Embed Size (px)

Citation preview

© 2010 Trajectory Group • Confidential & Proprietary 1

ACC 2011 Meeting, March 16-17, 2011

How to break out of the

commoditization trap?

Presented by Ralf Hug, President

Trajectory Group LLC

© 2010 Trajectory Group • Confidential & Proprietary 2

Your competition copied your winning features and is underselling you by a wide margin. Customers once delighted by your innovation/quality are now only interested in your price. Your largest customers are aggressively using bargaining power squeezing your prices and margins impacting your profitability. AND your marketing has become powerless!

Sound familiar?

© 2010 Trajectory Group • Confidential & Proprietary 3

Can you fight commoditization and win?

© 2010 Trajectory Group • Confidential & Proprietary 4

A Company With a Price Advantage

Can Be Undercut!

A Company With a Performance Advantage

Can Be Out Flanked!

But, a Company Owning the Category‟s USP

(Unique Selling Proposition)

Can Potentially Demand a Price Premium . . . Forever!

THINK ABOUT THIS…

© 2010 Trajectory Group • Confidential & Proprietary 5

DIFFERENTIATE

OR

DIE

ESCAPE

BY REINVENTING THE VALUE PROPOSITIONS

© 2010 Trajectory Group • Confidential & Proprietary 6

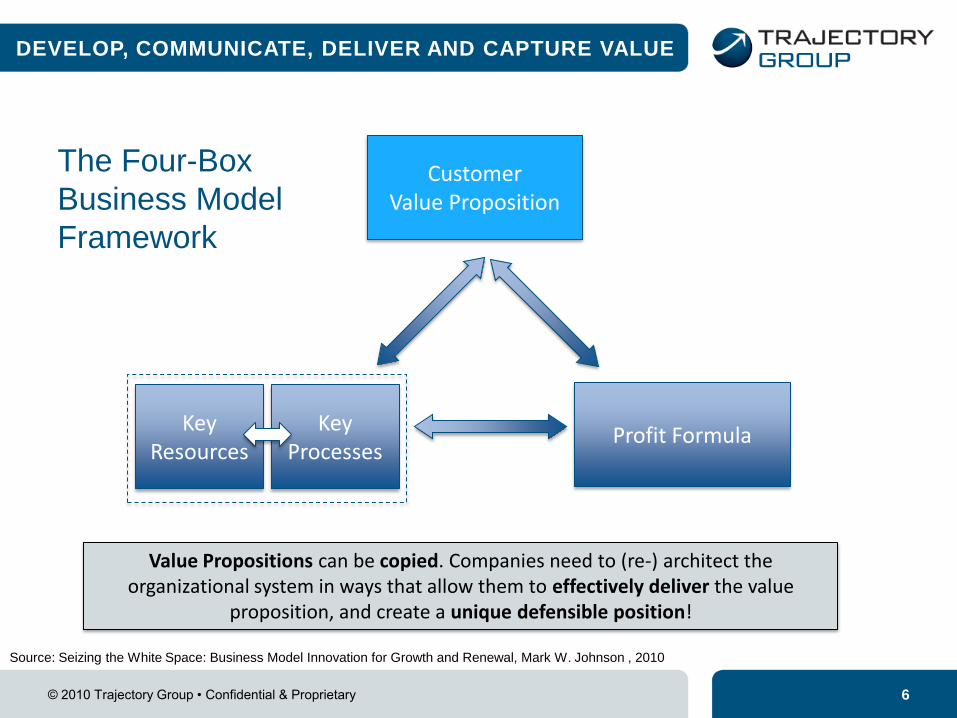

DEVELOP, COMMUNICATE, DELIVER AND CAPTURE VALUE

Customer Value Proposition

Profit Formula Key

Resources Key

Processes

Value Propositions can be copied. Companies need to (re-) architect the organizational system in ways that allow them to effectively deliver the value

proposition, and create a unique defensible position!

The Four-Box

Business Model

Framework

Source: Seizing the White Space: Business Model Innovation for Growth and Renewal, Mark W. Johnson , 2010

© 2010 Trajectory Group • Confidential & Proprietary 7

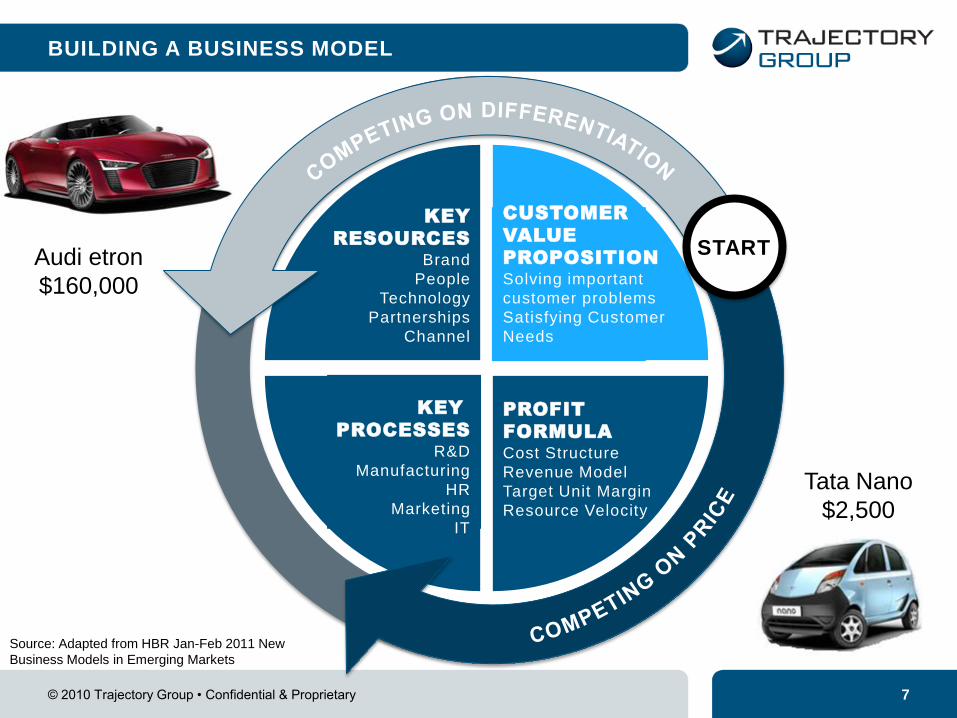

BUILDING A BUSINESS MODEL

START

KEY

RESOURCES

Brand

People

Technology

Partnerships

Channel

KEY

PROCESSES

R&D

Manufacturing

HR

Marketing

IT

CUSTOMER

VALUE

PROPOSITION

Solving important

customer problems

Satisfying Customer

Needs

PROFIT

FORMULA

Cost Structure

Revenue Model

Target Unit Margin

Resource Velocity

Audi etron

$160,000

Tata Nano

$2,500

Source: Adapted from HBR Jan-Feb 2011 New

Business Models in Emerging Markets

© 2010 Trajectory Group • Confidential & Proprietary 8

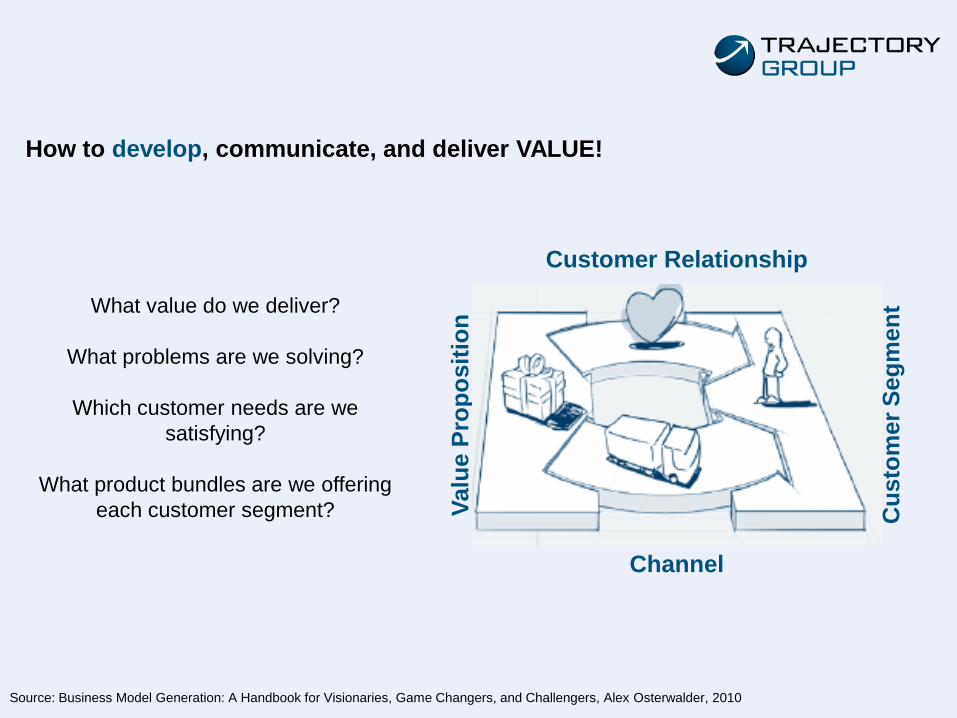

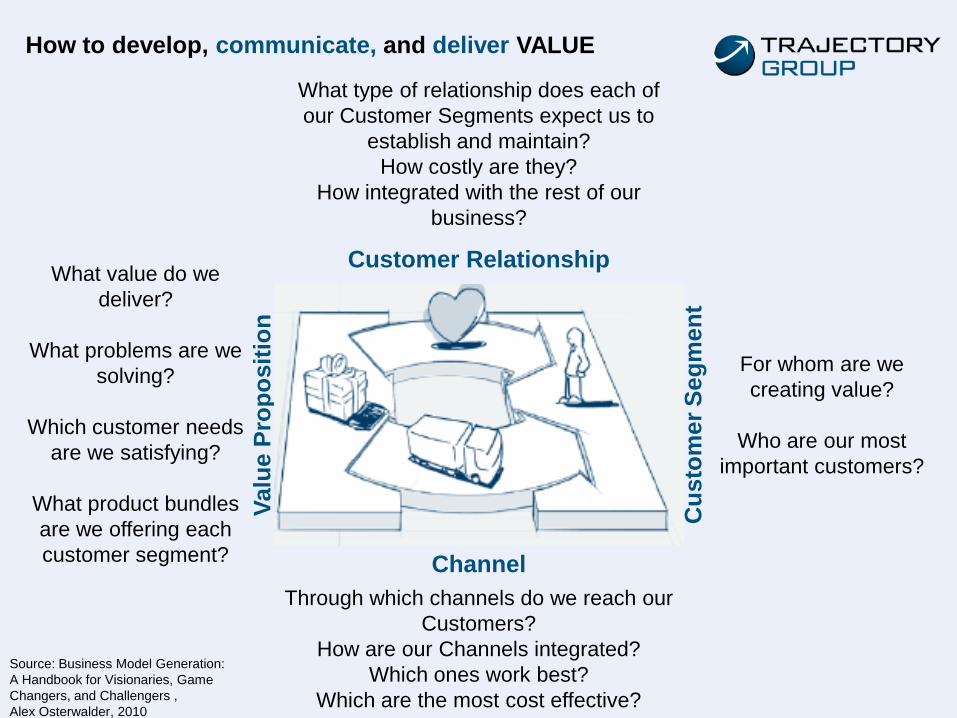

What value do we deliver?

What problems are we solving?

Which customer needs are we

satisfying?

What product bundles are we offering

each customer segment? Cu

sto

mer

Se

gm

en

t

Valu

e P

rop

os

itio

n

Customer Relationship

Channel

How to develop, communicate, and deliver VALUE!

Source: Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers, Alex Osterwalder, 2010

© 2010 Trajectory Group • Confidential & Proprietary 9

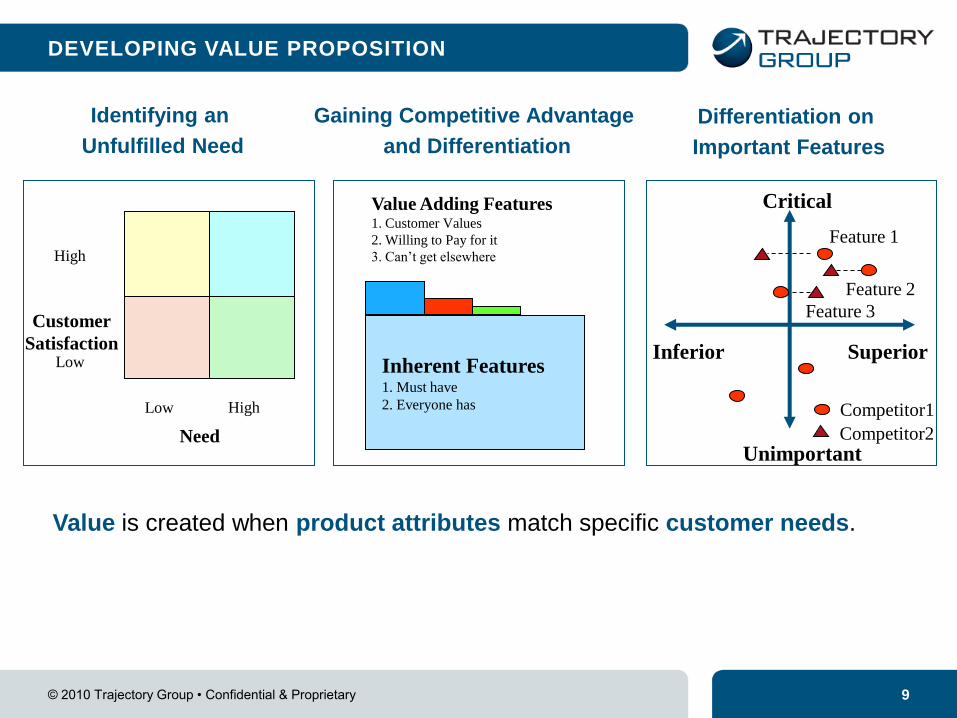

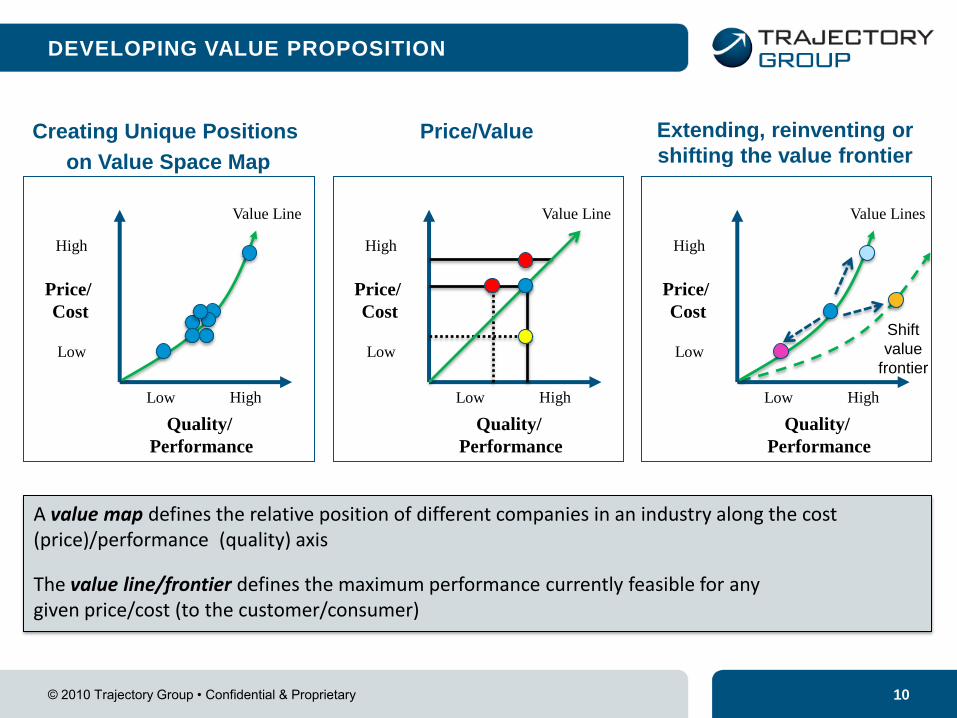

DEVELOPING VALUE PROPOSITION

Need

Customer

Satisfaction Low

High

Low High

Identifying an

Unfulfilled Need

Inherent Features 1. Must have

2. Everyone has

Value Adding Features 1. Customer Values

2. Willing to Pay for it

3. Can’t get elsewhere

Gaining Competitive Advantage

and Differentiation

Unimportant

Critical

Inferior Superior

Feature 2

Feature 3

Feature 1

Competitor1

Competitor2

Differentiation on

Important Features

Value is created when product attributes match specific customer needs.

© 2010 Trajectory Group • Confidential & Proprietary 10

Quality/

Performance

Low

High

Low High

Price/

Cost

Value Line

Creating Unique Positions

on Value Space Map

Quality/

Performance

Low

High

Low High

Price/

Cost

Value Line

Price/Value

A value map defines the relative position of different companies in an industry along the cost (price)/performance (quality) axis

The value line/frontier defines the maximum performance currently feasible for any given price/cost (to the customer/consumer)

Quality/

Performance

Low

High

Low High

Price/

Cost

Value Lines

Shift

value

frontier

Extending, reinventing or

shifting the value frontier

DEVELOPING VALUE PROPOSITION

© 2010 Trajectory Group • Confidential & Proprietary 11

Paradigm Shift

The most powerful competitive differentiators in today’s marketplace speak not only to functional benefits,

but also … and perhaps most importantly … to some meta benefit, above and beyond the functioning of

the product itself.

© 2010 Trajectory Group • Confidential & Proprietary 12

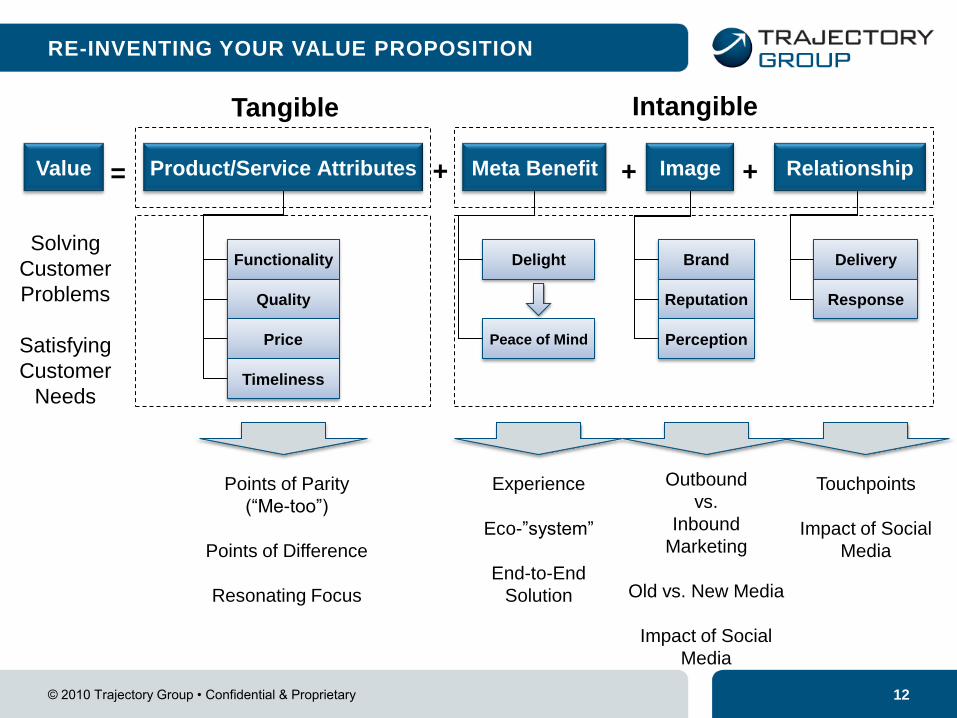

RE-INVENTING YOUR VALUE PROPOSITION

Value + =

Points of Parity

(“Me-too”)

Points of Difference

Resonating Focus

Touchpoints

Impact of Social

Media

Outbound

vs.

Inbound

Marketing

Old vs. New Media

Impact of Social

Media

Product/Service Attributes

Functionality

Quality

Price

Timeliness

Tangible

Image Relationship Meta Benefit + +

Intangible

Brand

Reputation

Delivery

Response

Perception

Delight

Peace of Mind

Solving

Customer

Problems

Satisfying

Customer

Needs

Experience

Eco-”system”

End-to-End

Solution

© 2010 Trajectory Group • Confidential & Proprietary 13

What value do we

deliver?

What problems are we

solving?

Which customer needs

are we satisfying?

What product bundles

are we offering each

customer segment?

For whom are we

creating value?

Who are our most

important customers?

Cu

sto

mer

Se

gm

en

t

Valu

e P

rop

os

itio

n

What type of relationship does each of

our Customer Segments expect us to

establish and maintain?

How costly are they?

How integrated with the rest of our

business?

Customer Relationship

Through which channels do we reach our

Customers?

How are our Channels integrated?

Which ones work best?

Which are the most cost effective?

Channel

How to develop, communicate, and deliver VALUE

Source: Business Model Generation:

A Handbook for Visionaries, Game

Changers, and Challengers ,

Alex Osterwalder, 2010

© 2010 Trajectory Group • Confidential & Proprietary 14

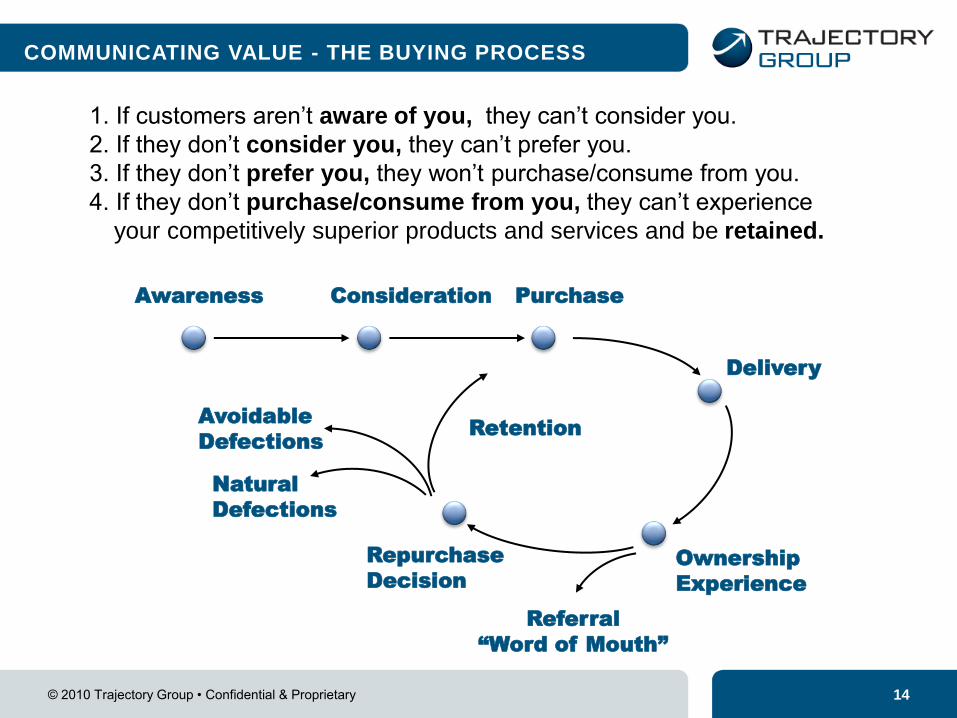

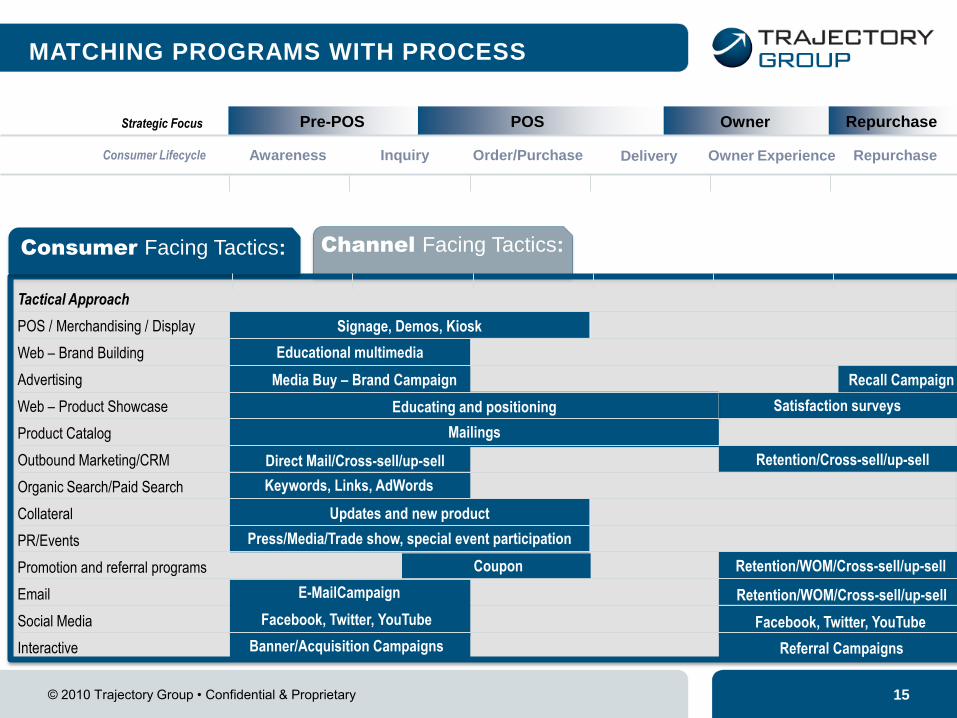

COMMUNICATING VALUE - THE BUYING PROCESS

Awareness Consideration Purchase

Delivery

Ownership

Experience

Repurchase

Decision

Retention Avoidable

Defections

Natural

Defections

Referral

“Word of Mouth”

1. If customers aren‟t aware of you, they can‟t consider you.

2. If they don‟t consider you, they can‟t prefer you.

3. If they don‟t prefer you, they won‟t purchase/consume from you.

4. If they don‟t purchase/consume from you, they can‟t experience

your competitively superior products and services and be retained.

© 2010 Trajectory Group • Confidential & Proprietary 15

Channel Facing Tactics:

Awareness Inquiry Order/Purchase Delivery Owner Experience Repurchase

Pre-POS POS Owner Repurchase

Consumer Lifecycle

Strategic Focus

MATCHING PROGRAMS WITH PROCESS

Educating and positioning

Press/Media/Trade show, special event participation

Updates and new product

Direct Mail/Cross-sell/up-sell

Keywords, Links, AdWords

Signage, Demos, Kiosk

Educational multimedia

Media Buy – Brand Campaign

Mailings

Satisfaction surveys

Tactical Approach

POS / Merchandising / Display

Web – Brand Building

Advertising

Web – Product Showcase

Product Catalog

Outbound Marketing/CRM

Organic Search/Paid Search

Collateral

PR/Events

Promotion and referral programs

Social Media

Interactive

Facebook, Twitter, YouTube Facebook, Twitter, YouTube

Retention/Cross-sell/up-sell

Retention/WOM/Cross-sell/up-sell

Banner/Acquisition Campaigns Referral Campaigns

Retention/WOM/Cross-sell/up-sell

Coupon

Consumer Facing Tactics:

Recall Campaign

E-MailCampaign

© 2010 Trajectory Group • Confidential & Proprietary 16

WHAT ABOUT SOCIAL MEDIA?

Share

Network Publish

OUTBOUND MARKETING “Interruption Marketing”

“Buy, Beg, or Bug Your Way In”

INBOUND MARKETING “Permission Marketing”

“Earn Your Way In”

Blog - SEO - Social

Fitting Social Media into the Marketing Mix:

Can’t ignore it. Have to go where the customers are!

© 2010 Trajectory Group • Confidential & Proprietary 17

© 2010 Trajectory Group • Confidential & Proprietary 18

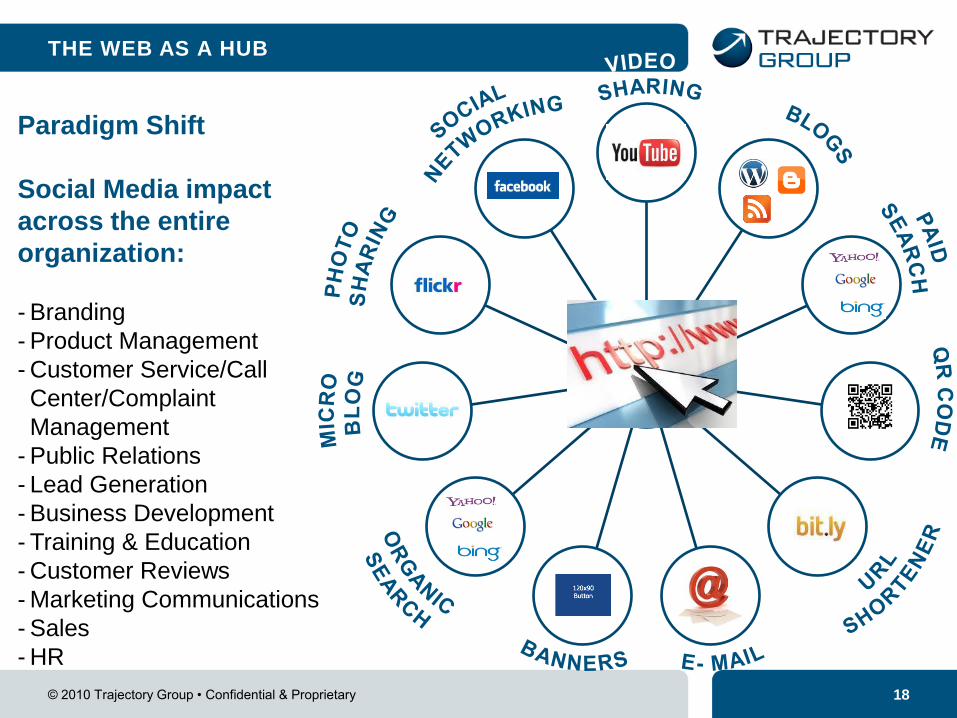

THE WEB AS A HUB

Website

Hub

Paradigm Shift

Social Media impact

across the entire

organization:

- Branding

- Product Management

- Customer Service/Call

Center/Complaint

Management

- Public Relations

- Lead Generation

- Business Development

- Training & Education

- Customer Reviews

- Marketing Communications

- Sales

- HR

© 2010 Trajectory Group • Confidential & Proprietary 19

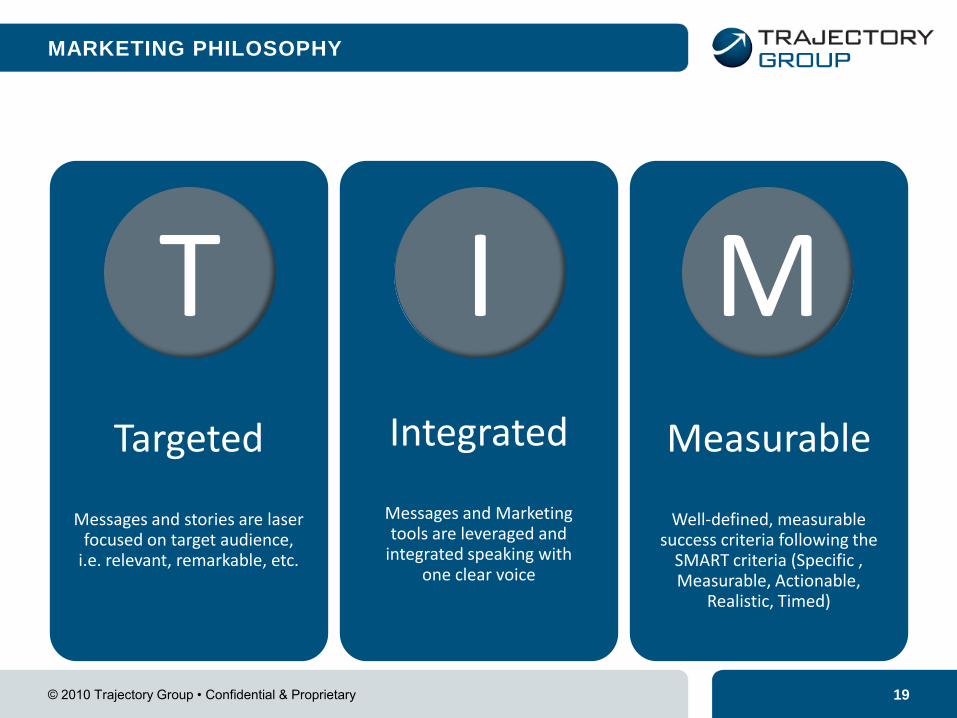

MARKETING PHILOSOPHY

Targeted

Messages and stories are laser focused on target audience,

i.e. relevant, remarkable, etc.

Integrated

Messages and Marketing tools are leveraged and

integrated speaking with one clear voice

Measurable

Well-defined, measurable success criteria following the

SMART criteria (Specific , Measurable, Actionable,

Realistic, Timed)

T I M

© 2010 Trajectory Group • Confidential & Proprietary 20

RAISING THE BAR

TOWARDS

BEST-IN-CLASS

MARKETING PROCESSES

© 2010 Trajectory Group • Confidential & Proprietary 21

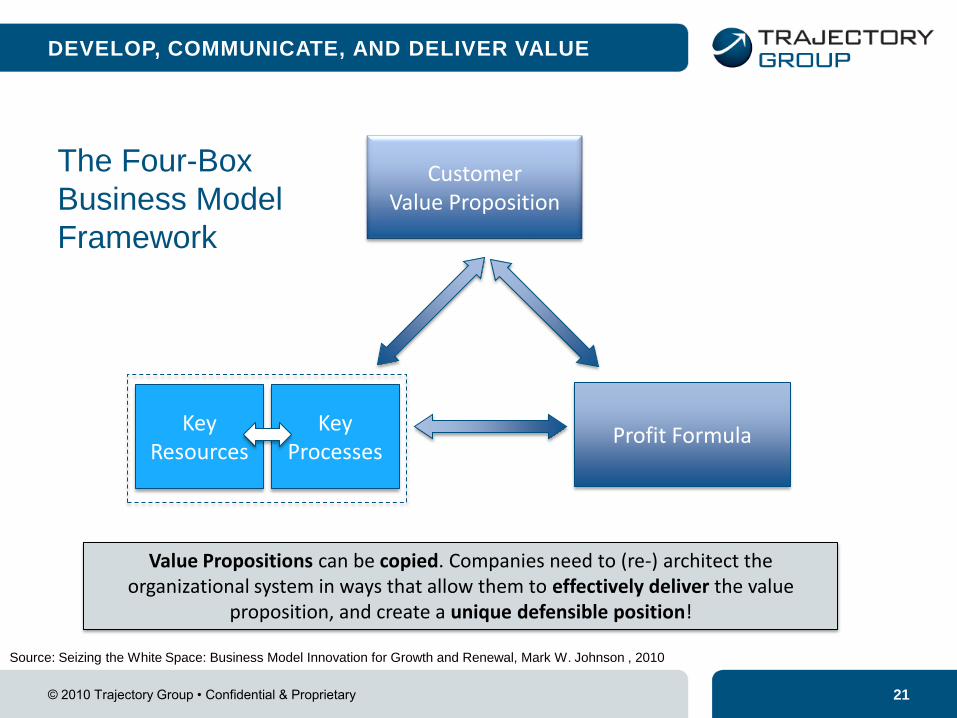

DEVELOP, COMMUNICATE, AND DELIVER VALUE

Customer Value Proposition

Profit Formula Key

Resources Key

Processes

Value Propositions can be copied. Companies need to (re-) architect the organizational system in ways that allow them to effectively deliver the value

proposition, and create a unique defensible position!

The Four-Box

Business Model

Framework

Source: Seizing the White Space: Business Model Innovation for Growth and Renewal, Mark W. Johnson , 2010

© 2010 Trajectory Group • Confidential & Proprietary 22

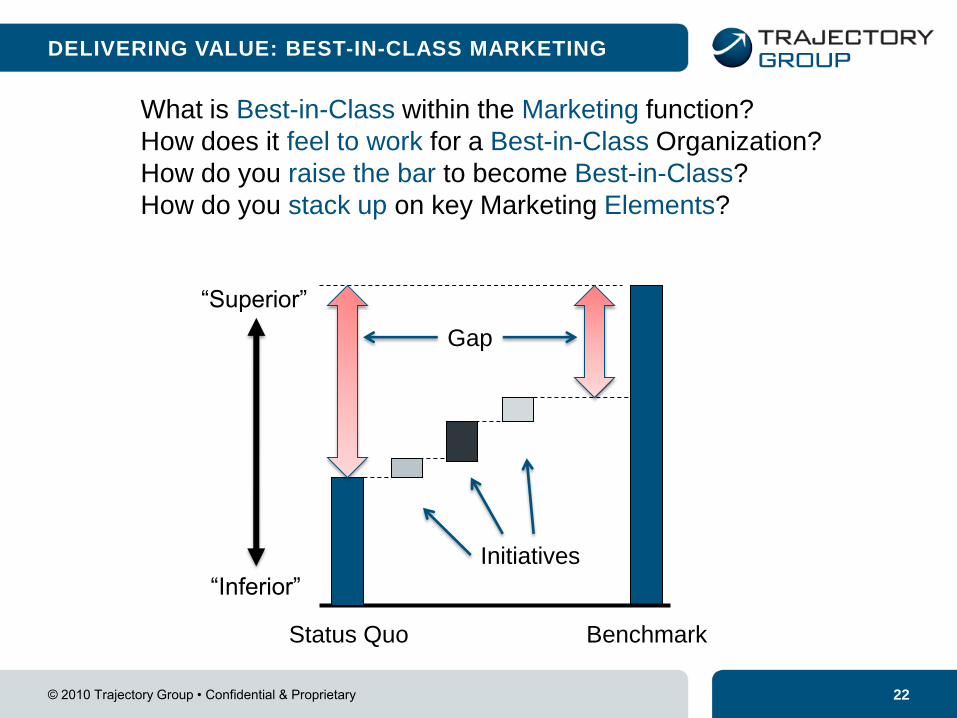

DELIVERING VALUE: BEST-IN-CLASS MARKETING

“Inferior”

“Superior”

Status Quo Benchmark

Gap

Initiatives

What is Best-in-Class within the Marketing function?

How does it feel to work for a Best-in-Class Organization?

How do you raise the bar to become Best-in-Class?

How do you stack up on key Marketing Elements?

© 2010 Trajectory Group • Confidential & Proprietary 23

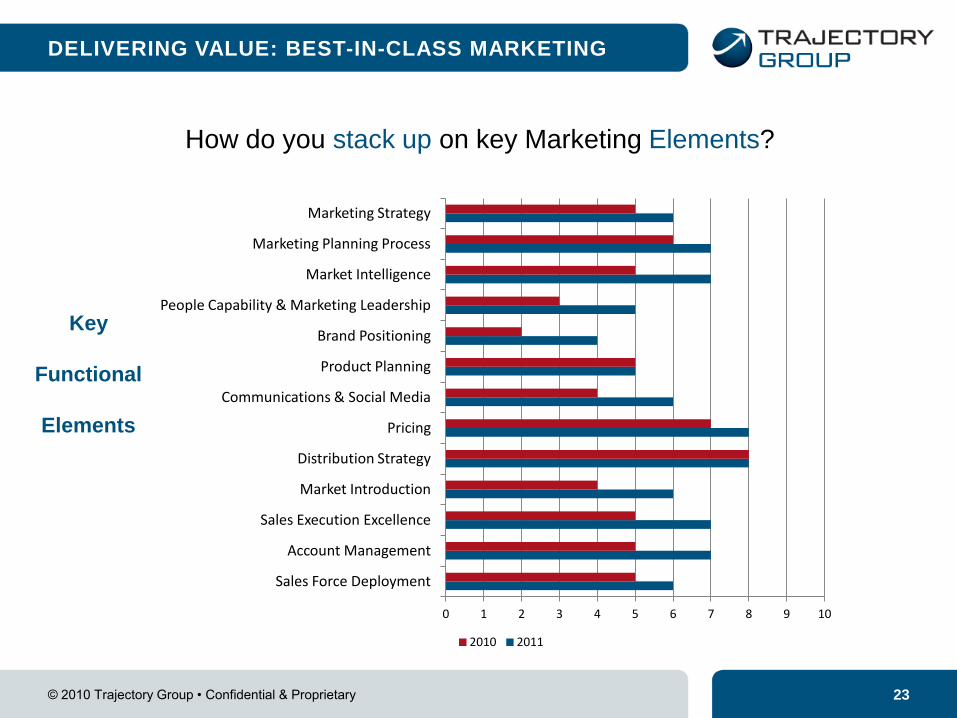

DELIVERING VALUE: BEST-IN-CLASS MARKETING

How do you stack up on key Marketing Elements?

0 1 2 3 4 5 6 7 8 9 10

Sales Force Deployment

Account Management

Sales Execution Excellence

Market Introduction

Distribution Strategy

Pricing

Communications & Social Media

Product Planning

Brand Positioning

People Capability & Marketing Leadership

Market Intelligence

Marketing Planning Process

Marketing Strategy

2010 2011

Key

Functional

Elements

© 2010 Trajectory Group • Confidential & Proprietary 24

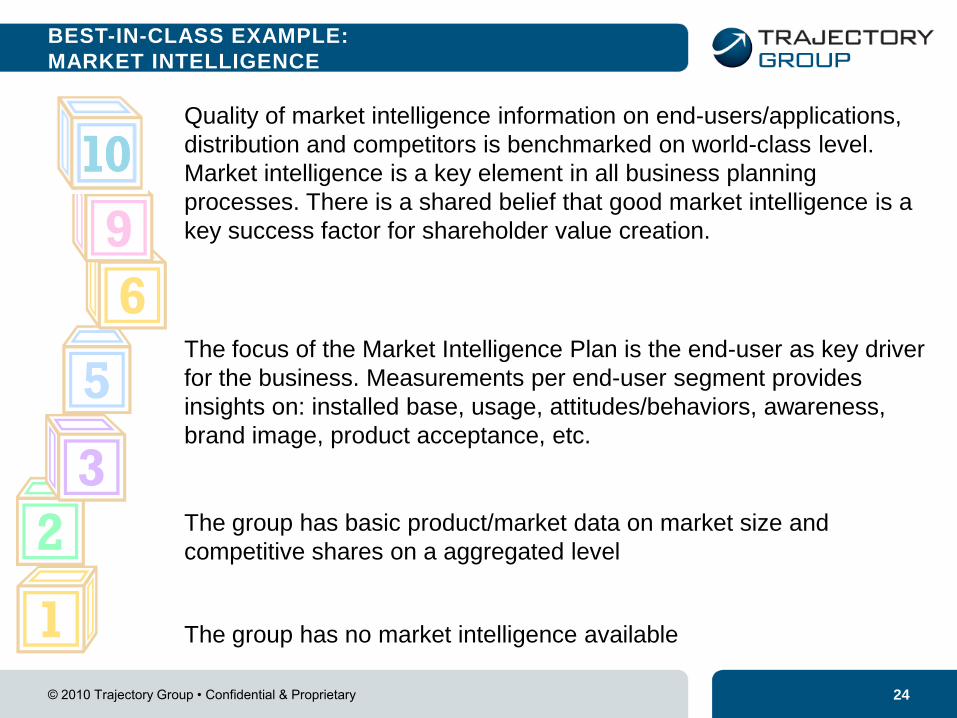

BEST-IN-CLASS EXAMPLE:

MARKET INTELLIGENCE

The group has no market intelligence available

The group has basic product/market data on market size and

competitive shares on a aggregated level

Quality of market intelligence information on end-users/applications,

distribution and competitors is benchmarked on world-class level.

Market intelligence is a key element in all business planning

processes. There is a shared belief that good market intelligence is a

key success factor for shareholder value creation.

The focus of the Market Intelligence Plan is the end-user as key driver

for the business. Measurements per end-user segment provides

insights on: installed base, usage, attitudes/behaviors, awareness,

brand image, product acceptance, etc.

© 2010 Trajectory Group • Confidential & Proprietary 25

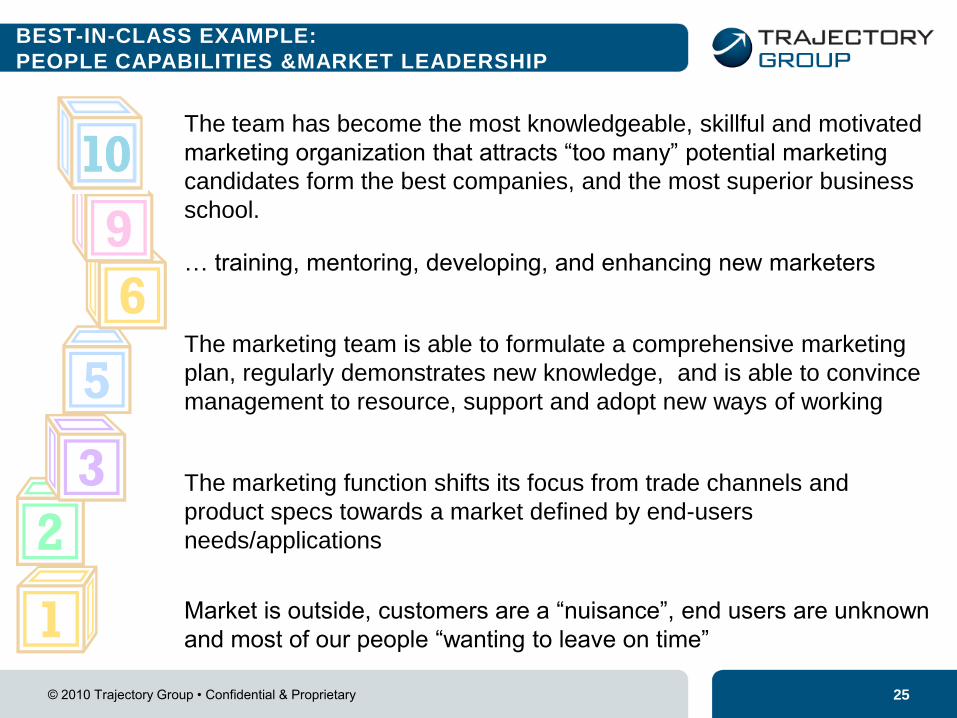

BEST-IN-CLASS EXAMPLE:

PEOPLE CAPABILITIES &MARKET LEADERSHIP

Market is outside, customers are a “nuisance”, end users are unknown

and most of our people “wanting to leave on time”

The marketing function shifts its focus from trade channels and

product specs towards a market defined by end-users

needs/applications

The team has become the most knowledgeable, skillful and motivated

marketing organization that attracts “too many” potential marketing

candidates form the best companies, and the most superior business

school.

The marketing team is able to formulate a comprehensive marketing

plan, regularly demonstrates new knowledge, and is able to convince

management to resource, support and adopt new ways of working

… training, mentoring, developing, and enhancing new marketers

© 2010 Trajectory Group • Confidential & Proprietary 26

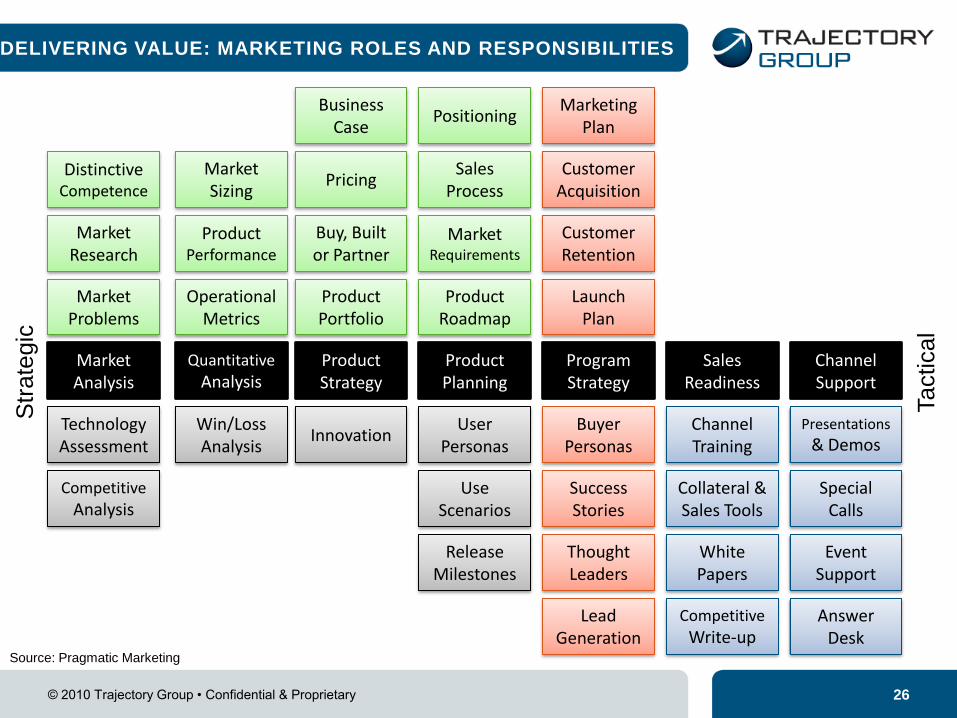

DELIVERING VALUE: MARKETING ROLES AND RESPONSIBILITIES

Quantitative

Analysis Product Strategy

Product Planning

Program Strategy

Sales Readiness

Channel Support

Product Roadmap

Market Requirements

Positioning

Sales Process

Release Milestones

User Personas

Use Scenarios

Lead Generation

Thought Leaders

Buyer Personas

Success Stories

Competitive

Write-up

White Papers

Channel Training

Collateral & Sales Tools

Answer Desk

Event Support

Presentations

& Demos

Special Calls

Launch Plan

Customer Retention

Marketing Plan

Customer Acquisition

Product Portfolio

Buy, Built or Partner

Business Case

Pricing

Operational Metrics

Product Performance

Market Sizing

Market Problems

Market Research

Distinctive Competence

Innovation Win/Loss Analysis

Technology Assessment

Competitive

Analysis

Market Analysis

Tactical

Str

ate

gic

Source: Pragmatic Marketing

© 2010 Trajectory Group • Confidential & Proprietary 27

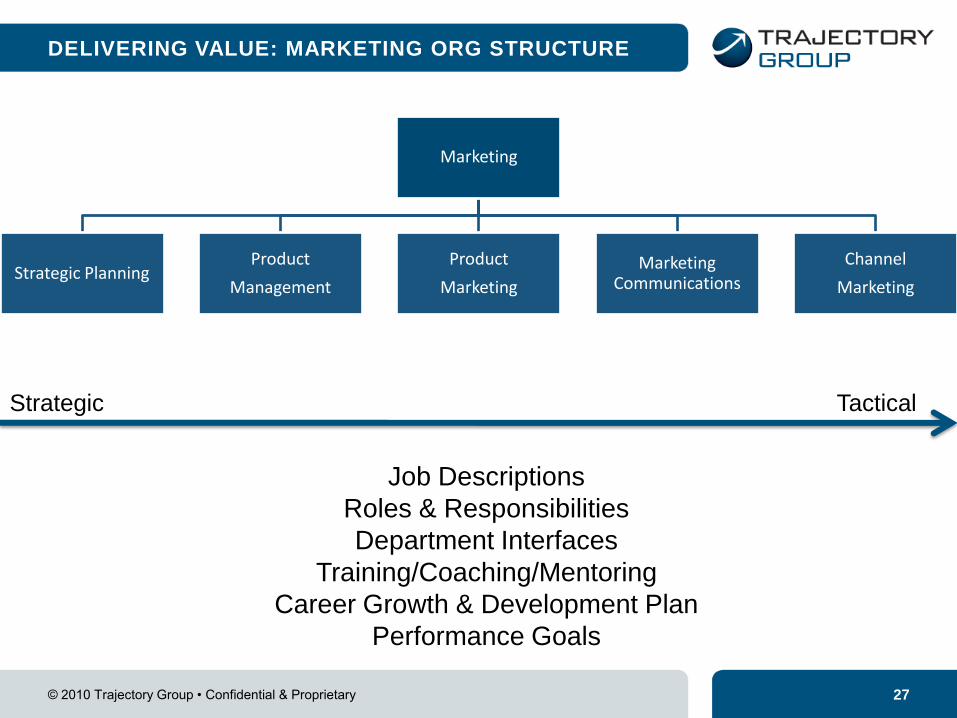

DELIVERING VALUE: MARKETING ORG STRUCTURE

Marketing

Strategic Planning Product

Management

Product

Marketing

Marketing Communications

Channel

Marketing

Job Descriptions

Roles & Responsibilities

Department Interfaces

Training/Coaching/Mentoring

Career Growth & Development Plan

Performance Goals

Strategic Tactical

© 2010 Trajectory Group • Confidential & Proprietary 28

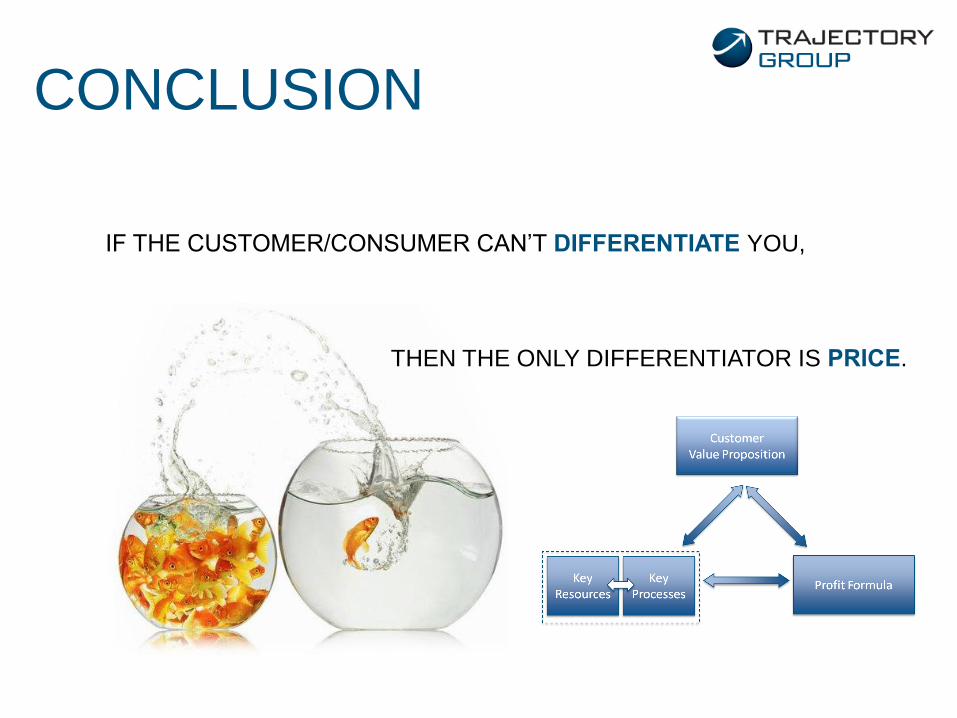

CONCLUSION

IF THE CUSTOMER/CONSUMER CAN‟T DIFFERENTIATE YOU,

THEN THE ONLY DIFFERENTIATOR IS PRICE.

© 2010 Trajectory Group • Confidential & Proprietary 29

CASE

STUDY

proprietary & confidential

Product Strategy 30

In a category where the

competition is stripping out

everything or simply adding

checkbox features, NAVIGON

delivers beyond the basics

with an experience that

truly adds value to the

end customer

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

Product Strategy 31

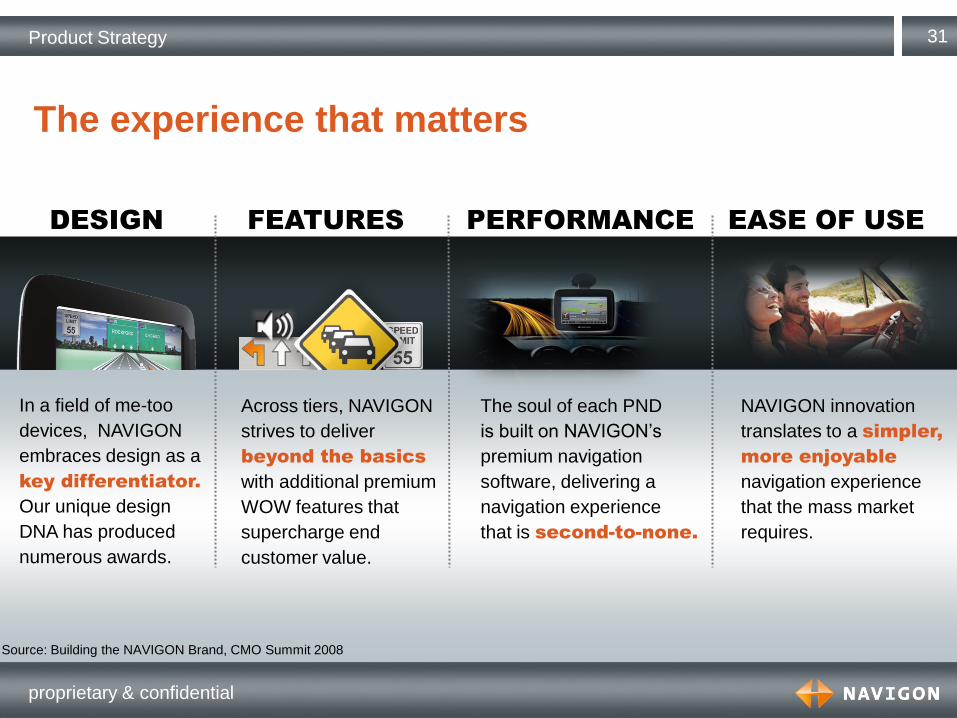

DESIGN

In a field of me-too

devices, NAVIGON

embraces design as a

key differentiator.

Our unique design

DNA has produced

numerous awards.

FEATURES

Across tiers, NAVIGON

strives to deliver

beyond the basics

with additional premium

WOW features that

supercharge end

customer value.

PERFORMANCE

The soul of each PND

is built on NAVIGON‟s

premium navigation

software, delivering a

navigation experience

that is second-to-none.

EASE OF USE

NAVIGON innovation

translates to a simpler,

more enjoyable

navigation experience

that the mass market

requires.

The experience that matters

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

Product Strategy 32

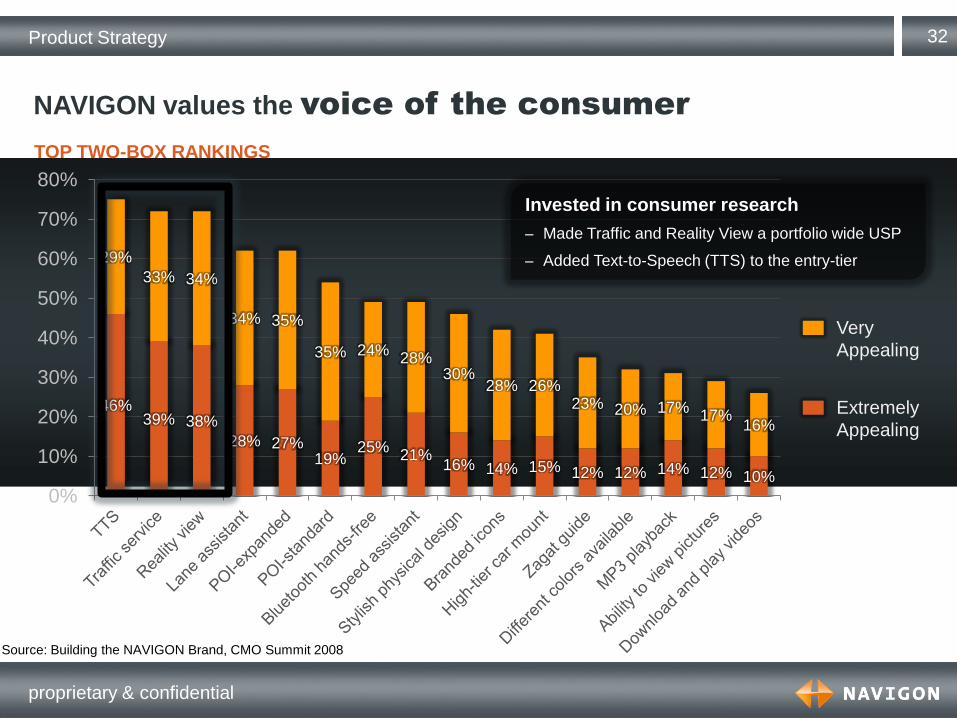

NAVIGON values the voice of the consumer

46% 39% 38%

28% 27% 19%

25% 21%

16% 14% 15% 12% 12% 14% 12% 10%

29%

33% 34%

34% 35%

35% 24% 28%

30% 28% 26%

23% 20% 17% 17%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Extremely

Appealing

Very

Appealing

TOP TWO-BOX RANKINGS

Invested in consumer research

– Made Traffic and Reality View a portfolio wide USP

– Added Text-to-Speech (TTS) to the entry-tier

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

Product Feature Spotlight 33

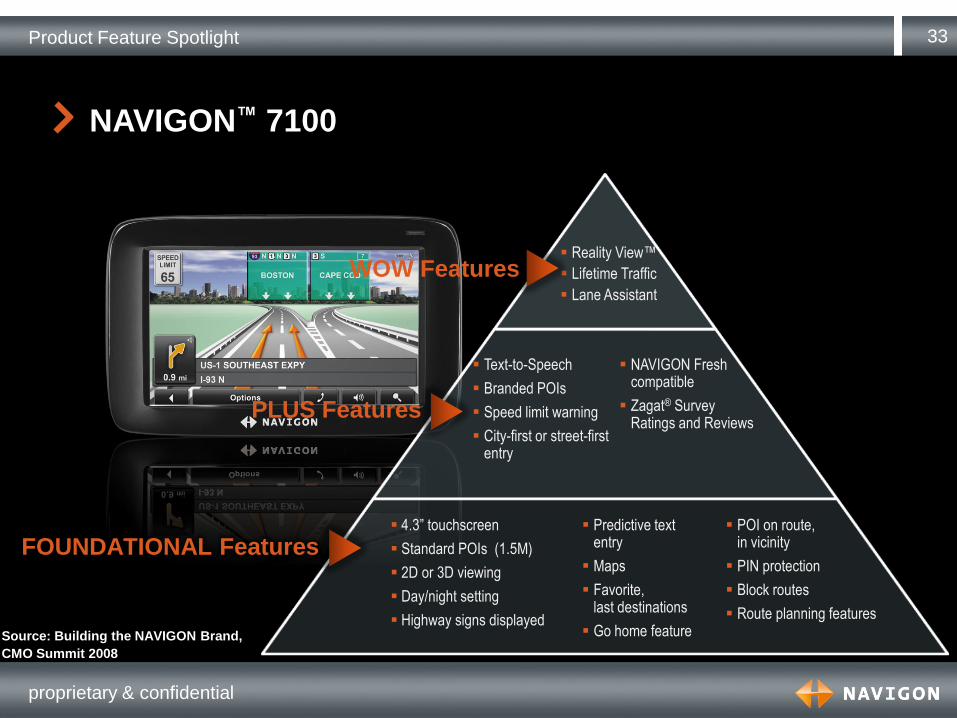

NAVIGON™ 7100

4.3” touchscreen

Standard POIs (1.5M)

2D or 3D viewing

Day/night setting

Highway signs displayed

POI on route, in vicinity

PIN protection

Block routes

Route planning features

Predictive text entry

Maps

Favorite, last destinations

Go home feature

Text-to-Speech

Branded POIs

Speed limit warning

City-first or street-first entry

NAVIGON Fresh compatible

Zagat® Survey Ratings and Reviews

Reality View™

Lifetime Traffic

Lane Assistant

WOW Features

PLUS Features

FOUNDATIONAL Features

Source: Building the NAVIGON Brand,

CMO Summit 2008

proprietary & confidential

34

2007 Product Highlights

NAVIGON® 7100

NAVIGON® 5100

NAVIGON® 2100/2120

BOLD INNOVATION

PRECISION TECHNOLOGY

AWARD-WINNING DESIGN

RELEVANT FEATURES

FOUND NOWHERE ELSE

A product portfolio that made the market take notice…

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

35 2007 Product Highlights

NAVIGON® 7100

NAVIGON® 5100

NAVIGON® 2100/2120

A product portfolio that made the market take notice…

NAVIGON® 7100 NAVIGON

® 5100 NAVIGON

® 2100/2120

Superior Experience

and Design

4.3” with all the bells and whistles Reality View™

Lifetime TrafficSM

Zagat® Survey Text–to-Speech Bluetooth®

Delivering More

for Less

3.5” with features never found at an entry-tier

Reality View™

Text-to-Speech Retail service

activations

Design Meets

Innovation

3.5” with unmatched feature set Reality View™

Lifetime TrafficSM

Zagat® Survey Text-to-Speech

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

2007 Marketing Campaign 36

Launched brand with an

integrated campaign aimed

at differentiating NAVIGON

from its competitors

TV

200M

213M

ONLINE

100M

RADIO

25M

POS

OVERALL Q4 „07

IMPRESSIONS

538M

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

TV Campaign 37

http://www.youtube.com/watch?v=MlSq-B4JAh8 Check out YouTube:

proprietary & confidential

Print Campaign 38

Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

Interactive Campaign 39

Between Oct ‟07 and Dec „07

brand campaign has sent over

400,000 users to NAVIGON‟s

microsite (experiencenavigon.com)

76% of the users (~304,000)

sent directly to channel partner

websites

Microsite: www.experiencenavigon.com Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

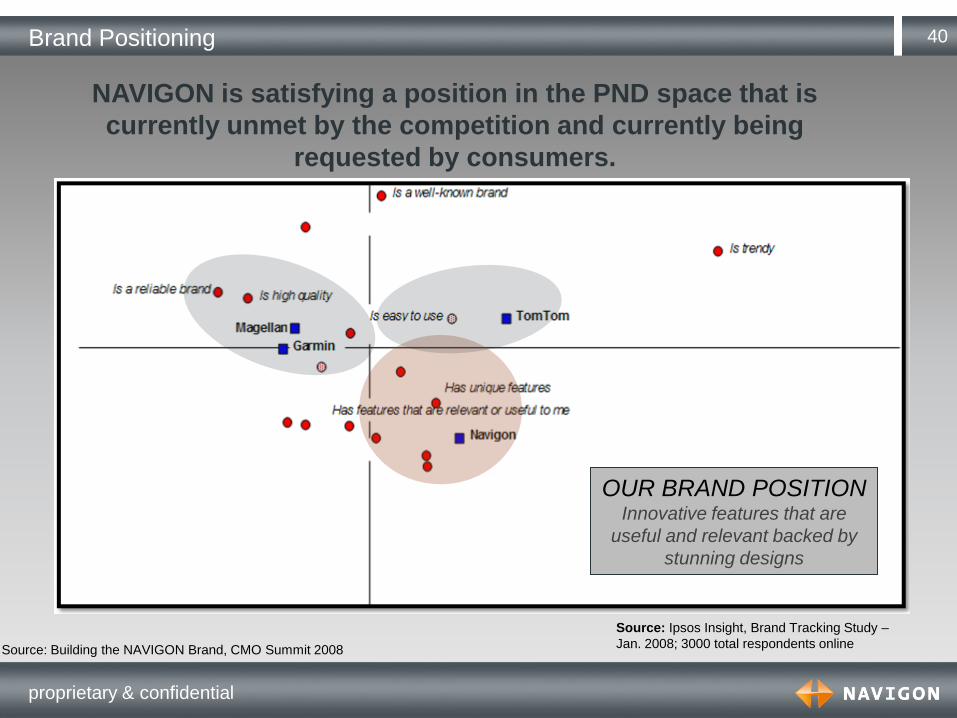

Brand Positioning 40

OUR BRAND POSITION Innovative features that are

useful and relevant backed by

stunning designs

NAVIGON is satisfying a position in the PND space that is

currently unmet by the competition and currently being

requested by consumers.

Source: Ipsos Insight, Brand Tracking Study –

Jan. 2008; 3000 total respondents online Source: Building the NAVIGON Brand, CMO Summit 2008

proprietary & confidential

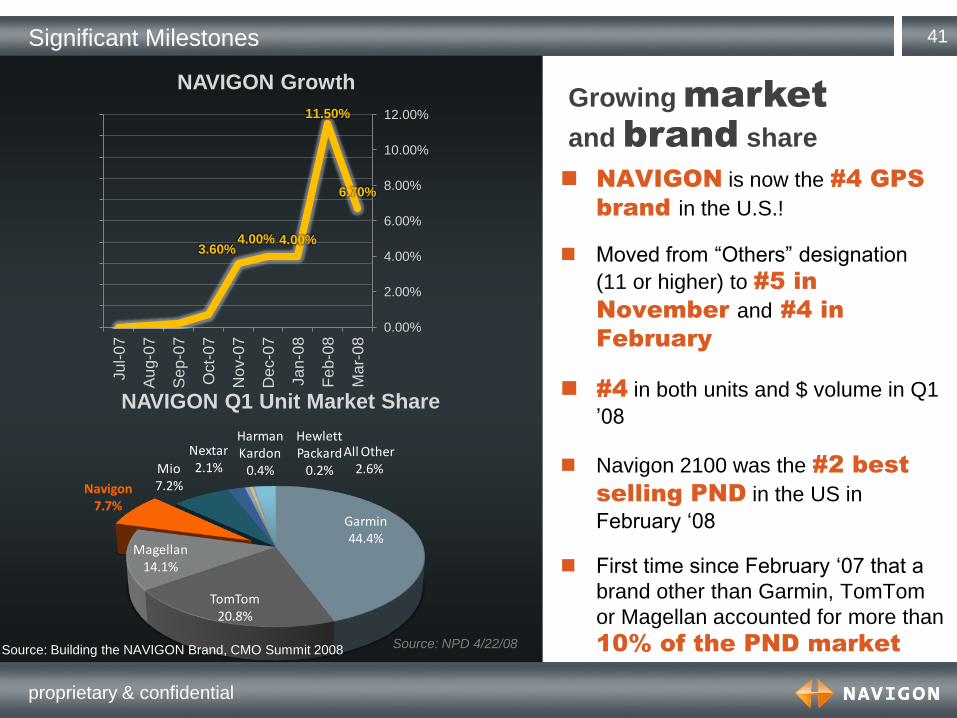

Significant Milestones 41

3.60% 4.00% 4.00%

11.50%

6.70%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00% Ju

l-0

7

Au

g-0

7

Se

p-0

7

Oct-

07

Nov-0

7

Dec-0

7

Ja

n-0

8

Fe

b-0

8

Ma

r-0

8

NAVIGON is now the #4 GPS

brand in the U.S.!

Moved from “Others” designation

(11 or higher) to #5 in

November and #4 in

February

#4 in both units and $ volume in Q1

‟08

Navigon 2100 was the #2 best

selling PND in the US in

February „08

First time since February „07 that a

brand other than Garmin, TomTom

or Magellan accounted for more than

10% of the PND market

Growing market

and brand share

NAVIGON Growth

Source: NPD 4/22/08

Garmin44.4%

TomTom20.8%

Magellan14.1%

Navigon7.7%

Mio7.2%

Nextar2.1%

Harman Kardon

0.4%

Hewlett Packard

0.2%

All Other2.6%

NAVIGON Q1 Unit Market Share

Source: Building the NAVIGON Brand, CMO Summit 2008

© 2010 Trajectory Group • Confidential & Proprietary 42

DEVELOP, COMMUNICATE, CAPTURE AND DELIVER VALUE

Customer Value Proposition

Profit Formula Key

Resources Key

Processes

Source: Seizing the White Space: Business Model Innovation for Growth and Renewal, Mark W. Johnson , 2010

© 2010 Trajectory Group • Confidential & Proprietary 43

WHAT HAPPENED TO NAVIGON?

#1 Top Grossing app in several

Countries during last 12 months

Two million smartphone apps sold

since launch in 7/2009

Expansion into Automotive

Acquired by Garmin in 2011

© 2010 Trajectory Group • Confidential & Proprietary 44 © 2010 Trajectory Group • Confidential & Proprietary 44

Ralf Hug, Founder & President

TRAJECTORY GROUP LLC

Email: [email protected]

Cell Phone: +1 773 733 6913

Skype: ralf_hug

LinkedIn: www.linkedin.com/in/ralfhug

Slideshare: www.slideshare.net/ralfhug

Twitter: @ralfhug

Questions? Please contact me at:

© 2010 Trajectory Group • Confidential & Proprietary 45

TRAJECTORY GROUP OVERVIEW

Ralf Hug Founder & President

15 Years of Global Management

Experience

Expertise in Strategy Development,

Business Development, Marketing and

Product Management

In-depth Industry Experience in

Automotive, Telematics, M2M, GPS/LBS,

Wireless, CE and Connected TV

MBA University of Bayreuth, Germany

Past Management Positions at:

Business development and strategic

advisory services firm with the very

specific conviction to help companies

to stay on the trajectory of success

Services include:

o Management Advisory

o Marketing Strategy and Planning

o Inbound and Outbound Marketing

o Business Development

o Product Strategy and Launch

o Interim Management

Deep Industry Expertise in:

o Automotive /Telematics/M2M

o GPS/LBS/Wireless/Apps

o Content/Media/Services

o CE/Connected TV

TRACTECORY GROUP LLC

Trajectory [trə′jektrē]: Plotting a realistic path

towards achieving a target over a period of time

© 2010 Trajectory Group • Confidential & Proprietary 46

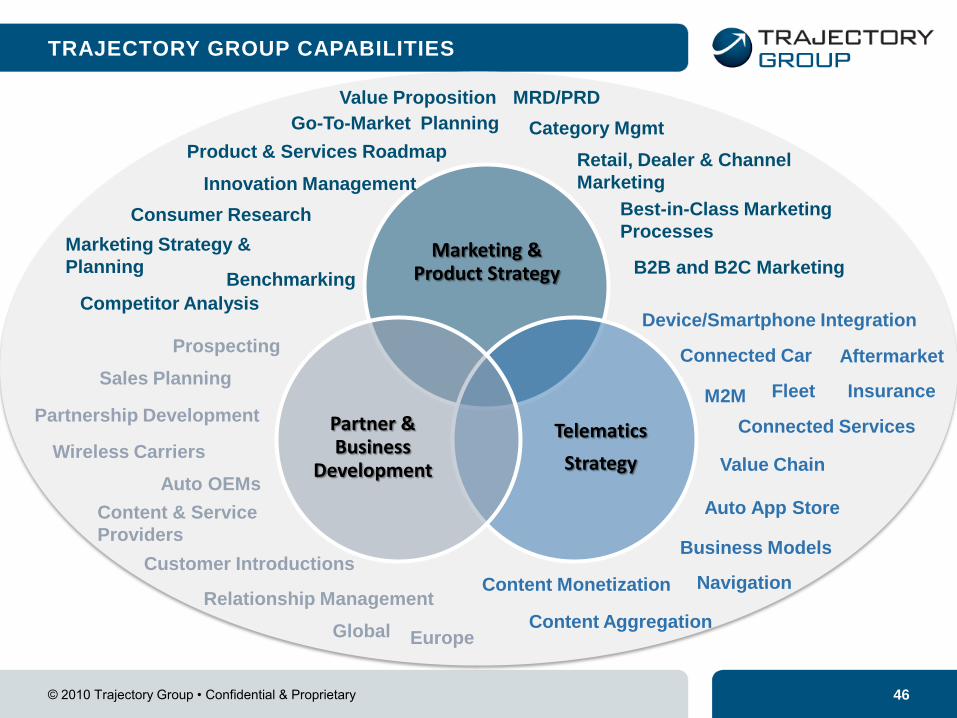

TRAJECTORY GROUP CAPABILITIES

Marketing & Product Strategy

Telematics

Strategy

Partner & Business

Development

M2M

Auto App Store

Value Chain

Business Models

Connected Car

Connected Services

Navigation

MRD/PRD

Consumer Research

Product & Services Roadmap

Best-in-Class Marketing

Processes

Content Aggregation Global

B2B and B2C Marketing Benchmarking

Content & Service

Providers

Retail, Dealer & Channel

Marketing

Content Monetization

Device/Smartphone Integration

Marketing Strategy &

Planning

Go-To-Market Planning

Prospecting

Sales Planning

Customer Introductions

Partnership Development

Relationship Management

Competitor Analysis

Value Proposition

Innovation Management

Fleet Insurance

Aftermarket

Auto OEMs

Wireless Carriers

Category Mgmt

Europe

© 2010 Trajectory Group • Confidential & Proprietary 47

BONUS DOCUMENTS ON SLIDESHARE

Presentation:

“The Connected Car

Comes in Many Flavors”

Article:

“To Find the Business Case for Telematics, Look Higher Up.”

http://slidesha.re/hkpRkW

http://slidesha.re/bFCv3V

Presentation: “Envision Automotive App Stores – Key Questions”

http://slidesha.re/eWnh0n

http://slidesha.re/hvKezS

Check out Ralf Hug SlideShare Channel