Embed Size (px)

Citation preview

special report:leisUre2013

october 2013

fl ightglobal.com/ab fl ightglobal.com/ab

“We are part of the group, we will participate

in the transformation of Thomas Cook”

CHRISTOPH DEBUSGroup head of air travel, Thomas Cook

“Quote, quote and quote and quote, four lines is

probably maximum length to be interesting”

QUOTE – PERSON NAMEQuote – person details

iMPRoVing PRognosisMedicine such as restructuring, cost reduction and scheduled services are helping the leisure industry rise from its sickbed

October 2013 | Airline Business | 4948 | Airline Business | October 2013

leisuRe stRategY

■

REPORTOLIVER CLARK LONDON

REPORTAUTHOR WHERE?

Despite facing political and eco-nomic turmoil in core markets such as north Africa and Greece, a sluggish European economy and competition from

low-cost carriers, leisure airlines appear to have had a remarkably good year so far.

UK leisure operator Thomas Cook, which is undergoing a major restructuring, reported a £1 million ($1.6 million) profi t in the third quarter of 2013. This was its fi rst positive quarterly result for two years and a turna-round from the £45 million loss reported dur-ing the same period in 2012.

This result is all the more impressive given that the leisure group was in a crisis just two years ago, having asked investors for an addi-tional £100 million loan – and leading some commentators to question whether the tour operator has a viable future.

The same trend is being repeated by other leisure carriers, such as Jet2 and its package holiday arm Jet2holidays. Owner Dart group reports that total leisure airline turnover for the year ended 31 March 2013 – including sales of seats to Jet2holidays – increased by more than 20% to £556.2 million, on the back of a 13% increase in scheduled passengers to 4.84 million.

TUI Travel reported a £76 million profi t for the third quarter ending 30 June – up by 3% on the same period last year – and predicts it will achieve a 10% increase in full-year underlying operating profi t.

So could predictions that the charter leisure market is in terminal decline be premature or even misplaced?

RESTRUCTURING MOVESSylviane Lust, director general of the Interna-tional Air Carrier Association (IACA) – which represents a number of leisure carriers includ-ing Condor, Thomas Cook and Thomson – says its members are increasingly moving to a hybrid business model, but the core proposi-tion of offering passengers an all-inclusive package holiday product remains a viable business proposition.

“We asked our members this question 10 years ago, and since then the market has been completely transformed. It’s now a mixture of business models, with even the tour operator airlines offering seat-only options. So the answer to the question is they are not in termi-nal decline at all,” she says.

“Our members are implementing cost con-

trol and effi ciencies on a similar model to the low-cost carriers, but they are also making improvements to the quality and comfort of the products they are offering,” adds Lust.

While leisure carriers and tour operators face fi erce competition from low-cost rivals, Lust says the market this year has been encouraging overall.

“While it is defi nitely true that some desti-nations are still suffering from political insta-bility – Egypt was the fi rst, and continues to suffer – there has been a shift of capacity to other destinations which leisure airlines have achieved without too much trouble,” she explains. She adds: “Turkey still has seen very high arrivals. Greece is coming back because it is still offering a good product at a relatively low price. Spain is always a very strong desti-nation and Tunisia and Morocco are also com-ing back, although Cyprus has been quite low this year.”

The Thomas Cook Group also reacted to the challenging market conditions with a wide-ranging restructure programme. This included axing 2,500 jobs, closing 175 high street shops in the UK alone and selling off its North American businesses.

Meanwhile its three airline divisions – Con-dor, Thomas Cook Airlines UK and Thomas Cook Airlines Belgium – have all been merged into a single division which is fronted by group head of air travel, Christoph Debus.

Previously chief fi nancial offi cer of Condor

and chief operating offi cer of Air Berlin, Debus brings signifi cant experience from both a leisure and low-cost background, and is expected to drive the profi tability of the air-lines as a single unit.

Some industry analysts have argued that this reorganisation is a prelude to selling off the leisure group’s airline arm. Debus defends the move, saying Thomas Cook is “commit-ted” to retaining its airline operation.

“We are part of the group – we will partici-pate in the transformation of Thomas Cook and we will work with the tour operator to reach targets we wish to achieve by 2015, on the way to delivering enhanced revenue and capacity management,” he says.

Debus says the amalgamated group brings together the various strengths of each airline, allowing them to share best practice and achieve cost savings through standardisation.

“Historically it has been a siloed business. This was not just a specifi c airline issue but group-wide. This [restructure] allows us to achieve greater co-operation with other mar-kets, our hotels, IT and procurement and share our strengths,” he says.

VIEW FROM NORTH AMERICADescribing both Thomas Cook and Condor as “iconic” brands, Debus sees no need at present to absorb them into one business, and indeed says they are “very well positioned in the long-haul business, and we do not plan to change that”.

Another airline that has moved to restruc-ture its leisure operations is Air Canada. In late 2012 the Canadian national airline cre-ated a new leisure group by combining the operations of its tour operator business – Air Canada Vacations – with a newly created low-cost division, Air Canada Rouge.

Headed by ex-Thomas Cook North America chief executive Michael Friisdahl, the new group seeks to combine a long established package tour brand offering typical sun and sand destinations with a dedicated fl eet of leased narrowbodies. These are being oper-ated under a low-cost model, with staff work-ing on lower salaries than their Air Canada mainline counterparts.

The new airline began operating in July and now fl ies to Edinburgh and Athens in Europe, Samana in the Dominican Republic, Kingston, Jamaica and Santa Clara and Varadero in Cuba, amongst others. It is doing this with a fl eet of two Airbus A319s and new Boeing

“Three line quote in here with no picture needed blah blah blah xxxx”

NAME NAMEJob title, Company name

No more than three lines in here xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxx

x%

No more than three lines in here xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxx

x%

COLOMBIAN CARRIERS XXXXXXXXXX

Carrier Market share Load factorJun-09 Jun-08 Jun-09

Avianca* 55.7% 61.0% 76.7%Aero Republica 17.3% 16.0% 67.6%Aires 14.8% 10.6% 57.7%Satena 8.1% 9.7% 64.0%EasyFly 2.4% 1.5% 61.5%Anitoquia 1.7% 1.3% 67.5%Total/Average 100% 100.1% 69.9%*Avianca fi gures include SAM subsidiary. NOTES: Market share is based on domestic passengers carried in June 2009 and June 2008. SOURCE: Colombian CAA monthly supply and demand data

FIRSTNAME SURNAME LOCATION

tWo DecK HeaDline HeRe Please

Text here please or bold up text to break up orBox text indent

CROSS HEAD

Pict

ure

- cre

dit s

tyle

Picture - caption. Style for caption

Michael Bell, who previously spent six years with McKinsey, co-leads the global aviation practice of executive search specialist Spencer Stuart Email: [email protected]

■

Xxxxx xxxxx xxxxxxxxx, read our analysis with xxxxxxxxx chief executive Xxxxxxx Xxxxxxxxxx fl ightglobal.com/??????????

AirT

eam

Imag

es

TUI’s UK arm Thomson Airways suffered a 3.1% decline in traffi c last

year, to 10.7 million passengers

fl ightglobal.com/ab fl ightglobal.com/ab

“We are part of the group, we will participate

in the transformation of Thomas Cook”

CHRISTOPH DEBUSGroup head of air travel, Thomas Cook

“Quote, quote and quote and quote, four lines is

probably maximum length to be interesting”

QUOTE – PERSON NAMEQuote – person details

iMPRoVing PRognosisMedicine such as restructuring, cost reduction and scheduled services are helping the leisure industry rise from its sickbed

October 2013 | Airline Business | 4948 | Airline Business | October 2013

leisuRe stRategY

■

REPORTOLIVER CLARK LONDON

REPORTAUTHOR WHERE?

Despite facing political and eco-nomic turmoil in core markets such as north Africa and Greece, a sluggish European economy and competition from

low-cost carriers, leisure airlines appear to have had a remarkably good year so far.

UK leisure operator Thomas Cook, which is undergoing a major restructuring, reported a £1 million ($1.6 million) profi t in the third quarter of 2013. This was its fi rst positive quarterly result for two years and a turna-round from the £45 million loss reported dur-ing the same period in 2012.

This result is all the more impressive given that the leisure group was in a crisis just two years ago, having asked investors for an addi-tional £100 million loan – and leading some commentators to question whether the tour operator has a viable future.

The same trend is being repeated by other leisure carriers, such as Jet2 and its package holiday arm Jet2holidays. Owner Dart group reports that total leisure airline turnover for the year ended 31 March 2013 – including sales of seats to Jet2holidays – increased by more than 20% to £556.2 million, on the back of a 13% increase in scheduled passengers to 4.84 million.

TUI Travel reported a £76 million profi t for the third quarter ending 30 June – up by 3% on the same period last year – and predicts it will achieve a 10% increase in full-year underlying operating profi t.

So could predictions that the charter leisure market is in terminal decline be premature or even misplaced?

RESTRUCTURING MOVESSylviane Lust, director general of the Interna-tional Air Carrier Association (IACA) – which represents a number of leisure carriers includ-ing Condor, Thomas Cook and Thomson – says its members are increasingly moving to a hybrid business model, but the core proposi-tion of offering passengers an all-inclusive package holiday product remains a viable business proposition.

“We asked our members this question 10 years ago, and since then the market has been completely transformed. It’s now a mixture of business models, with even the tour operator airlines offering seat-only options. So the answer to the question is they are not in termi-nal decline at all,” she says.

“Our members are implementing cost con-

trol and effi ciencies on a similar model to the low-cost carriers, but they are also making improvements to the quality and comfort of the products they are offering,” adds Lust.

While leisure carriers and tour operators face fi erce competition from low-cost rivals, Lust says the market this year has been encouraging overall.

“While it is defi nitely true that some desti-nations are still suffering from political insta-bility – Egypt was the fi rst, and continues to suffer – there has been a shift of capacity to other destinations which leisure airlines have achieved without too much trouble,” she explains. She adds: “Turkey still has seen very high arrivals. Greece is coming back because it is still offering a good product at a relatively low price. Spain is always a very strong desti-nation and Tunisia and Morocco are also com-ing back, although Cyprus has been quite low this year.”

The Thomas Cook Group also reacted to the challenging market conditions with a wide-ranging restructure programme. This included axing 2,500 jobs, closing 175 high street shops in the UK alone and selling off its North American businesses.

Meanwhile its three airline divisions – Con-dor, Thomas Cook Airlines UK and Thomas Cook Airlines Belgium – have all been merged into a single division which is fronted by group head of air travel, Christoph Debus.

Previously chief fi nancial offi cer of Condor

and chief operating offi cer of Air Berlin, Debus brings signifi cant experience from both a leisure and low-cost background, and is expected to drive the profi tability of the air-lines as a single unit.

Some industry analysts have argued that this reorganisation is a prelude to selling off the leisure group’s airline arm. Debus defends the move, saying Thomas Cook is “commit-ted” to retaining its airline operation.

“We are part of the group – we will partici-pate in the transformation of Thomas Cook and we will work with the tour operator to reach targets we wish to achieve by 2015, on the way to delivering enhanced revenue and capacity management,” he says.

Debus says the amalgamated group brings together the various strengths of each airline, allowing them to share best practice and achieve cost savings through standardisation.

“Historically it has been a siloed business. This was not just a specifi c airline issue but group-wide. This [restructure] allows us to achieve greater co-operation with other mar-kets, our hotels, IT and procurement and share our strengths,” he says.

VIEW FROM NORTH AMERICADescribing both Thomas Cook and Condor as “iconic” brands, Debus sees no need at present to absorb them into one business, and indeed says they are “very well positioned in the long-haul business, and we do not plan to change that”.

Another airline that has moved to restruc-ture its leisure operations is Air Canada. In late 2012 the Canadian national airline cre-ated a new leisure group by combining the operations of its tour operator business – Air Canada Vacations – with a newly created low-cost division, Air Canada Rouge.

Headed by ex-Thomas Cook North America chief executive Michael Friisdahl, the new group seeks to combine a long established package tour brand offering typical sun and sand destinations with a dedicated fl eet of leased narrowbodies. These are being oper-ated under a low-cost model, with staff work-ing on lower salaries than their Air Canada mainline counterparts.

The new airline began operating in July and now fl ies to Edinburgh and Athens in Europe, Samana in the Dominican Republic, Kingston, Jamaica and Santa Clara and Varadero in Cuba, amongst others. It is doing this with a fl eet of two Airbus A319s and new Boeing

“Three line quote in here with no picture needed blah blah blah xxxx”

NAME NAMEJob title, Company name

No more than three lines in here xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxx

x%

No more than three lines in here xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxx

x%

COLOMBIAN CARRIERS XXXXXXXXXX

Carrier Market share Load factorJun-09 Jun-08 Jun-09

Avianca* 55.7% 61.0% 76.7%Aero Republica 17.3% 16.0% 67.6%Aires 14.8% 10.6% 57.7%Satena 8.1% 9.7% 64.0%EasyFly 2.4% 1.5% 61.5%Anitoquia 1.7% 1.3% 67.5%Total/Average 100% 100.1% 69.9%*Avianca fi gures include SAM subsidiary. NOTES: Market share is based on domestic passengers carried in June 2009 and June 2008. SOURCE: Colombian CAA monthly supply and demand data

FIRSTNAME SURNAME LOCATION

tWo DecK HeaDline HeRe Please

Text here please or bold up text to break up orBox text indent

CROSS HEAD

Pict

ure

- cre

dit s

tyle

Picture - caption. Style for caption

Michael Bell, who previously spent six years with McKinsey, co-leads the global aviation practice of executive search specialist Spencer Stuart Email: [email protected]

■

Xxxxx xxxxx xxxxxxxxx, read our analysis with xxxxxxxxx chief executive Xxxxxxx Xxxxxxxxxx fl ightglobal.com/??????????

AirT

eam

Imag

es

TUI’s UK arm Thomson Airways suffered a 3.1% decline in traffi c last

year, to 10.7 million passengers

fl ightglobal.com/ab

“Quote, quote and quote and quote, four lines is

probably maximum length to be interesting”

QUOTE – PERSON NAMEQuote – person details

leisuRe stRategY

50 | Airline Business | October 2013

767-300ERs culled from the Air Canada main-line fl eet. So far Friisdahl says the routes are performing “very well”.

“Air Canada recognised that the growing leisure travel market offered an opportunity to create a largely leisure focused carrier that would operate at a lower cost than the main-line carrier,” explains Friisdahl.

“Air Canada was operating numerous largely leisure routes unprofi tably, and we saw that this was a chance to change that to profi table operations, still with an Air Canada brand,” he adds.

The combination of robust online booking, an excellent safety record and a well estab-lished loyalty programme combined with a low-cost operation gives the Air Canada lei-sure group a “powerful competitive advan-tage”, he adds.

“Air Canada continues to perform very well. Sales are strong as the leisure travel mar-ket continues to grow, and with the addition now of dedicated capacity on Air Canada Rouge the numbers have been very encourag-ing,” he says. “Caribbean travel remains very popular given its quick access from Montreal and Toronto [Air Canada Rouge’s main base of operations] and destinations in Europe are also very popular, in particular Venice with the cruise traveller.”

US-based MLT Vacations – a subsidiary arm of Delta Air Lines that handles Delta Vacations’ tour operations – has experienced a signifi cant shake-up recently. The compa-ny’s relocation to Delta’s headquarters in Atlanta this April was then followed by the prospect of partnering with Virgin Atlantic’s Virgin Holidays branch.

MLT, which not only handles Delta Vaca-tions bookings but United Vacations, Aer-omexico Vacations, Alitalia Vacations, Air France Vacations and Worry-Free Vacations as well, recorded in excess of 600,000 combined customers in 2012, making it – by MLT presi-dent John Caldwell’s estimation – one of the largest tour operators in the USA.

And following the acquisition of Virgin Atlantic by Delta earlier this year, Caldwell plans to develop a close partnership with its leisure arm, Virgin Holidays.

“Our business hub is expanding very nicely. Alitalia, Air France and now of course Virgin [are] really giving us great presence in both leisure and business destinations such as Paris, Rome and London. Our London sales are up 46% compared with last year [ending

31 December 2012] and we are 19% up on the Paris and Rome markets and seeing signifi cant increases in sales to Barcelona,” he says.

Caldwell says 2012 was the “best ever” year for the business, and expects the core markets of package holidays to Mexico and Caribbean to remain popular with customers.

“Some 60% of our business is in Mexico and the Caribbean. We’ve seen some nice growth specifi cally in Jamaica, Aruba, St Lucia [and] the Dominican Republic is really hot right now. Cancun remains our number one destination in Mexico, and we have a strong partnership with Aeromexico in that market,” says Caldwell.

MARKET OUTLOOKAccording to data compiled by Airline Busi-ness, all three of the largest leisure carriers registered a decline in traffi c in 2012, with Thomson Airways recording a fall of 3.1% to 10.7 million, while Air Europa reported an almost 7% drop to just over 8 million. Tho-mas Cook registered an almost 15% decline to 6.8 million passengers.

Nevertheless, several carriers grew their traffi c in 2012 – including Condor, which saw a 7% increase in traffi c to 6.6 million. Nether-lands-based Transavia Airlines saw a 7.6% increase to 5.8 million, while its French sister airline Transavia France’s traffi c also saw a rise in traffi c of 6.3% to 1.7 million.

“In terms of the package holiday sector, we see the three biggest source markets as the UK, Germany and Italy, while the highest growth in arrivals year-on-year are Denmark, Turkey and Romania, which grew by an average of 7% for 2012,” says Nadia Popova, a travel and tourism industry analyst at Euromonitor Inter-national. “Three other markets that are per-forming well are Poland, Bulgaria and Russia, which is really to do with the fact that charter operators are strong players in these markets, and they are bringing in tourists from the USA, Canada and Asia. Charter operators are providing the price and the destinations not necessarily offered by scheduled carriers.”

Popova says charter operators have benefi t-ted from one-off events such as the volcanic ash crisis, the failure of tour operators and the collapse of airlines. All of which is convinc-ing consumers in the UK of the benefi ts of an ATOL-protected holiday.

The leisure sector’s enthusiasm to embrace online and mobile technologies, says Popova – who cites a recent agreement between Ger-man leisure carrier FlyTUI and Travelport to introduce e-tickets – should give it the resil-ience to continue to compete effectively with its low-cost rivals. ■

■

■

Read how the outlook for leisure airlines has evolved from 12 months before:fl ightglobal.com/leisure

No more than three lines in here xxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxx

x%

Thomas Cook recently reported its first positive quarterly result for two years

Rex

Feat

ures

fl ightglobal.com/ab October 2013 | Airline Business | 51

leisuRe RanKings

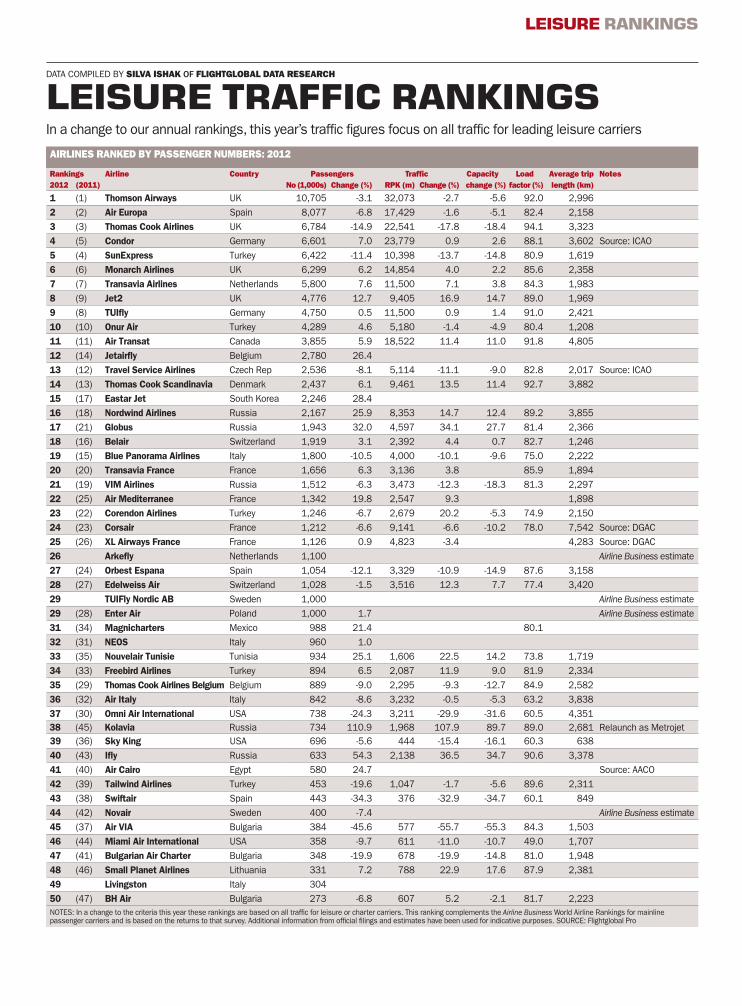

AIRLINES RANKED BY PASSENGER NUMBERS: 2012

Rankings Airline Country Passengers Traffi c Capacity Load Average trip Notes2012 (2011) No (1,000s) Change (%) RPK (m) Change (%) change (%) factor (%) length (km)

1 (1) Thomson Airways UK 10,705 -3.1 32,073 -2.7 -5.6 92.0 2,9962 (2) Air Europa Spain 8,077 -6.8 17,429 -1.6 -5.1 82.4 2,1583 (3) Thomas Cook Airlines UK 6,784 -14.9 22,541 -17.8 -18.4 94.1 3,3234 (5) Condor Germany 6,601 7.0 23,779 0.9 2.6 88.1 3,602 Source: ICAO5 (4) SunExpress Turkey 6,422 -11.4 10,398 -13.7 -14.8 80.9 1,6196 (6) Monarch Airlines UK 6,299 6.2 14,854 4.0 2.2 85.6 2,3587 (7) Transavia Airlines Netherlands 5,800 7.6 11,500 7.1 3.8 84.3 1,9838 (9) Jet2 UK 4,776 12.7 9,405 16.9 14.7 89.0 1,9699 (8) TUIfl y Germany 4,750 0.5 11,500 0.9 1.4 91.0 2,42110 (10) Onur Air Turkey 4,289 4.6 5,180 -1.4 -4.9 80.4 1,20811 (11) Air Transat Canada 3,855 5.9 18,522 11.4 11.0 91.8 4,80512 (14) Jetairfl y Belgium 2,780 26.4 13 (12) Travel Service Airlines Czech Rep 2,536 -8.1 5,114 -11.1 -9.0 82.8 2,017 Source: ICAO14 (13) Thomas Cook Scandinavia Denmark 2,437 6.1 9,461 13.5 11.4 92.7 3,88215 (17) Eastar Jet South Korea 2,246 28.4 16 (18) Nordwind Airlines Russia 2,167 25.9 8,353 14.7 12.4 89.2 3,85517 (21) Globus Russia 1,943 32.0 4,597 34.1 27.7 81.4 2,36618 (16) Belair Switzerland 1,919 3.1 2,392 4.4 0.7 82.7 1,24619 (15) Blue Panorama Airlines Italy 1,800 -10.5 4,000 -10.1 -9.6 75.0 2,22220 (20) Transavia France France 1,656 6.3 3,136 3.8 85.9 1,89421 (19) VIM Airlines Russia 1,512 -6.3 3,473 -12.3 -18.3 81.3 2,29722 (25) Air Mediterranee France 1,342 19.8 2,547 9.3 1,89823 (22) Corendon Airlines Turkey 1,246 -6.7 2,679 20.2 -5.3 74.9 2,15024 (23) Corsair France 1,212 -6.6 9,141 -6.6 -10.2 78.0 7,542 Source: DGAC25 (26) XL Airways France France 1,126 0.9 4,823 -3.4 4,283 Source: DGAC26 Arkefl y Netherlands 1,100 Airline Business estimate27 (24) Orbest Espana Spain 1,054 -12.1 3,329 -10.9 -14.9 87.6 3,15828 (27) Edelweiss Air Switzerland 1,028 -1.5 3,516 12.3 7.7 77.4 3,42029 TUIFly Nordic AB Sweden 1,000 Airline Business estimate29 (28) Enter Air Poland 1,000 1.7 Airline Business estimate31 (34) Magnicharters Mexico 988 21.4 80.132 (31) NEOS Italy 960 1.0 33 (35) Nouvelair Tunisie Tunisia 934 25.1 1,606 22.5 14.2 73.8 1,71934 (33) Freebird Airlines Turkey 894 6.5 2,087 11.9 9.0 81.9 2,33435 (29) Thomas Cook Airlines Belgium Belgium 889 -9.0 2,295 -9.3 -12.7 84.9 2,58236 (32) Air Italy Italy 842 -8.6 3,232 -0.5 -5.3 63.2 3,83837 (30) Omni Air International USA 738 -24.3 3,211 -29.9 -31.6 60.5 4,35138 (45) Kolavia Russia 734 110.9 1,968 107.9 89.7 89.0 2,681 Relaunch as Metrojet39 (36) Sky King USA 696 -5.6 444 -15.4 -16.1 60.3 63840 (43) Ifl y Russia 633 54.3 2,138 36.5 34.7 90.6 3,37841 (40) Air Cairo Egypt 580 24.7 Source: AACO42 (39) Tailwind Airlines Turkey 453 -19.6 1,047 -1.7 -5.6 89.6 2,31143 (38) Swiftair Spain 443 -34.3 376 -32.9 -34.7 60.1 84944 (42) Novair Sweden 400 -7.4 Airline Business estimate45 (37) Air VIA Bulgaria 384 -45.6 577 -55.7 -55.3 84.3 1,50346 (44) Miami Air International USA 358 -9.7 611 -11.0 -10.7 49.0 1,70747 (41) Bulgarian Air Charter Bulgaria 348 -19.9 678 -19.9 -14.8 81.0 1,94848 (46) Small Planet Airlines Lithuania 331 7.2 788 22.9 17.6 87.9 2,38149 Livingston Italy 30450 (47) BH Air Bulgaria 273 -6.8 607 5.2 -2.1 81.7 2,223NOTES: In a change to the criteria this year these rankings are based on all traffi c for leisure or charter carriers. This ranking complements the Airline Business World Airline Rankings for mainline passenger carriers and is based on the returns to that survey. Additional information from offi cial fi lings and estimates have been used for indicative purposes. SOURCE: Flightglobal Pro

DATA COMPILED BY SILVA ISHAK OF FLIGHTGLOBAL DATA RESEARCHDATA COMPILED BY LLOYD DUNNING-MITCHELL AND MICHAEL COX OF FLIGHTGLOBAL DATA RESEARCH ANALYSIS BY FLIGHTGLOBAL INSIGHT

leisuRe tRaFFic RanKingsIn a change to our annual rankings, this year’s traffi c fi gures focus on all traffi c for leading leisure carriers

nb: notes FRoM last YeaRNOTES: This ranking complements the Airline Business World Airline Rankings for mainline passenger carriers and is based on the returns to that survey. Additional information comes from offi cial fi lings and estimates have been used for indicative purpose. Figures for charter carriers include all passenger traffi c, while fi gures for scheduled carriers include only the charter element of their passenger traffi c. RPK=revenue passenger kilmetres, ASK=available seat kilometres, 1 mile=1.609km. *Edelweiss Air fi gures includes codeshare fl ights with Swiss.

Regionals subject

flightglobal.com/ab6 | Airline Business | February 2012

Flightglobal InsightQuadrant House, The Quadrant, Sutton, Surrey, SM2 5AS, UKTel: +44 20 8652 8724 Email: [email protected] Web: www.flightglobal.com/insight