Embed Size (px)

Citation preview

Factbase

Conducted by Navigate Australia

Dairy Globalization: 2011 Update

Commissioned by Lion Nathan Australia

FINAL May 21, 2011

Contents

•Project objectives and summary findings

•Geography-specific findings

-Net importers

-Net exporters

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

3

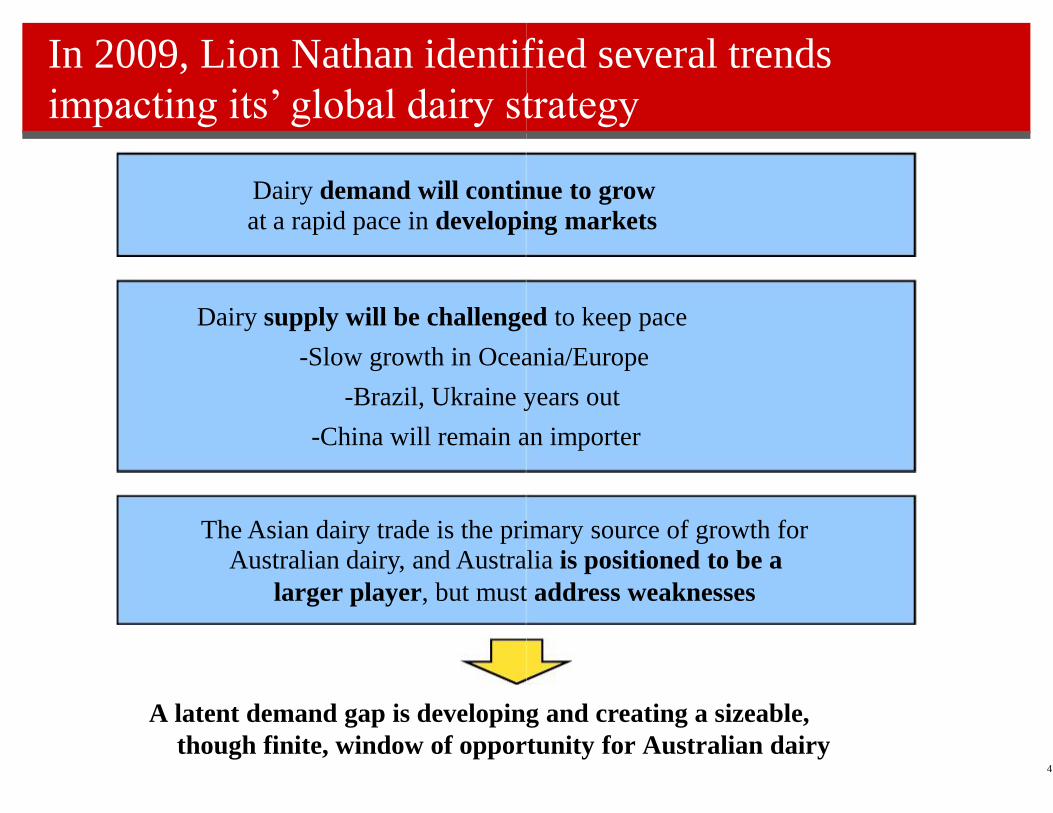

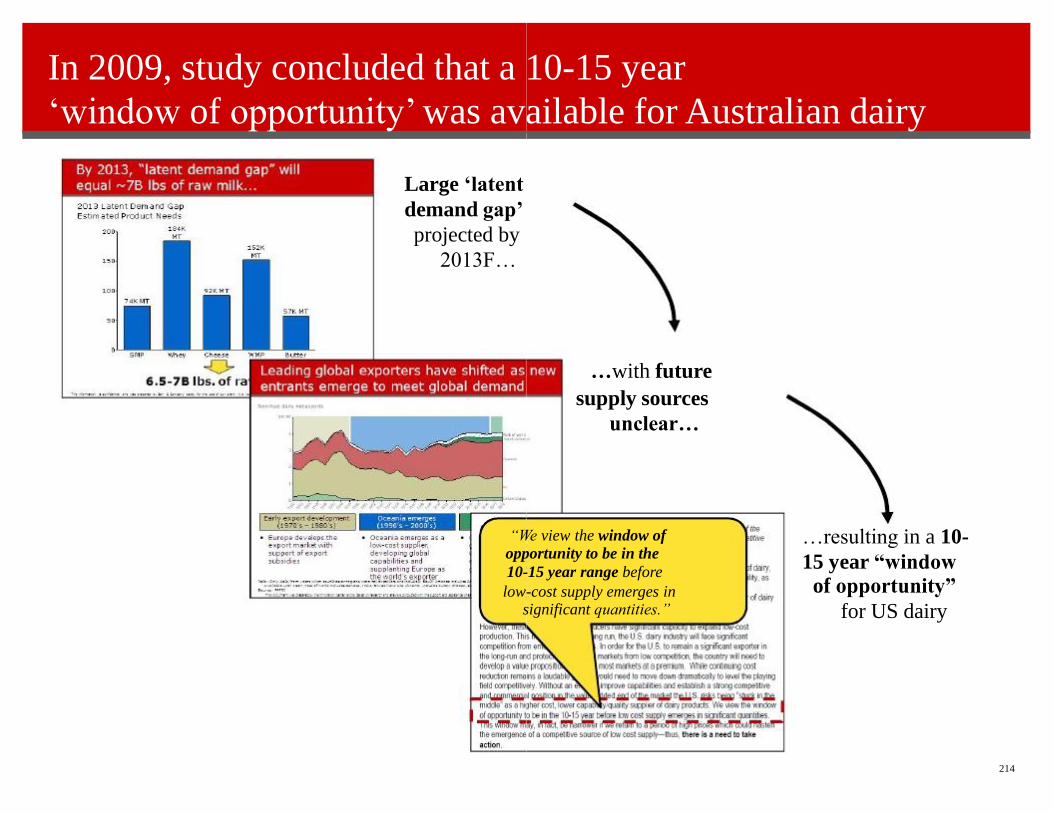

In 2009, Lion Nathan identified several trends

impacting its’ global dairy strategy

Dairy demand will continue to grow

at a rapid pace in developing markets

-Slow growth in Oceania/Europe

-China will remain an importer

A latent demand gap is developing and creating a sizeable,

though finite, window of opportunity for Australian dairy 4

Dairy supply will be challenged to keep pace

-Brazil, Ukraine years out

The Asian dairy trade is the primary source of growth for

Australian dairy, and Australia is positioned to be a

larger player, but must address weaknesses

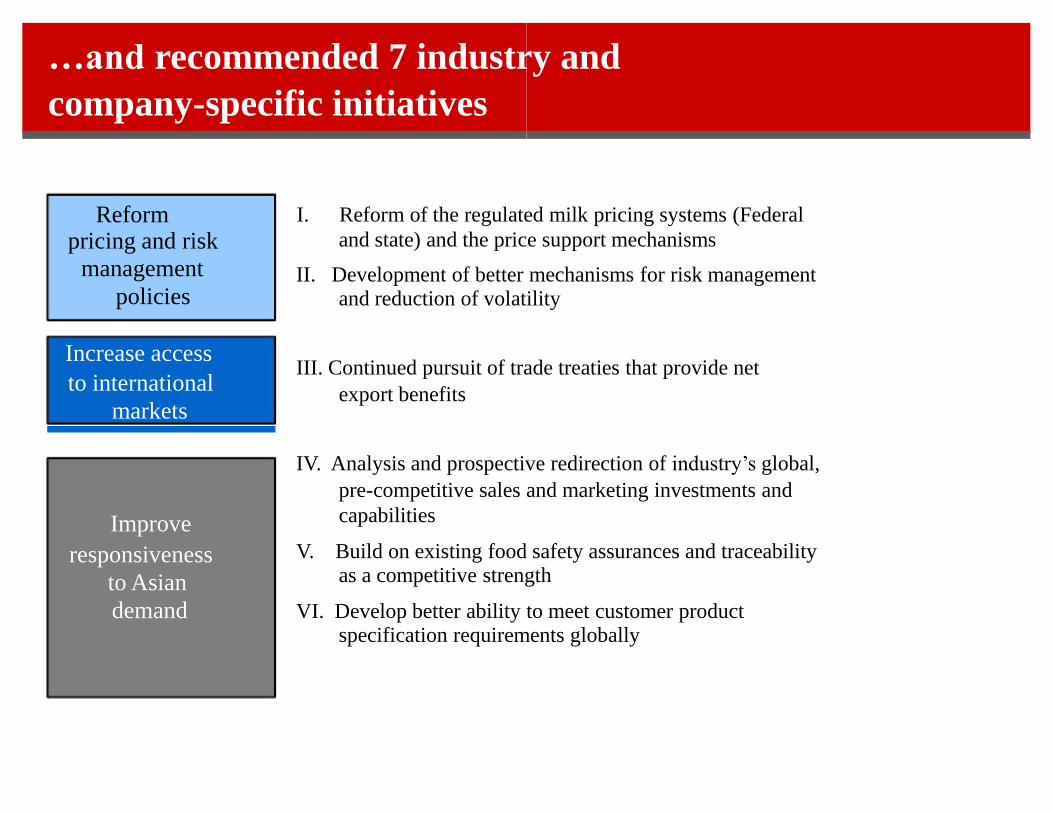

…and recommended 7 industry and

company-specific initiatives

Reform pricing and risk

management

policies Increase access

to international

markets

Improve

responsiveness

to Asian

demand

I. Reform of the regulated milk pricing systems (Federal

and state) and the price support mechanisms II. Development of better mechanisms for risk management and reduction of volatility III. Continued pursuit of trade treaties that provide net

export benefits IV. Analysis and prospective redirection of industry’s global,

pre-competitive sales and marketing investments and

capabilities V. Build on existing food safety assurances and traceability as a competitive strength VI. Develop better ability to meet customer product specification requirements globally

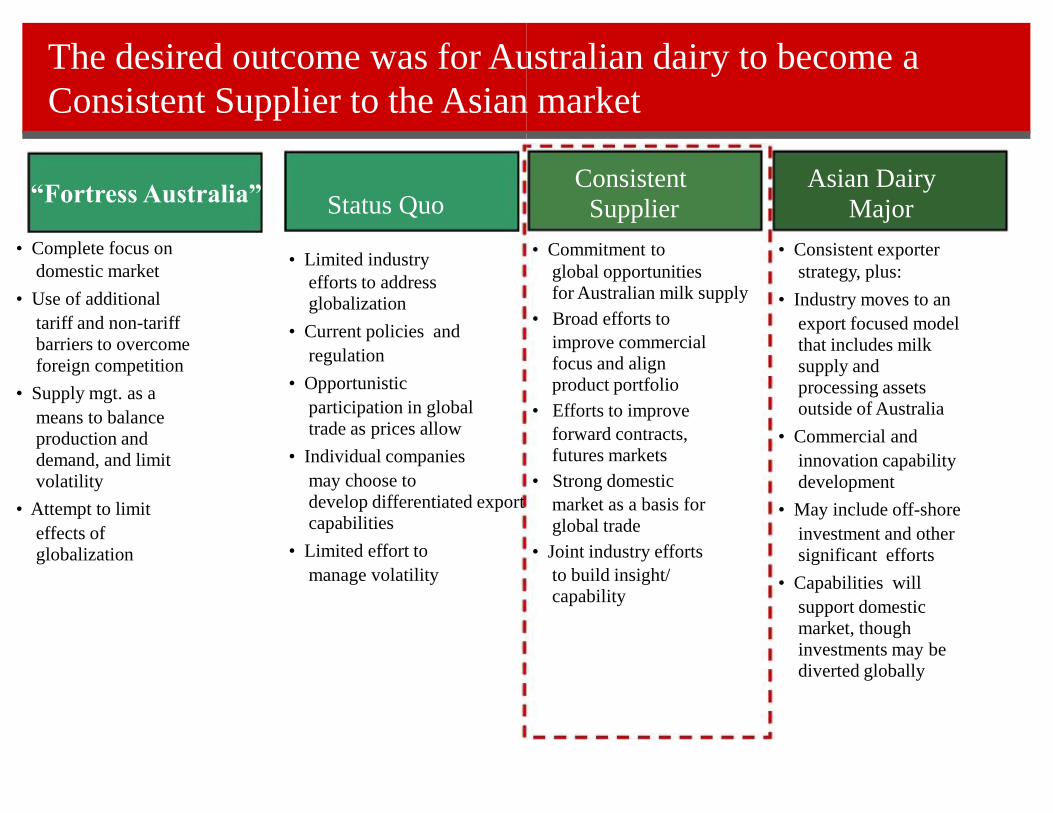

The desired outcome was for Australian dairy to become a

Consistent Supplier to the Asian market

Status Quo • Limited industry

efforts to address

globalization

• Current policies and

regulation

• Opportunistic

participation in global

trade as prices allow

• Individual companies

may choose to

develop differentiated export

capabilities

• Limited effort to

manage volatility

Consistent

Supplier • Commitment to

global opportunities

for Australian milk supply

• Broad efforts to

improve commercial

focus and align

product portfolio

• Efforts to improve

forward contracts,

futures markets

• Strong domestic

market as a basis for

global trade

• Joint industry efforts

to build insight/

capability

Asian Dairy

Major • Consistent exporter

strategy, plus:

• Industry moves to an

export focused model

that includes milk

supply and

processing assets outside of Australia

• Commercial and

innovation capability

development

• May include off-shore

investment and other

significant efforts

• Capabilities will

support domestic

market, though

investments may be

diverted globally

“Fortress Australia” • Complete focus on

domestic market

• Use of additional

tariff and non-tariff

barriers to overcome

foreign competition

• Supply mgt. as a

means to balance

production and

demand, and limit

volatility

• Attempt to limit

effects of

globalization

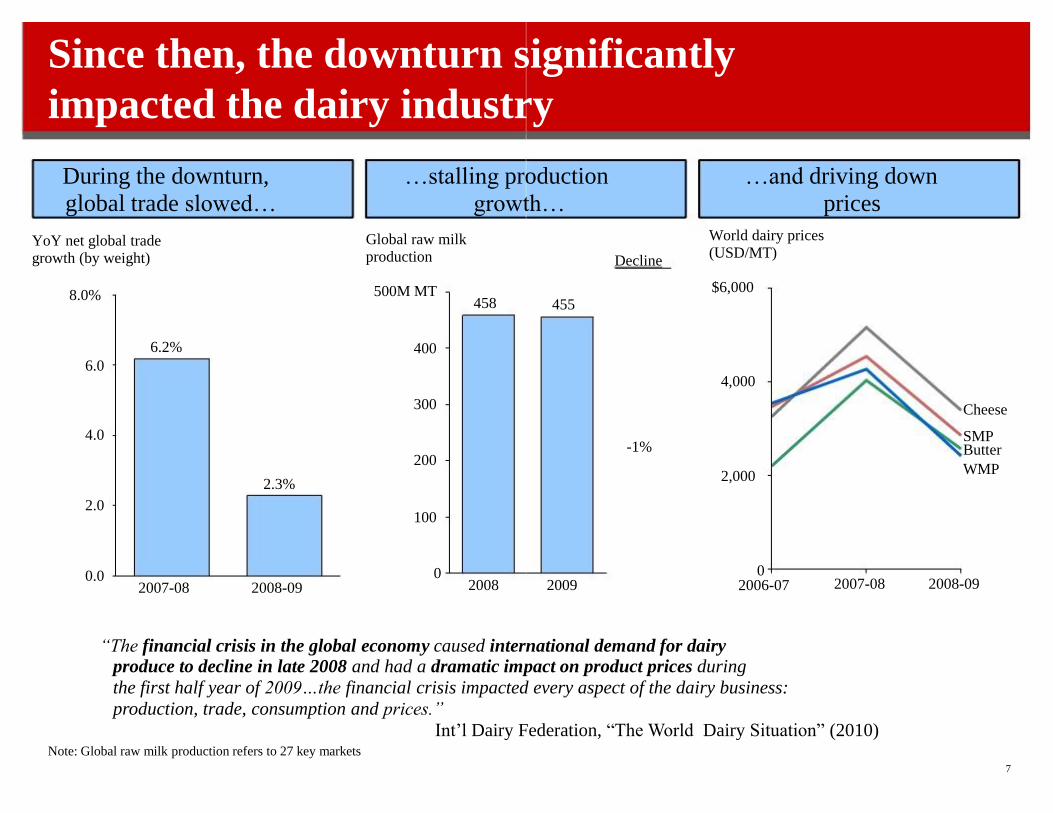

Since then, the downturn significantly

impacted the dairy industry

During the downturn,

global trade slowed…

…stalling production

growth…

0.0

2.0

4.0

8.0%

YoY net global trade growth (by weight)

2007-08

6.2%

2008-09

2.3%

0

100

200

300

400

500M MT

Global raw milk production

2008

458

7

…and driving down

prices

2009

455

-1%

Decline

2,000

6.0 4,000

$6,000

0 2006-07 2007-08 2008-09

World dairy prices (USD/MT)

Cheese

SMP Butter

WMP

“The financial crisis in the global economy caused international demand for dairy produce to decline in late 2008 and had a dramatic impact on product prices during

the first half year of 2009…the financial crisis impacted every aspect of the dairy business:

production, trade, consumption and prices.”

Int’l Dairy Federation, “The World Dairy Situation” (2010) Note: Global raw milk production refers to 27 key markets

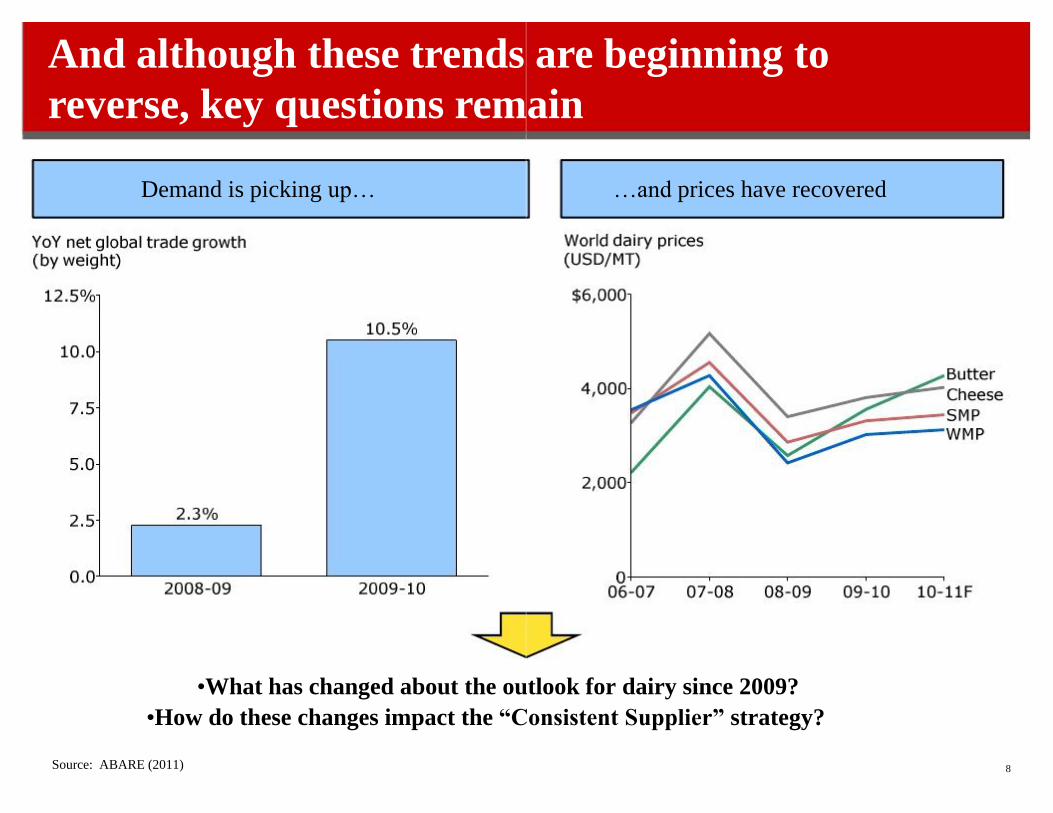

Demand is picking up…

•What has changed about the outlook for dairy since 2009?

•How do these changes impact the “Consistent Supplier” strategy?

And although these trends are beginning to

reverse, key questions remain

Source: ABARE (2011)

8

…and prices have recovered

To address these questions, Lion Nathan commissioned Navigate to undertake a refresh effort

Project objectives

conclusions of the original study

• Assess any expected change to the duration of the “window of

opportunity” facing the Australian dairy industry

• Communicate the findings of the project to key dairy stakeholders

and constituents

9

• Determine if globalization trends have substantively changed

• Agree on which changes could materially affect the primary

• Synthesize updated findings to determine potential impact on the Australian

dairy industry, the “Consistent Supplier” strategy and the

recommended industry initiatives derived in 2009

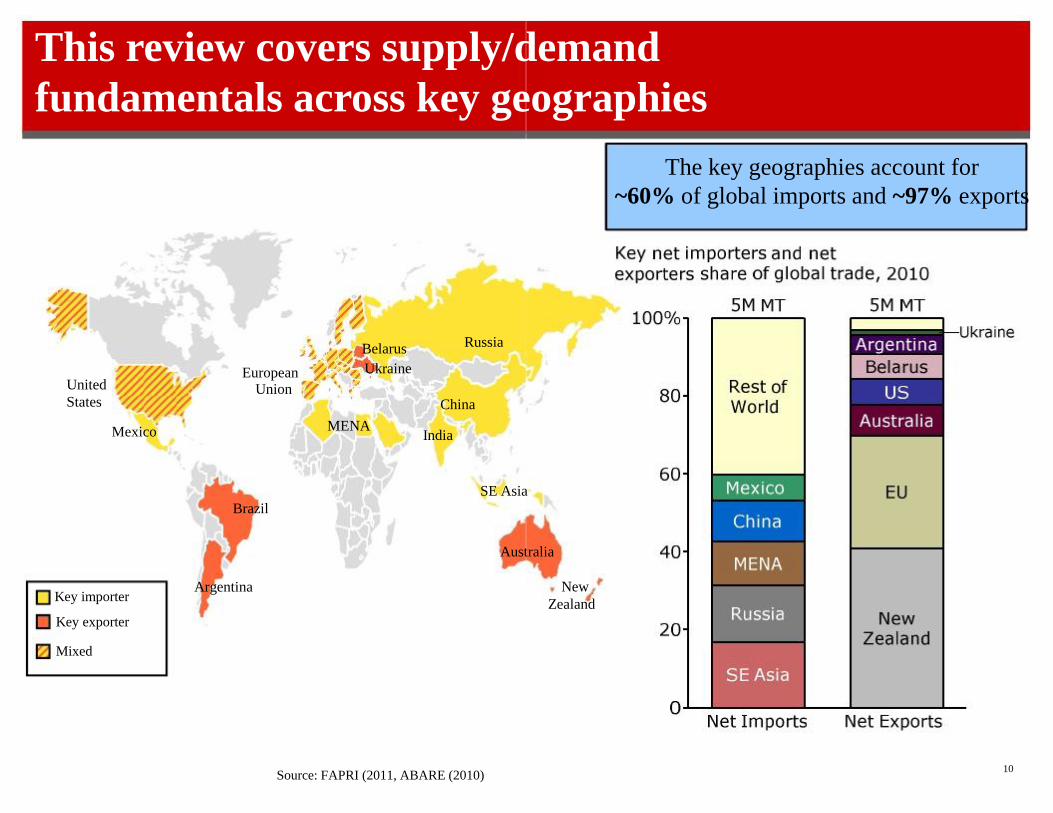

Key importer

United

States Mexico

European Union

Russia

SE Asia

Brazil Australia

Argentina

China India

Belarus

Ukraine MENA

Source: FAPRI (2011, ABARE (2010)

10

This review covers supply/demand

fundamentals across key geographies

New

Zealand

The key geographies account for

~60% of global imports and ~97% exports

Key exporter

Mixed

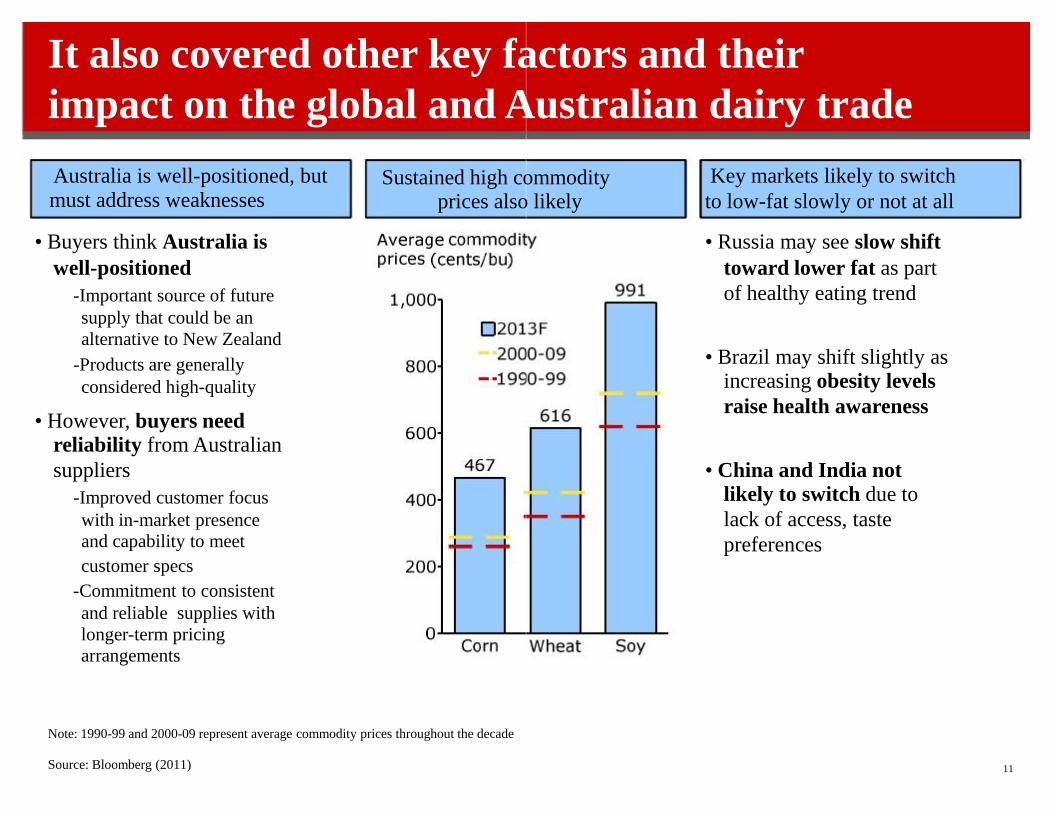

It also covered other key factors and their

impact on the global and Australian dairy trade

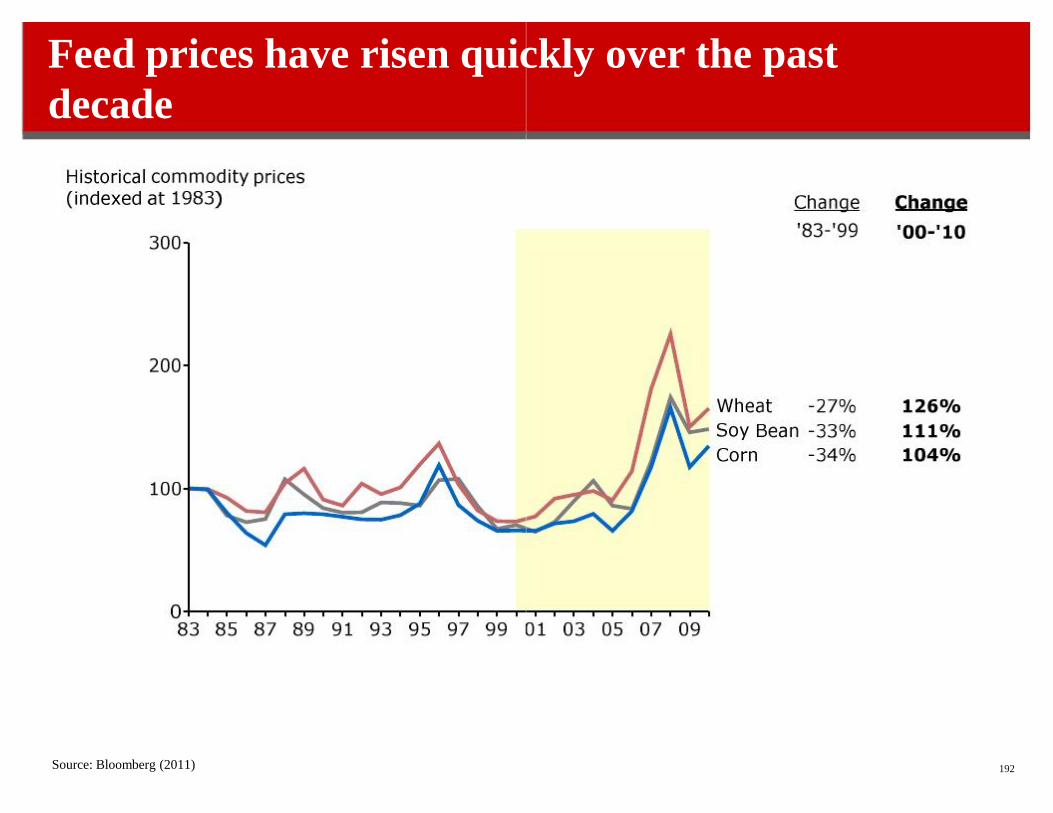

Sustained high commodity prices also likely

Australia is well-positioned, but must address weaknesses • Buyers think Australia is

well-positioned

-Important source of future

supply that could be an

alternative to New Zealand

-Products are generally

considered high-quality • However, buyers need

reliability from Australian

suppliers

-Improved customer focus

with in-market presence

and capability to meet

customer specs

-Commitment to consistent

and reliable supplies with

longer-term pricing

arrangements Note: 1990-99 and 2000-09 represent average commodity prices throughout the decade

Source: Bloomberg (2011)

11

Key markets likely to switch

to low-fat slowly or not at all • Russia may see slow shift

toward lower fat as part

of healthy eating trend • Brazil may shift slightly as increasing obesity levels

raise health awareness • China and India not

likely to switch due to

lack of access, taste

preferences

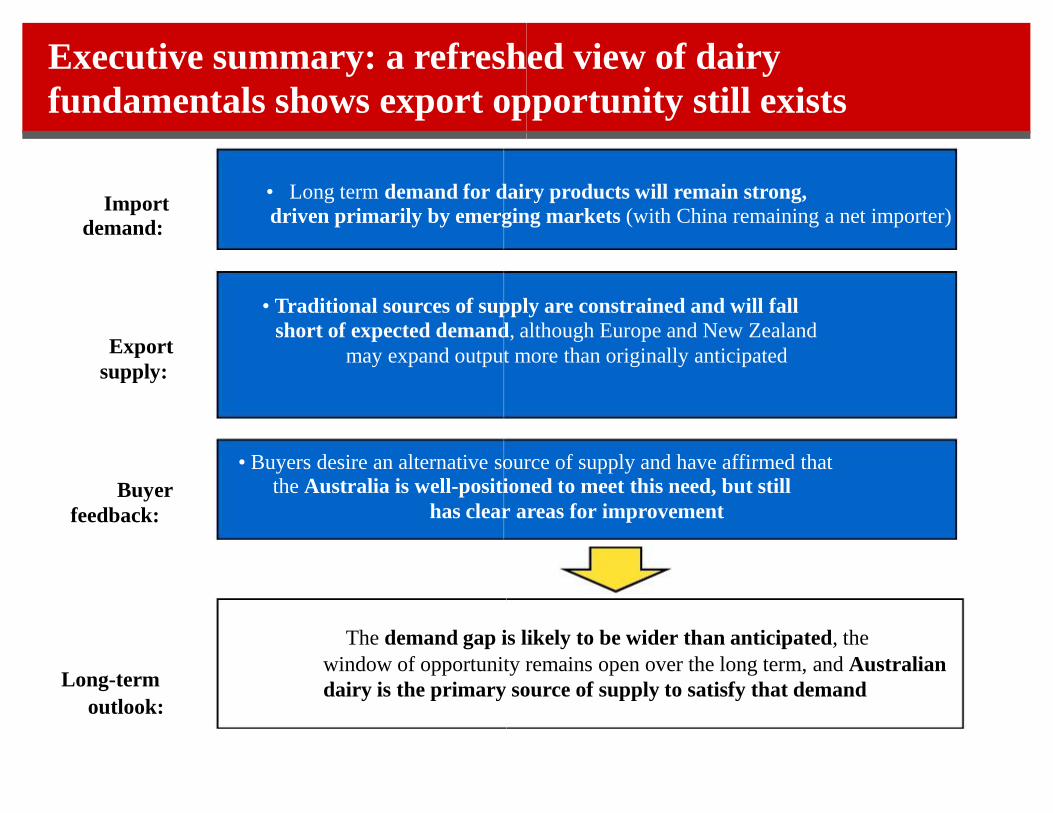

Executive summary: a refreshed view of dairy

fundamentals shows export opportunity still exists

Import

demand: Export

supply: Buyer

feedback: Long-term

outlook:

• Long term demand for dairy products will remain strong,

driven primarily by emerging markets (with China remaining a net importer) • Traditional sources of supply are constrained and will fall

short of expected demand, although Europe and New Zealand

may expand output more than originally anticipated • Buyers desire an alternative source of supply and have affirmed that the Australia is well-positioned to meet this need, but still

has clear areas for improvement

The demand gap is likely to be wider than anticipated, the

window of opportunity remains open over the long term, and Australian

dairy is the primary source of supply to satisfy that demand

Contents

•Project objectives and summary findings

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

14

•Geography-specific findings – net importers

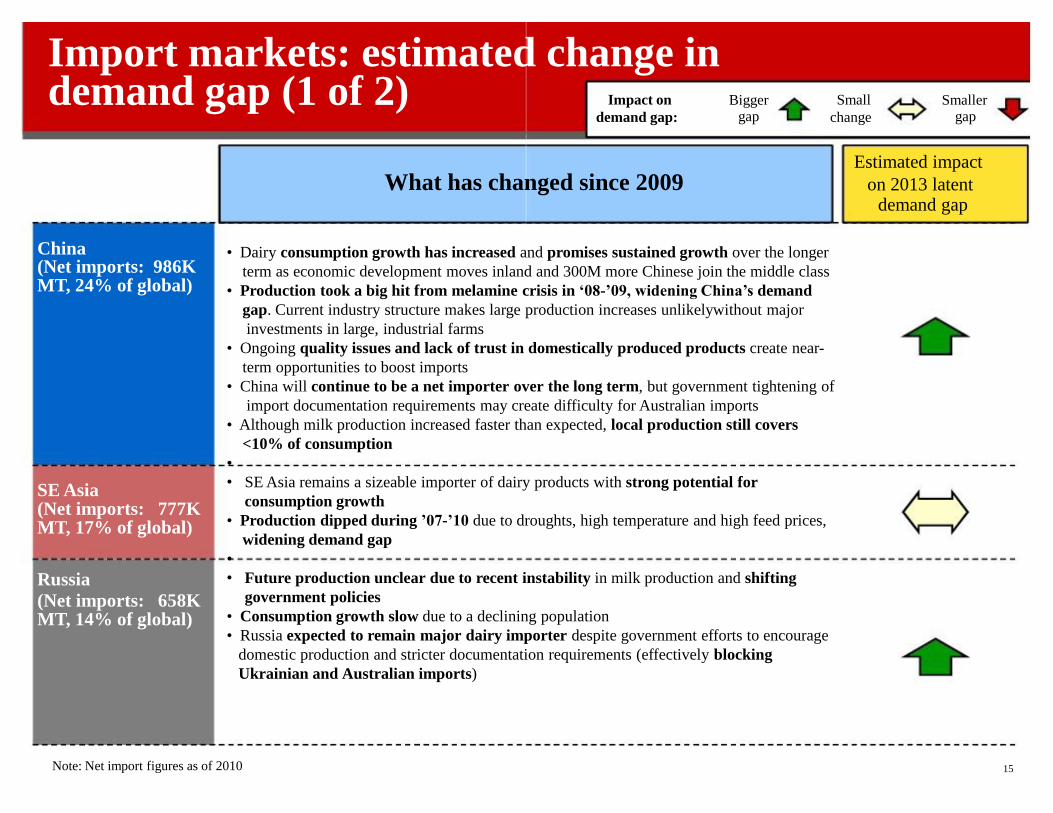

Import markets: estimated change in demand gap (1 of 2)

China (Net imports: 986K MT, 24% of global) SE Asia (Net imports: 777K MT, 17% of global) Russia

(Net imports: 658K MT, 14% of global)

What has changed since 2009

Note: Net import figures as of 2010

15

• Dairy consumption growth has increased and promises sustained growth over the longer

term as economic development moves inland and 300M more Chinese join the middle class

• Production took a big hit from melamine crisis in ‘08-’09, widening China’s demand

gap. Current industry structure makes large production increases unlikelywithout major

investments in large, industrial farms

• Ongoing quality issues and lack of trust in domestically produced products create near-

term opportunities to boost imports

• China will continue to be a net importer over the long term, but government tightening of

import documentation requirements may create difficulty for Australian imports

• Although milk production increased faster than expected, local production still covers

<10% of consumption

•

• SE Asia remains a sizeable importer of dairy products with strong potential for

consumption growth

• Production dipped during ’07-’10 due to droughts, high temperature and high feed prices,

widening demand gap

•

• Future production unclear due to recent instability in milk production and shifting

government policies

• Consumption growth slow due to a declining population

• Russia expected to remain major dairy importer despite government efforts to encourage

domestic production and stricter documentation requirements (effectively blocking

Ukrainian and Australian imports)

Estimated impact

on 2013 latent demand gap

Bigger gap

Small

change

Smaller gap

Impact on

demand gap:

Import markets: estimated change in

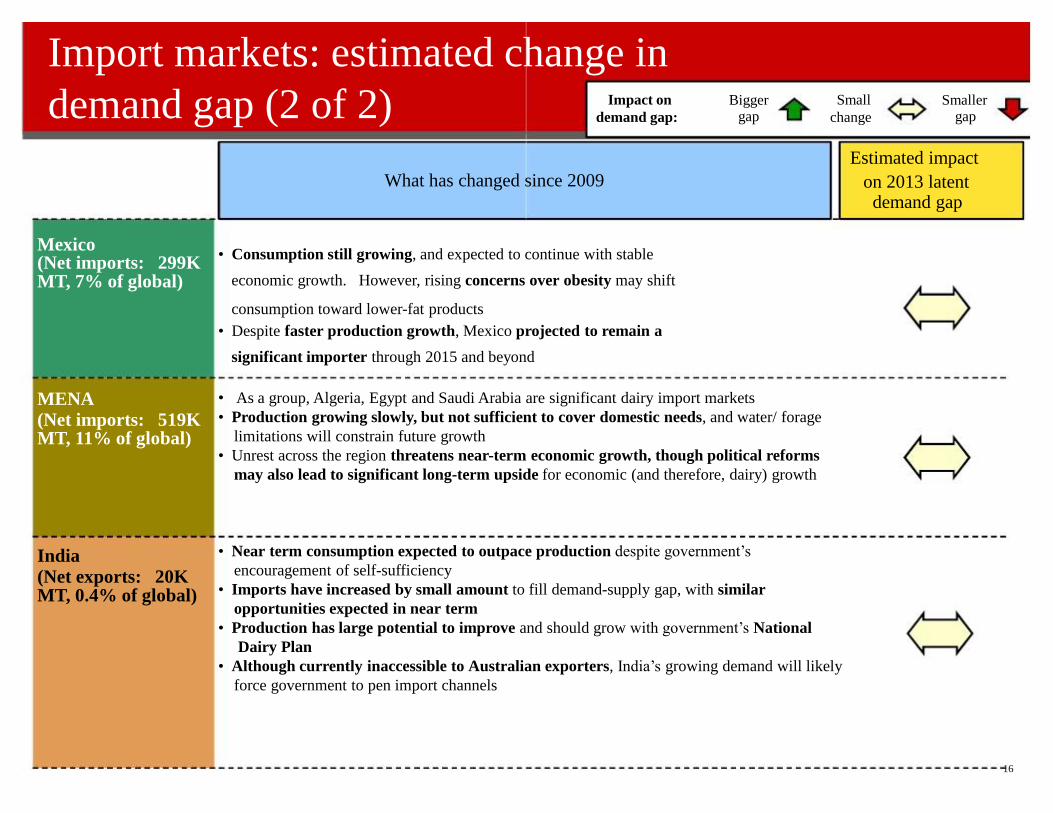

demand gap (2 of 2)

Mexico (Net imports: 299K MT, 7% of global) MENA

(Net imports: 519K MT, 11% of global) India

(Net exports: 20K MT, 0.4% of global)

What has changed since 2009

16

• Consumption still growing, and expected to continue with stable

economic growth. However, rising concerns over obesity may shift

consumption toward lower-fat products

• Despite faster production growth, Mexico projected to remain a

significant importer through 2015 and beyond

• As a group, Algeria, Egypt and Saudi Arabia are significant dairy import markets

• Production growing slowly, but not sufficient to cover domestic needs, and water/ forage

limitations will constrain future growth

• Unrest across the region threatens near-term economic growth, though political reforms

may also lead to significant long-term upside for economic (and therefore, dairy) growth

• Near term consumption expected to outpace production despite government’s

encouragement of self-sufficiency

• Imports have increased by small amount to fill demand-supply gap, with similar

opportunities expected in near term

• Production has large potential to improve and should grow with government’s National

Dairy Plan

• Although currently inaccessible to Australian exporters, India’s growing demand will likely

force government to pen import channels

Estimated impact

on 2013 latent demand gap

Bigger gap

Small

change

Smaller gap

Impact on

demand gap:

Summary: China

• Dairy consumption likely to outpace production growth through

2015, with sustained growth over the longer term as economic

development moves inland and 300M more Chinese join the middle class

• Recurring quality scandals are reducing confidence in local dairy

supplies, thus strengthening near-term demand for imports

-Milk production declined by 17% in 2009 due to the melamine crisis; continued quality challenges and stricter health/safety standards likely to hamper production

in the next several years

-Example: Fonterra has committed to local dairy production, though unlikely to reach >1%

share even in the mid-term

17

• Higher inflation and appreciating RMB has triggered some government

response to check it, though a rising currency will likely continue to

favor imports over domestic production

• Despite government and foreign investment, industrial production in

China likely to remain small and imports will continue to be an

important source of dairy

China

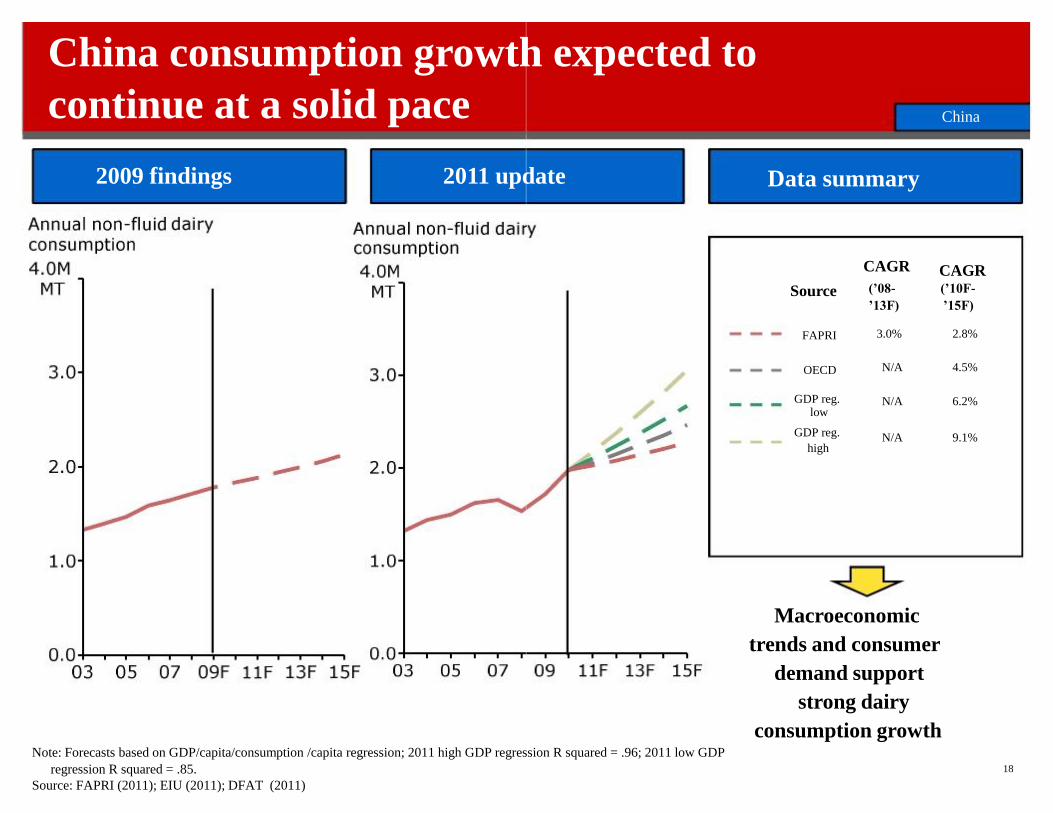

• Largest single import market in the world in 2010. On track to be twice the size of 2nd largest market Russia by 2015.

China consumption growth expected to

continue at a solid pace

2009 findings 2011 update

regression R squared = .85.

Source: FAPRI (2011); EIU (2011); DFAT (2011) 18

Data summary CAGR CAGR

Macroeconomic

trends and consumer

demand support

strong dairy

consumption growth Note: Forecasts based on GDP/capita/consumption /capita regression; 2011 high GDP regression R squared = .96; 2011 low GDP

Source FAPRI

OECD

GDP reg. low

GDP reg.

high

(’10F-

’15F) 2.8% 4.5%

6.2%

9.1%

(’08-

’13F) 3.0% N/A

N/A

N/A

China

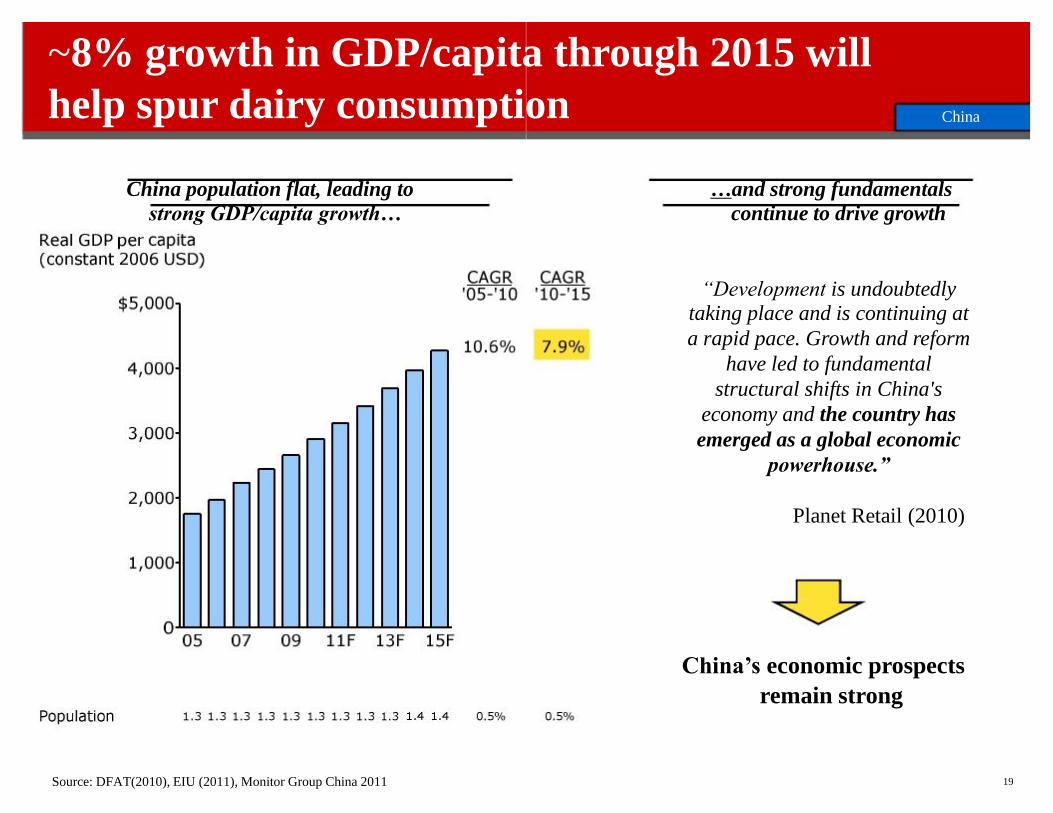

~8% growth in GDP/capita through 2015 will

help spur dairy consumption

China population flat, leading to

strong GDP/capita growth… Source: DFAT(2010), EIU (2011), Monitor Group China 2011

…and strong fundamentals

continue to drive growth

“Development is undoubtedly taking place and is continuing at

a rapid pace. Growth and reform

have led to fundamental

structural shifts in China's

economy and the country has

emerged as a global economic

powerhouse.” Planet Retail (2010)

China’s economic prospects

remain strong 19

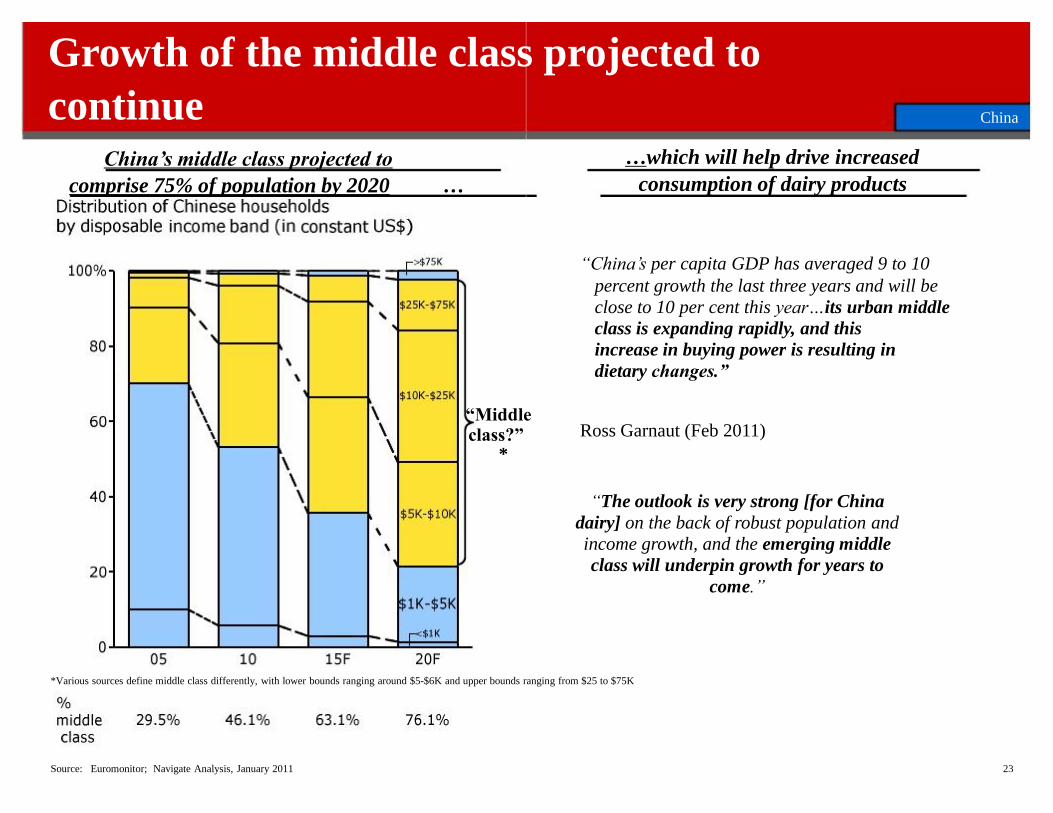

China

Growth of the middle class projected to

“Middle class?”

continue China’s middle class projected to

comprise 75% of population by 2020 …

Source: Euromonitor; Navigate Analysis, January 2011

23

Ross Garnaut (Feb 2011)

*

“The outlook is very strong [for China

dairy] on the back of robust population and

income growth, and the emerging middle

class will underpin growth for years to

come.” *Various sources define middle class differently, with lower bounds ranging around $5-$6K and upper bounds ranging from $25 to $75K

China …which will help drive increased

consumption of dairy products “China’s per capita GDP has averaged 9 to 10

percent growth the last three years and will be

close to 10 per cent this year…its urban middle

class is expanding rapidly, and this

increase in buying power is resulting in

dietary changes.”

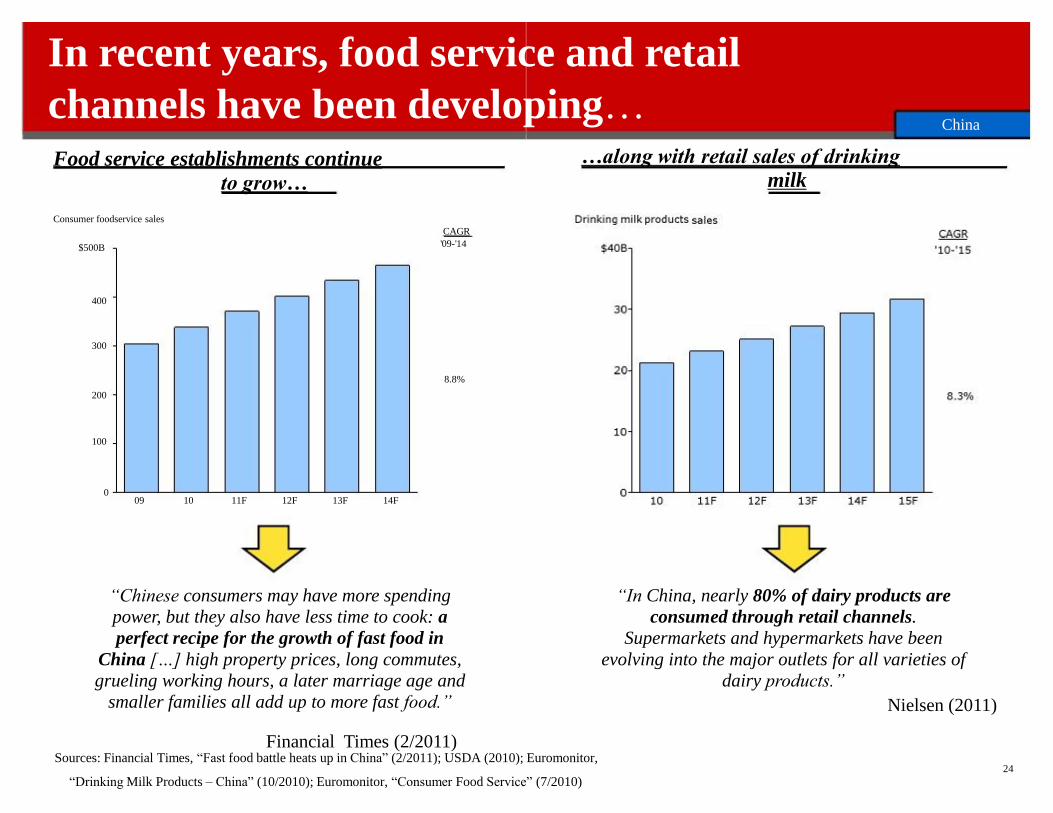

In recent years, food service and retail

channels have been developing…

“Chinese consumers may have more spending

power, but they also have less time to cook: a

perfect recipe for the growth of fast food in

China […] high property prices, long commutes,

grueling working hours, a later marriage age and

smaller families all add up to more fast food.”

Financial Times (2/2011) Sources: Financial Times, “Fast food battle heats up in China” (2/2011); USDA (2010); Euromonitor,

0

$500B

09 10 11F 12F 13F 14F

400

300

8.8%

200

100

'09-'14

Food service establishments continue

to grow… Consumer foodservice sales

CAGR

“Drinking Milk Products – China” (10/2010); Euromonitor, “Consumer Food Service” (7/2010) 24

“In China, nearly 80% of dairy products are

consumed through retail channels.

Supermarkets and hypermarkets have been

evolving into the major outlets for all varieties of

dairy products.”

Nielsen (2011)

…along with retail sales of drinking

milk

China

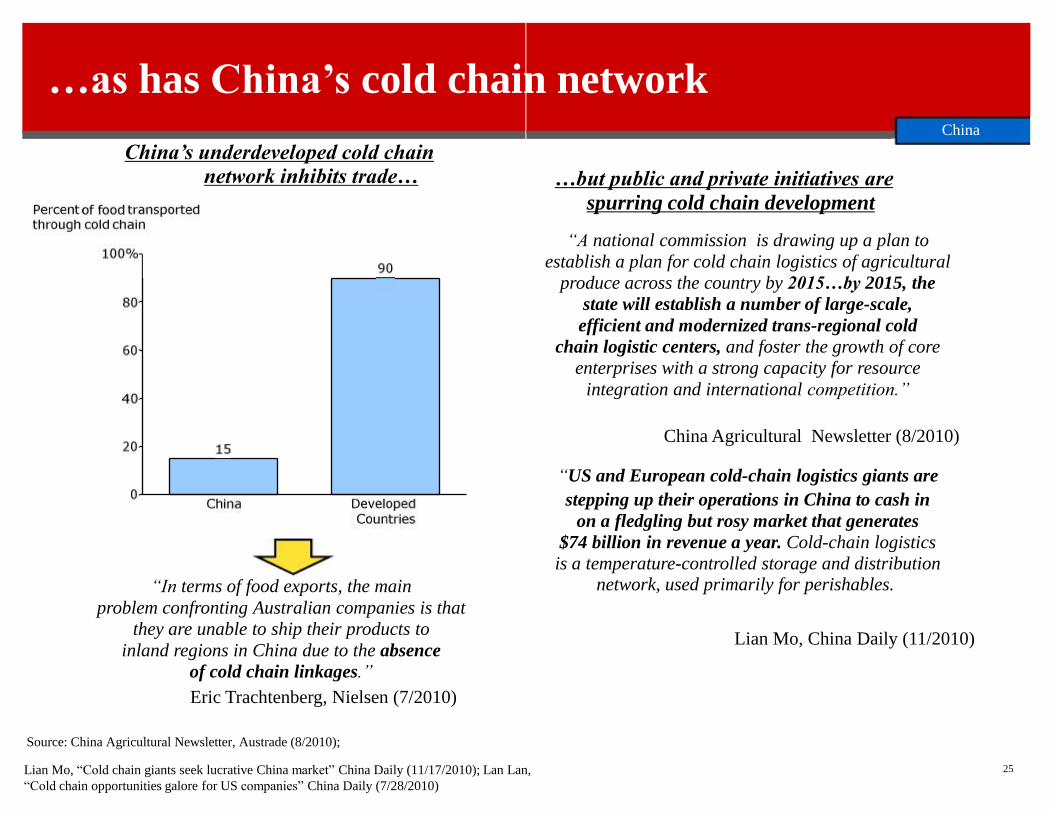

China’s underdeveloped cold chain

network inhibits trade…

“In terms of food exports, the main

problem confronting Australian companies is that

they are unable to ship their products to

inland regions in China due to the absence

of cold chain linkages.”

Eric Trachtenberg, Nielsen (7/2010)

Source: China Agricultural Newsletter, Austrade (8/2010);

Lian Mo, “Cold chain giants seek lucrative China market” China Daily (11/17/2010); Lan Lan,

“Cold chain opportunities galore for US companies” China Daily (7/28/2010) 25

…as has China’s cold chain network China

…but public and private initiatives are

spurring cold chain development

“A national commission is drawing up a plan to

establish a plan for cold chain logistics of agricultural

produce across the country by 2015…by 2015, the

state will establish a number of large-scale,

efficient and modernized trans-regional cold

chain logistic centers, and foster the growth of core

enterprises with a strong capacity for resource

integration and international competition.” China Agricultural Newsletter (8/2010)

“US and European cold-chain logistics giants are

stepping up their operations in China to cash in

on a fledgling but rosy market that generates

$74 billion in revenue a year. Cold-chain logistics

is a temperature-controlled storage and distribution network, used primarily for perishables.

Lian Mo, China Daily (11/2010)

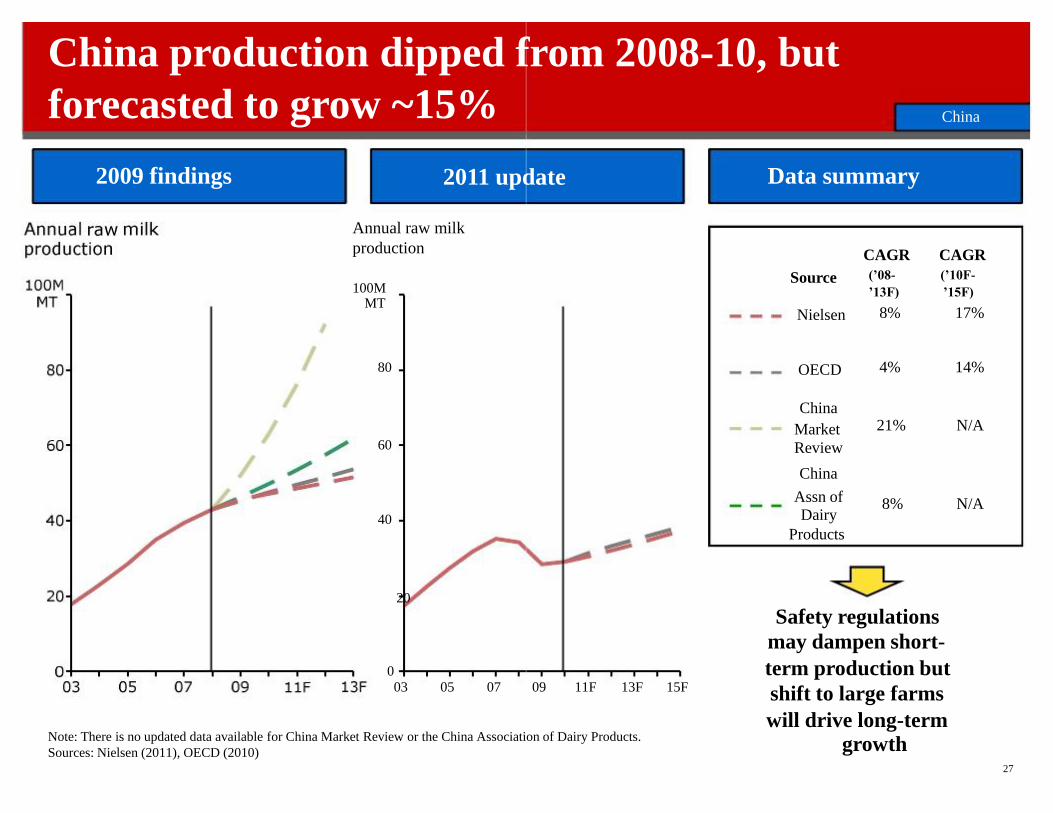

forecasted to grow ~15%

2009 findings

0

40

60

100M MT 80

2011 update Annual raw milk

production

03 05 07

Note: There is no updated data available for China Market Review or the China Association of Dairy Products.

Sources: Nielsen (2011), OECD (2010) 27

China production dipped from 2008-10, but

Data summary

CAGR CAGR

Source Nielsen OECD

(’10F-

’15F)

17% 14%

(’08-

’13F)

8% 4%

09 11F 13F 15F

20

Safety regulations

may dampen short-

term production but

shift to large farms

will drive long-term

growth

China N/A 21% Market

Review

China

Assn of Dairy

Products

N/A 8%

China

Austrade, China Dairy Report (2010)

0

20,000 10,000

Cows' milk production (K MT) 40,000 30,000

05 06 07 08 09 10F

2,011 2,108 2,099 2,086 2,085 1,988 Avg milk yield

(kg per cow)

13,694 15,151 16,791 16,446 13,646 14,637 Milk cows

(1,000 head)

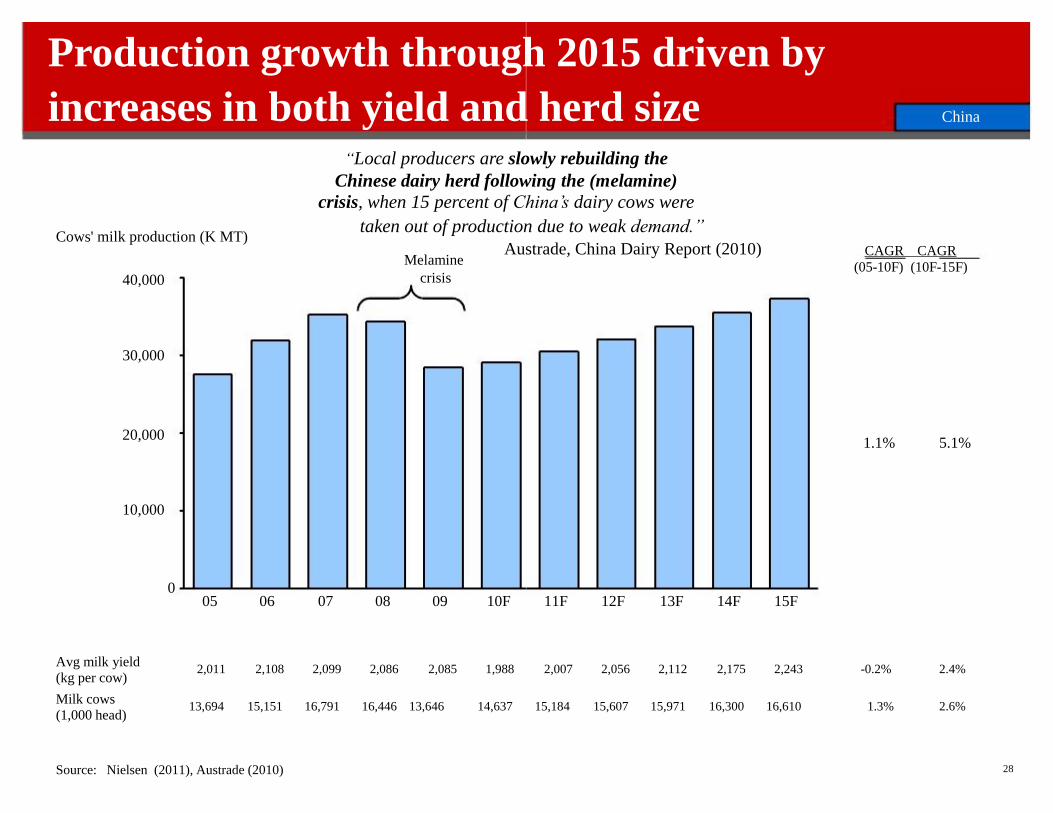

Production growth through 2015 driven by

increases in both yield and herd size

“Local producers are slowly rebuilding the

Chinese dairy herd following the (melamine)

crisis, when 15 percent of China’s dairy cows were

taken out of production due to weak demand.” Melamine

crisis

Source: Nielsen (2011), Austrade (2010)

28

11F 12F 13F 14F 15F

1.1% 5.1%

CAGR CAGR

(05-10F) (10F-15F)

2,175 2,243 2,007 2,056 2,112

16,300 16,610 15,184 15,607 15,971 1.3%

-0.2%

2.6%

2.4%

China

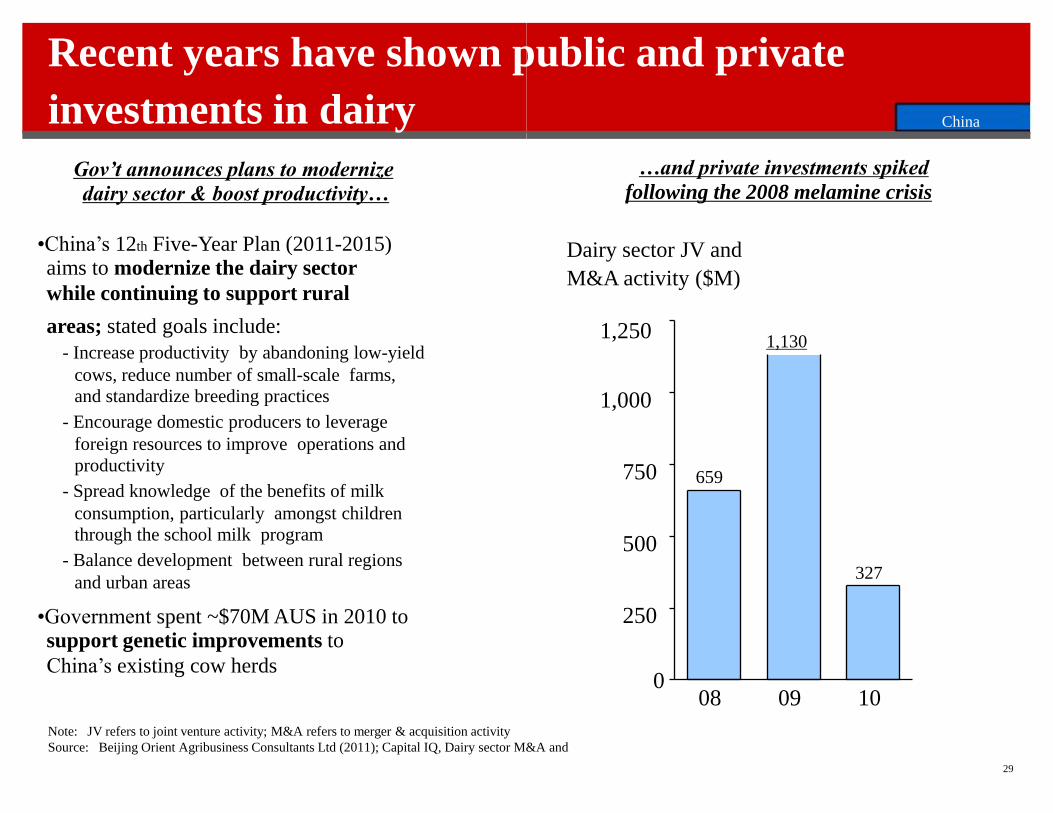

Recent years have shown public and private

Note: JV refers to joint venture activity; M&A refers to merger & acquisition activity

Source: Beijing Orient Agribusiness Consultants Ltd (2011); Capital IQ, Dairy sector M&A and

investments in dairy Gov’t announces plans to modernize

dairy sector & boost productivity… •China’s 12th Five-Year Plan (2011-2015) aims to modernize the dairy sector

while continuing to support rural

areas; stated goals include:

- Increase productivity by abandoning low-yield

cows, reduce number of small-scale farms,

and standardize breeding practices

- Encourage domestic producers to leverage

foreign resources to improve operations and

productivity

- Spread knowledge of the benefits of milk

consumption, particularly amongst children

through the school milk program

- Balance development between rural regions

and urban areas •Government spent ~$70M AUS in 2010 to support genetic improvements to

China’s existing cow herds

29

0

1,250 1,000 750 500 250

08

659

09

1,130

10

327

China

…and private investments spiked

following the 2008 melamine crisis Dairy sector JV and

M&A activity ($M)

Term Long

Term

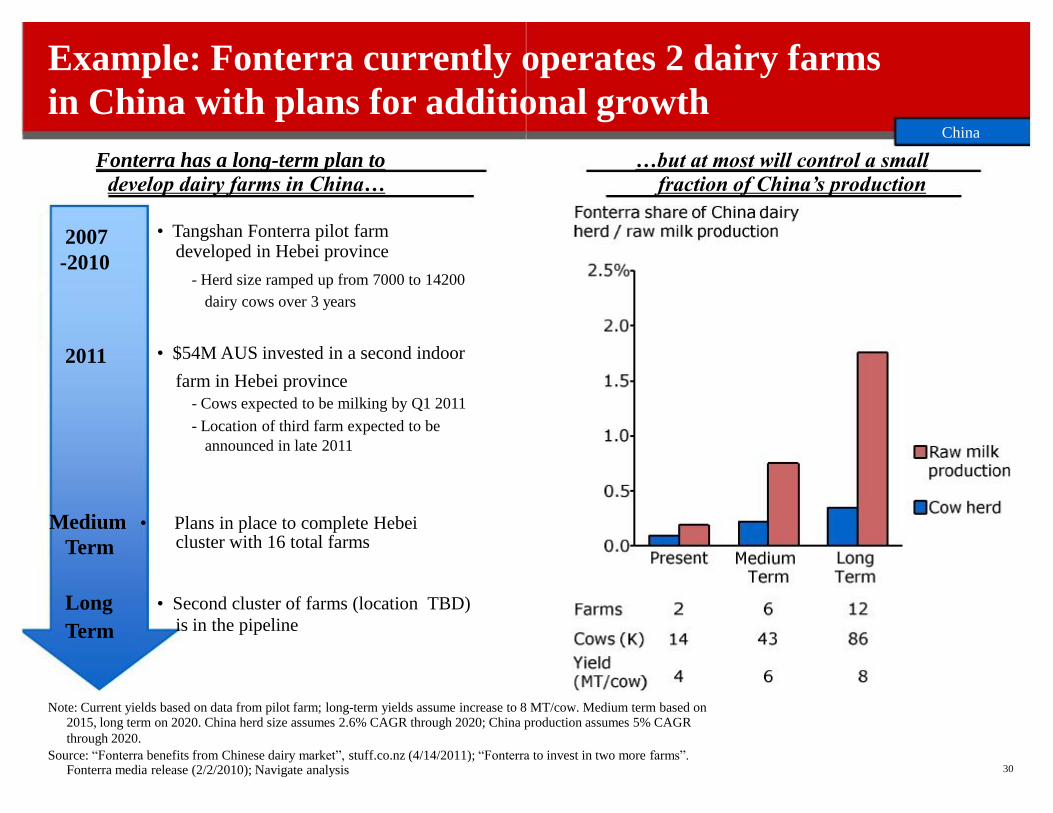

2007

-2010 2011

Fonterra has a long-term plan to

develop dairy farms in China…

• Tangshan Fonterra pilot farm developed in Hebei province

- Herd size ramped up from 7000 to 14200

dairy cows over 3 years • $54M AUS invested in a second indoor

farm in Hebei province

- Cows expected to be milking by Q1 2011

- Location of third farm expected to be

announced in late 2011 Medium • Plans in place to complete Hebei

cluster with 16 total farms • Second cluster of farms (location TBD)

is in the pipeline

Note: Current yields based on data from pilot farm; long-term yields assume increase to 8 MT/cow. Medium term based on 2015, long term on 2020. China herd size assumes 2.6% CAGR through 2020; China production assumes 5% CAGR

through 2020.

Source: “Fonterra benefits from Chinese dairy market”, stuff.co.nz (4/14/2011); “Fonterra to invest in two more farms”. Fonterra media release (2/2/2010); Navigate analysis 30

…but at most will control a small

fraction of China’s production

Example: Fonterra currently operates 2 dairy farms

in China with plans for additional growth China

Example: Chinese dairies making foreign

investments to secure milk supply

In 7/2010, China’s Bright Dairy invested

~$59M USD in New Zealand’s Synlait • Bright Dairy & Food announced

a $82M NZD (~$59M USD)

investment in Synlait to

expand processing capacity

-Bright Dairy would own 51%

stake in Synlait Milk processing

company and control 4 out of 7

Board seats

-Extra production capacity will

expand infant formula and whole

milk powder (WMP)

-Total production expansion equal

to 100K MT per year • Synlait Limited (Synlait’s parent

company) to continue owning

and operating Synlait’s

farming assets

Source: New Zealand Press Association, Reuters, Factiva news articles

31

China

In 4/2011, Synutra announced

potential venture with France’s Sodiaal • Synutra (a Chinese infant baby

formula maker) has announced

plans to secure milk supplies

from French dairy

cooperative Sodiaal

-Synutra plans to develop a baby

milk powder plant that would

process infant formula in France

-Under potential partnership

agreement, Sodiaal would supply

280-300M liters of milk to a

processing plant in northwest

France

-Construction of the plant would

start in 2013, hitting 60K MT

capacity by 2014

-

Note: Assumes 1 NZD = 0.79 AUS (2010 average) and 1 EUR = 1.45 AUS (5/5/10 exchange rates)

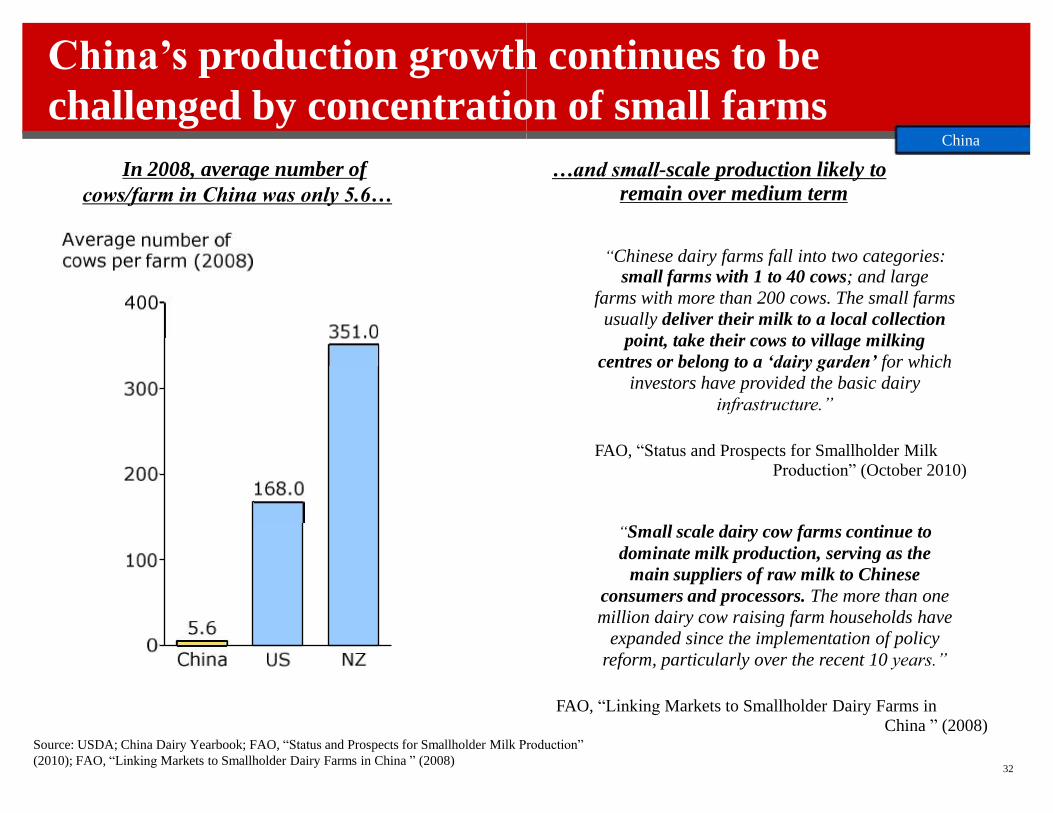

In 2008, average number of

cows/farm in China was only 5.6…

(2010); FAO, “Linking Markets to Smallholder Dairy Farms in China ” (2008)

32

“Chinese dairy farms fall into two categories: small farms with 1 to 40 cows; and large

farms with more than 200 cows. The small farms

usually deliver their milk to a local collection

point, take their cows to village milking

centres or belong to a ‘dairy garden’ for which

investors have provided the basic dairy

infrastructure.”

FAO, “Status and Prospects for Smallholder Milk

Production” (October 2010)

“Small scale dairy cow farms continue to

dominate milk production, serving as the

main suppliers of raw milk to Chinese

consumers and processors. The more than one

million dairy cow raising farm households have

expanded since the implementation of policy

reform, particularly over the recent 10 years.” FAO, “Linking Markets to Smallholder Dairy Farms in

China ” (2008) Source: USDA; China Dairy Yearbook; FAO, “Status and Prospects for Smallholder Milk Production”

…and small-scale production likely to

remain over medium term

China’s production growth continues to be

challenged by concentration of small farms China

Source: FAPRI (2011); Navigate analysis

33

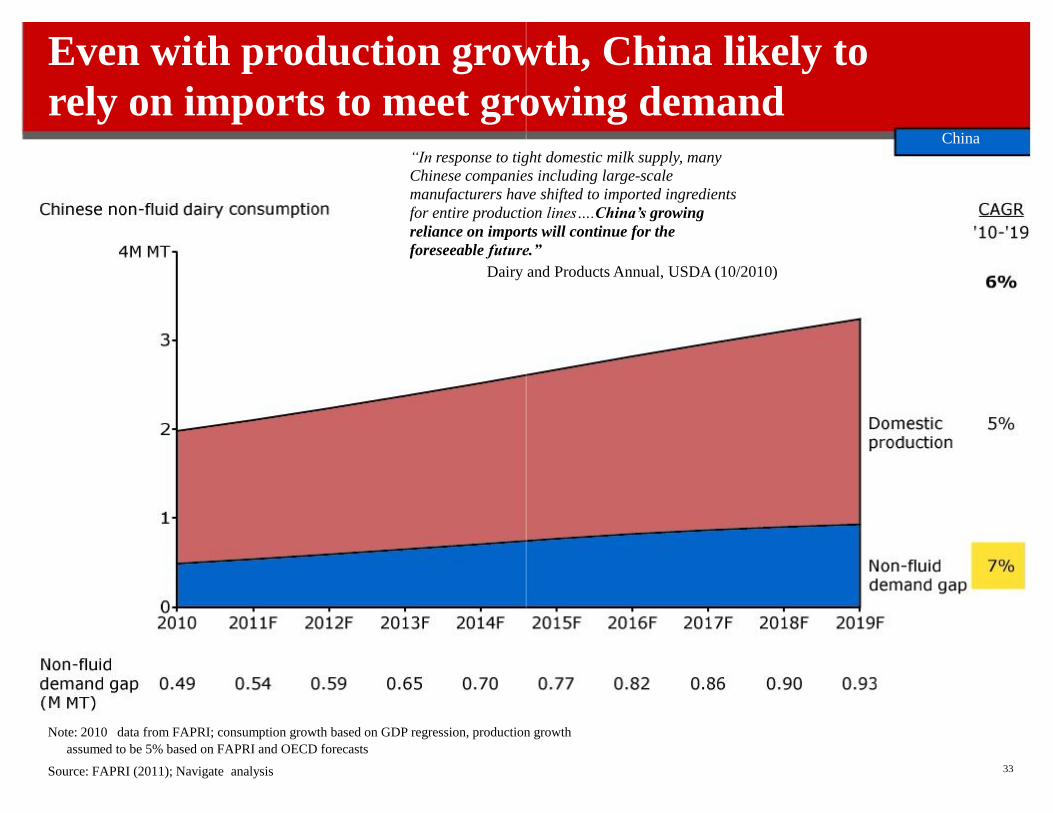

Even with production growth, China likely to

rely on imports to meet growing demand China

“In response to tight domestic milk supply, many

Chinese companies including large-scale

manufacturers have shifted to imported ingredients

for entire production lines….China’s growing

reliance on imports will continue for the

foreseeable future.”

Dairy and Products Annual, USDA (10/2010) Note: 2010 data from FAPRI; consumption growth based on GDP regression, production growth

assumed to be 5% based on FAPRI and OECD forecasts

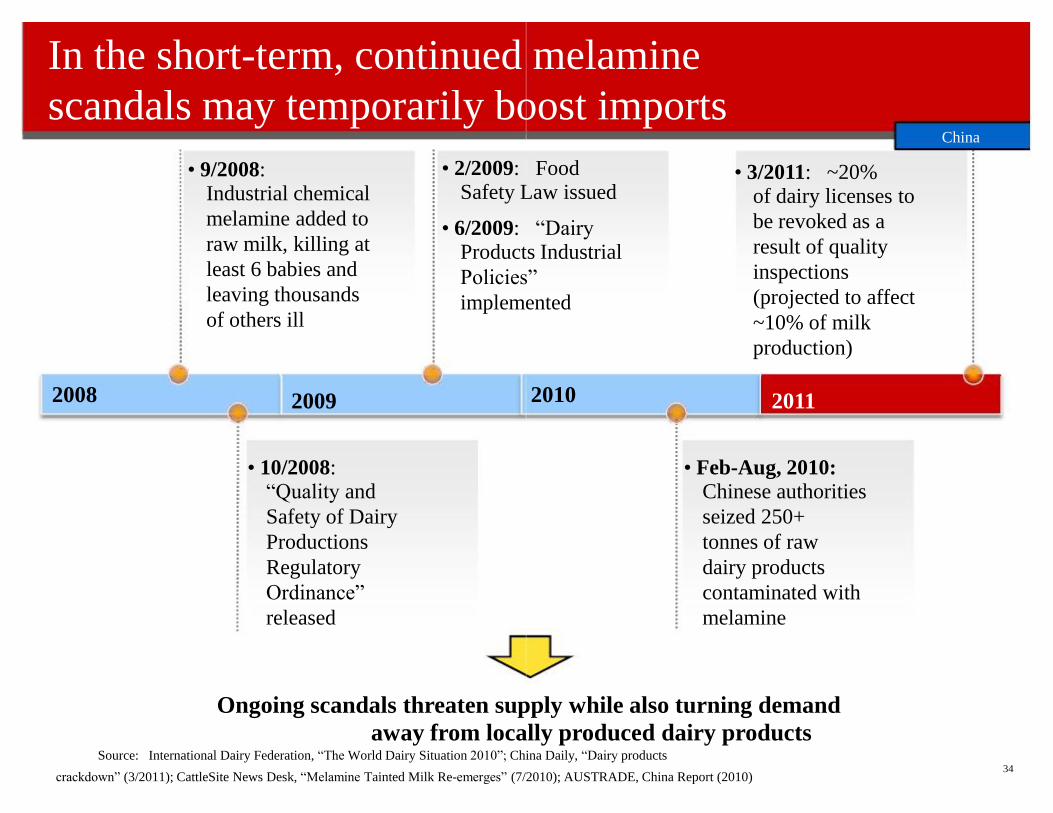

2008 2009 • 10/2008: “Quality and

Safety of Dairy

Productions

Regulatory

Ordinance”

released

• 9/2008: Industrial chemical

melamine added to

raw milk, killing at

least 6 babies and

leaving thousands

of others ill

34

2010

• 2/2009: Food Safety Law issued • 6/2009: “Dairy Products Industrial

Policies”

implemented

• 3/2011: ~20% of dairy licenses to

be revoked as a

result of quality

inspections

(projected to affect

~10% of milk

production)

2011 • Feb-Aug, 2010:

Chinese authorities

seized 250+

tonnes of raw

dairy products

contaminated with

melamine

crackdown” (3/2011); CattleSite News Desk, “Melamine Tainted Milk Re-emerges” (7/2010); AUSTRADE, China Report (2010)

In the short-term, continued melamine

scandals may temporarily boost imports China

Ongoing scandals threaten supply while also turning demand

away from locally produced dairy products Source: International Dairy Federation, “The World Dairy Situation 2010”; China Daily, “Dairy products

Contents

•Project objectives and summary findings

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

83

•Geography-specific findings – net exporters

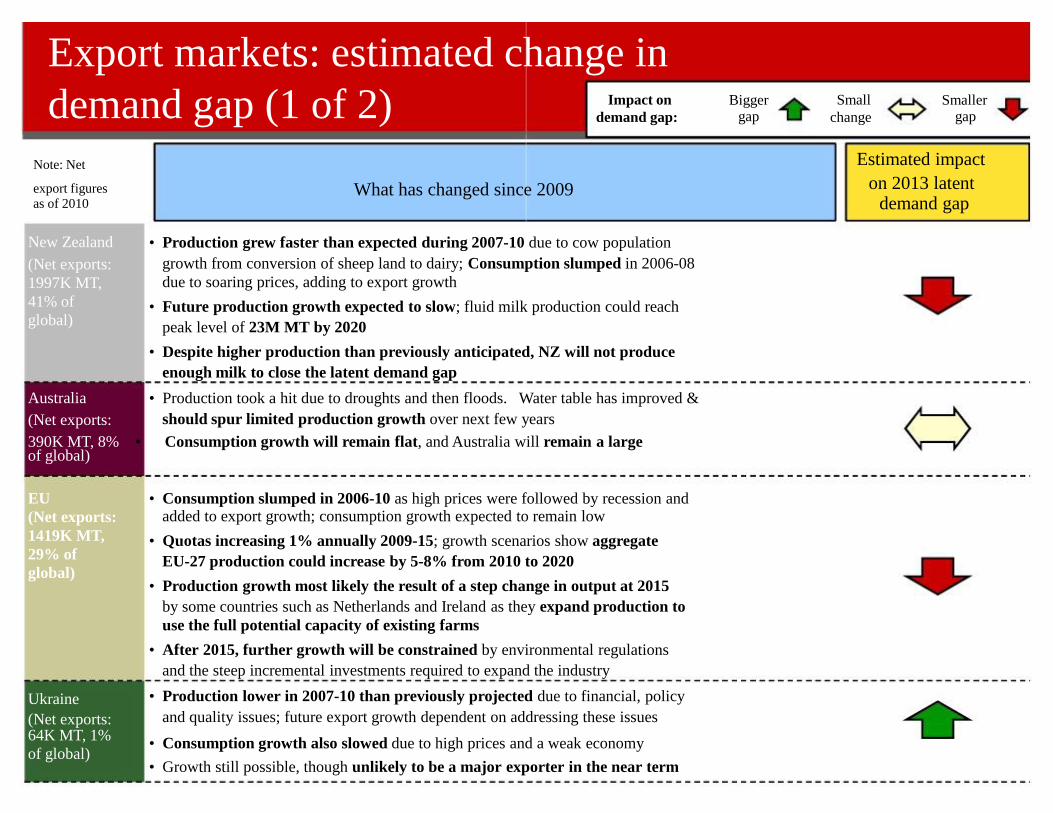

Export markets: estimated change in

demand gap (1 of 2)

EU

(Net exports:

1419K MT,

29% of

global) Ukraine

(Net exports: 64K MT, 1%

of global) • Consumption growth also slowed due to high prices and a weak economy

• Growth still possible, though unlikely to be a major exporter in the near term

Note: Net

export figures as of 2010 New Zealand

(Net exports:

1997K MT,

41% of

global) Australia

(Net exports:

What has changed since 2009 • Production grew faster than expected during 2007-10 due to cow population

growth from conversion of sheep land to dairy; Consumption slumped in 2006-08

due to soaring prices, adding to export growth

• Future production growth expected to slow; fluid milk production could reach

peak level of 23M MT by 2020

• Despite higher production than previously anticipated, NZ will not produce

enough milk to close the latent demand gap

• Production took a hit due to droughts and then floods. Water table has improved &

should spur limited production growth over next few years

390K MT, 8% • Consumption growth will remain flat, and Australia will remain a large of global)

• Consumption slumped in 2006-10 as high prices were followed by recession and added to export growth; consumption growth expected to remain low

• Quotas increasing 1% annually 2009-15; growth scenarios show aggregate

EU-27 production could increase by 5-8% from 2010 to 2020

• Production growth most likely the result of a step change in output at 2015

by some countries such as Netherlands and Ireland as they expand production to

use the full potential capacity of existing farms

• After 2015, further growth will be constrained by environmental regulations

and the steep incremental investments required to expand the industry

• Production lower in 2007-10 than previously projected due to financial, policy

and quality issues; future export growth dependent on addressing these issues

Estimated impact

on 2013 latent demand gap

Bigger gap

Small

change

Smaller gap

Impact on

demand gap:

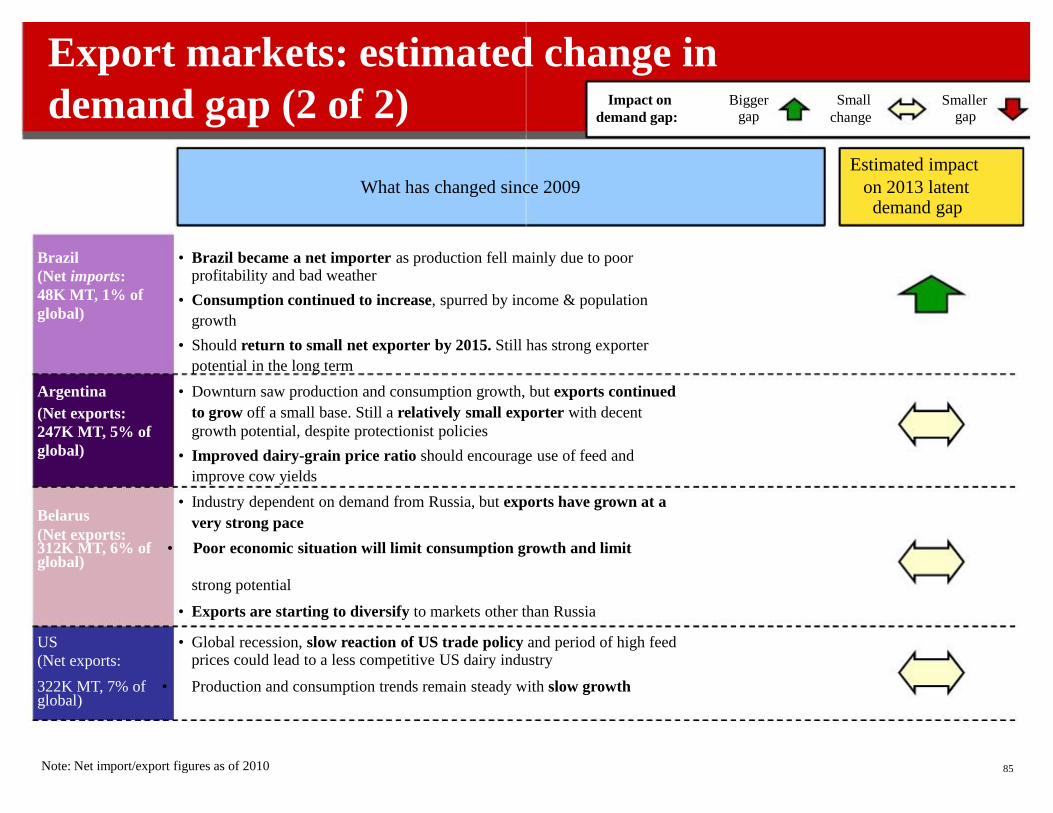

Export markets: estimated change in

demand gap (2 of 2)

Brazil

(Net imports:

48K MT, 1% of

global) Argentina

(Net exports:

247K MT, 5% of

global)

Belarus

(Net exports: 312K MT, 6% of • Poor economic situation will limit consumption growth and limit global)

strong potential

• Exports are starting to diversify to markets other than Russia

US

(Net exports:

What has changed since 2009

Note: Net import/export figures as of 2010

85

• Brazil became a net importer as production fell mainly due to poor profitability and bad weather

• Consumption continued to increase, spurred by income & population

growth

• Should return to small net exporter by 2015. Still has strong exporter

potential in the long term

• Downturn saw production and consumption growth, but exports continued

to grow off a small base. Still a relatively small exporter with decent

growth potential, despite protectionist policies

• Improved dairy-grain price ratio should encourage use of feed and

improve cow yields

• Industry dependent on demand from Russia, but exports have grown at a

very strong pace

• Global recession, slow reaction of US trade policy and period of high feed prices could lead to a less competitive US dairy industry

322K MT, 7% of • Production and consumption trends remain steady with slow growth global)

Estimated impact

on 2013 latent demand gap

Bigger gap

Small

change

Smaller gap

Impact on

demand gap:

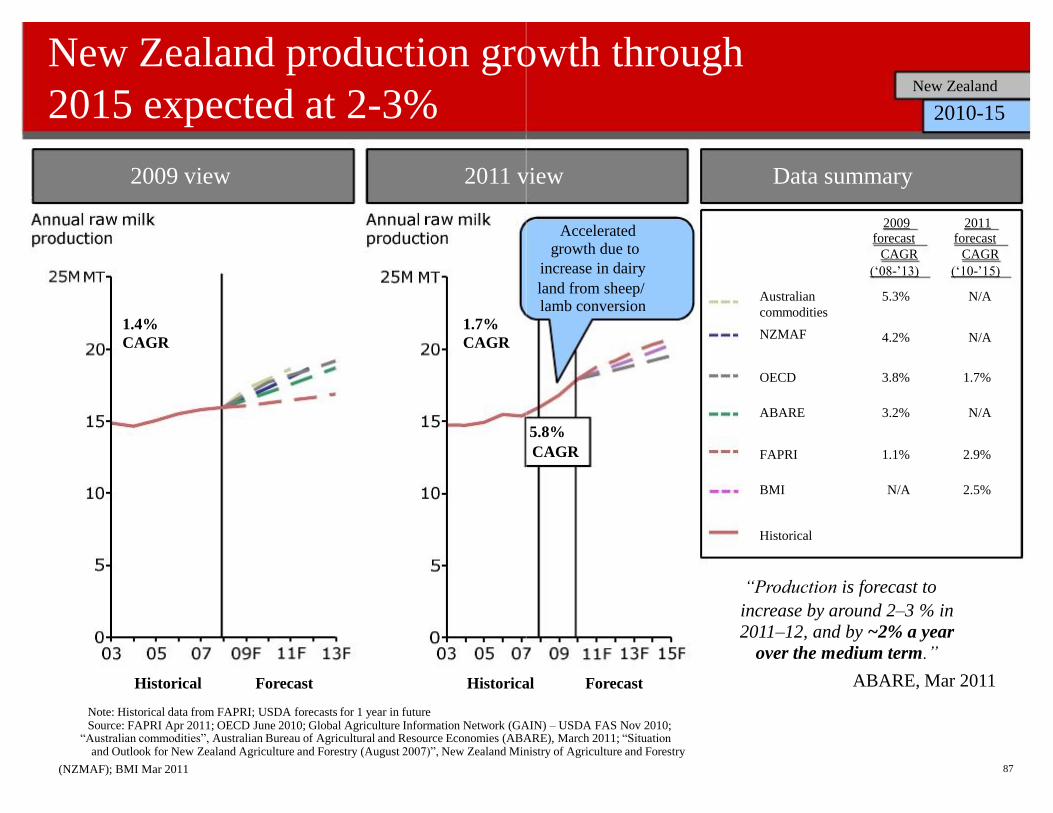

Summary: New Zealand

population growth of 2% and an expected yield increase of ~1%

• Due largely to land conversion, raw milk production expected to approach

peak of 23M MT by 2020, with very slow to flat growth thereafter

-Estimated 2020 production implies 27% expansion above 2010 levels (~2% CAGR), which is dependent on environmental regulation remaining weak and continued strong

milk prices vs. competing sheep/beef prices to support land conversion

-Beyond 2020, yield improvements likely to be the sole source of production growth,

which is expected to be very slow to flat

prices, mostly on butter and cheese

86

• Mid-term production growth is expected at 2-3% CAGR, driven by cow

• Non-fluid consumption fell by nearly 25% from 2006-08 due to soaring

New Zealand

New Zealand production growth through

2015 expected at 2-3%

2009 view 2011 view

1.4%

CAGR

1.7%

CAGR

Forecast Historical Historical

(NZMAF); BMI Mar 2011

87

Note: Historical data from FAPRI; USDA forecasts for 1 year in future Source: FAPRI Apr 2011; OECD June 2010; Global Agriculture Information Network (GAIN) – USDA FAS Nov 2010;

“Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE), March 2011; “Situation and Outlook for New Zealand Agriculture and Forestry (August 2007)”, New Zealand Ministry of Agriculture and Forestry

Data summary

2009 forecast

CAGR

(‘08-’13)

2011 forecast

CAGR

(‘10-’15)

Australian

commodities

NZMAF

5.3% 4.2%

N/A N/A

OECD ABARE

3.8% 3.2%

1.7% N/A

FAPRI BMI

1.1% N/A

2.9% 2.5%

Forecast

5.8%

CAGR

New Zealand

2010-15

Accelerated growth due to

increase in dairy

land from sheep/ lamb conversion

Historical

“Production is forecast to

increase by around 2–3 % in

2011–12, and by ~2% a year

over the medium term.”

ABARE, Mar 2011

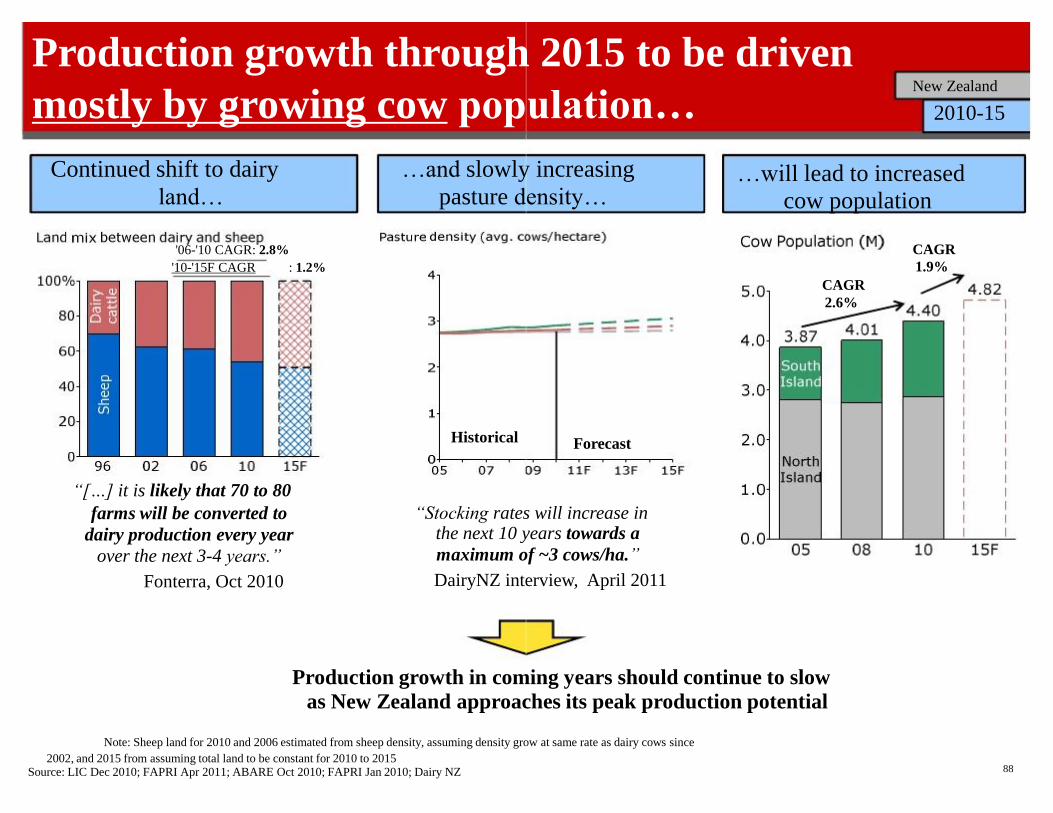

Production growth through 2015 to be driven

mostly by growing cow population…

Continued shift to dairy

land… '06-'10 CAGR: 2.8%

'10-'15F CAGR : 1.2%

“[…] it is likely that 70 to 80

farms will be converted to

dairy production every year

over the next 3-4 years.”

Fonterra, Oct 2010

Production growth in coming years should continue to slow

as New Zealand approaches its peak production potential

Note: Sheep land for 2010 and 2006 estimated from sheep density, assuming density grow at same rate as dairy cows since

2002, and 2015 from assuming total land to be constant for 2010 to 2015 Source: LIC Dec 2010; FAPRI Apr 2011; ABARE Oct 2010; FAPRI Jan 2010; Dairy NZ

88

…will lead to increased

cow population CAGR

1.9%

CAGR

2.6%

…and slowly increasing

pasture density… Historical Forecast

“Stocking rates will increase in the next 10 years towards a

maximum of ~3 cows/ha.”

DairyNZ interview, April 2011

New Zealand

2010-15

0

3 2

5MT

03 05 07 09 11F 13F 15F

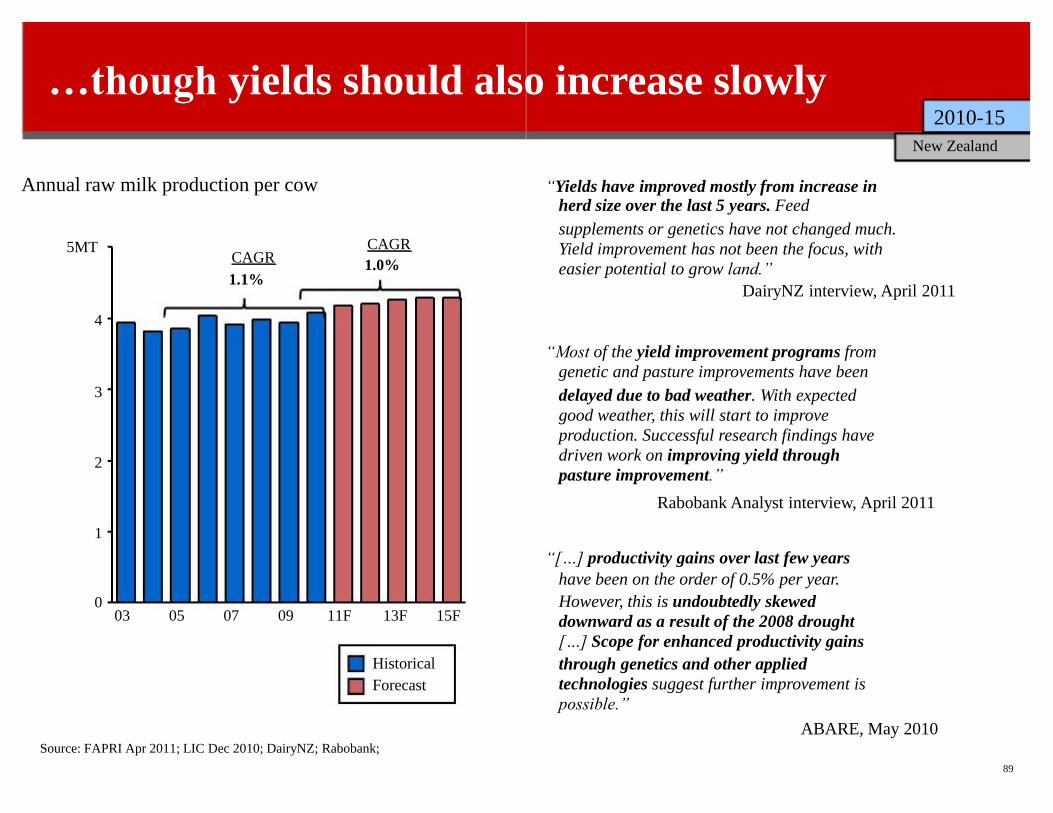

Annual raw milk production per cow

CAGR

1.1%

CAGR

1.0%

Historical

Forecast

89

“Yields have improved mostly from increase in herd size over the last 5 years. Feed

supplements or genetics have not changed much.

Yield improvement has not been the focus, with

easier potential to grow land.”

DairyNZ interview, April 2011

4 “Most of the yield improvement programs from

genetic and pasture improvements have been

delayed due to bad weather. With expected

good weather, this will start to improve

production. Successful research findings have

driven work on improving yield through

pasture improvement.”

Rabobank Analyst interview, April 2011 1

“[…] productivity gains over last few years

have been on the order of 0.5% per year.

However, this is undoubtedly skewed

downward as a result of the 2008 drought

[…] Scope for enhanced productivity gains

through genetics and other applied

technologies suggest further improvement is

possible.”

ABARE, May 2010 Source: FAPRI Apr 2011; LIC Dec 2010; DairyNZ; Rabobank;

…though yields should also increase slowly 2010-15

New Zealand

Source: Fonterra; Navigate analysis

90

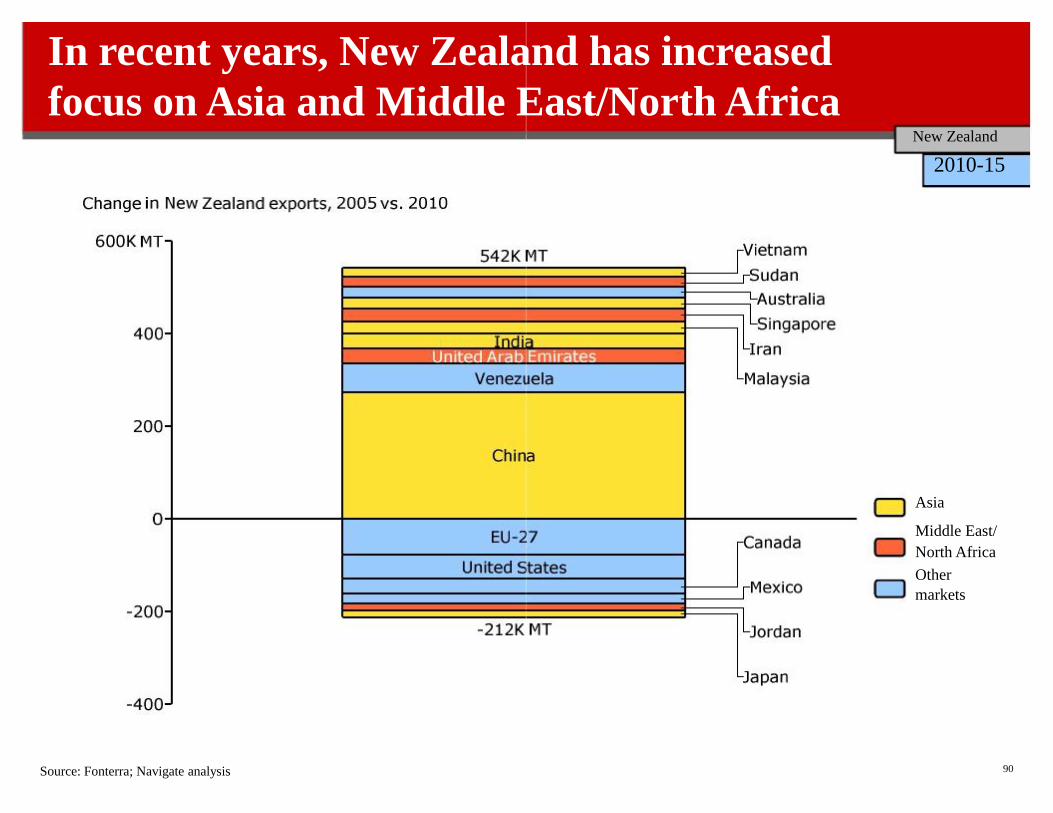

In recent years, New Zealand has increased

focus on Asia and Middle East/North Africa New Zealand

2010-15 Asia

Middle East/

North Africa

Other

markets

Constrained by several factors, dairy land

growth should reach peak by 2020

0.0

1.5 1.0 0.5

2.0

05

1.4 South

Island North

Island

10

1.6

15F 20F Peak

1.7

0.8%

CAGR 1.7

“We expect land growth to slow down in

this decade.”

DairyNZ interview, April 2011

Dairy land likely to grow slowly beyond 2015 and peak around 2020 Dairy Land (M Hectares)

1.2%

CAGR 2.1%

CAGR

Source: LIC Dec 2010, Dairy NZ, Lit. search, Navigate Analysis 91

difficult, as are tighter environmental rules […]

successful implementation of proposed irrigation

schemes would open up new areas to dairying. Its

rejection would curtail that expansion […]

New Zealand

2015+

Several factors are expected to constrain further land growth beyond 2020 “The end of cheap credit is making conversion

[…] if the profitability of sheep and beef farmers was to improve, that would also stop the drift of land to

dairying as many farmers felt forced to convert

to dairying for succession & viability issues but

preferred lifestyle of farming sheep & beef…”

Otago Daily Times, Oct 2010 “If agriculture were to be included in emission

trading scheme, the annual cost to the average

dairy farm would be NZ $3,900… Nitrogen leaching into water systems causes

degradation to water quality. There will likely be

many initiatives to limit this.”

NZ Dairy, Nov 2010

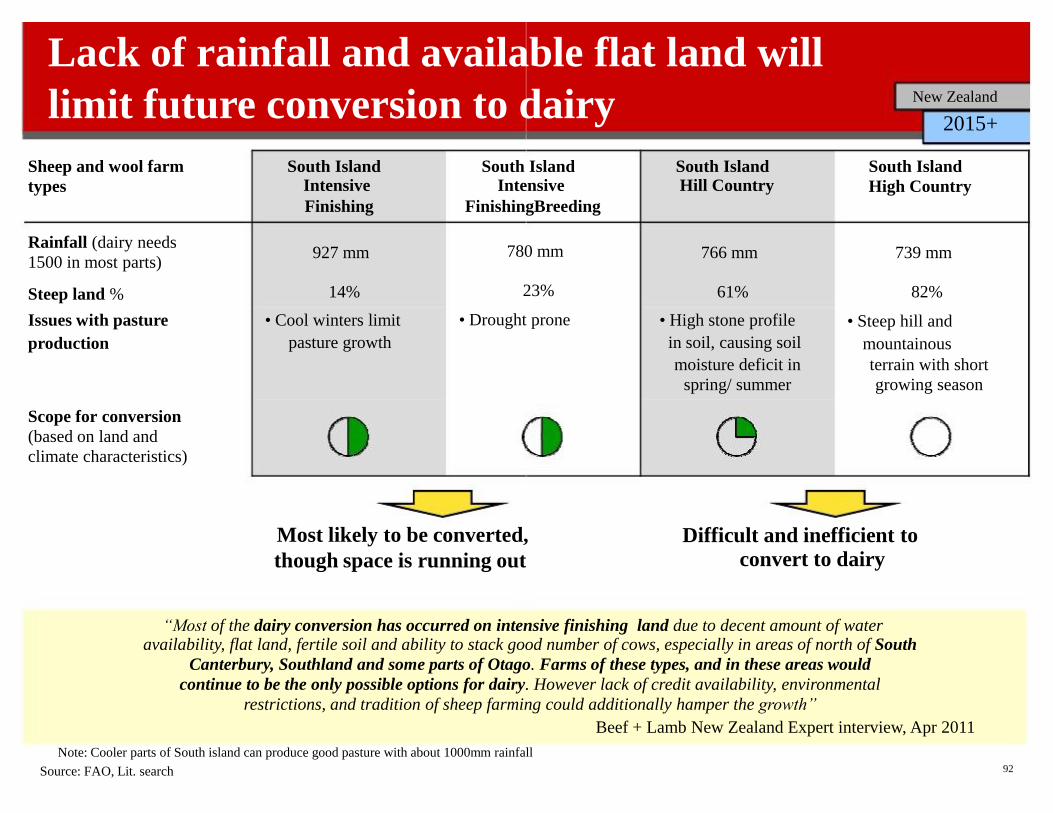

Sheep and wool farm

types

South Island Intensive

Finishing

South Island Intensive

FinishingBreeding

Rainfall (dairy needs

1500 in most parts) Steep land %

Issues with pasture

production

927 mm 14%

• Cool winters limit

pasture growth

780 mm 23%

• Drought prone

Scope for conversion

(based on land and

climate characteristics)

Source: FAO, Lit. search

92

Lack of rainfall and available flat land will

limit future conversion to dairy New Zealand

2015+

South Island Hill Country

South Island

High Country

766 mm 61%

• High stone profile

in soil, causing soil

moisture deficit in

spring/ summer

739 mm 82%

• Steep hill and

mountainous

terrain with short

growing season

“Most of the dairy conversion has occurred on intensive finishing land due to decent amount of water availability, flat land, fertile soil and ability to stack good number of cows, especially in areas of north of South

Canterbury, Southland and some parts of Otago. Farms of these types, and in these areas would

continue to be the only possible options for dairy. However lack of credit availability, environmental

restrictions, and tradition of sheep farming could additionally hamper the growth”

Beef + Lamb New Zealand Expert interview, Apr 2011

Note: Cooler parts of South island can produce good pasture with about 1000mm rainfall

Most likely to be converted,

though space is running out

Difficult and inefficient to

convert to dairy

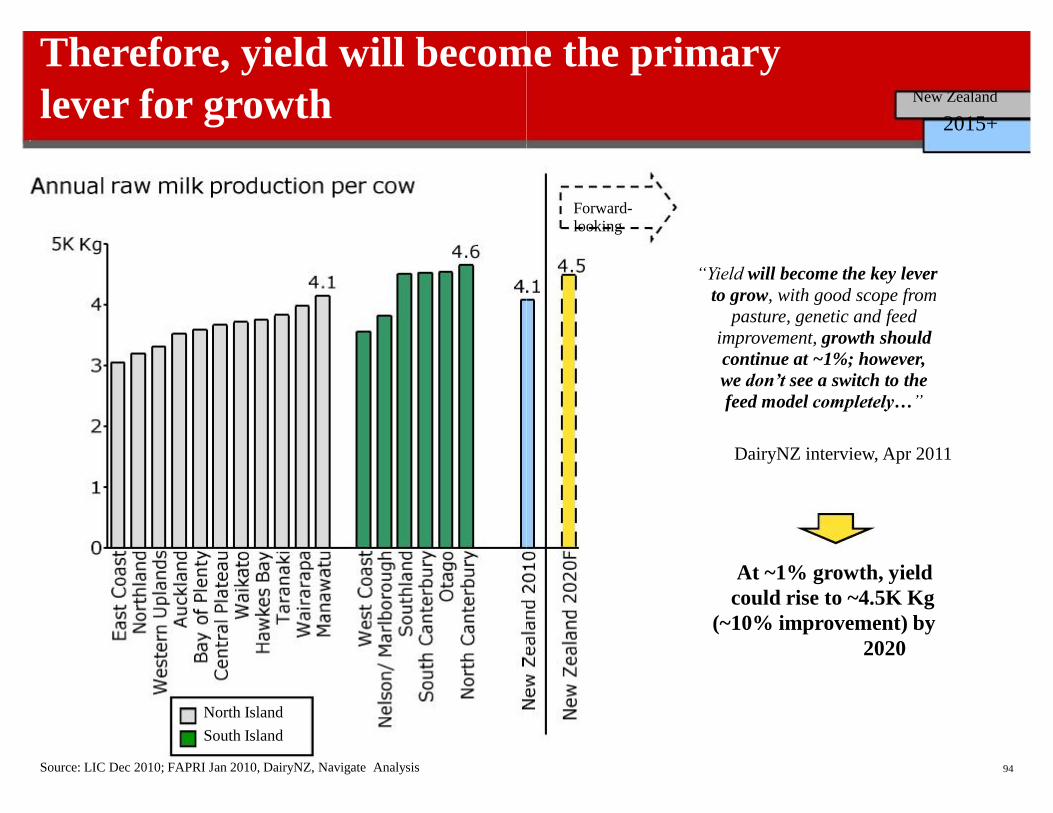

Therefore, yield will become the primary

lever for growth

Source: LIC Dec 2010; FAPRI Jan 2010, DairyNZ, Navigate Analysis

94

Forward- looking

“Yield will become the key lever

to grow, with good scope from

pasture, genetic and feed

improvement, growth should

continue at ~1%; however,

we don’t see a switch to the

feed model completely…” DairyNZ interview, Apr 2011

At ~1% growth, yield

could rise to ~4.5K Kg

(~10% improvement) by

2020 North Island

South Island

New Zealand

2015+

DIRECTIONAL 2.0%

CAGR 2.9%

CAGR

95 Source: LIC Dec 2010; DairyNZ, , Navigate Analysis; Lit. search

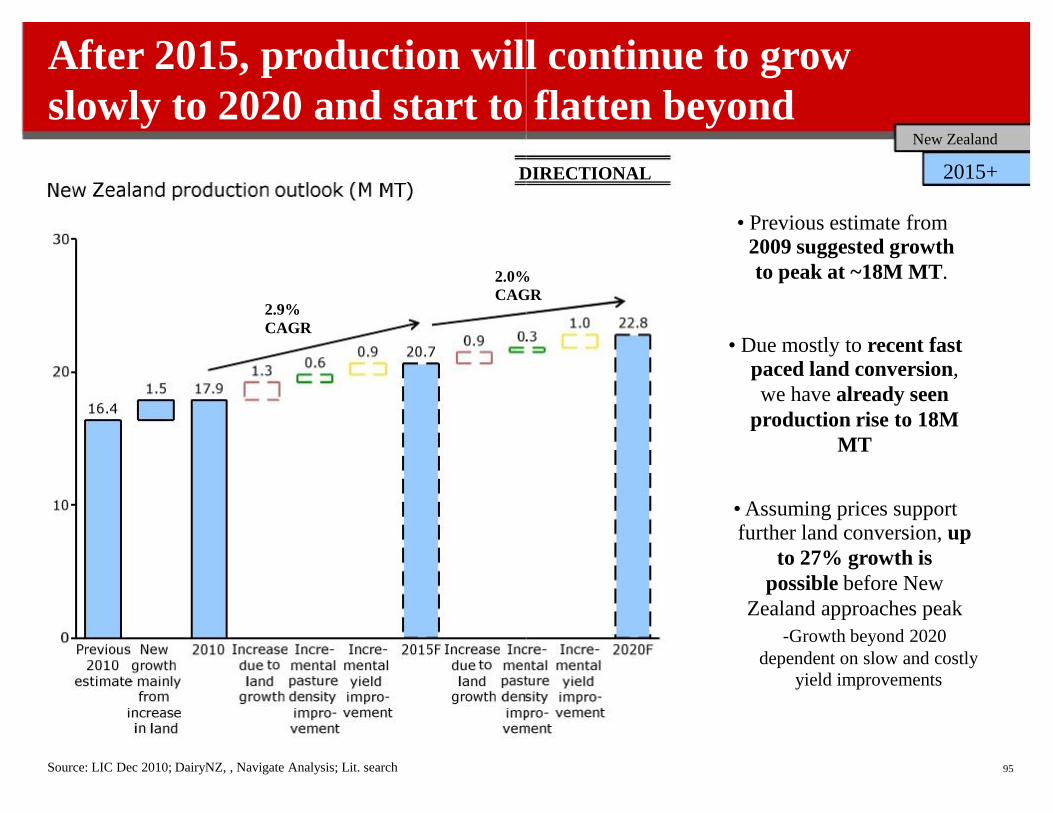

After 2015, production will continue to grow

slowly to 2020 and start to flatten beyond New Zealand

2015+

• Previous estimate from 2009 suggested growth

to peak at ~18M MT.

• Due mostly to recent fast

paced land conversion,

we have already seen

production rise to 18M

MT

• Assuming prices support further land conversion, up

to 27% growth is

possible before New

Zealand approaches peak

-Growth beyond 2020

dependent on slow and costly

yield improvements

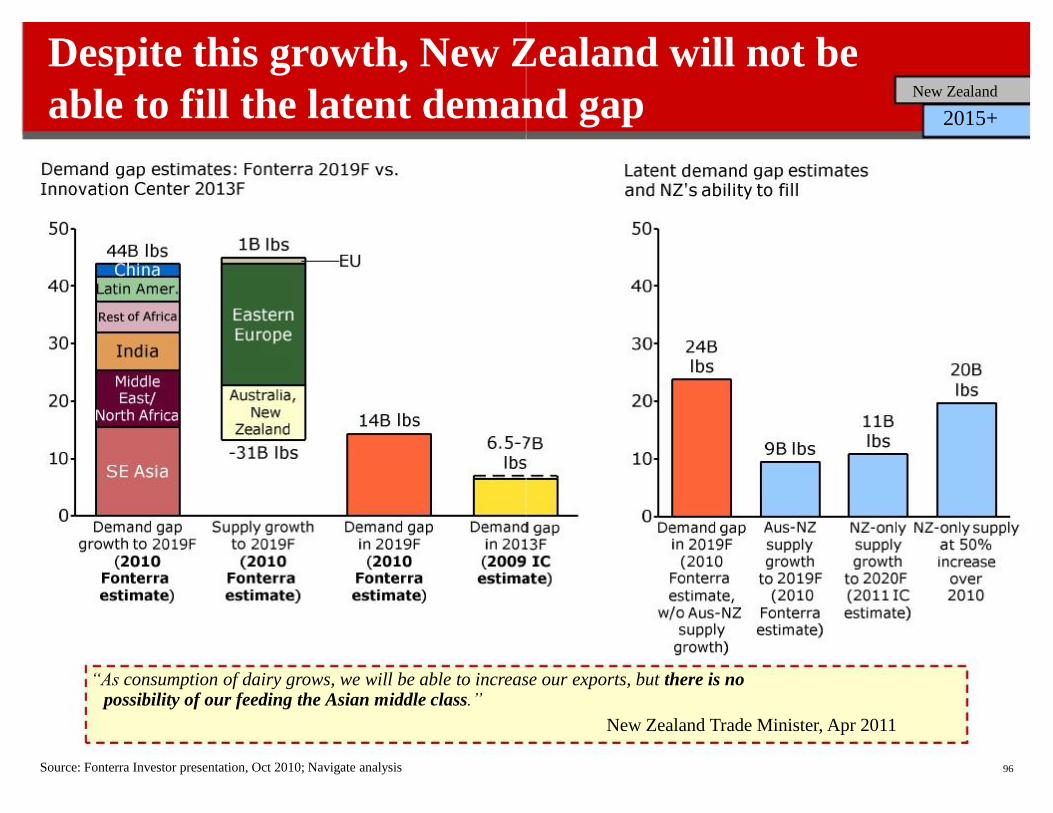

Despite this growth, New Zealand will not be

able to fill the latent demand gap

Source: Fonterra Investor presentation, Oct 2010; Navigate analysis

96

New Zealand

2015+

“As consumption of dairy grows, we will be able to increase our exports, but there is no possibility of our feeding the Asian middle class.”

New Zealand Trade Minister, Apr 2011

40 20

80K MT

Annual non-fluid dairy consumption

03 05 07 09F 11F 13F

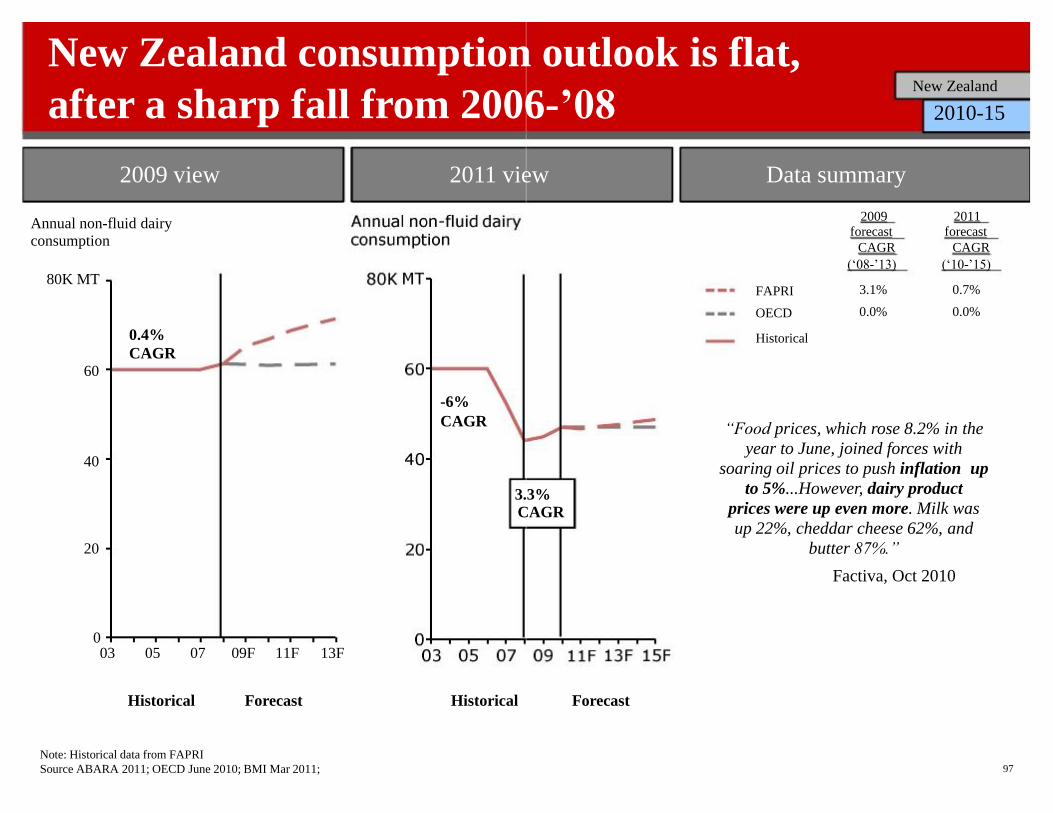

New Zealand consumption outlook is flat,

Note: Historical data from FAPRI

2009 view 2011 view

0.4%

CAGR 60 -6%

CAGR

Forecast Historical Historical

3.3% CAGR

Source ABARA 2011; OECD June 2010; BMI Mar 2011; 97

after a sharp fall from 2006-’08

Data summary

2009 forecast

CAGR

(‘08-’13)

2011 forecast

CAGR

(‘10-’15)

3.1%

0.0%

0.7%

0.0%

FAPRI

OECD

Historical

Forecast

“Food prices, which rose 8.2% in the

year to June, joined forces with

soaring oil prices to push inflation up

to 5%...However, dairy product

prices were up even more. Milk was

up 22%, cheddar cheese 62%, and

butter 87%.”

Factiva, Oct 2010 0

New Zealand

2010-15

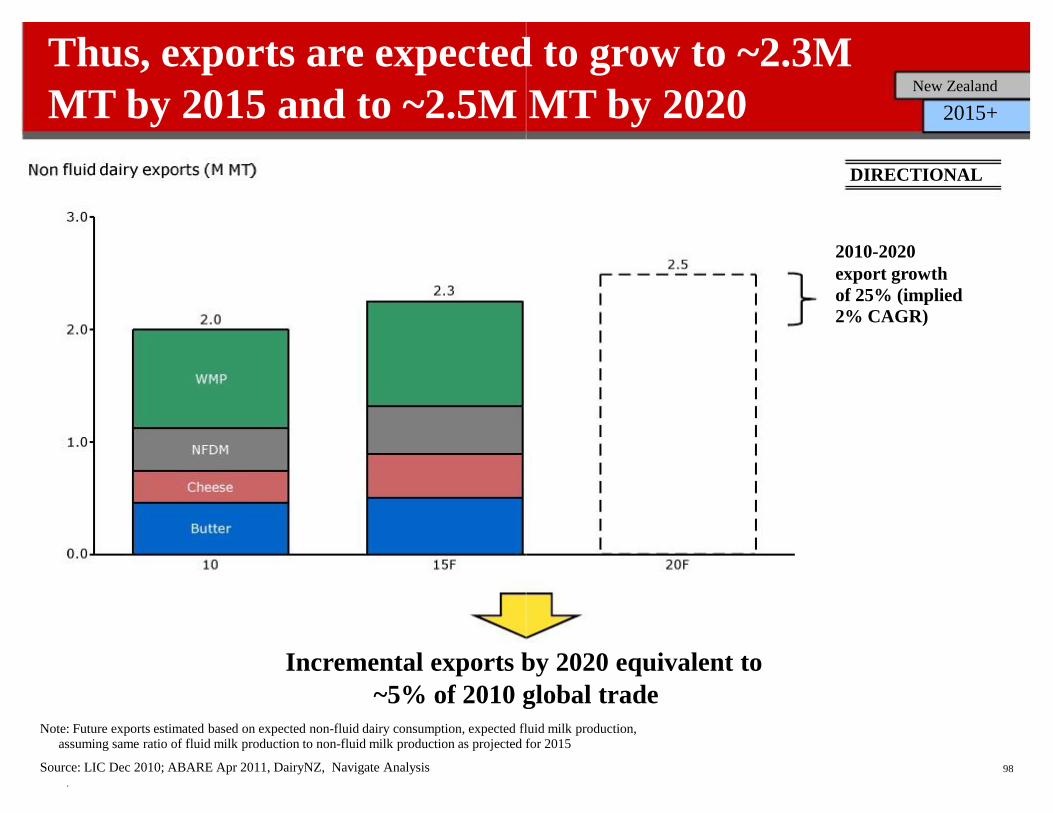

Thus, exports are expected to grow to ~2.3M

MT by 2015 and to ~2.5M MT by 2020

Source: LIC Dec 2010; ABARE Apr 2011, DairyNZ, Navigate Analysis .

98

DIRECTIONAL 2010-2020

export growth

of 25% (implied

2% CAGR) Incremental exports by 2020 equivalent to

~5% of 2010 global trade Note: Future exports estimated based on expected non-fluid dairy consumption, expected fluid milk production, assuming same ratio of fluid milk production to non-fluid milk production as projected for 2015

New Zealand

2015+

Summary: Australia

expected to grow at 1-2%

-Increments would be due to improved water availability in main dairying

regions from floods in 2010-2011

99

• Milk production declined during 2008-2010 by 1.3%, but is

-Milk production will be driven by increase in yield of ~1% p.a. driven by increased feeding of grains and forage crops, improved herd genetics as well

as advances in pasture management

• There is limited potential for Australia to grow beyond that due to

limited water, frequent bad weather spells and little potential to improve

yields

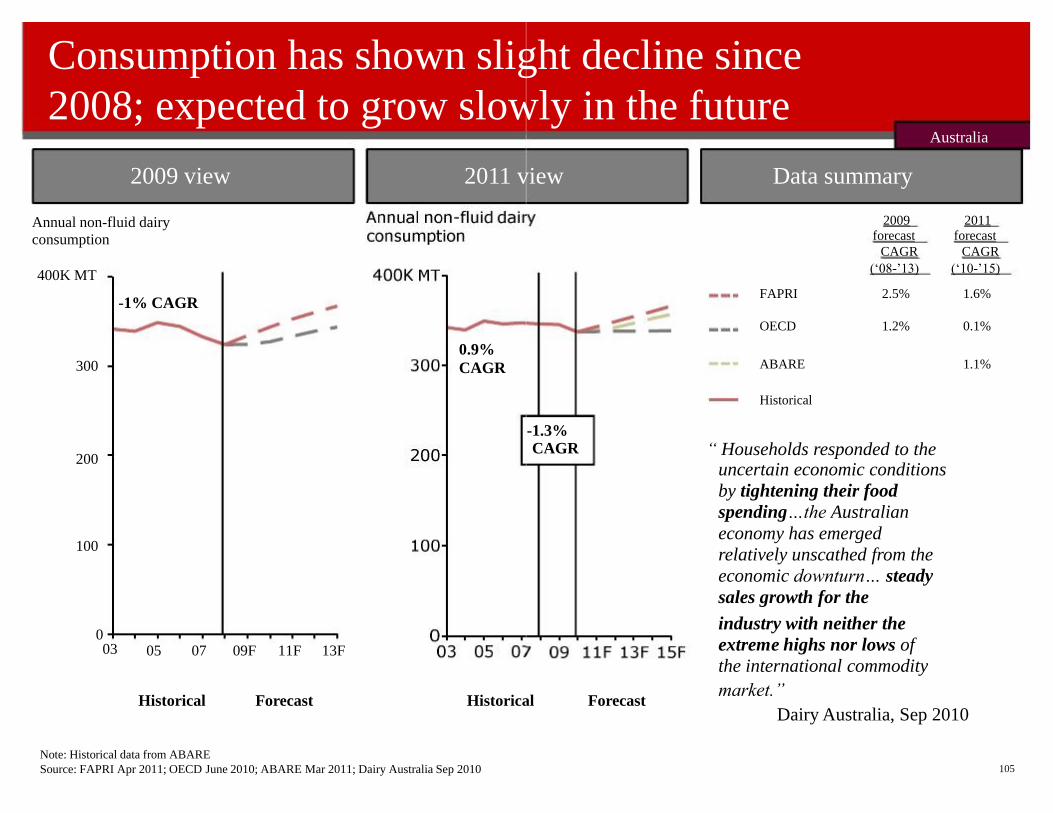

• Consumption has shown slight decline since ’08; expected to

grow slowly at ~1% in the future driven by population growth,

supported by growing incomes

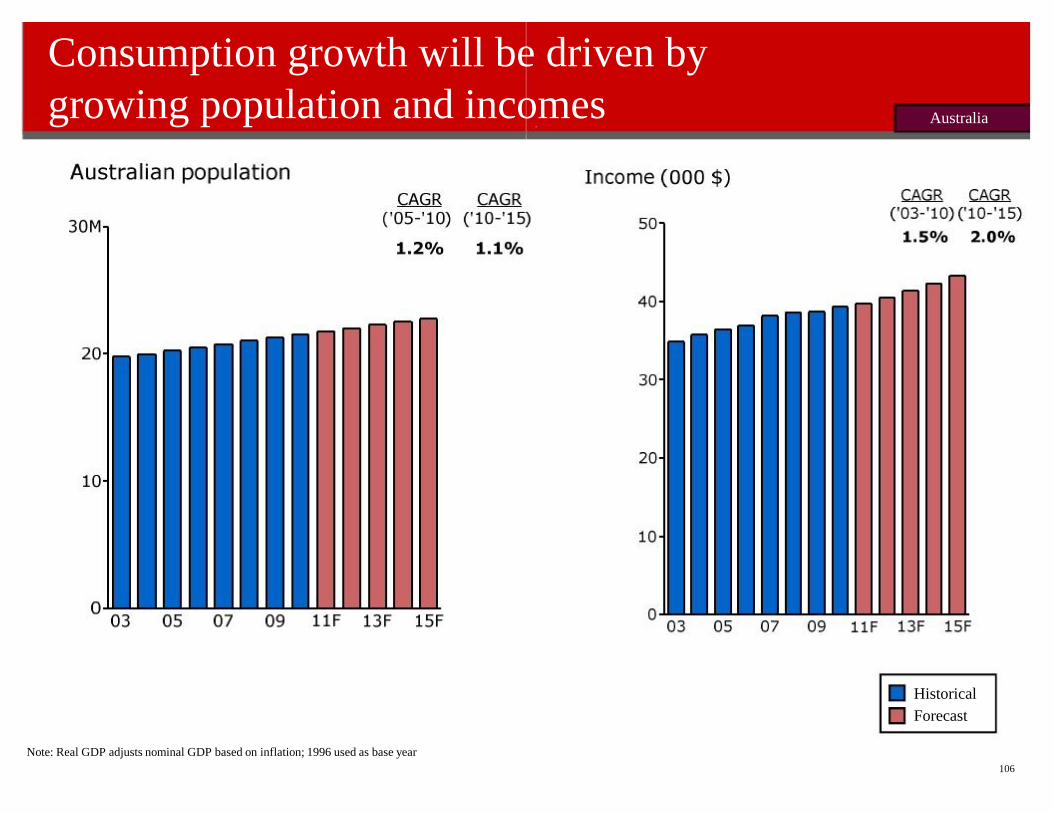

Australia

Australian raw milk production expected to

grow ~1.5%

Note: Historical data from ABARE Source: FAPRI Apr 2011; OECD June 2010, “Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE), March

2009 view 2011 view

-2.2%

CAGR

-1.8%

CAGR

Forecast Historical Historical

2011; Dairy Australia Sep 2010

.

100

Data summary

2009 forecast

CAGR

(‘08-’13)

2011 forecast

CAGR

(‘10-’15)

OECD Australian

commodities

3.3% 2.4%

1.8% 1.4%

Dairy

Australia FAPRI

2.1% 0.8%

NA 1.2%

Forecast

-1.3%

CAGR Historical “ Cow numbers will be the

limiting factor for growth.

Production should increase

by 1-2% in next 5 years”

Dairy Australia Interview, Apr

2011

South East

faced dry 2009 and wet 2010;

West Aus. had

drought in 2010

Australia

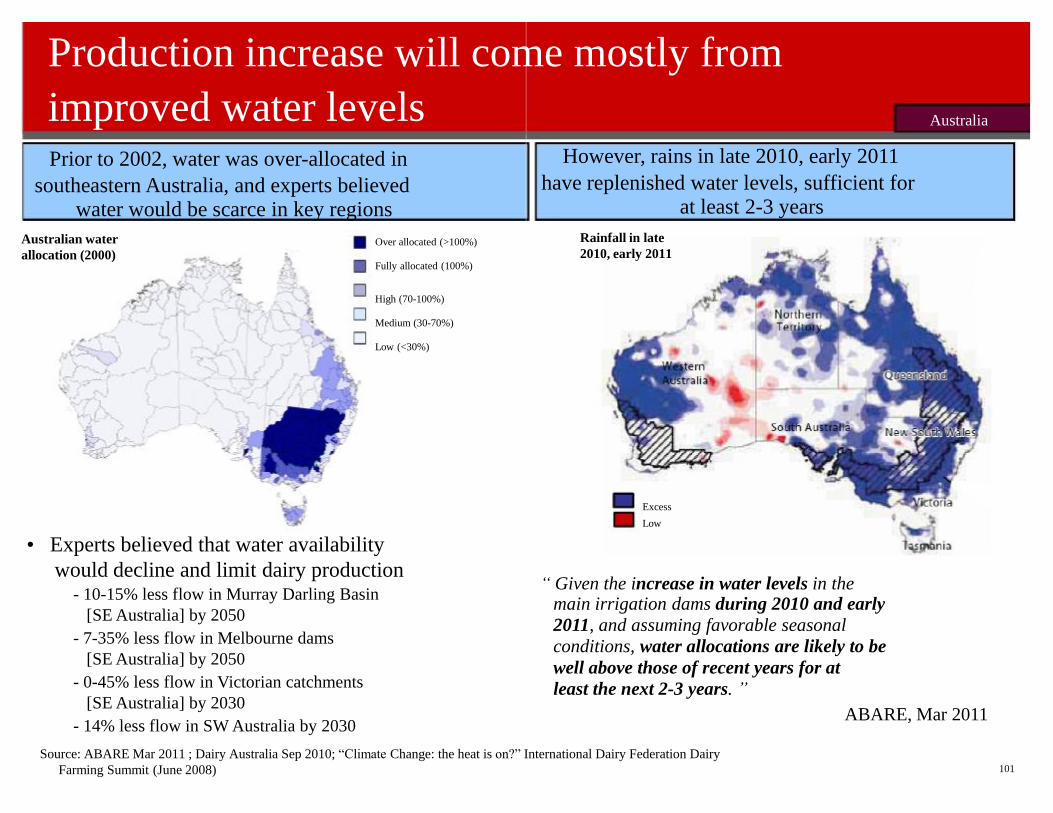

improved water levels Prior to 2002, water was over-allocated in

southeastern Australia, and experts believed water would be scarce in key regions

Australian water

allocation (2000) Over allocated (>100%)

Fully allocated (100%)

would decline and limit dairy production - 10-15% less flow in Murray Darling Basin

[SE Australia] by 2050

- 7-35% less flow in Melbourne dams

[SE Australia] by 2050

- 0-45% less flow in Victorian catchments

[SE Australia] by 2030

- 14% less flow in SW Australia by 2030

Farming Summit (June 2008)

101

Production increase will come mostly from

“ Given the increase in water levels in the main irrigation dams during 2010 and early

2011, and assuming favorable seasonal

conditions, water allocations are likely to be

well above those of recent years for at

least the next 2-3 years. ”

ABARE, Mar 2011

Source: ABARE Mar 2011 ; Dairy Australia Sep 2010; “Climate Change: the heat is on?” International Dairy Federation Dairy

High (70-100%)

Medium (30-70%)

Low (<30%)

Excess

Low

• Experts believed that water availability

Rainfall in late

2010, early 2011

Australia However, rains in late 2010, early 2011

have replenished water levels, sufficient for at least 2-3 years

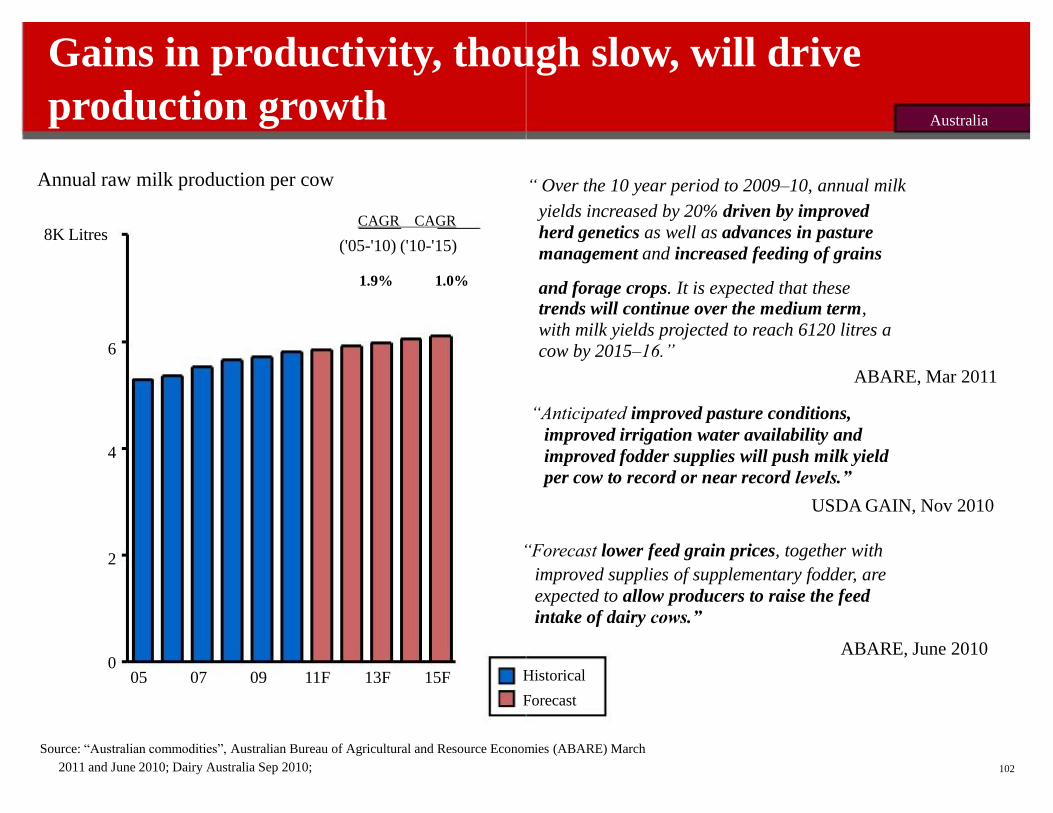

Gains in productivity, though slow, will drive

0

6 4 2

8K Litres

05 07 09 11F 13F 15F

production growth Annual raw milk production per cow

1.9% 1.0%

CAGR CAGR

('05-'10) ('10-'15)

Historical

Forecast Source: “Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE) March

2011 and June 2010; Dairy Australia Sep 2010; 102

yields increased by 20% driven by improved

herd genetics as well as advances in pasture

management and increased feeding of grains

ABARE, June 2010

and forage crops. It is expected that these trends will continue over the medium term,

with milk yields projected to reach 6120 litres a

cow by 2015–16.”

ABARE, Mar 2011 “Anticipated improved pasture conditions,

improved irrigation water availability and

improved fodder supplies will push milk yield

per cow to record or near record levels.”

USDA GAIN, Nov 2010 “Forecast lower feed grain prices, together with

improved supplies of supplementary fodder, are

expected to allow producers to raise the feed

intake of dairy cows.”

Australia “ Over the 10 year period to 2009–10, annual milk

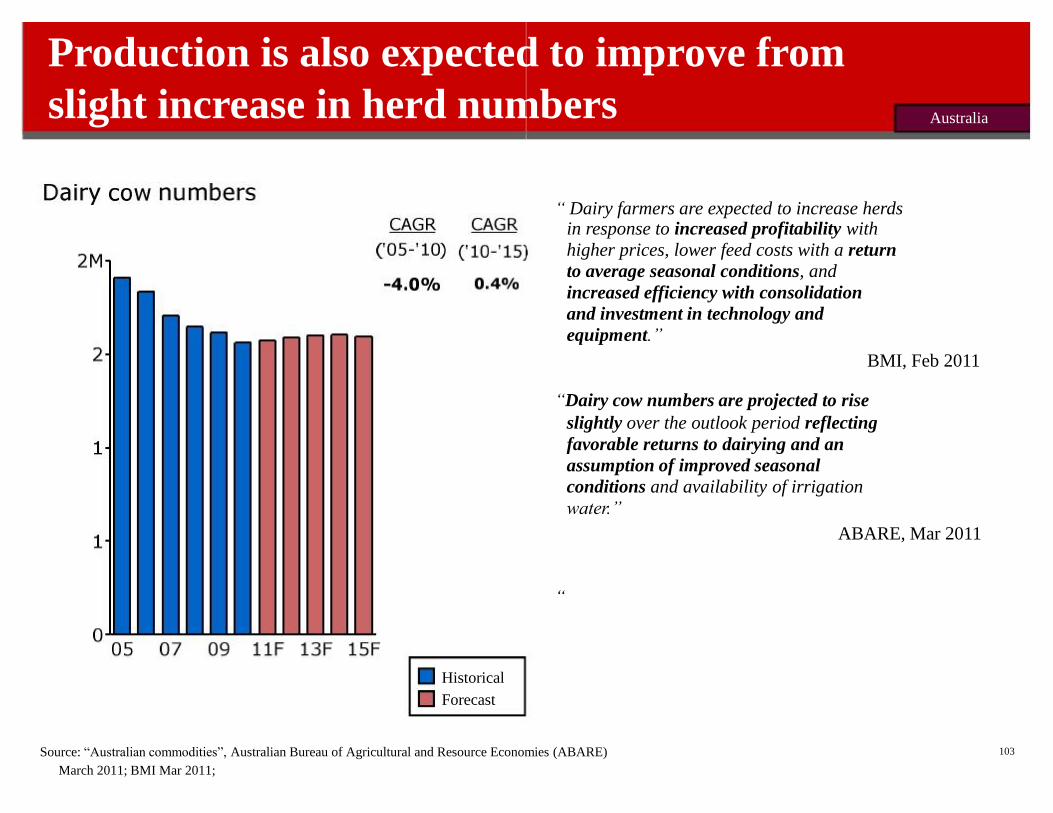

Production is also expected to improve from

slight increase in herd numbers

Historical

Forecast Source: “Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE)

March 2011; BMI Mar 2011;

“ Dairy farmers are expected to increase herds in response to increased profitability with

higher prices, lower feed costs with a return

to average seasonal conditions, and

increased efficiency with consolidation

and investment in technology and

equipment.”

BMI, Feb 2011 “Dairy cow numbers are projected to rise

slightly over the outlook period reflecting

favorable returns to dairying and an

assumption of improved seasonal

conditions and availability of irrigation

water.”

ABARE, Mar 2011 “

103

Australia

Dairy Australia Sep 2010; ABARE Nov 2010

104

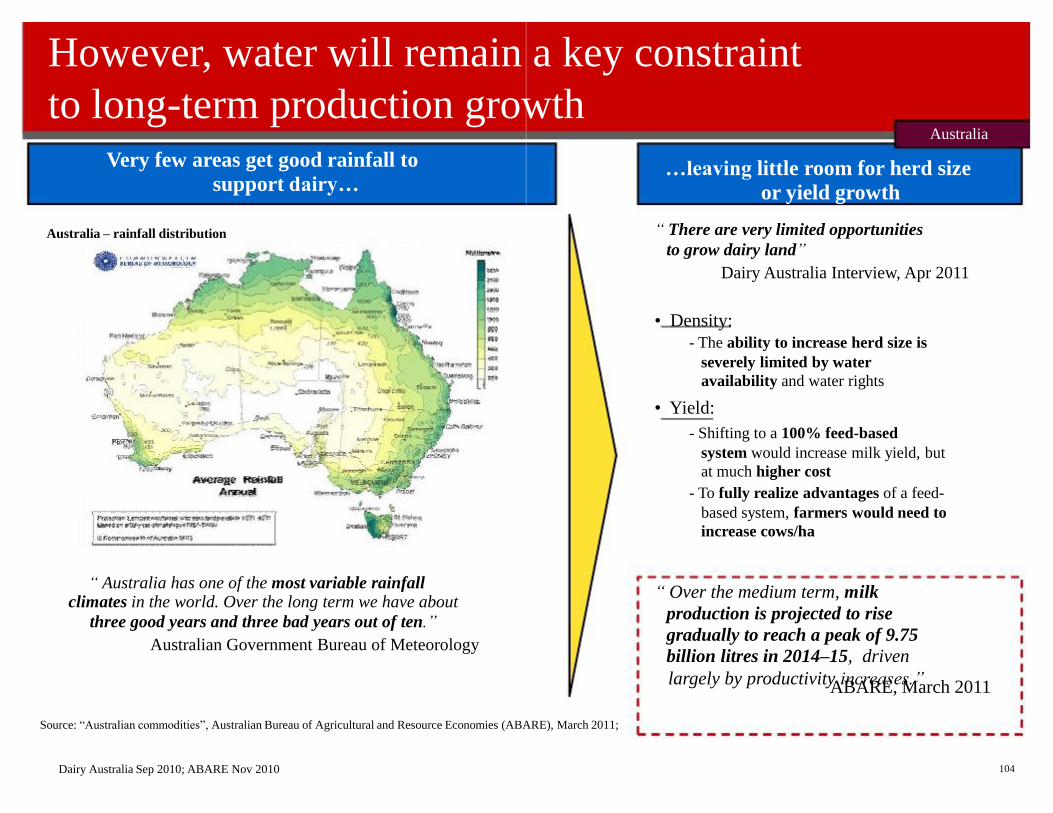

However, water will remain a key constraint

to long-term production growth

ABARE, March 2011 Source: “Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE), March 2011;

Very few areas get good rainfall to

support dairy… Australia – rainfall distribution

“ Australia has one of the most variable rainfall climates in the world. Over the long term we have about

three good years and three bad years out of ten.”

Australian Government Bureau of Meteorology

…leaving little room for herd size

or yield growth “ There are very limited opportunities

to grow dairy land”

Dairy Australia Interview, Apr 2011 • Density:

- The ability to increase herd size is

severely limited by water

availability and water rights

• Yield:

- Shifting to a 100% feed-based

system would increase milk yield, but

at much higher cost

- To fully realize advantages of a feed-

based system, farmers would need to

increase cows/ha “ Over the medium term, milk

production is projected to rise

gradually to reach a peak of 9.75

billion litres in 2014–15, driven

largely by productivity increases.”

Australia

200 100

300

Annual non-fluid dairy

consumption 400K MT

0 03 05 07 09F 11F 13F

Note: Historical data from ABARE

2009 view 2011 view

-1% CAGR

0.9%

CAGR

Forecast Historical Historical

Source: FAPRI Apr 2011; OECD June 2010; ABARE Mar 2011; Dairy Australia Sep 2010

105

Data summary

2009 forecast

CAGR

(‘08-’13)

2011 forecast

CAGR

(‘10-’15)

FAPRI OECD

2.5% 1.2%

1.6% 0.1%

ABARE 1.1%

Historical

Forecast

-1.3% CAGR “ Households responded to the

uncertain economic conditions

by tightening their food

spending…the Australian

economy has emerged

relatively unscathed from the

economic downturn… steady

sales growth for the

industry with neither the

extreme highs nor lows of

the international commodity

market.”

Dairy Australia, Sep 2010

Consumption has shown slight decline since

2008; expected to grow slowly in the future Australia

Consumption growth will be driven by

growing population and incomes

106

Historical

Forecast Note: Real GDP adjusts nominal GDP based on inflation; 1996 used as base year

Australia

Therefore, Australian exports are projected

Note: Historical data from ABARE Source: FAPRI Apr 2011; OECD June 2010, “Australian commodities”, Australian Bureau of Agricultural and Resource Economies (ABARE), March

400 200

to grow by 3-4%

Dairy net exports 600K MT

0 05 07 09 11F

2011; Dairy Australia Sep 2010

107

13F 15F

OECD Australian

commodities FAPRI

Historical “ Exports should see a 1-2%

increase over the next 5 years”

Dairy Australia Interview, Apr 2011

Australia 2011

forecast

CAGR

(‘10-’15) 4.7% 0.5%

2.5%

Contents

•Project objectives and summary findings

•Geography-specific findings

-Net importers

-Net exporters

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

180

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

181

Summary: buyers gave specific, consistent,

input on priorities for improvement

• Work more closely with them to better understand their needs • Make the commitment to be a consistent seller to global

markets

-Adjust underlying policy and regulatory influences to create proper

incentives to invest in relevant capacity

-Build direct organizations to market dairy ingredients to global buyers

-Develop a product portfolio that better meets buyers’ specs and quality

requirements

-Help buyers manage price volatility

-Remain committed to serve global buyers in good years and in bad

“These issues are addressable –

Australia has the potential to

become a major supplier.”

182

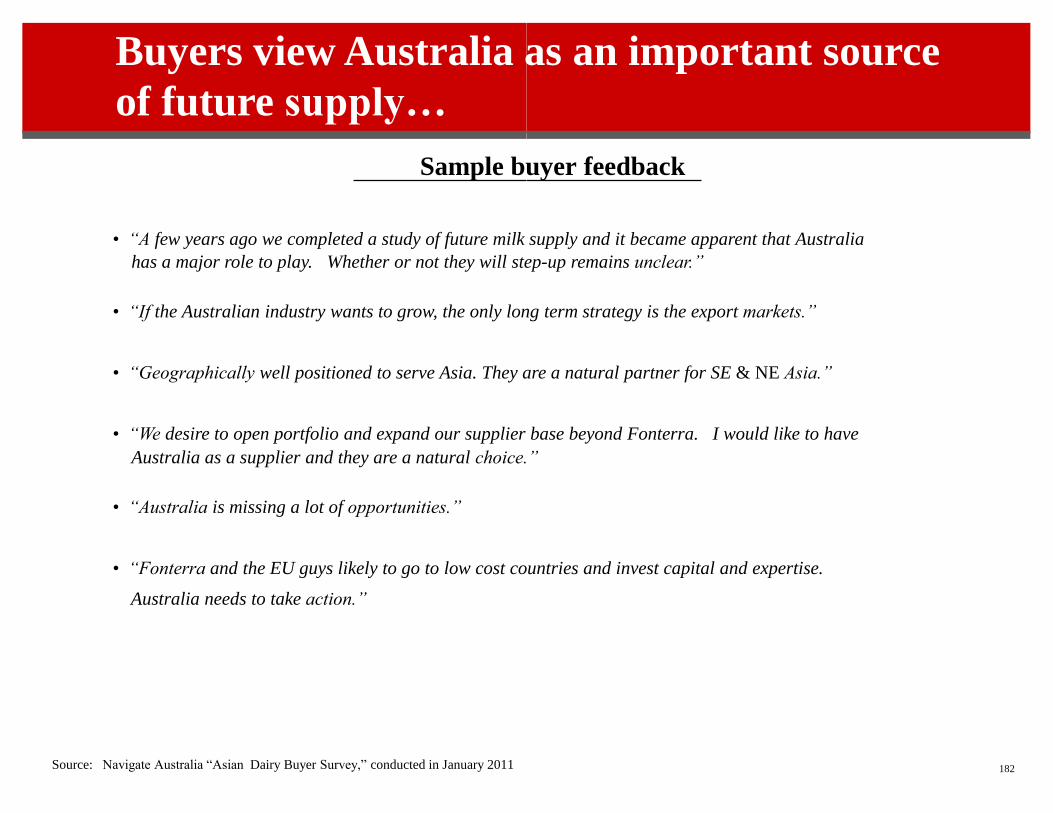

Buyers view Australia as an important source

of future supply… Sample buyer feedback • “A few years ago we completed a study of future milk supply and it became apparent that Australia

has a major role to play. Whether or not they will step-up remains unclear.”

• “If the Australian industry wants to grow, the only long term strategy is the export markets.”

• “Geographically well positioned to serve Asia. They are a natural partner for SE & NE Asia.”

• “We desire to open portfolio and expand our supplier base beyond Fonterra. I would like to have

Australia as a supplier and they are a natural choice.”

• “Australia is missing a lot of opportunities.”

• “Fonterra and the EU guys likely to go to low cost countries and invest capital and expertise.

Australia needs to take action.”

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

183

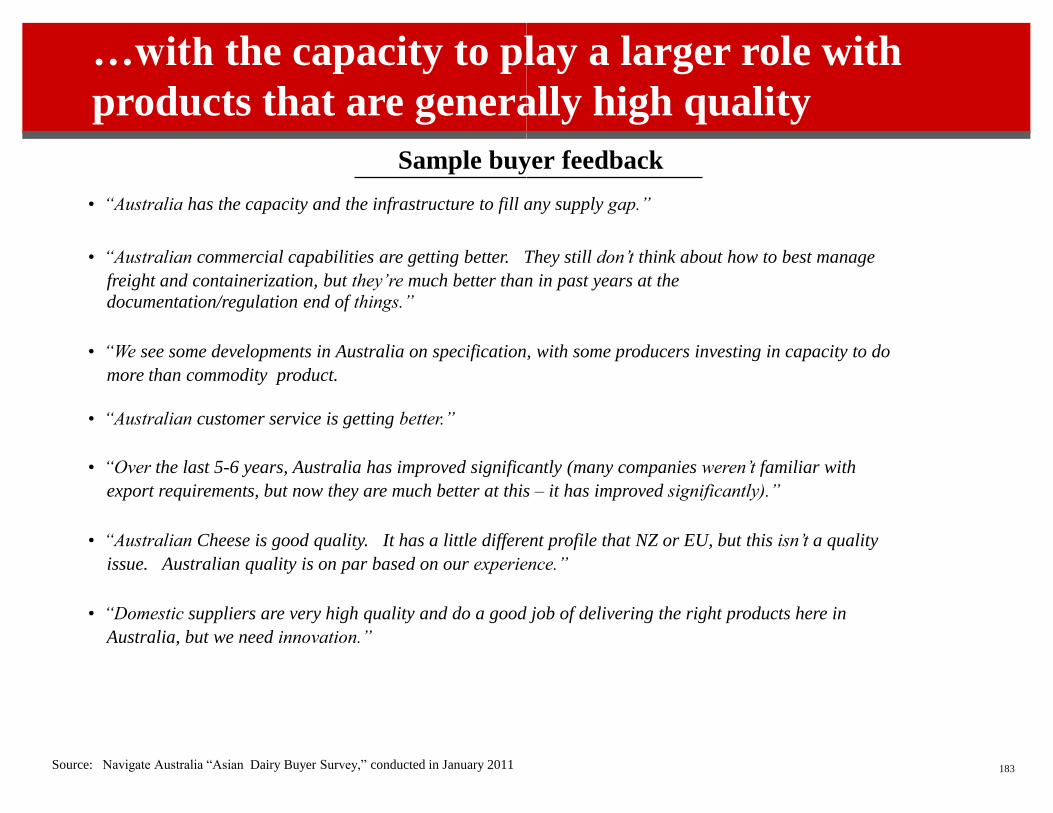

…with the capacity to play a larger role with

products that are generally high quality

Sample buyer feedback • “Australia has the capacity and the infrastructure to fill any supply gap.”

• “Australian commercial capabilities are getting better. They still don’t think about how to best manage

freight and containerization, but they’re much better than in past years at the

documentation/regulation end of things.”

• “We see some developments in Australia on specification, with some producers investing in capacity to do

more than commodity product.

• “Australian customer service is getting better.”

• “Over the last 5-6 years, Australia has improved significantly (many companies weren’t familiar with

export requirements, but now they are much better at this – it has improved significantly).”

• “Australian Cheese is good quality. It has a little different profile that NZ or EU, but this isn’t a quality

issue. Australian quality is on par based on our experience.”

• “Domestic suppliers are very high quality and do a good job of delivering the right products here in

Australia, but we need innovation.”

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

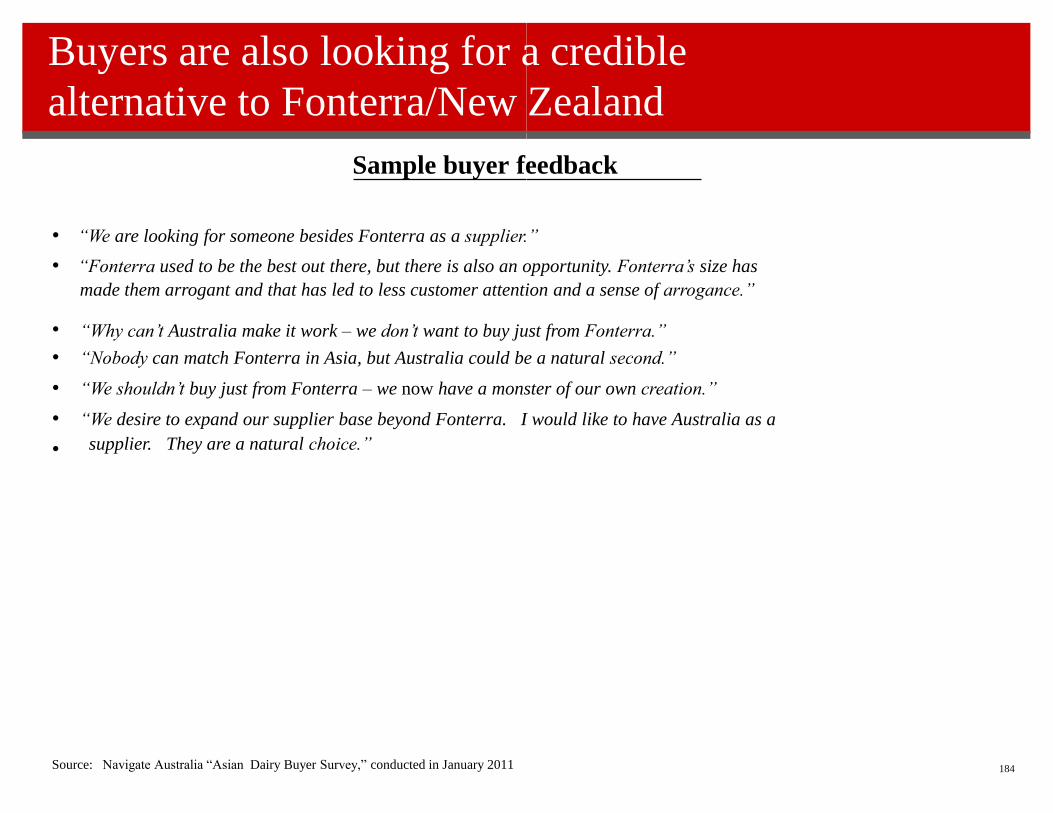

Buyers are also looking for a credible

alternative to Fonterra/New Zealand Sample buyer feedback • “We are looking for someone besides Fonterra as a supplier.”

• “Fonterra used to be the best out there, but there is also an opportunity. Fonterra’s size has

made them arrogant and that has led to less customer attention and a sense of arrogance.”

•

•

•

•

•

“Why can’t Australia make it work – we don’t want to buy just from Fonterra.”

“Nobody can match Fonterra in Asia, but Australia could be a natural second.”

“We shouldn’t buy just from Fonterra – we now have a monster of our own creation.”

“We desire to expand our supplier base beyond Fonterra. I would like to have Australia as a

supplier. They are a natural choice.”

184 Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

185

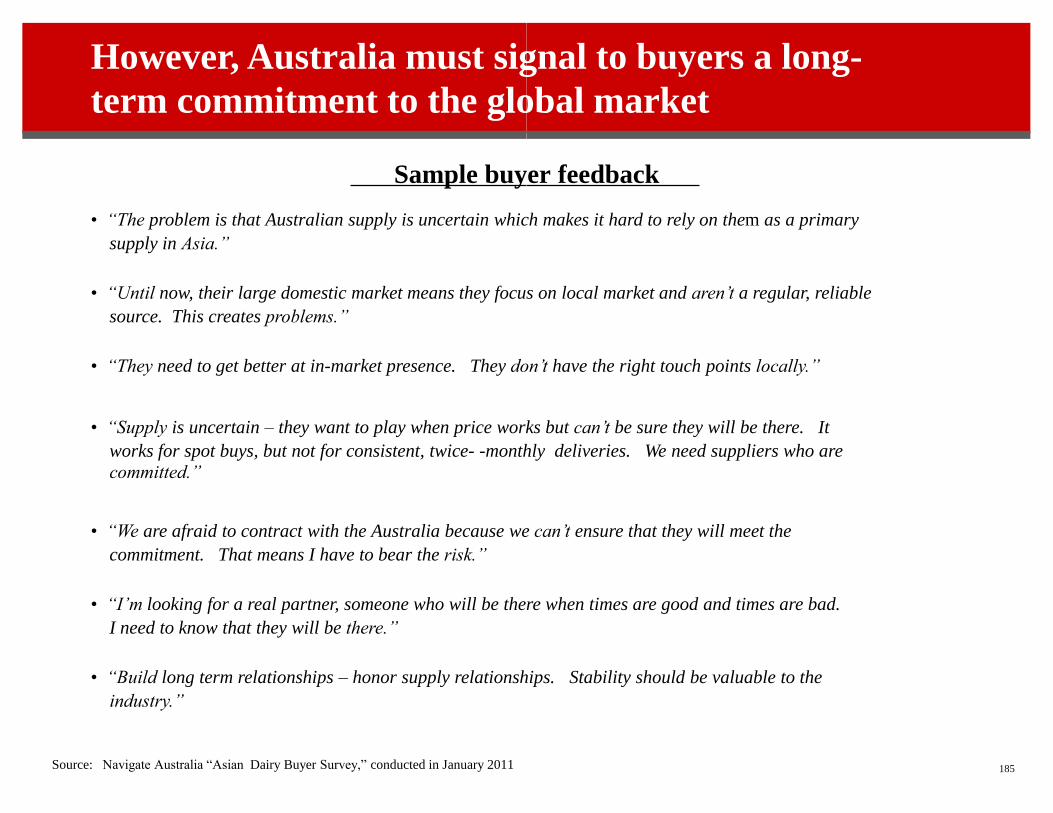

However, Australia must signal to buyers a long-

term commitment to the global market Sample buyer feedback • “The problem is that Australian supply is uncertain which makes it hard to rely on them as a primary

supply in Asia.”

• “Until now, their large domestic market means they focus on local market and aren’t a regular, reliable

source. This creates problems.”

• “They need to get better at in-market presence. They don’t have the right touch points locally.”

• “Supply is uncertain – they want to play when price works but can’t be sure they will be there. It

works for spot buys, but not for consistent, twice- -monthly deliveries. We need suppliers who are

committed.”

• “We are afraid to contract with the Australia because we can’t ensure that they will meet the

commitment. That means I have to bear the risk.”

• “I’m looking for a real partner, someone who will be there when times are good and times are bad.

I need to know that they will be there.”

• “Build long term relationships – honor supply relationships. Stability should be valuable to the

industry.”

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

186

This commitment requires Australian suppliers to

focus on meeting customer needs (1 of 2) Sample buyer feedback • “Most importantly, the Australia needs to figure out how to be more customer focused. Build to my requirements.”

• “If I can’t be sure that Australia will be a consistent source of supply, there is no way I can take the

risk of buying strategic inputs from them.”

• “Suppliers needs to have some responsibility in understanding and managing the market – very

reactive.”

• “Australia is friendly and well-intentioned, but struggle to deliver.”

• “Australia lacks product flexibility – hard to get Australian suppliers to make a unique spec.

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

187

This commitment requires Australian suppliers

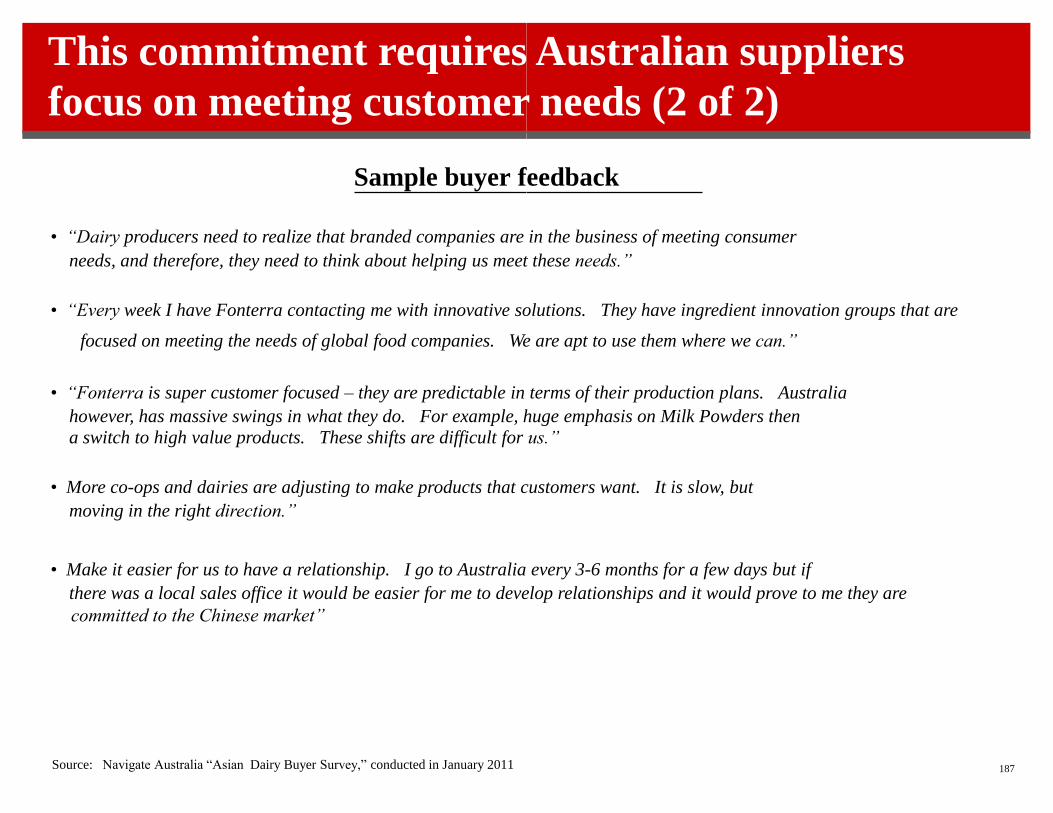

focus on meeting customer needs (2 of 2) Sample buyer feedback

• “Dairy producers need to realize that branded companies are in the business of meeting consumer

needs, and therefore, they need to think about helping us meet these needs.”

• “Every week I have Fonterra contacting me with innovative solutions. They have ingredient innovation groups that are

focused on meeting the needs of global food companies. We are apt to use them where we can.”

• “Fonterra is super customer focused – they are predictable in terms of their production plans. Australia

however, has massive swings in what they do. For example, huge emphasis on Milk Powders then

a switch to high value products. These shifts are difficult for us.”

• More co-ops and dairies are adjusting to make products that customers want. It is slow, but

moving in the right direction.”

• Make it easier for us to have a relationship. I go to Australia every 3-6 months for a few days but if

there was a local sales office it would be easier for me to develop relationships and it would prove to me they are

committed to the Chinese market”

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

189

…as well as pricing and risk management,

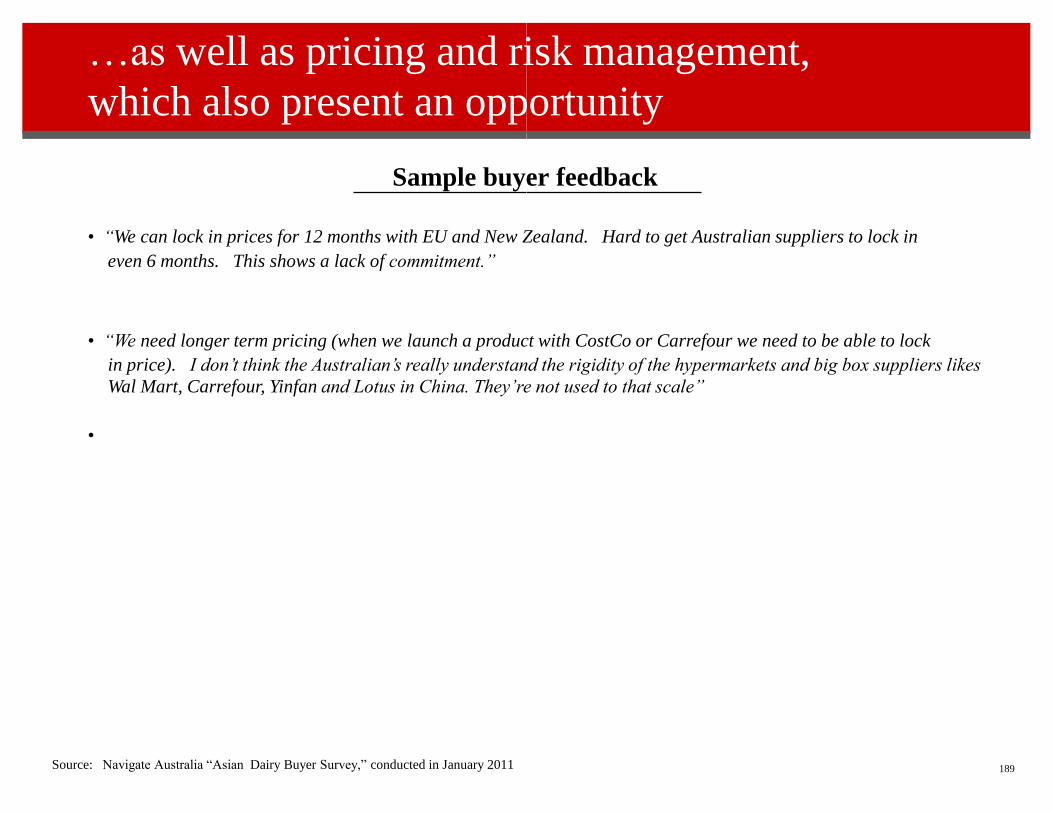

which also present an opportunity Sample buyer feedback

• “We can lock in prices for 12 months with EU and New Zealand. Hard to get Australian suppliers to lock in

even 6 months. This shows a lack of commitment.”

• “We need longer term pricing (when we launch a product with CostCo or Carrefour we need to be able to lock

in price). I don’t think the Australian’s really understand the rigidity of the hypermarkets and big box suppliers likes

Wal Mart, Carrefour, Yinfan and Lotus in China. They’re not used to that scale”

•

Source: Navigate Australia “Asian Dairy Buyer Survey,” conducted in January 2011

Contents

•Project objectives and summary findings

•Geography-specific findings

-Net importers

-Net exporters

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

190

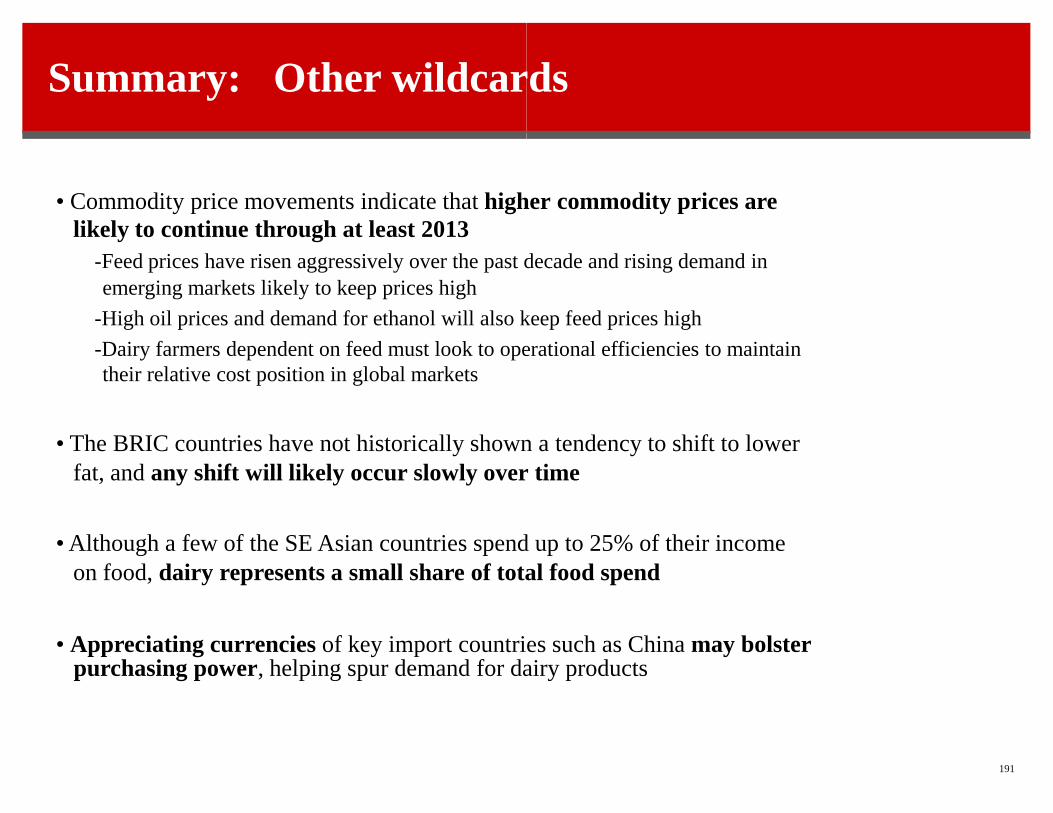

Summary: Other wildcards

likely to continue through at least 2013

-Feed prices have risen aggressively over the past decade and rising demand in

emerging markets likely to keep prices high

-High oil prices and demand for ethanol will also keep feed prices high

-Dairy farmers dependent on feed must look to operational efficiencies to maintain

their relative cost position in global markets

• The BRIC countries have not historically shown a tendency to shift to lower

fat, and any shift will likely occur slowly over time

• Although a few of the SE Asian countries spend up to 25% of their income

on food, dairy represents a small share of total food spend

191

• Commodity price movements indicate that higher commodity prices are

• Appreciating currencies of key import countries such as China may bolster purchasing power, helping spur demand for dairy products

Feed prices have risen quickly over the past

decade

Source: Bloomberg (2011)

192

Sta

rtin

g c

ost

(US

D/M

T)

Cost

incr

ease

du

e

to f

eed

% c

ash

cost

s fr

om

feed

2011F

aver

age

cost

s

Cost

incr

ease

du

e to

fee

d

% c

ash

cost

s fr

om

feed

2011F

larg

e fa

rm

cost

s

Sta

rtin

g

cost

(US

D/M

T)

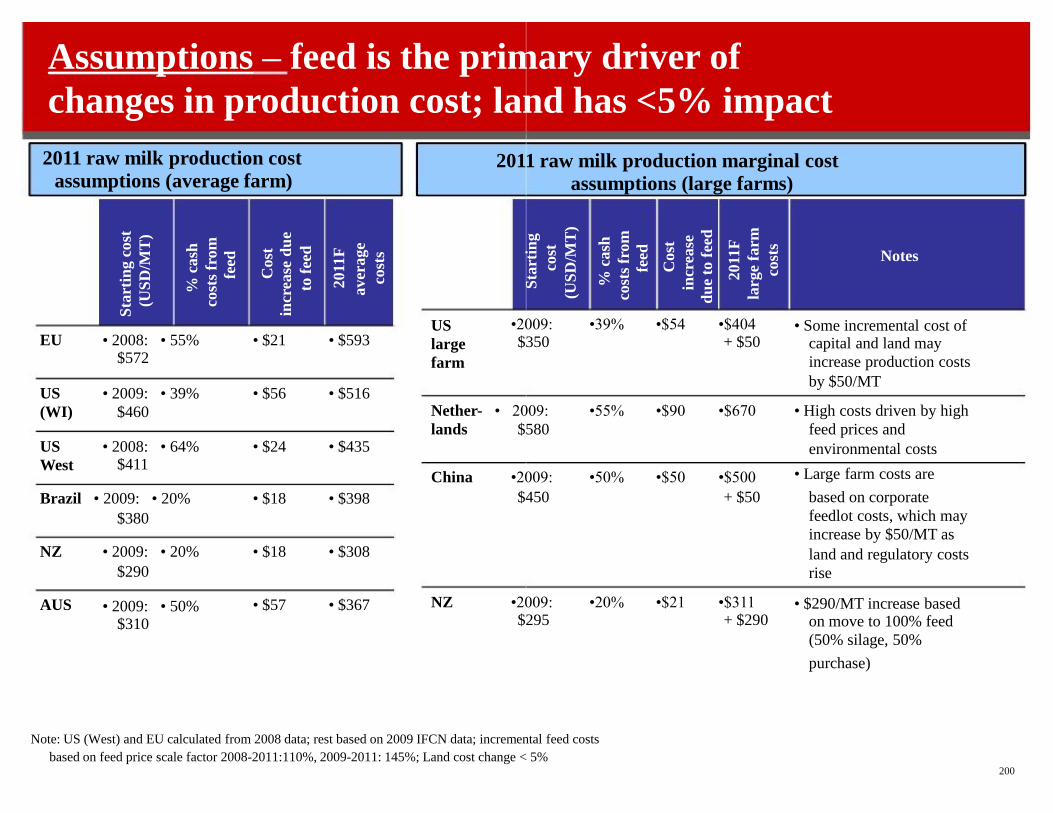

Assumptions – feed is the primary driver of

changes in production cost; land has <5% impact

EU • 2008: • 55% $572

• $21 • $593

US

(WI) $460

• 2009: • 39% • $56 • $516

US

West

• 2008: • 64% $411

• $24 • $435

$380

Brazil • 2009: • 20% • $18 • $398

NZ

$290

• 2009: • 20% • $18 • $308

AUS • 2009: • 50% $310

• $57 • $367

2011 raw milk production cost

assumptions (average farm)

US

large

farm

•2009: $350

lands

Nether- • 2009:

$580

China •2009:

$450

NZ •2009: $295

2011 raw milk production marginal cost

assumptions (large farms) Notes

•39% •$54 •$404 + $50

• Some incremental cost of capital and land may

increase production costs

by $50/MT

•55% •$90 •$670 • High costs driven by high

feed prices and

•50% •$50 •$500

+ $50

environmental costs

• Large farm costs are

based on corporate

feedlot costs, which may

increase by $50/MT as

land and regulatory costs

rise

•20% •$21 •$311 + $290

• $290/MT increase based on move to 100% feed

(50% silage, 50%

purchase) Note: US (West) and EU calculated from 2008 data; rest based on 2009 IFCN data; incremental feed costs

based on feed price scale factor 2008-2011:110%, 2009-2011: 145%; Land cost change < 5% 200

Executive summary: Potential impact of

consumption shifts to lower fat milk

• In 2009, developed markets in the EU were trending toward lower milk fat consumption, which had a potential impact on the butter latent demand gap

• Given the increasing global share of milk consumption in developing markets, similar

risks may exist if the developing markets move to lower fat milk

• These countries have not really shown such shifts in the past:

-China is unlikely to shift, as whole milk consumption is driven by taste preferences

• Additionally, increase in cream and ice-cream consumption will reduce the extra fat

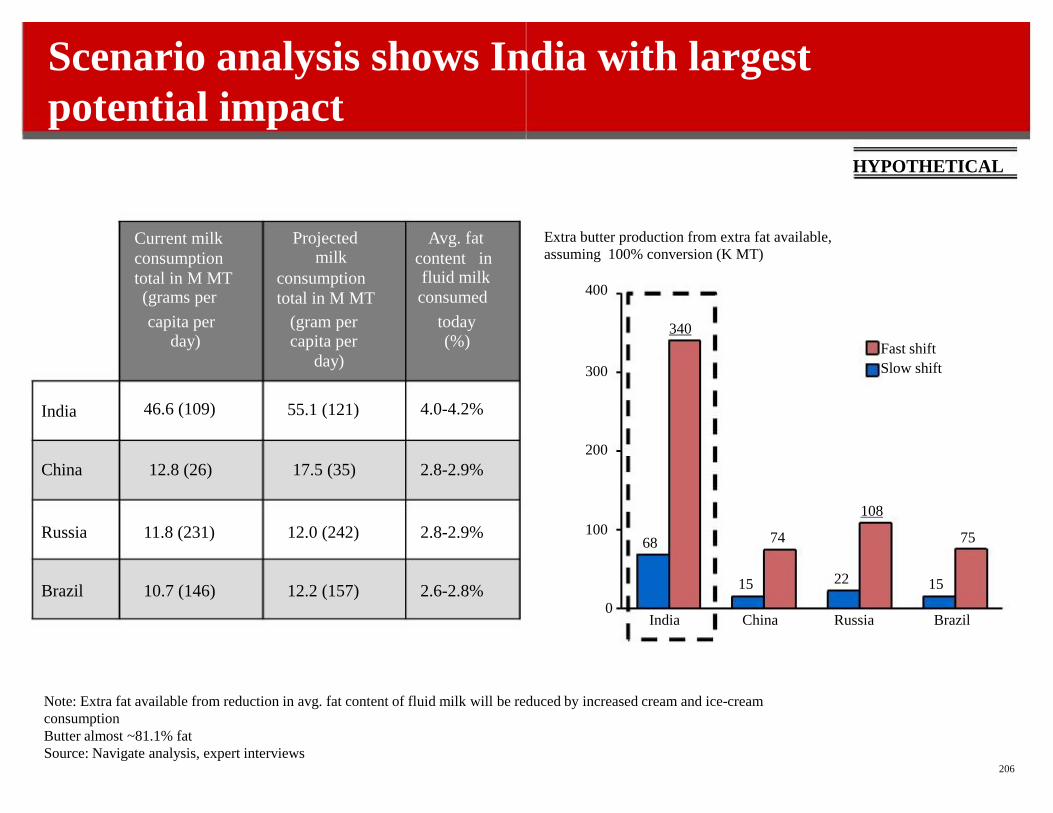

• Conversion scenarios show India with the biggest potential impact, China next

201

-India likely to see a much slower shift due to taste preferences for whole milk and limited availability of low fat milk in many areas, despite health concerns of a small urban-affluent

segment

available from any increase in skim and semi-skim consumption

China

“…taste drives

consumer

purchases, and

only a handful of

older people drink

lower fat milk… the

current young

population is sure

to drink full fat

milk.”

Shanghai University Expert

interview, Jan 2011

“China’s milk

consumption in

heavily

dependent on

children, where a

trend to lower fat

varieties is not

expected.”

Professor, WSU

interview, Jan 2011 Almost no shift

These markets have historically consumed

higher fat milk, though slow shift is possible

Source: Euromonitor, China and India expert interviews

India

“Most of India not showing shift–

rural usage of fresh milk continues

and most people in urban areas use

3%. UHT milk is very small, and fat

conscious segment is even smaller.”

Nestle Expert interview, Feb 2011

“Low availability of lower fat milk

in rural areas will limit shift”

Dairy expert, UNSW, Jan 2011

Apr 2011

“Majority of total milk consumed is

fresh at farm or purchased from

farm in its full fat form. Only a

handful of people are moving to

3% or 1.5% due to health.”

Rabobank Expert interview, Jan 2011

“Fresh milk was typically favored,

but… Long life/UHT milk is

expected to be fastest-growing

milk product… Semi-skimmed

milk is expected to drive growth

in long life/UHT milk.”

Euromonitor, Nov 2010

Likely very slow shift due to

Current milk

consumption

total in M MT (grams per

Projected milk

consumption

total in M MT

Avg. fat

content in fluid milk

consumed

India

capita per day) 46.6 (109)

(gram per capita per

day) 55.1 (121)

today (%) 4.0-4.2%

China 12.8 (26) 17.5 (35) 2.8-2.9%

Russia Brazil

11.8 (231) 10.7 (146)

12.0 (242) 12.2 (157)

2.8-2.9% 2.6-2.8%

Note: Extra fat available from reduction in avg. fat content of fluid milk will be reduced by increased cream and ice-cream

consumption

Butter almost ~81.1% fat

Source: Navigate analysis, expert interviews 206

Scenario analysis shows India with largest

potential impact HYPOTHETICAL

0

100

200

300

Extra butter production from extra fat available,

assuming 100% conversion (K MT) 400

India

68

340

China

15

74

Russia

22

108

Brazil

15

75

Fast shift

Slow shift

CAGR

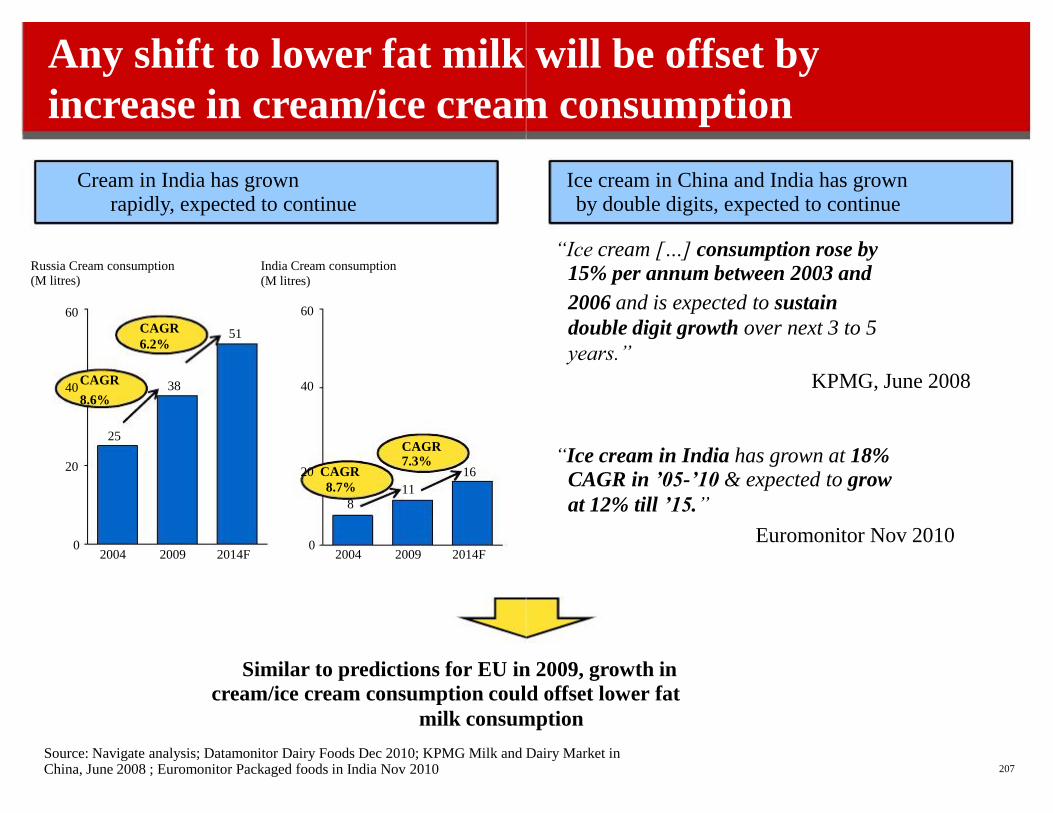

Any shift to lower fat milk will be offset by

increase in cream/ice cream consumption

0

20

2004

25

2009 2014F

51

Russia Cream consumption (M litres)

60 40 8.6%

CAGR

6.2% 38

Similar to predictions for EU in 2009, growth in

cream/ice cream consumption could offset lower fat

milk consumption Source: Navigate analysis; Datamonitor Dairy Foods Dec 2010; KPMG Milk and Dairy Market in

0

60 40

2004 2009 2014F

16

India Cream consumption

(M litres)

20 CAGR

8.7%

8

CAGR 7.3% 11

Cream in India has grown rapidly, expected to continue

China, June 2008 ; Euromonitor Packaged foods in India Nov 2010

207

“Ice cream […] consumption rose by

15% per annum between 2003 and

2006 and is expected to sustain

double digit growth over next 3 to 5

years.”

KPMG, June 2008

“Ice cream in India has grown at 18%

CAGR in ’05-’10 & expected to grow

at 12% till ’15.”

Euromonitor Nov 2010

Ice cream in China and India has grown by double digits, expected to continue

Fluid

milk Cream/

Ice -

cream

Source: Navigate analysis; Expert interviews

208

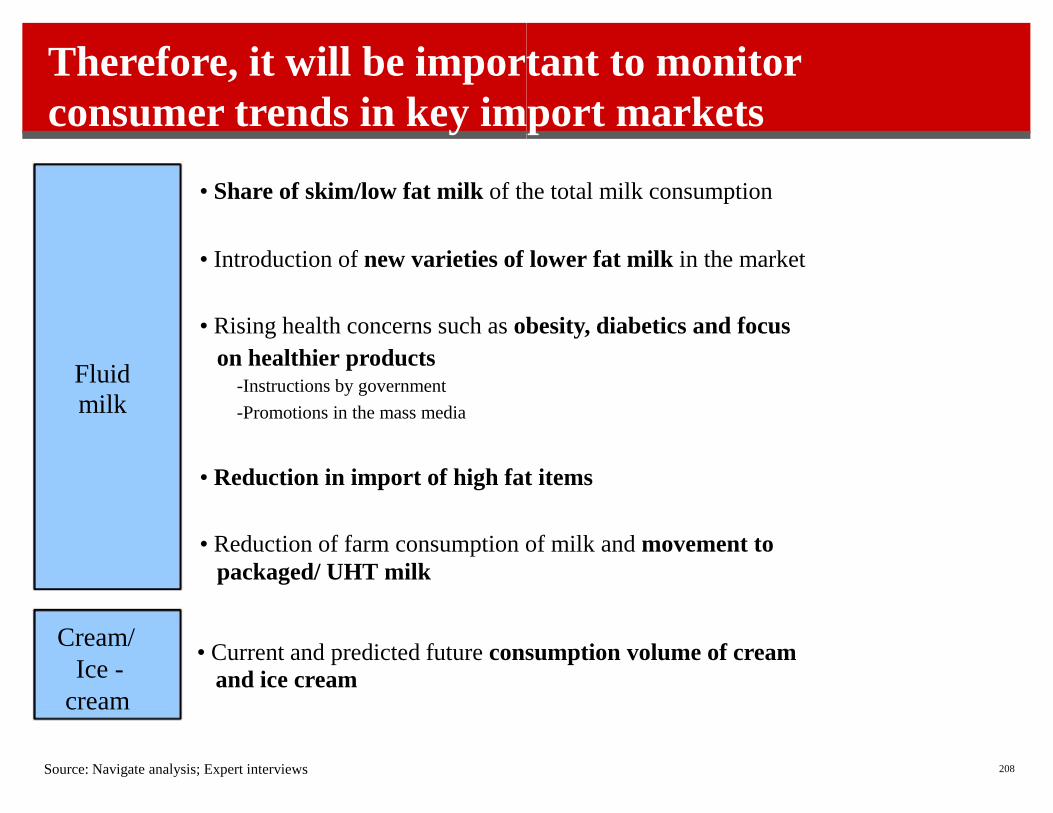

Therefore, it will be important to monitor

consumer trends in key import markets • Share of skim/low fat milk of the total milk consumption • Introduction of new varieties of lower fat milk in the market • Rising health concerns such as obesity, diabetics and focus

on healthier products -Instructions by government

-Promotions in the mass media • Reduction in import of high fat items • Reduction of farm consumption of milk and movement to

packaged/ UHT milk • Current and predicted future consumption volume of cream

and ice cream

Source: EIU Feb 2011; Euromonitor May 2011

209

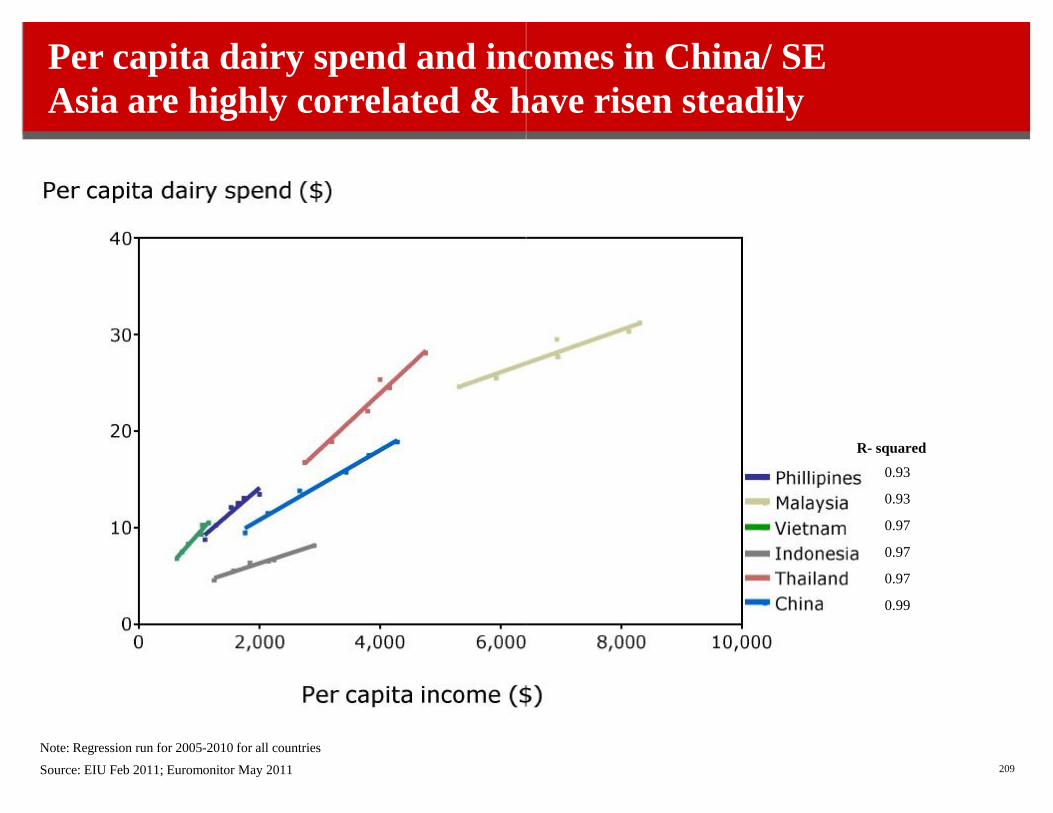

Per capita dairy spend and incomes in China/ SE

Asia are highly correlated & have risen steadily R- squared

0.93

0.93

0.97

0.97

0.97

0.99 Note: Regression run for 2005-2010 for all countries

Source: EIU Feb 2011; US Census Bureau International Database Dec 2010; Euromonitor May 2011

210

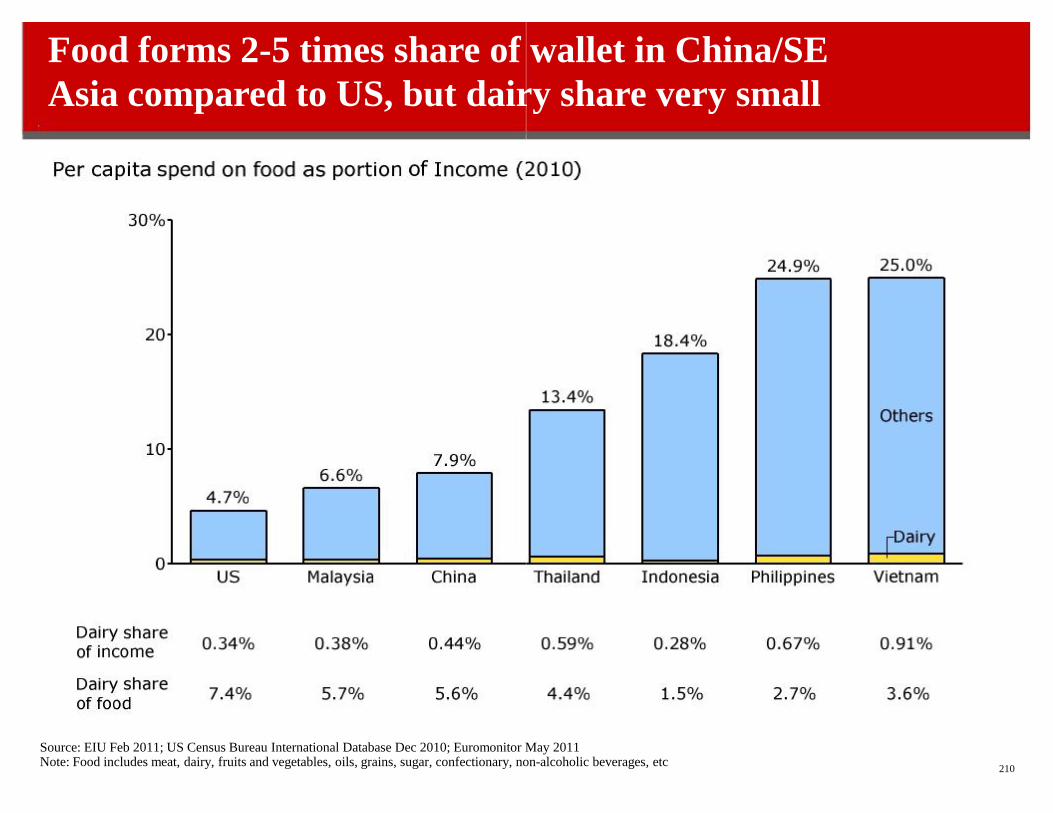

Food forms 2-5 times share of wallet in China/SE

Asia compared to US, but dairy share very small Note: Food includes meat, dairy, fruits and vegetables, oils, grains, sugar, confectionary, non-alcoholic beverages, etc

Contents

•Project objectives and summary findings

•Geography-specific findings

-Net importers

-Net exporters

•Global dairy buyers’ perspectives on Australian dairy

•Other wildcards

-Commodity price outlook

-Fat consumption trends

-Food spend analysis, currency outlook

•Summary

213

214

In 2009, study concluded that a 10-15 year

‘window of opportunity’ was available for Australian dairy Large ‘latent

demand gap’

projected by

2013F… …with future

supply sources

unclear…

…resulting in a 10-

15 year “window

of opportunity”

for US dairy

“We view the window of

opportunity to be in the

10-15 year range before

low-cost supply emerges in significant quantities.”

Imp

ort

ers

Ex

po

rter

s In summary, the window of opportunity

remains open and appears to be expanding

2013 demand gap widened during

the global economic downturn… China Russia Southeast Asia Mexico MENA India Brazil Ukraine New Zealand European Union Australia Argentina Belarus Net impact on 2013

demand gap:

Note: MENA includes Algeria, Egypt and Saudi Arabia. Southeast Asia includes Thailand,

Indonesia, Vietnam, Malaysia and Philippines 215

…leaving the window of opportunity open

at least through the medium term • China shows continued growth in

demand while ongoing melamine incidents

raise questions regarding future supply • Russia production dipped, forcing continued exports to satisfy domestic demand • Potential low-cost producers such as

Brazil and Ukraine stumbled in recent

years, with Brazil becoming a net importer • New Zealand and EU, despite expected growth and some production increases, are

unable to fill the demand gap • Other sources such as Argentina and

Belarus have good potential, but are still

relatively small The previously estimated latent demand

g ap of 6.5-7B lbs still exists and may be

larger than previously estimated

demand: Export

supply: Policy

reforms:

216

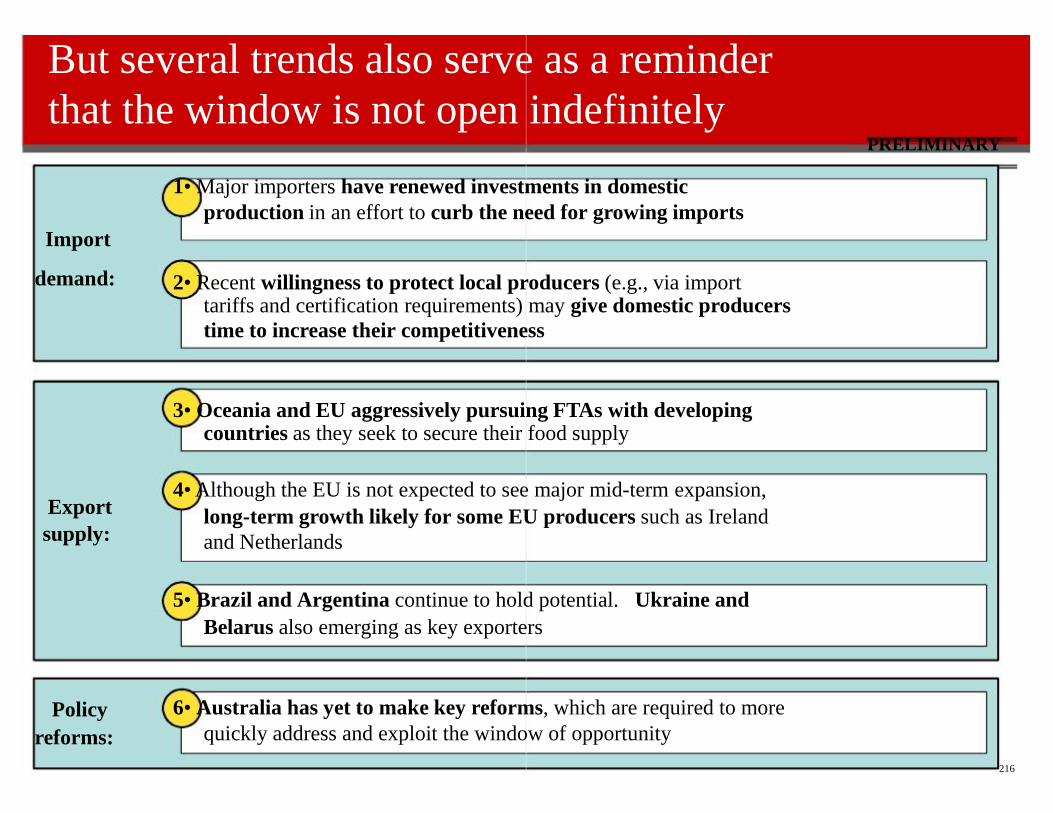

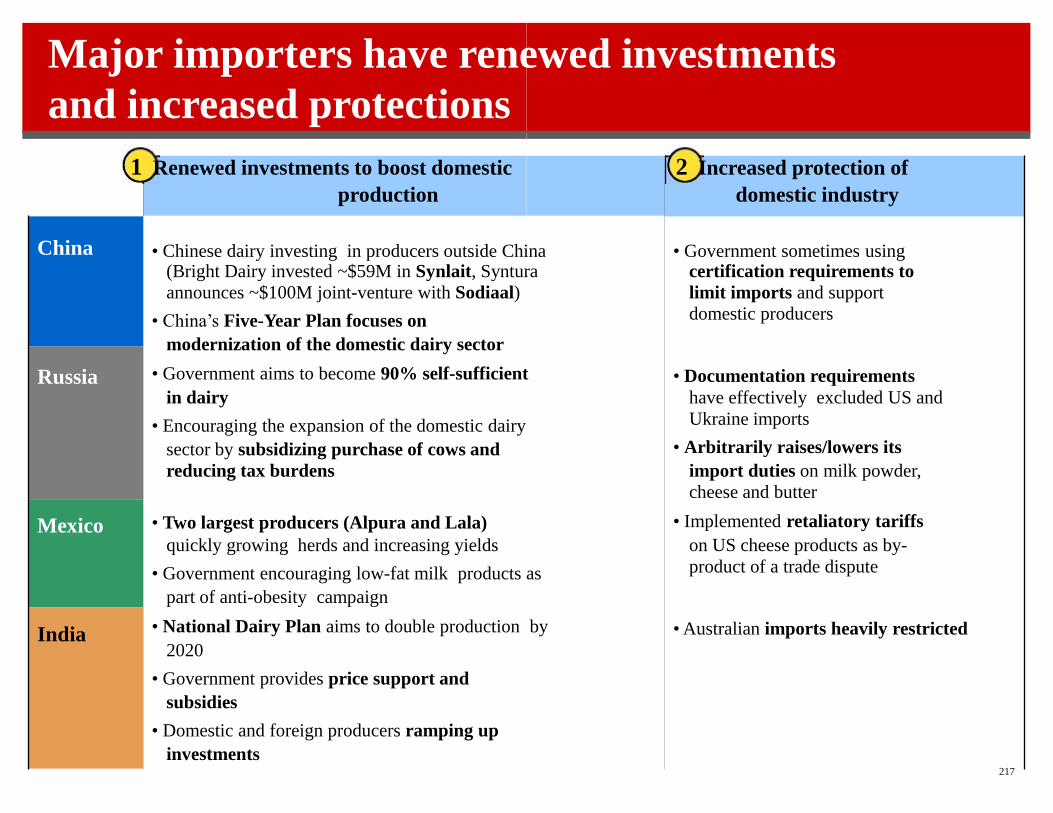

But several trends also serve as a reminder

that the window is not open indefinitely PRELIMINARY 1• Major importers have renewed investments in domestic

production in an effort to curb the need for growing imports

Import

2• Recent willingness to protect local producers (e.g., via import tariffs and certification requirements) may give domestic producers

time to increase their competitiveness 3• Oceania and EU aggressively pursuing FTAs with developing countries as they seek to secure their food supply 4• Although the EU is not expected to see major mid-term expansion,

long-term growth likely for some EU producers such as Ireland

and Netherlands 5• Brazil and Argentina continue to hold potential. Ukraine and

Belarus also emerging as key exporters 6• Australia has yet to make key reforms, which are required to more

quickly address and exploit the window of opportunity

Major importers have renewed investments

and increased protections

China Russia Mexico India

1 Renewed investments to boost domestic

production

• Chinese dairy investing in producers outside China (Bright Dairy invested ~$59M in Synlait, Syntura

announces ~$100M joint-venture with Sodiaal)

• China’s Five-Year Plan focuses on

modernization of the domestic dairy sector

• Government aims to become 90% self-sufficient

in dairy

• Encouraging the expansion of the domestic dairy

sector by subsidizing purchase of cows and

reducing tax burdens • Two largest producers (Alpura and Lala)

quickly growing herds and increasing yields

• Government encouraging low-fat milk products as

part of anti-obesity campaign

• National Dairy Plan aims to double production by

2020

• Government provides price support and

subsidies

• Domestic and foreign producers ramping up

investments

• Government sometimes using certification requirements to

limit imports and support

domestic producers • Documentation requirements

have effectively excluded US and

Ukraine imports

• Arbitrarily raises/lowers its

import duties on milk powder,

cheese and butter

• Implemented retaliatory tariffs

on US cheese products as by-

product of a trade dispute • Australian imports heavily restricted 217

2 Increased protection of

domestic industry

3

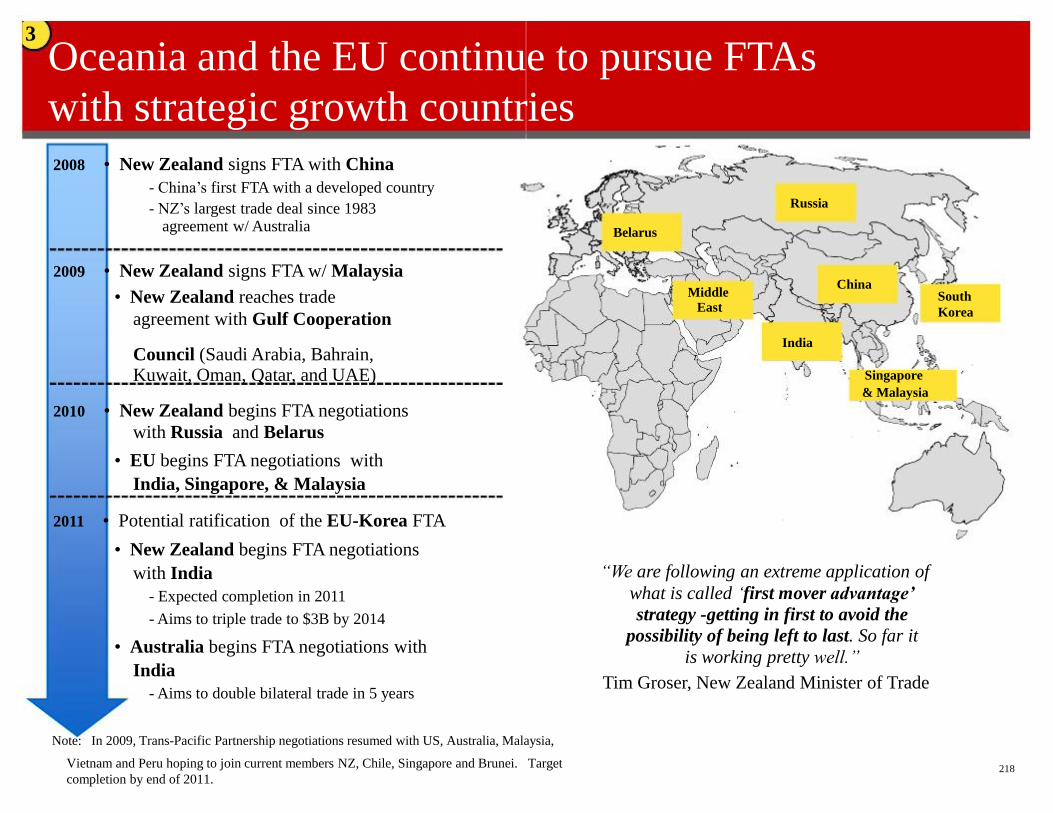

Oceania and the EU continue to pursue FTAs

with strategic growth countries 2008 • New Zealand signs FTA with China

- China’s first FTA with a developed country

- NZ’s largest trade deal since 1983 agreement w/ Australia

2009 • New Zealand signs FTA w/ Malaysia

• New Zealand reaches trade

agreement with Gulf Cooperation

Council (Saudi Arabia, Bahrain, Kuwait, Oman, Qatar, and UAE) 2010 • New Zealand begins FTA negotiations

with Russia and Belarus

• EU begins FTA negotiations with

India, Singapore, & Malaysia 2011 • Potential ratification of the EU-Korea FTA

• New Zealand begins FTA negotiations

with India

- Expected completion in 2011

- Aims to triple trade to $3B by 2014

• Australia begins FTA negotiations with

India

- Aims to double bilateral trade in 5 years

Note: In 2009, Trans-Pacific Partnership negotiations resumed with US, Australia, Malaysia,

218 Vietnam and Peru hoping to join current members NZ, Chile, Singapore and Brunei. Target

completion by end of 2011.

Belarus

Russia

China Middle

East

India Singapore

& Malaysia

“We are following an extreme application of

what is called ‘first mover advantage’

strategy -getting in first to avoid the

possibility of being left to last. So far it

is working pretty well.”

Tim Groser, New Zealand Minister of Trade

South

Korea

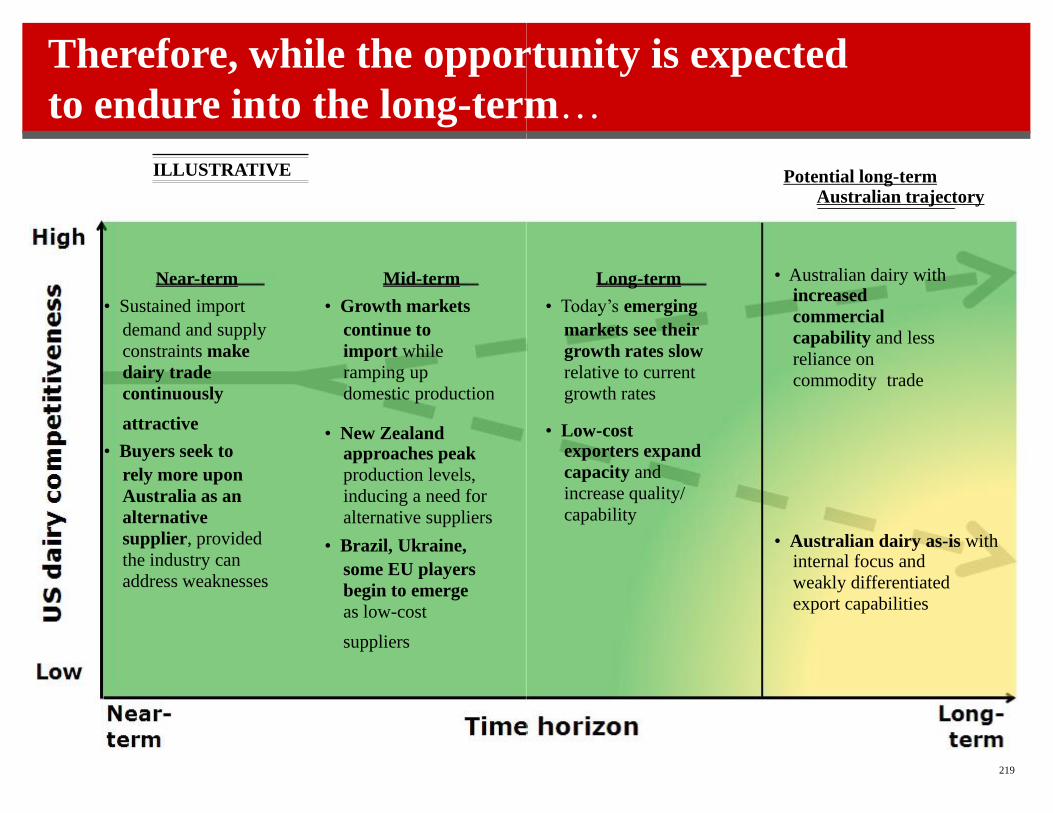

ILLUSTRATIVE

Near-term

• Sustained import

demand and supply

constraints make

dairy trade

continuously

attractive

• Buyers seek to

rely more upon

Australia as an

alternative

supplier, provided

the industry can

address weaknesses

Mid-term

• Growth markets

continue to

import while

ramping up

domestic production

• New Zealand approaches peak

production levels,

inducing a need for

alternative suppliers

• Brazil, Ukraine,

some EU players

begin to emerge

as low-cost

suppliers 219

Therefore, while the opportunity is expected

to endure into the long-term…

• Australian dairy with increased

commercial

capability and less

reliance on

commodity trade

• Australian dairy as-is with internal focus and

weakly differentiated

export capabilities

Long-term

• Today’s emerging

markets see their

growth rates slow

relative to current

growth rates

• Low-cost exporters expand

capacity and

increase quality/

capability

Potential long-term Australian trajectory

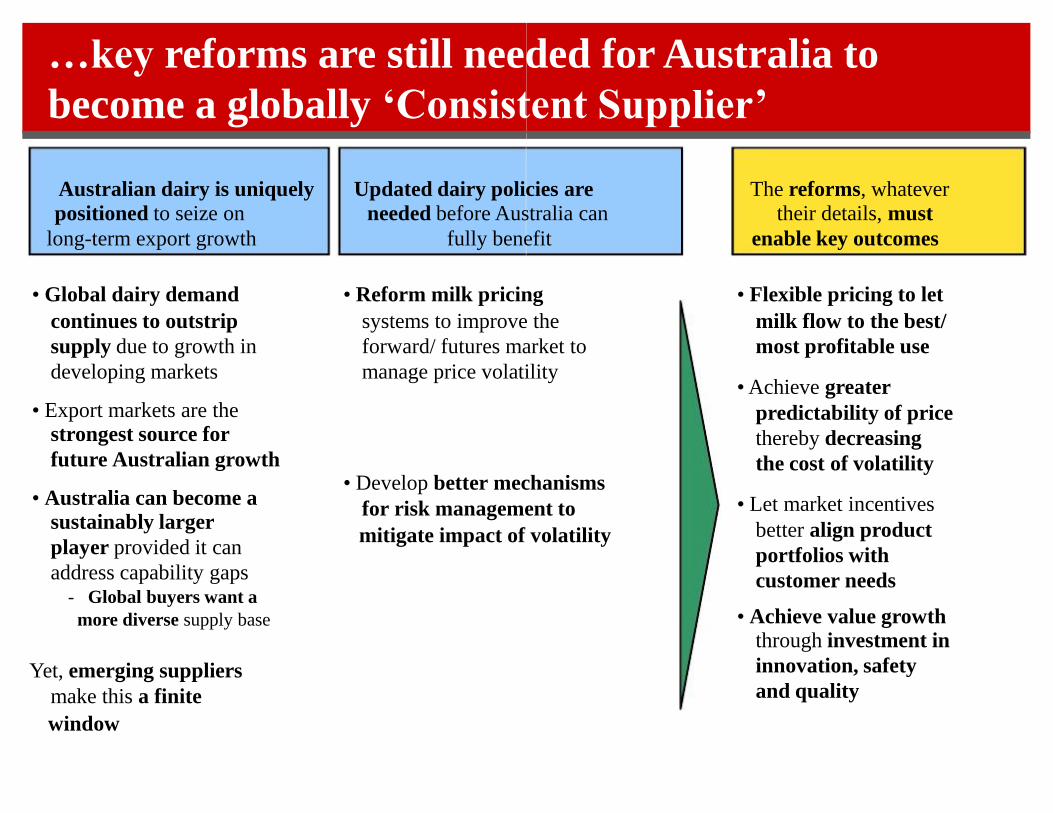

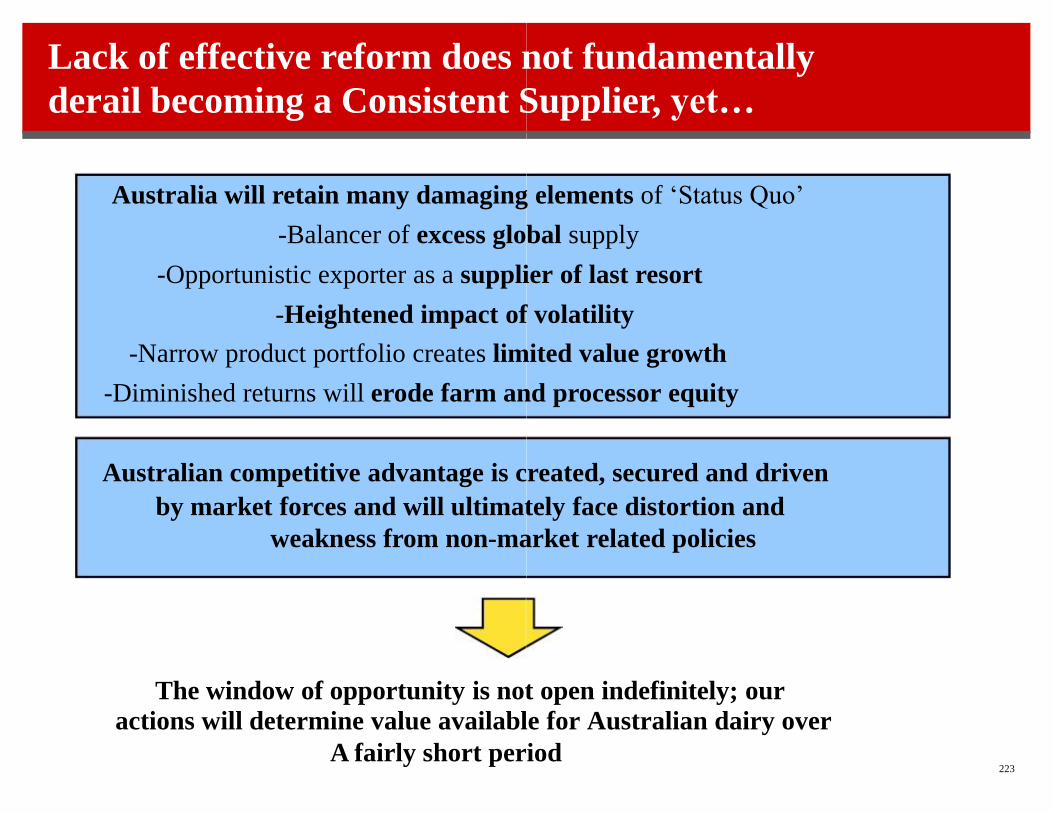

…key reforms are still needed for Australia to

become a globally ‘Consistent Supplier’

Australian dairy is uniquely

positioned to seize on

long-term export growth • Global dairy demand

continues to outstrip

supply due to growth in

developing markets • Export markets are the strongest source for

future Australian growth • Australia can become a

sustainably larger

player provided it can

address capability gaps - Global buyers want a more diverse supply base

Yet, emerging suppliers

make this a finite

window

The reforms, whatever their details, must

enable key outcomes • Flexible pricing to let

milk flow to the best/

most profitable use • Achieve greater

predictability of price

thereby decreasing

the cost of volatility • Let market incentives

better align product

portfolios with

customer needs

• Achieve value growth

through investment in

innovation, safety

and quality

Updated dairy policies are

needed before Australia can

fully benefit • Reform milk pricing

systems to improve the

forward/ futures market to

manage price volatility

• Develop better mechanisms

for risk management to

mitigate impact of volatility

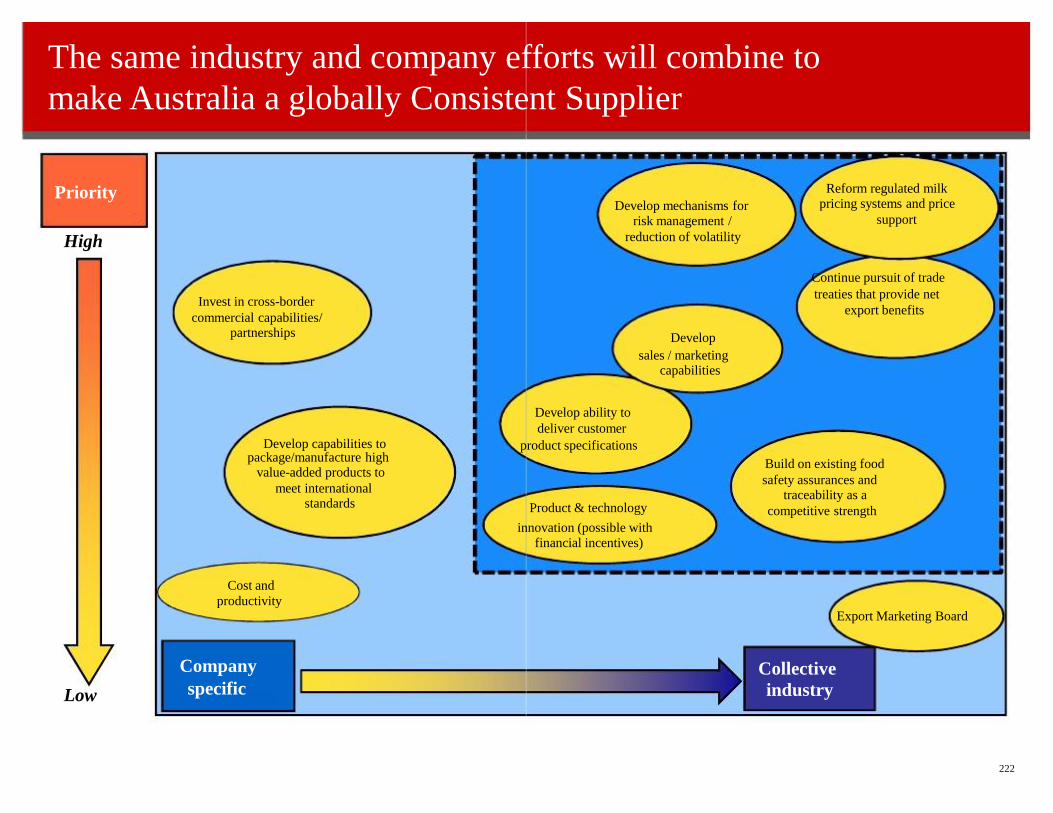

The same industry and company efforts will combine to

make Australia a globally Consistent Supplier

Company

specific

Priority High

Low

Invest in cross-border

commercial capabilities/ partnerships Develop capabilities to

package/manufacture high value-added products to

meet international standards

222

Collective

industry

Build on existing food

safety assurances and traceability as a

competitive strength

Reform regulated milk pricing systems and price

support Continue pursuit of trade

treaties that provide net

export benefits

Develop mechanisms for risk management /

reduction of volatility Develop

sales / marketing capabilities Develop ability to

deliver customer

product specifications

Product & technology

innovation (possible with financial incentives) Cost and

productivity Export Marketing Board

223