Embed Size (px)

DESCRIPTION

A comprehensive overview of the ever-changing world of compliance governing affiliate marketing, including a live review of a landing page and sales page. Experience level: Beginner, Intermediate, Advanced Target audience: Affiliate/Publisher Niche/vertical: FTC Amber Paul, Vice President, Business Development, Globalwide Media (Twitter @ambspaul) (Moderator) Sarah Cabello, Attorney, S. Cabello, PLLC Sarah de Diego, Attorney, De Diego Law Aaron Kelly, Attorney, Kelly / Warner, PLLC (Twitter @aaronklaw) CJ Montgomery, Attorney at Law, Online Legal Group

Citation preview

Compliance Mastery: Tips For Legal Landing Pages

January 14, 2013 2:00 – 3:00 pm

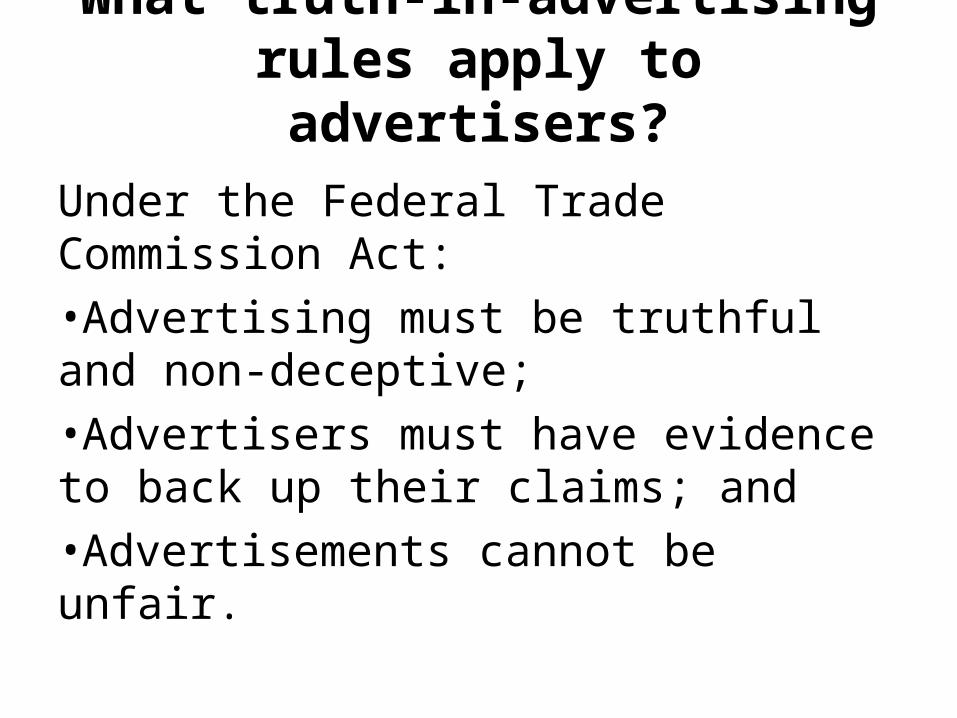

What truth-in-advertising rules apply to advertisers?

Under the Federal Trade Commission Act:•Advertising must be truthful and non-deceptive;•Advertisers must have evidence to back up their claims; and•Advertisements cannot be unfair.

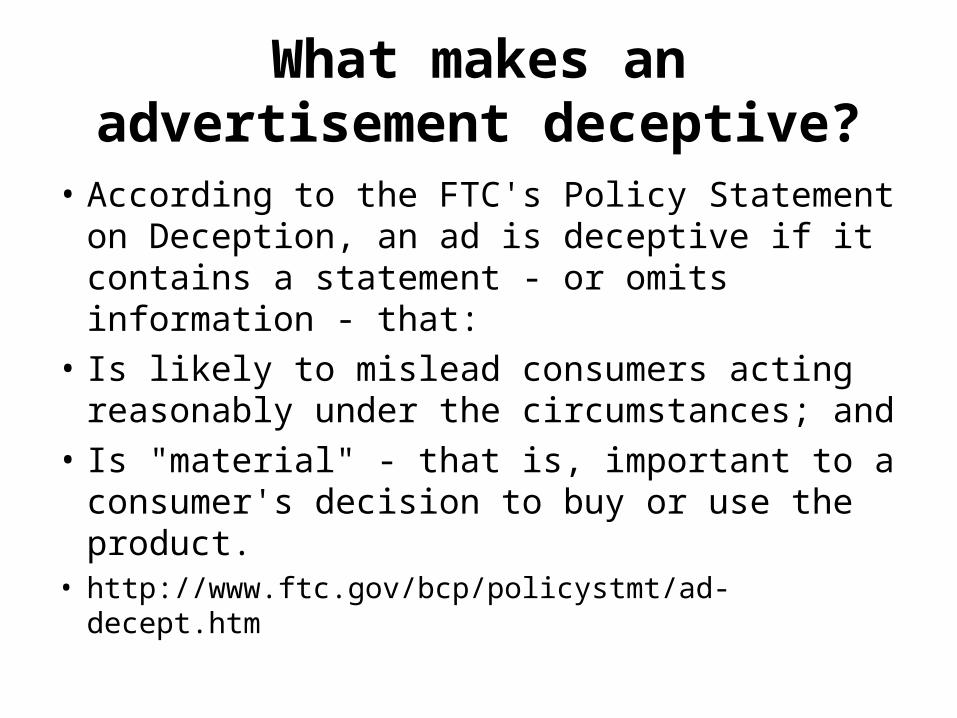

What makes an advertisement deceptive?

• According to the FTC's Policy Statement on Deception, an ad is deceptive if it contains a statement - or omits information - that:

• Is likely to mislead consumers acting reasonably under the circumstances; and

• Is "material" - that is, important to a consumer's decision to buy or use the product.

• http://www.ftc.gov/bcp/policystmt/ad-decept.htm

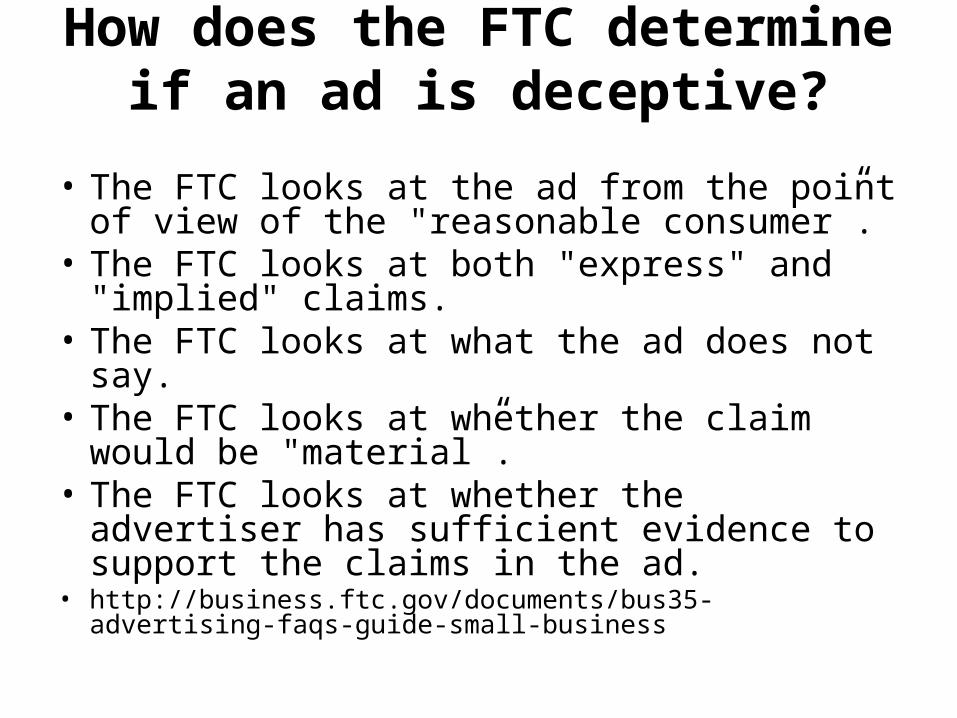

How does the FTC determine if an ad is deceptive?

• The FTC looks at the ad from the point of view of the "reasonable consumer”.

• The FTC looks at both "express" and "implied" claims.

• The FTC looks at what the ad does not say.• The FTC looks at whether the claim would be

"material”.• The FTC looks at whether the advertiser has

sufficient evidence to support the claims in the ad.

• http://business.ftc.gov/documents/bus35-advertising-faqs-guide-small-business

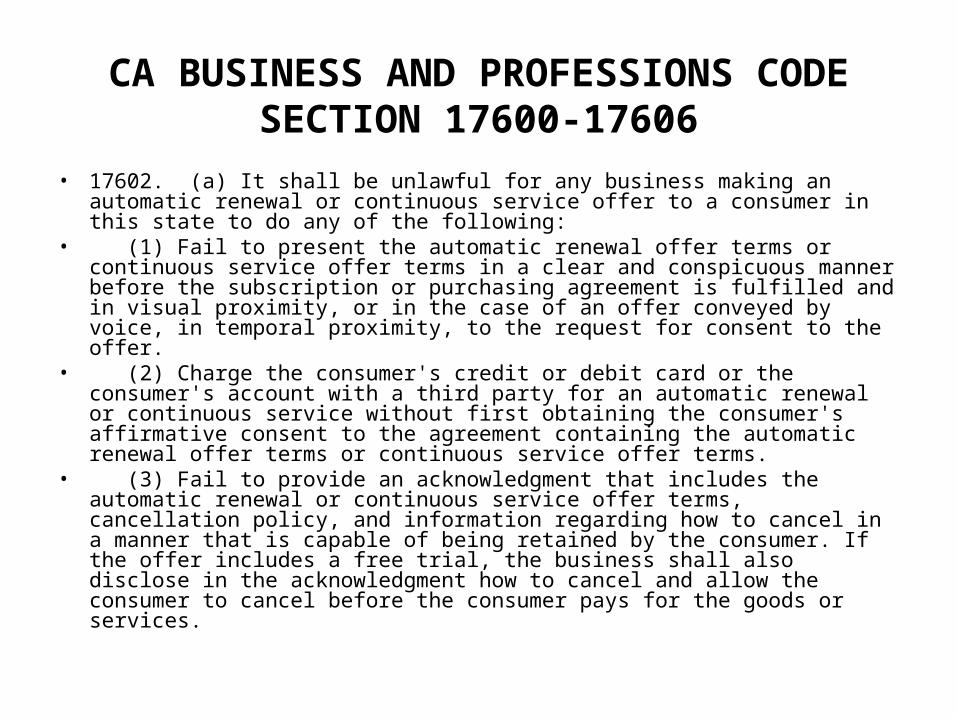

CA BUSINESS AND PROFESSIONS CODESECTION 17600-17606

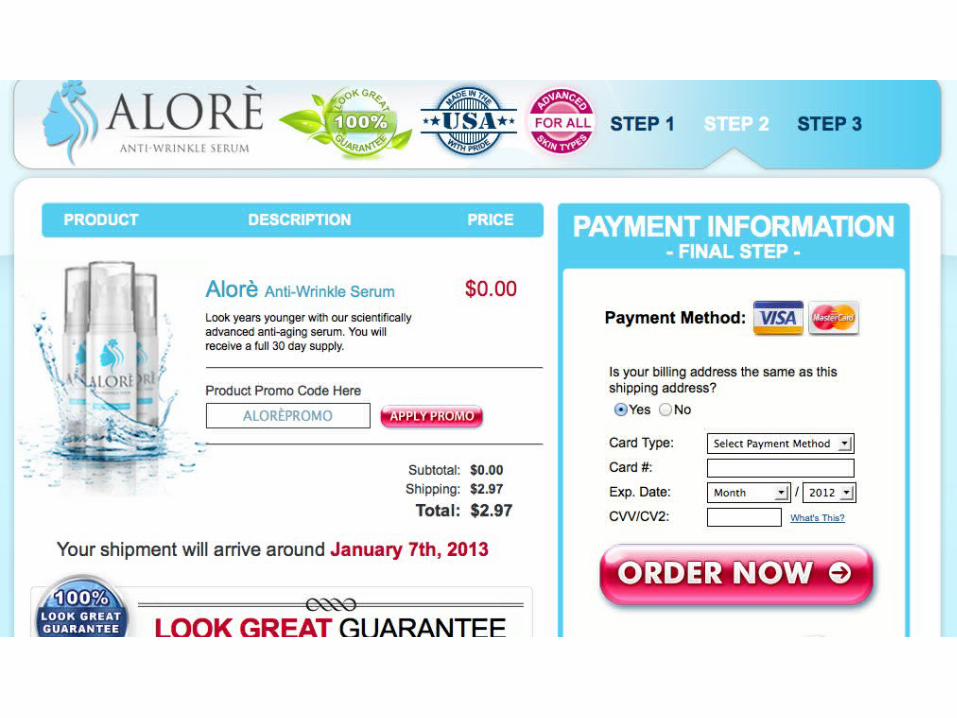

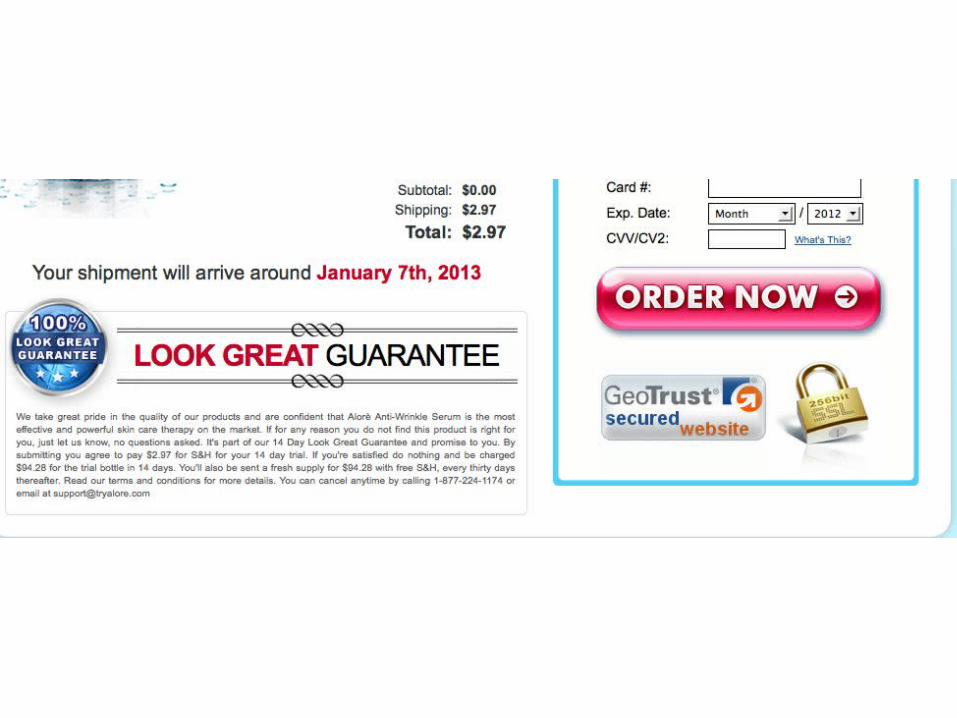

• 17602. (a) It shall be unlawful for any business making an automatic renewal or continuous service offer to a consumer in this state to do any of the following:

• (1) Fail to present the automatic renewal offer terms or continuous service offer terms in a clear and conspicuous manner before the subscription or purchasing agreement is fulfilled and in visual proximity, or in the case of an offer conveyed by voice, in temporal proximity, to the request for consent to the offer.

• (2) Charge the consumer's credit or debit card or the consumer's account with a third party for an automatic renewal or continuous service without first obtaining the consumer's affirmative consent to the agreement containing the automatic renewal offer terms or continuous service offer terms.

• (3) Fail to provide an acknowledgment that includes the automatic renewal or continuous service offer terms, cancellation policy, and information regarding how to cancel in a manner that is capable of being retained by the consumer. If the offer includes a free trial, the business shall also disclose in the acknowledgment how to cancel and allow the consumer to cancel before the consumer pays for the goods or services.

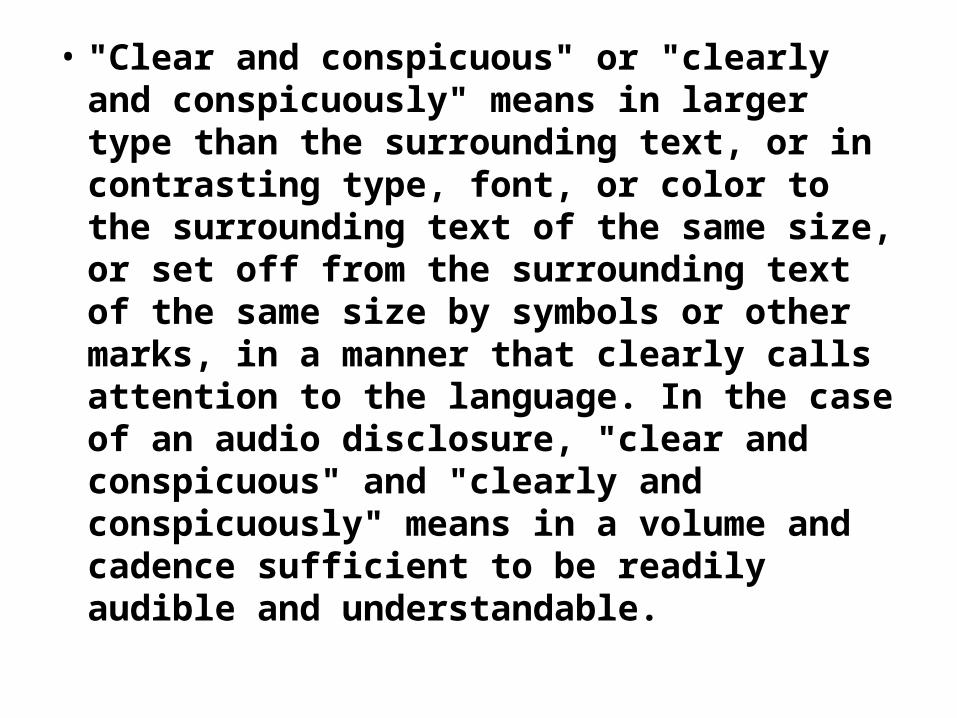

• "Clear and conspicuous" or "clearly and conspicuously" means in larger type than the surrounding text, or in contrasting type, font, or color to the surrounding text of the same size, or set off from the surrounding text of the same size by symbols or other marks, in a manner that clearly calls attention to the language. In the case of an audio disclosure, "clear and conspicuous" and "clearly and conspicuously" means in a volume and cadence sufficient to be readily audible and understandable.

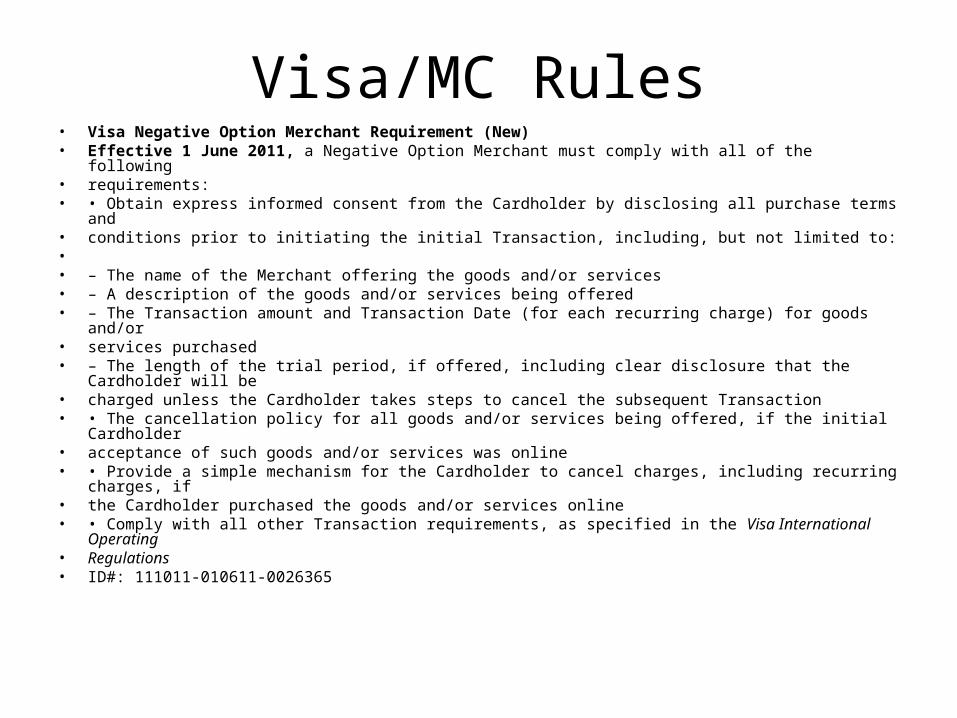

Visa/MC Rules• Visa Negative Option Merchant Requirement (New)• Effective 1 June 2011, a Negative Option Merchant must comply with all of the following• requirements:• • Obtain express informed consent from the Cardholder by disclosing all purchase terms and• conditions prior to initiating the initial Transaction, including, but not limited to:• • – The name of the Merchant offering the goods and/or services• – A description of the goods and/or services being offered• – The Transaction amount and Transaction Date (for each recurring charge) for goods and/or• services purchased• – The length of the trial period, if offered, including clear disclosure that the Cardholder will be• charged unless the Cardholder takes steps to cancel the subsequent Transaction• • The cancellation policy for all goods and/or services being offered, if the initial Cardholder• acceptance of such goods and/or services was online• • Provide a simple mechanism for the Cardholder to cancel charges, including recurring charges, if• the Cardholder purchased the goods and/or services online• • Comply with all other Transaction requirements, as specified in the Visa International Operating• Regulations• ID#: 111011-010611-0026365

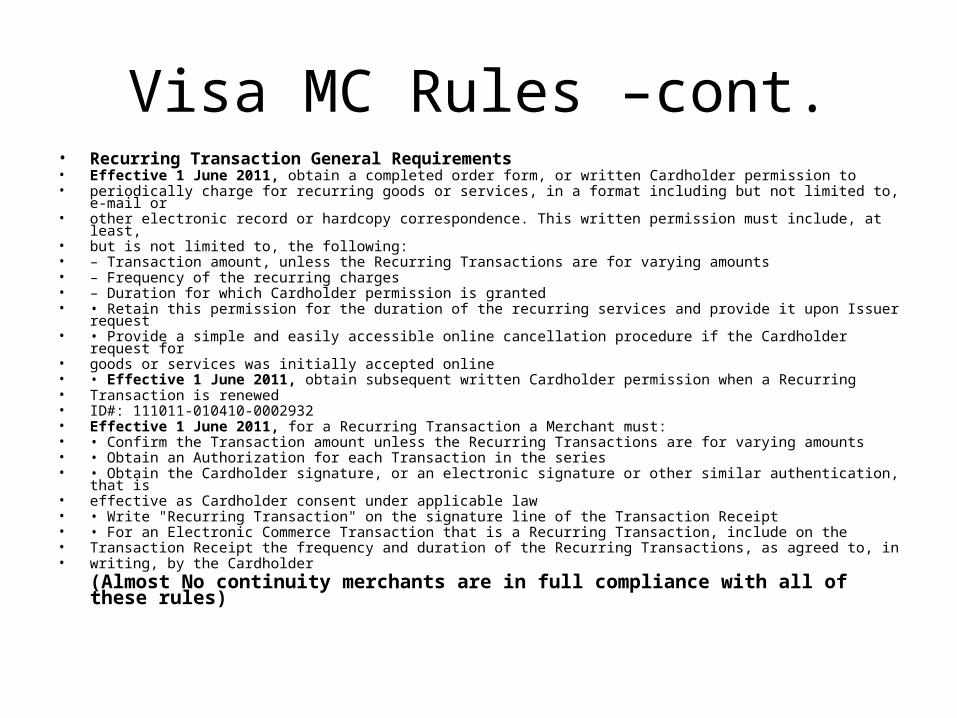

Visa MC Rules –cont.• Recurring Transaction General Requirements• Effective 1 June 2011, obtain a completed order form, or written Cardholder permission to• periodically charge for recurring goods or services, in a format including but not limited to, e-mail or• other electronic record or hardcopy correspondence. This written permission must include, at least,• but is not limited to, the following:• – Transaction amount, unless the Recurring Transactions are for varying amounts• – Frequency of the recurring charges• – Duration for which Cardholder permission is granted• • Retain this permission for the duration of the recurring services and provide it upon Issuer request• • Provide a simple and easily accessible online cancellation procedure if the Cardholder request for• goods or services was initially accepted online• • Effective 1 June 2011, obtain subsequent written Cardholder permission when a Recurring• Transaction is renewed• ID#: 111011-010410-0002932• Effective 1 June 2011, for a Recurring Transaction a Merchant must:• • Confirm the Transaction amount unless the Recurring Transactions are for varying amounts• • Obtain an Authorization for each Transaction in the series• • Obtain the Cardholder signature, or an electronic signature or other similar authentication, that is• effective as Cardholder consent under applicable law• • Write "Recurring Transaction" on the signature line of the Transaction Receipt• • For an Electronic Commerce Transaction that is a Recurring Transaction, include on the• Transaction Receipt the frequency and duration of the Recurring Transactions, as agreed to, in• writing, by the Cardholder

(Almost No continuity merchants are in full compliance with all of these rules)

Questions?Moderator:

Amber Paul, Global Wide [email protected]

Speakers: Aaron Kelly, Kelly Warner Law

CJ Montgomery, Wheeler, Montgomery, Sleight & [email protected]

Sarah de Diego, De Diego [email protected]