Embed Size (px)

Citation preview

NAVIGATING TURBULENT WATERS – AN ASSESSMENT & OUTLOOK FOR THE O&G INDUSTRY

Joseph Triepke Managing Director, Oilpro

KEYNOTE

STRATEGIES & OPPORTUNITIES: MANAGING IN A TURBULENT OIL & GAS WORLD

An Assessment & Outlook For The O&G Industry

Presented by Oilpro.com for WorkforceNEXT - April 2015

Navigating Turbulent Waters

A Look In The Rearview Mirror & Crystal Ball

• A small leak sinks a great ship – oil markets imbalanced by 1-2%, prices down 60%

• Sea changes can happen overnight –O&G cyclical inflection is always sharp

• Our lifestyle drafted up & adjusting to the new reality is painful

• US drilling is in midst of the worst downturn ever – US is the new swing producer

• Workforce contracting as we count >100,000 lay-offs with more to come

• $70 oil is the new $100 oil (just as $40- oil is unsustainable, so too is $100+ oil)

• A supply-driven collapse requires a supply-side solution, which means a lag to endure

• An elongated U-shaped recovery seems more likely than a V-shaped recovery

At The Center Of The Storm, Commodity Prices

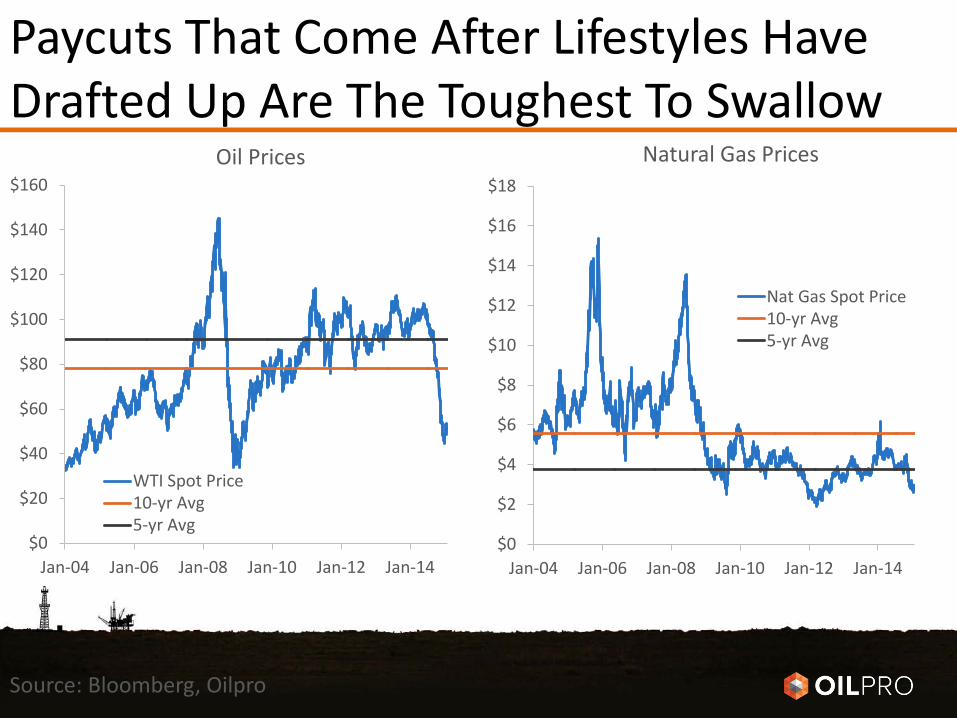

Paycuts That Come After Lifestyles Have Drafted Up Are The Toughest To Swallow

Source: Bloomberg, Oilpro

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Oil Prices

WTI Spot Price10-yr Avg5-yr Avg

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Natural Gas Prices

Nat Gas Spot Price10-yr Avg5-yr Avg

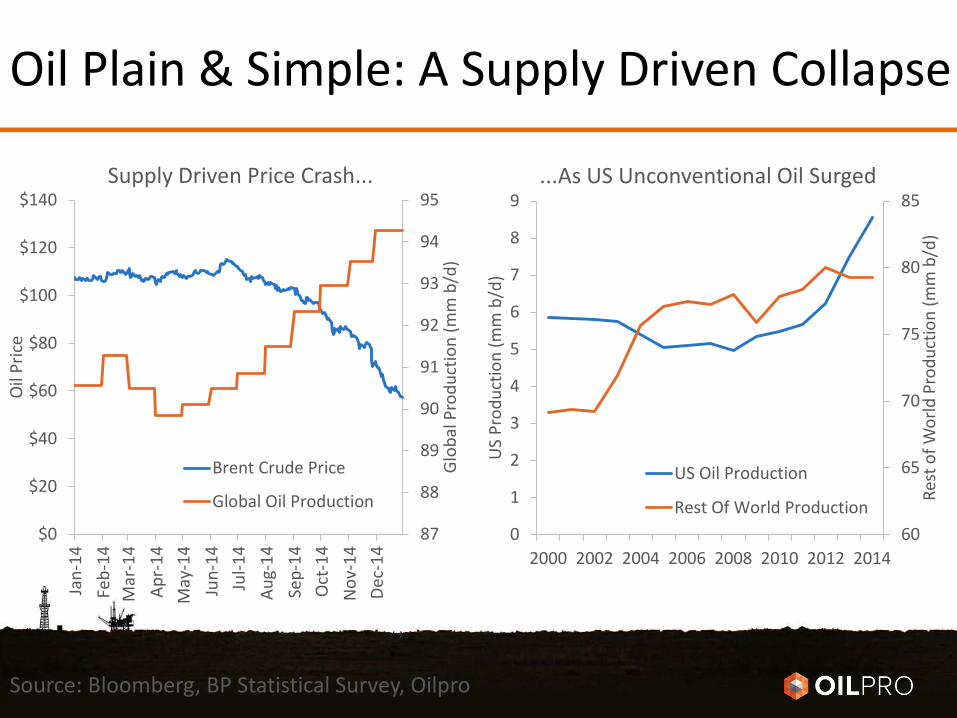

Oil Plain & Simple: A Supply Driven Collapse

87

88

89

90

91

92

93

94

95

$0

$20

$40

$60

$80

$100

$120

$140

Jan-

14Fe

b-14

Mar

-14

Apr-

14M

ay-1

4Ju

n-14

Jul-1

4Au

g-14

Sep-

14O

ct-1

4N

ov-1

4De

c-14

Glo

bal P

rodu

ctio

n (m

m b

/d)

Oil

Pric

e

Supply Driven Price Crash...

Brent Crude Price

Global Oil Production

60

65

70

75

80

85

0

1

2

3

4

5

6

7

8

9

2000 2002 2004 2006 2008 2010 2012 2014

Rest

of W

orld

Pro

duct

ion

(mm

b/d

)

US

Prod

uctio

n (m

m b

/d)

...As US Unconventional Oil Surged

US Oil Production

Rest Of World Production

Source: Bloomberg, BP Statistical Survey, Oilpro

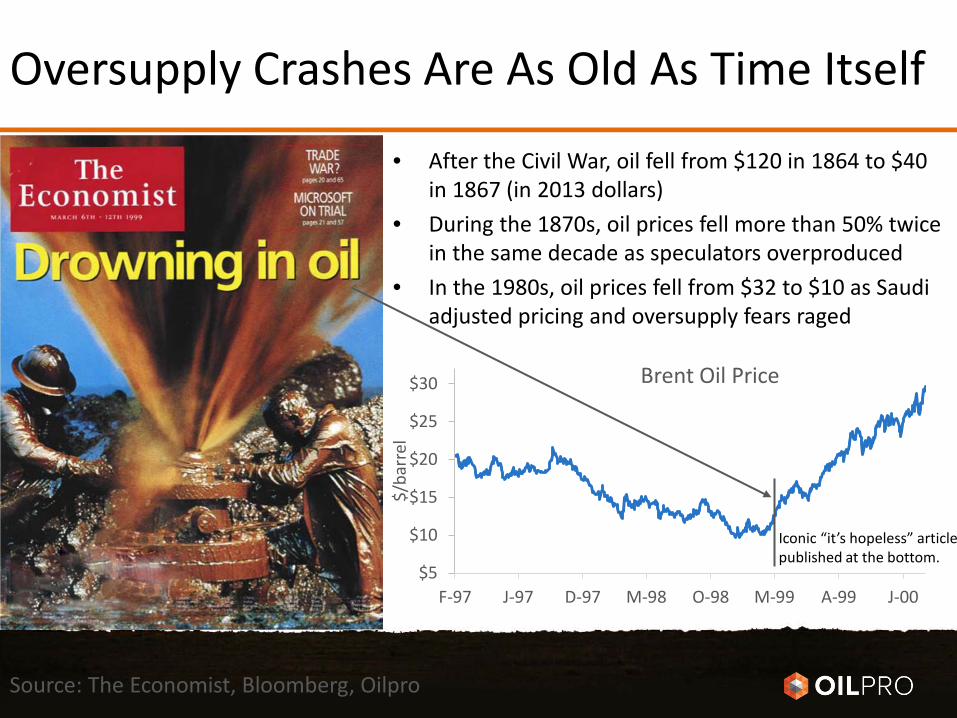

Oversupply Crashes Are As Old As Time Itself

• After the Civil War, oil fell from $120 in 1864 to $40 in 1867 (in 2013 dollars)

• During the 1870s, oil prices fell more than 50% twice in the same decade as speculators overproduced

• In the 1980s, oil prices fell from $32 to $10 as Saudi adjusted pricing and oversupply fears raged

$5

$10

$15

$20

$25

$30

F-97 J-97 D-97 M-98 O-98 M-99 A-99 J-00

$/ba

rrel

Brent Oil Price

Iconic “it’s hopeless” article published at the bottom.

Source: The Economist, Bloomberg, Oilpro

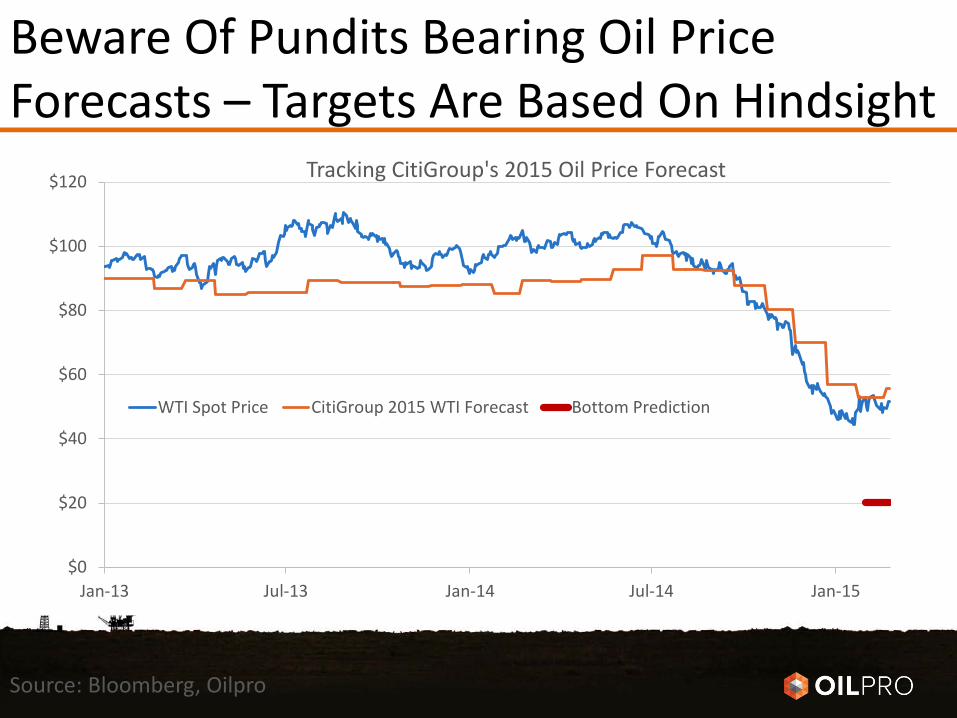

Beware Of Pundits Bearing Oil Price Forecasts – Targets Are Based On Hindsight

$0

$20

$40

$60

$80

$100

$120

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

Tracking CitiGroup's 2015 Oil Price Forecast

WTI Spot Price CitiGroup 2015 WTI Forecast Bottom Prediction

Source: Bloomberg, Oilpro

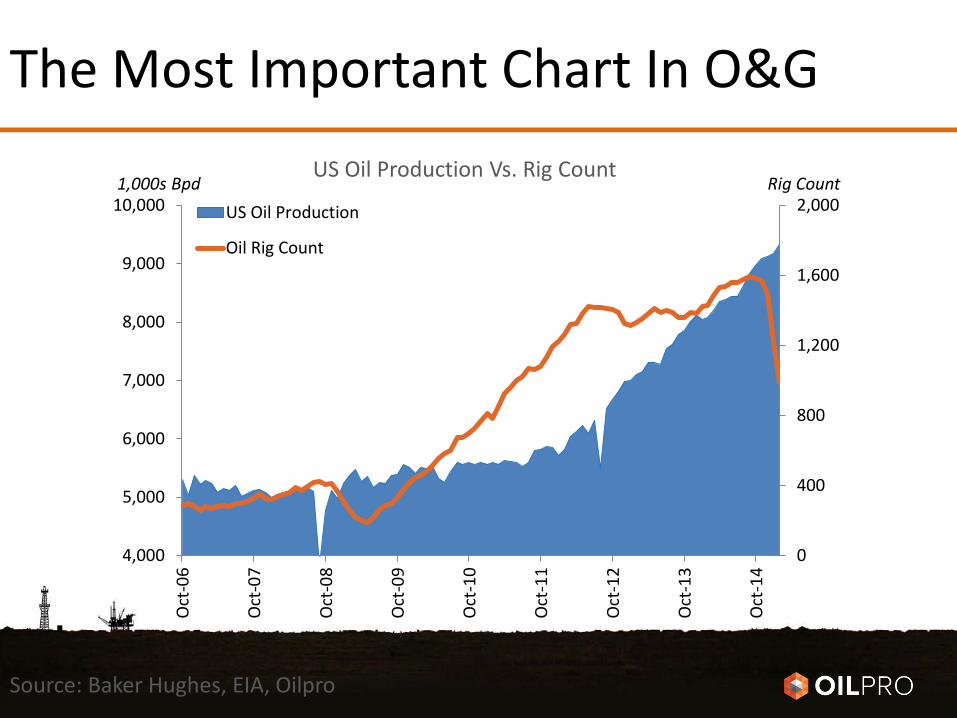

The Most Important Chart In O&G

0

400

800

1,200

1,600

2,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000O

ct-0

6

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

US Oil Production

Oil Rig Count

1,000s Bpd Rig Count US Oil Production Vs. Rig Count

Source: Baker Hughes, EIA, Oilpro

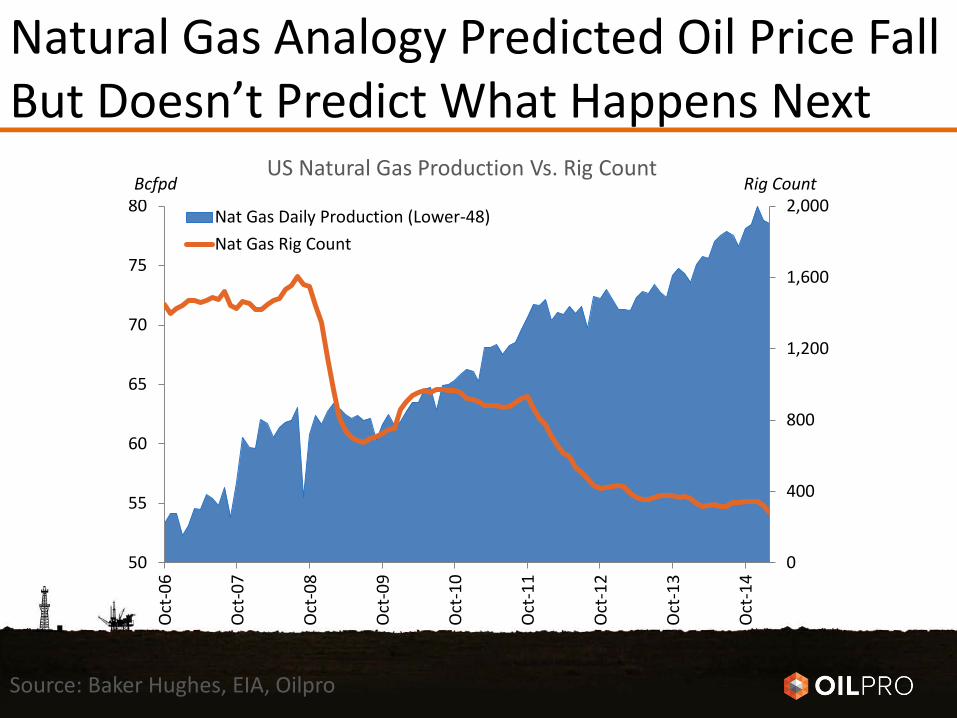

Natural Gas Analogy Predicted Oil Price Fall But Doesn’t Predict What Happens Next

0

400

800

1,200

1,600

2,000

50

55

60

65

70

75

80

Oct

-06

Oct

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

Nat Gas Daily Production (Lower-48)Nat Gas Rig Count

Bcfpd Rig Count US Natural Gas Production Vs. Rig Count

Source: Baker Hughes, EIA, Oilpro

260

310

360

410

460

Sep-

87

Sep-

89

Sep-

91

Sep-

93

Sep-

95

Sep-

97

Sep-

99

Sep-

01

Sep-

03

Sep-

05

Sep-

07

Sep-

09

Sep-

11

Sep-

13

Mill

ion

Barr

els o

f Oil

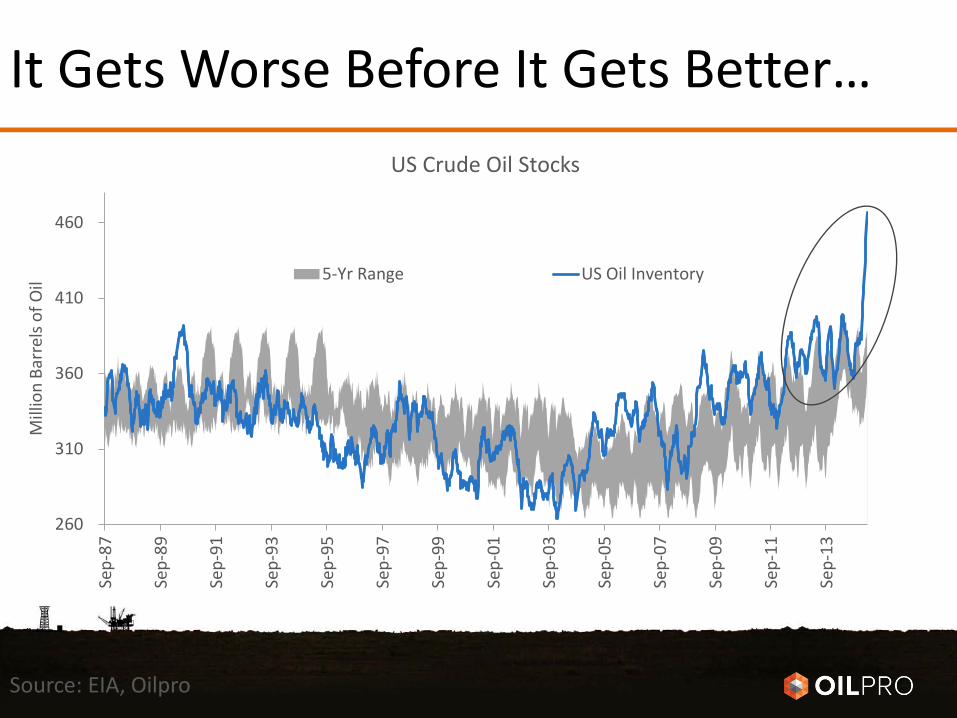

US Crude Oil Stocks

5-Yr Range 5-Yr Range US Oil Inventory

It Gets Worse Before It Gets Better…

Source: EIA, Oilpro

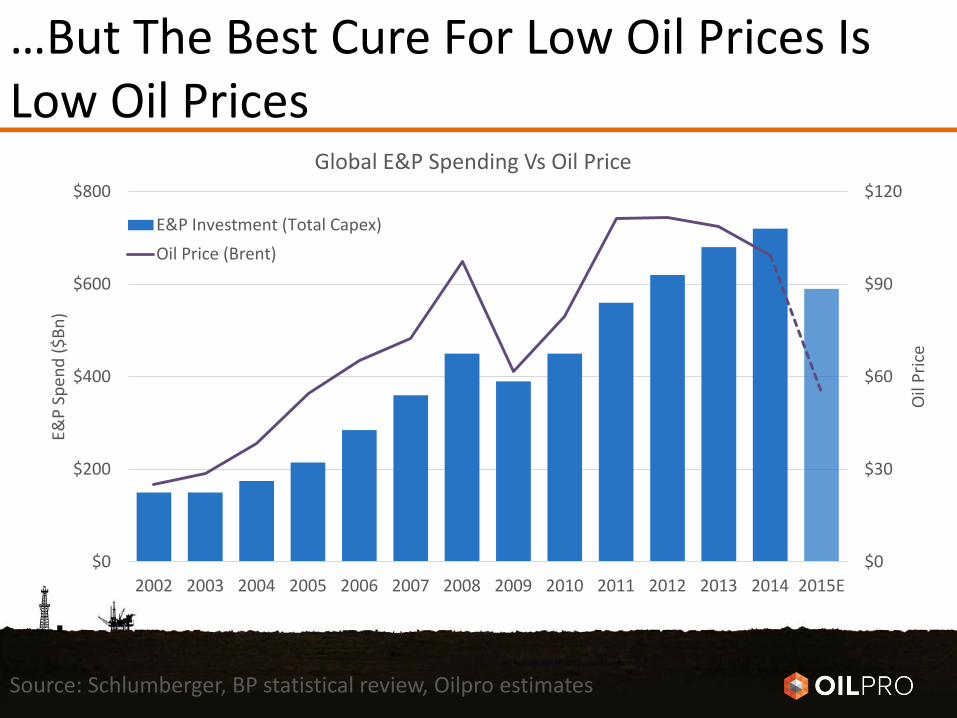

…But The Best Cure For Low Oil Prices Is Low Oil Prices

Source: Schlumberger, BP statistical review, Oilpro estimates

$0

$30

$60

$90

$120

$0

$200

$400

$600

$800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E

Oil

Pric

e

E&P

Spen

d ($

Bn)

Global E&P Spending Vs Oil Price

E&P Investment (Total Capex)Oil Price (Brent)

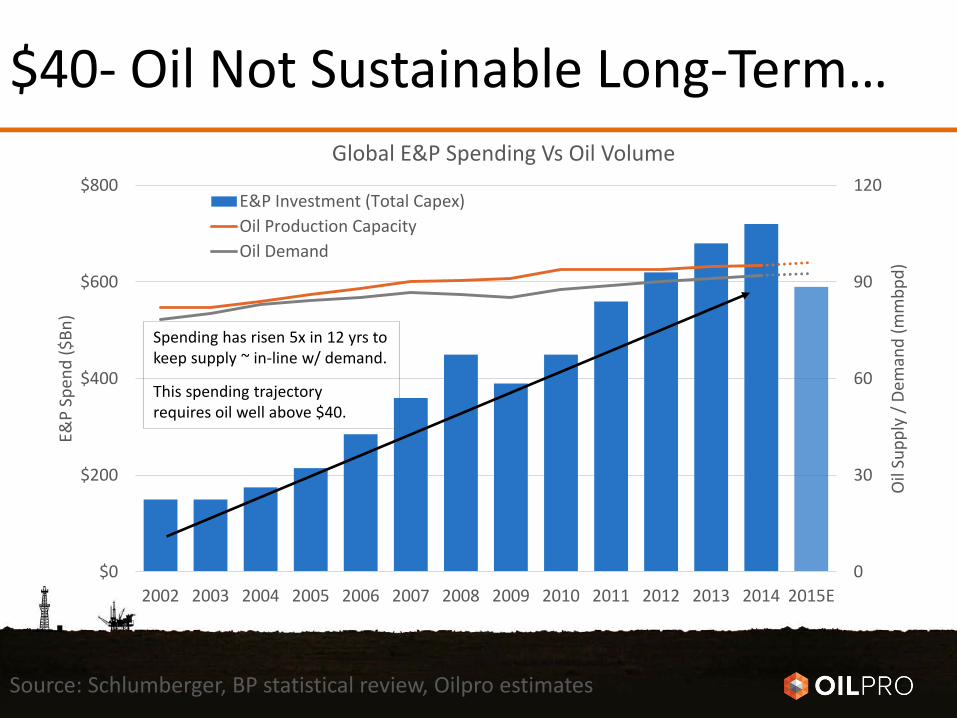

$40- Oil Not Sustainable Long-Term…

Source: Schlumberger, BP statistical review, Oilpro estimates

0

30

60

90

120

$0

$200

$400

$600

$800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E

Oil

Supp

ly /

Dem

and

(mm

bpd)

E&P

Spen

d ($

Bn)

Global E&P Spending Vs Oil Volume

E&P Investment (Total Capex)Oil Production CapacityOil Demand

Spending has risen 5x in 12 yrs to keep supply ~ in-line w/ demand.

This spending trajectory requires oil well above $40.

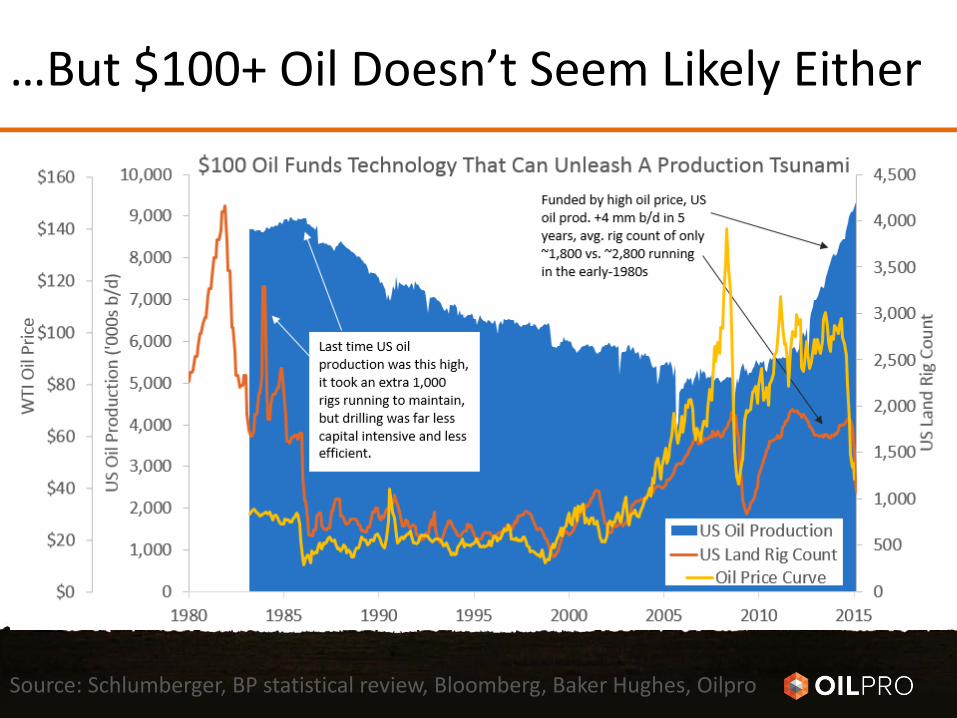

…But $100+ Oil Doesn’t Seem Likely Either

Source: Schlumberger, BP statistical review, Bloomberg, Baker Hughes, Oilpro

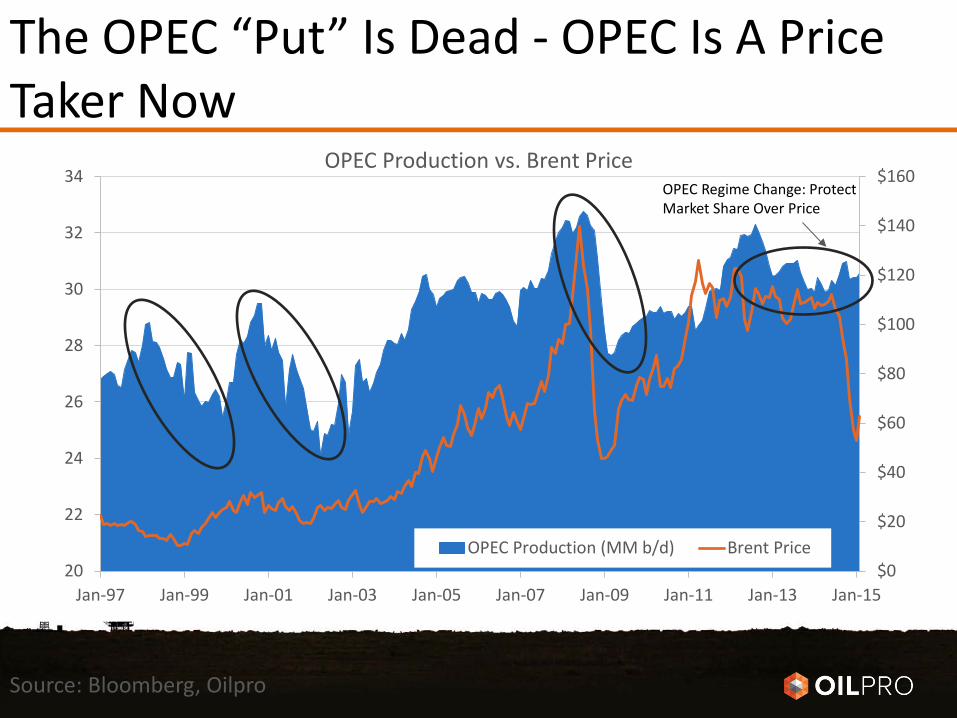

OPEC Rocked The Boat

The OPEC “Put” Is Dead - OPEC Is A Price Taker Now

Source: Bloomberg, Oilpro

$0

$20

$40

$60

$80

$100

$120

$140

$160

20

22

24

26

28

30

32

34

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

OPEC Production vs. Brent Price

OPEC Production (MM b/d) Brent Price

OPEC Regime Change: Protect Market Share Over Price

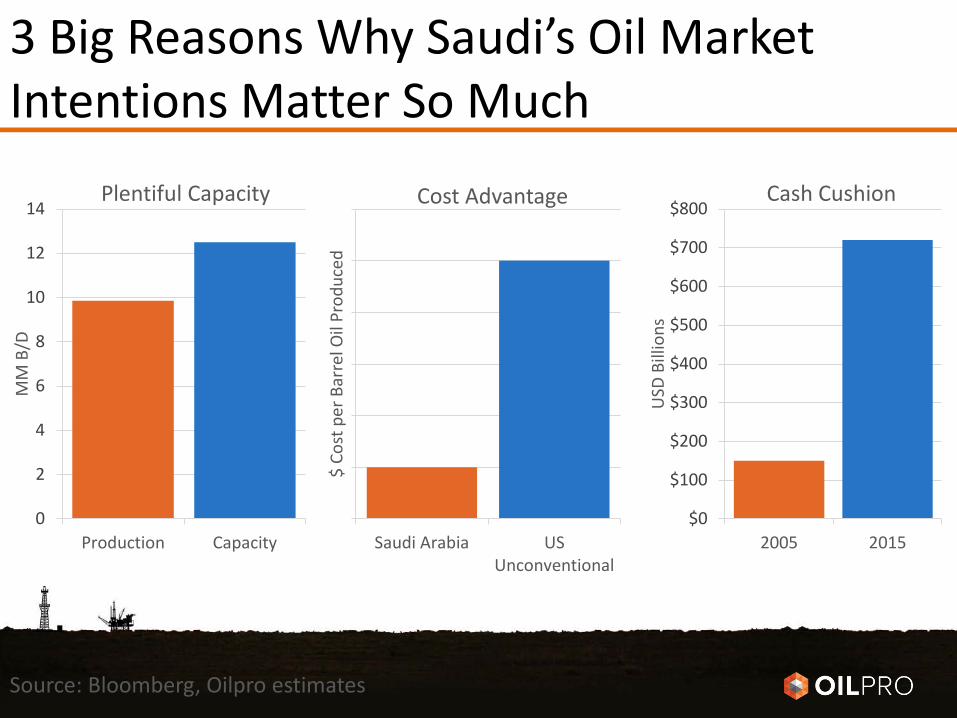

3 Big Reasons Why Saudi’s Oil Market Intentions Matter So Much

0

10

20

30

40

50

60

Saudi Arabia USUnconventional

$ Co

st p

er B

arre

l Oil

Prod

uced

Cost Advantage

0

2

4

6

8

10

12

14

Production Capacity

MM

B/D

Plentiful Capacity

$0

$100

$200

$300

$400

$500

$600

$700

$800

2005 2015

USD

Bill

ions

Cash Cushion

Source: Bloomberg, Oilpro estimates

Destabilization Spiral For Volatile Nations Is An Unpredictable Wildcard

Source: CNBC

$0 $20 $40 $60 $80 $100 $120 $140 $160

Libya

Venezuela

Iran

Bahrain

Nigeria

Oman

Russia

Saudi Arabia

UAE

Qatar

Kuwait

Kazakhstan

Oil Price Required To Balance Country Budgets

An Oil Tsunami Has Blitzed The Industry Marketplace

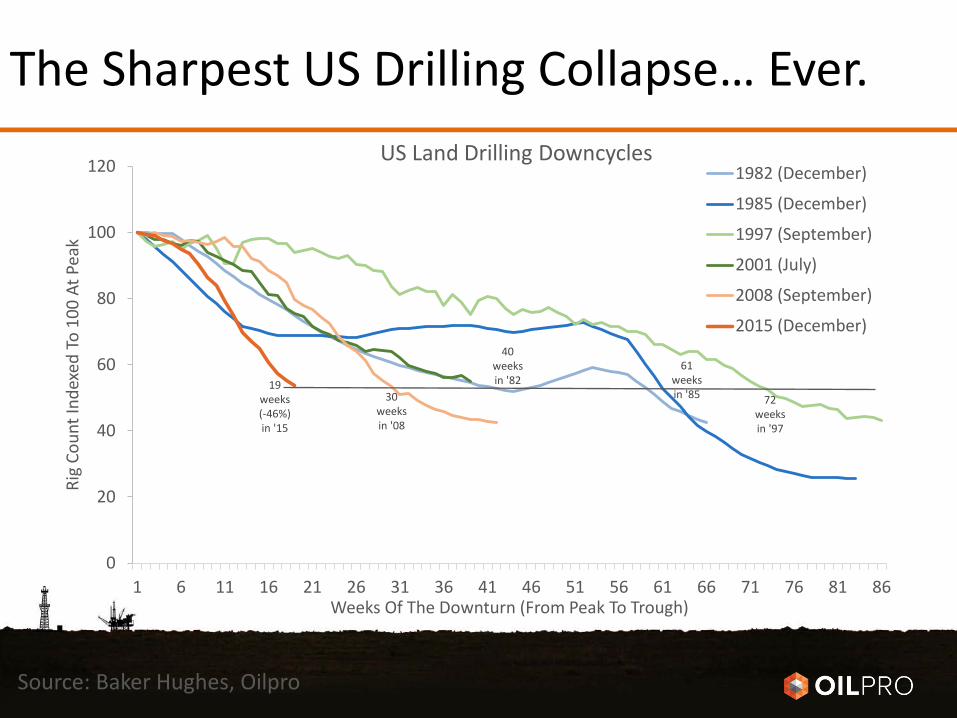

The Sharpest US Drilling Collapse… Ever.

Source: Baker Hughes, Oilpro

0

20

40

60

80

100

120

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86

Rig

Coun

t Ind

exed

To

100

At P

eak

Weeks Of The Downturn (From Peak To Trough)

US Land Drilling Downcycles 1982 (December)

1985 (December)

1997 (September)

2001 (July)

2008 (September)

2015 (December)

19 weeks (-46%) in '15

30 weeks in '08

40 weeks in '82

72 weeks in '97

61 weeks in '85

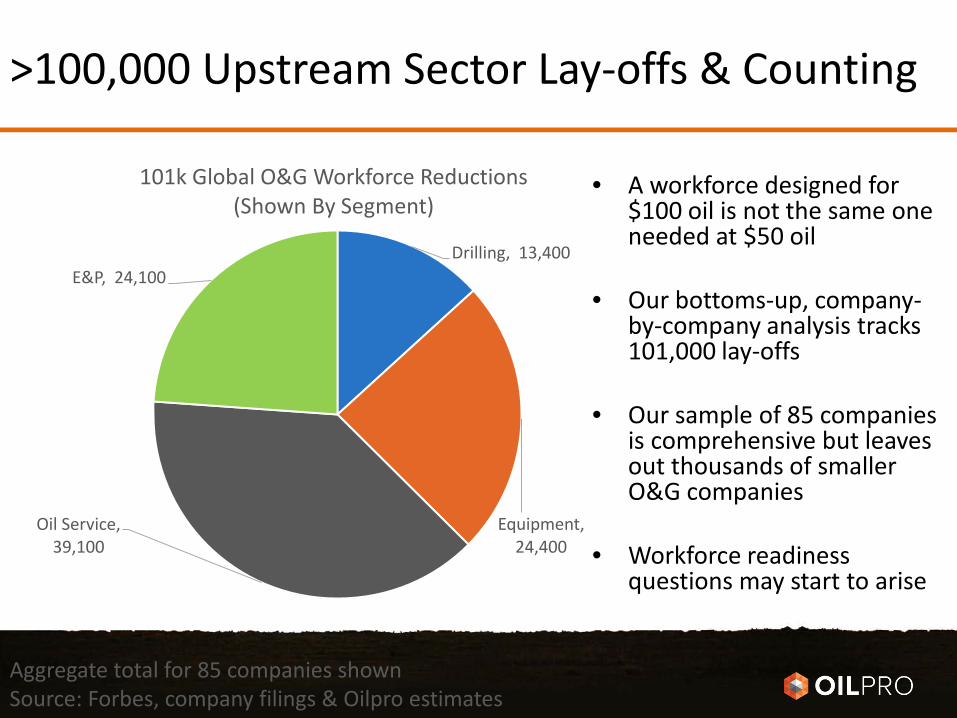

Drilling, 13,400

Equipment, 24,400

Oil Service, 39,100

E&P, 24,100

101k Global O&G Workforce Reductions (Shown By Segment)

>100,000 Upstream Sector Lay-offs & Counting

Aggregate total for 85 companies shown Source: Forbes, company filings & Oilpro estimates

• A workforce designed for $100 oil is not the same one needed at $50 oil

• Our bottoms-up, company-by-company analysis tracks 101,000 lay-offs

• Our sample of 85 companies is comprehensive but leaves out thousands of smaller O&G companies

• Workforce readiness questions may start to arise

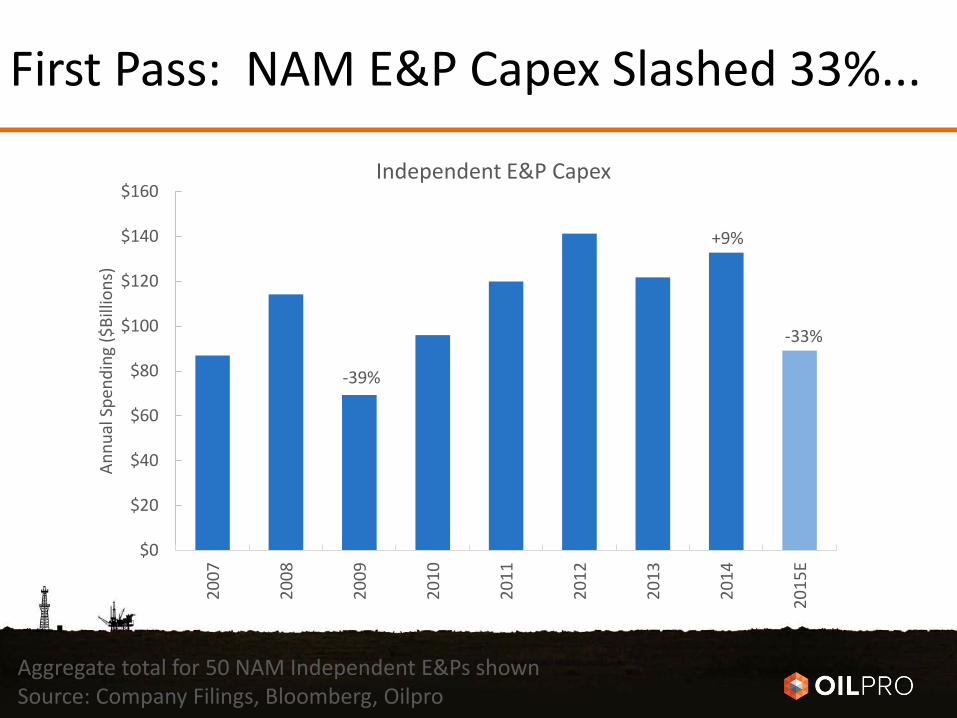

First Pass: NAM E&P Capex Slashed 33%...

Aggregate total for 50 NAM Independent E&Ps shown Source: Company Filings, Bloomberg, Oilpro

$0

$20

$40

$60

$80

$100

$120

$140

$16020

07

2008

2009

2010

2011

2012

2013

2014

2015

E

Annu

al S

pend

ing

($Bi

llion

s)

Independent E&P Capex

-39%

+9%

-33%

…But Rig Count Implies A Cut Closer To 50%

Data Input Sources: Spears, Halliburton, Baker Hughes, Oilpro estimates

• 1 working land rig = $75 million per year in Drilling & Completion (D&C) spending

• 2014 average rig count 1,800 * $75 million = $140 billion D&C market size

• Our best guess: the US will average about 1,100 land rigs working this year

• 2015 average rig count 1,100 * $75 million = $83 billion D&C market size

• Add in deferred completions and the US drilling & completion market could by shrink upwards of $65 billion in 2015, close to a 50% spending reduction

• Expect more capex reduction announcements, and more competition for D&C work

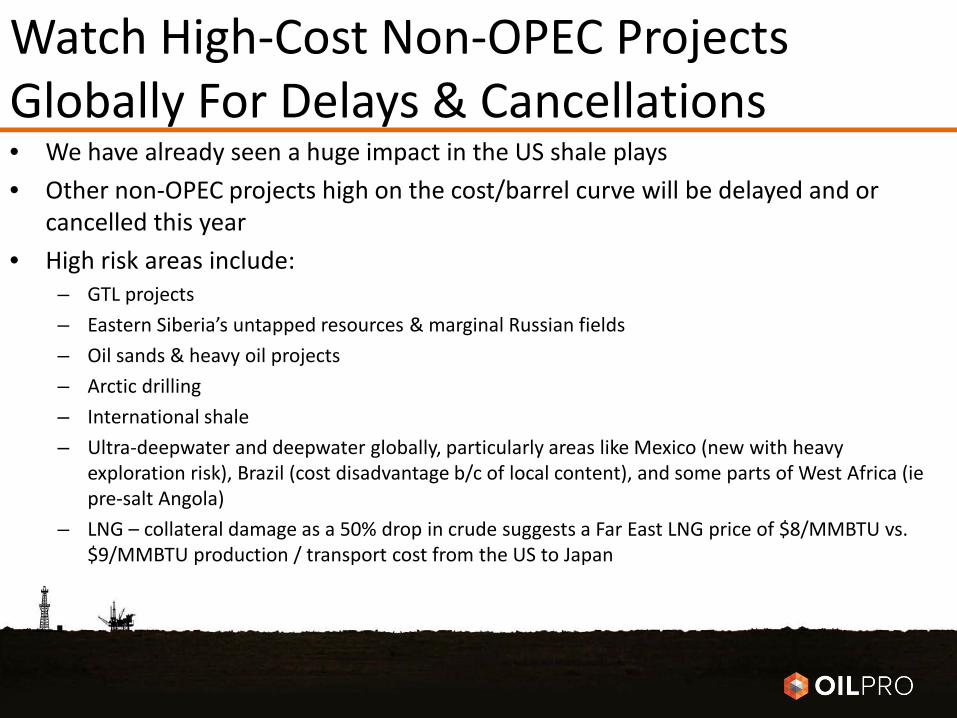

Watch High-Cost Non-OPEC Projects Globally For Delays & Cancellations • We have already seen a huge impact in the US shale plays • Other non-OPEC projects high on the cost/barrel curve will be delayed and or

cancelled this year • High risk areas include:

– GTL projects – Eastern Siberia’s untapped resources & marginal Russian fields – Oil sands & heavy oil projects – Arctic drilling – International shale – Ultra-deepwater and deepwater globally, particularly areas like Mexico (new with heavy

exploration risk), Brazil (cost disadvantage b/c of local content), and some parts of West Africa (ie pre-salt Angola)

– LNG – collateral damage as a 50% drop in crude suggests a Far East LNG price of $8/MMBTU vs. $9/MMBTU production / transport cost from the US to Japan

The Storm Is Reshaping The O&G Workforce – 7 Key Trends

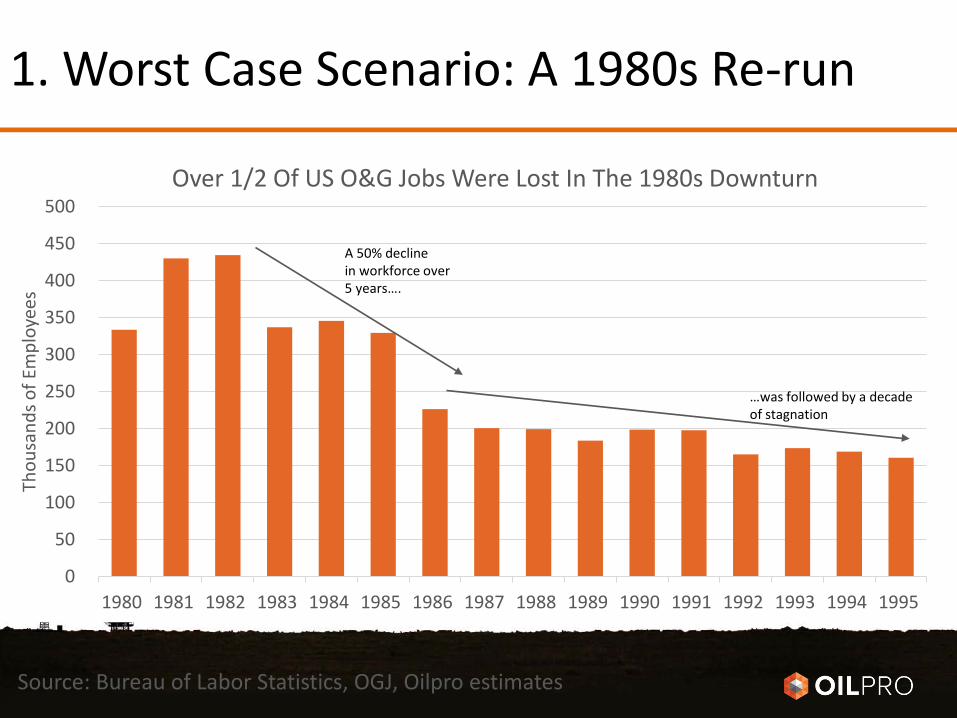

1. Worst Case Scenario: A 1980s Re-run

0

50

100

150

200

250

300

350

400

450

500

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995

Thou

sand

s of E

mpl

oyee

s

Over 1/2 Of US O&G Jobs Were Lost In The 1980s Downturn

A 50% decline in workforce over 5 years….

…was followed by a decade of stagnation

Source: Bureau of Labor Statistics, OGJ, Oilpro estimates

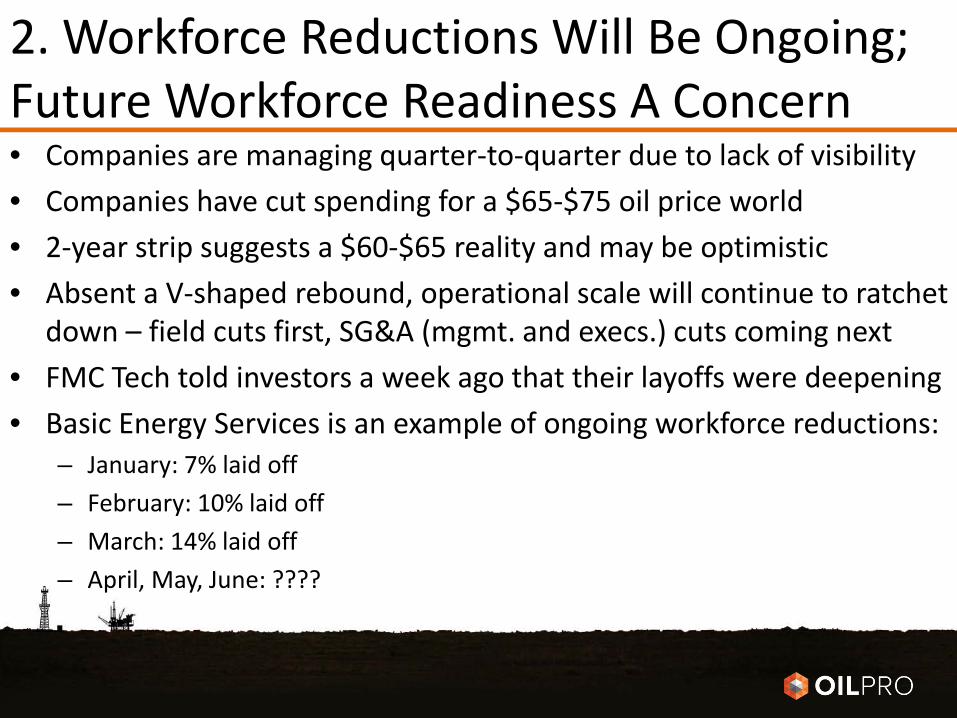

2. Workforce Reductions Will Be Ongoing; Future Workforce Readiness A Concern • Companies are managing quarter-to-quarter due to lack of visibility • Companies have cut spending for a $65-$75 oil price world • 2-year strip suggests a $60-$65 reality and may be optimistic • Absent a V-shaped rebound, operational scale will continue to ratchet

down – field cuts first, SG&A (mgmt. and execs.) cuts coming next • FMC Tech told investors a week ago that their layoffs were deepening • Basic Energy Services is an example of ongoing workforce reductions:

– January: 7% laid off – February: 10% laid off – March: 14% laid off – April, May, June: ????

3. International Workforce Likely To Hold Up Better Than The US

0

20

40

60

80

100

120

140

160

180

Mar-05 Mar-07 Mar-09 Mar-11 Mar-13 Mar-15

Rig

Coun

t (In

dexe

d to

100

in M

arch

200

5)

International Cycles Are More Muted Than In The US

US Land Rig Count

International Rig Count

Trend Line

Source: Baker Hughes, Oilpro

The US overshoots cyclical highs and lows more than the int’l average, resulting in more pronounced US workforce expansions and contractions.

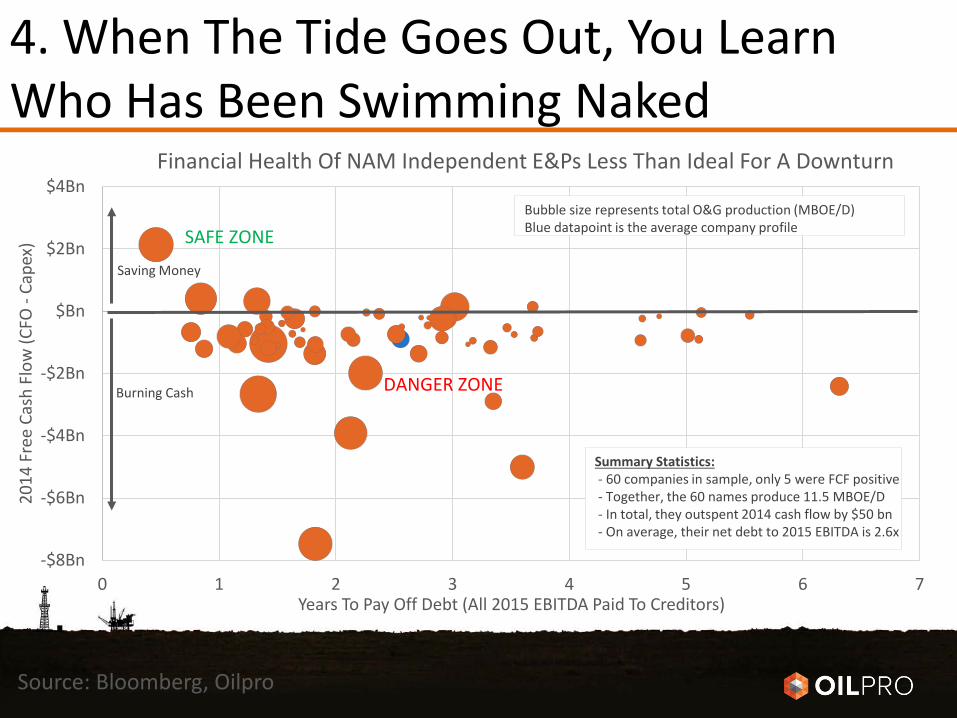

4. When The Tide Goes Out, You Learn Who Has Been Swimming Naked

-$8Bn

-$6Bn

-$4Bn

-$2Bn

$Bn

$2Bn

$4Bn

0 1 2 3 4 5 6 7

2014

Fre

e Ca

sh F

low

(CFO

- Ca

pex)

Years To Pay Off Debt (All 2015 EBITDA Paid To Creditors)

Financial Health Of NAM Independent E&Ps Less Than Ideal For A Downturn

Bubble size represents total O&G production (MBOE/D) Blue datapoint is the average company profile

Saving Money

Burning Cash

Summary Statistics: - 60 companies in sample, only 5 were FCF positive - Together, the 60 names produce 11.5 MBOE/D - In total, they outspent 2014 cash flow by $50 bn - On average, their net debt to 2015 EBITDA is 2.6x

SAFE ZONE

DANGER ZONE

Source: Bloomberg, Oilpro

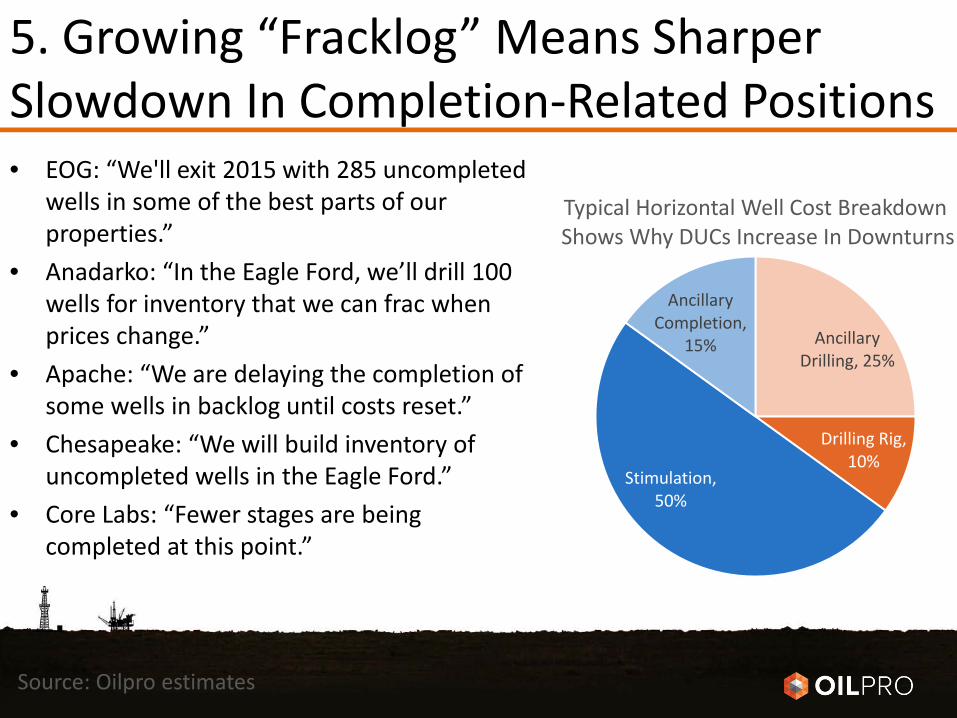

5. Growing “Fracklog” Means Sharper Slowdown In Completion-Related Positions • EOG: “We'll exit 2015 with 285 uncompleted

wells in some of the best parts of our properties.”

• Anadarko: “In the Eagle Ford, we’ll drill 100 wells for inventory that we can frac when prices change.”

• Apache: “We are delaying the completion of some wells in backlog until costs reset.”

• Chesapeake: “We will build inventory of uncompleted wells in the Eagle Ford.”

• Core Labs: “Fewer stages are being completed at this point.”

Ancillary Drilling, 25%

Drilling Rig, 10%

Stimulation, 50%

Ancillary Completion,

15%

Typical Horizontal Well Cost Breakdown Shows Why DUCs Increase In Downturns

Source: Oilpro estimates

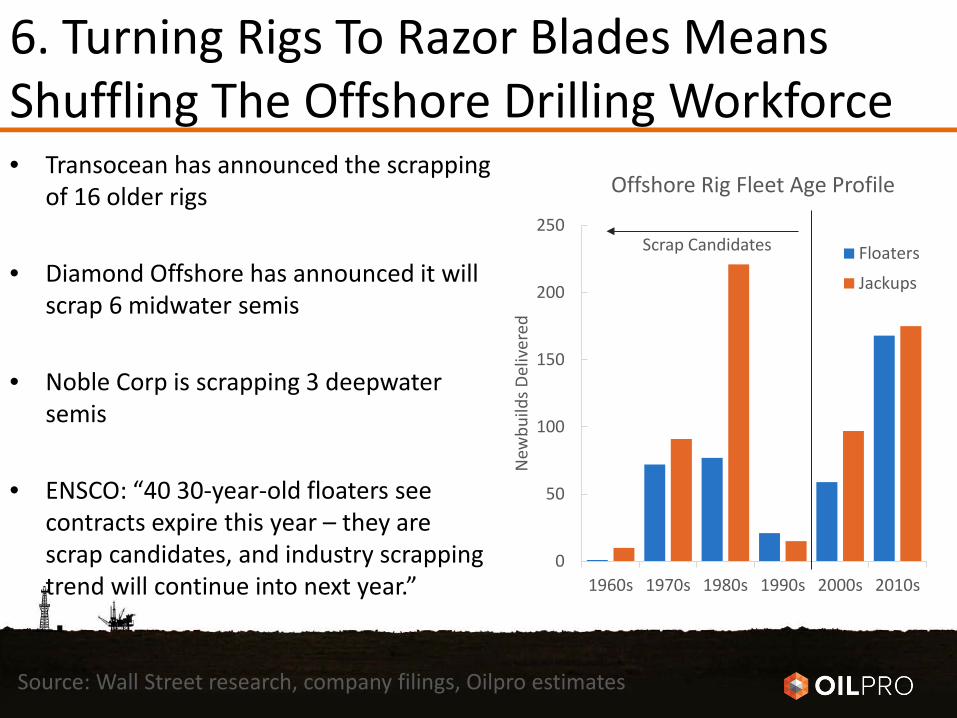

6. Turning Rigs To Razor Blades Means Shuffling The Offshore Drilling Workforce • Transocean has announced the scrapping

of 16 older rigs

• Diamond Offshore has announced it will scrap 6 midwater semis

• Noble Corp is scrapping 3 deepwater semis

• ENSCO: “40 30-year-old floaters see contracts expire this year – they are scrap candidates, and industry scrapping trend will continue into next year.”

0

50

100

150

200

250

1960s 1970s 1980s 1990s 2000s 2010s

New

build

s Del

iver

ed

Offshore Rig Fleet Age Profile

Floaters

Jackups

Scrap Candidates

Source: Wall Street research, company filings, Oilpro estimates

7. M&A Activity Will Pick Up • Plenty of good opportunities in the scorched earth of US shale

• Look for frequent smaller deals and a few large ones

• Bottom tier E&Ps will struggle in new environment, to become take-out candidates

• Majors, NOCs, Private Equity will all be looking at the US independent E&Ps

• HAL / BHI encourages more consolidation in oilfield services

Steady As She Goes – The Storm Before The Calm

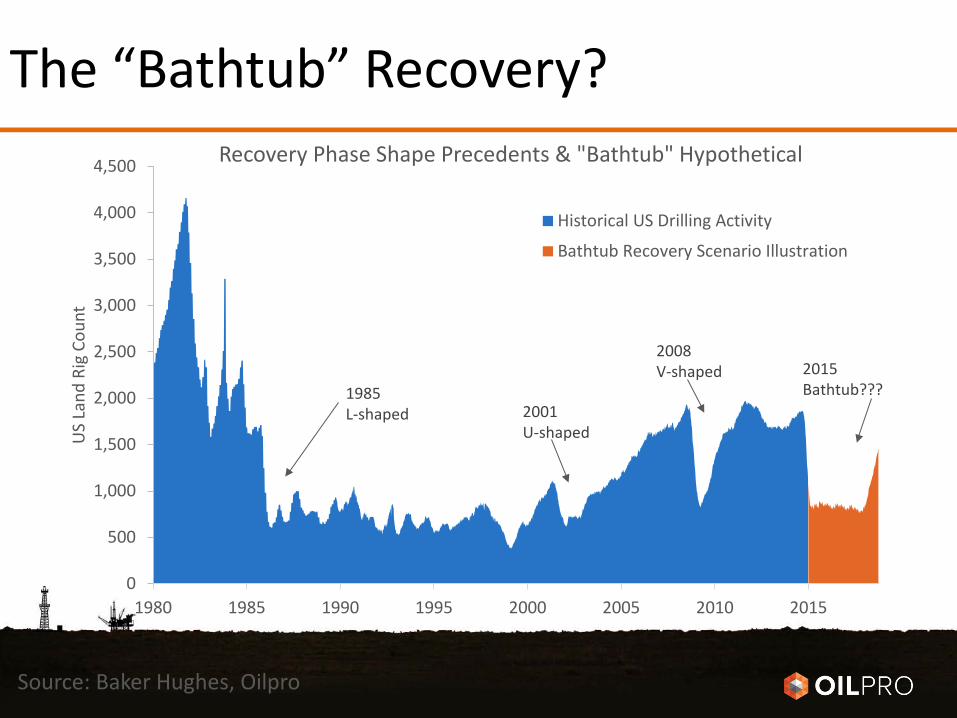

The “Bathtub” Recovery?

Source: Baker Hughes, Oilpro

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1980 1985 1990 1995 2000 2005 2010 2015

US

Land

Rig

Cou

nt

Recovery Phase Shape Precedents & "Bathtub" Hypothetical

Historical US Drilling Activity

Bathtub Recovery Scenario Illustration

1985 L-shaped

2008 V-shaped

2001 U-shaped

2015 Bathtub???

$50 Oil Solves Some Operational Challenges • War on talent fading

• Its an employer’s market

now

• Labor cost inflation gone

• Less temporary housing

• Lead times for key equipment and consumables falling

• Risk of overbuilding fading

• New entrants slowing

Busts Are Tough, But Booms Aren’t Easy Either

The “We’ve Always Done It This Way” Pitfall • $100 oil status quo doesn’t cut it at $50 oil

• The industry is known for its habits

• Surviving and succeeding now require

questioning everything

• Industry must undergo a structural re-tooling to drive cost/barrel down

• New ways of doing things and new technologies must be considered

Niches That Can Thrive In A $50 Oil World • Technology, integration & collaborative workflows that

reduce the cost of a barrel will gain traction

• New teams forming across non-traditional groupings

• Mature fields have a low-cost-barrel advantage

• Midstream & US oil storage capacity build out growing

• Production-related services to stay busy (EOR, well maintenance / servicing, re-fracturing old wells)

Final Thoughts • Operating costs are the problem today, but workforce readiness will be the problem

tomorrow

• $70 oil is the new $100 oil – just as $40- oil is unsustainable, so too is $100+ oil given the “flip the switch” factor on US oil production at $100 oil

• Elongated U-shaped recovery more likely than a V-shaped rebound

• Industry is recalibrating & will continue to re-tool for several years

• Layoffs & capex cuts come first, but new workflows, technologies, & teams are needed

• Opportunities exist for creative companies – lowering the cost per barrel is critical, it is an employer’s market now, revisiting mature fields is a big opportunity

• Recovery roadmap: Watch O&G equities, US oil production & storage data, 1Q EPS conference calls in April, and the June OPEC meeting results

Questions / Contact Info

• Questions about these trends and other O&G issues can be posed to an engaged community of industry professionals at Oilpro.com/questions

• You can connect with and contact Joseph Triepke at Oilpro.com or by email at [email protected]

About Author: Joseph Triepke Managing Director, Oilpro.com Joseph Triepke is a finance professional with a decade of upstream experience. As an energy investor and analyst for institutions like Citadel, Guggenheim, and Jefferies, he focused on O&G industry research and analysis. Today, he is Managing Director at Oilpro.com where he oversees content created by the community and publishes his own research on oil services, equipment and drilling. Joseph earned a Bachelor’s of Business Administration in Finance from UT Austin with Honors in 2004, has successfully completed 2/3 CFA examinations, and currently resides with his wife in Dallas, TX.

Appendix

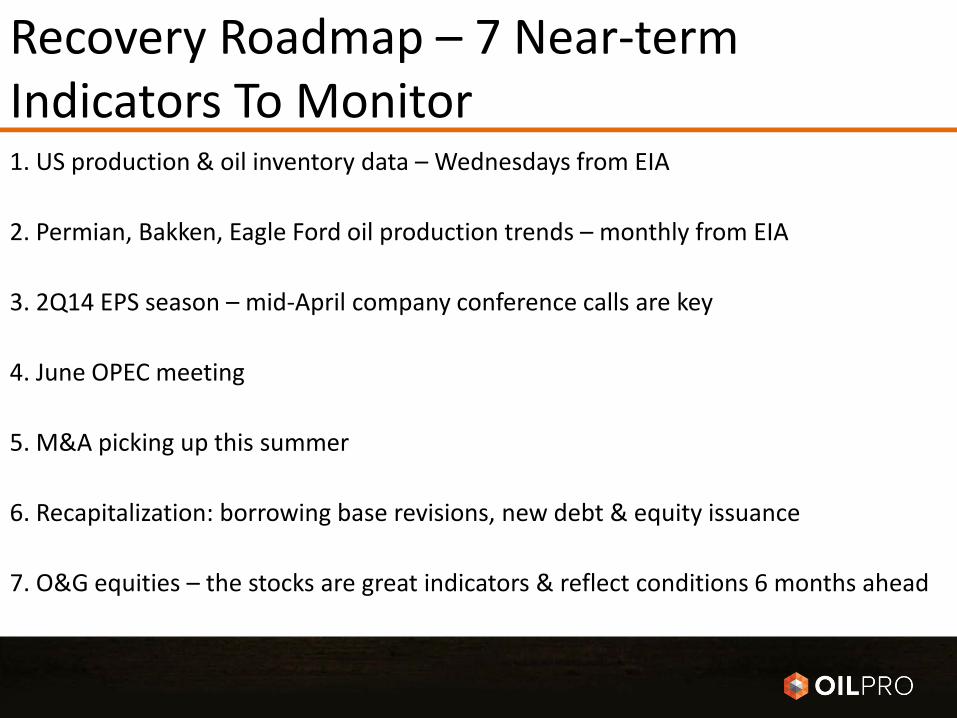

Recovery Roadmap – 7 Near-term Indicators To Monitor 1. US production & oil inventory data – Wednesdays from EIA

2. Permian, Bakken, Eagle Ford oil production trends – monthly from EIA

3. 2Q14 EPS season – mid-April company conference calls are key

4. June OPEC meeting

5. M&A picking up this summer

6. Recapitalization: borrowing base revisions, new debt & equity issuance

7. O&G equities – the stocks are great indicators & reflect conditions 6 months ahead

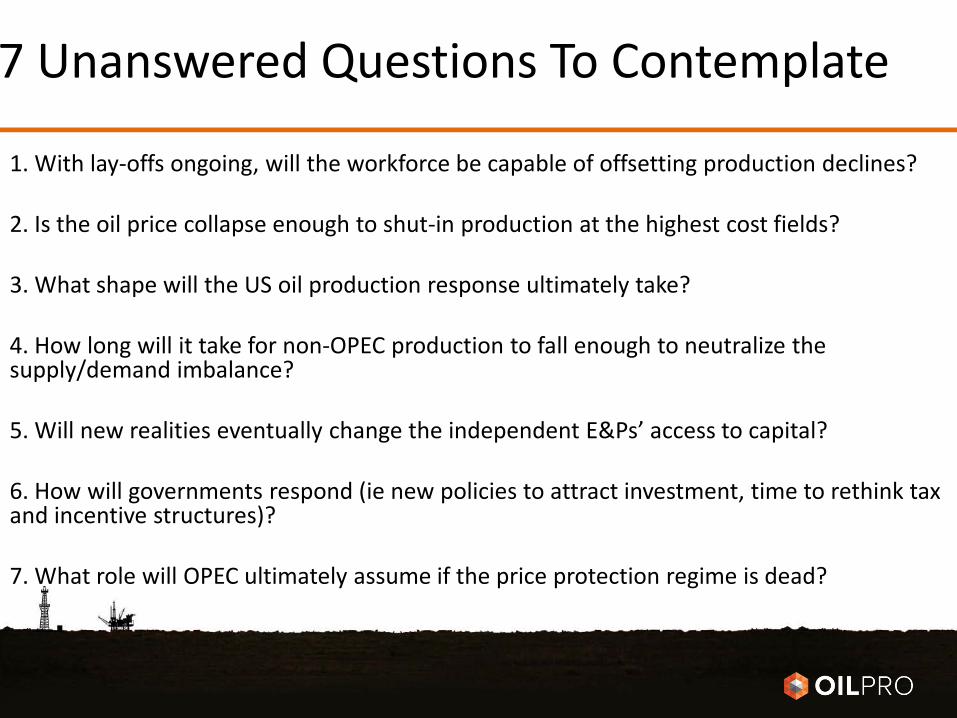

7 Unanswered Questions To Contemplate

1. With lay-offs ongoing, will the workforce be capable of offsetting production declines? 2. Is the oil price collapse enough to shut-in production at the highest cost fields?

3. What shape will the US oil production response ultimately take?

4. How long will it take for non-OPEC production to fall enough to neutralize the supply/demand imbalance?

5. Will new realities eventually change the independent E&Ps’ access to capital?

6. How will governments respond (ie new policies to attract investment, time to rethink tax and incentive structures)?

7. What role will OPEC ultimately assume if the price protection regime is dead?

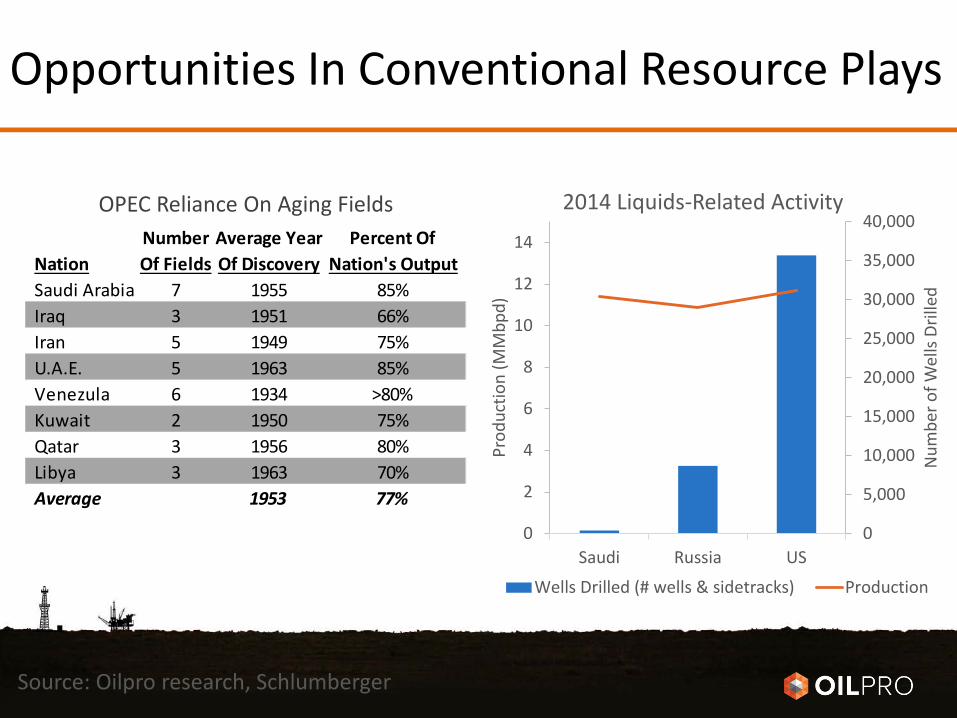

Opportunities In Conventional Resource Plays

Source: Oilpro research, Schlumberger

Number Average Year Percent OfNation Of Fields Of Discovery Nation's OutputSaudi Arabia 7 1955 85%Iraq 3 1951 66%Iran 5 1949 75%U.A.E. 5 1963 85%Venezula 6 1934 >80%Kuwait 2 1950 75%Qatar 3 1956 80%Libya 3 1963 70%Average 1953 77%

OPEC Reliance On Aging Fields

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

2

4

6

8

10

12

14

Saudi Russia US

Num

ber o

f Wel

ls Dr

illed

Prod

uctio

n (M

Mbp

d)

2014 Liquids-Related Activity

Wells Drilled (# wells & sidetracks) Production

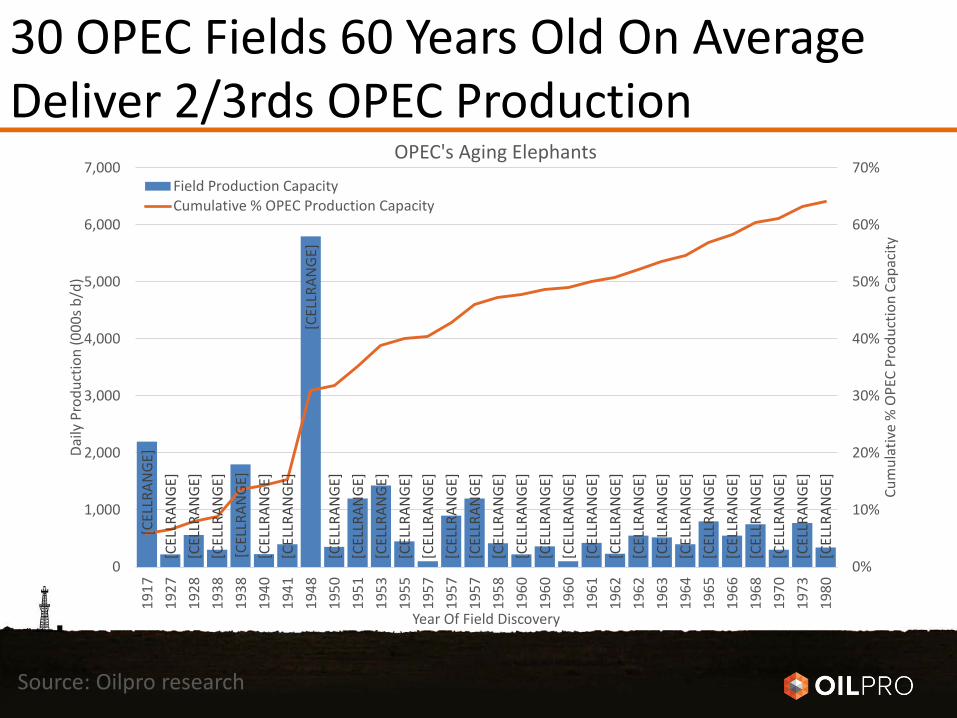

30 OPEC Fields 60 Years Old On Average Deliver 2/3rds OPEC Production

Source: Oilpro research

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

[CEL

LRAN

GE]

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,00019

1719

2719

2819

3819

3819

4019

4119

4819

5019

5119

5319

5519

5719

5719

5719

5819

6019

6019

6019

6119

6219

6219

6319

6419

6519

6619

6819

7019

7319

80

Cum

ulat

ive

% O

PEC

Prod

uctio

n Ca

paci

ty

Daily

Pro

duct

ion

(000

s b/d

)

Year Of Field Discovery

OPEC's Aging Elephants Field Production CapacityCumulative % OPEC Production Capacity

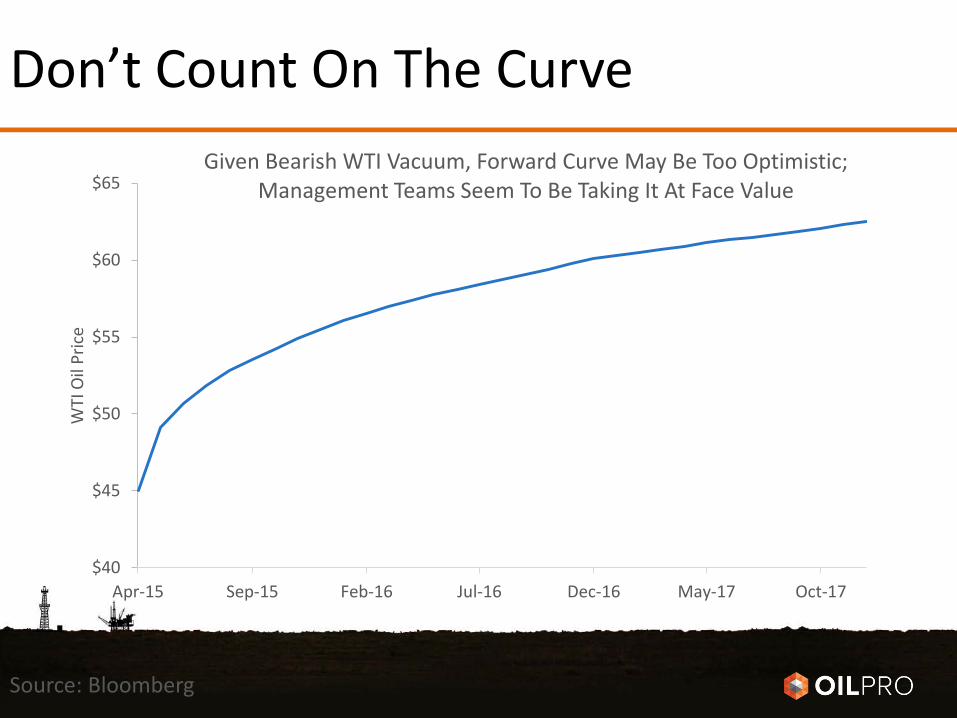

Don’t Count On The Curve

Source: Bloomberg

$40

$45

$50

$55

$60

$65

Apr-15 Sep-15 Feb-16 Jul-16 Dec-16 May-17 Oct-17

WTI

Oil

Pric

e

Given Bearish WTI Vacuum, Forward Curve May Be Too Optimistic; Management Teams Seem To Be Taking It At Face Value