Embed Size (px)

Citation preview

Santander Latin America Santander Latin America Energy & Materials Energy & Materials

October 2009 October 2009 -- LondonLondon

2

This presentation contains forward-looking statements. Such statements are not

statements of historical facts, and reflect the beliefs and expectations of

Braskem’s management. The words “anticipates”, “wishes”, “expects”,

“estimates”, “intends”, “forecasts”, “plans”, “predicts”, “projects”, “targets”

and similar words are intended to identify these statements. Although Braskem

believes that expectations and assumptions reflected in the forward-looking

statements are reasonable based on information currently available to Braskem’s

management, Braskem cannot guarantee future results or events.

Forward-looking statements included in this presentation speak only as of the

date they were made (June 30, 2009), and the Company does not undertake any

obligation to update them in light of new information or future developments.

Braskem shall not be responsible for any transaction or investment decisions that

are taken based on information included in this presentation.

ForwardForward--looking Statementslooking Statements

3

� The Company & 2Q09 Financials

� Key Differentiators

3

� Petrochemical Industry

AgendaAgenda

4

� Leading petrochemical company in Latin America

� Third largest resins producer in the Americas

� Diversified portfolio of petrochemical products, with focus on PE, PP and PVC

� 18 facilities plants in Brazil and annual production capacity of 11 million tons of chemical and petrochemical products

� Key financials, 2008Gross revenue = US$ 12.8 billionNet revenue = US$ 10.0 billion (78% in Brazil)EBITDA = US$ 1.3 billionAssets = US$ 9.7 billion

� Listed at BM&F Bovespa, NYSE and LATIBEX100% tag along

Braskem in a snapshotBraskem in a snapshot

5

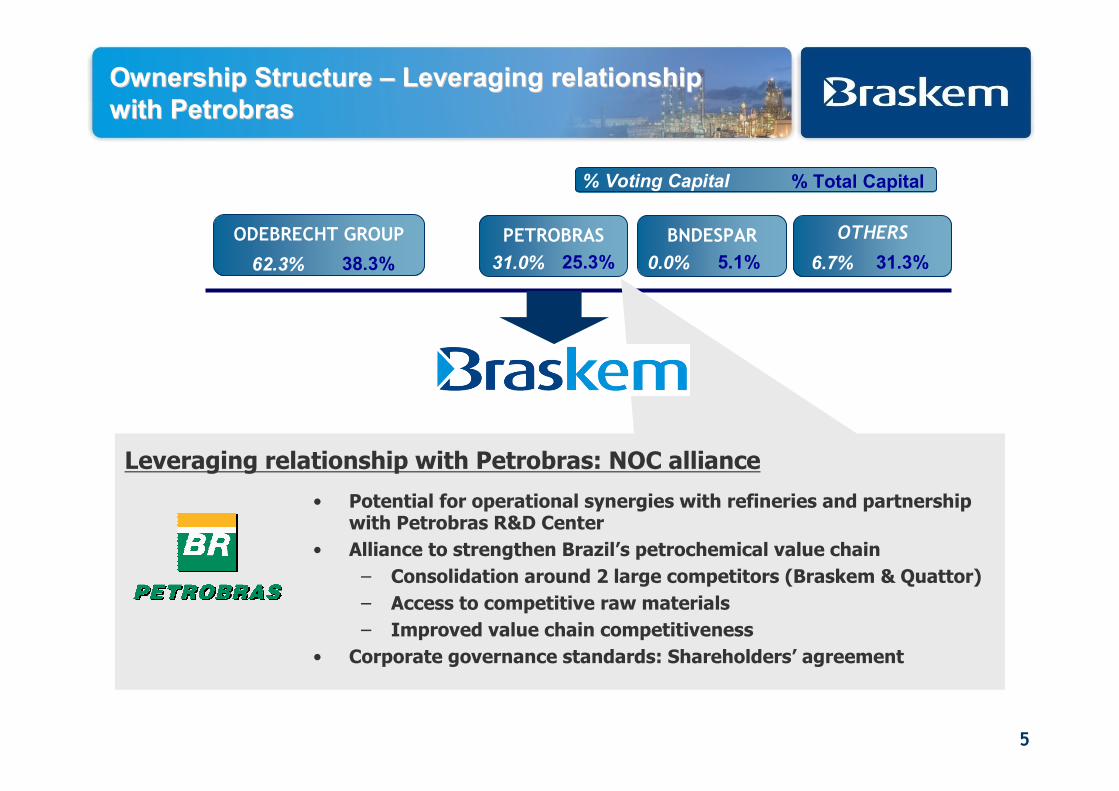

• Potential for operational synergies with refineries and partnership with Petrobras R&D Center

• Alliance to strengthen Brazil’s petrochemical value chain

– Consolidation around 2 large competitors (Braskem & Quattor)

– Access to competitive raw materials

– Improved value chain competitiveness

• Corporate governance standards: Shareholders’ agreement

Leveraging relationship with Petrobras: NOC alliance

ODEBRECHT GROUP

38.3%62.3%

PETROBRAS

25.3%31.0%

OTHERS

31.3%6.7%

BNDESPAR

5.1%0.0%

% Voting Capital % Total Capital

Ownership Structure Ownership Structure –– Leveraging relationship Leveraging relationship

with Petrobraswith Petrobras

6

ConvertersBasic petchem Resins

Industrial integration

PE/PP/PVCPE/PP/PVC

Oil/Gas-refineries

Naphtha/GasNaphtha/Gas

Source: Braskem / Abiquim

Resins Market Share Resins Market Share 20082008

51%51%

Enhanced competitiveness through value chain Enhanced competitiveness through value chain

integrationintegration

7

2012

2002

Rank amongst the Rank amongst the 10 10 largest petrochemical largest petrochemical companies companies in the worldin the world

measured bymeasured by EV*EV*

Become the Become the largestlargestthermoplastic resins thermoplastic resins producer in Latin producer in Latin

AmericaAmerica

2006TrikemTrikem

2007PolialdenPolialden

PolitenoPolitenoIPQ / CPSIPQ / CPS

2000 2002 2004 2005 2006 2007

1,734

3,045 3,2253,621

5,551

3,145

2008

5,901

Organic growth

Acquisitions

Braskem’s Ethylene and resins capacity (kt) 23% CAGR

2008

PauliniaPaulinia

* Enterprise Value

TriunfoTriunfo

2009

Track record of strong and consistent organic Track record of strong and consistent organic

growth and acquisitions growth and acquisitions

6,113

2009

8

Structured resource base to support client needs

�Over US$ 190 million in R&D assets

�> 170 researchers

�8 pilot plants

�> 240 patents filed

worldwide

�Partnership with universities and R&D centers in

Brazil and abroad

8

Applied Innovation and technology to strengthen Applied Innovation and technology to strengthen

value chain competitivenessvalue chain competitiveness

� Focus on product and application development

– 18% of resin sales derive from products developed in the last three years

– Focus on clients’ end users

� Targeted initiatives for breakthrough technology

– Intelligent packaging

– Renewables

Source: Braskem

9

� Venezuela:

� Polipropileno del Sur (Propilsur)

- Basic engineering and front end engineering design (FEED) concluded

- Program timetable altered: startup in 2013 and investments estimated at US$ 1.2 billion

� Polietilenos de America (Polimerica)

- Technology license agreements signed for the PE plants

- Program timetable altered: startup in 2014 and investments estimated at US$ 3.25 billion

� Peru:

− Braskem, Petrobras and PetroPerú concluded studies for the technical and economic pre-

feasibility phase of an integrated project to produce 700 kton to 1,200 kton of polyethylene using

the natural gas available in Peru as feedstock.

� Green PE:

− Cornerstone laid for its green ethylene plant in April/09

− Investments of R$488 million and startup expected for the end of 2010

− Financing package with BNDES approved in May/09

Growth combined withGrowth combined with

improved competitivenessimproved competitiveness

Source: Braskem

10

Global Scenario

� Oil price trend is still uncertain

− Economy recovery worldwide versus high inventory level

� Naphtha prices reflect the volatility of crude

� Petrochemical prices in the international market improved during 3Q09 but are expected to decrease for the 4Q09

− Commissioning of new plants

− Lower demand from converters

− Resin’s spread expected to be attractive

− Higher operating rates compared to 1H09

� Downturn cycle can last until 2011

Regional Scenario

� Braskem plants operating at full capacity

� Strong domestic demand during 3Q09 and favorable global scenario pressured prices upward

� Real appreciation and operational problems with Quattor lead imports to pick up again

� Inventory levels in the chain are still low

� Sales volume recovery for Mercosur, Bolivia and Andean countries

− Low consumer confidence and reduced liquidity still hurting Argentina’s economy

Global and Global and Regional Regional ScenarioScenario

Source: Braskem / CMAI / Quimax

11

100

500

900

1,300

1,700

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

PE PE US$/tonUS$/ton PPPP US$/tonUS$/ton

PVCPVC US$/tonUS$/ton

Source: CMAI (References PP, PE, PVC: Asia and Benzene: USA)

-31%

+55%

BenzeneBenzene US$/tonUS$/ton

-36%

+213%

+38%

-35%-44%

+48%

Recovery in resins and aromatics international Recovery in resins and aromatics international

prices till 3Q09prices till 3Q09

500

900

1,300

1,700

2,100

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

500

900

1,300

1,700

2,100

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

500

900

1,300

1,700

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

12

40

60

80

100

120

140

160

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

40

60

80

100

120

140

160

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

40

60

80

100

120

140

160

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

+37%

PE PE Dec07 = 100 basisDec07 = 100 basis PPPP

PVCPVC

Source: Quimax

-30%

-31%

+41%

+36%

-31%

Dec07 = 100 basisDec07 = 100 basis

Dec07 = 100 basisDec07 = 100 basis

FX impact on domestic pricesFX impact on domestic prices

13

27%18%

55%

29%

16%

PE PP PVC Total

Resins

Brazilian

Market *

Source: Braskem

Domestic Sales 1Q09 x 2Q09Domestic Sales 1Q09 x 2Q09 %%

Others

Imports

Resins Market Share 2Q09Resins Market Share 2Q09

* Braskem estimates: Domestic sales + imports

53%

28%

19%

Brazilian market showing significant evolutionBrazilian market showing significant evolution

14Source: Braskem

ResinsResins Sales Volume in the Sales Volume in the DomesticDomesticMarketMarket 3Q09 3Q09 TrendTrend in the in the DomesticDomestic MarketMarket

March performance shows trends for the March performance shows trends for the

upcoming quarterupcoming quarter

Volume Price Revenue Cost

PP

PE

PVC

BTX

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

15Source: Braskem

R$ million

EBITDA Higher basic petrochemicals prices and sales volume overcome exchange appreciation and raw material cost increase

EBITDA EBITDA Higher basic petrochemicals prices and sales volume Higher basic petrochemicals prices and sales volume overcome exchange appreciation and raw material cost increaseovercome exchange appreciation and raw material cost increase

FX Impact

on Costs

FX Impact

on Revenue

247

(334)

566

245787

96232

457

539 65

EBITDA

1Q09

Price Volume Raw

Material

Others

PIS/

COFINS

FX Other

Variable

Costs

Costs +

SG&A

EBITDA

2Q09

( ) ( )

( ) ( ) ( )

16Source: Braskem

R$ Million (06/30/09)

Gross DebtGross Debt: 10,583: 10,583

Net DebtNet Debt: 7,347: 7,347

Average TermAverage Term: 10.1 : 10.1 yearsyears

67% 67% of the debt are pegged to the USD of the debt are pegged to the USD

Net Debt / Net Debt / EbitdaEbitda (x) US$(x) US$Net Debt / Net Debt / EbitdaEbitda (x) R$(x) R$

526

1,091

1,6171,326 1,288 1,209

615

1,372976

1,768 610

1,468

PFICO

11% 10%

15%

13% 12%11%

6%

13%

9%

3,236

In US$

In R$Value related to the loan granted by a Petrobras subsidiary for the

delisting of Copesul, due in October 2009.

06/30/09 2009 2010 2011 2012 2013 2014/

20152016/

2017

2018/

20192020 onwards

Comfortable cash position, coveringComfortable cash position, covering

over 2 years of debt amortizationover 2 years of debt amortization

17

� The Company & 1Q09 Financials

� Key Differentiators

17

� Petrochemical Industry

AgendaAgenda

18

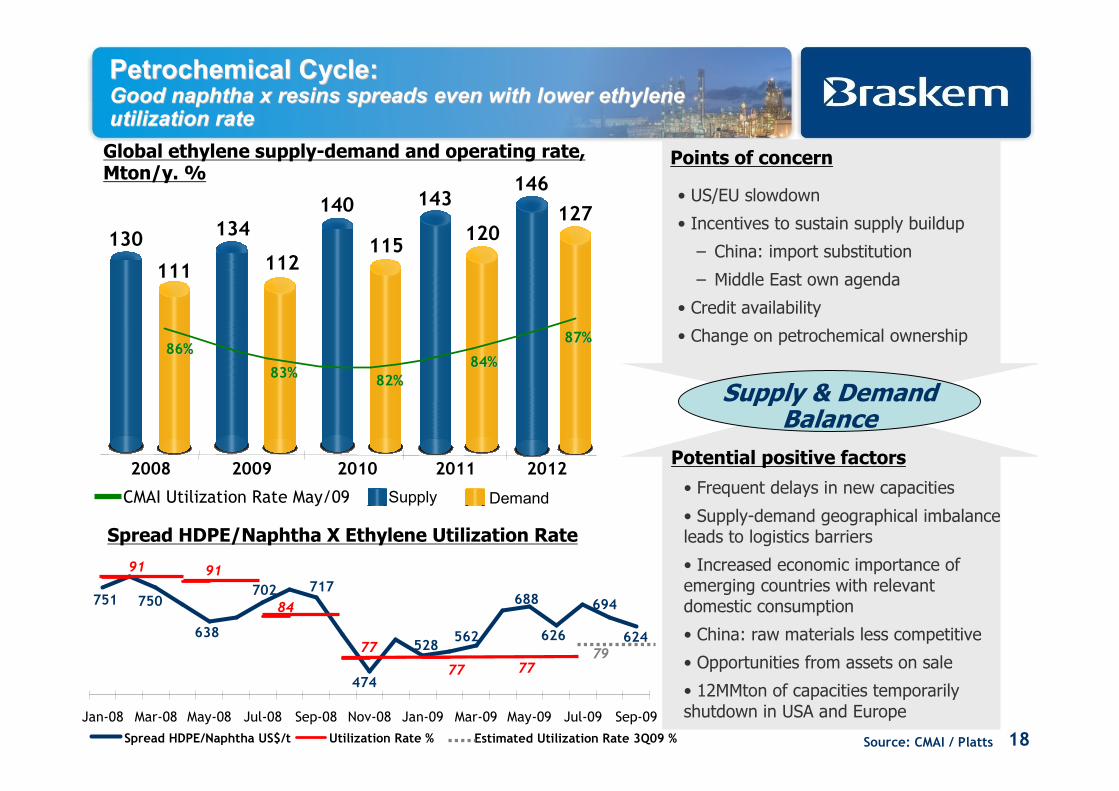

694

624562528

474

717751 750

638

702688

62677

91

84

91

77

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09

Spread HDPE/Naphtha US$/t Utilization Rate %

79

Estimated Utilization Rate 3Q09 %

77

Supply

130134

140 143

111 112115

120

2008 2009 2010 2011

146

127

2012

1 2 3 5CMAI Utilization Rate May/09 Demand

86%86%

83%83%82%82%

84%84%

87%87%

Source: CMAI / Platts

Spread HDPE/Naphtha X Ethylene Utilization Rate

Global ethylene supply-demand and operating rate, Mton/y. %

Potential positive factors

• Frequent delays in new capacities

• Supply-demand geographical imbalance leads to logistics barriers

• Increased economic importance of emerging countries with relevant domestic consumption

• China: raw materials less competitive

• Opportunities from assets on sale

• 12MMton of capacities temporarily shutdown in USA and Europe

Points of concern

• US/EU slowdown

• Incentives to sustain supply buildup

– China: import substitution

– Middle East own agenda

• Credit availability

• Change on petrochemical ownership

Supply & Demand Balance

Petrochemical Cycle:Petrochemical Cycle:Good naphtha x resins spreads even with lower ethylene Good naphtha x resins spreads even with lower ethylene utilization rateutilization rate

19

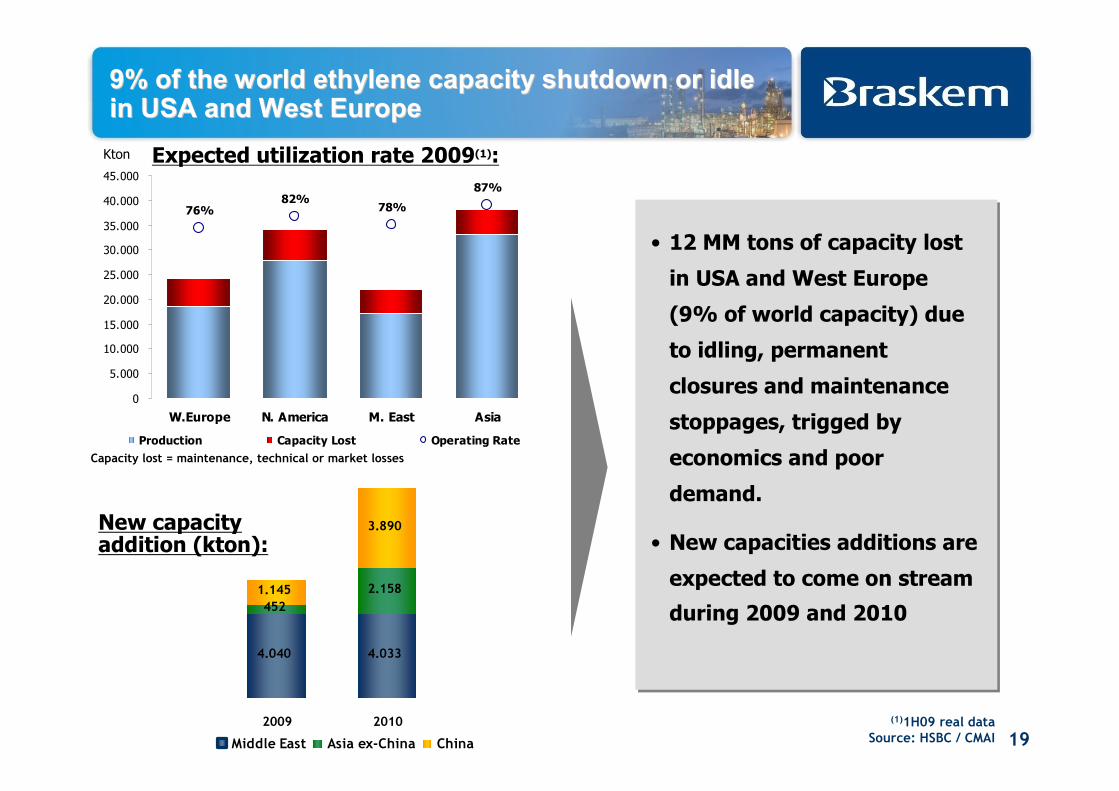

9% of the world ethylene capacity shutdown or idle 9% of the world ethylene capacity shutdown or idle in USA and West Europein USA and West Europe

76%82%

78%

87%

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

W.Europe N. America M. East Asia

Production Capacity Lost Operating Rate

(1)1H09 real dataSource: HSBC / CMAI

New capacity addition (kton):

Expected utilization rate 2009(1):

4.040 4.033

452

2.1581.145

3.890

2009 2010

Middle East Asia ex-China China

• 12 MM tons of capacity lost

in USA and West Europe

(9% of world capacity) due

to idling, permanent

closures and maintenance

stoppages, trigged by

economics and poor

demand.

• New capacities additions are

expected to come on stream

during 2009 and 2010

Kton

Capacity lost = maintenance, technical or market losses

20

� The Company & 2008 Financials

� Key Differentiators

20

� Petrochemical Industry

AgendaAgenda

21

-1

0

1

2

3

4

5

6

7

2007 2008 2009 2010

%

interest

-1

0

1

2

3

4

5

6

7

% GDP

GDP Inflation

Structural changes have prepared the country to the current environment

�Economic policy based on inflation target, fiscal responsibility and floating exchange rate

�Competitive, diversified and open economy

�Liquid financial system

�Mature democracy

�Broad and consumerist domestic market

�Greater competitiveness of Brazilian multinationals

�Focus on improving social conditions (health, education, income distribution)

�Sovereign debt in a record low, rated investment grade (S&P, Fitch)

Source: Tendências Consulting - Bradesco and Santander Perspectives (Sep/09)

GDP growth and inflation

Brazil: A stable economyBrazil: A stable economy

22

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

PE PP PVC

Brazil: dynamic market with still low per capita Brazil: dynamic market with still low per capita

consumptionconsumption

• PE, PP and PVC per capita consumption (Kg per person)

22

*Compound annual growth rate Source: CMAI

11.112.5

13.6 14.5 15.4 16.2 16.6 16.1 17.8 17.518.7 18.0

20.2

22.7

76

68

57

USA Europe Japan

Brazil

5.2%CAGR*

21.9

23

In Brazil, companies are exposed to a dynamic In Brazil, companies are exposed to a dynamic

market with resilient growthmarket with resilient growth……

• Domestic demand for resins

Source: Abiquim – domestic sales + imports

PEPPPVC

2,880

3,435 3,3773,694

2001 2004 2005 2006

4,048

2007

1,695

990

692

1,833

1,114

1,964

1,228

856

5.4%CAGR

10%

9%

749

• USA demand for resins (Kton)

23,276

25,90424,749

25,020

2001 2004 2005 2006

24,212

2007

6,350

6,081

6,287

12,826

6,153

12,638

5,421

-1.2%CAGR

-3%1%

5,907

12,318

Source: NAD - CMAI

4,172

2008

3%

5,922

11,091

5,563

4,328

1,833

1,114

749

2008

21,341

-12%

1,972

1,218

982

24

24

• 2 Top producers share• Number of Producers

Source: Braskem / CMAI

…… and a high level of consolidationand a high level of consolidation

2 2 2

1311

9

PE PP PVC

93%100% 100%

42%30%

52%

PE PP PVC

BRAZIL USA

25

Assure regional low-cost raw

material and energy supplies

B

Expand access to attractive markets

C

• Operational and commercial excellence

• Relationship with Petrobras

• Value-chain virtual integration– Refineries and raw materials

– Logistics and services

– Innovation and technology

• Enhancement of aromatics and crackers’products

• Regional leadership

• Gas crackers in Latin America

• Brazilian sugar cane ethanol

• Expansion of Green-PE and renewable

• M&As

• Global Alliances

Increase and protect core Latin American business

A

Strengthen current position

Grow w

ith val

ue cre

ation

Braskem is prepared to seize the opportunities Braskem is prepared to seize the opportunities

offered by this environmentoffered by this environment

Source: Braskem

26

Greater operational and financial strengthGreater operational and financial strength

� Continuous strengthening of long-term relationship with Clients

� Priority over financial health and liquidity

� Productivity Program: cost reduction

� Support the sustainability of the Brazilian petrochemical chain

� Construction of the Green PE plant

� Projects in Venezuela

� Analysis of opportunities arising from crisis: selective

acquisitions in North America

� Operational renewal: over 500 employees by 2011

FocusFocus

Santander Latin America Santander Latin America Energy & Materials Energy & Materials

October 2009 October 2009 -- LondonLondon

Appendix IAppendix I

28

29

Ideal product for kitchen cutting boards and playground toys

Internally developed technology for the production of UHMWPE

Pioneer on the production of metallocene PE in Brazil

Bags for Bread

Replacing paper bags

Shrink Films

Replacing paperboard boxes

Cisterns

PE replacing concrete

PE Innovation: Cases of SuccessPE Innovation: Cases of Success

30

High performance for the frigorific market

Developments for agricultural silo structure

Developments for truck liners:

anti-stick properties and high abrasion resistance

PE Innovation: Cases of SuccessPE Innovation: Cases of Success

31

Braskem product approved in

high speed BOPP production lines.PP Replacing PS

BOPP sealant layer High clarity PP grades

for rigid packaging

Disposable glasses replacing PS glasses

PP Innovation: Cases of SuccessPP Innovation: Cases of Success

32

PP Developments: Customer PartnershipPP Developments: Customer Partnership

Replacing steel in washing machine developments

Partnership in new packaging developments

33

33

Source: CMAI

Quattor** Solvay EcopetrolMexichemBraskem*

3,561

1,895

722 521 438692

Dow

**JV between Unipar (60%) and Petrobras (40%). The production is segregated between 1,020 kt in PE and 875 kt in PP

PVC

PEPP

2,340

FormosaDow LyondellBasell

Braskem ShintechIneos

5,416

3,561

4,706

2.902

2,895

400

4040

4,9762,469

2,237

1,995

1,040

526526

995

815

1,0921,092

810

Capacity of resins in Latin America, kton

Capacity of resins in Americas, kton

Brazilian assets

* Includes Petroquimica Triunfo´s plant

Resins Capacity in the Americas Resins Capacity in the Americas

1,085

34

World indicative ethylene cash costsWorld indicative ethylene cash costs

Source: CMAI

35

Financial highlightsFinancial highlights

Main Economic Main Economic IndicatorsIndicators

2Q09 2Q09 (A)(A)

1Q09 1Q09 (B)(B)

2Q08 2Q08 ( C)( C)

ChangeChange

% % (A)/(B)(A)/(B)

ChangeChange

% % (A)/( C)(A)/( C)

1H091H09(D)(D)

1H08 1H08 (E)(E)

Change Change

% % (D)/(E)(D)/(E)

Net Revenue 3,688 3,260 4,628 13 (20) 6,948 9,175 (24)

EBITDA 566 457 557 24 2 1,023 1,183 (14)

EBITDA Margin 15.3% 14.0% 12.0% 1.3 p.p. 3.3 p.p. 14.7% 12.9% 1.8 p.p.

Net Financial Result 1,192 (208) 386 - - 984 167 490

Net Income / Loss 1,156 10 404 - - 1,166 500 133

Source: Braskem

36

Revenues breakdown Revenues breakdown –– 2Q092Q09

BTX * 9%

Others 10%

Propylene 5%

Ethylene 4%

Resins 57%Fuel 4%

Butadiene 2%

Solvents 1%

Caustic Soda

3%

ETBE/MTBE 4%

Net Revenue by Product 1

(2Q09)

1 Does not include condensate processing and Ipiranga Química sales2 BTX - Benzene, Toluene, Ortoxylene and Paraxylene

37

COGS breakdown COGS breakdown –– 2Q092Q09

Naphtha /

Condensate

67,3%

Natural Gas 1,3%Fuel 1,6% Others 1,7%

Services 2,9%

Eletric Energy

6,3%

Labor 4,6%

Deprec / Amort

6,9%

Other Variable

Costs 7,3%

COGS 2Q091

1 Does not include condensate processing and costs of Ipiranga Química

sales

38

Utilization RateUtilization Rate %%

Source: Braskem

Resins ProductionResins Production KtonKton Basic Petrochemicals Basic Petrochemicals Production*Production* KtonKton

* Ethylene, Propylene and BTX

807636656

2Q08 1Q09 2Q09

+27

1,134874870

2Q08 1Q09 2Q09

+30%

Capacity utilization rates at normal levelsCapacity utilization rates at normal levels

99%

76%92%

74% 73%

93%

74% 73%

92%89%

70%88%

2Q08 1Q09 2Q09 2Q08 1Q09 2Q09 2Q08 1Q09 2Q09 2Q08 1Q09 2Q09

PE PP PVCETHYLENE

39

Outstanding Bonds & Outstanding RatingsOutstanding Bonds & Outstanding Ratings

7.07.250Jun/2018US$500 MM

9.59.750PerpetualUS$150 MM

Perpetual

Jan/2017

Jun/2015

Jan/2014

MaturityMaturity

6.88.000US$275 MM

8.8

5.9

5.5

Yield * Yield * (% p.a.) (% p.a.)

Outstanding BondsOutstanding BondsCoupon Coupon (% p.a.)(% p.a.)

US$250 MM 11.750

US$250 MM 9.375

US$200 MM 9.000

Corporate Credit Rating Corporate Credit Rating –– Global ScaleGlobal Scale

Source: Braskem / Bloomberg

Ba1

BB+

BB+

RatingRating

StableMoody’s

AgencyAgency OutlookOutlook

Fitch Ratings Stable

S&P Stable

* As of September, 29th

40

CovenantsCovenants

US$725 MM

US$80 MM

US$250 MM

R$800 MM

AmountAmount

MaintenanceUS$Nippon Export and Nippon Export and Investment InsuranceInvestment Insurance

Maintenance

Incurrence*

Incurrence*

TypeTypeFacilityFacility CurrencyCurrency

2010 and 2011 Debentures2010 and 2011 Debentures R$

2014 Medium Term Notes2014 Medium Term Notes R$

EPP (Export PreEPP (Export Pre--Payment) Payment) US$

Net Debt / EBITDA

< 4.5X3.25

Jun09

* The company is prevented from issuing any new debt for the period if it overcomes the 4.5x Net debt / Ebitda

ratio.

Net Debt / Net Debt / EbitdaEbitda (x)(x)

3.16

Jun09

RATIORATIO

R$R$US$US$

Source: Braskem

41

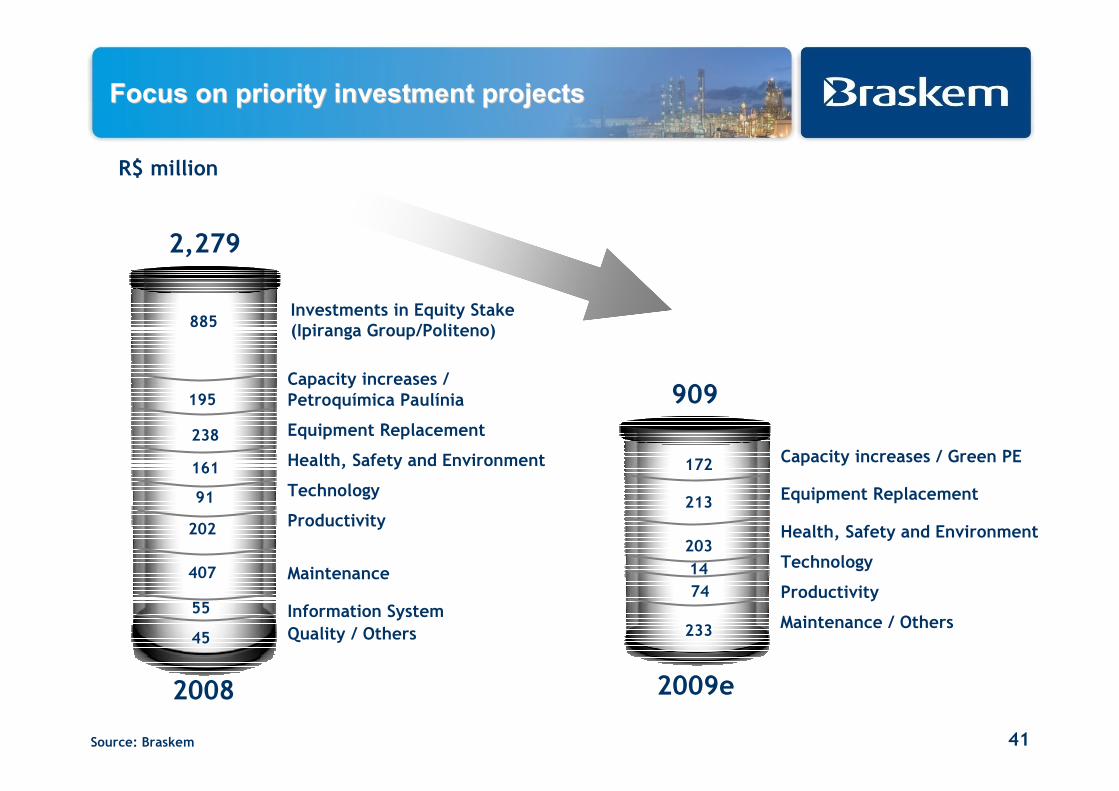

R$ million

Capacity increases /Petroquímica Paulínia

Health, Safety and Environment

Technology

Equipment Replacement

Productivity

Quality / Others

Information System

MaintenanceTechnology

Productivity

Maintenance / Others

Capacity increases / Green PE

Equipment Replacement

161

238

2,279

2008

45

195

91

202

407

55

885Investments in Equity Stake (Ipiranga Group/Politeno)

203

213

909

2009e

172

14

74

233

Source: Braskem

Health, Safety and Environment

Focus on priority investment projects Focus on priority investment projects