forging, metal strengthening with quenching) should be covered by the definition of metallurgical processes? Yes, but only on the condition that the crystalline structure of the metal is irreversibly changed.

6. What metal working processes would you include in the definition of metallurgical processes? Would you consider it necessary to introduce restricting conditions (e.g. forging is included only if it leads to changes in the physical properties of the metal) and what would these conditions be? See answer to question number 2 for definition.

7. Do you agree that, with the exception of propellant use, energy products and electricity used in mineralogical processes include uses only in the core production activities which involve furnaces, kilns but also, where necessary, uses in stationary motors such as compressors, cutting machines and in general all the equipment necessary to perform the processes, as defined by NACE codes? Yes, provided that all the steps of the core process are identified. See example glass: There is an integrated whole of core production steps that are considered as one installation: example: mixing, weighing, melting, fining, forming, annealing and (depending on products) coating, winding, cutting etc

8. Do you believe it is necessary to further consider the delineation between core and auxiliary production activities in the case of mineralogical processes? Can you provide practical examples in case you exempt from taxation the production processes which are outside the scope of the ETD? Yes, example cooling system and cooling fans, transport between process steps, ventilation

BACKUP SLIDES

Fair and Reasonable

- Recital 22: “Energy products should essentially be subject to a Community framework when used as heating fuel or motor fuel. To that extent, it is in the nature and the logic of the tax system to exclude from the scope of the framework dual uses and non-fuel uses of energy products as well as mineralogical processes. Electricity used in similar ways should be treated on an equal footing”

- Art 2.4b 2nd indent: An energy product has a dual use when it is used both as heating fuel and for purposes other than as motor fuel and heating fuel. The use of energy products for chemical reduction and in electrolytic and metallurgical processes shall be regarded as dual use

Dutch case law

• LJN: BL0646, Court of Arnhem, AWB 08/3457 (published 26-1-2010)

Examples of mineralogical production that should be covered by the definition

• Various products

– Flatglass, packaging glass, table ware, glass wool, fibre glass, special glass

– Bricks, tiles

– Limestones

– Rockwool

– Cement

• Highly automated processes

– 24/7 online production

– There is an integrated whole of core production steps that are considered as one installation: for example mixing, weighing, melting, fining, forming, annealing and (depending on products) coating, winding, cutting etc.

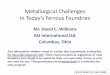

Example: float glass production

Waste

gases

Air

exhaust

Gas

Electricity

Raw materials Drying Firing Products

Steam cycle

Waste gas cleaner with

heat recycling

Drying

equipment

Humid

Refractory

mass

Example: ceramic production process

Heat Heat Heat

Forming

2nd and 3rd indent