Embed Size (px)

Citation preview

Navigating Turbulent Waters: Turbulent Times for

North American MROs

Nathan K. Smith, Industry Analyst

Aerospace & Defense

October 15, 2009

2

Focus Points

� Current Financial Crisis – Impact on North American MROs

� Market Dynamics – North American Commercial Aircraft MRO Market

� Aircraft MRO Market Analysis and Forecast

� Aircraft MRO Demand Analysis

� Conclusion

3

Current Financial Crisis – Impact on North American MROs

� Airline profitability is closely tied to economic growth and trade.

� In 2008, the airline industry was impaired by soaring fuel prices and an economic

crisis. In 2009, the industry continues to face a slow economy, weak travel

demands, and further reductions in aircraft capacity.

� Reductions in airline fleet capacity and the retiring of older, less efficient aircraft

across North America has resulted in fewer maintenance checks and decreased

revenues for MROs.

� When compared to 2008, the average aircraft utilization for the world's commercial

fleet in 2009 is expected to drop by an estimated four percent.

� Economic factors have pushed North American carriers to embrace outsourcing. These carriers continue to focus on total maintenance support as the most important factor in selecting an MRO provider.

� Despite the strong push towards outsourcing, the market has been in decline as a result of an industry-wide downturn effecting both airline in-house and third party MROs.

4

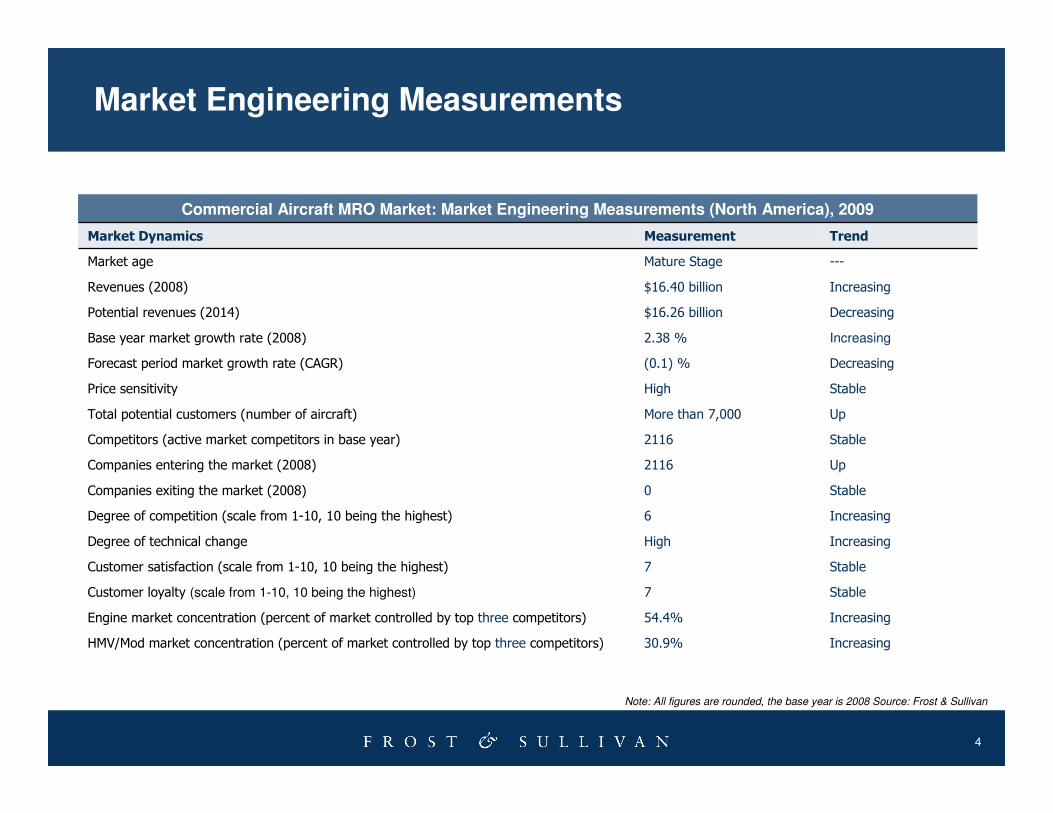

Market Engineering Measurements

StableHighPrice sensitivity

UpMore than 7,000Total potential customers (number of aircraft)

Stable2116Competitors (active market competitors in base year)

Up2116Companies entering the market (2008)

Stable0Companies exiting the market (2008)

Increasing6Degree of competition (scale from 1-10, 10 being the highest)

IncreasingHighDegree of technical change

Stable7Customer satisfaction (scale from 1-10, 10 being the highest)

Stable7Customer loyalty (scale from 1-10, 10 being the highest)

Increasing54.4%Engine market concentration (percent of market controlled by top three competitors)

Increasing30.9%HMV/Mod market concentration (percent of market controlled by top three competitors)

Commercial Aircraft MRO Market: Market Engineering Measurements (North America), 2009

Decreasing(0.1) %Forecast period market growth rate (CAGR)

Increasing2.38 %Base year market growth rate (2008)

Decreasing$16.26 billionPotential revenues (2014)

Increasing$16.40 billionRevenues (2008)

---Mature StageMarket age

TrendMeasurementMarket Dynamics

Note: All figures are rounded, the base year is 2008 Source: Frost & Sullivan

5

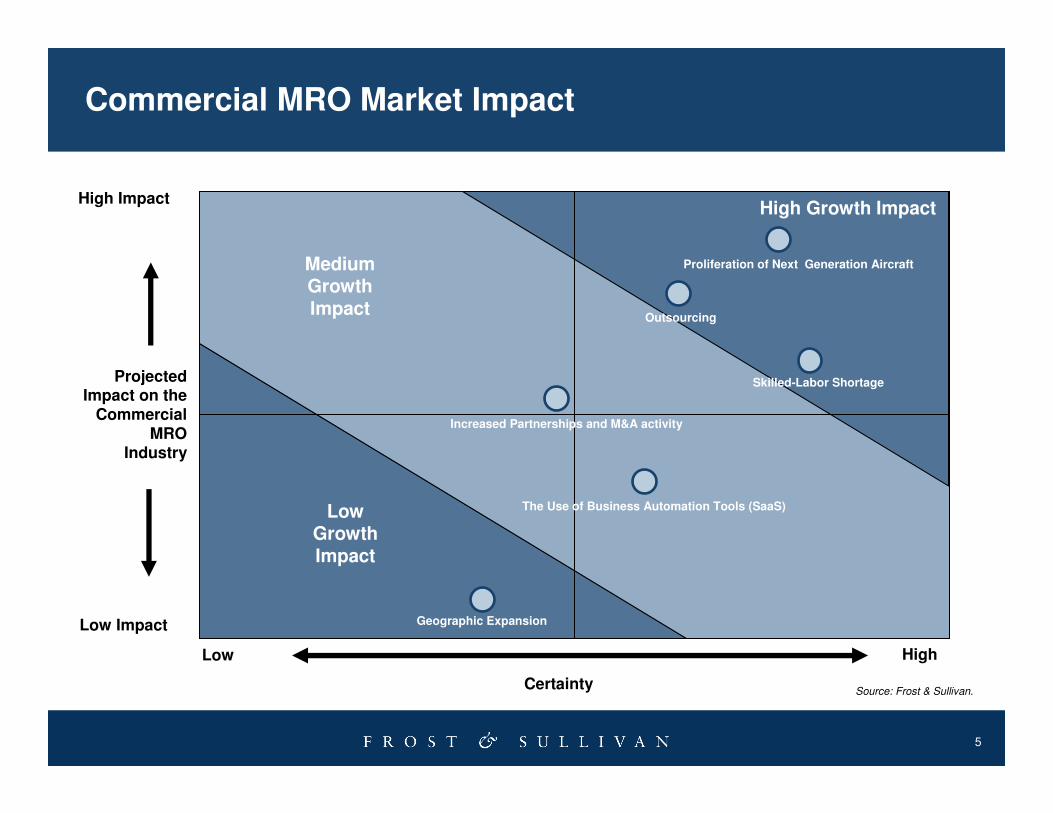

Commercial MRO Market Impact

ProjectedImpact on the

Commercial MRO

Industry

High Impact

Low Impact

Certainty

Low High

High Growth Impact

LowGrowthImpact

MediumGrowthImpact

Source: Frost & Sullivan.

Proliferation of Next Generation Aircraft

Outsourcing

Skilled-Labor Shortage

Increased Partnerships and M&A activity

The Use of Business Automation Tools (SaaS)

Geographic Expansion

6

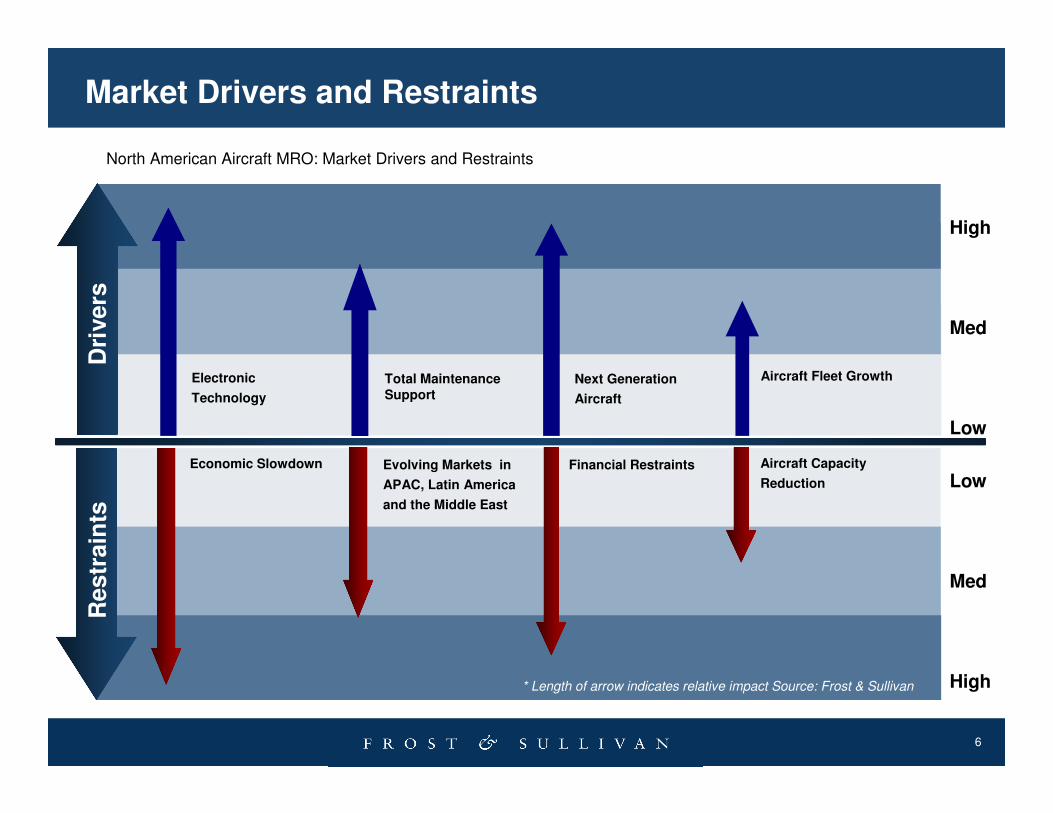

Market Drivers and RestraintsR

estr

ain

tsD

rivers

High

Med

Low

Low

Med

High

Electronic

Technology

* Length of arrow indicates relative impact Source: Frost & Sullivan

Economic Slowdown Evolving Markets in

APAC, Latin America

and the Middle East

Financial Restraints Aircraft Capacity

Reduction

Aircraft Fleet GrowthNext Generation

Aircraft

North American Aircraft MRO: Market Drivers and Restraints

Total MaintenanceSupport

7

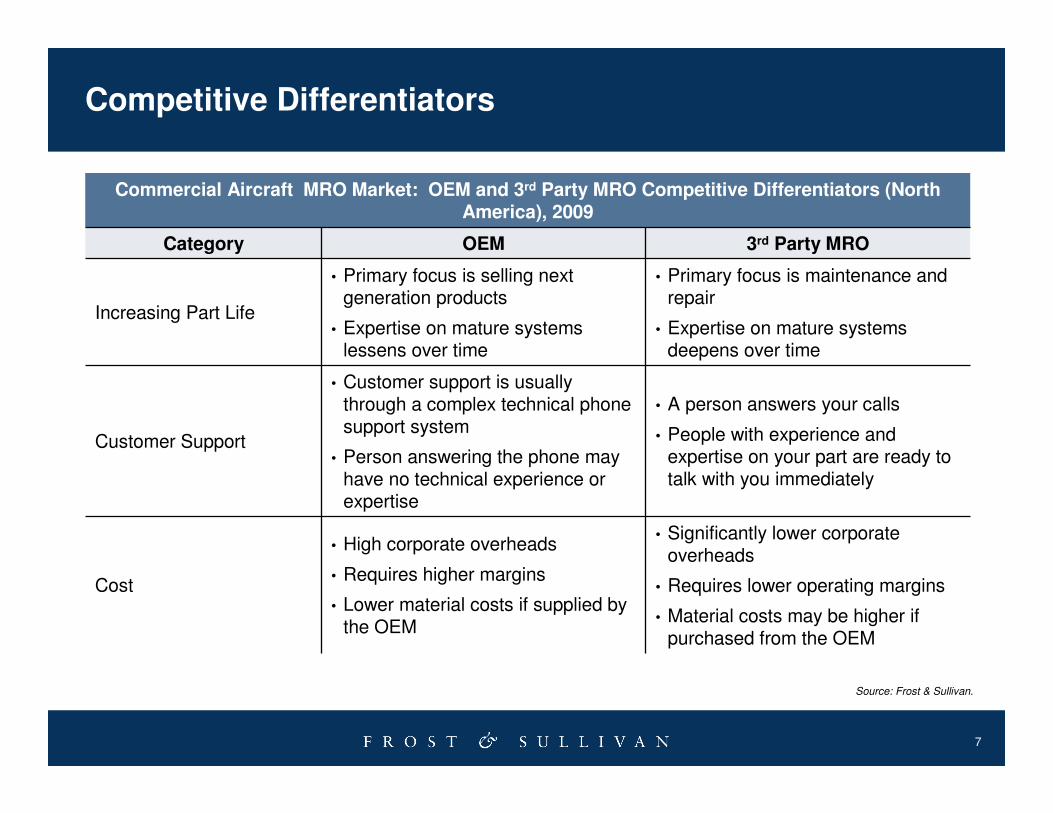

Competitive Differentiators

Commercial Aircraft MRO Market: OEM and 3rd Party MRO Competitive Differentiators (North America), 2009

• Significantly lower corporate overheads

• Requires lower operating margins

• Material costs may be higher if purchased from the OEM

• High corporate overheads

• Requires higher margins

• Lower material costs if supplied by the OEM

Cost

• A person answers your calls

• People with experience and expertise on your part are ready to talk with you immediately

• Customer support is usually through a complex technical phone support system

• Person answering the phone may have no technical experience or expertise

Customer Support

• Primary focus is maintenance and repair

• Expertise on mature systems deepens over time

• Primary focus is selling next generation products

• Expertise on mature systems lessens over time

Increasing Part Life

3rd Party MROOEM Category

Source: Frost & Sullivan.

8

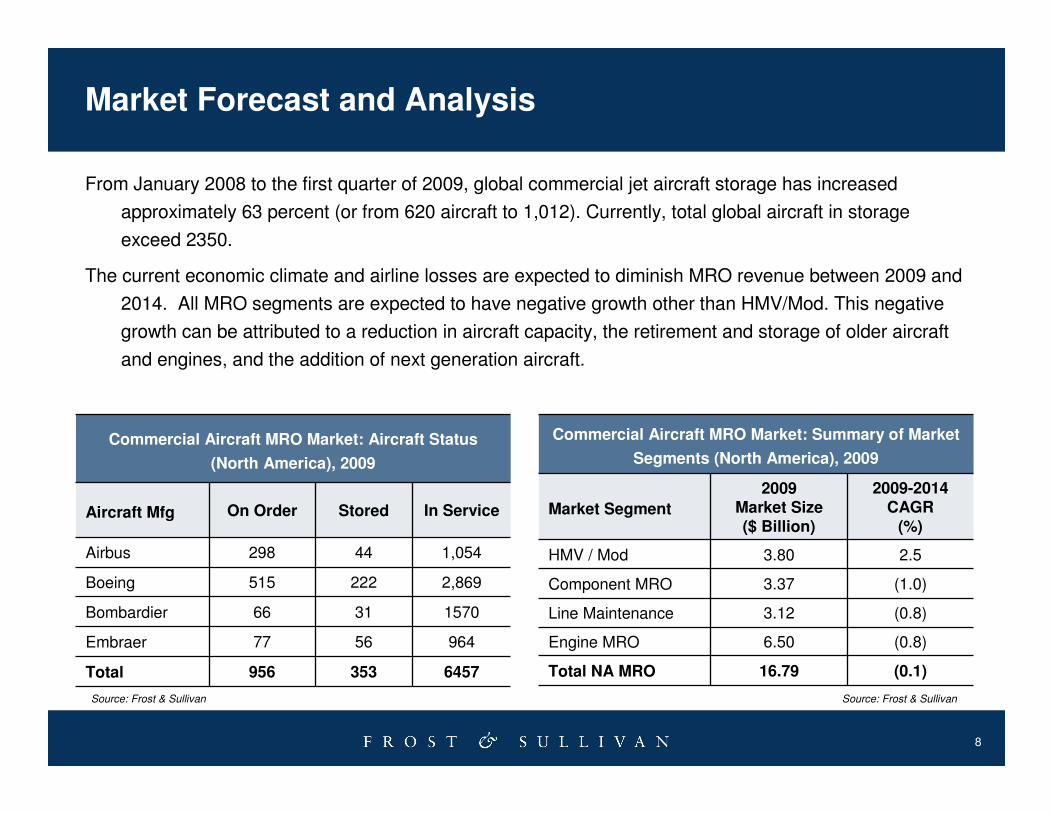

Market Forecast and Analysis

Commercial Aircraft MRO Market: Summary of Market

Segments (North America), 2009

(0.8)6.50Engine MRO

16.79

3.12

3.37

3.80

2009Market Size($ Billion)

(0.8)Line Maintenance

(0.1)Total NA MRO

(1.0)Component MRO

2.5HMV / Mod

2009-2014CAGR

(%)Market Segment

From January 2008 to the first quarter of 2009, global commercial jet aircraft storage has increased

approximately 63 percent (or from 620 aircraft to 1,012). Currently, total global aircraft in storage

exceed 2350.

The current economic climate and airline losses are expected to diminish MRO revenue between 2009 and

2014. All MRO segments are expected to have negative growth other than HMV/Mod. This negative

growth can be attributed to a reduction in aircraft capacity, the retirement and storage of older aircraft

and engines, and the addition of next generation aircraft.

Source: Frost & SullivanSource: Frost & Sullivan

Commercial Aircraft MRO Market: Aircraft Status

(North America), 2009

6457

964

1570

2,869

1,054

In Service

956

77

66

515

298

On Order

31Bombardier

56Embraer

353Total

222Boeing

44Airbus

StoredAircraft Mfg

9

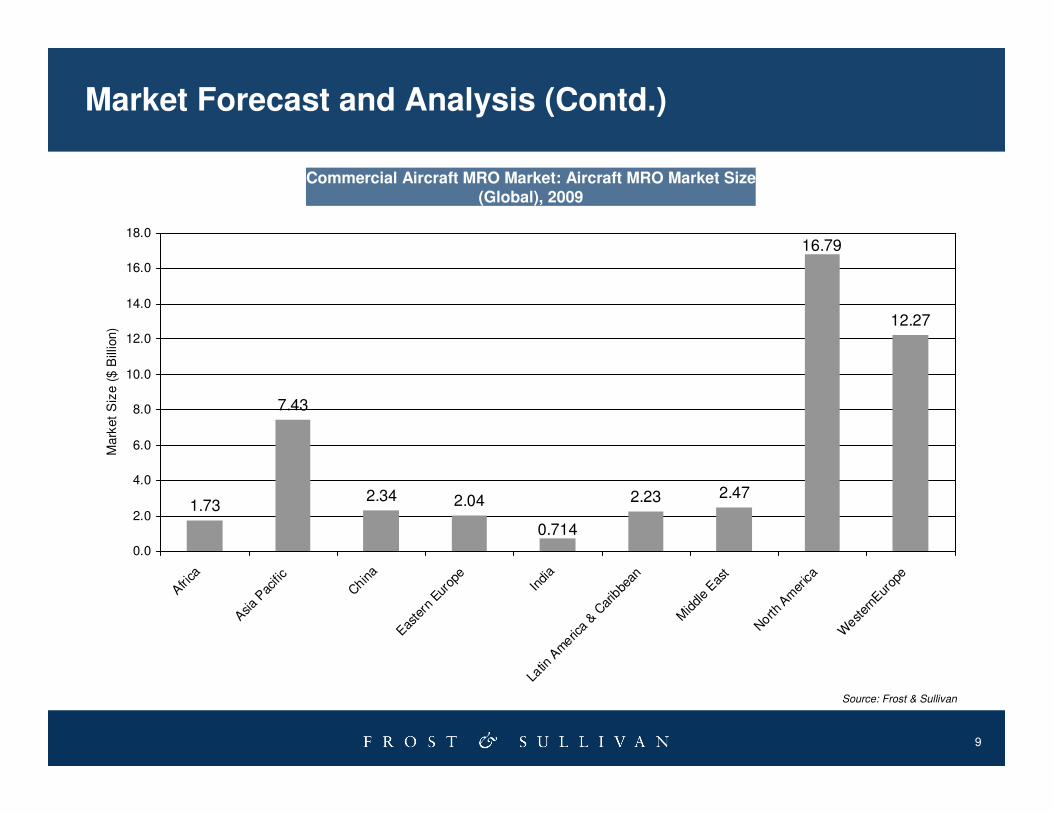

Market Forecast and Analysis (Contd.)

1.73

7.43

2.34 2.04 2.23 2.47

12.27

16.79

0.714

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Africa

Asia P

acifi

c

China

Easte

rn E

urop

e

Indi

a

Latin

Am

erica &

Car

ibbe

an

Mid

dle

East

North A

mer

ica

West

ernE

urop

e

Mark

et

Siz

e (

$ B

illio

n)

Commercial Aircraft MRO Market: Aircraft MRO Market Size (Global), 2009

Source: Frost & Sullivan

10

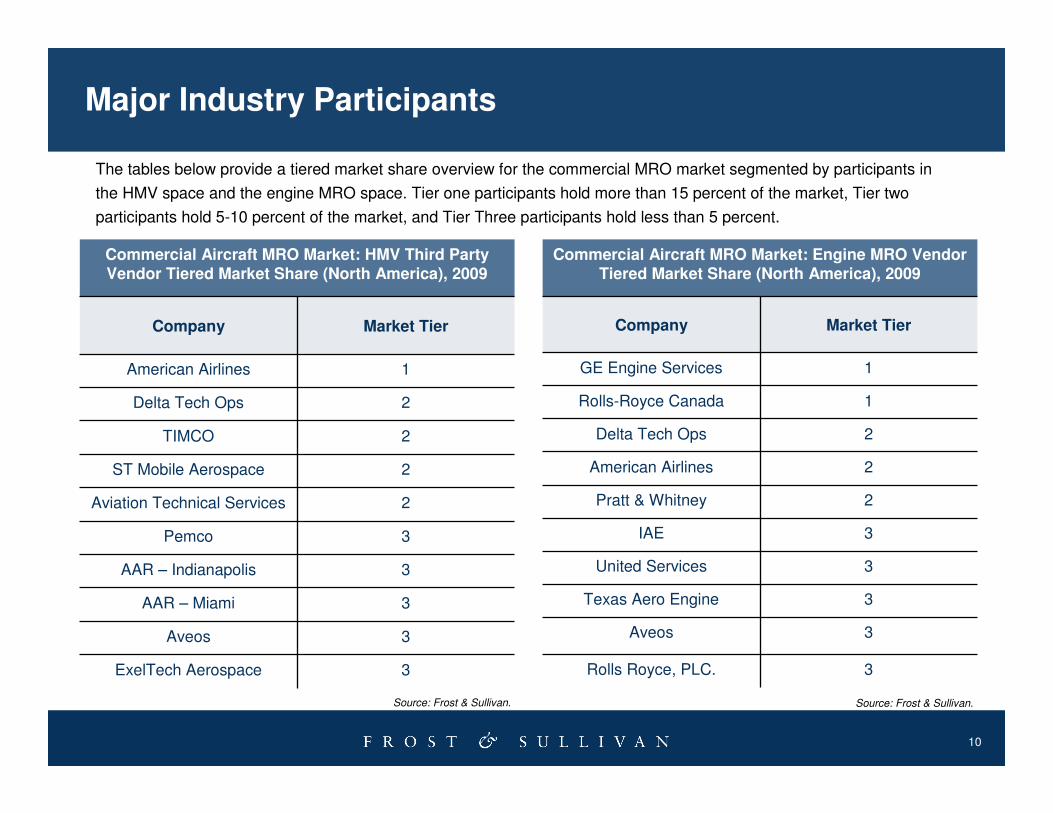

Major Industry Participants

3Pemco

3AAR – Indianapolis

3AAR – Miami

3Aveos

3ExelTech Aerospace

2Aviation Technical Services

2ST Mobile Aerospace

2TIMCO

2Delta Tech Ops

1American Airlines

Market Tier Company

Commercial Aircraft MRO Market: HMV Third Party Vendor Tiered Market Share (North America), 2009

3IAE

3United Services

3Texas Aero Engine

3Aveos

3Rolls Royce, PLC.

2Pratt & Whitney

2American Airlines

2Delta Tech Ops

1Rolls-Royce Canada

1GE Engine Services

Market Tier Company

Commercial Aircraft MRO Market: Engine MRO Vendor Tiered Market Share (North America), 2009

The tables below provide a tiered market share overview for the commercial MRO market segmented by participants in

the HMV space and the engine MRO space. Tier one participants hold more than 15 percent of the market, Tier two

participants hold 5-10 percent of the market, and Tier Three participants hold less than 5 percent.

Source: Frost & Sullivan. Source: Frost & Sullivan.

11

Demand Analysis

0

500

1000

1500

2000

2500

3000

3500

Airbus

WB

A319

A320

B737

B757

B767

B747

B777

MD

80

RJ/

TP

Aircra

ft (

Units

)

0

0.5

1

1.5

2

2.5

3

3.5

MR

O M

ark

et S

ize (

$ M

illio

n)

Aircraft

Market Size

0

500

1000

1500

2000

2500

3000

3500

Airbus

WB

A319

A320

B737

B757

B767

B747

B777

MD

80

RJ/

TP

Aircra

ft (

Units

)

0

0.5

1

1.5

2

2.5

3

3.5

MR

O M

ark

et S

ize (

$ M

illio

n)

Aircraft

Market Size

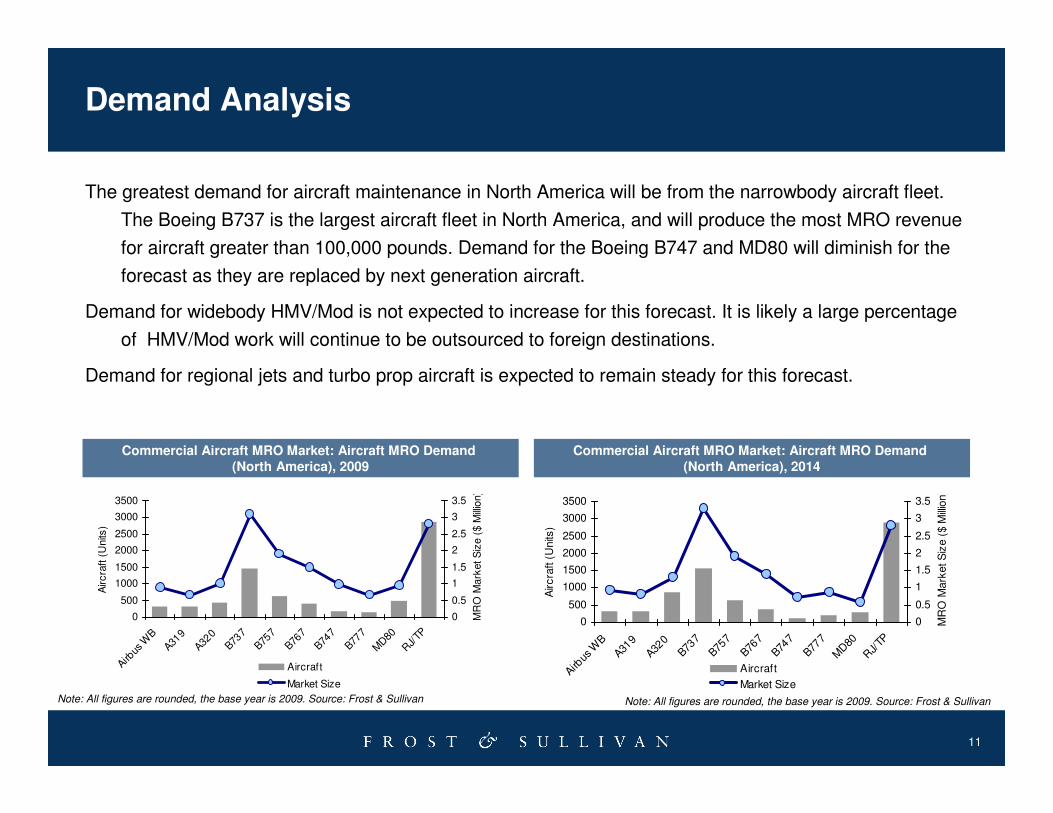

The greatest demand for aircraft maintenance in North America will be from the narrowbody aircraft fleet.

The Boeing B737 is the largest aircraft fleet in North America, and will produce the most MRO revenue

for aircraft greater than 100,000 pounds. Demand for the Boeing B747 and MD80 will diminish for the

forecast as they are replaced by next generation aircraft.

Demand for widebody HMV/Mod is not expected to increase for this forecast. It is likely a large percentage

of HMV/Mod work will continue to be outsourced to foreign destinations.

Demand for regional jets and turbo prop aircraft is expected to remain steady for this forecast.

Commercial Aircraft MRO Market: Aircraft MRO Demand (North America), 2009

Note: All figures are rounded, the base year is 2009. Source: Frost & Sullivan Note: All figures are rounded, the base year is 2009. Source: Frost & Sullivan

Commercial Aircraft MRO Market: Aircraft MRO Demand (North America), 2014

12

Conclusion

� Market participants will have to keep their

competitive position to maintain a viable

business. Strategically, the providers' intent

should be to provide reliable and cost-effective

maintenance services. North American MRO

vendors should rethink and respond to foreign

competition. They should revaluate their

organizational structure at present and continue

to seek improvements. Traditional cost cutting

and productivity measures will not enable the

MRO vendor to bridge the gap between wage

and productivity. The availability of skilled labor

will be a challenge for the industry. Therefore,

MRO providers must be prepared for the rise in

labor cost.

� North America is forecasted to lose three

percent of its market share during the forecast

because of growing competition. MRO growth is

forecasted at a CAGR of (0.1) percent or a

decrease of $0.14 billion.

� Global MRO growth from 2009 to 2014 is

expected to increase at a CAGR of 2.3 percent

with 2009-2011 expected to be relatively flat.

Beyond this period, the MRO market is

expected to accelerate at a CAGR of 2.9

percent.

13

Next Steps

� Register for the next Chairman’s Series on Growth:

The Growth Excellence Model: Competitive Benchmarking & Growth

Investing (November 3, 2009) (http://www.frost.com/growth)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities(www.frost.com/news)

14

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

15

For Additional Information

Johanna Haynes

Senior Corporate Communications ExecutiveCorporate Communications(210) 247-3870

Gary Leikin

VP Business Development

Aerospace & Defense

(310) 318-8551

Wayne Plucker

Industry Manager

Aerospace & Defense

(210) 247-3869

Nathan K. Smith

Industry Analyst

Aerospace & Defense

(512) 276-5162