Embed Size (px)

Citation preview

Landscape analysis of the Finnish

ITS/MaaS business

Presentation

4th of May 2016

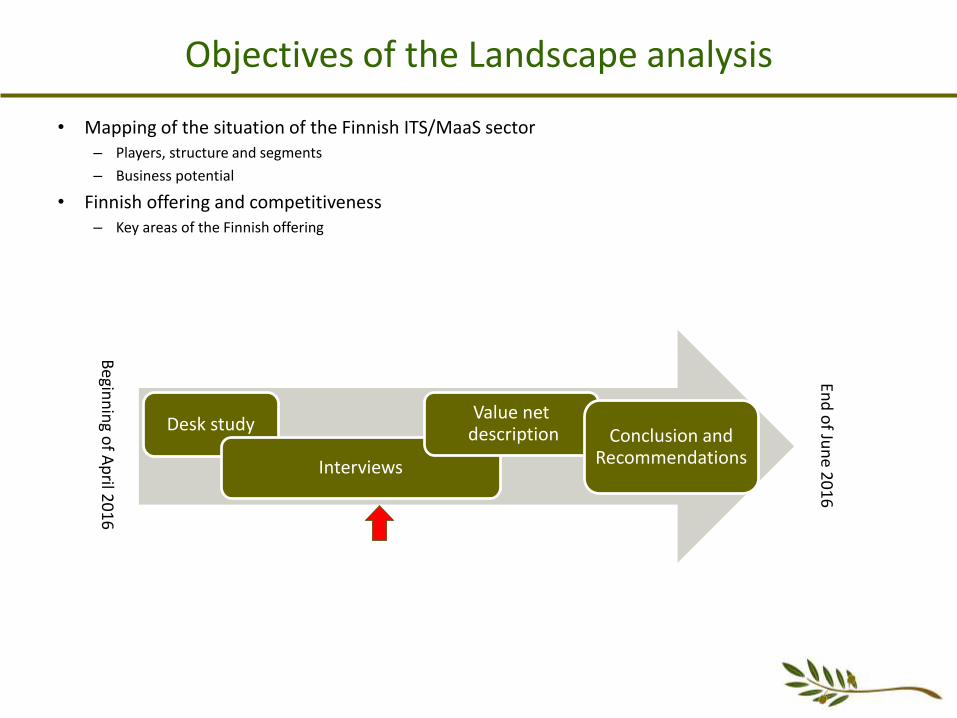

Objectives of the Landscape analysis

• Mapping of the situation of the Finnish ITS/MaaS sector– Players, structure and segments

– Business potential

• Finnish offering and competitiveness– Key areas of the Finnish offering

Desk study

Interviews

Value netdescription Conclusion and

Recommendations

Begin

nin

go

f Ap

ril20

16

End

of Ju

ne

20

16

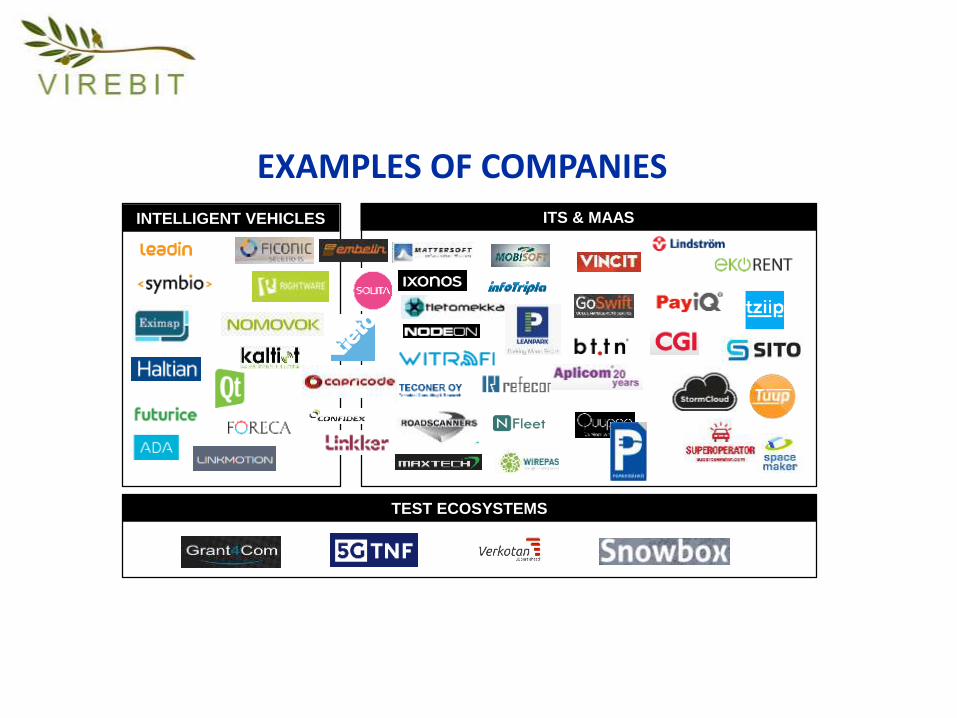

EXAMPLES OF COMPANIESINTELLIGENT VEHICLES ITS & MAAS

TEST ECOSYSTEMS

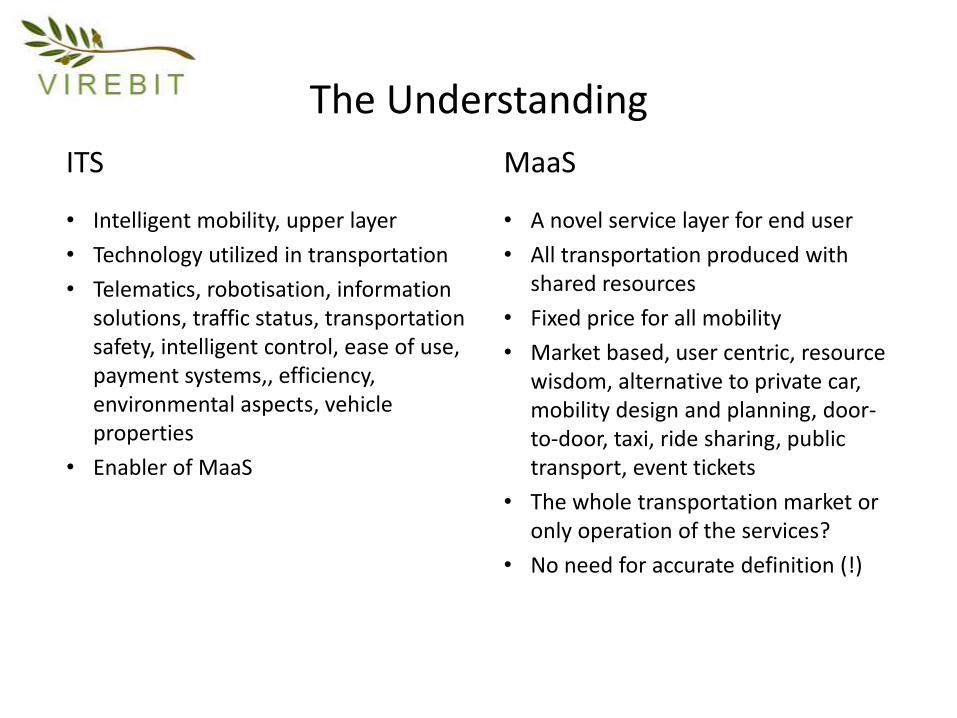

The Understanding

ITS

• Intelligent mobility, upper layer

• Technology utilized in transportation

• Telematics, robotisation, informationsolutions, traffic status, transportationsafety, intelligent control, ease of use, payment systems,, efficiency, environmental aspects, vehicleproperties

• Enabler of MaaS

MaaS

• A novel service layer for end user

• All transportation produced with shared resources

• Fixed price for all mobility

• Market based, user centric, resource wisdom, alternative to private car, mobility design and planning, door-to-door, taxi, ride sharing, publictransport, event tickets

• The whole transportation market or only operation of the services?

• No need for accurate definition (!)

The Need

• Ease, cost and/or security

• Everyone a potential customer, but not necessarily of all services

• Savings in transportation investments for private and public parties

• Less congestion, less pollutants

• Personal attitudes have biggest impact

• No cases yet, big operators in waiting mode

• Need for passenger cars may growwith MaaS

• Need for sticks and carrots bypublic authoritites

The Potential

• A lot is needed to enable MaaS

• Slow penetration, incremental development

• Until 2020 moderate growth to be expected,

• Currently public transportation vs. owning a car

• Hype and trend work for MaaS

• New service segments into the game, newactors will take theirshare

• Investments efficientlyused

• All kinds of movements towards MaaS, a lot of steps in the way

• Billions in five/ten years, 10 fold to telecom

• “15 %” of the transport-ation market passenger transportation, 20 % of that target for MaaS

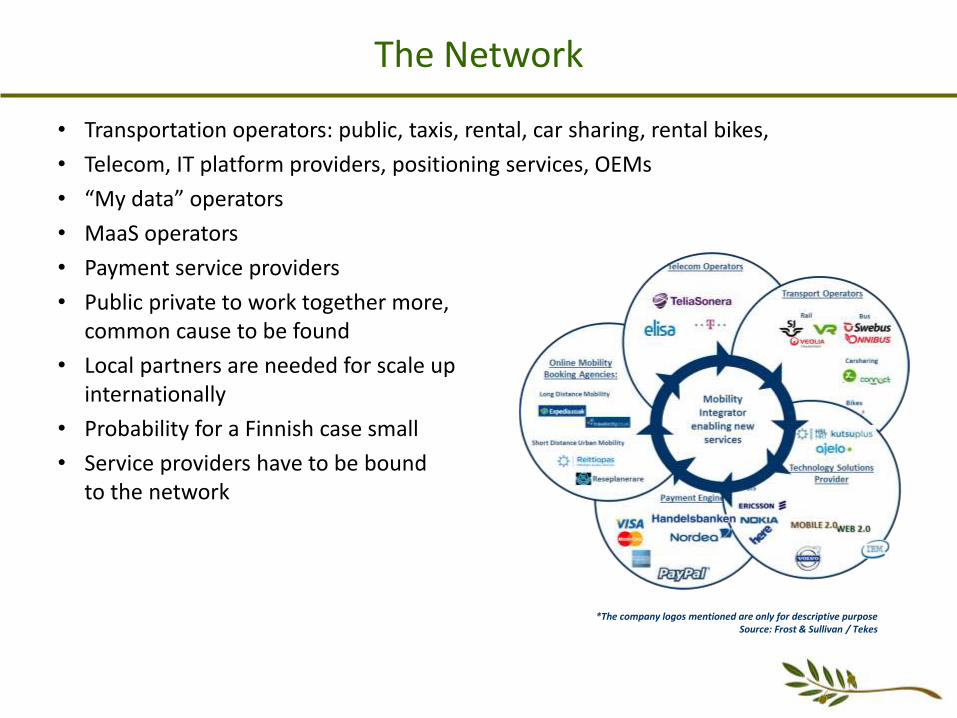

The Network

• Transportation operators: public, taxis, rental, car sharing, rental bikes,

• Telecom, IT platform providers, positioning services, OEMs

• “My data” operators

• MaaS operators

• Payment service providers

• Public private to work together more, common cause to be found

• Local partners are needed for scale up internationally

• Probability for a Finnish case small

• Service providers have to be bound to the network

*The company logos mentioned are only for descriptive purposeSource: Frost & Sullivan / Tekes

The Benchmarks

• Finnish competence is good, limited knowledge about the situation elsewhere a risk, though

• E.g. in Shanghai single card works in buses, trains and taxis

• A few shining stars, OEMs, digital service companies (Apple, Google etc.)

• US near to commercialization, a lot of startups

• Swedes to be followed, often more agile than Finns

• Finland to learn supporting of own industry from other countries

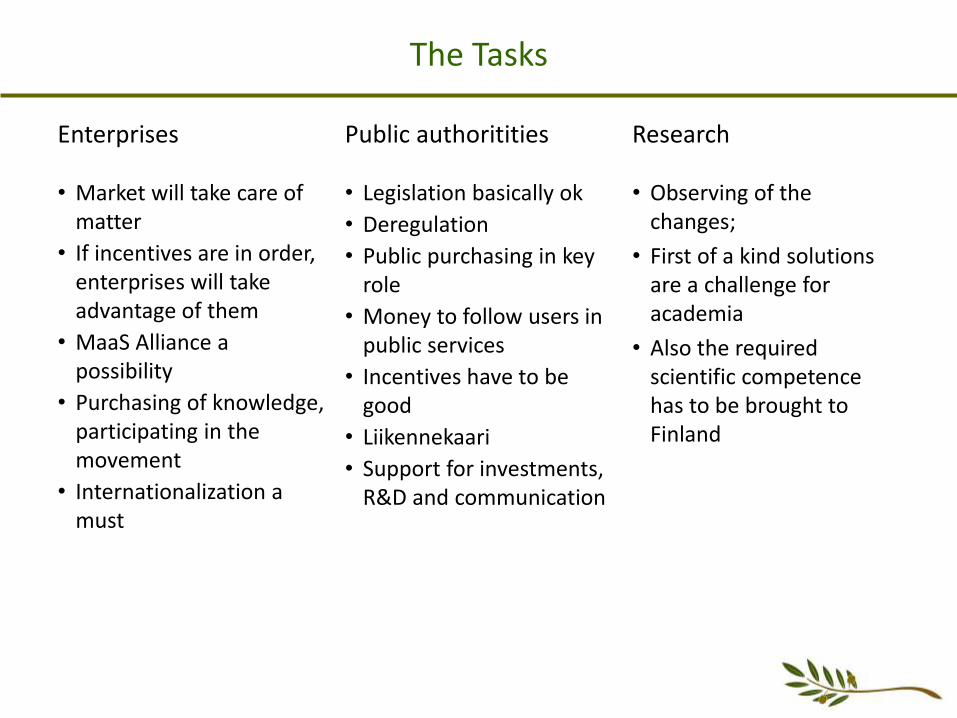

The Tasks

Enterprises Public authoritities Research

• Market will take care of matter

• If incentives are in order, enterprises will take advantage of them

• MaaS Alliance a possibility

• Purchasing of knowledge, participating in the movement

• Internationalization a must

• Legislation basically ok

• Deregulation

• Public purchasing in key role

• Money to follow users in public services

• Incentives have to be good

• Liikennekaari

• Support for investments, R&D and communication

• Observing of the changes;

• First of a kind solutionsare a challenge for academia

• Also the required scientific competence has to be brought to Finland

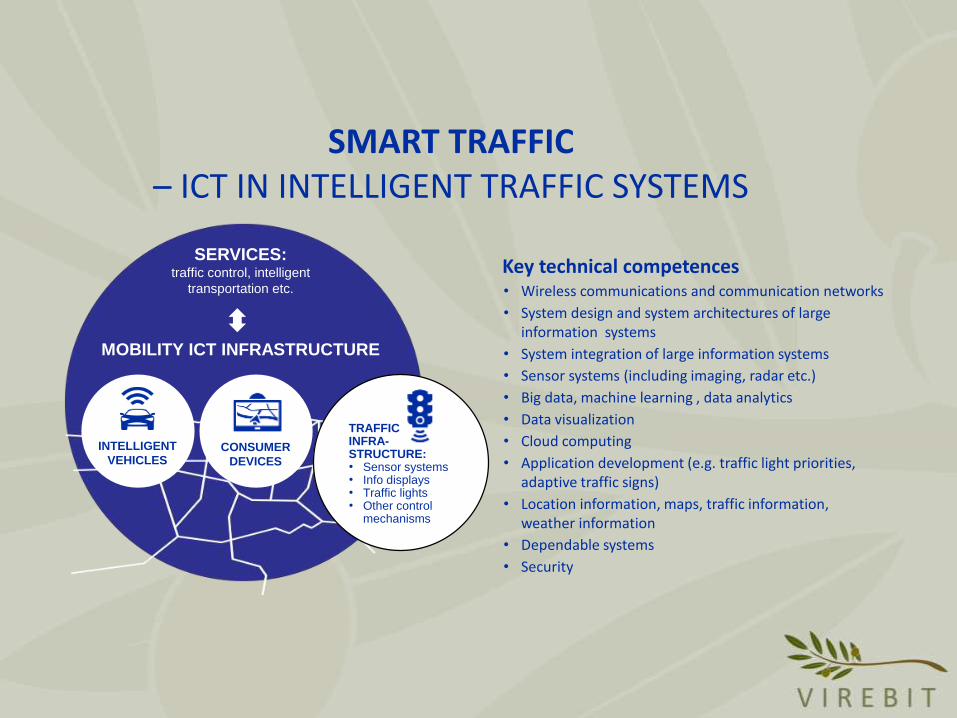

SMART TRAFFIC – ICT IN INTELLIGENT TRAFFIC SYSTEMS

Key technical competences• Wireless communications and communication networks

• System design and system architectures of large information systems

• System integration of large information systems

• Sensor systems (including imaging, radar etc.)

• Big data, machine learning , data analytics

• Data visualization

• Cloud computing

• Application development (e.g. traffic light priorities, adaptive traffic signs)

• Location information, maps, traffic information, weather information

• Dependable systems

• Security

SERVICES: traffic control, intelligent

transportation etc.

MOBILITY ICT INFRASTRUCTURE

INTELLIGENT

VEHICLESCONSUMER

DEVICES

TRAFFIC INFRA-STRUCTURE:• Sensor systems• Info displays• Traffic lights• Other control

mechanisms

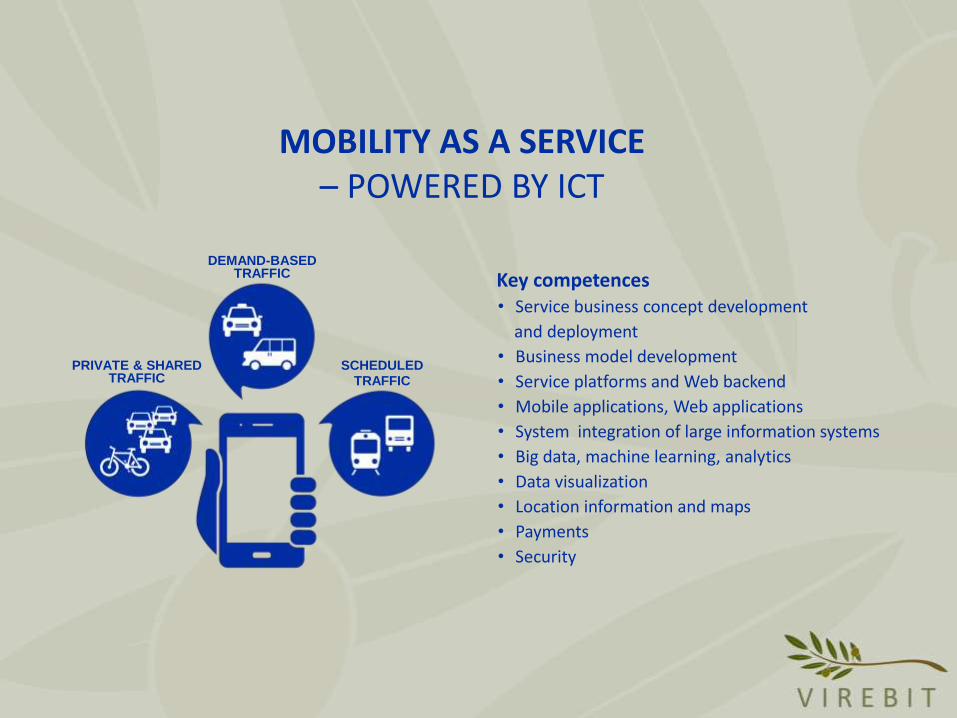

MOBILITY AS A SERVICE – POWERED BY ICT

Key competences• Service business concept development

and deployment

• Business model development

• Service platforms and Web backend

• Mobile applications, Web applications

• System integration of large information systems

• Big data, machine learning, analytics

• Data visualization

• Location information and maps

• Payments

• Security

SCHEDULED TRAFFIC

DEMAND-BASED TRAFFIC

PRIVATE & SHARED TRAFFIC

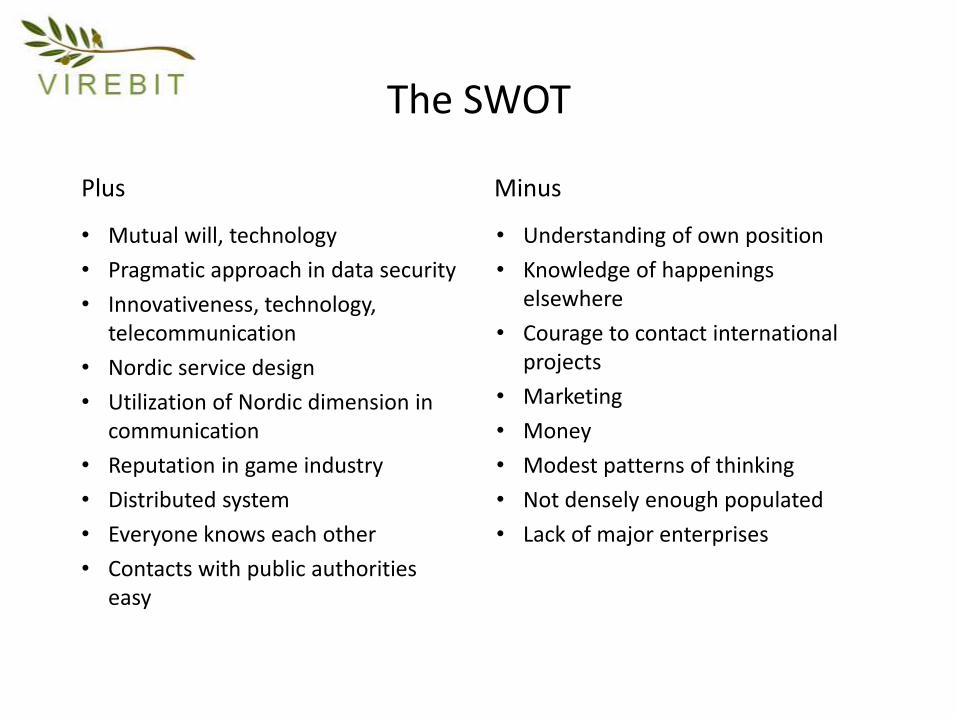

The SWOT

Plus

• Mutual will, technology

• Pragmatic approach in data security

• Innovativeness, technology, telecommunication

• Nordic service design

• Utilization of Nordic dimension in communication

• Reputation in game industry

• Distributed system

• Everyone knows each other

• Contacts with public authorities easy

Minus

• Understanding of own position

• Knowledge of happenings elsewhere

• Courage to contact international projects

• Marketing

• Money

• Modest patterns of thinking

• Not densely enough populated

• Lack of major enterprises