Embed Size (px)

Citation preview

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

Understanding tax strategies and managing your tax bill are an integral part of a sound financial approach. Conversely, ignoring the tax ramifications of your investment portfolio may result in lower overall per-formance. Some taxes can be deferred, and others can be managed through tax-efficient investing. With a careful and consistent preparation, you can potentially reduce the impact of taxes on your overall invest-ment returns.

Slide 1

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

This firm provides a wide range of services with the primary commitment of helping our clients pursue their unique financial objectives. We want to help you develop an overall strategy tailored to your goals, time horizon, and risk tolerance.

Slide 2

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

This firm is dedicated to helping individuals evaluate their financial situations. We want to provide people with tools that can help them make informed decisions. We offer informational material on a wide range of topics because we understand that individuals have diverse financial needs. If you have any questions or concerns during the course of this presentation, we invite you to take advantage of our complimentary consultation. During the consultation, we can discuss your questions and begin the process of helping you develop a financial approach that will address your individual needs.

Keep in mind that the information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult a professional for specific infor-mation regarding your individual situation.

Slide 3

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

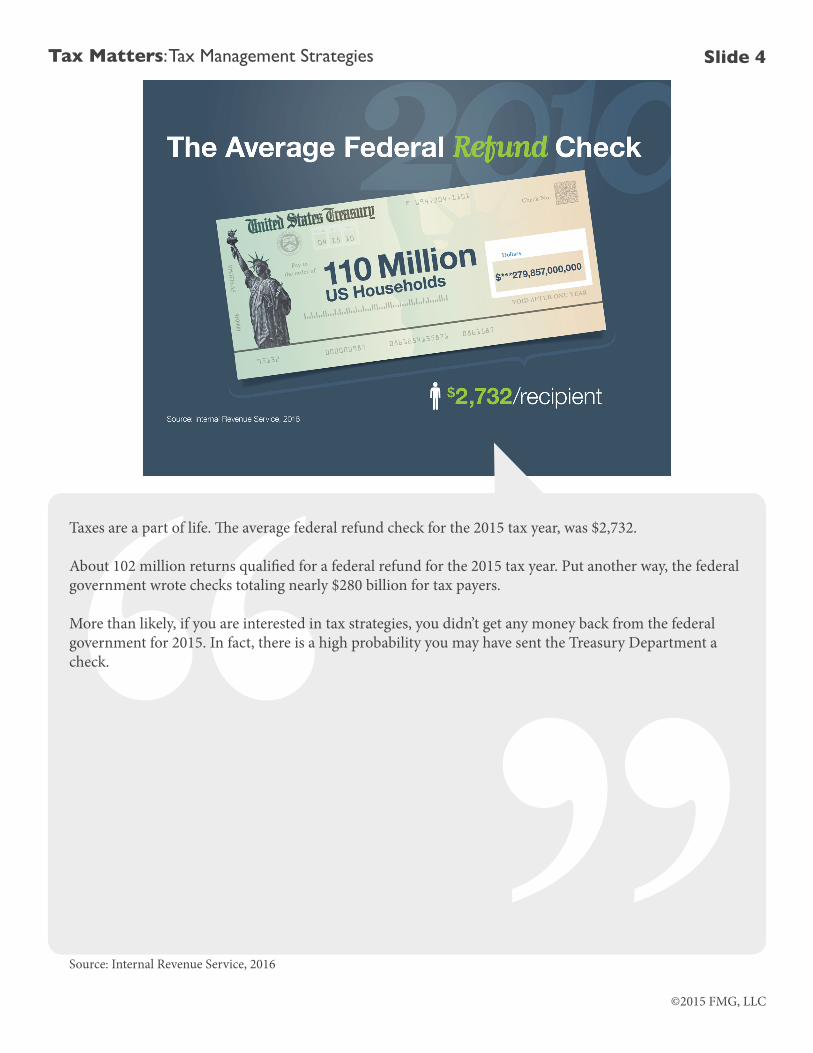

Taxes are a part of life. The average federal refund check for the 2015 tax year, was $2,732.

About 102 million returns qualified for a federal refund for the 2015 tax year. Put another way, the federal government wrote checks totaling nearly $280 billion for tax payers.

More than likely, if you are interested in tax strategies, you didn’t get any money back from the federal government for 2015. In fact, there is a high probability you may have sent the Treasury Department a check.

Source: Internal Revenue Service, 2016

Slide 4

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

After a few false starts, the federal income tax – in it’s current form – was instituted in 1913 when the 16th Amendment to the Constitution was adopted. The 16th Amendment states that Congress shall have power to lay and collect taxes on incomes. In 1913, the first Form 1040 appeared when Congress levied a 1% tax on net personal incomes above $3,000. Congress also levied a 6% surtax on incomes of more than $500,000 in 1913. Over the years, the tax law has changed and the tax code has increased. This short video highlights some of the facts about the current federal income tax program.

Slide 5

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

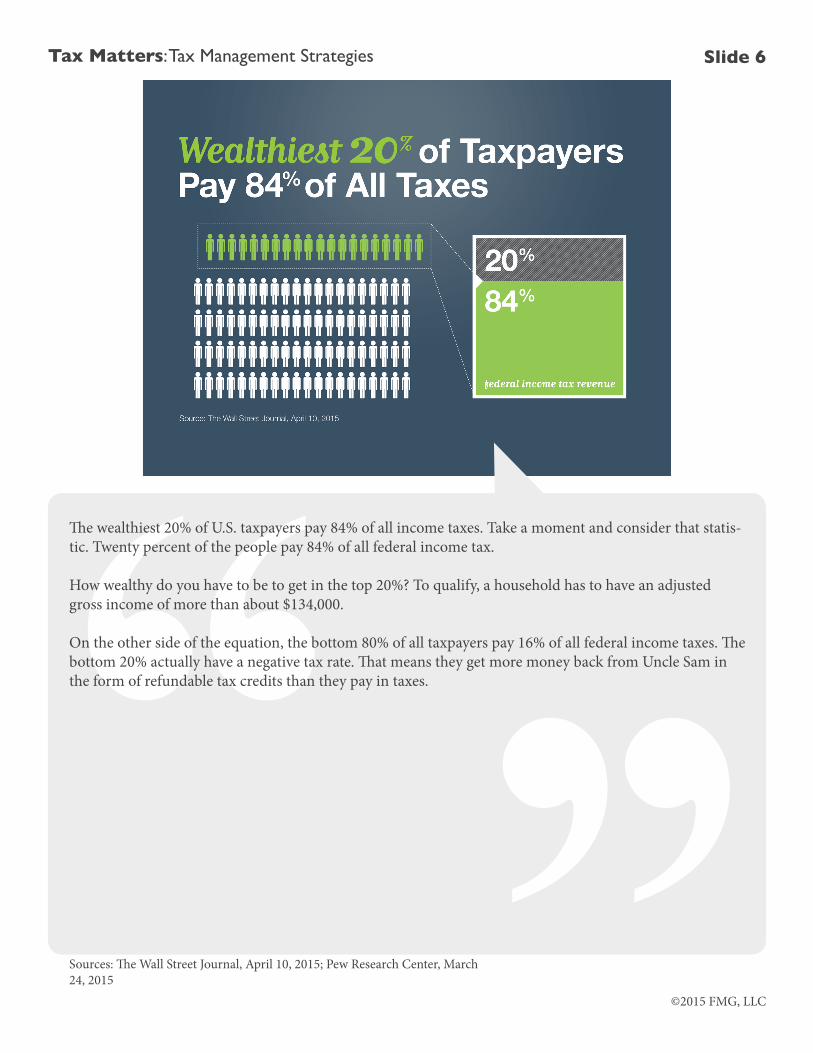

The wealthiest 20% of U.S. taxpayers pay 84% of all income taxes. Take a moment and consider that statis-tic. Twenty percent of the people pay 84% of all federal income tax.

How wealthy do you have to be to get in the top 20%? To qualify, a household has to have an adjusted gross income of more than about $134,000.

On the other side of the equation, the bottom 80% of all taxpayers pay 16% of all federal income taxes. The bottom 20% actually have a negative tax rate. That means they get more money back from Uncle Sam in the form of refundable tax credits than they pay in taxes.

Sources: The Wall Street Journal, April 10, 2015; Pew Research Center, March 24, 2015

Slide 6

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

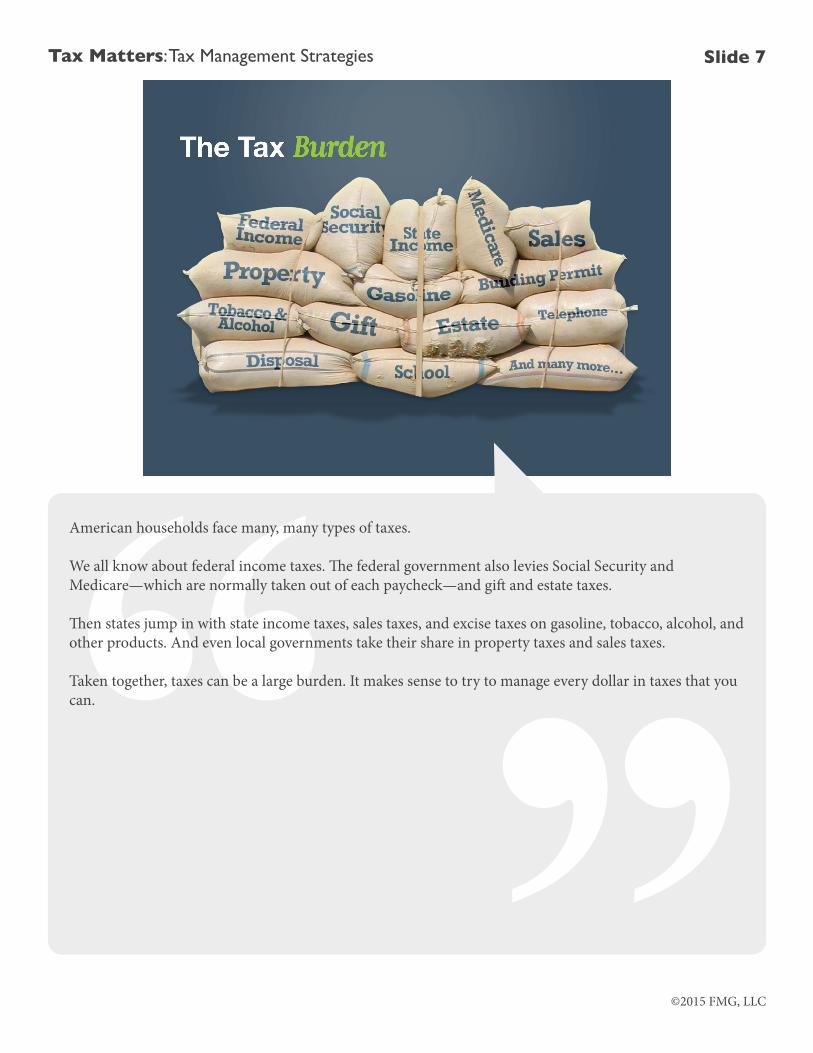

American households face many, many types of taxes.

We all know about federal income taxes. The federal government also levies Social Security and Medicare—which are normally taken out of each paycheck—and gift and estate taxes.

Then states jump in with state income taxes, sales taxes, and excise taxes on gasoline, tobacco, alcohol, and other products. And even local governments take their share in property taxes and sales taxes.

Taken together, taxes can be a large burden. It makes sense to try to manage every dollar in taxes that you can.

Slide 7

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

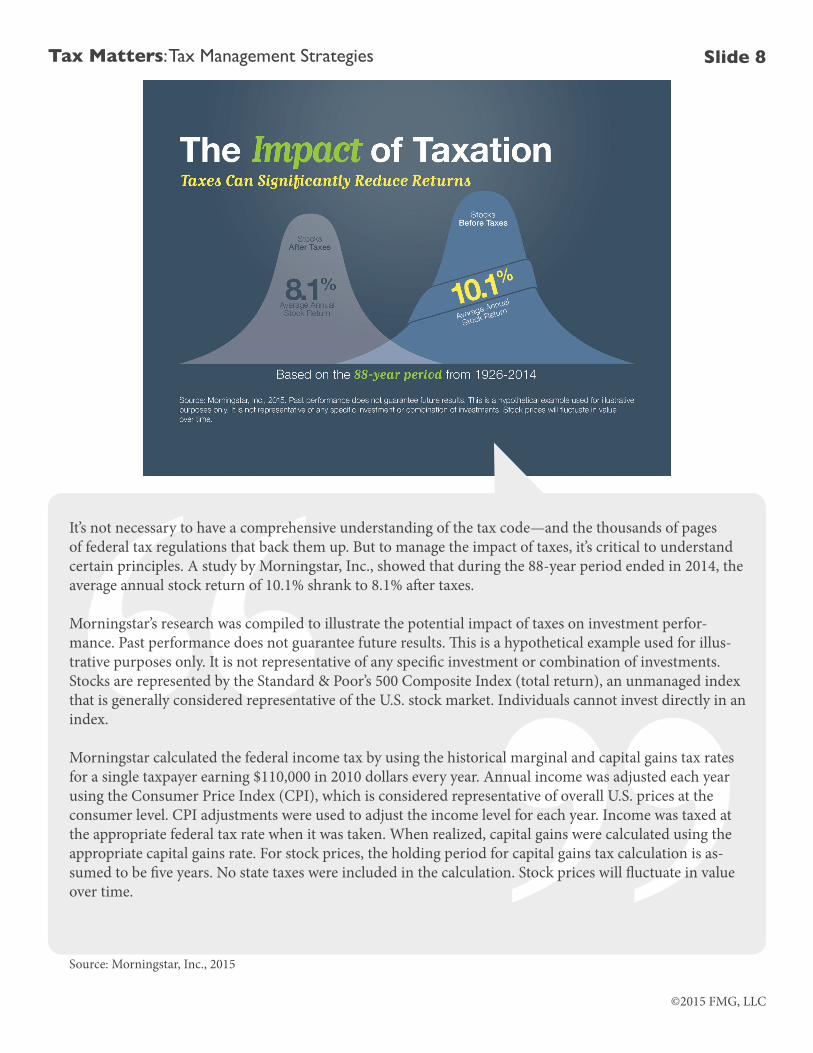

It’s not necessary to have a comprehensive understanding of the tax code—and the thousands of pages of federal tax regulations that back them up. But to manage the impact of taxes, it’s critical to understand certain principles. A study by Morningstar, Inc., showed that during the 88-year period ended in 2014, the average annual stock return of 10.1% shrank to 8.1% after taxes.

Morningstar’s research was compiled to illustrate the potential impact of taxes on investment perfor-mance. Past performance does not guarantee future results. This is a hypothetical example used for illus-trative purposes only. It is not representative of any specific investment or combination of investments. Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Individuals cannot invest directly in an index.

Morningstar calculated the federal income tax by using the historical marginal and capital gains tax rates for a single taxpayer earning $110,000 in 2010 dollars every year. Annual income was adjusted each year using the Consumer Price Index (CPI), which is considered representative of overall U.S. prices at the consumer level. CPI adjustments were used to adjust the income level for each year. Income was taxed at the appropriate federal tax rate when it was taken. When realized, capital gains were calculated using the appropriate capital gains rate. For stock prices, the holding period for capital gains tax calculation is as-sumed to be five years. No state taxes were included in the calculation. Stock prices will fluctuate in value over time.

Source: Morningstar, Inc., 2015

Slide 8

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

There’s an old joke that the difference between death and taxes is that death doesn’t get any worse when-ever Congress goes into session.

As administrations come and go, the tax rules change. And the rate of tax-rule changes appears to be ac-celerating.

Since 1940, there have been 80 major changes in tax legislation. The illustration shows the cumulative number of major changes to tax legislation.

Each time the tax rules change, your investment portfolio may be affected. It critical to stay current with changes in legislation that may affect your tax liability.

Source: Tax Policy Center, Urban Institute, and Brookings Institution, 2015

Slide 9

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

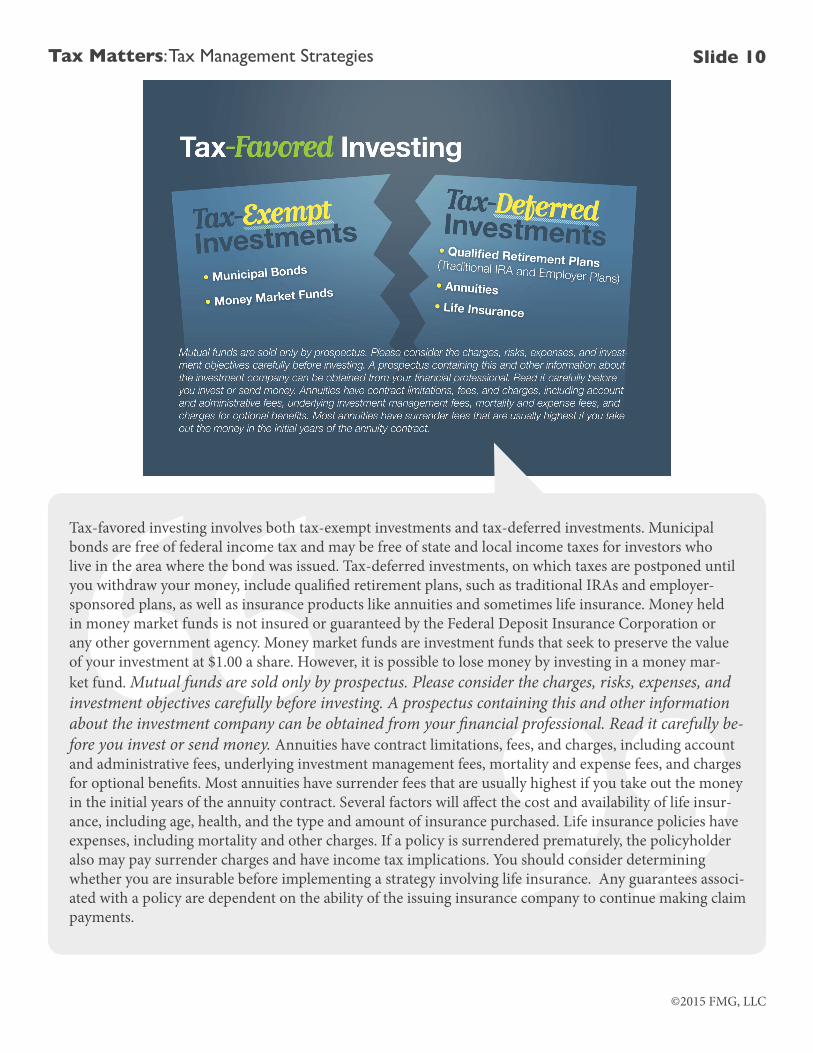

Tax-favored investing involves both tax-exempt investments and tax-deferred investments. Municipal bonds are free of federal income tax and may be free of state and local income taxes for investors who live in the area where the bond was issued. Tax-deferred investments, on which taxes are postponed until you withdraw your money, include qualified retirement plans, such as traditional IRAs and employer-sponsored plans, as well as insurance products like annuities and sometimes life insurance. Money held in money market funds is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Money market funds are investment funds that seek to preserve the value of your investment at $1.00 a share. However, it is possible to lose money by investing in a money mar-ket fund. Mutual funds are sold only by prospectus. Please consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully be-fore you invest or send money. Annuities have contract limitations, fees, and charges, including account and administrative fees, underlying investment management fees, mortality and expense fees, and charges for optional benefits. Most annuities have surrender fees that are usually highest if you take out the money in the initial years of the annuity contract. Several factors will affect the cost and availability of life insur-ance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associ-ated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Slide 10

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

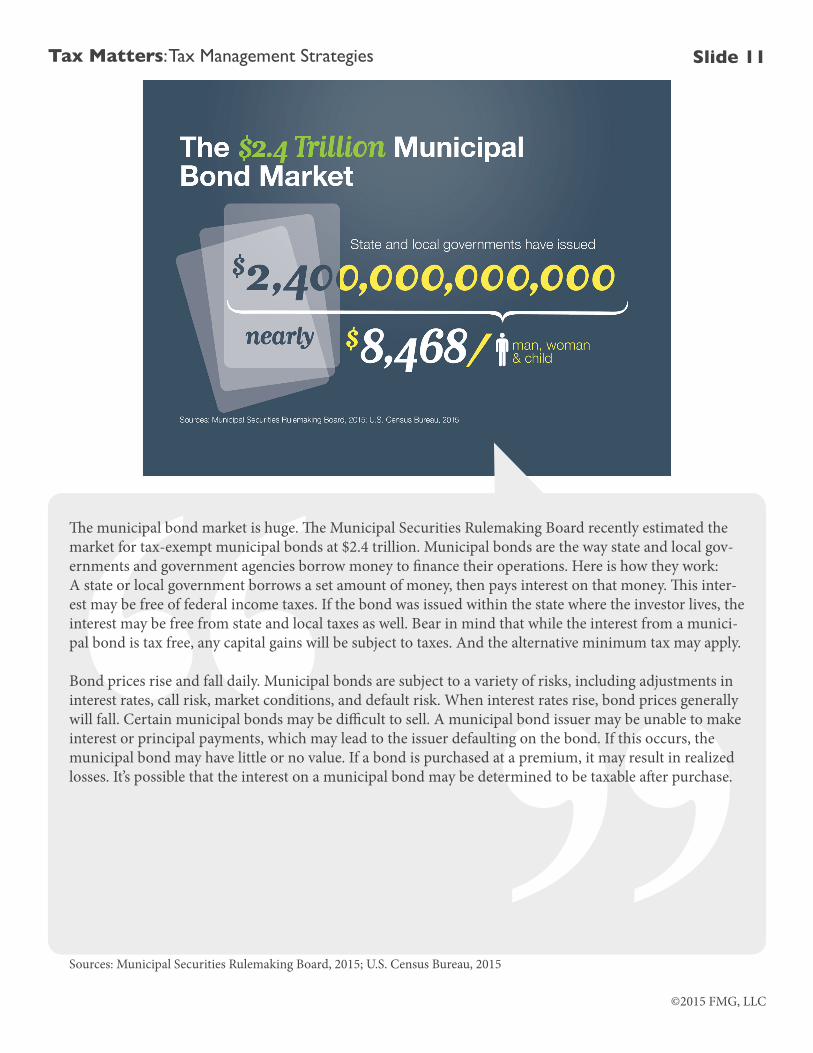

The municipal bond market is huge. The Municipal Securities Rulemaking Board recently estimated the market for tax-exempt municipal bonds at $2.4 trillion. Municipal bonds are the way state and local gov-ernments and government agencies borrow money to finance their operations. Here is how they work:A state or local government borrows a set amount of money, then pays interest on that money. This inter-est may be free of federal income taxes. If the bond was issued within the state where the investor lives, the interest may be free from state and local taxes as well. Bear in mind that while the interest from a munici-pal bond is tax free, any capital gains will be subject to taxes. And the alternative minimum tax may apply.

Bond prices rise and fall daily. Municipal bonds are subject to a variety of risks, including adjustments in interest rates, call risk, market conditions, and default risk. When interest rates rise, bond prices generally will fall. Certain municipal bonds may be difficult to sell. A municipal bond issuer may be unable to make interest or principal payments, which may lead to the issuer defaulting on the bond. If this occurs, the municipal bond may have little or no value. If a bond is purchased at a premium, it may result in realized losses. It’s possible that the interest on a municipal bond may be determined to be taxable after purchase.

Sources: Municipal Securities Rulemaking Board, 2015; U.S. Census Bureau, 2015

Slide 11

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

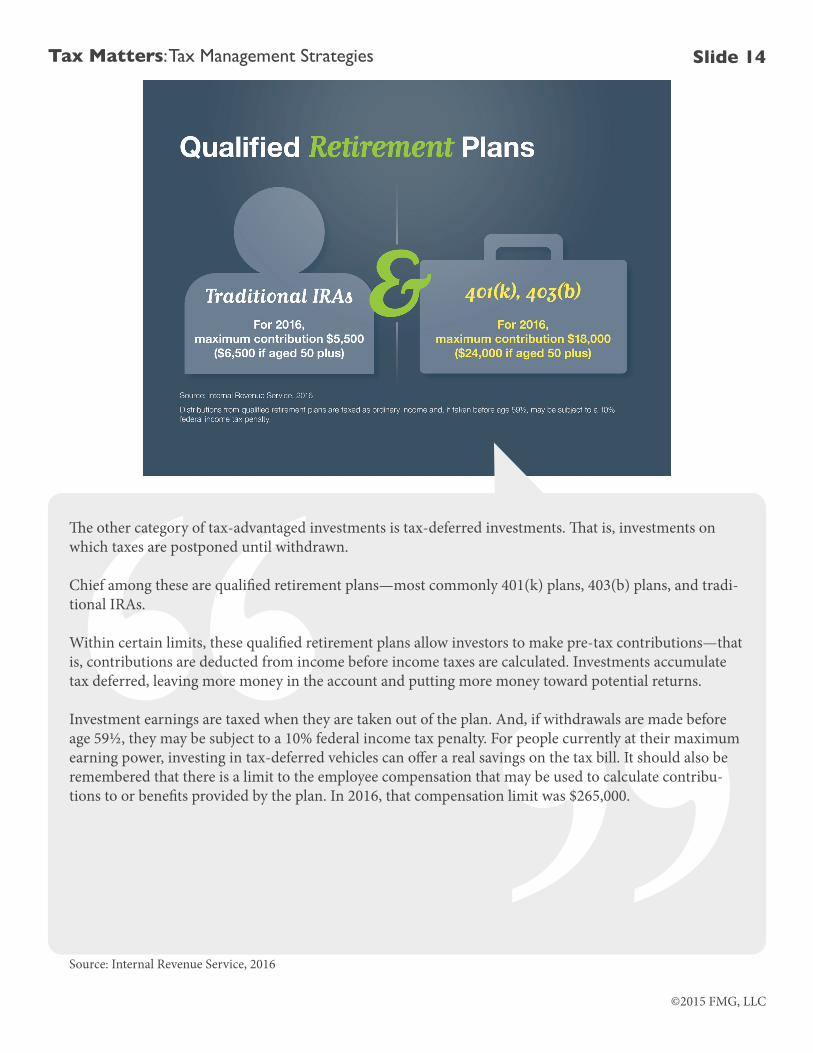

The other category of tax-advantaged investments is tax-deferred investments. That is, investments on which taxes are postponed until the money is withdrawn.

Chief among these are qualified retirement plans—most commonly 401(k) plans, 403(b) plans, and tradi-tional IRAs.

Within certain limits, these qualified retirement plans allow investors to make pre-tax contributions—that is, contributions are deducted from income before income taxes are calculated. Investments accumulate tax deferred, leaving more money in the account and putting more money toward potential returns.

Investment earnings are taxed when they are taken out of the plan. And, if withdrawals are made before age 59½, they may be subject to a 10% federal income tax penalty. For people currently at their maximum earn-ing power, investing in tax-deferred vehicles can offer a real savings on the tax bill. It should also be remem-bered that there is a limit to the employee compensation that may be used to calculate contributions to or benefits provided by the plan. In 2016, that compensation limit was $265,000.

Slide 12

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

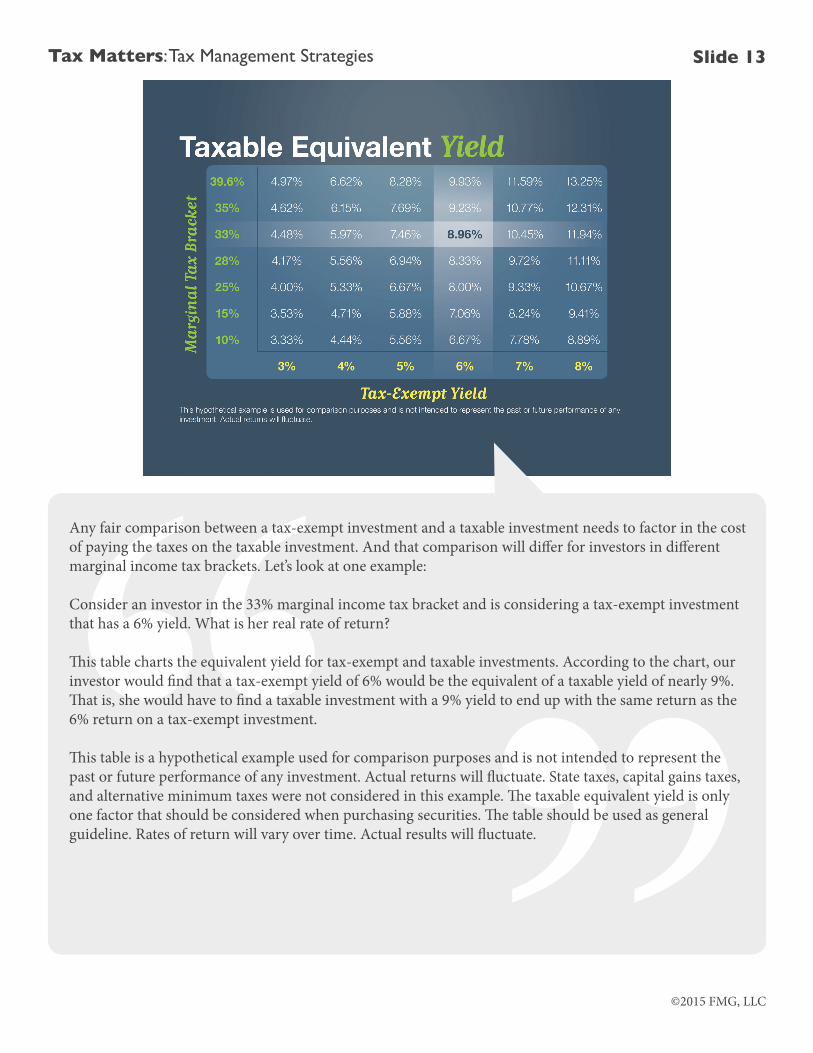

Any fair comparison between a tax-exempt investment and a taxable investment needs to factor in the cost of paying the taxes on the taxable investment. And that comparison will differ for investors in different marginal income tax brackets. Let’s look at one example:

Consider an investor in the 33% marginal income tax bracket and is considering a tax-exempt investment that has a 6% yield. What is her real rate of return?

This table charts the equivalent yield for tax-exempt and taxable investments. According to the chart, our investor would find that a tax-exempt yield of 6% would be the equivalent of a taxable yield of nearly 9%. That is, she would have to find a taxable investment with a 9% yield to end up with the same return as the 6% return on a tax-exempt investment.

This table is a hypothetical example used for comparison purposes and is not intended to represent the past or future performance of any investment. Actual returns will fluctuate. State taxes, capital gains taxes, and alternative minimum taxes were not considered in this example. The taxable equivalent yield is only one factor that should be considered when purchasing securities. The table should be used as general guideline. Rates of return will vary over time. Actual results will fluctuate.

Slide 13

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

The other category of tax-advantaged investments is tax-deferred investments. That is, investments on which taxes are postponed until withdrawn.

Chief among these are qualified retirement plans—most commonly 401(k) plans, 403(b) plans, and tradi-tional IRAs.

Within certain limits, these qualified retirement plans allow investors to make pre-tax contributions—that is, contributions are deducted from income before income taxes are calculated. Investments accumulate tax deferred, leaving more money in the account and putting more money toward potential returns.

Investment earnings are taxed when they are taken out of the plan. And, if withdrawals are made before age 59½, they may be subject to a 10% federal income tax penalty. For people currently at their maximum earning power, investing in tax-deferred vehicles can offer a real savings on the tax bill. It should also be remembered that there is a limit to the employee compensation that may be used to calculate contribu-tions to or benefits provided by the plan. In 2016, that compensation limit was $265,000.

Source: Internal Revenue Service, 2016

Slide 14

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

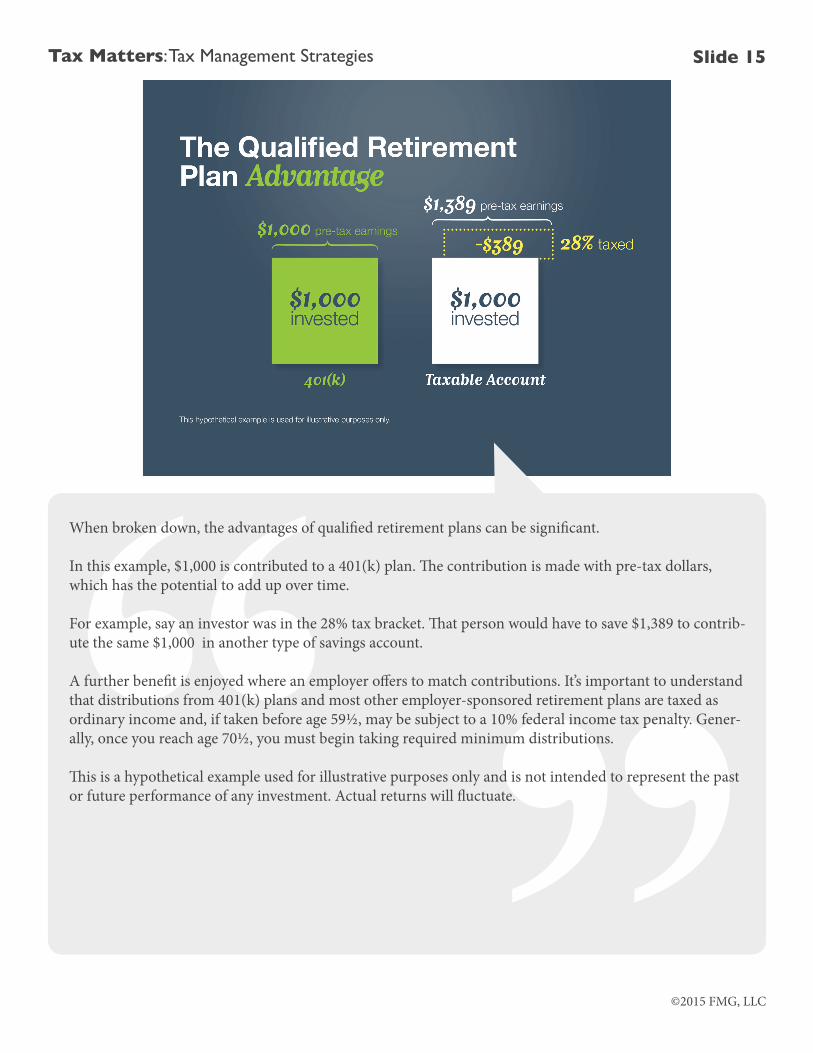

When broken down, the advantages of qualified retirement plans can be significant.

In this example, $1,000 is contributed to a 401(k) plan. The contribution is made with pre-tax dollars, which has the potential to add up over time.

For example, say an investor was in the 28% tax bracket. That person would have to save $1,389 to contrib-ute the same $1,000 in another type of savings account.

A further benefit is enjoyed where an employer offers to match contributions. It’s important to understand that distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Gener-ally, once you reach age 70½, you must begin taking required minimum distributions.

This is a hypothetical example used for illustrative purposes only and is not intended to represent the past or future performance of any investment. Actual returns will fluctuate.

Slide 15

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

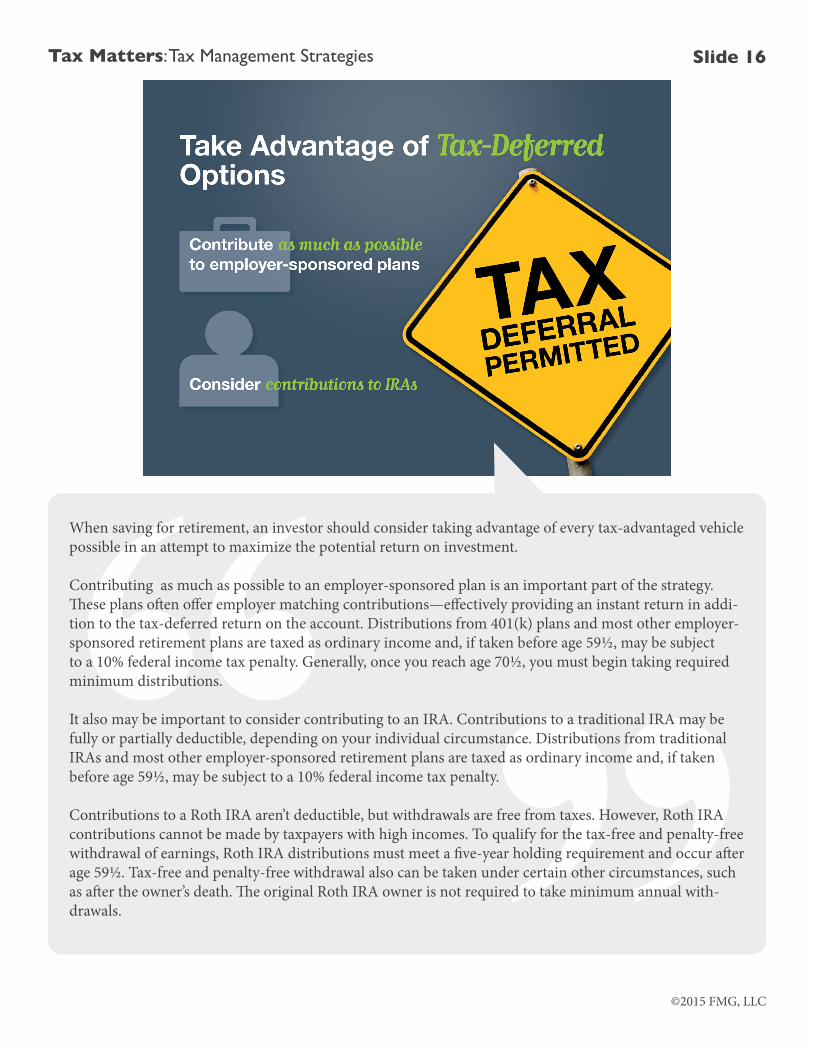

When saving for retirement, an investor should consider taking advantage of every tax-advantaged vehicle possible in an attempt to maximize the potential return on investment.

Contributing as much as possible to an employer-sponsored plan is an important part of the strategy. These plans often offer employer matching contributions—effectively providing an instant return in addi-tion to the tax-deferred return on the account. Distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

It also may be important to consider contributing to an IRA. Contributions to a traditional IRA may be fully or partially deductible, depending on your individual circumstance. Distributions from traditional IRAs and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Contributions to a Roth IRA aren’t deductible, but withdrawals are free from taxes. However, Roth IRA contributions cannot be made by taxpayers with high incomes. To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal also can be taken under certain other circumstances, such as after the owner’s death. The original Roth IRA owner is not required to take minimum annual with-drawals.

Slide 16

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

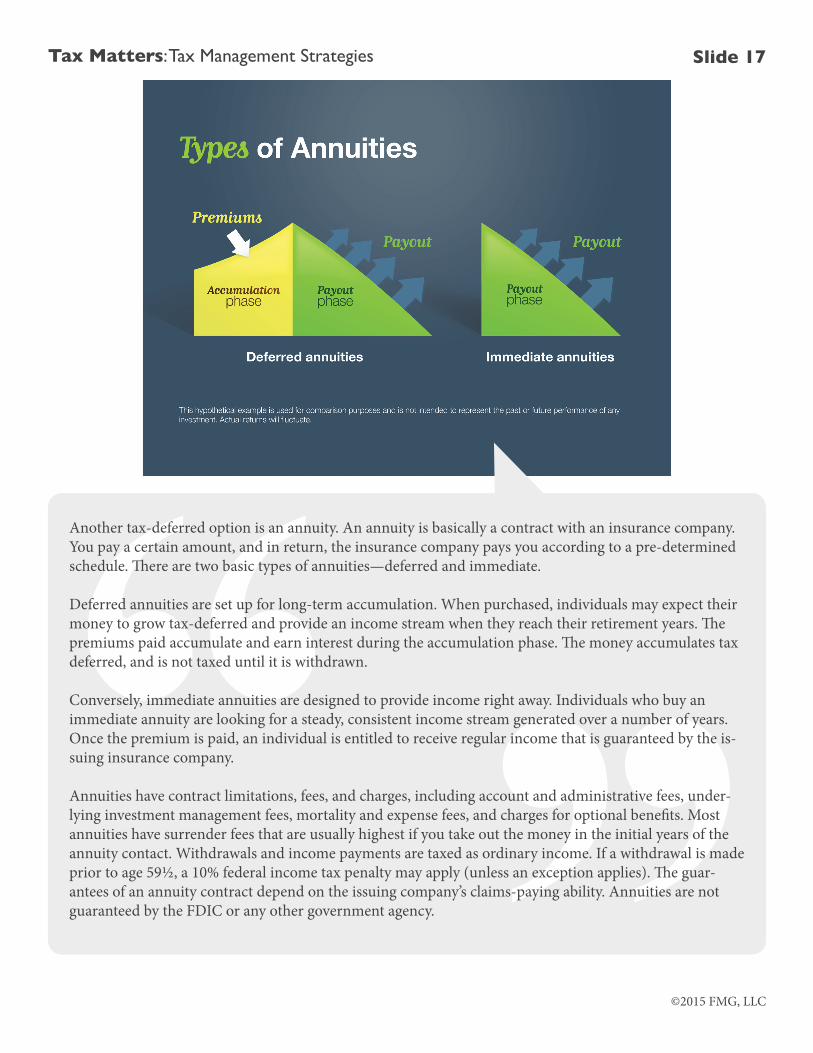

Another tax-deferred option is an annuity. An annuity is basically a contract with an insurance company. You pay a certain amount, and in return, the insurance company pays you according to a pre-determined schedule. There are two basic types of annuities—deferred and immediate.

Deferred annuities are set up for long-term accumulation. When purchased, individuals may expect their money to grow tax-deferred and provide an income stream when they reach their retirement years. The premiums paid accumulate and earn interest during the accumulation phase. The money accumulates tax deferred, and is not taxed until it is withdrawn.

Conversely, immediate annuities are designed to provide income right away. Individuals who buy an immediate annuity are looking for a steady, consistent income stream generated over a number of years. Once the premium is paid, an individual is entitled to receive regular income that is guaranteed by the is-suing insurance company.

Annuities have contract limitations, fees, and charges, including account and administrative fees, under-lying investment management fees, mortality and expense fees, and charges for optional benefits. Most annuities have surrender fees that are usually highest if you take out the money in the initial years of the annuity contact. Withdrawals and income payments are taxed as ordinary income. If a withdrawal is made prior to age 59½, a 10% federal income tax penalty may apply (unless an exception applies). The guar-antees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities are not guaranteed by the FDIC or any other government agency.

Slide 17

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

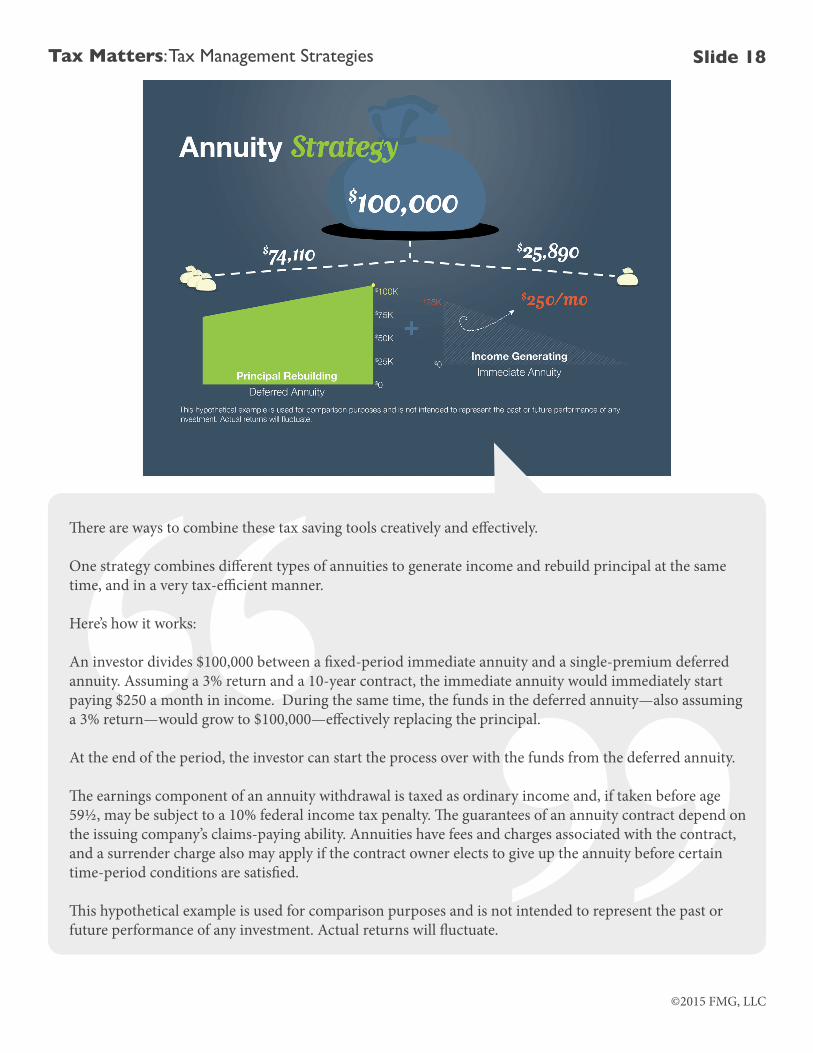

There are ways to combine these tax saving tools creatively and effectively.

One strategy combines different types of annuities to generate income and rebuild principal at the same time, and in a very tax-efficient manner.

Here’s how it works:

An investor divides $100,000 between a fixed-period immediate annuity and a single-premium deferred annuity. Assuming a 3% return and a 10-year contract, the immediate annuity would immediately start paying $250 a month in income. During the same time, the funds in the deferred annuity—also assuming a 3% return—would grow to $100,000—effectively replacing the principal.

At the end of the period, the investor can start the process over with the funds from the deferred annuity.

The earnings component of an annuity withdrawal is taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities have fees and charges associated with the contract, and a surrender charge also may apply if the contract owner elects to give up the annuity before certain time-period conditions are satisfied.

This hypothetical example is used for comparison purposes and is not intended to represent the past or future performance of any investment. Actual returns will fluctuate.

Slide 18

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

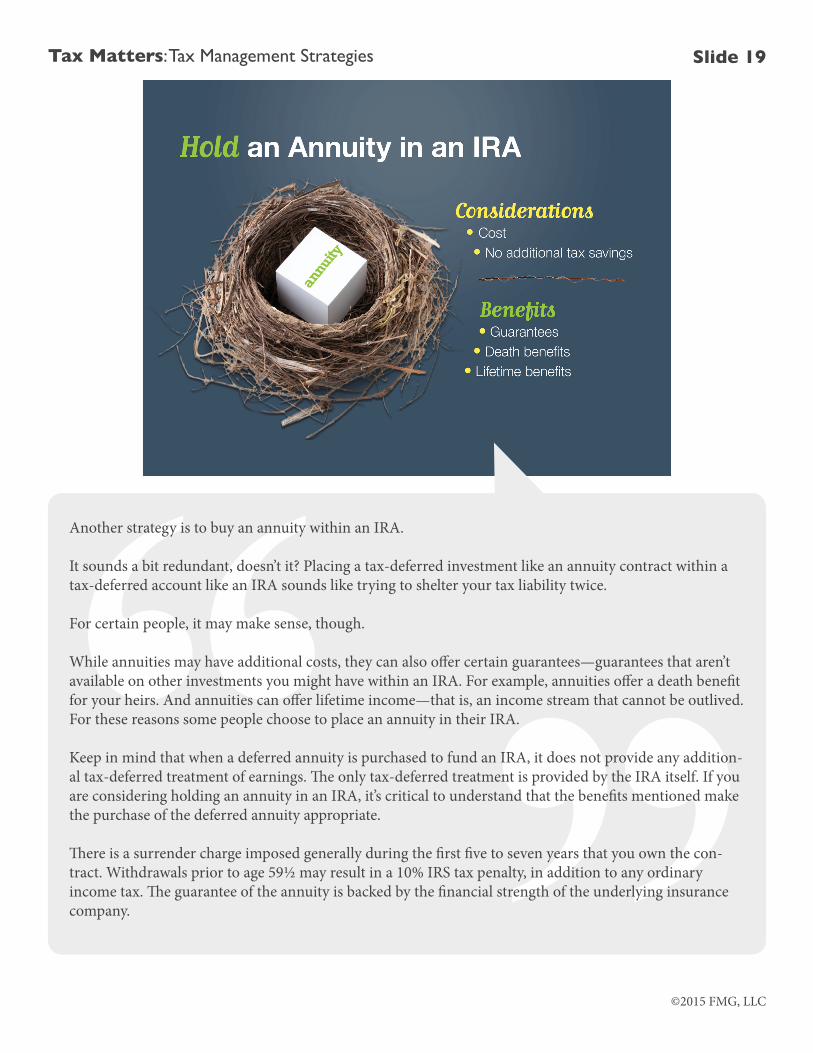

Another strategy is to buy an annuity within an IRA.

It sounds a bit redundant, doesn’t it? Placing a tax-deferred investment like an annuity contract within a tax-deferred account like an IRA sounds like trying to shelter your tax liability twice.

For certain people, it may make sense, though.

While annuities may have additional costs, they can also offer certain guarantees—guarantees that aren’t available on other investments you might have within an IRA. For example, annuities offer a death benefit for your heirs. And annuities can offer lifetime income—that is, an income stream that cannot be outlived. For these reasons some people choose to place an annuity in their IRA.

Keep in mind that when a deferred annuity is purchased to fund an IRA, it does not provide any addition-al tax-deferred treatment of earnings. The only tax-deferred treatment is provided by the IRA itself. If you are considering holding an annuity in an IRA, it’s critical to understand that the benefits mentioned make the purchase of the deferred annuity appropriate.

There is a surrender charge imposed generally during the first five to seven years that you own the con-tract. Withdrawals prior to age 59½ may result in a 10% IRS tax penalty, in addition to any ordinary income tax. The guarantee of the annuity is backed by the financial strength of the underlying insurance company.

Slide 19

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

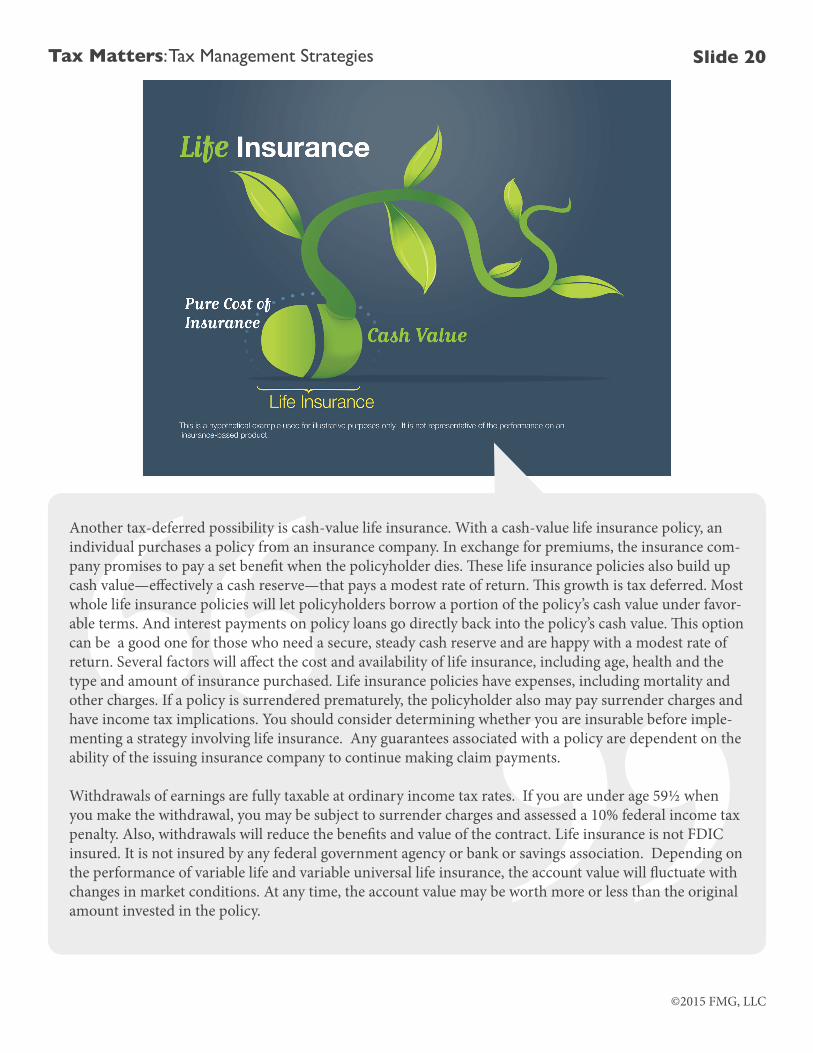

Another tax-deferred possibility is cash-value life insurance. With a cash-value life insurance policy, an individual purchases a policy from an insurance company. In exchange for premiums, the insurance com-pany promises to pay a set benefit when the policyholder dies. These life insurance policies also build up cash value—effectively a cash reserve—that pays a modest rate of return. This growth is tax deferred. Most whole life insurance policies will let policyholders borrow a portion of the policy’s cash value under favor-able terms. And interest payments on policy loans go directly back into the policy’s cash value. This option can be a good one for those who need a secure, steady cash reserve and are happy with a modest rate of return. Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before imple-menting a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Withdrawals of earnings are fully taxable at ordinary income tax rates. If you are under age 59½ when you make the withdrawal, you may be subject to surrender charges and assessed a 10% federal income tax penalty. Also, withdrawals will reduce the benefits and value of the contract. Life insurance is not FDIC insured. It is not insured by any federal government agency or bank or savings association. Depending on the performance of variable life and variable universal life insurance, the account value will fluctuate with changes in market conditions. At any time, the account value may be worth more or less than the original amount invested in the policy.

Slide 20

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

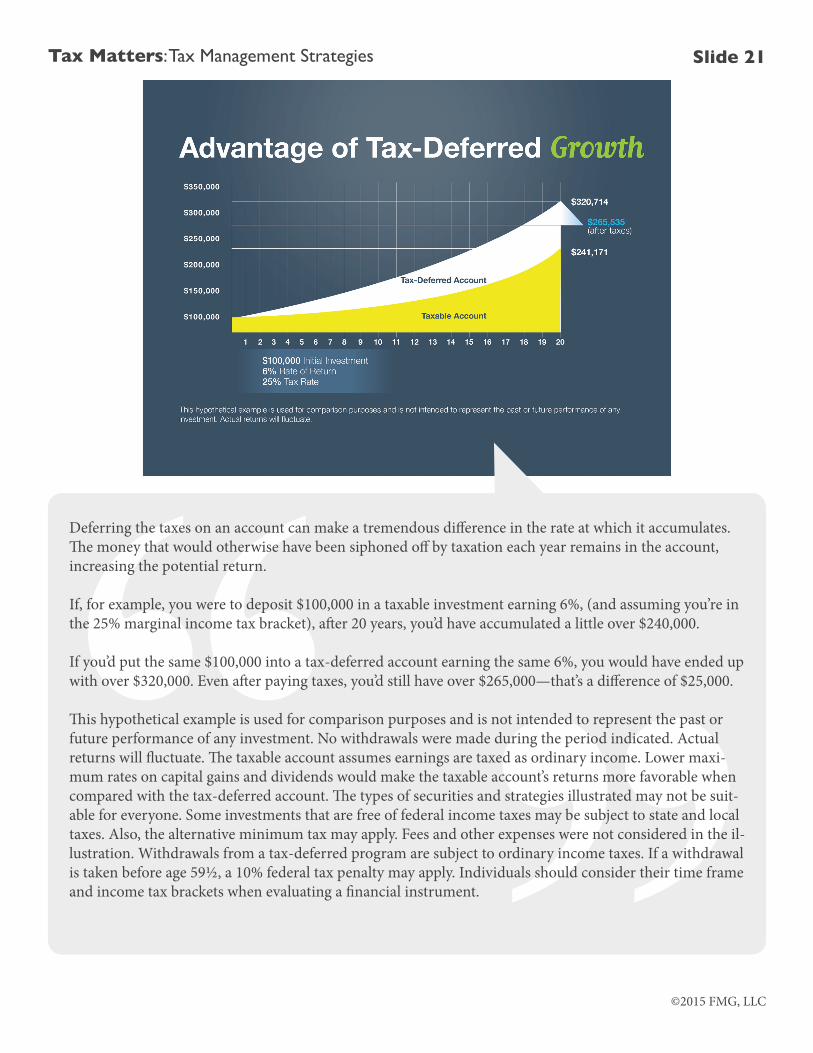

Deferring the taxes on an account can make a tremendous difference in the rate at which it accumulates. The money that would otherwise have been siphoned off by taxation each year remains in the account, increasing the potential return.

If, for example, you were to deposit $100,000 in a taxable investment earning 6%, (and assuming you’re in the 25% marginal income tax bracket), after 20 years, you’d have accumulated a little over $240,000.

If you’d put the same $100,000 into a tax-deferred account earning the same 6%, you would have ended up with over $320,000. Even after paying taxes, you’d still have over $265,000—that’s a difference of $25,000.

This hypothetical example is used for comparison purposes and is not intended to represent the past or future performance of any investment. No withdrawals were made during the period indicated. Actual returns will fluctuate. The taxable account assumes earnings are taxed as ordinary income. Lower maxi-mum rates on capital gains and dividends would make the taxable account’s returns more favorable when compared with the tax-deferred account. The types of securities and strategies illustrated may not be suit-able for everyone. Some investments that are free of federal income taxes may be subject to state and local taxes. Also, the alternative minimum tax may apply. Fees and other expenses were not considered in the il-lustration. Withdrawals from a tax-deferred program are subject to ordinary income taxes. If a withdrawal is taken before age 59½, a 10% federal tax penalty may apply. Individuals should consider their time frame and income tax brackets when evaluating a financial instrument.

Slide 21

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

Effectively managing your tax liability is a life-long process. Here are some questions that arise at different stages in life:

Anthony and Selena, a two-income couple with school-aged children, ask, “How do we take advantage of all available tax credits and deductions? Should we max out our 401(k) plans?”

Dave and Christine, a couple nearing retirement, want to know, “How do we allocate our assets for the best tax advantages? How can we gift assets to our children in the most tax-effective manner?”

Rebecca is a single parent and small business owner. She asks, “Can tax-advantaged investing help me manage my tax burden? What retirement plans are available for small business owners?”

Isaac likes to do his taxes online, but wonders, “Am I realizing all of the tax benefits available to me?Are there changes in the tax law that might affect my situation?”

Answers will depend on each unique situation, and may be found after a professional review.

Slide 22

©2015 FMG, LLC

Tax Matters: Tax Management Strategies

There are a number of strategies you can use to manage income taxes. You need a knowledgeable firm in place.

And that’s where our firm comes in. We specialize in helping people just like you make the most of every investment dollar.

If you think it may be time to take a closer look at ways to manage your tax liability, schedule a review today.

Slide 23