Embed Size (px)

DESCRIPTION

Citation preview

Trade Promotions Management An In-depth Review

Page 2 of 38

Table of Contents

1. Introduction .........................................................................................................................................3 What is trade promotion management? ...................................................................................... 3 Why is trade promotion management important?......................................................................... 3 How is trade promotion management performed?........................................................................ 4

2. Overall Flow .........................................................................................................................................6 3. Process Steps......................................................................................................................................7

STEP 1: Allocate Budget to Accounts ......................................................................................... 7 STEP 2: Create Promotion Plan ............................................................................................... 12 STEP 3: Sell-in Promotion Plan ................................................................................................ 19 STEP 4: Execute Promotion Plan ............................................................................................. 22 STEP 5: Monitor/Revise Promotion Plan ................................................................................... 25 STEP 6: Evaluate Promotion Effectiveness................................................................................ 28

4. Roles...................................................................................................................................................31 5. Key Process Measurements ............................................................................................................32 6. Overall Design Considerations........................................................................................................32 7. Trade Promotion Best Practices......................................................................................................33 8. Other Facts to Consider ...................................................................................................................34 Glossary.....................................................................................................................................................36

Page 3 of 38

1. Introduction

What is trade promotion management? Trade promotion management is defined as the process of planning, budgeting, presenting and executing incentive programs which occur between the manufacturer and the retailer to enhance sales of specific products. For example, a manufacturer paying a retailer to feature their product in the retailer’s weekly newspaper advertising or paying a retailer to build a special promotional display in their store are both considered trade promotions.

Why is trade promotion management important? Between 1978 and 1996 the dollars spent on trade promotions grew on average from 5% of sales to 13% of sales. This led to inefficient spending practices in the trade promotion area. There is a significant benefit potential to improving trade promotion practices by fully understanding the costs of promotions, running smarter promotions by knowing what works and what doesn’t, and focusing promotions on what will increase profits, rather than just gross revenues.

Our clients have achieved or are expecting to achieve significant benefits from improving their trade promotions processes. These include:

Value Proposition

• 10-25% reduction in trade promotion spending with no change in volume

• 1-4% increase in pre-tax earnings

• Trade promotion ROI increase of more than 25% on average (more than 200% on some events)

• 40% reduction in outstanding deductions balances

• Reduce trade spending from 17% of sales to 13% of sales

Improving trade promotion practices involves the coordination of strategy, process, people and technology. This document will focus on providing knowledge of the overall trade promotion process and will highlight best practices.

Page 4 of 38

How is trade promotion management performed? Incentive programs vary widely from account to account. Incentives can involve discounts on each product sold, payments of a fixed sum of money, or other special programs. In return, a retailer is expected to generate greater volume through special pricing, advertising and other programs. The following diagram provides listings of many of the types of incentives and programs that are run. Refer to the glossary for further definition on these programs.

BenefitsPerformanceCosts

Manufacturers Offer Incentivesto Trading Partners . . .

. . . In Return forPerformance . . .

. . . To GenerateConsumer Sales . . .

• Off-invoice allowances• Favorable payment terms• Market development funds• Sell-through guarantees/

failure fees• Co-op advertising• Bracket allowances

At Headquarters• Plan

merchandising• Buy in advance

of demand• Set prices• Authorize new

items• Develop

planograms

• Incremental Sales and ProfitsAt Retail• Merchandising

• Ad• Display• Reduced prices• Coupons

• Everday Low Price• Distribution• Shelving

• Space• Configuration• Location• Secondary

• Stock rotation The determination of the incentive programs that will be run is based on corporate customer and product strategies and specific account objectives. These programs are documented for each account and product in a promotion plan. For most companies, the account level for which plans are created is a national or headquarter account (i.e. one plan for the XYZ Grocery Chain); other companies may create a plan for a specific region of the account if the account is very large, or maybe even for each individual store if there are not many customers. On a similar note, the product level for which plans are created is often a group of related products (liquid soaps, breakfast pastries, or personal printers). Plans can be created for higher levels (soaps, ready-to-eat cereals, or printers) or even lower levels (6 oz. fresh scent soap, jumbo box of corn flakes, or the LT5275 printer).

NOTE: In this document, the words account and product are used to refer to whatever account and product level that the customer is planning. The development of the promotion plan is a subset of the overall account plan for each account. The account plan deals with higher level account issues, goals and types of promotions that will be run. The promotion plan provides a more detailed roadmap of the specific promotions that will be run for a given account. Developing the promotion plan is typically a quarterly or semi-annual process. The purpose of this process is to develop a clear plan for the promotional events that will be run to meet the revenue quotas and to provide the greatest return on investment. The process for developing the promotion plan for an account varies among manufacturers:

• Some manufacturers use more of a top down approach where national promotions are developed by marketing for all accounts.

Page 5 of 38

• Other manufacturers employ a bottom up approach where each account representative has free reign to develop individual promotions for their account.

• Other manufacturers fall somewhere in between.

This document will focus on the promotion planning, execution and post analysis activities performed by the sales organization. Marketing and other activities are not included. Variations in the process will be noted in the design considerations listed under each individual process step and for the overall trade promotion process. This document will detail the overall sales process and each of the steps involved. Key points to understand include:

KEY POINTS • Planning: In order to meet account objectives, it is imperative to have a solid promotion

plan for meeting those objectives. This plan should be based on past history, customer, brand/product, and corporate objectives, and good judgment. Currently, many companies have extremely informal or non existent processes. One company actually cites sales reps creating their plans on a cocktail napkin.

• Executing: A primary stumbling block in the execution of the account plan is accurate

and timely payment to retailers for promotion performance. Processes and tools are imperative to avoid costly deductions expenses and overspending due to poor accounting.

• Analyzing: Studies show that between 50-90% of promotions are not profitable. Many

companies are not performing any post analysis to determine which promotions are profitable. Without this analysis, the same unprofitable promotions are run over and over again.

Page 6 of 38

2. Overall Flow Trade Promotion Management is part of an overall Selling Effectiveness Process Architecture:

BusinessPlan

CustomerStrategy

MarketingStrategy

Account-Based Selling

Promotions Management

Category Management

Retail Execution

Account Management Distributor-Based Selling

Sales Planning

Opportunity-Based Selling

Pipeline Forecasting

Opportunity Management

The Trade Promotion Management process is depicted below:

•Sales Quota byAccount/Brand

•Overall SpendingBudgets

•Historical SalesData

•HistoricalConsumption Data

•Past PromotionResults

•RetailerPerformance

•Marketing Plan•Promotional

Strategy for theBrand/Product

•Account Plan•Customer

PromotionCalendar

•Historical AccountActivity

•Understanding ofCustomer

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

•Final PromotionPlan

•PromotionResults

3. Process Steps

STEP 1: Allocate Budget to Accounts

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION Before a detailed promotion plan can be developed for an account, there are two important inputs:

• Sales Quota by Account/Brand: How much am I expected to sell of each product/brand at my accounts? Sales quotas by account/brand and sales rep are established in the Territory Management process and are included as an input into this allocate budget to accounts process step.

• Spending Budgets by Account: How much promotional money do I have to spend at this account? There are several ways that these budgets are determined:

In some instances, the spending “budget” is determined through a bottom up method and therefore is not set until after the promotion plan is developed.

In other instances, the spending budget is developed through an accrual method where accounts accrue a certain amount of promotion dollars for each unit of product that is purchased. In this instance, the sales force is provided with per unit accrual rates for each product.

In most instances, however, there is some bucket or lump sum of money that is allocated to be spent at each account by sales management. This lump sum budget can be in addition to dollars accrued per unit. It will also most likely be confirmed through bottom up planning. The top down process of determining how much lump sum money should be spent at each account is described in this process step.

For additional information on alternate ways of establishing spending budgets, refer to the design considerations at the end of this process step description.

Page 8 of 38

FLOW

EstablishAllocation

Method

• Historical SalesData

• Sales Quota byAccount/Brand

• Overall SpendingBudgets

• PromotionalStrategy for theBrand/Product

• Spending Budgetsby Account

Allocate toAccount Group

or Region

Allocate toAccount

INPUTS

• Historical Sales Data: Historical sales data provides actual sales volumes shipped to each account in prior periods. This data is used when setting spending budgets based on past sales volume.

Historical sales data needs to be available at the same account and product levels designated in the promotion plan.

• Sales Quota by Account/Brand: Sales quotas need to be established for each account and product/brand. These are established in the territory management process.

The account level to break down sales quotas should be consistent with the level that we are developing promotion plans for. In some cases, each sales representative will be given a total quota for all of his accounts. The sales representative will then want to break down his overall quota into each of his accounts

The product level to break down sales quotas should be consistent with the level for which we are developing promotion plans. In some cases, a sales representative will be given a quota for a given product brand, but will be asked to plan at a lower level. He will want to ensure that his expected sales for the individual products roll up to the quota he was given for the product grouping.

• Overall Spending Budgets: Marketing will typically provide the sales organization with overall spending guidelines by product group. During this process step, sales management or brand management will allocate the total dollars to spend across accounts.

• Promotional Strategy for the Brand/Product: The promotional strategy is developed by marketing and sales executives to clearly outline how the company wants to promote their products. A key component of the promotion strategy is the role of trade promotions by brand. For example:

Drive incremental sales Increase market share and brand loyalty Buy-down everyday retail price

A clear understanding of the types of promotional dollars and activities available, as well as an understanding of how the promotional dollars should be allocated by account from a strategic perspective, is required to effectively allocate promotion dollars to accounts. Example: The brand strategy at one consumer products company documents what trade

promotion dollars are supposed to accomplish for each brand. For example, trade dollars should build brand awareness and trial for new product introductions, while maintaining market share without eroding baseline volume for established brands.

Page 9 of 38

Example: The promotional strategy for a given company focuses on driving incremental sales. They want to focus on getting current consumers to buy more of the product and getting new consumers to try the product. End aisle displays and other prominent advertising to draw attention to the product is important. The promotion plan specifies that all dollars will be allocated on a per case (rather than lump sum basis). All promotions are set up on an individual account (rather than national) level.

Example: The promotional strategy for an alternate company focuses on buying down the everyday retail price. This company does not offer any special promotions or coupons to retailers and consumers. The money they save is used to reduce costs everyday. This strategy is often referred to as Everyday Low Price (EDLP). This can be seen at retailers such as Wal-Mart and Home Depot which are forcing many manufacturers to follow suit.

OUTPUTS

• Spending Budgets by Account: Detailed spending budgets for each account by product, or product grouping, will be given as the output.

Example: An account manager for XYZ Grocery is given a quota of $250,000 for liquid soaps. To reach this quota, the sales representative has $32,500 of promotional spending allocated for liquid soaps.

ACTIVITIES

Activity 1: Establish Allocation Method

A. Review historical volumes B. Establish allocation method

• Typically based on historical volumes at the accounts. More leading edge companies will base on account potential.

• By law, must equally and equitably distribute promotion dollars to accounts.

Activity 2: Allocate to Account Group/Region (Iterative)

A. Allocate funds into first account grouping • May first divide overall funds from marketing into major customer types (i.e. Club Stores and

Grocery Stores) or may allocate by geography, etc. B. Continue to allocate funds until they are down to a sales representative level

Activity 3: Allocate to Account

A. Allocate spending budgets to account • Typically the person with the most knowledge of the account, the sales representative, will be

involved in confirming budgets at this lowest level.

DESIGN CONSIDERATIONS

There are several factors that will affect how, or even if, the allocate budget to accounts process step is performed. These factors are:

Page 10 of 38

Bottom up vs. Top down Budgeting

• Top down Budgeting: Spending budgets by account can be allocated by sales management to each sales representative or account as described in the above process step. The advantages of this method are:

Ensures budgets are allocated based on overall corporate Promotional Strategy for the Brand/Product.

Ensures that account level budgets will meet overall spending budget.

• Bottom up Budgeting: Each sales representative can determine the promotion dollars needed to meet their sales targets during the Create Promotion Plan process step. In this case, a bottom up approach is used where each individual account budget is rolled up to an overall spending level. The overall spending is compared to the total available dollars prior to approval. In this scenario, the Allocate Budget to Accounts process step is not performed. The advantages of this method are:

Budgets can be generated based on needs at the account.

Account opportunities rather than just historical sales can be included in the budgeting process.

Lump sum versus accrual spending budgets: Promotion spending budgets are typically allocated at the account/product level. Many manufacturers are struggling with whether this allocation should be given to their account managers in a lump sum or by accrual based spending.

• Lump Sum Budgets: Lump sum is when a sales representative receives a set dollar amount to spend on promotions for a particular category at a specific account. As an example, a sales representative may receive 32,500 for promotional spending on liquid soaps. Some of the advantages of lump sum are:

Maintenance Easier to maintain and track.

Adherence to budget Less likely to go over budget than with accrual based spending. It is important to note that with lump sum, there is still the issue of controlling promotion budgets. As an example, a sales representative may agree with a retailer to do a promotion where they run an ad for $5000 and give the retailer $2.00 off per case of a particular product. If the retailer buys a greater number of cases of the product than anticipated, the sales representative may go over budget on the promotion budget. Also, sales representatives may over commit on their promotion spending budgets.

• Accrual Based Budgets: Accrual based spending is where a sales representative accumulates their budget for promotion spending based on the number of cases sold in a particular category for a specific account. For example, a manufacturer may give a sales representative $2.00 for every case of liquid soap the account buys. Therefore, if the retailer purchased 20,000 cases of liquid soap from the manufacturer, the sales manager would have $40,000 to spend on promotions for liquid soaps for that account.

Some of the advantages of accrual based spending are:

Directly incents

Page 11 of 38

This method directly incents the sales representative to increase the volume of a product for a particular account.

Customer equity This method represents a fair way of distributing promotion spending across multiple accounts.

Greater control Sales representatives prefer this method because it gives them more control over the promotional dollars they have to spend.

Reduces incentive to forward buy or divert

Forward buy refers to the process of purchasing extra product while it is on promotion for selling at a later date (stocking up). Diverting refers to purchasing product in one area of the country or for an account that can get a cheaper price and sending (diverting) it to another area with a more expensive price. With accrual rates, everyone gets the same rate, every day thus reducing forward buy and diverting incentives.

Some of the disadvantages of accrual based spending are:

Adherence to budget Tend to go over budget easily with accrual based spending. The sales representative is spending the promotion dollars before they earn them. For example, the sales representative may estimate that they are going to sell 20,000 cases of liquid soap with their account and at an accrual spending rate of $2.00 per case, decides they have $40,000 to spend on promotions for liquid soap. After spending the $40,000, it may turn out that the customer only bought 15,000 cases of liquid soap. The sales representative has now gone $10,000 over budget.

Maintenance Accrual based spending is somewhat harder to track than lump sum dollars as the dollars spent and accrued are not always part of the same event. In addition, the total spending budget is constantly changing as more cases are shipped.

National vs. Account Specific Promotions: One of the issues manufacturers deal with today is what sort of guidelines to give their sales representatives when planning trade promotions. There are two different methods they may use or they may choose a combination of the two.

• Account Specific Promotion Programs One method companies use, is to give the sales representatives a budget for their trade promotions and allow them to tailor the promotions individually to the customer with no guidelines from corporate. The spending budgets are developed during this process step.

• National Promotion Programs Another method companies use is to have the marketing department define a list of national promotions. These promotions will be available to all accounts and can not be altered by the sales force. In this instance, the budgeting process step will not be performed. As an alternate example, a key account manager may identify a list of promotions for the overall account. Individual sales reps that call on the stores of this account choose from this list when defining store-specific promotional activities.

Page 12 of 38

• Account Specific and National Promotion Programs A final method is to set up both national programs that sales reps can choose to run at their accounts or not and potentially to supplement that with additional funds for establishing account specific promotions. In this instance, those spending budgets will be developed during this process step.

• For additional information on the lump sum vs. accrual decision, see the Overall Design Considerations section of this document.

STEP 2: Create Promotion Plan

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION

Creating the promotion plan is the largest component of the Manage Trade Promotions process. A good plan is the cornerstone to successful trade promotion activities. Typically promotions have been seen by manufacturers as short term initiatives to meet sales projections for a given period. Instead, trade promotions need to be considered more holistically to meet long term account objectives. Creating a formal promotion plan helps manufacturers to take this longer term view.

Developing the trade promotion plan by account requires a strong understanding of past sales and promotions and often simply a “gut feel” for future events. As a result, developing this plan can become a “black box” with the historical data going in and a promotion plan coming out. The challenge is to understand the thought processes that the best reps are using to create profitable promotion plans and to translate that into reusable process steps.

Given the breadth of knowledge required to develop the plan, this process step should not be solely completed by either marketing or sales. Instead it should be a collaborative approach. Typically marketing will provide initial strategic direction, sales representatives will use that direction as well as their extensive account knowledge to develop the detailed plan by account, and promotion specialists as well as sales management will review and approve the plan.

Promotion planning is often done twice a year for six month periods. As companies become more progressive in their promotion practices and utilize more tools, the goal is to move to more of a continuous planning process that allows them to apply learnings from the Q1 promotions to adjust the promotions for Q2.

Page 13 of 38

FLOW

DevelopPreliminary

Plan

Roll-up and

Adjust Plan

ObtainInternal

Approval•Promotion Plan by

Account/Product

• Sales Quota byAccount/Brand

• Spending Budgets byAccount

• Historical Sales Data• Historical

Consumption Data• Past Promotion

Results• Retailer Performance• Marketing Plan• Promotional Strategy

for theBrand/Product

• Account Plan• Customer Promotion

Calendar• Understanding of

Customer

INPUTS

• Sales Quota by Account/Brand: An understanding of the revenue and volume targets that must be met for each account and brand is a key input to the promotion plan. See step 1 inputs for a further definition of sales quotas.

• Spending Budgets by Account: If lump sum spending budgets are used, detailed spending budgets for each account by product, or product grouping, are needed in order to create the promotion plan. If spending budgets are determined based on accrual methods, the dollars accrued for each product sold are needed in order to create the promotion plan.

• Historical Sales Data: Historical sales data is used to understand baseline sales for the account. (See step G below). See step 1 inputs for a further definition of historical sales data.

• Historical Consumption Data: Consumption data refers to the amount of product the retailer sells to the end consumer. If consumption is much less than actual shipment volume, the retailer is not selling as much as he is purchasing. He is stocking up or “loading”. This loading is often done during promotion periods when prices are lower. The retailer will then need to purchase fewer products later on when prices are higher.

Because a manufacturers key objective is to have more product consumed by end users, not just ship it to sit in a retailer’s warehouse, he needs to focus on consumption data rather than simply sales or shipment data. For consumer products companies, consumption data can be purchased from third parties such as IRI and ACNielsen. Many retailers also have this data making it a best practice for the manufacturer to partner with his retailers to share information.

Page 14 of 38

The promotion plan should strive to increase the volume of product “consumed” by the end customers.

• Past Promotion Results: Knowledge of promotions that did and did not work well in the past is a key input to planning future promotion events. Results of prior promotions are compiled during step 6, evaluate promotion effectiveness. It is critical to capture qualitative data about each promotion in order for this history to be useful. For example, you may want to capture other “causal” information that had an impact on the success of the promotion, such as unusual weather conditions, competitive promotional activities, news stories about your company or your competitors, etc.

Example: Ran an end aisle display and reduced the price of liquid soaps in 10 oz. bottles to $1.59 from $1.89. There was a volume increase or “lift” over base sales of 25% during the time of the promotion. Competitor A also ran a promotion on their liquid soaps with Retailer XYZ during this time. Their price point for the 10 oz. bottles was $1.69.

• Retailer Performance: Retailer Performance has two components: Consumption Data:

Some companies will pay funds to their customers based on actual consumption data (sell through) rather than on shipments to prevent forward buying and diverting. In this instance, actual consumption data will be needed during the execute step as it becomes available.

Compliance Data: Syndicated data sources will provide information that can be used to see if the retailer complied with the parameters of the promotion (consumer price for the product, number of participating stores, % of stores displaying the product) The manufacturer may also receive some “proof of participation” from the retailer (such as a copy of an in-store ad or newspaper insert featuring the manufacturer’s product)

• Marketing Plan: To maximize the effectiveness of the trade promotion plan, account managers will want to take advantage of already existing marketing events and consumer promotions. As an example, if you are going to run a price reduction on bar soaps for Vons, a sales representative may want to time that price reduction for a time when commercials are running for their bar soaps.

Marketing will provide sales with a consumer promotion calendar showing when all events are running. They will also provide samples of ad slicks and other promotional materials.

The marketing plan contains four main components. Advertising: television, magazine, etc. Consumer Promotions: coupons (Free-standing inserts (FSIs)), rebates, etc. Marketing Promotions: “Win a Trip to the Super Bowl”, special packaging and displays, etc. Sales Promotions: sales contests, bonuses for gaining distribution for new products, etc.

• Promotional Strategy for the Brand/Product: The sales force must be provided with information about the overall strategy and any guidelines for using promotion funds prior to the planning period. In addition, they will be provided with information about how to spend promotion dollars and specific promotion details as appropriate.

A key component of the promotional strategy is the role of trade promotions by brand.

See step 1 inputs for further definition of the Promotional Strategy for the Brand/Product.

Page 15 of 38

• Account Plan: The account plan developed during the account planning process contains information about the goals for the account as well as types of promotions that should be run at the account. The promotion plan should be consistent with the objectives outlined in the overall account plan.

• Customer Promotion Calendar: Customer promotions are special events that are run by the retailer. Examples of customer promotions may include fall harvest days, turkey giveaways, etc. It is important for the sales representatives to take into consideration the promotional events occurring at their customer sites to ensure their trade promotions compliment the customer’s planned promotions and meet the customer’s needs. Example: XYZ Grocery may draw customers into their store by giving away a free turkey

at Thanksgiving to customers spending a certain amount at their stores. This would be a good time to run a promotion on specific items due to the increased traffic anticipated in XYZ stores during this promotion. If you carry items that complement a turkey such as stuffing or mashed potatoes, it would be an ideal time to run a promotion on those particular items.

• Understanding of Customer: Information required to understand the customer could include the customer’s: Products / Services Strategy Goals Objectives

OUTPUTS

• Promotion Plan by Account/Product: The promotion plan for the account will list all of the events that are planned during the planning period. Information about each event will include:

Event start and end dates as well as order and shipment dates for the promotion

Products included in the event

Expected base and incremental sales for each product (lift)

Event tactics (end-aisle display, temporary price reduction, ad feature, etc.)

Event costs (per case shipped to retailer, per case sold by retailer (scanned), lump sums)

Payment methods (off-invoice, bill back, separate check)

Expected profitability for the event (incremental Return on Investment (OI))

ACTIVITIES

Activity 1: Develop Preliminary Plan

A. Obtain Understanding of Past Performance • Review past sales figures to determine products sold at account and their base volumes • Review past consumption data to understand products sold to the end consumer vs. forward-

bought (products purchased by retailers at low promotion prices and stored for future sales). Affect of forward buying on base sales should be accounted for in the promotion plan.

Page 16 of 38

• Review past promotion history to understand learnings from past promotions.

B. Review account plan to understanding account goals

C. Review promotional strategy for the brand/product and marketing plan to understand corporate events/strategy

D. Gather/Create list of potential events.

E. Historical events can be used as the basis for the plan. • Where national promotions or promotion guidelines are used, a list of potential promotion events

will be supplied by marketing. F. Determine which products you expect to sell at the account during the planning period

• Based on sales of past products • Based on objectives identified in account plan

G. Enter base or everyday sales for each product • This is equal to how many units that we expect to sell at the account if we were to run no

promotions. The difference between these base sales and the target/quota as identified in the account plan is the volume that we need to generate through promotions.

H. Select or plan the preliminary events to run at that account by product • This step is completed based on knowledge of promotions that have successfully run in the past. • For companies who set up promotions at a national level, the sales representative may simply be

selecting the promotions to run from a “menu” of options. In companies that allow for truly account specific promotions, the sales rep will need to develop promotional events from scratch.

I. Determine the volume impact of the event based on past customer performance • Some companies may employ sophisticated computer modeling tools to perform this step.

These tools use lift factors that can be purchased from outside sources, such as IRI and ACNielsen, or lift factors that have been calculated internally based on past events to estimate the future volume for similar events.

• Other companies intentionally do not employ these expensive tools. Their feelings are that there are so many factors impacting future performance (competitor events, new product introductions, even weather . . .) that volume is better estimated by a person than a computer.

• Often, manufacturers will have a modeling tool to show the expected sales lift at different price points, based on the historical performance of the brand at that account.

J. Review event profitability/ROI for both the manufacturer and the retailer. • The selection of events is based on profitability for both the manufacturer and retailer. Sales

reps must develop “win-win” promotional events in order to get the retailer to agree to the promotion. Often, the sales rep will calculate the impact of the event on the retailer’s bottom line to use as a key selling tool.

In many instances, events are being run simply to generate volume. For example, if we are spending $20,000 to generate an increased volume of 10,000 cases where the net profit per case is $1.50, we may be meeting revenue goals, but we certainly are not meeting profitability goals. Activity 2: Roll-up and Adjust Plan as necessary

A. Roll-up each individual event to determine the overall volume and spending for the account by product or product group

Page 17 of 38

B. Adjust plan if necessary to meet corporate guidelines and targets (volume, spending and ROI) • The preliminary plan must be compared to corporate guidelines for promotion spending. • The preliminary plan must also be compared to the sales targets that have been established.

C. Adjust plan if necessary to make it “sellable” • The preliminary plan may need adjustment based on customer understanding and personal

knowledge of the account. While a plan may look good on paper, meeting the manufacturer’s targets and appearing profitable for the account, it may not achieve the account’s stated objectives.

Activity 3: Obtain Internal Plan Approval

A. Review plan with designated managers for approval

• Once the plan has been created, it must go through internal approval before being reviewed with the customer. The internal approval process and who reviews the promotion plans will vary for every company. This may include the regional sales managers, a company’s corporate promotion specialists (customer marketing) and the brand managers for each product line. These managers will analyze the following:

Aggregated event plans by Account, Market, and Channel. Each person reviewing account plans will want to ensure that the aggregate of the account plans that he is reviewing meets higher level spending budgets and sales quotas.

Overall promotional events. Regional managers and promotion specialists will use their knowledge to ensure that the promotions selected and the expected lift from each seem reasonable. They will provide advice on ways to obtain the greatest lift for promotion dollars spent.

B. Revise promotion plan as appropriate

C. Get Corporate approval

• The finalized promotion plan is signed off by the designated corporate approvers. This will vary from company to company but could include people such as the corporate promotion specialist, division vice presidents, etc.

DESIGN CONSIDERATIONS

Level of detail at which promotion planning is performed. • At what product level does a company perform its promotion planning process? As an example:

Deodorants - you could plan for all deodorants, or break it up by product type: roll-ons versus solids, or break down into the different scents. The lowest level of detail would be by size and scent (sku level).

• Most companies find a happy medium and base the level they perform their planning on a number of factors, including:

Information needed by other corporate departments such as finance, order entry, manufacturing and production planning.

Cost/benefit of time required to do specific level of planning to the sales force.

Page 18 of 38

Include customer needs/preferences in promotion planning.

• Utilize account teams and joint planning processes where applicable.

With key accounts or national accounts, a new model leading sales organizations are working towards is one made up of account teams where the members of the team represent areas/services the retailer values. As an example, if a retailer values category management, a category manager would be part of the account team. For every account team member on the manufacturing side, there is a corresponding member on the buyer’s side. Leading sales organizations are working towards collaboratively developing their promotion plans with this knowledgeable account team where the manufacturer and retailer work together to determine which promotions would be most effective for both of them.

Take into account customer promotions when creating your promotion plan. Simulation vs. Historical Planning

• Many companies simply plan based on their prior year events. “This seemed to work last year so let’s do it again”. Other, more progressive companies will incorporate these past events with current strategies and guidelines communicated by marketing and sales management for the coming year. At the leading edge, companies are developing plans based on simulation/”what if” projections of event volume, spending and ROI aggregated into a total projected plan. Software is available to perform this what-if analysis (IRI, ACNielsen and AIM within the

consumer products industry). It is important to note, however, that common sense and human interaction is still necessary to incorporate knowledge of upcoming events (i.e. a competitor just released a new product so past history is not as reliable).

Planning Horizon

• The length of time that a plan will cover will vary by manufacturer, with event by event planning at the low end and long term six month to one year plans at the high end. These longer range plans should be a collaborative effort created with the customer, based on volume, spending and ROI targets.

Approval Process Options

• Who approves promotions and when they need approval varies by manufacturer. Options include: All events require approval. Events outside of predetermined guidelines require approval. Total plan determines whether approval is required rather than individual events. Total plan

requires approval only if total projected plan does not meet target objectives (volume, spending, ROI).

Page 19 of 38

STEP 3: Sell-in Promotion Plan

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION

After a plan is developed and has received internal corporate approval, it is ready to be presented to the customer for their approval and to obtain the customer’s commitment to meeting the sales projections given the designated promotional spending.

During the account planning process, many companies will be meeting with their customers to finalize the account plan. The promotion plan will often be discussed at these meetings as well.

FLOW

INPUTS

• Promotion Plan by Account/Product: The promotion plan created in Step 2 is shown to the customer during the Sell-In Promotion Plan step.

See step 2 outputs for additional information on the components of the promotion plan.

Prepare for Customer Questions

Present Plan to

Customer

Revise Plan as Needed

• Committed Promotion Plan by Account/ Product

• Promotion Plan by Account/Product

• Historical shipments • Historical

consumption data • Past promotion

history • Customer Promotion

Calendar • Historical Account

Activity

Commit the Plan

Page 20 of 38

• Historical Shipments: Past shipment data will be used to show the customer how the current plan varies (or does not vary) from the past.

See step 1 inputs for a further definition of historical shipments.

• Historical Consumption Data: Past consumption data will be used to show the customer their historical sales to end-consumers and how the new plan compares to the past.

See step 2 inputs for a further definition of consumption data.

• Past Promotion Results: Past promotion results are used to show the customer what has and has not worked in the past and how the new plan compares to the past.

See step 2 inputs for further information about past promotion results.

• Customer Promotion Calendar: The promotion plan will be mapped against the customer’s promotion calendar to show how the planned events fit with the customer’s overall promotion plan.

See step 2 inputs for a further information about the customer promotion calendar.

• Historical Account Activity: Results of account meetings, activities and issues addressed should be maintained for each account. Information related to past promotion activities and issues is useful in anticipating customer questions and objections to future promotions.

OUTPUTS

• Committed Promotion plan by Account/Product: At the completion of this step, the promotion plan developed during Step 2 will be marked as committed to by the customer – the customer agrees to the volume goals given the spending provided.

ACTIVITIES

Activity 1: Prepare for Customer Questions

A. Review Historical Data

• Prior to meeting with the customer, it is important to review historical data on the customer and to understand past issues.

B. Anticipate customer questions and objections

• Using his understanding of customer “hot buttons”, the sales representative can anticipate questions and objections to the current promotion plan that will be presented.

• The sales representative should formulate responses to anticipated questions and objections in advance.

Activity 2: Present Plan to Customer

A. Prepare Customer Presentation

• Presentation to the customer should include several components:

Calendar showing all the promotional events you plan on running with the customer during a designated time frame alongside corporate merchandising and advertising events.

Page 21 of 38

Supporting materials for the promotion (display material, advertising material, contests, packaging)

Clearly stated expectations of the number of cases that the customer is expected to buy along with what you will be giving the customer to participate in promotional activities.

Anticipated customer volume (consumption) and profitability.

B. Schedule and Conduct Presentation

Activity 3: Revise Plan as Needed

A. Update Plan based on Customer comments

B. Obtain internal approval as needed

• If the customer revisions have an impact on projected revenues or budget, they need to be routed through internal approval once again.

Required secondary approval steps and guidelines will vary by manufacturer.

Activity 4: Commit the Plan

A. Interface plan with manufacturing for volume forecasting

• The overall sales plan is initially sent to manufacturing when completed. However, the promotion plan now gives an even further level of detail on the products to be sold. Manufacturing should reconcile this data to their production forecast.

B. Set up plans in order entry/invoicing system

• The specific promotions need to be set up in the order entry and invoicing system so that orders will be generated taking into account the guidelines and prices specified in the promotion plan. As an example, if part of the promotion plan involves $2.00 off invoice for every cased of bar soap sold to XYZ Grocery during the month of July, this needs to be recorded to ensure that Vons will receive the appropriate discount on the cases of bar soap they order during the month of July.

C. Set up plans in accounting system

• In order to ensure timely payment of promotion checks and to accurately track promotion spending, it is important to have promotions tightly integrated with accounting systems. If these are not automated interfaces, promotion information should be entered into accounting systems manually.

DESIGN CONSIDERATIONS Commitment of the Plan

• Plan commitment may take place either after internal approval or after the final customer acceptance.

• When a plan is committed, some manufacturers will want to save this plan as a “baseline” to compare to at the end of the planning period.

Approval of the plan

Page 22 of 38

• Whether or not the plan requires another round of approval after changes are made by the customer will vary by manufacturer. In many instances, the plan or events will only require additional approvals if the revenue or spending projections have changed.

• Companies may utilize the same approval process that was used during the creation of the promotion plan, or they may have a simplified approval approach for changes to the plan.

Integration with other systems and departments

• The promotion plan contains information that is useful across the company (customer accounting, manufacturing, customer service, etc.). Rather than keep this plan as a sales and marketing document, leading companies are sharing the plan across departments. This sharing can be manual or automatic links to other systems.

STEP 4: Execute Promotion Plan

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION The promotion plan documents what the manufacturer will do for the retailer in exchange for what the retailer will do for the manufacturer. During this step, the manufacturer needs to actually execute their side of the plan based on previous commitments. This will entail finalizing ads where appropriate, performing retail activities as needed, and giving appropriate payments and discounts. In addition, the manufacturer will want to monitor retail activities to ensure that their customers are acting as agreed.

FLOW

Assist inMerch and

Advertising

MonitorRetail

Activities

AuthorizePayments

• Completed Event/Proof ofPerformance

• Customer Payment• Closed Deduction

• Promotion Plan byAccount/Product

• Shipments• Retailer Performance Resolve Deductions

Page 23 of 38

INPUTS

• Promotion Plan by Account/Product: The promotion plan developed and committed in steps 2 and 3 is required to understand performance requirements of both the manufacturer and the retailer.

See step 2 outputs for additional information on the components of the promotion plan.

• Shipments: During this step, we will view the volume of actual product shipments sent to each account to confirm retailer performance and to make payments as applicable.

• Retailer Performance: Retailer Performance has two components: Consumption Data:

Some companies will pay funds to their customers based on actual consumption data (sell through) rather than on shipments to prevent forward buying and diverting. In this instance, actual consumption data will be needed during the execute step as it becomes available. See step 2 inputs for a further definition of consumption data.

Compliance Data: Syndicated data sources will provide information that can be used to see if the retailer complied with the parameters of the promotion (consumer price for the product, number of participating stores, % of stores displaying the product) The manufacturer may also receive some “proof of participation” from the retailer (such as a copy of an in-store ad or newspaper insert featuring the manufacturer’s product)

During this step, we will be looking at actual compliance and consumption data and comparing that to our planned consumption for the product.

OUTPUTS

• Completed Event/Proof of Performance: At the end of this step, the event will be completed and proof of retailer performance (did they really run the ad, display, etc). will be obtained. If the proof of performance is not available, payment should not be made.

• Customer Payment: Where proof of performance is met, payment will be made to the customer based upon the spending agreed to in the promotion plan.

• Closed Deduction: Deductions occur when the customer pays less than their full invoice amount. They often do this because prices and discounts on the invoice do not match what was agreed to with the manufacturer or because the manufacturer owes them money for promotion performance and has not yet paid. During this step, deductions will be reconciled against the promotion plan and proof of performances are cleared where appropriate.

ACTIVITIES

Activity 1: Assist in Store Merchandising and Advertising

A. Finalize ad, price, etc. as agreed to in the promotion plan

B. Execute any agreed to store level merchandising

• Some manufacturers utilize their own employees to set up displays or perform other merchandising activities. Other companies hire third parties to perform their merchandising. Some manufacturers

Page 24 of 38

pay the retailers to perform their merchandising activities. Merchandising activities can typically be performed by part-time and lower cost employees.

Activity 2: Monitor Retail Activities

A. Monitor Retail Activities/Conduct Store Checks on Major Sales Drives

B. Verify and document performance • This would include verifying an ad you agreed to run for your product in the retailer’s weekly

circular was actually run, an end aisle display was set up correctly, etc. Some companies will have their own account managers do these store checks; other companies will hire a third party company to do them. PIA is a common company used to perform these lower level merchandising/monitoring activities.

• Plans for a chain may include an expected level of participation in the promotion by stores in the chain. For example, 80% of stores in the chain are expected to have an end-of-aisle display.

Activity 3: Authorize Payments

A. Review event performance vs. commitments

B. Authorize payment to customer if customer is eligible

C. Send payment authorizations to Accounts Payable

D. Check to see if open deduction for performance before making payment

• If applicable, apply payment amount to deduction

Activity 4: Resolve Deductions

A. Establish agreed to process for dispute resolution

B. Receive open deductions for customer from Accounts Receivable

C. Match open deductions to promotion commitments

D. Send “matched” deductions to Customer Service/Accounts Receivable to clear DESIGN CONSIDERATIONS System Links with Order Entry

• When executing promotions, often times off-invoice payments are made. In these instances, the order entry and invoicing systems need to know the terms of promotion plan agreements. This process should happen via an automatic link, but may often be a manual interface until the promotion planning system becomes enterprise wide.

• Capturing promotions in order entry can also enhance deduction processing. Ideally, promotion numbers are captured on orders and processes are built in for the system to automatically clear most deductions.

Payment options

Page 25 of 38

• Manufacturers have many payment options available to them when promotion performance has occurred. Any of these payment methods are acceptable. However, it is important to explicitly communicate preferred payment options and to establish processes for executing those options. Many problems exist when retailers and manufacturers are expecting payments in different forms. Typically payment options include:

Gelco Draft: Gelco is a commonly used third party company for processing promotion payment checks.

Separate Check: The manufacturer may directly issue a check to retailers for promotion performance.

Credit Memo: The manufacturer may issue a credit memo to the retailer to apply to future invoices.

Off-invoice: The manufacturer may take money directly off the invoice. This is typically done on a per case basis. The invoice will show the regular price and a “sale” price.

Pre authorized deductions: In some cases, manufacturers welcome deductions from retailers. However, it is important that the manufacturer be expecting these deductions and have the appropriate clearing processes/systems in place to handle the deduction.

Prepayment: In this case, a manufacturer will pay the retailer prior to the promotion event being performed. This ensures that retailers are paid on a timely basis and eliminates the need for a deduction. However, many manufacturers do not favor this option because they are concerned with non performance on the retailer’s part.

STEP 5: Monitor/Revise Promotion Plan

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION The promotion plan acts as a guide for understanding the promotion spending and expected sales volume at each account. An effective account manager will follow this plan to ensure that he is meeting guidelines. During the planning period, any changes to the plan should be recorded along with actual performance so that there is always a clear picture of expected performance and so that changes can be made early on if expectations are not being met.

Page 26 of 38

FLOW

TrackActuals vs.

Plan

MonitorInventory/Shipments

MonitorTrade

Budgets

• Updated Promotion Planby Account/ Product(Current Forecast)

• Promotion Plan byAccount/Product

• Shipments• Retailer Performance

RevisePlan asNeeded

INPUTS

• Promotion Plan by Account/Product: The promotion plan developed and committed in steps 2 and 3 is required as the baseline to compare actuals to and to make revisions against.

See step 2 outputs for additional information on the components of the promotion plan.

• Shipments: During this step, we will be monitoring the volume of actual product shipments sent to each account as they occur. These shipments are compared to our planned shipments.

• Retailer Performance: Retailer Performance has two components: Consumption Data:

Some companies will pay funds to their customers based on actual consumption data (sell through) rather than on shipments to prevent forward buying and diverting. In this instance, actual consumption data will be needed during the execute step as it becomes available. See step 2 inputs for a further definition of consumption data.

Compliance Data: Syndicated data sources will provide information that can be used to see if the retailer complied with the parameters of the promotion (consumer price for the product, number of participating stores, % of stores displaying the product) The manufacturer may also receive some “proof of participation” from the retailer (such as a copy of an in-store ad or newspaper insert featuring the manufacturer’s product)

During this step, we will be looking at actual compliance and consumption data and comparing that to our planned consumption for the product.

OUTPUTS

• Updated Promotion Plan by Account/Product (Current Forecast): As promotion events are occurring and we are able to compare are actuals to our initial plan, we will modify the plan to account for variances. The outcome of this step will be a current version of the plan based on current knowledge and actuals. If updated diligently, this updated plan should always represent the current forecast of total sales and spending during the planning period.

ACTIVITIES

Activity 1: Track Actuals vs. Plan

A. Apply actual figures to planned as available

• Actual cases

Page 27 of 38

• Actual revenue generated

• Actual promotional spending

• Actual profitability

• Participation

• Compliance with promotion parameters (price, stores w/displays, copies of ad features.)

Activity 2: Monitor Inventory/Shipments

A. Compare next weeks planned shipments to inventory

• This is a best practice to prevent out of stocks during critical promotion periods. It is not currently seen at many clients.

• Timing of this activity (days, weeks) can vary based on cycle times.

Activity 3: Monitor Trade Budgets

A. Review and monitor trade budgets

• Capture promotion commitments/liabilities

Activity 4: Revise Plan as Needed

A. Identify variances to plan

• Progressive companies are using intelligent agents to scan for exception situations during execution. In other companies, more manual methods are used and events are often only spot checked.

B. Revise the plan as needed to meet new customer and business demands

• Significant differences to plan may require mid-course corrections. For example, expediting additional shipments to support strong early promotion results or seeking additional funding when promotion shipment volume is weak.

C. Obtain internal approval as needed

• If the customer revisions have an impact on projected revenues or budget, they need to be routed through internal approval once again.

Required secondary approval steps and guidelines will vary by manufacturer.

DESIGN CONSIDERATIONS Using the plan as a current “forecast”

• If the plan is monitored frequently and updated to show current actual shipments plus current expected shipments, it provides a detailed forecast of total expected shipments at the end of the period. The benefit of this forecast vs. the time commitment needed to keep the plan updated should be addressed.

Capturing qualitative information about the event

• To make historical information more useful, it is important to capture other “causal” information that may have impacted the success of the promotion for this account. This may include

Page 28 of 38

competitive activity, weather conditions, unusual publicity about the product or category (such as a story in Newsweek saying that oat bran lowers cholesterol), etc.)

Approval of the plan

• Whether or not the plan requires another round of approval after changes are made during execution will vary by manufacturer. At this stage in the process there is little that can be done about volume changes and thus approval is typically not required. Additional spending will often require approval.

• Companies may utilize the same approval process that was used during the creation of the promotion plan, or they may have a simplified approval approach for changes to the plan.

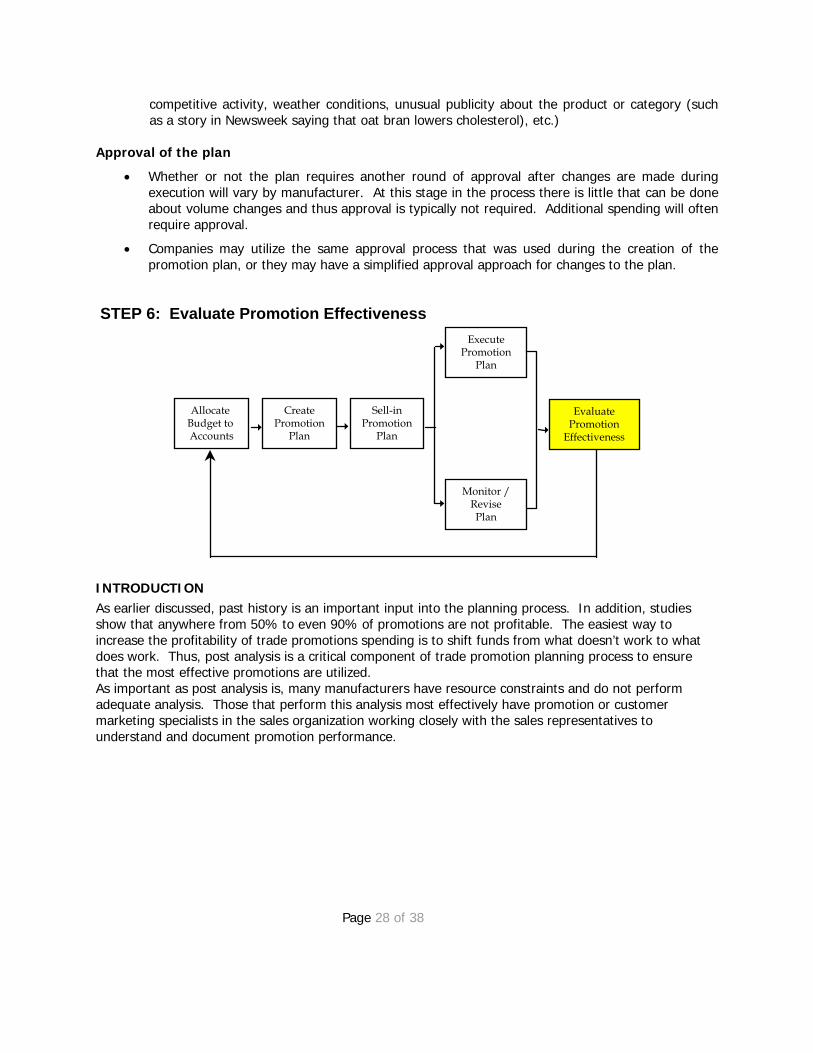

STEP 6: Evaluate Promotion Effectiveness

Allocate Budget to Accounts

CreatePromotion

Plan

Sell-inPromotion

Plan

ExecutePromotion

Plan

Monitor /RevisePlan

EvaluatePromotion

Effectiveness

INTRODUCTION As earlier discussed, past history is an important input into the planning process. In addition, studies show that anywhere from 50% to even 90% of promotions are not profitable. The easiest way to increase the profitability of trade promotions spending is to shift funds from what doesn’t work to what does work. Thus, post analysis is a critical component of trade promotion planning process to ensure that the most effective promotions are utilized. As important as post analysis is, many manufacturers have resource constraints and do not perform adequate analysis. Those that perform this analysis most effectively have promotion or customer marketing specialists in the sales organization working closely with the sales representatives to understand and document promotion performance.

Page 29 of 38

FLOW

INPUTS

• Promotion Plan by Account/Product: A copy of the baseline and current plans (if they are both available) is necessary for comparing actual performance to plan during the post analysis step.

See step 2 outputs for additional information on the components of the promotion plan.

• Shipments: Reports of actual product shipments to each account are required to compare to the plan.

• Consumption Data: Actual consumption data, if available, is needed to understand the end result of each promotion. How much was actually purchased by the end consumer?

See step 2 inputs for a further definition of consumption data. OUTPUTS

• Promotion Results: During this step, we will analyze and document the results of the promotion plan. These results are a key input to future planning sessions. This should include qualitative data about the other “causals” that may have impacted the plan.

• Promotion Effectiveness Scorecard: Leading edge manufacturers will develop a formal scorecard to consistently and effectively perform post analysis.

ACTIVITIES

Activity 1: Gather Promotion Results

A. Gather Actual Shipments

B. Gather Actual Consumption

C. Gather Actual Spending

Activity 2: Evaluate Individual Promotions

A. Calculate Performance Metrics

• Several metrics are used to analyze the effectiveness of a given promotion

% Lift: To determine which event type provided the largest sales increase.

Weighted Weeks of Support:

Gather Promotion

Results

Evaluate Individual

Promotions

Document Promotion Learnings

• Past Promotion Results

• Promotion Effectiveness Scorecard

• Promotion Plan by Account/Product

• Shipments • Consumption Data

Page 30 of 38

To understand the quality of support and type of ad support for the event activity.

Pass-through Analysis: To determine what amount of merchandising funds have been passed through in terms of reduced price to the consumer.

Trade Margin Analysis: To identify whether an account is inclined to invest in brands and categories.

Spending Efficiency: To determine the relative return on merchandising fund investment at the account level.

Cost Per Incremental Case: To determine the cost of each incremental case sold during an event.

Profit Per Incremental Case: To evaluate the profit generated by each incremental case sold during an event.

• Metrics can be documented on a promotion effectiveness scorecard for consistent documentation and easy viewing.

B. Review performance metrics and determine root cause of problems

Activity 3: Document Promotion Learnings

A. Document customer and event learnings

• Document external factors such as retail competitor actions, significant out-of-stocks or seasonality that may help interpret promotion results.

• Document additional learnings about what did and did not work well with the promotion.

B. Share findings within and between companies

• Communicate findings to other departments (marketing, manufacturing, customer accounting, etc.) and mutually develop recommendations for the next planning cycle.

• Communicate findings to business partners and customers to help them understand what does and does not work.

DESIGN CONSIDERATIONS

Tie consumption data back to promotions When estimating the effectiveness of a promotion, it is important to understand not only how much product was shipped to the retailer, but how much of your product was actually purchased by the end consumer. This data helps manufacturers control things such as diverting products and forward buying by the retailer. It also helps the manufacturer understand which promotions were truly effective and which were not.

• Don’t underestimate the complexity. Consumption data is purchased from third parties such as IRI and ACNielsen or from retailers. Because of this, the manufacturer does not have any control on how they get this data or how the 3rd parties track this data. If the manufacturer tracks and plans for their promotions at a different level than the 3rd parties track actual consumption, it is difficult to tie this data back to the promotions. Decide early what data you need to tie together and ensure that systems and processes are in place to appropriately track the data.

Page 31 of 38

At what level should analysis be performed – Product or Account? Post analysis should actually be performed at both the product/brand and the account levels.

• Typically overall product or brand analysis will be conducted by a marketing brand manager. He is interested in determining which brands and products should get future promotional dollars and how should future funds be allocated.

• Customer level analysis will be done by the field sales representatives and trade marketing specialists within the sales department. They are interested in which events look most promising for the account, in light of past performance, and how to maximize future event performance.

4. Roles There are several people involved in the trade promotion process, all with unique skills and responsibilities. In leading edge companies, these roles are assembled into a cross-functional account team to serve each customer as effectively as possible.

• Marketing Brand Managers:

Responsible for providing marketing plan and high level spending budgets to sales for a particular brand or brand group

Establishes national level promotions and promotion guidelines

Performs post promotion analysis at a brand level

• Sales Management:

Overall ownership for meeting sales volume and profitability goals within pre determined spending budgets

Allocates quotas and budgets to a sales representative or account level

Provides guidance during the creation of the promotion plan

Acts as a primary approver of the plan

• Field Sales Representative/Account Manager:

Primary responsibility for creating the promotion plan

Sells in promotion plan to customers

Executes and tracks plan

Performs post analysis at an account level

• Customer Marketing:

Promotion Specialists within the sales or marketing organization

Assists in plan creation and post analysis

Acts as a reviewer of the plan

• Customer Accounting:

Monitors spending budgets

Page 32 of 38

Oversees payment of promotion dollars

5. Key Process Measurements

• Trade Promotion Spending as a Percent of Sales: A common goal of initiating effective trade promotion practices and analysis is to be able to more efficiently spend trade promotion dollars – getting more revenue gains for fewer dollars. Measuring trade fund spending as a percent of sales will help to determine if we are meeting that goal.

• Return on Investment for Promotion Dollars: Currently many manufacturers look at revenue and case volumes rather than ROI. Implementation of effective trade promotion processes will enable us to capture ROI and to see it increasing.

• Accuracy of promotion plan – revenue and spending projections: Compare actuals to plan and document where differences occur. Over time we should see greater accuracy of the plans – eventually leading to better production scheduling and reductions in the number of out-of-stocks.

• Number of outstanding deductions: The overall deduction balance should decrease over time

• Time to resolve deductions: The amount of time needed to resolve and clear a deduction should decrease.

• Additional distribution for a product

• Adding more facings for an established brand: Gaining facings for a new product

• Consistency of product demand: While promotions are being run, we will often see huge increases in shipments of the promoted products followed by little or no demand for the product. This indicates that retailers are forward buying the product at the lower promotion price and storing it for future sales. The overall promotion strategy and plan should look to reduce the amount of forward buying and diverting by retailers and even out the demand.

6. Overall Design Considerations National versus account specific promotion planning

• One of the issues manufacturers deal with today is what sort of guidelines to give their sales representatives when planning trade promotions. There are two different methods they may use or they may choose a combination of the two.

Account Specific Promotion Spending: One method companies use is to give the sales representatives a budget for their trade promotions and allow them to tailor the promotions individually to the customer with no guidelines from corporate.

Advantages:

♦ Allows the sales representative, who knows the customer’s needs best, to tailor the plan specifically to meet their customer’s needs.

Disadvantages:

Page 33 of 38

♦ Sales representatives are not promotion experts and hence, may not know which promotions are most effective.

National Promotion Spending: Another method companies use is to have the marketing department define a list of national promotions. The sales representatives are given the list of these national promotions and choose which promotions they will run for their accounts.

Advantages:

♦ Gives sales representatives specific promotion guidelines and provides them a little lead way on customizing the promotions for their accounts.

♦ It is easier to set up the various promotions in the system since it can be done at a national level rather than by specific accounts.

Disadvantages:

♦ Less flexibility to tailor promotions to individual customer needs.

Common Problems / Issues

• Over-promoting the brand may erode baseline volume.

• Too much promotion creates an expectation for the consumer that they should only buy the brand when it is “on sale” leading to an erosion of baseline volume. In effect, you are “paying” the consumer to buy a product that they would have otherwise purchased at full price.

• Under-promoting the brand may lead to loss of market share and distribution. If the brand is not promoted, consumers may buy other brands that are “on sale” instead of paying full price.

• Plan not tied to clearly defined goals and customer strategy. There are several typical “disconnects” when creating a promotion plan. Before embarking on the trade promotion planning process, these “disconnects” should be addressed.

Targets are often not established up-front for trade promotions.

Brand/sku level spending efficiency and promotion profitability is not known.

Strategy decisions are made without factual basis.

The role of trade promotion by brand is not clearly articulated or communicated to the field.

7. Trade Promotion Best Practices • Deal Simplification

Deal simplification looks to reduce the administrative costs of running promotions. The complexity of managing many fund options across many events consumes an estimated 30% to 50% of an account manager’s time. The challenge lies in striking the right balance between automating and standardizing processes to manage this complexity and maintaining the incentive to perform.

Manufacturers have sought to simplify trade promotions by:

Reducing the number of options

Standardizing promotion frequency

Page 34 of 38

Offering advance payments

Simplifying off-invoice allowances

• Joint Planning

Although manufacturers can impose new promotion structures and plans on their own, it is a best practice to work in concert with retailers in planning promotions.

By planning promotions together, manufacturers and retailers can develop more informed production and operating plans.

Joint planning of events (their frequency, timing, conditions and configuration) greatly reduces the uncertainty in promotion events and performance thus helping to better understand the supply chain.

Processes and technology should be flexible enough to catalog, track, and share customer specific information and include customer preferences and needs as part of the standard process.

• Use of Post Analysis

As mentioned earlier, up to 90% of promotions ran are not profitable. Post analysis is an essential best practice to understand what does and does not work to better plan future promotions.

• Revisit the strategic role of the promotion

While trade promotions will not disappear from the industry landscape, manufacturers should reconsider its use.

The key question is, Would less traditional, more targeted alternatives for reaching consumers, like retailer’s card based programs and co-marketing solutions be a better use of marketing dollars?

Whatever the promotion strategy, it should be clearly communicated and incorporated into each individual promotion plan.

• Continuous planning – moving away from planning twice a year to continuous learning and plan adjustments throughout the year.

• Align incentives to specific performance

Currently, most sales representatives are incented on meeting specific volume projections.

To obtain maximum ROI, sales representatives should be incented on meeting profitability measures and account goals.

8. Other Facts to Consider • Amount of trade promotion spending is dependent on brand recognition The number of trade promotions you run is very dependent on where you stand in the overall

marketplace. As an example, for Dial, with the exception of their soap, most their products are not #1 in the marketplace. Hence, customers do not demand certain Dial products causing Dial to have to put money into trade promotions to move their products. On the other hand, Proctor and Gamble have a number of products that are #1 in the marketplace which do not require such a heavy investment in trade promotions to move their products. Specifically, Dial makes Purex soap. If a

Page 35 of 38

retailer does not carry Purex, most consumers would simple grab another brand of detergent and continue shopping at that retailer. On the other hand, Proctor and Gamble make Tide. If a retailer does not carry Tide, some consumers would actually go to another retailer who did carry that brand.

• Facts for ACNielsen’s Seventh Annual Survey of Manufacturer Trade Promotion Practices, 1997

Trends in Trade Promotion Spending Trade promotion spending as a percentage of sales is 13% and has been constant from 1991

- 1996. Food manufacturers are the only industry showing an increase in trade promotion spending, while both Health and Beauty Care and General Merchandise/Non Food manufacturers indicate lesser levels of spending.

Manufacturers report a slight drop off in the share of advertising and promotion dollars allocated to trade promotions in 1996. Trade promotion spending accounts for 54% of the advertising and promotion budget, compared to 58% in 1995.

The slight reduction in trade promotion spending as a percent of advertising is due to increases in the dollars spent on media advertising (i.e. commercials).

The allocation of trade promotion funds is becoming more fragmented as manufacturers use a variety of tools to influence sales. Off-invoice allowances still represent the largest part of trade promotion spending; however, this tool is declining in importance while street money, pay for performance plans, and frequent shopper programs are expected to increase.