Embed Size (px)

Citation preview

MARKET DYNAMICS FOR MONGOLIAN

COKING COAL IN THE CHINESE MARKET

Mongolian Mining Summit, Perth , 30 October 2013

ANGLO AMERICAN AT A GLANCE Anglo American is one of the top 5 diversified global mining companies

Global Headquarters: London

Stock Exchange Listings: London and Johannesburg

Over 100,000 full time employees

Gross revenue in 2012: US$28.7 billion

Operating Profit 2012: US$6.2 billion

Our commodity businesses:

• Iron ore and Manganese (4th largest producer globally)

• Metallurgical coal (2nd largest producer in Australia and 3rd largest exporter globally)

• Thermal coal (6th largest exporter globally)

• Copper (8th largest producer globally)

• Nickel (8th largest producer globally)

• Niobium (2nd largest producer globally)

• Phosphates

• Platinum group metals (global leader, 40% of global production)

• Diamonds (global leader, 35% of global rough diamond production by value)

3

Headquartered in London with 12 corporate and representative offices and 96 mining operations

A GLOBAL PLAYER

Platinum

Diamonds

Copper

Nickel

Iron Ore and Manganese

Thermal Coal

Corporate &

representative offices

Key

Headquarters

Metallurgical Coal

Niobium and Phosphates

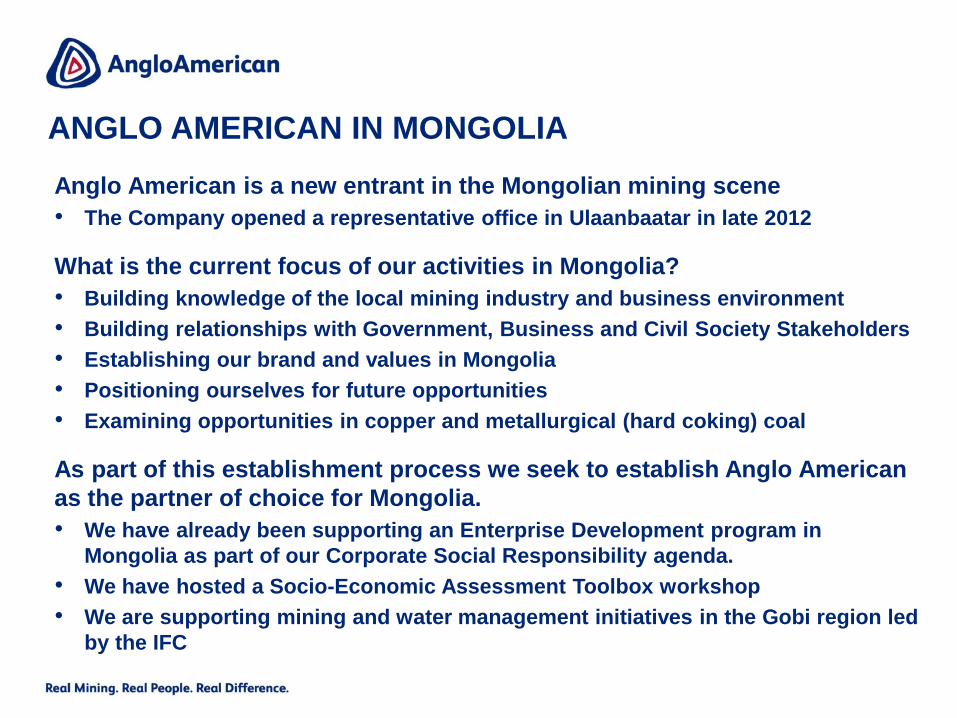

ANGLO AMERICAN IN MONGOLIA

Anglo American is a new entrant in the Mongolian mining scene

• The Company opened a representative office in Ulaanbaatar in late 2012

What is the current focus of our activities in Mongolia?

• Building knowledge of the local mining industry and business environment

• Building relationships with Government, Business and Civil Society Stakeholders

• Establishing our brand and values in Mongolia

• Positioning ourselves for future opportunities

• Examining opportunities in copper and metallurgical (hard coking) coal

As part of this establishment process we seek to establish Anglo American

as the partner of choice for Mongolia.

• We have already been supporting an Enterprise Development program in

Mongolia as part of our Corporate Social Responsibility agenda.

• We have hosted a Socio-Economic Assessment Toolbox workshop

• We are supporting mining and water management initiatives in the Gobi region led

by the IFC

MANAGING SOCIAL ISSUES

Respect human rights

Deliver lasting, positive net benefit

Identify and manage social impacts

Efficiently utilise resources

Obey all laws and regulations

Ensure contractors follow our standards

Set targets, review performance

Develop staff competencies

Engage employees and stakeholders

Report and investigate incidents

WE UNDERTAKE TARGETED CSR ACTIONS ENSURING WE UNDERSTAND THE LOCAL CONTEXT

• Our Socio-Economic Assessment Toolbox

(SEAT) is at the heart of our management of

social performance and developmental

issues

• SEAT is an award-winning manual that

provides extensive guidance on:

– Profiling and engaging with host

communities

– Assessing positive and negative impacts

– Managing relationships with host

communities

– Contributing to community development

• SEAT provides extensive guidance on

understanding our local context, and how we

as a company should respond

• Available at www.angloamerican.com/seat

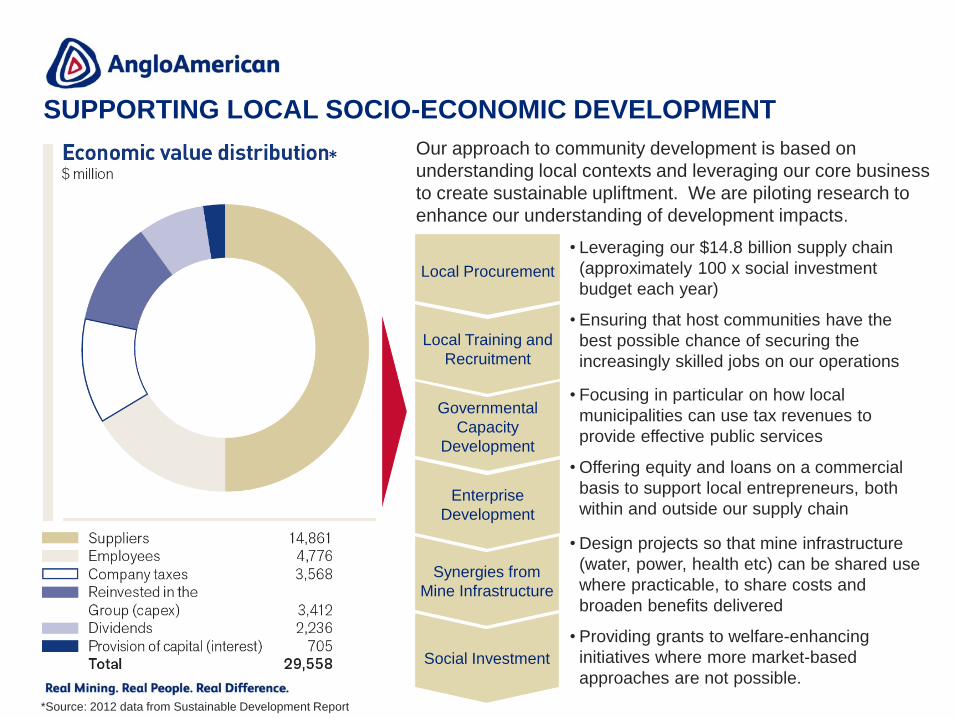

Our approach to community development is based on

understanding local contexts and leveraging our core business

to create sustainable upliftment. We are piloting research to

enhance our understanding of development impacts.

• Leveraging our $14.8 billion supply chain

(approximately 100 x social investment

budget each year)

• Ensuring that host communities have the

best possible chance of securing the

increasingly skilled jobs on our operations

• Focusing in particular on how local

municipalities can use tax revenues to

provide effective public services

• Offering equity and loans on a commercial

basis to support local entrepreneurs, both

within and outside our supply chain

• Design projects so that mine infrastructure

(water, power, health etc) can be shared use

where practicable, to share costs and

broaden benefits delivered

• Providing grants to welfare-enhancing

initiatives where more market-based

approaches are not possible.

Local Procurement

Local Training and

Recruitment

Governmental

Capacity

Development

Enterprise

Development

Synergies from

Mine Infrastructure

Social Investment

*

*Source: 2012 data from Sustainable Development Report

SUPPORTING LOCAL SOCIO-ECONOMIC DEVELOPMENT

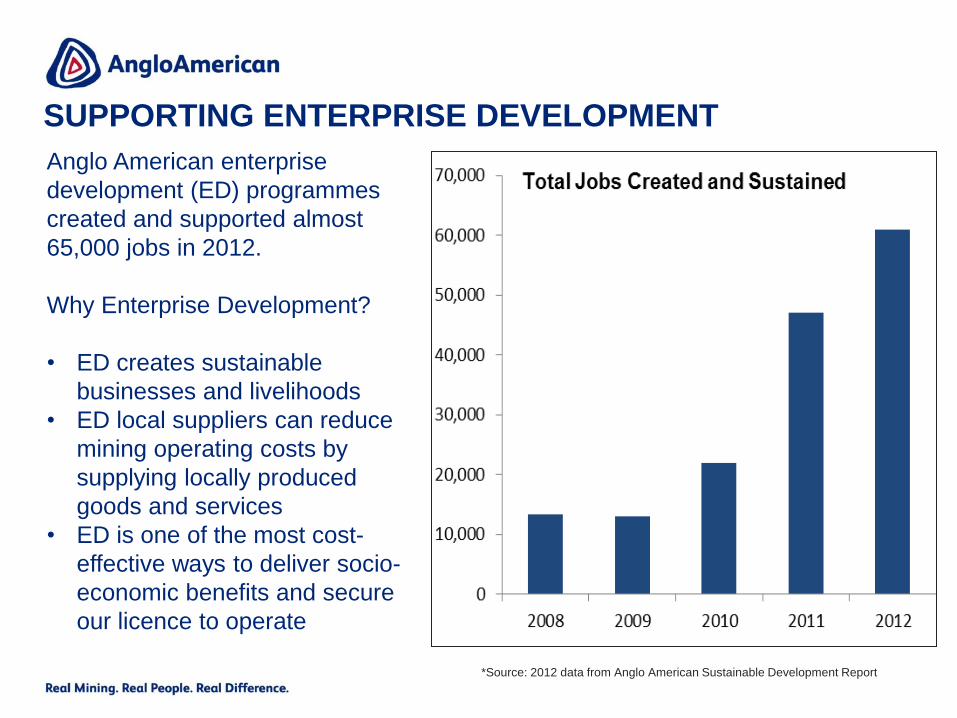

SUPPORTING ENTERPRISE DEVELOPMENT

8

Anglo American enterprise

development (ED) programmes

created and supported almost

65,000 jobs in 2012.

Why Enterprise Development?

• ED creates sustainable

businesses and livelihoods

• ED local suppliers can reduce

mining operating costs by

supplying locally produced

goods and services

• ED is one of the most cost-

effective ways to deliver socio-

economic benefits and secure

our licence to operate

*Source: 2012 data from Anglo American Sustainable Development Report

THE CURRENT MARKET SITUATION FOR

MONGOLIAN COAL

• Mongolian Met Coal Exports to the end of Sept 2013

• 11.38 million tons of coal - down 20.3 % yoy

• Valued at US$ 783 million - down 54.7% yoy

Some key questions • What has happened to Mongolian coal exports since Q1 13 and

how do the results relate to Chinese Market conditions?

• What are the main factors driving the current situation?

• What is the real price of Mongolian HCC in the Chinese Market?

• What are Mongolia’s competitor countries doing?

• Why are there discounts to Mongolian coal producers ?

• What needs to be done to ensure that Mongolia remains a

competitive and viable producer in the long term?

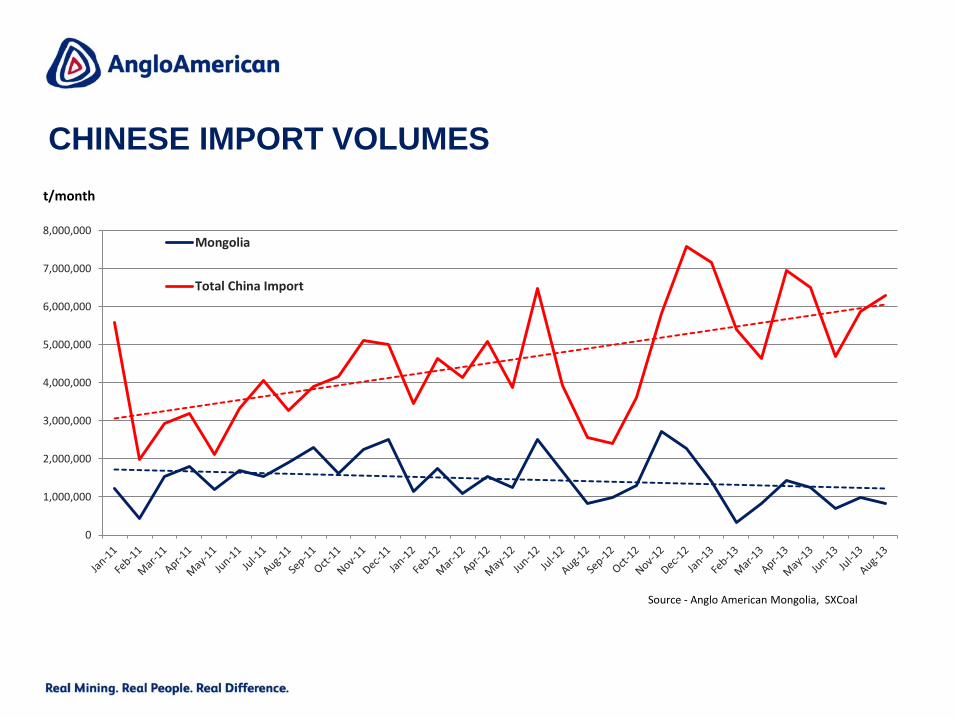

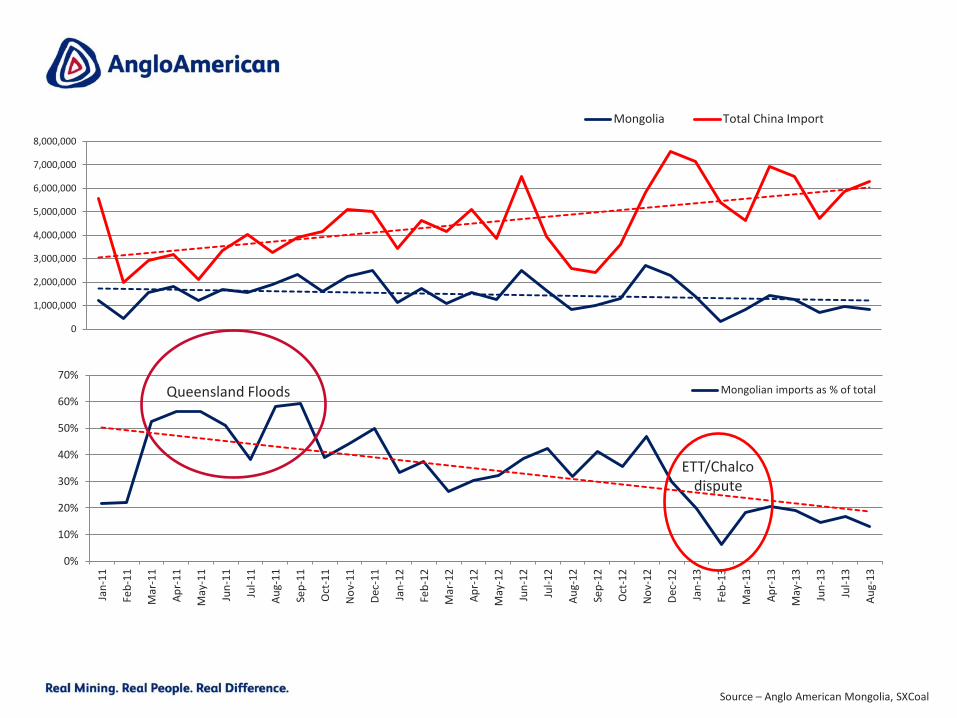

CHINESE IMPORT VOLUMES

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000Mongolia

Total China Import

Source - Anglo American Mongolia, SXCoal

t/month

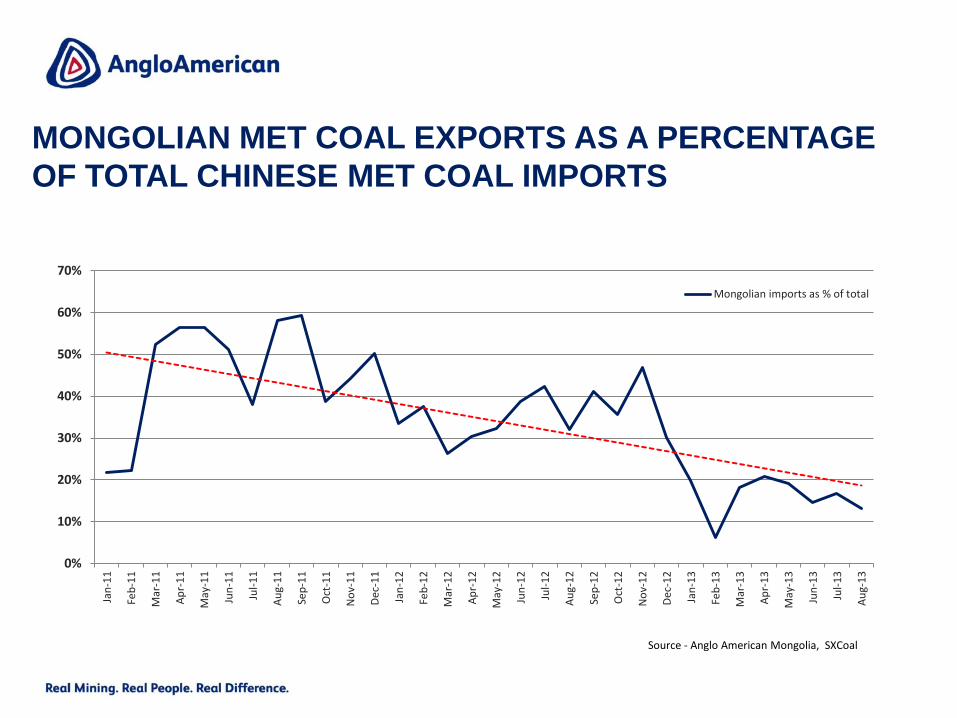

MONGOLIAN MET COAL EXPORTS AS A PERCENTAGE

OF TOTAL CHINESE MET COAL IMPORTS

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

Dec

-12

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

0%

10%

20%

30%

40%

50%

60%

70%

Mongolian imports as % of total

Source - Anglo American Mongolia, SXCoal

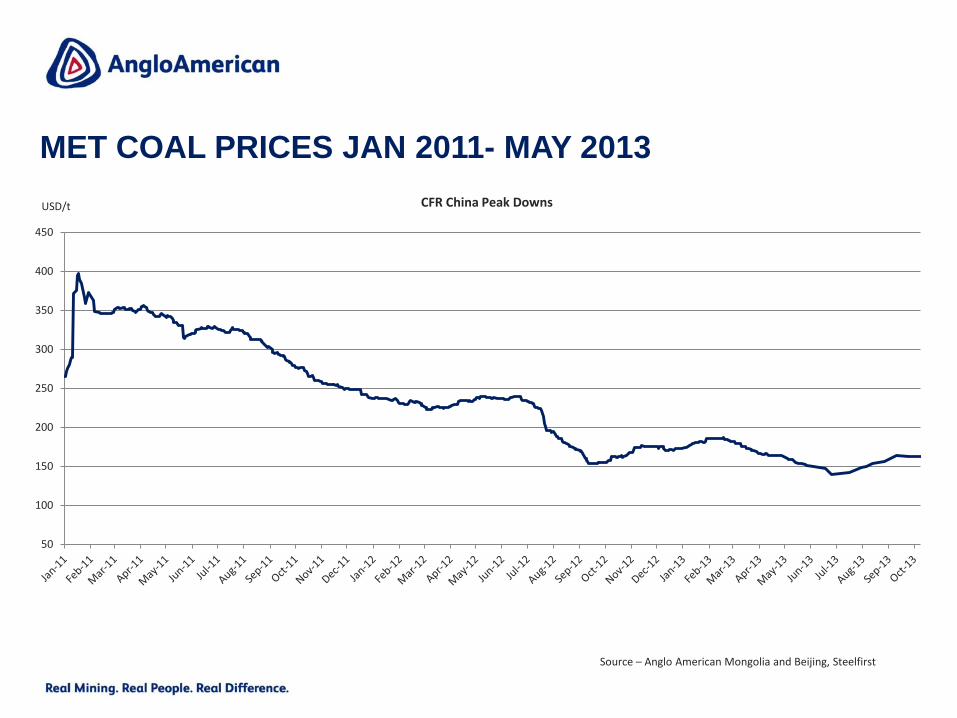

MET COAL PRICES JAN 2011- MAY 2013

Source – Anglo American Mongolia and Beijing, Steelfirst

50

100

150

200

250

300

350

400

450

CFR China Peak Downs USD/t

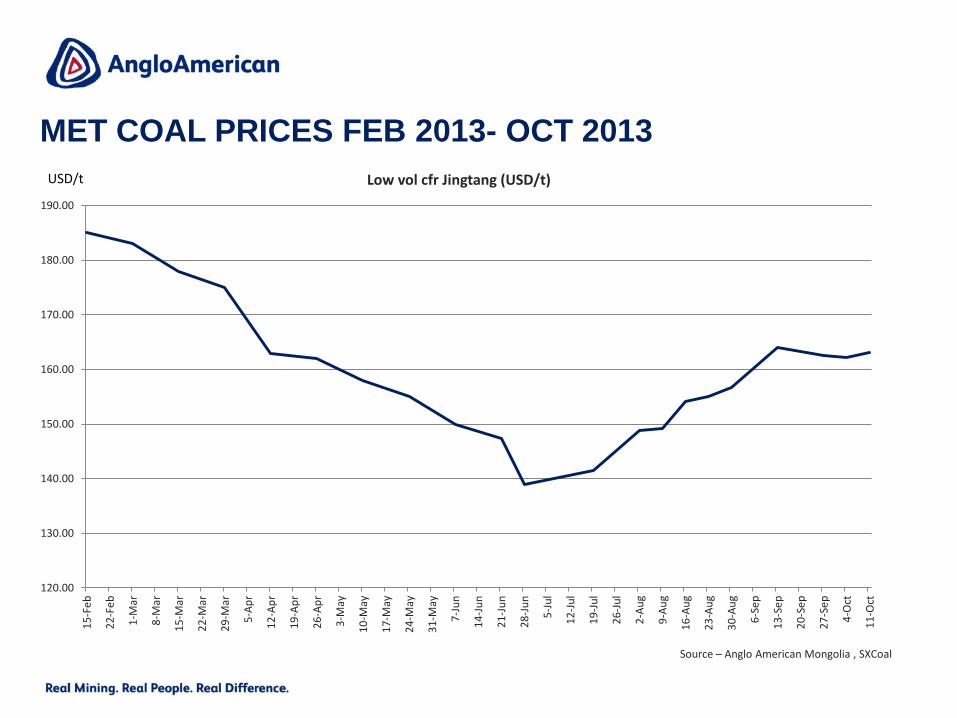

MET COAL PRICES FEB 2013- OCT 2013

Source – Anglo American Mongolia , SXCoal

120.00

130.00

140.00

150.00

160.00

170.00

180.00

190.00

15

-Fe

b

22

-Fe

b

1-M

ar

8-M

ar

15

-Mar

22

-Mar

29

-Mar

5-A

pr

12

-Ap

r

19

-Ap

r

26

-Ap

r

3-M

ay

10

-May

17

-May

24

-May

31

-May

7-J

un

14

-Ju

n

21

-Ju

n

28

-Ju

n

5-J

ul

12

-Ju

l

19

-Ju

l

26

-Ju

l

2-A

ug

9-A

ug

16

-Au

g

23

-Au

g

30

-Au

g

6-S

ep

13

-Se

p

20

-Se

p

27

-Se

p

4-O

ct

11

-Oct

Low vol cfr Jingtang (USD/t) USD/t

MONGOLIAN HCC PRICES (EX WAREHOUSE GANQIMAODU)

FEB 2012 - OCT 2013

Source – Anglo American Mongolia , SXCoal, Steelfirst

50

100

150

200

250

300

350

400

450

Au

g-1

0

Sep

-10

Oct

-10

No

v-1

0

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

Dec

-12

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

CFR ChinaPeak Downs

Mgl met coal

USD/t

Source – Anglo American Mongolia, SXCoal

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Mongolia Total China Import

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

Dec

-12

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

0%

10%

20%

30%

40%

50%

60%

70%Mongolian imports as % of totalQueensland Floods

ETT/Chalco dispute

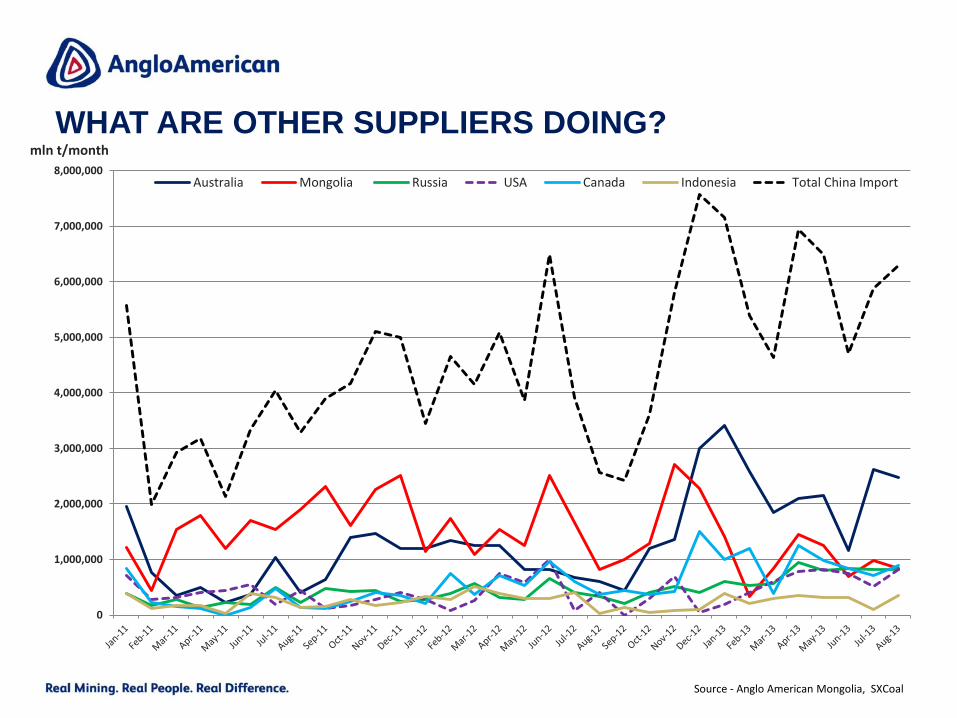

WHAT ARE OTHER SUPPLIERS DOING?

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000Australia Mongolia Russia USA Canada Indonesia Total China Import

Source - Anglo American Mongolia, SXCoal

mln t/month

0.0

50.0

100.0

150.0

200.0

250.0

300.0

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Generalised Chinese Domestic Producer Cost Curve for HCC USD/t CFR Bohai Sea

Current CFR Bohai Sea port coal price US$163

CAN WE EXPECT A SUPPLY RESPONSE FROM CHINESE

DOMESTIC PRODUCERS?

Source – Anglo American Mongolia and Beijing, SXCoal

US$/t

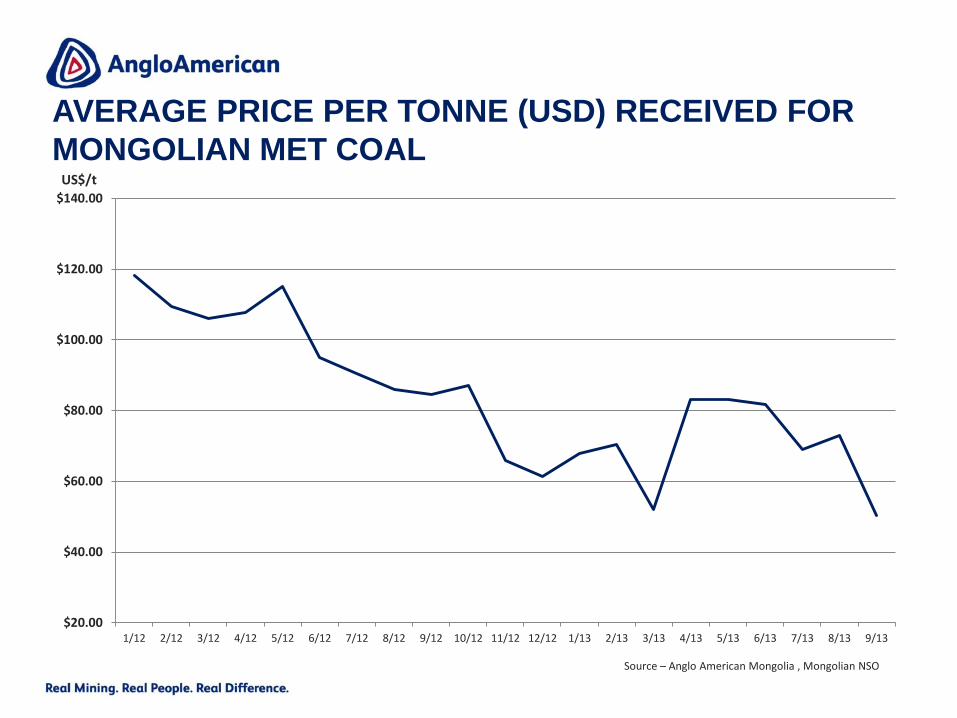

AVERAGE PRICE PER TONNE (USD) RECEIVED FOR

MONGOLIAN MET COAL

Source – Anglo American Mongolia , Mongolian NSO

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

1/12 2/12 3/12 4/12 5/12 6/12 7/12 8/12 9/12 10/12 11/12 12/12 1/13 2/13 3/13 4/13 5/13 6/13 7/13 8/13 9/13

US$/t

WHY DO MONGOLIAN PRODUCERS RECEIVE LOW PRICES?

• Local prices are not directly comparable to international seaborne prices

• Most Mongolian coal crosses the border raw (unwashed)

• Traders buy raw coal and wash it facing a loss of tonnage on washery yield

• The dirtier the coal the lower the yield and the lower the price to the producer

• Inconsistent quality

• Because coal is raw, quality varies from shipment to shipment and it appears

that traders are quoting based on the worst case quality received

• Seams are mixed, or roof and floor material included in exports reducing both

quality and consistency

• Unreliable Supply

• Irregular tonnages means that traders cannot enter into long term supply

agreements with offtakers and must trade spot often with lower price outcomes

• Congested transport systems and border crossings compound the challenges

faced by suppliers contributing to unreliable deliveries and increases costs for

buyers.

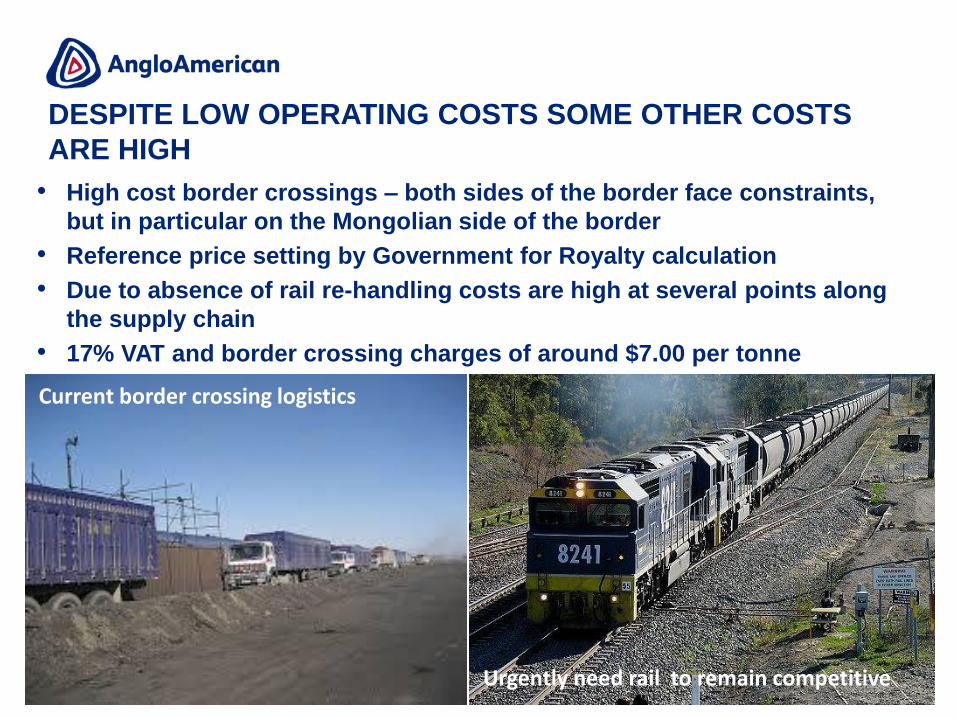

DESPITE LOW OPERATING COSTS SOME OTHER COSTS

ARE HIGH

• High cost border crossings – both sides of the border face constraints,

but in particular on the Mongolian side of the border

• Reference price setting by Government for Royalty calculation

• Due to absence of rail re-handling costs are high at several points along

the supply chain

• 17% VAT and border crossing charges of around $7.00 per tonne

Current border crossing logistics

Urgently need rail to remain competitive

POSSIBLE SOLUTIONS

• Most of the factors mentioned are under the control of the coal producer

or the Government

• Inconsistent quality – raw coal

• A move to washed coal production is essential to ensure consistent quality -

to reduce transportation costs and trader discounting

• Re-handling costs

• An efficient standard gauge rail system is required to ensure single handle

and no border re-handle as well as to reduce re-handling inside China

• Border crossings need upgrading for rail transit and 24 hour per day

operations

• Royalties need to reflect actual contract prices otherwise producers can

be taxed out of business

• Chinese pricing power – without standard gauge rail, Chinese off-takers

will retain their pricing power. Bonded cargo carriage through China is

needed in order to access international seaborne prices – this is not

possible without standard gauge rail in Mongolian territory

CONCLUSIONS

• The Chinese market for hard coking coal remains quite strong (around

70mt/yr and still growing) – however Mongolia is continuing to lose market

share

• Producer issues: Consistent quality, reliable supply and stable

relationships with off-takers are necessary for Mongolian producers to win

back market share and achieve better pricing

• Government issues: Enhancing the competitiveness of the Mongolian

coking coal industry requires a number of issues to be resolved:

• Progress on improving bulk cargo transportation (standard gauge rail) and

border crossing logistics

• Reducing re-handling by improving transportation logistics

• Ensuring that Mongolian coal is subject to a fair and reasonable royalty regime

• Mongolia has a comparative advantage in terms of proximity to the

Chinese market. Both the industry and the Government need to work

together to improve the competitiveness of the Mongolian Coal sector,

otherwise Mongolia may continue to lose market share.

THE PARTNER OF CHOICE FOR MONGOLIA

Thank you for your attention

Integrity Accountability Safety Care and respect Collaboration Innovation

OUR VALUES