Embed Size (px)

Citation preview

CONSUMER CREDIT RISK ASSESMENT, PREDICTION & MANAGEMENT SYSTEM

http://www.datamine.gr

Contents

System Overview

System Objectives

Credit checking: a typical case

Automated Credit checking: Overview

Technology - System Architecture

Customer Model

Scoring Model

Credit Scoring: Properties - Key Input

Business Logic: Policies & Rules

Customer Viewer – Sample screen

Reporting capabilities

http://www.datamine.gr

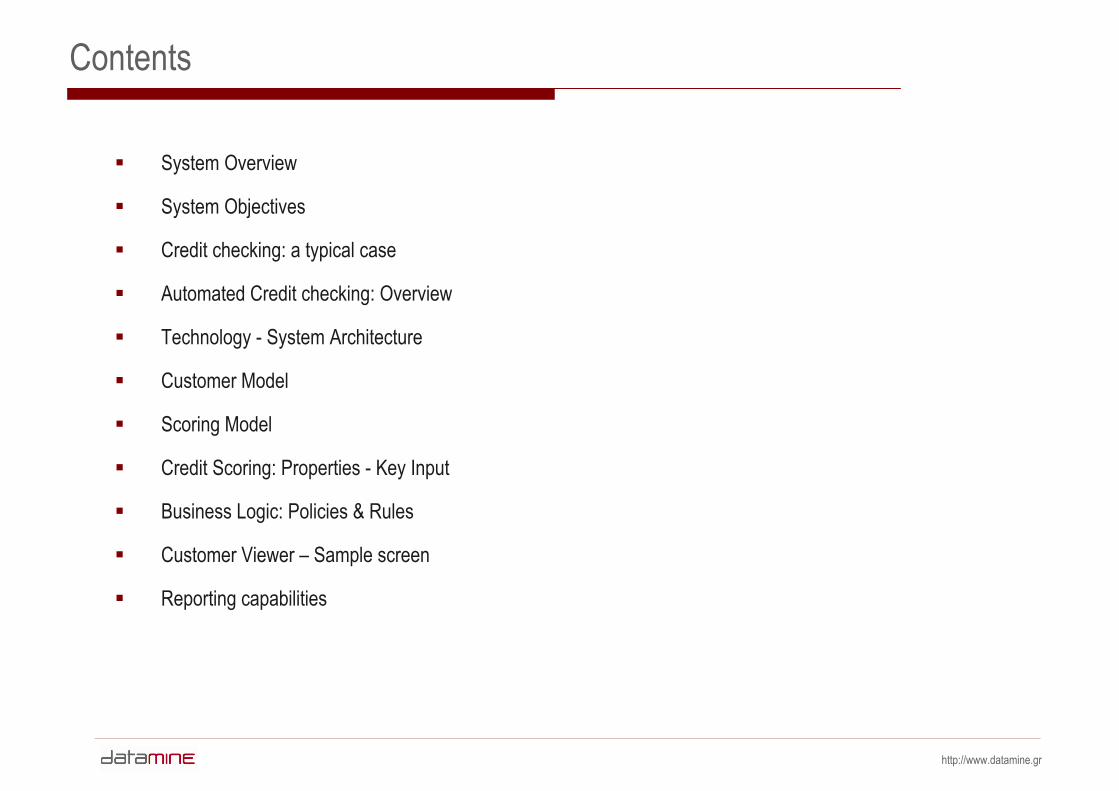

A specialized Information System that combines cutting edge technologies, statistical models and business knowledge in order to optimize and automate the manual credit checking within contract activation process. Key characteristics of the system are:

System Overview

Single point of reference: a centralized system with up-to-date Information regarding customer evaluation, usage & payment

Overall customer picture: physical customer metadata, statistical scores, descriptive statistics, billing & payment history, product & services information organized in a single enterprise-wide application (‘Customer Viewer’ – web interface).

Business Logic Interface: a subsystem that allows policy and rule management. Supports unlimited policies with unlimited rules over a large set of parameters that ensure maximum flexibility in designing or implementing business logic.

Performance Measurement infrastructure: advanced reporting and analysis capabilities allow policy & rule performance evaluation and optimization.

Business Intelligence infrastructure: a general, extensible data mart that can be enriched with scores, traffic patterns thus enhanced into a ‘Marketing Database’

decision

decision

POS - USER

CUSTOMER

BILLING ACTIVATION

PAYMENT FRAUD

Raw data

request

Credit Checking Process

CREDIT CHECKING LOGIC

USER DEFINED RULES

INTERFACES

SYNC PROCESSES

STATISTICAL MODELS

CREDIT CHECKING SYSTEM

request

http://www.datamine.gr

System Objectives

Automate & optimize credit checking – contract activation processMinimize & control bad deptUnderstand bad payment behavior - Identify systematic behaviors-patterns, Fraudulent casesMeasure Risk – provide quantitative figures at customer levelProvide business flexibility: support unlimited, user-defined rulesIntegrate related processes (external credit check, deposit schemes etc)Exchange credit risk information with other companies, without exposing sensitive customer data (within the same group of companies)Design a robust, extensible database with enhanced data quality, ready to be extended a customeranalytics database or Marketing DatabaseProvide advanced reporting capabilities for monitoring & performance evaluationIncorporate predictive modeling

http://www.datamine.gr

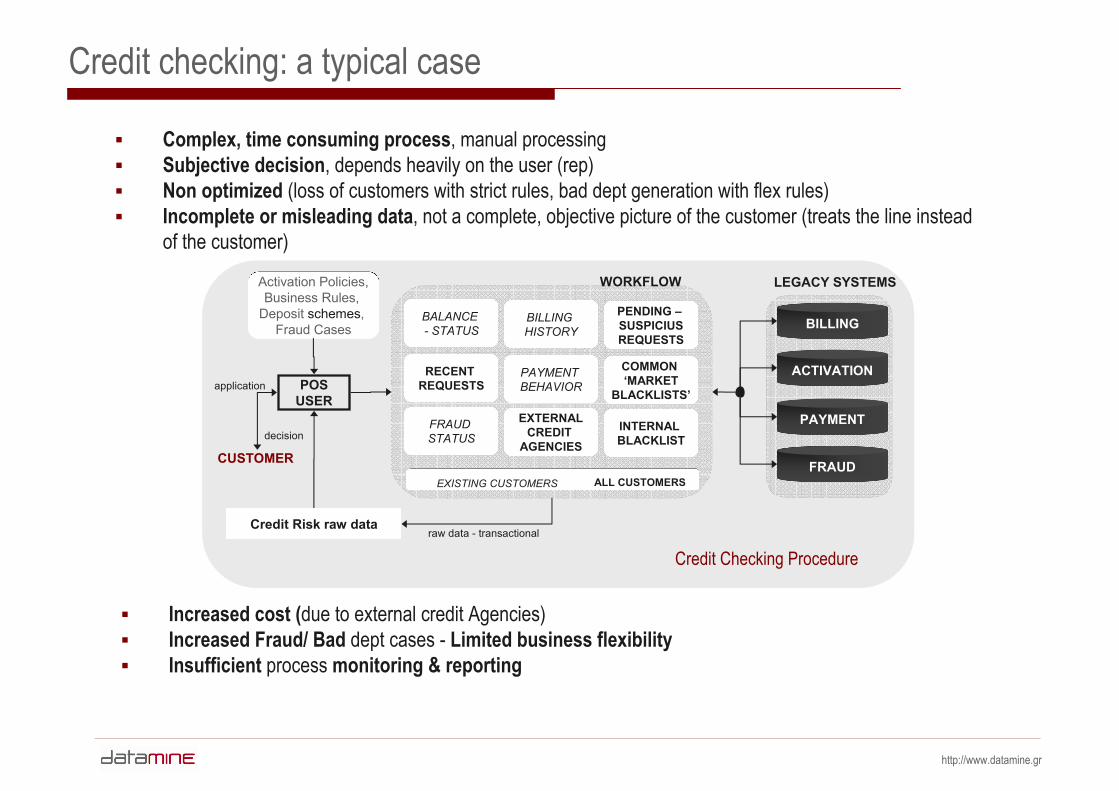

Credit checking: a typical case

Complex, time consuming process, manual processingSubjective decision, depends heavily on the user (rep)Non optimized (loss of customers with strict rules, bad dept generation with flex rules) Incomplete or misleading data, not a complete, objective picture of the customer (treats the line instead of the customer)

Activation Policies,Business Rules,

Deposit schemes, Fraud Cases

POS USER

CUSTOMER

WORKFLOW

BALANCE - STATUS

RECENT REQUESTS

FRAUD STATUS

BILLING HISTORY

PAYMENT BEHAVIOR

EXTERNALCREDIT

AGENCIES

COMMON ‘MARKET

BLACKLISTS’

INTERNAL BLACKLIST

PENDING –SUSPICIUSREQUESTS

EXISTING CUSTOMERS ALL CUSTOMERS

application

raw data - transactionalCredit Risk raw data

decision

BILLING

ACTIVATION

PAYMENT

FRAUD

LEGACY SYSTEMS

Credit Checking Procedure

Increased cost (due to external credit Agencies)Increased Fraud/ Bad dept cases - Limited business flexibilityInsufficient process monitoring & reporting

http://www.datamine.gr

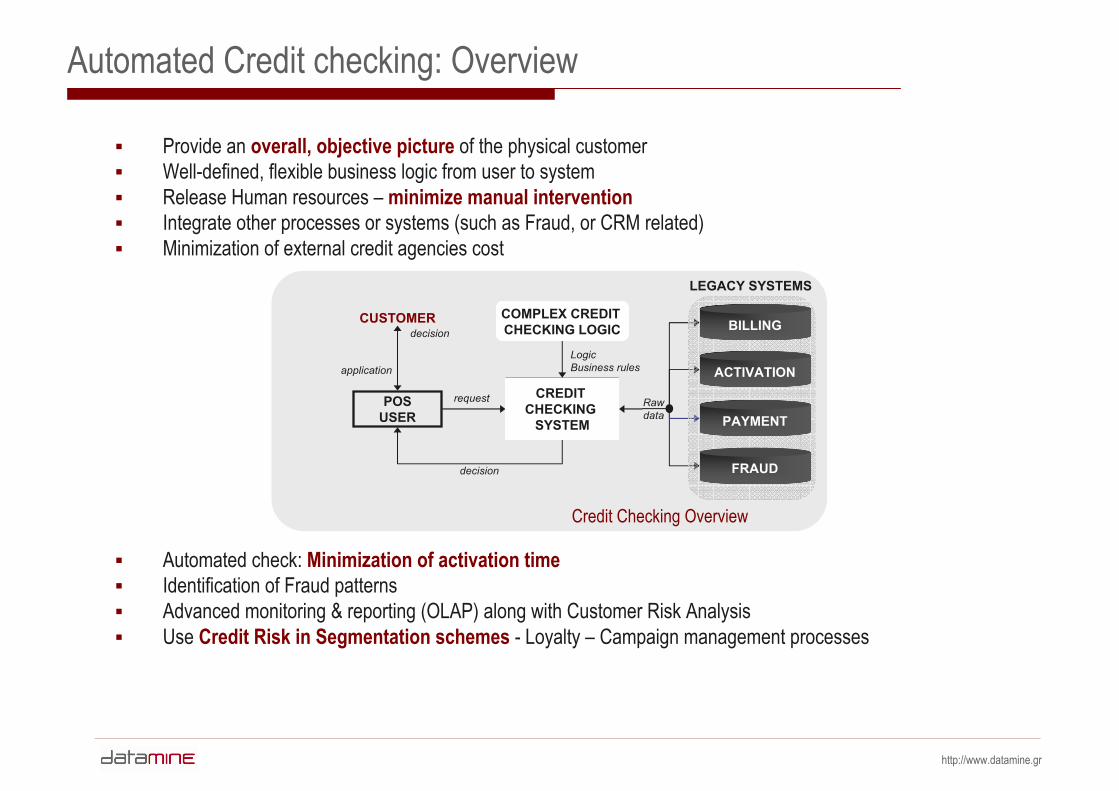

Automated Credit checking: Overview

application

decision

POS USER

CUSTOMER

CREDIT CHECKING

SYSTEM

COMPLEX CREDIT CHECKING LOGIC BILLING

ACTIVATION

PAYMENT

FRAUD

LEGACY SYSTEMS

decision

Raw data

LogicBusiness rules

request

Credit Checking Overview

Provide an overall, objective picture of the physical customerWell-defined, flexible business logic from user to systemRelease Human resources – minimize manual interventionIntegrate other processes or systems (such as Fraud, or CRM related)Minimization of external credit agencies cost

Automated check: Minimization of activation timeIdentification of Fraud patternsAdvanced monitoring & reporting (OLAP) along with Customer Risk AnalysisUse Credit Risk in Segmentation schemes - Loyalty – Campaign management processes

http://www.datamine.gr

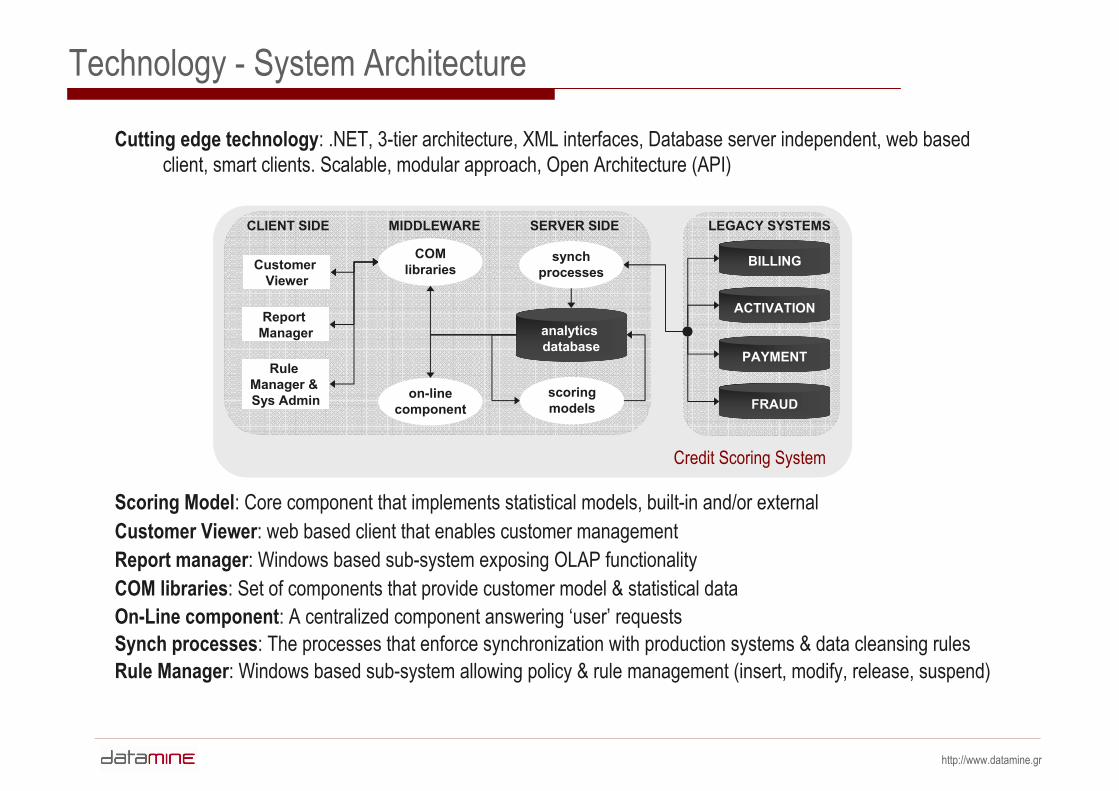

Technology - System Architecture

BILLING

ACTIVATION

PAYMENT

FRAUD

Customer Viewer

LEGACY SYSTEMS

Credit Scoring System

synchprocesses

analytics database

scoring models

on-line component

COM libraries

Report Manager

Rule Manager & Sys Admin

SERVER SIDEMIDDLEWARECLIENT SIDE

Cutting edge technology: .NET, 3-tier architecture, XML interfaces, Database server independent, web based client, smart clients. Scalable, modular approach, Open Architecture (API)

Scoring Model: Core component that implements statistical models, built-in and/or externalCustomer Viewer: web based client that enables customer managementReport manager: Windows based sub-system exposing OLAP functionalityCOM libraries: Set of components that provide customer model & statistical dataOn-Line component: A centralized component answering ‘user’ requestsSynch processes: The processes that enforce synchronization with production systems & data cleansing rules Rule Manager: Windows based sub-system allowing policy & rule management (insert, modify, release, suspend)

http://www.datamine.gr

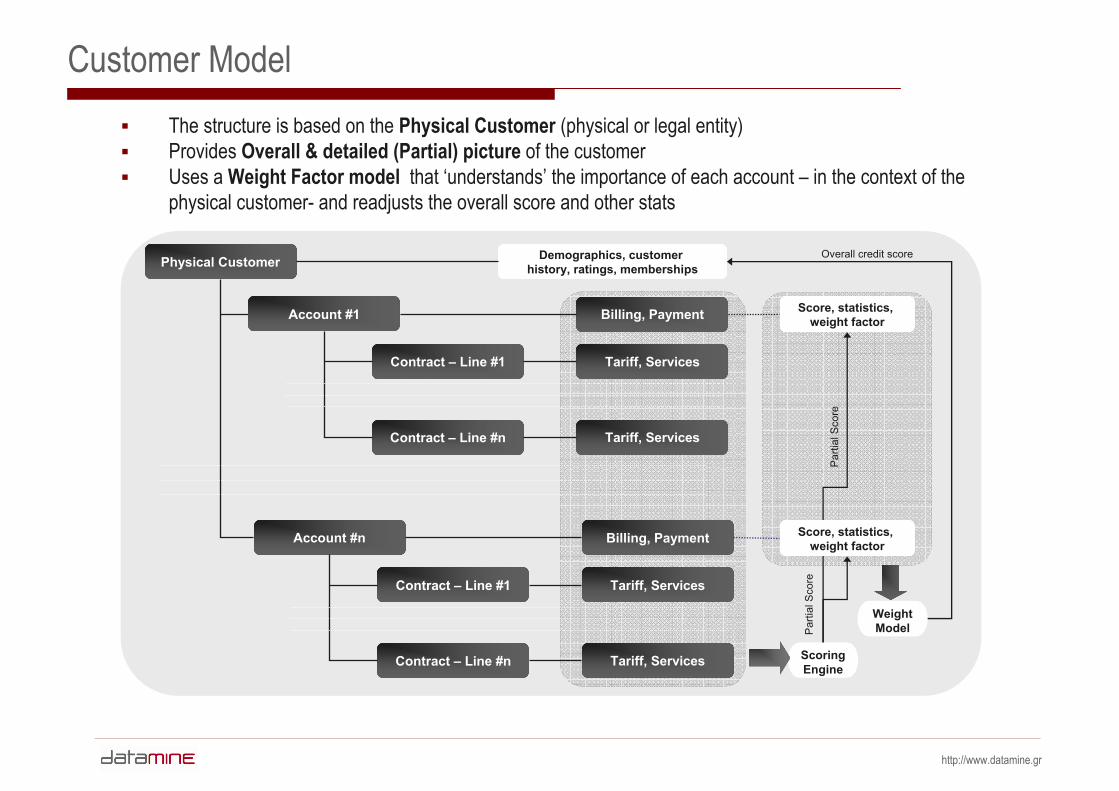

Customer ModelThe structure is based on the Physical Customer (physical or legal entity)Provides Overall & detailed (Partial) picture of the customerUses a Weight Factor model that ‘understands’ the importance of each account – in the context of the physical customer- and readjusts the overall score and other stats

Physical Customer

Account #1

Contract – Line #1

Contract – Line #n

Billing, Payment

Tariff, Services

Tariff, Services

Demographics, customer history, ratings, memberships

Account #n

Contract – Line #1

Contract – Line #n

Billing, Payment

Tariff, Services

Tariff, Services Scoring Engine

Score, statistics, weight factor

Score, statistics, weight factor

Weight Model

Overall credit score

Par

tial S

core

Par

tial S

core

http://www.datamine.gr

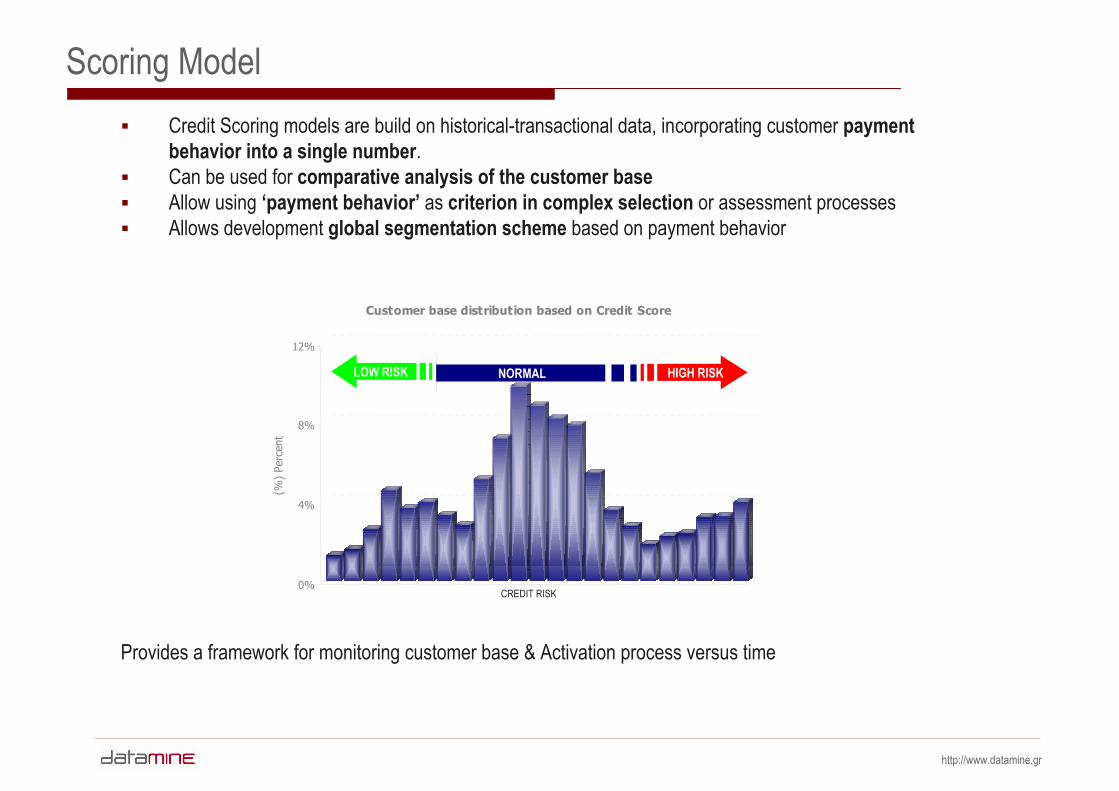

Scoring ModelCredit Scoring models are build on historical-transactional data, incorporating customer payment behavior into a single number. Can be used for comparative analysis of the customer baseAllow using ‘payment behavior’ as criterion in complex selection or assessment processesAllows development global segmentation scheme based on payment behavior

Provides a framework for monitoring customer base & Activation process versus time

0%

4%

8%

12%

(%)

Perc

ent

Customer base distribution based on Credit Score

HIGH RISKLOW RISK

CREDIT RISK

NORMAL

http://www.datamine.gr

Credit Scoring: Properties

Expressed as percent (%) - easy to interpretIt is ‘event based’ which means that it can be extended to ‘near real time’It is weighted,assigns different importance to different accounts of the same customer, or different events of the same account.It is dynamic, the system tends to ‘forget’ previous ‘bad’ history data given a recent ‘good’ behaviorIt is configurable, receives several parameters (weights for reasons, ‘memory factor’ or event reasons)

Billing: monthly bill invoicesPayment detailed payment data (optional)Events on customer behavior (ticklers) communication with customer care along with reason and resultsAccount Event History: Suspension, Reactivation, Cancellation Service activation & usage History: which services, for how long and with what usage. Account life Statistics: tenure, special properties (tariff model, services)Customer level Statistics: geo-demographics, socioeconomic, total billing & payment figures, typologies

Credit Scoring: Key Input

http://www.datamine.gr

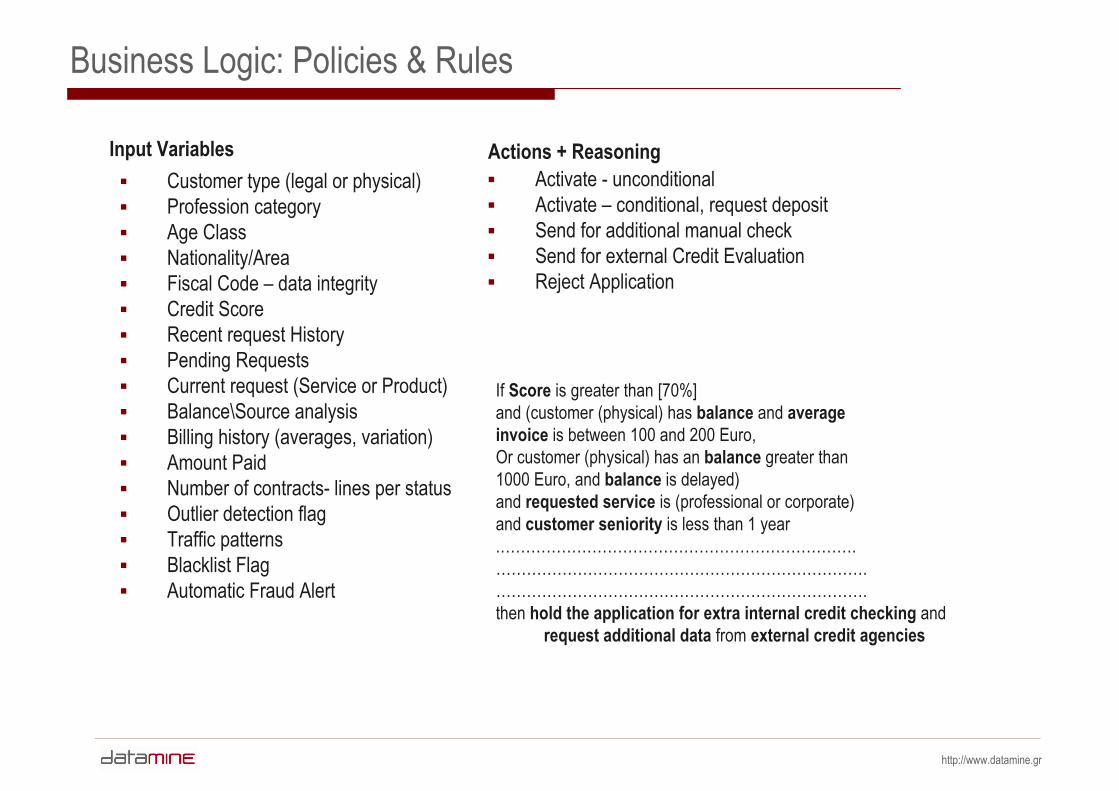

Business Logic: Policies & Rules

A ‘policy’ is defined as a set of complex business rules that enable different treatment of (potential) customers based on several characteristics. Policies can be

User Defined, based on business logic over a set of predefined parameters – UDPStatistically Derived based on a statistical\data mining models - SDP

UDP are easy to be implemented through the graphical user interface of the system (Policy Manager). Apply mostly to existing customers (having at least a basic history within the company).

UDR, are arbitrarily developed based mostly on user experience, perception and business understanding

SDP can be used for new customers with no further (internal) information. SDP are usually Decision trees \ rule sets.

UDR & SDR can work in parallel with a complementary logic.

Policies & rules can be defined as conditional based of time period or flow management requests. For example during a peak-period (e.g. Christmas) with massive promotions the system automatically activates a different set of rules.

http://www.datamine.gr

Business Logic: Policies & Rules

Customer type (legal or physical)Profession categoryAge ClassNationality/AreaFiscal Code – data integrityCredit ScoreRecent request HistoryPending RequestsCurrent request (Service or Product)Balance\Source analysisBilling history (averages, variation)Amount Paid Number of contracts- lines per statusOutlier detection flagTraffic patternsBlacklist FlagAutomatic Fraud Alert

Input VariablesActivate - unconditionalActivate – conditional, request depositSend for additional manual checkSend for external Credit EvaluationReject Application

Actions + Reasoning

If Score is greater than [70%] and (customer (physical) has balance and average invoice is between 100 and 200 Euro, Or customer (physical) has an balance greater than 1000 Euro, and balance is delayed)and requested service is (professional or corporate) and customer seniority is less than 1 year.…………………………………………………………….……………………………………………………………….……………………………………………………………….then hold the application for extra internal credit checking and

request additional data from external credit agencies

http://www.datamine.gr

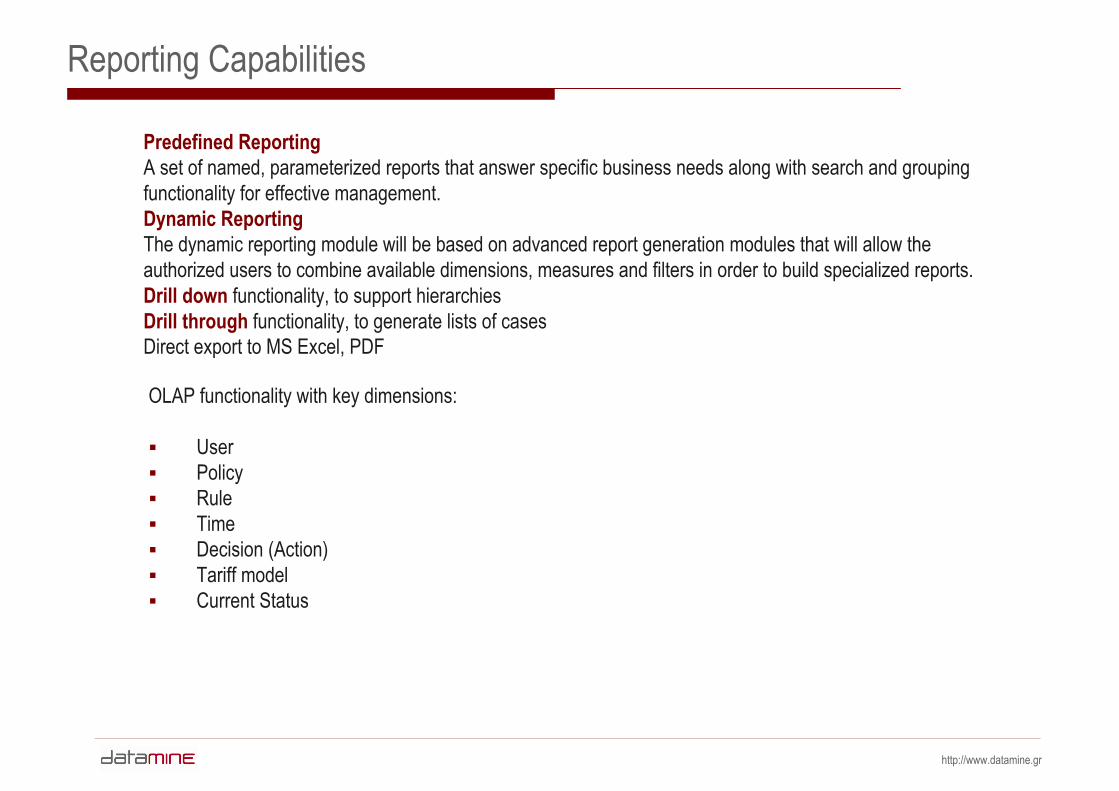

Reporting Capabilities

OLAP functionality with key dimensions:

UserPolicyRuleTimeDecision (Action)Tariff modelCurrent Status

Predefined ReportingA set of named, parameterized reports that answer specific business needs along with search and grouping functionality for effective management.Dynamic ReportingThe dynamic reporting module will be based on advanced report generation modules that will allow the authorized users to combine available dimensions, measures and filters in order to build specialized reports. Drill down functionality, to support hierarchiesDrill through functionality, to generate lists of casesDirect export to MS Excel, PDF

http://www.datamine.gr

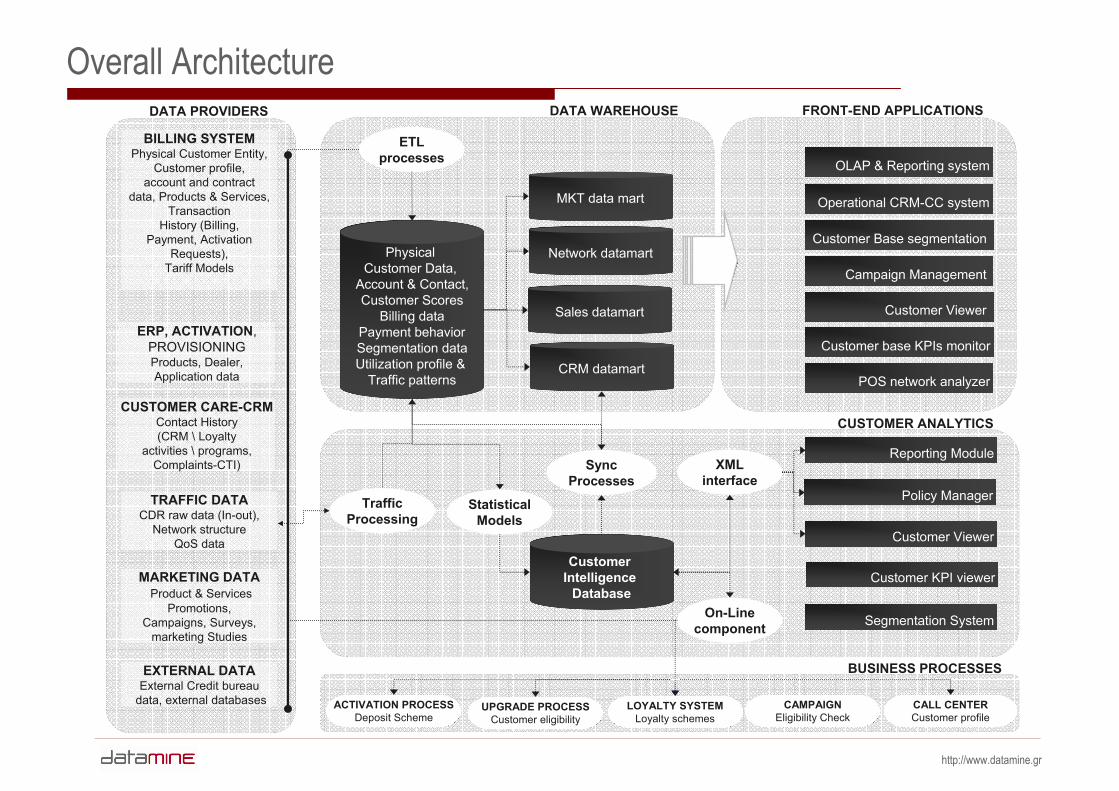

Overall ArchitectureDATA PROVIDERS

BILLING SYSTEMPhysical Customer Entity,

Customer profile, account and contract

data, Products & Services, Transaction

History (Billing, Payment, Activation

Requests), Tariff Models

CUSTOMER CARE-CRMContact History(CRM \ Loyalty

activities \ programs, Complaints-CTI)

MARKETING DATAProduct & Services

Promotions, Campaigns, Surveys,

marketing Studies

EXTERNAL DATAExternal Credit bureau

data, external databases

TRAFFIC DATACDR raw data (In-out),

Network structureQoS data

ERP, ACTIVATION,PROVISIONING Products, Dealer, Application data

OLAP & Reporting system

FRONT-END APPLICATIONS

Operational CRM-CC system

Customer Base segmentation

Campaign Management

Customer Viewer

Customer base KPIs monitor

POS network analyzer

Physical Customer Data,

Account & Contact,Customer Scores

Billing dataPayment behaviorSegmentation dataUtilization profile &

Traffic patterns

ETL processes

DATA WAREHOUSE

CRM datamart

Sales datamart

Network datamart

MKT data mart

Statistical Models

Customer Intelligence

Database

Traffic Processing

XML interface

Policy Manager

Reporting Module

Customer Viewer

Sync Processes

Customer KPI viewer

Segmentation System

CUSTOMER ANALYTICS

ACTIVATION PROCESSDeposit Scheme

UPGRADE PROCESSCustomer eligibility

LOYALTY SYSTEMLoyalty schemes

CAMPAIGNEligibility Check

CALL CENTERCustomer profile

BUSINESS PROCESSES

On-Line component

http://www.datamine.gr

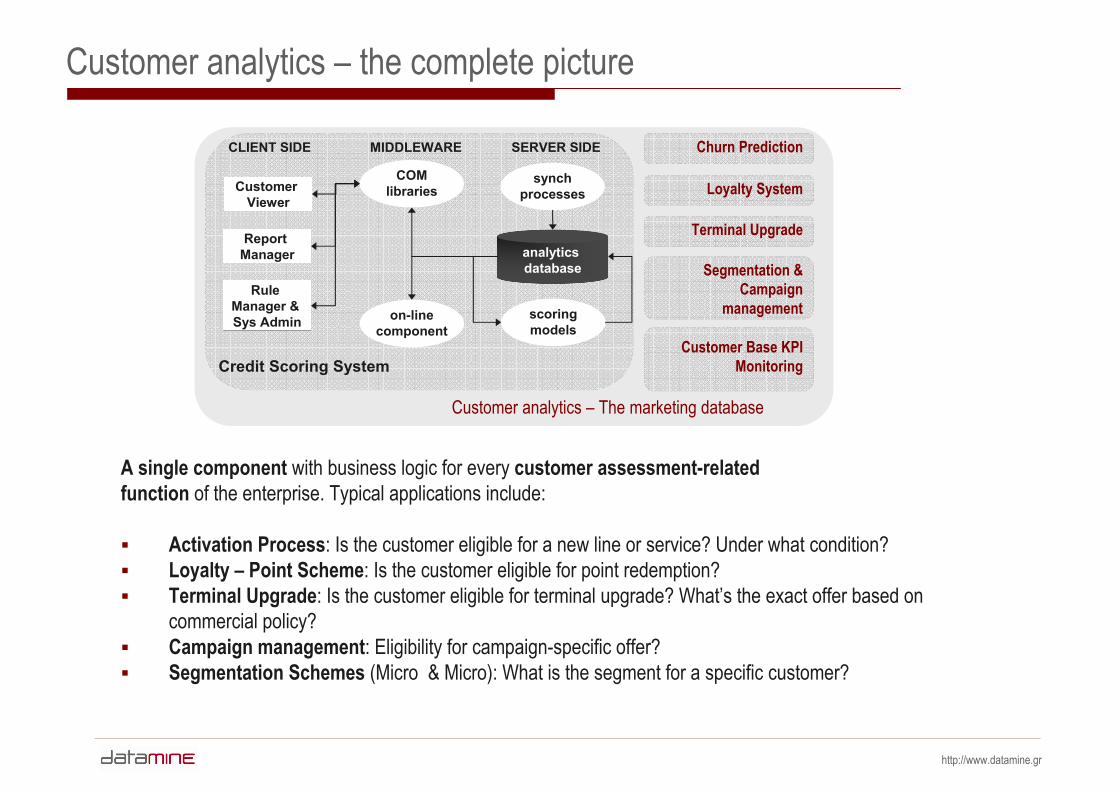

Customer analytics – the complete picture

A single component with business logic for every customer assessment-related function of the enterprise. Typical applications include:

Activation Process: Is the customer eligible for a new line or service? Under what condition?Loyalty – Point Scheme: Is the customer eligible for point redemption?Terminal Upgrade: Is the customer eligible for terminal upgrade? What’s the exact offer based on commercial policy?Campaign management: Eligibility for campaign-specific offer?Segmentation Schemes (Micro & Micro): What is the segment for a specific customer?

Customer Viewer

Credit Scoring System

synchprocesses

analytics database

scoring models

on-line component

COM libraries

Report Manager

Rule Manager & Sys Admin

SERVER SIDEMIDDLEWARECLIENT SIDE Churn Prediction

Loyalty System

Terminal Upgrade

Segmentation & Campaign

management

Customer Base KPI Monitoring

Customer analytics – The marketing database

http://www.datamine.gr

22 Ethnikis Antistasis Avenue,15232 Chalandri, Athens, Greece

[email protected]@datamine.gr

http://www.datamine.gr

December 2003