Embed Size (px)

Citation preview

1

Disclaimer

This presentation contains forward-looking statements regarding the prospects of thebusiness, estimates for operating and financial results, and those regarding Cia. Hering'sgrowth prospects. These are merely projections and, as such, are based exclusively onthe expectations of Cia. Hering management concerning the future of the business andits continued access to capital to fund the Company’s business plan. Such forward-looking statements depend, substantially, on changes in market conditions, governmentregulations, competitive pressures, the performance of the Brazilian economy and theindustry, among other factors and risks disclosed in Cia. Hering’s filed disclosuredocuments and are, therefore, subject to change without prior notice.

2

AGENDA:AGENDA:AGENDA:AGENDA:

• Highlights• Operating Performance• Operating Performance• Business Strategy and Outlook

4Q08 Highlights

CIA. HERING ENDS UP 4Q08 WITH GROWTH

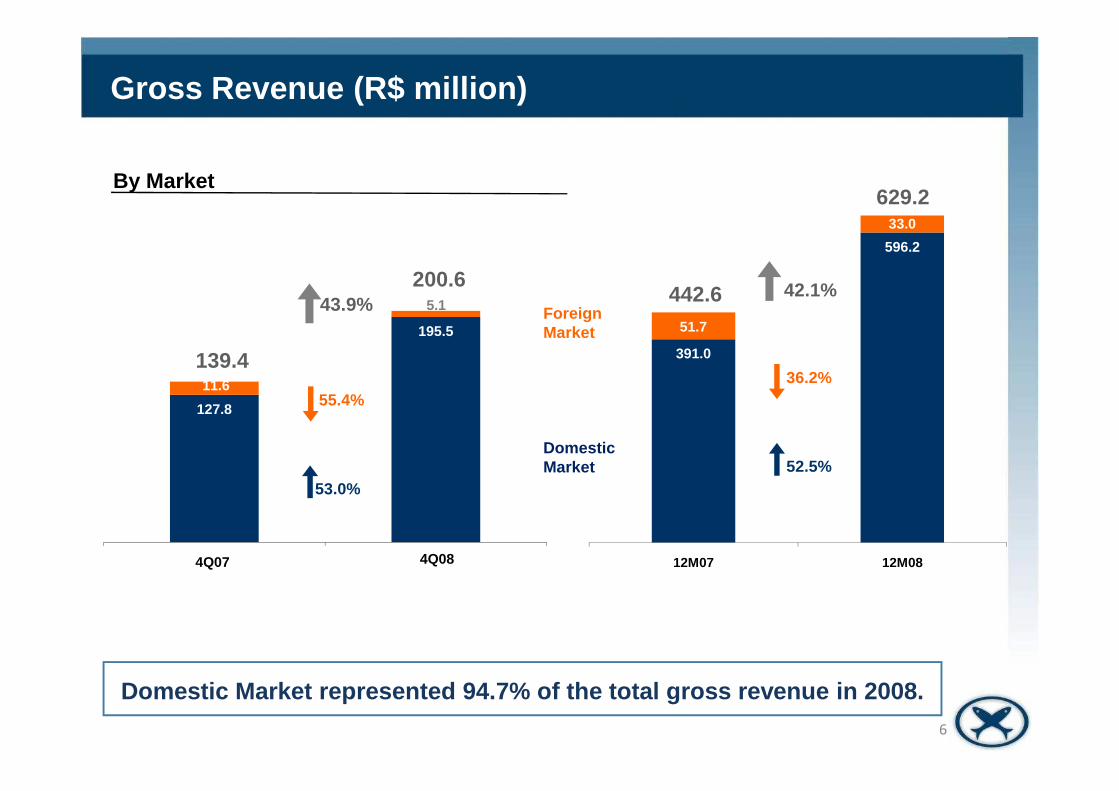

• Gross revenue in domestic market increased 53.0%

• Hering brand sales rose 63.7%

• Same-store sales growth of 29.1% in the Hering Stores

• Ajusted EBITDA Margin of 31.6% (Comparable EBITDA Margin: 2 3.1%)

CONTINUED GROWTH PLAN

• 21 Hering Stores opened in the 4Q08 with the new architectura l project

• Marketing campaign “eu uso Hering…” with new celebrities

• Actions focused on store operating performance optimizati on

• New store architectural project for PUC brand

• New business plan for dzarm. brand

SUSTAINABLE GROWTH

• Capex of R$ 10.5 million4

AGENDA:AGENDA:AGENDA:AGENDA:

•Highlights

• Operating Performance• Operating Performance• Business Strategy and Outlook

195.5

11.6

5.1

55.4%

43.9% Foreign Market

139.4

200.6

By Market

Gross Revenue (R$ million)

391.0

596.2

51.7

33.0

36.2%

42.1%442.6

629.2

127.8

4Q07 4T08

55.4%

53.0%

Domestic Market

Domestic Market represented 94.7% of the total gross reve nue in 2008.6

12M07 12M08

52.5%

4Q07 4Q08

99.3200

Gross Revenue – Domestic Market (R$ million) – 4Q08

160.0

19.811.7

3.3

3.9

By Brand

195.5

2.0%

PUC

dzarmOthers

127.8Multi -

By Distribution Channel

53.0%

195.5

127.8

64.8

96.2

63.0

0

50

100

150

4Q07 4Q08

97.715.311.5

3.3

4Q07 4Q08

2.0%

29.7%

63.7% Franchise/Own Store

Multi -Brand

57.7%

48.4%

Hering

127.8

Multi-brand sales rose more than the franchises and ownstores together.

7

314.2

400

500

600

473.8

61.947.6

10.9

12.9

596.2

8.8%

391.044.9%

52.5%

596.2

391.0

Gross Revenue – Domestic Market (R$ million) – 2008

By Brand By Distribution Channel

PUC

dzarmOthers

Multi -

174.1

282.0

216.9

0

100

200

300

400

12M07 12M08

288.448.043.7

10.9

12M07 12M08

8.8%

29.2%

64.3%

44.9%

62.0%

Relevant growth for Hering brand and Franchise and OwnStore in the domestic market.

8

Hering

Franchise/Own Store

Multi -Brand

4.2

7.5

Private Label vs. Own Brands

100.0%

11.6

55.4%

By Destination

11.6

Gross Revenue – Foreign Market (R$ million) – 4Q08

0.8 0.5

2.0 2.1

1.0

3.6

2.5

-

4T07 4T08

4.1

5.2

4Q07 4Q08

North AmericaPrivate Label

Own Brands

5.2

26.8%

9

5.2

Mercosul

Europe

OthersLatin America

Own brands are the Export focus .

4Q07 4Q08

18.4

35.9

14.433

43

53

59.9%

51.6

33.0

36.0%

33.0

51.6

Gross Revenue – Foreign Market (R$ million) – 2008

Private Label vs. Own Brands By Destination

3.8 1.6

8.15.1

5.9

1.1

15.4

18.5

6.7

12M07 12M08

15.718.6

14.4

-7

3

13

23

12M07 12M08

18.2%

10

Descontinuity of the private label production had animpact on the export commercial results in 2008.

Private Label

Own Brands

North America

Mercosul

Europe

OthersLatin America

31.6%83.2

44.5%

51.0%6.5 p.p.

Gross Profit and Gross Margin Ajusted EBITDA and Adjusted EBITDA Margin

Gross Profit and EBITDA (R$ million) – 4Q08

12.0 p.p.

22.7

51.5

19.6%

4T07 4T08

51.4

4T07 4T08

61.8%

11

More participation of the own stores and cost dilution rose up the gross profit and EBITDA margins.

4Q07 4Q08 4Q07 4Q08

127.5%

238.539.4%

46.3%7.0 p.p.

Gross Profit and EBITDA (R$ million) – 2008

Gross Profit and Gross Margin Ajusted EBITDA and Adjusted EBITDA Margin

6.7 p.p.

145.3

12M07 12M08

64.2%

12

EBITDA growth reflects the increase in revenue of t he domestic market and the improvement of the Company’s operating margins. The reversals in 2008 for

expense and tax provisions set up in previous years also impacted this growth.

51.1

105.413.8%

20.5%

12M07 12M08

106.3%

51.5

19.6%

31.6%

19.6%

23.1%

Comparable EBITDA and EBITDA Margin (R$ million)

106.3%127.5%

105.4

91.513.8%

20.5%

13.8%

17.8%66.4%

79.2%

22.7 22.7

37.7

EBITDA EBITDA comparável

4T07 4T08

13

Significant Comparable EBITDA growth of 79.2% even without considering the impacts neither of Law no. 11,638 n or of the

reversals in 2008 for expense and tax provisions se t up in previous years.

51.1 51.1

EBITDA EBITDA comparável

2007 20084Q07 4Q08

Comparable EBITDA Comparable EBITDAAdjusted EBITDA Adjusted EBITDA

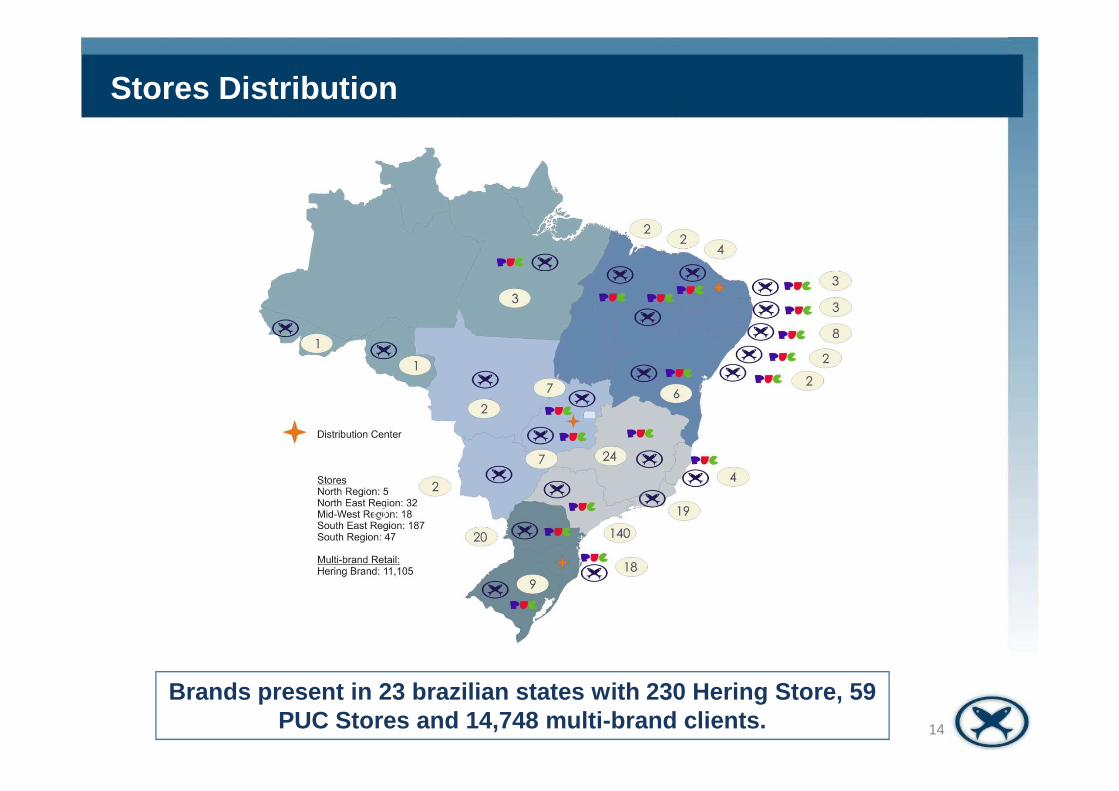

Stores Distribution

Brands present in 23 brazilian states with 230 Hering St ore, 59 PUC Stores and 14,748 multi-brand clients.

14

38

151

268

32557

181

Hering Store Expansion

Expansion Plan

230

Own StoresFranchise* estimated

* *

Review of the Hering own Stores opening, adapting t he priorities to the expansion and remodeling of the existing stores , as well as

possible acquisitions of franchises.15

39

4419

23

22

59

Goal: 172

248

311

209

Goal: 224

Goal: 57

Distribution Network (number of stores)

Distribution Network Evolution

151181

230

2006 2007 2008

Hering PUC Abroad

Goal: 172

Cia. Hering surpassed the opening plan in 6 Hering Stores and 2 PUC stores estimated for the year.

16

Period State City Location Status

1Q08 PI Teresina Shopping Riverside Walk Opened1Q08 SP São Paulo Bourbon Shopping Pompéia Opened2Q08 SP São Paulo Rua Dr. Diogo de Farias Opened2Q08 SP Santa B.D'Oeste Tivoli Shopping Opened2Q08 SP São Paulo Rua Juventus Opened2Q08 MG Juiz de Fora Independência Shopping Opened2Q08 SP Guaratinguetá Shopping Buriti Guará Opened2Q08 PB João Pessoa Shopping Tambiá Opened2Q08 SE Aracaju Shopping Jardins Opened

Status

1Q08

2 Franchises Opened

2Q08

10 Franchises Opened

Expansion 2008 – Franchise

2Q08 SE Aracaju Shopping Jardins Opened2Q08 PR Maringá Shopping Avenida Center Opened2Q08 PE Caruaru Shopping Caruaru Opened2Q08 DF Brasília Liberty Mall Opened3Q08 MG Divinópolis Rua A.Olimpio de Morais Opened3Q08 SP Botucatu Rua Monsenhor Ferrari Opened3Q08 SC Florianópolis Floripa Shopping Opened

3Q08 SP São Vicente Brisamar Shopping Opened

3Q08 SP Campinas Campinas Shopping Opened3Q08 BA Feira de Santana Shopping Iguatemi Opened3Q08 MG Patos de Minas Rua Agenor Maciel Opened3Q08 SP Jau Rua Amaral Gurgel Opened3Q08 PR S. José dos Pinhais Shopping São José Opened3Q08 SP São Paulo Rua Bernardino de Campos Opened

10 Franchises Opened

3Q08

10 Franchises Opened

17

Period State City Location Status

4Q08 SP São Paulo Shopping Metrô Blvd. Tatuapé Opened

4Q08 SP São Paulo Rua Min. Roberto Cardoso Alves Opened

4Q08 PE Recife Shopping Plaza Casa Forte Opened

4Q08 SP Votuporanga Rua Pernambuco Opened

4Q08 SC Criciuma Shopping Della Giustina Opened

4Q08 MG Três Corações Rua Julião Arbex Opened

4Q08 GO Rio Verde Shopping Rio Verde Opened

4Q08 SP Limeira Center Plaza Shopping Opened

Status

4Q08

21 Franchises Opened

Expansion 2008 – Franchise

4Q08 SP Limeira Center Plaza Shopping Opened

4Q08 SC Jaraguá do Sul Shopping Center Breithaupt Opened

4Q08 MG Montes Claros Montes Claros Shopping Center Opened

4Q08 SP São Paulo Shopping Central Plaza Opened

4Q08 RO Porto Velho Porto Velho Shopping Opened

4Q08 RS Porto Alegre Barra Shopping Sul Opened

4Q08 MG Sete Lagoas Rua Santa Helena Opened

4Q08 GO Anápolis Brasil Park Shopping Opened

4Q08 SC Itajaí Itajaí Shopping Opened

4Q08 MG Uberaba Rua Arthur Machado Opened

4Q08 PR Curitiba Shopping Jardins das Américas Opened

4Q08 PR Londrina Royal Plaza Shopping Opened

4Q08 SP Pindamonhangaba Rua Bicudo Leme Opened

4Q08 SP Taubaté Taubaté Shopping Opened18

Period State City Location Status

2Q08 RJ Rio de Janeiro Ilha Plaza Shopping Opened

2Q08 SP São Paulo Shopping Taboão Opened

2Q08 PR Curitiba Palladium Shopping Center Opened

3Q08 SP São Paulo Shopping Penha Opened

3Q08 SP São Paulo Shopping Metrô Itaquera Opened

3Q08 RJ Rio de Janeiro Shopping Tijuca Opened

3Q08 PR Curitiba Rua XV de Novembro Opened

Status

2Q08

3 Stores Opened

3Q08

Expansion 2008 – Own Stores

3Q08 PR Curitiba Rua XV de Novembro Opened

4Q08 RJ Rio de Janeiro Shopping Grande Rio Opened4 Stores Opened

4Q08

1 Store Opened

19

Hering Store Indicators

Hering Store Performance 4Q07 4Q08 Var. 2007 2008 Var.

Number of Stores 181 230 27.1% 181 230 27.1%

Franchise 156 193 23.7% 156 193 23.7%

Own 25 37 48.0% 25 37 48.0%

Sales (R$ thousand) 108,242 169,028 56.2% 276,121 438,844 58.9%

Same Store Sales Growth 29.0% 29.1% 0.1 p.p. 29.0% 32.4% 3.4 p.p.

20

Sales per square meter in 2008 reached its goal of R$ 1 6,100/ m².

Sales Area (m²) 24,106 29,791 23.6% 24,106 29,791 23.6%

Sales (R$ per m²) 4,619 5,776 25.0% 12,625 16,256 28.8%

Check-Outs 1,380,553 2,040,928 47.8% 3,353,403 5,225,865 55.8%

Units 3,303,859 4,760,440 44.1% 7,973,839 12,222,332 53.3%

Average Sales Ticket (R$) 78.40 82.82 5.6% 82.34 83.98 2.0%

1,7 1,20,1 0,410

13.04.7

6.1

0.3

1.2

20

25

30

3535.8

25.3

Stores

IT

Others

By activity

10.510.3

Capex (R$ million)

3,1

6,6

5,52,2

1,2

0

2

4

6

8

4Q07 4Q08

8.4

15.511.8

0

5

10

15

2007 2008

Industry

Stores

21

In 2008, capex was mainly for store remodeling andopening as well as updating of industrial technolog y.

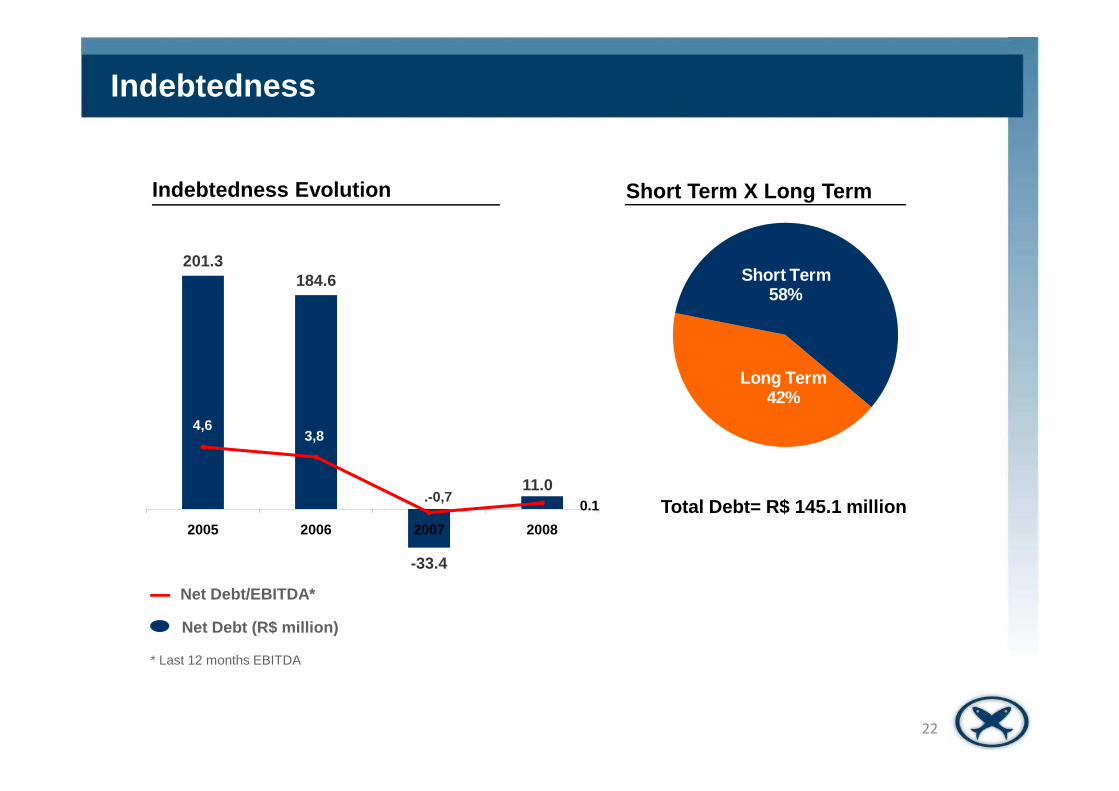

Long Term42%

Short Term58%

Indebtedness Evolution Short Term X Long Term

Indebtedness

201.3184.6

42%

Total Debt= R$ 145.1 million

22

* Last 12 months EBITDA

Net Debt/EBITDA*

Net Debt (R$ million)

-33.4

11.0

4,63,8

.-0,70.1

2005 2006 2007 2008

Financial Result

- In 2008, Law no. 11,638/07 changed the method of measuring fi nancialinstruments, generating an atypical effect in the financia l expense.

R$ thousand 2007 2008 Var.

Net Financial Expenses (30,571) (42,345) 38.5%Net Foreign Exchange Variation 13,198 (3,894) -129.5%Total Financial Expenses (17,373) (46,239) 166.2%

23

-On 12/31/08, Cia. Hering registered an expense of R$ 46.7 mil lion as derivatives’fair value.

- Main derivative: Swap with 19 verifications (Apr/09 to Oct/ 10), amounts betweenR$ 25 to 30 million, with effective losses if the exchange rat e rises above R$/US$2.80.

- The Company is actively monitoring the exchange market in o rder to minimizethe exchange risk arising from derivative transactions.

Payment to Shareholders

Interest on Shareholders Equity

� Payment amounting to R$ 4.8 million (R$0.09/share) on Febru ary 22, 2008,

related to the year ended on December 31, 2007;

� Payment amounting to R$ 4.8 million (R$ 0.09/share) on Septe mber 19,2008,

related to the year ended on December 31, 2008.

24

Dividends

� The payment of dividends amounting to R$ 10.6 million (R$ 0.1 9616/share),

related to the year ended on December 31, 2008, will be propos ed at the

General Shareholders’ Meeting to be held on April 28, 2009.

AGENDA:AGENDA:AGENDA:AGENDA:

• Highlights• Operating Performance

• Business Strategy and Outlook

Strategy & Outlook

Hering Store chain

� Continue expansion plan – 325 stores by the end of 2010

� Maximize operation performance

– Store space allocation review and optimization

– Automatic replenishment for basic items

26

– Fast response for best sellers

– Continuous promotional sales for slow movers

� Promote the Hering Store credit card

Marketing campaign “eu uso Hering desde sempre”

New architectural project for the PUC Stores

Implementation of dzarm. brand relaunching plan

InvestorInvestor RelationRelation TeamTeam

Fabio Hering Fabio Hering –– Vice Vice PresidentPresident andand IR IR DirectorDirectorFrederico de Aguiar Oldani Frederico de Aguiar Oldani –– Financial Financial DirectorDirectorKarina Koerich Karina Koerich –– IR ManagerIR ManagerGracila Camargo Lopes Gracila Camargo Lopes –– IR IR AnalystAnalyst

Tel.: +55 (47) 3321Tel.: +55 (47) 3321--3469 3469 EE--mailmail: [email protected]: [email protected]: www.ciahering.com.br/ir: www.ciahering.com.br/ir

27

Investor Relations Consulting Firm

FIRB – Financial Investor Relations Brasil

Ligia Montagnani – IR Consultant

Tel: +55 (11) 3897-6857

E-mail: [email protected]