Embed Size (px)

Citation preview

Fraud Prevention for Nonprofits:Avoiding Fraud Schemes and Fraudsters

Richard Wolf, CPA, CGMA, CFE

Introductions

• CPA, CGMA, CFE

• Principal at Gross Mendelsohn

• 19 years of public accounting experience in the nonprofit sector

Today You’ll Learn

• Why nonprofit fraud education matters

• Common fraud schemes in nonprofits

• Why some employees commit fraud

• General fraud prevention and deterrence

• What to do if an issue is discovered

WHY NONPROFIT FRAUDEDUCATION MATTERS

Susceptibility

Disclosure requirements

Cost

Public image

Susceptibility

Disclosure requirements

Cost

Public image

Susceptibility

Disclosure requirements

Cost

Public image

Susceptibility

Disclosure requirements

Cost

Public image

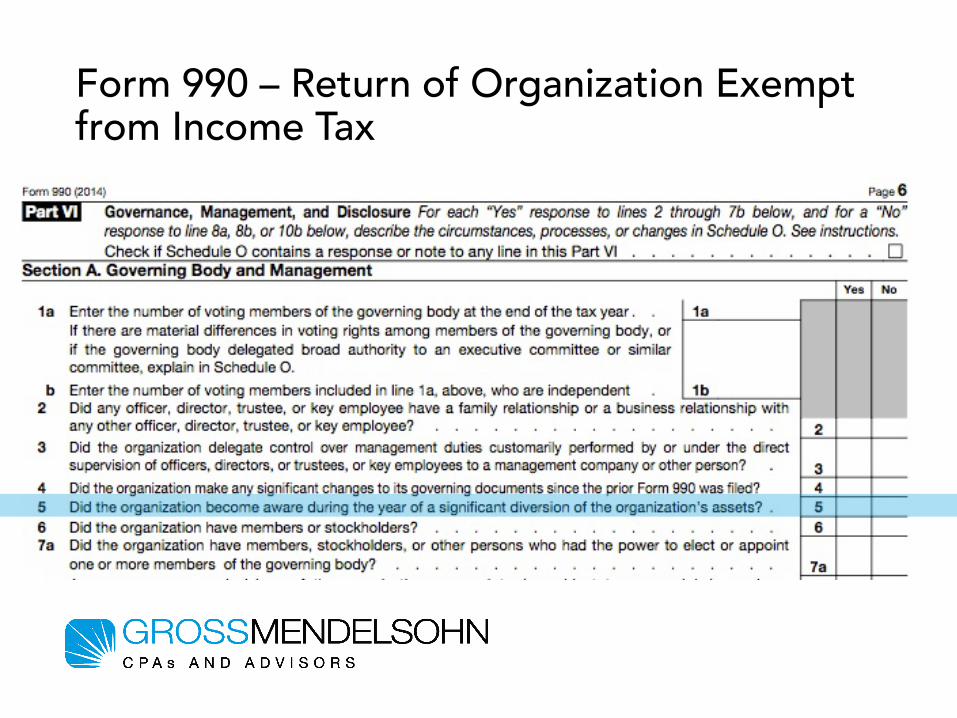

Form 990 – Return of Organization Exempt from Income Tax

Nonprofits must explain thenature of a diversion of assets.

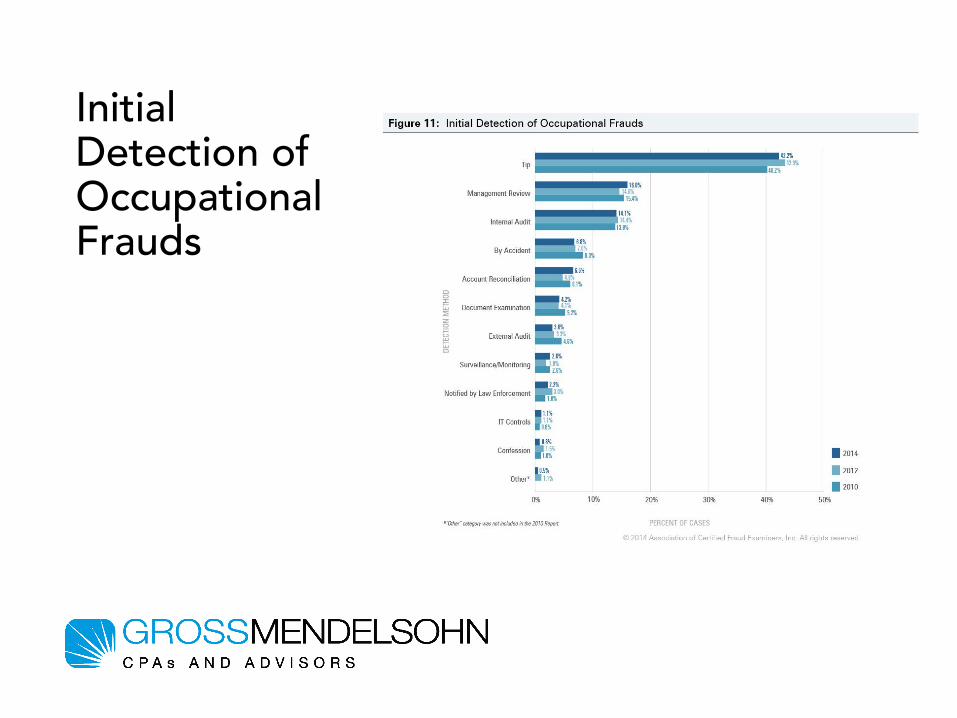

Initial Detection of Occupational Frauds

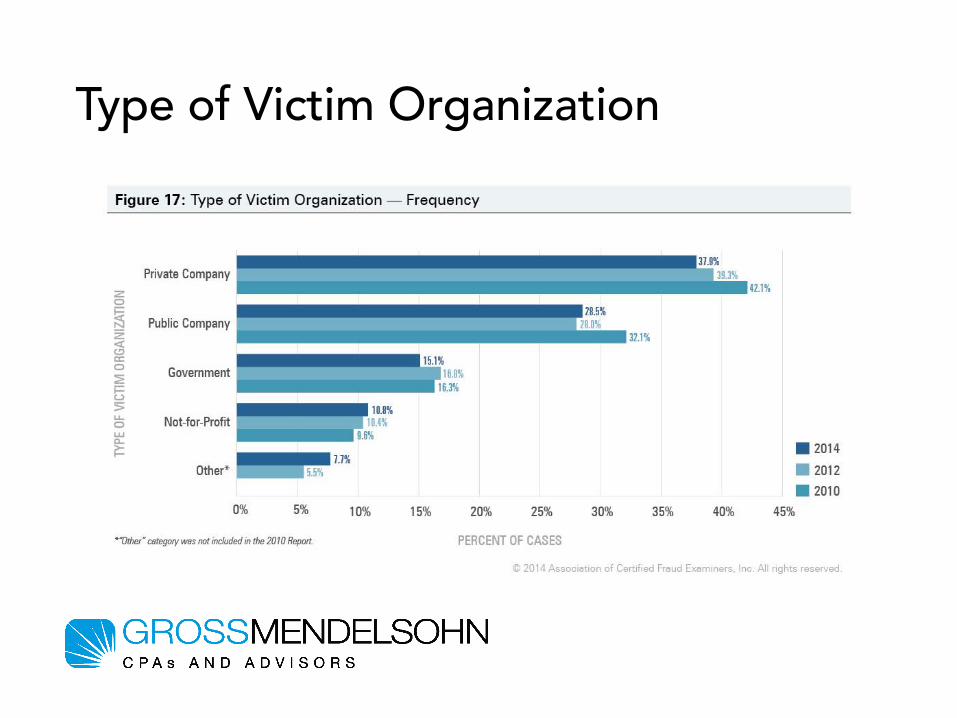

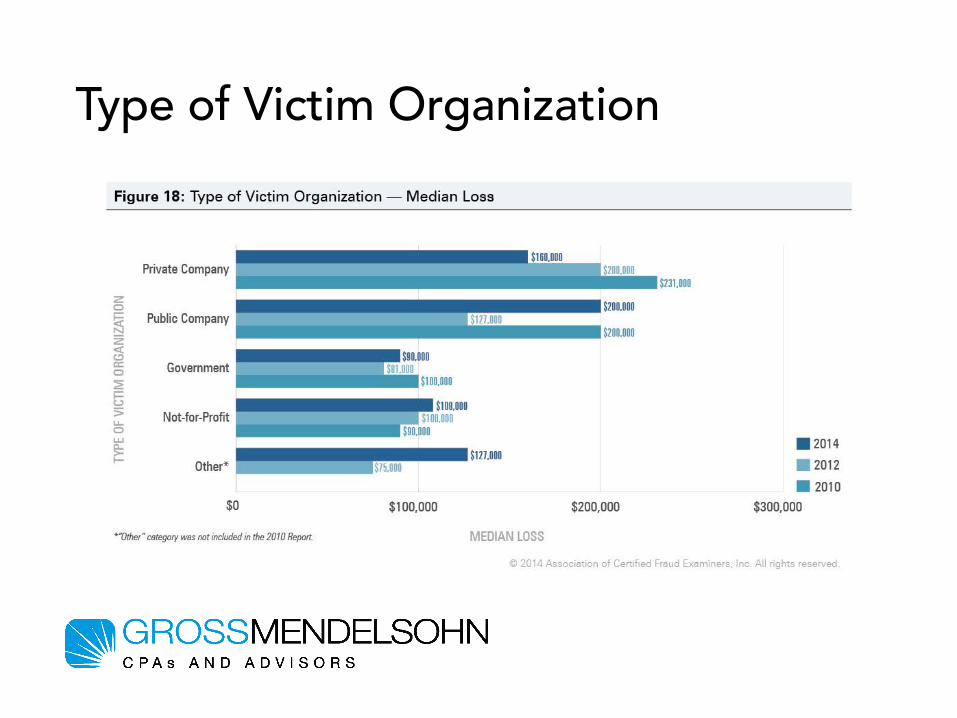

Type of Victim Organization

Type of Victim Organization

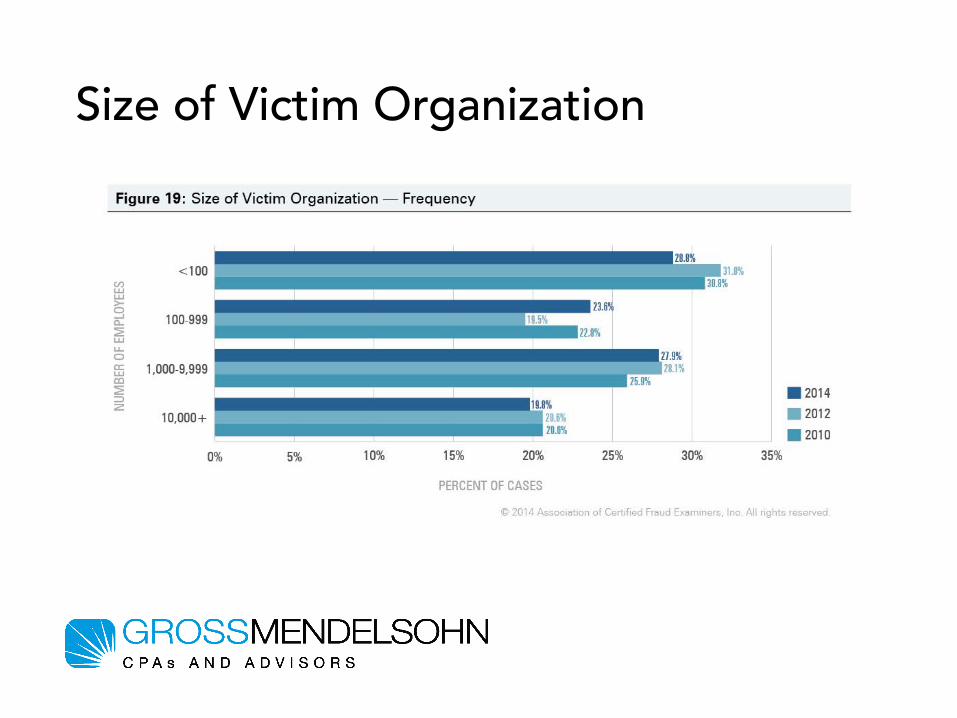

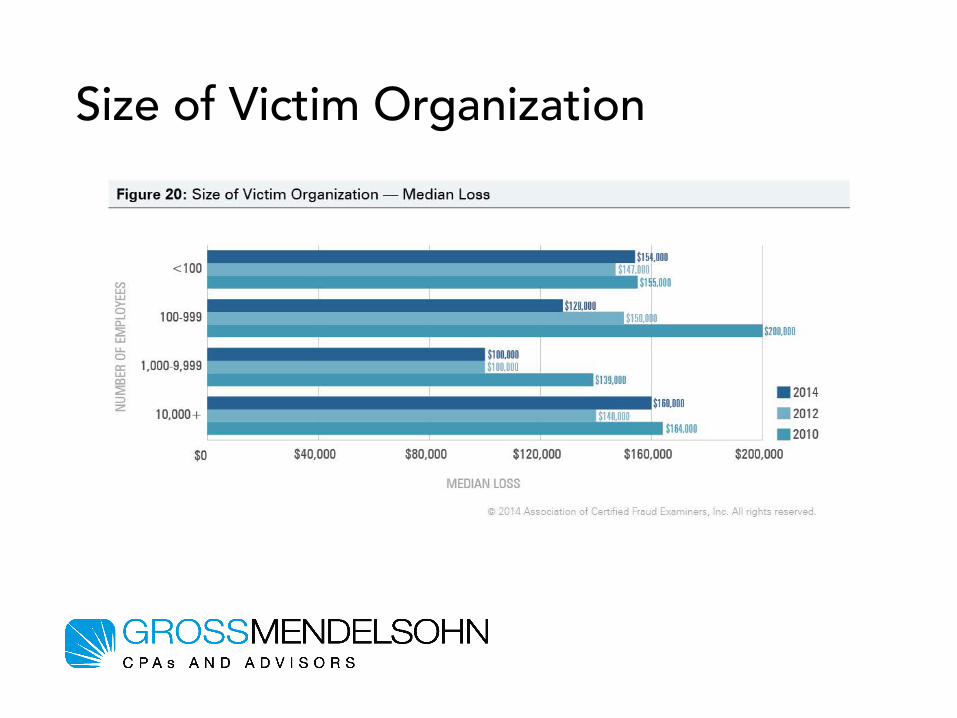

Size of Victim Organization

Size of Victim Organization

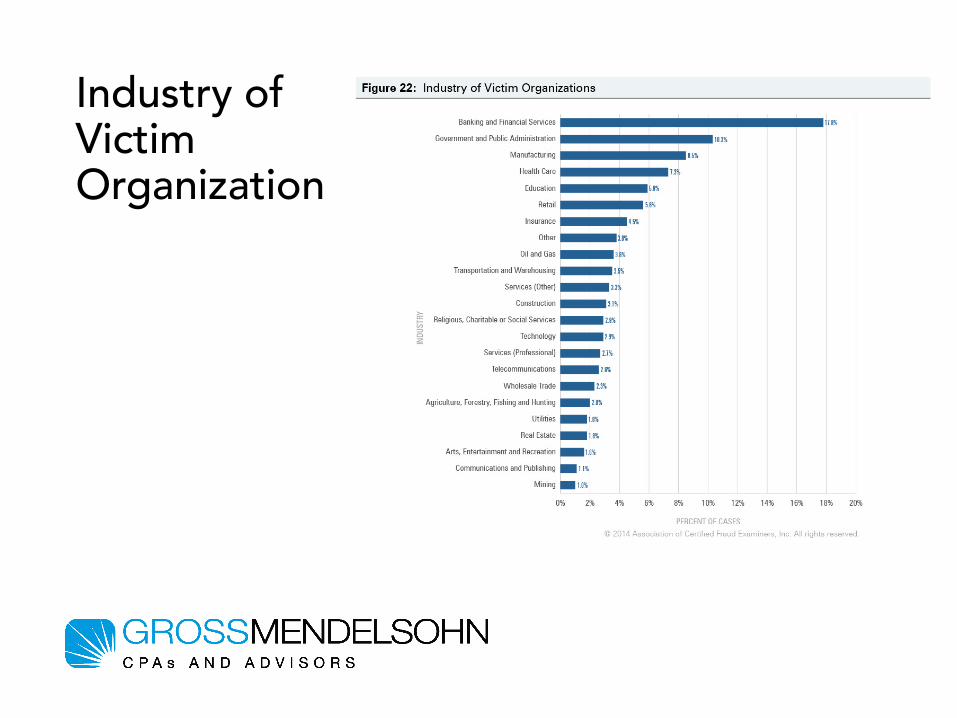

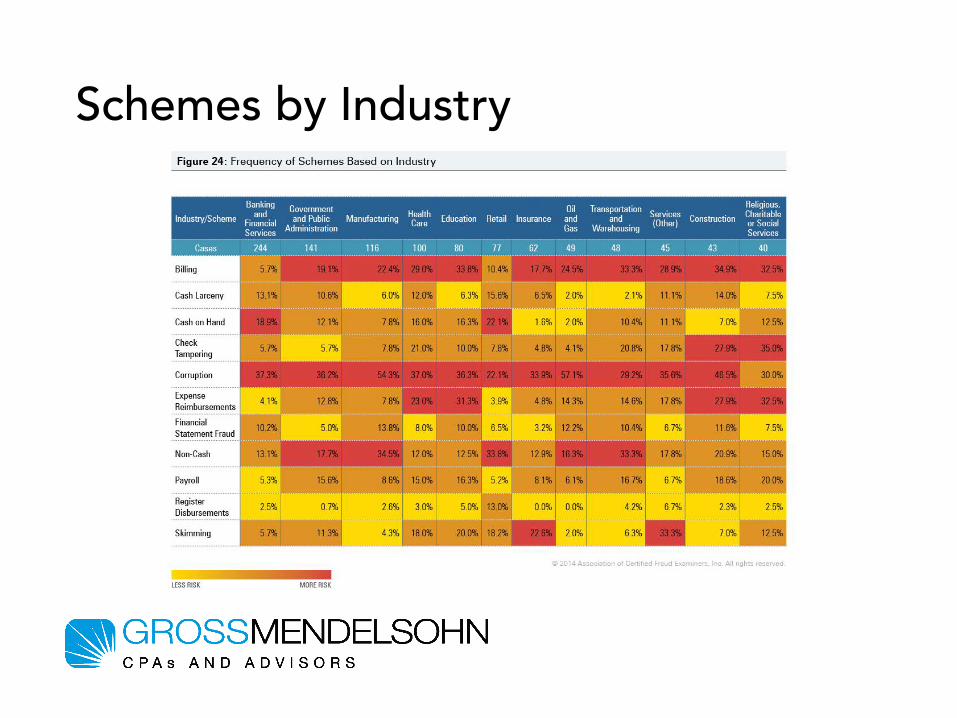

Industry of Victim Organization

Schemes by Industry

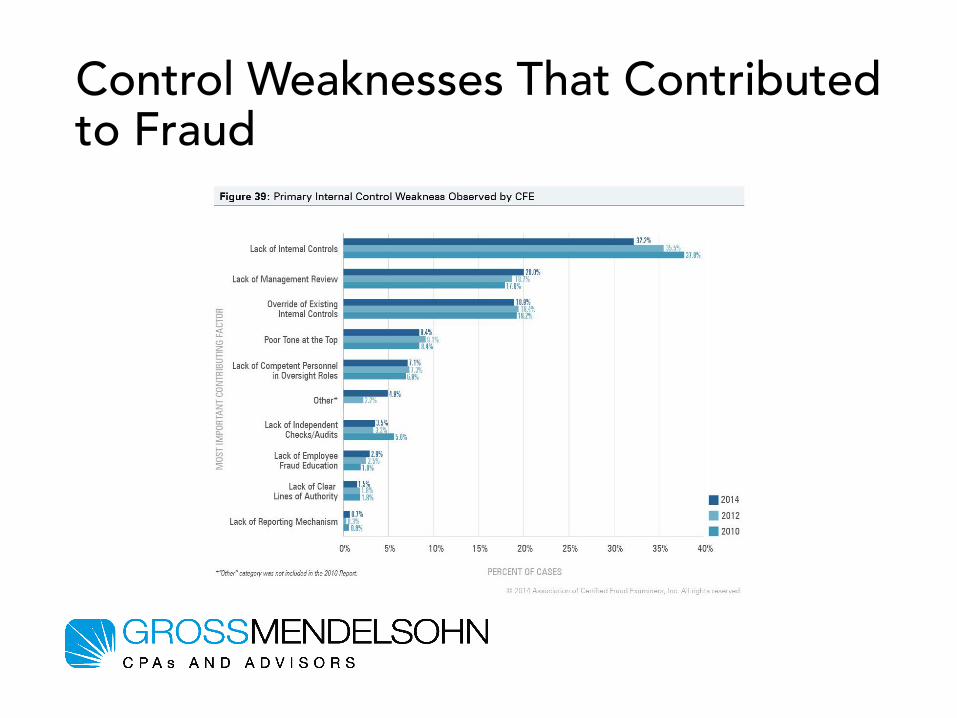

Control Weaknesses That Contributed to Fraud

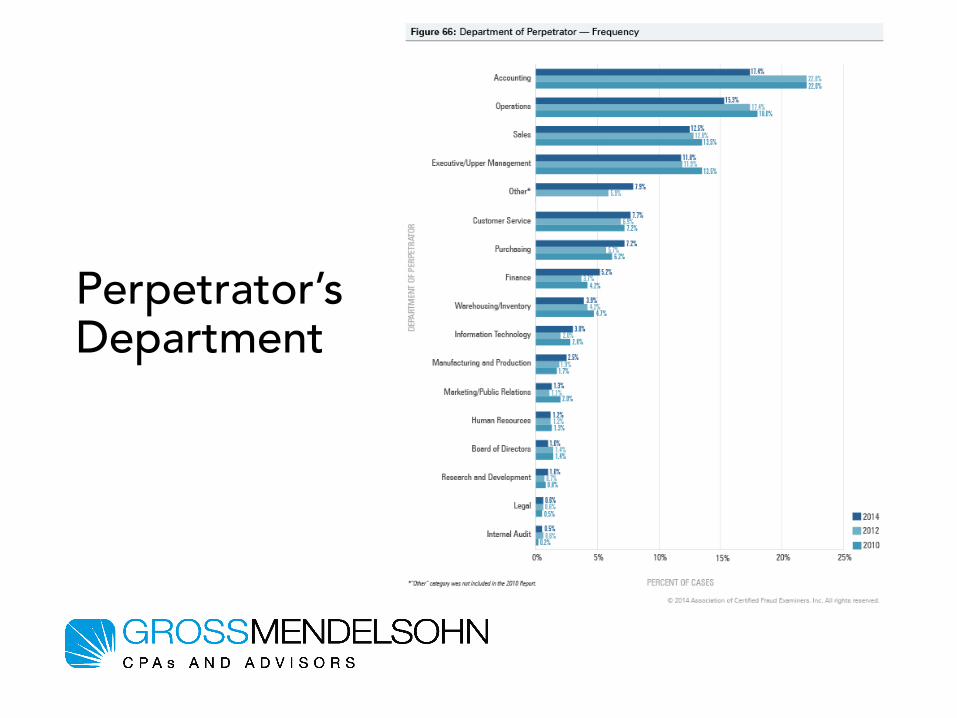

Perpetrator’s Department

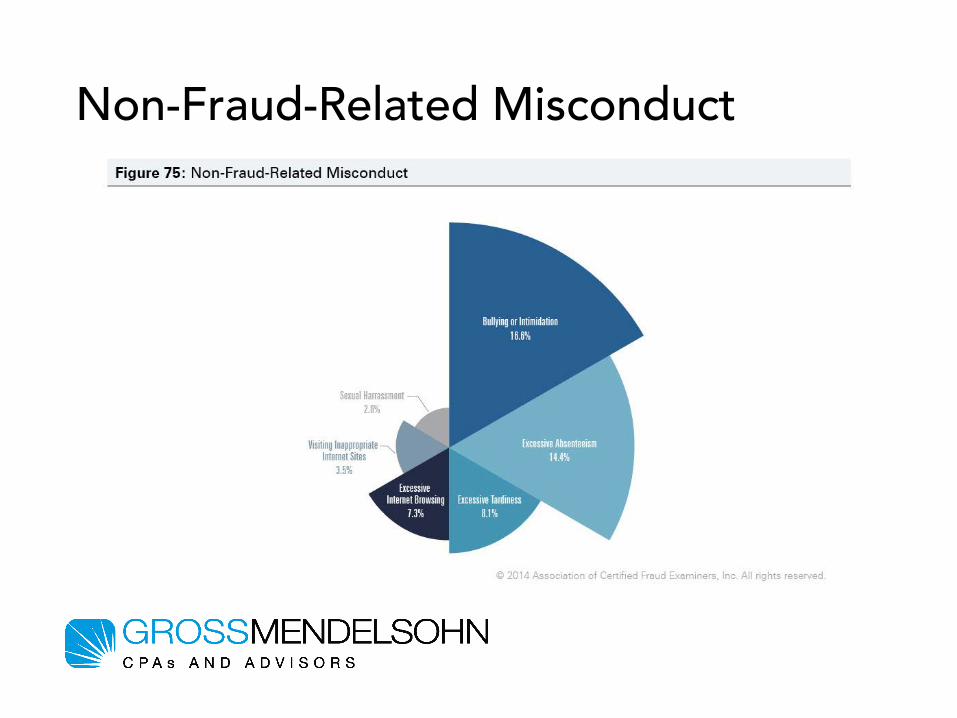

Non-Fraud-Related Misconduct

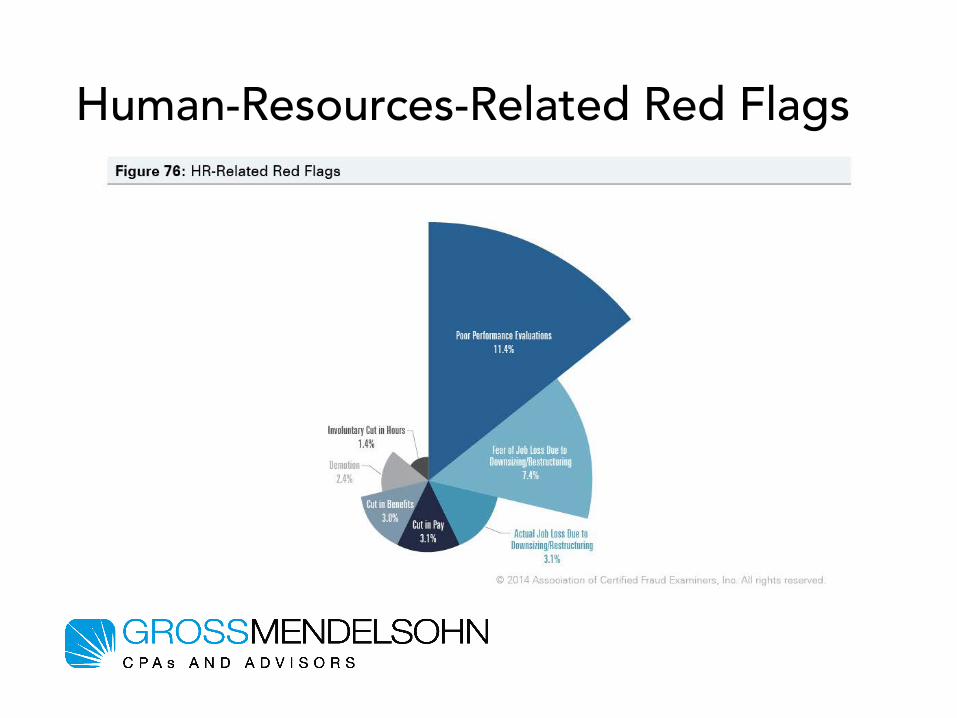

Human-Resources-Related Red Flags

COMMON FRAUD SCHEMES INNONPROFITS

Billing Schemes

False invoicing via shell companies

False invoicing via non-accomplice vendors

Personal purchases with company funds

Billing Schemes

False invoicing via shell companies

False invoicing via non-accomplice vendors

Personal purchases with company funds

Billing Schemes

False invoicing via shell companies

False invoicing via non-accomplice vendors

Personal purchases with company funds

Billing Schemes

False invoicing via shell companies

False invoicing via non-accomplice vendors

Personal purchases with company funds

Red Flags forBilling Schemes

Detection of Billing Schemes

Fraud Prevention: Billing Schemes

• Review vendor list• Approval by multiple employees• Analyze vendor purchase

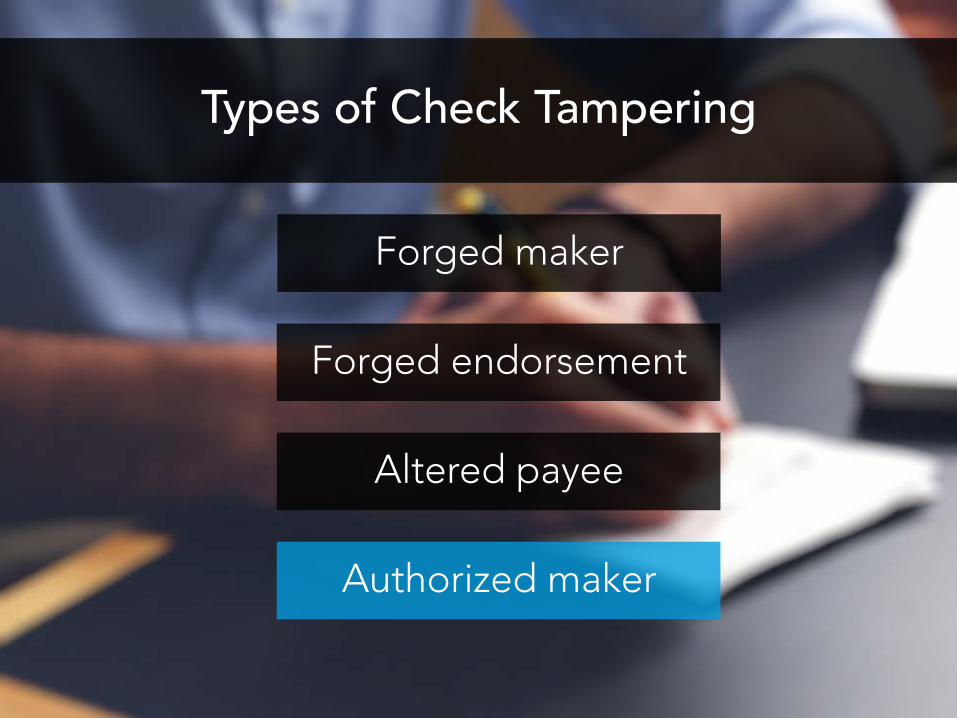

Types of Check Tampering

Forged maker

Forged endorsement

Altered payee

Authorized maker

Types of Check Tampering

Forged maker

Forged endorsement

Altered payee

Authorized maker

Types of Check Tampering

Forged maker

Forged endorsement

Altered payee

Authorized maker

Types of Check Tampering

Forged maker

Forged endorsement

Altered payee

Authorized maker

Types of Check Tampering

Forged maker

Forged endorsement

Altered payee

Authorized maker

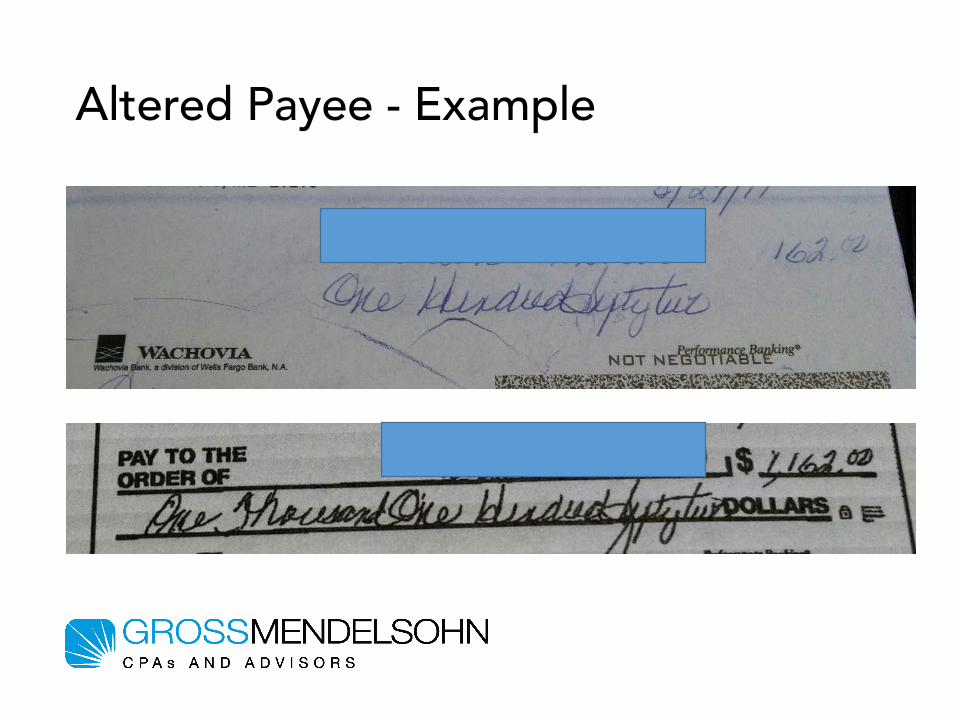

Altered Payee - Example

The majority of check tampering schemes do not consist of a single

occurrence but instead continue over an extended period of time.

Red Flags forCheck Tampering

Schemes

Detection of Check Tampering

• Account analysis through bank cut-off statements or online access

• Bank reconciliations• Examine for possible alterations• Examine cancelled checks and review

endorsements

Fraud Prevention: Check Tampering

• Bank assisted controls • Physical tampering prevention on checks• Avoid pre-signing checks• Check cutting• Mail delivery

Expense Reimbursement Schemes

Mischaracterized expenses

Overstated expenses

Fictitious expenses

Multiple reimbursements

Expense Reimbursement Schemes

Mischaracterized expenses

Overstated expenses

Fictitious expenses

Multiple reimbursements

Expense Reimbursement Schemes

Mischaracterized expenses

Overstated expenses

Fictitious expenses

Multiple reimbursements

Expense Reimbursement Schemes

Mischaracterized expenses

Overstated expenses

Fictitious expenses

Multiple reimbursements

Expense Reimbursement Schemes

Mischaracterized expenses

Overstated expenses

Fictitious expenses

Multiple reimbursements

Detection of Expense Reimbursement Schemes

• Review and analysis of expense accounts• Detailed review of expense reports

Fraud Prevention: Expense Reimbursement Schemes

• Clearly defined expense reimbursement policies and procedures

• Detailed review of expense reports

Types of Payroll Fraud

Ghost employee schemes

Falsified hours and salary schemes

Commission schemes

Types of Payroll Fraud

Ghost employee schemes

Falsified hours and salary schemes

Commission schemes

Types of Payroll Fraud

Ghost employee schemes

Falsified hours and salary schemes

Commission schemes

Types of Payroll Fraud

Ghost employee schemes

Falsified hours and salary schemes

Commission schemes

Detection of Payroll Schemes

Fraud Prevention: Payroll Schemes

• Segregation of duties• Periodic review and analysis of payroll

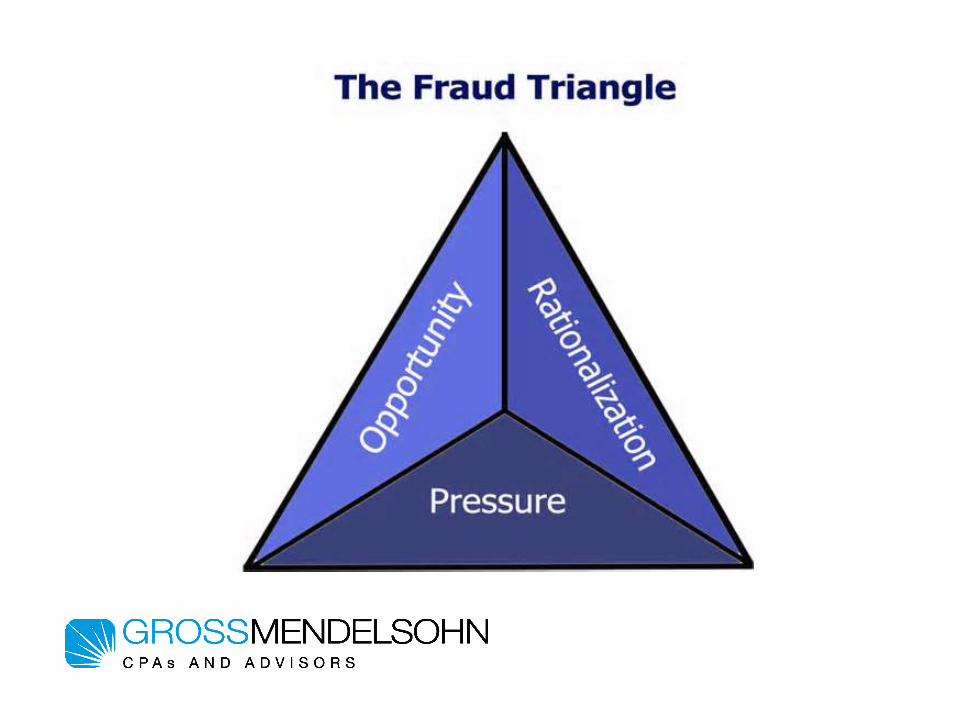

WHY SOME EMPLOYEES COMMITFRAUD

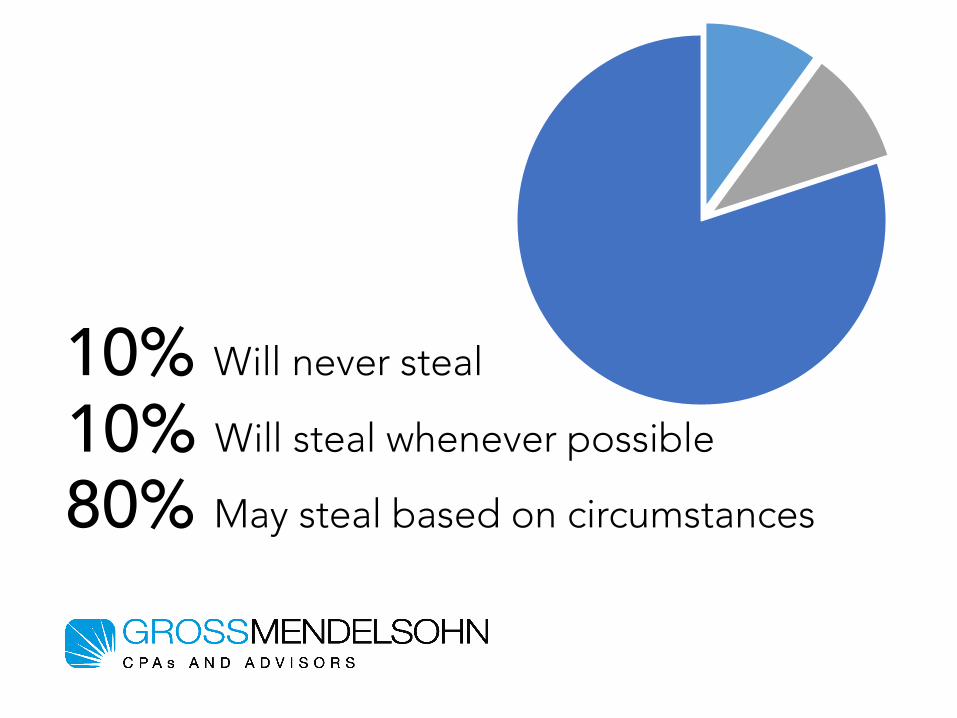

10% Will never steal

10% Will steal whenever possible

80% May steal based on circumstances

BEHAVIORAL RED FLAGS

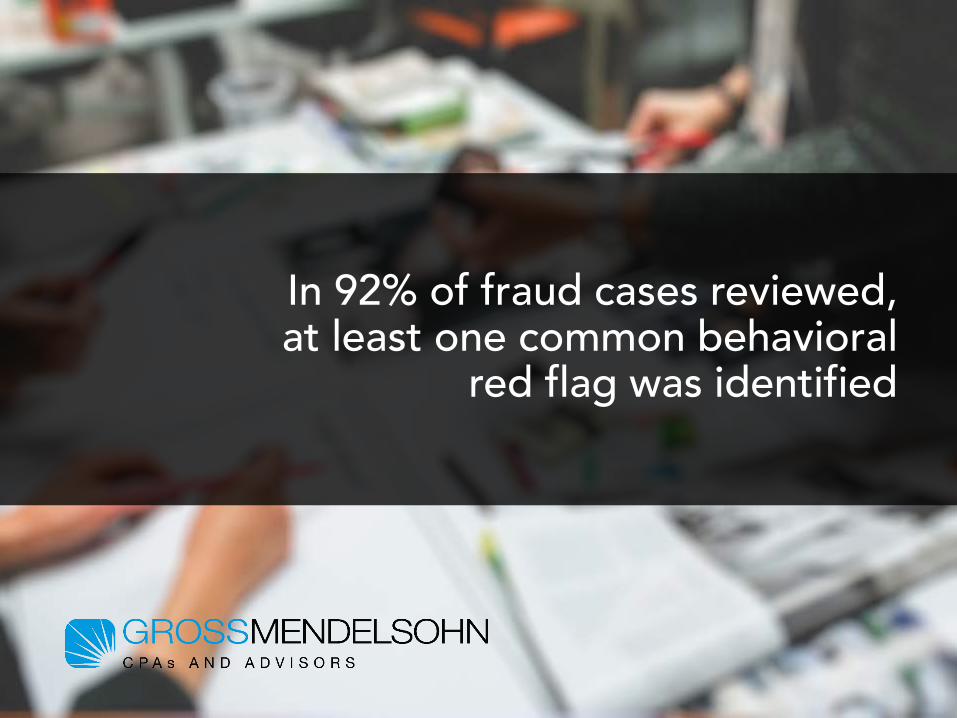

In 92% of fraud cases reviewed, at least one common behavioral

red flag was identified

Living Beyond Means

Living Beyond Means

Financial Difficulties

Living Beyond Means

Financial Difficulties

Unusually Close Associationwith Vendor/Customer

Unwillingness to Share Duties

Living Beyond Means

Financial Difficulties

Unusually Close Associationwith Vendor/Customer

Unwillingness to Share Duties

FRAUD PREVENTION

How can I prevent fraud in my organization?

Effective management oversight | Establish a tone at the top | Increasing the perception of detection | Segregation of duties (as best as possible for the size of the organization) | Bank reconciliations should be done on a monthly basis and appropriately reviewed | Enforcement of mandatory vacations | Job rotation policy | Conduct fixed asset inventories | Perform background checks on new employees and volunteer leaders | Fraud risk assessment by management to determine areas of highest risk | Perform self-audits; don’t assume your year-end audit will catch instances of fraud | Acquire proper insurance coverage | Tip line – should be anonymous, managed by a 3rd party, and available 24/7 | Ethics programs and training | Employee support programs | Clearly defined code of conduct

There are many ways to prevent fraud…

Effective management oversight | Establish a tone at the top | Increasing the perception of detection | Segregation of duties (as best as possible for the size of the organization) | Bank reconciliations should be done on a monthly basis and appropriately reviewed | Enforcement of mandatory vacations | Job rotation policy | Conduct fixed asset inventories | Perform background checks on new employees and volunteer leaders | Fraud risk assessment by management to determine areas of highest risk | Perform self-audits; don’t assume your year-end audit will catch instances of fraud | Acquire proper insurance coverage | Tip line – should be anonymous, managed by a 3rd party, and available 24/7 | Ethics programs and training | Employee support programs | Clearly defined code of conduct

There are many ways to prevent fraud…

CASE STUDY

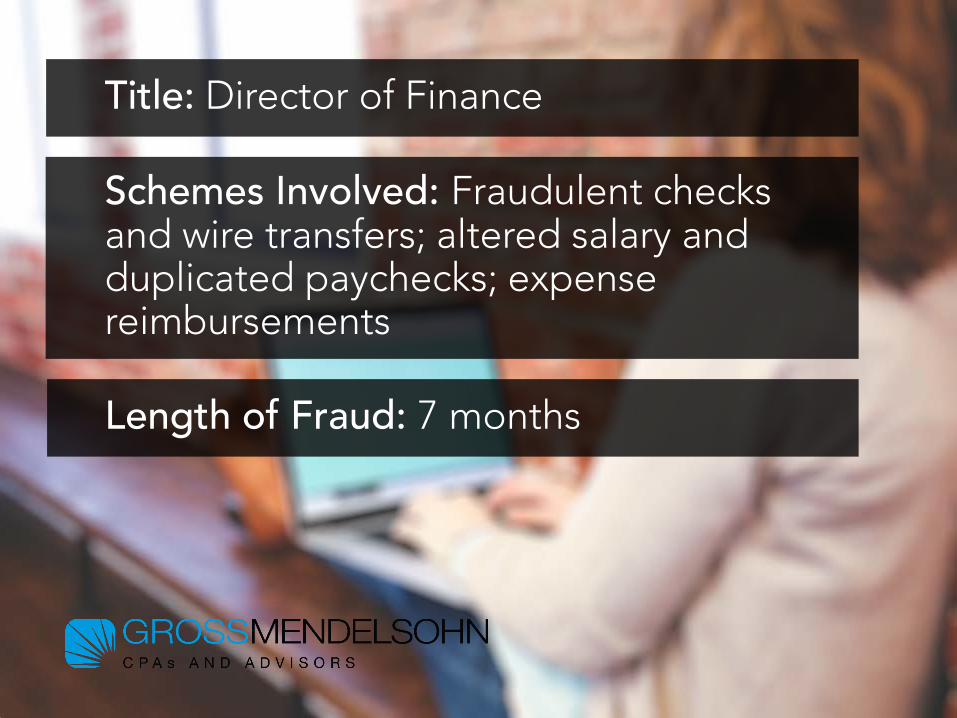

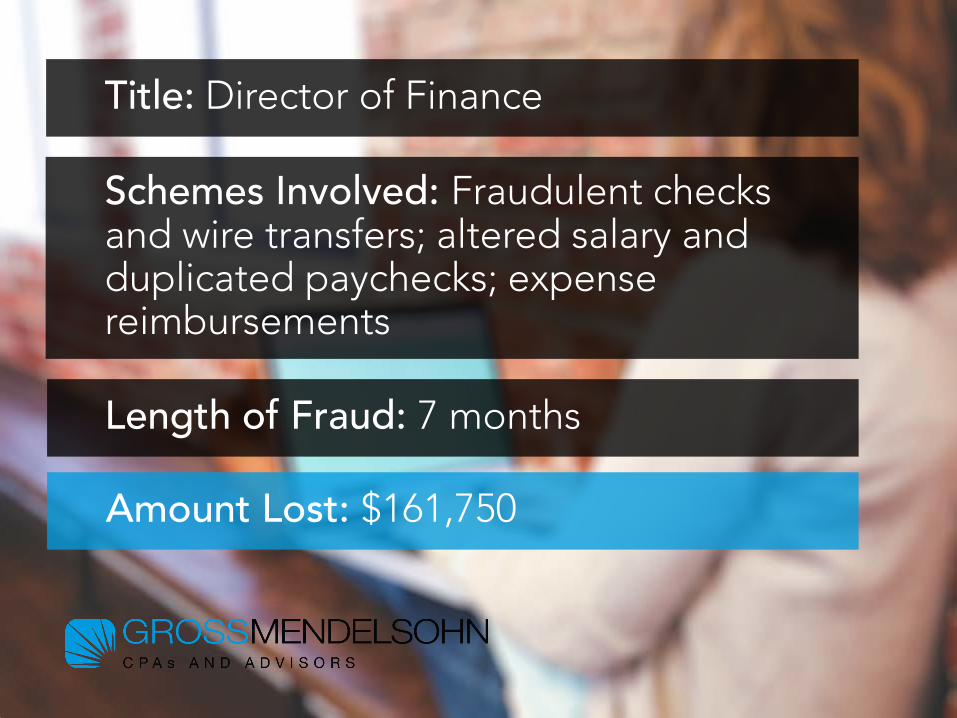

Title: Director of Finance

Schemes Involved: Fraudulent checks and wire transfers; altered salary and duplicated paychecks; expense reimbursements

Length of Fraud: 7 months

Title: Director of Finance

Schemes Involved: Fraudulent checks and wire transfers; altered salary and duplicated paychecks; expense reimbursements

Length of Fraud: 7 months

Amount Lost: $161,750

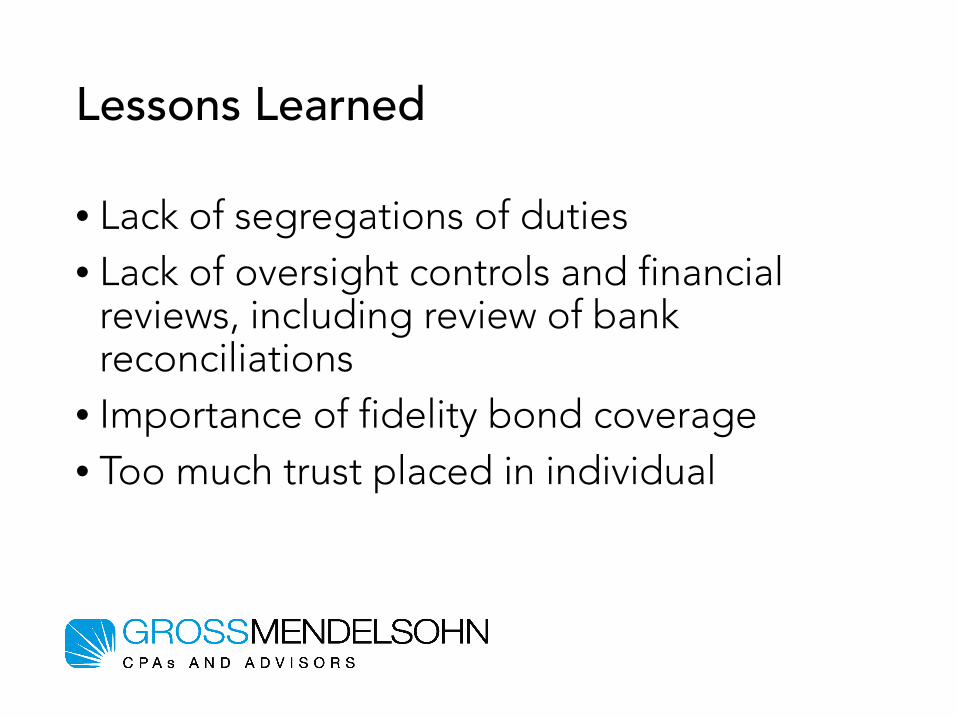

Lessons Learned

• Lack of segregations of duties• Lack of oversight controls and financial

reviews, including review of bank reconciliations

• Importance of fidelity bond coverage• Too much trust placed in individual

WHAT DO I DO IF AN ISSUE ISDISCOVERED?

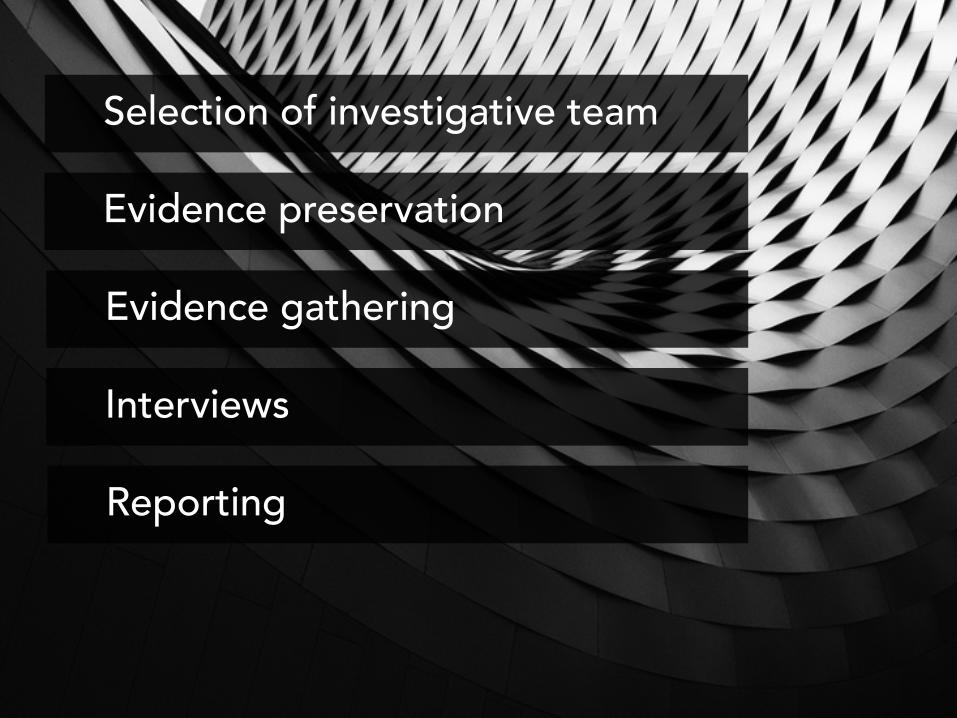

Interviews

Selection of investigative team

Evidence preservation

Evidence gathering

Reporting

Interviews

Selection of investigative team

Evidence preservation

Evidence gathering

Reporting

Interviews

Selection of investigative team

Evidence preservation

Evidence gathering

Reporting

Interviews

Selection of investigative team

Evidence preservation

Evidence gathering

Reporting

Additional Items to Consider

• Consult employment counsel before attempting to recover any funds from final paycheck or vacation time

• Need to manage internal and public disclosure

Downloadthe Webinar

CLICK HERE

Contact Me

Richard L. Wolf, CPA, CGMA, CFE [email protected] | LinkedIn

Gross, Mendelsohn & Associates36 S. Charles Street, 18th FloorBaltimore, MD 21201www.gma-cpa.com 800.899.4623

Feel free to contact us anytime with questions.

![1 Mining Fraudsters and Fraudulent Strategies in Large ...yangy.org/works/telecom_fraud/TKDE_Fraud_Yang.pdf · detection [5] and insurance fraud detection [6] technologies, to the](https://img.pdfslide.us/doc/110x75/5f9d057eabb22b5d0767f6e5/1-mining-fraudsters-and-fraudulent-strategies-in-large-yangyorgworkstelecomfraudtkdefraudyangpdf.jpg)