Embed Size (px)

Citation preview

TOPIC

FINANCIAL ANALYSIS OF *RAHIM TEXTILE* (2009-2013)

1. Hossain, Mohammad Sazzad ID: 12-21618-22. Haque, Nadia ID: 12-21865-23. Islam, Shafiqul ID: 12-21987-2

*FINANCIAL MANAGEMENT*TEACHER: ABEDIN,MD

JOYNAL SECTION: D

INTRODUCTION

To evaluate the firm’s financial performance. To compare the strength and weakness of

various company . To measure the company productivity. To identify the opportunity and risk in the

company performance. To review the financial performance Provide the key information regarding the

companies financial performance . Help to take the decision to invest the money.

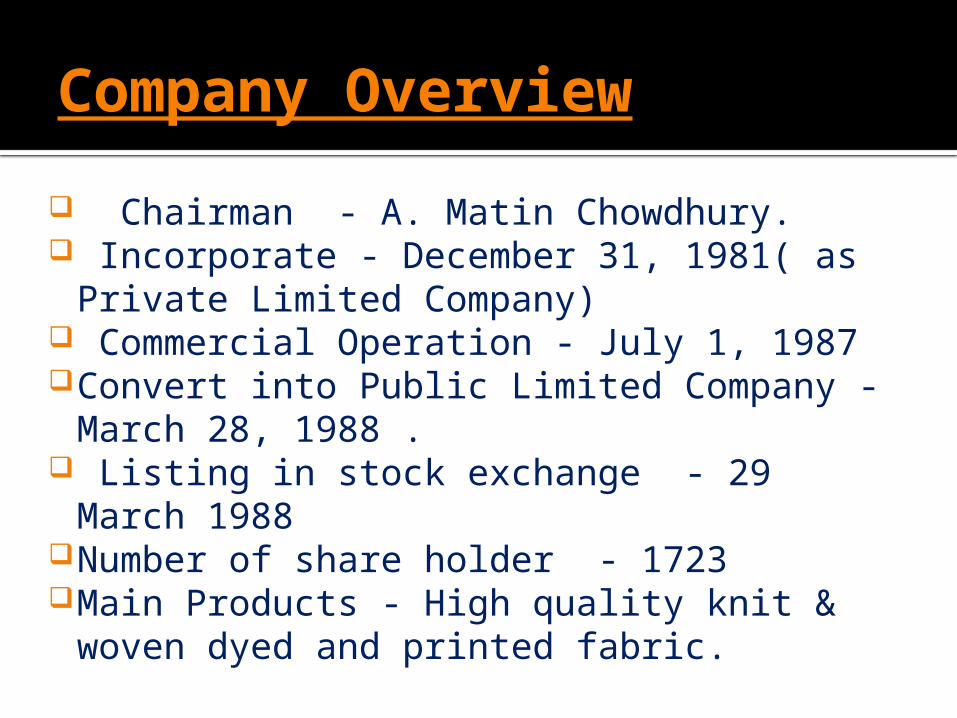

Company Overview Chairman - A. Matin Chowdhury. Incorporate - December 31, 1981( as

Private Limited Company) Commercial Operation - July 1, 1987 Convert into Public Limited Company -

March 28, 1988 . Listing in stock exchange - 29 March 1988Number of share holder - 1723Main Products - High quality knit & woven

dyed and printed fabric.

'RATIO ANALYSIS'

There are four types of Ratio1. Liquidity Ratio2. Leverage Ratio3. Turnover Ratio4. Profitability Ratio

Liquidity ratio:

There are three types of Liquidity Ratio

I. Current RatioII. Quick RatioIII.Cash Ratio

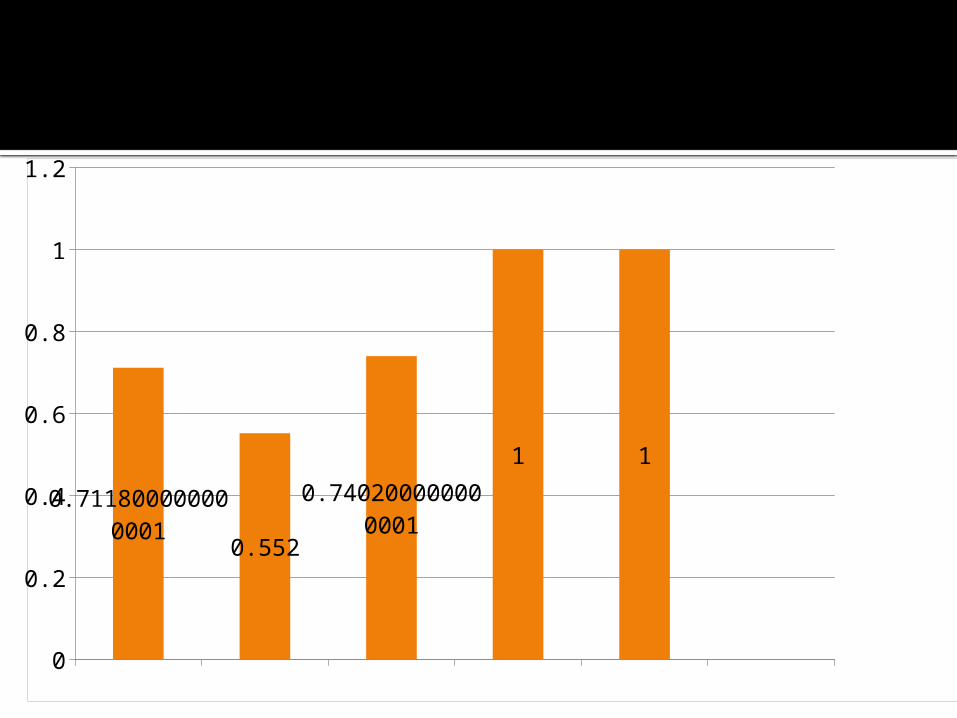

Current ratioFormula: current asset/current liabilities

2009 2010 2011 2012 20130

0.2

0.4

0.6

0.8

1

1.2

0.711800000000001 0.552

0.740200000000001

1 1

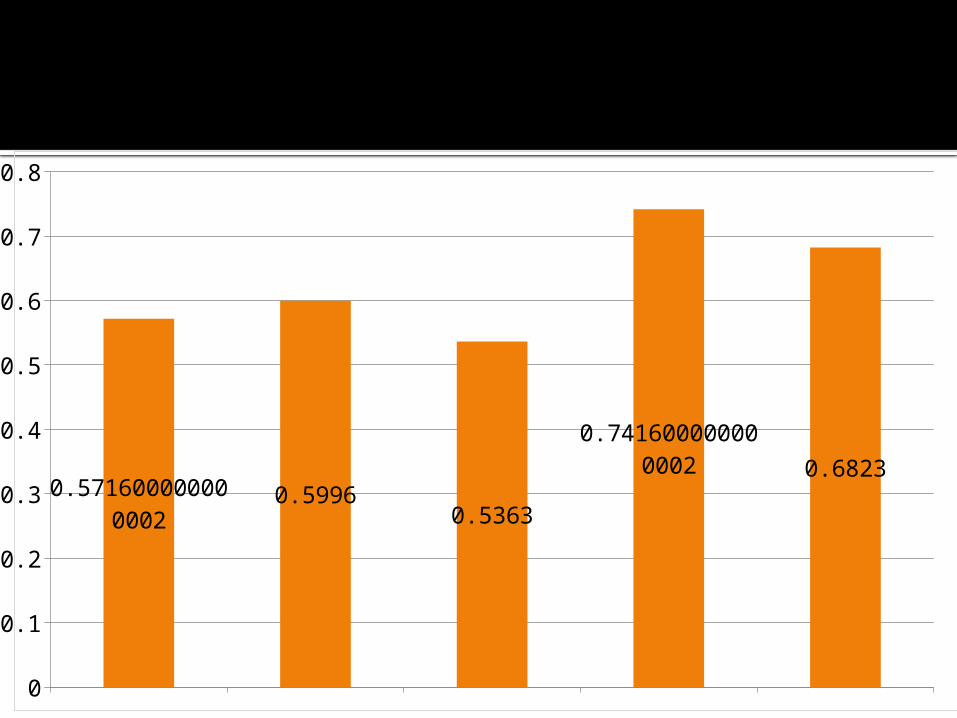

Quick ratio

Formula: current asset-inventories/current liabilities.

2009 2010 2011 2012 20130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.571600000000002

0.59960.5363

0.741600000000002 0.6823

Cash ratio:

formula: cash + cash equivalent /current liabilities

2009 2010 2011 2012 20130

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.0892 0.0790000000000002 0.0791

0.1129

0.158

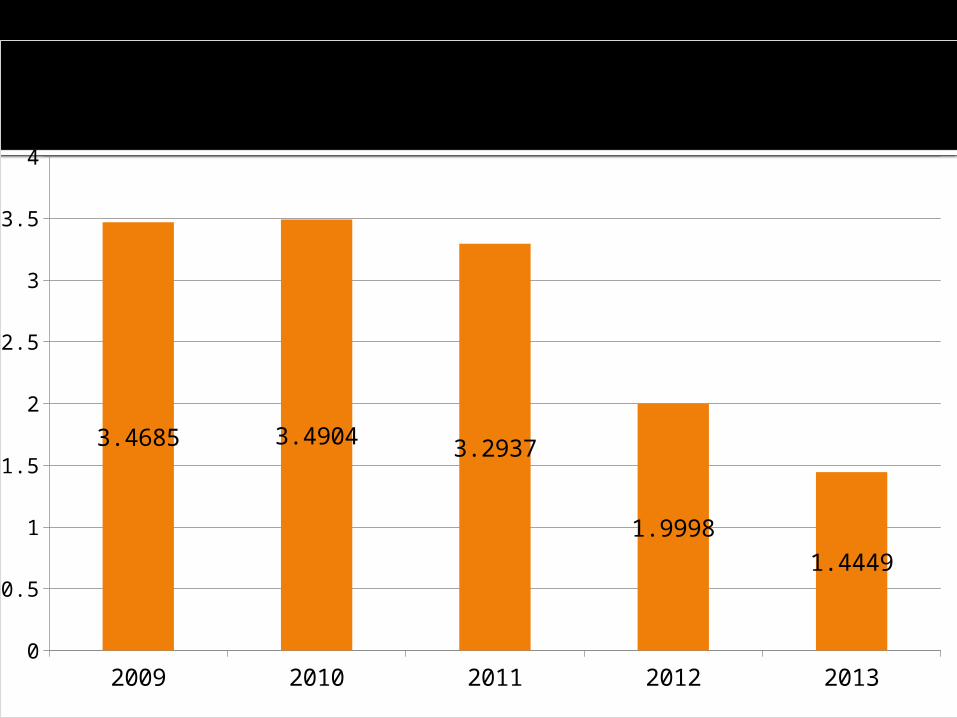

Leverage ratio:

Debt to equity ratio Formula: Total Debt/ shareholder

equity

2009 2010 2011 2012 20130

0.5

1

1.5

2

2.5

3

3.5

4

3.4685 3.4904 3.2937

1.99981.4449

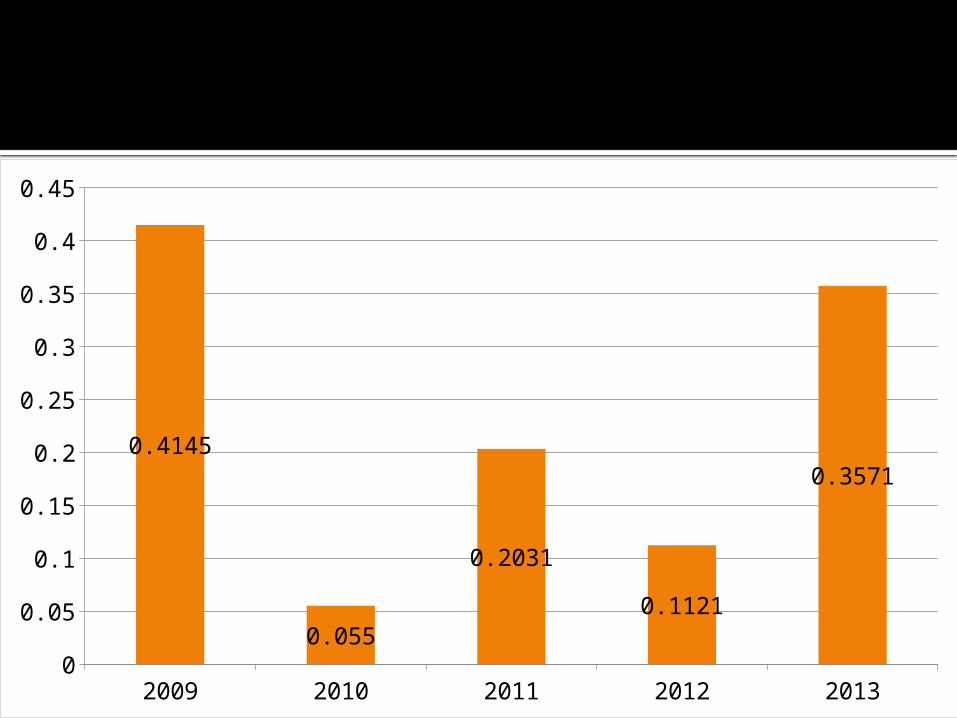

Interest coverage ratio:

Formula: earnings before interest and tax/interest expense

2009 2010 2011 2012 20130

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.4145

0.055

0.20310.1121

0.3571

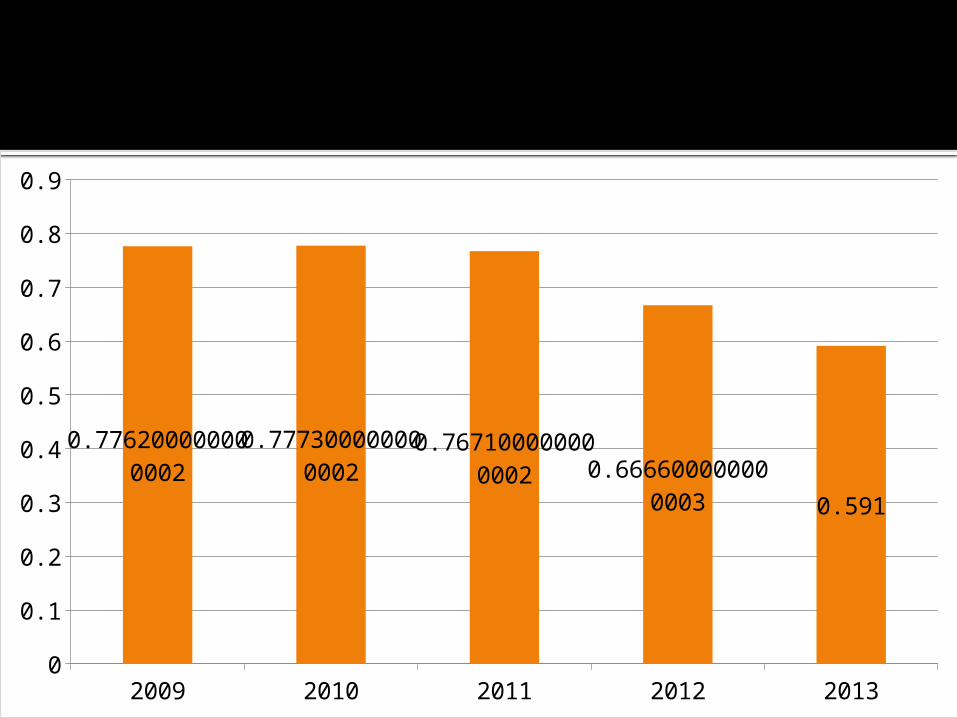

Debt to capital ratio:

formula: Total Debt/shareholders equity

2009 2010 2011 2012 20130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.776300000000002

0.777300000000002

0.767100000000002 0.6666000000000

03 0.591

Debt to Total Assets:

Formula: (short term debt + long term debt) / total asset

2009 2010 2011 2012 20130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.776200000000002

0.777300000000002

0.767100000000002 0.66660000000

0003 0.591

Turnover ratio:

There are four ratio in the turnover ratio.

1. Receivable turnover ratio 2. Receivable turnover in days 3. Inventory turnover ratio 4. Inventory turnover ratio in days

Receivable turnover ratio=sales/ account receivable

year2009 tear2010 year2011 year2012 year20130

1

2

3

4

5

6

7

8

9

10

3.62993.229

4.7498 4.7421

8.7343

Receivable turnover

Series 1

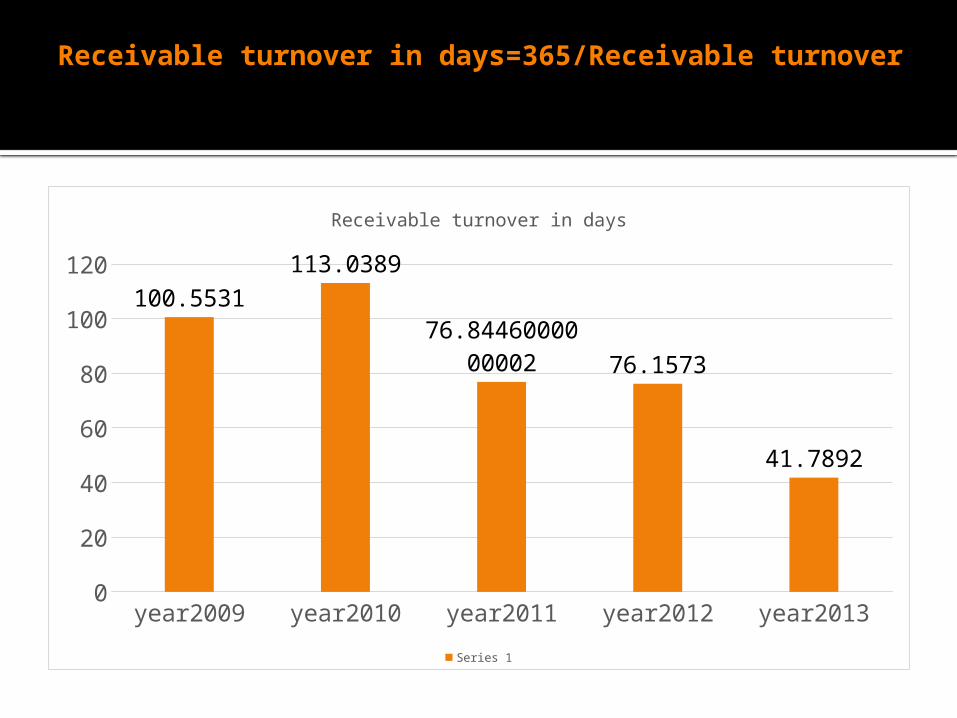

Receivable turnover in days=365/Receivable turnover

year2009 year2010 year2011 year2012 year20130

20

40

60

80

100

120100.5531

113.0389

76.8446000000002 76.1573

41.7892

Receivable turnover in days

Series 1

Inventory turnover ratio

Inventory turnover ratio: cogs/inventory

year2009 year2010 yar2011 year2012 year20130

2

4

6

8

10

12

9.56068.7914

7.2482

8.7727

11.049

Invntory turnover

Series 1

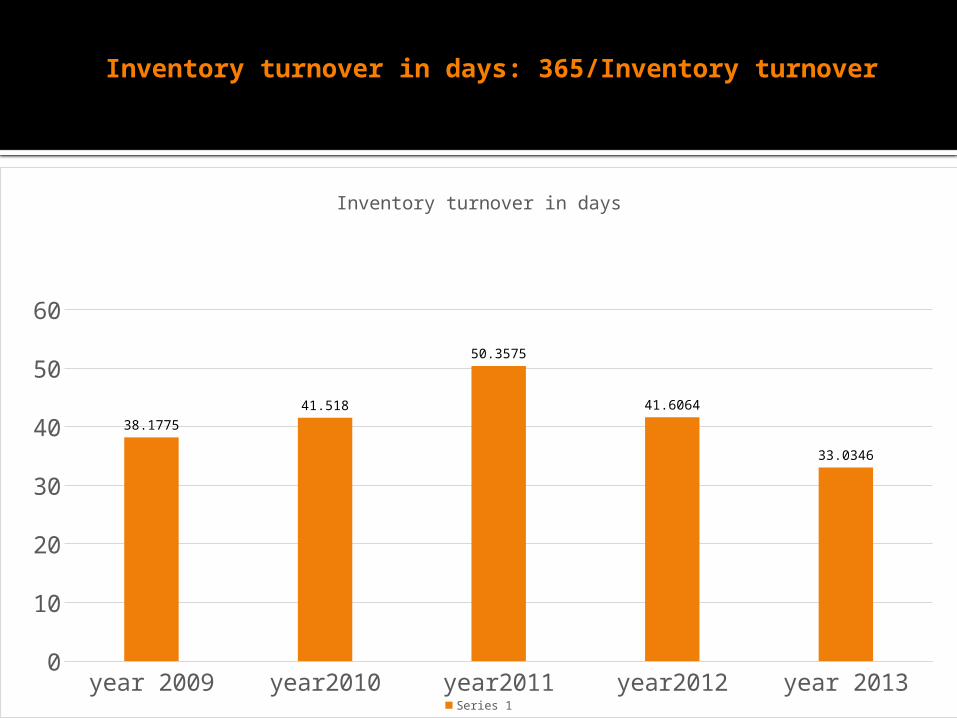

Inventory turnover in days: 365/Inventory turnover

year 2009 year2010 year2011 year2012 year 20130

10

20

30

40

50

60

38.177541.518

50.3575

41.6064

33.0346

Inventory turnover in days

Series 1

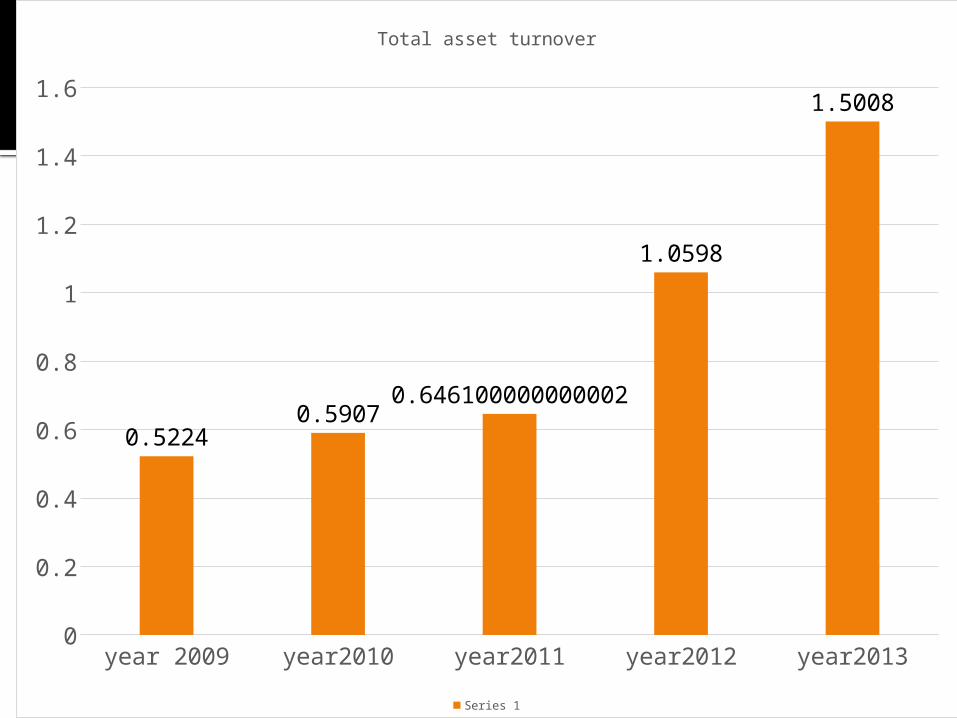

Total asset Turnover

Total asset turnover: Net sales/total assets

year 2009 year2010 year2011 year2012 year20130

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0.52240.5907

0.646100000000002

1.0598

1.5008

Total asset turnover

Series 1

Profitability ratio

Profitability ratio has four ratioI. Gross Profit MarginII. Net Profit MarginIII. Return On EquityIV. Return On Asset

Gross profit margin ratio = (sales-cogs)/sales

year 2009 year2010 year 2011 year 2012 year 201313

13.514

14.515

15.516

16.517

17.517.07 16.89 16.81

14.49 14.51

gross profit margin

gross profit margin

Net profit margin

Net profit margin ratio= Net income /sales

year 2009 year2010 year2011 year2012 year 20130

0.5

1

1.5

2

2.5

3

3.53.26

0.55

1.87

0.940000000000001

2.23

Net profit margin

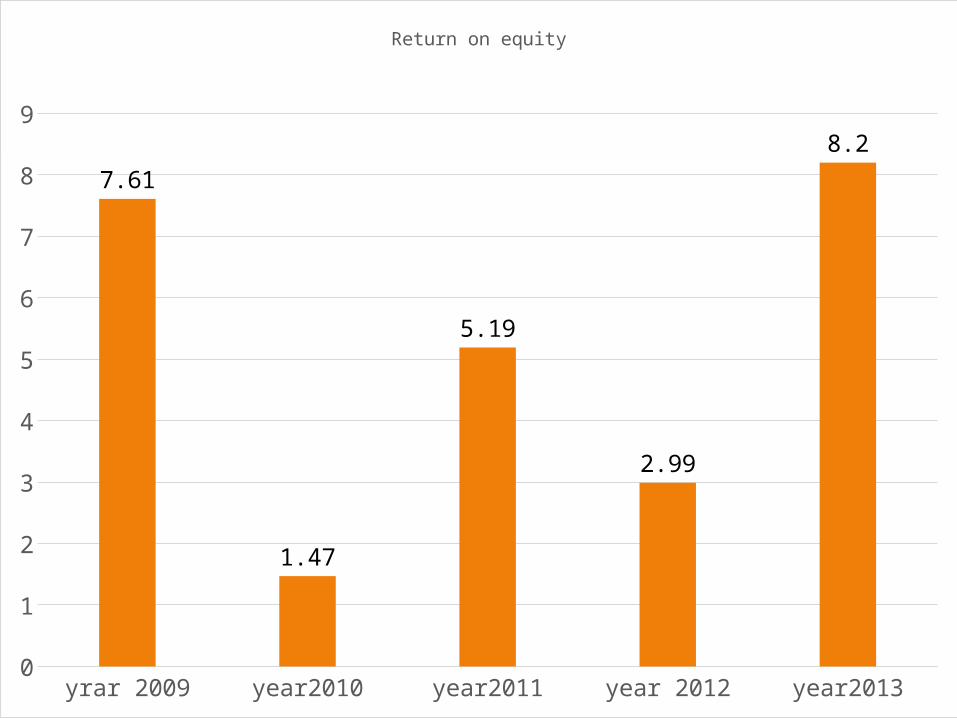

Return on equity

Return on equity= Net profit after

tax/ total equity

yrar 2009 year2010 year2011 year 2012 year20130

1

2

3

4

5

6

7

8

9

7.61

1.47

5.19

2.99

8.2

Return on equity

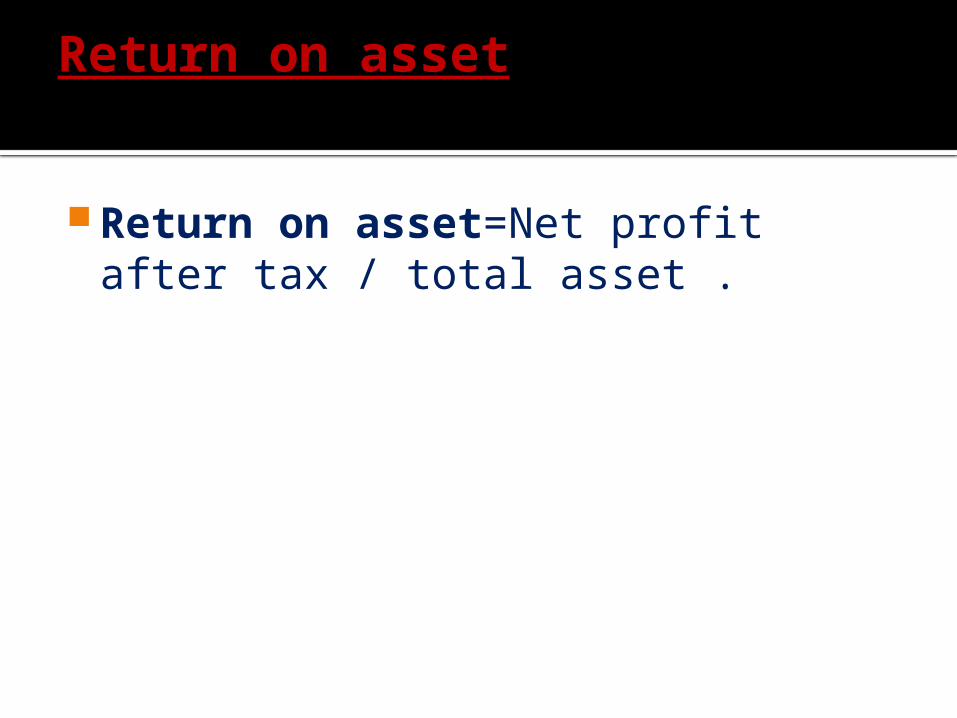

Return on asset

Return on asset=Net profit after tax / total asset .

year2009 year2010 year2011 year20120

0.5

1

1.5

2

2.5

3

3.5

4

1.7

0.330000000000001

1.21

3.35

Return on assest

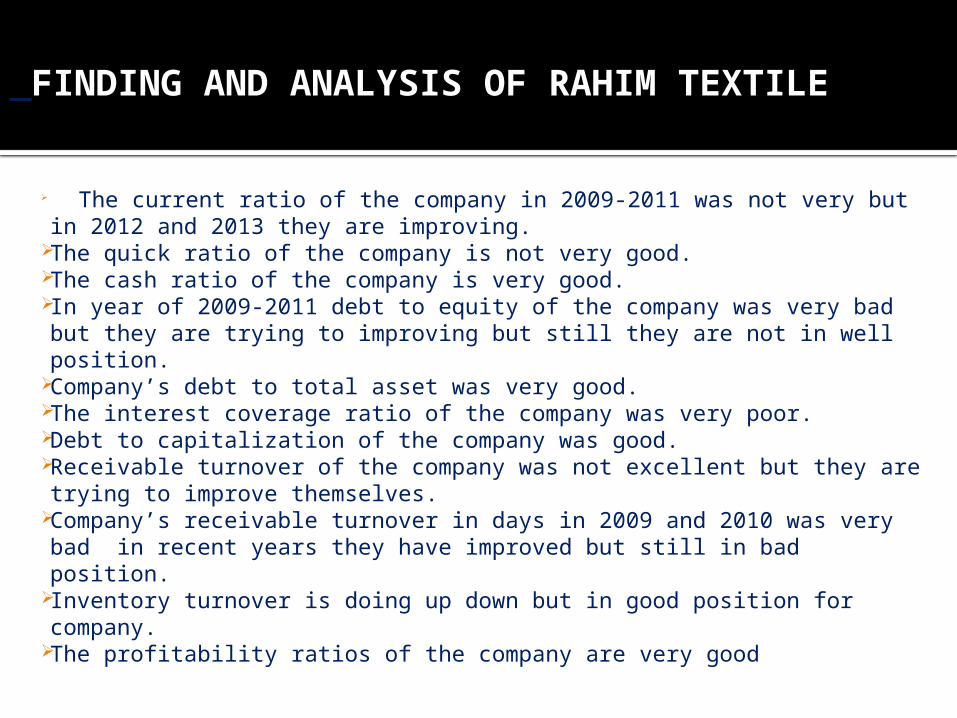

FINDING AND ANALYSIS OF RAHIM TEXTILE

The current ratio of the company in 2009-2011 was not very but in 2012 and 2013 they are improving.

The quick ratio of the company is not very good. The cash ratio of the company is very good. In year of 2009-2011 debt to equity of the company was very bad but

they are trying to improving but still they are not in well position. Company’s debt to total asset was very good. The interest coverage ratio of the company was very poor. Debt to capitalization of the company was good. Receivable turnover of the company was not excellent but they are

trying to improve themselves. Company’s receivable turnover in days in 2009 and 2010 was very

bad in recent years they have improved but still in bad position. Inventory turnover is doing up down but in good position for company. The profitability ratios of the company are very good

CONCLUSION

We know that the progress of a

company depend on appropriate financing and keeping statement. Rahim textile company should have analysis their performance to overcome their problems.