Embed Size (px)

Citation preview

14/08/2012

1

From “Sickman” to “New Tiger”

The Philippine Economy in an Asian Perspective

Norio Usui

Philippines Country Office

ASCEND Forum, 23 August, 2012

Presentation

Question 1

– How can we assess the Philippine economy?

– From “Sickman” to “Next Tiger” A real story?

Question 2

– How inclusive the past growth was?

– What can we do to make the growth more inclusive? What are missing here?

How can we assess the recent jump? Surprising 6.4% growth in Q1, 2012

2012

4.9 3.6 3.2 4.0

6.4

-15

-10

-5

0

5

10

15

20

25

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Private Consumption Government Consumption Capital Formation

Exports Imports Statistical Discrepancy

GDP

2009 2010 2011 2008

%

Strong private consumption backed by remittances and lower inflation

2.9

-

1

2

3

4

5

6

Jan-1

1

Feb

Mar

Ap

r

May

Jun

e

July

Au

g

Sep

Oct

No

v

Dec

Jan-1

2

Feb

Mar

Ap

r

May

Food and Non-Alcoholic Beverages Fuel, light, water Transport Others Headline Inflation

%

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010

Asia Americas

Middle East Europe

Others

$ billion Remittance inflows Inflation

Slowdown of investment? Significant 23.5% drop in Q1, 2012

Peso million (constant prices)

TYPE OF EXPENDITURE Q1 2011 Q1 2012 Growth (%)

Capital Formation 333,866 255,556 -23.5

Fixed Capital 319,949 328,887 2.8

Construction 108,012 108,290 0.3

Durable Equipment 179,019 185,428 3.6

Breeding Stock & Orchard Dev't 26,808 27,103 1.1

Intellectual Property Products 6,110 8,066 32.0

Changes in Inventories 13,917 -73,331

Construction Is private construction really weak?

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1 2011 Q1 2012

Public Private

↓ 9.9%

↑62.2%

↑ 0.3%

Peso million (constant prices)

6.6

-9.9

-60

-40

-20

0

20

40

60

80

Mar-07

Au

g-07

Jan-08

Jun

-08

No

v-08

Ap

r-09

Sep-0

9

Feb-10

Jul-10

Dec-10

May-1

1

Oct-1

1

Mar-12

Building permit issued

Private construction (GVA)

Building permit and Private construction

%

14/08/2012

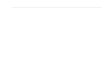

2

Monthly infrastructure spending

(Peso billion)

Infrastructure spending 2011 vs 2012 Program

(Peso billion)

0

5

10

15

20

25

30

35

40

45

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012

0

50

100

150

200

250

300

Jan Apr May-Dec *

2012 2011 * 2012 Program

Public infrastructure spending can further increase

Investment in durable equipment remains strong

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Q1 2011 Q1 2012

Miscellaneous equipment Transport Equipment General Industrial Machinery and Equipment Machinery specialized for particular Industries

↑ 3.6%

↑ 15.2%

↓ 18.9%

↓ 5.2%

Peso million (constant prices)

↑ 10.2%

-10

0

10

20

30

40

50

60

70

20

07

Q1

Q

2

Q3

Q

4

Q1

20

08

Q

2

Q3

Q

4

Q1

20

09

Q

2

Q3

Q

4

Q1

20

10

Q

2

Q3

Q

4

Q1

20

11

Q

2

Q3

Q

4

Q1

20

12

Q

2 2

01

2

Business Outlook

-60

-40

-20

0

20

40

60

80

100

Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Ja

n-1

2

Ap

r-1

2

Global Semiconductor Sales Philippines' Semiconductor Exports

Sign of export recovery?

Global semiconductor sales

Philippines’ semiconductor export

Philippines’ exports ($ billion)

Global semiconductor sales and Philippines’ semiconductor exports

(% change, year-on-year)

0

1

2

3

4

5

6

Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Ja

n-1

2

Ap

r-1

2

Total exports Electronics Semiconductors

Now exports has been declining even in your neighbors

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

Jan-07

Ap

r-07

Jul-07

Oct-07

Jan-08

Ap

r-08

Jul-08

Oct-08

Jan-09

Ap

r-09

Jul-09

Oct-09

Jan-10

Ap

r-10

Jul-10

Oct-10

Jan-11

Ap

r-11

Jul-11

Oct-11

Jan-12

Ap

r-12

INO THA MAL PHI

%

Recent economic situation Returning to the potential growth rate?

PDP target: 7-8%

1.1

7.6

3.9

5.0

-4

-2

0

2

4

6

8

10

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Potential growth (HP Filter) Actual growth

% GDP growth in the past 5 decades

(annual average, %)

4.9

5.9

1.7

2.9

4.8

0

1

2

3

4

5

6

7

1960s 1970s 1980s 1990s 2000s

Solid growth over the 2000s

14/08/2012

3

Let it be….

Let it be, let it be

Let it be, let it be

There will be an answer

Let it be

Let it be, let it be

Let it be, let it be

Whisper words of wisdom

Let it be

Policy Option I don’t think so. Why?

Structural weaknesses

– Weak link between growth and development

– Rising growth and declining investment

– Limited diversification of exports

Long-term development puzzle

Sector Contributions to GDP Growth (1980-2009, %)

Your growth has depended more on services

13.2 18.8

24.1 27.0

15.4 14.5 10.3

19.6

30.4

41.5 38.7

59.5

32.8

50.3

18.9

38.9

0

20

40

60

80

100

1980 2009 1980 2009 1980 2009 1980 2009

Indonesia Malaysia Philippines Thailand

Industry Services

Employment Shares (1980 and 2009, % of total employment)

50.1 49.4

26.3

48.3

38.5 43.5

66.6

43.2

11.4 7.2 7.1 8.6

0

20

40

60

80

100

INO MAL PHI THA

Industry Services Agriculture

0

2,500

5,000

7,500

10,000

12,500

0

1,500

3,000

4,500

6,000

7,500

1980 1985 1990 1995 2000 2005

Indonesia Philippines Thailand

Malaysia Viet Nam

Economy-wide labor productivity 1980-2009

Constant 2000 $

MAL (RHS)

THA

INO

PHI

VIE

71.3

105.6

-1.8

77.8

35.8

9.0

12.2

98.2

-50

0

50

100

150

200

Indonesia Malaysia Philippines Thailand

Sectoral productivity growth

Structural transfromation

Growth Decomposition

Sector productivity and labor shift

0

2,000

4,000

6,000

8,000

10,000

12,000

Agriculture Industry Services Manufacturing

0

2,000

4,000

6,000

8,000

10,000

12,000

Agriculture Industry Services Manufacturing

0

10

20

30

40

50

60

70

80

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

0

10

20

30

40

50

60

70

80

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

Employment by sector

Labor productivity by sector

Growing business process outsourcing

5,288

7,717

0

4

8

12

16

20

0

2,000

4,000

6,000

8,000

10,000

2004 2005 2006 2007 2008 2009

Contact Center

Transcription

Animation

Software Development

Other BPOs

% of total export of goods & services (RHS)

355,135

444,811

0.0

0.4

0.8

1.2

1.6

2.0

0

100,000

200,000

300,000

400,000

500,000

2004 2005 2006 2007 2008 2009

Contact Center

Transcription

Animation

Software Development

Other BPOs

% of total labor force (RHS)

Export (million $) Employment (persons)

14/08/2012

4

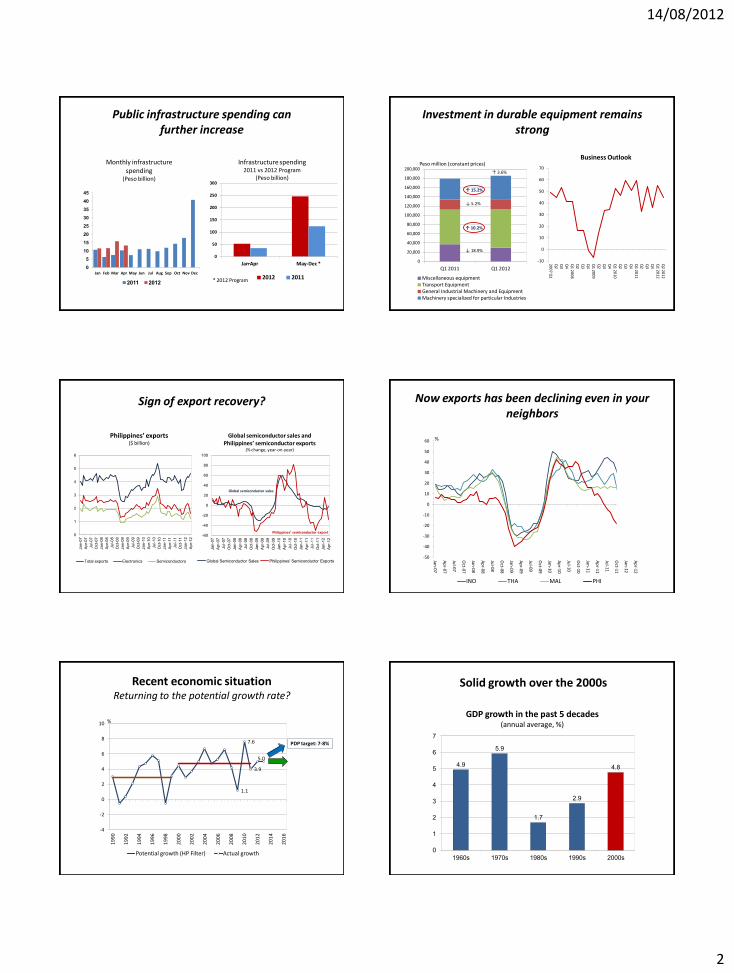

You need to create jobs for further increasing workforce

26.0

94.9

23.7

38.7

0

10

20

30

40

50

60

70

80

90

100

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

Population, total Labor force, total

3.15

2.87 2.73

2.29

1.89

2.70

2.26

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

60s 70s 80s 90s 00s

Population Labor force

(million) (average annual %)

Population Population Growth Rate

Country

Capabilities

Products

“LegoLego” and Development

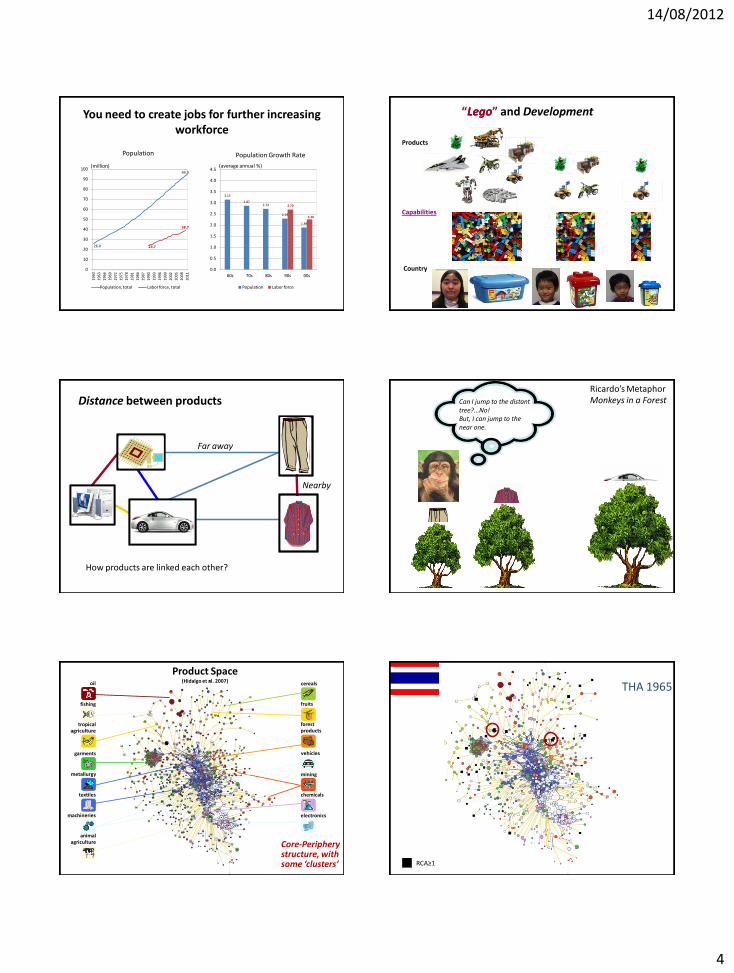

Distance between products

Nearby

Far away

How products are linked each other?

Ricardo’s Metaphor Monkeys in a Forest Can I jump to the distant

tree?...No! But, I can jump to the near one.

oil

fishing

agriculture tropical

garments

metallurgy

textiles

agriculture animal

machineries

fruits

cereals

vehicles

electronics

chemicals

mining

products forest

Product Space (Hidalgo et al. 2007)

Core-Periphery structure, with some ‘clusters’

THA 1965

RCA≥1

14/08/2012

5

THA 1975 THA 1985

THA 1995 THA 2005

THA 2008 PHL 1965

RCA≥1

14/08/2012

6

PHL 1975 PHL 1985

PHL 1995 PHL 2005

PHL 2008 How many of your products have comparative

advantage?

35

0

74

4

134

21

132

34

91

29

110

40

0

25

50

75

100

125

150

175

200

core core core core core core

1965 1975 1985 1995 2005 2008

51

2

84

9

159

12

183

46

179

63

186

70

0

25

50

75

100

125

150

175

200

core core core core core core

1965 1975 1985 1995 2005 2008

14/08/2012

7

Assessment - Summing up -

• The past growth has been largely led by services

• Lagged growth is rooted in persistent productivity growth deficit due to stagnant industrialization, in particular lack of product diversification

• Limited job opportunities resulted in the slow poverty reduction

• The service-led growth did not require a relatively high investment

• Booming BPOs create jobs, but its impact is limited given the scale of utilized workforce, and its bias toward educated labor

• To join the growth club in the region and translate the growth into inclusive one, the country needs to “walk on two legs” both in industry and modern services

How can we help entrepreneurs jump to new products?

• Resolving long-standing issues:

– Infrastructure

– Business and investment climate

• Horizontal interventions: Is that all?

• Critical importance of focusing on product-specific constraints

High electricity price Is it a real headache for all?

Share of electricity cost in total production cost (including labor cost, depreciation, net tax)

1: Ave: 0.79

3: Ave: 4.63

2: Ave: 7.67

4: Ave: 0.27 5: Ave: 3.86 6: Ave: 0.57 7: Ave: 5.33 8: Ave: 2.42 9: Ave: 0.48 11: Ave: 0.99

10: Ave: 3.77

Manufacturing

Electronics…….have you fully exploited the opportunities?

RCA≥1

RCA<1

Targeted Public Sector Support - My Proposal -

Headache 1: Product identification (targeting)

Headache 2: Diagnostics of binding constraints for the targeted products

How can we “choose”?

Key dimensions of product identification

Easiness to jump: Nearby? Middle? Far Away?

– Above average sophistication (direct effect)

– Opportunities for further structural change (spillover effects)

– Capacity to absorb labor (job creation)

– Others such as global demand growth

14/08/2012

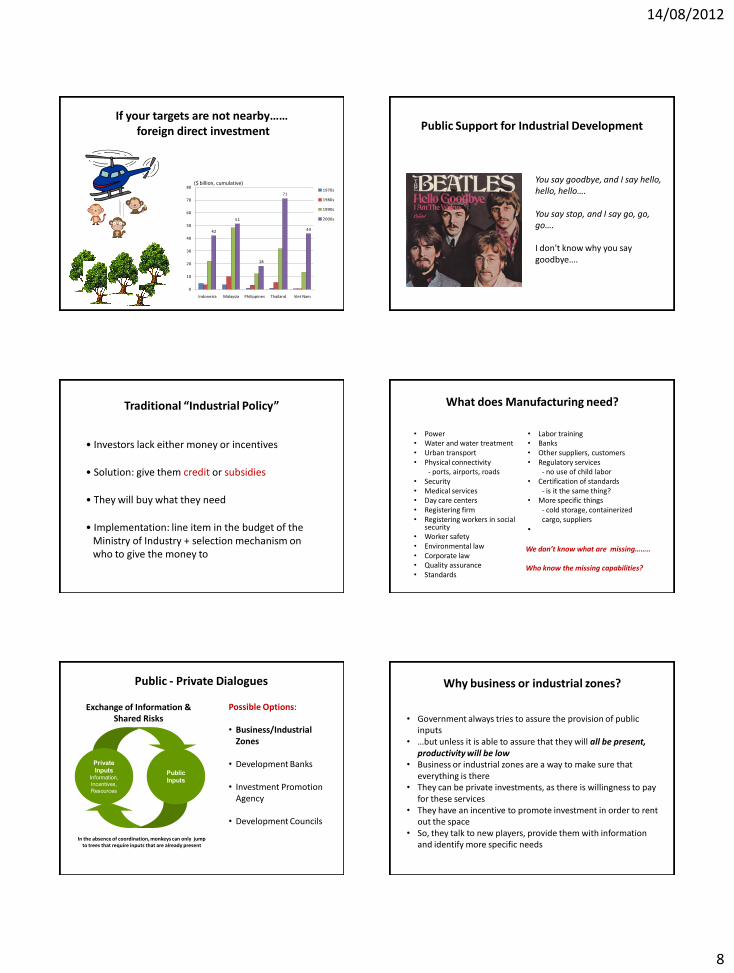

8

If your targets are not nearby…… foreign direct investment

42

51

18

71

43

0

10

20

30

40

50

60

70

80

Indonesia Malaysia Philippines Thailand Viet Nam

1970s

1980s

1990s

2000s

($ billion, cumulative) You say goodbye, and I say hello, hello, hello…. You say stop, and I say go, go, go…. I don't know why you say goodbye….

Public Support for Industrial Development

Traditional “Industrial Policy”

• Investors lack either money or incentives

• Solution: give them credit or subsidies

• They will buy what they need

• Implementation: line item in the budget of the Ministry of Industry + selection mechanism on who to give the money to

What does Manufacturing need?

• Power • Water and water treatment • Urban transport • Physical connectivity

- ports, airports, roads • Security • Medical services • Day care centers • Registering firm • Registering workers in social

security • Worker safety • Environmental law • Corporate law • Quality assurance • Standards

• Labor training • Banks • Other suppliers, customers • Regulatory services

- no use of child labor • Certification of standards

- is it the same thing? • More specific things

- cold storage, containerized cargo, suppliers

•

We don’t know what are missing…….. Who know the missing capabilities?

Public - Private Dialogues

Private

Inputs Information,

Incentives,

Resources

Public

Inputs

Exchange of Information & Shared Risks

In the absence of coordination, monkeys can only jump to trees that require inputs that are already present

Possible Options: • Business/Industrial

Zones

• Development Banks

• Investment Promotion Agency

• Development Councils

Why business or industrial zones?

• Government always tries to assure the provision of public inputs

• …but unless it is able to assure that they will all be present, productivity will be low

• Business or industrial zones are a way to make sure that everything is there

• They can be private investments, as there is willingness to pay for these services

• They have an incentive to promote investment in order to rent out the space

• So, they talk to new players, provide them with information and identify more specific needs

14/08/2012

9

You already have enough information sources Coordination within the Government

Public and Private Dialogues Identifying product specific constraints:

Port infrastructure Road system Cold-storage facilities Phytosanitary regulations Market access agreements etc.

Who can resolve the identified problems? DTI alone cannot resolve the identified problems!

Are your concerned for possible failures?

• What we are thinking are “risk-taking entrepreneurial decisions”

• Private firms try to picking winners all the time, and often failed

• Failures are inevitable in any risk taking decision

• The real question is how improve “batting average”

Won: 54 (KO 38) Lost: 4 (KO 2) Drawn: 2 KO%: 63.3

A Boxer

A Basketball Player

0.497

0.400

0.450

0.500

0.550

0.600

21 22 23 24 25 26 27 28 29 31 32 33 34 38 39 age

FG%

What can we do to improve the batting average?

Sunset clauses

Exit strategies

Clear objectives

Cost recovery

Performance indicators

Simple design

Monitoring & evaluation mechanisms

Flexibility to adjust

Stakeholder consultation & participation

14/08/2012

10

Hey Jude, begin

You're waiting for someone to perform with

And don't you know that it's just you

Hey Jude, you'll do

The movement you need is on your shoulder

Hey Jude….

Thank you

The findings, interpretations, and views expressed are entirely those of the author, and do not necessarily represent the views of the Asian Development Bank, its executive directors, or the countries they represent.

For further information, please contact: Norio Usui ([email protected])

Philippine Country Office, Asian Development Bank

Limited job opportunities and persistent poverty

Series break

7.1*

19.1*

-

5

10

15

20

25

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Unemployment Underemployment

Slow Poverty Reduction (%, poverty incidence)

33.1

24.9 26.4 26.5

28.3

20.1 21.1 20.9

0

10

20

30

40

1991 2003 2006 2009

by Population by Families

Weak Labor Market Indicators (% of total labor force)

*Average: Jan-April 2012

Rising Growth and Declining Investment

22.1

20.8 20.6 20.7

20.3

19.9 20.1

19.9 19.7

19.0

20.5

19.3

16

18

20

22

24

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nominal gross fixed capital formation (% of GDP)

Long-term growth puzzle

Real GDP per capita 1960 (constant 2000 $)

Real GDP per capita 1960 – 2010 (constant 2000 $)

Once upon a time……. After five decades…….

105 145

201

1,154

813

692

321

0

200

400

600

800

1,000

1,200

1,400

PR

C

Ind

ia

Ind

on

esi

a

Kore

a, R

ep.

Mal

aysi

a

Ph

ilip

pin

es

Th

aila

nd

0

1,000

2,000

3,000

4,000

5,000

6,000

196

0

196

5

197

0

197

5

198

0

198

5

199

0

199

5

200

0

200

5

201

0

China India Indonesia

Malaysia Philippines Thailand

Vietnam

Producing (& exporting) mango requires: • a certain type of soil • mechanized farming equipment • agribusinesses firms that know the market,

etc.,

but also “public goods” such as: • specific property rights • port infrastructure • road system • cold-storage facilities • phytosanitary regulations • market access agreements, etc.

Capabilities

14/08/2012

11

Your export basket Your capabilities What can you make with the

available capabilities?

Product Identification Where do you want to go?

Nearby Middle Far away

For example, if you want to choose “sophisticated products”

Export

value

(M US$)

7522 Complete digital data processing machines Machinery 28,109 3,403 1.347 0.327 164.24 0.74 24.76

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.16 20.84 0.238 -7.89

7622 Portable radio receivers Machinery 13,995 3,808 0.957 0.034 0.61 0.034 -1.67

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

7512 Calculating, accounting, cash registers, ticketing, etc, machines Machinery 13,485 8,199 0.383 0.031 0.72 0.036 2.96

0344 Fish fillets, frozen Animal products 13,286 5,413 1.611 0.762 44.87 0.09 12.67

0612 Refined sugar etc Tropical Agruculture 12,595 7,539 0.647 0.008 0.33 0.063 12.59

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

0814 Flours and meals, of meat, fish,etc, unfit for human; greaves Cereals 11,284 4,220 1.022 0.152 3.25 0.031 6.67

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

7757 Domestic electro-mechanical appliances; and parts thereof, nes Machinery 10,866 8,559 0.505 0.092 8.02 0.142 11.13

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

Table 1.2: Ranked based on Strategic Value

Export

value

(M US$)

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

6674 Synthetic or reconstructed precious or semi-precious stones Labor intensive 10,643 8,688 16.177 0.070 0.20 0.004 3.05

7757 Domestic electro-mechanical appliances; and parts thereof, nes Machinery 10,866 8,559 0.505 0.092 8.02 0.142 11.13

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.160 20.84 0.238 -7.89

8998 Small-wares and toilet articles, nes; sieves; tailors' dummies, etc Labor intensive 10,275 8,317 3.547 0.272 7.47 0.043 7.24

7512 Calculating, accounting, cash registers, ticketing, etc, machines Machinery 13,485 8,199 0.383 0.031 0.72 0.036 2.96

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

0612 Refined sugar etc Tropical Agruculture 12,595 7,539 0.647 0.008 0.33 0.063 12.59

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

6552 Knitted, not elastic nor rubberized, of fibres other than synthetic Capital intensive 10,446 7,267 4.594 0.142 11.15 0.125 14.25

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

1124 Distilled alcoholic beverages, nes Tropical Agruculture 10,808 6,214 0.473 0.170 18.91 0.172 10.77

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

High opportunities for further structural change

Table 1.3: Ranked based on Labor Intensity

Export

value

(M US$)

6674 Synthetic or reconstructed precious or semi-precious stones Labor intensive 10,643 8,688 16.177 0.070 0.20 0.004 3.05

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

6552 Knitted, not elastic nor rubberized, of fibres other than synthetic Capital intensive 10,446 7,267 4.594 0.142 11.15 0.125 14.25

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

8998 Small-wares and toilet articles, nes; sieves; tailors' dummies, etc Labor intensive 10,275 8,317 3.547 0.272 7.47 0.043 7.24

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

0344 Fish fillets, frozen Animal products 13,286 5,413 1.611 0.762 44.87 0.090 12.67

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

7522 Complete digital data processing machines Machinery 28,109 3,403 1.347 0.327 164.24 0.740 24.76

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.160 20.84 0.238 -7.89

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

0814 Flours and meals, of meat, fish,etc, unfit for human; greaves Cereals 11,284 4,220 1.022 0.152 3.25 0.031 6.67

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

7622 Portable radio receivers Machinery 13,995 3,808 0.957 0.034 0.61 0.034 -1.67

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

High labor absorption