Embed Size (px)

Citation preview

HELP MY INDUSTRY IS

CONSOLIDATINGFive foolproof growth strategies to

trounce the competition in 2016

Brad Mewes

Principal, Supplement

supp-co.com

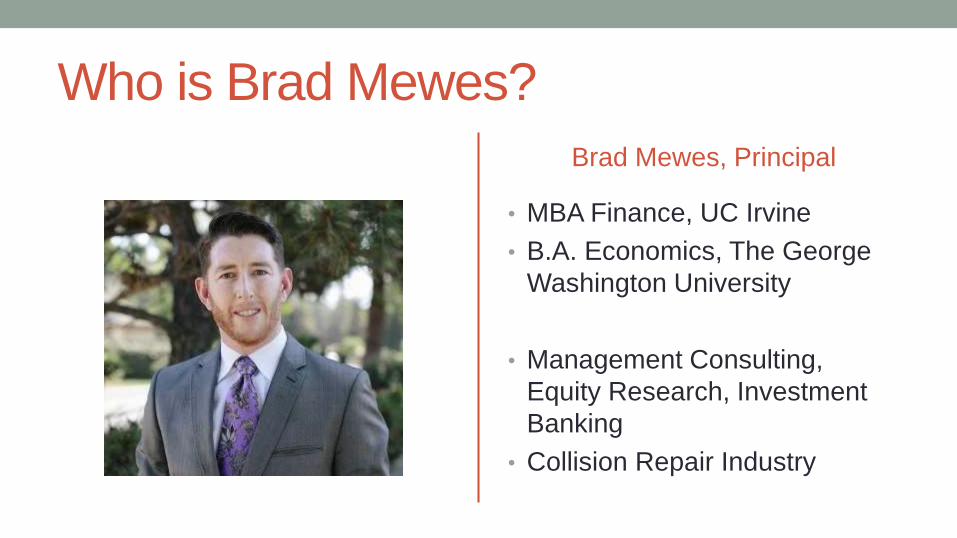

Who is Brad Mewes?

Brad Mewes, Principal

• MBA Finance, UC Irvine

• B.A. Economics, The George

Washington University

• Management Consulting,

Equity Research, Investment

Banking

• Collision Repair Industry

What We DoWe increase the value of your business

using the tools of corporate finance.

Buy Side

(Acquisitions)

Sell Side

(Business Sale)

CFO

&

Financial Advisory

Strategy

&

Execution

Why We Do ItThe industry is rapidly evolving. What used to work no

longer does.

State of the Industry

Consolidation Curve

Inorganic Growth

What Not to Do

Pricing Trends

STATE OF THE INDUSTRYThe Current State of the Industry and Why

Consolidation Will Likely Continue

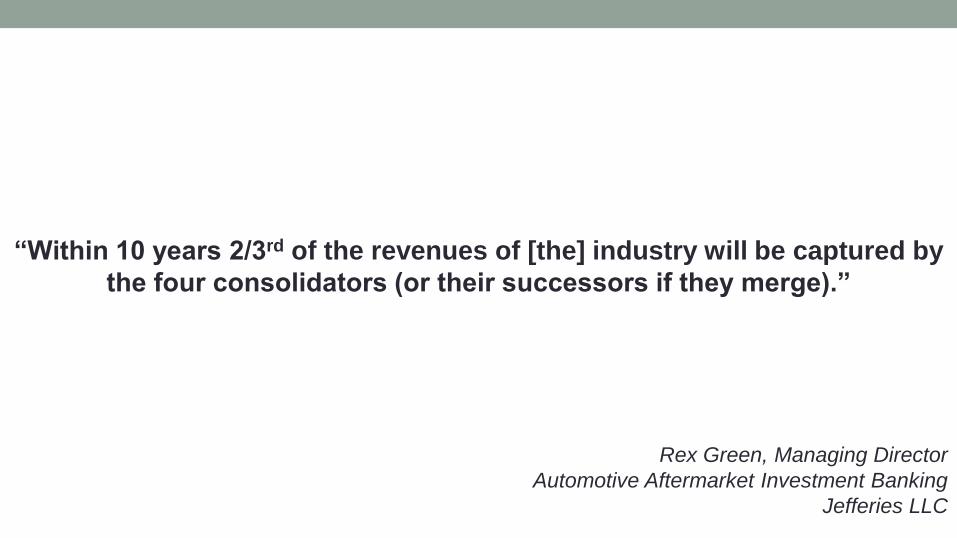

“Within 10 years 2/3rd of the revenues of [the] industry will be captured by

the four consolidators (or their successors if they merge).”

Rex Green, Managing Director

Automotive Aftermarket Investment Banking

Jefferies LLC

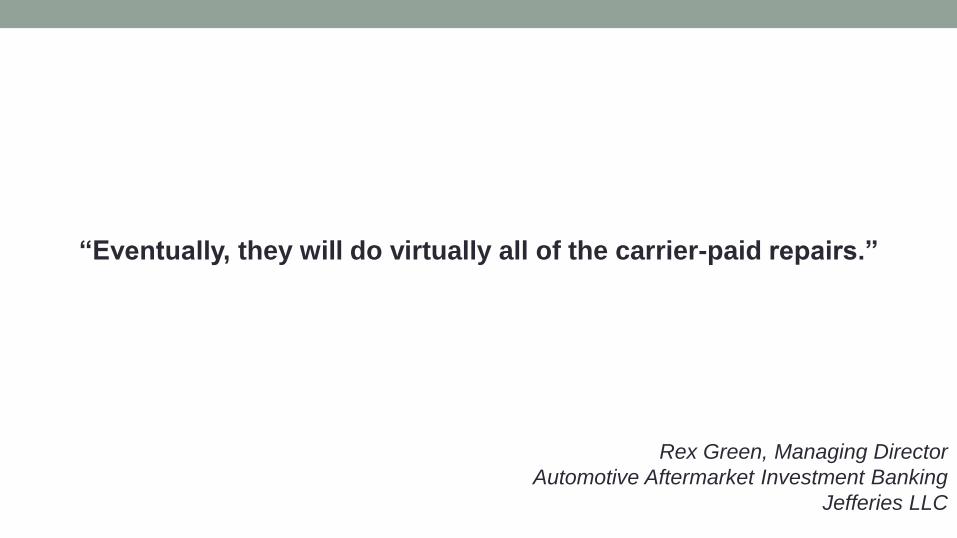

“Eventually, they will do virtually all of the carrier-paid repairs.”

Rex Green, Managing Director

Automotive Aftermarket Investment Banking

Jefferies LLC

Despair.com

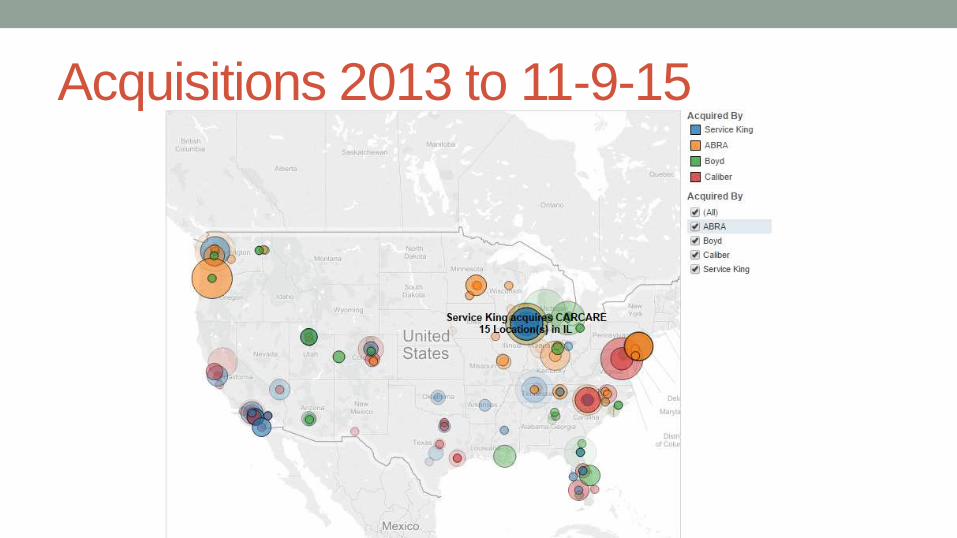

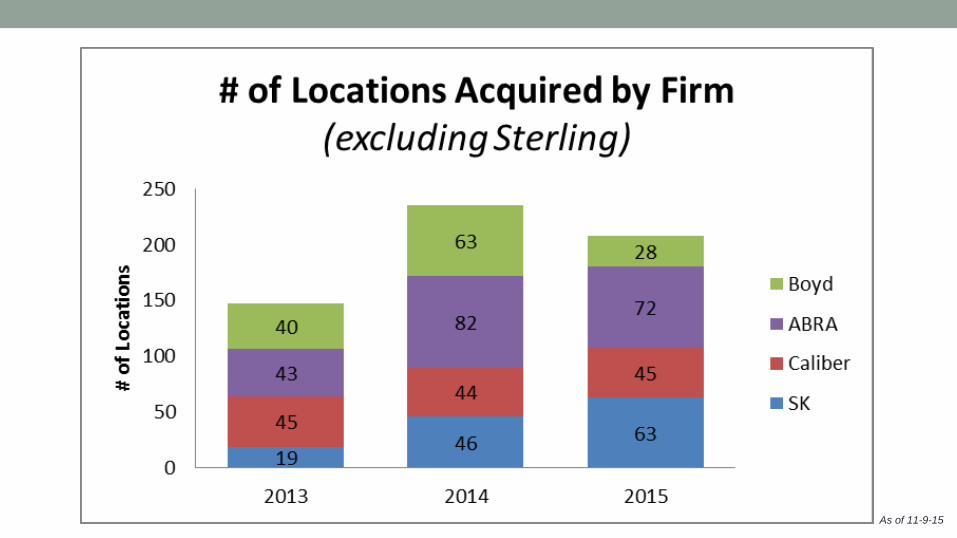

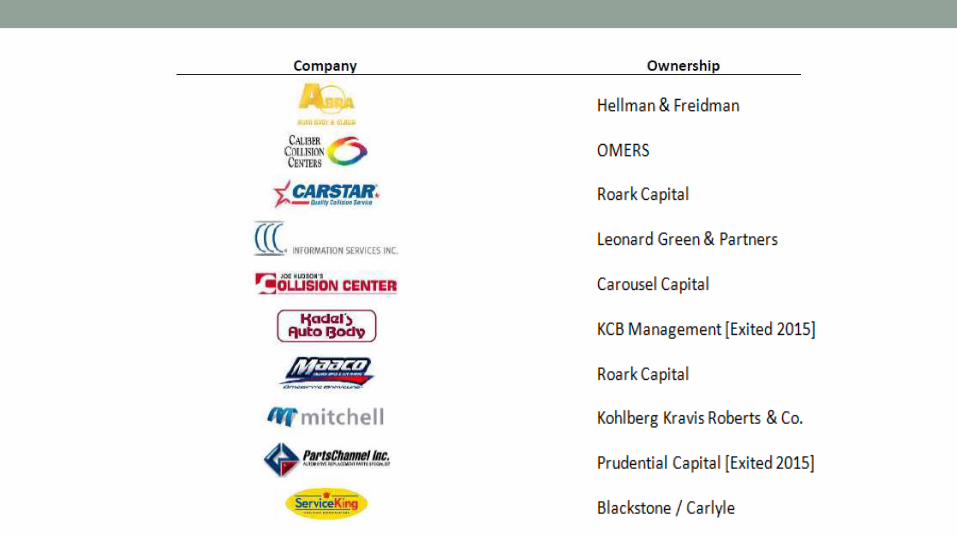

Acquisitions 2013 to 11-9-15

History of Collision Consolidation

Source: BB&T Capital; IBIS

As of 11-9-15

What is Private Equity???

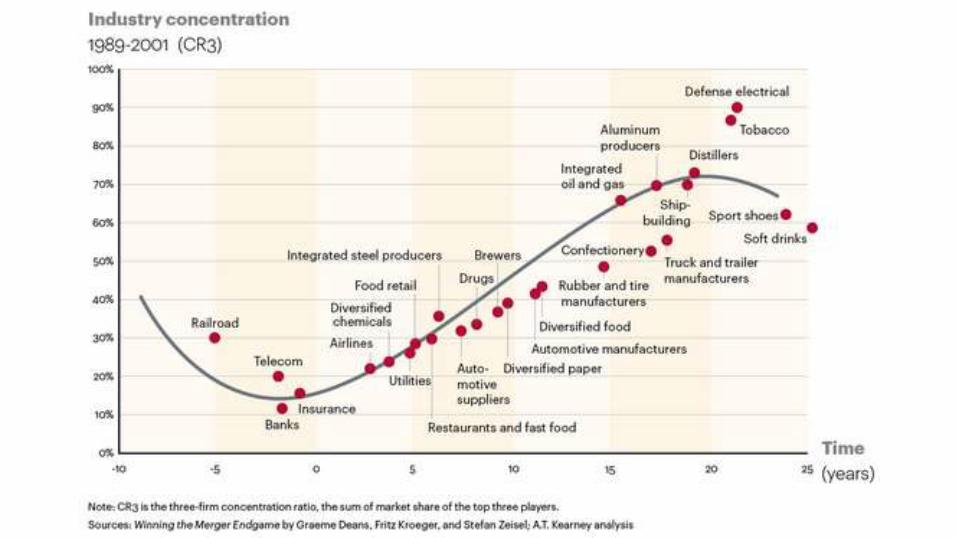

CONSOLIDATION CURVEThe big get bigger. How industry lifecycles impact

competition and consolidation.

“I believe there will be more consolidation.”

“Let’s face facts: There are a lot of independents out there. Dealerships are struggling in this environment. When you have a well-capitalized multishop operation, that creates more opportunity.”

Steve Grimshaw, CEO

Caliber Collision Centers

July, 2010 Interview with FenderBender

“The industry has been fragmented and is in an overcapacity situation.

Since the industry itself isn’t growing quickly, the better operators are

taking market share from the

marginal operators.”

Duane Rousse, CEO

ABRA Auto Body

September, 2012 Interview with Bodyshop Business

“The trend is for consolidation. The biggest question is,

who will be the successful consolidator?

Cathy Bonner, Chairman

Service King Collision Repair Center

July, 2012 Interview with Bodyshop Business

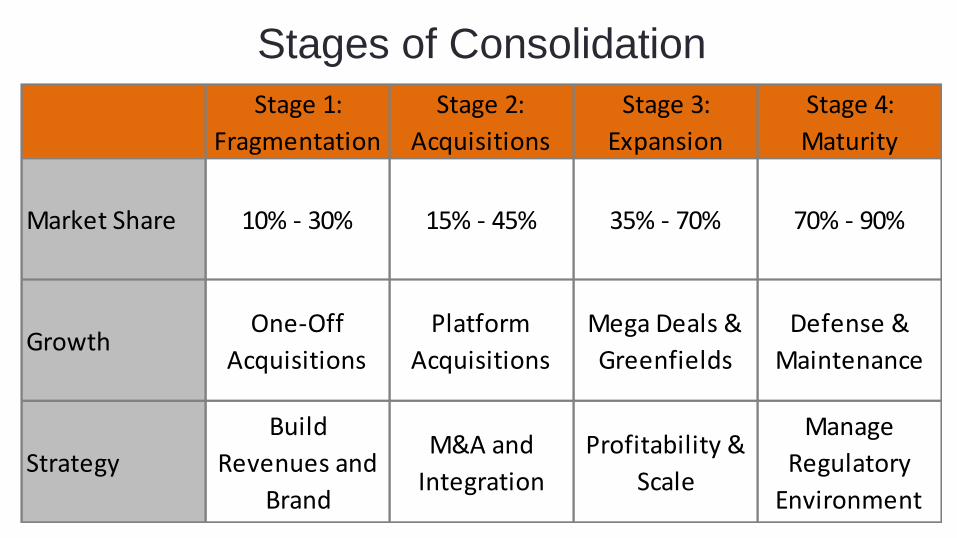

Stage 1:

Fragmentation

Stage 2:

Acquisitions

Stage 3:

Expansion

Stage 4:

Maturity

Market Share 10% - 30% 15% - 45% 35% - 70% 70% - 90%

Growth One-Off

Acquisitions

Platform

Acquisitions

Mega Deals &

Greenfields

Defense &

Maintenance

Strategy

Build

Revenues and

Brand

M&A and

Integration

Profitability &

Scale

Manage

Regulatory

Environment

Stages of Consolidation

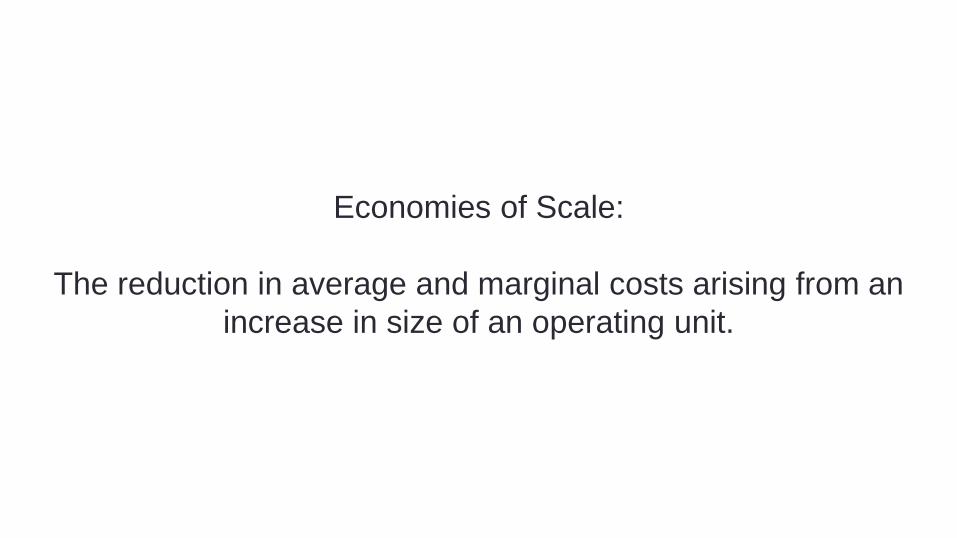

Economies of Scale:

The reduction in average and marginal costs arising from an

increase in size of an operating unit.

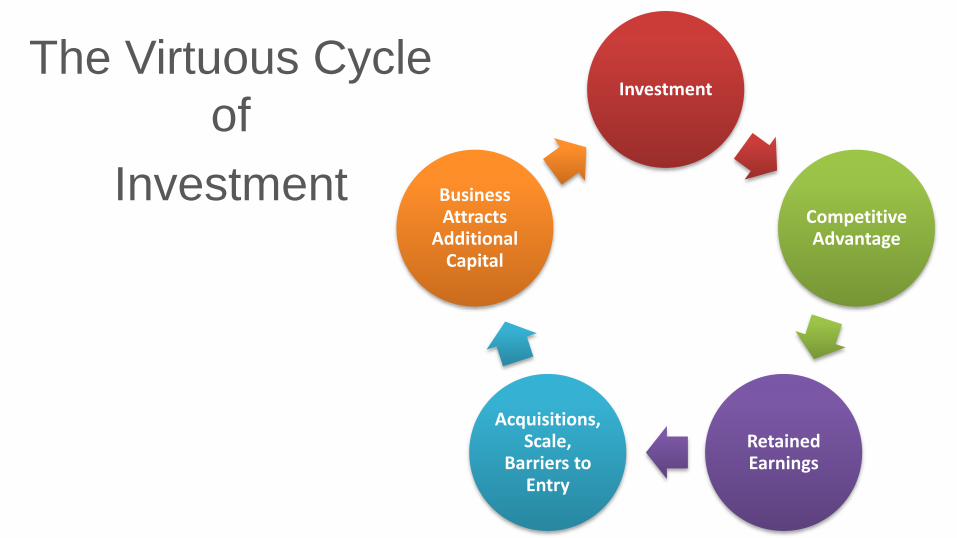

Investment

Competitive Advantage

Retained Earnings

Acquisitions, Scale,

Barriers to Entry

Business Attracts

Additional Capital

The Virtuous Cycle

of

Investment

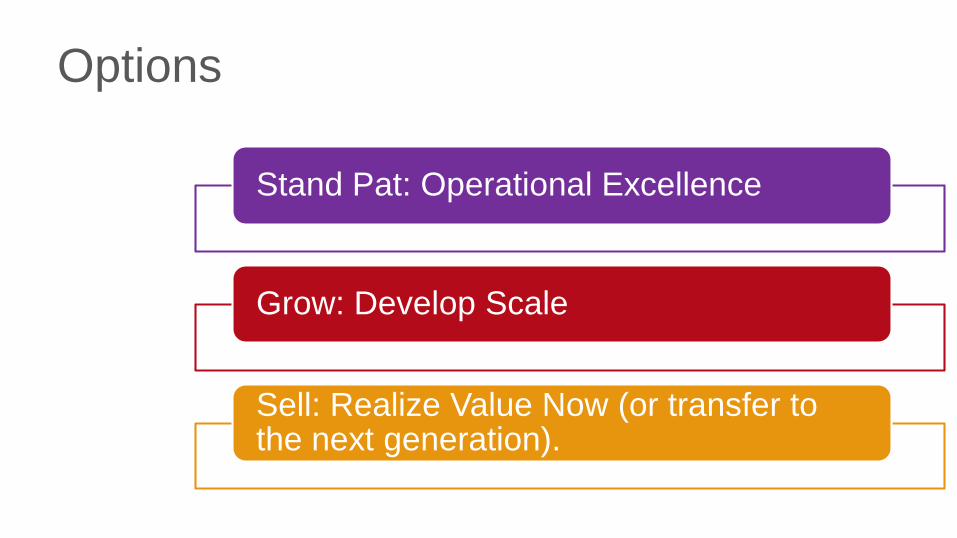

Options

Stand Pat: Operational Excellence

Grow: Develop Scale

Sell: Realize Value Now (or transfer to the next generation).

INORGANIC GROWTHBuild and Execute an Inorganic Growth Strategy

• Start with the end in mind

• Build a team; both internally and

externally

• A proactive acquisition strategy

• Develop non-auction deal flow

• Evaluate your alternatives

Five Inorganic Growth Success Factors

Start with the End in Mind

Build a Team,

Internally and Externally

Proactive

Acquisition Strategy

Non-Auction

Deal Flow

Evaluate Your

Investment Alternatives

WHAT NOT TO DOIdentify and avoid common buy side pitfalls

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

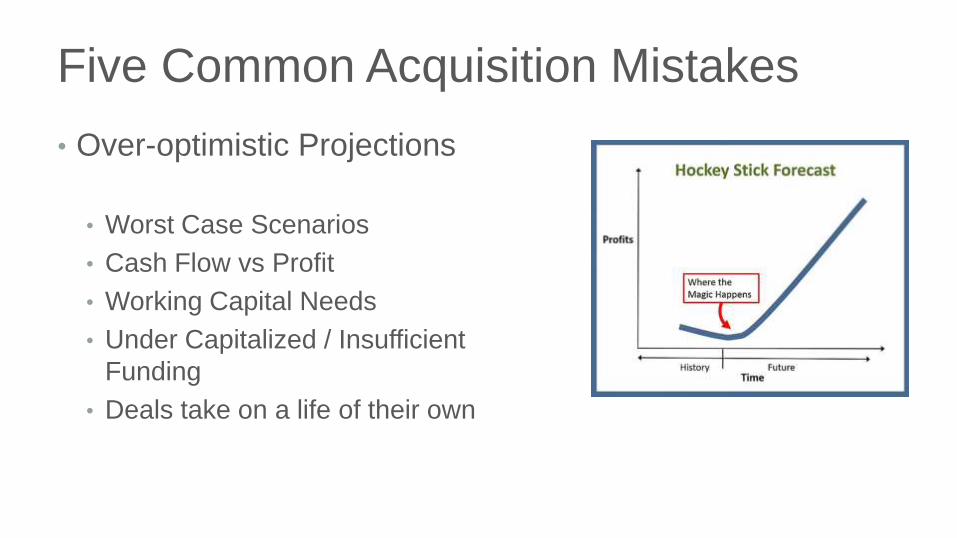

• Over-optimistic Projections

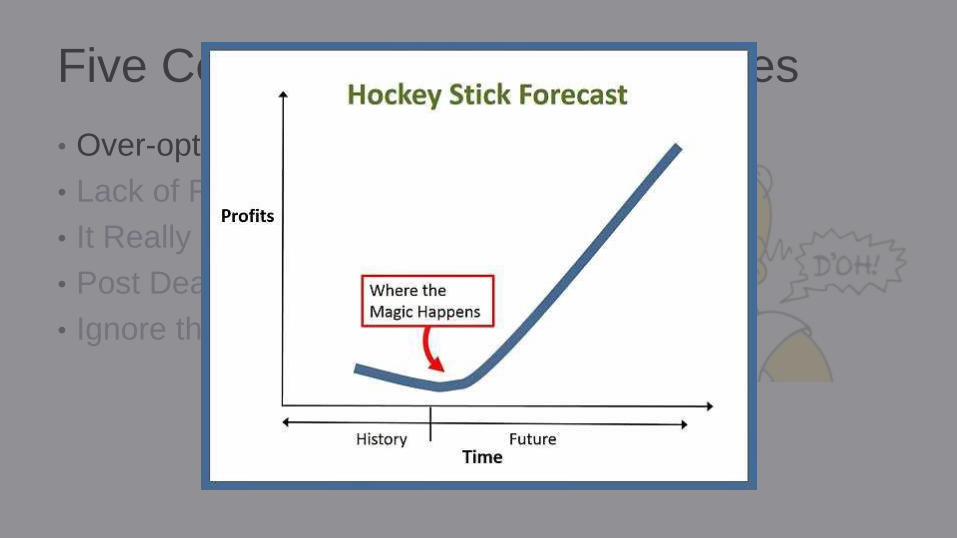

• Worst Case Scenarios

• Cash Flow vs Profit

• Working Capital Needs

• Under Capitalized / Insufficient

Funding

• Deals take on a life of their own

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• Lack of Focus

• Strategic Drift

• Diligent Due Diligence

• Existing Team Bandwidth

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• It Really Is All About the People

• Ego

• Culture

• New Team Integration

• Who’s Responsible for What?

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• Post Deal Integration

• Employee Retention

• Cost Synergies

• Cash Needs

• IT, HR, Accounting, Shared

Services, etc.

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

• Over-optimistic Projections

• Lack of Focus

• It Really Is All About the People

• Post Deal Integration

• Ignore the Advisors

Five Common Acquisition Mistakes

WHAT IS IT WORTH?Pricing Trends and Valuation Methods

A Primer on Valuation

• EBITDA and Multiples

• DCF, IRR & Hurdle Rates

• Multiples & Comps

• Strategic vs Financial

• Control & Liquidity Premiums

• BASF Collision Center Expansion Model

• Brand

• Location / Market

• Management Team

• Facility

• Operational Excellence

Non Financial Premiums

Let’s Grow Together

Contact:

Supplement

Financial Insight for the Automotive

Professional

714.658.5518

http://supp-co.com