Embed Size (px)

Citation preview

Fundraising / Security Law for Entrepreneurs By : Matthew Moisan / Moisan Law

April 2015

Fundraising / Security Law for Entrepreneurs BY: MATTHEW J. MOISAN

MOISAN LEGAL PC

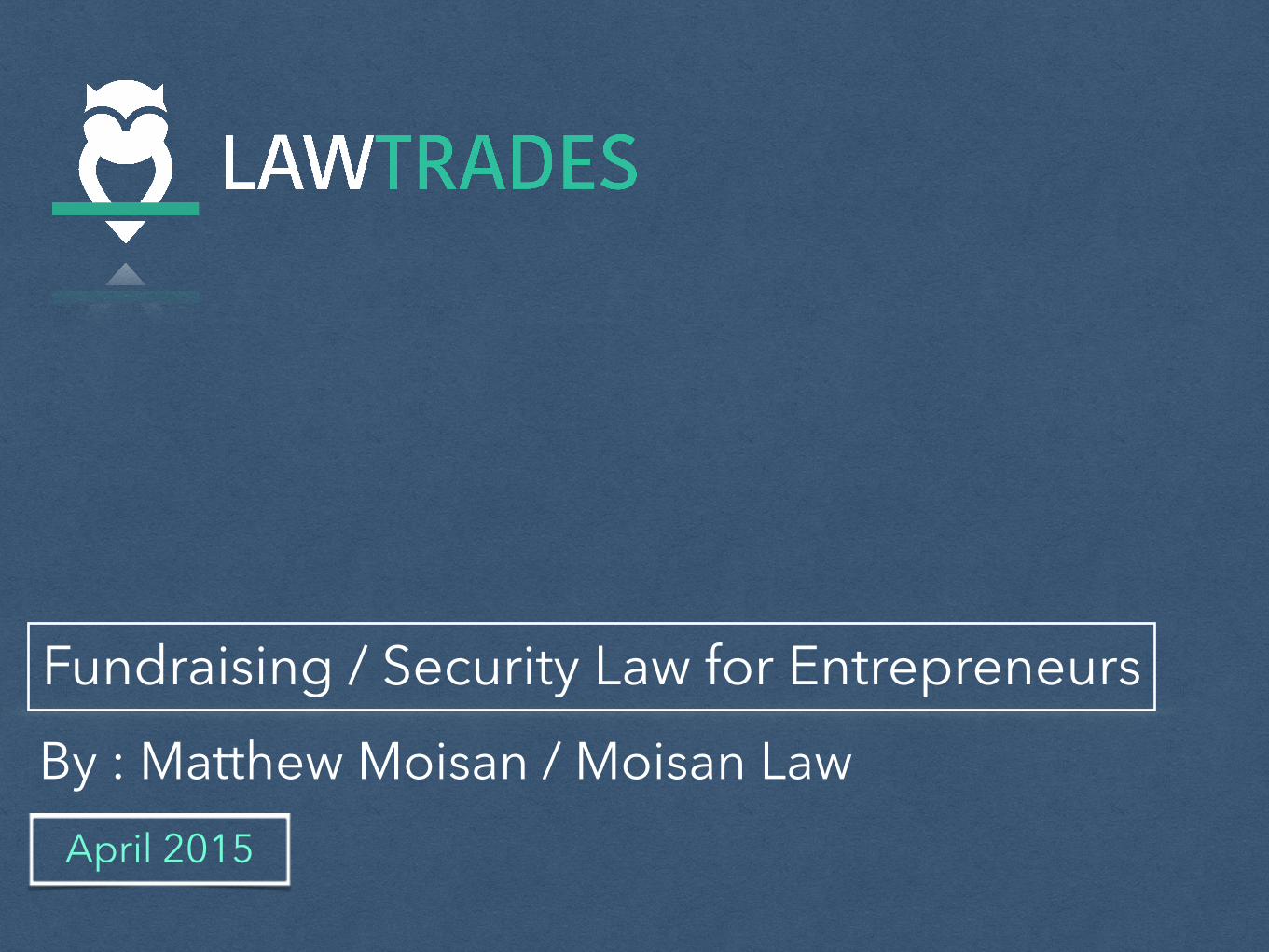

What is a “Security”

! The term ‘‘security’’ means any note, stock, treasury stock, security future, security-based swap, bond, debenture, evidence of indebtedness, certificate of interest or participation in any profit-sharing agreement, collateral-trust certificate, preorganization certificate or subscription, transferable share, investment contract, voting-trust certificate, certificate of deposit for a security, fractional undivided interest in oil, gas, or other mineral rights, any put, call, straddle, option, or privilege on any security, certificate of deposit, or group or index of securities (including any interest therein or based on the value thereof), or any put, call, straddle, option, or privilege entered into on a national securities exchange relating to foreign currency, or, in general, any interest or instrument commonly known as a ‘‘security’’, or any certificate of interest or participation in, temporary or interim certificate for, receipt for, guarantee of, or warrant or right to subscribe to or purchase, any of the foregoing. Securities Act of 1933.

What does that mean?

! Courts have struggled with this definition ! Howey Test – from SEC v. W.J. Howey Co., Seminal Supreme Court Case

on this subject ! “A contract, transaction or scheme whereby a person invests his

money in a common enterprise and is led to expect profits solely from the efforts of the promotor or third party”

! Example – Stock in a Company. If I give a company money, I have an expectation of profits and am reliant upon the company (a third party) to produce those profits

! NOTE – form of investment is irrelevant ! Promissory notes – complicated

TEST – Continued

! 1. Motivations of buyer and seller ! 2. “Plan of distribution” ! 3. Reasonable expectations of investing pubic ! 4. Risk (is there another statute that mitigates risk?)

! AKA – I’ll know it when I see it.

That was fun – So what?

! Any offer or sale of securities in interstate commerce must be registered pursuant to Section 5 of the Securities Act of 1933.

! AKA every single time you talk about a convertible note – you are implicating the security laws.

! Quick History – Similar to all financial legislation, this was a result of an event, the Stock Market Crash of 1929 - enacted to restore the public’s trust in the capital system and prevent fraud

! Prior to this legislation, all sales of securities were regulated by “Blue Sky” laws (each state had (and continues to have) its own regulations)

! Why “Blue Sky”? Because financial pirates would sell citizens everything in the state but the “blue sky”

Exemptions

! But for the exemption in Section 4(a)(2) – all transactions involving a security would require registration.

! Section 4(a)(2) of the Securities Act - Is an exemption to the filing requirement for transactions by an issuer not involving a public offering.

! What the heck is a public offering? ! I’ll know it when I see it.

Factors in considering what is “Public”

! In 1935 the General Counsel of the SEC stated: ! Number of offerees (not purchasers)

! Relationship to one another ! Number of units offered ! Value of offering ! Manner of offering

! Supreme Court stated that the exemption “should turn on whether the particular class of persons affected needs the protection of the Act. An offering to those who are shown to be able to fend for themselves is a transaction ‘not involving any public offering’

Regulation D

! If you comply with Regulation D you have not engaged in a public offering – three different regulations, 504, 505, 506 – bear in mind, any time you sell to “non-accredited investors” there are heightened requirements.

! National Securities Markets Improvement Act (NSMIA)

Changing Gears - Exchange Act of 1934

! In its simplest form, governs secondary trading of securities … AKA investor A selling to investor B

! ’33 Act is a one night stand (one disclosure requirement) ! ‘34 Act is an affair (ongoing disclosure requirements) IF the

company has more than 500 shareholders or more than 10 million in assets; Proxy Statements, 8K Current Report, 10K Annual Reports, 10Q Quarterly Reports etc.

But Matthew, I still don’t care!

! Yes, young Trep. You do. ! The failure to abide by the security laws has criminal and civil implications. ! Three types of offerings:

! Registered ! Exempt ! Illegal

JOBS Act of 2012

! Made some drastic changes – specifically with regards to public solicitation and crowdfunding.

! For the first time, you CAN use public solicitation in a 506 offering. ! Crowdfunding, raising money in an equity financing from a group of

people in small amounts. Still not finalized. ! Regulation A+ (proposal drafted on March 25, 2015) – mini IPO, less

onerous requirements than full ‘34 Act registration

JOBS Act Continued

! New 2015 Regulation A+ Benefits

! Can raise up to $50 Million in crowd funding (instead of previous $5 million)

! No longer have to register state by state under Blue Sky Laws

! Don’t have to be an accredited investor to invest

! Restriction is now can only invest 10% of the greater of either investor’s: (a) net worth, or (b) annual income

! Implications:

! Potentially create new wave of investment

! Broader base of capital raising for companies raising funding

Full circle - Fundraising

! Most companies follow the same financing path: ! Friends and Family

! Angels

! VC or Public VC

! NOTE: VCs only fund 2% of all startups.

Friends and Family

! Typically squeeze into the grey area of Rule 4(a)(2) ! 50/50 equity investments versus convertible ! Sometimes that investment is first money out, sometimes not. ! Typical raise between 10 – 150,000 and typically takes 2-3 months to

complete.

Angels

! Typically Regulation D, 506 offerings ! Typically Convertible Notes ! 100,000 – 2 million ! 4-8 months to complete

VC

! Typically Regulation D, 506 offerings ! Typically preferred equity or convertible debt ! 2 Million to ___ ! 6-12 months

Fundraising – generally

! Why are they investing? ! Usually the answer is because they trust you! ! Valuation - Impossible to accurately ascertain – based upon

“gut” and “instinct” ! Guidelines:

! Pre-revenue companies, friends and family rounds typically value the company at .5 – 1 million. They might offer more, but don’t accept. The goal here is fairness and alignment of interests.

Promoters – Broker / Dealers

! It is illegal to pay someone a success fee in connection with a financing unless that person is a broker / dealer.

! Only a registered broker / dealers can engage in the business of effecting a transaction in connection with securities on the account of another.

! Harsh penalties. ! 10b-5 criminal and civil penalties

! Rescission of transaction

! Bad actor qualification

Basic terms

! Money in (valuation / option pool) ! Treatment (preemptive rights, Anti-dilution, right of first refusual) ! Money out (preferential returns / liquidation preference) ! Management (Board / voting, etc.) ! Transfer

get started at www.lawtrades.com

Need Help Fundraising?