Embed Size (px)

Citation preview

HANIWAR

EXCUTIVE DIRECTOR NAMPA

BRISBANE, 22 – 23 AUGUST 2013

“Opportunities in Meat Intermediate Industry"

Introduction

o Nowadays, Beef consumption in Indonesia is still low, it’s only about 2 to 2.2 kg per capita.

o Total national beef consumption is about 500 ,000 tons in 2012. Only about 8% or 40,000 tons was processed. By which Nampa members processed 20,000 tons into variety of products such as sausages, meatballs hamburgers, smoked beef, etc.

o In Singapore, Malaysia and Vietnam meat consumption in 2010 was at least 7 kg per capita, or almost 3-4 times compared to Indonesia (Table 1).

o Meat processed to meat consumption ratio in those neighboring countries was estimated at least 15%, or at least twice compared to Indonesia.

Table 1. Meat Consumption per Capita 2010 ( USDA ) http://www.indexmundi.com/agriculture/?country=vn&commodity=beef-and-veal-mea

Argentina 56 Australia 36

Malaysia 7 Singapore 7

Brazil 39 Vietnam 7

Mexico 17 Egypt 8

Philipine 4 Japan 10

Indonesia 2 Iran 10

Table 2. Sausage Production Volume in Indonesia vs Asean Year 2007(based on meter casing imported )

Country Population ( million )

Sausage production ( m casing)

Average Mtr/person

Indonesia

Philipine

Thailand

Malaysia

220

83

64

27

57.600.000

635.000.000

465.000.000

150.000.000

0.26

7.65

7,26

5.55

Table 2 compares sausage production volume between Indonesia and some neighboring countries in 2007, it shows that Indonesia’s sausage production volume was far below neighboring countries.

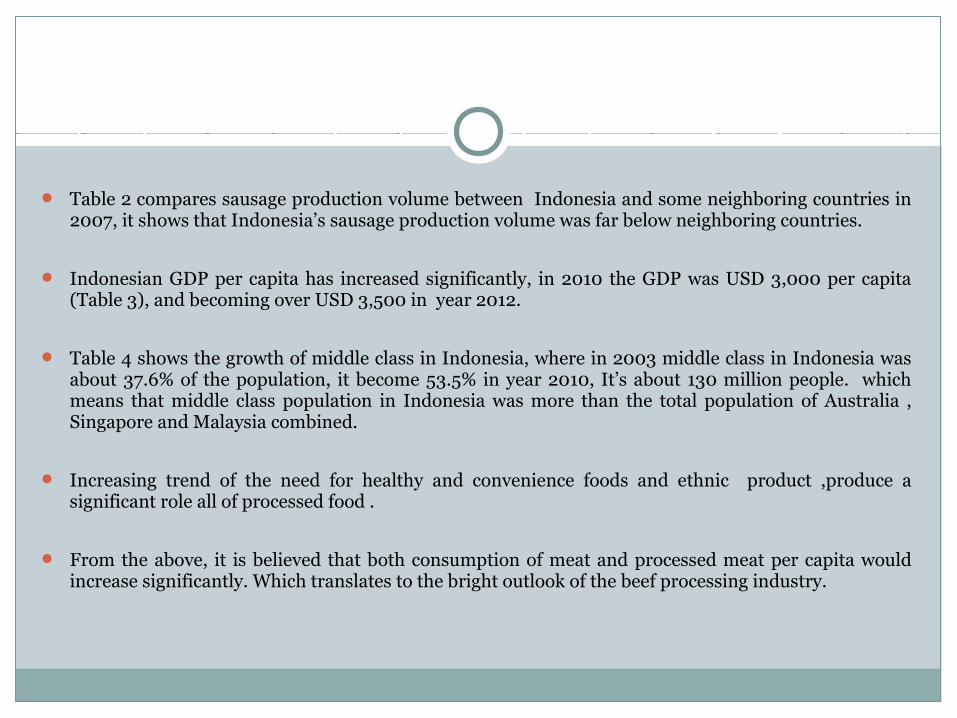

Indonesian GDP per capita has increased significantly, in 2010 the GDP was USD 3,000 per capita (Table 3), and becoming over USD 3,500 in year 2012.

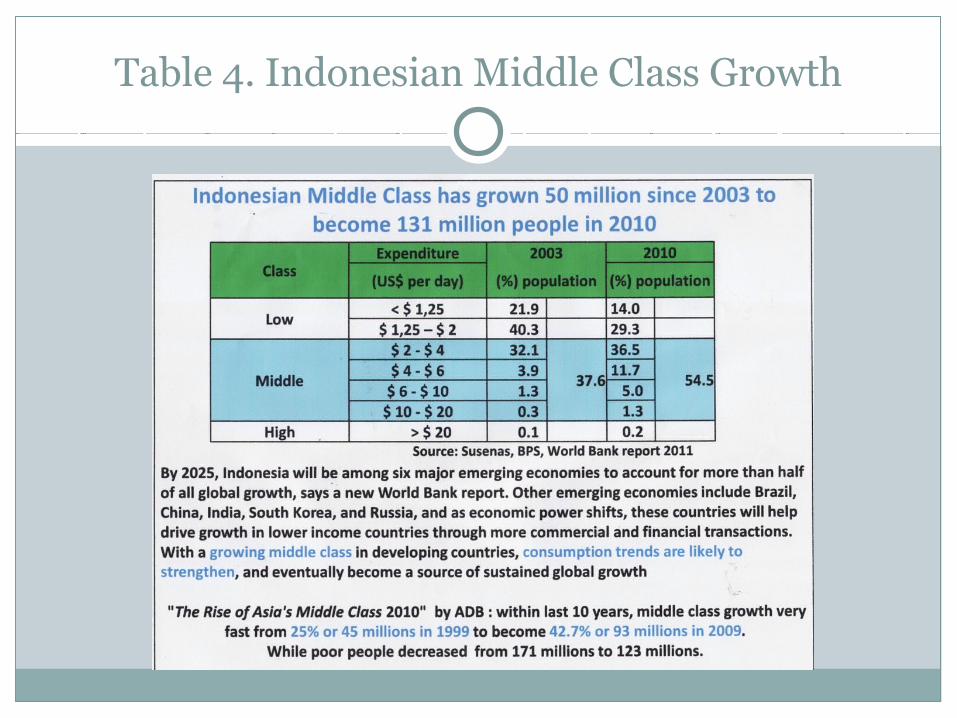

Table 4 shows the growth of middle class in Indonesia, where in 2003 middle class in Indonesia was about 37.6% of the population, it become 53.5% in year 2010, It’s about 130 million people. which means that middle class population in Indonesia was more than the total population of Australia , Singapore and Malaysia combined.

Increasing trend of the need for healthy and convenience foods and ethnic product ,produce a significant role all of processed food .

From the above, it is believed that both consumption of meat and processed meat per capita would increase significantly. Which translates to the bright outlook of the beef processing industry.

Tabel 3. The GDP per Capita is Growing

Table 4. Indonesian Middle Class Growth

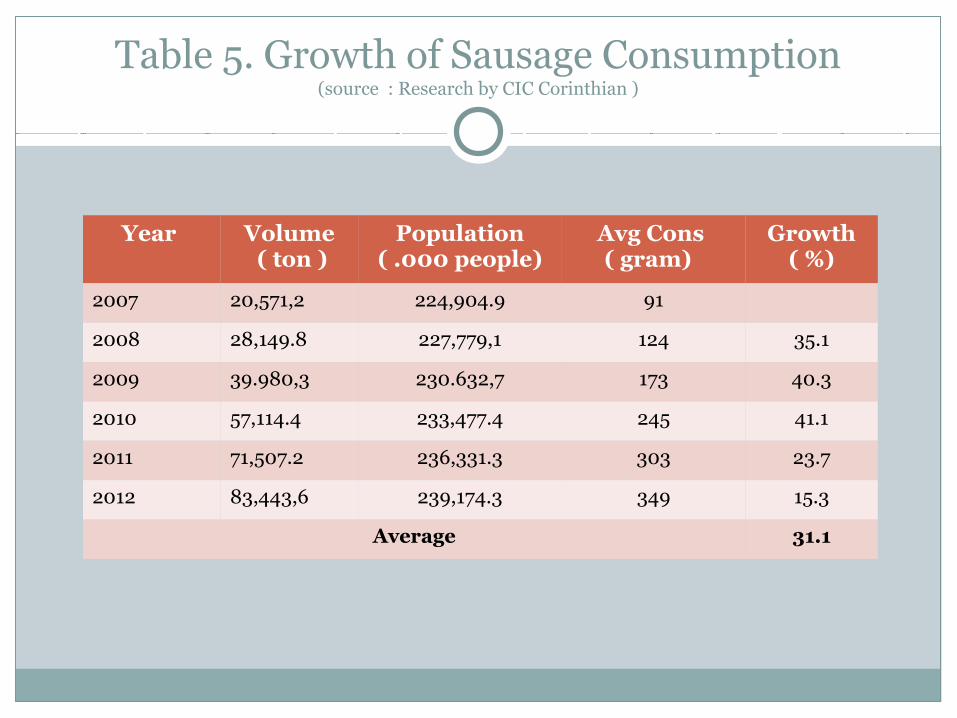

Table 5. Growth of Sausage Consumption(source : Research by CIC Corinthian )

Year Volume ( ton )

Population( .000 people)

Avg Cons ( gram)

Growth( %)

2007 20,571,2 224,904.9 91

2008 28,149.8 227,779,1 124 35.1

2009 39.980,3 230.632,7 173 40.3

2010 57,114.4 233,477.4 245 41.1

2011 71,507.2 236,331.3 303 23.7

2012 83,443,6 239,174.3 349 15.3

Average 31.1

Table 5 shows that sausage industry growth between 2007 to 2012 is 31%.

But Table 6 shows that trend for products made from processed chicken grow faster than those made from beef. The data shows, that in 2007 products made from beef is 197% or 1.97 times products made from chicken, while in 2012 decreased to 112.4 % or 1.1 times products made from chicken.

It’s happened due to government policy to achieve self-sufficiency in beef by 2014, which made beef become so scarce and prices soared . While the other side, chicken’s raw material is more available and cheaper. That’s why the growth of processed chicken is higher than meat.

Table 6. The Growth of Sausage by Raw Material (source : Research by CIC Corinthian )

Raw material

2012 ( ton )

2011(ton)

2010(ton)

2009(ton)

2008(ton)

2007(ton)

Avg Growth

Beef 42,299.6 38,864.2 30.143,0 22.458,8 16.511,6 12,843.5 27.2

Chicken 37,518.5 31,280.5 24,194.0 15,305.0 9,942.5 6,499.6 42,8

Beef/chicken (%)

112.74 117.85 124.59 146.66 166,07 197,60

Meat Industry Problem for Having Beef as Raw Material

Two main problems faced by meat processing industry since 2012 are, one inability of local cattle farms to meet the needs of industrial raw materials, and second decrease the amount of meat imports from approximately 100,000 tons per year in 2010 and 2011 to 34,000 tons in 2012 and 32,000 tons in 2013.

As a result of this policy, at the end of the 1st semester in 2012 meat processing industry was finding difficulty in obtaining raw materials, and had informed the government about the possibility of some beef processing industry to collapse. The government then gave a positive reaction by giving an exclusive quota to Nampa’s member for amount 7,000 tons in the 2nd semester of 2012, resulting the total import quota to be 41,000 tons from the original 34,000 tons quota, which include quota for APMISO and ADDI for 750 tons each.

For 2013, the national quota is reduced again to 32,000 tons, in which it includes 14.500 tons exclusive quota for Nampa members , and also approximately 4,500 tons for small processed beef industry represented by 3 associations, namely APMISO, ADDI and ASPERDATA.

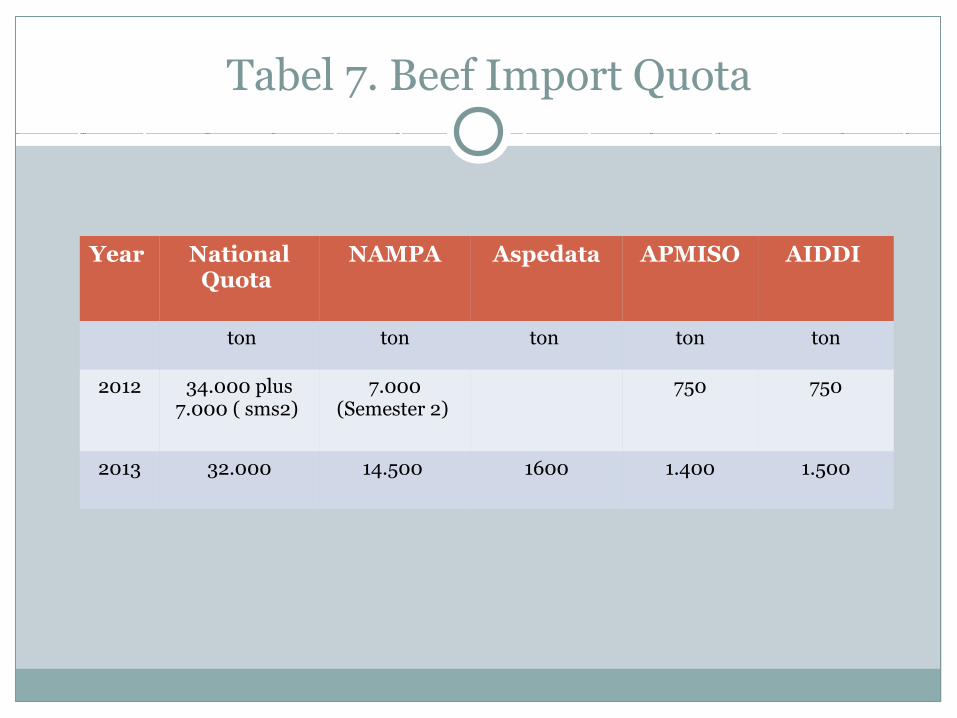

Details of which can be seen in Table 7: Beef Import Quota.

Tabel 7. Beef Import Quota

Year National Quota

NAMPA Aspedata APMISO AIDDI

ton ton ton ton ton

2012 34.000 plus7.000 ( sms2)

7.000(Semester 2)

750 750

2013 32.000 14.500 1600 1.400 1.500

Explanation for Table Beef Import Quota

Nampa : National Meat Processor : Big and medium size industry, have 31 members.

Aspedata : small size industry.

Apmiso : association of Mie bakso (chicken / meatballs noodles) stalls / small restaurants who also produce bakso ( meat ball ).

AIDDI : small size industry .

On 2012 , The government approved additional quota exclusively for NAMPA for 7.000 ton, so the total quota is 41.000 ton.

On 2013 , until August 2013 no additional quota yet.

On 2011 : the total import for Beef was 90.000 ton.

Given the meat processing industry increase during recent years and the future potential growth of 20%, the quota is inadequate to meet the industry’s demand.

Due to current quota, NAMPA could only manage to keep the existing capacity and can not growth to higher industry.

To ensure that the import quota for 2014 also takes into account industry’s demand to growth, currently (August 2013) a survey is being carried out by an independent surveyor.

It is believed that if with the win-win base support of Australian industry , the industry’s growth could reach 30 percent and maybe even up to 50%, which means that there are great prospects in this field.

Moreover, Indonesian processed products have not yet produced typical Indonesian ethnic products such as rendang, rawon, and semur. The industry is currently focused to western product such as sausages, burgers, smoked beef etc.

If we added the Indonesian typical ethnic products on our line of production , it is estimated an excellent export opportunities other than domestic market .

NAMPA was build in 2002 with 15 members. Now, we have 31 members consisted of big and medium-scale enterprises which accounted from at least 80% of the total production of big scale and medium processed meats in Indonesia. There is still some medium enterprises that are not becoming Nampa’s member yet. Other than big and medium size industry , there are also many (estimated to be thousands) small businesses with huge numbers (to thousands) of which their total output is estimated, at maximum, to equal the production by 31 NAMPA members.

Constraints

Supply of local beef with good quality and competitive prices are still limited , and also inadequate quota for supply from import, are hindering the beef processing industry to grow.

Lack of cold storage facilities for the domestic market, lack of well certified slaughter house . (From more than 1,000 slaughterhouses in Indonesia, only a few dozen certified slaughterhouses ).

Lack of domestic supply of production supplies and food additives such as sausage casings, binders, food coloring , TVP and seasoning, which made most of them are imported, with the risk of lack of continuity supply.

No industry specialized in manufacturing meat processing machines, neither simple or sophisticated, ranging from knives to integrated meat processing engine.

Lack of trained manpower and competence based training institute to improve skills of processing Industry employees.

Lack of incorporate international specifications for export products because lack of experienced to exports processed meat products.

No specific research institute for the development of processed meat products industry, there is only for food in general .

Investment / Cooperation Opportunities

Existing regulations in Indonesia allowed to import beef for raw materials for meat processing industry if it can not supply by domestic products either because the amount is insufficient or the specification does not match the need of meat industry.

This gives an opportunity for industry to get win-win cooperation from Australia. Because the need to import Australian meat products will still increase despite the growth of domestic meat production.

Currently 80 percent of beef supply for NAMPA’s member is imported mainly from Australia, or about 16,000 to 20,000 tons per year and is projected at least to increase by 25 to 35 % per year.

Table 8. Simulated Increase in Production on Growth of 25, 35 and 50% Sales per Year (in ton of beef raw material)

Year Existing 15 % 25 % 35 % 50 %

2012 20. 000

2013 20.000

2014 23.000 25 .00027,000 30,000

2015 26.450 31.250 36,450 45,0002016 30.418 39,063 49,208 67,5002017 34.980 48,828 66,430 101,2502018 40.227 61,035 89,681 151,875

Growth target of 50% is an optimistic target while 15% is a conservative target.

While between 25% to 35% is very likely to be achieved with further cooperation or investment by Australia, because 25% to 30% increase have been occurred. Furthermore, the acceleration of the increase will be supported by increasing in number of Indonesian middle class, rising GDP per capita , trend for fast food consumption, convenience and healthy foods.

Table 8 simulates the growth of production, using basic assumption that production in 2013 will be the same with 2012. Within 5 years, if projected growth is only 15% per year, it will be 40,000 tons, if 25 % 61,000 tons, if 35% 89 ,000 tons and if 50% will be 151,000 tons. In summary, with conservative estimate, it’s projected that there will be an increase by 3 to 4 times from the amount needed this year.

Competency-based training aid for processed meat industry employees by conducting training both in the Australia and establishing competency-based training institute for meat industry in Indonesia.

Improving skill of worker’s will have a significant impact to push the growth of the Indonesian meat processing industry which in turn also provide opportunities for Australia to supply the demands increased for the processed meat industry in Indonesia.

Direct investments in meat industry supplies such as sausage casing, spices , knife, processing machine, will also give good impact for both countries because the potential market is big and also can be used by factory using chicken and fish as raw material and also by food processor in general , which is also growing fast in Indonesia .

Establishing cold storage chain as part of marketing mix so that the domestic market can be opened wider, and also allows the distribution of raw materials and finished products more quickly and widely spread to all area of Indonesia.

Cooperation to increase the ability to produce processed meat based on original Indonesian food like rendang, rawon, semur so that we can supply the local and export market with good quality products and reasonable price.

Work together to improve Indonesian Meat processing industry so the International chain restaurants such as Mc Donalds and Burger King agree to use the products from Indonesian processed meat industry

Upgrade the quality of indonesian meat processed products using Australian meat, meet the standard for Australian / International market for Indonesia ethnic food and halal certified products.

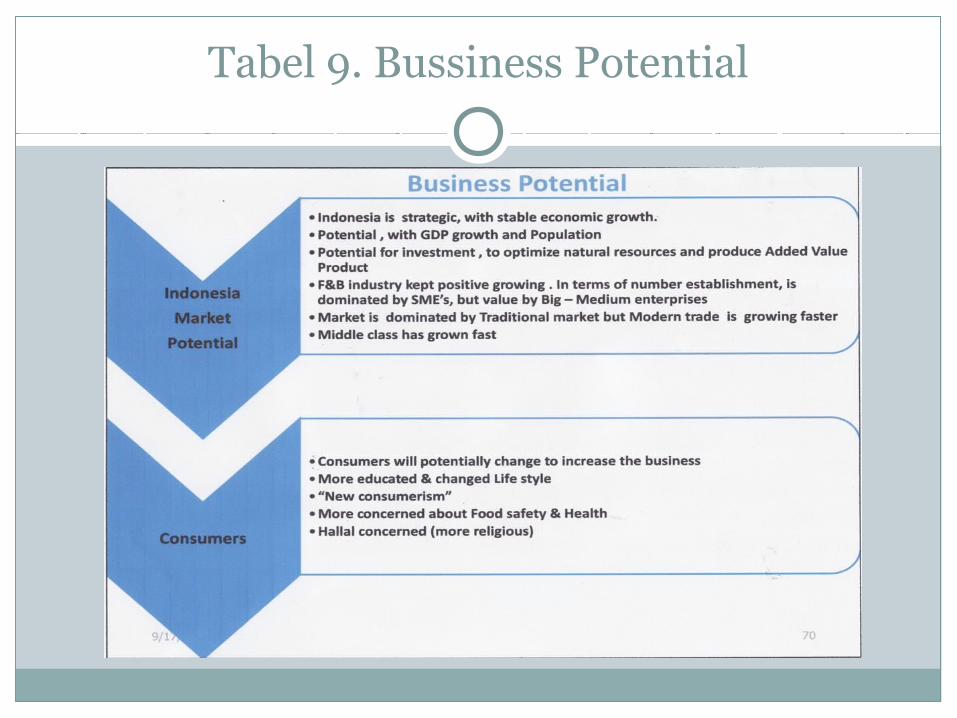

Tabel 9. Bussiness Potential

Conclusion

Prospects of growth of the beef processing industry In Indonesia is huge and could reach at least between 25% -35% per year due to:

The low per capita consumption of beef and processed meat. Indonesian per capita income growing along with rising GDP resulting that there are already

more than 130 million middle-income citizens who are potential consumer. There is a tendency of consumers asking for convenient, healthy, and original Indonesia

products, all of which are potential to be fulfilled by Indonesian meat processing industry. According to the research results by CORINTHIAN, sausages production posted average

growth between 2007 to 2012 of 31%, was achieved without further cooperation with Australia.

Australia is a major producer of beef and also has the advanced processing technology, so the willingness to work together based on win-win will yield a big benefit for both country.

Fields that can be done by Australia. In the short and medium term ,can supply beef as raw material for industry direct from

Australia, long-term can supply form Australian livestock farm investment in Indonesia. Investment in plant producing : Casing, spices, filler, binder, coloring agent and Investment

in making machine for meat processing machine. Out put of these two investment can supply also the need of chicken processor ,fish processor and in general all food processor. Which also growing fast in Indonesia.

Doing competence based training for processed meat worker in Australian training institution and helped establish ,meat processed competence training institutions in Indonesia.

Help create and enhance Indonesia's processed products to be acceptable purposes including developing export Indonesian ethnic products such as rendang, rawon, stews.

Help access export original indonesian meat processed product to other countries by meat distribution network already owned by Australian exporter so Indonesia can export the product like rendang, rawon, etc .

THANK YOU

NAMPAGrand Wijaya Centre Blok F No. 83 B

Jl. Wijaya II, Kebayoran Baru, Jakarta SelatanIndonesia

Ph. +6221-7248455 Fax. +6221-7262087Website : www.nampa-ind.com Email : [email protected]