Embed Size (px)

Citation preview

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 1

NewBase 02 March 2017 - Issue No. 1007 Senior Editor Eng. Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

UAE:How the crude slump has strengthened national oil companies Salem Abdo Khalil is a technical adviser to the Government of Fujairah. ( + NewBase )

A question that has circulated in energy boardrooms for decades is finally being answered. It is a yes – the GCC’s national oil companies can effectively spearhead the development and management of the region’s oil.

Historically, these companies have leaned heavily on international oil companies’ expertise for the development and management of oil reserves. But the tide is turning. The national oil companies have demonstrated their financial acumen by swiftly and smartly slashing budgets and payrolls – while preserving oil supply and security – in response to the decline in oil prices since mid-2014.

Having previously enjoyed bloated balance sheets, these companies are getting used to being on the front line of a cash-strapped battlefield to protect profit margins. Increasingly strict global environmental policies and a soaring energy demand add to the need for change.

The national oil companies must match the commercial acumen long demonstrated by their international counterparts while meeting the social responsibilities that come with playing an integral role in a nation’s identity.

Saudi Aramco’s surprise announcement last year of an initial public offering pencilled in for next year is a good example of how national oil companies, unlike international players, must navigate a three-point agenda: one of commercial success; one of social responsibility; and one that supports the nation’s political agenda.

To kick-start the evolution, there have been leadership changes in the national oil companies of Abu Dhabi, Kuwait, Qatar and Saudi Arabia since 2013. The new chief executive of the Abu Dhabi National Oil Company (Adnoc), Sultan Al Jaber, has said the company must operate efficiently in a way that is more akin to an international super major.

To facilitate this transition, Adnoc plans to merge the operations of the Abu Dhabi Marine Operating Company

and Zakum Development Company into a new company by 2018. Adnoc also intends to combine three of its shipping and ports services units into one.

While national oil companies and international companies have always collaborated, their key performance indicators will forever remain fundamentally different. The Saudi Aramcos and Adnocs of the region manage their assets as part of a long-term energy security strategy. Sustainability is also not just a buzzword for the national oil companies, as illustrated by Qatar’s

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 2

efforts to preserve the North Field by enforcing a moratorium on additional gas development since 2005.

Collaboration between national oil companies and international companies with historic relationships will strengthen over the coming decade in a bid to bat away other increasingly robust competitors. For the GCC countries the primary rivals are Iran and the United States. The opening of the newly widened Panama Canal in mid-2016 gave a significant boost to the latter’s oil and gas export ambitions to East Asia, for example.

Modern and expanded port facilities are a vital part of the GCC national oil companies’ ability to enhance their global offering. The Port of Fujairah is already one of the world’s largest bunkering hubs, and in the past year it has launched a US$175 million very large crude carrier (VLCC) jetty. There are plans to build a second such jetty and increase petroleum storage capacity by 75 per cent to 14 million cubic metres by 2020.

The release of weekly oil inventory data by the Fujairah Oil Industry Zone has spearheaded market discussions on hosting the region’s first independent pricing benchmark for oil products.

National oil companies still need to up their game to match the technological expertise of the international oil companies. The national companies’ easy access to national oil reserves has meant they have fallen behind international companies, who had to become tech-savvy and think outside the box to maximise potential from more challenging assets. What was once to the national companies’ advantage is now their Achilles heel.

National oil companies do not have long to sharpen their game as population growth is increasing domestic usage. The Middle East’s energy demand is forecast to climb 49 per cent by 2035, according to BP’s Energy Outlook, while the International Energy Agency expects the region’s gas demand to double by 2040.

The region’s national oil companies are rapidly maturing. But the jury is still out on whether their dedication to transforming into canny managers will fade if oil prices rise.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 3

Aramco-Malaysia deal set to boost Saudi’s Asia oil exports Reuters/

Top global oil exporter Saudi Arabia broke from the pack in the race to lock up Asian market share after agreeing yesterday to pump $7bn into a refinery-petrochemical complex in Malaysia, analysts said.

State oil giant Saudi Aramco’s investment into Malaysia’s RAPID project will secure an outlet for its crude oil for at least two decades and beefs up its downstream portfolio ahead of its initial public offering (IPO) next year.

The competition in Asia among producers, including Russia and other Middle Eastern suppliers such as Iraq, Kuwait and Iran, is sharp.

Asia’s growing oil demand provides the only home for the producers’ output, especially as they have lost market share in the United States to rising domestic shale oil production. Buying a

share of a large oil refinery with a promise to provide crude is a time-tested producer tactic for locking up customers.

Russia, the world’s largest oil producer, has bought a major stake in India’s Essar refinery and plans to build one in Indonesia with state-owned Pertamina. “The investment is wise as it ensures Saudi can increase its market share in Asia, at a time when rising US shale oil is displacing Saudi oil from the US market,” Gordon Kwan, Nomura’s head of Asia oil and gas research said.

“Being a shareholder of a refinery will give Aramco the upper hand when competing with other Opec countries such as Iran and Iraq, all targeting more oil sales into Asia.”

Under the deal with Malaysia’s Petroliam Nasional Bhd (Petronas), Aramco will supply up to 70 % of the crude for RAPID, which will consist of a 300,000 barrel per day (bpd) oil refinery and petrochemical plants.

Aramco has also strengthened its ties with Indonesia, Southeast Asia’s largest economy, providing 270,000 bpd of crude to the Cilacap refinery owned by Pertamina after taking a 45% stake. The deal “will provide Aramco and the Kingdom a sustainable demand for the Saudi crude and will allow the companies to add value to that crude by making high quality products, fuels or petrochemicals for the Malaysian and neighbouring markets,” Saudi Energy Minister Khalid al-Falih told Saudi state television.

Saudi Arabia exported an average of 6.96mn bpd in 2016 to the top six oil buyers in Asia, including China, India, Japan, South Korea, Taiwan and Singapore, out of total imports of 31mn bpd, according to Thomson Reuters Eikon data.

The Malaysian deal should bolster Aramco’s IPO, which Saudi officials have predicted will value the company at a minimum of $2tn through the sale of 5% stake. “It’s a sound deal and looks good for the IPO.

Saudi Aramco is paying 25% of the project’s costs and securing the right to supply 50% of its feedstock,” industry veteran John Driscoll, director of Singapore-based consultancy JTD Energy said.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 4

Saudi Arabia wants oil prices to rise to around $60 in 2017 Reuters + NewBase - By Rania El Gamal and Alex Lawler

Saudi Arabia wants crude oil prices to rise to around $60 a barrel this year, five sources from OPEC countries and the oil industry said.

This is the level the OPEC heavyweight and its Gulf allies - the United Arab Emirates, Kuwait and Qatar - believe would encourage investment in new fields but not lead to a jump in U.S. shale output, the sources said.

The Organization of the Petroleum Exporting Countries, Russia and other producers pledged last year to cut production by about 1.8 million barrels per day (bpd) from Jan. 1. The first cut in eight years is intended to boost prices and get rid of a supply glut.

Crude prices LCOc1 have risen by more than 14 percent since the November pact but are still only trading around $56 a barrel despite record compliance by OPEC and non-OPEC members.

OPEC officials have repeatedly said the group does not target a specific oil price and their focus is on drawing global oil inventories and

helping the market to re-balance.

But behind closed doors, Riyadh and its Gulf OPEC allies hope to see a higher level because the low price has pressured their finances and stoked fears of a future supply shortage.

However, they do not want the price to be so high that it encourages rival U.S. shale producers, which were hard hit by the slump in oil prices, to ramp up production again. Advances in technology have made it easier for them to adapt quickly to oil price fluctuations.

"They (the Saudis) want to see oil prices at $60 towards the end of this year. It's good for (oil) investments," said a Gulf oil industry source familiar with the matter.

Another non-Gulf industry source said "OPEC and particularly the Saudis want higher prices" not just for investment but also as Riyadh as it seeks to offload a stake in state-owned oil giant Saudi

Aramco.

Over $1 trillion worth of oil projects have been canceled or delayed since mid-2014. A decline in investments in future oil projects triggered worries that this could lead to a supply shortage and spike in oil prices.

Oil fields take around four years to develop before production can start whereas U.S. shale oil can now be extracted within a few months of a decision.

"In general, something around $60 this year is good. $60 will not encourage that big increase in shale," said one OPEC source, adding that shale oil production is expected to grow by about 300,000 bpd this year.

ABSORBING SHALE

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 5

U.S. shale producers started to grow production again when crude prices first topped $50 a barrel in May 2016 after a two year price slump due to a global glut starting in mid 2014.

U.S. drillers have added more than 280 oil rigs since the end of May, and the U.S. Energy Information Administration (EIA) has forecast that U.S. domestic production will rise by 430,000 bpd between December 2016 and December 2017.

Despite the advances in technology, another OPEC source said that shale producers who survived the downturn may be cautious about responding quickly to a change in oil prices.

A third OPEC source said it was difficult to see oil prices rising to $60 or above this year due to a lingering oversupply.

That source also said that even if shale oil production rose by more than 300,000 bpd the market could absorb it if it comes during the cold winter season when demand peaks.

"The catch is the timing. If this happened, as it is widely projected, during the fourth quarter, the impact will be manageable and could be absorbed by the market," the source said.

OPEC could extend its oil supply-reduction pact with non-members or even apply deeper cuts from July if global crude inventories fail to drop to a targeted level, OPEC sources have told Reuters.

The Gulf industry source said OPEC and non-OPEC members may extend the supply curb pact because a return to a pump-at-will oil policy would crash prices and destabilize markets again.

"If we go back to a race to raise production, then we haven't achieved anything and prices will fall again," the source said.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 6

NewBase 02 March 2017 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Oil falls for third day as U.S. inventories hit record high

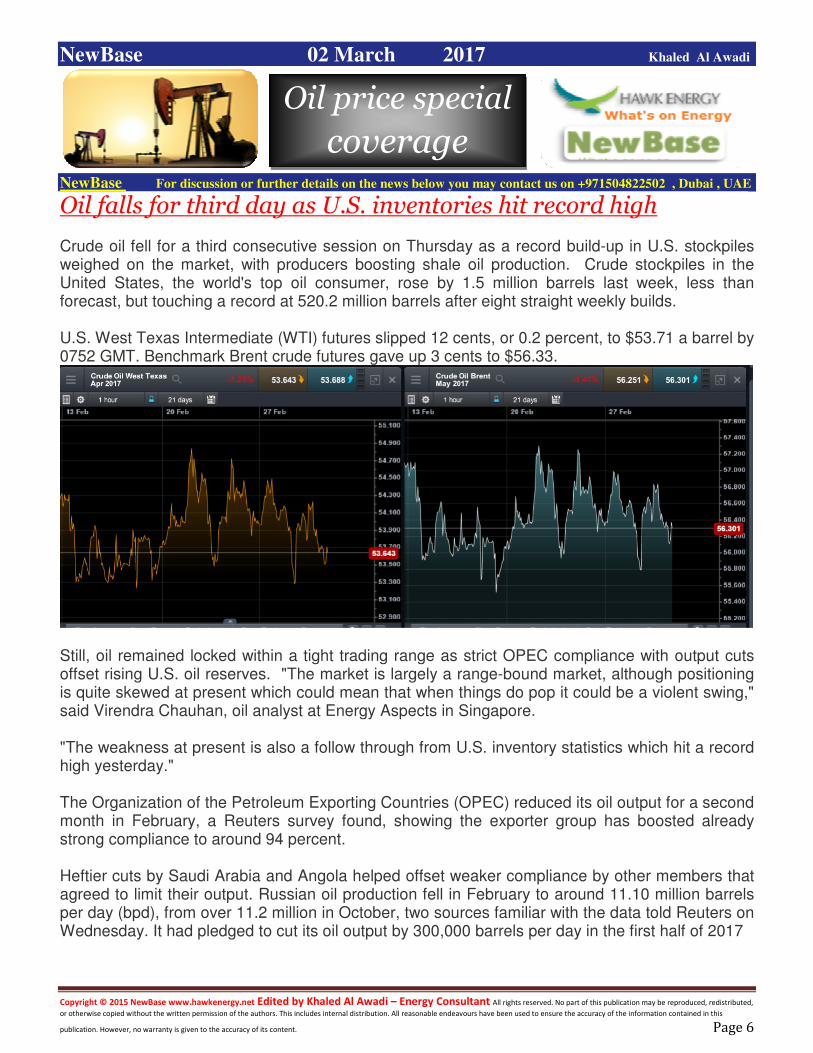

Crude oil fell for a third consecutive session on Thursday as a record build-up in U.S. stockpiles weighed on the market, with producers boosting shale oil production. Crude stockpiles in the United States, the world's top oil consumer, rose by 1.5 million barrels last week, less than forecast, but touching a record at 520.2 million barrels after eight straight weekly builds. U.S. West Texas Intermediate (WTI) futures slipped 12 cents, or 0.2 percent, to $53.71 a barrel by 0752 GMT. Benchmark Brent crude futures gave up 3 cents to $56.33.

Still, oil remained locked within a tight trading range as strict OPEC compliance with output cuts offset rising U.S. oil reserves. "The market is largely a range-bound market, although positioning is quite skewed at present which could mean that when things do pop it could be a violent swing," said Virendra Chauhan, oil analyst at Energy Aspects in Singapore. "The weakness at present is also a follow through from U.S. inventory statistics which hit a record high yesterday." The Organization of the Petroleum Exporting Countries (OPEC) reduced its oil output for a second month in February, a Reuters survey found, showing the exporter group has boosted already strong compliance to around 94 percent. Heftier cuts by Saudi Arabia and Angola helped offset weaker compliance by other members that agreed to limit their output. Russian oil production fell in February to around 11.10 million barrels per day (bpd), from over 11.2 million in October, two sources familiar with the data told Reuters on Wednesday. It had pledged to cut its oil output by 300,000 barrels per day in the first half of 2017

Oil price special

coverage

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 7

US Crude Oil Production Boost On Collision Course With OPEC Cuts by Deon Daugherty|Rigzone Armed with $50-plus oil prices, exploration and production (E&P) companies aren’t wasting any time. As the fourth quarter 2016 earnings season comes to a close, a key trend to emerge is that U.S. E&Ps are planning to spend more than analysts expected this year. Capital spending (CAPEX) tracking at 8 percent higher than consensus estimates, according to information from Wells Fargo (WF). That reflects capital budgets today that are 53 percent higher than 2016 levels. And that extra cash could generate as much as 1 million more barrels of oil per day next year, analysts at Simmons & Company International, said. For its part, OPEC has suggested the United States should consider its own production cuts – not increases. In November, the organization pledged cuts to help rebalance the market; soon afterward, several non-OPEC nations – including Russia – followed suit. Oil prices react daily to U.S. drilling activity, losing ground when domestic increases overshadow OPEC and non-OPEC cuts, who are on track to meet reduction goals. Member nations of the Organization of the Petroleum Exporting Countries and their non-OPEC counterparts agreed last year to remove almost 1.8 million barrels per day (MMbpd) from the market beginning last month. To date, they have met 1.5 MMbpd of the goal.

In the United States, about 40 E&Ps and large integrated companies that Simmons covers account for roughly 50 percent of current domestic production; of those companies, more than 70 percent have released guidance that suggests production growth in the mid-single digits this year and low double-digits in 2018, Simmons said.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 8

“We believe investors need to begin entertaining the possibility of 1 million barrels per day of oil production growth in 2018,” the analysts wrote. Coming into 2017, those estimates were closer to 700,000 barrels per day (bpd) and the higher volumes were expected in 2019 – not a year early. “The tension will be the ongoing contest and collision of U.S. vitality juxtaposed against international non-OPEC stagnation and the durability of OPEC's return to rational guardianship,” Simmons said. “We continue to be impressed by an industry that has driven the cost curve dramatically lower from a few years ago and is now capable of delivering double digit oil production growth in a lower commodity environment.” But that equates to a production outlook at that is “good for the companies; not as good for the macro,” the analysts said. Not everyone is convinced.

Analysts at R.W. Baird & Co. said exploration and production companies are leaning in with an optimistic outlook on crude this year, but investors remain wary. “Higher spend is driving higher growth outlooks,” the analysts wrote in a research note Tuesday. “However, growing cash needs are creating a negative sentiment shift as cautious investors hold a ‘prove it to me’ attitude, with skeptical views” of second-half growth guidance. A chunk of the new spending this year will fund increased service costs. Analysts have said service costs are poised to increase between 5 and 15 percent. And while production is set to increase next year, for 2017, guidance is about 1 percent lower than consensus expectations, analysts at Wells Fargo said in a recent note. The dominant theme WF identified appears to be a “deliberate attempt by operators to shift the focus away from 2017,” and instead, they highlight growth targets for 2018 and beyond. “We also see more inherent risk in future (vs. immediate) production combining poorly with a macro environment that remains volatile and uncertain,” WF said.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 9

NewBase Special Coverage

News Agencies News Release 02 Mar. 2017

With Shale Oil Production Like This, Who Needs Trump? By Julian Lee

The second coming of shale could be even more powerful than the first. OPEC seems to be getting caught unawares.

The current boom in U.S. oil production is even stronger now than the run from July 2011 to April 2015. And this is with oil prices at half their previous level and before President Donald Trump has done anything to meet his pledge to "lift the restrictions on American energy and allow this wealth to pour into our communities." Output growth could accelerate if prices rise, or costs fall further.

This is not how it was meant to be. OPEC launched a strategy to protect market share in 2014 with a specific aim to knock out high-cost oil production such as shale. After the group succumbed to internal financial pressures and agreed in November to cut output by around 1.2 million barrels a day, Saudi oil minister Khalid Al-Falih said he didn't expect a big supply response from American shale producers in 2017.

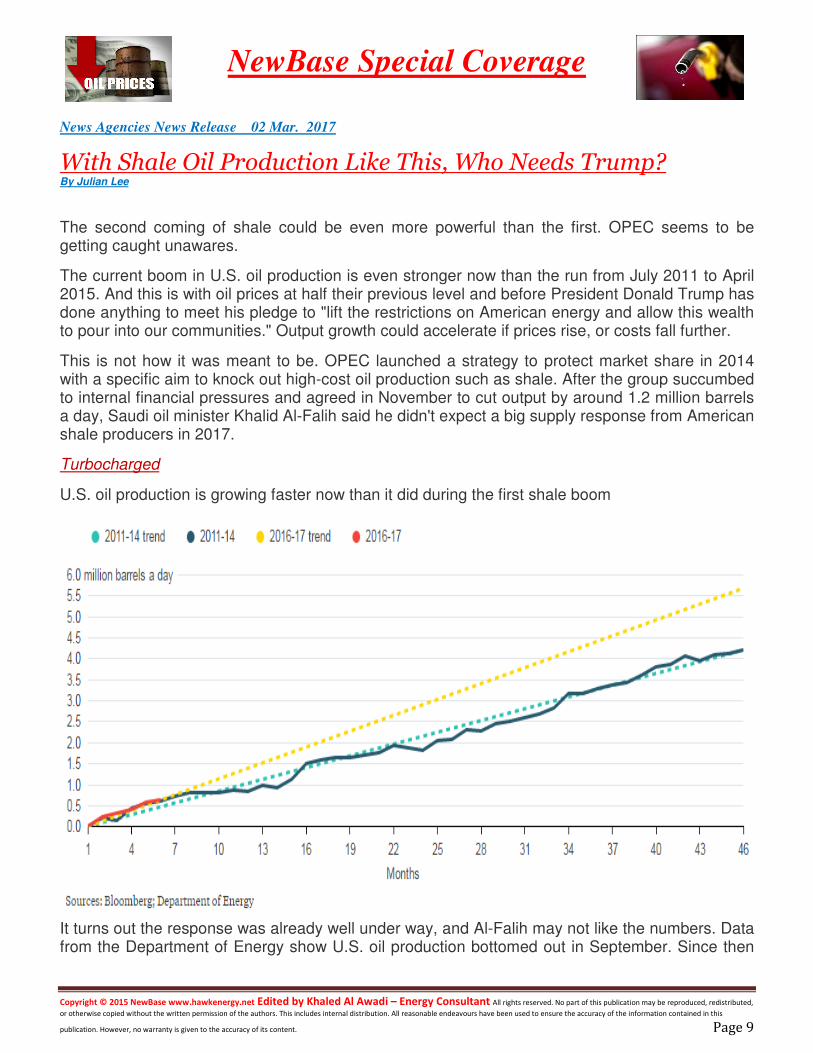

Turbocharged

U.S. oil production is growing faster now than it did during the first shale boom

It turns out the response was already well under way, and Al-Falih may not like the numbers. Data from the Department of Energy show U.S. oil production bottomed out in September. Since then

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 10

oil companies have added an average of 125,000 barrels a day of production each month, taking output back above 9 million barrels a day for the first time since April.

What should really trouble OPEC, though, is that this rate of growth is even faster than the first shale boom. Over that earlier period, U.S. oil production rose at an average monthly rate of 93,000 barrels a day.

Market anticipation of the agreement between OPEC and its friends in November last year, and the actual deal, lifted WTI from a low reached in early 2016 of around $26. This time, shale producers aren't waiting around -- their output started picking up with WTI crude selling for around $45. During the last boom, WTI traded in a range at about double or triple that.

Okay, so part of the growth is coming from the Gulf of Mexico, where BP Plc's Thunder Horse South and Royal Dutch Shell Plc's Stones projects have both started producing in recent months. But that region also made a positive contribution to the earlier boom, as did Alaska. Most of the current growth is coming from the onshore, lower 48 states -- home of the shale industry.

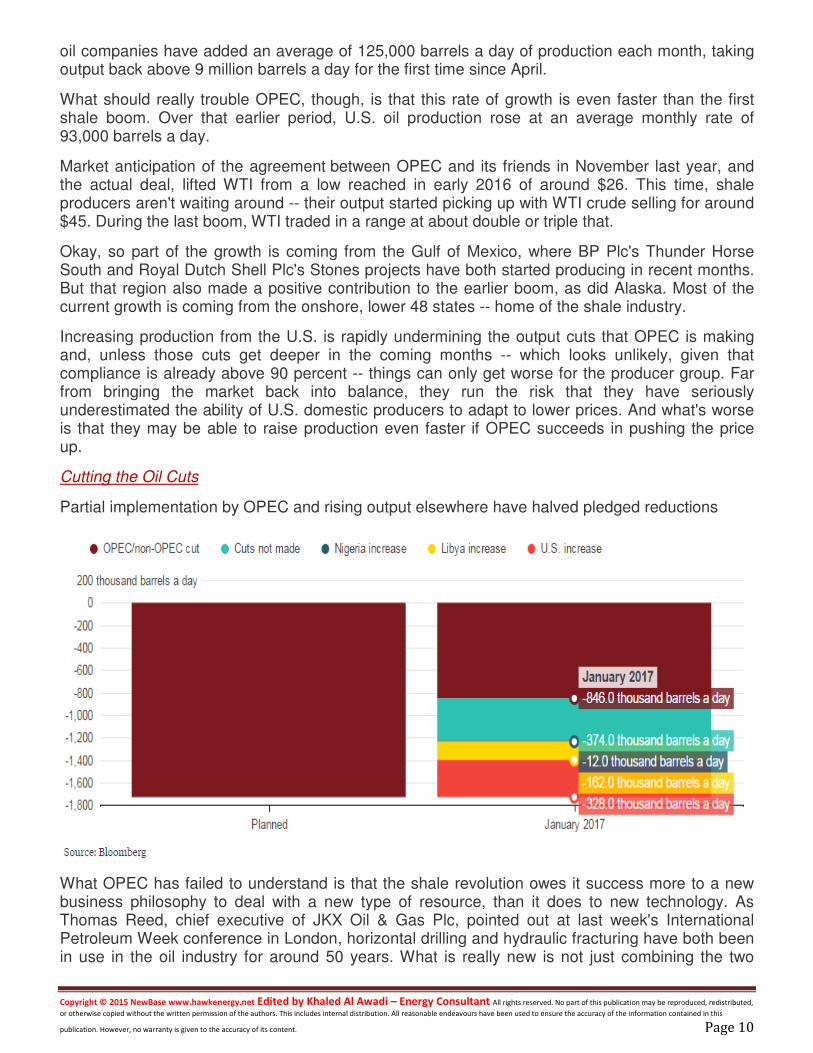

Increasing production from the U.S. is rapidly undermining the output cuts that OPEC is making and, unless those cuts get deeper in the coming months -- which looks unlikely, given that compliance is already above 90 percent -- things can only get worse for the producer group. Far from bringing the market back into balance, they run the risk that they have seriously underestimated the ability of U.S. domestic producers to adapt to lower prices. And what's worse is that they may be able to raise production even faster if OPEC succeeds in pushing the price up.

Cutting the Oil Cuts

Partial implementation by OPEC and rising output elsewhere have halved pledged reductions

What OPEC has failed to understand is that the shale revolution owes it success more to a new business philosophy to deal with a new type of resource, than it does to new technology. As Thomas Reed, chief executive of JKX Oil & Gas Plc, pointed out at last week's International Petroleum Week conference in London, horizontal drilling and hydraulic fracturing have both been in use in the oil industry for around 50 years. What is really new is not just combining the two

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 11

techniques in a single well but, more importantly, the industrialization of the process of drilling and completing wells.

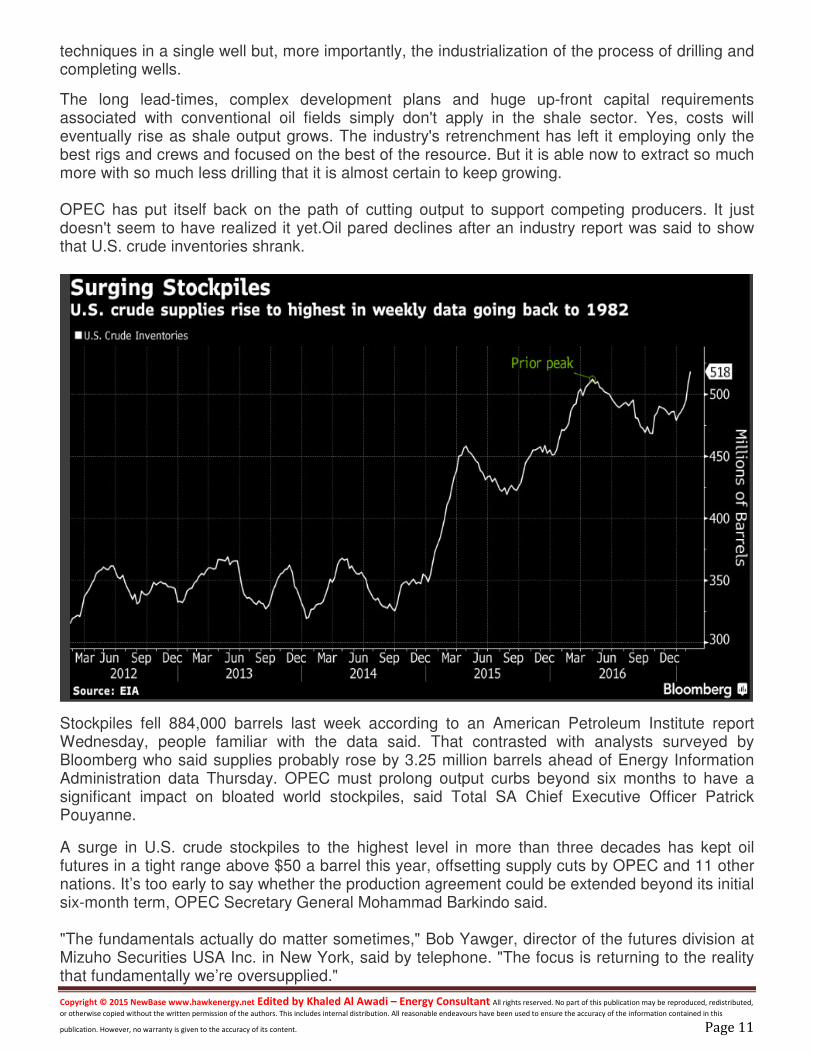

The long lead-times, complex development plans and huge up-front capital requirements associated with conventional oil fields simply don't apply in the shale sector. Yes, costs will eventually rise as shale output grows. The industry's retrenchment has left it employing only the best rigs and crews and focused on the best of the resource. But it is able now to extract so much more with so much less drilling that it is almost certain to keep growing. OPEC has put itself back on the path of cutting output to support competing producers. It just doesn't seem to have realized it yet.Oil pared declines after an industry report was said to show that U.S. crude inventories shrank.

Stockpiles fell 884,000 barrels last week according to an American Petroleum Institute report Wednesday, people familiar with the data said. That contrasted with analysts surveyed by Bloomberg who said supplies probably rose by 3.25 million barrels ahead of Energy Information Administration data Thursday. OPEC must prolong output curbs beyond six months to have a significant impact on bloated world stockpiles, said Total SA Chief Executive Officer Patrick Pouyanne.

A surge in U.S. crude stockpiles to the highest level in more than three decades has kept oil futures in a tight range above $50 a barrel this year, offsetting supply cuts by OPEC and 11 other nations. It’s too early to say whether the production agreement could be extended beyond its initial six-month term, OPEC Secretary General Mohammad Barkindo said. "The fundamentals actually do matter sometimes," Bob Yawger, director of the futures division at Mizuho Securities USA Inc. in New York, said by telephone. "The focus is returning to the reality that fundamentally we’re oversupplied."

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 12

BP Targets $40 Break-Even Oil Price to Reassure Investors by Rakteem Katakey

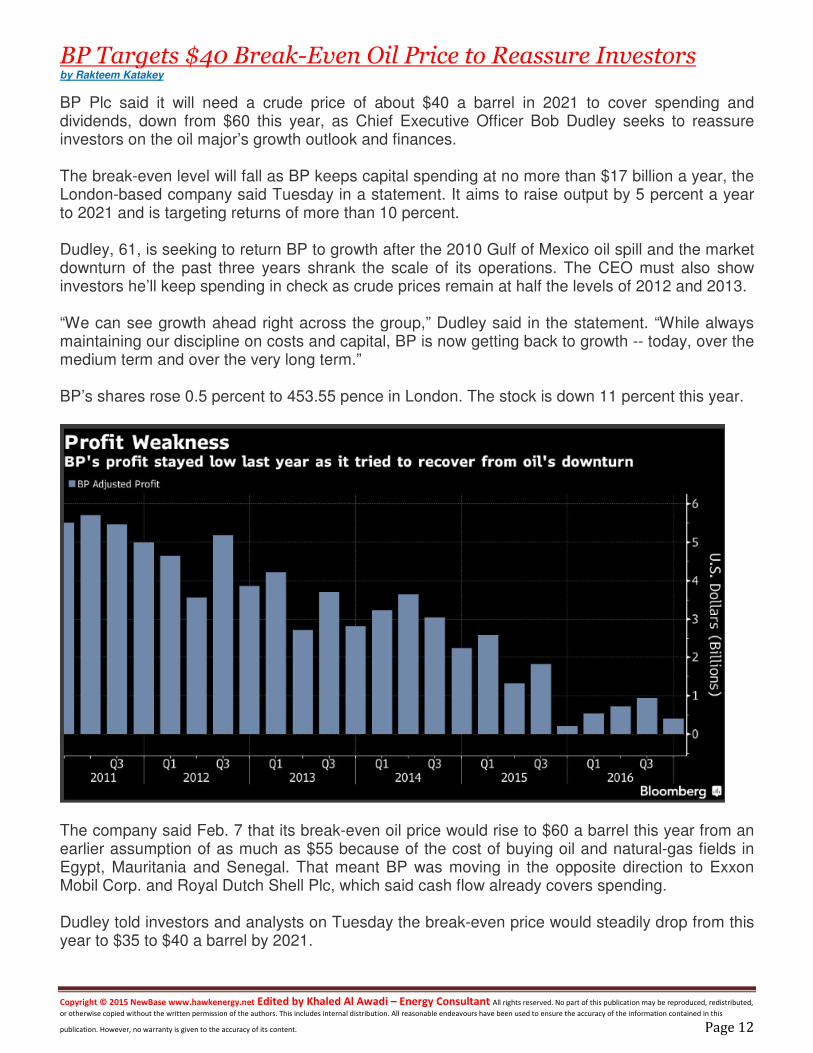

BP Plc said it will need a crude price of about $40 a barrel in 2021 to cover spending and dividends, down from $60 this year, as Chief Executive Officer Bob Dudley seeks to reassure investors on the oil major’s growth outlook and finances. The break-even level will fall as BP keeps capital spending at no more than $17 billion a year, the London-based company said Tuesday in a statement. It aims to raise output by 5 percent a year to 2021 and is targeting returns of more than 10 percent. Dudley, 61, is seeking to return BP to growth after the 2010 Gulf of Mexico oil spill and the market downturn of the past three years shrank the scale of its operations. The CEO must also show investors he’ll keep spending in check as crude prices remain at half the levels of 2012 and 2013. “We can see growth ahead right across the group,” Dudley said in the statement. “While always maintaining our discipline on costs and capital, BP is now getting back to growth -- today, over the medium term and over the very long term.” BP’s shares rose 0.5 percent to 453.55 pence in London. The stock is down 11 percent this year.

The company said Feb. 7 that its break-even oil price would rise to $60 a barrel this year from an earlier assumption of as much as $55 because of the cost of buying oil and natural-gas fields in Egypt, Mauritania and Senegal. That meant BP was moving in the opposite direction to Exxon Mobil Corp. and Royal Dutch Shell Plc, which said cash flow already covers spending. Dudley told investors and analysts on Tuesday the break-even price would steadily drop from this year to $35 to $40 a barrel by 2021.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 13

Cash Flow

The company also sees as much as $14 billion of free cash flow from its oil and gas exploration and production business by 2021 at an average oil price of $55, Bernard Looney, the unit’s boss said at a briefing in London. That compares with guidance last year of as much as $8 billion of cash flow by 2020 at $50 a barrel, with the increase broken down as follows: A little more than $2 billion from new fields BP bought at the end of last year. Another $2 billion from higher oil-price expectations. Extending the period of guidance by a year to 2021 adds $1 billion. Making operations more efficient adds $1 billion Another $9 billion to $10 billion of free cash flow will come from refining, marketing and trading oil, BP said. “It’s good to see them bring the cash break-even guidance that low, even though it is long-dated,” said Rohan Murphy, an analyst at Allianz Global Investors, which owns 0.6 percent of BP shares. “The jump in upstream free cash flow guidance goes hand in hand with this, but its good to see it quantified and shows the portfolio is stronger than the market gives credit for.” BP did balance its books toward the end of last year, giving the company confidence to make acquisitions, but the hunt to secure future supply forced it to push back its cash break-even target for 2017 as a whole. The buying spree at the end of 2016 -- taking in fields around Africa that are yet to begin production -- will result in a cash shortfall this year, Chief Financial Officer Brian Gilvary said Feb. 7. BP is not looking for any new big acquisitions, Dudley said. The company plans to start seven projects this year and is working on nine others that could begin from 2018 to 2021, Looney said. BP sees total production rising by more than 1 million barrels a day by 2021, Dudley said.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 14

BP and EOG Test OPEC's Beliefs Liam Denning

Both of these CEOs -- the first runs EOG Resources Inc., the second BP PLC -- hosted analyst calls on Tuesday. One is a U.S. shale producer and the other a global oil major. But in one central aspect their message was the same: We're getting ever more efficient.

They're just coming from different places.

EOG, reporting results for 2016, laid out a plan to raise its oil production this year by 18 percent, assuming an oil price of $50 a barrel (the average to date has been about $53). More importantly, EOG expects to do this while cutting the cost of each well -- in a year when higher oil prices and drilling activity should spark industry inflation as workers and services contractors demand some payback after two years of cuts.

It isn't as if EOG thinks its employees and contractors are especially meek when it comes to demanding money. For one thing, it can rely on internal sourcing of some products, such as sand for fracking, and long-term contracts signed during the crash for some insulation. For the 40 percent of costs EOG says are subject to inflation, it says continuing productivity gains will offset it.

EOG has some credibility on this front. It began 2016 expecting to drill 200 wells and complete 270 with an investment budget of $2.5 billion. As it turned out, it spent a little more -- $2.7 billion -- but drilled 280 wells and completed 445, net. Indeed, while EOG's realized price per barrel of oil equivalent fell to its lowest level since 2009, so did its all-in cost of production:

Digging In

While EOG's realized oil and gas prices have collapsed, it has also cut its unit cost by more than a quarter since 2014

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 15

Hearing all this, it perhaps isn't surprising that one analyst on Tuesday's call, Paul Sankey of Wolfe Research, asked the following:

I think a lot of people, when they hear you talk, get very bearish on oil prices. And I don't think that's the way you look at the world. Bill, can you remind us why what you're doing isn't replicable across the industry? Which I guess is the reason why people would be very bearish.

If that is the question that haunts OPEC, Thomas' response offered a measure of comfort. He acknowledged, rightly, that part of EOG's edge lies in having acquired rights to some of the best geology and another part lies in applying in-house expertise to those rocks to get the best out of them at a competitive cost:

Well, it's two parts. It's better rock and you have to capture that better rock...And then using our very advanced, very proprietary completion technique. So it's a combination of all that technology and that is not very duplicable. It has taken us nearly a decade to get to this point.

OPEC, and anyone else hoping for a big swing back up in oil prices, had best hope EOG really is an outlier. In certain respects, the company does walk a different path from its peers. In contrast to many rivals, it pays a dividend and has an explicit target for return on capital employed, above 13 percent.

This is backed by a relatively unusual set of bonus drivers for EOG's management. Return on capital, for example, has a 20 percent weighting in their plan, against just 4 percent, on average, for peers, according to a survey published in September by ISI Evercore. And whereas production growth has a 16 percent average weighting in competitors' incentive plans, it is just 8 percent at EOG.

OPEC shouldn't rest too easy, though. EOG being much better than many of its peers isn't the same as being unique. In particular, Pioneer Natural Resources Co.'s recent presentation of a 10-year growth plan suggests more than one E&P company has taken some important lessons from the crash. It is clear the sector has weathered the storm of low prices better than anyone expected -- and has been provided some succor of late, courtesy of OPEC itself.

Meanwhile, another disconcerting message emanated from London on Tuesday. BP's CEO told assembled analysts the company aims to be able to cover its investment budget and dividend payments at a real Brent crude oil price of between $35 and $40 a barrel.

In this instance, there's more of a credibility gap to bridge. Only three weeks ago, BP spooked investors by raising its breakeven oil price for 2017 to $60 due to higher capital expenditure. Similar to the other oil majors, BP has to go the extra mile in prioritizing payments to shareholders over growth.

BP, like EOG, aims to become a leaner operation in order to deliver good returns even at relatively low oil prices. For a company more exposed to deepwater drilling than shale, doing that will require transforming the way giant projects get developed. On that front, new partnering approaches proposed by oilfield services companies could help BP.

OPEC may rightly scoff at such medium-term aspirations in a market that's undergone big changes just in the past five years, especially given BP's apparent turnaround on costs.

What OPEC can't be feeling is certainty. By and large, its members need cyclical upswings in oil prices to balance their bloated budgets. Their confidence won't be strengthened by the sight of competitors working toward opposite ends.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 16

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

Your partner in Energy Services

NewBase energy news is produced daily (Sunday to Thursday) and

sponsored by Hawk Energy Service – Dubai, UAE.

For additional free subscription emails please contact Hawk Energy

Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010

Mobile: +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 25 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years, he has developed great experiences in the designing & constructing of gas pipelines, gas metering &

regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation, operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally, via GCC leading satellite Channels.

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase March 2017 K. Al Awadi

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 17

Hilton hotel 1B AZADLIG AVENUE, BAKU, AZ1000, AZERBAIJAN

Please send your request by email at [email protected], or call +994 55 5993345

About Summit

Azerbaijan Oil and Gas Summit will host by FA Events. Summit will cover main oil and gas topics and latest trends. The Summit will gather main market key players and experts around globe.

Social Networking Contact

• Address: Jafar Jabbarli str., 44. Caspian Plaza. Baku, Azerbaijan. AZ1065 Baku Azerbaijan

• Contact Us: +994 55 599 33 45

• Email: [email protected]

The Oil and Gas Summit

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 18