Embed Size (px)

Citation preview

Headquartered in Gurgaon, Valueonshore Advisors is a specialized professional ser-

vices firm of Big 4 alumni and Industry exec-utives. Our client portfolio includes multi-billion dollar companies, mid-cap public, and

pre IPO companies that range from late stage to early stage. We are a partner of choice for numerous multinational and Indian

clients who engage us for our unique combi-nation of functional expertise and industry knowledge, and for our objective solutions to

complex problems. The respect and rever-ence that the Firm commands is evident from the fact that it is consistently recog-

nized for the work done for its clients.

Service Lines:

Transaction Advisory Services

Business Risk Services

Assurance and Accounting Advisory

Strategic Outsourcing

Indian GAAP and Ind AS

Executive Summary

India has made a commitment for convergence of Indian Accounting standards (‘Ind AS’) with International Financial Reporting Standards (‘IFRS’). The aim is to harmonize the difference between two set of standards to the extent possi-ble. Accordingly, The Ministry of Corporate Affairs (‘MCA’) has notified the com-panies (Indian accounting standards) Rules 2015 on 16th February, 2015 which specify the applicability, recognition and measurement of items related to Finan-cial Statements in accordance with Indian Accounting Standards. We have briefly compared the present IGAAP with Ind AS to understand how

Fair Valuation will impact Financial Statements of Companies in India.

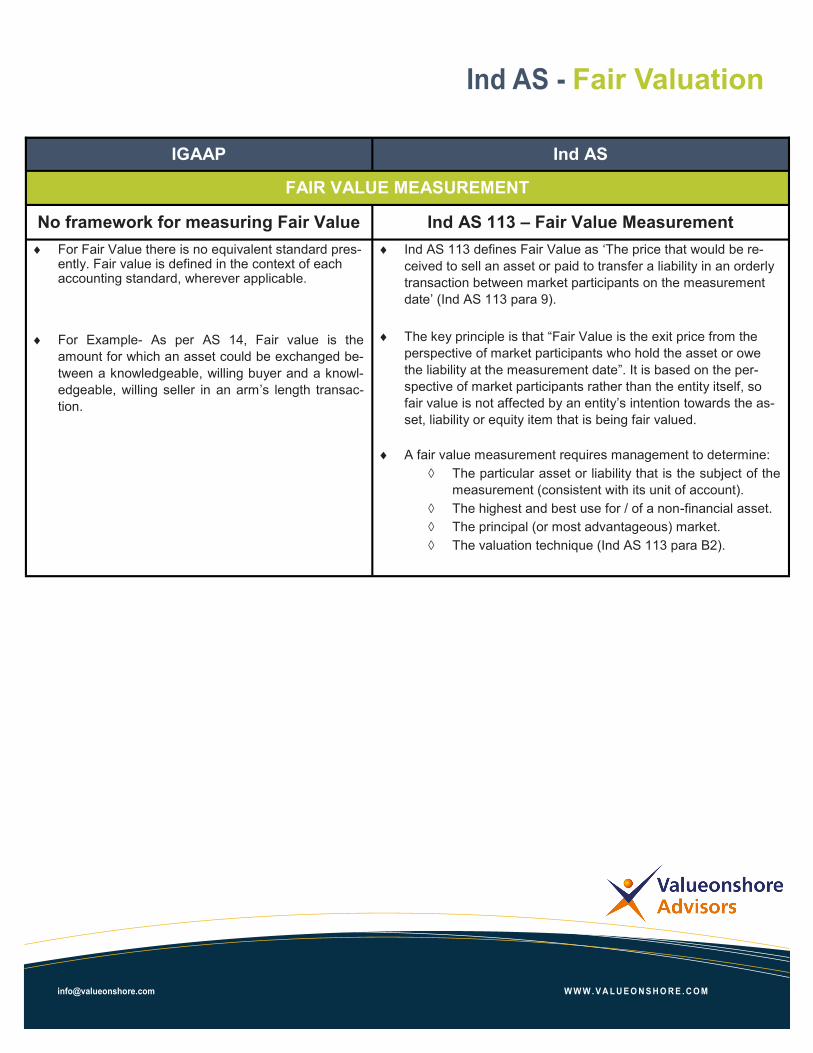

Fair Valuation

IGAAP Ind AS

FAIR VALUE MEASUREMENT

No framework for measuring Fair Value Ind AS 113 – Fair Value Measurement

For Fair Value there is no equivalent standard pres-ently. Fair value is defined in the context of each accounting standard, wherever applicable.

For Example- As per AS 14, Fair value is the

amount for which an asset could be exchanged be-

tween a knowledgeable, willing buyer and a knowl-

edgeable, willing seller in an arm’s length transac-

tion.

Ind AS 113 defines Fair Value as ‘The price that would be re-

ceived to sell an asset or paid to transfer a liability in an orderly

transaction between market participants on the measurement

date’ (Ind AS 113 para 9).

The key principle is that “Fair Value is the exit price from the

perspective of market participants who hold the asset or owe

the liability at the measurement date”. It is based on the per-

spective of market participants rather than the entity itself, so

fair value is not affected by an entity’s intention towards the as-

set, liability or equity item that is being fair valued.

A fair value measurement requires management to determine:

The particular asset or liability that is the subject of the

measurement (consistent with its unit of account).

The highest and best use for / of a non-financial asset.

The principal (or most advantageous) market.

The valuation technique (Ind AS 113 para B2).

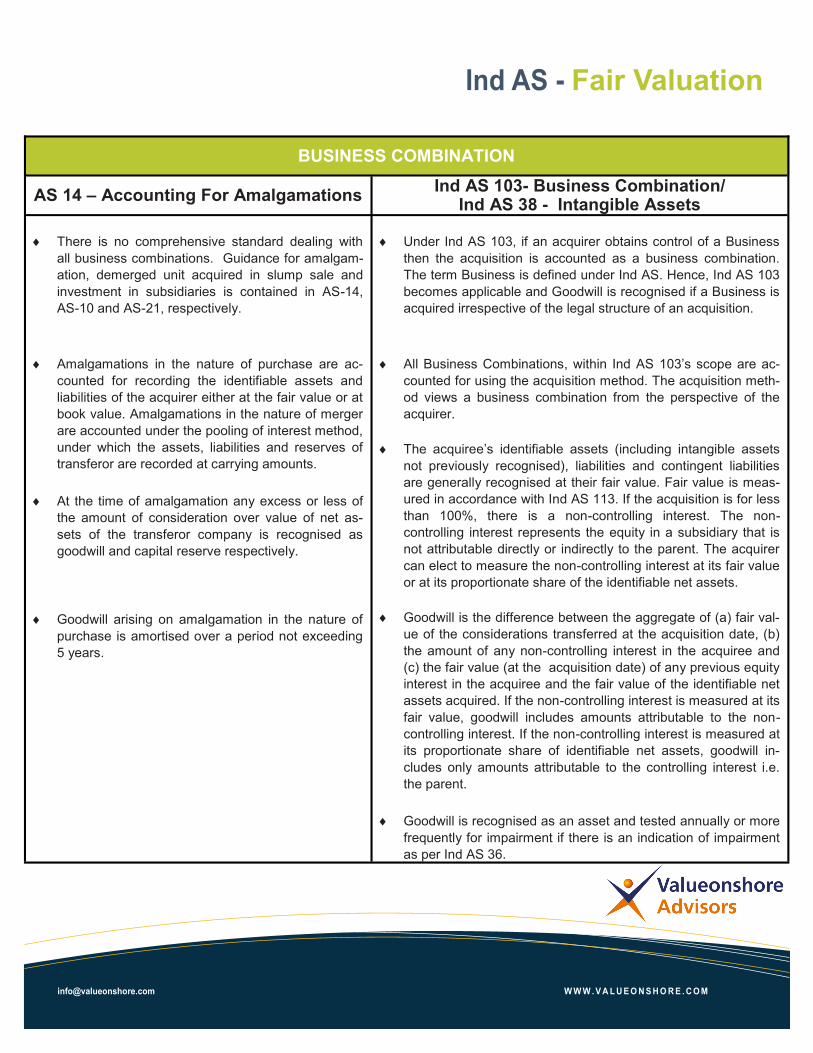

BUSINESS COMBINATION

AS 14 – Accounting For Amalgamations Ind AS 103- Business Combination/

Ind AS 38 - Intangible Assets

There is no comprehensive standard dealing with

all business combinations. Guidance for amalgam-

ation, demerged unit acquired in slump sale and

investment in subsidiaries is contained in AS-14,

AS-10 and AS-21, respectively.

Amalgamations in the nature of purchase are ac-

counted for recording the identifiable assets and

liabilities of the acquirer either at the fair value or at

book value. Amalgamations in the nature of merger

are accounted under the pooling of interest method,

under which the assets, liabilities and reserves of

transferor are recorded at carrying amounts.

At the time of amalgamation any excess or less of

the amount of consideration over value of net as-

sets of the transferor company is recognised as

goodwill and capital reserve respectively.

Goodwill arising on amalgamation in the nature of

purchase is amortised over a period not exceeding

5 years.

Under Ind AS 103, if an acquirer obtains control of a Business

then the acquisition is accounted as a business combination.

The term Business is defined under Ind AS. Hence, Ind AS 103

becomes applicable and Goodwill is recognised if a Business is

acquired irrespective of the legal structure of an acquisition.

All Business Combinations, within Ind AS 103’s scope are ac-

counted for using the acquisition method. The acquisition meth-

od views a business combination from the perspective of the

acquirer.

The acquiree’s identifiable assets (including intangible assets

not previously recognised), liabilities and contingent liabilities

are generally recognised at their fair value. Fair value is meas-

ured in accordance with Ind AS 113. If the acquisition is for less

than 100%, there is a non-controlling interest. The non-

controlling interest represents the equity in a subsidiary that is

not attributable directly or indirectly to the parent. The acquirer

can elect to measure the non-controlling interest at its fair value

or at its proportionate share of the identifiable net assets.

Goodwill is the difference between the aggregate of (a) fair val-

ue of the considerations transferred at the acquisition date, (b)

the amount of any non-controlling interest in the acquiree and

(c) the fair value (at the acquisition date) of any previous equity

interest in the acquiree and the fair value of the identifiable net

assets acquired. If the non-controlling interest is measured at its

fair value, goodwill includes amounts attributable to the non-

controlling interest. If the non-controlling interest is measured at

its proportionate share of identifiable net assets, goodwill in-

cludes only amounts attributable to the controlling interest i.e.

the parent.

Goodwill is recognised as an asset and tested annually or more

frequently for impairment if there is an indication of impairment

as per Ind AS 36.

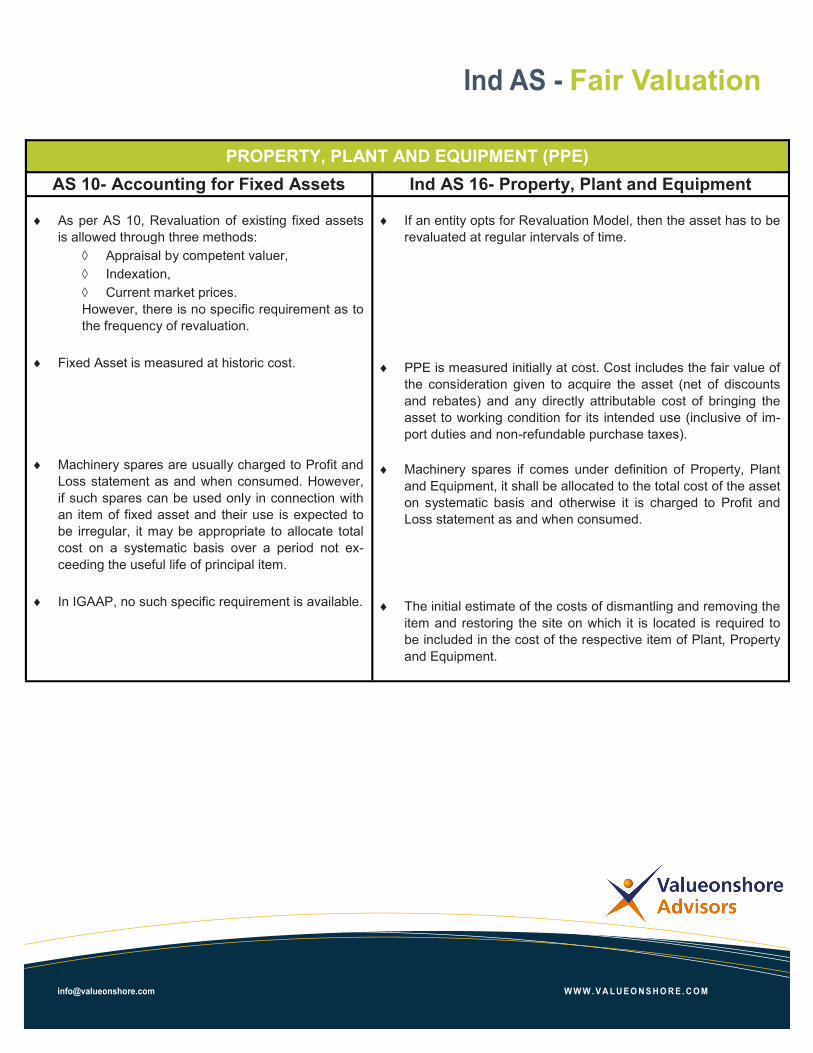

Fair Valuation

PROPERTY, PLANT AND EQUIPMENT (PPE)

AS 10- Accounting for Fixed Assets Ind AS 16- Property, Plant and Equipment

As per AS 10, Revaluation of existing fixed assets

is allowed through three methods:

Appraisal by competent valuer,

Indexation,

Current market prices.

However, there is no specific requirement as to

the frequency of revaluation.

Fixed Asset is measured at historic cost.

Machinery spares are usually charged to Profit and

Loss statement as and when consumed. However,

if such spares can be used only in connection with

an item of fixed asset and their use is expected to

be irregular, it may be appropriate to allocate total

cost on a systematic basis over a period not ex-

ceeding the useful life of principal item.

In IGAAP, no such specific requirement is available.

If an entity opts for Revaluation Model, then the asset has to be

revaluated at regular intervals of time.

PPE is measured initially at cost. Cost includes the fair value of

the consideration given to acquire the asset (net of discounts

and rebates) and any directly attributable cost of bringing the

asset to working condition for its intended use (inclusive of im-

port duties and non-refundable purchase taxes).

Machinery spares if comes under definition of Property, Plant

and Equipment, it shall be allocated to the total cost of the asset

on systematic basis and otherwise it is charged to Profit and

Loss statement as and when consumed.

The initial estimate of the costs of dismantling and removing the

item and restoring the site on which it is located is required to

be included in the cost of the respective item of Plant, Property

and Equipment.

Fair Valuation

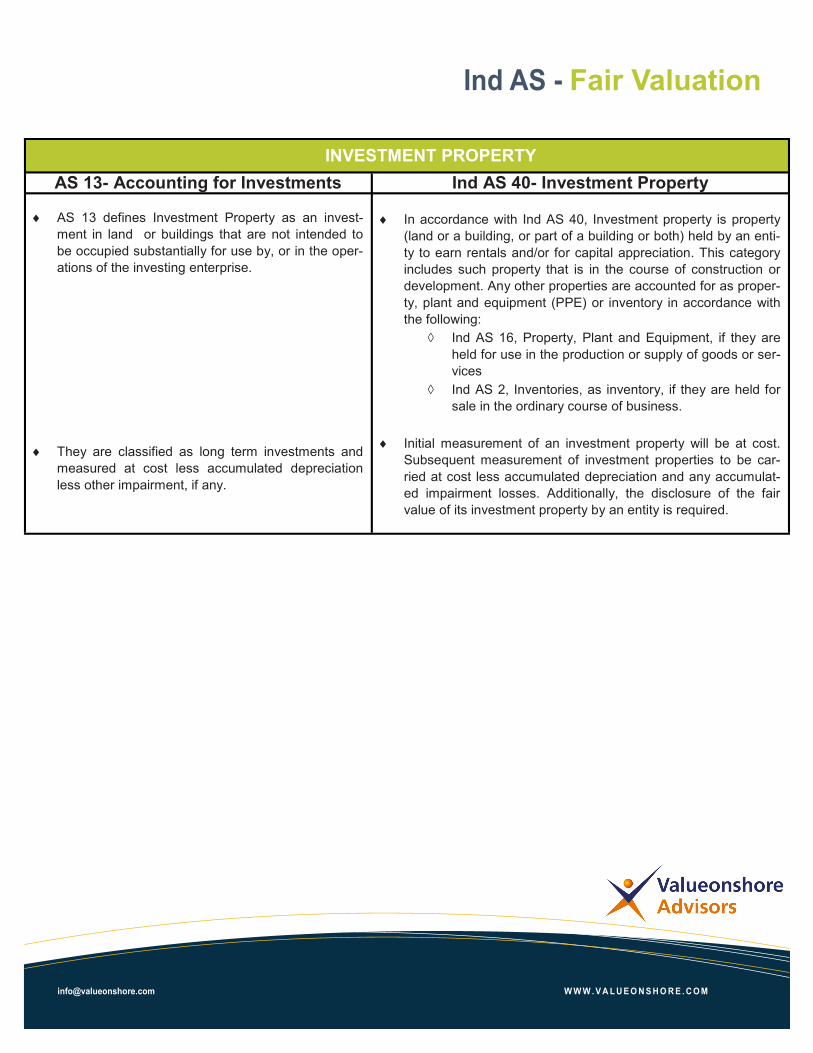

INVESTMENT PROPERTY

AS 13- Accounting for Investments Ind AS 40- Investment Property

AS 13 defines Investment Property as an invest-

ment in land or buildings that are not intended to

be occupied substantially for use by, or in the oper-

ations of the investing enterprise.

They are classified as long term investments and

measured at cost less accumulated depreciation

less other impairment, if any.

In accordance with Ind AS 40, Investment property is property

(land or a building, or part of a building or both) held by an enti-

ty to earn rentals and/or for capital appreciation. This category

includes such property that is in the course of construction or

development. Any other properties are accounted for as proper-

ty, plant and equipment (PPE) or inventory in accordance with

the following:

Ind AS 16, Property, Plant and Equipment, if they are

held for use in the production or supply of goods or ser-

vices

Ind AS 2, Inventories, as inventory, if they are held for

sale in the ordinary course of business.

Initial measurement of an investment property will be at cost.

Subsequent measurement of investment properties to be car-

ried at cost less accumulated depreciation and any accumulat-

ed impairment losses. Additionally, the disclosure of the fair

value of its investment property by an entity is required.

Fair Valuation

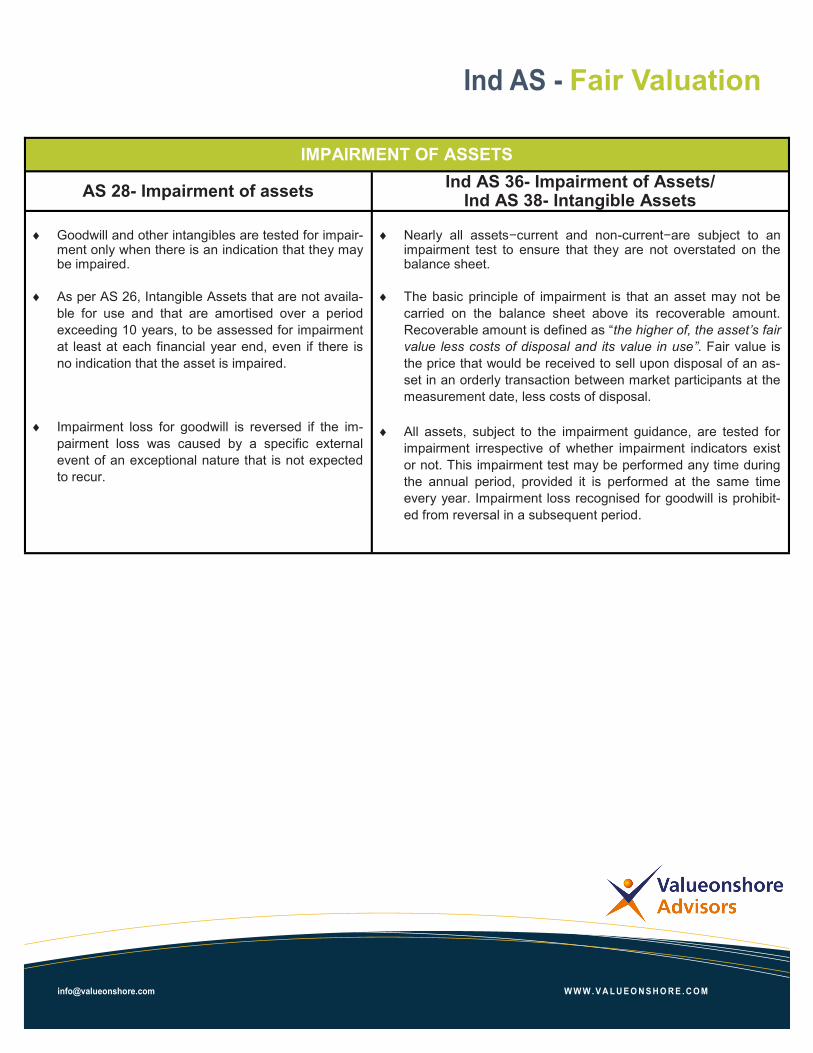

IMPAIRMENT OF ASSETS

AS 28- Impairment of assets Ind AS 36- Impairment of Assets/

Ind AS 38- Intangible Assets

Goodwill and other intangibles are tested for impair-

ment only when there is an indication that they may be impaired.

As per AS 26, Intangible Assets that are not availa-

ble for use and that are amortised over a period

exceeding 10 years, to be assessed for impairment

at least at each financial year end, even if there is

no indication that the asset is impaired.

Impairment loss for goodwill is reversed if the im-

pairment loss was caused by a specific external

event of an exceptional nature that is not expected

to recur.

Nearly all assets−current and non-current−are subject to an

impairment test to ensure that they are not overstated on the balance sheet.

The basic principle of impairment is that an asset may not be

carried on the balance sheet above its recoverable amount.

Recoverable amount is defined as “the higher of, the asset’s fair

value less costs of disposal and its value in use”. Fair value is

the price that would be received to sell upon disposal of an as-

set in an orderly transaction between market participants at the

measurement date, less costs of disposal.

All assets, subject to the impairment guidance, are tested for

impairment irrespective of whether impairment indicators exist

or not. This impairment test may be performed any time during

the annual period, provided it is performed at the same time

every year. Impairment loss recognised for goodwill is prohibit-

ed from reversal in a subsequent period.

Fair Valuation

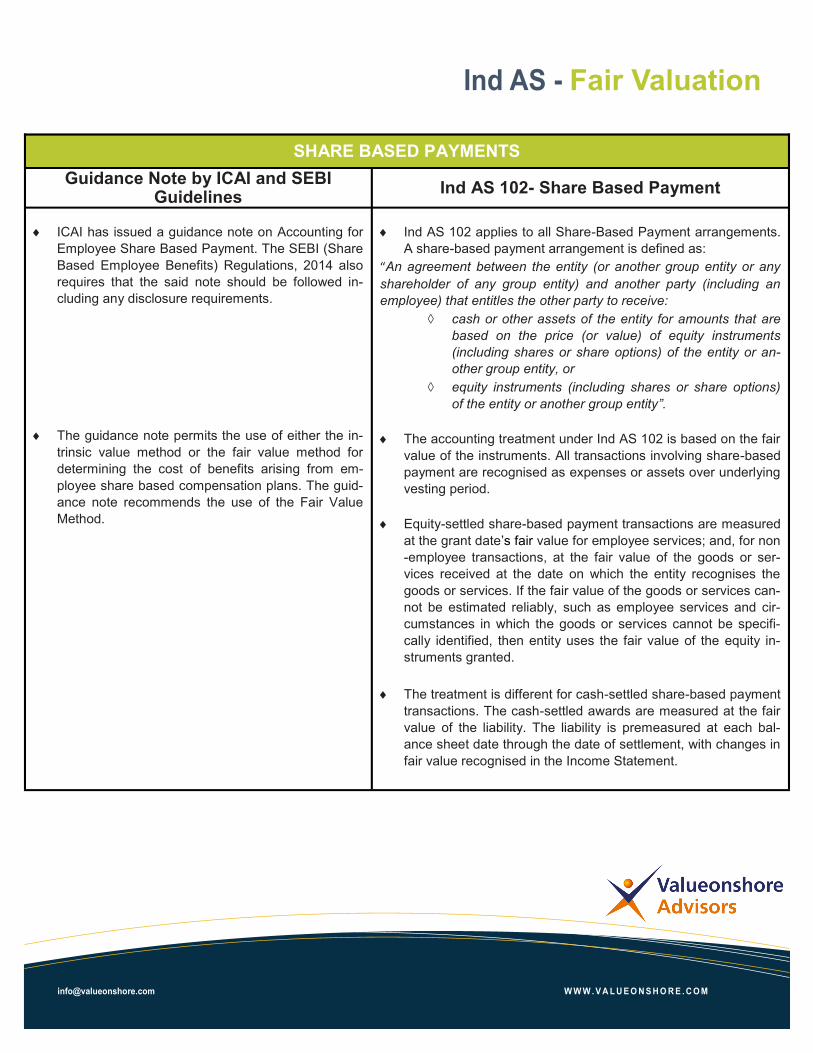

SHARE BASED PAYMENTS

Guidance Note by ICAI and SEBI Guidelines

Ind AS 102- Share Based Payment

ICAI has issued a guidance note on Accounting for

Employee Share Based Payment. The SEBI (Share

Based Employee Benefits) Regulations, 2014 also

requires that the said note should be followed in-

cluding any disclosure requirements.

The guidance note permits the use of either the in-

trinsic value method or the fair value method for

determining the cost of benefits arising from em-

ployee share based compensation plans. The guid-

ance note recommends the use of the Fair Value

Method.

Ind AS 102 applies to all Share-Based Payment arrangements.

A share-based payment arrangement is defined as:

“An agreement between the entity (or another group entity or any

shareholder of any group entity) and another party (including an

employee) that entitles the other party to receive:

cash or other assets of the entity for amounts that are

based on the price (or value) of equity instruments

(including shares or share options) of the entity or an-

other group entity, or

equity instruments (including shares or share options)

of the entity or another group entity”.

The accounting treatment under Ind AS 102 is based on the fair

value of the instruments. All transactions involving share-based

payment are recognised as expenses or assets over underlying

vesting period.

Equity-settled share-based payment transactions are measured

at the grant date’s fair value for employee services; and, for non

-employee transactions, at the fair value of the goods or ser-

vices received at the date on which the entity recognises the

goods or services. If the fair value of the goods or services can-

not be estimated reliably, such as employee services and cir-

cumstances in which the goods or services cannot be specifi-

cally identified, then entity uses the fair value of the equity in-

struments granted.

The treatment is different for cash-settled share-based payment

transactions. The cash-settled awards are measured at the fair

value of the liability. The liability is premeasured at each bal-

ance sheet date through the date of settlement, with changes in

fair value recognised in the Income Statement.

Fair Valuation

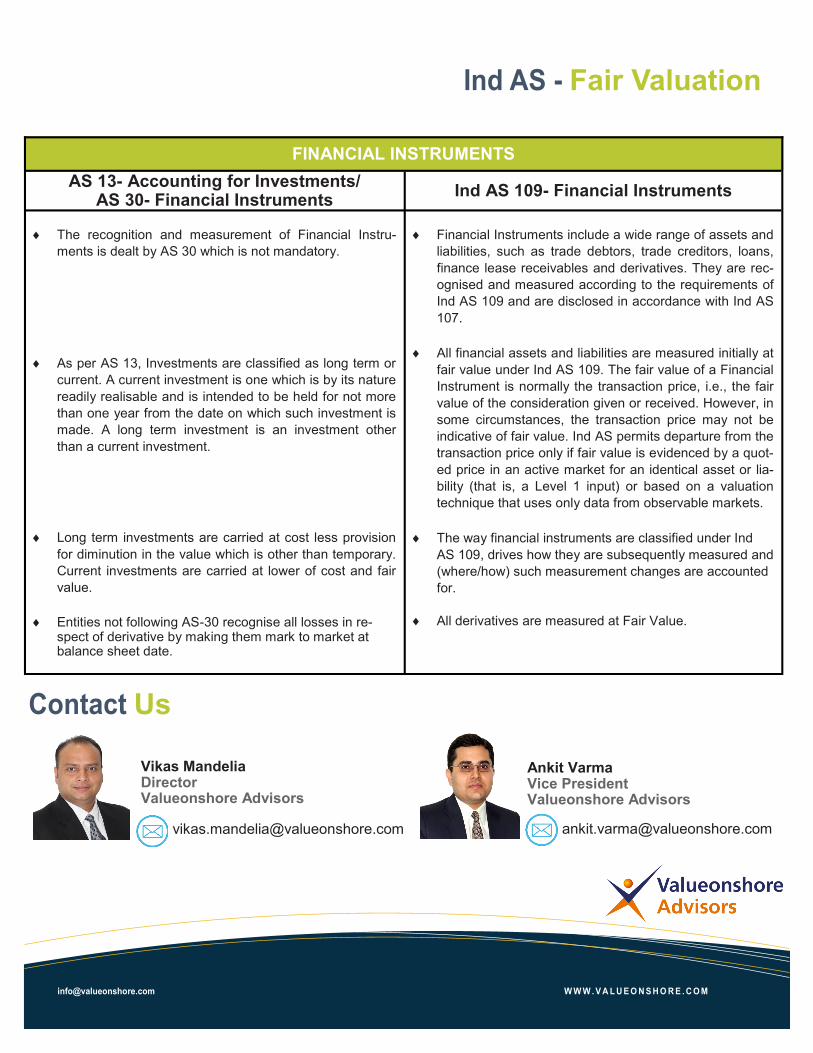

FINANCIAL INSTRUMENTS

AS 13- Accounting for Investments/ AS 30- Financial Instruments

Ind AS 109- Financial Instruments

The recognition and measurement of Financial Instru-

ments is dealt by AS 30 which is not mandatory.

As per AS 13, Investments are classified as long term or

current. A current investment is one which is by its nature

readily realisable and is intended to be held for not more

than one year from the date on which such investment is

made. A long term investment is an investment other

than a current investment.

Long term investments are carried at cost less provision

for diminution in the value which is other than temporary.

Current investments are carried at lower of cost and fair

value.

Entities not following AS-30 recognise all losses in re-spect of derivative by making them mark to market at balance sheet date.

Financial Instruments include a wide range of assets and

liabilities, such as trade debtors, trade creditors, loans,

finance lease receivables and derivatives. They are rec-

ognised and measured according to the requirements of

Ind AS 109 and are disclosed in accordance with Ind AS

107.

All financial assets and liabilities are measured initially at

fair value under Ind AS 109. The fair value of a Financial

Instrument is normally the transaction price, i.e., the fair

value of the consideration given or received. However, in

some circumstances, the transaction price may not be

indicative of fair value. Ind AS permits departure from the

transaction price only if fair value is evidenced by a quot-

ed price in an active market for an identical asset or lia-

bility (that is, a Level 1 input) or based on a valuation

technique that uses only data from observable markets.

The way financial instruments are classified under Ind

AS 109, drives how they are subsequently measured and

(where/how) such measurement changes are accounted

for.

All derivatives are measured at Fair Value.

Fair Valuation

Us

Vikas Mandelia Director Valueonshore Advisors

Ankit Varma Vice President Valueonshore Advisors