Embed Size (px)

Citation preview

PRIVATE WATER INSIGHT SERVICE GREENFIELD + WATER = BLUEFIELD

FOCUS REPORT

Private Water U2li2es: Global Rankings & Company Strategies July 2015

Water Pressure // Flickr // Cropped // Hans Splinter // CC BY-ND 2.0

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

About This Focus Report

2

Private Water Utilities: Global Rankings & Company Strategies Publication Date: July 2015 Key Report Takeaways:

1. The 65 major companies profiled in the report supply more than 20 billion cubic meters of drinking water annually, generating over US$53 billion in revenue.

2. Movers among the top five largest groups globally were Suez surpassing Veolia for the top ranking and Thames Water overtaking American Water in the 4th position.

3. Emerging market utilities’ large urban service areas place them for growth, entering the rankings by population served.

4. France, the UK, USA, and Brazil host the largest private water utility markets. The USA, Brazil, Chile, Italy, and Spain topping Bluefield's 2015 market attractiveness ranking.

Bluefield’s 110-page report is designed to support companies addressing opportunities for participation in water utilities globally with in-depth analysis, detailed company data, and multi-metric business ranking with a transparent methodology.

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

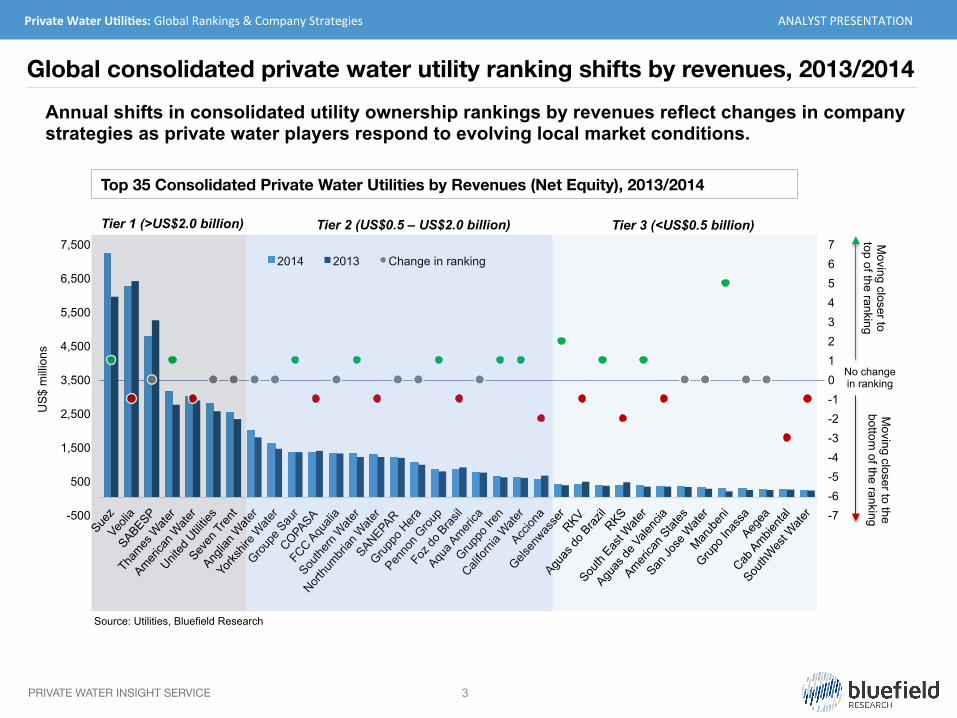

Top 35 Consolidated Private Water Utilities by Revenues (Net Equity), 2013/2014

3

Global consolidated private water utility ranking shifts by revenues, 2013/2014

-7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7

-500

500

1,500

2,500

3,500

4,500

5,500

6,500

7,500

US

$ m

illio

ns

2014 2013 Change in ranking

Source: Utilities, Bluefield Research

Tier 1 (>US$2.0 billion) Tier 2 (US$0.5 – US$2.0 billion) Tier 3 (<US$0.5 billion)

Moving closer to

top of the ranking M

oving closer to the bottom

of the ranking

No change in ranking

Annual shifts in consolidated utility ownership rankings by revenues reflect changes in company strategies as private water players respond to evolving local market conditions.

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

Source: Utilities, Bluefield Research

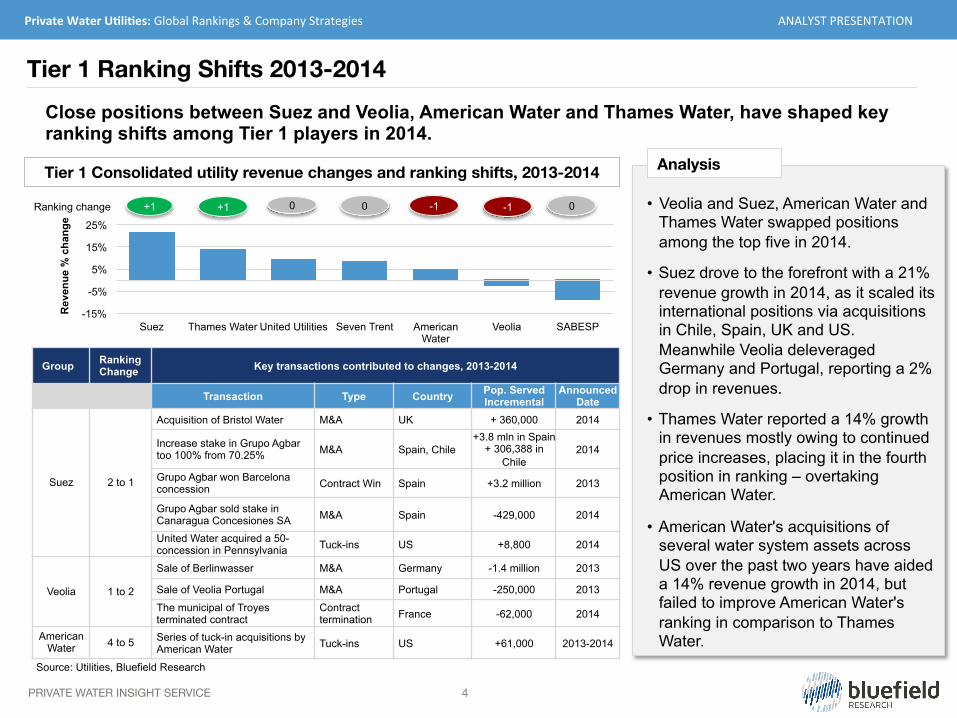

Tier 1 Consolidated utility revenue changes and ranking shifts, 2013-2014

Close positions between Suez and Veolia, American Water and Thames Water, have shaped key ranking shifts among Tier 1 players in 2014.

4

Tier 1 Ranking Shifts 2013-2014

• Veolia and Suez, American Water and

Thames Water swapped positions among the top five in 2014.

• Suez drove to the forefront with a 21% revenue growth in 2014, as it scaled its international positions via acquisitions in Chile, Spain, UK and US. Meanwhile Veolia deleveraged Germany and Portugal, reporting a 2% drop in revenues.

• Thames Water reported a 14% growth in revenues mostly owing to continued price increases, placing it in the fourth position in ranking – overtaking American Water.

• American Water's acquisitions of several water system assets across US over the past two years have aided a 14% revenue growth in 2014, but failed to improve American Water's ranking in comparison to Thames Water.

Analysis

-15%

-5%

5%

15%

25%

Suez Thames Water United Utilities Seven Trent American Water

Veolia SABESP

Rev

enue

% c

hang

e

-1 Ranking change 0 +1 -1 0 0

Group Ranking Change Key transactions contributed to changes, 2013-2014

Transaction Type Country Pop. Served Incremental

Announced Date

Suez 2 to 1

Acquisition of Bristol Water M&A UK + 360,000 2014

Increase stake in Grupo Agbar too 100% from 70.25% M&A Spain, Chile

+3.8 mln in Spain + 306,388 in

Chile 2014

Grupo Agbar won Barcelona concession Contract Win Spain +3.2 million 2013

Grupo Agbar sold stake in Canaragua Concesiones SA M&A Spain -429,000 2014

United Water acquired a 50-concession in Pennsylvania Tuck-ins US +8,800 2014

Veolia 1 to 2

Sale of Berlinwasser M&A Germany -1.4 million 2013

Sale of Veolia Portugal M&A Portugal -250,000 2013

The municipal of Troyes terminated contract

Contract termination France -62,000 2014

American Water 4 to 5 Series of tuck-in acquisitions by

American Water Tuck-ins US +61,000 2013-2014

+1

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

Source: Utilities, Bluefield Research

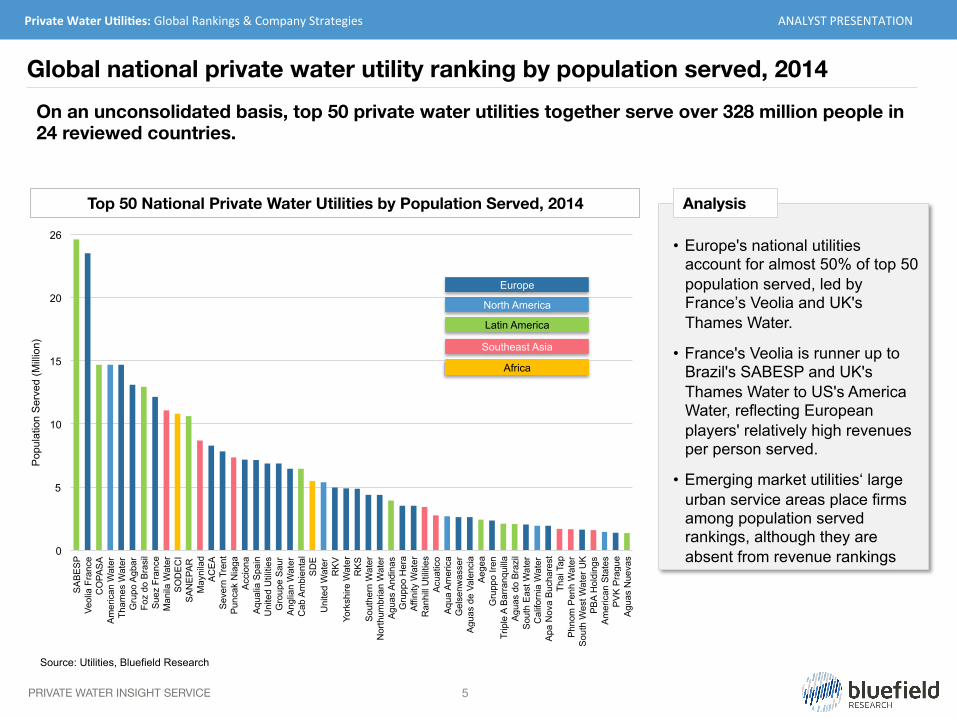

On an unconsolidated basis, top 50 private water utilities together serve over 328 million people in 24 reviewed countries.

Global national private water utility ranking by population served, 2014

5

0

5

10

15

20

26

SA

BE

SP

Veol

ia F

ranc

e C

OPA

SA

Am

eric

an W

ater

Th

ames

Wat

er

Gru

po A

gbar

Fo

z do

Bra

sil

Sue

z Fr

ance

M

anila

Wat

er

SO

DE

CI

SA

NE

PAR

M

ayni

lad

AC

EA

Sev

ern

Tren

t P

unca

k N

iaga

A

ccio

na

Aqu

alia

Spa

in

Uni

ted

Util

ities

G

roup

e S

aur

Ang

lian

Wat

er

Cab

Am

bien

tal

SD

E

Uni

ted

Wat

er

RK

V

York

shire

Wat

er

RK

S

Sou

ther

n W

ater

N

orth

umbr

ian

Wat

er

Agu

as A

ndin

as

Gru

ppo

Her

a A

ffini

ty W

ater

R

anhi

ll U

tiliti

es

Acu

atic

o A

qua

Am

eric

a G

else

nwas

ser

Agu

as d

e Va

lenc

ia

Aeg

ea

Gru

ppo

Iren

Trip

le A

Bar

ranq

uilla

A

guas

do

Bra

zil

Sou

th E

ast W

ater

C

alifo

rnia

Wat

er

Apa

Nov

a B

ucha

rest

Th

ai T

ap

Phn

om P

enh

Wat

er

Sou

th W

est W

ater

UK

P

BA

Hol

ding

s A

mer

ican

Sta

tes

PV

K P

ragu

e A

guas

Nue

vas

Pop

ulat

ion

Ser

ved

(Mill

ion)

Top 50 National Private Water Utilities by Population Served, 2014

Europe

North America

Latin America

Southeast Asia

Africa

• Europe's national utilities

account for almost 50% of top 50 population served, led by France’s Veolia and UK's Thames Water.

• France's Veolia is runner up to Brazil's SABESP and UK's Thames Water to US's America Water, reflecting European players' relatively high revenues per person served.

• Emerging market utilities‘ large urban service areas place firms among population served rankings, although they are absent from revenue rankings

Analysis

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

6

Chile: Early-privatizing market, key regional entry point for European (Agbar), Japanese players (Marubeni)

The private water utility model is concentrated in four regions led by Europe, followed by Latin America, with an increasing level of private participation in Southeast Asia.

Brazil: Rapidly scaling private concession model led by Odebrecht Ambiental, Àguas do Brasil, Aegea

Central/Southern Europe: France, Spain hub for global leaders Veolia, Suez, Aqualia – trend towards increased municipalization

Eastern Europe: Select cities within EU licensed concessions (Prague, Ostrava, Bucharest, Gdansk)

Private Water Utility Model – Global Footprint Overview

England: Host of largest group of private utilities through monopoly market structure

Malaysia: Concession restructure solidifies position of Ranhill, PBA Holdings

Thailand: Bulk water supply concessions deliver scale to Thai Tap, Eastern Water Philippines: Manila private

concessions builds regional player Manila Water Co.

Western Africa: France’s Eranove holds beachhead positions in Senegal, Ivory Coast

USA: Led by American Water, six players account for over half the

investor-owned utility market

Mature (>20% Private)

Scaling (10-20% Private)

Nascent (<10% Private)

Colombia: EPM, Inassa scaling as domestic leaders expanding regionally

Indonesia: Acuatico positioned with major concessions in select provinces

Russia: Rosvodokanal, RKS, building concession portfolios

Source: Bluefield Research

PRIVATE WATER INSIGHT SERVICE

MARKET INSIGHT Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

7

PRIVATE WATER: STRATEGIES & OPPORTUNITIES IN WATER ASSET OWNERSHIP & OPERATION INSIGHT SERVICE

CLIENT FOCUS: The Private Water Insight Service is designed for companies that need to track market trends, competitive shifts, and unique opportunities in private water asset ownership, including:

• Municipal water and wastewater operators with concessions/O&M contracts

• Independent water (and power) providers • Water infrastructure investors seeking to scale asset portfolios • Water service providers seeking new industrial wastewater

opportunities • Water technology providers targeting private water asset owners

RESEARCH COVERAGE: a 12-month cycle of data- and analytics-driven research provided in multiple formats to support client strategies, covering:

• Market environment attractiveness for private asset ownership • Historical trends and upcoming private sector opportunities for

concessions, PPPs, DBO, BOO, BOT, other contract types • Private water asset portfolio rankings in terms of equity ownership,

total revenues, connections, population served, location, project type • Player segmentation and expansion strategy analysis including entry

into emerging markets, vertical integration, and service/segment diversification initiatives

METRICS: primary research and analysis is supported by proprietary market, project and company databases updated continuously:

• Private water asset portfolio database (water, wastewater, desalination/concession, PPP, DBO, etc.)

• Comparative data driving private water valuations: tariffs, NRW, connections, volume, cost structures

• M&A transaction database tracking water asset deals • Country-specific private water sector data (PPPs, infrastructure

spending, private ownership penetration, tariffs)

Insight Service Description

SELECT LIST OF COMPANIES COVERED:

PRIVATE WATER SEGMENTS COVERED:

Ownership Structures

Valuation Drivers

M&A Activity

Regulatory Drivers Rankings

MARKET SEGMENTS COVERED:

Regional Analysis • Asia Pacific • China • Europe • Latin America • MENA • North America • Sub-Saharan Africa

Water Treatment

Desalination

Utility Concessions

Independent Water

Producers

Independent Water & Power

Producers

Wastewater Treatment

Water Reuse

PRIVATE WATER INSIGHT SERVICE

Private Water U2li2es: Global Rankings & Company Strategies ANALYST PRESENTATION

© 2015 BLUEFIELD RESEARCH, LLC.

Global companies across the value chain are developing strategies to capitalize on greenfield opportunities in water– new build, new business models, and private investment. Bluefield Research supports a growing roster of companies across key technology segments and industry verticals addressing risks and opportunities in the new water landscape. Companies are turning to Bluefield for in-depth, actionable intelligence into the water sector and the sector's impacts on key industries. The insights draw on primary research from the water, energy, power, mining, agriculture, financial sectors, and their respective supply chains. Bluefield works with key decision-makers at utilities, project development companies, independent water and power providers, EPC companies, technology suppliers, manufacturers, and investment firms. Bluefield’s services gives these companies tools to define and execute strategies.

Contact Bluefield Research

NORTH AMERICA 34 Farnsworth St // Floor 3 Boston, MA 02210 T +1 617 910 2540 EUROPE C/ de Santa Eulàlia 5-9 // 3a

08012 Barcelona Spain T +34 673 408 963 [email protected] www.bluefieldresearch.com

About Bluefield Research

PRIVATE WATER INSIGHT SERVICE GREENFIELD + WATER = BLUEFIELD