Embed Size (px)

Citation preview

The Venetian Macao Marina Bay Sands, Singapore

Sands Macao Four Seasons Macao Sands Bethlehem The Venetian Las Vegas The Palazzo, Las Vegas

2Q15 Earnings Call PresentationJuly 22, 2015

The Parisian MacaoSands Cotai Central, Macao

This presentation contains forward-looking statements that are made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new development, construction and ventures, substantial leverage and debt service, government regulation, tax law changes, legalization of gaming, interest rates, future terrorist acts, influenza, insurance, gaming promoters, risks relating to our gaming licenses, certificate and subconcession, infrastructure in Macao, our ability to meet certain development deadlines, our subsidiaries’ ability to make distribution payments to us, and other factors detailed in the reports filed by Las Vegas Sands Corp. with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date thereof. Las Vegas Sands Corp. assumes no obligation to update such information.

Forward Looking Statements

2

The global leader in Integrated Resort development and operation, delivering strong and diversified cash flow and earnings as well as growing recurring dividends

Best positioned operator to deliver long-term growth in Asia, with the pre-eminent destination Integrated Resort properties in the world’s largest and fastest growing consumer markets

Uniquely positioned to bring unmatched track record, powerful convention-based business model and the industry’s strongest balance sheet to the world’s most promising IntegratedResort development opportunities

Committed to maximizing shareholder returns by delivering long-term growth while continuing the return of capital to shareholders through recurring dividend and stock repurchase programs

The industry’s most experienced leadership team: visionary, disciplined and dedicated todriving long-term shareholder value

The Investment Case for Las Vegas Sands

3

Maximizing Return to Shareholders by:1. Delivering long-term growth in current markets 2. Using leadership position in convention-based Integrated Resort development and

operation to pursue global growth opportunities3. Continuing to return excess capital to shareholders

Net revenue was $2.92 billion

Consolidated adjusted property EBITDA was $1.02 billion

Consolidated EBITDA margin was 34.8% (35.2% on a hold-normalized basis)

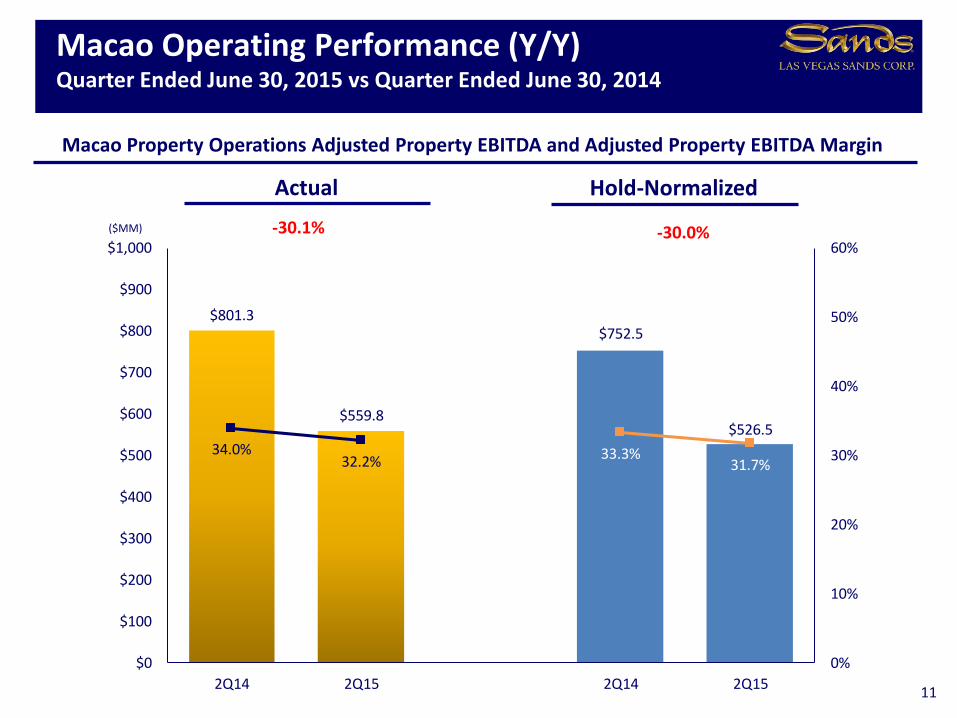

Macao – Adjusted property EBITDA was $559.8 million

Strong cost discipline drove a 150 basis point sequential increase in hold-normalized adjusted property EBITDA margin to 31.7%

Marina Bay Sands – Despite headwind of stronger US dollar, Adjusted property EBITDA was $363.3 million (Hold-normalized Adjusted property EBITDA increased 6.1% on a constant currency basis)

Adjusted diluted EPS was $0.60 per share

LVS returned a total of $583.8 million to shareholders during the quarter through:

Recurring dividend of $0.65 per share

Stock repurchase program ($65.0 million repurchased at a weighted average price of $50.46 during the quarter)

Second Quarter 2015 Financial HighlightsContinued Return of Capital to Shareholders Despite Current Headwinds in Macao

4NOTE: All comparisons in this presentation compare the second quarter 2015 against the second quarter 2014 unless otherwise specified.

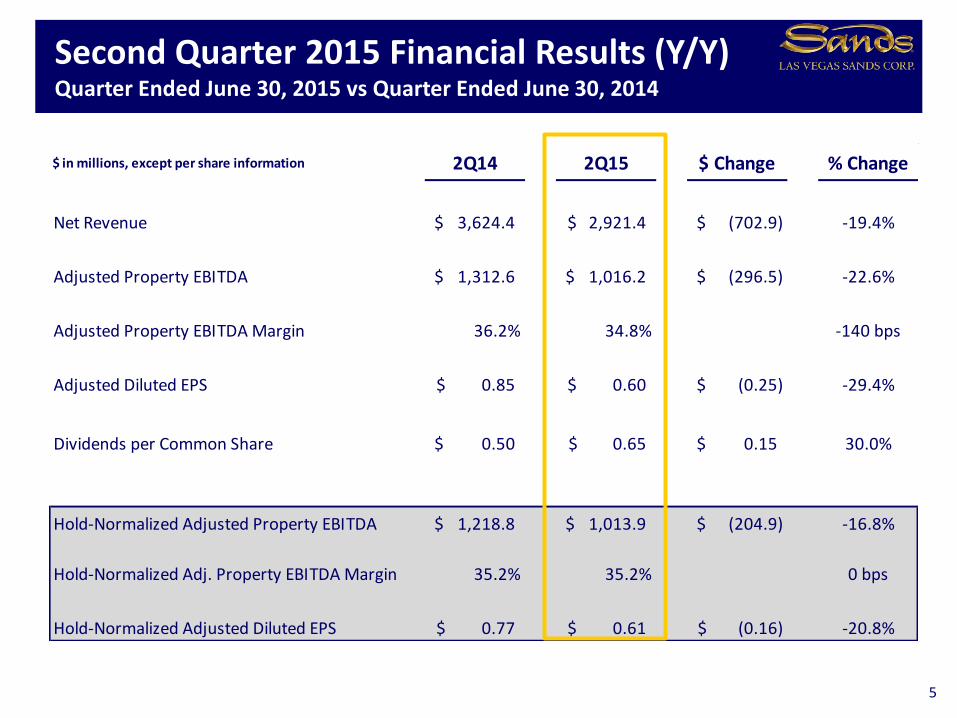

$ in millions, except per share information 2Q14 2Q15 $ Change % Change

Net Revenue 3,624.4$ 2,921.4$ (702.9)$ -19.4%

Adjusted Property EBITDA 1,312.6$ 1,016.2$ (296.5)$ -22.6%

Adjusted Property EBITDA Margin 36.2% 34.8% -140 bps

Adjusted Diluted EPS 0.85$ 0.60$ (0.25)$ -29.4%

Dividends per Common Share 0.50$ 0.65$ 0.15$ 30.0%

Hold-Normalized Adjusted Property EBITDA 1,218.8$ 1,013.9$ (204.9)$ -16.8%

Hold-Normalized Adj. Property EBITDA Margin 35.2% 35.2% 0 bps

Hold-Normalized Adjusted Diluted EPS 0.77$ 0.61$ (0.16)$ -20.8%

Second Quarter 2015 Financial Results (Y/Y)Quarter Ended June 30, 2015 vs Quarter Ended June 30, 2014

5

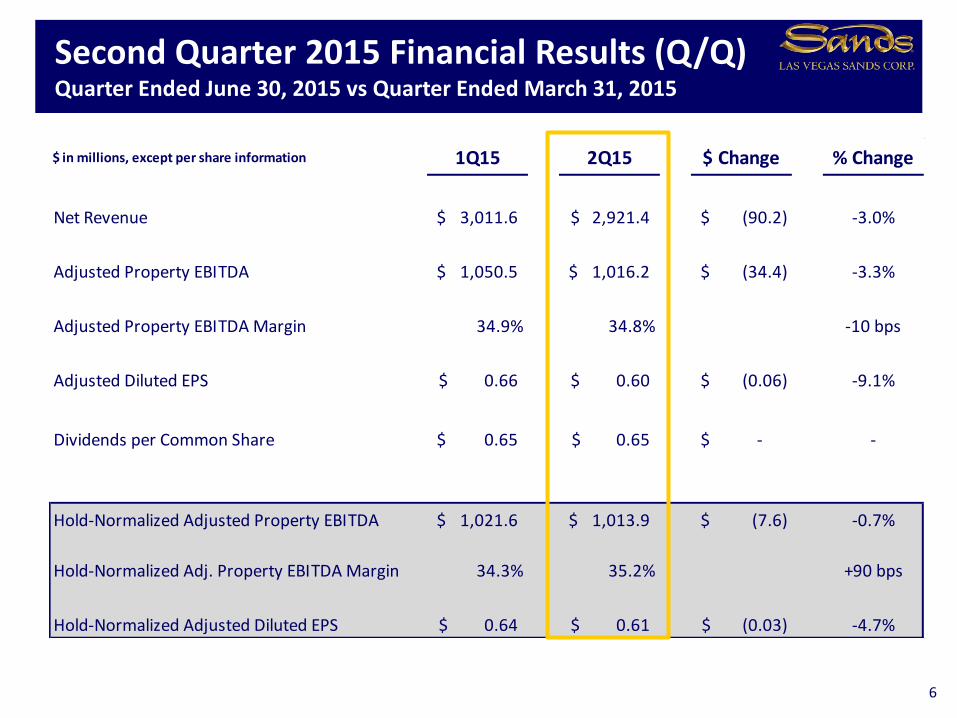

$ in millions, except per share information 1Q15 2Q15 $ Change % Change

Net Revenue 3,011.6$ 2,921.4$ (90.2)$ -3.0%

Adjusted Property EBITDA 1,050.5$ 1,016.2$ (34.4)$ -3.3%

Adjusted Property EBITDA Margin 34.9% 34.8% -10 bps

Adjusted Diluted EPS 0.66$ 0.60$ (0.06)$ -9.1%

Dividends per Common Share 0.65$ 0.65$ -$ -

Hold-Normalized Adjusted Property EBITDA 1,021.6$ 1,013.9$ (7.6)$ -0.7%

Hold-Normalized Adj. Property EBITDA Margin 34.3% 35.2% +90 bps

Hold-Normalized Adjusted Diluted EPS 0.64$ 0.61$ (0.03)$ -4.7%

Second Quarter 2015 Financial Results (Q/Q)Quarter Ended June 30, 2015 vs Quarter Ended March 31, 2015

6

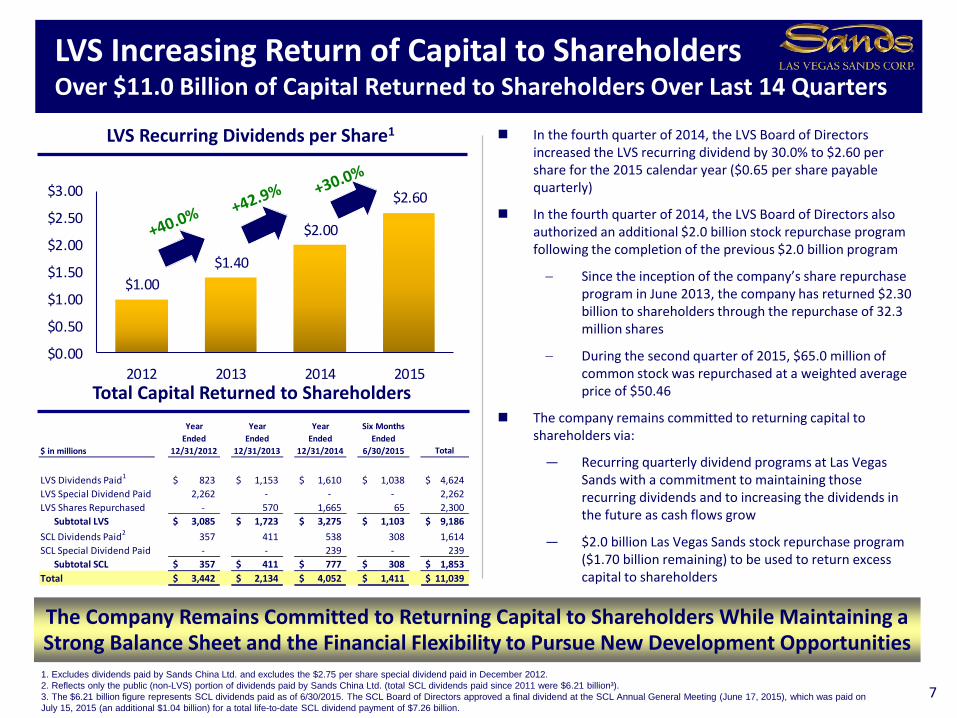

Year Year Year Six Months

Ended Ended Ended Ended

$ in millions 12/31/2012 12/31/2013 12/31/2014 6/30/2015 Total

LVS Dividends Paid1 823$ 1,153$ 1,610$ 1,038$ 4,624$

LVS Special Dividend Paid 2,262 - - - 2,262

LVS Shares Repurchased - 570 1,665 65 2,300

Subtotal LVS 3,085$ 1,723$ 3,275$ 1,103$ 9,186$

SCL Dividends Paid2 357 411 538 308 1,614

SCL Special Dividend Paid - - 239 - 239

Subtotal SCL 357$ 411$ 777$ 308$ 1,853$

Total 3,442$ 2,134$ 4,052$ 1,411$ 11,039$

$1.00

$1.40

$2.00

$2.60

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2012 2013 2014 2015

7

LVS Increasing Return of Capital to ShareholdersOver $11.0 Billion of Capital Returned to Shareholders Over Last 14 Quarters

LVS Recurring Dividends per Share1 In the fourth quarter of 2014, the LVS Board of Directors increased the LVS recurring dividend by 30.0% to $2.60 per share for the 2015 calendar year ($0.65 per share payable quarterly)

In the fourth quarter of 2014, the LVS Board of Directors also authorized an additional $2.0 billion stock repurchase program following the completion of the previous $2.0 billion program

Since the inception of the company’s share repurchase program in June 2013, the company has returned $2.30 billion to shareholders through the repurchase of 32.3 million shares

During the second quarter of 2015, $65.0 million of common stock was repurchased at a weighted average price of $50.46

The company remains committed to returning capital to shareholders via:

— Recurring quarterly dividend programs at Las Vegas Sands with a commitment to maintaining those recurring dividends and to increasing the dividends in the future as cash flows grow

— $2.0 billion Las Vegas Sands stock repurchase program ($1.70 billion remaining) to be used to return excess capital to shareholders

1. Excludes dividends paid by Sands China Ltd. and excludes the $2.75 per share special dividend paid in December 2012.

2. Reflects only the public (non-LVS) portion of dividends paid by Sands China Ltd. (total SCL dividends paid since 2011 were $6.21 billion³).

3. The $6.21 billion figure represents SCL dividends paid as of 6/30/2015. The SCL Board of Directors approved a final dividend at the SCL Annual General Meeting (June 17, 2015), which was paid on

July 15, 2015 (an additional $1.04 billion) for a total life-to-date SCL dividend payment of $7.26 billion.

The Company Remains Committed to Returning Capital to Shareholders While Maintaining aStrong Balance Sheet and the Financial Flexibility to Pursue New Development Opportunities

Total Capital Returned to Shareholders

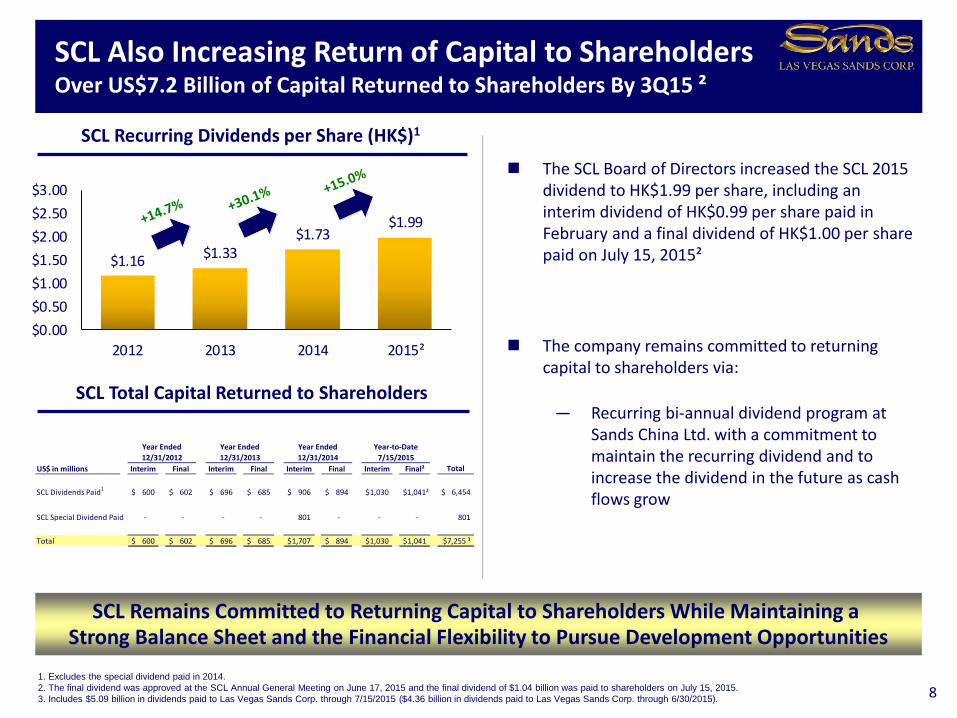

US$ in millions Interim Final Interim Final Interim Final Interim Final² Total

SCL Dividends Paid1

600$ 602$ 696$ 685$ 906$ 894$ 1,030$ $1,041² 6,454$

SCL Special Dividend Paid - - - - 801 - - - 801

Total 600$ 602$ 696$ 685$ 1,707$ 894$ 1,030$ 1,041$ $7,255 ³

Year-to-Date

7/15/201512/31/2012

Year Ended Year Ended Year Ended

12/31/2013 12/31/2014

$1.16$1.33

$1.73$1.99

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2012 2013 2014 2015²

8

SCL Also Increasing Return of Capital to ShareholdersOver US$7.2 Billion of Capital Returned to Shareholders By 3Q15 ²

SCL Recurring Dividends per Share (HK$)1

The SCL Board of Directors increased the SCL 2015 dividend to HK$1.99 per share, including an interim dividend of HK$0.99 per share paid in February and a final dividend of HK$1.00 per share paid on July 15, 2015²

The company remains committed to returning capital to shareholders via:

— Recurring bi-annual dividend program at Sands China Ltd. with a commitment to maintain the recurring dividend and to increase the dividend in the future as cash flows grow

1. Excludes the special dividend paid in 2014.

2. The final dividend was approved at the SCL Annual General Meeting on June 17, 2015 and the final dividend of $1.04 billion was paid to shareholders on July 15, 2015.

3. Includes $5.09 billion in dividends paid to Las Vegas Sands Corp. through 7/15/2015 ($4.36 billion in dividends paid to Las Vegas Sands Corp. through 6/30/2015).

SCL Remains Committed to Returning Capital to Shareholders While Maintaining a Strong Balance Sheet and the Financial Flexibility to Pursue Development Opportunities

SCL Total Capital Returned to Shareholders

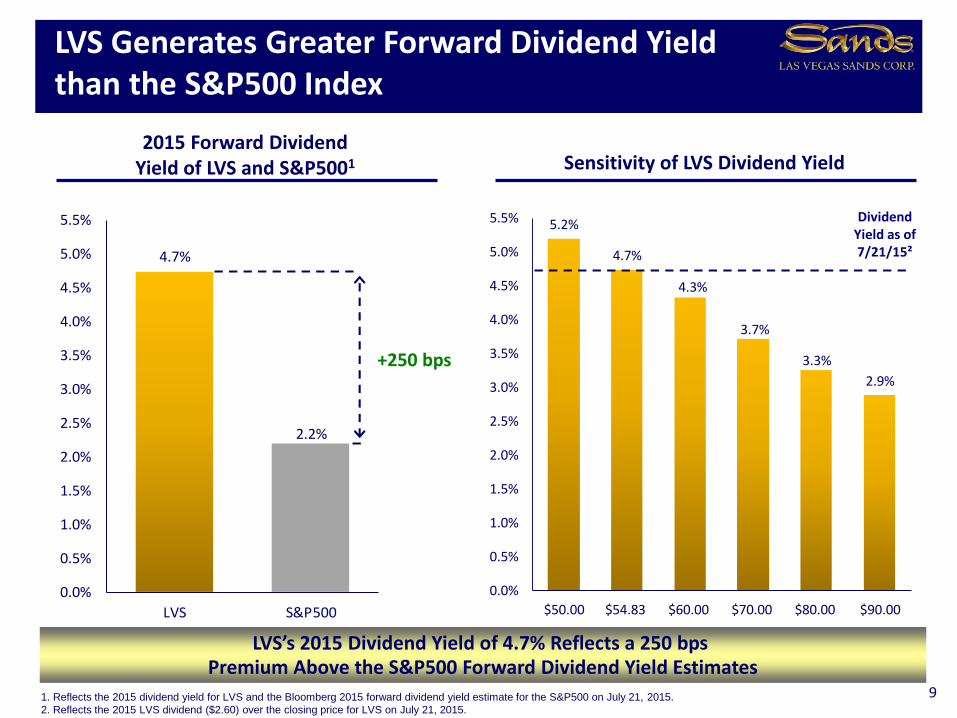

4.7%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

LVS S&P500

5.2%

4.7%

4.3%

3.7%

3.3%

2.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

$50.00 $54.83 $60.00 $70.00 $80.00 $90.00

LVS Generates Greater Forward Dividend Yield than the S&P500 Index

2015 Forward Dividend Yield of LVS and S&P5001

1. Reflects the 2015 dividend yield for LVS and the Bloomberg 2015 forward dividend yield estimate for the S&P500 on July 21, 2015.

2. Reflects the 2015 LVS dividend ($2.60) over the closing price for LVS on July 21, 2015.

LVS’s 2015 Dividend Yield of 4.7% Reflects a 250 bps Premium Above the S&P500 Forward Dividend Yield Estimates

Sensitivity of LVS Dividend Yield

Dividend Yield as of 7/21/15²

+250 bps

9

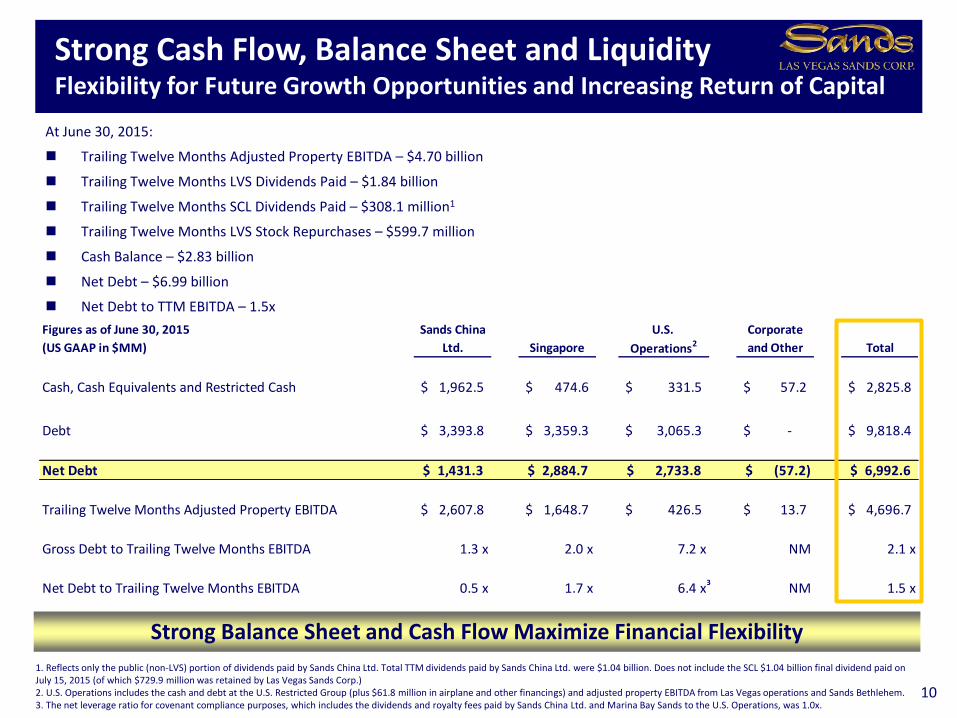

Figures as of June 30, 2015 Sands China U.S. Corporate

(US GAAP in $MM) Ltd. Singapore Operations2 and Other Total

Cash, Cash Equivalents and Restricted Cash 1,962.5$ 474.6$ 331.5$ 57.2$ 2,825.8$

Debt 3,393.8$ 3,359.3$ 3,065.3$ -$ 9,818.4$

Net Debt 1,431.3$ 2,884.7$ 2,733.8$ (57.2)$ 6,992.6$

Trailing Twelve Months Adjusted Property EBITDA 2,607.8$ 1,648.7$ 426.5$ 13.7$ 4,696.7$

Gross Debt to Trailing Twelve Months EBITDA 1.3 x 2.0 x 7.2 x NM 2.1 x

Net Debt to Trailing Twelve Months EBITDA 0.5 x 1.7 x 6.4 x NM 1.5 x

At June 30, 2015:

Trailing Twelve Months Adjusted Property EBITDA – $4.70 billion

Trailing Twelve Months LVS Dividends Paid – $1.84 billion

Trailing Twelve Months SCL Dividends Paid – $308.1 million1

Trailing Twelve Months LVS Stock Repurchases – $599.7 million

Cash Balance – $2.83 billion

Net Debt – $6.99 billion

Net Debt to TTM EBITDA – 1.5x

Strong Cash Flow, Balance Sheet and LiquidityFlexibility for Future Growth Opportunities and Increasing Return of Capital

10

1. Reflects only the public (non-LVS) portion of dividends paid by Sands China Ltd. Total TTM dividends paid by Sands China Ltd. were $1.04 billion. Does not include the SCL $1.04 billion final dividend paid on July 15, 2015 (of which $729.9 million was retained by Las Vegas Sands Corp.)2. U.S. Operations includes the cash and debt at the U.S. Restricted Group (plus $61.8 million in airplane and other financings) and adjusted property EBITDA from Las Vegas operations and Sands Bethlehem.3. The net leverage ratio for covenant compliance purposes, which includes the dividends and royalty fees paid by Sands China Ltd. and Marina Bay Sands to the U.S. Operations, was 1.0x.

Strong Balance Sheet and Cash Flow Maximize Financial Flexibility

3

$801.3

$559.8

$752.5

$526.534.0%

32.2% 33.3%31.7%

0%

10%

20%

30%

40%

50%

60%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2Q14 2Q15 2Q14 2Q15

Macao Operating Performance (Y/Y)Quarter Ended June 30, 2015 vs Quarter Ended June 30, 2014

11

($MM)

Macao Property Operations Adjusted Property EBITDA and Adjusted Property EBITDA Margin

Actual Hold-Normalized

-30.0%-30.1%

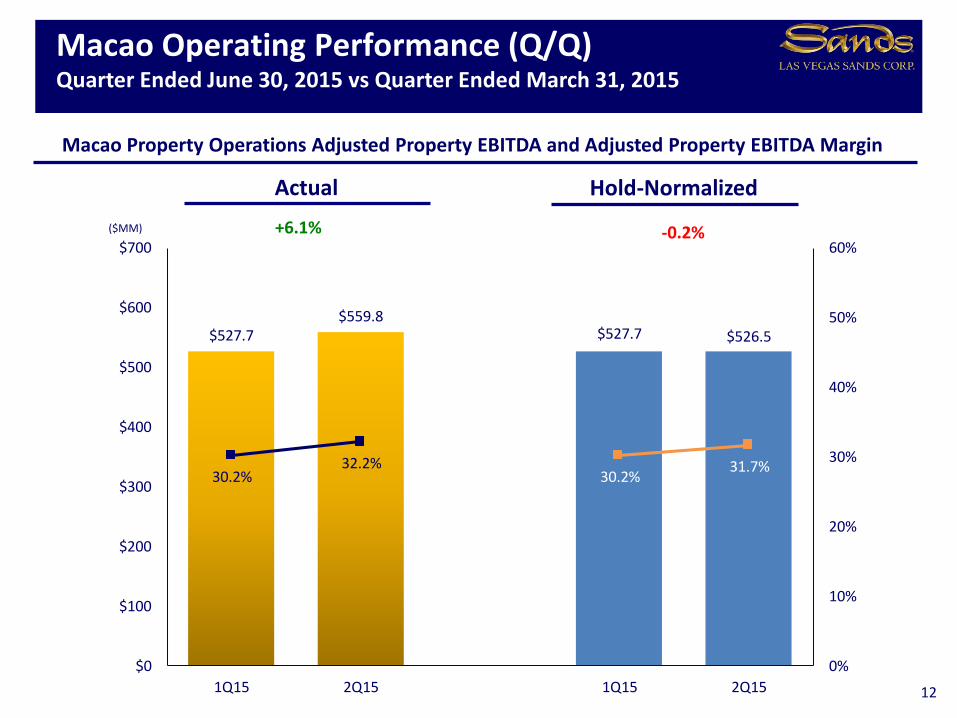

$527.7$559.8

$527.7 $526.5

30.2%32.2%

30.2%31.7%

0%

10%

20%

30%

40%

50%

60%

$0

$100

$200

$300

$400

$500

$600

$700

1Q15 2Q15 1Q15 2Q15

Macao Operating Performance (Q/Q)Quarter Ended June 30, 2015 vs Quarter Ended March 31, 2015

12

($MM)

Macao Property Operations Adjusted Property EBITDA and Adjusted Property EBITDA Margin

Actual Hold-Normalized

-0.2%+6.1%

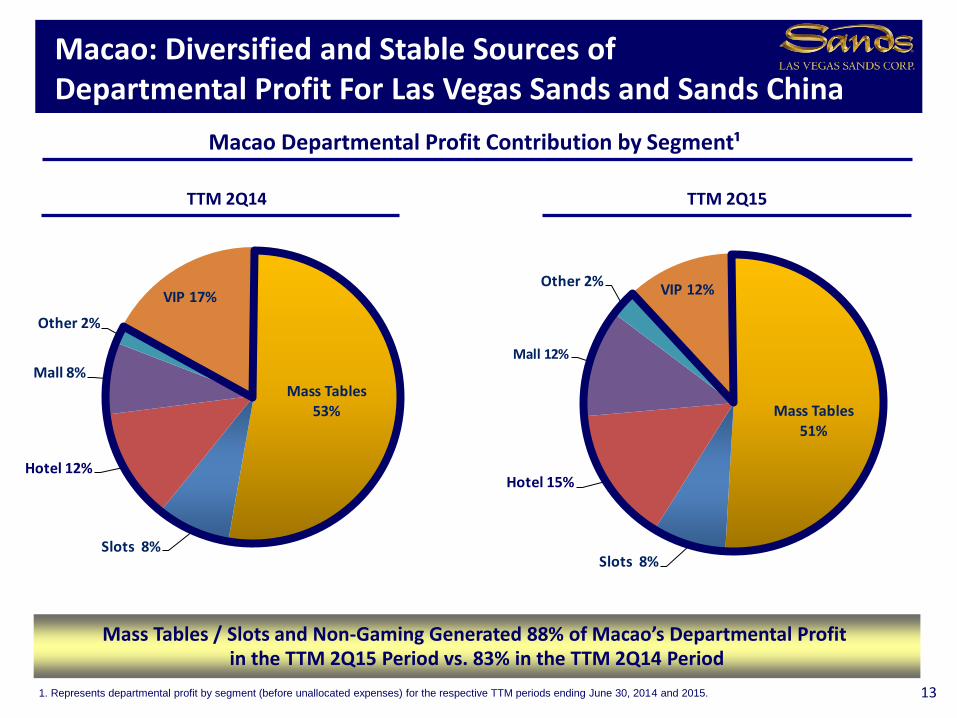

Mass Tables53%

Slots 8%

Hotel 12%

Mall 8%

Other 2%

VIP 17%

Mass Tables51%

Slots 8%

Hotel 15%

Mall 12%

Other 2%VIP 12%

TTM 2Q14

Macao: Diversified and Stable Sources of Departmental Profit For Las Vegas Sands and Sands China

13

Mass Tables / Slots and Non-Gaming Generated 88% of Macao’s Departmental Profit in the TTM 2Q15 Period vs. 83% in the TTM 2Q14 Period

Macao Departmental Profit Contribution by Segment¹

TTM 2Q15

1. Represents departmental profit by segment (before unallocated expenses) for the respective TTM periods ending June 30, 2014 and 2015.

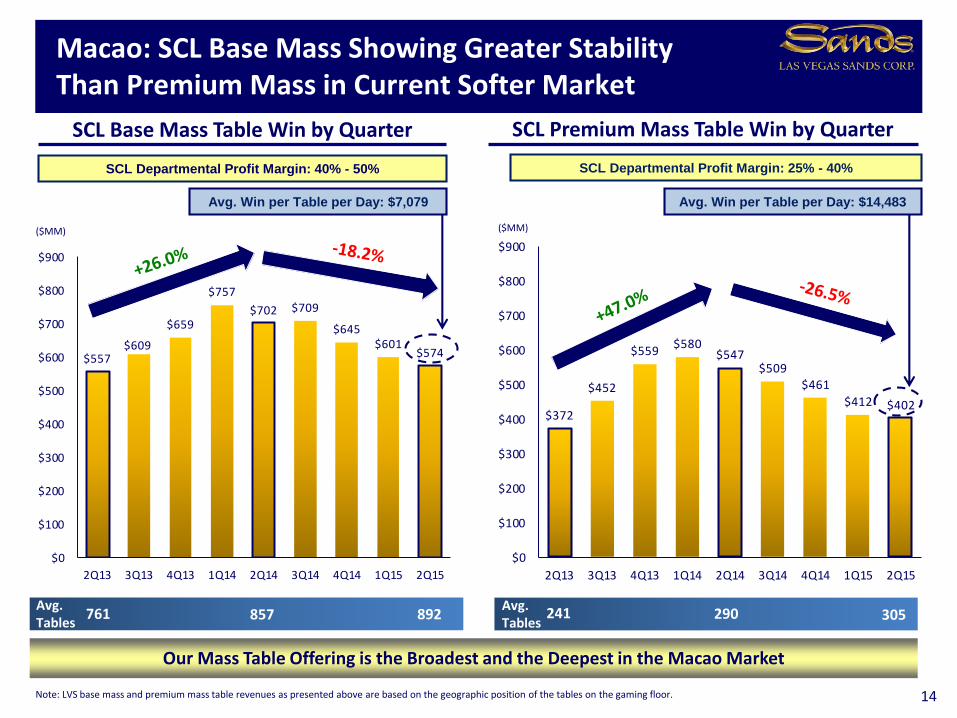

$372

$452

$559$580

$547$509

$461

$412 $402

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

$557$609

$659

$757

$702 $709

$645$601

$574

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

14

SCL Base Mass Table Win by Quarter

Macao: SCL Base Mass Showing Greater Stability Than Premium Mass in Current Softer Market

Note: LVS base mass and premium mass table revenues as presented above are based on the geographic position of the tables on the gaming floor.

Our Mass Table Offering is the Broadest and the Deepest in the Macao Market

($MM)

SCL Premium Mass Table Win by Quarter

SCL Departmental Profit Margin: 40% - 50% SCL Departmental Profit Margin: 25% - 40%

($MM)

241Avg.Tables

290 305761Avg.Tables

857 892

Avg. Win per Table per Day: $7,079 Avg. Win per Table per Day: $14,483

Executing Our Mass Strategy in Macao

Expansion of Mass Market

Offerings Underway with The Parisian

Family-friendly Entertainment World Class Concerts, Sporting Events

and Other Entertainment Offerings

Over 1.5 million sq. feet

of World Class Shopping

Market-Leading Customer Database

Highly Themed Tourism Attractions

Portfolio of Nearly

9,300 Suites and Hotel Rooms

Over 2 million sq. feet of Conference,

Exhibition and Carpeted Meeting Space

The Broadest

and Deepest

Mass

Tourism

Offerings

in Macao

Our Diversified Convention-based Integrated Resort Offerings Appeal to the Broadest Set of Customers and Comprise a Unique Competitive Advantage in the Macao Market 15

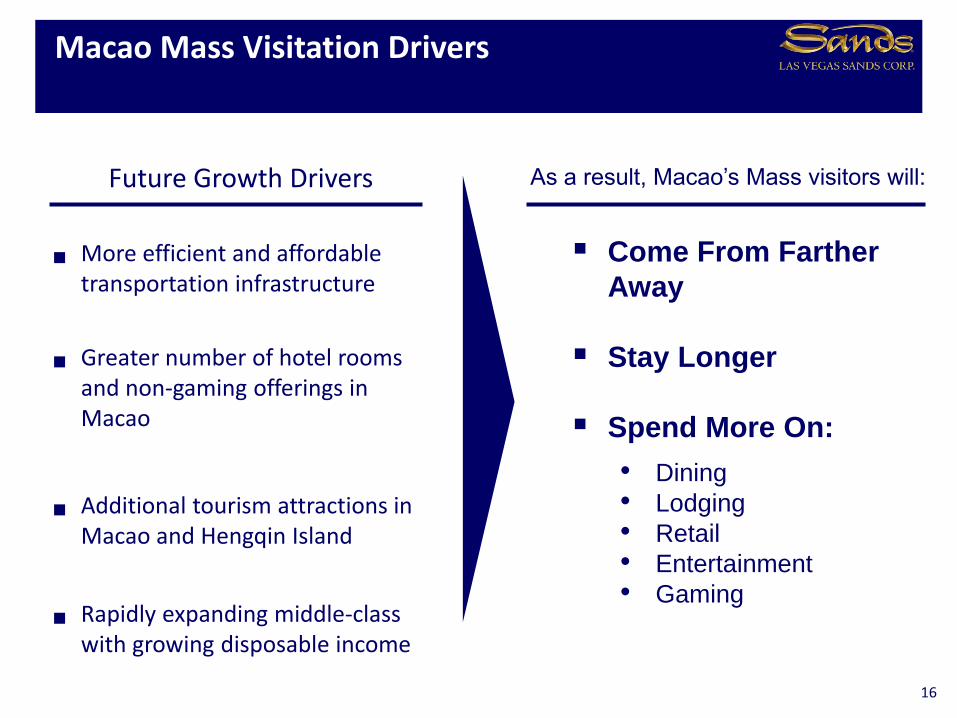

Macao Mass Visitation Drivers

Future Growth Drivers

More efficient and affordable transportation infrastructure

Greater number of hotel rooms and non-gaming offerings in Macao

Additional tourism attractions in Macao and Hengqin Island

Rapidly expanding middle-class with growing disposable income

16

As a result, Macao’s Mass visitors will:

Come From Farther

Away

Stay Longer

Spend More On:

• Dining

• Lodging

• Retail

• Entertainment

• Gaming

Xinjiang

Tibet

Qinghai

SichuanChongqing

Henan

Hubei

ShanxiHebei

Shandong

Beijing

Liaoning

Jilin

Heilongjiang

Jiangsu

Anhui

Hunan Jiangxi

Zhejiang

Guangxi

Guizhou

Yunnan

Ningxia

Shaanxi

Inner Mongolia

Gansu

Guangdong

Fujian

Shanghai

Tianjin

Hong Kong

Macao

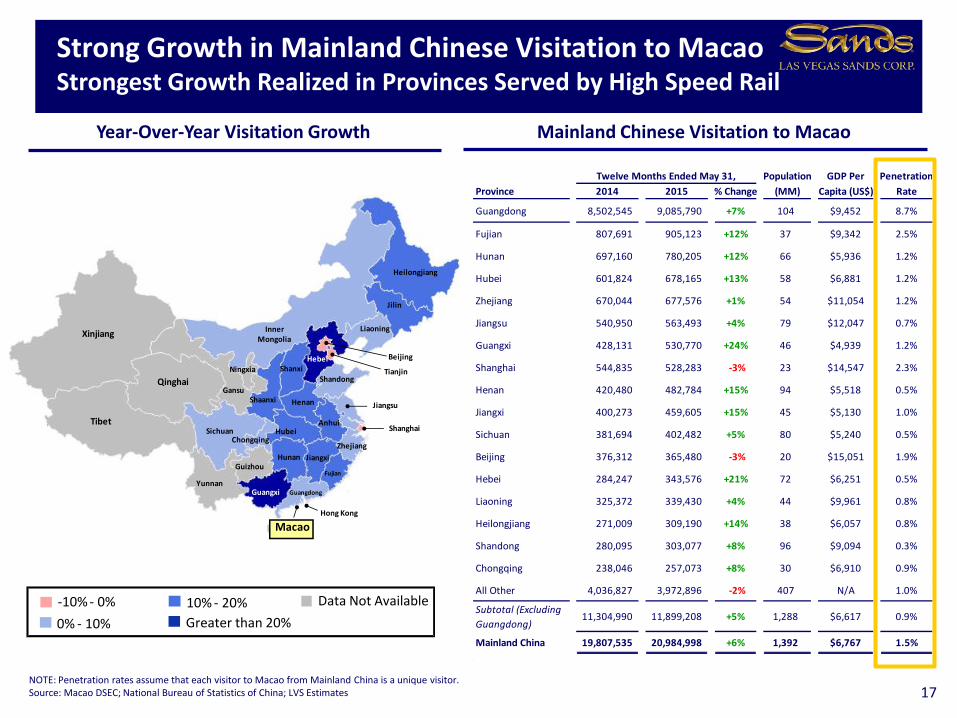

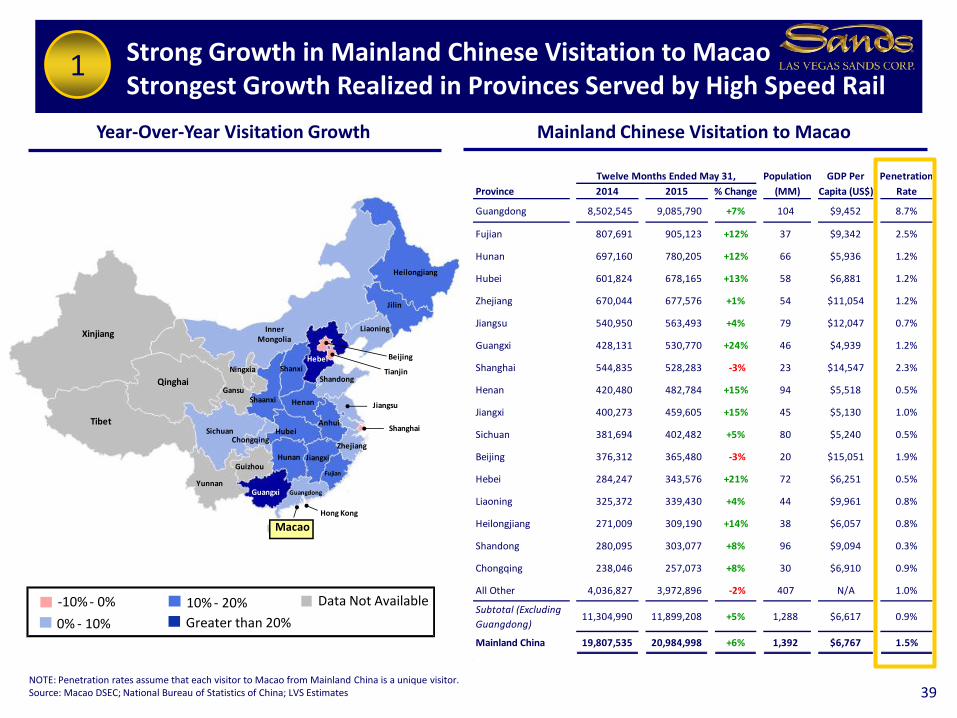

Twelve Months Ended May 31, Population GDP Per Penetration

Province 2014 2015 % Change (MM) Capita (US$) Rate

Guangdong 8,502,545 9,085,790 +7% 104 $9,452 8.7%

Fujian 807,691 905,123 +12% 37 $9,342 2.5%

Hunan 697,160 780,205 +12% 66 $5,936 1.2%

Hubei 601,824 678,165 +13% 58 $6,881 1.2%

Zhejiang 670,044 677,576 +1% 54 $11,054 1.2%

Jiangsu 540,950 563,493 +4% 79 $12,047 0.7%

Guangxi 428,131 530,770 +24% 46 $4,939 1.2%

Shanghai 544,835 528,283 -3% 23 $14,547 2.3%

Henan 420,480 482,784 +15% 94 $5,518 0.5%

Jiangxi 400,273 459,605 +15% 45 $5,130 1.0%

Sichuan 381,694 402,482 +5% 80 $5,240 0.5%

Beijing 376,312 365,480 -3% 20 $15,051 1.9%

Hebei 284,247 343,576 +21% 72 $6,251 0.5%

Liaoning 325,372 339,430 +4% 44 $9,961 0.8%

Heilongjiang 271,009 309,190 +14% 38 $6,057 0.8%

Shandong 280,095 303,077 +8% 96 $9,094 0.3%

Chongqing 238,046 257,073 +8% 30 $6,910 0.9%

All Other 4,036,827 3,972,896 -2% 407 N/A 1.0%

Subtotal (Excluding

Guangdong)11,304,990 11,899,208 +5% 1,288 $6,617 0.9%

Mainland China 19,807,535 20,984,998 +6% 1,392 $6,767 1.5%

17NOTE: Penetration rates assume that each visitor to Macao from Mainland China is a unique visitor.Source: Macao DSEC; National Bureau of Statistics of China; LVS Estimates

Year-Over-Year Visitation Growth Mainland Chinese Visitation to Macao

Greater than 20%

Data Not Available-10% - 0%

0% - 10%

10% - 20%

Strong Growth in Mainland Chinese Visitation to MacaoStrongest Growth Realized in Provinces Served by High Speed Rail

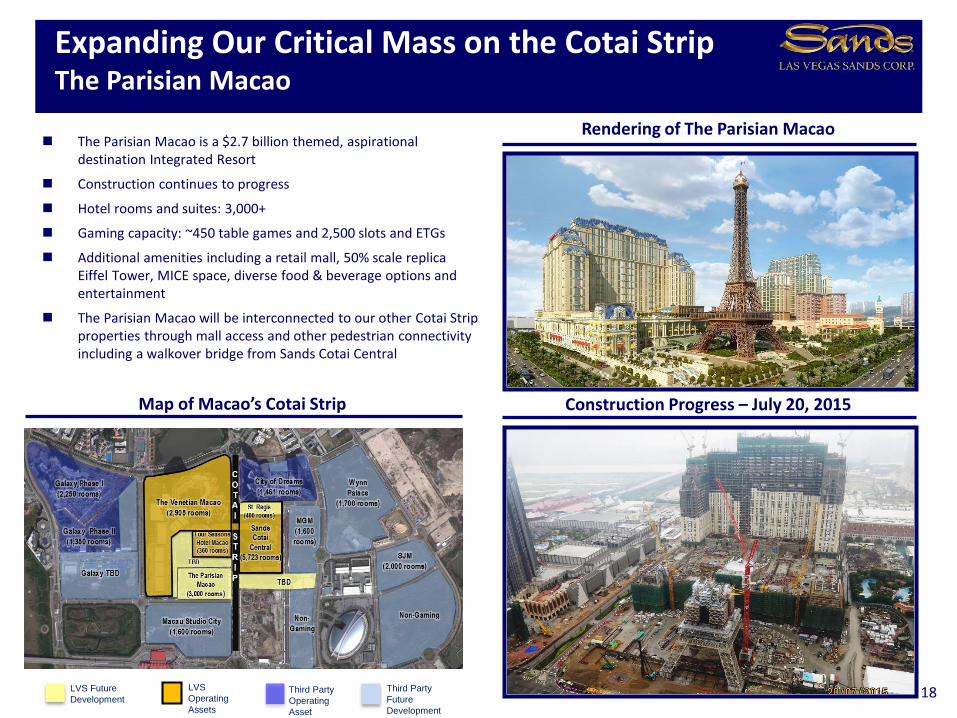

Expanding Our Critical Mass on the Cotai StripThe Parisian Macao

18LVS

Operating

Assets

Third Party

Operating

Asset

Third Party

Future

Development

Construction Progress – July 20, 2015Map of Macao’s Cotai Strip

The Parisian Macao is a $2.7 billion themed, aspirational destination Integrated Resort

Construction continues to progress

Hotel rooms and suites: 3,000+

Gaming capacity: ~450 table games and 2,500 slots and ETGs

Additional amenities including a retail mall, 50% scale replica Eiffel Tower, MICE space, diverse food & beverage options and entertainment

The Parisian Macao will be interconnected to our other Cotai Strip properties through mall access and other pedestrian connectivity including a walkover bridge from Sands Cotai Central

Rendering of The Parisian Macao

LVS Future

Development

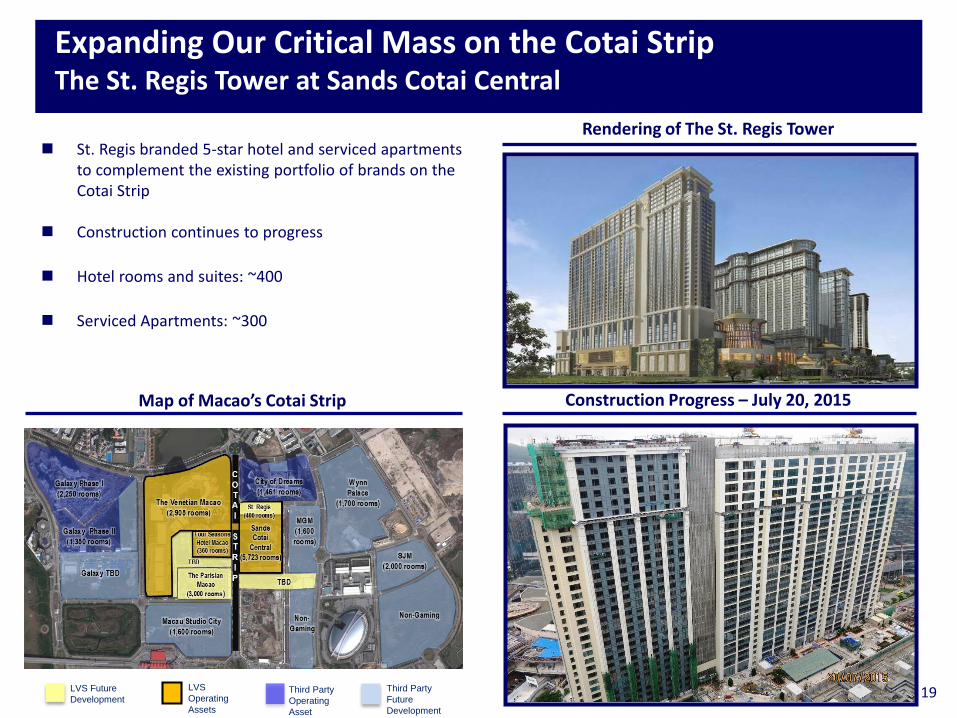

Expanding Our Critical Mass on the Cotai StripThe St. Regis Tower at Sands Cotai Central

19

Construction Progress – July 20, 2015Map of Macao’s Cotai Strip

St. Regis branded 5-star hotel and serviced apartments to complement the existing portfolio of brands on the Cotai Strip

Construction continues to progress

Hotel rooms and suites: ~400

Serviced Apartments: ~300

Rendering of The St. Regis Tower

LVS

Operating

Assets

Third Party

Operating

Asset

Third Party

Future

Development

LVS Future

Development

18% 18% 18%

14% 15% 14%

14% 12% 11%

16% 14%13%

10%9%

10%

0%

20%

40%

60%

80%

2012 2013 TTM 1Q15

28%32%

34%

0%

10%

20%

30%

40%

2012 2013 TTM 1Q15

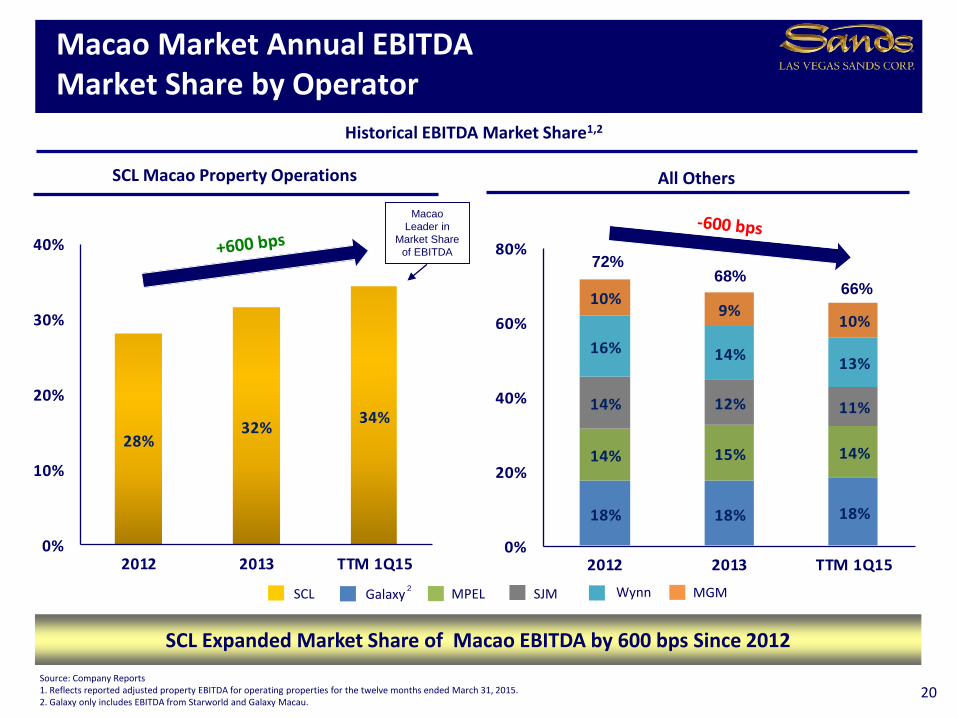

Macao Market Annual EBITDA Market Share by Operator

SCL Expanded Market Share of Macao EBITDA by 600 bps Since 2012

Source: Company Reports1. Reflects reported adjusted property EBITDA for operating properties for the twelve months ended March 31, 2015.2. Galaxy only includes EBITDA from Starworld and Galaxy Macau.

Historical EBITDA Market Share1,2

20

Galaxy MPELSCL2

SJM Wynn MGM

SCL Macao Property Operations All Others

Macao

Leader in

Market Share

of EBITDA72%

68%66%

$3.02 $3.16

$1.66 $1.57

$4.68 $4.73

$0.0

$2.0

$4.0

$6.0

2Q14 2Q15

Non-Rolling Tables Slot Machines

$417.8$363.3 $368.5 $363.3

51.9% 50.9% 49.6% 50.9%

20%

30%

40%

50%

60%

70%

80%

$0

$100

$200

$300

$400

$500

$600

2Q14 2Q15 2Q14 2Q15

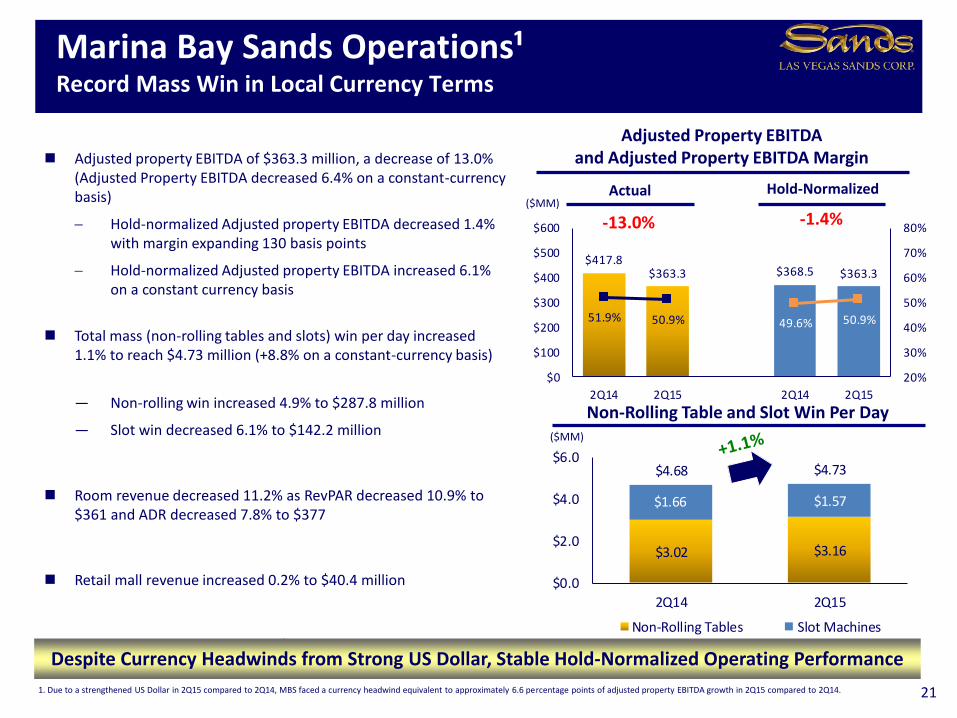

Marina Bay Sands Operations¹Record Mass Win in Local Currency Terms

21

Actual

Adjusted property EBITDA of $363.3 million, a decrease of 13.0% (Adjusted Property EBITDA decreased 6.4% on a constant-currency basis)

Hold-normalized Adjusted property EBITDA decreased 1.4% with margin expanding 130 basis points

Hold-normalized Adjusted property EBITDA increased 6.1% on a constant currency basis

Total mass (non-rolling tables and slots) win per day increased 1.1% to reach $4.73 million (+8.8% on a constant-currency basis)

— Non-rolling win increased 4.9% to $287.8 million

— Slot win decreased 6.1% to $142.2 million

Room revenue decreased 11.2% as RevPAR decreased 10.9% to $361 and ADR decreased 7.8% to $377

Retail mall revenue increased 0.2% to $40.4 million

Rolling win decreased 26.6% to $264.5 million (rolling volume decreased 9.0% to $9.51 billion)

($MM)

($MM)

Adjusted Property EBITDA and Adjusted Property EBITDA Margin

Despite Currency Headwinds from Strong US Dollar, Stable Hold-Normalized Operating Performance

Non-Rolling Table and Slot Win Per Day

Hold-Normalized

1. Due to a strengthened US Dollar in 2Q15 compared to 2Q14, MBS faced a currency headwind equivalent to approximately 6.6 percentage points of adjusted property EBITDA growth in 2Q15 compared to 2Q14.

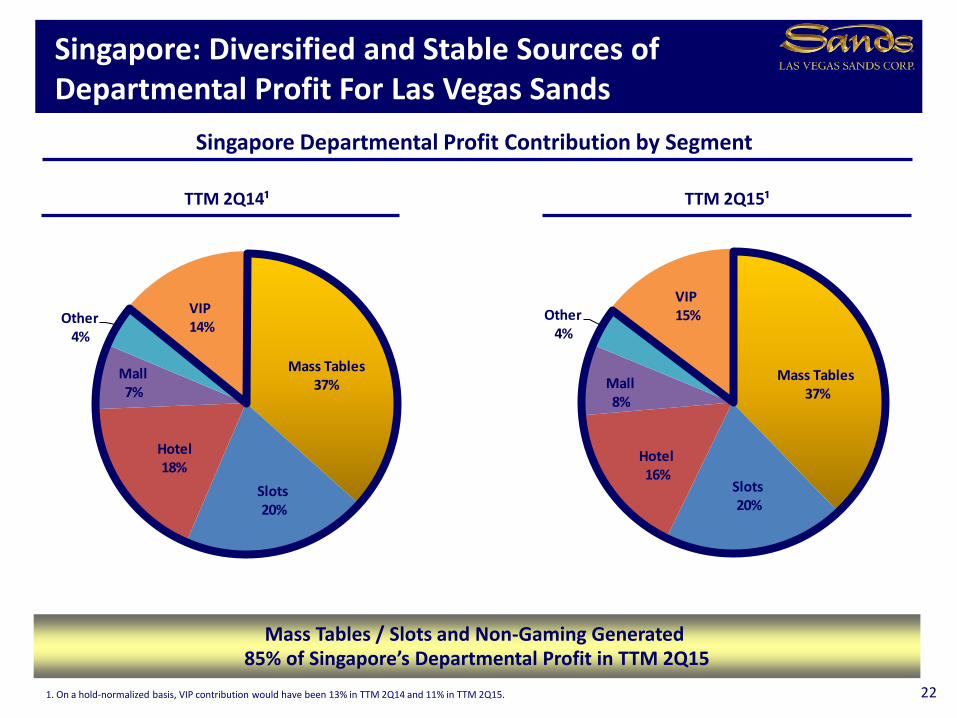

VIP15%

Mass Tables37%

Slots20%

Hotel16%

Mall8%

Other4%

VIP14%

Mass Tables37%

Slots20%

Hotel18%

Mall7%

Other4%

TTM 2Q14¹

Singapore: Diversified and Stable Sources of Departmental Profit For Las Vegas Sands

22

Mass Tables / Slots and Non-Gaming Generated 85% of Singapore’s Departmental Profit in TTM 2Q15

Singapore Departmental Profit Contribution by Segment

TTM 2Q15¹

1. On a hold-normalized basis, VIP contribution would have been 13% in TTM 2Q14 and 11% in TTM 2Q15.

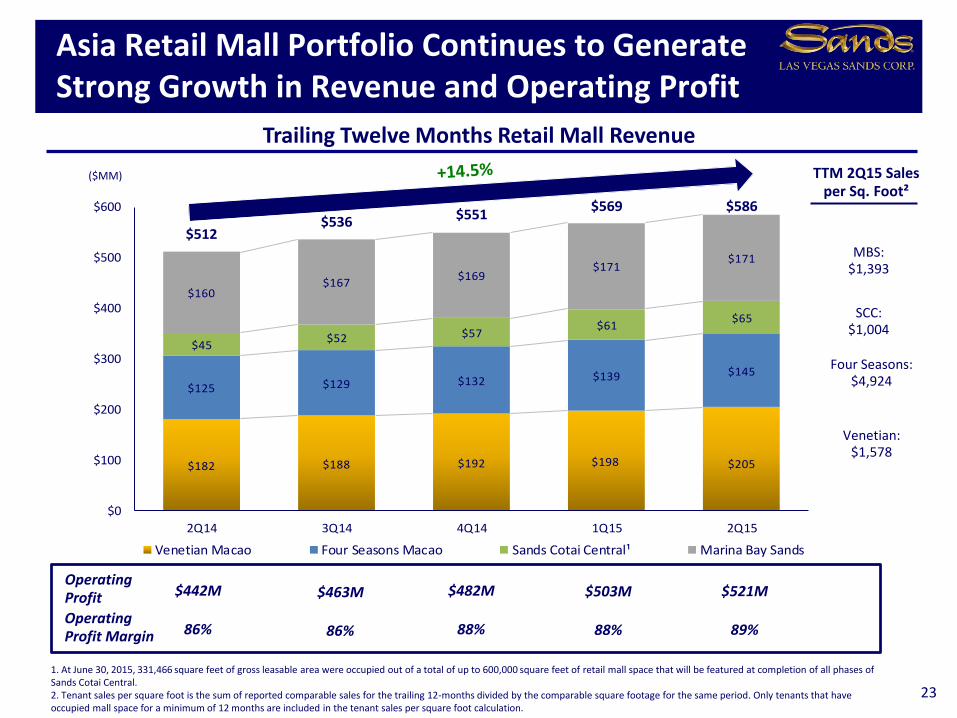

$182 $188 $192 $198 $205

$125 $129 $132 $139 $145

$45$52 $57

$61$65

$160$167

$169$171

$171

$512$536 $551

$569 $586

$0

$100

$200

$300

$400

$500

$600

2Q14 3Q14 4Q14 1Q15 2Q15

Venetian Macao Four Seasons Macao Sands Cotai Central¹ Marina Bay Sands

Asia Retail Mall Portfolio Continues to Generate Strong Growth in Revenue and Operating Profit

23

($MM)

Trailing Twelve Months Retail Mall Revenue

88% 89%86% 86%Operating Profit Margin 88%

1. At June 30, 2015, 331,466 square feet of gross leasable area were occupied out of a total of up to 600,000 square feet of retail mall space that will be featured at completion of all phases of Sands Cotai Central. 2. Tenant sales per square foot is the sum of reported comparable sales for the trailing 12-months divided by the comparable square footage for the same period. Only tenants that have occupied mall space for a minimum of 12 months are included in the tenant sales per square foot calculation.

$503M $521M$442M $463MOperating Profit $482M

TTM 2Q15 Sales per Sq. Foot²

MBS:$1,393

SCC:$1,004

Four Seasons:$4,924

Venetian:$1,578

South Korea

Principal Areas of Future Development Interest for Las Vegas Sands

Japan

As the global leader in Integrated Resort development and operation, Las Vegas Sands is uniquely positioned to bring its unmatched track record and powerful convention-based business model to the world’s most promising Integrated Resort development opportunities

Development opportunity parameters:

— Targeting minimum of 20% return on total invested capital

— 25% - 35% of total project costs to be funded with equity (project financing to fund 65% - 75% of total project costs)

Disciplined Execution of Our Global Growth Strategy

24

Macao

The Parisian Macao

St. Regis Tower atSands Cotai Central

Appendix

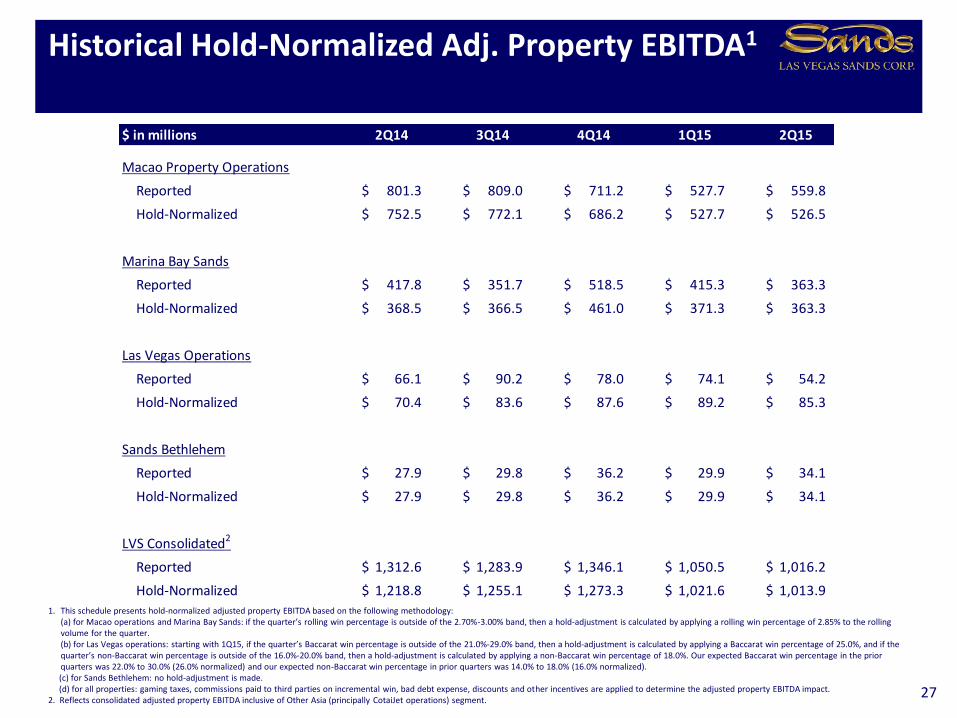

$ in millions 2Q14 3Q14 4Q14 1Q15 2Q15

Macao Property Operations

Reported 801.3$ 809.0$ 711.2$ 527.7$ 559.8$

Hold-Normalized 752.5$ 772.1$ 686.2$ 527.7$ 526.5$

Marina Bay Sands

Reported 417.8$ 351.7$ 518.5$ 415.3$ 363.3$

Hold-Normalized 368.5$ 366.5$ 461.0$ 371.3$ 363.3$

Las Vegas Operations

Reported 66.1$ 90.2$ 78.0$ 74.1$ 54.2$

Hold-Normalized 70.4$ 83.6$ 87.6$ 89.2$ 85.3$

Sands Bethlehem

Reported 27.9$ 29.8$ 36.2$ 29.9$ 34.1$

Hold-Normalized 27.9$ 29.8$ 36.2$ 29.9$ 34.1$

LVS Consolidated2

Reported 1,312.6$ 1,283.9$ 1,346.1$ 1,050.5$ 1,016.2$

Hold-Normalized 1,218.8$ 1,255.1$ 1,273.3$ 1,021.6$ 1,013.9$

Historical Hold-Normalized Adj. Property EBITDA1

27

1. This schedule presents hold-normalized adjusted property EBITDA based on the following methodology:(a) for Macao operations and Marina Bay Sands: if the quarter’s rolling win percentage is outside of the 2.70%-3.00% band, then a hold-adjustment is calculated by applying a rolling win percentage of 2.85% to the rolling volume for the quarter.(b) for Las Vegas operations: starting with 1Q15, if the quarter’s Baccarat win percentage is outside of the 21.0%-29.0% band, then a hold-adjustment is calculated by applying a Baccarat win percentage of 25.0%, and if the quarter’s non-Baccarat win percentage is outside of the 16.0%-20.0% band, then a hold-adjustment is calculated by applying a non-Baccarat win percentage of 18.0%. Our expected Baccarat win percentage in the prior quarters was 22.0% to 30.0% (26.0% normalized) and our expected non-Baccarat win percentage in prior quarters was 14.0% to 18.0% (16.0% normalized).(c) for Sands Bethlehem: no hold-adjustment is made.(d) for all properties: gaming taxes, commissions paid to third parties on incremental win, bad debt expense, discounts and other incentives are applied to determine the adjusted property EBITDA impact.

2. Reflects consolidated adjusted property EBITDA inclusive of Other Asia (principally CotaiJet operations) segment.

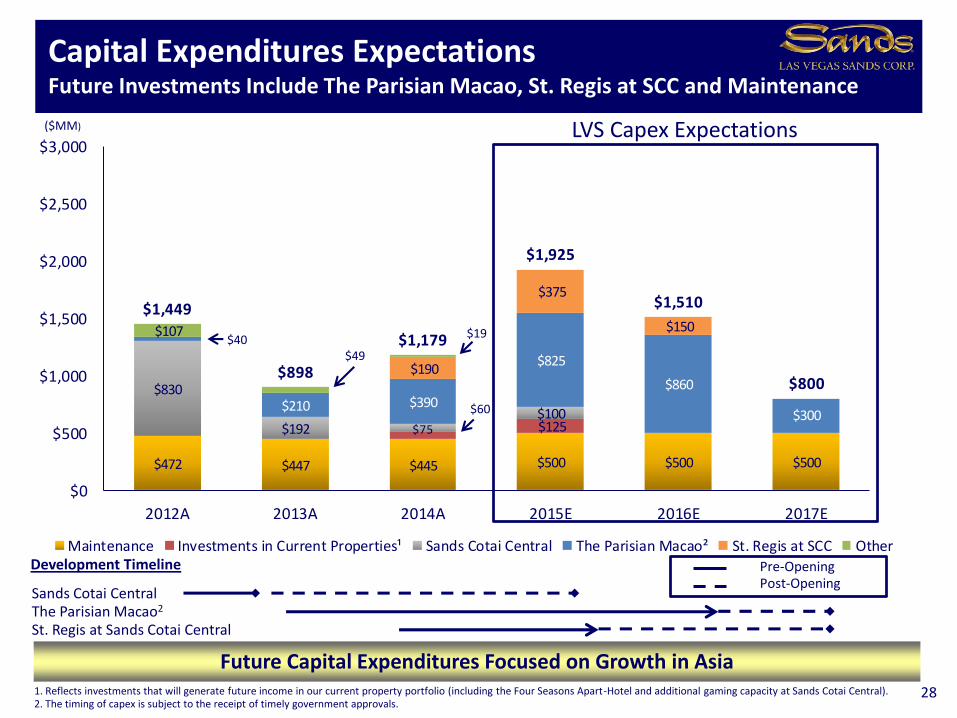

$472 $447 $445 $500 $500 $500

$125

$830

$192 $75$100

$210 $390

$825

$860

$300

$190

$375

$150 $107

$1,449

$898

$1,179

$1,925

$1,510

$800

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2012A 2013A 2014A 2015E 2016E 2017E

Maintenance Investments in Current Properties¹ Sands Cotai Central The Parisian Macao² St. Regis at SCC Other

Capital Expenditures ExpectationsFuture Investments Include The Parisian Macao, St. Regis at SCC and Maintenance

Future Capital Expenditures Focused on Growth in Asia

($MM)

1. Reflects investments that will generate future income in our current property portfolio (including the Four Seasons Apart-Hotel and additional gaming capacity at Sands Cotai Central). 2. The timing of capex is subject to the receipt of timely government approvals.

Sands Cotai CentralThe Parisian Macao2

St. Regis at Sands Cotai Central

LVS Capex Expectations

Development Timeline Pre-OpeningPost-Opening

28

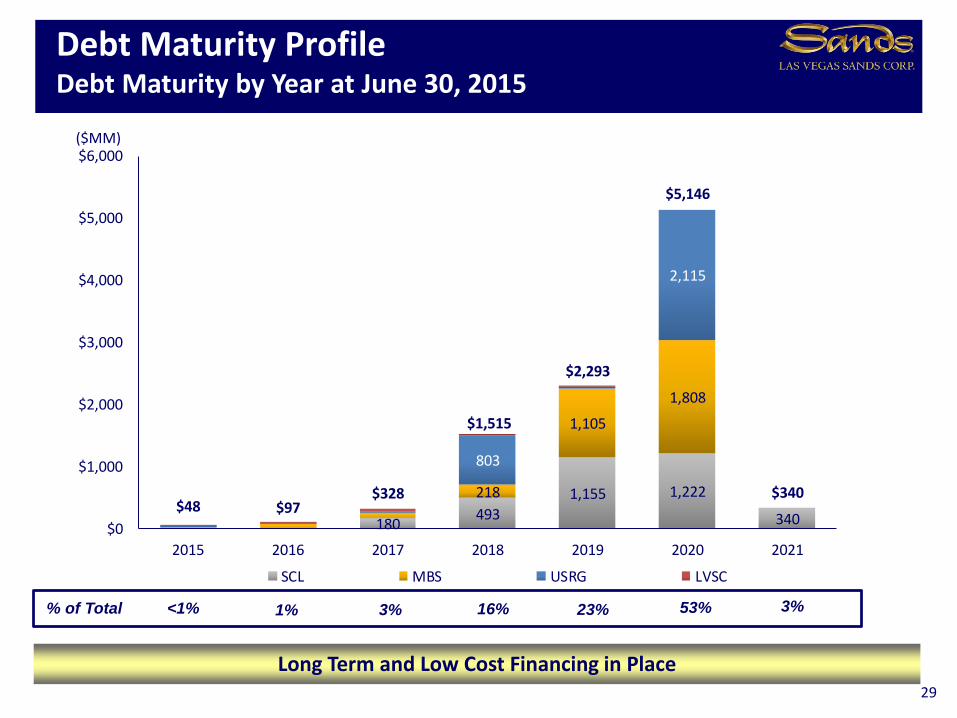

$40$49

$60

$19

180 493

1,155 1,222

340

218

1,105

1,808

803

2,115

$48 $97$328

$1,515

$2,293

$5,146

$340

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

2015 2016 2017 2018 2019 2020 2021

SCL MBS USRG LVSC

Debt Maturity ProfileDebt Maturity by Year at June 30, 2015

Long Term and Low Cost Financing in Place

($MM)

<1% 1% 16%% of Total 3% 23% 53%

29

3%

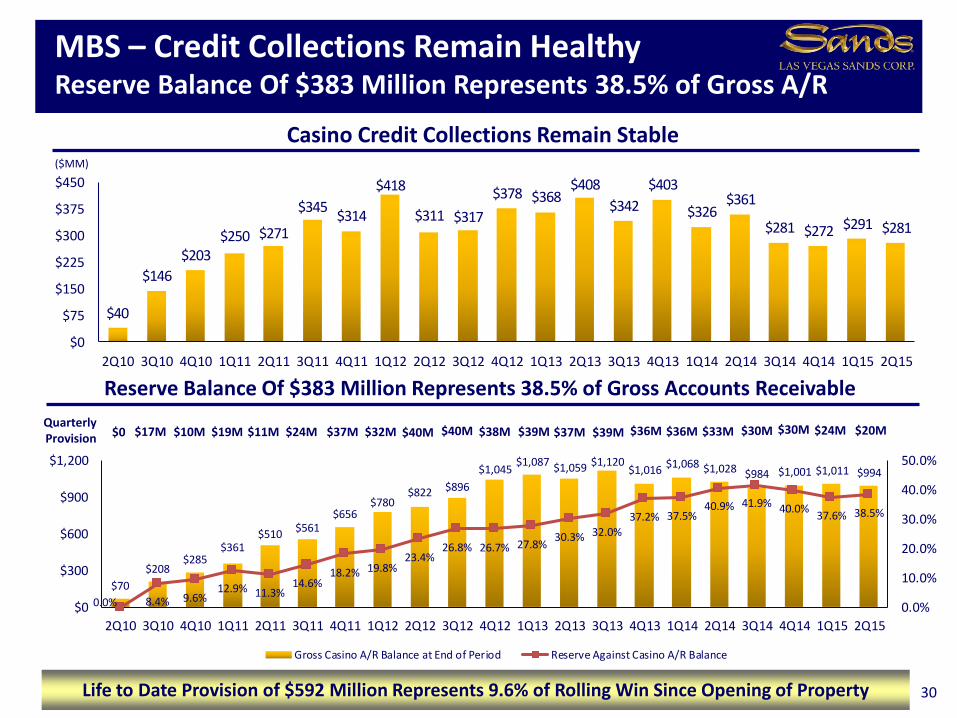

$70

$208$285

$361$510

$561$656

$780$822 $896

$1,045$1,087 $1,059 $1,120

$1,016$1,068 $1,028 $984 $1,001 $1,011 $994

0.0% 8.4% 9.6%12.9% 11.3%

14.6%18.2% 19.8%

23.4%26.8% 26.7% 27.8%

30.3% 32.0%

37.2% 37.5%40.9% 41.9% 40.0%

37.6% 38.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

$0

$300

$600

$900

$1,200

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Gross Casino A/R Balance at End of Period Reserve Against Casino A/R Balance

$40

$146

$203$250 $271

$345$314

$418

$311 $317

$378 $368$408

$342

$403

$326$361

$281 $272 $291 $281

$0

$75

$150

$225

$300

$375

$450

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

MBS – Credit Collections Remain Healthy Reserve Balance Of $383 Million Represents 38.5% of Gross A/R

30

($MM)

Reserve Balance Of $383 Million Represents 38.5% of Gross Accounts Receivable

Casino Credit Collections Remain Stable

$0Quarterly Provision

$17M $24M $37M $32M $40M $40M$11M$19M$10M

Life to Date Provision of $592 Million Represents 9.6% of Rolling Win Since Opening of Property

$38M $39M $37M $39M $36M $36M $33M $30M $30M $24M $20M

$252 $225

$188 $242

$440 $467

$0

$100

$200

$300

$400

$500

$600

$700

2Q14 2Q15

Baccarat Non-Baccarat

$66.1

$54.2

$70.4

$85.3

18.7%15.7%

19.6%22.2%

0%

10%

20%

30%

40%

$0

$20

$40

$60

$80

$100

2Q14 2Q15 2Q14 2Q15

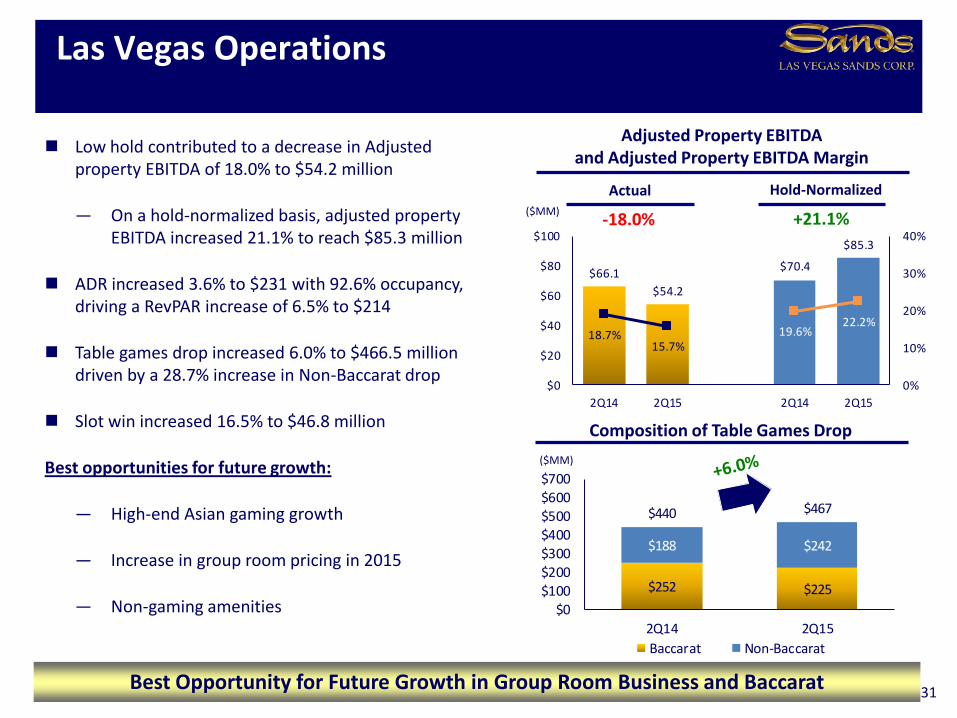

Las Vegas Operations

31

Composition of Table Games Drop

Low hold contributed to a decrease in Adjusted property EBITDA of 18.0% to $54.2 million

— On a hold-normalized basis, adjusted property EBITDA increased 21.1% to reach $85.3 million

ADR increased 3.6% to $231 with 92.6% occupancy, driving a RevPAR increase of 6.5% to $214

Table games drop increased 6.0% to $466.5 million driven by a 28.7% increase in Non-Baccarat drop

Slot win increased 16.5% to $46.8 million

Best opportunities for future growth:

— High-end Asian gaming growth

— Increase in group room pricing in 2015

— Non-gaming amenities

($MM)

Adjusted Property EBITDA and Adjusted Property EBITDA Margin

Best Opportunity for Future Growth in Group Room Business and Baccarat

Actual($MM)

Hold-Normalized

$27.9

$34.1

22.1%24.8%

0%

10%

20%

30%

40%

$0

$10

$20

$30

$40

2Q14 2Q15

$128 $139

$133$148

$261 $287

$0

$100

$200

$300

2Q14 2Q15

Baccarat Non-Baccarat

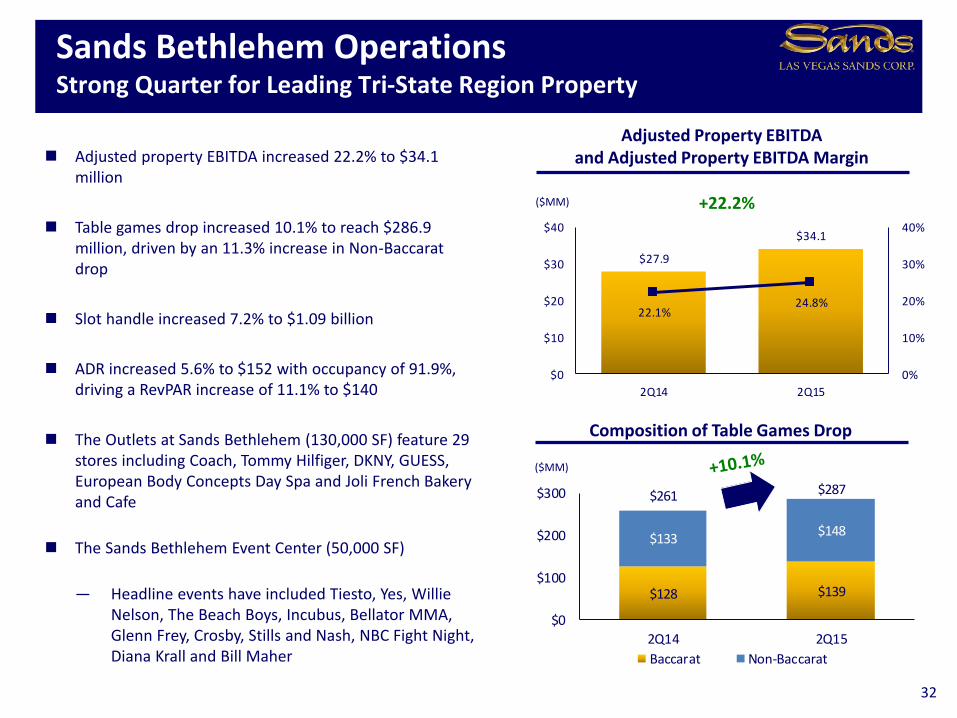

Sands Bethlehem OperationsStrong Quarter for Leading Tri-State Region Property

32

Adjusted property EBITDA increased 22.2% to $34.1 million

Table games drop increased 10.1% to reach $286.9 million, driven by an 11.3% increase in Non-Baccarat drop

Slot handle increased 7.2% to $1.09 billion

ADR increased 5.6% to $152 with occupancy of 91.9%, driving a RevPAR increase of 11.1% to $140

The Outlets at Sands Bethlehem (130,000 SF) feature 29 stores including Coach, Tommy Hilfiger, DKNY, GUESS, European Body Concepts Day Spa and Joli French Bakery and Cafe

The Sands Bethlehem Event Center (50,000 SF)

— Headline events have included Tiesto, Yes, Willie Nelson, The Beach Boys, Incubus, Bellator MMA, Glenn Frey, Crosby, Stills and Nash, NBC Fight Night, Diana Krall and Bill Maher

($MM)

($MM)

Adjusted Property EBITDA and Adjusted Property EBITDA Margin

Composition of Table Games Drop

Macao Market Background and Infrastructure Slides

42%

74%

58%

26%

0%

20%

40%

60%

80%

100%

Gross Gaming Revenue Operating Profit

Mass Tables and Slots VIP Gaming

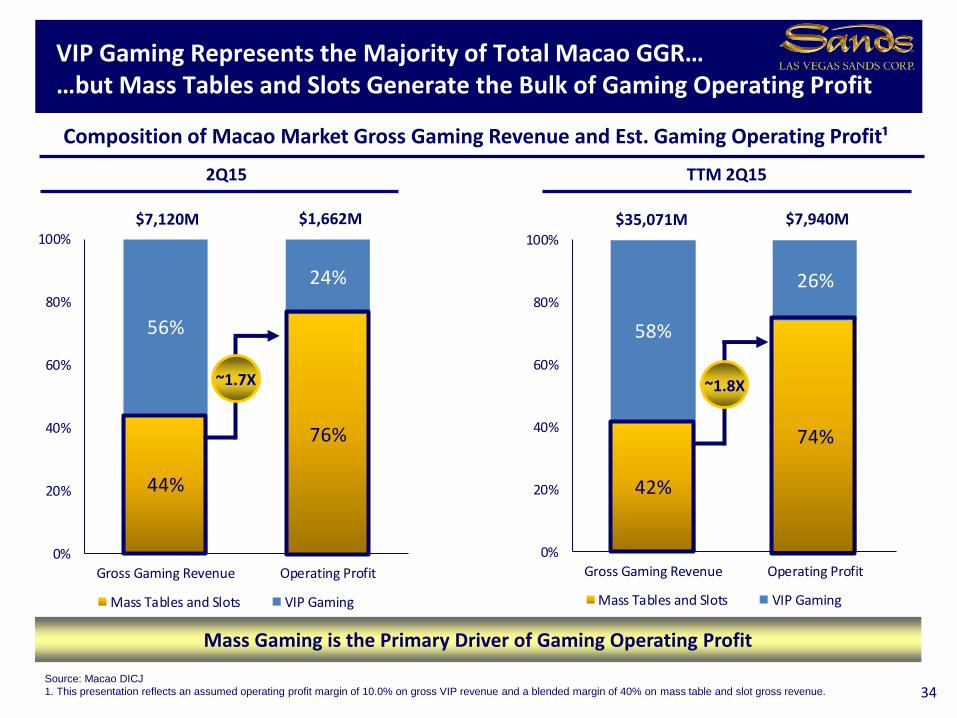

VIP Gaming Represents the Majority of Total Macao GGR……but Mass Tables and Slots Generate the Bulk of Gaming Operating Profit

Composition of Macao Market Gross Gaming Revenue and Est. Gaming Operating Profit¹

Source: Macao DICJ

1. This presentation reflects an assumed operating profit margin of 10.0% on gross VIP revenue and a blended margin of 40% on mass table and slot gross revenue.

Mass Gaming is the Primary Driver of Gaming Operating Profit

34

~1.8X

2Q15 TTM 2Q15

44%

76%

56%

24%

0%

20%

40%

60%

80%

100%

Gross Gaming Revenue Operating Profit

Mass Tables and Slots VIP Gaming

~1.7X

$35,071M $7,940M$7,120M $1,662M

$3,579

$4,670

$6,123

$6,960

$5,911

$2,446

$2,637

$2,985

$2,661

$2,029 $6,026

$7,307

$9,108 $9,621

$7,940

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2011 2012 2013 2014 TTM 2Q15

Mass Tables, Slots and ETGs VIP Tables

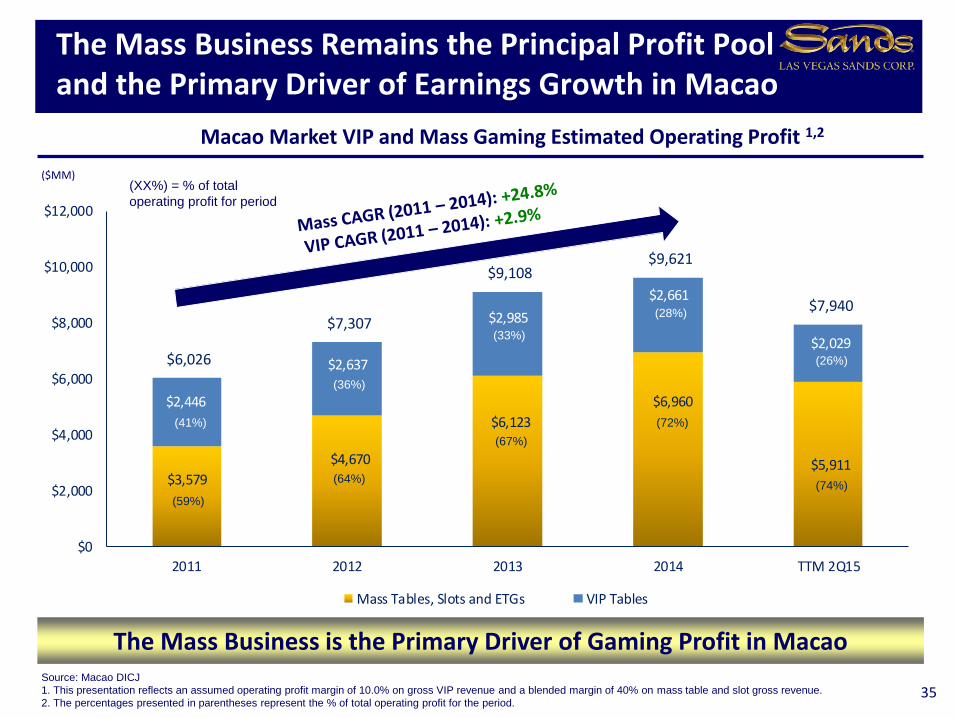

Macao Market VIP and Mass Gaming Estimated Operating Profit 1,2

The Mass Business Remains the Principal Profit Pool and the Primary Driver of Earnings Growth in Macao

($MM)

Source: Macao DICJ

1. This presentation reflects an assumed operating profit margin of 10.0% on gross VIP revenue and a blended margin of 40% on mass table and slot gross revenue.

2. The percentages presented in parentheses represent the % of total operating profit for the period.

The Mass Business is the Primary Driver of Gaming Profit in Macao

35

(59%)

(64%)

(67%)

(72%)(41%)

(36%)

(33%)

(28%)

(XX%) = % of total

operating profit for period

(74%)

(26%)

Five Trends that Should Contribute To Growth in the Macao Market In The Future

1

2

3

4

5

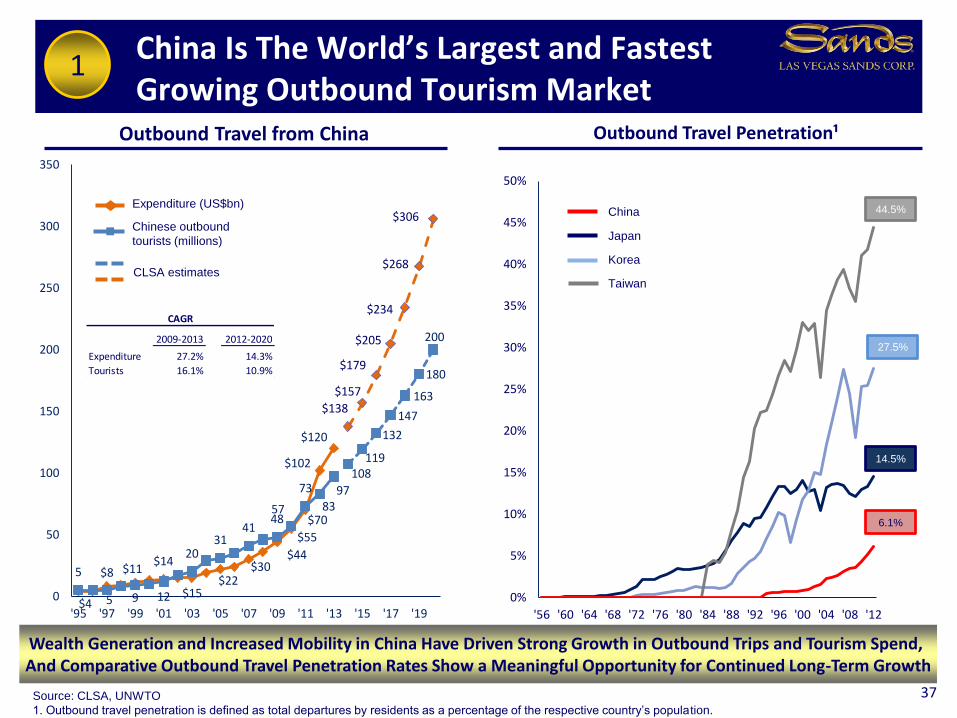

200 million Chinese are expected to travel outside of China by 2020, compared to 107 million in 2014

Infrastructure and transportation connectivity throughout China, especially in the Pearl River Delta region, will be meaningfully expanded

Increasing length of stay in Macao

Hengqin Island will contribute to Macao’s diversification and to its further development as a business and leisure tourism destination

Over 12,000 new hotel rooms will open in Macao by 2018

Sources: McKinsey, Ernst & Young, CLSA

36

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

'56 '60 '64 '68 '72 '76 '80 '84 '88 '92 '96 '00 '04 '08 '12$4

$8 $11 $14

$15 $22

$30 $44

$55

$70

$102

$120

5

5 9 12

2031

414857

73

8397

108119

132

147

163

180

200

$138

$157

$179

$205

$234

$268

$306

0

50

100

150

200

250

300

350

'95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

Outbound Travel from China

China Is The World’s Largest and Fastest Growing Outbound Tourism Market

37

Outbound Travel Penetration¹

Wealth Generation and Increased Mobility in China Have Driven Strong Growth in Outbound Trips and Tourism Spend, And Comparative Outbound Travel Penetration Rates Show a Meaningful Opportunity for Continued Long-Term Growth

Expenditure (US$bn)

Chinese outbound

tourists (millions)

CLSA estimates

Source: CLSA, UNWTO

1. Outbound travel penetration is defined as total departures by residents as a percentage of the respective country’s population.

1

China

Japan

Taiwan

Korea

2009-2013 2012-2020

Expenditure 27.2% 14.3%

Tourists 16.1% 10.9%

CAGR

44.5%

27.5%

14.5%

6.1%

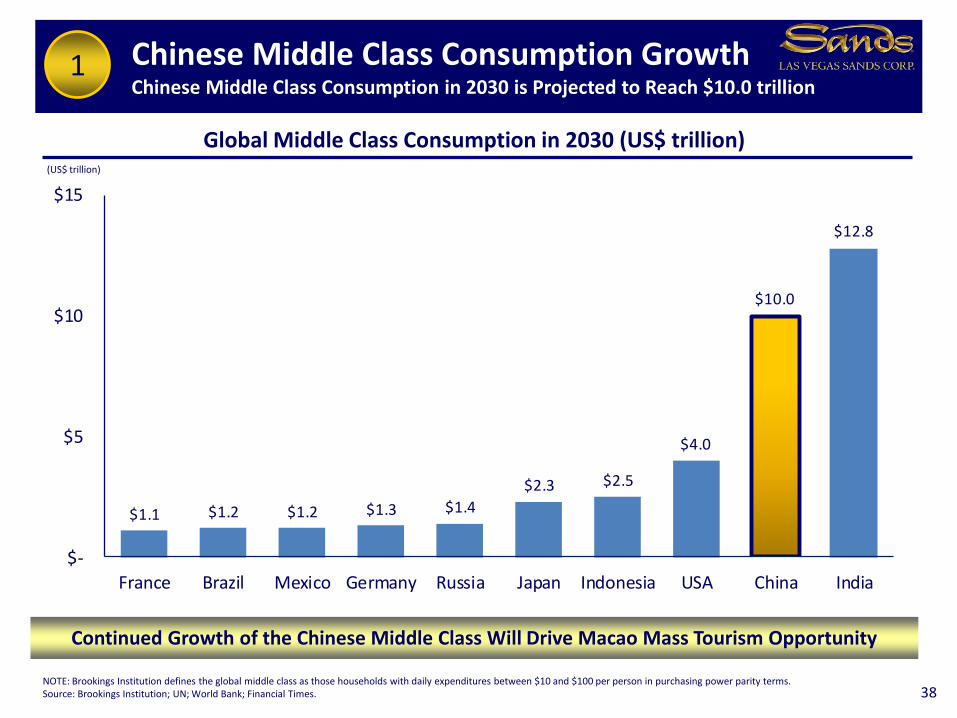

$1.1 $1.2 $1.2 $1.3 $1.4

$2.3 $2.5

$4.0

$10.0

$12.8

$-

$5

$10

$15

France Brazil Mexico Germany Russia Japan Indonesia USA China India

Chinese Middle Class Consumption GrowthChinese Middle Class Consumption in 2030 is Projected to Reach $10.0 trillion

38

Global Middle Class Consumption in 2030 (US$ trillion)

NOTE: Brookings Institution defines the global middle class as those households with daily expenditures between $10 and $100 per person in purchasing power parity terms.Source: Brookings Institution; UN; World Bank; Financial Times.

Continued Growth of the Chinese Middle Class Will Drive Macao Mass Tourism Opportunity

1

(US$ trillion)

Xinjiang

Tibet

Qinghai

SichuanChongqing

Henan

Hubei

ShanxiHebei

Shandong

Beijing

Liaoning

Jilin

Heilongjiang

Jiangsu

Anhui

Hunan Jiangxi

Zhejiang

Guangxi

Guizhou

Yunnan

Ningxia

Shaanxi

Inner Mongolia

Gansu

Guangdong

Fujian

Shanghai

Tianjin

Hong Kong

Macao

Twelve Months Ended May 31, Population GDP Per Penetration

Province 2014 2015 % Change (MM) Capita (US$) Rate

Guangdong 8,502,545 9,085,790 +7% 104 $9,452 8.7%

Fujian 807,691 905,123 +12% 37 $9,342 2.5%

Hunan 697,160 780,205 +12% 66 $5,936 1.2%

Hubei 601,824 678,165 +13% 58 $6,881 1.2%

Zhejiang 670,044 677,576 +1% 54 $11,054 1.2%

Jiangsu 540,950 563,493 +4% 79 $12,047 0.7%

Guangxi 428,131 530,770 +24% 46 $4,939 1.2%

Shanghai 544,835 528,283 -3% 23 $14,547 2.3%

Henan 420,480 482,784 +15% 94 $5,518 0.5%

Jiangxi 400,273 459,605 +15% 45 $5,130 1.0%

Sichuan 381,694 402,482 +5% 80 $5,240 0.5%

Beijing 376,312 365,480 -3% 20 $15,051 1.9%

Hebei 284,247 343,576 +21% 72 $6,251 0.5%

Liaoning 325,372 339,430 +4% 44 $9,961 0.8%

Heilongjiang 271,009 309,190 +14% 38 $6,057 0.8%

Shandong 280,095 303,077 +8% 96 $9,094 0.3%

Chongqing 238,046 257,073 +8% 30 $6,910 0.9%

All Other 4,036,827 3,972,896 -2% 407 N/A 1.0%

Subtotal (Excluding

Guangdong)11,304,990 11,899,208 +5% 1,288 $6,617 0.9%

Mainland China 19,807,535 20,984,998 +6% 1,392 $6,767 1.5%

39NOTE: Penetration rates assume that each visitor to Macao from Mainland China is a unique visitor.Source: Macao DSEC; National Bureau of Statistics of China; LVS Estimates

Year-Over-Year Visitation Growth Mainland Chinese Visitation to Macao

Greater than 20%

Data Not Available-10% - 0%

0% - 10%

10% - 20%

Strong Growth in Mainland Chinese Visitation to MacaoStrongest Growth Realized in Provinces Served by High Speed Rail

1

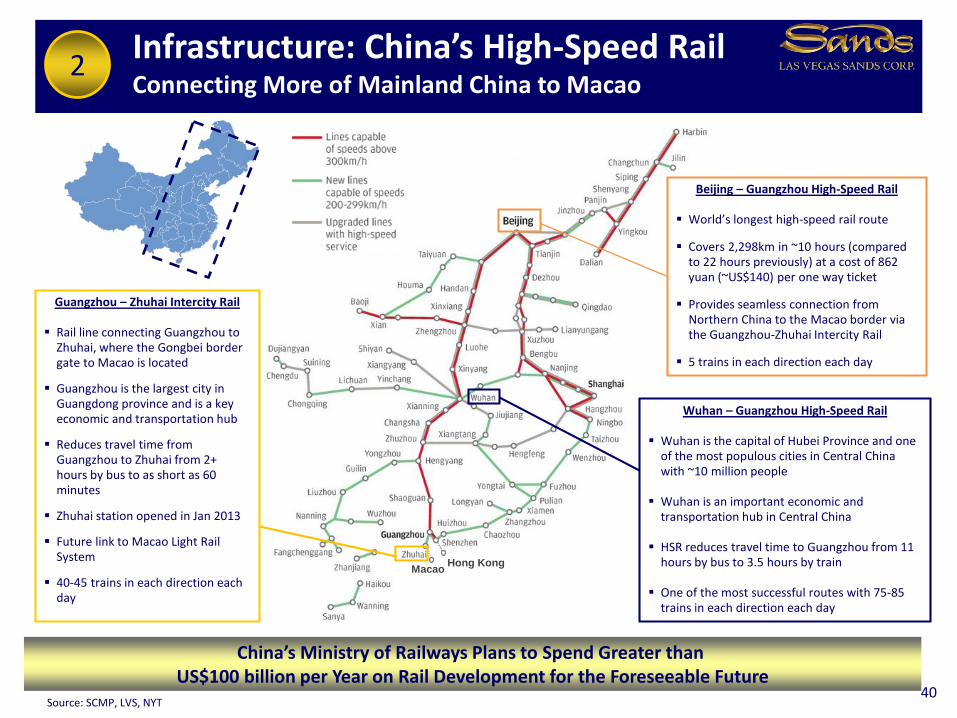

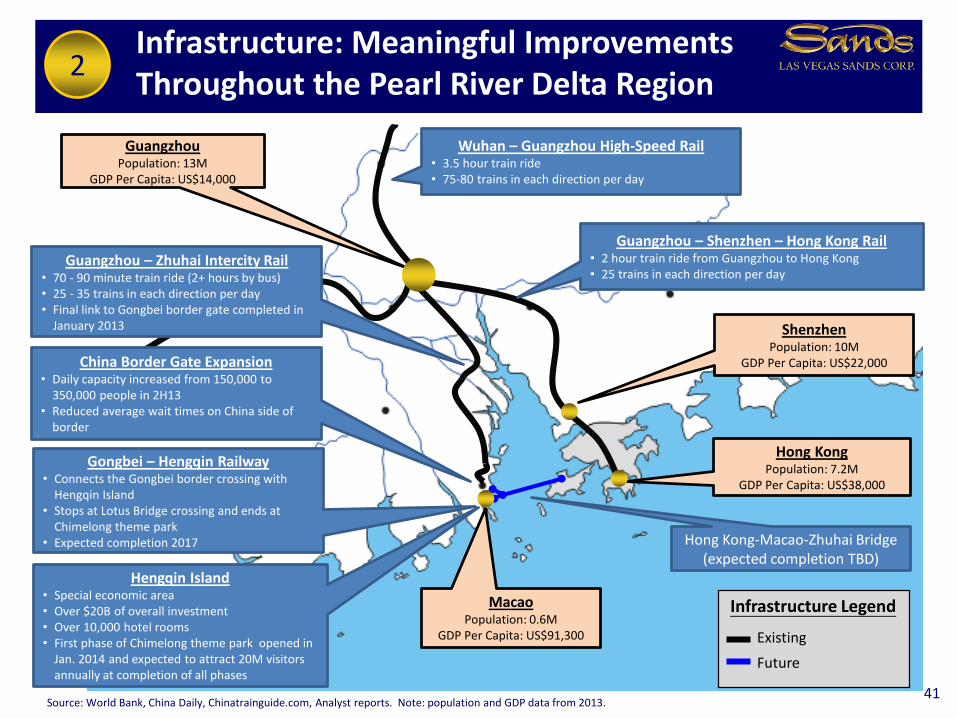

Infrastructure: China’s High-Speed RailConnecting More of Mainland China to Macao

Source: SCMP, LVS, NYT40

2

China’s Ministry of Railways Plans to Spend Greater than US$100 billion per Year on Rail Development for the Foreseeable Future

Beijing – Guangzhou High-Speed Rail

World’s longest high-speed rail route

Covers 2,298km in ~10 hours (compared to 22 hours previously) at a cost of 862 yuan (~US$140) per one way ticket

Provides seamless connection from Northern China to the Macao border via the Guangzhou-Zhuhai Intercity Rail

5 trains in each direction each day

Guangzhou – Zhuhai Intercity Rail

Rail line connecting Guangzhou to Zhuhai, where the Gongbei border gate to Macao is located

Guangzhou is the largest city in Guangdong province and is a key economic and transportation hub

Reduces travel time from Guangzhou to Zhuhai from 2+ hours by bus to as short as 60 minutes

Zhuhai station opened in Jan 2013

Future link to Macao Light Rail System

40-45 trains in each direction each day

Wuhan – Guangzhou High-Speed Rail

Wuhan is the capital of Hubei Province and one of the most populous cities in Central China with ~10 million people

Wuhan is an important economic and transportation hub in Central China

HSR reduces travel time to Guangzhou from 11 hours by bus to 3.5 hours by train

One of the most successful routes with 75-85 trains in each direction each day

Hong KongMacao

Infrastructure: Meaningful Improvements Throughout the Pearl River Delta Region

Source: World Bank, China Daily, Chinatrainguide.com, Analyst reports. Note: population and GDP data from 2013.41

GuangzhouPopulation: 13M

GDP Per Capita: US$14,000

MacaoPopulation: 0.6M

GDP Per Capita: US$91,300

Hengqin Island• Special economic area• Over $20B of overall investment• Over 10,000 hotel rooms• First phase of Chimelong theme park opened in

Jan. 2014 and expected to attract 20M visitors annually at completion of all phases

Hong KongPopulation: 7.2M

GDP Per Capita: US$38,000

Hong Kong-Macao-Zhuhai Bridge (expected completion TBD)

Wuhan – Guangzhou High-Speed Rail• 3.5 hour train ride• 75-80 trains in each direction per day

ShenzhenPopulation: 10M

GDP Per Capita: US$22,000China Border Gate Expansion• Daily capacity increased from 150,000 to

350,000 people in 2H13• Reduced average wait times on China side of

border

Guangzhou – Zhuhai Intercity Rail• 70 - 90 minute train ride (2+ hours by bus)• 25 - 35 trains in each direction per day• Final link to Gongbei border gate completed in

January 2013

Guangzhou – Shenzhen – Hong Kong Rail• 2 hour train ride from Guangzhou to Hong Kong• 25 trains in each direction per day

Infrastructure Legend

Existing

Future

Gongbei – Hengqin Railway• Connects the Gongbei border crossing with

Hengqin Island• Stops at Lotus Bridge crossing and ends at

Chimelong theme park• Expected completion 2017

2

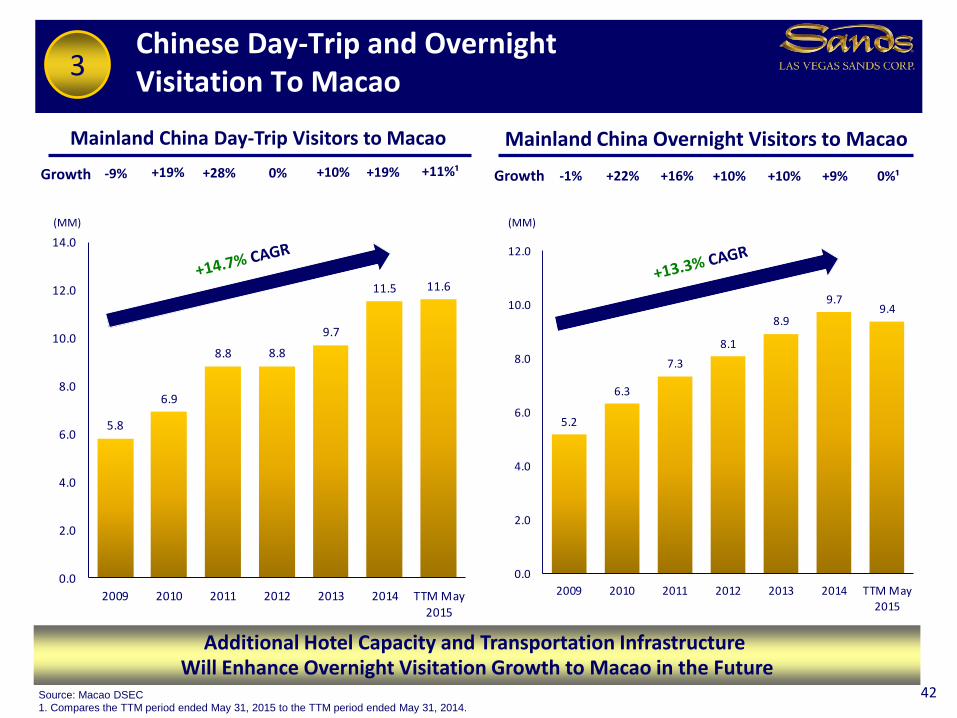

5.2

6.3

7.3

8.1

8.9

9.79.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2009 2010 2011 2012 2013 2014 TTM May

2015

5.8

6.9

8.8 8.8

9.7

11.5 11.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2009 2010 2011 2012 2013 2014 TTM May

2015

Mainland China Day-Trip Visitors to Macao Mainland China Overnight Visitors to Macao

Chinese Day-Trip and Overnight Visitation To Macao

(MM)

Source: Macao DSEC

1. Compares the TTM period ended May 31, 2015 to the TTM period ended May 31, 2014.

42

-9% +19% +28% 0%

(MM)

Growth -1% +22% +16% +10%Growth

Additional Hotel Capacity and Transportation Infrastructure Will Enhance Overnight Visitation Growth to Macao in the Future

+10% +10%

3

+19% +9%+11%¹ 0%¹

11.013.2

16.2 16.918.6

21.3

18.0

22.7

28.1

34.9

40.7

47.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

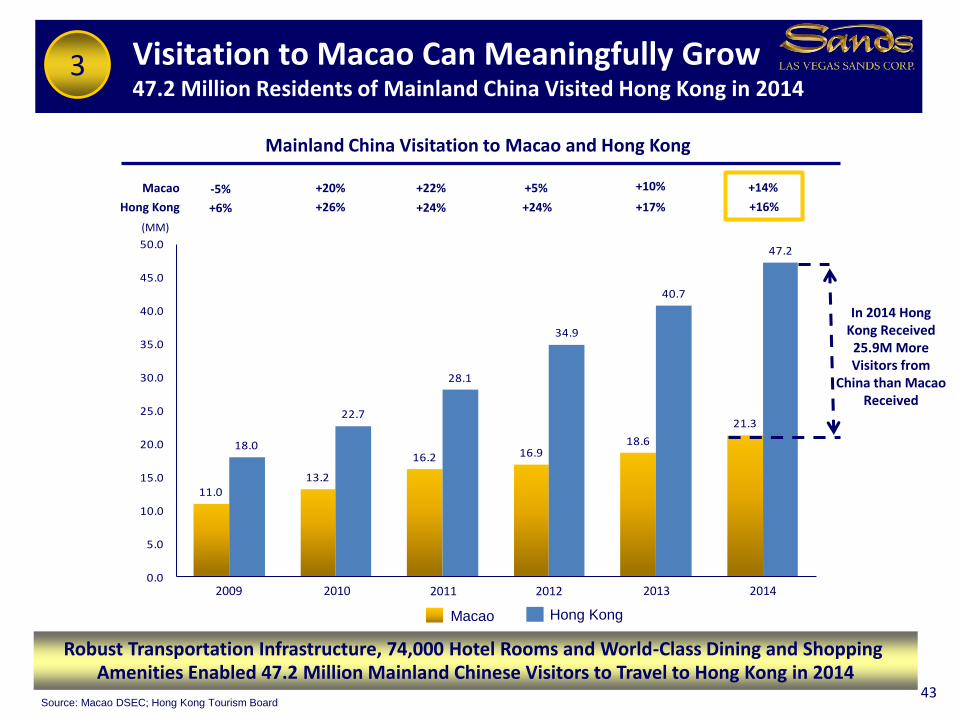

Mainland China Visitation to Macao and Hong Kong

Visitation to Macao Can Meaningfully Grow47.2 Million Residents of Mainland China Visited Hong Kong in 2014

(MM)

Source: Macao DSEC; Hong Kong Tourism Board43

-5% +20% +22% +5%Macao

+6%Hong Kong +26% +24% +24%

Robust Transportation Infrastructure, 74,000 Hotel Rooms and World-Class Dining and Shopping Amenities Enabled 47.2 Million Mainland Chinese Visitors to Travel to Hong Kong in 2014

In 2014 Hong Kong Received 25.9M More Visitors from

China than Macao Received

2009 2010 2011 2012 2013

+10%

+17%

3

Macao Hong Kong

2014

+14%

+16%

19.5

63.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2.0

3.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

(Days)

Total 2014 Mainland Chinese Visitor Nights¹

(MM)(MM)

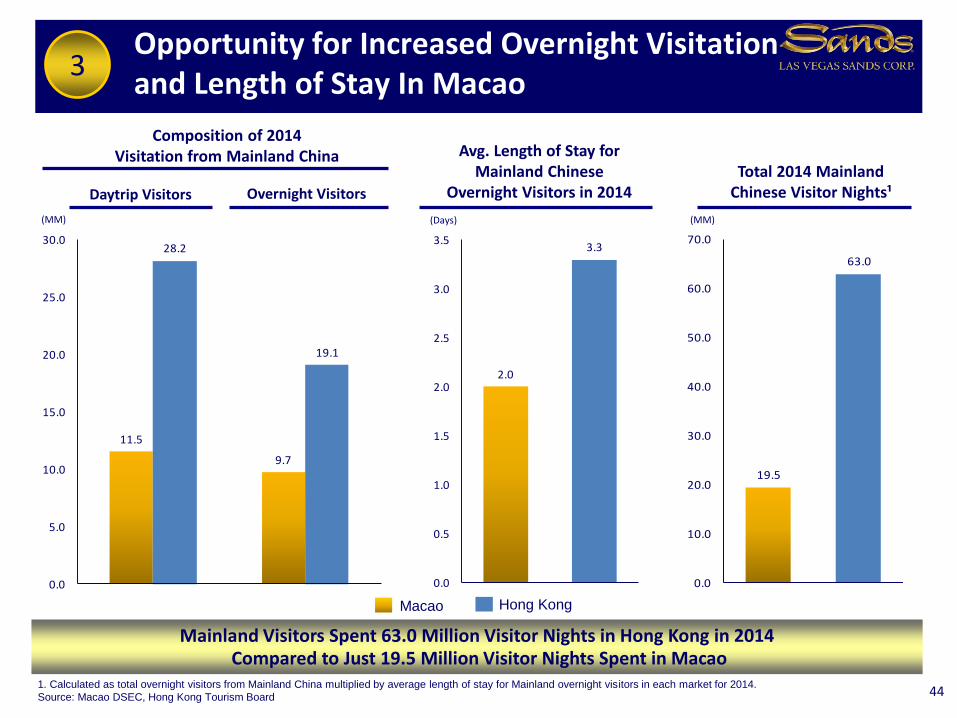

Daytrip Visitors

Opportunity for Increased Overnight Visitation and Length of Stay In Macao

441. Calculated as total overnight visitors from Mainland China multiplied by average length of stay for Mainland overnight visitors in each market for 2014.

Source: Macao DSEC, Hong Kong Tourism Board

Composition of 2014 Visitation from Mainland China

Mainland Visitors Spent 63.0 Million Visitor Nights in Hong Kong in 2014Compared to Just 19.5 Million Visitor Nights Spent in Macao

Overnight Visitors

Avg. Length of Stay for Mainland Chinese

Overnight Visitors in 2014

Macao Hong Kong

3

11.5

9.7

28.2

19.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

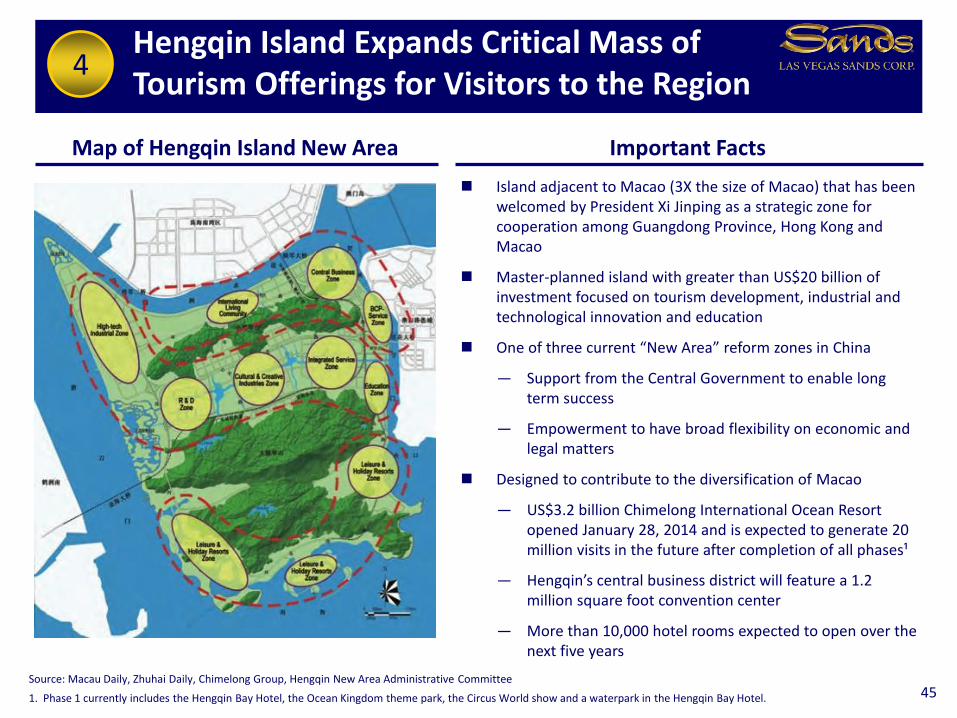

Hengqin Island Expands Critical Mass of Tourism Offerings for Visitors to the Region

45

Map of Hengqin Island New Area Important Facts

Island adjacent to Macao (3X the size of Macao) that has been welcomed by President Xi Jinping as a strategic zone for cooperation among Guangdong Province, Hong Kong and Macao

Master-planned island with greater than US$20 billion of investment focused on tourism development, industrial and technological innovation and education

One of three current “New Area” reform zones in China

— Support from the Central Government to enable long term success

— Empowerment to have broad flexibility on economic and legal matters

Designed to contribute to the diversification of Macao

— US$3.2 billion Chimelong International Ocean Resort opened January 28, 2014 and is expected to generate 20 million visits in the future after completion of all phases¹

— Hengqin’s central business district will feature a 1.2 million square foot convention center

— More than 10,000 hotel rooms expected to open over the next five years

Source: Macau Daily, Zhuhai Daily, Chimelong Group, Hengqin New Area Administrative Committee

1. Phase 1 currently includes the Hengqin Bay Hotel, the Ocean Kingdom theme park, the Circus World show and a waterpark in the Hengqin Bay Hotel.

4

Sands Cotai Central

5,723

The Venetian Macao

2,905

Sands Macao, 289

Galaxy Macau³

Phase I: 2,250Phase II: 1,350

Broadway Macau, 320Starworld, 509

City of Dreams1,461

Altira Macau, 216

Wynn Macau1,014 Grand Lisboa, 431

Sofitel Macau, 408MGM Grand, 587

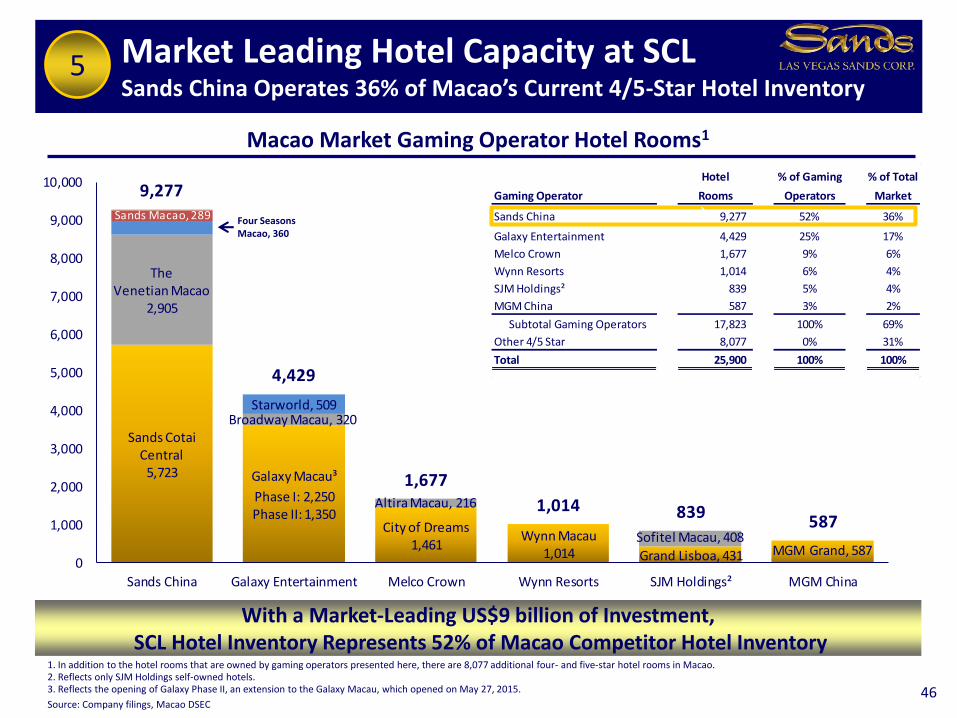

9,277

4,429

1,677

1,014 839587

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Sands China Galaxy Entertainment Melco Crown Wynn Resorts SJM Holdings² MGM China

Hotel % of Gaming % of Total

Gaming Operator Rooms Operators Market

Sands China 9,277 52% 36%

Galaxy Entertainment 4,429 25% 17%

Melco Crown 1,677 9% 6%

Wynn Resorts 1,014 6% 4%

SJM Holdings² 839 5% 4%

MGM China 587 3% 2%

Subtotal Gaming Operators 17,823 100% 69%

Other 4/5 Star 8,077 0% 31%

Total 25,900 100% 100%

Market Leading Hotel Capacity at SCLSands China Operates 36% of Macao’s Current 4/5-Star Hotel Inventory

1. In addition to the hotel rooms that are owned by gaming operators presented here, there are 8,077 additional four- and five-star hotel rooms in Macao.2. Reflects only SJM Holdings self-owned hotels.3. Reflects the opening of Galaxy Phase II, an extension to the Galaxy Macau, which opened on May 27, 2015.

Source: Company filings, Macao DSEC46

With a Market-Leading US$9 billion of Investment,SCL Hotel Inventory Represents 52% of Macao Competitor Hotel Inventory

Macao Market Gaming Operator Hotel Rooms1

Four Seasons Macao, 360

5

`

Sands Cotai Central

5,723

The Venetian Macao

2,905

Sands Macao, 289

The Parisian Macao3,000

Galaxy Macau³

Phase I: 2,250Phase II: 1,350

Broadway Macau, 320Starworld, 509

City of Dreams1,461

Altira Macau, 216

Macau Studio City1,600

Grand Lisboa, 431Sofitel Macau, 408

SJM Cotai2,000

Wynn Macau, 1,014

Wynn Palace1,700

MGM Grand, 587

MGM Cotai1,600

12,677

4,429

3,277 2,839 2,7142,187

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Sands China Galaxy Entertainment Melco Crown SJM Holdings² Wynn Resorts MGM China

Hotel % of Gaming % of Total

Gaming Operator Rooms Operators Market

Sands China 12,677 45% 35%

Galaxy Entertainment 4,429 16% 12%

Melco Crown 3,277 12% 9%

SJM Holdings² 2,839 10% 8%

Wynn Resorts 2,714 9% 7%

MGM China 2,187 8% 6%

Subtotal Gaming Operators 28,123 100% 77%

Other 4/5 Star 8,277 0% 23%

Total 36,400 100% 100%

1. In addition to the hotel rooms that are owned by gaming operators presented here, there will be 8,277 additional four- and five-star hotel rooms in Macao at December 31, 2017.2. Reflects only SJM Holdings self-owned hotels.3. Reflects the opening of Galaxy Phase II, an extension to the Galaxy Macau, which opened on May 27, 2015.

Source: Company filings, Macao DSEC

47

Macao Market Gaming Operator Hotel Rooms at December 31, 20171

Four Seasons Macao, 360

St. Regis Macao, 400

5

`

With a Market-Leading US$13 billion of Investment,SCL Hotel Inventory Will Represent 45% of Macao Competitor Hotel Inventory

Market Leading Hotel Capacity at SCLProjected Macao Market 4/5 Star Hotel Rooms at December 31, 2017

Supplemental Sands China Information

$7.0

$5.2

$1.0

$13.3

$2.4

$15.7

$5.3

$4.2

$0.7

$10.3

$1.9

$12.2

$0.0

$5.0

$10.0

$15.0

$20.0

VenetianMacao

Sands CotaiCentral

Plaza Casino(Four Seasons)

TotalCotai Strip

Sands Macao TotalMacao Ops

2Q14 2Q15

Mass Table, Slot and ETG Win Per Day

($MM)

SCL’s Mass Gaming Segment Impacted by Headwinds… Especially at the High-End of the Mass Market

49

Cotai Strip Properties Peninsula Total

Mass Tables 503 393 95963 238 1,197

Slots

ETGs

1,437 1,041 2,624146 559 3,183

681 654 1,3438 384 1,727

2Q15 Average Table, Slot and ETG Units

$10,190$10,961

$12,143

$13,210

$11,963$11,518

$10,469

$9,447$8,966

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

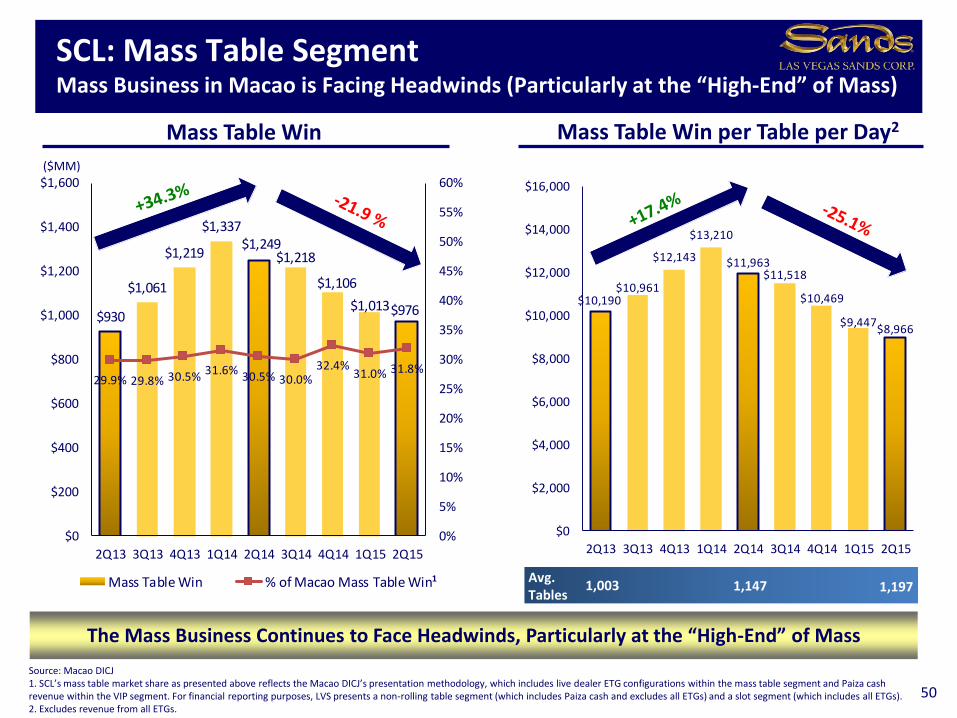

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

$930

$1,061

$1,219

$1,337$1,249

$1,218

$1,106

$1,013$976

29.9% 29.8% 30.5% 31.6% 30.5% 30.0%32.4%

31.0% 31.8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Mass Table Win % of Macao Mass Table Win

Mass Table Win Mass Table Win per Table per Day2

50

($MM)

1,197Avg. Tables

1,147

The Mass Business Continues to Face Headwinds, Particularly at the “High-End” of Mass

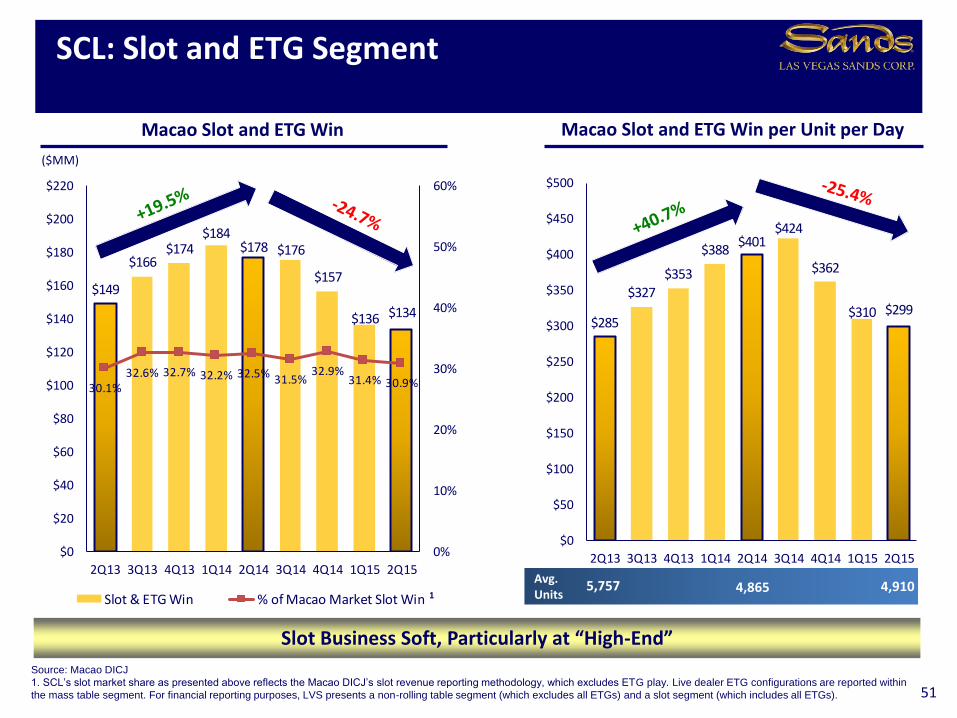

Source: Macao DICJ1. SCL’s mass table market share as presented above reflects the Macao DICJ’s presentation methodology, which includes live dealer ETG configurations within the mass table segment and Paiza cash revenue within the VIP segment. For financial reporting purposes, LVS presents a non-rolling table segment (which includes Paiza cash and excludes all ETGs) and a slot segment (which includes all ETGs).2. Excludes revenue from all ETGs.

SCL: Mass Table SegmentMass Business in Macao is Facing Headwinds (Particularly at the “High-End” of Mass)

11,003

$285

$327

$353

$388$401

$424

$362

$310 $299

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

$149

$166$174

$184$178 $176

$157

$136 $134

30.1%32.6% 32.7% 32.2% 32.5% 31.5%

32.9%31.4% 30.9%

0%

10%

20%

30%

40%

50%

60%

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

$220

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Slot & ETG Win % of Macao Market Slot Win

Macao Slot and ETG Win Macao Slot and ETG Win per Unit per Day

51

($MM)

4,910Avg. Units

4,865

Slot Business Soft, Particularly at “High-End”

Source: Macao DICJ

1. SCL’s slot market share as presented above reflects the Macao DICJ’s slot revenue reporting methodology, which excludes ETG play. Live dealer ETG configurations are reported within

the mass table segment. For financial reporting purposes, LVS presents a non-rolling table segment (which excludes all ETGs) and a slot segment (which includes all ETGs).

SCL: Slot and ETG Segment

15,757

$24,763

$30,365

$32,837

$39,167

$32,568

$29,893

$24,084

$19,012

$22,250

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

$1,184

$1,303$1,327

$1,445

$1,117

$1,019

$838

$592 $641

16.8%

18.4%

16.9%18.3%

16.8%

17.9%

15.6%

14.6%

18.9%

0%

5%

10%

15%

20%

25%

30%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

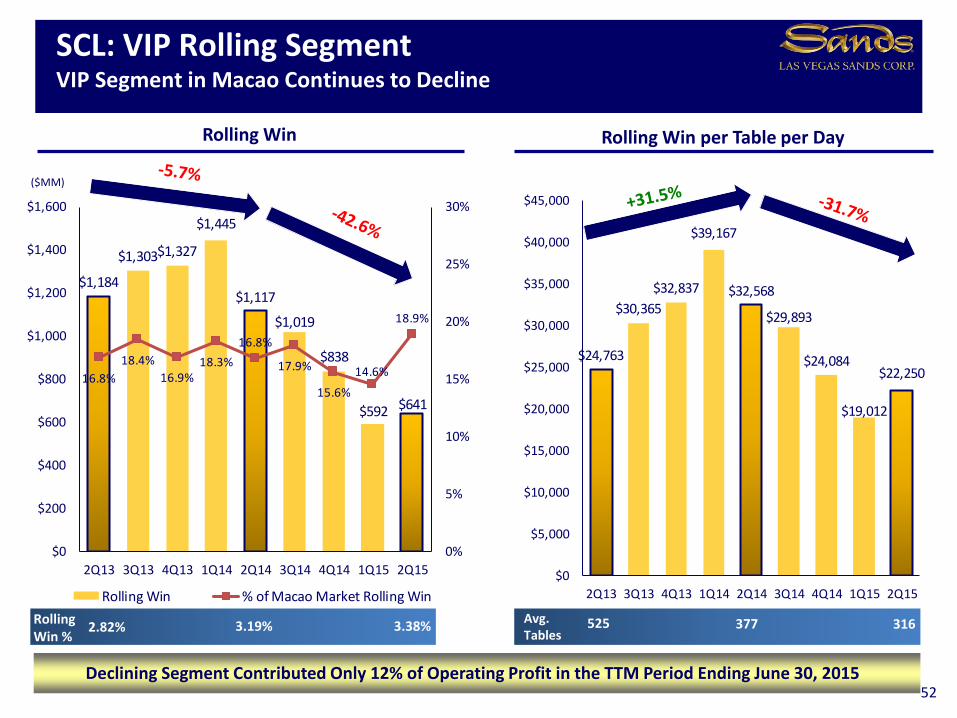

Rolling Win % of Macao Market Rolling Win

Rolling Win per Table per Day

52

Rolling Win

316Avg. Tables

377

Declining Segment Contributed Only 12% of Operating Profit in the TTM Period Ending June 30, 2015

($MM)

SCL: VIP Rolling SegmentVIP Segment in Macao Continues to Decline

3.38%3.19%RollingWin %

5252.82%

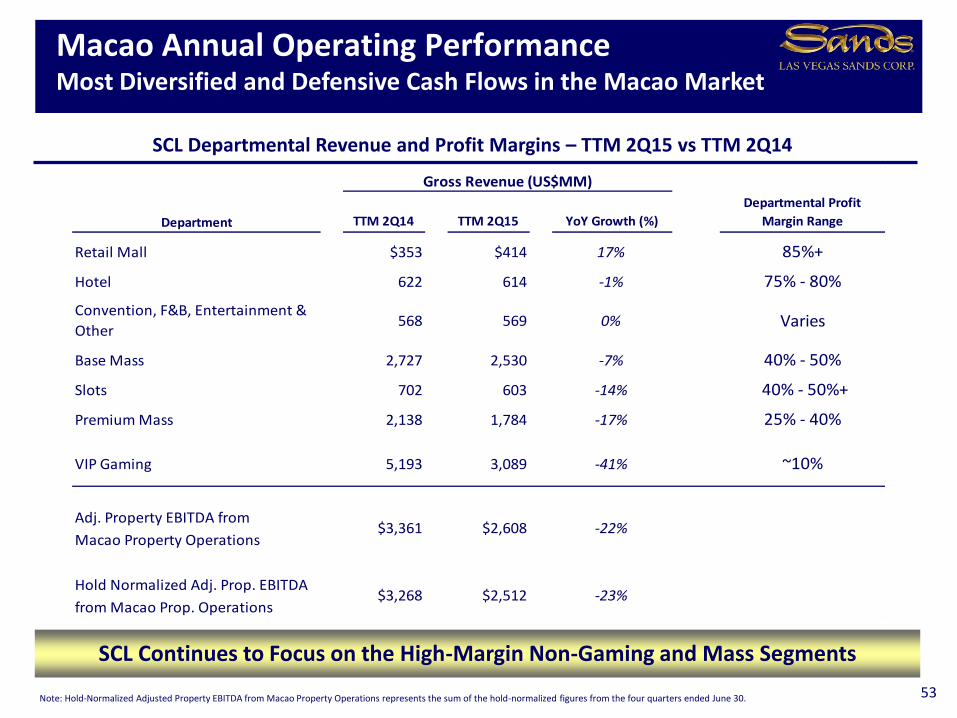

Department TTM 2Q14 TTM 2Q15 YoY Growth (%)

Departmental Profit

Margin Range

Retail Mall $353 $414 17% 85%+

Hotel 622 614 -1% 75% - 80%

Convention, F&B, Entertainment &

Other568 569 0% Varies

Base Mass 2,727 2,530 -7% 40% - 50%

Slots 702 603 -14% 40% - 50%+

Premium Mass 2,138 1,784 -17% 25% - 40%

VIP Gaming 5,193 3,089 -41% ~10%

Adj. Property EBITDA from

Macao Property Operations

Hold Normalized Adj. Prop. EBITDA

from Macao Prop. Operations-23%

Gross Revenue (US$MM)

$3,361 $2,608 -22%

$3,268 $2,512

Macao Annual Operating PerformanceMost Diversified and Defensive Cash Flows in the Macao Market

53

SCL Departmental Revenue and Profit Margins – TTM 2Q15 vs TTM 2Q14

SCL Continues to Focus on the High-Margin Non-Gaming and Mass Segments

Note: Hold-Normalized Adjusted Property EBITDA from Macao Property Operations represents the sum of the hold-normalized figures from the four quarters ended June 30.

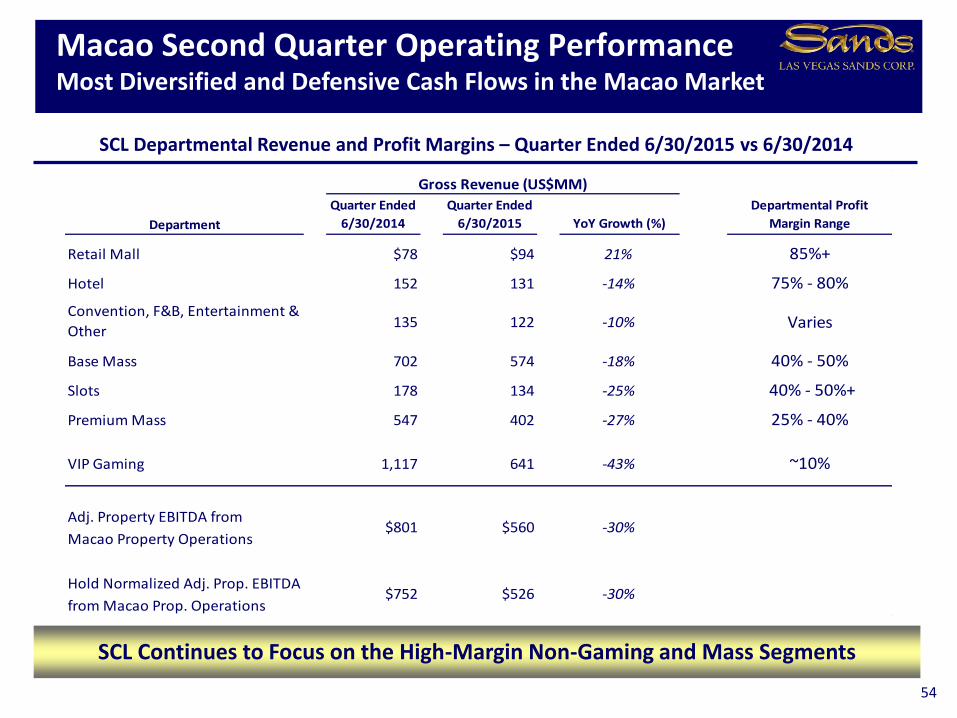

Department

Quarter Ended

6/30/2014

Quarter Ended

6/30/2015 YoY Growth (%)

Departmental Profit

Margin Range

Retail Mall $78 $94 21% 85%+

Hotel 152 131 -14% 75% - 80%

Convention, F&B, Entertainment &

Other135 122 -10% Varies

Base Mass 702 574 -18% 40% - 50%

Slots 178 134 -25% 40% - 50%+

Premium Mass 547 402 -27% 25% - 40%

VIP Gaming 1,117 641 -43% ~10%

Adj. Property EBITDA from

Macao Property Operations

Hold Normalized Adj. Prop. EBITDA

from Macao Prop. Operations

Gross Revenue (US$MM)

$801 $560 -30%

$752 $526 -30%

Macao Second Quarter Operating PerformanceMost Diversified and Defensive Cash Flows in the Macao Market

54

SCL Departmental Revenue and Profit Margins – Quarter Ended 6/30/2015 vs 6/30/2014

SCL Continues to Focus on the High-Margin Non-Gaming and Mass Segments

$40 $49

$198

$576 $593$688

$817

$1,030

$1,381

$1,626 $1,597

$0

$500

$1,000

$1,500

$2,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM 2Q15

Non-Gaming Revenue (US$MM)

Macao Annual Non-Gaming RevenueMost Diversified and Defensive Cash Flows in the Macao Market

55

($MM)

SCL Gross Non-Gaming Revenue

SCL’s High-Margin Non-Gaming Revenue Has Remained Strong Despite Headwinds in the Gaming Segments