Embed Size (px)

DESCRIPTION

Citation preview

Syeda Wajiha Zaidi

ID# 8424

Subject: Finance For managers

Submitted to: Sir Muhammad Farhan

Date: 8/04/2014

COMPANY PROFILEKohinoor Mills Limited's vision is to achieve and then remain as the most

progressive and profitable textile organization in Pakistan. Incorporated in 1987 as a small weaving mill, today Kohinoor Mills broadly undertakes three

major businesses, weaving, dyeing and power generation. It has, and continues to develop, a portfolio of businesses that are major players within their respective industries. Bringing together outstanding knowledge of

customer needs with leading edge technology platforms your company undertakes to provide superior products to its customers.With an annual turnover of over Rs. 8 billion, today Kohinoor Mills Limited employs over 1,400 employees. It aims to create superior value for Kohinoor's customers and stakeholders without compromising its commitment to safety, environment and health for the communities in which it operates. Its products range from greige fabric to processed fabric.

MISSION & VISION STATEMENT

The Kohinoor Mills Limited's stated mission is to become and then remainas the most progressive and profitable company in Pakistan in terms of industry standards and stakeholders interest.The Company shall achieve its mission through a continuous process of having sourced, developed, implemented and managed the best leading edge technology, industry best practices, human resource and innovative products and services and sold these to its customers, suppliers and stakeholders.

BUSINESS ACTIVITIES

The Company is principally engaged in the business of textile manufacturing covering weaving, bleaching, dyeing, buying and selling and otherwise dealing in yarn, cloth and other goods and fabrics made

from raw cotton and synthetic fiber and to generate, distribute, supply and sell electricity.

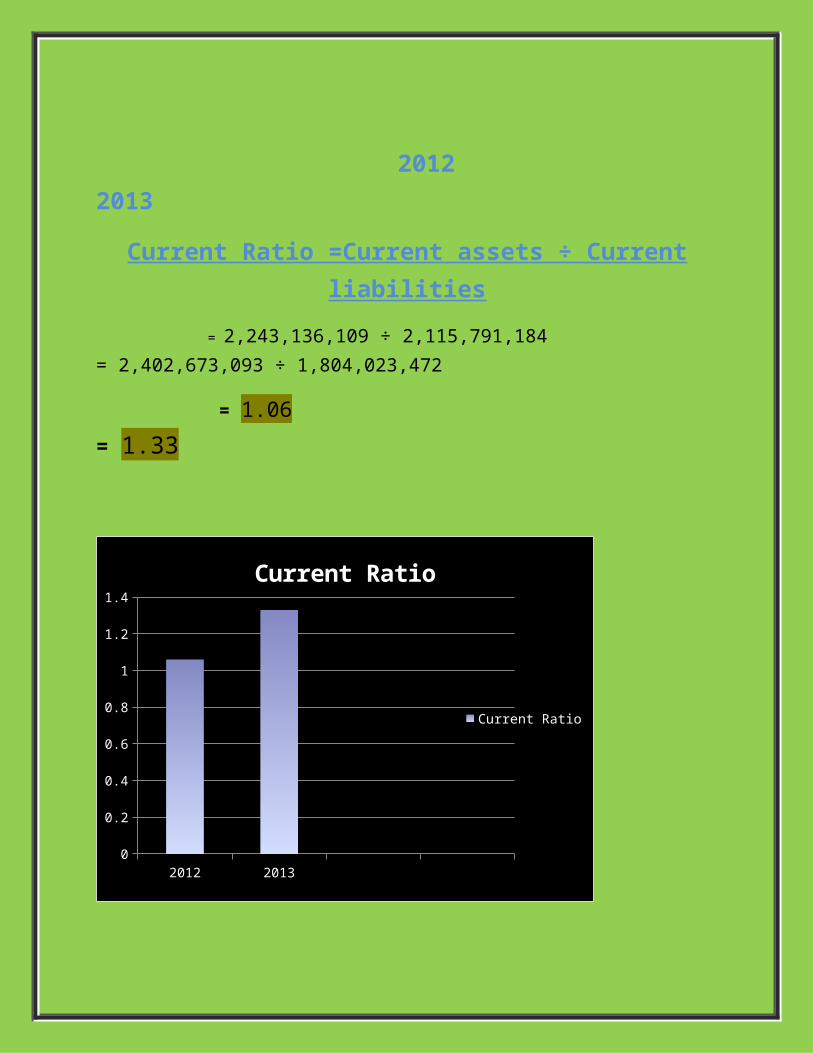

1: Current Ratio

2012 2013

Current Ratio =Current assets ÷ Current liabilities

= 2,243,136,109 ÷ 2,115,791,184 = 2,402,673,093 ÷ 1,804,023,472

= 1.06 = 1.33

2012 20130

0.2

0.4

0.6

0.8

1

1.2

1.4

Current Ratio

Current Ratio

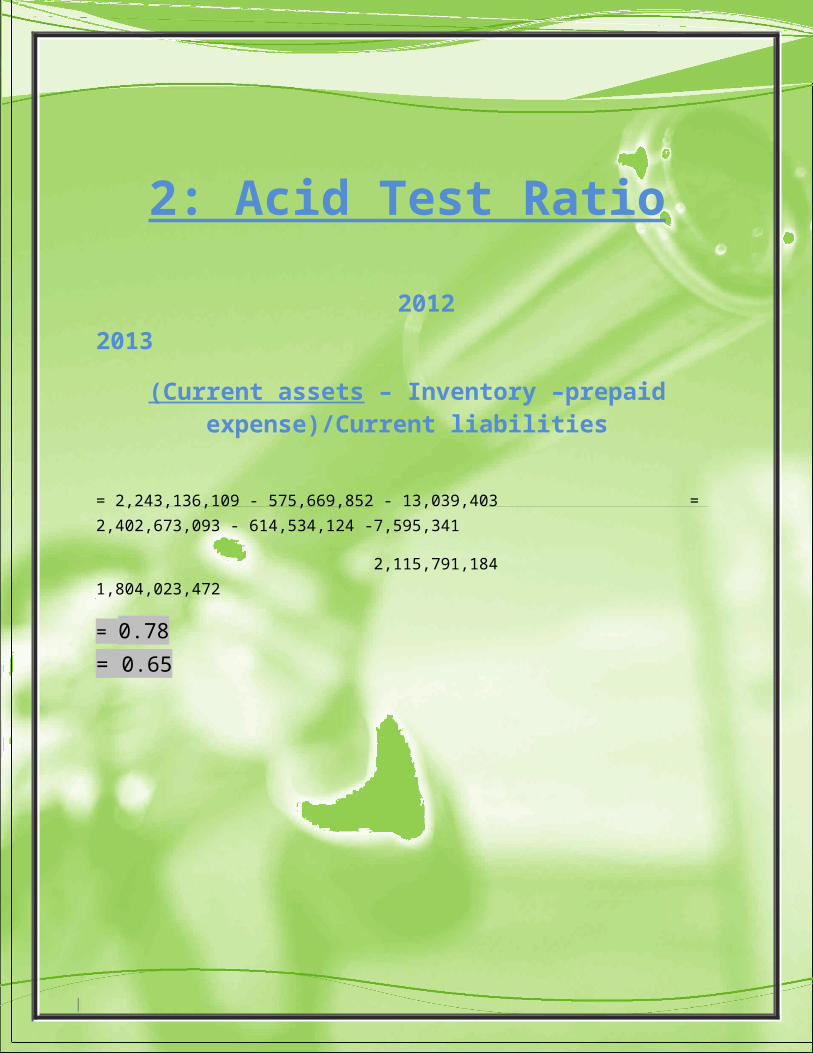

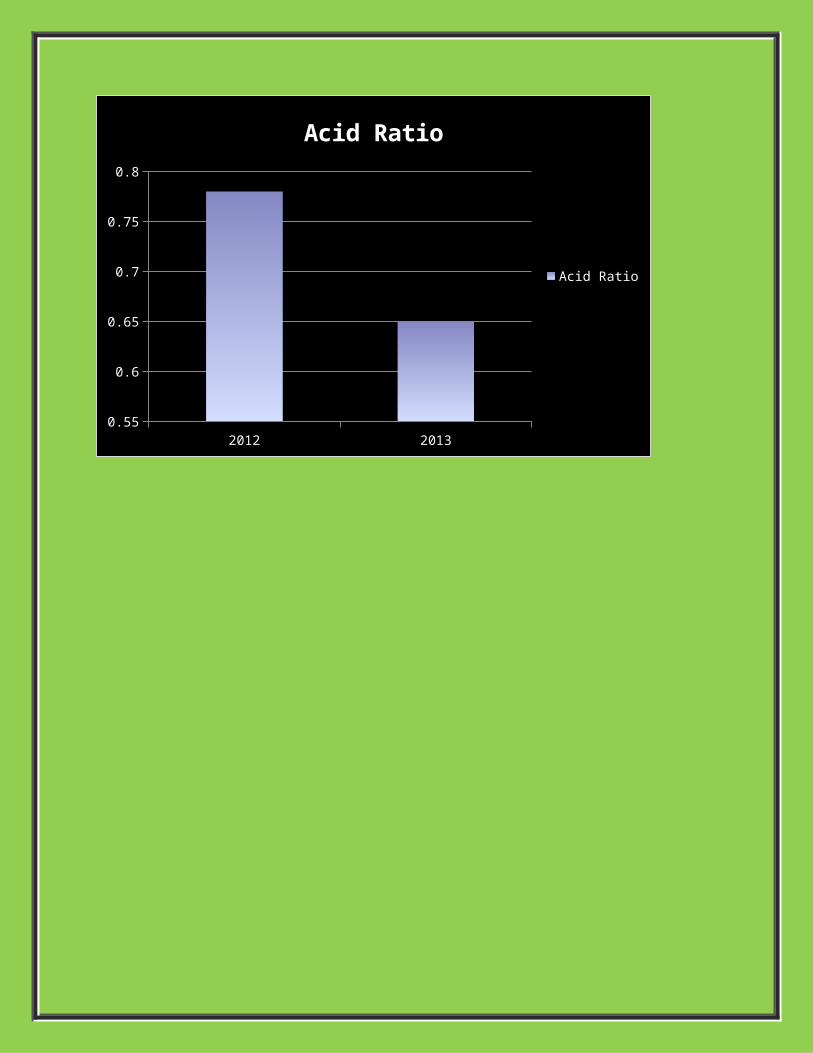

2: Acid Test Ratio

2012 2013

(Current assets – Inventory –prepaid expense)/Current liabilities

= 2,243,136,109 - 575,669,852 - 13,039,403 = 2,402,673,093 - 614,534,124 -7,595,341

2,115,791,184 1,804,023,472

= 0.78 = 0.65

2012 20130.55

0.6

0.65

0.7

0.75

0.8

Acid Ratio

Acid Ratio

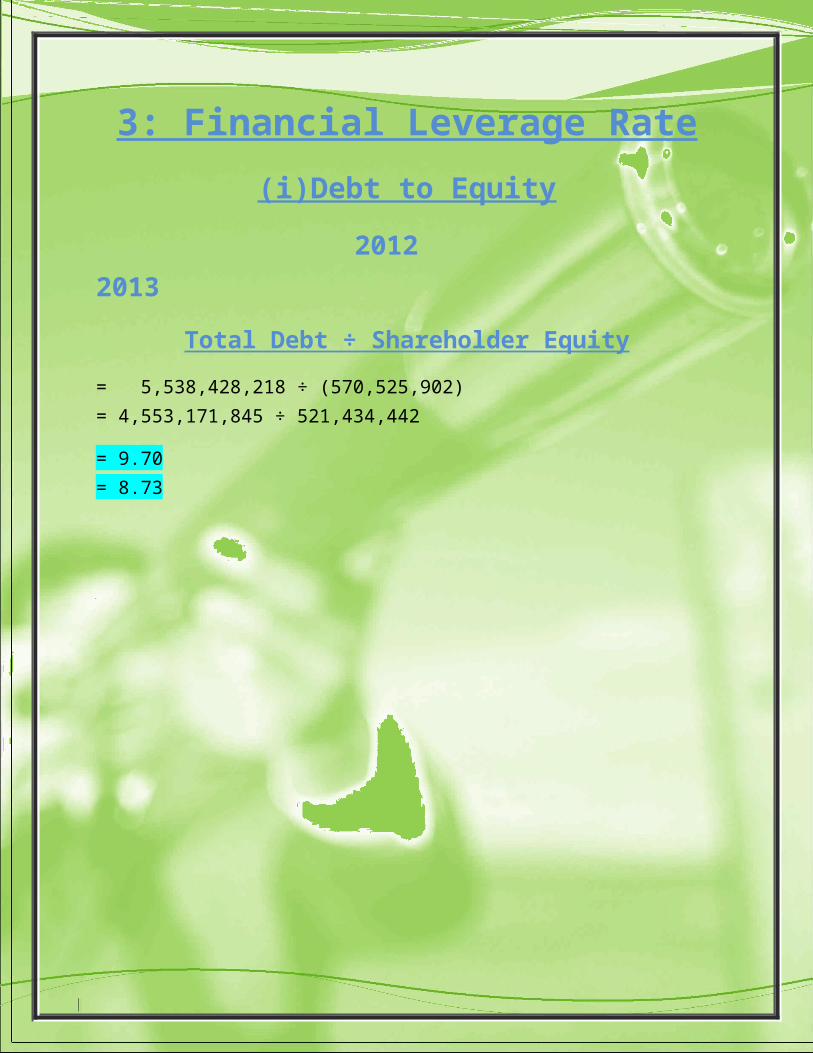

3: Financial Leverage Rate

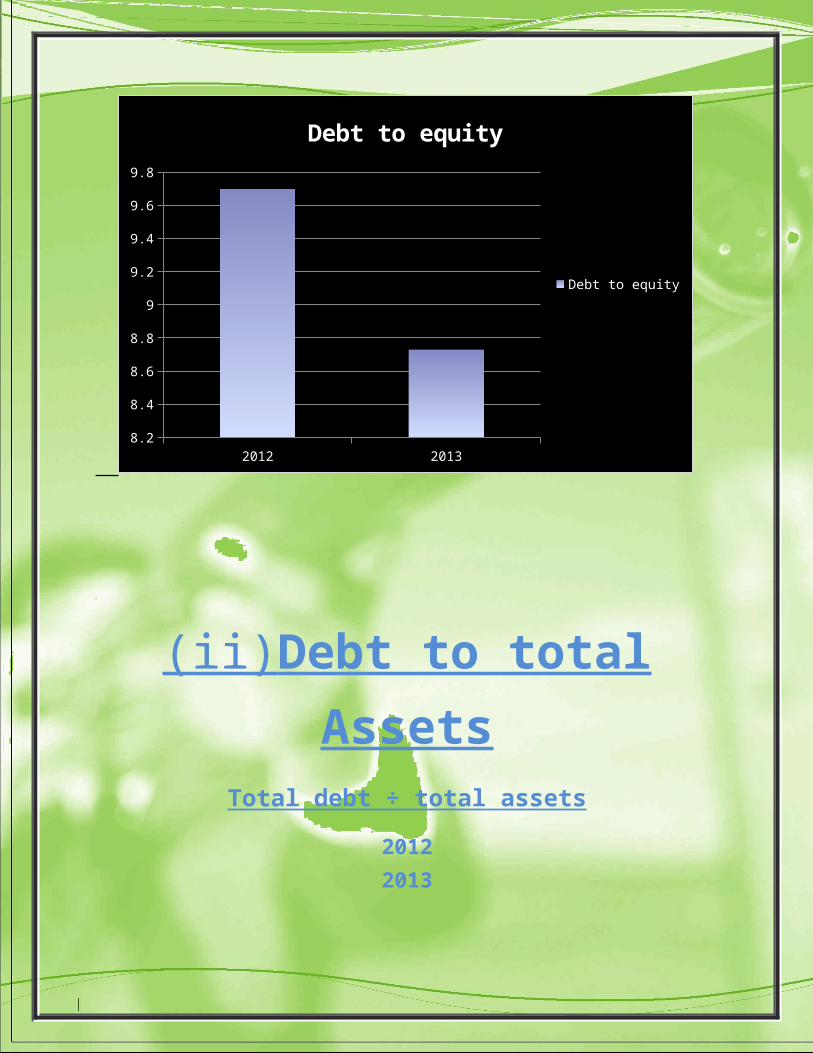

(i)Debt to Equity

2012 2013

Total Debt ÷ Shareholder Equity

= 5,538,428,218 ÷ (570,525,902) = 4,553,171,845 ÷ 521,434,442

= 9.70 = 8.73

2012 20138.2

8.4

8.6

8.8

9

9.2

9.4

9.6

9.8

Debt to equity

Debt to equity

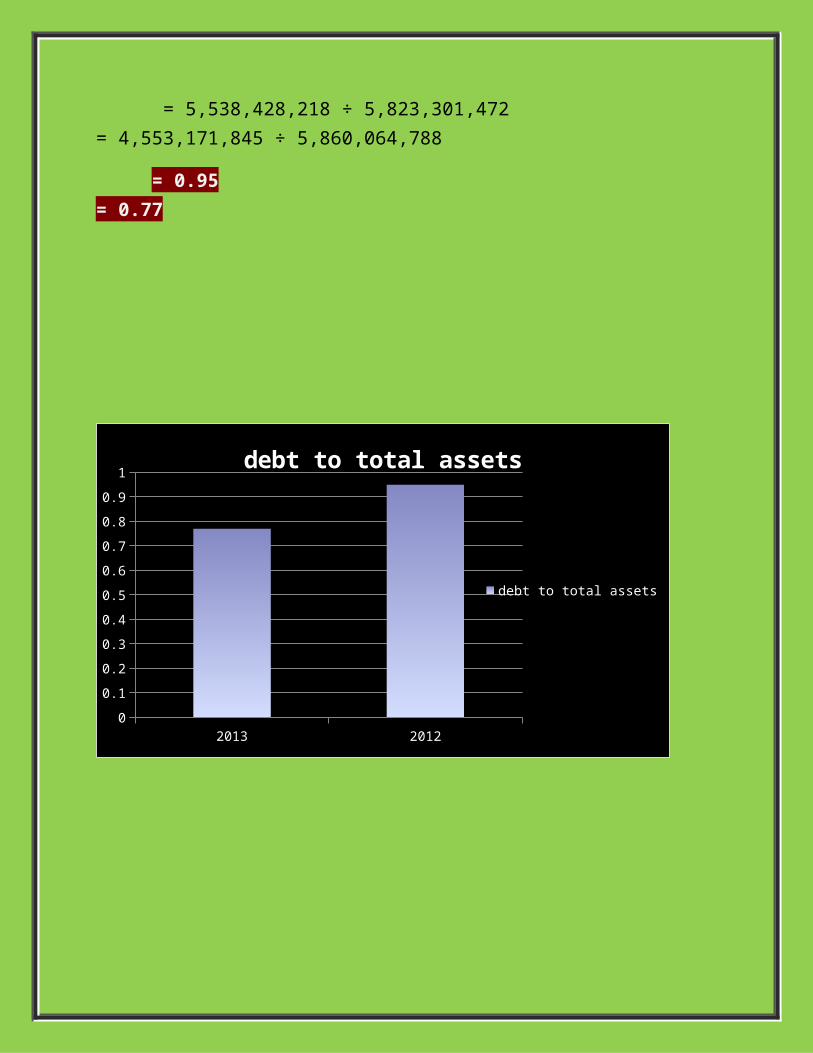

(ii) Debt to total Assets Total debt ÷ total assets

2012 2013

= 5,538,428,218 ÷ 5,823,301,472 = 4,553,171,845 ÷ 5,860,064,788

= 0.95 = 0.77

2013 2012

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1debt to total assets

debt to total assets

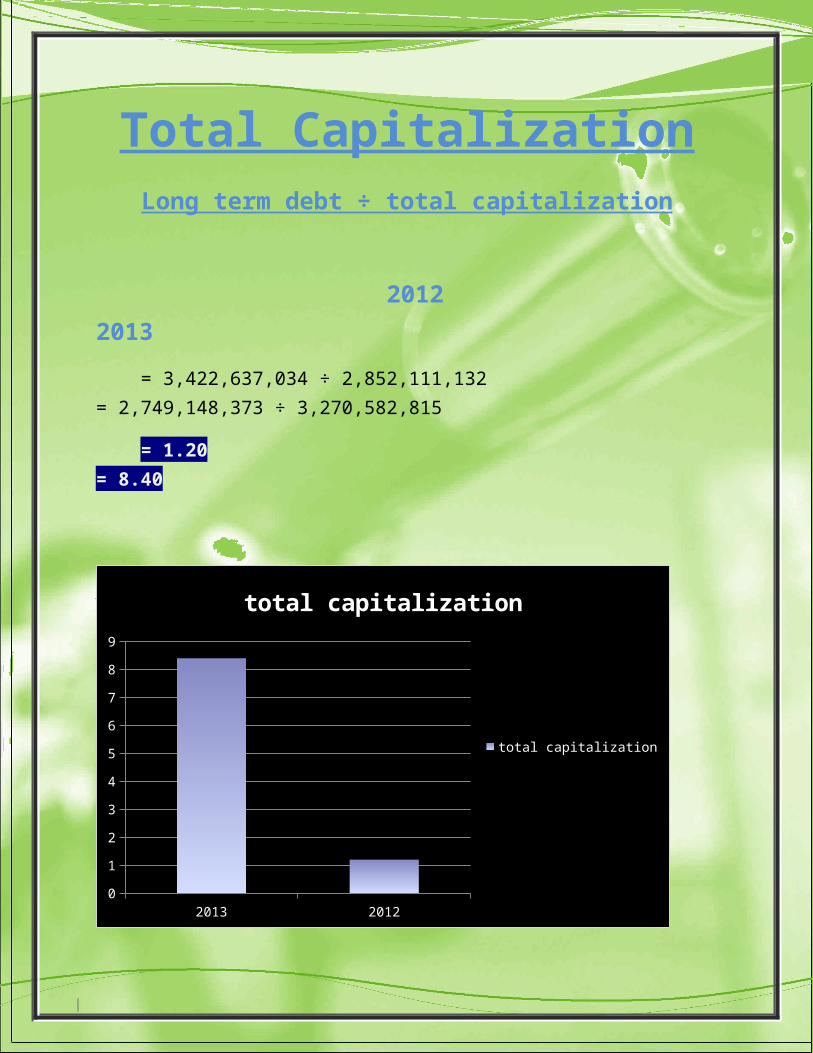

Total CapitalizationLong term debt ÷ total capitalization

2012 2013

= 3,422,637,034 ÷ 2,852,111,132 = 2,749,148,373 ÷ 3,270,582,815

= 1.20 = 8.40

2013 20120

1

2

3

4

5

6

7

8

9

total capitalization

total capitalization

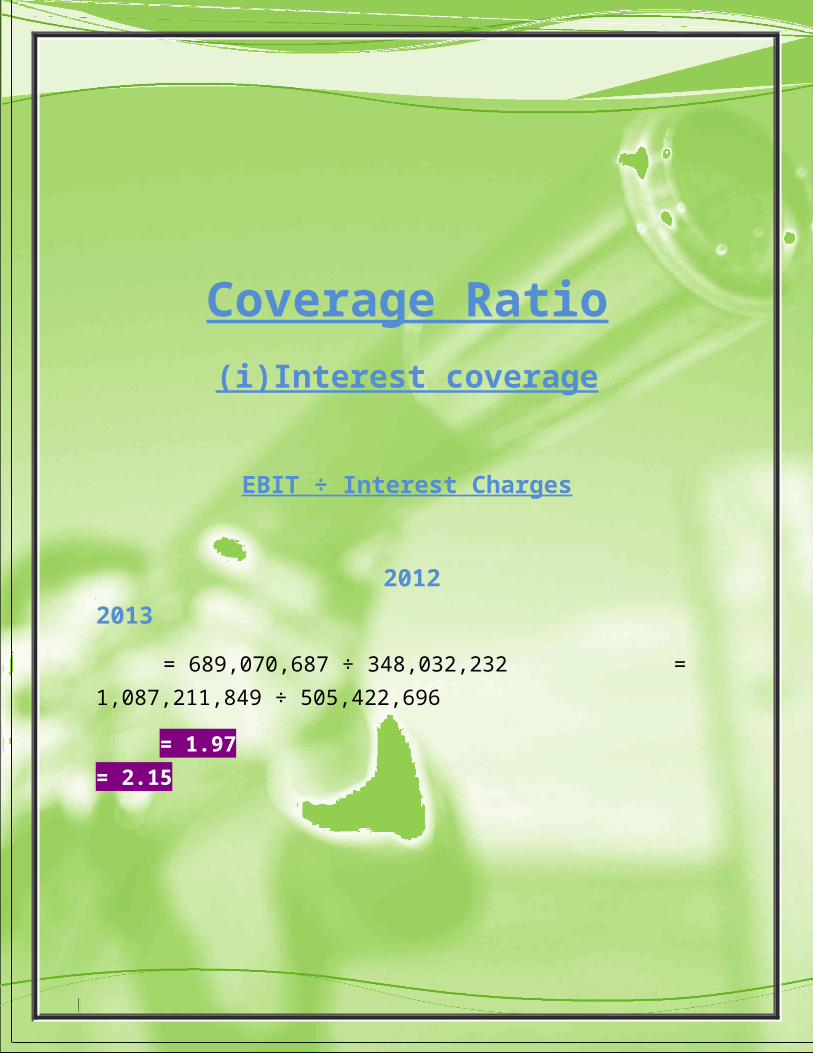

Coverage Ratio(i)Interest coverage

EBIT ÷ Interest Charges

2012 2013

= 689,070,687 ÷ 348,032,232 = 1,087,211,849 ÷ 505,422,696

= 1.97 = 2.15

2013 2012

1.85

1.9

1.95

2

2.05

2.1

2.15

2.2

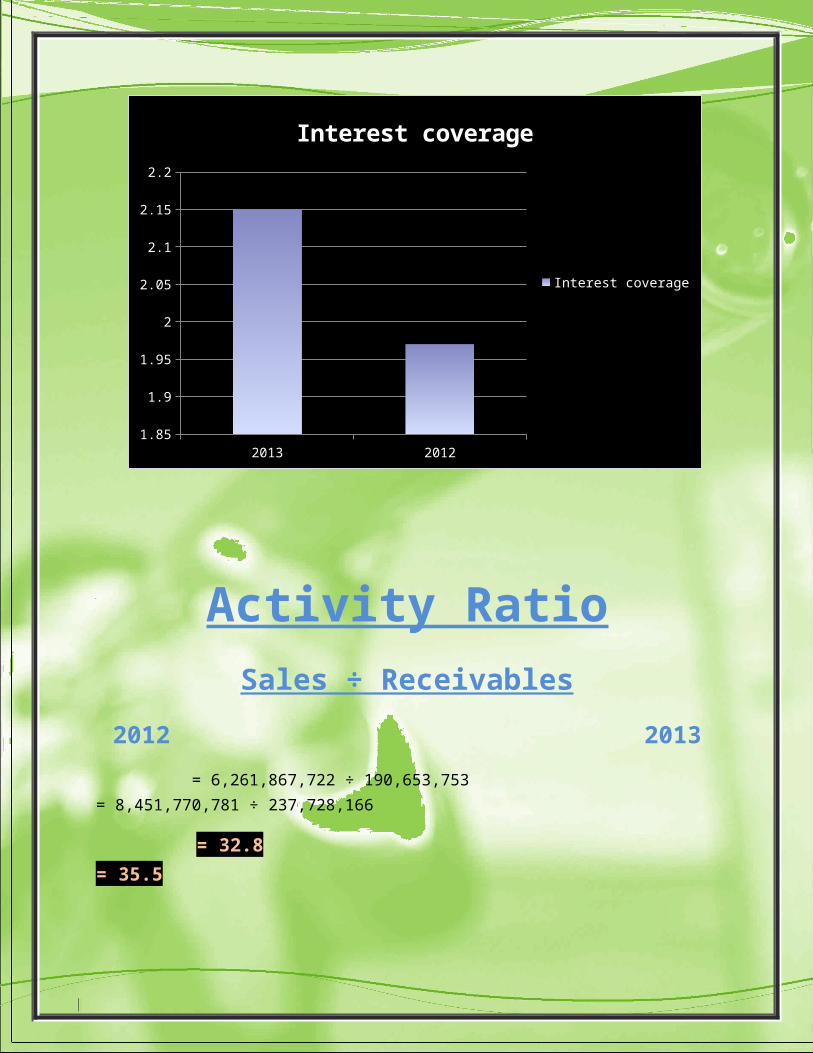

Interest coverage

Interest coverage

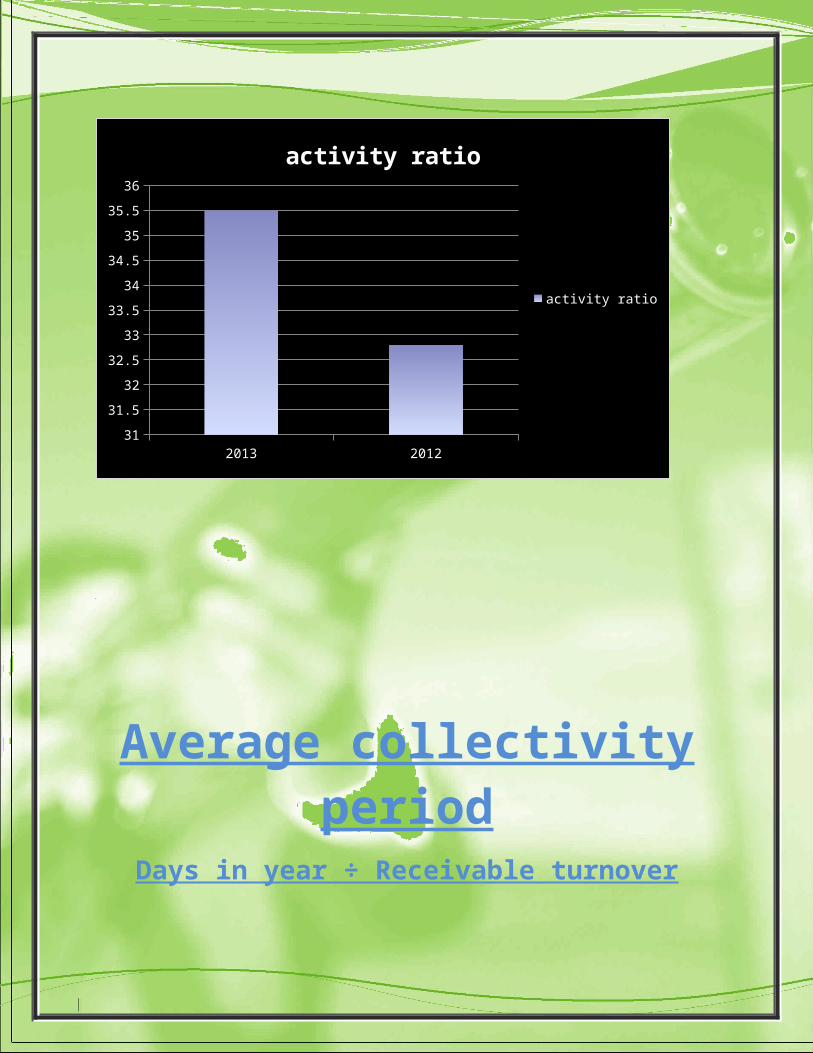

Activity RatioSales ÷ Receivables

2012 2013

= 6,261,867,722 ÷ 190,653,753 = 8,451,770,781 ÷ 237,728,166

= 32.8 = 35.5

2013 201231

31.5

32

32.5

33

33.5

34

34.5

35

35.5

36

activity ratio

activity ratio

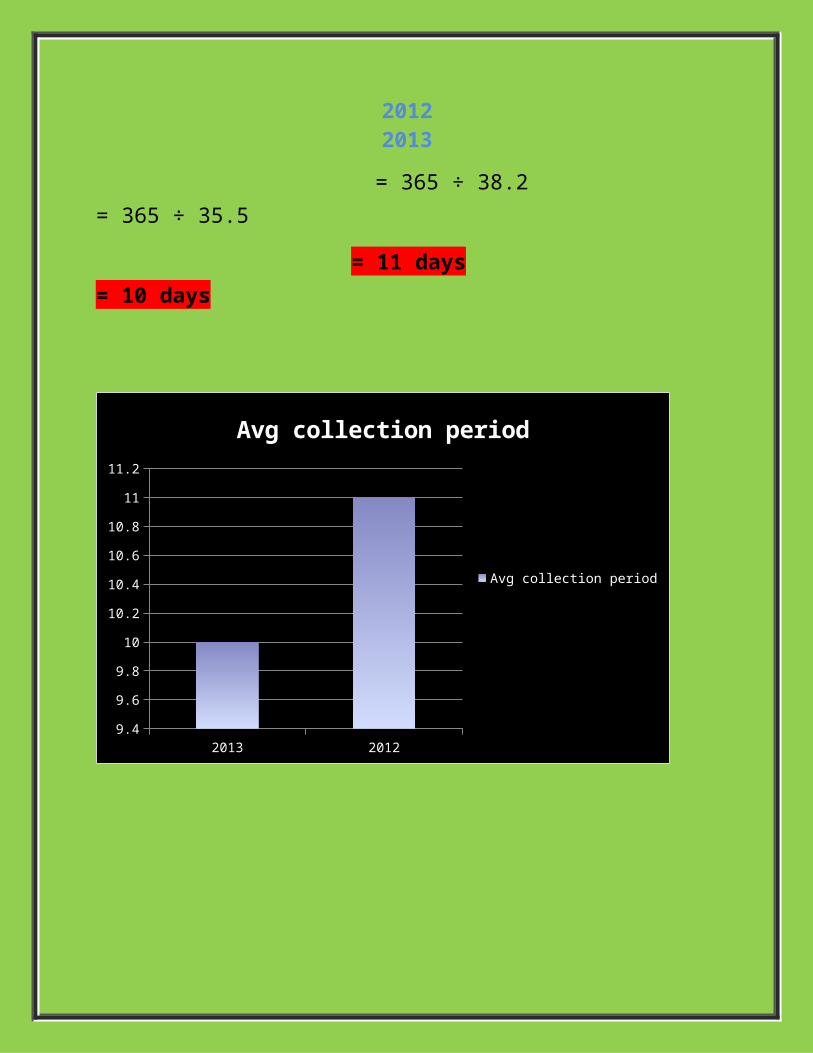

Average collectivity period

Days in year ÷ Receivable turnover

2012 2013

= 365 ÷ 38.2 = 365 ÷ 35.5

= 11 days = 10 days

2013 20129.4

9.6

9.8

10

10.2

10.4

10.6

10.8

11

11.2

Avg collection period

Avg collection period

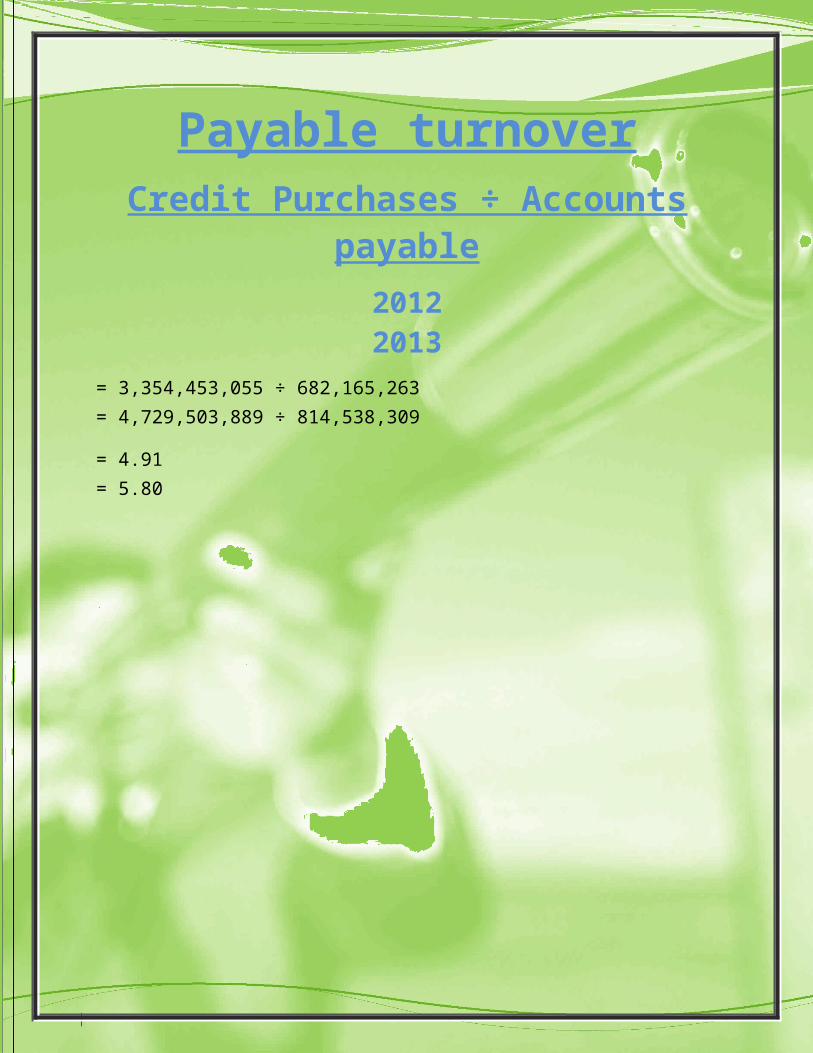

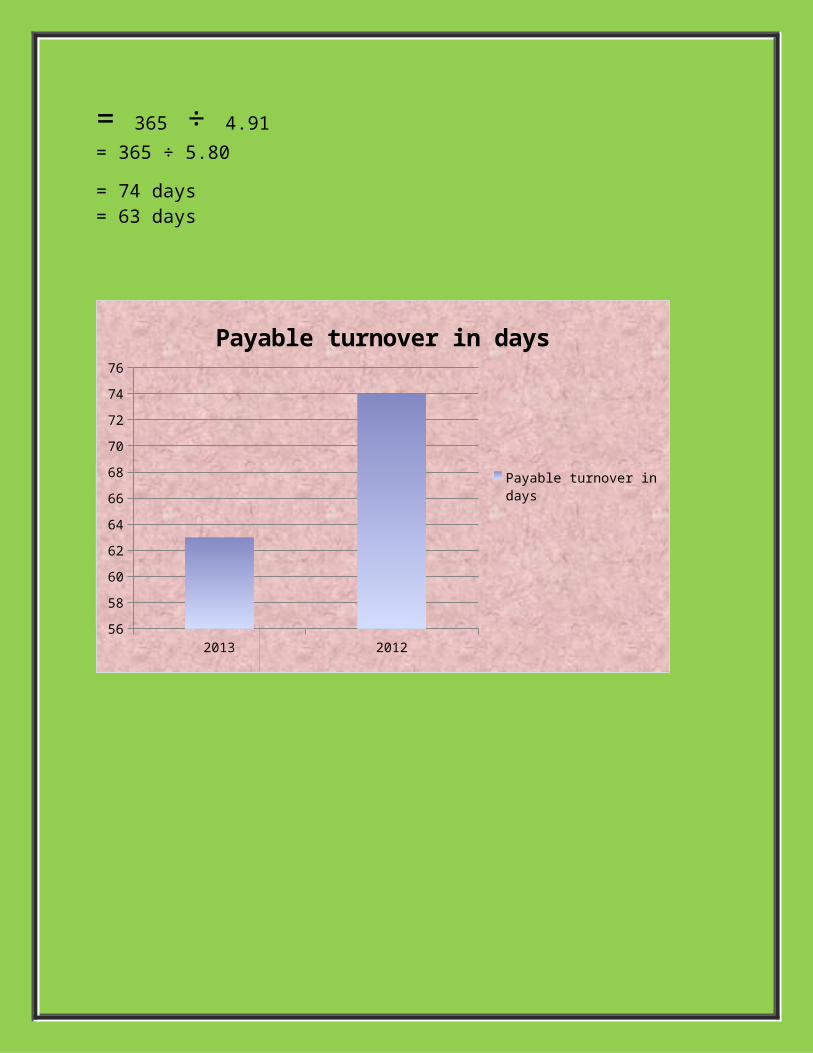

Payable turnoverCredit Purchases ÷ Accounts

payable

2012 2013= 3,354,453,055 ÷ 682,165,263 = 4,729,503,889 ÷ 814,538,309

= 4.91 = 5.80

2013 2012

4.4

4.6

4.8

5

5.2

5.4

5.6

5.8

6

Payable turnover

Payable turnover

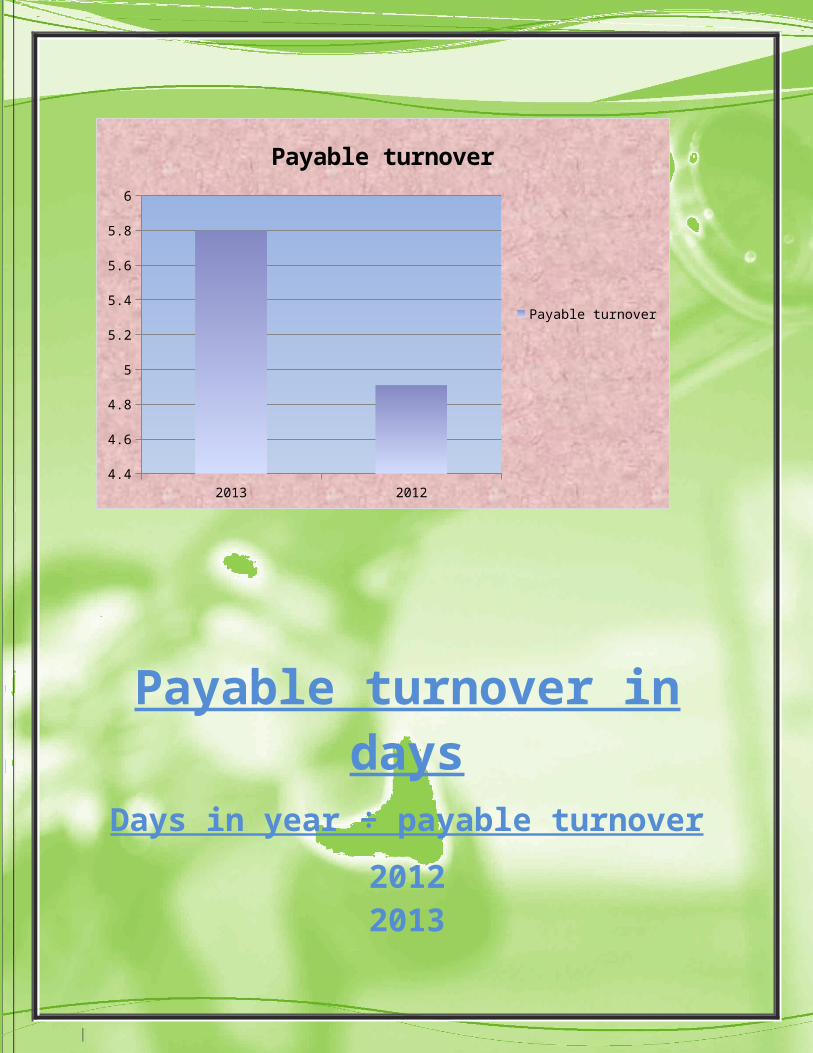

Payable turnover in days

Days in year ÷ payable turnover

2012 2013

= 365 ÷ 4.91 = 365 ÷ 5.80

= 74 days = 63 days

2013 201256

58

60

62

64

66

68

70

72

74

76

Payable turnover in days

Payable turnover in days

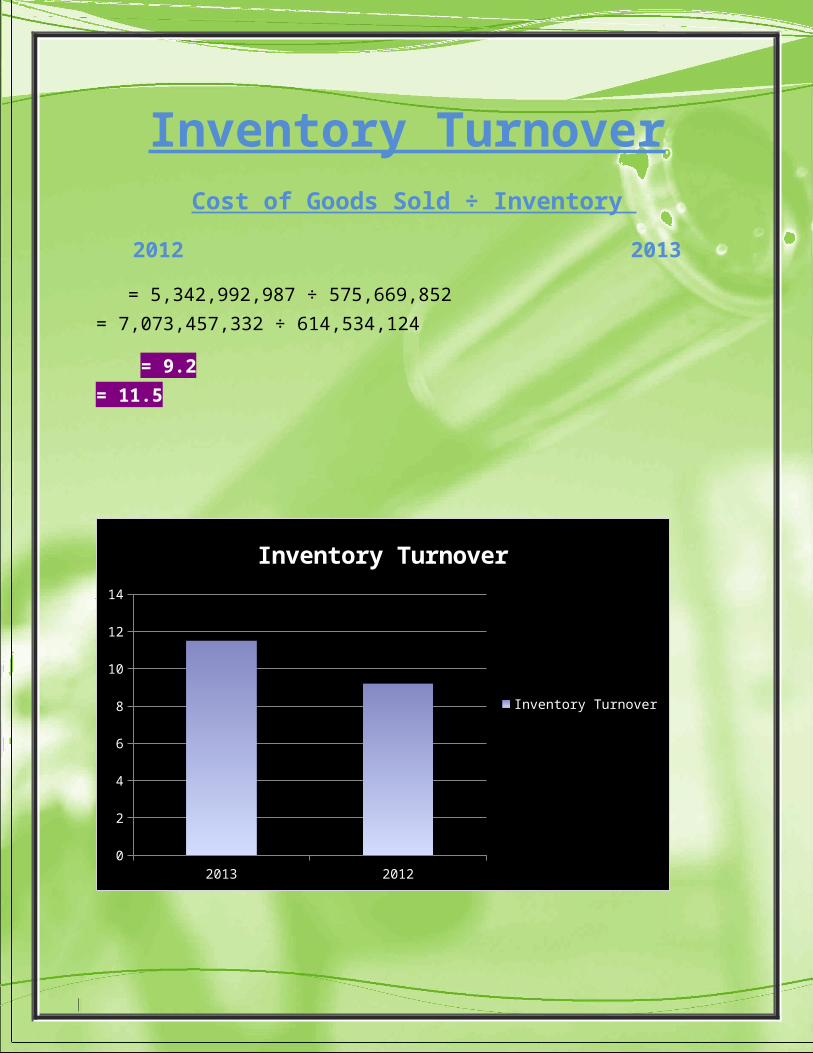

Inventory TurnoverCost of Goods Sold ÷ Inventory

2012 2013

= 5,342,992,987 ÷ 575,669,852 = 7,073,457,332 ÷ 614,534,124

= 9.2 = 11.5

2013 20120

2

4

6

8

10

12

14

Inventory Turnover

Inventory Turnover

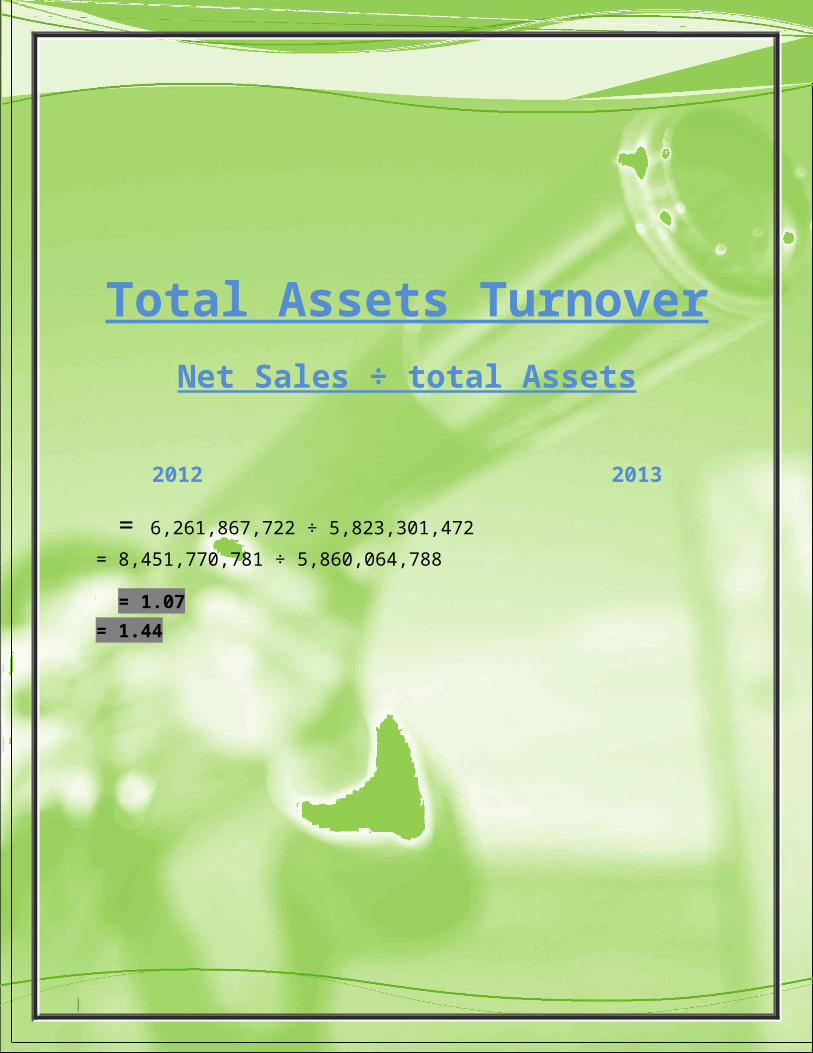

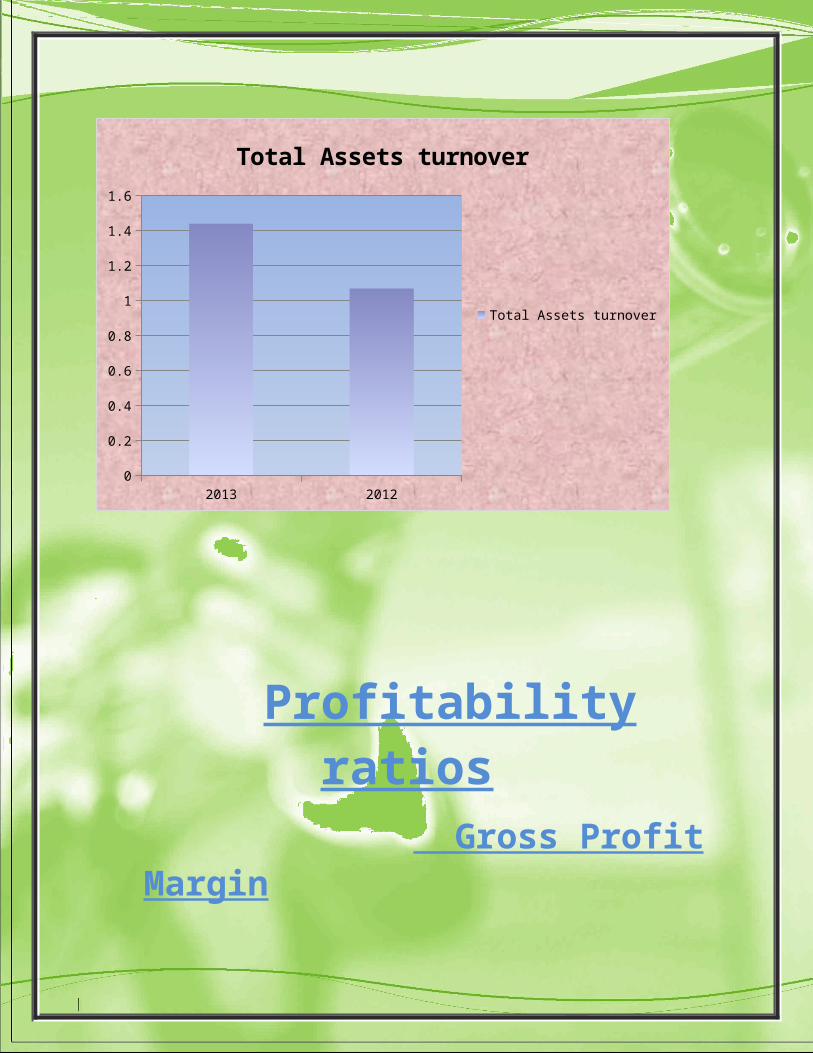

Total Assets TurnoverNet Sales ÷ total Assets

2012 2013

= 6,261,867,722 ÷ 5,823,301,472 = 8,451,770,781 ÷ 5,860,064,788

= 1.07 = 1.44

2013 2012

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Total Assets turnover

Total Assets turnover

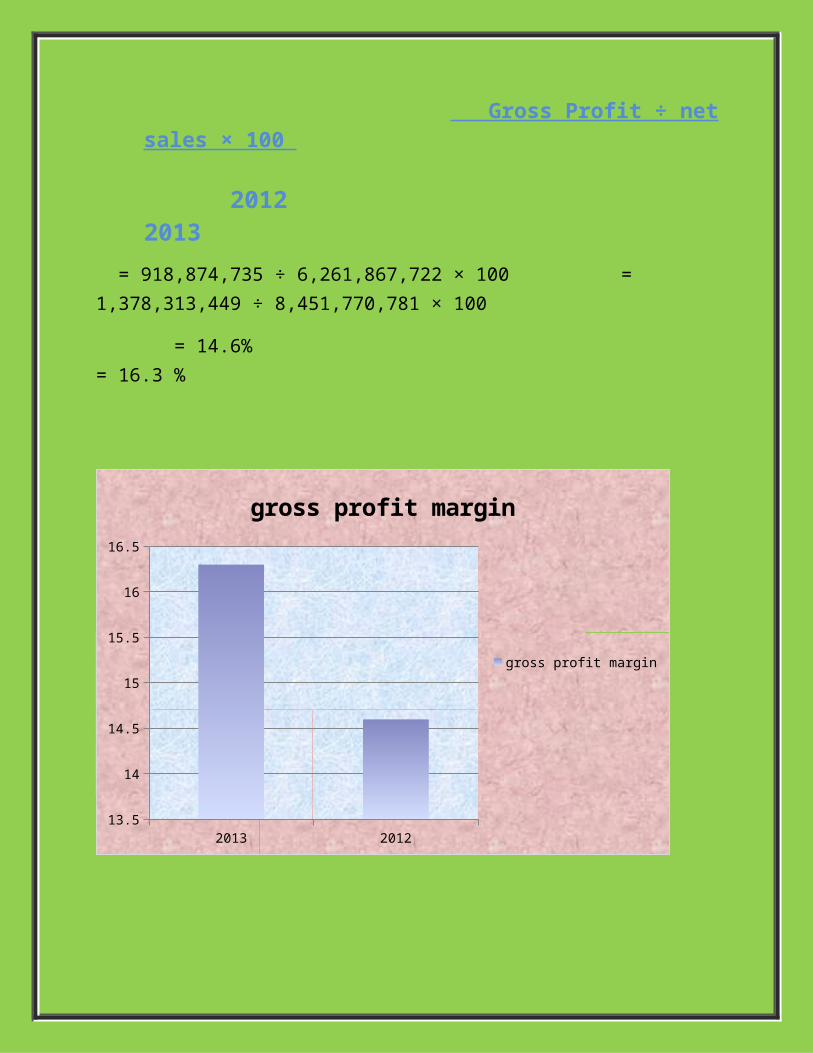

Profitability ratios Gross Profit Margin

Gross Profit ÷ net sales × 100

2012 2013

= 918,874,735 ÷ 6,261,867,722 × 100 = 1,378,313,449 ÷ 8,451,770,781 × 100

= 14.6% = 16.3 %

2013 201213.5

14

14.5

15

15.5

16

16.5

gross profit margin

gross profit margin

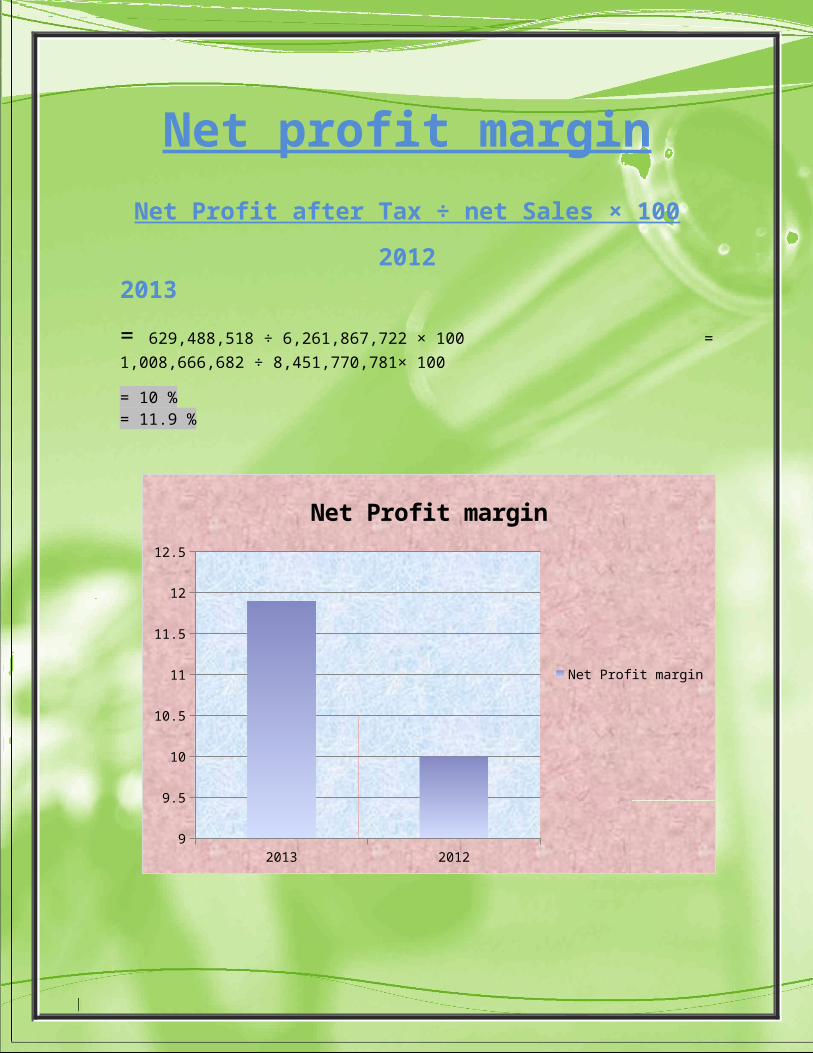

Net profit marginNet Profit after Tax ÷ net Sales × 100

2012 2013

= 629,488,518 ÷ 6,261,867,722 × 100 = 1,008,666,682 ÷ 8,451,770,781× 100

= 10 % = 11.9 %

2013 2012

9

9.5

10

10.5

11

11.5

12

12.5

Net Profit margin

Net Profit margin

Return on investment

Net profit after tax ÷ total assets

2012 2013

= 629,488,518 ÷ 5,823,301,472 = 1,008,666,682 ÷ 5,860,064,788

= 0.10 = 0.17

2013 20120

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

Return on investment

Return on investment

RETURN ON EQUITY

Net profit after tax ÷ Shareholder equity

2012 2013

= 629,488,518 ÷ (570,525,902) = 1,008,666,682 ÷ 521,434,442

= 1.1 = 1.9

2013 2012

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

return on equity

return on equity

After analyzing financial statement of Kohinoor Mills limited it is concluded that companies financial is very strong its profit increase in 2013 by 60.2% i.e. from 6,29M to 1,008M also their sale is increased from 6,261M to 8,451M which caused increase in Gross profit to 50% which mainly because of a cost cutting strategy of management.

Total Reserve of Kohinoor Mills Limited increased from -570M (which is due to negative reserve) to 521M which is a result of increase in total reserves as well as increase in accumulated profit as above mention. Their long term liability is also decreased in 2013 by 19.6% i.e. from 3,422M to 2,749M where as current liability is

decreased to 14.7% so this decrease in total liability is a great sign for company as they are paying off all their debts. The total asset of company is not much increase it is just increased to 0.63% where as long term asset is decreased which is mainly because of depreciation of their fixed assets.

As far as ratios are concern their current asset in 2013 is 1.33 which means that they have 1.33 rupees of asset for every 1 rupees of liability. Moreover they have acid test ratio of 0.65 which is not a good sign as they couldn’t spontaneously fulfill their all current liability by current liquid assets.

While debt to equity ratio is also not good it is 8.73 which means their debt is 8.73 times more than their shareholders equity. Their total debt is 0.77 times less then total assets. They also have decreased their average collection period from 11 to 10 days which leads to good cash conversion cycle.

![21325300 Ratio Analysis Project Report[1]](https://img.pdfslide.us/doc/110x75/577d2a721a28ab4e1ea93506/21325300-ratio-analysis-project-report1.jpg)