Embed Size (px)

Citation preview

Kick Start Your Fraud Prevention Program

What To Do, How To Do It

and

How We Can Help!

Shannon Walker

•Shannon Walker is the founder and CEO of Whistleblower Security Inc., an ethics and risk management company with clients worldwide, that protects and shelters organizations by allowing employees to anonymously report fraud, embezzlement, harassment, and other workplace misconduct and ethics violations.

•Shannon founded WhistleBlower Security to assist organizations in creating a more transparent and accountable environment for their employees and other stakeholders. WhistleBlower Security delivers anonymous ethics hotline and risk reporting services on a global basis meeting regulatory and compliance needs and improving an organization's culture and commitment to long-term sustainability and growth.

Key Highlights

• Fraud Statistics

• Types of Frauds

• Red Flags

• Characteristics of Fraudulent Employees

• Protecting Your Assets

• Fraud Prevention Tips

• Improving Your Anti-Fraud Programming

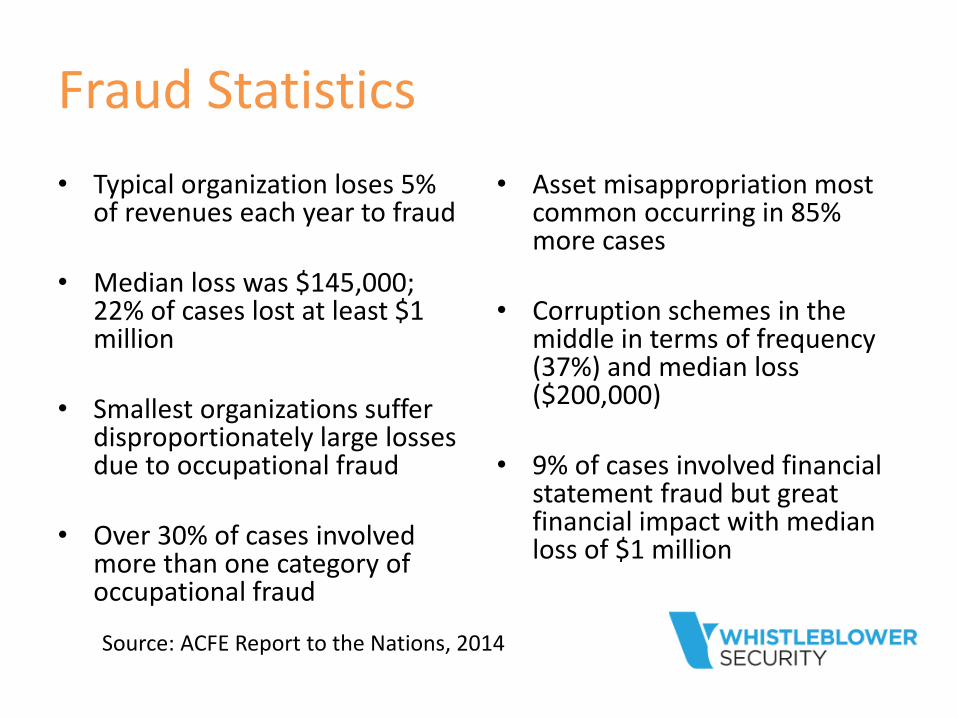

Fraud Statistics

• Typical organization loses 5% of revenues each year to fraud

• Median loss was $145,000; 22% of cases lost at least $1 million

• Smallest organizations suffer disproportionately large losses due to occupational fraud

• Over 30% of cases involved more than one category of occupational fraud

• Asset misappropriation most common occurring in 85% more cases

• Corruption schemes in the middle in terms of frequency (37%) and median loss ($200,000)

• 9% of cases involved financial statement fraud but great financial impact with median loss of $1 million

Source: ACFE Report to the Nations, 2014

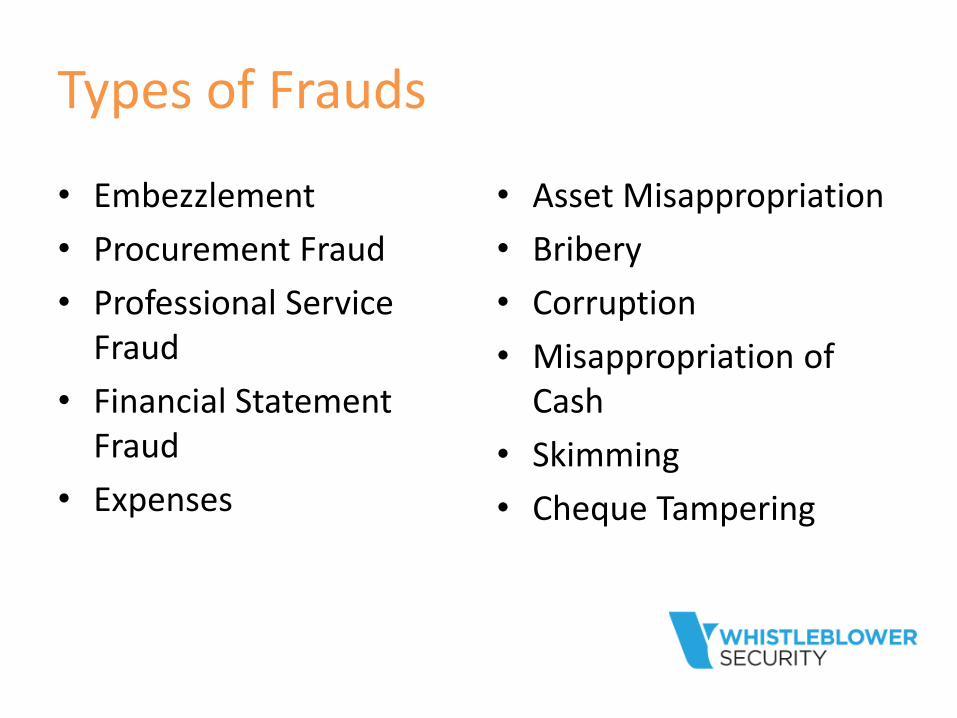

Types of Frauds

• Embezzlement

• Procurement Fraud

• Professional Service Fraud

• Financial Statement Fraud

• Expenses

• Asset Misappropriation

• Bribery

• Corruption

• Misappropriation of Cash

• Skimming

• Cheque Tampering

Behavioral Red Flags

Source: Association of Certified Fraud Examiners

Fraud Statistics

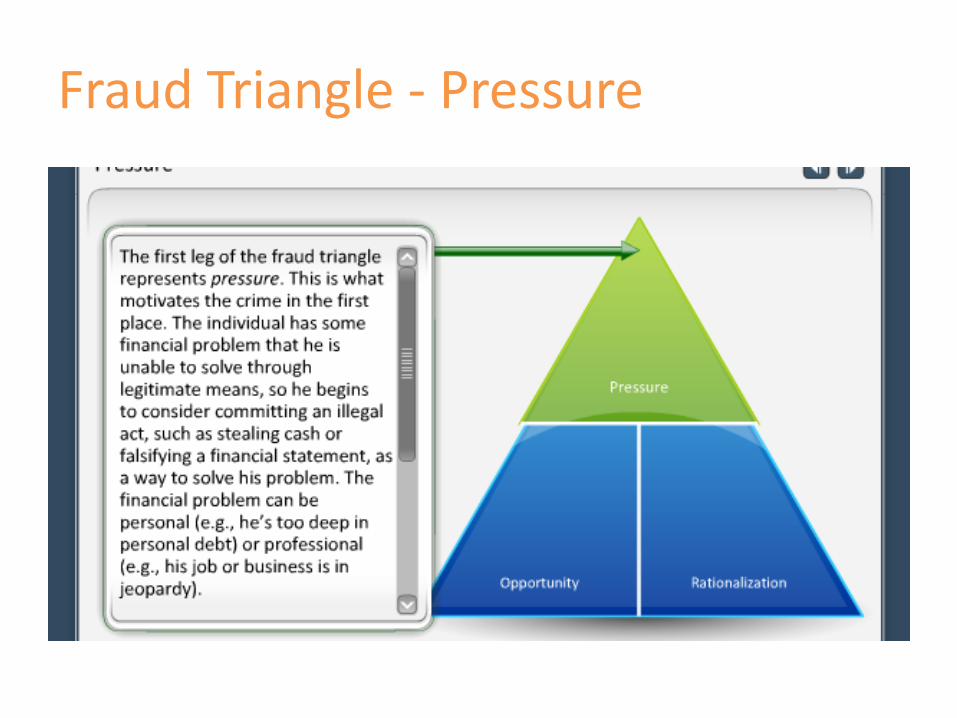

Fraud Triangle - Pressure

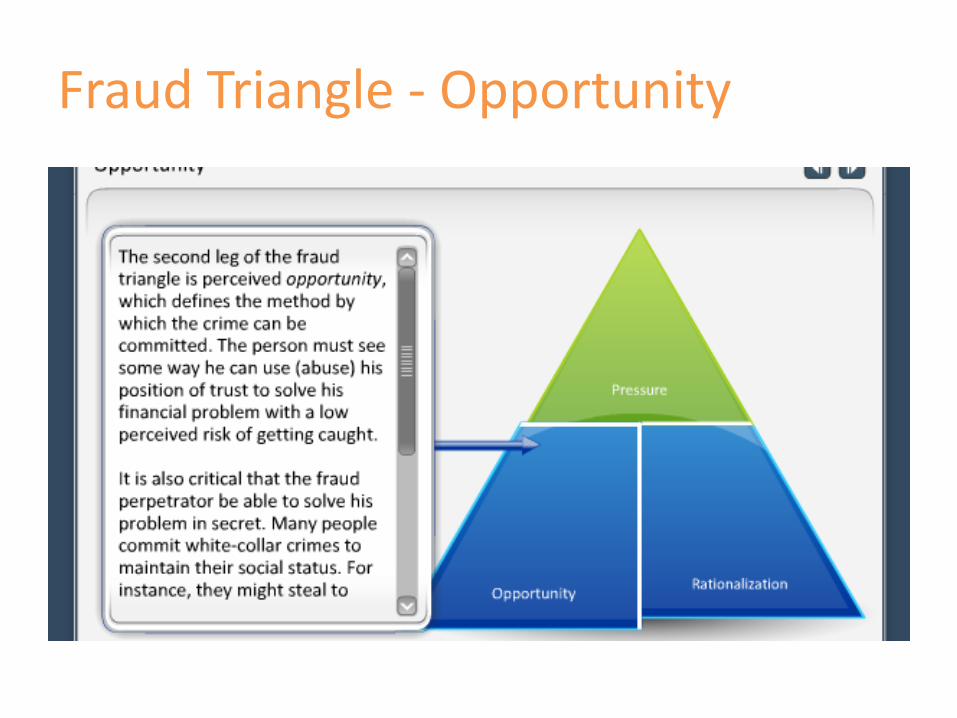

Fraud Triangle - Opportunity

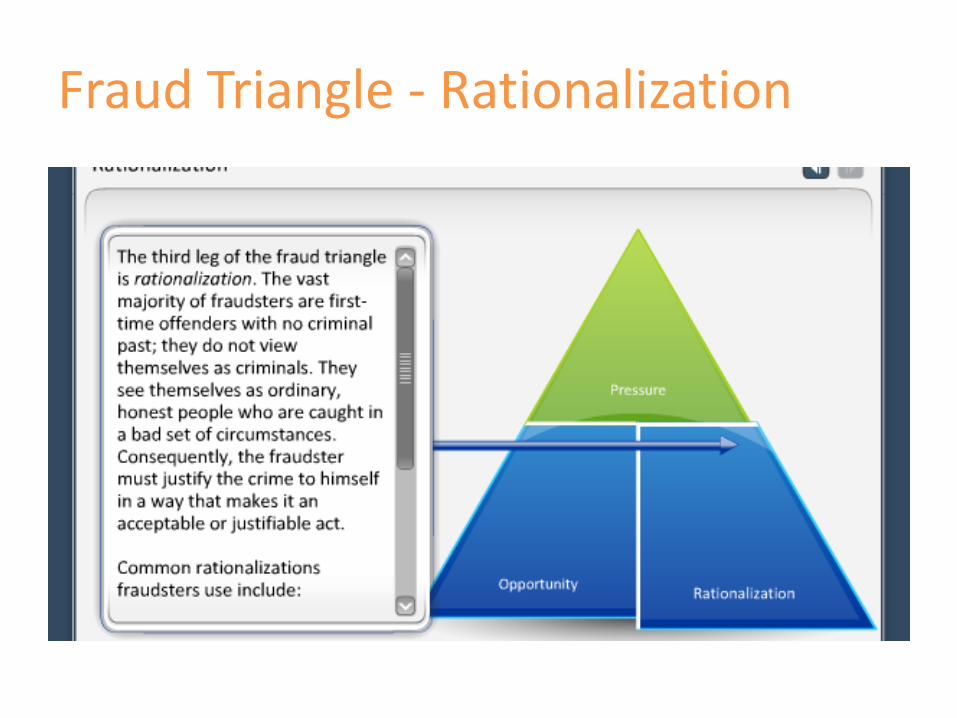

Fraud Triangle - Rationalization

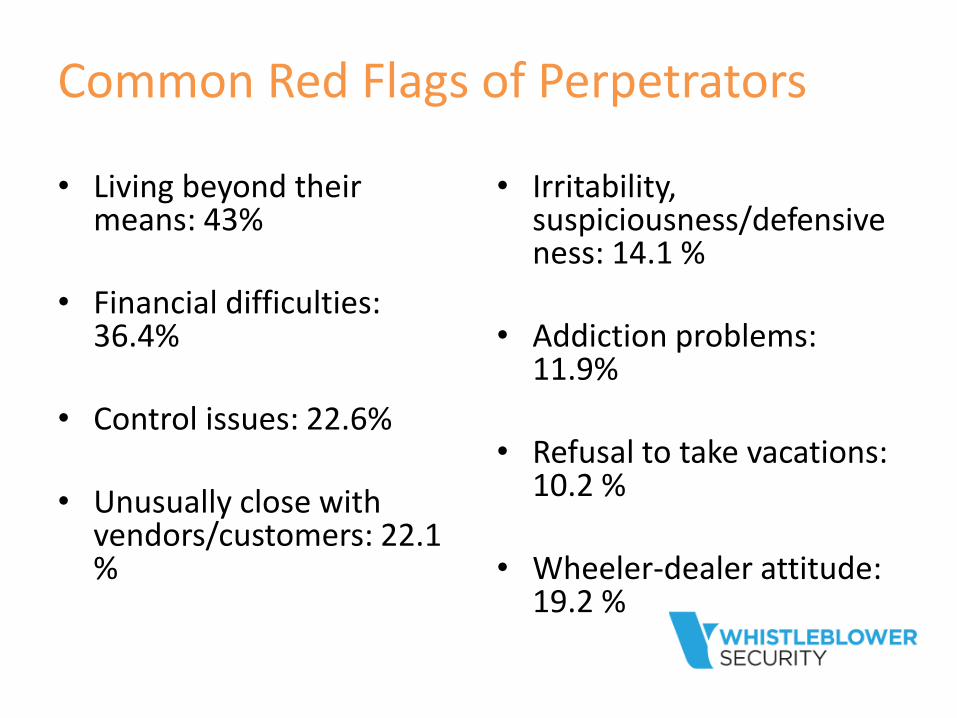

Common Red Flags of Perpetrators

• Living beyond their means: 43%

• Financial difficulties: 36.4%

• Control issues: 22.6%

• Unusually close with vendors/customers: 22.1 %

• Irritability, suspiciousness/defensiveness: 14.1 %

• Addiction problems: 11.9%

• Refusal to take vacations: 10.2 %

• Wheeler-dealer attitude: 19.2 %

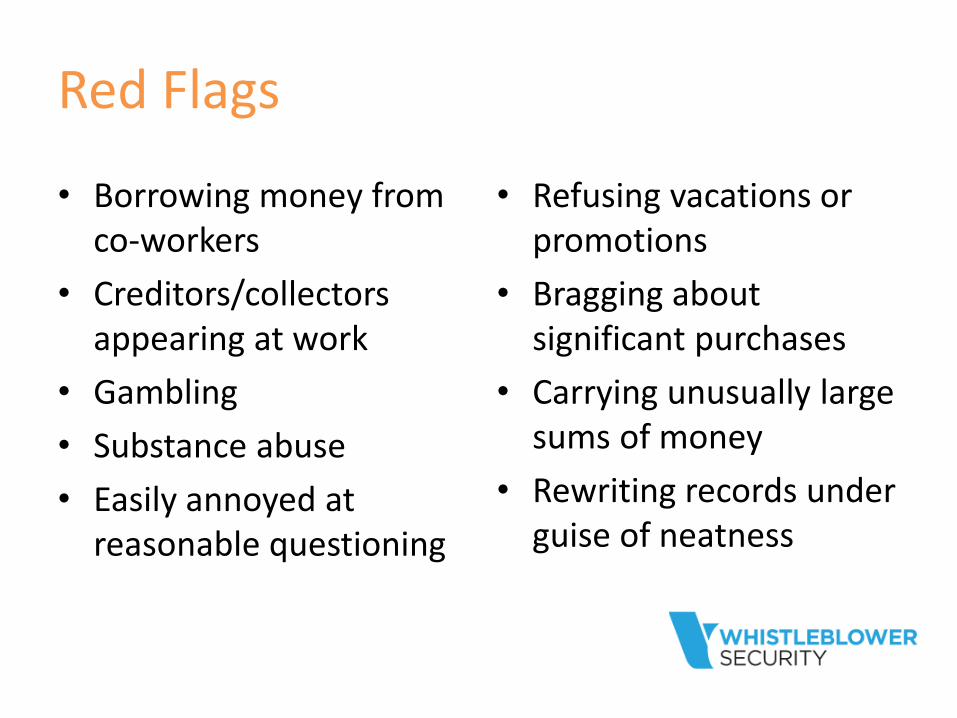

Red Flags

• Borrowing money from co-workers

• Creditors/collectors appearing at work

• Gambling

• Substance abuse

• Easily annoyed at reasonable questioning

• Refusing vacations or promotions

• Bragging about significant purchases

• Carrying unusually large sums of money

• Rewriting records under guise of neatness

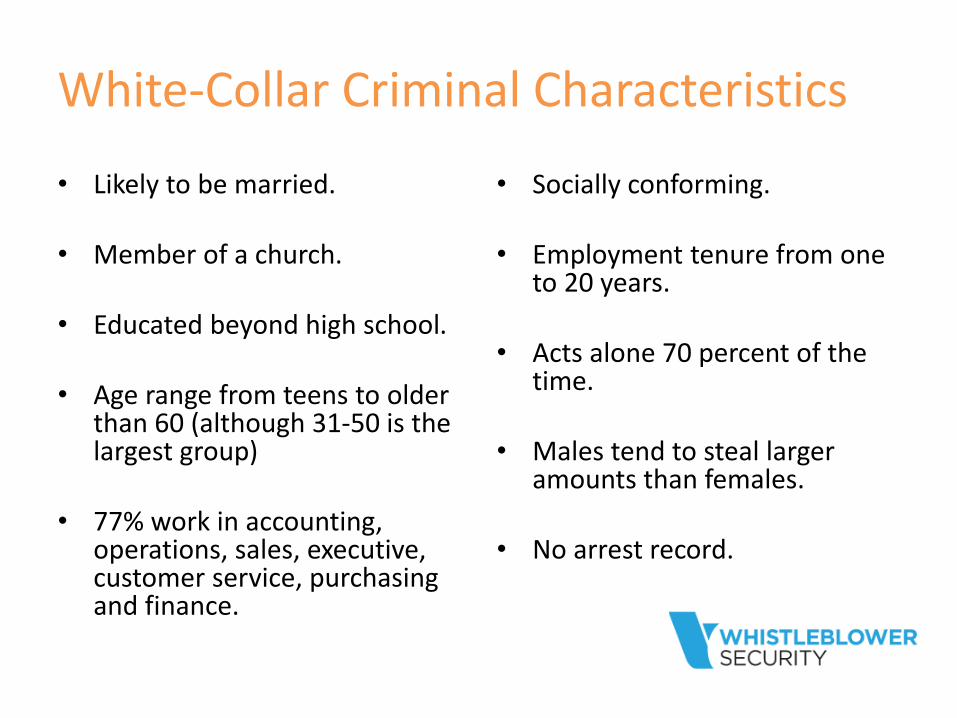

White-Collar Criminal Characteristics

• Likely to be married.

• Member of a church.

• Educated beyond high school.

• Age range from teens to older than 60 (although 31-50 is the largest group)

• 77% work in accounting, operations, sales, executive, customer service, purchasing and finance.

• Socially conforming.

• Employment tenure from one to 20 years.

• Acts alone 70 percent of the time.

• Males tend to steal larger amounts than females.

• No arrest record.

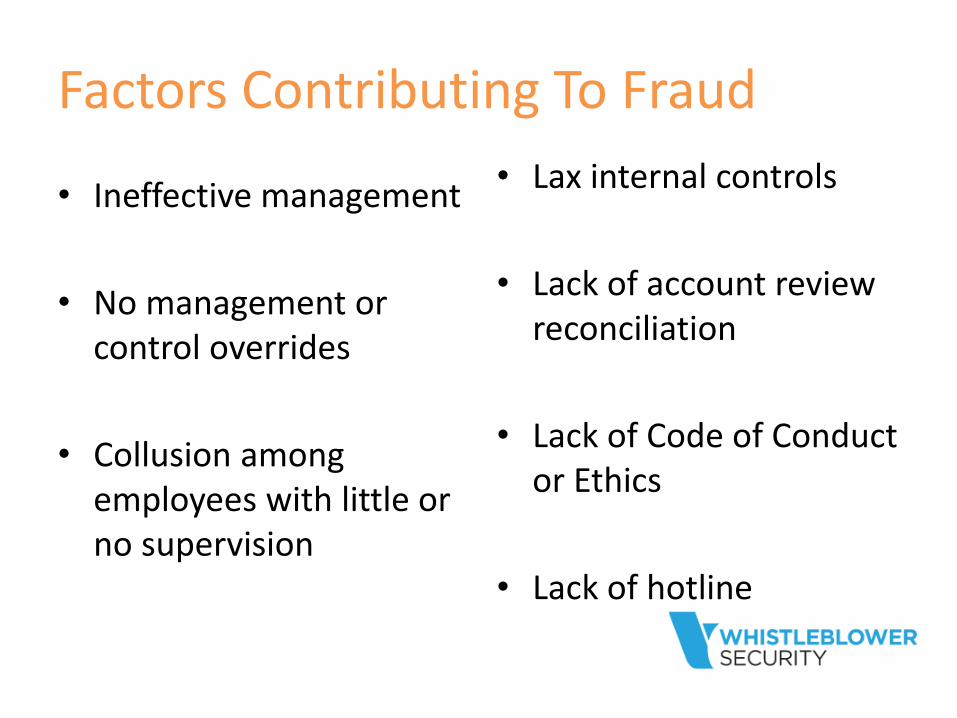

Factors Contributing To Fraud

• Ineffective management

• No management or control overrides

• Collusion among employees with little or no supervision

• Lax internal controls

• Lack of account review reconciliation

• Lack of Code of Conduct or Ethics

• Lack of hotline

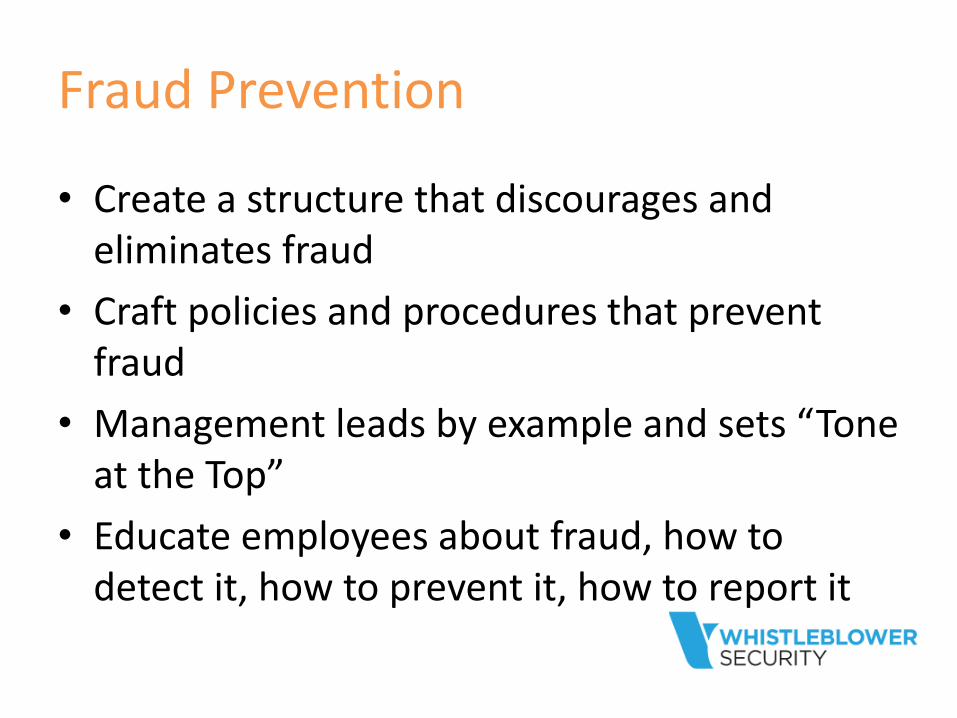

Fraud Prevention

• Create a structure that discourages and eliminates fraud

• Craft policies and procedures that prevent fraud

• Management leads by example and sets “Tone at the Top”

• Educate employees about fraud, how to detect it, how to prevent it, how to report it

Commit the Resources

• Small businesses more susceptible because of lack of resources for internal controls, audits

• Often misplaced sense of trust in small organizations

• Ensure tools are put in place

• Invest in IT security

• Conduct surprise audits and inventory counts

10 Ways to Improve Fraud Detection

① Use a HotlineWhistleBlower tips are the most common fraud detection technique

② Multiple Report MechanismsWhether by phone, email, web portal, mail or fax, all stakeholders can report on fraud

③ Outsourced HotlineThird-party anonymous hotlines ensure employees feel safe and secure when reporting

④ Training EmployeesTrain on what fraud looks like, what to look our for and how to report it

① Train AgainMost of us need a little repetition. It’s okay. Keep the training going all the time

and use real-life scenarios to put it in context for your employees

Improving Fraud Detection

⑥ Fraud TriangleLook for behavioral traits, red flags

⑦ Reduce OpportunitySegregate sensitive duties amongst more than one employee

⑧ Protect AssetsFrom petty cash to company issued credit cards, reconcile everything

⑨ Spot AuditImplement spot audit programs and conduct random audits on particular

sensitive areas

⑩ Policies Get your policies in place, make them available, and ensure all employees from

the top down, obey them.

Internal Controls = Fraud Prevention

• Important consideration is:

– Company’s attitude towards fraud

– Internal Controls

– Ethical organizational culture

Provide self assessment check lists to departments and management and then go through process of reconciliation

Internal Controls

• Fluid set of tools involving business, technology and environment

• Assess and review current policies, protocols

• Comprehensiveness of network across departments

• Ensure ownership of controls is shared throughout the organization

Internal Controls

• Effective internal controls comprised of team:

– Human Resources

– Compliance

– Investigations

– Audit

– General Counsel

– Senior Management

– Security (information and physical)

Internal Controls

• Given fluid environment, key to review, evaluate, test and re-introduce on a regular basis

• Ensure interdisciplinary team is in place

• Ensure open-door policy and speak up culture

Communication Protocols

• Timely notification and sharing of events

• Regular interaction and communications between departments is paramount

• Ensure employees know of hotline or complaint procedures and how to file a report

• Include mandatory reporting of fraud concerns in all related policies

• Promotion of hotline through handbook, newsletter, lunch and learns and company website

• Fraud awareness training provided to all staff to help spot red flags of fraud

Post Mortem- Event Analysis

• Ask the tough questions

• Was there a policy, procedure, guideline in place to address the situation?

• If so, was the employee not versed in the guideline?

• Corrective action and education needs to be taken to circumvent same situation in the future

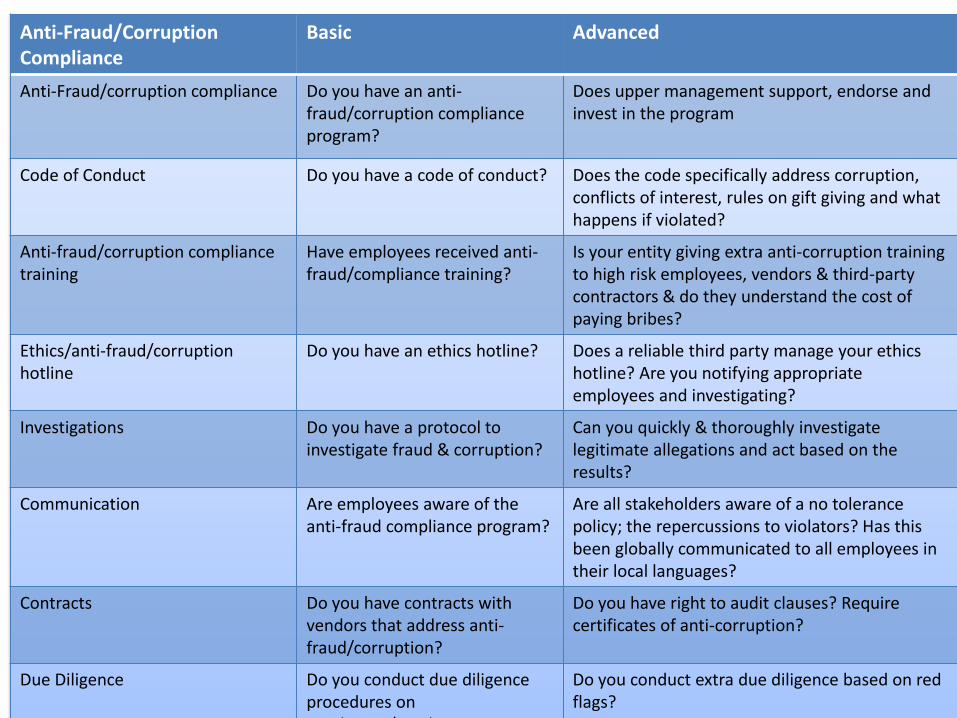

Anti-Fraud/CorruptionCompliance

Basic Advanced

Anti-Fraud/corruption compliance Do you have an anti-fraud/corruption compliance program?

Does upper management support, endorse and invest in the program

Code of Conduct Do you have a code of conduct? Does the code specifically address corruption, conflicts of interest, rules on gift giving and what happens if violated?

Anti-fraud/corruption compliance training

Have employees received anti-fraud/compliance training?

Is your entity giving extra anti-corruption training to high risk employees, vendors & third-party contractors & do they understand the cost of paying bribes?

Ethics/anti-fraud/corruptionhotline

Do you have an ethics hotline? Does a reliable third party manage your ethics hotline? Are you notifying appropriate employees and investigating?

Investigations Do you have a protocol to investigate fraud & corruption?

Can you quickly & thoroughly investigatelegitimate allegations and act based on the results?

Communication Are employees aware of the anti-fraud compliance program?

Are all stakeholders aware of a no tolerance policy; the repercussions to violators? Has this been globally communicated to all employees in their local languages?

Contracts Do you have contracts with vendors that address anti-fraud/corruption?

Do you have right to audit clauses? Require certificates of anti-corruption?

Due Diligence Do you conduct due diligence procedures on employees/vendors

Do you conduct extra due diligence based on red flags?

Consequences of Lack Of Diligence

• Loss of reputation

• Fraud losses

• Financial instability

• Plummeting employee morale

• Regulatory fines

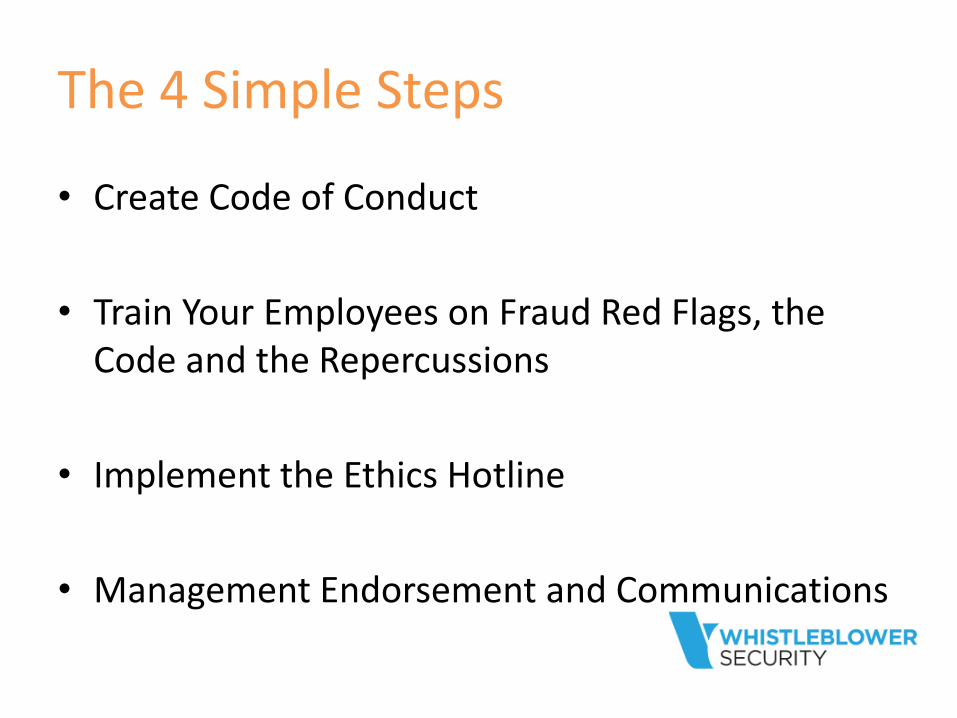

The 4 Simple Steps

• Create Code of Conduct

• Train Your Employees on Fraud Red Flags, the Code and the Repercussions

• Implement the Ethics Hotline

• Management Endorsement and Communications

Questions?

Get in Touch:

Shannon Walker

WhistleBlower Security

www.whistleblowersecurity.com

604.921.6875