Embed Size (px)

Citation preview

By Ben Youn

Copyright 2014 Quantum Business House

WELCOME to QUANTUM BUSINESS HOUSE

2 hours for each session

10 minutes tea time

Bathroom & Kitchen

Today’s Speaker

Please network each other

Future Plan

- Business Forum

- Networking Events

- Business Mentoring

Copyright 2014 Quantum Business House

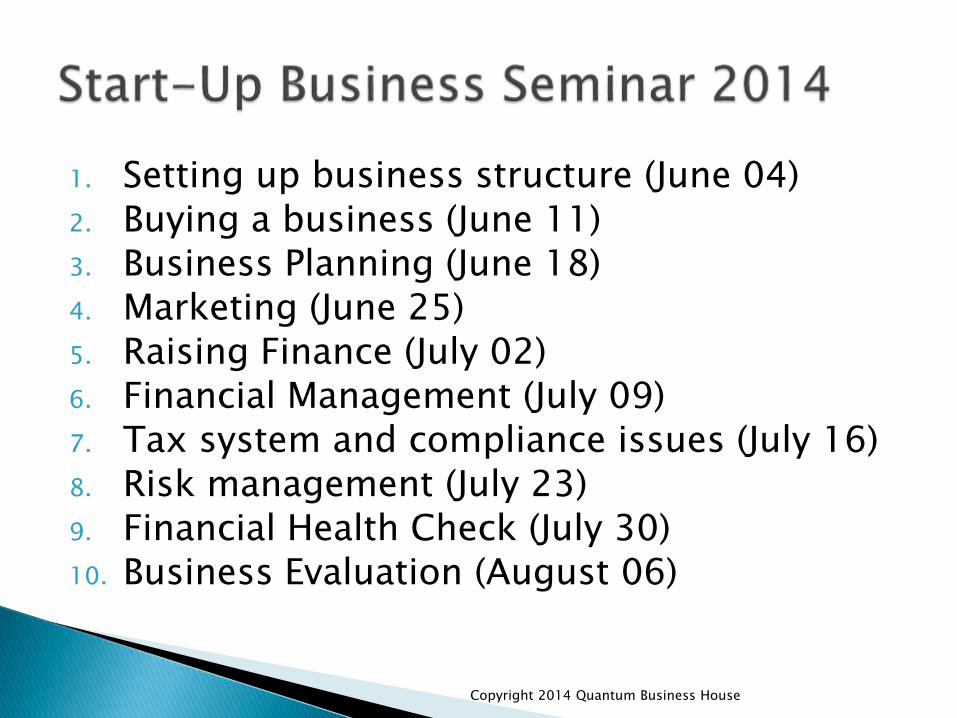

1. Setting up business structure (June 04) 2. Buying a business (June 11)3. Business Planning (June 18)4. Marketing (June 25)5. Raising Finance (July 02)6. Financial Management (July 09)7. Tax system and compliance issues (July 16)8. Risk management (July 23)9. Financial Health Check (July 30)10. Business Evaluation (August 06)

Copyright 2014 Quantum Business House

Copyright 2014 Quantum Business House

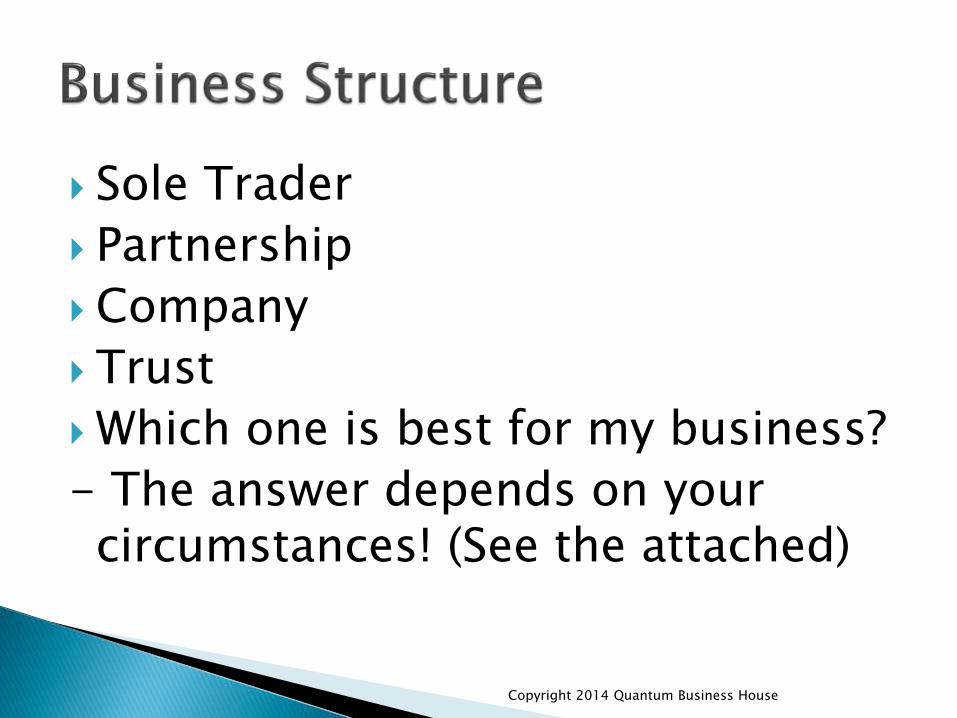

Sole Trader

Partnership

Company

Trust

Which one is best for my business?

- The answer depends on your circumstances! (See the attached)

Copyright 2014 Quantum Business House

Sole Trader

- Easy to setup (ABN & TFN)

- Combined income tax with the individual TFN

- Asset protection? – think again!

- Business Liabilities including employee’s wrongdoing – Owner’s Personal Liability

- Difficult to raise finance

- Difficult to sell the business when time comes.

- Higher tax rate (marginal tax rate)

Copyright 2014 Quantum Business House

Partnership

- Partnership agreement (essential)

- Splitting income between partners

- Partnership business loss can be offset against other income of the partner

- Each partner liable to pay tax

- Each partner holds liability for the partnership business (separately and as a group)

- Not a big deal for tax concession perspective

- Break Up – New partnership and capital gains tax

Copyright 2014 Quantum Business House

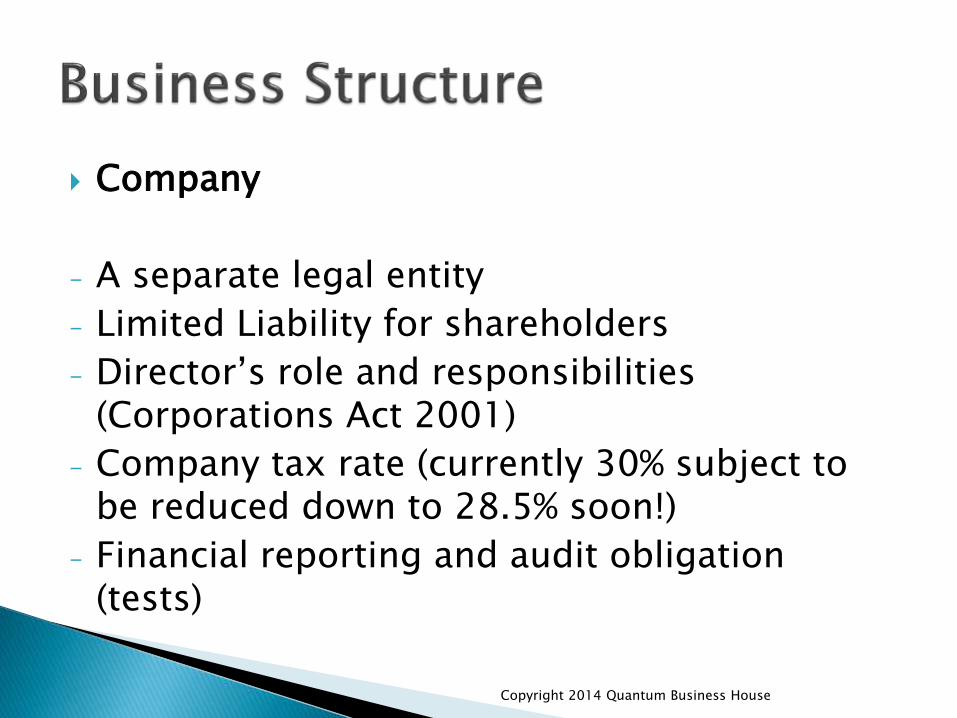

Company

- A separate legal entity

- Limited Liability for shareholders

- Director’s role and responsibilities (Corporations Act 2001)

- Company tax rate (currently 30% subject to be reduced down to 28.5% soon!)

- Financial reporting and audit obligation (tests)

Copyright 2014 Quantum Business House

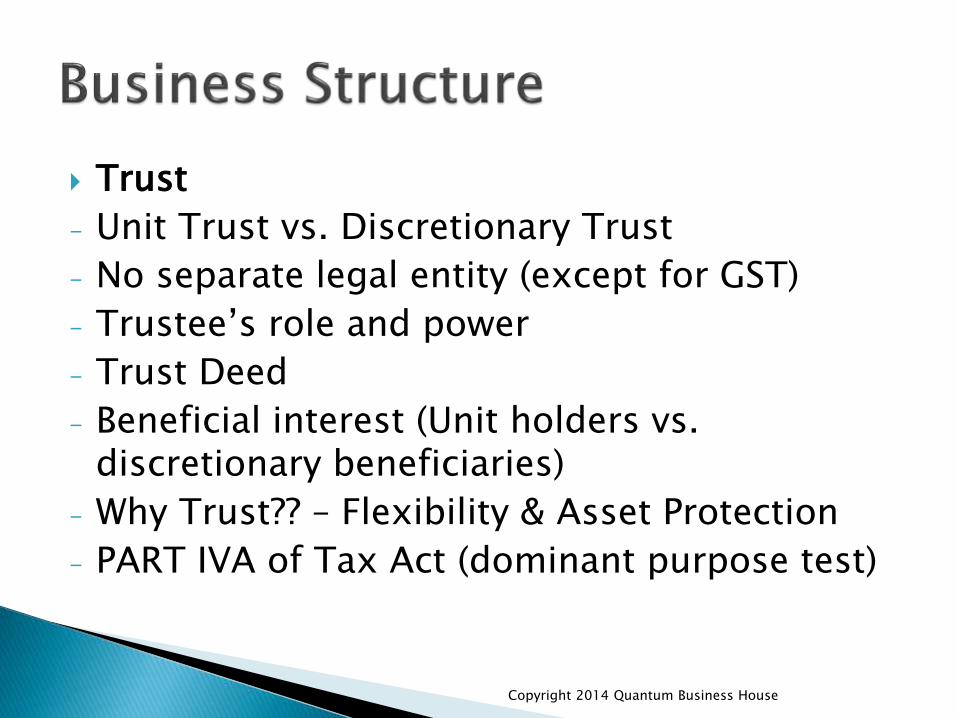

Trust

- Unit Trust vs. Discretionary Trust

- No separate legal entity (except for GST)

- Trustee’s role and power

- Trust Deed

- Beneficial interest (Unit holders vs. discretionary beneficiaries)

- Why Trust?? – Flexibility & Asset Protection

- PART IVA of Tax Act (dominant purpose test)

Copyright 2014 Quantum Business House

Trust

- Two ownerships (legal ownership & beneficial ownership)

- Protecting trust properties (beneficial ownership)

- Income Splitting

- Trustee’s liability for business and reimbursement from trust property (trustee’s entitlement)

- But beneficiaries are safe from debts.

Copyright 2014 Quantum Business House

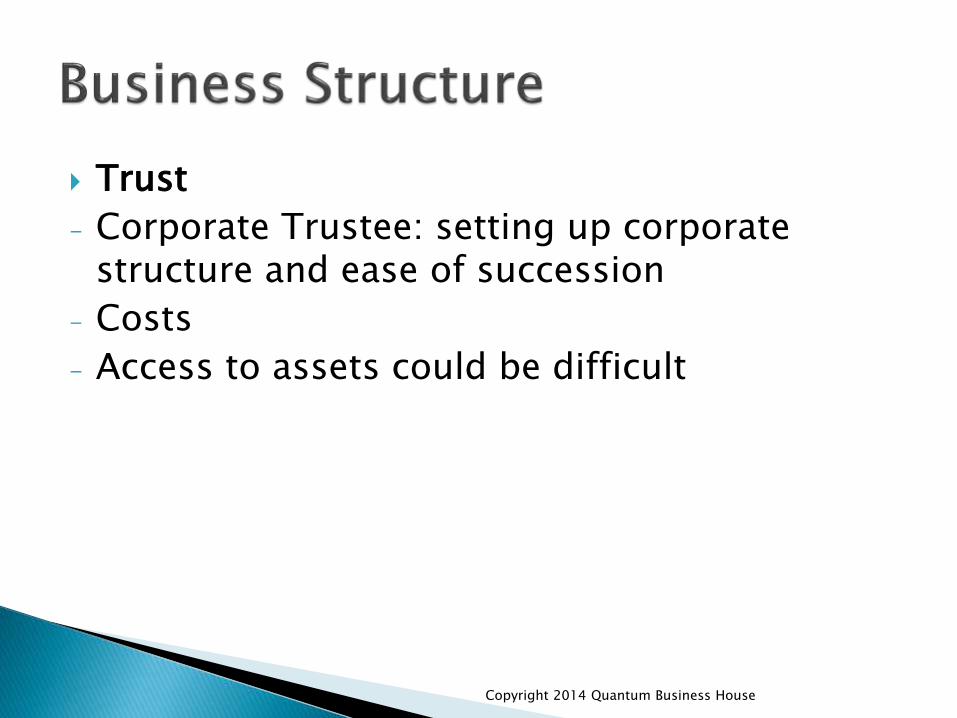

Trust

- Corporate Trustee: setting up corporate structure and ease of succession

- Costs

- Access to assets could be difficult

Copyright 2014 Quantum Business House

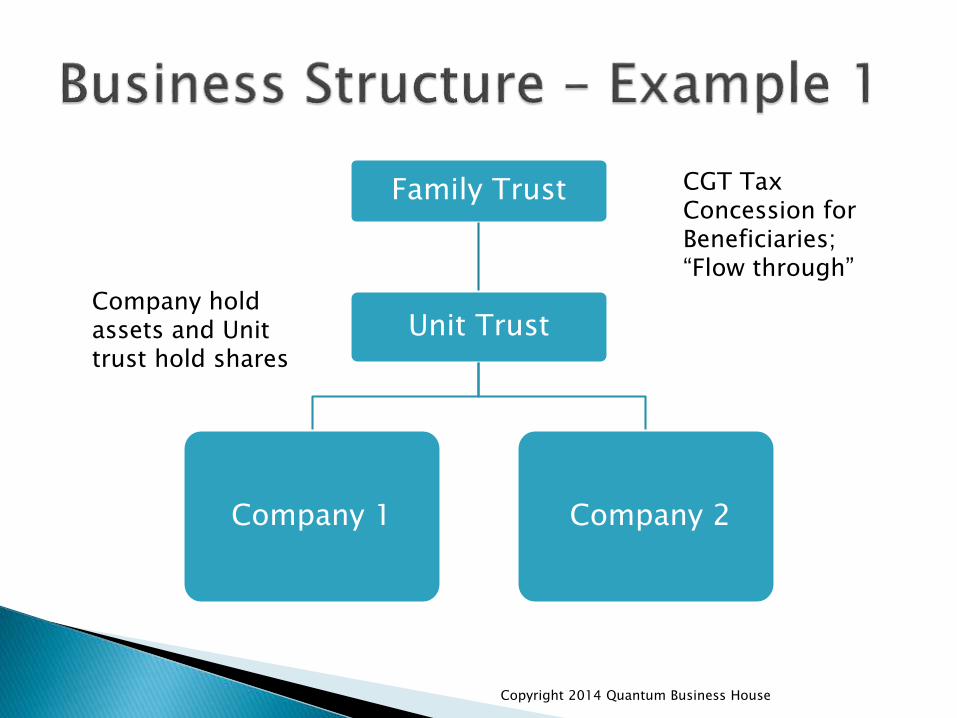

Family Trust

Unit Trust

Company 1 Company 2

CGT Tax Concession for Beneficiaries; “Flow through”

Company hold assets and Unit trust hold shares

Copyright 2014 Quantum Business House

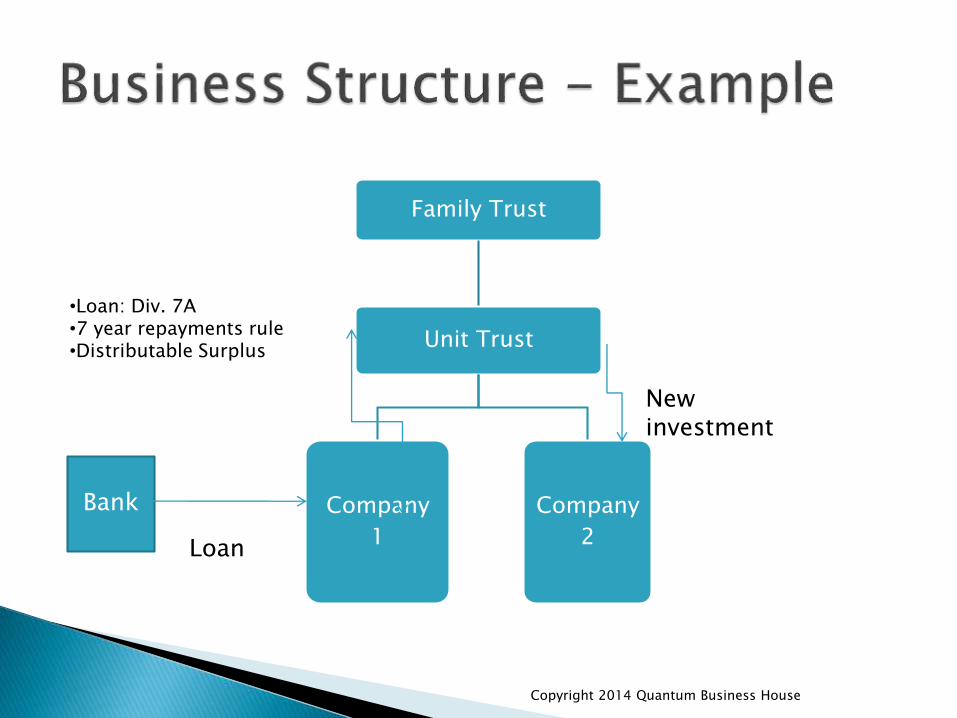

Family Trust

Unit Trust

Company

1

Company

2

Bank

Loan

•Loan: Div. 7A•7 year repayments rule•Distributable Surplus

New investment

Copyright 2014 Quantum Business House

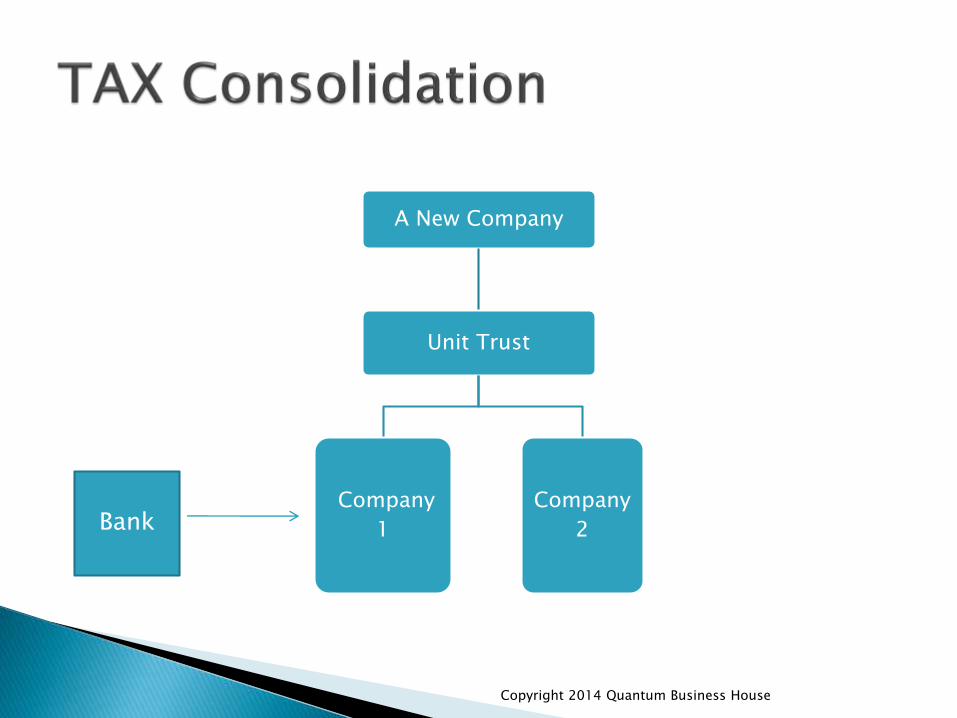

A New Company

Unit Trust

Company

1

Company

2Bank

Copyright 2014 Quantum Business House

Rollover of units for shares (Sub Div.124H)

Then tax consolidation

Conditions:

- Exchanging shares must be non-redeemable

- Must hold the same proportion of units & value in share

Copyright 2014 Quantum Business House

Spouse not exposed to business risks

Family law issue (family home is an asset of marriage) – legal ownership vs. marriage entitlement

Capital Gains Tax – Main residence exemption

A discretionary trust

Copyright 2014 Quantum Business House

Risk minimisation

- Business risks

- Default risks

- Personal guarantee

- Relationship breakdown

Tax minimisation

- Income tax and CGT (50% discount)

Answer: a discretionary trust

Copyright 2014 Quantum Business House

Negative Gearing Issue – The owner must ensure there is other income to offset the loss created by the negative gearing.

Copyright 2014 Quantum Business House

Please use us as free business adviser

Free Initial Consultation

Packaged Services with fixed fee

Copyright 2014 Quantum Business House

Buying a business

Business Planning

Marketing

Raising Finance

Financial Management

Tax system and compliance issues

Risk management

Financial Health Check

Business Evaluation

Copyright 2014 Quantum Business House