Embed Size (px)

Citation preview

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

1 Compiled by Partha Sarathi De

Contents Pg. No

Abbreviations used 1

Chapters 1 Introduction 3

Table 1.1 IND AS TO CORRESPONDING AS/ GUIDANCE NOTE (GN) 9

Chapter 2 PARA WISE COMPARATIVE STUDY OF IND AS I PRESENTATION OF FS WITH AS 1- DISCLOSURE OF ACCOUNTING POLICIES AND SCHEDULE III OF COMPANIES ACT, 2013 AND OTHERS AS MENTIONED

13

Chapter 3 COMPARATIVE STUDY OF SOME IND ASs (other than Ind AS I)

87

-IND AS :2

:7

:8

:10

:11

:12

:16

:17

:18

:19

:20

:21

:23

:24

:27

:28

:31

:32

:33

:34

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

2 Compiled by Partha Sarathi De

:36

:37

:38

:39

:103

:105

:107

:108

Appendix A Companies (Accounting Standards) Amendment Rules, 2016, dated 30.03.16 121

Appendix B Pronouncement , Enactment, AS, GN issued by ICAI books, publication, media report perused for making the study

212

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

3 Compiled by Partha Sarathi De

Abbreviations used

AS Accounting Standard(s) established by ICAI

SA Standard(s) on Auditing established by ICAI

ASB Accounting Standard Board, ICAI

AOCI Accumulated Other Comprehensive Income

EPS Earnings Per Share

FASB Financial Accounting Standards Board

FVTOCI Fair Value Through Other Comprehensive Income

FVTPL Fair Value Through Profit or Loss

GAAP Generally Accepted Accounting Principles

IAS International Accounting Standards

IASB International Accounting Standards Board

ICAI The Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

IFRIC International Financial Reporting Interpretations Committee (now renamed as IFRS Interpretations Committee) and the Interpretations issued by that Committee

Ind AS Indian Accounting Standards converged with IFRS

MCA Ministry of Corporate Affairs

NBFC Non-banking financial company

OCI Other comprehensive income

RBI Reserve Bank of India

Schedule III Schedule III to the Companies Act, 2013

SIC Standing Interpretations Committee of the International Accounting Standards Committee and the interpretations issued by that committee

SEBI Securities and Exchange Board of India

Rule Companies (Indian Accounting Standard) Rules, 2015

GN Guidance Note to AS, ICAI

The Act Companies Act, 2013

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

4 Compiled by Partha Sarathi De

Chapter I Introduction

1.1. In the age of Globalisation, Convergence with IASs /IFRSs issued by IASB, is requirement. More than hundred countries are currently requiring and permitting the use of or have a policy of convergence.

1.2. The MCA issued a notification dated 16.02.15 announcing (Indian Accounting Standard) Rules 2015 for applicability of Ind ASwith the amendments made vide Companies (Indian Accounting Standards) (Amendment)Rules, 2016 dated 30 March 2016

1.3. ‘Indian GAAP” or AS are standards notified by the Central Government under the Companies (Accounting Standard) Rules, 2006 (applicable to all companies) vide notification G.S.R.739(E) dated 07.12.06 as amended and to the relevant requirements od the companies act 2013. Ind AS refers to the accounting standard as specified in the Annexure to the Companies (Indian Accounting Standards) Rules 2015.

1.4. Companies not covered in the Rule

Banking, insurance and NBFCs have been excluded. As mentioned in the Finance Minister’s Budget speech, it is expected that the implementation date for these companies shall be notified separately.

Companies whose securities are listed or are in the process of listing on SME exchanges as referred to in chapter XB or on the institutional trading platform without initial public offering in accordance with the provisions of chapter XC of Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009. These companies shall continue to comply with the existing accounting standards unless they choose otherwise.

Overseas subsidiaries, associates, joint ventures and other similar entities of an Indian company may prepare their standalone financial statements in accordance with the requirements of the specific jurisdiction provided that the concerned Indian company prepares its consolidated financial statements in accordance with Ind AS either voluntarily or mandatorily if it meets the criteria.

Companies not covered by the rules shall continue to apply the existing accounting standards prescribed in the Annexure to the Companies (Accounting Standards) Rules, 2006.

1.5. Road Map of Mandatory Applicability

Phase I

Ind AS will be mandatorily applicable to the following companies for periods beginning on or after 1 April 2016, with comparatives for the period

ending 31 March 2016 or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having

net worth of 500 crore INR or more.

Companies having net worth of 500 crore INR or more other than those covered above.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

5 Compiled by Partha Sarathi De

Holding, subsidiary, joint venture or associate companies of companies covered above.

Phase II

Ind AS will be mandatorily applicable to the following companies for periods beginning on or after 1 April 2017, with comparatives for the period

ending 31 March 2017 or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of being listed on any stock exchange in India or outside India and

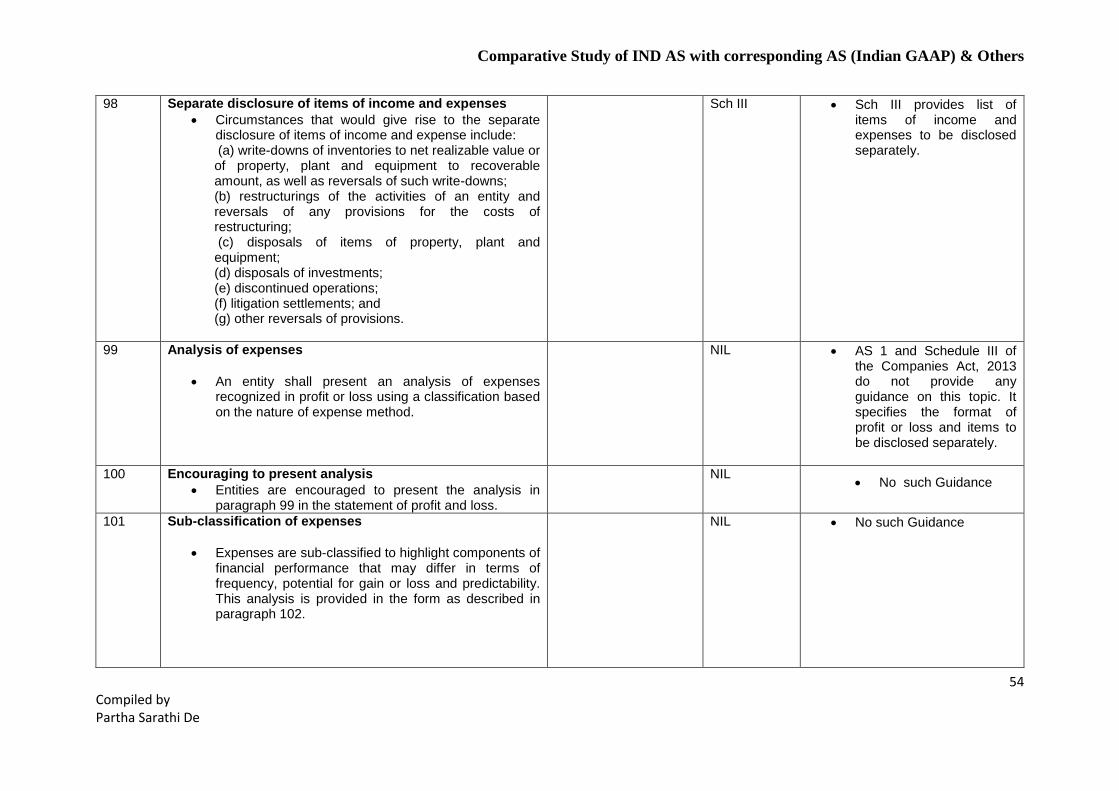

having net worth of less than rupees 500 Crore.

Unlisted companies other than those covered in Phase I and Phase II whose net worth are more than 250 crore INR but less than 500 crore INR.

Holding, subsidiary, joint venture or associate companies of above companies.

The Roadmap for IND AS implementation in Banks, NBFC & Insurance companies has been rolled out from 2018-19.

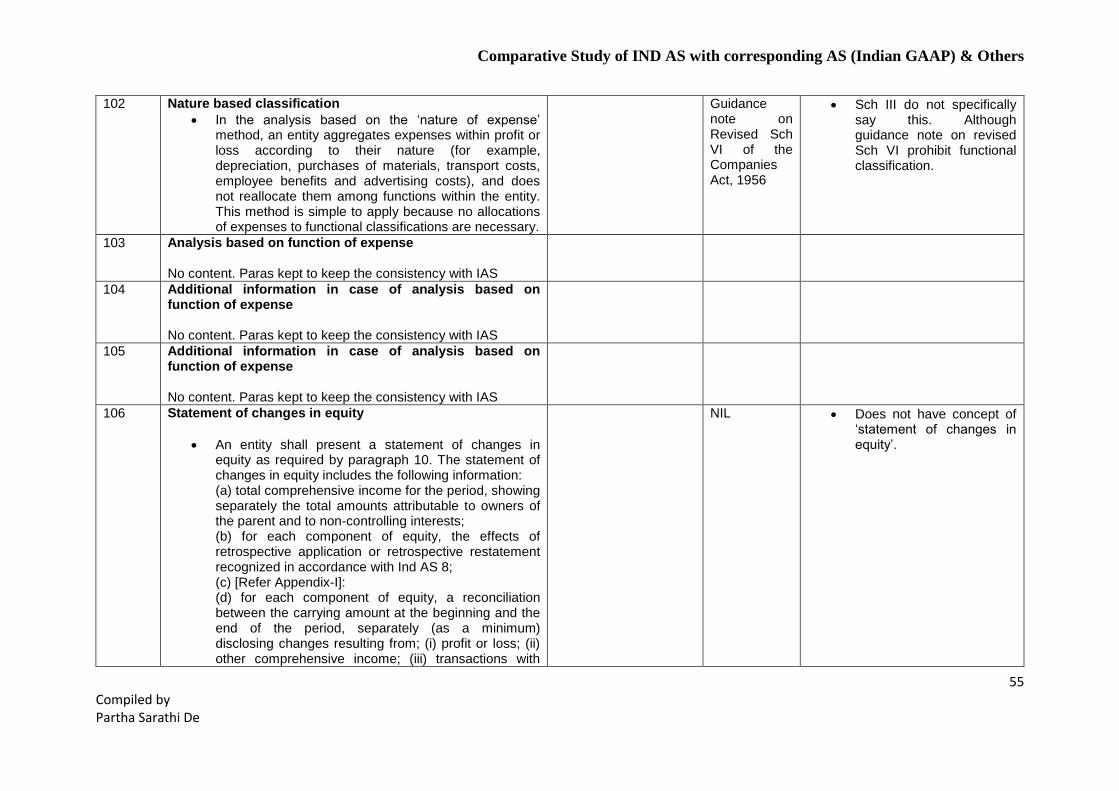

1.6. Voluntary adoption

Companies can voluntarily adopt Ind AS for accounting periods beginning on or after 1 April 2015 with comparatives for period ending 31 March

2015 or thereafter. However, once they have chosen this path, they cannot switch back.

1.7. Deviations Notified Ind ASs contain a number of deviations from IFRS because of convergence; some differences have resulted into non- compliance with IFRS. A few differences between Ind ASs and IFRSs are because of removal of certain options or alternatives given in IFRS have been minimized. Because of this an Ind ASs entity cannot be treated as non- compliant with IFRS.

1.8. Clarification in the Notification to Open Questions

The notification has clarified many open questions.Some of the clarifications are given below: -

The date and manner of calculation of net worth has been spelled out. It has been clarified that net worth will be determined based on the

standalone accounts of the company as on 31 March 2014 or the first audited period ending after that date.

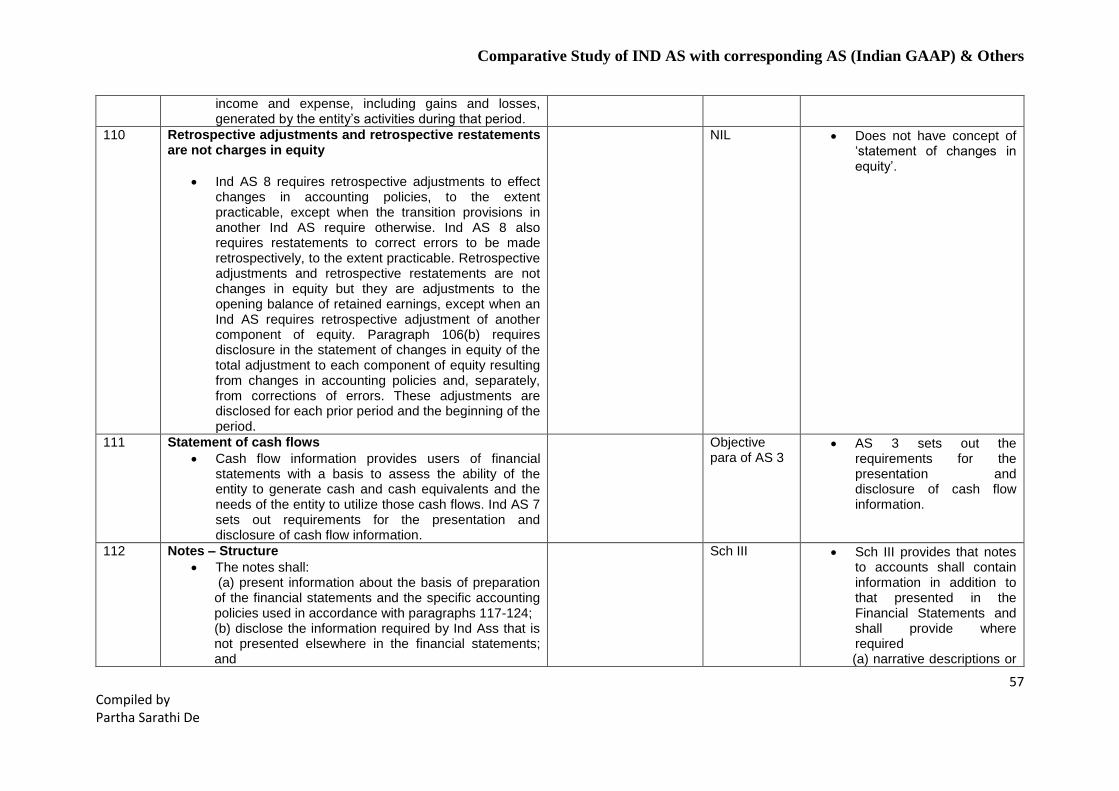

Net worth has been defined to have the same meaning as per section 2(57) of the Companies Act, 2013. It is the aggregate value of the paid-

up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the

accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not

include reserves created out of revaluation of assets, write-back of depreciation and amalgamation

It is now clear that Ind AS will apply to both consolidated and stand-alone FSs of a company covered by the roadmap. This is helpful as

companies will not have to maintain dual accounting systems.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

6 Compiled by Partha Sarathi De

It is a relief that an overseas subsidiary, associate or joint venture of an Indian company is not required to prepare its stand-alone FSs as per

the Ind AS, and instead, may continue with its jurisdictional requirements. However, these entities will still have to report their Ind AS adjusted

numbers for their Indian parent company to prepare consolidated Ind AS accounts.

All listed companies (except companies listed on SME exchanges) and companies having a net worth of 250 crore INR or more will be

required to adopt Ind AS. Companies not covered by the rules will continue to apply the existing accounting standards.

The requirement to present comparatives implies that companies impacted by phase I will require an Ind -AS compliant opening balance

sheet as of 1 April 2015.

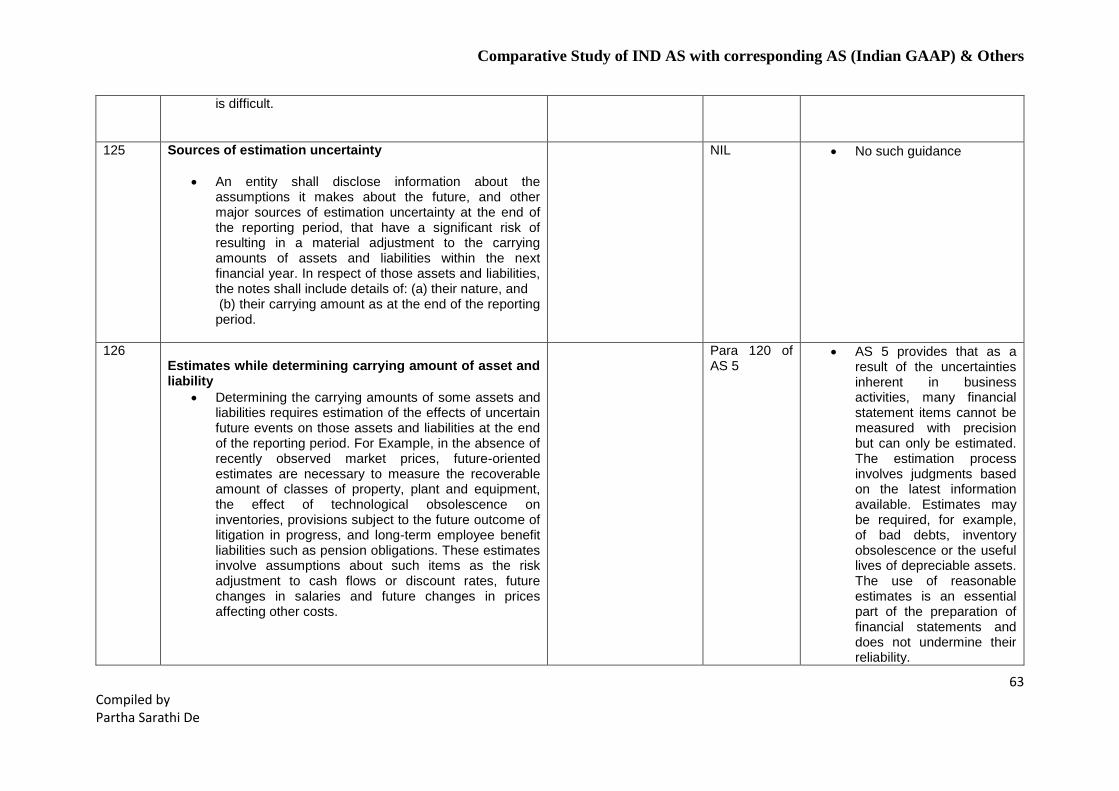

The debate on two of the most significant standards, Revenue Recognition and Financial Instruments has now been settled with them being

notified. Interestingly, India will be one of the first countries to mandatorily adopt these standards from 1 April 2015 while the rest of the world

will follow from 2017. These two standards will have a significant effect on entities, impacting not only their financial results but also catalysing

numerous organisational and business changes.

There was hope that companies will be given an option to prepare their FSs as per IFRS issued by the IASB (the true IFRS), which has been

now ruled out.

The rules specify that in case of conflict between Ind AS and a law, the provisions of the law shall prevail and the FSs shall be

prepared in conformity with it.

1.9. Transition : Carve Outs There are also certain general differences between Ind AS and IFRS/IAS.The transitional provisions, wherever considered appropriate, have been included Terminology, used in Ind AS,is not similar to IFRS. The term balance sheet is used instead of statement of financial position and ‘statement of Profit & Loss’ is used instead of ‘statement of Comprehensive income’.

Some of these carve outs diminish comparability of Ind AS with the globally accepted IFRS/IAS. These need to be carefully evaluated , to overcome facilitate comparisons. Some significant carve outs to be considered, are in the areas of negative goodwill arising on business combinations, operating leases with rent escalations, accounting for foreign currency convertible bonds and major breaches of long tenure debt covenants.

1.10.1 Contents in Companies (Indian Accounting Standards) (Amendment)Rules, 2016 dated 30 March 2016 are in Appendix A 1.10.2 Key highlights of the Amendment made are

Notification of Ind AS 11

Notification of Ind AS 18

Ind AS 115, ‘Revenue from contracts with customers’, omitted

Amendment to IND AS 1 regarding - ' Materiality' , 'Disaggregations & subtotals', 'Notes structure' and 'Disclosure'

Amendment to Ind AS 34,‘Interim financial reporting’

Amendment to IND AS 28, 112 and 110

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

7 Compiled by Partha Sarathi De

Furthermore, the rules also amended existing Ind AS to reflect the amendments made by IASB to the IFRS

1.10.3 The Rules also amended Ind AS 101, ‘First-time adoption of Indian Accounting Standards’, to remove the option to use fair value for investment property as the deemed cost on the date of transition.

1.11 Framework Quote The existing Framework for the Preparation and Presentation of FSs (issued by ICAI in July 2000) will continue to remain effective for the existing Accounting Standards as these standards contain references to it. There are certain minor differences in the Framework for the existing Accounting Standards and the Framework for the Indian Accounting Standards which are included as Appendix A to the Framework. In near future, the ICAI proposes to integrate both – the Framework for the existing Accounting Standards and the Framework for Indian Accounting Standards – and issue one Framework for both sets of the Standards. Appendix A Note: This Appendix is not a part of the Framework for the Preparation and Presentation of FSs in accordance with Indian Accounting Standards. The purpose of this Appendix is only to bring out the differences between the Framework for the Preparation and Presentation of FSs in accordance with Indian Accounting Standards and the Framework for the Preparation and Presentation of FSs issued in July 2000 for the existing Accounting Standards

Comparison with existing Framework for the Preparation and Presentation of FSs issued in July 2000.

1. Consistency has been given separately in the existing Framework as one of the underlying assumptions. However, in the Framework in

accordance with Indian Accounting Standards, the same has been covered under the head ‘comparability’. (Paragraph 24 of the exiting Framework and Paragraph 39 of the Framework in accordance with Indian Accounting Standards )

2. The existing Framework provides that relevance of information is affected by its materiality. However, as per the Framework in accordance with

Indian Accounting Standards, relevance of information is affected by its nature and materiality. It provides that in some cases, irrespective of materiality, nature of information could alone determine the relevance of information. (Paragraph 30 of the exiting Framework and Paragraph 29 of the Framework in accordance with Indian Accounting Standards )

3. The Framework in accordance with Indian Accounting Standards provides that balance sheets drawn up in accordance with current Indian

Accounting Standards may include items that do not satisfy the definitions of an asset or liability and are not shown as part of equity. The definitions set out in the framework will, however, underlie future reviews of the Indian Accounting Standards and the formulation of further Standards. The existing Framework is silent on this aspect. (Paragraph 24 of the exiting Framework and Paragraph 39 of the Framework in accordance with Indian Accounting Standards)

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

8 Compiled by Partha Sarathi De

4. The Framework in accordance with Indian Accounting Standards provides that gains are often reported net of related expenses. Similarly, losses are often reported net of related income. Netting of gains or losses is not there in the existing Framework. (Paragraphs 76 and 80 of the Framework in accordance with Indian Accounting Standards)

Unquote

1.11.1 While discharging the attest function it is duty of member of ICAI that AS are implemented in the presentation of FS covered by the audit report. ICAI established ASB way back in 1977. Since then, the ASB has been working relentlessly in this direction by formulating new Accounting Standards as well as by revising the existing ASs, so as to bring them in line with the best international practices.

1.11.2 The ICAI has from time to time issued GN, primarily designed to provide guidance to members on matters which may arise in the course of their

professional work and on which they may desire assistance in resolving issues which may pose difficulty. These are recommendatory in nature.ASs have been last issued by the ICAI as on September1, 2014.

1.11.3 As per 143(3)(e) of Companies Act, 2013 (The act) it is required that the auditor’s report shall also state, whether in his opinion , the FSs complying

with the AS. Section 2(2) of the act defines the standards of accounting or any addendum thereto for companies or class of companies referred to in section 133 of the act.

1.11.4 As per section 133 of the act The central government may prescribed the standards of accounting or any addendum thereto, as recommended by the Institute of Chartered Accountants of India, constituted under Section 346 of the Chartered Accountants Act 1949 (38 of 1949), in consultation with and after examination of the recommendation made by the national financial reporting authority.

1.11.5 The companiesfor whom the Ind AS is mandatorily applicable are to comply Ind AS. Other companies are to comply AS if not they adopt Ind AS voluntarily.

1.12 Methodology

The study assigned was carried out in the following sequence

Review of the related pronouncement, enactment and the materials contained in the publication and web.

Analysis and assessment of comparison

Focus in the study is on differences that are commonly found in practice.

Comparison based on Ind AS pronounced under (Indian Accounting Standard) Rules 2015. No comparison could be made with those as amended

vide Companies (Indian Accounting Standards) (Amendment)Rules, 2016 dated 30 March 2016. Readers are requested to refer to Appendix A and

also with reference to the highlights provided in para 1.10.2 above

1.13.1 Conclusion Now India will have two sets of accounting standards viz. existing accounting standards under Companies (Accounting Standard) Rules, 2006 and IFRS converged Indian Accounting Standards(Ind AS). The Ind AS are named and numbered in the same way as the corresponding IFRS/IAS. NACAS recommend these standards to the Ministry of Corporate Affairs. The basic objective of Accounting Standards is to remove variations in the treatment

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

9 Compiled by Partha Sarathi De

of several accounting aspects and to bring about standardization in presentation. They intent to harmonize the diverse accounting policies followed in the preparation and presentation of FSs by different reporting enterprises so as to facilitate intra-firm and inter-firm comparison.

Ind AS corresponding to AS/ (GN) is tabled in Table 1 below with

Para- wise comparative study of Ind AS I Presentation of FS in Chapter II for its relevance of understanding and with summary

Summarised comparative study for the other Ind ASs in Chapter III.*(Note) * (Note) Focus in the summarised study is on differences that are commonly found in practice. All of the differences that exist or that may

be material to a particular entity’s financial statements are not included and need to be looked into as per requirement.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

10 Compiled by Partha Sarathi De

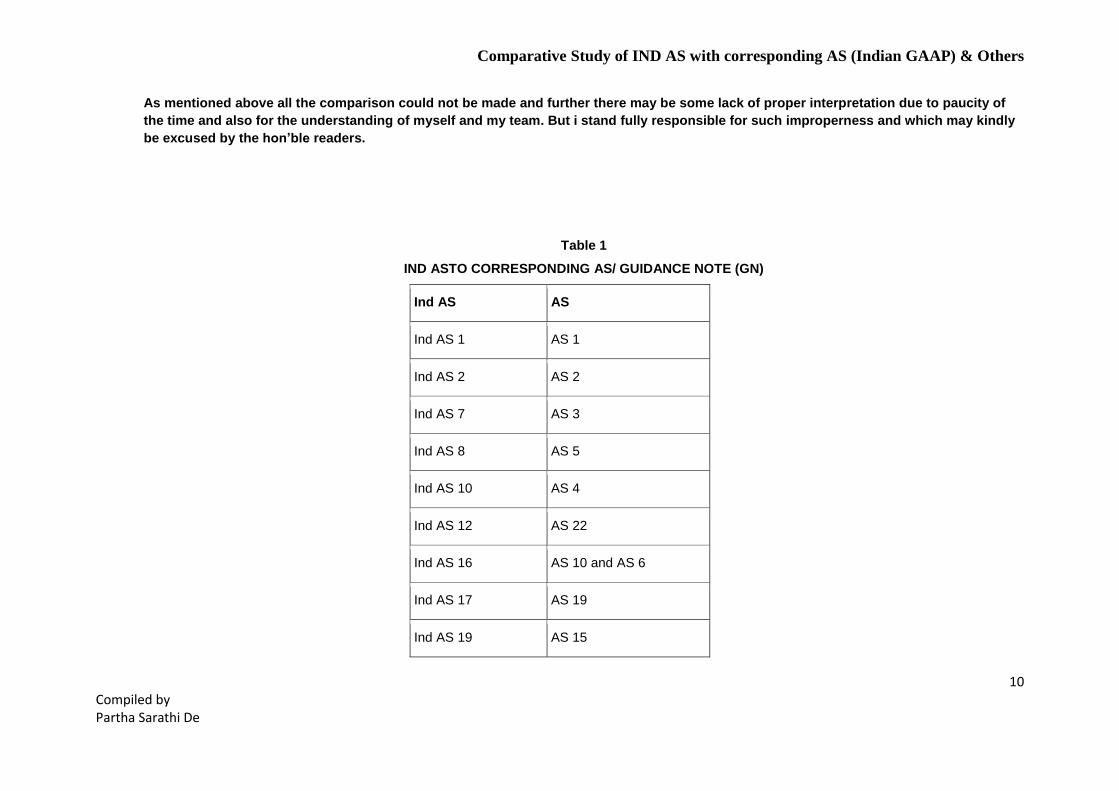

As mentioned above all the comparison could not be made and further there may be some lack of proper interpretation due to paucity of

the time and also for the understanding of myself and my team. But i stand fully responsible for such improperness and which may kindly

be excused by the hon’ble readers.

Table 1

IND ASTO CORRESPONDING AS/ GUIDANCE NOTE (GN)

Ind AS AS

Ind AS 1 AS 1

Ind AS 2 AS 2

Ind AS 7 AS 3

Ind AS 8 AS 5

Ind AS 10 AS 4

Ind AS 12 AS 22

Ind AS 16 AS 10 and AS 6

Ind AS 17 AS 19

Ind AS 19 AS 15

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

11 Compiled by Partha Sarathi De

Ind AS AS

Ind AS 20 AS 12

Ind AS 21 AS 11

Ind AS 23 AS 16

Ind AS 24 AS 18

Ind AS 27 AS 21

Ind AS 28 AS 23 and AS 27

Ind AS 29 -

Ind AS 32 AS 31

Ind AS 33 AS 20

Ind AS 34 AS 25

Ind AS 36 AS 28

Ind AS 37 AS 29

Ind AS 38 AS 26

Ind AS 40 AS 13

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

12 Compiled by Partha Sarathi De

Ind AS AS

Ind AS 41 -

Ind AS 101 -

Ind AS 102 GNON EMPLOYEE SHARE-BASED PAYMENTS

Ind AS 103 AS 14

Ind AS 104 -

Ind AS 105 AS 24

Ind AS 106 -

Ind AS 107 AS 32

Ind AS 108 AS 17

Ind AS 109 AS 30

Ind AS 110 AS 21

Ind AS 111 AS 27

Ind AS 112 AS 21, AS 23 and AS 27

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

13 Compiled by Partha Sarathi De

Ind AS AS

Ind AS 113 -

Ind AS 114 -

Ind AS 115 AS 9 and AS 7

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

14 Compiled by Partha Sarathi De

Chapter 2 PARA WISE COMPARATIVE STUDY OF IND AS I PRESENTATION OF FS WITH AS 1- DISCLOSURE OF ACCOUNTING POLICIES AND SCHEDULE III OF COMPANIES ACT, 2013 AND OTHERS AS MENTIONED

IND AS I

Corresponding AS I, Sch III & those as mentioned

Para Particulars AS/GN Corresponds to

1 Objective

basis for presentation of FS to ensure Comparability both with the entity’s FS of

previous periods and with the FS of other entities.

overall requirements for the presentation of FS guidelines for their structure and minimum requirements for their content.

AS 1- Disclosure of Accounting Policies

And SCHEDULE III OF COMPANIES ACT,

2013 And others as

mentioned

Paras 1 & 8 of AS 1 & Sch III

AS 1

disclosure of significant accounting policies followed in preparing and presenting FS to promote better

understanding of FS by establishing through an AS

facilitate a more meaningful comparison between FS of different enterprises.

Sch III

Provides general instructions for preparation of FS

2 Scope

To apply this Standard in preparing and presenting FS

Sch III Schedule III

Change in treatment or disclosure in the FSs or statements forming part thereof, for compliance with the requirements of the Act, shall be made with the modification the requirements of this Schedule accordingly.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

15 Compiled by Partha Sarathi De

The disclosure requirements specified are in addition to and not in substitution of the

disclosure requirements specified in the AS.

Additional disclosures specified in the AS shall be made in the notes to

accounts or by way of additional

statement unless required to be disclosed on the face of the FSs.

All other disclosures as required by the Act shall be made in the notes to accounts in addition to the requirements set out in this Schedule.

3 Others Ind AS Others Ind AS set out the recognition, measurement and disclosure requirements for specific transactions and other events.

NIL

No such Guidance

4 Structure of interim FSs

Prepared in accordance with Ind AS 34, Interim Financial Reporting.

However, paragraphs 15-35 apply to such FSs,equally applicable to all entities, including those that present consolidated FSs in

accordance with Ind AS 110, Consolidated FSs, and

those that present separate FSs as per Ind AS

NIL

Not specifically stated

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

16 Compiled by Partha Sarathi De

27, Separate FSs.

5 Entities for not for profit activities

Uses terminology that is suitable for profit oriented entities, including public sector business entities.

If entities with not for profit activities in the private sector or the public sector apply this Standard, they may need to amend the descriptions used for particular line items in the FSs and for the FSs themselves.

NIL

No such guidance.

6 Entities whose share capital is not equity

May need to adapt the FS presentation of members’ interests.

NIL No such guidance.

7 Definition – General purpose FSs

Those intended to meet the needs of users not in a position to require an entity to prepare reports tailored to their particular information needs.

NIL

No such definition.

7 Definition – Impracticable

Applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so.

NIL Not defined

7 Definition – Indian Accounting Standards (Ind AS)

Standards prescribed under section 133 of the Companies Act, 2013.

NIL

Defined in Companies (Accounting Standards) Rules, 2006.

7 Definition – Materiality

Material omissions or misstatements of items defined also in SA 320 which is similar as defined in Ind AS I

Principles defined in Standard on Auditing 320 ‘Materiality in planning and performing an

Material omissions or misstatements of items are defined in SA which is similar to definition of Ind AS 8.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

17 Compiled by Partha Sarathi De

audit’

7 Definition – Notes

Shall contain information in addition to that presented in the FSs and shall provide where required (a) narrative descriptions or disaggregations of items recognized in those statements; and (b) information about items that do not qualify for recognition in those statements.

Sch III SchIII provides that notes to accounts shall contain information, in addition to that presented in the FS, where required.This is similar to as defined in Ind AS

7 Definition – Other comprehensive income

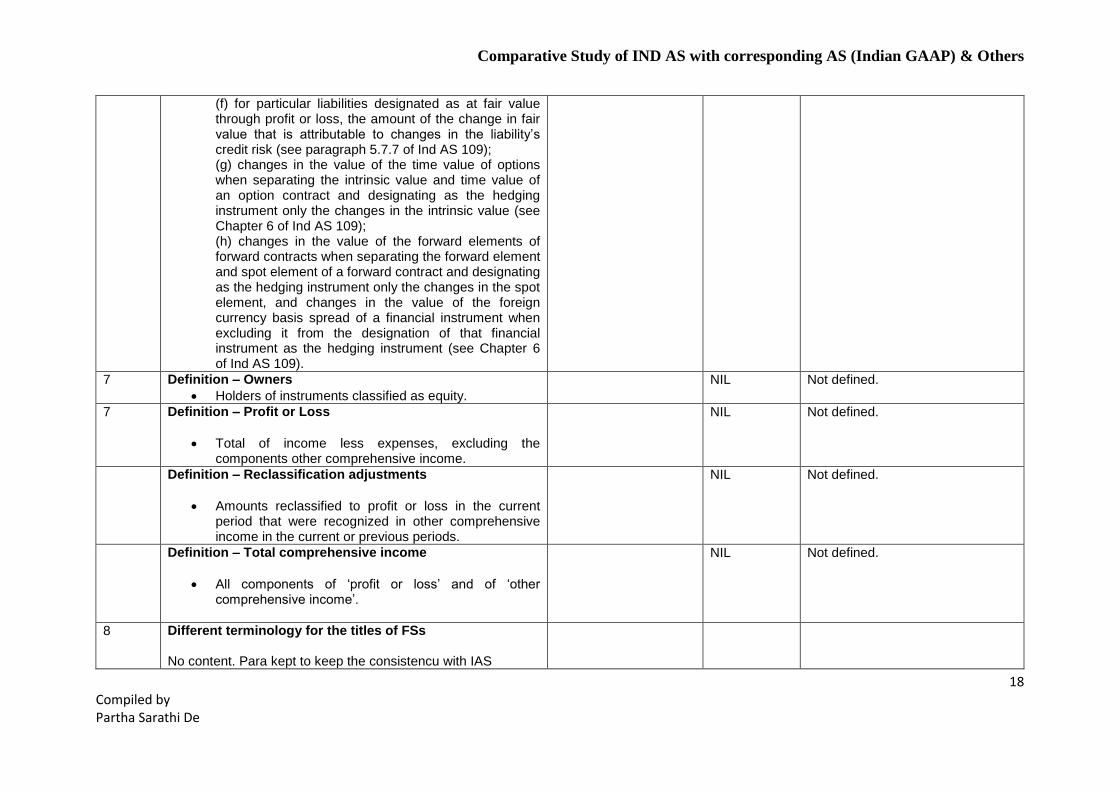

Income and expenses (including reclassification adjustments) that are not recognized in profit or loss as required or permitted by other Ind Ass. The components of other comprehensive income include (a) changes in revaluation surplus (see Ind AS 16, Property, Plant and Equipment and Ind AS 38, Intangible Assets); (b) remeasurements of defined benefit plans (see Ind AS 19, Employee Benefits); (c) gains and losses arising from translating the FSs of a foreign operation (see Ind AS 21. The Effects of Changes in Foreign Exchange Rates); (d) gains and losses from investments in equity instruments designated at fair value through other comprehensive income in accordance with paragraph 5.7.5 of Ind AS 109, Financial instruments; (da) gains and losses on financial assets measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of Ind AS 109. (e) the effective portion of gains and losses on hedging instruments in a cash flow hedge and the gains and losses on hedging instruments that hedge investments in equity instruments measured at fair value through other comprehensive income in accordance with 5.7.5 of Ind AS 109 (see Chapter 6 of Ind AS 109);

NIL Not defined

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

18 Compiled by Partha Sarathi De

(f) for particular liabilities designated as at fair value through profit or loss, the amount of the change in fair value that is attributable to changes in the liability’s credit risk (see paragraph 5.7.7 of Ind AS 109); (g) changes in the value of the time value of options when separating the intrinsic value and time value of an option contract and designating as the hedging instrument only the changes in the intrinsic value (see Chapter 6 of Ind AS 109); (h) changes in the value of the forward elements of forward contracts when separating the forward element and spot element of a forward contract and designating as the hedging instrument only the changes in the spot element, and changes in the value of the foreign currency basis spread of a financial instrument when excluding it from the designation of that financial instrument as the hedging instrument (see Chapter 6 of Ind AS 109).

7 Definition – Owners

Holders of instruments classified as equity.

NIL Not defined.

7 Definition – Profit or Loss

Total of income less expenses, excluding the components other comprehensive income.

NIL Not defined.

Definition – Reclassification adjustments

Amounts reclassified to profit or loss in the current period that were recognized in other comprehensive income in the current or previous periods.

NIL Not defined.

Definition – Total comprehensive income

All components of ‘profit or loss’ and of ‘other comprehensive income’.

NIL Not defined.

8 Different terminology for the titles of FSs No content. Para kept to keep the consistencu with IAS

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

19 Compiled by Partha Sarathi De

8A Financial Instruments

Ind AS 32, (a) Puttable financial instrument classified as an equity instrument (described in paragraphs 16A and 16B of Ind AS 32) (b) an instrument that imposes on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation and is classified as an equity instrument (described in paragraphs 16C and 16D of Ind AS 32).

NIL

No such guidance.

9 FSs – Purpose of FSs

FSs are a structured representation of the financial position and performance of an entity.

This information, along with other information in the notes, assists users of FSs in predicting the entity’s future cash flows and, in particular, their timing and certainty.

NIL AS 1 does not provide any guidance on this topic although principles are same.

10 Complete set of FS

Comprises: (a) a balance sheet as at the end of the period; (b) a statement of profit and loss for the period; (c) Statement of changes in equity for the period; (d) a statement of cash flows for the period; (e) notes, comprising a summary of significant accounting policies and other explanatory information; and (ea) comparative information in respect of the preceding period as specified in paragraphs 38 and 38A; and (f) a balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements in

Sec 2 of the Act & Sch III

Section 2 of Companies Act, 2013 provides similar components of financial statement as provided in Ind AS 1 except that it does not specifically requires a balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements in

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

20 Compiled by Partha Sarathi De

accordance with paragraphs 40A-40D. accordance with paragraphs 40A-40D of Ind AS 1. Schedule III of Companies Act, 2013 requires comparative for immediately preceding period.

10A Statement of profit and loss

An entity shall present a single statement of profit and loss, with profit or loss and other comprehensive income presented in two sections. The sections shall be presented together, with the profit or loss section presented first followed directly by the other comprehensive income section.

NIL Schedule III of the Companies Act, 2013 does not provide concept of other comprehensive income.

11 Prominence of FS

An entity shall present with equal prominence all of the FSs in a complete set of FSs.

NIL Sch III of the Companies Act, 2013 does not state this specifically however the principles are similar to Ind AS 1.

12 No content. Para kept to keep the consistency with IAS

13 Financial review presented outside FSs

Many entities present, outside the FSs, a financial review by Management that describes and explains the main features of the entity’s financial performance and financial position, and the principal uncertainties it faces. Such a report may include a review of:

(a) the main factors and influences determining financial performance, including changes in the environment in which the entity operates the entity’s response to those changes and their effect, and the entity’s policy for investment to maintain

NIL No such Guidance.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

21 Compiled by Partha Sarathi De

and enhance financial performance including its dividend policy; (b) the entity’s sources of fundi8ng and its targeted ratio of liabilities to equity; and (c) the entity’s resources not recognized in the balance sheet in accordance with Ind Ass.

14 Reports and statement presented outside FSs

Many entities also present, outside the FSs, reports and statements such as environmental reports and value added statements, particularly in industries in which environmental factors are significant and when employees are regarded as an important user group. Reports and statements presented outside FSs are outside the scope of Ind Ass.

NIL

No such Guidance

15 General Features – Presentation of True and fair view and compliance with Ind AS

Sec 129 of the Act No Difference

16 Ind AS Compliance statements

Entity whose FSs comply with Ind ASs shall make an explicit and unreserved statement of such compliance in the notes.

An entity shall not describe FSs as complying with Ind Ass unless they comply with all the requirements of Ind Ass.

NIL

No such requirement.

17(a) True and fair view – Selection of accounting policies

In virtually all circumstances, presentation of a true and fair view is achieved by compliance with applicable Ind Ass. Presentation of a true and fair view also requires an entity to select and apply accounting policies in accordance with Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors. Ind AS 8

Para 16 of AS 1

AS 1 provides that the primary consideration in the selection of accounting policies by an enterprise is that the financial statements prepared and presented on the basis of such accounting policies

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

22 Compiled by Partha Sarathi De

sets out a hierarchy of authoritative guidance that management considers in the absence of an Ind AS that specifically applies to an item.

should represent a true and fair view of the state of affairs of the enterprise as at the balance sheet date and of the profit or loss for the period ended on that date.

17B Provide information which is reliable, comparable and understandable

In virtually all circumstances, presentation of a true and fair view is achieved by compliance with applicable Ind Ass. Presentation of a true and fair view also requires an entity to present information, including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information.

NIL

No such guidance

17C Provide additional disclosures

in virtually all circumstances, presentation of a true and fair view is achieved by compliance with applicable Ind Ass. Presentation of a true and fair view also requires an entity to provide additional disclosures when compliance with the specific requirements in Ind Ass is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance.

NIL

No such Guidance.

18 Inappropriate Accounting Policies

An entity cannot rectify inappropriate accounting policies either by disclosure of the accounting policies used or by notes or explanatory material.

Para 23 of AS 1

Disclosure of accounting policies or of changes therein cannot remedy a wrong or inappropriate treatment of the item in the accounts.

19 When compliance with Ind AS shall be misleading

NIL Not arising.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

23 Compiled by Partha Sarathi De

In the extremely rare circumstances in which management concludes that compliance with a requirement in an Ind AS would be so misleading that it would conflict with the objective of FSs set out in the Framework, the entity shall depart from that requirement in the manner set out in paragraph 20 if the relevant regulatory framework requires, or otherwise does not prohibit, such a departure.

20 When an entity departs from Ind AS requirement

When an entity departs from a requirement of an Ind AS in accordance with paragraph 19, it shall disclose: (a) that management has concluded that the FSs present a true and fair view of the entity’s financial position, financial performance and cash flows; (b) that it has complied with applicable Ind Ass, except that it has departed from a particular requirement to present a true and fair view; (c) the title of the Ind AS from which the entity has departed, the nature of the departure, including the treatment that the Ind AS would require, the reason why that treatment would be so misleading in the circumstances that it would conflict with the objective of FSs set out in the Framework, and the treatment adopted; and (d) for each period presented, the financial effect of the departure on each item in the FSs that would have been reported in complying with the requirement.

SA As per SA, non-compliance of accounting standards requires auditors to report the matter in accordance with Auditing standards.

The requirements of SA are principally similar to Ind AS 1.

21 When an entity departed from a requirement of an Ind AS in prior period

When an entity has departed from a requirement of an Ind AS in a prior period, and that departure affects the

NIL

Not arising.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

24 Compiled by Partha Sarathi De

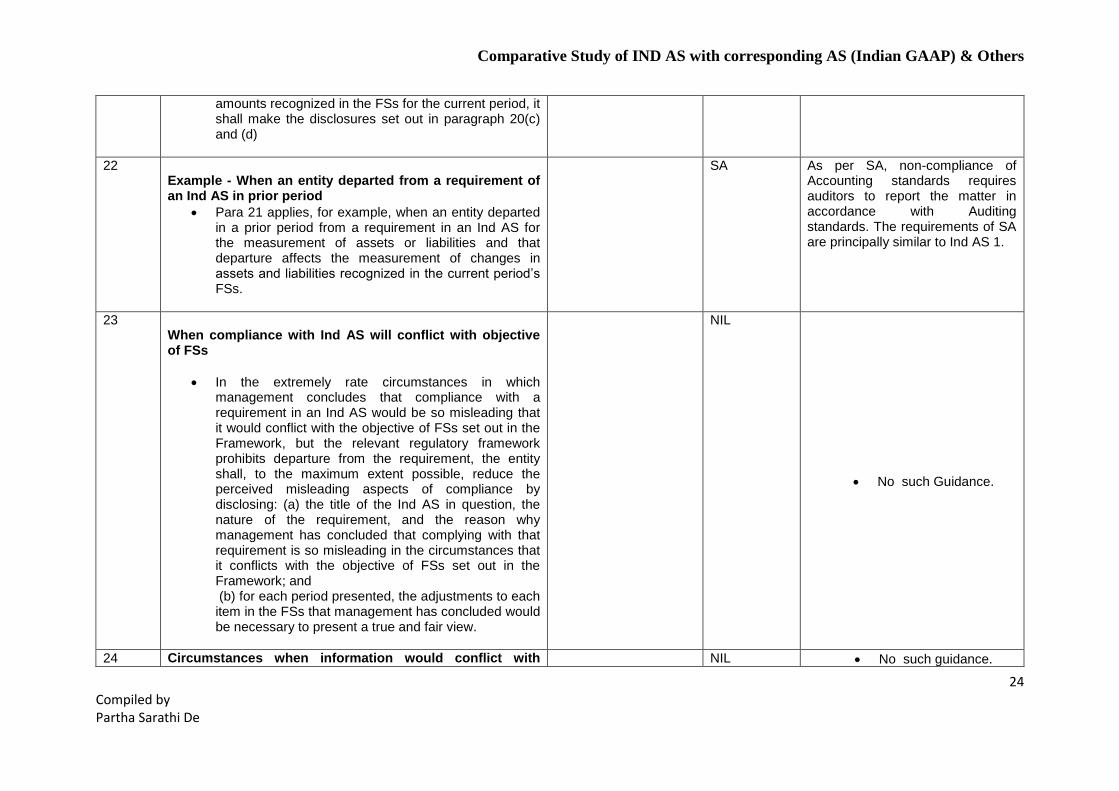

amounts recognized in the FSs for the current period, it shall make the disclosures set out in paragraph 20(c) and (d)

22 Example - When an entity departed from a requirement of an Ind AS in prior period

Para 21 applies, for example, when an entity departed in a prior period from a requirement in an Ind AS for the measurement of assets or liabilities and that departure affects the measurement of changes in assets and liabilities recognized in the current period’s FSs.

SA As per SA, non-compliance of Accounting standards requires auditors to report the matter in accordance with Auditing standards. The requirements of SA are principally similar to Ind AS 1.

23 When compliance with Ind AS will conflict with objective of FSs

In the extremely rate circumstances in which management concludes that compliance with a requirement in an Ind AS would be so misleading that it would conflict with the objective of FSs set out in the Framework, but the relevant regulatory framework prohibits departure from the requirement, the entity shall, to the maximum extent possible, reduce the perceived misleading aspects of compliance by disclosing: (a) the title of the Ind AS in question, the nature of the requirement, and the reason why management has concluded that complying with that requirement is so misleading in the circumstances that it conflicts with the objective of FSs set out in the Framework; and (b) for each period presented, the adjustments to each item in the FSs that management has concluded would be necessary to present a true and fair view.

NIL

No such Guidance.

24 Circumstances when information would conflict with NIL No such guidance.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

25 Compiled by Partha Sarathi De

objective of FSs

For the purpose of para 19-23, an item of information would conflict with the objective of FSs when it does not represent faithfully the transactions, other events and conditions that it either purports to represent or could reasonably by expected to represent and, consequently, it would be likely to influence economic decisions made by users of FSs. When assessing whether complying with a specific requirement in an Ind AS would be so misleading that it would conflict with the objective of FSs set out in the Framework, management considers: (a) why the objective of FSs is not achieved in the particular circumstances; and (b) how the entity’s circumstances differ from those of other entities that comply with the requirement. If other entities in similar circumstances comply with the requirement, there is a rebuttable presumption that the entity’s compliance with the requirement would not be so misleading that it would conflict with the objective of FSs set out in the Framework.

25 Going concern

Ind AS 1 provides that when preparing financial statements, management shall make an assessment of an entity’s ability to continue as a going concern. An entity shall prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so. When management is aware, in making its assessment, of material uncertainties related to events or conditions that may cast significant doubt upon the entity’s ability to

Paras 10(a) and 27 of AS 1

AS 1 provides that the enterprise is normally viewed as a going concern, that is, as continuing in operation for the foreseeable future. It is assumed that the enterprise has neither the intention nor the necessity of liquidation or of curtailing materially the scale of the operations. If the fundamental accounting assumptions,

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

26 Compiled by Partha Sarathi De

continue as a going concern, the entity shall disclose those uncertainties. When an entity does not prepare financial statements on a going concern basis, it shall disclose the fact, together with the basis on which it prepared the financial statements and the reason why the entity is not regarded as a going concern.

viz. Going Concern, Consistency and Accrual are followed in financial statements, specific disclosure is not required. If a fundamental accounting assumption is not followed, the fact should be disclosed.

26 Assessing going concern assumption

In assessing whether the going concern assumption appropriate, management takes into account all available information about the future, which is at least, but is not limited to, twelve months from the end of the reporting period. The degree of consideration depends on the facts in each case. When an entity has a history of profitable operations and ready access to financial resources, the entity may reach a conclusion that the going concern basis of accounting is appropriate without details analysis. In other cases, management may need to consider a wide range of factors relating to current and expected profitability, debt repayment schedules and potential sources of replacement financing before it can satisfy itself that the going concern basis is appropriate.

NIL

No such guidance.

27 Accrual basis of accounting

Ind AS 1 provides that an entity shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting.

Para 9 of AS 1

AS 1 provides that revenues and costs are accrued, that is, recognized as they are earned or incurred (and not as money is received or paid) and recorded in the financial statements of the periods to which they relate.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

27 Compiled by Partha Sarathi De

28 Accrual basis – Recognition of assets, liabilities, equity, income and expenses

When the accrual basis of accounting is used, an entity recognizes items as assets, liabilities, equity, income and expenses (the elements of FSs) when they satisfy the definitions and recognition criteria for those elements in the Framework.

NIL AS 1 does not state this specifically however the principles are similar to Ind AS 1.

29 Materiality and aggregation

An entity shall present separately each material class of similar items. An entity shall present separately items of a dissimilar nature or function unless they are immaterial except when required by law.

Para 17(c) of AS 1

AS 1 provides that financial statements should disclose all “material” items, i.e. items the knowledge of which might influence the decisions of the user of the financial statements.

30 Aggregation

FSs result from processing large numbers of transactions or other events that are aggregated into classes according to their nature or function. The final stage in the process of aggregation and classification is the presentation of condensed and classified data, which form line items in the FSs. If a line item is not individually material, it is aggregated with other items either in those statements or in the notes. An item that is not sufficiently material to warrant separate presentation in those statements may warrant separate presentation in the notes.

Sch III AS 1 does not provide any guidance on this topic. Schedule III of the Companies Act, 2013 provides that in preparing the FSs including the notes to accounts, a balance shall be maintained between providing excessive detail that may not assist users of FSs and not providing important information as a result of too much aggregation.

31 Disclosure of information not material

An entity need not provide a specific disclosure required by an Ind AS if the information is not material except when required by law.

NIL AS 1 and Schedule III of the Companies Act, 2013 do not provide any guidance on this however the principles are similar to

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

28 Compiled by Partha Sarathi De

Ind AS 1.

32 Offsetting asset and liabilities or income and expenses

An entity shall not offset assets and liabilities or income and expenses, unless required or permitted by an Ind AS.

NIL

No such Guidance.

33 Offsetting in statements

An entity reports separately both assets and liabilities, and income and expenses. Offsetting in the statement of profit and loss or balance sheet, except when offsetting reflects the substance of the transaction or other event, detracts from the ability of users both to understand the transactions, other events and conditions that have occurred and to assess the entity’s future cash flows. Measuring assets net of valuation allowances – for example, obsolescence allowances on inventories and doubtful debts allowances on receivables – is not offsetting.

NIL

No such Guidance.

34 Offsetting any Income with related expenses arising on same transaction

Ind AS 115, Revenue from Contracts with Customers requires an entity to measure revenue from contracts with customers at the amount of consideration to whichs the entity expects to be entitled in exchange for transferring promised goods or services. For example, the amount of revenue recognized reflects any trade discounts and volume rebates the entity allows. An entity undertakes, in the course of its ordinary activities, other transactions that do not generate revenue but are incidental to the main revenue generating activities. An entity presents the results of such transactions, when this presentation reflects the substance of the transaction or other event, by netting any income with related expenses arising on the same transaction. For example:

NIL

No such Guidance.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

29 Compiled by Partha Sarathi De

(a) an entity presents gains and losses on the disposal of non-current assets, including investments and operating assets, by deducting from the amount of consideration on disposal the carrying amount of the asset and related selling expenses; and (b) an entity may net expenditure related to a provision that is recognized in accordance with Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets, and reimbursed under a contractual arrangement with a third party (for example, a supplier’s warranty agreement) against the related reimbursement.

35 Offsetting gains and losses from a group of similar transactions

In addition, an entity presents on a net basis gains and losses arising from a group of similar transactions, for example, foreign exchange gains and losses or gains and losses arising on financial instruments held for trading.

However, an entity presents such gains and losses separately if they are material.

NIL

No such Guidance.

36 Frequency of reporting

An entity shall present a complete set of FSs (including comparative information) at least annually. When an entity changes the end of its reporting period and presents FSs for a period longer or shorter than one year, an entity shall disclose, in addition to the period covered by the FSs: (a) the reason for using a longer or shorter period, and (b) the fact that amounts presented in the FSs are not entirely comparable.

Sec 129 of the Act

Section 129 of the Companies Act, 2013 provides that at every annual general meeting of a company, the Board of Directors of the company shall lay before such meeting financial statements for the financial year.

37 Some entities prefers to report 52 week period FSs

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

30 Compiled by Partha Sarathi De

No content. Para kept to keep the consistency with IAS

38 Comparative information

Ind AS 1 provides that except when Ind Ass permit or require otherwise, an entity shall present comparative information in respect of the preceding period for all amounts reported in the current period’s financial statements. An entity shall include comparative information for narrative and descriptive information if it is relevant to understanding the current period’s financial statements.

Sch III Schedule III of the Companies Act, 2013 provides that except in the case of the first Financial Statements laid before the Company (after its incorporation) the corresponding amounts (comparatives) for the immediately preceding reporting period for all items shown in the Financial Statements including notes shall also be given.

38A Present at least two statements

An entity shall present, as a minimum, two balance sheets, two statements of profit and loss, two statements of cash flows and two statements of changes in equity, and related notes.

Sch III Sch III requires preparation of balance sheet, statement of profit & loss, cash flow statement and related notes along with comparatives.

38B Narrative information provided in FS

Ind AS 1 provides that in some cases, narrative information provided in the financial statements for the preceding period(s) continues to be relevant in the current period. For example, an entity discloses in the current period details of a legal dispute, the outcome of which was uncertain at the end of the preceding period and is yet to be resolved. Users may benefit from the disclosure of information that the uncertainty existed at the end of the preceding period and from the disclosure of information about the steps that have

Sch III Sch III, does not state this specifically however the principles are similar to Ind AS 1.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

31 Compiled by Partha Sarathi De

been taken during the period to resolve the uncertainty.

38C Additional comparative information

An entity may present comparative information in addition to the minimum comparative financial statements required by Ind Ass, as long as that information is prepared in accordance with Ind Ass. This comparative information may consist of one or more statements referred to in paragraph 10, but need not comprise a complete set of financial statements. When this is the case, the entity shall present related note information for those additional statements.

NIL AS 1 and Sch III do not state this specifically however the principles are similar to Ind AS 1.

38D Additional Comparative Information - Example

For example, an entity may present a third statement of profit and loss (thereby presenting the current period, the preceding period and one additional comparative period). However, the entity is not required to present a third balance sheet, a third statement of cash flows or a third statement of changes in equity (i.e. an additional FS comparative). The entity is required to present, in the notes to the FSs,. The comparative information related to that additional statement of profit and loss.

NIL AS 1 & Sch III do not State this specifically. However the principles are similar to Ind AS 1.

39 & 40 No content. Paras kept to keep the consistency with IAS

40A Change in accounting policy, retrospective restatement or reclassification

An entity shall present a third balance sheet as at the beginning of the preceding period in addition to the minimum comparative financial statements required in paragraph 38A if: (a) it applies an accounting policy retrospectively, makes a retrospective restatement of items in its financial statements or reclassifies items in its financial

Para 22 of AS 1

AS 1 does not have such requirement. AS 1 provides that any change in an accounting policy which has a material effect should be disclosed. The amount by which any item in the financial statements is affected by such change

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

32 Compiled by Partha Sarathi De

statements; and (b) the retrospective application, retrospective restatement or the reclassification has a material effect on the information in the balance sheet at the beginning of the preceding period.

should also be disclosed to the extent ascertainable. Where such amount is not ascertainable, wholly or in part, the fact should be indicated.

If a change is made in the accounting policies which has no material effect on the financial statements for the current period but which is reasonably expected to have a material effect in later periods, the fact of such change should be appropriately disclosed in the period in which the change is adopted.

40B Additional balance sheet

In the circumstances described in paragraph 40A, an entity shall present three balance sheets as at¨ (a) the end of the current period; (b) the end of the preceding period; and (c) the beginning of the preceding period.

Para 22 of AS 1

AS 1 does not have such requirement. AS 1 provides that any change in an accounting policy which has a material effect should be disclosed. The amount by which any item in the financial statements is affected by such change should also be disclosed to the extent ascertainable. Where such amount is not ascertainable, wholly or in part, the fact should be indicated. If a change is made in the accounting policies which has no

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

33 Compiled by Partha Sarathi De

material effect on the financial statements for the current period but which is reasonably expected to have a material effect in later periods, the fact of such change should be appropriately disclosed in the period in which the change is adopted.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

34 Compiled by Partha Sarathi De

40C Disclosure in additional balance sheet

When an entity is required to present an additional balance sheet in accordance with paragraph 40A, it must disclose the information required by paragraphs 41-44 and Ind AS 8. However, it need not present the related notes to the opening balance sheet as at the beginning of the preceding period.

Para 22 of AS 1

AS 1 does not have such requirement. AS 1 provides that any change in an accounting policy which has a material effect should be disclosed. The amount by which any item in the financial statements is affected by such change should also be disclosed to the extent ascertainable. Where such amount is not ascertainable, wholly or in part, the fact should be indicated. If a change is made in the accounting policies which has no material effect on the financial statements for the current period but which is reasonably expected to have a material effect in later periods, the fact of such change should be appropriately disclosed in the period in which the change is adopted.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

35 Compiled by Partha Sarathi De

40D Date of opening balance sheet

The date opening balance sheet shall be as at the beginning of the preceding period regardless of whether an entity’s FSs present comparative information for earlier periods (as permitted in paragraph 38C).

NIL AS 1 does not have such requirement.

41 Reclassification of comparatives

if an entity changes the presentation or classification of items in its FSs, it shall reclassify comparative amounts unless reclassification is impracticable. When an entity reclassifies comparative amounts, it shall disclose (including as at the beginning of the preceding period): (a) the nature of the reclassification; (b) the amount of each item or class of items that is reclassified; and (c) the reason for the reclassification.

NIL

No such guidance

42 Disclosures when reclassification of comparative is impracticable

when it is impracticable to reclassify comparative amounts, an entity shall disclose: (a) the reason for not reclassifying the amounts, and (b) the nature of the adjustments that would have been made if the amounts had been reclassified.

NIL

No such Guidance

43 Examples when reclassification of comparative is impracticable

For enhancing the inter-period comparability of information assists users in making economic decisions, especially by allowing the assessment of trends in financial information for predictive purposes. In some circumstances, it is impracticable to reclassify comparative information for a particular prior period to achieve comparability with the current period. For example, an entity may not have collected data in the

NIL

No such Guidance

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

36 Compiled by Partha Sarathi De

prior period(s) in a way that allows reclassification, and it may be impracticable to recreate the information.

44 Changes due to change in accounting policy or correction of an error

Ind AS 8 sets out the adjustments to comparative information required when an entity changes an accounting policy or corrects an error.

NIL

No such Guidance

45 Consistency of presentation

An entity shall retain the presentation and classification of items in the FSs from one period to the next unless: (a) it is apparent, following a significant change in the nature of the entity’s operations or a review of its FSs, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in Ind AS 8; or (b) an Ind AS requires a change in presentation.

Para 10(b) of AS 1

AS 1 provides that the consistency is generally accepted as fundamental accounting assumptions. It is assumed that accounting policies are consistent from one period to another.

46 Change in presentation - Example

For example, a significant acquisition or disposal, or a review of the presentation of the FSs, might suggest that the FSs need to be presented differently. An entity changes the presentation of its FSs only if the changed presentation provides information that is reliable and more relevant to users of the FSs and the revised structure is likely to continue, so that comparability is not impaired. When making such changes in presentation, an entity reclassifies its comparative information in accordance with paragraphs 41 and 42.

NIL

No such Guidance

47 Structure and content

Requires particular disclosures in the balance sheet or in the statement of profit and loss, or in the statement of changes in equity and requires disclosure of other line items either in those statements or in the notes. Ind AS 7, Statement of Cash Flows, sets out

Sch III & AS 3

Sch III provides the structure of balance sheet and statement of profit and loss. AS 3 sets out the requirement for presentation of cash flow

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

37 Compiled by Partha Sarathi De

requirements for the presentation of cash flow information.

statement.

48 Disclosure

Sometimes uses the term ‘disclosure’ in a broad sense, encompassing items presented in the FSs. Disclosures are also required by other Ind Ass. Unless specified to the contrary elsewhere in this Standard or in another Ind AS, such disclosures may be made in the FSs.

NIL

Not specifically stated.

49 Identification of FSs

An entity shall clearly identify the FSs and distinguish them from other information in the same published document.

NIL

Not specifically stated.

50 Other information presented in Annual report/regulatory filling

Apply only to FSs, and not necessarily to other information presented in an annual report, a regulatory filing, or another document.

Therefore, it is important that users can distinguish information that is prepared using Ind AS from other information that may be useful to users but is not the subject of those requirements.

NIL

Not specifically stated.

51 Display certain information prominently

An entity shall clearly identify each FS and the notes. In addition, an entity shall display the following information prominently, and repeat it when necessary for the information presented to be understandable: (a) the name of the reporting entity or other means of identification, and any change in that information from the end of the preceding reporting period; (b) whether the FSs are of an individual entity or a group of entities; (c) the date of the end of the reporting period or the

NIL

Not specifically stated.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

38 Compiled by Partha Sarathi De

period covered by the set of FSs or notes; (d) the presentation currency, as defined in Ind AS 21; and (e) the level of rounding used in presenting amounts in the FSs.

52 Appropriate headings

An entity meets the requirements in paragraph 51 by presenting appropriate headings for pages, statements, notes, columns and the like. Judgment is required in determining the best way of presenting such information. For example, when an entity presents the FSs electronically, separate pages are not always used; and entity then presents the above items to ensure that the information included in the FSs can be understood.

NIL

not specifically stated.

53 Rounding off the amount presented

An entity often makes financial statements more understandable by presenting information in thousands, lakhs, millions or crores of units of the presentation currency.

This is acceptable as long as the entity discloses the level of rounding and does not omit material information.

Sch III

Sch III provides that depending upon the turnover of the company, the figures appearing in the Financial Statements may be rounded off as given below:- Turnover (a) less than one hundred crore rupees. Rounding off to the nearest hundreds, thousands, lakhs or millions, or decimals thereof. Turnover (b) one hundred crore rupees or more. Rounding off to the nearest lakhs, millions or crores, or decimals thereof. Once a unit of measurement is used, it

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

39 Compiled by Partha Sarathi De

shall be used uniformly in the Financial Statements.

54 Balance sheet – Information to be presented in the balance sheet

As a minimum, the balance sheet shall include line items that present the following amounts: (a) property, plant and equipment; (b) investment property; (c) intangible assets; (d) financial assets (excluding amounts shown under (e), (h) and (i)); (e) investments accounted for using the equity method; (f) biological assets within the scope of Ind AS 41 Agriculture; (g) inventories; (h) trade and other receivables; (i) cash and cash equivalents; (j) the total of assets classified as held for sale and assets included in disposal groups classified as held for sale in accordance with Ind AS 105, Non-current Assets Held for Sale and Discontinued Operations; (k) trade and other payables; (l) provisions; (m) financial liabilities (excluding amounts shown under (k) and (l); (n) liabilities and assets for current tax, as defined in Ind AS 12, Income Taxes; (o) deferred tax liabilities and deferred tax assets, as defined in Ind AS 12; (p) liabilities included in disposal groups classified as held for sale in accordance with Ind AS 105; (q) non-controlling interests, presented within equity; and ® issued capital and reserves attributable to owners of the parent.

Sch III Sch III requires similar disclosures in balance sheet except that Ind AS 1 requires following additional disclosures:-

Biological assets within the scope of Ind AS 41 ‘Agriculture’, total of the assets classified as held for sale and assets included in disposal groups classified as held for sale in accordance with Ind AS 105 ‘Non-current assets held for sale and discontinued operations’, liabilities included in disposal groups classified as held for sale in accordance with Ind AS 105 and issued, capital and reserves attributable to owners of the parent.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

40 Compiled by Partha Sarathi De

55 Additional line items

Sch III No Change

56 Deferred tax – Current and non-current

Sch III No Change

57 Order of presentation

This Standard does not prescribe the order or format in which an entity presents items. Paragraph 54 simply lists items that are sufficiently different in nature or function to warrant separate presentation in the balance sheet. In addition: (a) line items are included when the size, nature or function of an item or aggregation of similar items is such that separate presentation is relevant to an understanding of the entity’s financial position; and (b) the descriptions used and the ordering of items or aggregation of similar items may be amended according to the nature of the entity and its transactions, to provide information that is relevant to an understanding of the entity’s financial position. For example, a financial institution may amend the above descriptions to provide information that is relevant to the operations of a financial institution.

Sch III Sch III provides that this part of Schedule sets out the minimum requirements for disclosure on the face of the Balance Sheet, and the Statement of Profit and Loss (hereinafter referred to as “Financial Statements” for the purpose of this Schedule) and Notes. Line items, sub-line items and sub-totals shall be presented as an addition on substitution of the face of the Financial Statements when such presentation is relevant to an understanding of the company’s financial position on performance or to cater to industry/sector-specific disclosure requirements or when required for compliance with the amendments to the Companies Act or under the Accounting Standards.

58 Additional items

NIL No such Guidance

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

41 Compiled by Partha Sarathi De

An entity makes the judgment about whether to present additional items separately on the basis of an assessment of: (a) the nature and liquidity of assets; (b) the functi8on of assets within the entity; and (c) the amounts, nature and timing of liabilities.

59 Different measurement basis for different classes of assets

Use of different measurement bases for different classes of assets suggests that their nature or function differs and, therefore, that an entity presents them as separate line items. For example, different classes of property, plant and equipment can be carried at cost or at revalued amounts in accordance with Ind AS 16.

NIL No such guidance

60 Current/non-current distinction

An entity shall present current and non-current assets, and current and non-current liabilities, as separate classifications in its balance sheet in accordance with paragraphs 66-76 except when a presentation based on liquidity provides information that is reliable and more relevant. When that exception applies, an entity shall present all assets and liabilities in order of liquidity.

Sch III Schedule III of the Companies Act, 2013 provides that assets and liabilities should be disclosed as per current and non-current classification.

61 Disclose items to be recovered or settled after more than twelve months

Whichever method of presentation is adopted, an entity shall disclose the amount expected to be recovered or settled after more than twelve months for each asset and liability line item that combines amounts expected to be recovered or settled: (a) no more than twelve months after the reporting period, and (b) more than twelve months after the reporting period.

Sch III Act provides only presentation basis on current and non-current. It does not provides option of providing on liquidity basis

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

42 Compiled by Partha Sarathi De

62 Clearly identifiable operating cycle

When an entity supplies goods or services within a clearly identifiable operating cycle, separate classification of current and non-current assets and liabilities in the balance sheet provides useful information by distinguishing the net assets that are continuously circulating as working capital from those used in the entity’s long-term operations. It also highlights assets that are expected to be realized within the current operating cycle, and liabilities that are due for settlement within the same period.

NIL

Not specifically stated

63 Presenting assets or liabilities in decreasing order of liquidity

For some entities, such as financial institutions, a presentation of assets and liabilities in increasing or decreasing order of liquidity provides information that is reliable and more relevant than a current/non-current presentation because the entity does not supply goods or services within a clearly identifiable operating cycle.

NIL

No such Guidance

64 Current/non-current and order of liquidity

In applying paragraph 60, an entity is permitted to

Sch III Sch III requires only classification based on

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

43 Compiled by Partha Sarathi De

present some of its assets and liabilities using a current/non-current classification and others in order of liquidity when this provides information that is reliable and more relevant. The need for a mixed basis of presentation might arise when an entity has diverse operations.

current and non-current only.

65 Assessing liquidity

Information about expected dates of realization of assets and liabilities is useful in assessing the liquidity and solvency of an entity. Ind AS 107, Financial Instruments: Disclosures, requires disclosure of the maturity dates of financial assets and financial liabilities. Financial assets include trade and other receivables, and financial liabilities include trade and other payables. Information on the expected date of recovery of non-monetary assets such as inventories and expected date of settlement for liabilities such as provisions is also useful, whether assets and liabilities are classified as current or as non-current. For example, an entity discloses the amount of inventories that are expected to be recovered more than twelve months after the reporting period.

NIL

Not specifically stated.

66 Current assets Sch III No change

67 Non-current

this Standard uses the term ‘non-current’ to include tangible, intangible and financial assets of a long-term nature. It does not prohibit the use of alternative descriptions as long as the meaning is clear.

NIL

No such Guidance

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

44 Compiled by Partha Sarathi De

68 Operating cycle

The operating cycle of an entity is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. When the entity’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months. Current assets include assets (such as inventories and trade receivables) that are sold, consumed or realized as part of the normal operating cycle even when they are not expected to be realized within twelve months after the reporting period. Current assets also include assets held primarily for the purpose of trading (examples include some financial assets that meet the definition of held for trading in Ind AS 109) and the current portion of non-current financial assets.

Sch III Sch III merely provides that an operating cycle is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Where the normal operating cycle cannot be identified, it is assumed to have a duration of twelve months.

69 Current liabilities

Sch III No change

70 Current liabilities despite items are due to be settled more than twelve months after reporting date

Some current liabilities, such as trade payables and some accruals for employee and other operating costs, are part of the working capital used in the entity’s normal operating cycle. An entity classifies such operating items as current liabilities even if they are due to be settled more than twelve months after the reporting period. The same normal operating cycle applies to the classification of an entity’s assets and liabilities. When the entity’s normal operating cycle is not clearly identifiable, it is assumed to be twelve months.

NIL

Not specifically stated.

71 Other current liabilities

Other current liabilities are not settled as part of the normal operating cycle, but are due for settlement within twelve months after the reporting period or held primarily for the purpose of trading. Examples are

NIL

Not specifically stated.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

45 Compiled by Partha Sarathi De

some financial liabilities that meet the definition of held for trading in Ind AS 109, bank overdrafts, and the current portion of non-current financial liabilities, dividends payable, income taxes and other non-trade payables. Financial liabilities that provide financing on a long-term basis (i.e. are not part of the working capital used in the entity’s normal operating cycle) and are not due for settlement within twelve months after the reporting period are non-current liabilities, subject to paragraphs 74 and 75.

72 Financial liabilities as current

An entity classifies its financial liabilities as current when they are due to be settled within twelve months after the reporting period, even if: (a) the original term was for a period longer than twelve months, and (b) an agreement to refinance, or to reschedule payments, on a long-term basis is completed after the reporting period and before the FSs are approved for issue.

NIL

No such Guidance

73 When entity has discretion to refinance or rollover

If an entity expects, and has the discretion, to refinance or roll over an obligation for at least twelve months after the reporting period under an existing long facility, it classifies the obligation as non-current, even if it would otherwise be due within a shorter period. However, when refinancing or rolling over the obligation is not at the discretion of the entity (for example, there is no arrangement for refinancing), the entity does not consider the potential to refinance the obligation and classifies the obligation as current.

NIL

No such Guidance

74 Breach of loan arrangement

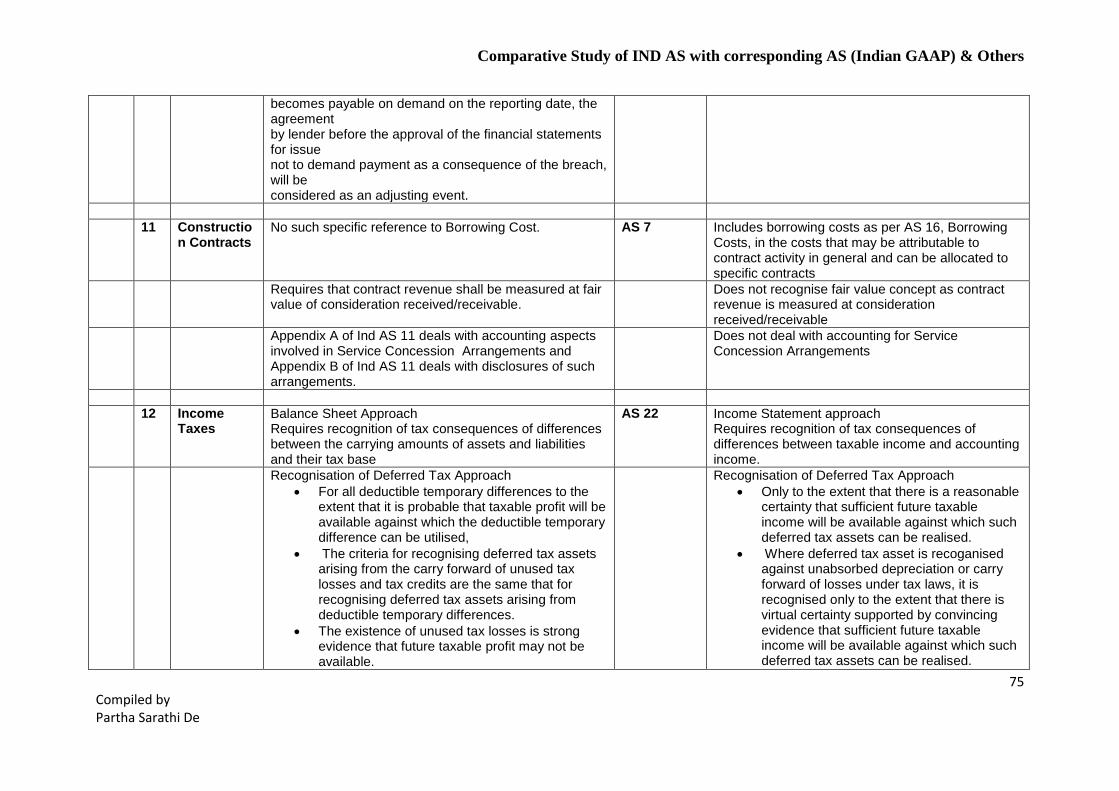

Where there is a breach of a material provision of a

NIL

No such Guidance

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

46 Compiled by Partha Sarathi De

long-term loan arrangement on or before the end of the reporting period with the effect that the liability becomes payable on demand on the reporting date, the entity does not classify the liability as current, if the lender agreed, after the reporting period and before the approval of the FSs for issue, not to demand payment as a consequence of the breach.

75 Period of grace from lender

However, an entity classifies the liability as non-current if the lender agreed by the end of the reporting period to provide a period of grace ending at least twelve months after the reporting period, within which the entity can rectify the breach and during which the lender cannot demand immediate repayment.

NIL

No such Guidance

76 Non-adjusting events No content. Paras kept to keep the consistency with IAS

77 Information to be presented either in the balance sheet or in the notes

An entity shall disclose, either in the balance sheet or in the notes, further sub-classifications of the line items presented, classified in a manner appropriate to the entity’s operations.

Sch III Sch III requires the sub-classification of the line items (presented in balance sheet) to be presented in notes.

78 Sub-classification

The detail provided in sub-classifications depends on the requirements of Ind Ass and on the size, nature and function of the amounts involved. An entity also uses the factors set out in paragraph 58 to decide the basis of sub-classification. The disclosures vary for each item, for example: (a) items of property, plant and equipment are disaggregated into classes in accordance with Ind AS 16; (b) receivables are disaggregated into amounts receivable from trade customers, receivables from related parties, prepayments and other amounts;

Sch III Sch III provides details to be sub-classified.

Comparative Study of IND AS with corresponding AS (Indian GAAP) & Others

47 Compiled by Partha Sarathi De